Confidence Intervals for Stochastic Arithmetic

Abstract

Quantifying errors and losses due to the use of Floating-Point (FP) calculations in industrial scientific computing codes is an important part of the Verification, Validation and Uncertainty Quantification (VVUQ) process. Stochastic Arithmetic is one way to model and estimate FP losses of accuracy, which scales well to large, industrial codes. It exists in different flavors, such as CESTAC or MCA, implemented in various tools such as CADNA, Verificarlo or Verrou. These methodologies and tools are based on the idea that FP losses of accuracy can be modeled via randomness. Therefore, they share the same need to perform a statistical analysis of programs results in order to estimate the significance of the results.

In this paper, we propose a framework to perform a solid statistical analysis of Stochastic Arithmetic. This framework unifies all existing definitions of the number of significant digits (CESTAC and MCA), and also proposes a new quantity of interest: the number of digits contributing to the accuracy of the results. Sound confidence intervals are provided for all estimators, both in the case of normally distributed results, and in the general case. The use of this framework is demonstrated by two case studies of industrial codes: Europlexus and code_aster.

1 Introduction

Modern computers use the IEEE-754 standard for implementing floating point (FP) operations. Each FP operand is represented with a limited precision. Single precision numbers have 23 bits in the fractional part and double precision numbers have 52 bits in the fractional part. This limited precision may cause numerical errors [higham2002accuracy] such as absorption or catastrophic cancellation which can result in loss of significant bits in the result.

Floating Point computations are used in many critical fields such as structure, combustion, astrophysics or finance simulations. Determining the precision of a result is an important problem. For well known algorithms, bounds of the numerical error can be derived mathematically for a given dataset [higham2002accuracy].

The Stochastic Arithmetic field proposes automatic methods for estimating the number of significant digits for complex programs. Two main methods have been proposed: CESTAC [VIGNES2004] and Monte Carlo Arithmetic (MCA) [PARKER1997], which differ in many subtle ways, but share the same general principles. Numerical errors are modeled by introducing random perturbations at each FP operation. This transforms the output of a given simulation code into realizations of a random variable. Performing a statistical analysis of a set of sampled outputs allows to stochastically approximate the impact of numerical errors on the code results.

In this paper, we propose a solid statistical analysis of Stochastic Arithmetic that does not necessarily rely on the normality assumption and provides strong confidence intervals. As stated in [PARKER1997, p.45], “MCA is not committed to any assumption of normality. Sampling is an art and the right approach to sampling can settle very tricky problems.” and, a little further: “MCA is not committed to a statistical inference model”. Unlike traditional analysis which only considers the number of reliable significant digits, this paper introduces a new quantity of interest: the number of digits contributing to the accuracy of the final result.

Section 2 reviews the stochastic arithmetic methods. Section 3 formulates the problem rigorously and defines several interesting scopes of study. Then we provide in section 4 a statistical analysis for normal distributions and in section 5 for general distributions. Section 6 validates our statistical framework on two industrial scientific computing codes: Europlexus and code_aster. Finally, section LABEL:sec:limitations discusses some of the remaining limitations of stochastic arithmetic methods, which should be addressed in future work.

2 Background on Stochastic Arithmetic Methods

Automatic methods for deriving bounds on round-off errors can be loosely categorized into two categories: exact methods and approximate methods.

Exact methods give a conservative and proven bound on the error of a computation. One well established exact method for deriving error bounds is Interval Arithmetic [moore2009introduction], in which each real value in the algorithm is replaced by an interval that contains all the possible values of the computation. The operations are redefined to handle intervals operands and guarantee that the resulting interval provide rigorous bounds on the computation. Multiple software frameworks [rump1999intlab, revol2005motivations] for interval arithmetic have been released. Interval arithmetic have been applied to derive error bounds and optimize numerical methods [moore1979methods, kahan1996improbability], linear algebra [hansen1965interval], and physical simulation [dessombz2001analysis]. Because intervals are conservative, they tend to become overly large when the algorithm or control flow is complex. It is possible to refine the analysis by considering a union of interval subdivisions [hickey2001interval] or more sophisticate objects such as zonotopes [goubault2006static]; nevertheless in general for complex computer programs of thousands of code lines, deriving such an analysis is intractable. Exact approaches also include floating point proof assistants [de2006assisted, boldo2009combining, boldo2011flocq] which can derive semi-automatic certified proofs on floating point errors on small programs.

On the other hand, approximate methods, do not provide deterministic bounds on the numerical error and may not always model exactly IEEE-754 behavior but are able to efficiently analyze large and complex programs, such as found in industrial codebases. For a more detailed comparison between stochastic and exact numerical analysis methods please refer to [kahan1996improbability] and [PARKER1997, p. 71]. This paper contributions focus solely on the stochastic arithmetic methods, which we will present in the following.

2.1 Modeling accuracy loss using randomness

When a program is run on an IEEE-754-compliant processor, the result of each floating-point operation is replaced by a rounded value: . For example, the default rounding mode for IEEE-754 binary formats is given by:

where denotes rounding to nearest, ties to even, for the considered precision (binary32 or binary64).

When , i.e. when is not in the set of representable FP values for the considered precision, rounding causes a loss of accuracy. Stochastic arithmetic methods model this loss of accuracy using randomness.

2.1.1 CESTAC

The CESTAC method models round-off errors by replacing rounding operations with randomly rounded ones [VIGNES1974, chesneauxvignes]. The result of each FP operation is substituted with , where random_round is a function which randomly rounds FP values upwards or downwards equiprobably:

where and respectively represent the downward and upward rounding operations for the considered precision, and is a random variable such that . CESTAC proposes different variants by changing the probability distribution .

2.1.2 Monte Carlo Arithmetic

MCA can simulate the effect of different FP precisions by operating at a virtual precision . To model errors on a FP value at virtual precision , MCA uses the noise function

where is the order of magnitude of and is a uniformly distributed random variable in the range . During the MCA run of a given program, the result of each FP operation is replaced by a perturbed computation modeling the losses of accuracy [PARKER1997, verificarlo, frechtling2014tool]. It allows to simulate the computation at virtual precision . Three possible expressions can be substituted to , defining variants of MCA:

-

1.

“Random rounding” only introduces perturbation on the output:

-

2.

“Inbound” only introduces perturbation on the input:

-

3.

“Full MCA” introduces perturbation on operand(s) and the result:

In any case, using stochastic arithmetic, the result of each FP operation is replaced with a random variable modeling the losses of accuracy resulting from the use of finite-precision FP computations. Since the result of each FP operation in the program is in turn used as input for the following FP operations, it is natural to assume that the outputs of the whole program in stochastic arithmetic are random variables.

Stochastic Arithmetic methods run the program multiple times in order to produce a set of output results (i.e. a set of realizations or samples of the random variable modeling the program output). The samples are then statistically analyzed in order to assess the quality of the result.

2.2 Estimating the result quality: significant digits

Let us denote by the quantity computed by a deterministic numerical program. Different values can be defined for this result:

-

•

is the value of that would be computed with an infinitely precise, real arithmetic;

-

•

is the value that is computed by the program, when run on a computer that uses standard IEEE arithmetic with default rounding;

-

•

are the values returned by runs of the program using stochastic arithmetic. These are seen as realizations of the same random variable .

Figure 1 illustrates some of the quantities of interest that can be useful to analyze the quality of the results given by the program. The real density of random variable is unknown, but some of its characteristics can be estimated using sample values . In particular:

-

•

the expected value can be estimated by the empirical average value of , ;

-

•

the standard deviation can be estimated by the empirical standard deviation, .

To estimate the numerical quality of the result, we would like to compute the number of significant bits. In the following we review the definitions of significance used in CESTAC and MCA. Then, we introduce the definition that will be used in this paper.

2.2.1 CESTAC definition of significant bits

In CESTAC, the average of the small set of samples (usually three) is taken as the computed result, and the analysis then estimates the accuracy of this quantity, seen as an approximation of .

Definition 1.

With the notations defined above, the CESTAC number of exact significant bits [VIGNES2004] is defined as the number of bits in common between and :

In order to estimate the number of exact significant digits, the CESTAC analysis is based on two hypotheses:

-

1.

the distribution is normal, and

-

2.

the distribution is centered on the real result .

Since is assumed normal, one can derive the following Student t-distribution interval with confidence :

where is the quantile of the Student distribution with degrees of freedom.

The maximum error between and is bounded by this interval for a normal distribution; it follows [Li2013Numerical] that an estimated lower bound for the number of exact significant bits is given by

| (1) |

This definition suffers from a few shortcomings. First, the two hypotheses, while reasonable in many cases, do not always hold [chatelin88, kahan1996improbability]: Stott Parker shows that the normality assumption of is not always true [PARKER1997, p. 49] and it is not necessarily centered on the real result. The robustness of CESTAC with respect to violations of these hypotheses is discussed in [chesneauxvignes].

Second, and more important, the CESTAC definition of the number of significant digits may not necessarily be the most useful for the practitioner. Oftentimes, the objective of the numerical verification process consists in evaluating the precision of the actual IEEE computer arithmetic. CESTAC does not evaluate the number of significant digits of the IEEE result but rather of the average of the CESTAC samples. But in practice, does not match .

Last, with this definition, a problem clearly appears when considering the asymptotic behavior of the bound: . Increasing the number of samples arbitrarily increases the number of significant digits computed by CESTAC. On the one hand, this is expected because, according to the definition proposed, any computation is actually infinitely precise when since the strong law of large numbers states that the empirical average is in this case almost surely the expected value. On the other hand, however, this asymptotic case also questions the pertinence of the CESTAC metric for the evaluation of the quality of the results produced by IEEE-754 computations. CESTAC is usually applied to three samples [chesneauxvignes], the validity of the special case where is discussed in section 4.3.

2.2.2 MCA definition of significant bits

In his study of MCA, Stott Parker proposes another definition for the number of significant digits. Stott Parker lays this definition on the habits of biology and physics regarding the precision of a measurement: if an MCA-instrumented program is seen as a measurement instrument111In most applications, a measurement is modeled by a random variable following a normal distribution., then the number of significant digits can be defined as the number of digits expected to be found in agreement between successive runs/measurements.

Definition 2.

With the notations defined above, the MCA number of significant bits is defined as

This definition, which computes the magnitude of the coefficient of variation, is a form of signal to noise ratio: if most random samples share the same first digits, these digits can be considered significant. On the contrary, digits varying randomly among sampled results are considered noise. Another way of giving meaning to this definition is to consider as one possible realization of the random variable . As such, its distance to is characterized by . A problem with the MCA definition of significant bits is that it is empirical: the actual meaning of “significance” is not clearly laid, as well as the consequences one can draw from it.

The MCA number of significant bits can be estimated by

| (2) |

a quantity which can be computed regardless of any hypothesis on the distribution of . However, since the number of samples is finite, is only an approximation of the exact value . And no confidence interval is provided in order to help choose an appropriate number of samples. As shall be seen in section 4.3, this estimate is nevertheless a good basis when the underlying phenomenon is normal.

Our definition of significance generalizes Stott Parker’s. It requires a reference which can be either a scalar value222Good choices for the scalar reference are , or depending on the aims of the study or another random variable333Using a second random variable as reference allows comparing two versions of a program or two algorithms variants, more details are given in section 3.. Informally, in this paper, the significant digits are the digits in common between the samples of and the reference (up to a rounding effect on the last significant digit). Section 3 formalizes this definition in a probabilistic framework and provides sound confidence intervals.

2.3 Software tools presentation

The experimental validation of the presented confidence intervals on synthetic and industrial use cases has been conducted thanks to the Verificarlo and Verrou tools which are presented in the next subsections.

2.3.1 Verificarlo

Verificarlo [verificarlo, verificarloproject] is an open-source tool based on the LLVM compiler framework replacing at compilation each floating point operation by custom operators. After compilation, the program can be linked against various backends [Chatelain2018veritracer, Chatelain2019automatic, Defour2020CustomPrecision], including MCA to explore random rounding and virtual precision impact on an application accuracy.

Doing the interposition at compiler level allows to take into account the compiler optimization effect on the generated FP operation flow. Furthermore, it allows to reduce the cost of this interposition by optimizing its integration with the original code.

2.3.2 Verrou

Verrou [fevotte2016, verrouproject] is an open-source floating point diagnostics tool. It is based on Valgrind [nethercote2007] to transparently intercept floating point operations at runtime and replace them by their random rounding counterpart. The interposition at runtime allows to address large and complex-code applications with no intervention of the end-user.

Verrou also provides two methods allowing to locate the origin of precision losses in the sources of the analyzed computing code. The first one is based on the code coverage comparison between two samples. Discrepancies in the code coverage are good indicators of potential branch instabilities. The second localization method leverages the delta-debugging algorithm [zeller2009] to perform a binary search to find a maximal scope for which MCA perturbations do not produce errors or large changes in results. The remaining symbols (or lines if the binary is compiled with debug mode) are good candidates for correction.

2.4 Synthetic example: Ill-conditioned linear system

To illustrate these methods in the following we use a simple synthetic example proposed by Kahan [KAHAN66]: solving an ill-conditioned linear system,

| (3) |

The exact and IEEE binary64 solutions of equation (3) are:

| (4) |

To keep the example simple, the floating-point solution has been obtained by solving the system with the naive C implementation of Cramer’s formula in double precision, as shown in listing 1.

The condition number of the above system is approximately , therefore we expect to lose at least bits of accuracy or, equivalently, decimal digits. By comparing the IEEE and exact values, we see that indeed the last decimal digits differ. The number of common bits between and is given by

Now let us use MCA to estimate the number of significant digits. We compile the above program with Verificarlo [verificarlo] which transparently replaces every FP operation by its noisy MCA counterpart. Here a virtual precision of 52 is used to simulate roundoff errors. Then, we run the produced binary times and observe the resulting output distribution .

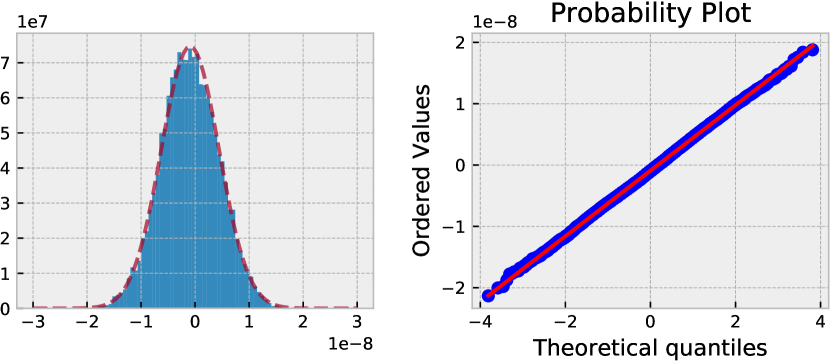

Both and are normal with high Shapiro-Wilk test p-values 73 % and 74 % respectively.444Interestingly fails the Anderson-Darling test, 27 % p-value, due to some anomalies on the tail. Figure 2 shows the distribution and quantile-quantile (QQ) plots for , for which the empirical average and standard deviation are given by

Using Stott Parker’s formula (2) to compute for , we get a figure close to the expected value :

| (5) |

But how confident are we that is a good estimate of ? Could we have used a smaller number of samples and still get a reliable estimate of the results quality?

On the other hand, using these samples to compute the CESTAC lower bound defined in equation (1) with confidence 95 % gives

| (6) |

which is a clear overestimation of the quality of the IEEE result, but also of the CESTAC result, since the number of bits in common between the real result and the sample average is given by

Such a large exhibits the bias between and , invalidating the CESTAC hypotheses. In practice, CESTAC implementations such as CADNA use , a choice of which the validity is discussed in section 4.3. For the Cramer benchmark, computing for only 3 samples of X[0] yields a conservative estimate:

In the following, we present a novel probabilistic formulation to get a confidence interval for the number of significant bits with and without assumption of normality.

3 Probabilistic accuracy of a computation

3.1 Definitions

We consider one output of a program performing FP operations as a random variable . The output is a random variable either because the program is inherently nondeterministic or because we are artificially introducing numerical errors through MCA, CESTAC, or another stochastic arithmetic model. We want to study how the probabilistic properties of the computation impact its accuracy. The real distribution of is unknown but we can approximate it with samples, .

The accuracy of a result must be defined against a reference value. If a real mathematical result is known, it is a natural choice. If the program is deterministic when executed in IEEE arithmetic, the IEEE result is one straightforward choice for the reference value. If the program is nondeterministic, one can also choose as reference, the empirical average of . Finally a third option consists in computing the accuracy against a second random variable , which allows computing the accuracy between runs of the same program or allows finding the accuracy between two different programs, such as when comparing two different versions or implementations of an algorithm. We will write the reference value when it is a constant and when it is another random variable.

Four types of studies can be led, depending on whether we are interested in absolute or relative error, and whether we have a reference value. For each study we can model the errors as a random variable defined as follows

| reference | reference | |

|---|---|---|

| absolute precision | ||

| relative precision |

We have reduced the four types of problems to study the probabilistic properties of whose error distribution represents the error of a computation in a broad sense. If is unbiased wrt. the reference, (a constant reference can be for instance the exact result of a computation that introduces a bias, for instance when a division by a value close to 0 occurs; in such cases we observe ).

To define the significance of a digit we use Stott Parker’s ulsp algorithm [PARKER1997, p. 19]. The significant bit is at the rightmost position at which the digits differ by less than one half unit in the last place. That is to say, two values and have significant digits555A non-strict inequality is often used in this definition. Under the assumption made by most previous works that the underlying distribution is continuous (e.g. normal), both definitions agree. We chose a strict inequality that better fits with the notion of contributing digit that we introduce. iff

| (scaled absolute error) | |||||

| (relative error) | (7) |

Without loss of generality, to unify the definition for the relative and scaled absolute cases, in the following sections we assume . When working with absolute errors, one should therefore shift the number of digits by , the normalizing term666When is a random variable, we choose ..

The first quantity of interest is the probability that the result is significant up to a given bit for a stochastic computation. The stochastic computation can be for example a program instrumented with CESTAC or MCA. By generalizing equation 7 to random variables, we define the probability of the -th digit being significant as .

Definition 3.

For a given stochastic computation, the -th bit of is said to be significant with probability if

The number of significant digits in with probability is defined as the largest number such that

Note that, by definition, if the -th bit of is significant with probability , then any bit of rank is also significant with probability . In the remainder of this paper, when not otherwise specified, the simple notation will refer to the notion defined above.

The second quantity we will consider is the probability that a given bit contributes to the precision of the result: even if a bit on its left is already wrong, a bit can either improve the result precision, or deteriorate it. As noted in [PARKER1997, p.45]: ”In other words, in inexact values it can be worthwhile to carry a nontrivial number of random least significant bits”. Because the expected result of is 0, a bit will improve the accuracy if it is 0 and deteriorate it if it is 1.

Definition 4.

The -th bit of is said to be contributing with probability if and only if it is with this probability, i.e. if and only if

Now, the -th bit of is 0 if and only if there exists an integer such that,

| (8) |

One should note that the notions of significance and contribution are distinct, but related: if there are significant bits with probability , then all bits at ranks are contributing, with probability . Indeed,

However, the -th bit of being contributing with probability does not imply that all bits at ranks are also contributing777Although, it is the case for example when follows a Gaussian distribution.. This prevents the definition of such a notion as the number of contributing bits.

3.2 Summary of the results

In the remainder of this paper, we obtain the following results, unifying the various definitions of significance seen above and generalizing their validity to the non-Gaussian case.

Under the Centered Normality Hypothesis (CNH), i.e. if follows a Gaussian law centered around the reference value or, equivalently, if follows a Gaussian law centered around , it is shown in section 4.1 that a lower bound of the number of significant digits (as introduced in definition 3) with probability and confidence level is given by

where denotes the standard deviation of samples of , and all notations are relatively standard and are introduced in section 4. Furthermore, the following results are established:

-

•

can be computed simply by shifting the usual estimator (introduced in definition 2) by a certain number of bits, depending on , and and tabulated in Appendix LABEL:sec:abaque, Table LABEL:tab:shift;

-

•

Consequently, can be re-interpreted in this framework; it is a lower bound on the number of significant bits with a certain probability and a given confidence level;

-

•

Although was not originally meant to do so, it can also be re-interpreted as an estimate of . For example in the CADNA case, where the number of samples is set to and a 95% confidence level is used, estimates with probability .

In the general case, when no assumption can be made about the distributions of or , we introduce the Bernoulli significant bits estimator

It is shown in section 5 that provides a sound lower bound for , provided that the number of samples is chosen accordingly to the desired probability and confidence level :

The required number of samples is tabulated in Appendix LABEL:sec:abaque, Table LABEL:tab:nsamples

Regarding contributing bits, it is proved in section 4.2 that all bits of rank are contributing with probability and confidence level under the centered normality hypothesis, with

In section 5, it is proved that in the general case, the -th bit of is contributing with probability and confidence level if

provided that the number of samples follows the rules described above.

4 Accuracy under the Centered Normality Hypothesis

In this section we consider that is a random variable with normal distribution . In practice, we only know an empirical standard deviation , measured over samples. Because is normal, the following confidence interval [saporta2006probabilites, p. 282] with confidence based on the distribution with degrees of freedom is sound 888 This interval is bilateral. If we were only interested in a lower bound for significant and contributing bits we could use the unilateral bound .:

| (9) |

It is important to note that is the standard deviation of and not of . For example, when taking a second independent random variable as reference, if and both follow a distribution , follows .

4.1 Significant bits

The theorem below is a more precise restatement of Stott Parker’s Theorem 1: “the difference in the orders of magnitude of the mean and the standard deviation measures the number of significant digits of (if , ).” We define the notion of “measuring the number of significant digits” as the estimation of the probability that a given bit is significant at a given confidence level. We then prove that the number of significant bits is given by as exposed by Stott Parker (since in a relative precision analysis, if is normal and centered at the reference value), but adjusted by a quantity that depends only on the target probability and confidence level (so, constant wrt the sample). This new formulation allows to assess the consequences of taking the considered bits into account or not.

Theorem 1.

For a normal centered error distribution , the -th bit is significant with probability

with the cumulative distribution function of the normal distribution with mean 0 and variance 1.

Proof.

The probability that the -th bit is significant is . Now by symmetry of the normal distribution, so that . Therefore,

∎

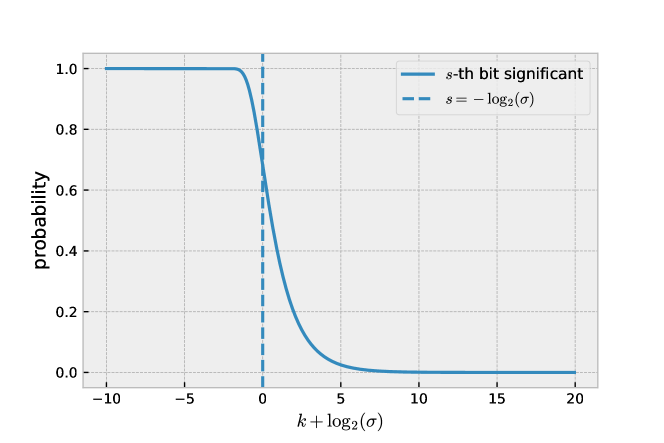

The number of significant digits with probability is such that , i.e. , so that

The above formula is remarkable because, whatever , the confidence interval to reach a given probability is constant and can be computed from a table for . Therefore, one just needs to subtract a fixed number of bits from to reach a given probability, as illustrated in figure 3.

In practice, only the sampled standard deviation can be measured, but it can be used to bound thanks to the the confidence interval in equation (9). This allows computing a sound lower bound on the number of significant digits in the Centered Normality Hypothesis:

| (10) |

Again, this formula is interesting since can be determined by just measuring the sample standard deviation and shifting by a value , which only depends on a few parameters: the size of the sample , the confidence and the probability . Some values for this shift are tabulated in appendix LABEL:sec:abaque, table LABEL:tab:shift. This is an improvement over the proposition of [PARKER1997, p.23] to use a confidence interval on the estimate of . Instead, we propose a confidence interval directly on the quantity of interest, namely, the number of significant digits.

Application

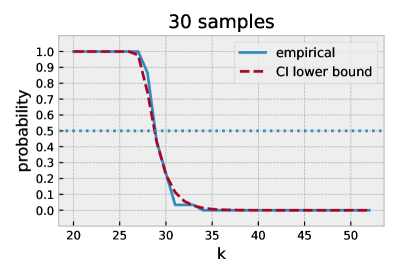

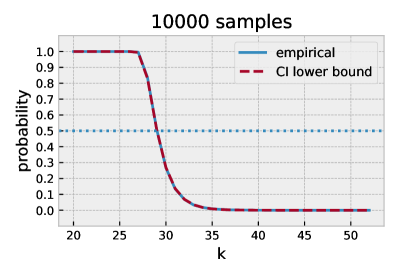

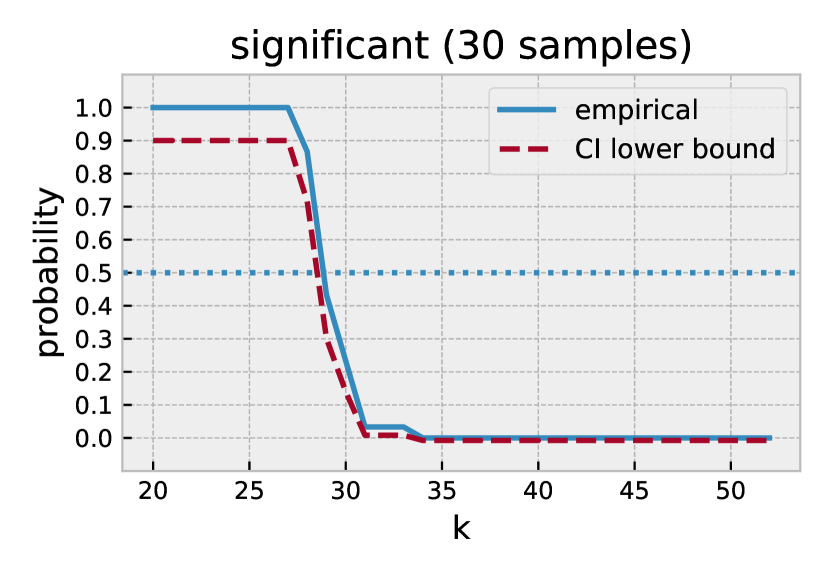

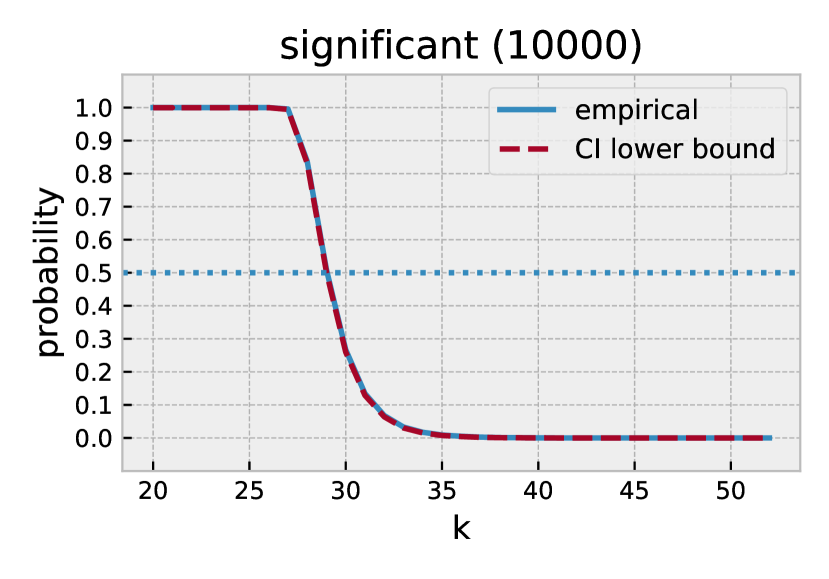

Let us consider the variable from the the ill-conditioned Cramer system from section 2.4. Statistical tests did not reject the normality hypothesis for . Here we would like to compute the number of significant digits relative to the mean of the sample with a 99 % probability. Following section 3, we consider the relative error, . Here will be estimated from with the 95 % confidence interval presented in equation (9). Computing for , and (or reading it in table LABEL:tab:shift), yields . Recalling the sampled measurements from section 2.4, we get .

Therefore, at least bits are significant, with probability 99 % at a 95 % confidence level. Figure 4 shows that the proposed confidence interval closely matches the empirical probability on the samples. When the number of samples increases, the confidence interval tightness increases.

4.2 Contributing Bits

In the previous section we computed the number of significant bits. Now we are interested in the number of contributing bits: even if a bit is after the last significant digit, it may still contribute partially to the accuracy if it brings the result closer to the reference value.

The theorem below gives an approximation of the number of contributing bits which has the same property as theorem 1: this approximation computes the number of bits to shift from to obtain the contributing bits based on the same few parameters (sample size , confidence and probability ), and the shift being independent of .

Theorem 2.

For a normal centered error distribution , when , the -th bit contributes to the result accuracy with probability

Proof.

As shown in equation 8, the -th bit of contributes if and only if there exists an integer such that , i.e. there exists an integer such that or such that . being continuous, .

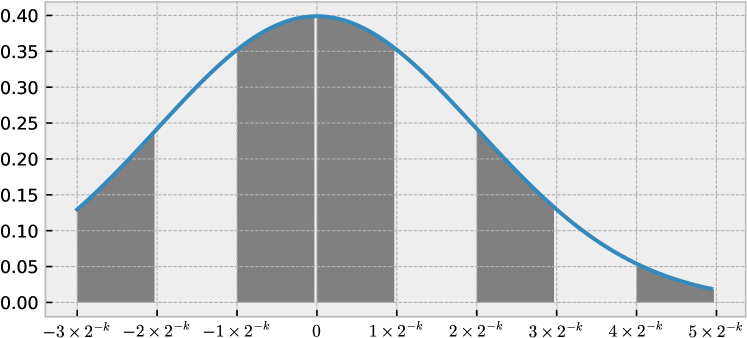

For a normal centered distribution, this inequality corresponds to the gray stripes in figure 5. Let us write the integral of one stripe as,

where is the probability density function of . The probability of contribution for the -th bit, , is therefore

| (by symmetry of ). | ||||

Now, according to the trapezoidal rule, there exists in the interval such that

Introducing and , we have , and

Now we compute the alternate series . Since the series is alternate and its terms tend to 0, all term cancellations are sound. All trapezoidal terms cancel, except the first half-term:

We can also sum the error terms . We have:

| (11) |

The second derivative is increasing between 0 and and decreasing from onward. We distinguish four possible cases, based on the monotony of (if is increasing on , , ; if it is decreasing, , ; and if , ):

-

•

Case 1: when , then

-

•

Case 2: when then

-

•

Case 3: when then

-

•

Case 4: when , then

The bounds on these error terms also cancel two by two, except the first one, and the two terms around (we consider cases with , so that the maximum of is not in the first stripe). At worst, and with remain on the right side, and and with on the left (these worst cases cannot all occur at once).

All in all, we are left with (using that reaches its maximum at ):

Finally:

| (12) |

It follows that, when is small, bit contributes to the result accuracy with probability

| (13) |

∎

Remark.

Equation 12 shows that is closer to than to . Now, is increasing, and for , less than 0.05. Hence, for ,

If we wish to keep only bits improving the result with a probability greater than , then we will keep contributing bits, with

| (14) |

As above, this formula can be further refined by replacing with and adding a term taking into account the confidence level:

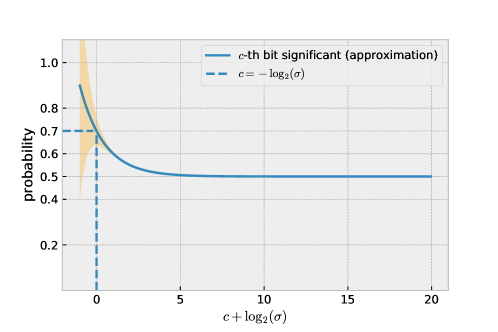

Figure 6 plots the approximation of equation 13. We note that for a centered normal distribution the probability of contribution decreases monotonically towards . Close to , bits become more and more indistinguishable from random noise since their probability is not affected by the computation.

The approximation of equation 13 is tight for : in this case, the absolute error of the approximation formula is less than . The probability of contribution at is . Therefore, equation 14 can be safely used for probabilities less than . In this paper, we want to find the limit after which bits are random noise. This limit corresponds to a probability of and the approximation is tight for .

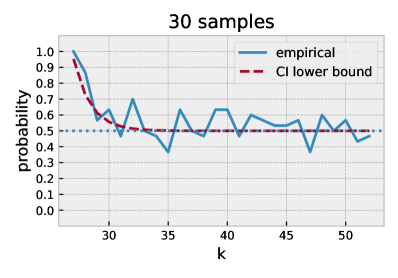

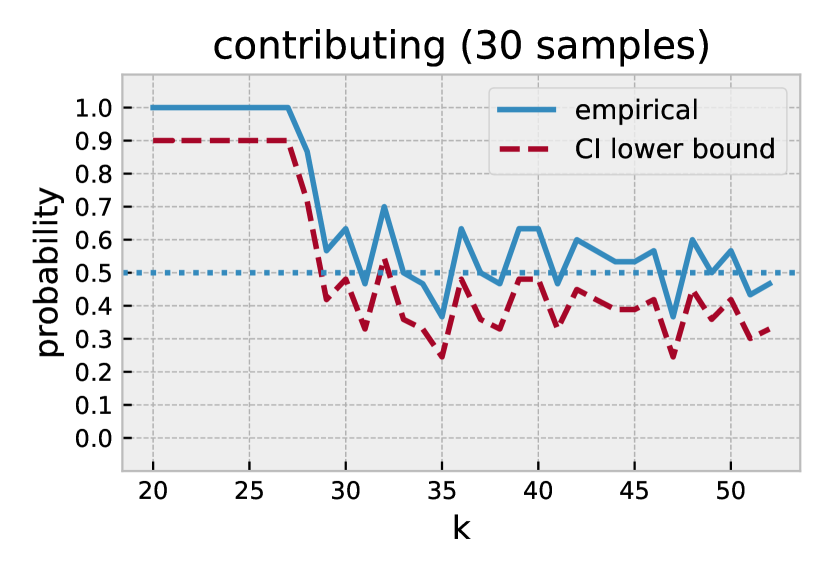

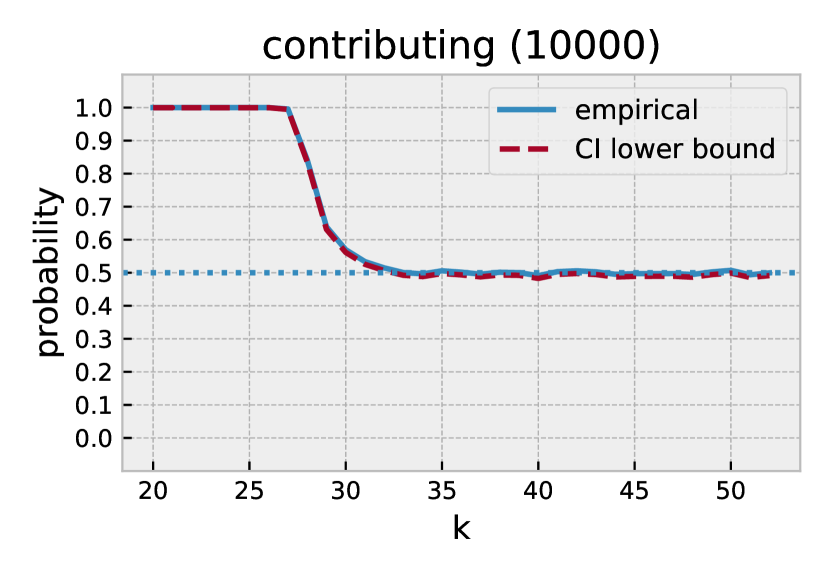

Application

Figure 7 shows that the approximation proposed in this section tightly estimates the empirical samples in Cramer example.

If we consider a 51 % threshold for the contribution of the bits we wish to keep, then we should keep . As in section 4.1, we estimate with a 95 % Chi-2 confidence interval, and compute .

This means that with probability 51% the first 32 bits of the mantissa will round the result towards the correct reference value. After the 34th bit the chances of rounding correctly or incorrectly are even: the noise after the 34th bit is random and does not depend on the computation. Bits 34 onwards can be discarded.

4.3 Summary of results for a Normal Centered Distribution

Under the normality hypothesis, the quantity introduced by Stott Parker is pivotal, but needs to be refined. In our framework, Stott Parker’s definition maps to , which computes the relative error to the mean. In this case Stott Parker’s formula computes the position of the bit until which the result has 68 % chance of being significant, and that contributes to the result precision with a probability of 70 %.

However, from this bit, for each desired probability level, there is a simple way to compute a quantity by which to move back to be sure that the result is significant. It is also easy to compute a quantity by which to move forward in order to guarantee that all bits contributing more than a fixed level are kept. Figure 8 demonstrates this on the Cramer’s example.

We recall from section 2.4 that in this example . First a lower bound, 28.45, on is computed with the Chi-2 95 % confidence interval. With this confidence level, it is a lower bound of (as introduced in definition 2). It is also a lower bound of with 68 % probability (as introduced in definition 3). To compute a lower bound on bits that are significant with probability 99 %, we simply subtract 1.37 from this number. By adding 4.32 to this number we get the number of bits that contribute or round towards the reference with a probability of 51 %. The remaining bits in the mantissa are random noise.

It is important to understand the difference between contributing and significant bits. To illustrate this difference, we show in figure 8 the number of significant bits with 50 % probability which we estimate at 29 bits (28.45 shifted by +0.57 bits). We deduce, since the probability of significant bits decreases monotonically, that bits in the range 30-33 are significant with a probability under 50 %; in other words they are likely to be non significant. Yet taken individually, these bits are contributing with probability over 51%. Therefore, bits in the range 30-33 still contain useful information about the computation and cannot be considered random noise. It is up to the practitioner to decide how many bits to keep depending on their use-case.

Taking this into account, we propose to give a result, by printing all contributing bits at the chosen probability and confidence levels and an annotation bounding the error term at the chosen probability and confidence levels. This would result, for , in the following: for an absolute error with bits with the annotation at 99 %; for a relative error with and at 99 % for a relative error. In this notation, only digits that are likely to round correctly the final result with a probability greater than 1 % are written; the error at probability 99 % is written. In decimal, this notation takes up to two additional digits ( digits) that are probably wrong, but still have a chance to contribute to the result precision. As an example, using this notation to display the IEEE-754 result of Cramer’s yields, with 9 contributing digits and 8 significant digits:

1.999999996 1.4e-08 (at 99% with confidence 95%).

These 10 digits contain all the valuable information in the result, and are the only ones that it would make sense to save, for example in a checkpoint-restart scheme.

Interestingly enough, the CESTAC definition of significance can be reinterpreted in this statistical framework. Equation (1) defines the CESTAC estimator as

This estimator was originally designed to estimate (as introduced in definition 1) under the CESTAC model hypothesis. We showed previously that the formula tends to infinity when increasing the number of samples . Yet CADNA [lamotte2010cadna_c], the most popular library implementing CESTAC, sets and . In this case,

Reinterpreting the -1.31 shift as the term from equation (10), we see that can be seen as an estimator for our stochastic definition of significant bits, , with probability 30.8% at a 95% confidence level. With only three samples, using as an estimator of can introduce a strong error. The term which accounts for this error inside becomes important, which explains the low probability (30.8%) of the estimation.

To mitigate this issue, it is recommended to take a safety margin of 1 decimal digit from the number of significant digits estimated by CADNA. In our formalism, shifting further by 1 decimal digit (or approximately 3.32 bits), the result can be reinterpreted as a shift of bits, estimating with probability over 99% (with 95% confidence).

5 Accuracy in the General Case

The hypothesis that the distribution is normal, or that it has expectation is not always true. We propose statistical tools to study the significance of bits as well as their contribution to the result accuracy that do not rely on any assumption regarding the distribution of the results.

To address the problem in the general case we reframe it in the context of Bernoulli estimation, which is interesting because:

-

•

it does not rely on any assumptions on the distribution of ;

-

•

it provides a strong confidence interval for determining the number of significant digits when using stochastic arithmetic methods;

-

•

thanks to a more conservative bound, it allows to estimate a priori in all cases for a given probability and confidence a safe number of sample to draw from the Monte Carlo experiment.

5.1 Background on Bernoulli estimation

In the next section, we restate the problem of estimating the number of significant bits as a series of estimations of Bernoulli parameters. We present here some basic results on such estimations.

Consider a sequence of independent identically distributed Bernoulli experiments with an unknown parameter and outcomes . Each value of the parameter gives a model of this experiment, and, among them, we will only keep an interval of model parameters under which the probability of the given observation is greater than . The set of possible values for will then be called a confidence interval of level for : if the actual value of is not in the confidence interval computed from the outcome, it means that the observed outcome was an “accident” the probability of which is less than .

A case of particular interest in our study is the one when all experiments succeed. Then, the probability of this outcome is under the model that the Bernoulli parameter value is . We then reject models (i.e., values of ) such that . Now, and is a first order approximation when is close to 1. Thus, taking leads to a probability of the observation less than , and one can reject these values of . In particular, taking , we keep values of greater than , and is a confidence interval. This result is known in clinical trial’s literature as the Rule of Three [Eypasch619]. Vice versa, in an experiment with no negative outcome, one can conclude with confidence that the probability of a positive outcome is greater than after positive trials.

The general case can be dealt with by using the Central Limit Theorem, which shows that for a number of experiments large enough (with respect to ), is close to a Gaussian random variable with law . This approximation is known to be unfit in many cases, and can be improved by considering rather than as shown by Brown et al. [brown2001interval] (this paper also presents other estimators to build confidence intervals in this situation; in particular, it proposes a revised method when is close to 0 or 1, a situation in which the confidence interval below may be overly optimistic). Then, with the cumulative distribution function of ,

is an confidence interval for . If we focus on a lower bound on the parameter , we can also use as a confidence interval of level .

Thus, from independent experiments, of which have been a success, we can affirm with confidence 95 % that the probability of success is greater than . We can note that when , this confidence interval is valid, but much more conservative than the one obtained above, that can thus be preferred in this particular case.

5.2 Statistical formulation as Bernoulli trials

Now, for each of the four discussed settings, presented in section 3, we can form two series of Bernoulli trials based on collected data.

| reference | reference | |

|---|---|---|

| absolute precision | ||

| relative precision |

When the reference is a constant , we consider samples . We form pieces of data by computing or respectively.

When the reference is another random variable , we form pieces of data by computing or . In the case where and we study the distance between samples of a random process, this requires samples from .

From these pieces of data, we form Bernoulli trials by counting the number of success of

for studying -th bit significance, and

for studying -th bit contribution, where is the indicator function.

From these two Bernoulli samples, the estimation can be made as above to determine the probability that the -th bit is significant and the probability that it contributes to the result, for any . The result can then be plotted as two probability plots, one for significance, the other for the contribution. The significance plot is non-increasing by construction, should start at 1 if at least one bit can be trusted, and tends to 0. The contribution plot should tend to in most cases, since the last digits are pure noise and are not affected by the computation.

5.3 Evaluation

The main goal of the Bernoulli formulation is to deal with non normal distributions. In this section, we evaluate the Bernoulli estimate on Cramer’s samples which follow a normal distribution. This is to keep a consistent example across the whole paper and to compare the results with the Normal formulation estimates. Later, in section 6, we will apply the Bernoulli estimate to distributions produced by the industrial simulation codes EuroPlexus and code_aster, some of which are not normal.

Figure 9 plots the significance and the contribution per bit probabilities for using the Bernoulli estimation. The estimation closely matches the empirical results. It is interesting to compare the Bernoulli estimates with 30 samples to the Normal estimates in figures 4 and 7. The Bernoulli estimates are less tight and more conservative. This is expected since they do not build upon the normality assumption of the distribution.

If we are only interested in the number of significant digits, we can consider the Bernoulli trial with no failed outcomes since it provides an easy formula giving the required number of samples. In this case, the number of needed samples is . We then determine the maximal index for which the first bits of all sampled results coincide with the reference:

| (15) |

We applied this method to the sample from section 2.4. Assuming a confidence interval and a probability of of getting significant digits, we gather samples. Among the collected samples, the th digit is sometimes different compared with the reference solution, but the first digits coincide for all samples. Therefore we conclude with probability and confidence, that the first binary digits are significant.

6 Experiments on industrial use-cases

6.1 Reproducibility analysis in the Europlexus Simulation Software

In this section we show how to apply our methodology to study the numerical reproducibility of the state-of-the-art Europlexus [EPXweb] simulator. Europlexus is a fast transient dynamic simulation software co-developed by the French Commissariat à l’Énergie Atomique et aux Énergies Alternatives (CEA), the Joint Research Center (JRC) of the European Commission, and other industrial and academic partners. While its first lines of code date back to the mid seventies, the current source code has grown to about 1 million lines of Fortran 77 and Fortran 90. Europlexus runs in parallel on distributed memory architectures through a domain decomposition strategy, and on shared memory architectures through loop parallelism.

Europlexus has two main fields of application: simulation of severe accidents in nuclear reactors to check the soundness of the mechanical confinement barriers of the radioactive matters for the CEA; and simulation of explosions in public places in order to measure their impact on the surrounding citizens and structures for the JRC.

It handles several non-linearities, geometric or material, some of which lead to a loss of unicity of the evolution problem considered. This is for example the case for some configurations with frictional contact between structures, or when the loadings cause fracture and fragmentation of the matter. Another obvious source of bifurcations of the dynamical system is the dynamic buckling.

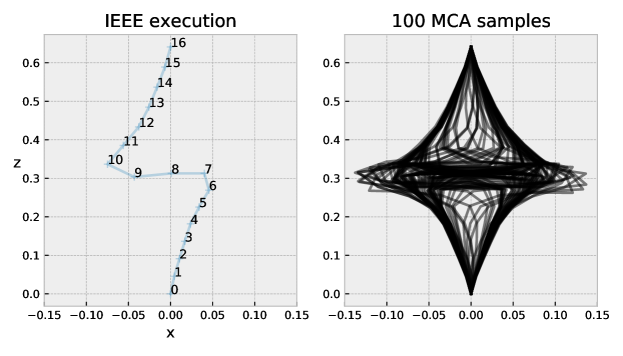

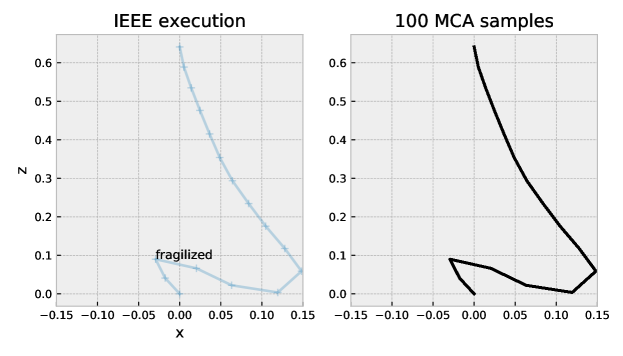

Due to the small errors introduced by the floating point arithmetic, the introduction of parallel processing in Europlexus raises a difficulty for the developer and the users: the solutions of a given simulation may differ when changing the number of processors used for the computation. We show here how the confidence intervals proposed in this paper help the developer to design relevant non-regression tests. To this end, we study in the following a simple case which could serve as a non-regression test, and which is symptomatic of a non-reproducibility related to FP arithmetic. It involves a vertical doubly clamped column to top and bottom plates. A vertical pressure is applied by lowering the top plate, which causes buckling of the column. The column is modeled as a set of discrete elements (here segments) connected at moving points called nodes.

The left plot in figure 10 shows the result after 300 simulation time-steps with the out-of-the-box Europlexus software using standard IEEE arithmetic. The sequential result is deterministic and does not change when run multiple times. We wish to study how the simulation is affected by small numerical errors.

We run the same simulations but this time using the Verificarlo [verificarlo] compiler to introduce MCA randomized floating point errors with a precision of . The cost to instrument the whole Europlexus software and its accompanying mathematical libraries was low. In particular no change to the source-code was necessary thanks to the transparent approach to instrumentation of Verificarlo, only the build system had to be configured to use the Verificarlo compiler.

The right plot in figure 10 shows the result of one hundred Verificarlo executions. The direction of the buckling is chaotic and completely dominated by the small FP errors introduced. This is not surprising as the buckling direction is physically unstable.

When parallelizing Europlexus or making changes to the code, it is important to check that there are no regression on standard benchmarks. Changing the order of the floating point operations may introduce small rounding errors. As we just saw, even small numerical errors change the buckling direction. This makes such a benchmark unsuitable for classical non-regression tests.

The column is modeled as a set of discrete elements connected by nodes. The distribution on the -axis is normal but whatever the node there are no significant digits among the samples. The variation between samples is strong on the -axis, the position clearly cannot be used as a regression test.

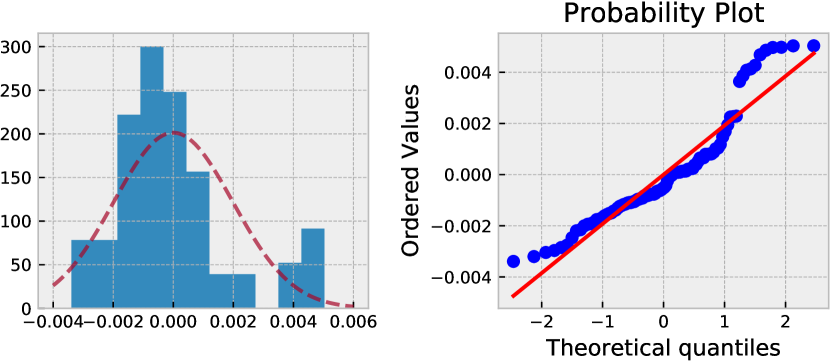

The distribution along the axis is more interesting as it is non normal for all the nodes. Figure 11 shows the quantile-quantile plot for node 1 (Shapiro-Wilk rejects normality with and ). Because the distribution on the axis is non normal we should apply the Bernoulli significant bits estimator. In this study, we measure the number of significant digits considering the relative error against the sample mean, so .

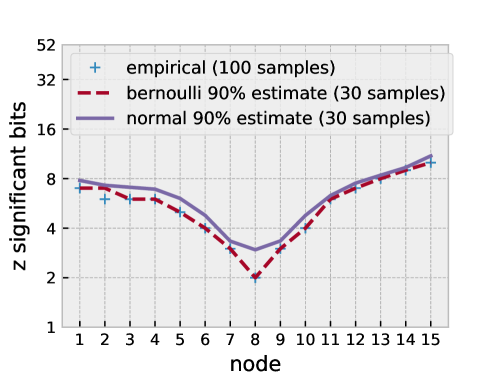

To test the robustness of the proposed confidence interval, we computed the Bernoulli estimate on the first 30 samples of the distribution. This corresponds to a probability of 90% with a confidence of 95%. We also computed the Normal estimate on the first 30 samples with the same probability and confidence.

Figure 12 compares the estimates to the empirical distribution observed on 100 samples. The Bernoulli estimate on 30 samples is fairly precise and accurately predicts the number of significant bits (except for node 2). The clamped node 16 has a fixed position and therefore all its digits are significant. The other nodes have between 2 and 10 significant digits depending on their position.

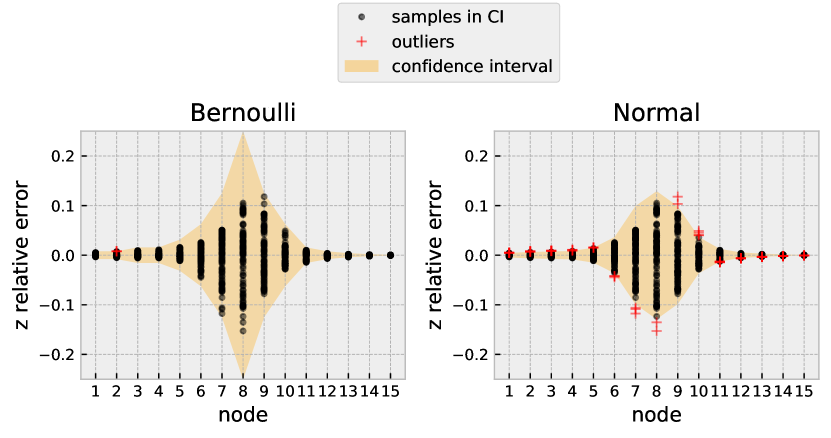

Figure 13 shows the expected relative error on each node. We see that the Bernoulli estimate is robust and only mis-predicts the error on three samples of node 2. On the other hand, as expected, the Normal formula is not a good fit in this case due to the strong non normality of the distribution: the normal estimate is too optimistic and fails to capture the variability of the distribution.

The previous experiments show that the -axis has no significant digits and that the -axis distribution has between 2 and 10 significant digits. For example node 6 has 4 significant digits on the -axis. Therefore, if the practitioner uses the -axis position in this benchmark as a regression test, she should expect the first four digits of the mantissa to match in 90 % of the runs. If the error is higher than that then a numerical bug has probably been introduced in the code.

Another possibility for the practitioner is to adapt slightly the benchmark to make it more robust to numerical noise so it can be used in regression tests. For example, we can introduce a small perturbation in the numerical model by slightly moving node 2 along the x-axis. Then the buckling is expected to always occur in the same direction. Figure 14 shows what happens when node 2 is slightly displaced: the buckling becomes deterministic and robust to numerical noise: 51 bits are significant for the -axis and -axis samples with probability 90 %; the two bits of precision lost correspond to the stochastic noise introduced. In this case, stochastic methods allow checking that the benchmark has become deterministic and assessing its resilience to noise.

6.2 Verification of a numerical stability improvements in code_aster

code_aster [aster] is an open source scientific computation code dedicated to the simulation of structural mechanics and thermo-mechanics. It has been actively developed since 1989, mainly by the R&D division of EDF, a French electricity utility. It uses the finite elements method to solve models coming from the continuum mechanics theory, and can be used to perform simulations in a wide variety of physical fields such as mechanics, thermal physics, acoustics, seismology and others. code_aster has a very large source code base, with more than 1,500,000 lines of code. It also uses numerous third-party software, such as linear solvers or mesh manipulation tools. Its development team has been dedicated to code quality for a long time, and has accumulated several hundreds of test cases which are run daily as part of the Verification & Validation process.

In a previous study [fevotte2017studying] of code_aster, the Verrou tool was used to assess the numerical quality of quantities tested in the non-regression database. The error localization features of Verrou were used to find the origin of errors in the source code, and improvements were proposed. In this section, we first summarize the results of this study, before using the new estimators described in this paper to confidently assess the benefits of the proposed corrections.

The study focuses on one test case named sdnl112a [sdnl112], which computes 6 quantities related to the vibrations of steam generator tubes in nuclear reactors. These quantities will be denoted here as , , , , and . In the original implementation of code_aster – which will be referred to as version0 in the following – the test case successfully completes on some hardware architectures, and fails on others. In this case, failing means that some quantities are computed with relative discrepancies larger than with respect to some reference values. Using the Verrou tool to assess the numerical quality of these results fails: some runs perturbated by random rounding bail out without producing results. This exhibits somewhat severe instabilities, but does not allow quantifying their impact on the results accuracy.

The methodology then proceeds to finding the origin of such instabilities using Verrou. In a first stage, a test coverage comparison between two samples uncovers an unstable branch which is reproduced, after simplification, in figure 6.2. A reformulation of the incriminated computation (cf. figure LABEL:aster:fun1:cor) is proposed, which leads to a first corrected implementation, which will be referred to as version1. This version still does not pass automated non-regression testing. However, this time, assessing the stability of the results using Verrou and the standard MCA estimator (with 6 samples) yields meaningful results. Quantity is evaluated to be the most problematic, with only 5 reliable significant decimal digits (19 bits), when users expect at least 6. Other computed quantities seem to meet the expected precision. For example, 9 decimal digits (30 bits) are estimated to be reliably computed for quantity . In the following, we will use notations consistent with the rest of this paper, the computed result being either quantity or .