Deep Learning-Based BSDE Solver for Libor Market Model with Application to Bermudan Swaption Pricing and Hedging

First version: July 10, 2018)

Abstract

The Libor Market Model, also known as the BGM Model, is a term structure model of interest rates. It is widely used to price interest rate derivatives, especially Bermudan swaptions, and other exotic Libor callable derivatives. For numerical implementation purposes, Monte Carlo simulation is used for Libor Market Model to compute the prices of derivatives. The PDE grid approach is not particularly feasible due to the “Curse of Dimensionality”. The standard Monte Carlo method for American swaption pricing more or less uses regression to estimate the expected value by a linear combination of basis functions as demonstrated in the classical paper of Longstaff and Schwartz [1]. However, the paper [1] only provides the lower bound for American option price. Another complexity arises from applying Monte Carlo simulation is the computation of the sensitivities of the option, the so-called “Greeks”, which are fundamental for a trader’s hedging activity. Recently, an alternative numerical method based on deep learning and backward stochastic differential equations (BSDEs) appeared in quite a few research papers [2, 3]. For European style options the feedforward deep neural networks (DNN) show not only feasibility but also efficiency in obtaining both prices and numerical Greeks. The standard LMM implementation requires dimension of five or higher in factor space even after PCA, which cannot be solved by traditional PDE solvers, such as finite differences or finite elements methods. In this paper, a new backward DNN solver is proposed to price Bermudan swaptions. Our approach is representing financial pricing problems in the form of high dimensional stochastic optimal control problems, Forward-Backward SDEs, or equivalent PDEs. We demonstrate that using backward DNN the high-dimensional Bermudan swaption pricing and hedging can be solved effectively and efficiently. A comparison between Monte Carlo simulation and the new method for pricing vanilla interest rate options manifests the superior performance of the new method. We then use backward DNN to calculate prices and Greeks of Bermudan swaptions as a prelude for other Libor callable derivatives.

KEY WORDS: Libor Market Model, Backward Deep Neural Network, Derivatives Pricing, Forward-Backward Stochastic Differential Equation, General Feynman-Kac Formulae, Libor Callables.

1 Introduction

The Libor Market Model (LMM), also known as BGM Model, is a widely used interest rate term structure model. As an extension of the Heath, Jarrow, and Morton (HJM) [4] model on continuous forward rates, the LMM takes market observables as direct inputs to the model. Whereas the HJM model describes the behavior of instantaneous forward rates expressed with continuous compounding, LMM postulates dynamical propagation of the forward Libor rates, which are the floating rates to index the interest rate swap funding legs. Libor rates are simple add-on rates for the payment period; and therefore, LMM overcomes some technical problems, such as exploding rates, associated with the lognormal version of the HJM model (see [5] for details). For vanilla options such as cap/floor, European swaption, with appropriate numeraires there exist even Black style formulae which can speed up the model calibration.

LMM is mainly implemented using Monte Carlo simulation. However, to evaluate American and Bermudan swaptions using Monte Carlo simulation, some additional numerical procedures have to be implemented to avoid Monte Carlo simulation on Monte Carlo simulation and to approximate the decision on early exercise. Some of the related works are: (1) In 1998, Andersen proposed an approach involving a direct search for an early exercise boundary parameterized in intrinsic value and the values of still-alive options [6]. (2) In 1997, Broadie and Glasserman proposed an approach involving a stochastic recombining tree [7]. (3) In 1998, Longstaff and Schwartz assumed that the value of an option, if not exercised, was a simple function of variables observed at the exercise date in question. However, these approaches mostly only provide pricing bounds of American options. Another complexity is the computing of sensitivities using Monte Carlo simulation. The sensitivities or “Greeks” are fundamental quantities used by traders in hedging strategies.

To compute derivative Greeks, the numerical PDE method is generally the most natural alternative due to the following advantages: (1) dependent variables of PDEs are still-alive and there is no need to estimate them by extra numerical methods; (2) the Greeks are directly given by the partial derivatives of the PDE solutions; (3) for various path-dependent options only the boundary conditions need be changed. However one well-known hard restriction in these PDE formulations is the dimensionality in their states space. For example, for Libor6M European swaption with expiry 10Y and tenor 20Y, there are 60 6M Libor rates, and that requires implementation of 60 dimensional numerical PDEs. In order to cope with this so-called “Curse of Dimensionality”, several traditional methods are available in the literature, see [8, 9, 10], which can be generally put into three categories. The first category uses the Karhunen–Loeve transformation to reduce the stochastic differential equation to a lower dimensional equation. This reduction results in a lower dimensional PDE associated to the previously reduced SDE. The second category collects those methods which try to reduce the dimension of the PDE itself. For example, we have mentioned dimension-wise decomposition algorithms. The third category groups the methods which reduce the complexity of the problem in the discretization layer, for example, the method of sparse grids. It is inconclusive if any of the aforementioned method can accurately solve the option pricing in very high dimension.

Most recently, groups of computational mathematics researchers, such as Weinan E of Princeton University, proposed new algorithms to solve nonlinear parabolic partial differential equations (PDEs) based on formulation of equivalent backward stochastic differential equations (BSDEs) in high dimension (See [2, 3]). Theoretically, this approach is founded on the amazing generalized Feynman-Kac theorems (see works by Pardoux and Peng [13][14]). The second step in the new approach utilizes the deep connection between the BSDE/FBSDE theories and the stochastic optimal control theories (See [15, 16, 17, 18, 19, 20]). The third step borrows ideas and tools from the most recent amazing developments in machine learning, reinforcement learning, and deep neural networks (DNN) learning. As standardized since the early days of machine learning the backpropagation, first proposed in a seminal paper by Rumelhart, Hinton, and Williams[21], is naturally embedded in neural networks. In a DNN the gradient of the value function plays the role of a control/policy function, and the well-posed loss function is to be optimized along the descending direction to speed up convergence. The results are astonishing as people watch in awe when the applications of DNN achieved great successes in facial recognition, image reconstruction, natural speech, self-driving car, Go-game play, and numerous others.(See [22, 23, 24, 25]) The policy function is then approximated through a few layers of nonlinear functional combination, convolution and other types of nesting, as shown in the vast literature of deep learning and reinforcement learning (See [26] for a survey of deep learning.). In addition the deep learning-based algorithms are highly scalable and can be applied to BSDE, Stochastic Optimal Control, or PDE problems without changing much of their implementation.

Our approach is also inspired by the recent developments in artificial intelligence and deep learning researches. However, our research focus differs from the computational mathematics world. For example, Weinan E and co-authors have used forward DNN to solve various nonlinear PDEs where the classical numerical methods suffer from the “Curse of Dimensionality”. They used forward DNN to solve high dimensional parabolic PDEs in particular through BSDE representations based on nonlinear Feynman-Kac formulae. In their examples of European style derivatives pricing, their method projects the option value forward with prescribed SDE to the terminal time and approximates the gradient of option value function in a feedforward DNN. The loss function is proposed to minimize the error between the prescribed terminal value and the projected value at terminal time. The training data are simulated sample paths of standard Brownian Motions. Thus it belongs to the rule-based learning category.

For comparison purposes, we recognize that the conventional forward DNN could be used only in European style derivatives pricing. In financial engineering, the more complex derivatives are callable instruments, such as callable bonds, convertible bonds, American swaptions, and especially Bermudan swaptions. Bermudan swaptions are widely used to hedge interest rate risk by swap desks and other fixed income desks. However, the conventional forward solver is suitable only for European style financial derivatives pricing. In general the pricing of Bermudan style derivatives needs to handle early exercise appropriately. A general guideline is the famous Bellman dynamic programming principle to make this type of optimal decision. For example, a recombining tree or PDE grids are used in low dimensional implementation of Bermudan swaption pricing, and the valuation process is backward starting from the terminal time. At each exercise date the immediate exercise value is compared to the computed holding value of the option to make an optimal decision for exercise.

According to our knowledge our paper is the first in the financial engineering literature to apply backward DNN to price callable derivatives. We have developed a new method which uses a similar DNN structure/layers but marching backwards to project flows. The idea is quite natural and consistent to BSDE formulation. Our approach is specifically designed for callable derivatives pricing. When option price is projected backwards, it is easy to make an early exercise decision of Bermudan swaption following the same Bellman dynamic programming principle. Instead of matching the final payoff at terminal time, our new approach learns the parameters by minimizing the variance of the projected initial values from different simulated paths. We thus call this new approach the backward DNN learning. Clearly, the approach demonstrated in our paper can readily be applied to general callable derivatives pricing in financial engineering. Our approach is directly taking the financial engineering problem in hand and makes the use of intrinsic connections among three major fields of knowledge: Stochastic Optimal Control, FBSDE theory, and PDE theories, especially parabolic and elliptic PDEs. We can represent the financial derivative pricing problem in any of these three formulations and choose the one that is most computationally efficient.

The paper is organized in five sections. In Section 2, we introduce the basics about Libor market model, including probability measure, pricing numeraire, and dynamic evolution. In Section 3, we first represent the financial derivative pricing problems in PDE and BSDE formulations under LMM. We then discuss the deep learning-inspired forward and backward DNN solvers. We explain the major contribution of this paper of backward-feeding DNN algorithm in details, and its unique advantage to solve the pricing problem for callable options. We also compare the forward and backward DNN to highlight their differences, advantages, and disadvantages. In Section 4, we use the LMM setting in QuantLib111QuantLib is a free/open-source library for quantitative finance. to conduct some numerical experiments to show the performance of forward and backward DNN solvers such as numerical accuracy, convergence speed, and stability. For this purpose, we have drawn comparisons between our backward DNN results and Monte Carlo simulation results from QuantLib in the pricing of European swaptions. This serves as the benchmark for our further development on Bermudan swaptions evaluated using DNN backward solver. Concretely, we analyze the performance of backward DNN solver in pricing Bermudan swaption by increasing the number of exercise dates and using different spot yield curves. We conclude our paper in Section 5 by pointing out our view on future DNN research directions in financial engineering and derivatives pricing and hedging.

2 Description of Libor Market Model

In this section, we introduce the Libor market model (LMM) and set up the theoretical framework for numerical implementation using deep neural networks. We mostly follow notations in Andersen-Piterbarg [11]. Later, our neural network pricing approach is discussed in the context of interest rate options under the LMM setting. Bear in mind that our methodology can be applied to other general dynamics and financial derivative products.

2.1 LMM Dynamics and Pricing Measures

Let and be a complete filtered probability space satisfying the usual conditions, where the filtration is the natural filtration generated by the standard Brownian motion (possibly high-dimensional) and augmented by all null sets.

In the implementation of the Libor market model, it is customary to start from the definition of the fixed tenor structure. The model tenor structure is a set of dates, i.e.

| (2.1) |

characterized by intervals , . We then specify the vector standard Brownian Motions for all generated . The function values are typically set to be either three or six months corresponding to a pre-specified day-count basis indicated by the function . Here are two examples for day-count fractionals:

Now we recall several important definitions and propositions.

Definition 1.

(Forward Libor Rate) Let denote the time price of a zero-coupon bond delivering for certain $1 at maturity , for the tenor structure aforementioned. The forward Libor rates are defined by:

| (2.2) |

where represents the unique integer such that

We denote .

must be a martingale in the - forward measure such that follows SDE222In our subsequent analysis and implementation we assmue the duffusion coefficient is a loacl volatility function that is, we work on a lognowmal version of LMM. :

| (2.3) |

where is a 333is a positive integer in general.-dimensional Brownian motion in forward measure , and is a row vector in .

To simplify the notation we denote Under the terminal measure , the process for is

| (2.4) |

where is a one-dimensional standard Brownian motion for the forward Libor rate in terminal measure The is the Euclidean-norm in We have assumed the constant correlation for components of We can write explicitly for the drift term as:

| (2.5) |

Under the spot measure , the process for is

| (2.6) |

where is a -dimensional Brownian motion in spot measure , and is a one-dimensional Brownian motion driving forward Libor rate in spot measure . We can write explicitly for this case the drift term as:

| (2.7) |

Under the spot measure, the numeraire is

| (2.8) |

which is simple compounded discrete money market account.

2.2 Separable Deterministic Volatility Functinon

In order to make the Libor Market Model Markovian, we have to specify the vector volatility function, in the following form (See Andersen-Piterbarg [11]):

| (2.9) |

where is a bounded row-vector of deterministic functions and is a time-homogeneous local volatility function. Some standard parameterizations of are shown in the following Table:

| Name | (x) |

|---|---|

| Log-normal | |

| CEV | |

| LCEV | |

| Displaced log-normal |

2.3 Correlation Structure

In general, the LMM can capture non-trivial curve movements, including not only parallel shifts, but also “rotational steepening” and “humps”, which is achieved through the use of vector-valued Brownian motion drivers with correlation. Later in the simulation, we use the simple correlation structure such that the Libor rates are controlled by the correlation function: . This is a simple postulation but is sufficient for our current work to demonstrate the effectiveness of the backward deep neural networks. For the subsequent sections we will fix , that is, each is driven by one Brownian Motion .

With this postulation we can now write the Brownian Motion , Here, is a standard Brownian Motion in .

3 Deep Neural Network Implementation

In this section, we will first state the PDE/BSDE formulation for the European/Bermudan pricing for LMM setting, and then move on to the neural network solver for the derived PDE/BSDE problem.

3.1 PDE Derivation for European Option Pricing

An European option is characterized by its payoff function , which determines the amount that the option pays at option expiry . The arbitrage-free discounted value function of the option relative to a numeraire (discounted option price) is then given by:

| (3.1) |

where is the vector of all forward Libor rates . Using Itï¿œ’s formula, the stochastic differential equation for is given by:

| (3.2) |

where and

Substituting Eq. (2.4) under terminal measure or (or similar Eq. (2.6) under spot measure ) in Eq. (3.2), we have

| (3.3) |

In order to comply with the arbitrage-free condition, the process has to be a martingale under the measure which corresponds to the numeraire process . Thus, to satisfy this requirement, the drift term must be equal to zero. We then obtain the PDE as following:

| (3.4) |

We can also write PDE (3.4) in the matrix as following :

| (3.5) |

It follows that the PDE is:

| (3.6) |

where is -dimensional vector, and is the matrix .

3.2 Equivalent BSDE for European Option Pricing

By the basic BSDE theory the solution of the parabolic PDE (3.6) is connected to the following decoupled FBSDE

| (3.7) |

where we define function . A standard generalized Feynman-Kac formula states:

3.3 From European Option to Bermudan Option

In this section,we first state the basics of Bermudan swaptions in the Libor market model setting. We then explain how to construct PDE/BSDE for a Bermudan swaption using results from sections 3.1 and 3.2.

Bermudan option is a type of derivative securities with early exercises that could take place on a discrete set of dates. It is characterized by an adapted payout process , payable to the option holder at a stopping time (an exercise date) chosen by the option holder. Let the allowed (and deterministic) set of exercise dates larger than or equal to be denoted by ; and suppose that we are given at time a particular exercise policy taking values in as well as a pricing numeraire corresponding to a unique martingale measure . Let be the time value of a derivative security that pays at exercise time. Under some technical conditions on we can write for the value of the derivative security as:

Let be the time set of (future) stopping times taking values in . In the absence of arbitrage, the time value of a security with early exercise into is then given by the optimal stopping problem:

Suppose we have where (The unusual notation here is used for the convenience of the discretization later in 3.4.4). For define as the time value of the Bermudan option when exercise is restricted to the dates . That is

At time can be interpreted as the hold value of the Bermudan option, that is, the value of the Bermudan option if not exercised at time . If an optimal exercise policy is followed, clearly we must have at time

such that for ,

| (3.10) |

Starting with the terminal condition , Eq.3.10 defines a useful iteration backwards in time for the value . In more details, for an we can price for similarly as in Eq.3.1 given that is already priced in advance. Therefore, the processes discussed in sections3.1 and 3.2 can be applied with backward iteration in time for sub-intervals . Later we will see the essence of our backward neural network solver is to take advantage of this backward iteration property and to parameterize and learn/approximate all altogether in one backward discretization run instead of learning them one by one. It is clear that this approach exactly follows the famous Bellman Dynamic Programming principle and the finding of the optimal exercise policy is assured.

3.4 Deep Neural Network-Based BSDE Forward/Backward Solvers for the LMM

In this section, we mainly cover (1) forward solvers; and (2) backward solvers in using DNN. Forward solvers have been developed mainly by Weinan E et al. [2, 3]. The forward feed DNN is suitable to price European style options, but it presents difficulties to price Bermudan options as explained below:

-

•

For a Bermudan style option, there are multiple exercise dates. At any future time of an exercise date, according to the dynamic programming principle for optimality, the continuation value of the option must be known as well. Given a numerical scheme for pricing, forward estimation of the continuation value could be very difficult. For example, Monte Carlo simulation scheme is generally forward looking and one needs special method, such as regression, or basis function approximation to estimate the expected continuation value.

Therefore, it is generally infeasible or inefficient to use forward solvers to price Bermudan swaptions. For neural network implementation it encounters similar problem such as those simulation methods (See [1, 6, 7]) encountered. The major contribution of our work is to explore a new approach: Backward DNN solver. With our limited knowledge, this paper is the first work in the literature in the DNN application to derivatives pricing area to show that the backward DNN is effective and efficient for pricing Bermudan options.

We provide the details of these two solvers in the next two subsections.

3.4.1 Discretization of Libor Rate SDE and Option Price BSDE

To derive the deep neural network-based BSDE solver, we first need to discretize the Libor rate SDE and the option price BSDE. Before the discretization, the time discretization is set to be:

| (3.11) |

where is the total number of grid points and the terminal time/last grid point is .

We mainly discretize Libor rate SDE in Eq. (2.4 or 2.6) under terminal measure or spot measure for Libor rates :

| (3.12) |

for . There are quite a few discretization schemes to discretize the Libor SDEs, among which are Euler scheme and predictor-corrector scheme.

For the discretization of the BSDE of discounted option price, there is a slight difference between the forward solver and the backward solver. Their descretizations are listed as follows.

-

•

Forward solver:

| (3.13) |

for .

-

•

Backward solver:

| (3.14) |

for , which is obtained by reordering the terms in Eq.(3.13).

3.4.2 Multilayer Feedforward Neural Network Based Algorithms

Given this temporal discretization, the path can be easily sampled using Eq. (3.12). Our key step next is to approximate the function at each time step by a multilayer feed forward neural network for

| (3.15) |

where denotes the parameters of the neural network approximating at . Thereafter, we have stacked all the sub-networks in Eq. (3.15) together to form a deep neural network as a whole, based on Eq. (3.13) or Eq. (3.14). Specifically, this network takes the Libor rate path and Brownian motion path as the input data and provides the final outputs. The forward and backward solvers are different in approximating the target function. For forward solver, the output is the approximated terminal payoff; while for the backward solver the initial value and gradient is the output. For detail, we refer to the following two subsections.

3.4.3 Stochastic Optimization Algorithms for Forward DNN Solver

First we apply the forward solver methodology [2, 3] to price European option in the Libor market model setting. We basically use Eqs. (3.12, 3.13) to project Libor rates and discounted option price samples forward from to . The final outputs for BSDE in Eq. (3.13) are , as an approximation of final actual discounted option payoff . The whole network flow is the following:

-

•

Input: Brownian motion path and the Libor rate path from Eq. (3.12).

-

•

Parameters: . The first parameter is the initial discounted option price, the second parameters are the gradients w.r.t underlying Libor rates at the initial point, and the remaining components of are the parameters used to approximate the option price gradients w.r.t Libor rates . The parameters across all simulated Libor samples are identical.

-

•

Forward projection iterations: for ,

| (3.16) |

where the initial price parameter =and the final output is .

After obtaining the neural network approximated final discounted payoff and actual discounted payoff, we need minimize the expected loss function below:

| (3.17) |

when samples of Monte Carlo simulation are used, can also be re-written as:

| (3.18) |

We can now use a stochastic gradient descent (SGD) algorithm to optimize the parameters, just as in the training of deep neural networks. After the optimization, the initial option price and Delta can be obtained. In our numerical examples, we use the Adam optimizer. For details of the methodology, we refer to papers [2, 3].

As aforementioned, this forward solver is only suitable for pricing European style options. The main advantages of this solver are as follows:

-

•

The Deltas are the direct outputs of this solver; while in Monte Carlo simulation, Deltas are normally calculated by using shock and revaluation method. Therefore, this method can save a large amount of computation times, which is critical for trading desks especially during periods when financial markets are very volatile.

-

•

This solver can handle high dimensional problems, which can not be handled by traditional PDE numerical method like finite difference method or finite element method. Therefore, this new approach makes it possible that some complex high-dimensional financial models like Libor market model can be solved in acceptable time intervals.

3.4.4 Stochastic Optimization Algorithms for Backward DNN Solver

In this subsection we present the new backward solver algorithm to solve European option pricing which mainly follows the steps below. Later, we discuss how the second step can be easily adjusted to meet the needs of Bermudan option pricing.

-

•

First, use Eq.(3.12) to project Libor rates forward from to .

Second, use obtained in previous step to calculate the final discounted option payoff ,

and then we use Eq.(3.14) to project discounted option price backward from to via

| (3.19) |

for .

-

•

Third, in theory, across all the backward simulated samples should be identical. Therefore our main idea is that after obtaining the neural network approximated sample initial option prices , we should minimize the expected loss function:

(3.20) which is also the variance of . When samples of Monte Carlo are generated, can also be re-written as:

(3.21) After minimizing the loss function, is defined as the initial discounted option price; and neural network approximated can be used as the initial Libor Delta. The complete set of parameters are adjusted in the process of approximating the option price gradients. The essential difference lies in the fact that for backward DNN solver the initial option price and gradients are not included in this parameter set. Other than the backward projection, our backward solver shares a similar structure in discretization and parameterization compared to the forward solver which we discussed in prior two subsections. We aslo refer to section 4.1 of paper [2] for more detail. We use a stochastic gradient descent (SGD) algorithm to optimize the parameters, same approach adopted for the training of forward feed deep neural networks. In our numerical examples, we continue to use the Adam optimizer.

Figure 3.1 illustrates the architecture of the deep BSDE backward solver with .

There are three types of connections in this network:

-

1.

is characterized by (3.12) using Euler/predictor-corrector scheme. There are no parameters to be optimized in this type of connection.

-

2.

is the multilayer feed forward neural network approximating the spatial gradients at time Here we have hidden layers for each time point. The weights of this sub-network are the parameters we aim to optimize. Basically, decides the linear/nonlinear transformation from input layer to hidden layer, between hidden layers and from last hidden layer to gradient output, and includes all the potential batch-normalization parameters involved in the process as well. We will illustrate more in our simulation. For more detail, we refer to Section 4.1 of paper [2].

-

3.

is the backward iteration that finally outputs an approximation of , completely characterized by (3.19) . There are no parameters to be optimized in this type of connections.

The backward solver enjoys many same advantages of the forward solver, which we discussed in the previous sections. Additionally, this backward solver can not only to price European options, but also to price Bermudan swaptions which we will soon discuss in Section 4. The option price BSDE (3.9) is projected backward. When passing one exercise date, the exercise information on this exercise date can be easily used to update the value by the following formula:

| (3.22) |

where represents the time immediately before the exercise time, represents the time immediately after the exercise time. represents discounted intrinsic value for option at the exercise time, which depends on the type of option. For example, the discounted intrinsic value for a receiver Bermudan swaption at exercise time t is:

| (3.23) |

where is the fixed rate of the underlying swap, is the index of the first Libor rate which is not reset at exercise time , is the total number of Libor rates, is the accrual time. Here we assume accrual time for fixed leg and float leg is the same and exercise time t is part of the reset dates of Libor rates.

In more detail, suppose a Bermudan swaption has exercise dates on (For a Bermudan swaption, all the exercise dates are part of Libor reset dates) where the last exercise date . The only adjustment needed on exercise date for the Bermudan swaption is to replace the Eq.(3.19) with the following backward projected evaluation:

| (3.24) |

Here, the exercise dates partition the time horizon into multiple time intervals and iteration formula within each time interval remains the same as the European swaption case, but there is only one difference in the exercise dates where the backward update is now the max of (1) first order approximation of price function with information carried backwards and (2) the current exercise value.

Between any two consecutive exercise dates, e.g. within , is the approximation of holding value for that specific sub-interval, i.e. as in subsection3.3. The validity of this approximation is guaranteed by Eq. 3.10 which is a backward iteration to price the holding values. Similar to the backward simulation approach in papers[1, 6, 7], the backward BSDE solver actually still forward simulates the dynamics of Libor rates. However, the application of Bellman dynamic programming based on the simulated underlying Libor rate dynamics a reliable approximation of holding value in a later period helps to determine the holding value for the period right before, and hence the approximation of holding values for all the simulated paths in a backward way is made feasible. Unlike the conventional Monte Carlo pricer that may relies on exponentially growing number of paths to evaluate the expected future value, our neural network BSDE solver needs to use very limited number of sample paths since it uses a parametric form gradient approximation which achieves the efficient use of information across all sample scenarios. Compared with classical approach in papers [1, 6, 7] the neural network approach adopts a trainable and more complex form of function approximation that leads to accuracy much efficiently.

The capability of backward solver to price Bermudan swaption shoes the potential application of DNN based BSDE solver in a wide range of different Bermudan- style rate options, such as Bermudan swaptions, Callable CMS spread options, Callable Bonds and Callable Range Accruals, to name a few.

In the next section, we will test the robustness of forward and backward solvers under varying trade settings to price interest rate options with respect to solver convergence, stability and accuracy.

4 Numerical Results

We show numerical examples using deep neural network BSDE solver to price various interest rate options in this section. The first example is to price co-terminal European swaptions using the forward solver. The second example assumes a flat yield curve to price European swaptions using forward and backward solvers respectively. The pricing differences are very small between the two solvers. The third example uses a real market yield curve instead of a flat yield curve. The pricing results again show the differences between the two BSDE solvers are non-material. The fourth example is to price a short maturity Bermudan swaption pricing using the backward solver. The last example is for a long maturity Bermudan swaption pricing by the backward solver. Each of the numerical examples is performed with Python programming using TensorFlow444An open-source library for data flow programming across a range of tasks..

4.1 Co-terminal European Swaption Pricing using Forward Solver

First, we use the forward solver to price European swaptions. Under spot measure, we can build the BSDE solver by combining Eqs.(2.6, 3.6, 3.7 and 3.9).

The swaption, market inputs, and LMM set-up are listed as follows:

-

•

The swaptions we use for testing are ATM co-terminal swaptions with notional equal to 1 and terminal time . The expiry time is listed in the following table:

T Expiry 0.0000 0.5028 1.0139 1.5167 2.0278 2.5333 3.0472 3.5528 4.0583 4.5639

Table 2: The expiries of co-terminal swaptions -

•

In order to price these swaptions, there are nine dynamic processes in LMM corresponding to Libor rates . There are nine Brownian motions driving these processes, and the model is of nine factors. Since the first Libor rate is already reset at time , there is no stochastic process driving this rate.

-

•

The volatility term structure for each Libor rate is a hump-shaped function: . The values of volatility parameters are listed in the following table:

Parameter a b c d Value 0.291 1.483 0.116 0.00001

Table 3: The values of vol parameters -

•

The correlation structure of Libor rates , are defined by function: , where is set to be 0.5.

-

•

Yield curve is a flat zero curve with continuous compounding rate 4.00%, from which the initial Libor rates are calculated, which are listed in the following table:

Libor Rate Value 4.0405% 4.0412% 4.0405% 4.0412% 4.0407% 4.0414% 4.0407% 4.0407% 4.0407% 4.0409%

Table 4: The initial Libor rates.

We use predictor-corrector method to discretize Eq.(2.6) and the time step is one month. We show some of the projected shapes of the yield curves Figure 4.1. From the figure, we can observe that this 9-factor LMM can generate rich shapes of yield curves: inverted, flat, and upward.

The deep neural network setting is: each of the sub neural network approximating gradient consists of 4 layers (1 input layer [d-dimensional], 2 hidden layers [both d+10-dimensional], and 1 output layer [d-dimensional]). In this case d = 10. The inputs of this sub-neural network are Libor rates and its outputs are the gradient of option prices with respect to the inputs. In the test, we run 10,000 optimization iterations and use 4096 Monte Carlo samples for optimization.

We compare the results with the the results from Quantlib for sort of benchmarking. The method used in QuantLib is conventional Monte Carlo simulation with 50,000 scenarios. In the test, we take notional of swaption to be 1. The results are very close and their relative differences are well within 0.5%. The details are listed in the Table 5 through Table 7.

Expiry\Tenor 1.0139 2.0250 3.0444 3.5556 4.0583 4.5694 0.5028 0.004050 1.0139 0.005312 1.5167 0.005879 2.0278 0.006034 3.0472 0.005394 4.0583 0.003554

Expiry\Tenor 1.0139 2.0250 3.0444 3.5556 4.0583 4.5694 0.5028 0.004068 1.0139 0.005328 1.5167 0.005883 2.0278 0.006024 3.0472 0.005385 4.0583 0.003566

Expiry\Tenor 1.0139 2.0250 3.0444 3.5556 4.0583 4.5694 0.5028 0.44% 1.0139 0.31% 1.5167 0.06% 2.0278 -0.16% 3.0472 -0.17% 4.0583 0.35%

Another benefit of the DNN-based forward solver is that the first order sensitivity Delta can be direct outputs from the valuation process, which saves a large amount of computational time. While in conventional Monte Carlo simulation, the Delta is calculated by shock and revalue method, Table 8 shows their comparison for swaption (expiry: 1.5167Yr, tenor: 3.5556Yr). From the table, we conclude the results are very close: for Libor rates , they are mainly used to discount cash flows and have very small exposure to the swaption price. Hence, Deltas w.r.t those rates are very small and their relative differences are relatively large.

Libor Rate QuantLib -0.0029 -0.0029 -0.0029 -0.2234 -0.2131 -0.2144 -0.2096 -0.2084 -0.2075 -0.2074 Forward solver 0.0007 -0.0028 -0.0018 -0.2249 -0.2127 -0.2149 -0.2099 -0.2095 -0.2083 -0.2077 Relative_Diff -125.14% -2.97% -37.31% 0.67% -0.19% 0.25% 0.12% 0.51% 0.39% 0.15%

Overall, we found that deep neural network based BSDE solver is effective for derivative pricing under LMM. One of the great benefits is that it can generate the first order sensitivity directly.

4.2 Comparison of Forward Solver and Backward Solver in European Swaption Pricing

In this subsection, we use both DNN-based forward and backward solvers to price European swaptions and then we compare their performance from the perspective of accuracy and convergence. The Libor market model set-up, market information, BSDEs, and Neural Network setting are the same as in Section 4.1. The European swaption we use for testing is ATM with expiry and terminal time for underlying swap , and its notional is 1.

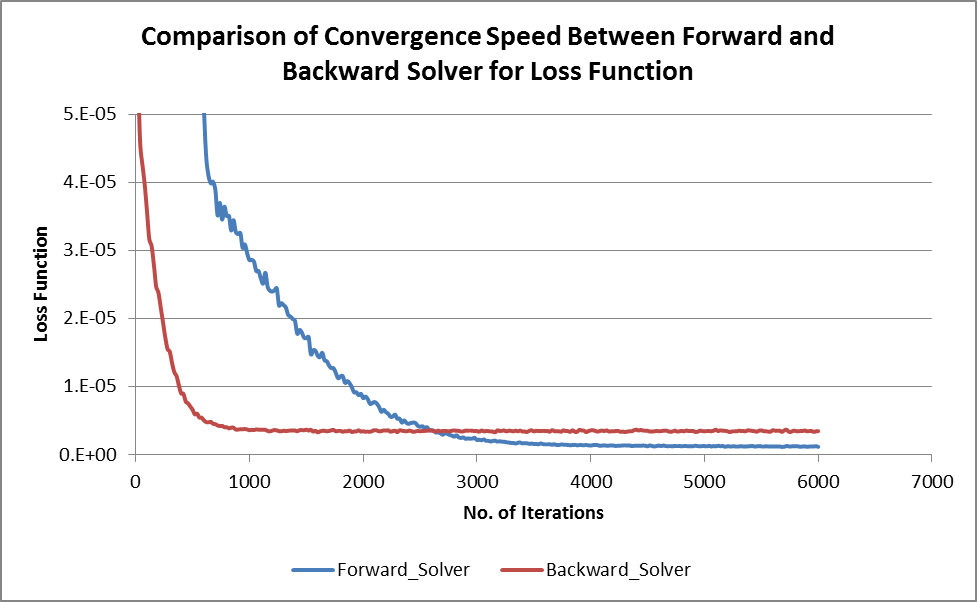

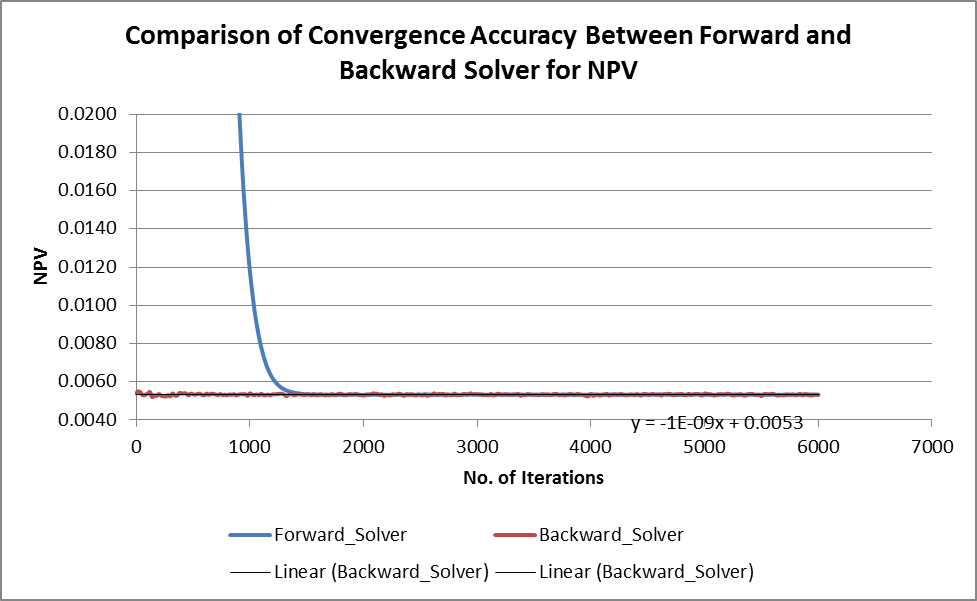

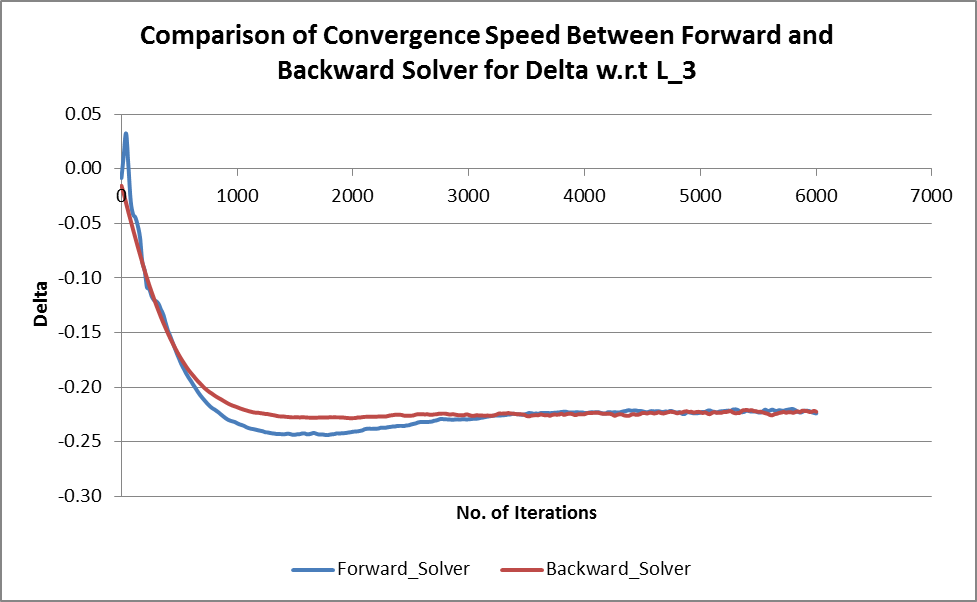

Table 9 and Table 10 present the calculation of the mean of , the standard deviation of , the mean of the loss function , the standard deviation of the loss function , and the run time in seconds needed to calculate one realization of against number of optimization iterations based on 5 independent runs and 4096 Monte Carlo samples with monthly time step. From the tables, we conclude the following:

-

•

The approximated Europen swaption prices from the two solvers converge very fast to around 0.00532. For forward solver, the price converges with 4,000 iterations while it needs only 2,000 iterations for backward solver.

-

•

The tests run on one V100 GPU in DGX-1 server, the speed is similar for forward and backward solver.

Number of Iteration Steps m Mean of STD of Mean of the Loss Function STD of the Loss Function Runtime in sec. for one run 2000 0.005330 4.39E-06 1.70E-05 4.31E-06 37 4000 0.005330 1.14E-06 1.67E-06 4.48E-07 74 6000 0.005329 1.53E-06 1.18E-06 2.90E-08 106

Number of Iteration Steps m Mean of u STD of u Mean of the Loss Function STD of the Loss Function Runtime in sec. for one run 2000 0.005318 3.31E-06 3.39E-06 1.13E-08 38 4000 0.005315 7.94E-06 3.31E-06 5.55E-09 73 6000 0.005322 7.17E-06 3.30E-06 1.01E-08 109

Figure 4.2 through Figure 4.5 show the convergence speed and accuracy of NPVs and Deltas from the two solvers. From the figures, we conclude that

-

•

the accuracy of the two solvers are are quite close, but the convergence speed of the back solver is faster than that of the forward solver;

-

•

the loss function of the backward solver is above that of the forward solver because they represent two different targets. The loss function of the backward solver represents the variance of while the loss function of the forward solver represents mean of square of difference between the projected terminal payoffs and the actual terminal payoffs. It is clear that the performance of a BSDE solver closely depends the on the loss function imposed for convergence.

4.3 Comparison of Forward Solver and Backward Solver in Co-terminal European Swaption Pricing

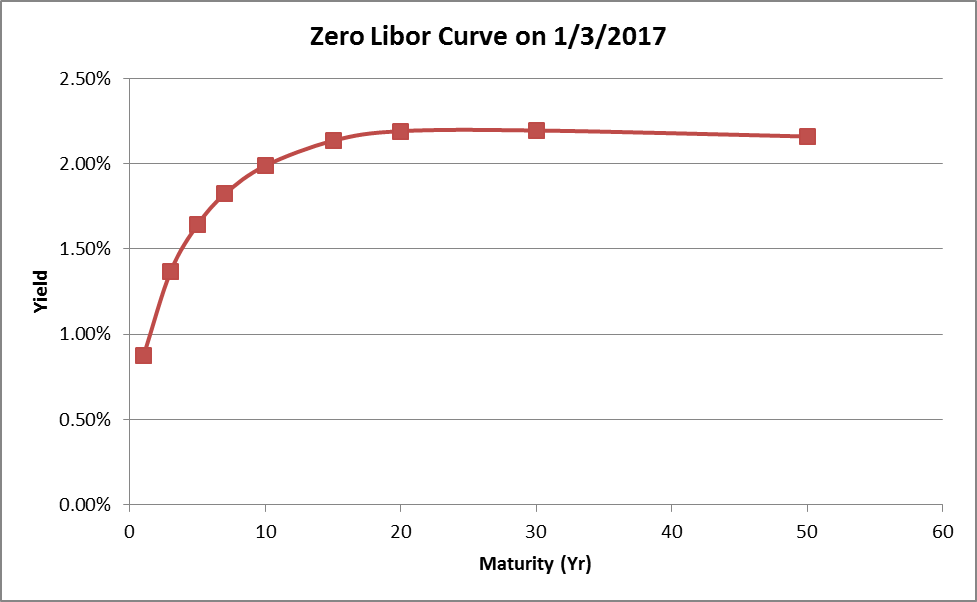

In this subsection, we use a real market yield curve on January 3, 2017, for interest rate option pricing. The curve is shown in the following figure:

.

It is an upward yield curve, used for the calculation of the initial Libor rates, which are listed in the Table 11:

Libor Rate Value 1.1842% 1.1843% 1.9085% 1.9087% 1.9067% 1.9035% 2.3785% 2.3826% 2.3826% 2.3827%

.

Except the yield curve, all the other information such as swaption data, market data, LMM set-up, and neural network set-up are the same as those contained in Section 4.1. We mainly compare three numerical results:

-

•

Result from forward solver.

-

•

Result from backward solver.

-

•

Result from QuantLib.

The numerical results include NPVs of ATM co-terminal European swaptions and direct outputs of Deltas for one swaption (expiry: 1.5167Yr, tenor: 3.5556Yr). The results are listed in Table 12 through Table 17. Checking the results, we conclude the following:

-

•

All the NPVs are very close and their relative differences to QuantLib are all within 0.5%.

-

•

All the Detlas are very close except those w.r.t. Libor rates , which are mainly used to discount cash flows and have very small exposure to the swaption price. Hence, Deltas w.r.t. these three Libor rates are very small and close to 0 although their relative differences are much larger.

-

•

Using QuantLib as the base, the forward solver is slightly more accurate than the backward solver. Relative differences of Delta from the forward solver are mostly within 0.5% range, while those of the backward solver are mostly within 1.0%.

Therefore, this comparison helps us to conclude that DNN-based solver is accurate to price swaptions under distinct initial yield curves.

Expiry\Tenor 1.0139 2.0250 3.0444 3.5556 4.0583 4.5694 0.5028 0.002107 1.0139 0.002933 1.5167 0.003339 2.0278 0.003550 3.0472 0.003482 4.0583 0.002316

Expiry\Tenor 1.0139 2.0250 3.0444 3.5556 4.0583 4.5694 0.5028 0.002114 1.0139 0.002948 1.5167 0.003337 2.0278 0.003542 3.0472 0.003479 4.0583 0.002326

Expiry\Tenor 1.0139 2.0250 3.0444 3.5556 4.0583 4.5694 0.5028 0.35% 1.0139 0.51% 1.5167 -0.07% 2.0278 -0.23% 3.0472 -0.07% 4.0583 0.42%

Expiry\Tenor 1.0139 2.0250 3.0444 3.5556 4.0583 4.5694 0.5028 0.002104 1.0139 0.002940 1.5167 0.003335 2.0278 0.003539 3.0472 0.003475 4.0583 0.002324

Expiry\Tenor 1.0139 2.0250 3.0444 3.5556 4.0583 4.5694 0.5028 -0.15% 1.0139 0.24% 1.5167 -0.13% 2.0278 -0.31% 3.0472 -0.20% 4.0583 0.35%

Libor Rate QuantLib -0.0017 -0.0017 -0.0016 -0.2356 -0.2266 -0.2291 -0.2240 -0.2242 -0.2250 -0.2324 Forward solver 0.0010 -0.0031 -0.0012 -0.2363 -0.2262 -0.2303 -0.2236 -0.2250 -0.2254 -0.2284 Relative_Diff_1 -160.76% 79.71% -24.44% 0.29% -0.17% 0.54% -0.19% 0.34% 0.17% -1.73% Backward solver 0.0005 -0.0015 -0.0018 -0.2371 -0.2286 -0.2302 -0.2261 -0.2250 -0.2261 -0.2281 Relative_Diff_2 -130.82% -13.12% 9.94% 0.63% 0.90% 0.47% 0.94% 0.35% 0.49% -1.85%

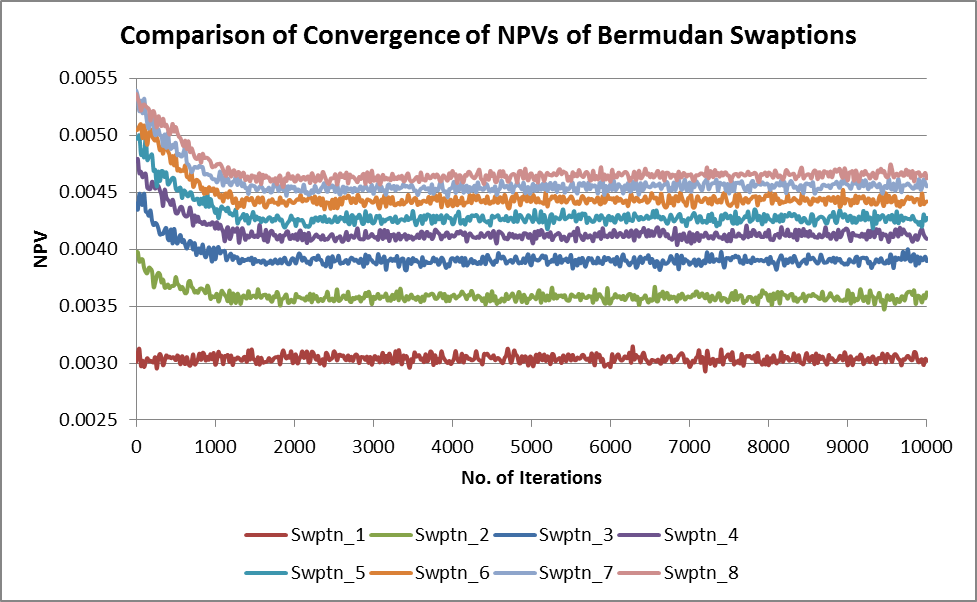

4.4 Short Maturity Bermudan Swaption Pricing using Backward Solver

In this subsection, we use backward solver to price Bermudan swaptions with short maturity. The Libor market model set-up, market information, BSDEs and Neural Network setting are the same as those in Section 4.3. A total of 4096 simulated samples/paths are used for optimization. The Bermudan swaptions we use for testing are listed in Table 18.

-

•

The exercise times of Bermudan swaptions are listed in the following table

T Expiry 1.0139 1.5167 2.0278 2.5333 3.0472 3.5528 4.0583 4.5639

Table 18: The exercise time of short term Bermudan swaption .

-

•

There are 8 Bermudan swaptions in total: Bermudan swaption 1 (swaption 1) contains one exercise time which is ; Bermudan swaption 2 (swaption 2) contains two exercise time which is , ; … ; Bermudan swaption 8 (swaption 8) contains eight exercise time which is , , …, .

-

•

Their underlying swaps have the same terminal time which is 5.0722 Yr.

-

•

They have the same notional, which is 1 and they have the same strike, which is 2.1442%.

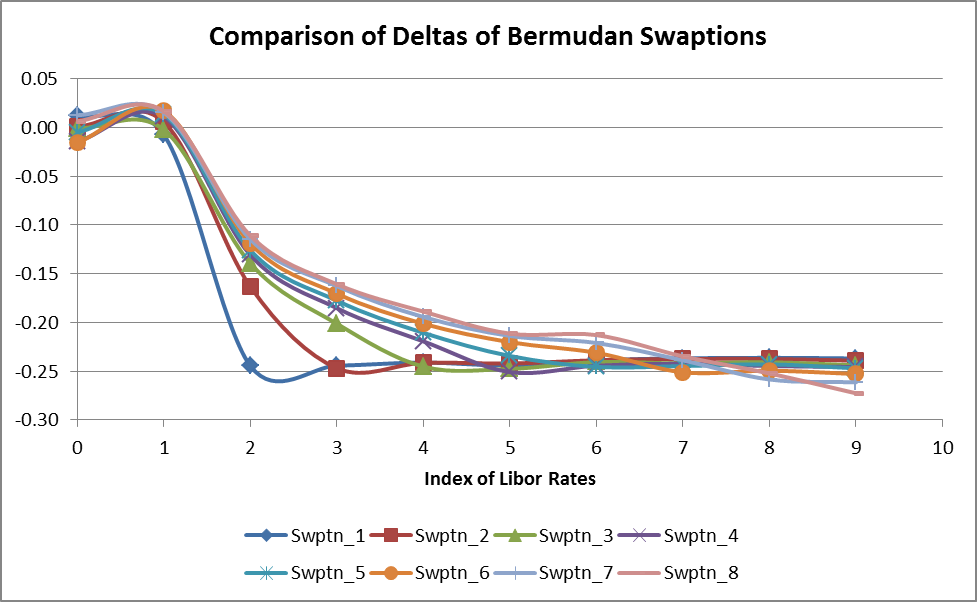

Table 19, Table 21, and Figure 4.7 through Figure 4.9 show the NPVs and Deltas of Bermudan swaptions. From the results, we have the following observations:

-

•

The convergence of NPVs is steady. With increasing number of exercise times, the convergence speed slows down.

-

•

With the increase of exercise times, NPVs also increase quite smoothly with the rate of increase slowing down.

-

•

Deltas w.r.t and are very small and close to 0 for all swaptions, because they are ahead of all exercise time and are mainly used for discounting.

-

•

With the increase of exercise times, magnitudes of Deltas w.r.t near term Libor rates such as decrease, while magnitudes of Deltas w.r.t farther term Libor rates such as increase. Here we treat Delta in absolute value. The detail findings are listed below.

-

–

For swptn_1, Libor rates , , …, are all behind exercise time: and hence all of them are the underlyings of swptn_1. Therefore Deltas w.r.t , , …, are very close.

-

–

For swptn_2, Libor rate is the underlying of the first exercise time: , , , …, are the underlyings of the two exercise time: and . Therefore compared to swptn_1, Delta w.r.t decreases, while Deltas w.r.t , , …, increase.

-

–

With the same logic, other remaining swaptions demonstrate similar pattern. For example, for swptn_9, is the underlying of the first exercise time: , is the underlying of the first two exercise time: and , …, is the underlying of all exercise time: , , …, . Therefore we can see the clear pattern that

-

–

-

•

The computational speed is fast. We run the tests on one V100 GPU and it takes around 1~2 minutes with quarterly time step.

Therefore, we can conclude that the prices and Deltas from the backward solver are effective and efficient. The backward solver is well-adapted to price Bermudan swaptions.

Swptn_1 Swptn_2 Swptn_3 Swptn_4 Swptn_5 Swptn_6 Swptn_7 Swptn_8 Time (s) 64 79 95 106 127 135 137 149 NPV 0.003005 0.003553 0.003882 0.004097 0.004263 0.004412 0.004541 0.004628 Diff_NPV 0.000548 0.000329 0.000215 0.000166 0.000149 0.000129 0.000087

Swptn_1 Swptn_2 Swptn_3 Swptn_4 Swptn_5 Swptn_6 Swptn_7 Swptn_8 Time (s) 64 79 95 106 127 135 137 149 NPV 0.003005 0.003553 0.003882 0.004097 0.004263 0.004412 0.004541 0.004628 Diff_NPV 0.000548 0.000329 0.000215 0.000166 0.000149 0.000129 0.000087

Swptn\Underlying Swptn_1 0.0119 -0.0077 -0.2445 -0.2443 -0.2410 -0.2440 -0.2388 -0.2367 -0.2362 -0.2369 Swptn_2 0.0009 0.0055 -0.1634 -0.2469 -0.2413 -0.2421 -0.2387 -0.2374 -0.2373 -0.2392 Swptn_3 -0.0010 -0.0024 -0.1394 -0.2013 -0.2453 -0.2475 -0.2406 -0.2420 -0.2408 -0.2440 Swptn_4 -0.0146 0.0109 -0.1309 -0.1853 -0.2193 -0.2508 -0.2442 -0.2423 -0.2446 -0.2456 Swptn_5 -0.0052 0.0133 -0.1260 -0.1776 -0.2106 -0.2343 -0.2455 -0.2446 -0.2429 -0.2470 Swptn_6 -0.0157 0.0170 -0.1192 -0.1704 -0.2013 -0.2202 -0.2311 -0.2510 -0.2494 -0.2529 Swptn_7 0.0125 0.0153 -0.1148 -0.1627 -0.1944 -0.2138 -0.2210 -0.2387 -0.2584 -0.2613 Swptn_8 0.0063 0.0166 -0.1110 -0.1608 -0.1888 -0.2114 -0.2129 -0.2347 -0.2522 -0.2726

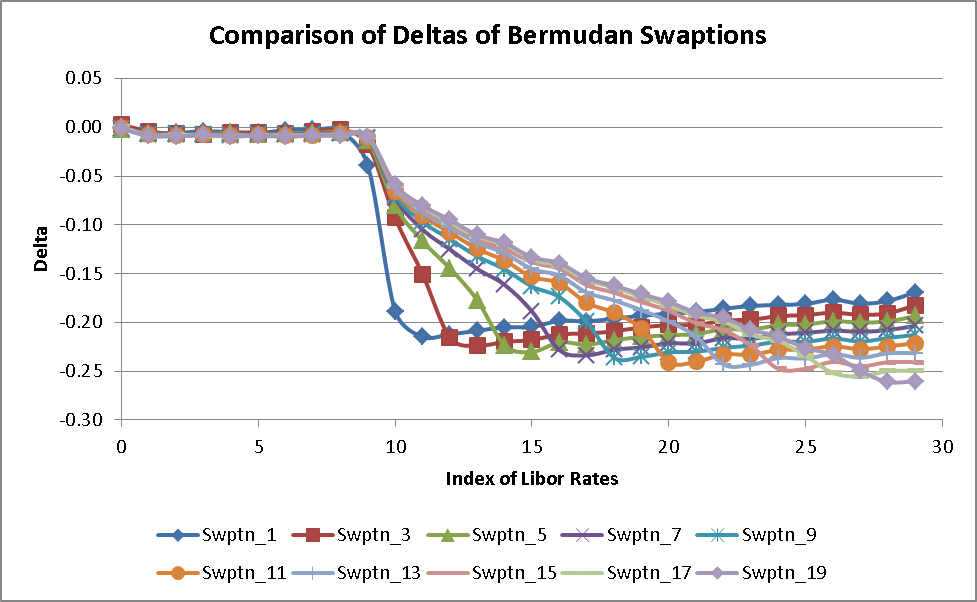

4.5 Long Maturity Bermudan Swaption Pricing using Backward Solver

In this last example, we use backward solver to price long maturity Bermudan swaptions. The Libor market model set-up, market information, BSDEs and Neural Network setting are the same as those in Section 4.4, except that the dimensions of PDEs increase from 10 to 30 since there is a total of 30 Libor rates involved. A total of 4096 simulated samples/paths are used for optimization. The Bermudan swaptions we use in testing are listed below.

-

•

The exercise times of long maturity Bermudan swaption are listed in the following table with each time interval around 0.5Yr.

T … Expiry 5.0667 5.5694 6.0861 … 14.2028 14.7083

Table 22: The exercise time of long term Bermudan swaption .

-

•

There are 10 Bermudan swaptions in total: Bermudan swaption 1 (swaption 1) contains one exercise time which is ; Bermudan swaption 3 (swaption 3) contains three exercise time which is , , ; …; Bermudan swaption 19 (swaption 19) contains 19 exercise time which is , , , …, .

-

•

Their underlying swaps have the same terminal time, which is .

-

•

They have the same notional, which is 1 and they have the same strike, which is 2.7155%.

Table 23 and Figure 4.10 through Figure 4.12 show the NPVs and Deltas of long term Bermudan swaptions. From the results, we have the following observations:

-

•

The convergence of NPVs is steady. With increasing number of exercise times, the convergence speed slows down. Therefore we use more iterations for Bermudan swaptions with more exercise times.

-

•

With the increase of exercise times, NPVs also increase quite smoothly with the rate of increase slowing down.

-

•

Deltas w.r.t the first 10 Libor rates are very small and close to 0 for all swaptions, because they are ahead of all exercise time and are mainly used for discounting.

-

•

With the increase of exercise times, magnitudes of Deltas w.r.t near term Libor rates such as decrease, while magnitudes of Deltas w.r.t further term Libor rates such as increase. Here we treat Delta in absolute value. The detail findings are as follows:

-

–

For swptn_1, Libor rates , , …, are all behind exercise time and hence all of them are the underlyings of swptn_1. Therefore Deltas w.r.t , , …, are close with the trend going down due to the discounting.

-

–

For swptn_2, Libor rate is the underlying of the first exercise time , , , …, are the underlyings of the two exercise time and . Therefore compared to swptn_1, Delta w.r.t decreases, while Deltas w.r.t , , …, increase.

-

–

With the same logic, other remaining swaptions have similar pattern. For example, for swptn_19, is the underlying of the first exercise time , is the underlying of the first two exercise time and , …, is the underlying of all exercise time , , …, . Therefore we can see the clear pattern that

-

–

-

•

The computational speed is fast. We run the tests on one V100 GPU and it takes about 3 minutes for swptn_1, 4.5 minutes for swptn_3, … , 20 minutes for swptn_19. The time step is quarterly.

Therefore, we can conclude that the prices and Deltas from the backward solver are reasonable. The backward solver is effective to price the Bermudan swaption with long maturity.

Swptn_1 Swptn_3 Swptn_5 Swptn_7 Swptn_9 Swptn_11 Swptn_13 Swptn_15 Swptn_17 Swptn_19 Time(Min) 3 4.5 6 7.5 10 12 14 16 18 20 NPV 0.01012 0.01173 0.01286 0.01384 0.01468 0.01539 0.01601 0.01657 0.01700 0.01725 Diff_NPV 0.00161 0.00113 0.00099 0.00084 0.00071 0.00062 0.00056 0.00043 0.00025

It is quite encouraging that the DNN-based BSDE backward solver works well for Bermudan swaptions of all maturities.

5 Conclusion

In this work, we have developed a deep neural network-based BSDE solver for Libor Market Model (LMM) based on the recent works on Artificial Intelligence and Machine Learning developments. Our forward deep learning implementation adopts a similar approach as the one explored by Weinan E et al. [2, 3], which uses neural network to solve high dimensional parabolic PDEs (or their equivalent BSDEs). However, the standard forward DNN solver is only suitable for pricing European style options. Therefore, in order to price callable derivatives such as Bermudan interest rate options, we developed a backward DNN solver, which has a parallel neural network structure as forward solver. Our new methodology projects the option price backward to the initial time with the loss function given by the variance of the projected option price at initial time. We have tested a few numerical examples to illustrate that the backward solver works as accurately as forward solver and Monte Carlo simulation method in QuantLib. The prices of Bermudan swaption calculated using backward DNN solver are quite reasonable. These deep neural network based solvers have clear advantage over traditional methods:

(1) They can produce gradients of option price (Delta) directly.

(2) They are highly scalable and can be applied to many high dimensional PDEs without changing its implementation.

(3) They can easily be implemented in Python using TensorFlow, which runs efficiently in GPU.

(4) The capability of backward solver to price Bermudan swaption makes deep learning-based solver suitable for a wide range of different applications, since most of the traded financial instruments in hedging risks are Bermudan style rate options such as Bermudan style swaptions, Callable CMS spread options, and Callable Range Accruals, etc.

This general methodology can also be applied to other asset groups such as equity, foreign exchange, commodity, and various value adjustment processes. Our immediate further work will be focused on putting more structures in LMM with DNN implementation. Some theoretical questions in mathematics and DNN structure are interesting for us to explore when we will apply this new approach in our model risk management, including model validation.

References

- [1] Francis A. Longstaff, Eduardo S. Schwartz. Valuing American Options by Simulation: A Simple Least-Squares Approach, The Review of Financial Studies, Volume 14, Issue 1, 1 January 2001, Pages 113–147.

- [2] Weinan E, Jiequn Han, and Arnulf Jentzen. Deep learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations, A. Commun. Math. Stat. (2017) 5: 349.

- [3] Jiequn Han, Arnulf Jentzen, and Weinan E. Overcoming the curse of dimensionality: Solving high-dimensional partial differential equations using deep learning, arXiv:1707.02568.

- [4] Heath D., R. Jarrow, and A. Morton. Bond Pricing and the Term Structure of Interest Rates: A New Methodology, Econometrica, 60, 1 (1992), 77105.

- [5] Brace A, D. Gararek, and M. Musiela. The Market Model of Interest Rate Dynamics, Mathematical Finance, 7, 2 (1997), 12755.

- [6] Andersen, L. A Simple Approach to the Pricing of Bermudan Swaptions in the Multifactor LIBOR Market Model, Working paper, Gen Re Financial Products, 1998.

- [7] Broadie, M. and P. Glasserman. A Stochastic Mesh Method for Pricing High Dimensional American Options, Working Paper, Columbia University, New York, 1997.

- [8] T. Gerstner, P. Kloeden (Eds.), Recent Developments in Computational Finance. Foundations, Algorithms and Applications, World Scientific Publishers, Interdisciplinary Mathematical Science, 2013.

- [9] G. Beylkin, M.J. Mohlenkamp, Algorithms for numerical analysis in high dimensions, SIAM J. Sci. Comput. 26 (6) (2005) 2133–2159.

- [10] Josï¿œ G. Lï¿œpez-Salas, Carlos Vï¿œzquez, PDE formulation of some SABR/LIBOR market models and its numerical solution with a sparse grid combination technique, Computers and Mathematics with Applications 75 (2018) 1616–1634.

- [11] Leif B. G. Andersen and Vladimir V. Piterbarg. Interest Rate Modeling. Volume 1, 2: Term Structure Models, Atlantic Financial Press.

- [12] N. El Karoui, S. Peng and M. C. Quenez. Backward Stochastic Differential Equations in Finance, Mathematical Finance, Vol. 7, No. 1 (January 1997), 1-71

- [13] E. Pardoux and S.G. Peng. Adapted solution of a backward stochastic differential equation, Systems & Control Letters 14 (1990) 55-61

- [14] E. Pardoux and S.G. Peng. Backward stochastic differential equations and quasilinear parabolic partial differential equations. Stochastic Partial Differential Equations and Their Applications pp 200-217

- [15] Jin Ma and Jiongmin Yong. Forward-Backward Stochastic Differential Equations and their Applications (Lecture Notes in Mathematics) Corrected Edition

- [16] E. Pardoux and Aurel Rascanu. Stochastic Differential Equations, Backward SDEs, Partial Differential Equations (Stochastic Modelling and Applied Probability) 2014th Edition

- [17] Wendell H. Fleming and Raymond W. Rishel. Deterministic and Stochastic Optimal Control (Stochastic Modelling and Applied Probability) (v. 1) 1st Edition

- [18] Huyï¿œn Pham. Continuous-time Stochastic Control and Optimization with Financial Applications (Stochastic Modelling and Applied Probability) 2009th Edition

- [19] Jiongmin Yong and Xun Yu Zhou. Stochastic Controls: Hamiltonian Systems and HJB Equations (Stochastic Modelling and Applied Probability) 1999th Edition

- [20] Jianfeng Zhang. Backward Stochastic Differential Equations: From Linear to Fully Nonlinear Theory (Probability Theory and Stochastic Modelling) 1st ed. 2017 Edition

- [21] Rumelhart, D. E., Hinton, G. E., and Williams, R. J. Learning representations by back-propagating errors. Nature (1986), 323, 533–536.

- [22] Goodfellow, I., Bengio, Y., and Courville, A. Deep Learning. MIT Press, 2016. http://www.deeplearningbook.org.

- [23] Hinton, G. E., Deng, L., Yu, D., Dahl, G., Mohamed, A., Jaitly, N., Senior, A., Vanhoucke, V., Nguyen, P., Sainath, T., and Kingsbury, B. Deep neural networks for acoustic modeling in speech recognition. Signal Processing Magazine 29 (2012), 82–97

- [24] Krizhevsky, A., Sutskever, I., and Hinton, G. E. Imagenet classification with deep convolutional neural networks. Advances in Neural Information Processing Systems 25 (2012), 1097–1105.

- [25] LeCun, Y., Bengio, Y., and Hinton, G. Deep learning. Nature 521 (2015), 436–444.

- [26] Kai , Marc Peter Deisenroth, Miles Brundage, Anil Anthony Bharath. A Brief Survey of Deep Reinforcement arXiv:1708.05866