Optimal Exploitation of a Resource

with Stochastic Population Dynamics

and Delayed Renewal

Abstract

In this work, we study the optimization problem of a renewable resource in finite time. The resource is assumed to evolve according to a logistic stochastic differential equation. The manager may harvest partially the resource at any time and sell it at a stochastic market price. She may equally decide to renew part of the resource but uniquely at deterministic times. However, we realistically assume that there is a delay in the renewing order. By using the dynamic programming theory, we may obtain the PDE characterization of our value function. To complete our study, we give an algorithm to compute the value function and optimal strategy. Some numerical illustrations will be equally provided.

Key words : impulse control, renewable resource, optimal harvesting, execution delay, viscosity solutions, states constraints.

MSC Classification (2010) : 93E20, 62L15, 49L20, 49L25, 92D25

1 Introduction

The management of renewable resources is fundamental for the survival and growth of the human population. An excessive exploitation of such resources may lead to their extinction and may therefore affect the economies of depending populations with, for instance, high increases of prices and higher uncertainty on the future. The typical examples are fishery [8, 14, 17] or forest management [3, 9]. Most early studies in fishery or forest management were mainly focusing on identifying the optimal harvesting policy. In forest economics literature, it may be illustrated by the well-known “tree-cutting” problem. The most basic “tree-cutting” problem is about identifying the optimal time to harvest a given forest. Studies extending this initial tree-cutting problem have been carried by many authors. We may, for instance, refer to [9] and [20], where the authors investigate both single and ongoing rotation problems under stochastic prices and forest’s age or size. Rotation problem means once all the trees are harvested, plantation takes place and planted trees may grow up to the next harvest. In terms of mathematical formulation, rotation problem may be reduced to an iterative optimal stopping problem. In [16], the authors go a step further by studying optimal replanting strategy. To be more precise, they analyze optimal tree replanting on an area of recently harvested forest land. However, the attempt to incorporate replanting policy in the study of tree-cutting problem remains relatively very few, especially when delay has to be taken into account. Indeed, the renewed resources need some delay to become available for harvesting. There is also an uncertainty on the renewed quantities. In other words, the resource obtained after a renewing decision may differ from the expected one due to some losses. To our knowledge, these above aspects are not taken into account in the existing literature on renewable resources management. The aim of this paper is precisely to provide a more realistic model in the study of optimal exploitation problems of renewable resources by taking into account all the above features.

We suppose that the resource population evolves according to a stochastic logistic diffusion model. Such a logistic dynamics is classic in the modelling of populations evolution. The stochastic aspect allows us to take into account the uncertainties of the evolution. Since the interventions of the manager are not continuous in practice, we consider a stochastic impulse control problem on the resource population. We suppose that the operator has the ability to act on the resource population through two types of interventions. First, the manager may decide to harvest the resource and sell the harvested resource at a given exogenous market price. The second kind of intervention consists in renewing the resource. Due to physical or biological constraints, the effect of renewing orders may have some delay, i.e. a lag between the times at which renewing decisions are taken and the time at which renewed quantities appear in the global inventory of the available resources. Renewing or harvesting orders are assumed to carry both fixed and proportional costs.

From a mathematical point of view, control problems with delay have been studied in [6] and [19], where all interventions are delayed. Our model may be considered as more general since some interventions are delayed while some others are not. Another novelty of our model is the state constraints. Indeed, the level of owned resource is a physical quantity, and hence cannot be negative. Control problems under state constraints, but without delay, have been studied in the literature, see for instance [18] for the study of optimal portfolio management under liquidity constraints. To deal with such problems, the usual approach is to consider the notion of constrained viscosity solutions introduced by Soner in [23, 24]. This definition means that the value function associated to the constrained problem is a viscosity solution in the interior of the domain and only a semi-solution on the boundary. In particular, the uniqueness of the viscosity solution is usually obtained only on the interior of the domain.

In our case, we are able to characterize the behavior of the value function on the boundary by deriving the PDE satisfied on the frontier of the constrained domain. We therefore get the uniqueness property of the value function on the whole closure of the constrained domain. As a by product, we obtain the continuity of the value function on the closure of the domain (except at renewing dates), which improves the existing literature where this property is obtained only on the interior of the domain, see for instance [18].

To complete our study, we provide an algorithm to compute the value function and an associated strategy that is expected to be optimal and apply this algorithm on a specific example.

The rest of the paper is organized as follows. In Section 2, we describe the model and the associated impulse control problem. In Section 3, we give a characterization of the value function as the unique viscosity solution to a PDE in the class of functions satisfying a given growth condition. In Section 4, we provide an algorithm to compute the value function and an optimal strategy. Finally Section 5 is devoted to the proof of the main results.

2 Problem formulation

2.1 The control problem

Let be a complete probability space, equipped with two mutually independent one-dimensional standard Brownian motions and . We denote by the right-continuous and complete filtration generated by and .

We consider a manager who owns a field of some given resource, which may be exploited up to a finite horizon time . The aim of the manager is to manage optimally this resource in order to maximize the expected terminal wealth which may be extracted.

In resource management, the manager may decide to either harvest part of the resource or renew it. Resource renewal may be done only at discrete times with , where . We consider an impulse control strategy where

-

•

, , is an -measurable random variable valued in a compact set , with being a positive constant, and corresponds to the maximal quantity of resource that the manager can renew,

-

•

a nondecreasing finite or infinite sequence of -stopping times representing the harvest times before ,

-

•

, , an -measurable random variable, valued in , corresponding to the harvested quantity of resource at time .

We assume the quantity of resource renewed at time cannot be harvested before time for any where with a nonnegative integer. We suppose that for a given quantity of resource renewed at time , the manager may get an additional harvestable resource at time , with being a function satisfying the following assumption.

(H) is a nondecreasing and Lipschitz continuous function: there exists a positive constant such that

for all .

For a given strategy , we denote by the associated size of resource which is available for harvesting at time . When no intervention of the manager occurs, the evolution of the process is assumed to follow the below logistic stochastic differential equation

| (2.1) |

where , and are three positive constants. Since at each time , the quantity is harvested we have

Moreover, we suppose that there is a natural renewal of the resource at each time of a deterministic quantity . Since the renewed quantity at time only appears in the total resource at time and increases this one of , we have

for , and

for .

The process is then given by

| (2.2) | |||||

We assume that the price by unit of the resource is governed by the following stochastic differential equation

| (2.3) |

with and two positive constants.

We also define the cost at time to renew a unit of the resource. We suppose that it follows the below stochastic differential equation

| (2.4) |

where and are two positive constants.

For a given strategy , there are several costs that the manager has to face.

-

•

At each time , the manager has to pay a cost to harvest the quantity , where and are two positive constants. As such, by selling the harvested quantity at price , she may get at time .

-

•

To renew quantity of resource at time , the manager has to pay , where is a positive constant.

Given a control and an initial wealth , the wealth process may be expressed as follows

We define the set of admissible controls as the set of strategies such that

| and | (2.5) |

where denotes the negative part. We note that for , the set is nonempty as it contains the strategy with no intervention.

We denote by the set . We define the liquidation function by

From condition (2.5), the expectation is well defined for any . We can therefore consider the objective of the manager which consists in computing the optimal value

| (2.6) |

and finding a strategy such that

| (2.7) |

2.2 Value functions with pending orders

In order to provide an analytic characterization of the value function defined by the control problem (2.6), we need to extend the definition of this control problem to general initial conditions. Moreover, since the renewing decisions are delayed, we have to take into account the possible pending orders.

Given an impulse control , we notice that the state of the system is not only defined by its current state value at time but also by the quantity at time of the resource that has been renewed between and . We therefore introduce the following definitions and notations. For any , we denote by the number of possible renewing dates before

and by the set of renewing resource times and the associated quantities between and

| (2.8) |

with the convention that if .

For any and , we denote by the set of strategies which take into account the pending renewing decisions taken between and

For , and , we denote by the quadruple of processes defined by

| (2.9) | |||||

| (2.10) | |||||

| (2.11) | |||||

| (2.12) |

for . We denote by the set of strategies such that

| and | (2.13) |

We then consider for , , the following benefit criterion

which is well defined under conditions (2.13). We define the corresponding value function by

where is the definition domain of defined by

For simplicity, we also introduce the operators , and given by

for all and . The operator corresponds to the new position of the state process after a resource consumption decision: if the manager harvests at time , then the state process is

and and correspond to the new position of the state process after a renewal decision: if the manager renews at times , then the state process is given by

We first give a new expression of the value function . To this end, we introduce the set

Proposition 2.1.

The value function can be expressed as follows

| (2.14) |

Proof. Fix with and denote by the right hand side of (2.14).

We first notice that . Indeed, for , we have

Since follows the dynamics (2.12), we have and we get . We therefore deduce that

We turn to the reverse inequality. Fix and define the associated strategy by

where the sequence is defined by

is obtained from by keeping only harvesting orders such that .

3 PDE characterization

3.1 Boundary condition and dynamic programming principle

We first provide a boundary condition for the value function associated to the optimal management of renewable resource.

Proposition 3.2.

The value function satisfies the following growth condition: there exists a constant such that

| (3.15) |

for all , , and .

The proof of this proposition is postponed to Section 5.1.

With this bound, we are able to state the dynamic programming relation on the value function of our control problem with execution delay. For any , and , we denote

with the convention that if . We notice that corresponds to the set of renewing orders that have been given before and whose delayed effects appear after . We also denote by the set of -stopping times valued in .

Theorem 3.1.

The value function satisfies the following dynamic programming principle.

-

(DP1)

First dynamic programming inequality:

for all and all .

-

(DP2)

Second dynamic programming inequality: for any , there exists such that

for all .

The proof of this proposition is postponed to Section 5.2.

3.2 Viscosity properties and uniqueness

The PDE system associated to our control problem is formally derived from the dynamic programming relations. We first decompose the domain as follows

where

for and

We also decompose the sets , , as follows

where

We define the operators , , , and by

for any and any function defined on ,

for any with , and any function defined on , and

for any with , and any function defined on .

This provides equations for the value function which takes the following nonstandard form

| (3.18) |

for , with ,

| (3.19) |

for , with ,

| (3.20) |

for ,

| (3.21) |

for , with , and

| (3.22) |

for , with .

Here is the second order local operator associated to the diffusion with no intervention. It is given by

for any with and any function .

As usual, we do not have any regularity property on the value function . We therefore work with the notion of (discontinuous) viscosity solution. Since our system of PDEs (3.18) to (3.22) is nonstandard, we have to adapt the definition to our framework.

First, for a locally bounded function defined on , we define its lower semicontinuous (resp. upper semicontinuous) envelop (resp. ) by

for , with . We also define its left lower semicontinuous (resp. upper semicontinuous) envelop at time by

for .

Definition 3.1 (Viscosity solution to (3.18) – (3.22)).

A locally bounded function defined on is a viscosity supersolution (resp. subsolution) if

(i) for any , and such that

we have

(ii) for any , and such that

we have

(iii) for any we have

(iv) for any , we have

(v) for any , we have

The next result provides the viscosity properties of the value function .

4 Numerics

We describe, in this section, a backward algorithm to approximate the value function and an optimal strategy. Some numerical illustrations are also provided.

4.1 Approximation of the value function

Initialization step.

For we have

We can therefore approximate it by which is the associated Monte Carlo estimator.

Step .

Once we have an approximation of for we are able to get an approximation of on as follows.

Case 1: .

For we have

We can therefore approximate it by which is the Monte Carlo estimator of

On the function is solution to the PDE (3.19) with the terminal condition (3.21). Since we already have approximations of on and , we can compute an approximation using an algorithm computing optimal values of impulse control problem with boundary on (see e.g. [11]) and the terminal value given by

Case 2: . The procedure is the same as in Case 1 but with and instead of and respectively.

4.2 An optimal strategy for the approximated problem

We turn to the computation of an optimal strategy. From the general optimal stopping theory (see [13]), we provide the following strategy . This strategy is constructed as usually done for optimal strategies of impulse control problem but using the approximation instead of the value function . We start with an initial data . We denote by the strategy constructed step by step and by the process controlled by the truncated strategy . We also denote by the pending orders at time .

Initialization step.

We first start by computing the first harvesting time by

and the associated harvested quantity by

Step for harvesting orders.

We then compute the -th harvesting time by

and the associated harvested quantity by

Step for renewing orders.

Denote by the (random) number of harvesting orders on . We then distinguish two cases.

Case 1: .

Suppose first that

Then we compute the optimal renewed resource at time by

If we now suppose that

Then we compute the optimal renewed resource at time by

which is also given by the same expression as in the first inequality

Case 2: .

As in the first case we do not need to distinguish the subcases and and the optimal renewed quantity at time is given by

4.3 Examples

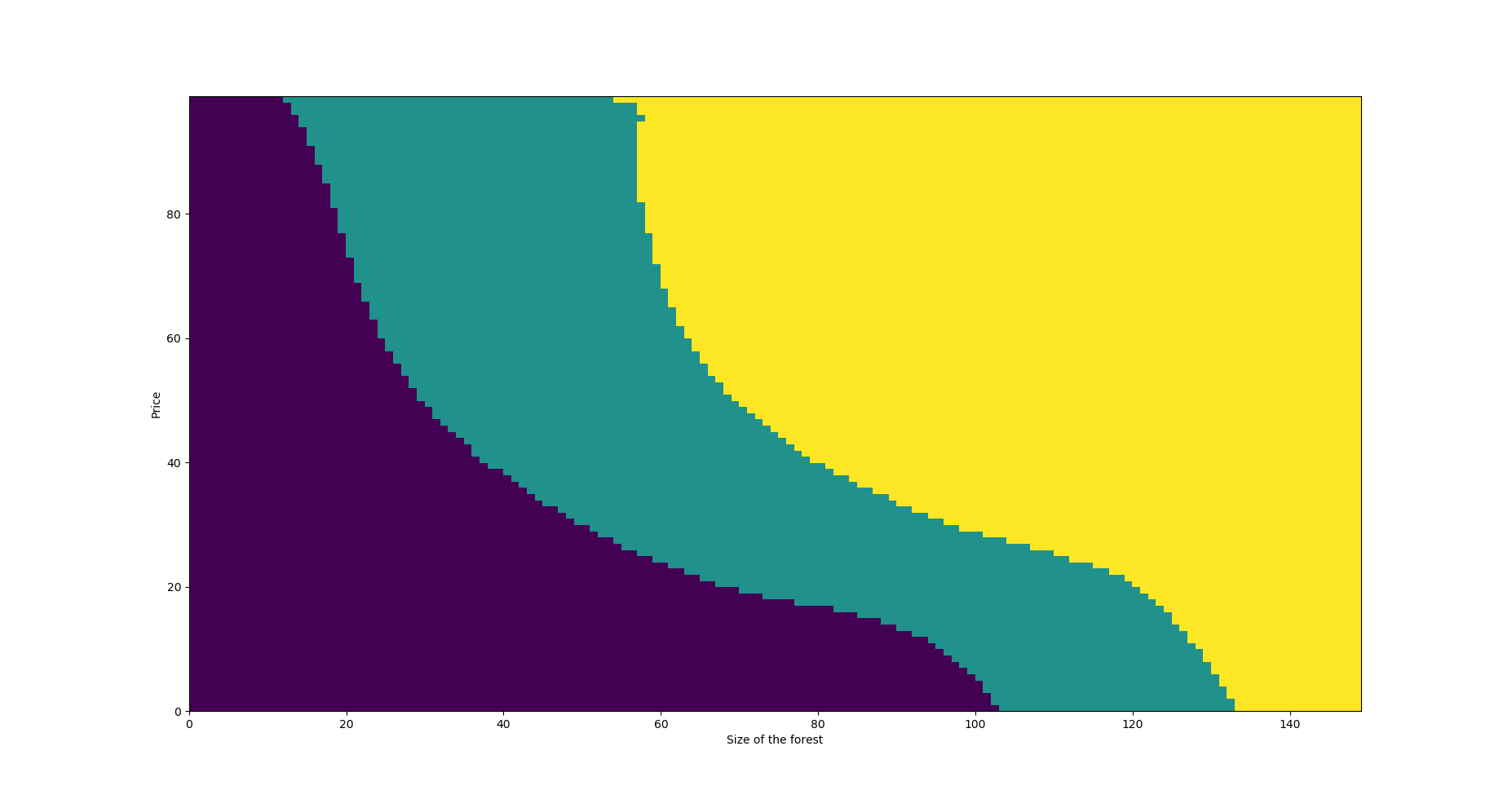

In this part we present numerical illustrations that we get by using an implicit finite difference scheme mixed with an iterative procedure which leads to the resolution of a Controlled Markov Chain by assuming that the resource is a forest . This class of problems is intensively studied by Kushner and Dupuis [15]. The convergence of the solution of the numerical scheme towards the solution of the HJB equation, when the time-space step goes to zero, can be shown using the standard local consistency argument i.e. the first and second moments of the approximating Markov chain converge to those of the continuous process . We assume that the maximal size of the forest is 1 and we use a discretization step of for the size of the forest. About the discretization of the price we discretize the process with , we consider and , and the discretization step is .

We compute the optimal strategy to harvest and renew, and the value function. We assume the parameters of the logistic SDE are , and . The parameter of natural renewal is of the forest. The delay before to able to harvest a tree which is renewed is 1 and the function is equal to . The initial price is . The parameters of the price are and , and the costs to harvest and renew are , and . We assume that the price is equal to the price . We can renew at times and the terminal time is .

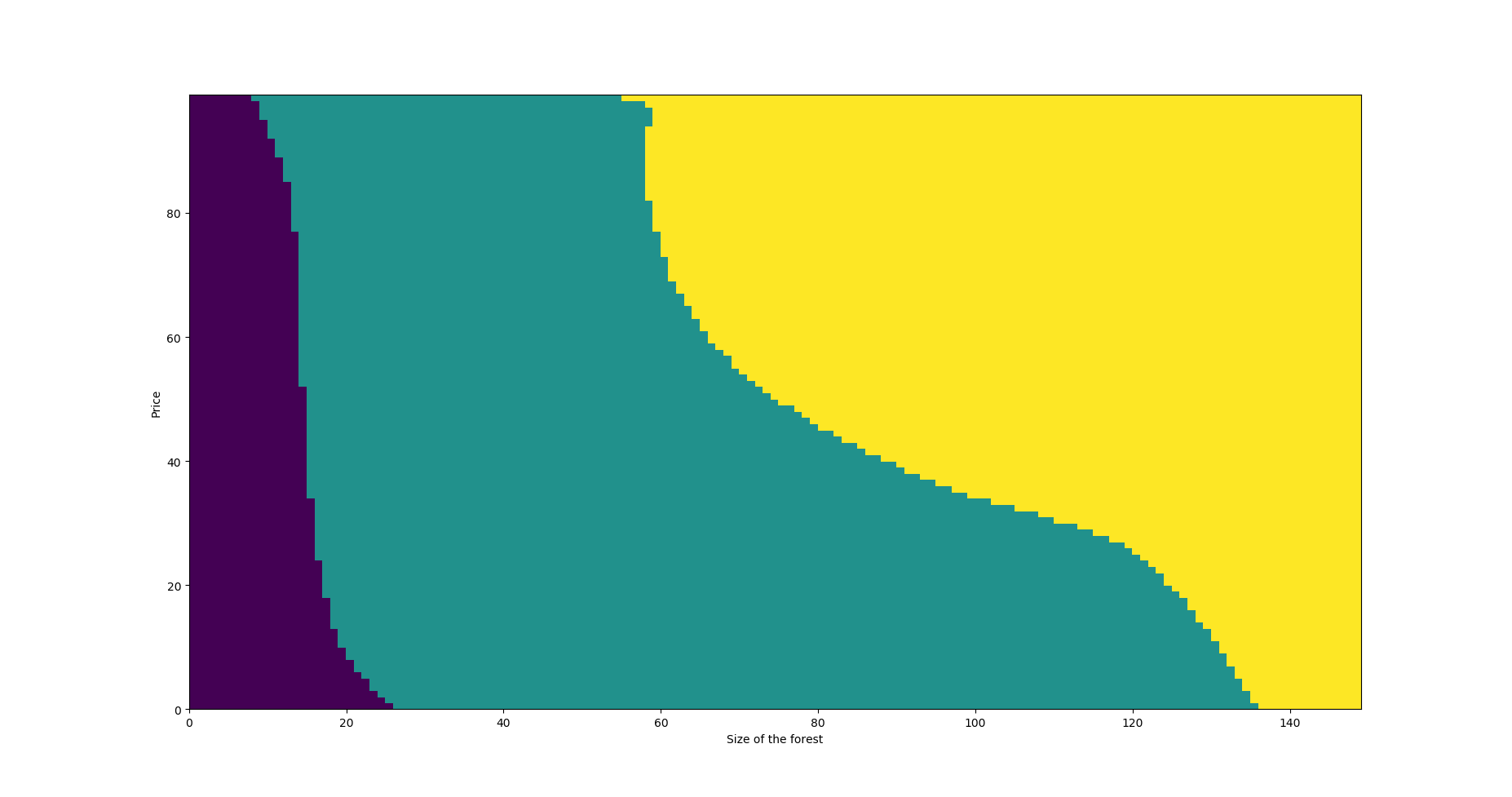

We remark that the value function is increasing w.r.t. the price and the size of the forest, which are expected.

We note that the region to harvest is increasing with the price, and the region to renew is decreasing with the price. We never plant and harvest in the same time.

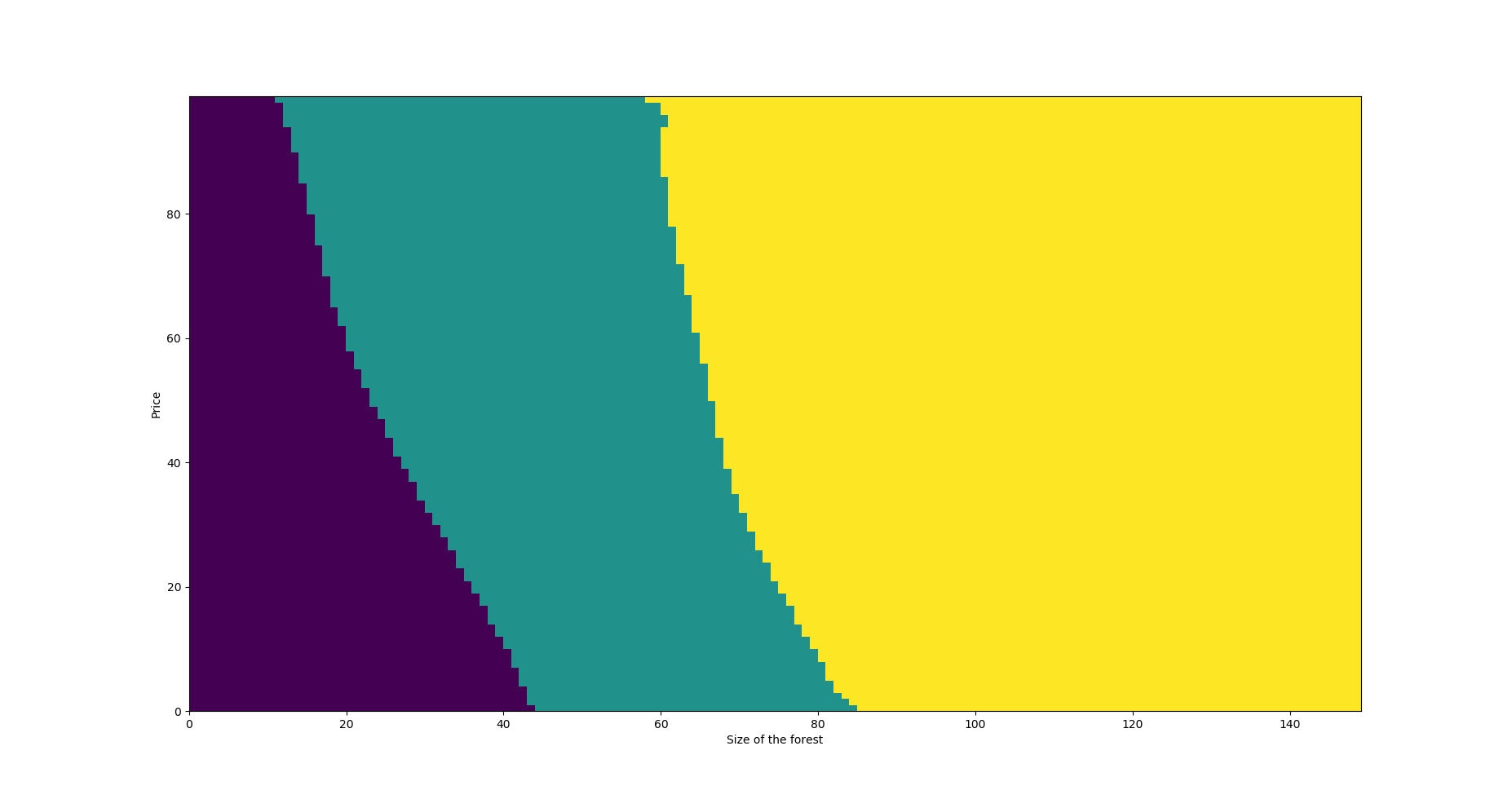

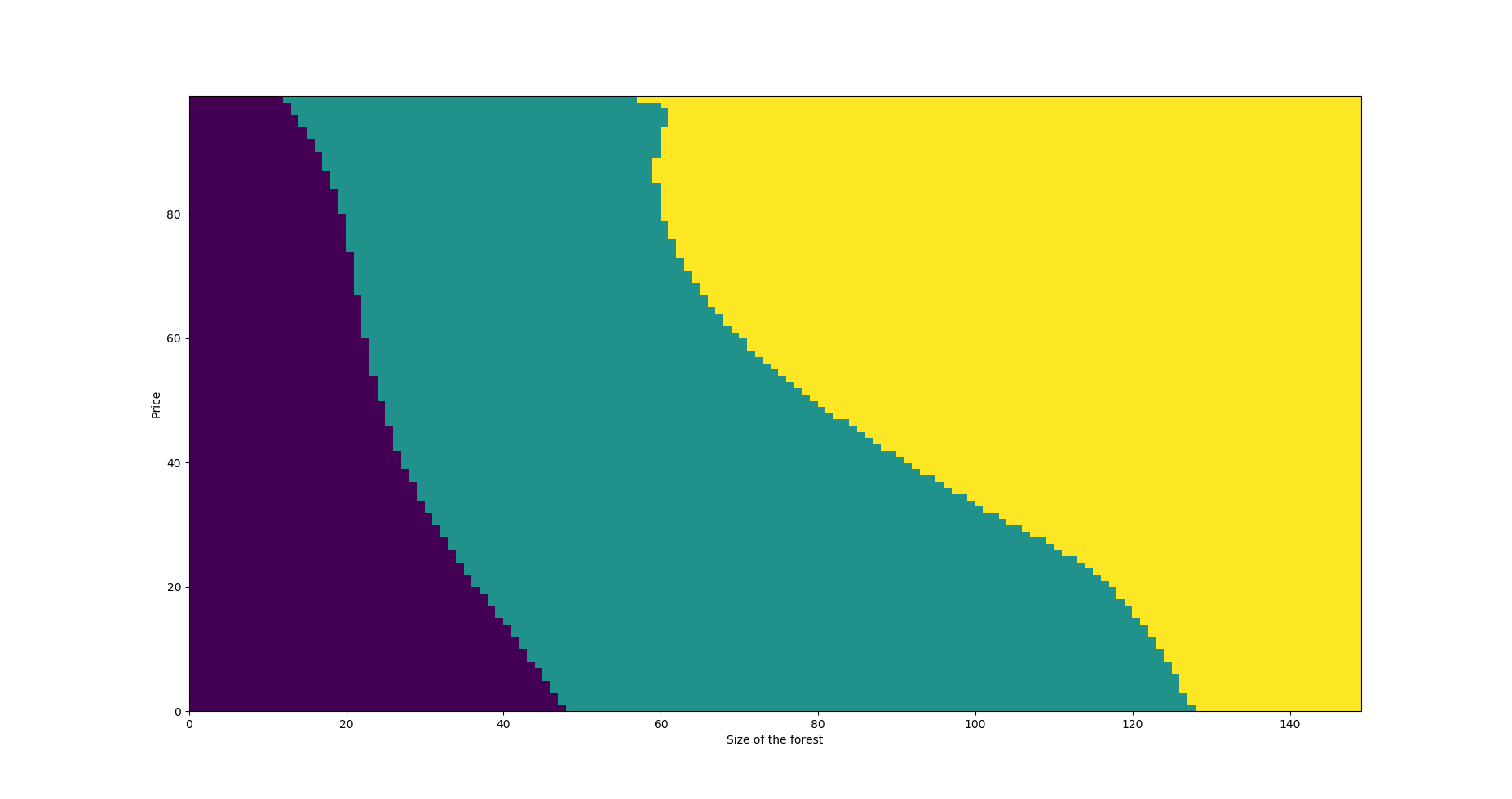

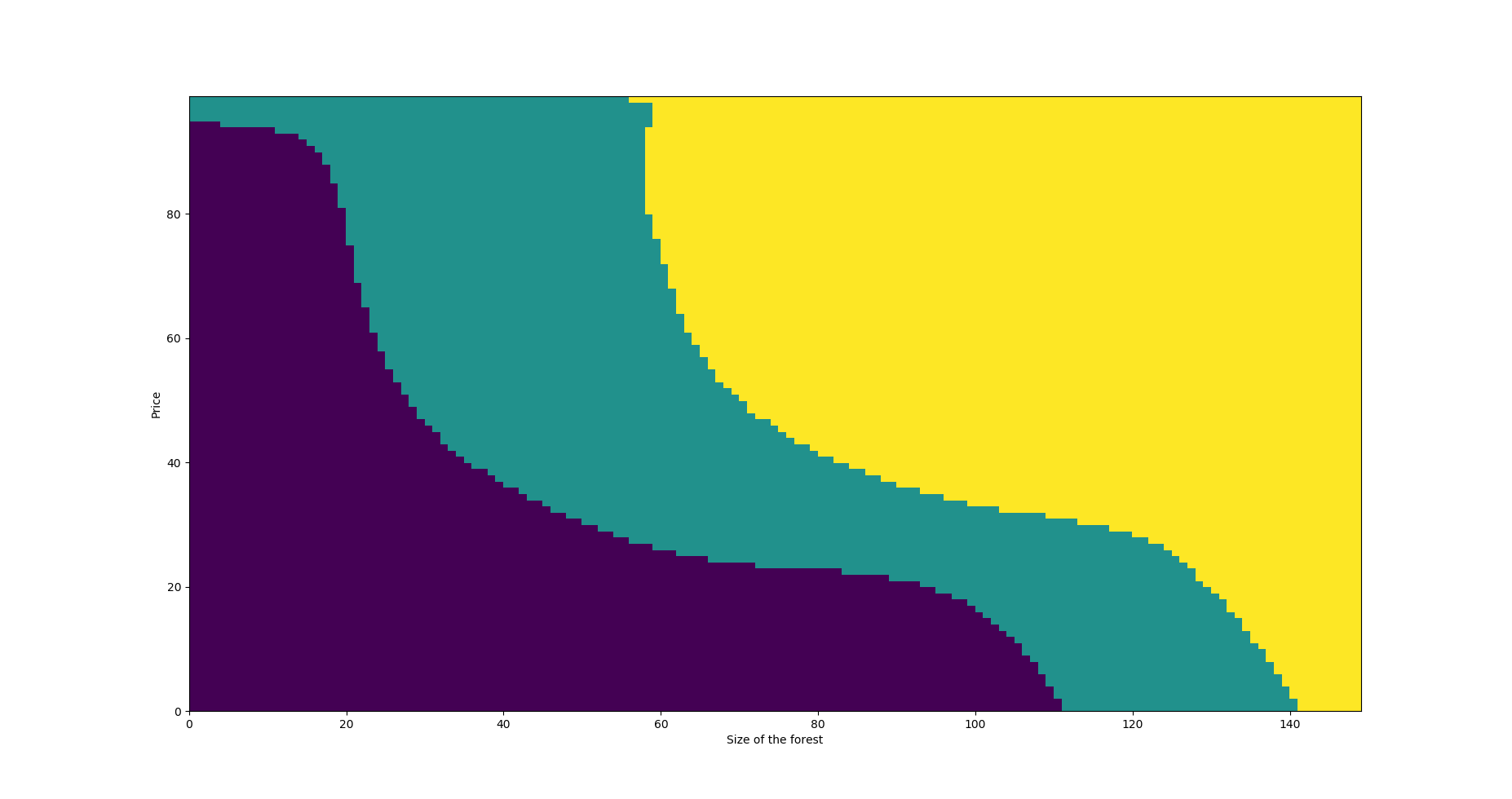

We now study the sensitivity w.r.t. the different parameters. For that we will change parameter by parameter.

If is bigger in this case the region to harvest is more important and the region to renew is less important, since the growth is more important.

If is bigger in this case the region to renew is less important if the price is cheap, since the growth is slow and it is not interesting to renew except if the size of the forest is really small.

If the drift of the price is more important, the region to harvest is less important for a low price since the manager prefer to wait except if the size is too important because in this case the growth is negative, and the region to renew is more important because we know that the price will be better in the future.

If the costs are more expensive, the region to renew is less important because it es expensive to renew and harvest so we renew only if the size is really small.

5 Proof of the main results

5.1 Growth condition on

We provide in this subsection an upper-bound for the growth of the function .

For any , we define the process by and

where . We remark that the process can be written under the following form

for . That corresponds to never harvest and renew always the maximum.

We then have the following estimate on the process .

Lemma 5.1.

For any , there exists a constant such that

| (5.27) |

for all .

Proof. We first prove that for any , there exists a constant such that

| (5.28) |

for all . We argue by induction and we prove that for each there exists a constant such that

| (5.29) |

for all and .

For , using the closed formula of the logistic diffusion, we have

for all . Therefore we get

for all . Therefore (5.29) holds true.

Suppose that the property holds for . Still using the closed formula of the logistic diffusion, we have

for all . Therefore we get

Using the induction assumption and Fatou’s Lemma, we get the result, and (5.29) holds true for each . Taking , we get (5.28).

We now prove (5.27). Still using the closed formula of the logistic diffusion we have

for all . Therefore, we get from the independence of with and (5.28)

for some constant .

Proposition 5.3.

(i) For any , there exists a constant such that

for any strategy .

(ii) There exists a constant such that

for any strategy .

Proof. (i) Fix . Using the definition of we have

for all . Therefore we get from Lemma 5.1

(ii) We turn to the second estimate. From the dynamics (2.9) of , and since we have

where we recall that . Therefore, we get

Therefore there exists a constant depending only on , , , , and such that

Using estimate (i) we get the result.

We turn to the proof of the growth estimation for the value function .

Proof of Proposition 3.2. Fix . From the definition of the function and the dynamics (2.10) and (2.11) of and we have

for any strategy . From classical estimates there exists a constant such that

for all . Using this estimate and Proposition 5.3 we get

Then by considering the strategy with no more intervention than , we get

5.2 Dynamic programming principle

Before proving the dynamic programming principle, we need the following results.

Lemma 5.2.

For any and any control we have the following properties.

-

(i)

The pair satisfies the following Markov property

for any bounded measurable function , and any such that .

-

(ii)

Causality of the control

and for any where we set and

-

(iii)

The state process satisfies the following flow property

for any .

Proof. These properties are direct consequences of the dynamics of .

We turn to the proof of the dynamic programming principles (DP1) and (DP2). Unfortunately, we have not enough information on the value function to directly prove these results. In particular, we do not know the measurability of and this prevents us from computing expectations involving as in (DP1) and (DP2). We therefore provide weaker dynamic programing principles involving the envelopes and as in [5]. Since we get the continuity of at the end, these results implies (DP1) and (DP2).

Proposition 5.4.

For any we have

Proof. Fix , and . By definition of the value function , for any and , there exists , which is an -optimal control at , i.e.

By a measurable selection theorem (see e.g. Theorem 82 in the appendix of Chapter III in [12]) there exists s.t. a.s., and so

| (5.30) |

We now define by concatenation the control strategy consisting of the impulse control components of on , and the impulse control components on . By construction of the control we have , on , , and . From Markov property, flow property, and causality features of our model, given by Lemma 5.2, the definition of the performance criterion and the law of iterated conditional expectations, we get

Together with (5.30), this implies

Since , and are arbitrarily chosen, we get the result.

We now prove (DP2), which is equivalent to the following proposition.

Proposition 5.5.

For all , we have

Proof. Fix , and . From the definitions of the performance criterion and the value functions, the law of iterated conditional expectations, Markov property, flow property, and causality features of our model given by Lemma 5.2, we get

Since and are arbitrary, we obtain the required inequality.

5.3 Viscosity properties

We first need the following comparison result. We recall that and is given by (2.8).

Proposition 5.6.

Fix (resp. ) and a continuous function. Let a viscosity subsolution to (3.18)-(3.19) and

| (5.31) | |||||

and a viscosity supersolution to (3.18)-(3.19)

| (5.32) | |||||

Suppose there exists a constant such that

| (5.33) | |||||

| (5.34) |

for all with . Then on . In particular there exists at most a unique viscosity solution to (3.18)-(3.19)-(5.31)-(5.32), satisfying (5.33)-(5.34) and is continuous on .

The proof is postponed to the end of this section. We are now able to state viscosity properties and uniqueness of .

Viscosity property on .

Fix and with and .

1) We first prove the viscosity supersolution. Let such that

| (5.35) |

Consider a sequence of such that

Applying Proposition 5.4 with where . We have for large enough

where stands for with the strategy with no more interventions than . From (5.35), we get

with as . Taking and applying Ito’s formula we get

Sending to , we get the supersolution property from the mean value theorem.

2) We turn to the viscosity subsolution. Let such that

| (5.36) |

Consider a sequence of such that

From Proposition 5.5 we can find for each a control such that

where stands for and is a constant that will be chosen later.

We first notice that

| (5.37) |

Indeed, we have

| (5.38) |

where is given by

Since (and ), we have as and we get (5.37). In particular, we deduce that up to a subsequence

| (5.39) |

Indeed, we have from (2.9) and (5.38)

From BDG inequality and (5.38), we get from (5.37)

and hence, up to a subsequence as . From this convergence (5.37) and (5.3), we get (5.39).

Viscosity property on .

Viscosity property and continuity on .

We prove it by a backward induction on .

Suppose that .

1) We first prove the subsolution property. Fix some and and consider a sequence with and such that

By considering a strategy with a single renewing order with and the stopping time , we get from the definition of

From the continuity of the functions , and , we get

From Fatou’s Lemma and since is arbitrarily chosen, we get by sending to

| (5.41) |

Fix now and denote . By considering a strategy with an immediate harvesting order and a single renewing order and , we get from the definition of

From the continuity of the functions , , and , we get

From Fatou’s Lemma and since and are arbitrarily chosen, we get by sending to

| (5.42) |

From (5.41) and (5.42), we get the subsolution property at .

2) We turn to the supersolution property. We argue by contradiction and suppose that there exist and such that

with . We fix a sequence in such that

| (5.43) |

We then can find and a sequence of smooth functions on such that on , on as and

| (5.44) |

on some neighborhood of in . Up to a subsequence, we can assume that for sufficiently small. Since is locally bounded, there is some such that on . We therefore get on . We then define the function by

and we observe that

| (5.45) |

Since as , we can choose large enough such that

| (5.46) |

From the definition of we can find such that

| (5.47) |

where stands for . Denote by . From Ito’s formula, (5.44), (5.45) and (5.46) we have

From (5.47) and the Markov property given by Lemma 5.2 (i), we get by taking the conditional expectation given ,

We therefore get

Sending and to we get a contradiction with (5.43).

Suppose that the property holds true for . From Proposition 5.6, the function is continuous on . Therefore, we get from Propositions 5.4 and 5.5

for all .

We can then apply the same arguments as for and we get the viscosity property at for all .

Proof of Proposition 5.6.

We fix the functions and as in the statement of Proposition 5.6. We then introduce as classically done a perturbation of to make it a strict supersolution.

Lemma 5.3.

Consider the function defined by

where and are two positive constants and define for the function on by

Then there exist and (large enough) such that the following properties hold.

- •

-

•

We have

(5.48)

Proof. A straightforward computation shows that

on . Since is a viscosity supersolution to (3.19), we get

| (5.49) |

on . Then, from the definition of the operator we get for large enough

In particular, since is continuous, we get

| (5.50) |

for any compact subset of . By writing the viscosity supersolution property of , we deduce from (5.49) and (5.50) the desired strict viscosity supersolution property for .

To prove the comparison result, it suffices to prove that

for all . We argue by contradiction and suppose that there exists such that

Since is u.s.c. on and , we get from (5.48) the existence of an open subset of and such that is compact and

We then consider the functions and defined on by

for all and . From the growth properties of and , there exists such that

By classical arguments we get, up to a subsequence, the following convergences

| (5.51) |

In particular, we have for large enough. We then apply Ishii’s Lemma (see Theorem 8.3 in [10]) to which realizes the maximum of and we get for any , the existence of and such that

| (5.52) | |||||

| (5.53) |

and

| (5.54) |

for all . We then distinguish two cases.

Case 1: there exists a subsequence of still denoted such that

From the viscosity subsolution property of and the strict viscosity supersolution property of we have

| (5.55) | |||||

| (5.56) |

where

for any , , , and any symmetric matrix . We then distinguish the following two possibilities in (5.55).

1. Up to a subsequence we have

Using (5.56), we have . Therefore, we get

Sending to we get

where we used the upper semicontinuity of and the lower semicontinuity of . Since is upper semicontinuous there exists (with ) such that . Therefore we get the following contradiction

2. Up to a subsequence we have

Using (5.56) we get

| (5.57) |

and we obtain from (5.51) that

| (5.58) |

Moreover, by (5.51) and (5.54) , we have using classical arguments

From this last inequality and (5.58) and by sending to in (5.57) we get , which is the required contradiction.

Case 2: we have

Then we are in the same situation as in the second possibility of Case 1 and we get a contradiction.

References

- [1] R. Aid, S. Federico, H. Pham, and B. Villeneuve (2015) Explicit investment rules with time-to-build and uncertainty. Journal of Economic Dynamics and Control, 51, 240-256

- [2] L. Alvarez and E. Koskela (2007) Optimal harvesting under resource stock and price uncertainty. Journal of Economic Dynamics and Control, 31 (7), 2461-2485.

- [3] G.S. Amacher, M. Ollikainen and E. Koskella (2009) Economics of forest resources, Cambridge: MIT Press (397 p.).

- [4] B. Bouchard (2009) A stochastic target formulation for optimal switching problems in finite horizon. Stochastics and Stochastics Reports, 81 (2), 171-197.

- [5] B. Bouchard and N. Touzi (2011) Weak dynamic programming principle for viscosity solutions. SIAM Journal on Control and Optimization, 49 (3), 948-962.

- [6] B. Bruder and H. Pham (2009) Impulse control problem on finite horizon with execution delay. Stochastic Processes and their Applications, 119, 1436-1469.

- [7] E. Cerdas and D. Martin-Barosso (2013) Optimal control for forest management and conservation analysis in dehesa ecosystems. European Journal of Operational Research 227 (2013) 515 526.

- [8] C. W. Clark (1990) Mathematical Bioeconomics: The Optimal Management of Renewable Resource. John Wiley and Sons, New York, NY, USA, 2nd edition.

- [9] H. R. Clarke and W. J. Reed (1989) The tree-cutting problem in a stochastic environment: the case of age dependent growth. Journal of Economic Dynamics and Control, 13, 569-595.

- [10] Crandall M., Ishii H. and P.L. Lions (1992) User’s guide to viscosity solutions of second order partial differential equations. Bulletin of the American Mathematical Society, 27, 1-67.

- [11] J.P. Chancelier, B. Oksendal and A. Sulem (2002) Combined stochastic control and optimal stopping, and application to numerical approximation of combined stochastic and impulse control. Stochastic Financial Mathematics, Proceedings of the Steklov Mathematical Institute, 237, 149-173.

- [12] C. Dellacherie and P.A. Meyer (1975) : Probabilités et Potentiel, I-IV, Hermann, Paris.

- [13] N. El Karoui (1979) Les aspects probabilistes du contrôle stochastique. Ecole d’été de probabilit s de Saint Flour IX, Lecture Notes in Mathematics, 876, 73-238.

- [14] R. Q. Grafton, T. Kompas, and D. Lindenmayer (2005) “Marine reserves with ecological uncertainty”, bulletin of mathematical biology, 67, 957-971.

- [15] H. Kushner and P. Dupuis (2001) : Numerical Methods for Stochstic Control Problems in Continuous Time, volume 24 of Stochastic Modelling and Applied Probability. Springer, New York second edition.

- [16] G. Lien, S. Stordal, J.B. Hardaker, and L.J. Asheim (2007) Risk aversion and optimal forest replanting: A stochastic efficiency study. European Journal of Operational Research, 181, 1584 1592.

- [17] A. Leung and A.-Y. Wang (1976) Analysis of models for commercial fishing: mathematical and economical aspects. Econometrica, 44(2), 295-303.

- [18] V. Ly Vath, M. Mnif and H. Pham (2007) A model of portfolio selection under liquidity risk and price impact. Finance and Stochastics, 11, 51-90.

- [19] B. Oksendal and A. Sulem (2008) Optimal Stochastic Impulse Control with Delayed Reaction. Applied Mathematics and Optimization, 58 (2), 243-255.

- [20] W. J. Reed and H. R. Clarke (1990) Harvest Decisions and Asset Valuation for Biological Resources Exhibiting Size-Dependent Stochastic Growth. International Economic Review Vol. 31 (1), pp. 147-169

- [21] J.-D. Saphores (2003) Harvesting a renewable resource under uncertainty. Journal of Economic Dynamics & Control, 28(3).

- [22] C. H. Skiadas (2010) Exact Solutions of Stochastic Differential Equations: Gompertz, Generalized Logistic and Revised Exponential. Methodology and Computing in Applied Probability, 12, 261-270.

- [23] H. M. Soner (1986) Optimal Control with State-Space Constraint. I, SIAM Journal of Control and Optimzation, 24 (3), 552-561.

- [24] H. M. Soner (1986) Optimal Control with State-Space Constraint. II, SIAM Journal of Control and Optimzation, 24 (6), 1110-1122.

- [25] S. Tang and J. Yong (1993) Finite horizon stochastic optimal switching and impulse controls with a viscosity solution approach. Stochastics, 45 (3-4), 145-176.

- [26] Y. Willassen (1997) The stochastic rotation problem: A generalization of Faustmann’s formula to stochastic forest growth. Journal of Economic Dynamics & Control, 22, 573-596.