At the Mercy of the Common Noise: Blow-ups in a Conditional McKean–Vlasov Problem

Abstract

We extend a model of positive feedback and contagion in large mean-field systems, by introducing a common source of noise driven by Brownian motion. Although the driving dynamics are continuous, the positive feedback effect can lead to ‘blow-up’ phenomena whereby solutions develop jump-discontinuities. Our main results are twofold and concern the conditional McKean–Vlasov formulation of the model. First and foremost, we show that there are global solutions to this McKean–Vlasov problem which can be realised as limit points of a motivating particle system with common noise. Furthermore, we derive results on the occurrence of blow-ups, thereby showing how these events can be triggered or prevented by the pathwise realisations of the common noise.

1 Introduction

This paper studies a model of positive feedback and contagion in large mean-field systems, focusing on the interplay between positive feedback loops and a common source of noise in the driving dynamics. Specifically, we consider the convergence of the underlying finite-dimensional particle system as the number of particles tends to infinity, and we illuminate the emergence of ‘blow-up’ phenomena in the limiting McKean–Vlasov problem

| (MV) |

Here the random drivers and are independent Brownian motions, and the start point is an independent random variable taking values in the positive half-line , while and are constant parameters. By a solution to (MV) we understand an increasing process that is càdlàg with values in and zero at zero, i.e., .

As we will see, the common noise, , plays a pivotal role: in certain cases it has the power to provoke or prevent a blow-up, where a blow-up is defined as a jump discontinuity of . A key property of (MV) is that these blow-ups occur endogenously: all the random drivers are continuous, yet jump discontinuities can develop through the positive feedback effect alone.

The main technical results in this paper are twofold. Firstly, we analyse the blow-up phenomena of (MV) and derive some simple conditions for if and when such blow-ups occur, with the aim of highlighting the essential role played by the common noise (see Theorem 2.1). Secondly, we show that solutions to (MV) arise as large population limits of a ‘contagious’ particle system, which provides the theoretical justification for the various applications discussed below. We establish this convergence result for more general drift and diffusion coefficients than the case (MV), and we allow for a large class of natural initial conditions (see Theorem 3.2).

To get a better feel for the workings of (MV), consider the conditional law of , with absorption at the origin, given the common noise . This defines a flow of random sub-probability measures , where

thus describing how the ‘surviving’ mass of the system evolves. In particular, we can then write , which gives the accumulated loss of mass up to time . From this point of view, a blow-up corresponds to a strictly positive amount of mass being absorbed at the origin in an infinitesimal period of time. A priori, the associated jump of is not uniquely specified by the equation (MV) alone, however, we can fix a canonical choice in terms of the left limits of , at any given time , according to the minimality constraint (2.2), which will be introduced in Section 2.

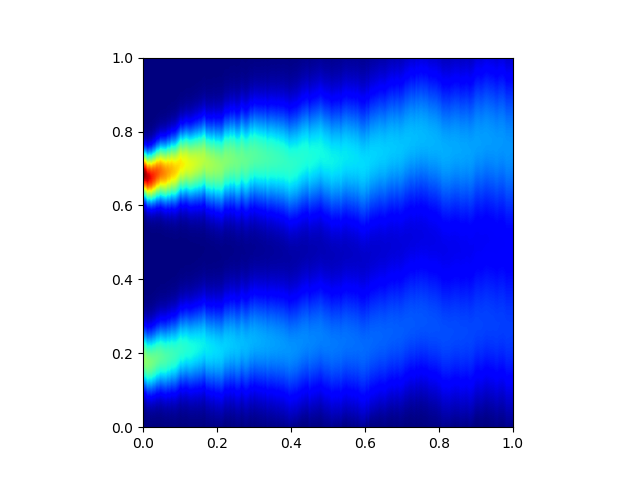

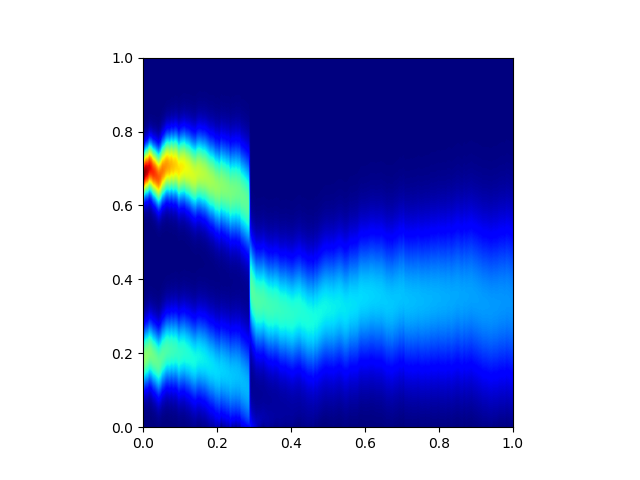

In Lemma 2.2 below, we show that there is a density of , as defined above, for all positive times . Figure 1.1 illustrates the flow of these densities, for two given realisations of the common noise —one of which leads to a blow-up, whose timing and magnitude is specified by the aforementioned minimality constraint.

Remark 1.1 (Stochastic evolution equation).

As we show in Proposition 3.7, in a generalized sense, the flow of the densities is governed by the stochastic evolution equation

on the positive half-line with an absorbing boundary at the origin (where we recall that the jump sizes are specified by (2.2) as mentioned above). Noting that the nonlinearity ‘’ gives the flux of mass across the origin, this evolution equation provides the connection between (MV) and the mathematical neuroscience literature discussed below. We refer to Section 3.3 for further details, but we note here that the equation is quite different from typical stochastic PDEs treated in the literature, as it is nonlocal in space, and, in time, one cannot expect anything like absolute continuity of or, say, for an exogenous driver .

1.1 Applications and related literature

Our main interest in (MV) stems from its potential to serve as a mean-field model for the interplay between common exposures and contagion in large financial systems, as also discussed in [18]. In this setting, gives the distance-to-default of a ‘typical’ bank or credit-risky asset, captures the extent of common exposures, and imposes a contagious feedback effect from defaults. It then follows that a jump discontinuity of corresponds to a ‘default cascade’ in which the feedback from default contagion explodes and a macroscopic proportion of the financial system is lost instantaneously.

The above mentioned model without the common noise motivates the analysis in [17] and numerical schemes for this model have been explored in [26]. A similar financial framework also provides the motivation for [23, 24]—the latest paper extending the idiosyncratic () model to more generic random drivers and replacing the constant feedback parameter with a graph of interactions for a finite number of groups. At a more heuristic level, an analogous model for the emergence of macroeconomic crises was proposed in [15], based on a PDE version of the stochastic evolution equation in Remark 1.1, albeit without addressing the possibility of blow-ups and hence not accounting for the jump component.

Concerning the presence of a common noise, more generally, we note that this has recently become a subject of great interest in the context of mean-field games—see e.g. [4, 5] for a start. In particular, this also leads to the study of so-called conditional McKean–Vlasov type problems, however, the focus is quite different.

Another important motivation for studying (MV) comes from mathematical neuroscience, where (MV) models the voltage level across a typical neuron in a large mean-field network. This application (with ) is the focus of [6, 7, 8, 10, 11], where the feedback term describes the jump in voltage level experienced when a neighbouring neuron spikes (i.e., hits a threshold, thus emitting an action potential and then being reset). The addition of a common noise () is novel and can capture the effect of some systemic random stimulus influencing all neurons simultaneously, for example due to some external influence in the environment. While such common noise mean-field models are discussed in the neuroscience literature, see e.g. [2, 22, 27], they have not been treated rigorously.

We note that, in the mathematical neuroscience literature, the focus is not so much on the McKean–Vlasov formulation (MV), but rather the corresponding deterministic or stochastic Fokker–Planck equation, where ‘’ gives the infinitesimal change in the proportion of spiking neurons over ‘’ units of time. Since neurons are reset after spiking, one works with a mass preserving version of the evolution equation from Remark 1.1, obtained by adding a source term to reintroduce the mass flowing through the origin.

Forgetting about the blow-up component in Remark 1.1, various formulations of such stochastic Fokker–Planck equations appear in the mathematical neuroscience literature (see e.g. [2, 3, 21, 27]), but so far there have been no attempts at attaching a rigorous meaning to neither the stochastic evolution equation itself nor how it emerges from a finite particle system with common noise. For further details, we refer to the aforementioned references as well as Proposition 3.7 and Remark 3.8 in Section 3.3.

Results on well-posedness

Questions of existence and uniqueness for (MV) are delicate, not least because of the possibility of blow-ups. While the series of papers [6, 7, 8] studied the deterministic Fokker–Planck equation, working with a classical notion of solution that may cease to exist in finite time, the papers [10, 11] were the first to consider the probabilistic formulation (MV) with . In particular, for , [11] showed that global solutions can be obtained as limit points of a suitable particle system, using ideas that have inspired our approach in Section 3 and which will be expanded upon there.

The present paper contributes to the literature on well-posedness by introducing a ‘relaxed’ notion of solution for (MV) with that is shown to characterize the limit points of a ‘contagious’ particle system with common noise. This provides the justification for the applications discussed above. We mention here that the ‘relaxation’ of (MV) concerns the measurability of (or ) with respect to the common Brownian motion , but further details are left to Section 3.

Prior to the first version of this paper, well-posedness results for (MV) were only available for the idiosyncratic version of the problem [10, 11, 17, 23] with uniqueness only known before the first blow-up [17, 23]. However, by ruling out blow-ups, the latter becomes global uniqueness if is small enough [10, 17]. Concerning , it has now been shown in the second version of the preprint [24] that global solutions to (MV) can also be constructed from a generalised Schauder fixed point argument, thus complementing the results in Section 3 of the present paper.

Additionally, there has been some interesting new developments on the question of uniqueness. For the case , it was shown in [20] that there is local uniqueness when restarting solutions after a blow-up, and, even more recently, a complete well-posedness theory for (MV) with was then developed in the preprint [12], giving global uniqueness under mild assumptions on the initial condition. Finally, [20] also gives global uniqueness for under a smallness condition on the feedback parameter that rules out blow-ups.

1.2 Overview of the paper

The rest of the paper is split into three sections. In Section 2, immediately below, we begin our analysis by deriving a number of results about the possibility and timing of blow-ups for solutions to (MV). The main results in this regard are collected in Theorem 2.1, which serves to illustrate the critical distinction between the idiosyncratic problem and the common noise problem. In Section 3, we proceed to formulate the ‘contagious’ particle system that motivates our analysis of (MV) and analyse its convergence. The main result is Theorem 3.2, which shows that the limit points of the empirical measures for this particle system can be characterized as ‘relaxed’ solutions of (MV) satisfying the minimality constraint (2.2). Finally, Section 4 provides some results on filtrations that are utilised in Section 3, and we also give a brief outline of the numerical scheme used to generate the simulations in Figure 1.1.

2 On the occurrence of blow-ups

As emphasised in the introduction, a solution to (MV) comes with a flow of random sub-probability measures on the positive half-line, namely , defined by

We will return to the dynamics of this flow later, but for now we simply need it for a concise characterization of the jump sizes at blow-ups, which, due to the càdlàg nature of the system, depends on the left limits , taking the form

with the convention that (corresponding to and ).

Given a sample path of undergoing a jump discontinuity at some time , we can deduce from (MV) that the jump size must agree with the loss of mass resulting from a negative shift of the system by the amount . That is, we have the constraint

| (2.1) |

almost surely. While this places a restriction on the admissible jump sizes, it is not sufficient to determine the jumps uniquely, and so it becomes necessary to have a selection principle. Therefore, we enforce the following minimality constraint, stipulating that the jump sizes should satisfy

| (2.2) |

where the equality holds almost surely (recall the conventions and ). As we prove in Proposition 3.5, this constraint amounts to only considering càdlàg solutions and always selecting the minimal jump size satisfying the requirement (2.1).

In the special case , the constraints (2.1) and (2.2) are of course deterministic, with taking the unconditional form

and we stress that they correspond precisely to the notion of a ‘physical solution’ first introduced in [10] (see [17] for a treatment closer to the present one, and see also [23] for a slightly different setup). A simple pictorial illustration of these constraints, focused on the special case , can be found in [17, Fig. 2.1]. Crucially, we mention here that, in Section 3, the solutions arising as limit points of the motivating particle system will be shown to satisfy the minimality constraint (2.2).

2.1 Idiosyncratic vis-à-vis common noise

The purpose of Section 2 is to present a clear and simple juxtaposition of the phenomenon of blow-ups for (MV) with and without the common noise. In particular, we will illustrate how the addition of a common noise can determine whether or not the model undergoes a blow-up. We stress that the methods employed are not sharp, as they are only intended to guarantee the existence of non-trivial blow-up probabilities, rather than defining precise conditions under which they occur. Even in the idiosyncratic setting, one should not expect to find a neat closed-form condition on the choice of initial law and feedback parameter in a way that determines if and when a blow-up occurs, and so we shall not pursue this here.

Nevertheless, we note that the proofs rely on constructive arguments (in Sections 2.2 and 2.3), thereby outlining specific events on which a blow-up does or does not occur for certain initial conditions. When constructing events on which a blow-up is excluded, the key ingredient will be the minimality constraint (2.2) introduced above. Conversely, in arguments about enforcing blow-ups, one of our main tools will be a variant of the moment method from [17, Thm. 1.1].

The next theorem is the main result of this section and it serves to illustrate the decisive role played by the common noise in relation to blow-ups. As in the original contribution [10] for the idiosyncratic problem (MV) with , we focus on a fixed starting point . That is, the system is started from a Dirac mass at some . In this setting, it follows from [10, Thm. 2.3 & 2.4] that, if is small enough as a function of , then (MV) with admits a unique (continuously differentiable) solution with no blow-ups on any given time interval. With the common noise, however, the situation is markedly different.

Theorem 2.1 (Blow-ups).

Consider the McKean–Vlasov problem (MV) with a fixed starting point . We have the following dichotomy for the phenomena of blow-ups, depending on the presence or absence of the common noise.

-

(i)

Idiosyncratic model: given any , has a blow-up for starting points close enough to the origin, while there are no blow-ups for starting points far enough from the origin.

-

(ii)

Common noise model: given any , blow-ups are random events with

for any starting point .

The proof of this theorem is the subject of the next two subsections, where we will shed further light on the blow-up behaviour for the idiosyncratic and common noise versions of (MV). The first part of Theorem 2.1 follows from Proposition 2.4 in Section 2.2, while the second and main part of the result is a consequence of Proposition 2.10 in Section 2.3. The dichotomy pointed out by Theorem 2.1 is illustrated in Figures 2.1 and 2.2 in Section 2.3. These figures give a simple pictorial account of how the common noise may provoke and/or prevent a blow-up, as compared to how the idiosyncratic system evolves.

Before proceeding with the analysis of blow-ups, we make the following general observation which was alluded to already in the introduction: for all strictly positive times , the flow is given by a flow of bounded densities , regardless of the nature of the initial condition . This is analogous to the situation for [17, Prop. 2.1], except of course for the randomness of the flow in the setting.

Lemma 2.2 (Existence of densities).

Suppose there is a solution to (MV). For every , the associated random sub-probability measure has a (random) density .

Proof.

Fix any and let denote the density of the Brownian motion . Omitting the absorption at the origin, and using Tonelli’s theorem to change the order of integration, we have

for any Borel set , where we have used the independence of , , and , as well as the -measurability of . Consequently,

for all Borel set , so the result follows from the Radon–Nikodym theorem. ∎

As in the above, we will always use to denote the law of the initial random variable for (MV), where it is understood that is a Borel probability measure on . Furthermore, throughout the rest of the paper, we will say that is supported on a given Borel set if assigns zero mass to the complement of .

2.2 The idiosyncratic model with

Without the common noise, the flow and the loss are deterministic. Hence the blow-ups for (MV) with are completely deterministic events. Since we know from above that each has a density, a simple observation concerning blow-ups is the following. If, for a given , we have in a right-neighbourhood of the origin, then is fixed by (2.2), and so a blow-up cannot occur at that time. In the opposite direction, we can similarly observe that if, in stead, we have in a right-neighbourhood of the origin, then a blow-up must occur at time .

Furthermore, from the proof of Lemma 2.2 above, we can see that

| (2.3) |

with interpreted as if does not have a density. Thus, referring again to , we obtain the following result as an immediate consequence of the previous proof of Lemma 2.2.

Corollary 2.3 (Initial curbs on blow-up).

For any initial condition, , no blow-up can occur in (MV) strictly after time . Furthermore, if has a density, , satisfying , then a blow-up never occurs.

By working harder, we can extend this approach to show that if the initial density is supported far enough from the boundary, then there is insufficient time for the mass to reach the boundary before the time decay in (2.3) prevents a blow-up. By exploiting this, the next result gives a linear range in , which is clearly not sharp, but it is nonetheless illustrative and useful for what follows.

Proposition 2.4 (Linear spatial bounds for blow-up).

If the initial condition is supported on then a blow-up must occur in (MV). If is supported on then a blow-up will never occur.

Proof.

If is supported on , then we have , so the first part is immediate from [17, Thm. 1.1]. For the second part, notice that, by disregarding the absorption at the origin, we obtain the upper bound

Suppose is supported on for some . Since , the previous bound gives

for every . Noting also that has maximum value of , we can thus deduce that

for all , provided . Since , taking is sufficient, and so the proof is complete. ∎

2.2.1 Transformed loss processes

A natural question, arising for example from [23], is what happens when we replace the linear loss term in (MV, ) with a general function of the loss process. This leads to the similar problem

| (2.4) |

for a given function . The particular example is the focus of [23]. To avoid mass escaping to infinity, we can restrict to bounded below—then we know that as . In particular, we note that this leads to a useful simplification of the right-hand side in Proposition 2.5 below.

While we focus on in this as paper, as in the motivating papers [10, 11, 17, 18], we note that our results extend immediately to (2.4) for any Lipschitz continuous . Also, it takes only minor adaptations (see e.g. [23, Sec. 7] for the kind of changes that are needed) to allow for functions whose Lipschitz constant explodes when such as mentioned previously or e.g. .

For a discontinuous , one would have to be more careful. In particular, a first simple observation is that if has a positive jump at , then will have a blow-up at , however, if has a negative jump, then might still be continuous.

In any case, assuming there is a solution to (2.4) for a given function , the following result presents the natural extension of [17, Thm. 1.1] to this problem.

Proposition 2.5 (Blow-up for transformed loss).

Suppose gives a solution to (2.4) for some function . If we have

at some time , where , then a blow-up must occur before or at this time .

Proof.

For a contradiction, suppose that is continuous up to and including time . Then, by stopping at the first time it reaches zero, we get

since must be continuous up to this time, by our assumption. Taking expectations, and observing that gives the law of the stopping time , we thus have

The proof is now complete by noting that is of finite variation, since it is increasing, and continuous up to and including time , by assumption, so the integral on the right-hand side can be re-written as in the statement of the result. ∎

By taking and sending in Proposition 2.5, we recover [17, Thm. 1.1]. Notice that, as soon as the integral of over is positive, then for any initial condition we can take large enough to cause a blow-up. In addition, if is chosen so that its integral over is positively infinite (for example, ), then a blow-up is guaranteed for any initial condition and any feedback parameter . Note, however, that the case from [23] has finite integral, so, in this case, Proposition 2.5 does not determine whether or not a blow-up must occur for any value of the (strictly positive) feedback parameter.

2.3 The common noise model with

For the idiosyncratic () model, the only parameters controlling blow-ups are the feedback strength, , and initial condition, . In this regard, an important novelty in the common noise model () is that there are choices of initial condition for which the realisations of the common noise determine whether a blow-up occurs or not. Furthermore, as the solution is no longer deterministic, the occurrence of a blow-up is now a random event.

In the case of a Dirac initial condition , Theorem 2.1 says that, if the support is far enough from the origin, then we do not have a blow-up in the idiosyncratic model, while there is always a non-zero probability of blow-up with common noise ().

The proof of this uses an explicit construction to show that a blow-up is forced if the sample path of is sufficiently negative so as to quickly transport the initial mass towards the boundary without loosing too much mass along the way.

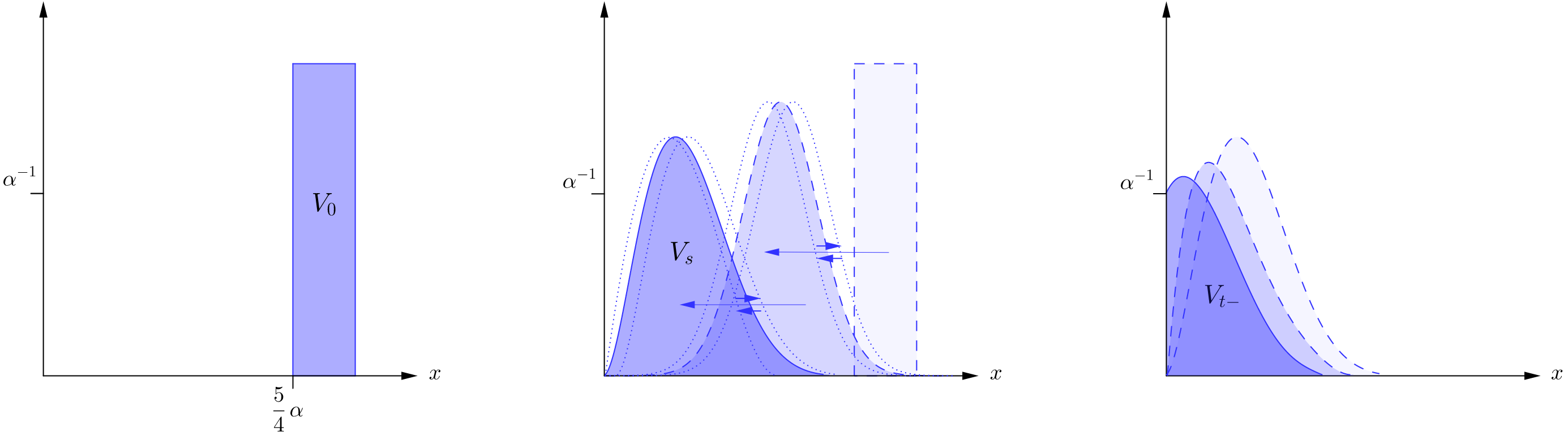

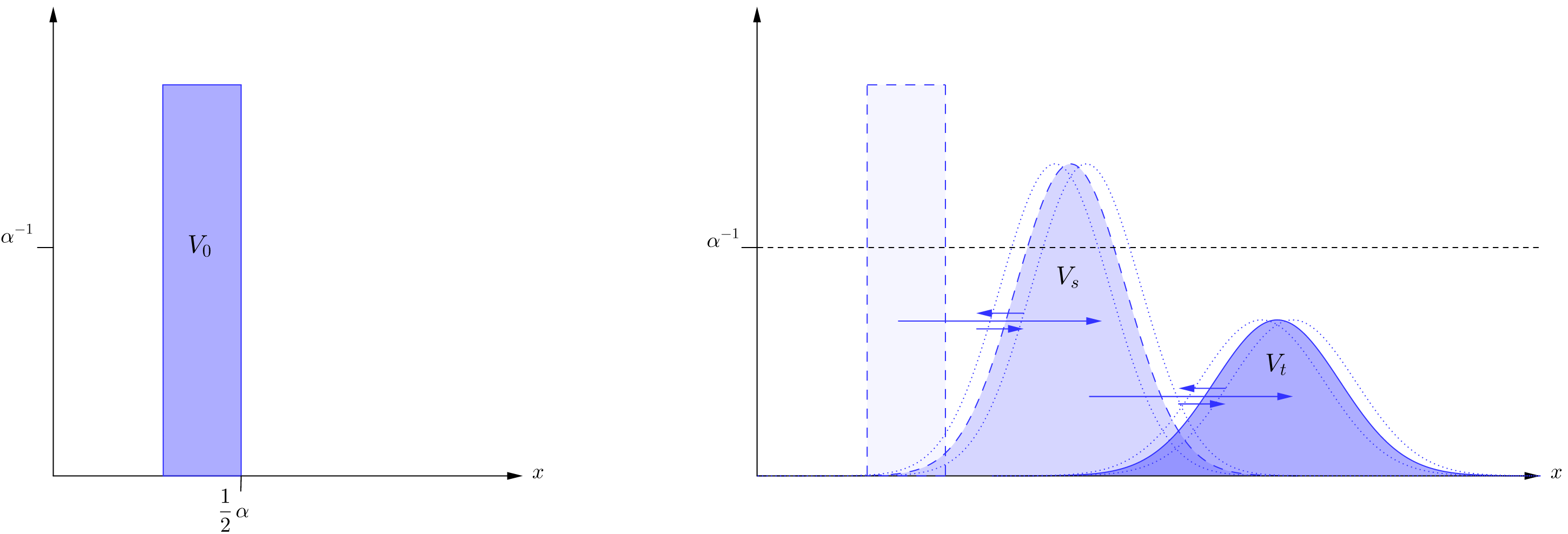

With the same amount of work, the arguments can be phrased in a slightly more general way that also applies to a uniform distribution concentrated near a point away from the origin. The latter case is well suited for illustrative purposes, and so we rely on it for Examples 2.6 and 2.7 below. Both examples are accompanied by a simplified pictorial account in Figures 2.1 and 2.2, respectively. In addition to illustrating the interplay between the common noise and blow-ups, these figures also give an intuitive idea of the mechanisms underlying the proofs of Propositions 2.9 and 2.10. However, we stress that these figures are only meant as simplified ‘cartoons’ (in particular, the axes are not in the same scale, and the shape and size of the densities are not precise).

Example 2.6 (Forcing blow-up).

Let the initial condition be a uniform distribution with density for constants and , as in the leftmost picture of Figure 2.1. For such initial conditions, Proposition 2.4 guarantees there is no blow-up in the idiosyncratic model. On the other hand, Proposition 2.10 below shows that there is a non-zero probability of blow-up in the common noise model. This happens when the common Brownian motion transports mass quickly towards the origin, thus creating a strong enough concentration of mass near zero so that a blow-up is forced to occur, essentially by comparison with [17, Thm 1.1] for the idiosyncratic model.

The previous example dealt with how the common noise can provoke a blow-up. In the next example, we consider the converse situation, illustrating how the common noise may prevent blow-ups, while starting from an initial condition for which the idiosyncratic model blows up.

Example 2.7 (Averting blow-up).

This time, we let the initial condition be a uniform distribution with density for positive constants and such that , as in the leftmost picture of Figure 2.2. Since , the idiosyncratic model must have a blow-up for such initial conditions by [17, Thm. 1.1]. In contrast, it follows from Proposition 2.9 below that the common noise model has a strictly positive probability of never blowing up. Briefly, the common noise can keep the mass of the system sufficiently away from the origin, so that the diffusive effect can do its work and eventually rule out a blow-up from ever emerging, since the mass has become too dispersed. This is illustrated in Figure 2.2.

In the arguments that follow, we are interested in bounds on the loss of mass that are uniform over a given family of realisations of the common noise. This begins with a simple comparison argument.

Lemma 2.8 (No-crossing lemma).

Let be a probability measure supported on , for some , and let be two continuous deterministic functions satisfying . Let and be solutions to

respectively, where is distributed according to . If for all and is continuous on , then for all . If is also continuous at , then for all .

Proof.

As in the statement, we have for all , where the time is given, and we assume is continuous on . Observe that if is continuous on , for some , and for all , then

| (2.5) |

In particular, the claim of the lemma follows if only we can show that for all . To this end, we let be the first time such that . By definition of a solution, we have , so the assumption gives . Combining this with the right-continuity of solutions, it follows that .

Now suppose, for a contradiction, that we have . Then is continuous on , by the assumption that it is continuous on , so we also have continuity of on . Noting that only has downwards jumps ( has only upwards jumps), we must therefore have , and this forces

But this is a contradiction, because the left-hand side is non-negative by (2.5), since is continuous on and for , by construction. This completes the proof. ∎

2.3.1 Averting blow-ups

Keeping in mind the case of a Dirac mass and the example in Figure 2.2, we now turn to a precise construction of events on which blow-ups are excluded for all feedback parameters , when starting the system from a general initial condition supported away from the origin.

Proposition 2.9 (Non-certain blow-up).

Let the initial condition be supported on , for some . Then the conditional McKean–Vlasov problem (MV) with common noise satisfies

for all feedback parameters .

Proof.

Let be as in the statement of the proposition, and fix a such that . Then define to be a solution to the idiosyncratic problem

noting that . By the right-continuity of as well as , by our notion of solution, we then have as . In particular, we can take small enough so that . Since is increasing, we have for , so an adaptation of the argument in Proposition 2.4 shows that we can take small enough such that is continuous on . Indeed, this amounts precisely to the bound (2.7) below for .

For a general , we can exploit that is independent of and , with being -measurable, and this way we obtain the bound

| (2.6) |

for any , where we have simply disregarded the absorption at the origin.

For the rest of the proof, we restrict attention to the event , where the latter is a family of paths defined by

for a positive constant to be determined later. On this event, for any given , we have for all . In order to also control the loss of mass, we stop before it exceeds , which amounts to looking at the stopping time

By the right-continuity of with , we have , and we also stress that of course inherits -measurability from .

Since is supported on , we can deduce that, on the event , the bound (2.3.1) yields

for every . By lowering if necessary, it follows that there is a constant such that

| (2.7) |

Based on the above, we now argue that cannot have a blow-up on the full interval , when restricting to the event . First of all, restricting to this event, the bound (2.7) and the minimality constraint (2.2) already ensures that is continuous on with . Now, if has a blow-up on , then there must be a realisation of and some time such that is continuous on while failing to be continuous on any right-neighbourhood with . Noting that

on the event , so the conditions of the no-crossing lemma are satisfied. Therefore, the continuity of on gives

| (2.8) |

precisely by the no-crossing lemma (Lemma 2.8), and thus the bound (2.7) now reads as

This, in turn, implies , by the minimality constraint (2.2), and, in particular, we then get from (2.8). By right-continuity, it follows from here that, for any , we have for close enough to . Thus, we can conclude that there is a bound of the form with , which continues to hold (for sufficiently close to zero) on a small enough right-neighbourhood of , only we may need to take (but of course still strictly less than one). This means that must remain continuous on for an close enough to , and so it is indeed the case that, on the event , the loss does not have a blow-up on .

Given the above, we fix a later time by setting

Since , it follows from the bound in the proof of Lemma 2.2 that

for every . Therefore, the minimality constraint (2.2) gives us that cannot have a blow-up after time . It remains to ensure that there is no blow-up on the intermediate time interval . To this end, we can consider events where the realisation of the common Brownian motion belong to a family of paths of the form

The work so far has been independent of , so we can certainly take it to be given by , where we are free to choose the constant . This choice of gives us that

On the event . Insisting also on , we can therefore deduce from (2.3.1) that

for every , for all , on the event . Taking large enough, we can in turn ensure that , for any near the origin, for all . By the minimal jump constraint (2.2), this means that cannot have a blow-up on , and hence we conclude that

as desired. This completes the proof. ∎

2.3.2 Provoking blow-ups

The next result establishes the most interesting direction of part (ii) in Theorem 2.1. Namely that, if (MV) is started from a fixed start point , then there is a strictly positive probability of blow-up for all . While the former concerns Dirac initial conditions, the statement below is phrased slightly more generally in order to also include the initial conditions considered in Examples 2.6 and 2.7 above.

Proposition 2.10 (Non-trivial blow-up).

Let the initial condition be supported on , for some , and suppose we have . In this case, the conditional McKean–Vlasov problem (MV) with common noise satisfies

for the given feedback parameter .

Proof.

The first claim, that the probability of a blow-up is strictly less than one, is a consequence of Proposition 2.9, so we only need to consider the second claim. In order to construct an event on which has a blow-up, we fix as in the statement, and we then fix a small such that . As in the proof Proposition 2.9, we write

but this time we take

where and are to be determined. Furthermore, we let be a solution to the idiosyncratic problem

where is distributed according to , which we recall is supported in by assumption. Notice that, on the event , we have

Consequently, it follows from the no-crossing result of Lemma 2.8 that either has a blow-up on or else is continuous on this interval and then on .

In the former case, the claim is immediate, so for the rest of the proof we restrict to the latter case, where we then have

Note that we are free to tune in the above. Since is right-continuous with , we have as , so we can take small enough such that . On the event , we therefore have

| (2.9) |

by the above comparison with . Moreover, as is increasing, we can always decrease , so it is no loss of generality to insist on for the remainder of the proof.

In the remaining part of the proof, we modify the moment argument from [17, Thm 1.1] to show that a blow-up must occur after time , provided the common Brownian motion stays close to its value at . First of all, we can observe that, if is continuous up to and including some time , then is also continuous there, so stopping at its first hitting time of the origin, namely , we get

| (2.10) |

for , where we have used the notation for increments. Noting that is of finite variation and that it is precisely the distribution function for the hitting time conditional on , we obtain the explicit expression

provided is continuous on , where we have also used that as , by comparison with Brownian motion. On the event we certainly have by (2.9), and of course , so taking conditional expectations in (2.10) and rearranging yields the inequality

| (2.11) |

for , on the aforementioned event, provided is continuous there.

Now fix a time , to be determined, and consider the event , where we recall the definition

We will show that cannot be continuous on for any realisation of on the event , as this would lead to a contradiction based on (2.11). To estimate the first term on the right-hand side of (2.11), notice that continuity of implies

Furthermore, we have on the event by (2.9), and a simple computation gives as is independent of . Therefore,

since we fixed . Next, we can observe that, on the event , we have and , so we get

and hence

Concerning the second term on the right-hand side of (2.11), we of course have

on the event , and thus the continuity of on would imply that the inequality (2.11) becomes

| (2.12) |

for , on the event .

It remains to utilize that we are free to tune the variable . In view of Lemma 2.8, we can bound from below on , on the given event, by an idiosyncratic problem whose loss of mass goes to one when time goes to infinity, since Brownian motion hits every level almost surely. Therefore, we can certainly take small enough and large enough in order to get a contradiction in (2.12), as soon as is continuous on for any given realisation of the common noise contained in the event . In other words, we have

as desired, and thus the proof is complete. ∎

We end this section by concluding the proof of Theorem 2.1. First, we can recall that part (i) of the theorem is an immediate consequence of Proposition 2.4 from the previous subsection. Next, we can note that, for any given , every Dirac initial condition with satisfies the conditions of the above Proposition 2.10. Indeed, we can simply take , for a small , and then we have , so part (ii) of Theorem 2.1 follows from Proposition 2.10.

3 From particles to the mean-field

In what follows we will show how solutions to a ‘relaxed’ version of (MV) emerge as the limit points of a finite-dimensional particle system with positive feedback. It is this particle system that motivates the applications described in the introduction, and hence it is a salient point that ‘relaxed’ solutions to (MV) indeed describe the large population mean-field limit.

3.1 The finite particle system

For the rest of Section 3 we shall be interested in characterizing the large population limit of the particle system

| (3.1) |

for , where is a family of independent Brownian motions, and are i.i.d. copies of a given initial condition (independent of the Brownian motions). Here the coefficients for the drift, volatility, and correlation of the diffusive dynamics are given by deterministic functions , , and , respectively, with the basic formulation (MV) corresponding to constant coefficients , , and .

Effectively, one should think of the particles in (3.1) as being absorbed when they first reach (or jump below) the origin, at which point they contribute to the current value of the loss process . However, to avoid clouding the notation unnecessarily, we define the particles globally by the dynamics in (3.1) for all times .

Some care has to be taken in specifying what is meant by in (3.1). Clearly, it only jumps when for some particle that has not already crossed the origin at an earlier time (in other words, the particle was previously unabsorbed). However, if taking means that for more previously unabsorbed particles , then these particles also jump to or below the origin at time , hence contributing further to , and so forth. That is, a cascade is initiated, which is resolved by demanding that equals the smallest such that a downward shift of the particles by results in no more than previously unabsorbed particles reaching (or crossing) the origin at time , based on the positions of the particles at ‘time ’.

The above can be formulated more succinctly as saying that we require to be the unique piecewise constant càdlàg process satisfying

| (3.2) |

where we have introduced the finite-dimensional flows of sub-probability measures

| (3.3) |

for each , which have left-limits

The condition (3.2), of course, is nothing but the discrete analogue of the physical jump condition presented in (2.2).

From here, the existence and uniqueness of the finite particle system (3.1) becomes immediate, under Assumption 3.4, as a unique strong solution can be constructed recursively on the intervals of constancy for with (3.2)-(3.3) dictating when and by how much it jumps.

We note that we have included a spatial drift with up to linear growth in space to e.g. allow for Ornstein–Uhlenbeck type dynamics, as this is of interest for the motivating financial [18] and neuroscience [2] applications. Our arguments for such a drift extend immediately to a drift also depending on the empirical mean in a Lipschitz way, but we leave this out for simplicity of presentation.

Throughout what follows, we let be the space of real-valued càdlàg paths, and we let denote the canonical process on with denoting its first hitting time of zero, that is, . In particular, we can then write

where

| (3.4) |

noting that the empirical measures, , should be understood as random probability measures on . In terms of notation, we will consistently use the boldface font (e.g. and ) for random measures, whereas the blackboard font (e.g. and its expectation operator ) is reserved for fixed background spaces.

3.2 Limit points of the particle system

Heuristically, one could hope that, along a subsequence and in a suitable topology, the pair will converge in law to some limit , where is again a Brownian motion and is the conditional law of given , for a càdlàg process satisfying (MV) with . However, the idea that , and hence also , should automatically turn out to be -measurable is asking too much of the weak limit point . Anyhow, this property can be relaxed vis-à-vis the original formulation of (MV) without altering the essential features of the problem. We define this relaxation next, noting that it is an essential part of our endeavours to recover (MV) as a large population limit of the finite system (3.1).

Definition 3.1 (Relaxed solutions).

Let the coefficient functions , , and be given along with the initial condition and feedback parameter . Then we define a relaxed solution to (MV) as a family on a probability space of choice such that

| (rMV) |

with , and , where is a Brownian motion, is a càdlàg process, and is a random probability measure on the space of càdlàg paths . By the notation , we mean the conditional law of given which indeed defines a random -measurable probability measure on .

We stress that the fixed point type constraint is a crucial part of our relaxed notion of solution, which characterizes the extra information in the conditioning and encodes the fact that , as should be required for a limit point of with . Observe also that, if the random measure is -measurable, then the above simplifies to the exact form of (MV). In the absence of -measurability, however, the independence of and constitutes the most important point, which allows (rMV) to retain all the essential aspects of (MV). In particular, this independence ensures that the results from Section 2 are equally valid for (rMV), by conditioning on the pair whenever we conditioned on . The nature of relaxed solutions and their agreement with (MV) is explored further in Section 3.3.

We now present the main result of this section, showing that solutions to (rMV) arise as limit points of the finite particle system (3.1).

Theorem 3.2 (Existence and convergence).

Suppose Assumption 3.4 below is satisfied, and let be the empirical measure (3.4) for the finite particle system (3.1). Then any subsequence of the pair has a further subsequence, which converges in law to some , where is a Brownian motion and is a random probability measure . Given this limit , there is a background space , which carries another Brownian motion and a stochastic process such that is a solution to (rMV) according to Definition 3.1. Moreover, if we define

| (3.5) |

then we have the minimality constraint

| (3.6) |

for all , which determines the jump sizes of .

As in Section 2, it is understood that and . The full list of structural conditions that we impose on (3.1) and (rMV) are collected in Assumption 3.4 immediately below. However, the proof of the theorem is postponed, as it requires several auxiliary results which form the subject of Sections 3.4 and 3.5. For now, we pause instead to explore the contents of the theorem a little further.

Note, in particular, that the requirement of right-continuity and in Definition 3.1 corresponds to not having a jump at time , so the minimality constraint (3.6) says that the initial condition should satisfy .

Remark 3.3 (Schauder fixed point approach).

While this paper focuses on convergence of the particle system, one can of course also frame (MV) as a fixed point problem. Such an approach has now been implemented in Remark 2.5 of [24], based on a Schauder fixed point argument generalised to Skorokhod’s M1 topology on . This yields a direct proof of existence for solutions to (MV) rather than (rMV). However, the results in [24] do not address a condition for the jump sizes such as the minimality constraint (3.6), which is an integral part of Theorem 3.2 (see also Proposition 3.5 below). Finally, we note in passing that the M1 topology is also key to our arguments in the subsections that follow (as in [11] for ).

We do not address uniqueness in this paper, but we reiterate here, as in the introduction, that there has been some important new developments on this front (at least in the constant coefficient case). If the law of has a density , then global uniqueness has been shown for under the smallness condition [20] and for under the general condition that does not change monotonicity infinitely often on compacts [12]. In these situations, we have full convergence in law of the particle system, and the relaxed limiting solutions (rMV) for simplify to the form (MV), as explained in [20, Thm. 2.3].

For general initial conditions, uniqueness remains an open problem when , and we note that Theorem 3.2 does not yield full propagation of chaos in the absence of such uniqueness.

Assumption 3.4 (Structural conditions).

The drift, , is assumed to be Lipschitz in space with linear growth bound . The volatility, , and the correlation, , are taken to be deterministic functions in , for some , satisfying the non-degeneracy conditions and , for some . Furthermore, we assume that , and that for all sufficiently small, for some , where is the distribution of the initial condition which takes values in .

Notice that, following a standard Grönwall argument, the moment assumption on the initial law guarantees that is bounded uniformly in , for any given . When making use of this observation in later subsections, we will simply refer to Assumption 3.4 without writing out the details.

Our next result touches on an essential aspect of Theorem 3.2 that was in fact anticipated already in Section 2, when we motivated the minimality constraint (2.2). Indeed, we can observe that (2.2) is precisely the property (3.6) enjoyed by the limiting solutions obtained in Theorem 3.2. As we pointed out in Section 2, this property amounts to picking out the smallest possible jump sizes whilst also insisting on the system being càdlàg. This claim is verified by the next result, based on an adjustment to the argument in [17, Prop. 1.2] which established the corresponding result for the idiosyncratic model. As usual, we employ the conventions and .

Proposition 3.5 (Minimality of jumps).

Proof.

We will proceed by contradiction, so suppose is a càdlàg solution for which the inequality (3.7) is violated at some time .

By following the strategy in the proof of [17, Prop. 1.2] and [17, Remark 2.6], we can always consider the restarted system, so it is no loss of generality to take with and . Thus, assuming for a contradiction that (3.7) is violated at , we can find such that

| (3.8) |

We will show that this leads to a violation of the right-continuity of at , by achieving a bound on from below as .

Compared to [17, Prop. 1.2], we must account for the common noise and the drift term in the dynamics of . To this end, we introduce the notation

Using the linear growth bound on the drift from Assumption 3.4, we then have

for all . In turn, applying Grönwall’s lemma gives

where we have used the short-hand notation

and we have furthermore used that, with this definition, we have .

Since as , we can take a -random subsequence of for which (recall that is a deterministic time-change of the Brownian motion ). In turn, we have

along that subsequence for sufficiently small. For the rest of the proof, we restrict to this (-random) subsequence. It then follows that

| (3.9) |

Clearly, the integrand on the right-hand side of (3.9) is differentiable and decreasing as a function of . Thus, returning to (3.8), we can repeat the argument from the start of the proof of [17, Prop. 1.2] to deduce that

where was fixed as part of (3.8).

Next, we can observe that is independent of , and that, conditionally on , it is thus normally distributed with mean and variance , where we have defined

Therefore, after a change of variables, we get

for along the aforementioned subsequence, with denoting the standard normal cdf. At this point the remainder of the proof is identical to that of [17, Prop. 1.2] (for each realization of the -dependent sequence ), which gives us the desired contradiction. ∎

By definition of , we can write , for all , with the jump sizes fully determined by the left limit via the minimality constraint (3.6). Hence it is natural to consider as the leanest way of writing the solution, where is viewed as a measure-valued stochastic process. In line with this point of view, we have the following result, whose proof is postponed to Section 4.

Proposition 3.6 (Filtration).

Define as the stochastic process whose marginals are the random measures given by (3.5) in Theorem 3.2, where is the space of measures on equipped with its Borel -algebra under the total variation norm. Then there is a filtration , forming a filtered space , for which is adapted and is a 2d Brownian motion.

In the formulation of Definition 3.1 and Theorem 3.2 it is not necessary to refer to a filtration, but the previous proposition emphasises that one can indeed work with a filtration to which and are adapted without affecting the Brownian dynamics. This observation leads us naturally to the next subsection, where we derive a stochastic evolution equation for the flow of the adapted stochastic process .

3.3 Stochastic evolution equation

Following on from the above, we can think of the McKean–Vlasov system (rMV) in terms of the adapted stochastic process . However, instead of working with the full filtration from Proposition 3.6, we now wish to consider the subfiltration generated only by the common noise and the stochastic process itself. The explicit construction of this is given in Section 4 (along with the proof of Proposition 3.6), verifying that is indeed a standard Brownian motion in and that this subfiltration is independent of .

The next result shows that satisfies a generalized stochastic evolution equation driven by the common noise . While we work with the relaxed formulation (rMV), we stress that identical arguments reveal that (MV) leads to the very same evolution equation. The only difference is whether or not the solution is automatically adapted to the driving noise , which provides another point of view on the distinction between (rMV) and (MV). Aside from this, our main aim here is to make more clear the connection between the McKean–Vlasov formalism of the present paper and the focus on Fokker–Planck equations in the related PDE and mathematical neuroscience literature, as further discussed in Remark 3.8 below.

Proposition 3.7 (Stochastic evolution equation).

Before turning to the proof, we take a moment to interpret the equation (3.10). Most importantly, we know that is of finite variation, so it is clear that all the terms in (3.10) make sense. Now suppose there is a blow-up at some time . Then the dynamics in (3.10) yield

From Lemma 2.2, we know that has a density , for all , so we deduce that a blow-up can be described as the system restarting from the shifted density

Furthermore, by performing a formal integration by parts, we see that (3.10) gives a generalized notion of solution for the evolution equation presented in Remark 1.1 phrased for the flow of the densities . Finally, we recall that Figure 1.1 shows two heat plots illustrating how these densities evolve in time, with the right-hand plot displaying a blow-up given by a shift of the density as described above.

Remark 3.8 (Integrate-and-fire models).

In the mathematical neuroscience literature, stochastic Fokker–Planck equations analogous to (3.10) appear e.g. in [2, Eqn. (32)], [3, Eqn. (3.24)], [21, Eqn. (2.29)], and [27, Eqn. (4)] as ‘integrate-and-fire’ models for networks of electrically coupled excitatory neurons. However, there is no discussion of a jump component in these works, while Theorem 2.1 shows that blow-ups are an inevitable part of the stochastic evolution starting from a Dirac mass. Moreover, it is heuristically assumed that has a derivative, which is then referred to as the ‘firing rate’ and is identified with the flux across the boundary. Since is increasing, it is indeed differentiable almost everywhere, and the equation (3.10) formally gives the flux condition

in line with [21, Eqn. (2.6)]. Nevertheless, for , one can no longer expect to be absolutely continuous even in between blow-ups, nor will be well-defined (due to the roughness of ). In this respect, it is clear that the McKean–Vlasov formulation is better suited for working with blow-ups, and it entirely avoids the aforementioned regularity issues.

Proof of Proposition 3.7.

Let be defined by (3.5), for a solution to (rMV) given by Theorem 3.2, and consider on the filtered space from Proposition 3.6. By construction, . Since is of finite variation, the sum of jumps is convergent, and hence the continuous part is given by the well-defined expression

Moreover, this means that integrals against both and are well-defined in the Lebesgue–Stieltjes sense. As concerns the final condition on the jump sizes , this is just the minimality constraint (3.6), which is satisfied by Theorem 3.2. In order to derive (3.10), we let be the corresponding filtration generated by and , as detailed in Section 4. The adaptedness of to this filtration implies that and can be written as

for , with . As explained in Section 4, is a subfiltration of the filtration from Proposition 3.6, remains a Brownian motion with respect to this filtration, and, crucially, the filtration is independent of the other Brownian motion . In view of the above expression for , we see that its action on test functions is given by

for . Applying Itô’s formula for general (càdlàg) semimartingales to , we obtain

| (3.11) |

for , for all , where we have used that is of finite variation. From here, we note that

by definition of , so equals the conditional expectation given of the right-hand side of (3.3). Since the filtration is independent of , the integral against is killed under this operation of taking conditional expectation, whereas the -adaptedness of and means that this operation commutes with the integrals against these processes (see e.g. [16, Lemma 8.9]). Therefore, by the previous two observations and Fubini’s theorem, we can deduce (3.10) from (3.3). ∎

In addition to the formulation (3.10) being weak in the sense of generalized functions, we stress that the solution given by the flow for (rMV) is also probabilistically weak in the sense that the filtration is allowed to be strictly larger than that generated by the driving noise alone. For a similar situation, see also the classical paper [9]. In other words, the fact that the loss process in (rMV) is conditional on , rather than just , simply amounts to the corresponding solution of the stochastic evolution equation (3.10) not necessarily being adapted to the driving noise .

3.4 Preliminary estimates

In this subsection we establish several important estimates concerning the behaviour of , , and a tagged particle as . These estimates are then used to establish suitable tightness and continuity results in the next subsection. Throughout both subsections, and indeed for the remainder of the paper, we shall always be working on the premise that Assumption 3.4 is satisfied.

Due to our particular setup and the choice of topology in Section 3.2 below, the key prerequisite for tightness is sufficient control over the loss process near the initial time . To achieve this, we need to exploit some control on the initial condition near the origin. The assumption is by no means optimal, but it is already quite general (for example, for , [11, 23] assumes is supported away from the boundary) and it allows for an intuitive argument to control the loss of mass. The point of the constant is that we can utilise . Moreover, we rely on the fact that is bounded away from , as we need to single out the contribution of the common noise and utilise the averaging of the independent Brownian motions in a law of large numbers argument.

Proposition 3.9 (Initial control of the loss).

Proof.

For clarity, we split the proof into three concise steps.

Step 1. Given from Assumption 3.4, we fix two constants and such that . Setting , we then have

for each , where we have defined the initial empirical measures

Observe that, for all sufficiently small, we must have

by the law of large numbers and Assumption 3.4. Note also that if and only if . Thus, letting denote the random index set

for our , we get the estimate

Step 2. Next we define

Then we claim that, for every with , we have

| (3.12) |

Suppose, for a contradiction, that but . Then

so even if all these particles are killed in the interval , their total contribution to is less than . In particular, this means that, at time , the largest possible downward jump for the remaining particles (indexed by ) is . Notice, however, that these remaining particles all satisfy and

so we must have . Consequently, a translation by cannot cause any of them to drop below the origin and hence , so , which certainly implies . This yields the desired contradiction.

Step 3. Note that for . Therefore, using the linear growth assumption on the drift, we deduce that implies

| (3.13) |

where

From here, we split the analysis on the intersection of the events

and their complements. It is easily verified that both complements occur with probability as , uniformly in . On the intersection of the two events, it follows from the previous observation (3.13) that

for all . Hence we can conclude from the final estimate in Step 1 and the claim (3.12) in Step 2 that

as and , where the terms in are uniform in . Recall that . Since is bounded away from (by Assumption 3.4), we can perform a time-change in each , and then the law of large numbers yields

as , for some , where is the standard normal cdf. Noting that evaluated at the given point is of order , the indicator eventually becomes zero as and thus the proof is complete. ∎

The minimality constraint (2.2) will be recovered from the following lemma, together with Proposition 3.5. The proof follows by essentially the same reasoning as in Proposition 5.3 of [11], but we provide the full details for completeness. The main point is that, unlike the previous lemma, there is no need to isolate the effects of the common and idiosyncratic noise.

Lemma 3.10.

Fix any . There is a constant such that, for every sufficiently small, we have

whenever .

Proof.

Fixing and , we note that equals the number of particles that are absorbed in the interval . Let

for , and define the events

for a given . Then it must be the case that

| (3.14) |

Now fix an arbitrary and set

This way, (3.14) applies to and we have as well as . Introducing the additional events

for , it follows that, on each event , we have , and hence

Consequently,

Defining the event , we deduce that, on ,

Since we are working with , we have , so we can finally conclude that

| (3.15) |

for our arbitrary choice of . Thus, it only remains to observe that there exists a constant , independent of , such that . To see this, we can apply Markov’s inequality twice, the Cauchy–Schwarz inequality, and the Burkholder–Davis–Gundy inequality (to ) in order to find that

Recalling (3.15) and taking finishes the proof. ∎

Finally, for reasons of continuity, we will need the following lemma, which is conveniently phrased at the level of a tagged particle. It captures the simple, yet essential, fact that the Brownian drivers cause each particle to dip strictly below any level immediately after hitting it.

Lemma 3.11.

Let be given by (3.1). For any and , we have

Proof.

Since can only cause the particles to jump down, we can simply neglect it in the dynamics. Using also the linear growth bound on the drift from Assumption 3.4, we can therefore deduce that probability in question is controlled by

| (3.16) |

for any given , where we have set

Since has the law of a time-changed Brownian motion, the first term in (3.16) is of order as , uniformly in , for any fixed . Furthermore, sending , the second term in (3.16) vanishes uniformly in , and hence the result follows. ∎

3.5 Compactness, Continuity, and Convergence

To establish the convergence of the finite particle system, we follow the ideas of [11]. In particular, we extend the particles from (3.1) to , for a fixed , by adding purely Brownian noise on . This amounts to replacing the empirical measures by

| (3.17) |

For simplicity of notation, we will drop the ‘’ and simply write and , with the understanding that is given by when we are working on the full interval . Notice that this construction automatically extends Proposition 3.9 to hold at the endpoint , and the choice of Brownian noise on ensures the validity of Lemma 3.11 with in place of (of course, we are only actually interested in the dynamics of the system up to time ).

As in [11, Sec. 4.1], we endow with Skorokhod’s M1 topology because it will allow us to circumvent irregularities in the loss, , by virtue of its monotonicity. For properties of this topology we will be referring to [19, 28] (in [28] it is called the strong M1 topology and denoted ). Importantly, these properties rely on the members of being left-continuous at the terminal time, which is the reason for the continuous extension of the particle system to . Furthermore, we emphasise that is a Polish space [28, Thm. 12.8.1] and that its Borel sigma algebra is generated by the marginal projections [28, Thm. 11.5.2].

Similarly to the analysis in [11, Lemmas 5.4 and 5.5], once we have a result such as Proposition 3.9 at both endpoints and , the tightness of the empirical measures becomes an easy consequence of the properties of the M1 topology (see Proposition 3.12). From Prokhorov’s theorem [1, Thm. 5.1], we thus obtain a weakly convergent subsequence of the pair , and the goal is then to relate the resulting limit point to a solution of (rMV).

Before seeking to characterize the limit points , our first task is to ensure that converges to whenever converges . This is achieved through a continuity result (namely Lemma 3.13), which is an analogue of [11, Lemma 5.6, Prop. 5.8, Lemma 5.9], and its proof follows by similar arguments after observing that it suffices to rely on Lemma 3.11.

Finally, we need to characterize as the conditional law of a process satisfying the desired conditional McKean–Vlasov equation such that is independent of the idiosyncratic Brownian motion (which is constructed as part of the solution). For this part, we rely on a martingale argument (Lemma 3.11 and Proposition 3.12) which—although close in spirit—differs from the approach in [11] and is useful for dealing with the common noise. Compared to [11], another advantage of this argument is that it is not sensitive to the specific form of the volatility, , whereas the approach in [11] is tailored to a constant volatility. Aside from our approach to the independence result for and in Lemma 3.13, all our arguments extend to a bounded and non-degenerate Lipschitz continuous , so without the common noise we easily obtain such a generalization of the results in [11], but we leave out the details of this. Instead we push ahead and implement the plan outlined above, starting with the tightness of the empirical measures in the M1 topology.

Proposition 3.12 (Tightness of the empirical measures).

Let denote the topology of weak convergence on induced by the M1 topology on . Then the empirical measures are tight on under Assumption 3.4.

Proof.

Since is a Polish space, so is . Therefore, by a classical result [25, Ch.I, Prop. 2.2], it suffices to verify that is tight on . Let

Following [19, Sec. 4], we can deduce the tightness of by showing that

| (3.18) |

for all , and , along with

| (3.19) |

for every . For the first condition, observe that

where is given by

Since is increasing, the final term on the right-hand side is zero and hence (3.18) follows easily from Markov’s inequality by controlling the increments of . Finally, (3.19) holds by virtue of Proposition 3.9 and the fact that it also applies at the artificial endpoint , as remarked above. ∎

Recall that each is a random probability measure on , and that , where is the first hitting time of zero for the canonical process on . That is, written as a random variable on , we have

The next lemma provides a continuity result for with respect to limit points of . It will play a central role in our further weak convergence analysis.

Lemma 3.13 (Continuity result for the loss).

Suppose converges weakly to on and let . At -a.e. in , the mapping is continuous with respect to , for all , where is the set of continuity points of .

Proof.

First of all, we claim that, for any , we have

| (3.20) |

To see this, consider the set of times

which is co-countable in , since each realization of is a probability measure on . For every , we can then deduce that

| (3.21) |

Note that, if necessary, we can always replace by a smaller value such that , so the infimum in (3.21) is continuous as a mapping from to for almost all realizations of (see e.g. [28, Thm. 12.4.1] and [28, Thm. 13.4.1], as also utilised below).

By Lemma 3.11, the right-hand side of (3.21) vanishes in the limit, and hence the claim (3.20) is indeed true, by (3.21) and Tonelli’s theorem. It follows that almost every realization of is supported on a subset of paths with satisfying that, for almost every , we have for any .

Consider now a convergent sequence of probability measures with in as , where the limit is supported on the aforementioned set of paths, noting that the collection of such probability measures has full measure under .

Applying Skorokhod’s representation theorem (see e.g. [1, Thm. 6.7]), there are càdlàg processes and (defined on the same background space) such that converges almost surely to in with

By [28, Thm. 12.4.1], we have almost surely, as , so we immediately deduce from dominated convergence that .

For , more work is needed. Let be a set of full probability on which in the M1 topology. Then, by [28, Thm. 13.4.1], it holds for each that there is a set of times of full Lebesgue measure in such that as for every . Moreover, by our assumption on the support of , we can assume that the event and each associated set of times are such that, for all , we have , for any , for all .

Since for and , it is immediate that, for each , we have

for all , except possibly the set of times for which . However, recalling the properties of from above (due to the support of ), the latter set can at most be a singleton. Indeed, if at some time , then the path would dip strictly below the origin immediately after time .

In view of the last observation, we can conclude that, for each , we must have

for almost every . Therefore, dominated convergence yields the almost sure convergence

In turn, after taking expectations and using Tonelli, another application of dominated convergence gives

as . Now let and consider the truncation of given by

for and . Then for and is automatically relatively compact in the M1 topology [28, Thm. 12.12.2], so we can pass to a convergent subsequence . By [28, Thm. 12.4.1], converges pointwise to , as , on the co-countable set of continuity points for . In particular, dominated convergence yields

as Using the right-continuity, we thus deduce that everywhere on , and, consequently, we must have as for every . Sending , and noting that we would reach the same conclusion for any subsequence, we can finally conclude that as for all . This completes the proof. ∎

Using the tightness of from Proposition 3.12, we can fix a limit point of on . From now on, we shall work with this particular limit point (keeping in mind that the arguments apply to any limit point) and, despite having passed to a subsequence, we shall simply write . For concreteness, we define and introduce the random variables and on the background space . Note that the joint law of is with . Given this, we define along with the co-countable set of times

| (3.22) |

By Proposition 3.9 and the proof of Proposition 3.12, we knew from the outset that is tight in on . By Lemma 3.13 and the continuous mapping theorem [1, Thm. 2.7], we can deduce that the finite dimensional distributions of its limit (along our fixed subsequence) agree with those of , and hence we identify as the limit. Of course, we are actually interested in the dynamics on , so we note that we also have convergence at the process level in on , for any , since the restriction is continuous so long as is -almost surely a continuity point of .

We now proceed to derive some further properties of the limiting law , which will ultimately enable us to construct a probability space that supports a solution to (rMV). First of all, we define the map by

| (3.23) |

Fix an arbitrary choice of times with and , for as defined in (3.22), and let be given by

| (3.24) |

for arbitrary . Based on this, we define the functionals

As an application of Lemma 3.13, we obtain the following continuity result.

Lemma 3.14 (Functional continuity).

For -almost every , we have , and converging to , and whenever in along a sequence for which is bounded uniformly in , for some , at any .

Proof.

By definition of , it holds for -almost every that and for all . Appealing to Lemma 3.13, we can thus restrict to a set of ’s with probability one under such that converges to for and . Fix any one of these ’s and suppose in with satisfying the above integrability assumption. We start by showing that . Invoking Skorokhod’s representation theorem [1, Thm. 6.7], we can write

where almost surely in with , , and for . By standard properties of M1 convergence [28, Thm. 12.4.1], we have pointwise convergence at the continuity points of and, in particular, for almost every . As is a convergent and hence bounded sequence, we deduce from the continuity of and its linear growth bound that, almost surely,

| (3.25) |

by dominated convergence. In turn, we conclude that converges almost surely to in . It remains to observe that is uniformly integrable, since

and equals , which is uniformly bounded for some , by assumption. Hence the convergence of to follows from Vitali’s convergence theorem. The proof is analogous for and , using the boundedness assumption for . ∎

Define a new background space equipped with its Borel sigma algebra and the probability measure given by

| (3.26) |

For simplicity of presentation, we shall not distinguish notationally between random variables defined on and their canonical extensions to .

Proposition 3.15.

Proof.

Recall that , where is the law of . Using Skorokhod’s representation theorem, we can find an almost surely convergent sequence in with

Notice that we simply have

for any given power . This converges with probability one to a functional of the given , where is bounded in terms of its argument, e.g. by the Birkhoff–Khinchin ergodic theorem. Since the laws of and agree, for each , we deduce that converges to zero in probability, and using also that almost surely, with bounded in terms of , we can thus find a subsequence for which is bounded in with probability one (the bound being random). After passing to this subsequence, satisfies the assumptions of Lemma 3.14 with probability one, so the functional continuity in Lemma 3.14 gives that converges in law to along a subsequence (still indexed by ). Analogous arguments apply to and . Next, we can observe that, for all ,

Furthermore, is clearly uniformly bounded in , for any given , so we have uniform integrability. Since converges weakly to , as we argued above, the uniform integrability gives convergence of the means [1, Thm. 3.5] and so it holds by construction of that

By definition of we can thus deduce that is indeed a martingale under . For the pathwise continuity of , note that

where is a standard Brownian motion and the last equality follows from Burkholder–Davis–Gundy. By Kolmogorov’s continuity criterion [13, Chp. 3, Thm. 8.8], we conclude that has a continuous version. The proof is similar for the two other processes, using the convergence in law (along a subsequence) of to and of to , respectively. ∎

Based on the previous proposition, we can now finalise the proof of Theorem 3.2.

Proof of Theorem 3.2.

Fix the probability space as introduced in (3.26) and recall that this includes fixing a limit point of . Now define a càdlàg process on by . Then it holds by construction of that

where we recall that is the joint law of . Consequently, we have

as desired. Next, Proposition 3.15 gives that

is a continuous martingale with

By Lévy’s characterisation theorem, we deduce that there exists a Brownian motion, , that is independent of and for which

By the law of large numbers and continuity of the projection , one readily verifies that is distributed according to under . However, we need Lemma 3.16 below to ensure that and . By virtue of this lemma, we conclude that is a solution to (rMV).

It remains to verify that the limit point of really does become independent of the idiosyncratic Brownian motion in the large population limit.

Lemma 3.16.

In the proof of Theorem 3.2, we have mutual independence of , , and under .

Proof.

By Assumption 3.4, is in for some . Hence the map

makes sense as a Young integral for any Brownian path [14, Thm. 6.8] and it agrees almost surely with the corresponding Itô integral against under . Moreover, if a sequence in converges uniformly to , then the pathwise integrals also converge [14, Prop. 6.11-6.12].

Given an arbitrary bounded continuous function , let

where is defined as in (3.24).Using the above observations on Young integrals, by analogy with Lemma 3.14 we then get where

whenever , for -almost every , provided satisfies the integrability assumption of Lemma 3.14 and provided is a sequence of Brownian paths. By the same reasoning as in the proof of Proposition 3.15, a Skorokhod representation argument gives that it suffices to only have continuity of along such sequences, in order for us conclude that converges in law to .

Next, we define the process

By definition, we then have

It is immediate that is uniformly integrable, so the convergence in law of to , as established above, yields convergence of the means. Hence we get

| (3.28) |

where we have used that

as , by the properties of the ’s and the definition of . Indeed, since the ’s are independent Brownian motions, and since they are independent of the initial conditions, the definition of and the tower law yield

for all , which kills the cross terms when writing out the expression for .

From (3.28) and the definition of , we can conclude that, for -a.e. , the process is a martingale under conditional on the random variable .

A similar argument, this time for

shows that the quadratic variation of is conditionally on . Therefore, as in the proof of Theorem 3.2, Levy’s characterisation theorem allows us to deduce that, for -a.e. , the process is a time-changed Brownian motion under conditional on . Furthermore, by the strong law of large numbers, one easily sees that is distributed according to under , and so is under . In particular, we can thus deduce that

Finally, we can observe that is given as the uniform limit in probability (under ) of Riemann sums of . By the above result, we have that , , and any one of these finite sums are mutually independent under , so the same is true for in the limit. This finishes the proof. ∎

4 Filtrations and a remark on numerics

This final section is concerned mainly with the construction of the filtrations discussed at the start of Section 3. First, we prove Proposition 3.6 concerning the overall filtration , and we then derive verify the properties of the subfiltration used in Section 3.3 above. Next, we dedicate Section 4.2 to a brief outline of the numerical scheme used to generate the simulations presented in Figure 1.1 in the introduction.

4.1 Construction of filtrations and their properties

As in the proof of Theorem 3.2 above, we continue to work with the background space from (3.26), and the co-countable set of times from (3.22), for a fixed limit point . Associated to this limit point, we have the absorbing marginal flow

where, as in the previous subsections, denotes the canonical process on and is its first hitting time of zero.

Recall that with its product Borel -algebra . Recall also that and , and note that . Finally, we can observe that, by virtue of these processes satisfying (rMV), will be adapted to any filtration that makes , , and adapted.

Let us begin by constructing the desired filtration for just and . As formulated in Proposition 3.6, we want each marginal to be measurable as an -valued random variable, where the Borel-sigma algebra for comes from the duality with (a closed subspace of) the bounded continuous functions in the uniform topology. Therefore, we will work with the filtration which, at time , is generated by the projections and for all and all . That is, we define

The critical point is now to ensure that remains a Brownian motion in this filtration. The next lemma will allow us to deduce just that.

Proposition 4.1 (Convergence of the absorbing marginal flow).

Proof.

Fix an arbitrary and any . We can then observe that

and likewise for . Noting that with , we therefore have the decomposition

and, again, the same is true for the limit . Hence the proposition will follow from the continuous mapping theorem if we can show that, given any , for -almost every ,

| (4.1) |

whenever in . Since , we have for -almost every , so the claim is true for the second part of (4.1) by Lemma 3.13.

Noting that also implies for -almost every , Skorokhod’s representation theorem allows us to rewrite the first part of (4.1) as whenever a.s. in with .

Since is almost surely a continuity point of , there is an event of probability one, for which and , by [28, Thms. 12.4.1 & 13.4.1]. On the event , we eventually have , which converges to . Similarly, on the event , we eventually have , which agrees with . For the remaining event , it follows as in the proof of Theorem 3.13 that, up to a null set, and hence . In principle, may oscillate between the values and , but the latter converges to . Combining the above, we have almost surely, so is indeed the limit of , by dominated convergence. ∎

Let be an arbitrary bounded continuous function . Fixing any and , the previous proposition gives that

| (4.2) |

Here the second equality follows from the simple observation that is independent of , since the finite particle system has a unique strong solution with independent of . We deduce from (4.1) that the future increments of are independent of and so remains a Brownian motion in this filtration. Furthermore, the filtration is independent of , since both and are independent of , as ensured by Lemma 3.16.

Finally, we need a larger filtration for which the full solution is adapted. This is achieved by also including the pre-images of the projections , and we therefore define