11institutetext: Wenyuan Wang 22institutetext: School of Mathematical Sciences, Xiamen University

Fujian 361005, China

wwywang@xmu.edu.cn

33institutetext: Yuebao Wang 44institutetext: School of Mathematics, Soochow University

Suzhou, 215006, China

ybwang@suda.edu.cn

55institutetext: Xueyuan Wu, Corresponding Author 66institutetext: The University of Melbourne

VIC 3010, Australia

xueyuanw@unimelb.edu.au

Dividend and Capital Injection Optimization with Transaction Cost for Spectrally Negative Lévy Risk Processes

Wenyuan Wang

Yuebao Wang

Xueyuan Wu

Abstract

For an insurance company with reserve modelled by a spectrally negative Lévy process, we study the optimal impulse dividend and capital injection (IDCI) strategy for maximizing the expected accumulated discounted net dividend payment subtracted by the accumulated discounted cost of injecting capital. In this setting, the beneficiary of the dividends injects capital to ensure a non-negative risk process so that the insurer never goes bankrupt. The optimal IDCI strategy together with its value function are obtained. Finally, a Brownian motion example is presented to illustrate the optimal IDCI strategy numerically.

Keywords:

Spectrally negative Lévy process De Finetti’s optimal dividend problem Stochastic control Hamilton-Jacobi-Bellman inequality

MSC:

49K45 49N25

††journal: JOTA

1 Introduction

This paper aims to discuss the optimal impulse dividend and capital injection (IDCI) strategy for an insurance company. The surplus level is modelled by a spectrally negative Lévy (SNL) risk process, a widely used model in the literature. To enhance the practical relevance of the optimal dividend problem considered in this paper, we consider two real-life factors: the transaction costs on dividends and the capital injections. First, having the transaction costs included in the total cost of dividends is a natural addition; and second, allowing capital injections can protect the insurance company against the bankruptcy, thereby sustaining dividend payments in the long run. Through maximizing the expected accumulated discounted net dividend payments subtracted by the accumulated discounted cost of injecting capital under the proposed surplus process, we obtain the optimal IDCI strategy, which provides a useful reference for insurance companies when designing their long-term profit-sharing strategies.

The optimal dividend payout strategies have remained an active research field in the actuarial science literature for almost 60 years. Two survey papers, Albrecher09 and Avanzi09 , provide thorough and insightful reviews on the classical contributions and recent progress in the field. The earliest paper in the field, Finetti57 , proved that with the option to pay out dividends from its surplus to the beneficiary until the discrete time of ruin, an insurance company should adopt a barrier dividend strategy to maximize the expected total amount of discounted dividends until ruin. However, when dividends are imposed with fixed transaction costs, recent research findings in the literature suggest that the dividend optimization problem becomes an impulse (dividend) control problem and the optimal dividend strategy is an optimal impulse dividend (OID) strategy.

Research on OID strategies has attracted much attention for a decade and has progressed well under various surplus processes. In the classical Cramér-Lundberg (CL) risk model, Bai10a studied an OID problem with transaction cost and tax on dividends as well as exponentially distributed claims. The obtained OID strategy reduces the reserve to level whenever it is above or equal to level , also called a strategy.

In the dual classical CL risk model, Zhou14 also considered an OID problem with fixed/proportional transaction cost on dividends and derived the OID strategy via a quasi-variational inequality argument. Bai10b studied the OID problem with transaction costs on dividends for a class of general diffusion risk processes and derived the OID strategy. In the context of SNL risk process, Loeffen09b discussed an OID problem with transaction cost and showed that a strategy maximizes the expected accumulated present value of the net dividends. For the spectrally positive Lévy (SPL) risk process with fixed transaction costs on dividends, Bayraktar14 proved that a strategy is again the OID. For more results on impulse dividend control problems, we refer readers to Hernandez18 -Yao11 and the references therein.

In the literature, capital injection is another factor to consider when designing dividend payout. Under risk models with dividends as well as fixed transaction costs imposed on the capital injections, the corresponding optimization problem is also an impulse (capital injection) control problem. In the setting of the dual classical CL risk model, Yao11 found that the optimal dividend and capital injection (ODCI) strategy, which maximizes the expected present value of the dividends subtracted by the discounted cost of capital injections, pays out dividends according to a barrier strategy and injects capitals to bring the reserve up to a critical level whenever it falls below .

Under the drifted diffusion risk model, Peng12 investigated the optimal dividend problem of an insurance company which controls risk exposure by reinsurance and by issuing new equity to protect the insurance company from bankruptcy. The corresponding ODCI strategy also pays dividends by a barrier strategy and injects capital to bring reserve up to a critical level whenever it falls below . In the setting of SPL risk process with the dividend rate restricted,

Zhao17a and Zhao17b considered an ODCI problem and found that the optimal method of paying dividends is a threshold strategy.

For more information on dividend optimization in risk models with capital injection being imposed with proportional or fixed transaction cost, we refer readers to Zhao15 , Zhu17 -Bayraktar13 , and the references therein.

Regarding SNL risk processes, the majority of dividend optimization problems are formulated as non-impulse stochastic control problems. Using the expected present value of dividends until ruin (the expected present value of the dividends subtracted by the discounted costs of capital injections) as the value function, Avram07 identified the condition under which the barrier strategy (respectively, the barrier dividend strategy together with capital injection strategy that reflects the reserve process at ) is optimal among all admissible strategies. More results of non-impulse dividend optimization under the SNL risk processes can be found in Avram15 , Loeffen08 -Gerber69 , and the references therein. The non-impulse dividends optimization under the SPL risk processes can be found in Bayraktar14 , Avanzi11 , Zhao17a , Zhao17b , Avanzi17 -Avram07 , Kyprianou12 , Yin13 , and others.

Motivated by Loeffen09b and Avram07 , this paper studies a general optimal IDCI problem through

maximizing the expected accumulated discounted net dividend payment subtracted by the accumulated discounted cost of injecting capital in the setup of the SNL risk process.

The novelty in this paper lies as follows: (i) compared with the existing OID results under diffusion or general Lévy setup, the present model brings in the capital injection in an optimal way to reflect the corresponding risk process at ; and (ii) compared with the existing OID results concerning capital injections, the present model studies the Lévy setup, a more general driven process. In this paper, the discussion follows the standard treatment of Hamilton-Jacobi-Bellman (HJB) inequality in the control theory. We first find the optimal strategy among all IDCI strategies, and then we prove that it is optimal among all IDCI strategies via a verification argument. To facilitate the standard HJB framework, we employ subtle approaches within each step, for example, the novel technique to derive Proposition 3.3 and Lemma 4.6, and the mollifying argument to prove the modified verification lemma (see, Lemma 4.3 and Lemma 4.4).

We acknowledge that there is a parallel paper in the literature, Junca18 , which was also finished independently around the same time. The first version of both papers were available on internet in the middle of 2018. The authors of Junca18 considered the bail-out optimal dividend problem under fixed transaction costs for a Lévy risk model with a constraint on the expected net present value of injected capital. While the main results in this paper and those in Junca18 appear to be very similar, the primary objectives of these two papers are notably different as well as the methods adopted in the proof of certain main results (for instance, the verification Lemma 4.3 and Lemma 4.4 in this paper vs Theorem 4.10 in Junca18 ). We believe both papers make interesting contributions to the literature.

The remainder of this paper is organized as follows:

Section 2 comprises preliminaries concerning the SNL process and the mathematical setup of the dividend optimization problem. In Section 3 we represent the value function of a IDCI strategy using the scale function associated with the SNL process. This facilitates the characterization of the optimal strategy among all IDCI strategies, which is further proved to be optimal among all admissible IDCI strategies. In Section 4, we first prove that a solution to the HJB inequalities coincides with the optimal value function via a verification lemma. Next, the solution to the HJB inequality is constructed, and the optimal strategy is found to be a IDCI strategy under which the risk process is reflected at . In Section 5, we also illustrate the optimal IDCI strategy by using one numerical example.

2 Formulation of the dividend optimization problem

Let with probability law and natural filtration be a SNL process, which is not a pure increasing linear drift or the negative of a sub-ordinator. Denote the running supremum for . Assume that in the case of no control (dividend is not deducted and capital is not injected), the risk process evolves as for .

An impulse dividend strategy, denoted by , is a one-dimensional, non-decreasing,

left-continuous, -adapted, and pure jump process started at , i.e., and defines the cumulative dividend that the company has paid out until time .

For the insurance company not to go bankrupt, the beneficiary of the dividend is required to inject capital into the insurance company to ensure that the risk process is non-negative.

A capital injection strategy, denoted by , is a one-dimensional, non-decreasing,

càdlàg, -adapted process started at , i.e., and defines

the cumulative capital that the beneficiary has injected until time . The combined pair is called an IDCI strategy. More explicitly, an impulse dividend strategy is characterized by

where and are the -th time and amount of dividend lump sum payment, respectively.

With dividends deducted according to and capital injected according to , the controlled aggregate reserve process is then given by

An IDCI strategy is defined to be admissible if for all and

almost sure in the sense of ,

where is a discount factor.

Let be the set of all admissible

dividend and capital injection strategies.

For an IDCI strategy , denote its value function as

where is the transaction cost for each lump sum dividend payment and is the cost of per unit capital injected. The goal is to identify the optimal strategy and the corresponding optimal value function

Intuitively speaking, because of and , it would be better if the capital is injected as late as possible with no further capital injection being made rather than just injecting enough amounts to keep the corresponding risk process non-negative.

The Laplace exponent of is

where is the Lévy measure with .

Alternatively,

where is the standard Brownian motion, is an independent Poisson random measure on with intensity measure , and denotes the compensated random measure.

It is known that for , in which case it is strictly convex and infinitely differentiable.

As in Bertoin96 , the -scale function of , for each , is the unique strictly increasing and continuous function with Laplace transform

where is the largest solution of the equation . Further, let for and write for the -scale function .

For any and , there exists the well-known exponential change of measure for an

SNL process

Furthermore, under the probability measure , remains an SNL

process and we denote by and respectively the -scale function and the -scale function for under .

Note that we do not impose the safety loading condition . Instead, is assumed throughout the paper.

3 The type dividend and capital injection strategy

For the Lévy process , denote the reflected process at infimum (or at )

Define and , respectively, to be the up-crossing times of level of the processes and , with the convention . Define further

Then, for and , Proposition 2 of Pistorius04 holds that

(1)

For , let us consider an important type of IDCI strategy, such as the strategy : a lump sum of dividend payment is made to bring the reserve level down to the level once the reserve hits or is above the level , while no dividend payment is made whenever the reserve level is below . Capital is injected in such a way that the reserve process is reflected at

, i.e., . To be precise, we define recursively

and

(2)

Then, the strategy can be re-expressed as

(3)

and

In the following result, the value function of a strategy, denoted by , is expressed in terms of the scale functions.

Proposition 3.1

Given and , we have

(4)

and

(5)

Proof

Denote by the expected discounted total lump sum dividend payments, and we have

and

which yield

, i.e.

Hence

(6)

Denote by the expected discounted total capital injections. By a similar argument as that which derives (4.8) of Avram07 , one gets for

Collecting , (6), (7), and (8) yields (4) and (5) immediately. This completes the proof.

∎

Define, for ,

(9)

Then, .

The set of maximizers of is written as

(10)

Denote by

(11)

the first passage time of the Lévy process reflected at its supremum.

The following result gives a useful link between the second derivative of (in ) and the Laplace transform of .

Lemma 3.2

Let and be defined respectively by (9) and (11). We have

(12)

Proof

It follows from Proposition 2 (ii) of Pistorius04 that

For IDCI strategies and with and , let be defined via (2) with replaced by (i=1,2). Then, by (2), (3) and the technique of mathematical induction, we have,

for ,

By (18) and the definition of in (9), we may rule out the possibility that attains its maximum value in the line .

Indeed, if is a maximum point of with , then by (18) we should have , contradicting (17).

Now, we have proved that .

Thus, if is a maximizer of , then it holds that , i.e., (15) holds true.

∎

For an IDCI strategy , the following result, an immediate consequence of (4), (5), and (15), presents an alternative expression for the value function . It is interesting to see that this expression is independent of , which is not the case for arbitrary IDCI strategy (see (4) and (5)).

Proposition 3.4

For , the value function of the IDCI strategy

is

Remark 3.5

Given , one can verify that

is continuous over . If the scale function is differentiable, then one can also verify that

is continuous on and . However, is not evidently continuous at . In fact, twice differentiability at is not guaranteed even if continuous differentiability is imposed on .

Furthermore, if the scale function is only assumed to be piece-wise continuously differentiable over all compact subsets of (as in Lemmas 4.3-4.4 and Theorem 4.8), then is also piece-wise well-defined and piece-wise continuous.

∎

The following result characterizes several desirable properties of for .

Proposition 3.6

Given , is continuous and over , and

Proof

We readily have .

By , , and ,

one can verify

By Lemma 1 of Avram07 one has for , which, combined with and for , yields

In combination with these arguments, we reach for .

This section is devoted to verifying that an IDCI strategy serves as the optimal IDCI strategy dominating all other admissible IDCI strategies.

We first present a result characterizing the optimal value function , which helps with motivating the verification Lemma 4.4.

Proposition 4.1

The function is continuous and over .

Also, for .

Proof

By definition, any admissible IDCI strategy associated with the initial reserve also serves as an admissible IDCI strategy associated with the initial reserve . Then it follows from (2) that is non-decreasing.

For any and , one can find an admissible IDCI strategy such that

(20)

where because the latter is the minimum amount of capital injection needed to keep the reserve (applying dividend strategy ) being non-negative.

Define the admissible IDCI strategy

where is the time-shift operator. Then,

is indeed an admissible IDCI strategy associated with the initial reserve . Denote

Owing to the non-decreasing property of , it follows from (21) that

By setting and then (, respectively) in the above we reach continuity of .

For any and , denote an admissible IDCI strategy associated with the initial reserve such that .

Without loss of generality, is expressed as

where and are respectively the -th time and amount of dividend payout, and a.s. .

Define a new admissible strategy associated with the initial reserve such that and are characterized as

According to , we have

which yields after setting .

The inequality over can be proved if we have

which, in the case of (proof for the case of is quite similar), can be accomplished by considering an IDCI strategy that injects a capital of amount at time to the reserve process starting from .

∎

Put , , and . Define

which is a proper subset of . Intuitively, the condition

requires that the lump sum dividend paid at time is strictly greater than and is no more than the available reserve after covering the down-ward jump of at time , i.e., . For , it is seen that whenever .

The following result tells us that we can confine ourselves within when searching for the optimal IDCI strategy among . This finding is used in the proof of the verification Lemma 4.4.

Lemma 4.2

The optimal IDCI strategy lies in .

Proof

For any , one needs to find a such that

.

For this purpose, let

then one can see that and

(22)

Indeed, by the definition of , we have

which implies

(23)

At the same time, one has

It implies that

which combined with (23) and a choice of càdlàg version gives (22).

By (22) we have

(24)

Furthermore, there is a such that

or

at least one inequality in (24) is a strict inequality at . Otherwise, , contradicting the fact that .

The above arguments combined with (22) and the definition of yield

which completes the proof.

∎

As pointed out in Remark 3.5,

even if the continuous differentiability over is assumed on , the twice differentiability of at is still absent in general, as is the continuity of at .

Furthermore, imposing on the assumption of continuous differentiability over will exclude important sub-classes of spectrally negative Lévy processes. For example, for a spectrally negative compound Poisson process which has jumps of exact size

, the arrival rate , and a positive drift such that , the corresponding 0-scale function is identified by Asmussen00 and Hubalek11 as

with being the integer part of .

Note that the above example of scale function corresponds to a Lévy process that has sample paths of bounded variation and whose Lévy measure has atoms; otherwise, the scale function should be continuously

differentiable over .

In the sequel, it is assumed that is piece-wise continuously differentiable over all compact subsets of , i.e., for any , is continuously differentiable over , with being a non-negative integer. Hence, recalling that is linear over , one knows that is twice continuously differentiable over with and being an integer.

For any function for some integer , define an operator acting on as

for .

Also, define a sequence of mollified functions (of ) as

(25)

where and with .

In order to verify the optimality of a particular IDCI strategy producing the value function , which lacks twice continuous differentiability at finitely many points , we need a modified version of verification argument, i.e., Lemma 4.4. Before presenting this verification argument, we show the following Lemma 4.3.

Lemma 4.3

Let be a function such that

(26)

and

(27)

with and being a non-negative integer.

Suppose that

(28)

and

(29)

then defined through (25) are twice differentiable over , satisfy (28) and

(30)

and

(31)

Proof

It is a direct consequence of differentiation under

the integral sign. The proof is omitted. ∎

Now we are ready to present the following verification argument. For this purpose, let be a candidate optimal admissible IDCI strategy with value function . We extend the domain of to the entire real line by setting for . With a little abuse of notation, the extended function is still denoted by .

Lemma 4.4 (Verification)

If the function defined over

fulfills (26), (27), (28), and (29),

then is the optimal strategy, and .

Proof

By Lemma 4.2, we only need to prove that dominates all strategies among .

Let and be the continuous part of and , respectively. Let, for

be the sequence of localization stopping times. Then, for all , it holds that

(32)

i.e., both and are restricted to the bounded compact set .

Let be defined via (25) with replaced by . Hence, is twice differentiable over , and satisfies (28) and (30).

By Theorem 4.57 (Itô’s formula) in Jacod02 , we have, for and ,

(33)

where and . Due to , one knows that implies a jump of at time (i.e., whenever there is a jump in , there must be a jump in ).

By (28) and the fact that , we have, for ,

(34)

(35)

Therefore, by (28), (30), (33), (34), and (35), we have

(36)

In addition, according to Ikeda81 (page 62), the compensated sum

is an -martingale with zero mean. Indeed, the integrand of the above stochastic integration is bounded from below and above owing to (32) and

where we have used and the second equality in (25).

Similarly, the integration

is also an -martingale with zero mean.

Taking expectations on both sides of (36), we have

By setting in (37), and then using (31) and the bounded convergence theorem ( is bounded), we get

By the arbitrariness of , it follows that

for all ,

which, along with the continuity of and (see Proposition 4.1), implies

Hence, by assumption we reach

Since the reverse of the above inequality is trivial, we conclude with the desired equality. The proof is completed.

∎

Remark 4.5

Because lacks twice differentiability at , an appropriate generalized version of the Itô’s lemma such as the

Itô-Tanaka-Meyer formula (see Protter95 ) should be applied to prove the verification argument.

In our case, we employed an alternative mollifying technique (see Lemmas 4.3 and 4.4) to deal with

the difficulty of lack of sufficient differentiability.

The mollifying arguments given in Lemmas 4.3 and 4.4 are rigorous and differ from the approach adopted in Junca18 when proving their verification theorem.

∎

The following Lemma 4.6 and Lemma 4.7 are useful for characterizing the optimal IDCI strategy and the associated optimal value function in Theorem 4.8.

Lemma 4.6

Given , we have

(38)

Proof

It is seen that

(39)

where .

By (13) and we know that decreases in with .

Let be the unique zero of the function when , then the inequality (38)

is equivalent to

Since holds trivially, we only need to show that holds when .

Given , by (39) and the decreasing property of , the function is increasing (decreasing) over (), and attains its maximum at . So, when we must have . Further, when we should have

. Otherwise, will be in the range , which leads to

This result contradicts the fact that attains its maximum at , so . The proof is completed.

∎

In the sequel, we extend the function to the entire real axis by setting for . We denote by the value function of the barrier dividend and capital injection strategy with barrier level and initial reserve (cf., Equation (5.4) in Avram07 ), i.e.,

The following theorem characterizes the optimal IDCI strategy among all admissible IDCI strategies. The ideas in the proof are partly obtained from Avram07 and Loeffen08 . This theorem shows that any IDCI strategy is optimal and dominates all admissible IDCI strategies.

Theorem 4.8

Suppose that the scale function is piece-wise continuously differentiable over all compact subsets of .

Let . Then the strategy is optimal among all admissible IDCI strategies.

Proof

By the fact that the scale function is left and right differentiable over (see for example, Lemma 1 in Pistorius04 ), Remark 3.5, and the extended definition for , one can verify that satisfies (27).

Let () be the first up-crossing (down-crossing) time of level () by the process

(41)

By Proposition 3.6, we need only to prove

for . Here, with is the set of points where the continuous differentiability is absent for .

Given , without loss of generality we may assume for some .

Let with and defined via (41). By the strong Markov property of the process , we have

which implies that the right-hand side of the above equation is a martingale.

Here, we have used the fact that no dividends are paid out and no capital is injected during the time interval ; i.e., for .

The martingale property of the process implies

(42)

Indeed, for and , Itô’s formula gives

Taking expectations on both sides of the above display after localization, we have

Being divided by on both sides and then setting in the above equation, we get (42) for by the mean value theorem together with the dominated convergence theorem. For a more detailed proof of (42), we can also turn to Proposition 2.1 of Hojgaard99 . Thus, it suffices to further prove

(43)

By using similar arguments as those used in proving (42) we can get

which implies

(44)

where is well-defined due to (40).

Meanwhile, because the function is continuous over (actually, for , see Proposition 3.4), we have

(45)

Combining (44) and (45), to prove (43) it suffices to show

For , we can use the dominated

convergence theorem to deduce

By (48) one can verify that

,

excluding the possibility for the maximizer of to lie on the line .

Since it is proved (cf., Proposition 3.3) that the maximizer of cannot be attained on the line , we claim that the is maximized at an interior point of the set for some bounded (see the arguments immediately following (10)).

Thus, if is the maximizer of , then (47), (49) and (51) should hold simultaneously.

Combining (49) and (51) yields

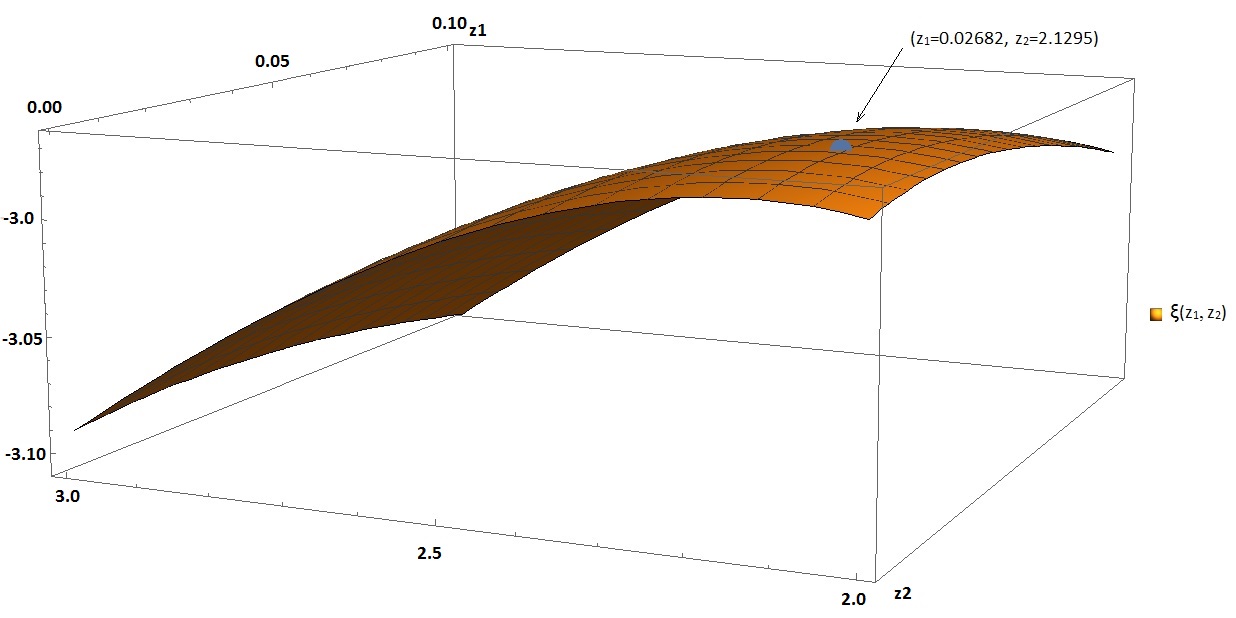

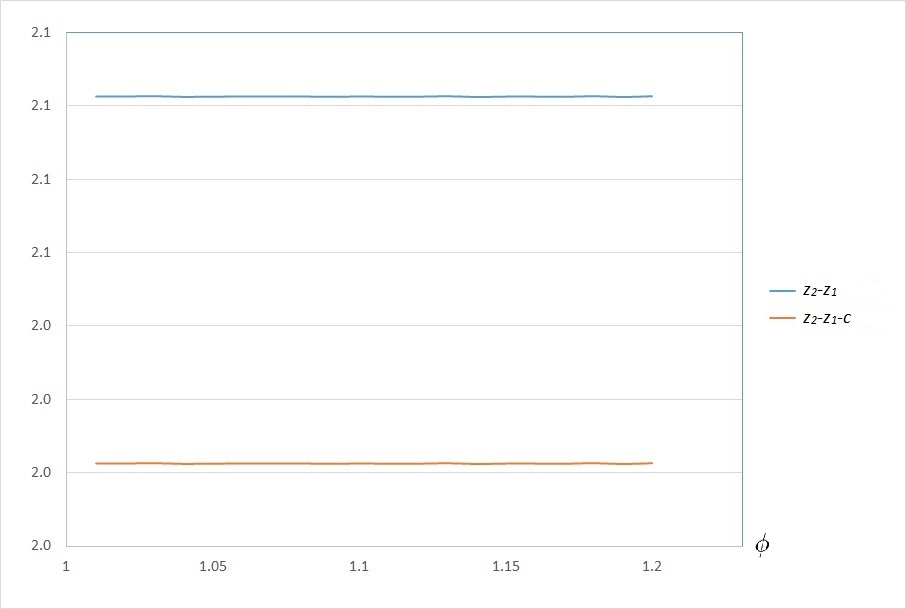

Now, we are ready to present the numerical results. First, we set , and . Numerically, (52) and (53) are uniquely solved by , a maximizer of . According to the previous argument, it must be the maximizer of . In fact, by routine calculus we can verify that, at ,

and hence

,

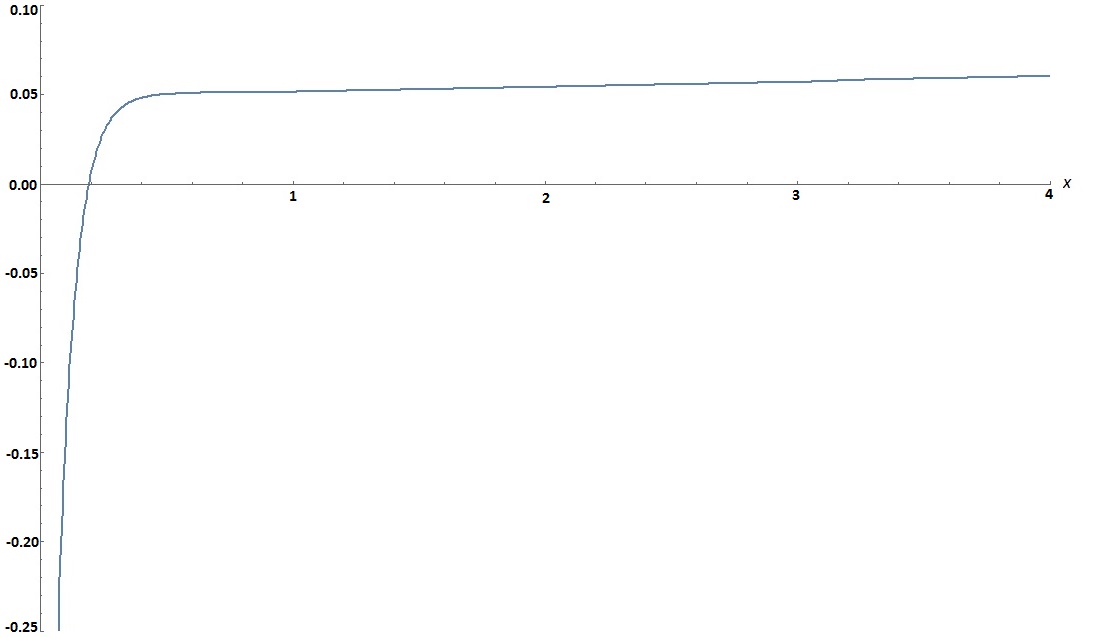

verifying that is the maximizer of . This is also confirmed in Figure 1(a). Also, as seen in Figure 1(b),

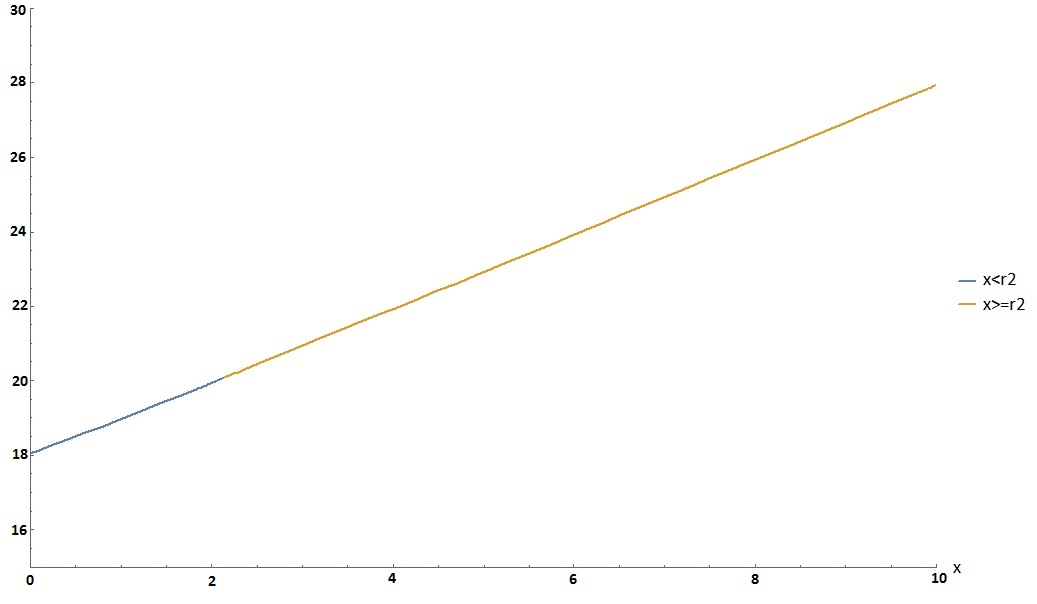

With the optimal strategy, we can plot its associated value function . According to Proposition 3.2, we have

It is observed in Figure 2(a) that the segment in blue (i.e. ) is shaped similar to a straight line, even though its underlying function is actually a combination of exponential functions.

(a)Curve of

(b)Optimal lump sum dividend amount w.r.t.

Figure 2: Function and optimal dividends

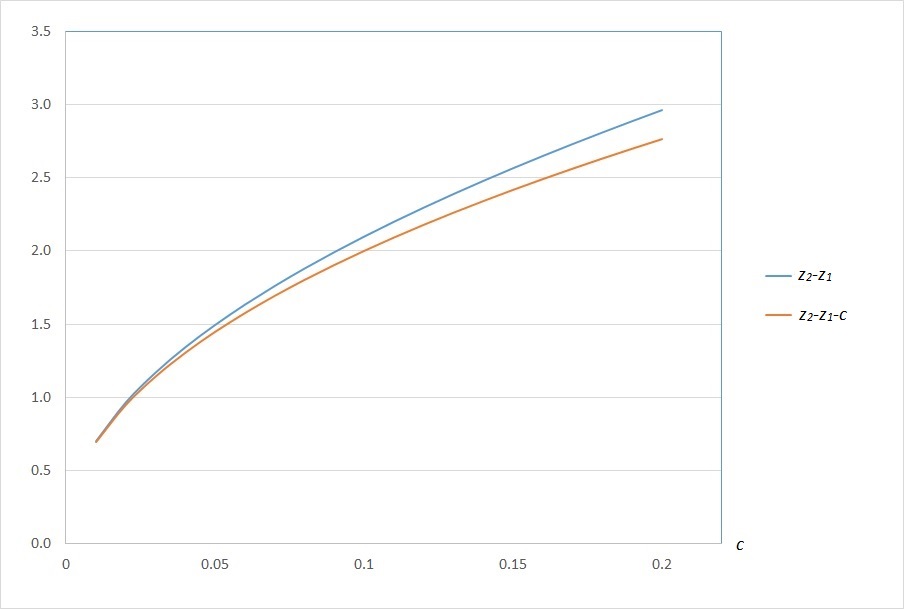

Next, let us examine the parameter sensitivity concerned with and , both playing a critical role in our model. To avoid repetitiveness, we omit the checking arguments of the maximizers of . Also, for ease of comparison, we set , and thereafter. For , in Table 1 of the maximizer of for , is seen to have a slow but steady downward trend when increases while has a solid upward trend. Further, in Figure 2(b), the individual dividend amount and the net individual dividend amount both display a solid increasing trend when the transaction cost increases. This is reasonable because the better way of paying dividends is to pay out more each time with a higher dividend threshold when transaction cost increases.

0.01

0.06002

0.76463

0.11

0.02583

2.22967

0.02

0.04818

1.01761

0.12

0.02496

2.32560

0.03

0.04195

1.21568

0.13

0.02418

2.41782

0.04

0.03787

1.38447

0.14

0.02348

2.50673

0.05

0.03491

1.53426

0.15

0.02284

2.59269

0.06

0.03262

1.67044

0.16

0.02226

2.67598

0.07

0.03077

1.79622

0.17

0.02172

2.75685

0.08

0.02924

1.91373

0.18

0.02123

2.83550

0.09

0.02794

2.02447

0.19

0.02077

2.91212

0.10

0.02682

2.12950

0.20

0.02034

2.98686

Table 1: Maximizer of with respect to when

1.01

0.00635

2.10904

1.11

0.04877

2.15145

1.02

0.01212

2.11481

1.12

0.05179

2.15447

1.03

0.01741

2.12010

1.13

0.05467

2.15736

1.04

0.02229

2.12497

1.14

0.05743

2.16011

1.05

0.02682

2.12950

1.15

0.06008

2.16276

1.06

0.03104

2.13373

1.16

0.06262

2.16530

1.07

0.03501

2.13769

1.17

0.06506

2.16774

1.08

0.03873

2.14142

1.18

0.06741

2.17010

1.09

0.04226

2.14494

1.19

0.06968

2.17236

1.10

0.04559

2.14828

1.20

0.07187

2.17456

Table 2: Maximizer of with respect to when

Figure 3: Optimal lump sum dividend amount w.r.t.

For , Table 2 lists the maximizer for . Both and are seen to have steady upward trends when increases. However, and in this case almost keep constant no matter how changes. As seen in Figure 3, when the cost of capital injection goes up, it is more beneficial to have a higher dividend threshold, which partially reduces the chance of needing capital injection. Also, the increasing trend of upon lowers the negative impact of dividends on the solvency of the insurer, while at the same time helping the company to reduce the need of additional capital. On the other hand, the amount of money paid out in each dividend does not depend on , but on the value of which has been observed in the previous case.

Acknowledgements.

The authors are grateful to the anonymous referees for their very careful reading of the paper, and for their very constructive and helpful suggestions and comments.

The authors are also grateful to Professor Xiaohu Li in the Department of Mathematical Sciences at the Stevens Institute of Technology (USA) for helping to polish the English writing of this paper.

References

(1) Albrecher, H., Thonhauser, S.: Optimality results for dividend problems in insurance. Rev. R. Acad. Cien. Serie A. Mat. 103(2), 295-320 (2009).

(2) Avanzi, B.: Strategies for dividend distribution: A review. N. Am. Actuar. J. 13(2), 217-251 (2009).

(3) De Finetti, B.: Su un’impostazion alternativa dell teoria collecttiva del rischio. In Trans. XVth Internat. Congress Actuaries 2, 433-443 (1957).

(4) Bai, L., Guo, J.: Optimal dividend payments in the classical risk model when payments are subject to both transaction costs and taxes. Scand. Actuar. J. 2010(1), 36-55 (2010).

(5) Zhou, M., Yiu, K.: Optimal dividend strategy with transaction costs for an upward jump model. Quant. Financ. 14(6), 1097-1106 (2014).

(6) Bai, L., Paulsen, J.: Optimal dividend policies with transaction costs for a class of diffusion processes, SIAM J. Control Optim. 48, 4987-5008 (2010).

(7) Loeffen, R.: An optimal dividends problem with transaction costs for spectrally negative Lévy processes. Insur. Math. Econ. 45, 41-48 (2009).

(8) Bayraktar, E., Kyprianou, A., Yamazaki, K.: Optimal dividends in the dual model under transaction costs. Insur. Math. Econ. 54, 133-143 (2014).

(9) Hernández, C., Junca, M., Moreno-Franco, H.: A time of ruin constrained optimal dividend problem for spectrally one-sided Lévy processes. Insur. Math. Econ. 79, 57-68 (2018).

(10) Avram, F., Palmowski, Z., Pistorius, M.: On Gerber-Shiu functions and optimal dividend distribution for a Lévy risk process in the presence of a penalty function.

Ann. Appl. Probab. 25(4), 1868-1935 (2015).

(11) Zhao, Y., Wang, R., Yao, D., Chen, P.: Optimal dividends and capital injections in the dual model with a random time horizon. J. Optimiz. Theory App. 167, 272-295 (2015).

(12) Guan, H., Liang, Z.: Viscosity solution and impulse control of the diffusion model with reinsurance and fixed transaction costs. Insur. Math. Econ. 54, 109-122 (2014).

(13) Hunting, M., Paulsen, J.: Optimal dividend policies with transaction costs for a class of jump-diffusion processes. Financ. Stoch. 17(1), 73-106 (2013).

(14) Avanzi, B., Shen, J., Wong, B.: Optimal dividends and capital injections in the dual model with diffusion. ASTIN Bull. 41(2), 611-644 (2011).

(15) Yao, D., Yang, H., Wang, R.: Optimal dividend and capital injection problem in the dual model with proportional and fixed transaction costs. Eur. J. Oper. Res. 211(3), 568-576 (2011).

(16) Peng, X., Chen, M., Guo, J.: Optimal dividend and equity issuance problem with proportional and fixed transaction costs. Insur. Math. Econ. 51(3), 576-585 (2012).

(17) Zhao, Y., Wang, R., Yin, C.: Optimal dividends and capital injections for a spectrally positive Lévy process. J. Ind. Manag. Optim. 12(4), 1-21 (2017).

(18) Zhao, Y., Chen, P., Yang, H.: Optimal periodic dividend and capital injection problem for spectrally positive Lévy processes. Insur. Math. Econ. 74, 135-146 (2017).

(19) Zhu, J.: Optimal financing and dividend distribution with transaction costs in the case of restricted dividend rates. ASTIN Bull. 47(1), 239-268 (2017).

(20) Avram, F., Pérez, J., Yamazaki, K.: Spectrally negative Lévy processes with Parisian reflection below and classical reflection above. Stoch. Proc. Appl. 128(1), 255-290 (2018).

(21) Avanzi, B., Pérez, J., Wong, B., Yamazaki, K.: On optimal joint reflective and refractive dividend strategies in spectrally positive Lévy models. Insur. Math. Econ. 72, 148-162 (2017).

(22) Yin, C., Yuen, K.: Optimal dividend problems for a jump-diffusion model with capital injections and proportional transaction costs. J. Ind. Manag. Optim. 11(4), 1247-1262 (2015).

(23) Bayraktar, E., Kyprianou, A.E., Yamazaki, K.: On optimal dividends in the dual model. ASTIN Bull. 43(3), 359-372 (2013).

(24) Avram, F., Palmowski, Z., Pistorius, M.: On the optimal dividend problem for a spectrally negative Lévy process. Ann. Appl. Probab. 17, 156-180 (2007).

(25) Loeffen, R.: On optimality of the barrier strategy in de Finetti’s dividend problem for spectrally negative Lévy processes. Ann. Appl. Probab. 18, 1669-1680 (2008).

(26) Loeffen, R.: An optimal dividends problem with a terminal value for spectrally negative Lévy processes with a completely monotone jump density. J. Appl. Probab. 46(1), 85-98 (2009).

(27) Loeffen, R., Renaud J.: De Finetti’s optimal dividends problem with an affine penalty function at ruin. Insur. Math. Econ. 46(1), 98-108 (2010).

(28) Kyprianou, A., Palmowski, Z.: Distributional study of de Finetti’s dividend problem for a general Lévy insurance risk process. J. Appl. Probab. 44(2), 428-443 (2007).

(29) Renaud, J., Zhou, X.: Distribution of the present value of dividend payments in a Lévy risk model. J. Appl. Probab. 44, 420-427 (2007).

(30) Kyprianou, A., Loeffen, R., Pérez, J.: Optimal control with absolutely continuous strategies for spectrally negative Lévy processes. J. Appl. Probab. 49(1), 150-166 (2012).

(31) Boguslavskaya, E.: Optimization problems in financial mathematics: Explicit solutions for diffusion models. Doctoral Thesis, University of Amsterdam (2008).

(32) Thonhauser, S., Albrecher, H.: Dividend maximization under consideration of the time value of ruin. Insur. Math. Econ. 41, 163-184 (2007).

(33) Azcue, P., Muler, N.: Optimal reinsurance and dividend distribution policies in the Cramér Lundberg model. Math. Financ. 15, 261-308 (2005).

(35) Yin, C., Wen, Y.: Optimal dividend problem with a terminal value for spectrally positive Lévy processes. Insur. Math. Econ. 53(3), 769-773 (2013).

(36) Junca, M., Moreno-Franco, H., Pérez, J.: Optimal bail-out dividend problem with transaction cost and capital injection constraint. Risks 7(1), 13 (2019).

(37) Bertoin, J.: Lévy Processes. Cambridge University Press, Cambridge (1996).

(38) Pistorius, M.: On exit and ergodicity of the spectrally one-sided Lévy process reflected at its infimum. J. Theor. Probab. 17(1), 183-220 (2004).

(39)

Kyprianou, A.: Introductory Lectures on Fluctuations of Lévy Processes with Applications. Springer,

Berlin (2006).

(40)

Wang, W., Zhou, X.: General draw-down based de Finetti optimization for spectrally negative Lévy risk processes. J. Appl. Probab. 55(2), 513 C542 (2018).

(41) Asmussen,S.: Ruin Probabilities. World Scientific Publishing, Singapore (2000).

(42)

Hubalek, F., Kyprianou, A.: Old and new examples of scale functions for spectrally negative Lévy processes. In Sixth Seminar on Stochastic Analysis, Random

Fields and Applications (R. Dalang, M. Dozzi and F. Russo, Eds.) 119-145. Springer, Basel (2011).