Nash equilibrium for risk-averse investors in a market impact game with transient price impact

This version: May 19, 2019)

Abstract

We consider a market impact game for risk-averse agents that are competing in a market model with linear transient price impact and additional transaction costs. For both finite and infinite time horizons, the agents aim to minimize a mean-variance functional of their costs or to maximize the expected exponential utility of their revenues. We give explicit representations for corresponding Nash equilibria and prove uniqueness in the case of mean-variance optimization. A qualitative analysis of these Nash equilibria is conducted by means of numerical analysis.

Keywords: Market impact game, high-frequency trading, Nash equilibrium, transient price impact, market impact, predatory trading

1 Introduction

In a market impact game, financial agents compete with each other in a market framework where each trade creates price impact. Early papers on this subject, such as Brunnermeier and Pedersen [6], Carlin et al. [7], and Schöneborn and Schied [24], consider risk-neutral agents that are active in a linear Almgren–Chriss market impact model. Already in this relatively simple setup, interesting effects appear, such as transitions in the predatory or cooperative behavior of agents. Extensions to risk-averse agents in the Almgren–Chriss framework were given, e.g., in [9, 21]. For further developments in the literature on market impact games, we refer to [8, 16, 10].

In this paper, we consider risk-averse agents that are active in a discrete-time model with linear transient price impact. For single-agent optimization problems, such price-impact models were introduced by Obizhaeva and Wang [17] and later further developed, e.g., in [2, 12]. A market impact game with two risk-neutral agents was first considered by Schöneborn [23], who observed that equilibrium strategies may exhibit strong oscillations between buy and sell trades if trading speed is sufficiently high. This situation was further investigated in [20, 22], where the model was also enhanced by introducing additional quadratic transaction costs, whose strength is parameterized by a number . It was shown in particular that there exists an explicitly given critical value such that the equilibrium strategies show at least some oscillations for , whereas all oscillations disappear for .

In [22], only two competing risk-neutral agents are considered. The main goal of the present paper is to extend the results and observations from [22] to a more flexible setting, in which an arbitrary (but finite) number of agents optimize their strategies under risk aversion. More precisely, the agents either minimize a mean-variance functional of the trading costs over deterministic strategies or they maximize the expected CARA utility of their revenues over adaptive strategies. We show that both problems admit an identical Nash equilibrium, which is given in explicit form and which is unique in the case of mean-variance optimization. More precisely, the equilibrium strategies arise as linear combinations of two extreme base strategies and . The first, , is the normalized common strategy of all players if each player has the same initial position. The second, , is the normalized common strategy of all players if the initial positions of all players add up to zero.

Then we use numerical analysis of the equilibrium strategies to determine numerically the critical threshold for the transaction costs above which all oscillations cease. In contrast to the risk-neutral two-player case studied in [22], we now observe two different thresholds for and . Moreover, the threshold for will not depend on the risk-aversion but on the number of players. By contrast, the threshold for will not depend on the number of players but on the risk aversion.

If agents exhibit strictly positive risk aversion, it is possible to study the market impact game with an infinite time horizon. This question is interesting when one does not want to impose an externally given time horizon and instead aims at an intrinsic derivation of a trading horizon. We show that such an infinite-horizon market impact game admits a Nash equilibrium in case is equal to the critical value , which was determined numerically for finite time horizons. If , a Nash equilibrium may not exist.

This conjectured nonexistence is a consequence of the idealization of admitting infinitely many trades, an idealization that also in the context of continuous-time models has turned out to be not as innocent as one might initially hope. Specifically, it was shown in [20] that in the case of two risk-neutral agents, a nontrivial Nash equilibrium can only exist if . This negative result has motivated Strehle [25] to include in the cost functional an additional penalization of the derivatives of the continuous-time strategies. This additional term regularizes the admissible strategies so that Nash equilibria exist in general.

2 Main results

2.1 Finite time horizon

We consider an -agent extension of the discrete-time market impact model with linear transient price impact that was studied, e.g., in [1, 2, 17, 22, 23]. This model is sometimes also called the discrete-time linear propagator model, and we refer to [13] for a discussion and further background.

Suppose that financial agents are active in a market impact model for one risky asset. As commonly assumed in the market impact literature, the unaffected price process will be a square-integrable and right-continuous martingale on the filtered probability space . An important special case will be the Bachelier model of the form

| (1) |

for constants and a standard Brownian motion . All agents trade at a finite number of times . The trading strategy of agent will be a vector where represents the number of shares sold at time . That is, represents a sell order and means a buy order. The matrix of all strategies is denoted by .

When all the agents apply their strategies, the asset price is given by

| (2) |

where is called the decay kernel. The quantity describes the time- price impact of a unit transaction made at time . When agent first places an order at time , the asset price is moved linearly from to . The liquidation cost for agent is thus:

Suppose that immediately after agent , another agent places an order . The liquidation cost for agent is the following:

| (3) |

where is an additional cost term due to the latency in execution time. On average, fifty percent of times, the order of agent will be executed before the order of agent . The latency costs for agent at time will thus be of the form

In addition to the execution costs described above, we follow [20, 22] in assuming quadratic transaction costs with . One of our goals will be to analyze the qualitative effects these transaction costs will have on optimal strategies. Such quadratic transaction costs are often used to model “slippage” arising from various costs incurred by a transaction (see [3, 5] and [12, Section 2.2]) or a transaction tax (see [20, 22]). As discussed by Strehle [25, p. 5], these transaction costs should not be understood as resulting from temporary price impact, as all costs arising from price impact are already contained in (3). Moreover, one can argue as in Proposition 2.6 of [22] to see that our quadratic transaction cost function can be replaced by proportional transaction costs in a neighborhood of the origin without affecting the Nash equilibrium we are going to derive. Since the main difference of quadratic and proportional transaction costs is their behavior at the origin, it is therefore highly plausible that similar results as obtained in the following sections for quadratic transaction costs might also hold for proportional transaction costs. The previous discussion thus motivates the following definition.

Definition 2.1.

Given a time grid , the execution costs of the strategy given all other strategies with are defined as

| (4) |

where .

In the sequel, we will suppose that agent has an initial position of shares and is constrained to hold a zero terminal position by the end of the trading day. It is often assumed [17, 22] that agents aim to minimize the expected costs over the following class of strategies,

In practice, however, it is also popular to incorporate the agents’ risk aversion and to optimize the following mean-variance functional of the trading costs,

| (5) |

Here, is a risk-aversion parameter. For , the mean-variance functional (5) is typically only time-consistent if strategies are deterministic; see, e.g., [3, 15]. Therefore, its minimization is usually restricted to the class of deterministic strategies in , which we denote by

for . It can also make sense to maximize the expected utility of the revenues, which are nothing else than the negative costs. Here, we will use the following utility functional,

where is the following exponential – or CARA – utility function,

Due to the time consistency of the expected utility functional, we can consider its maximization over all adapted strategies from the class . Moreover, as, e.g., in [7, 20, 21, 22, 25], we assume henceforth that each agent has full information about the strategies used by the other agents.

Definition 2.2.

Suppose there are agents with initial inventories and risk aversion parameter and that is a fixed time grid.

-

(a)

A Nash equilibrium for mean-variance optimization is a collection of strategies such that each minimizes the mean-variance functional over .

-

(b)

A Nash equilibrium for CARA utility maximization is a collection of strategies such that each maximizes the CARA utility functional over .

In the preceding definition, we have assumed that all agents share the same risk aversion parameter . The case in which the agents have different risk aversion parameters is a straightforward but tedious extension of the current model. It will substantially complicate the notation while not providing significant additional insights. For this reason, we will only consider the case of identical risk aversion parameters. Now let

We define for ,

| (6) |

where is the Kronecker delta. Then we define

| (7) |

Note that . We further define

| (8) | ||||

| (9) |

Recall that a function is called strictly positive definite (in the sense of Bochner) if for all and , the matrix is positive definite.

Assumption 2.3.

We henceforth assume that the function is strictly positive definite.

According to Pólya [18], Assumption 2.3 is satisfied as soon as is convex, nonincreasing, and nonconstant (see also Young [26] for an earlier argument). It implies that the matrix is positive definite for all time grids . As observed in [2], Assumption 2.3 also rules out the existence of price manipulation strategies in the sense of Huberman and Stanzl [14]. Now we can state our first result on the existence and uniqueness of a Nash equilibrium. It extends Theorem 2.5 from [22], where the case and was treated.

Theorem 2.4.

Suppose Assumption 2.3 holds. Then, for any time grid , parameters , initial inventories , and , the strategies

| (10) |

form the unique Nash equilibrium for mean-variance optimization. If, moreover, is a Bachelier model of the form (1), then the strategies (10) also form a Nash equilibrium for CARA utility maximization.

Remark 2.5.

Note that the Nash equilibrium for mean-variance optimization is unique, but that we do not know whether the Nash equilibrium for CARA utility maximization is also unique. This has to do with the larger class of adapted strategies that is admitted for CARA utility maximization. However, it follows easily from the first part of Theorem 2.4 that the strategies (10) form a unique Nash equilibrium for CARA utility maximization when is a Bachelier model and all agents are restricted to use deterministic strategies.

It follows from Theorem 2.4 that in the following two special cases the Nash equilibrium has a particularly simple structure:

-

•

if , then for ;

-

•

if , then for .

It was shown in Corollary 1 of [2] that, for convex and nonincreasing and convex , single-agent strategies () are always buy-only or sell-only. On the other hand, Schöneborn [23] observed that for , , , and the equilibrium strategies oscillate between buy and sell orders. These oscillations are thus a genuine effect of the interaction between the two agents. This effect was explained in [20, 22, 23] as a result of the need for protection against predatory trading by the competitor. These oscillations also have a similarity to the “hot-potato” game between high-frequency traders during the flash crash of May 10, 2010 (see [11, p. 2]). In [22], the influence of on the oscillations of the equilibrium strategies was analyzed for and . It was found that there exists a critical level such that the equilibrium strategies show at least some oscillations for , whereas all oscillations disappear for . In [22], the critical level was identified as . Here, our goal is to analyze numerically the influence of the number of agents and the level of their risk aversion on the value of .

Assumption 2.6.

In the numerical analysis, we make the following assumptions.

-

(i)

We have and the time grid is equidistant: for

-

(ii)

is of the form .

-

(iii)

is a Bachelier model of the form (10) with .

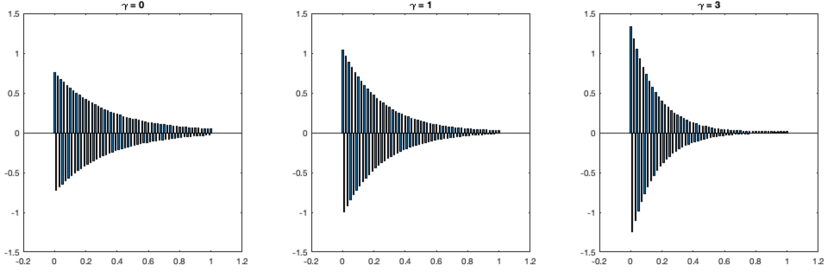

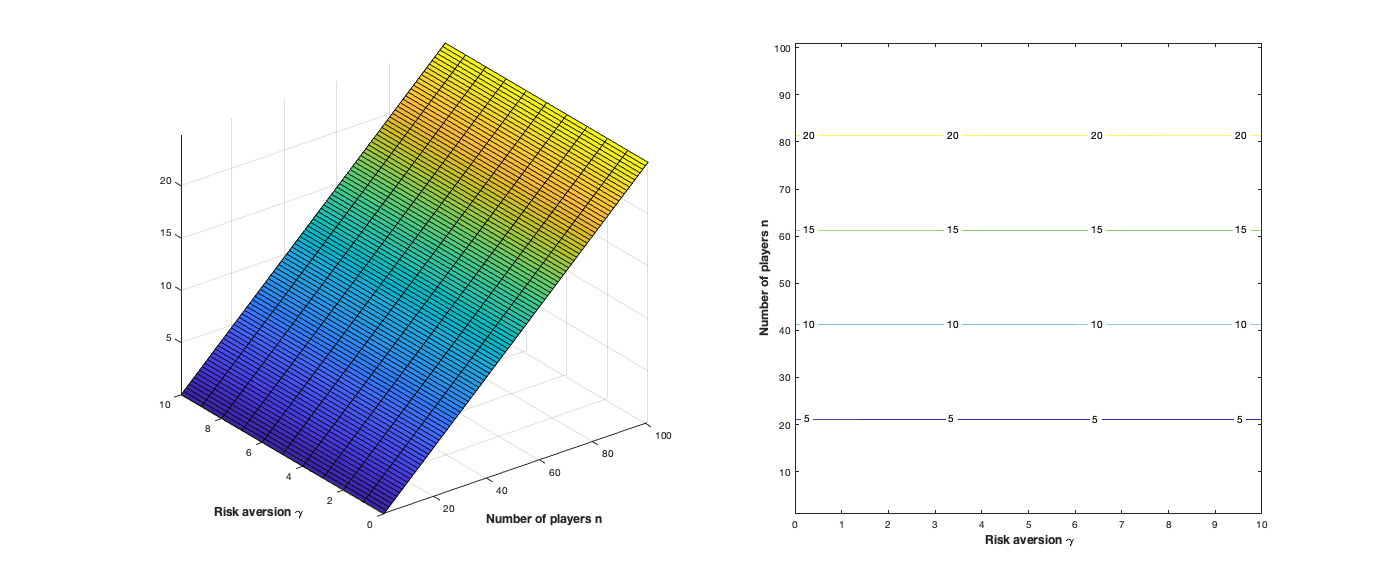

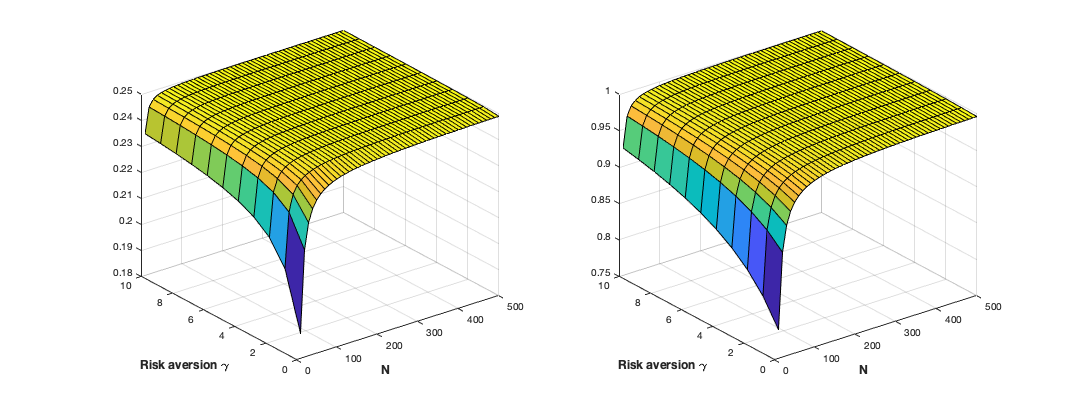

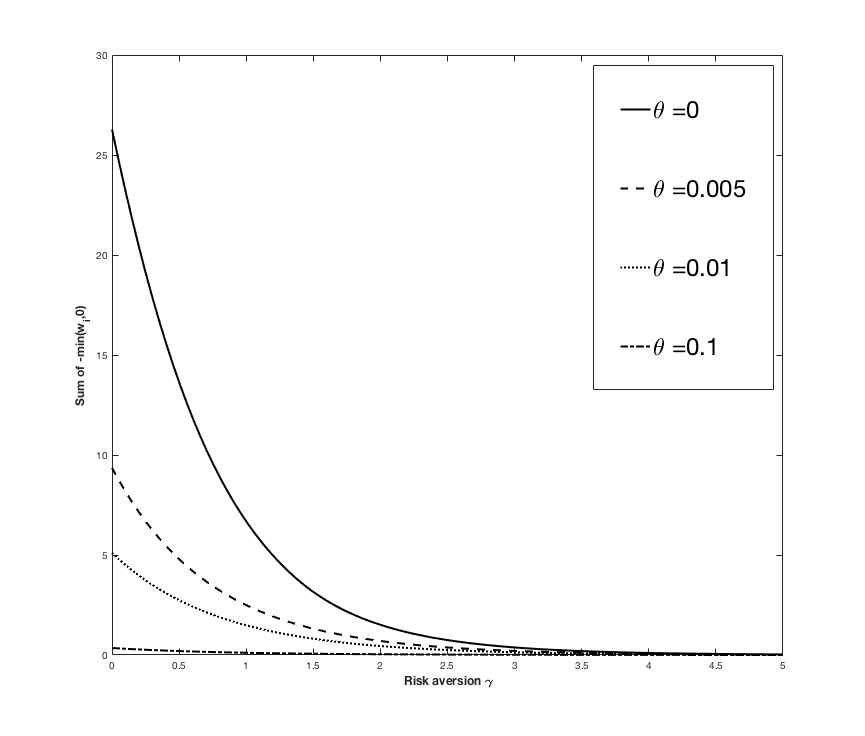

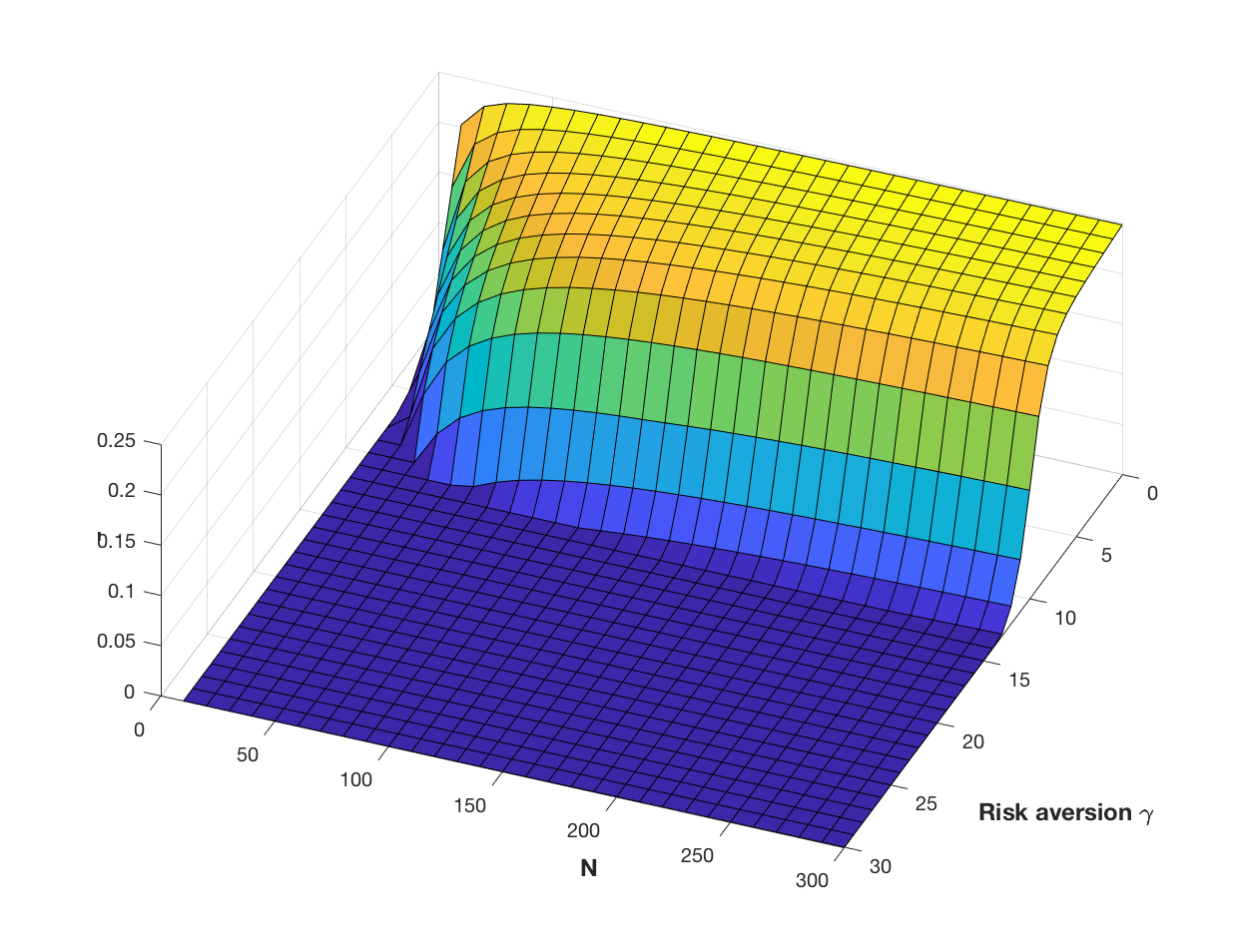

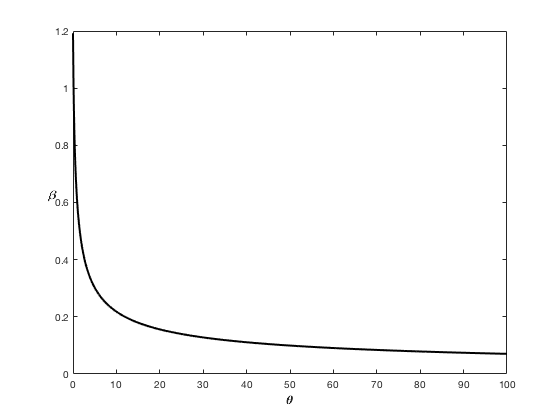

In Figure 1 we observe that increasing the risk aversion does not stop the oscillations in the vector . On the contrary, increasing actually magnifies the oscillations during the early trading periods. Increasing the level of transaction costs, however, will clearly diminish the size of oscillations. For fixed , , and , we can therefore look for that level at which becomes nonnegative. Figure 2 suggests that, at least for sufficiently large , this level is completely independent of the risk aversion parameter , an observation we find highly surprising. In Figure 3, we provide numerical surface plots for the function with and . Together with additional simulations carried out by the authors, Figures 3 and 2 suggest that for each there is a critical level at which all oscillations of cease and that it is given by

| (11) |

This conjecture is consistent with the theoretical results obtained in [2] and [22] for and , respectively.

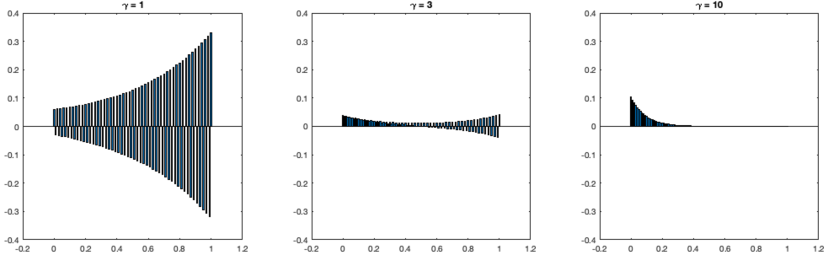

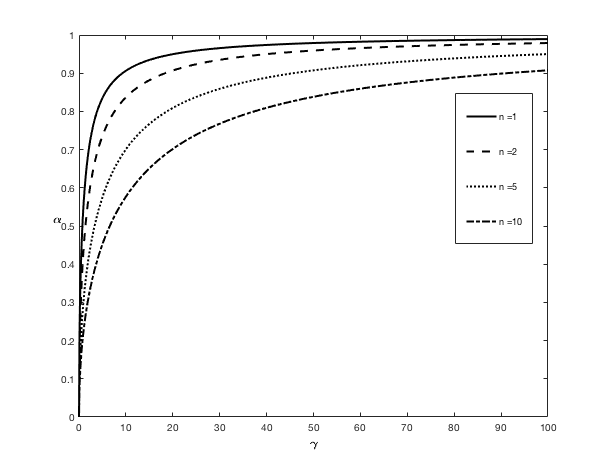

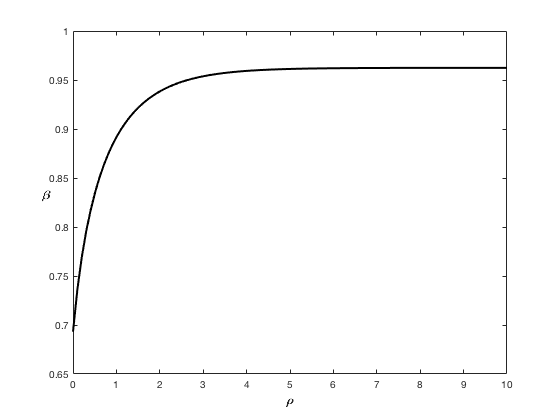

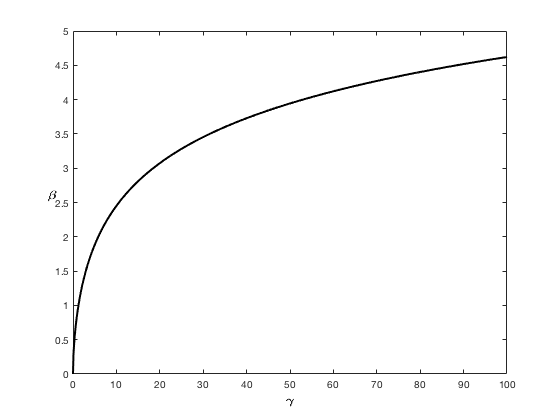

Now we turn to vector . The first observation is that is independent of the number of agents. Thus, the critical level at which oscillations cease is a function of and only. For , must be identical to the one studied in [20, 22], and it follows from Theorem 2.7 of [22] that the critical transaction cost level in this case is . Moreover, it can be seen from Figures 4 and 5 that, in contrast to , the oscillations of the vector are influenced by changing the risk aversion . More precisely, increasing does have a diminishing effect on the oscillations of . Therefore, we conjecture that

| (12) |

This conjecture is also supported by Figure 6 and consistent with Theorem 2.7 of [22].

Remark 2.7.

For simplicity, we performed the above simulations under the assumption that is of the form . One can instead assume that for some and verify that the above numerical results remain valid. Note that for large , one will need a sufficiently large to visualize the convergence of to the critical values. Moreover, we have extended the simulations to a power law decay kernel of the form with . The behaviours of vector and as well as the critical values for are again consistent with the above analysis. The corresponding plots are therefore omitted.

Remark 2.8.

As mentioned above, conjectures (11) and (12) are proved in [22] for the special case of two risk-neutral agents. Already in this special case, the proof of (11) is quite involved. It relies in part on the fact that is a Kac–Murdock–Szegő matrix, whose inverse is known explicitly. For , however, the inverse of is not known, and so the proof method from [22]. The proof of (12) in the special case of [22] relies on the fact that is an upper triangular Toeplitz matrix. The inverse of such a matrix can be computed by the coefficients of the reciprocal of the power series formed from the coefficients of . Then the celebrated Kalusza sign criterion is applied in [22] so as to characterize the case in which all coefficients of the reciprocal power series are nonnegative. For , however, is no longer an upper triangular Toeplitz matrix, and so the proof from [22] cannot be extended to our present situation.

It is interesting to note that for and , the vector has a particularly simple structure. This is stated in the following theoretical result.

Proposition 2.9.

Under Assumption 2.6 (i), (iii), and with , for and ,

2.2 Infinite time horizon

For non-vanishing risk aversion , it is possible to study our problem also for an infinite time horizon. The intuitive reason is that any risk-averse investor will automatically try to liquidate any position held in an asset whose price process is a martingale.

Assumption 2.10.

Under Assumption 2.10 (i), the strategy of an agent with initial position will be represented by a sequence of random variables such that the following conditions are satisfied:

-

•

each is -measurable;

-

•

the random variable takes values in the space of absolutely summable real sequences;

-

•

the random variable is bounded in the Banach space of bounded sequences;

-

•

we have for each .

The set of all these strategies will be denoted by . Again, the class of all deterministic strategies in will be denoted by . Since , it is clear that (4) can be extended as follows to strategies , ,

Again, each agent will aim to minimize the following mean-variance functional,

or to maximize the CARA utility functional

The notion of Nash equilibria for mean-variance optimization and CARA utility maximization can be defined in exactly the same way as in Definition 2.2. However, it is not clear a priori whether the formulas (8) and (9) for and can also be extended to an infinite time horizon, because it is no longer clear whether the vector belongs to the range of the linear operators and . The following result states the existence of an infinite-horizon Nash equilibrium in a specific situation.

Theorem 2.11.

In addition to Assumption 2.10, suppose that and

| (13) |

Then there exist unique positive solution and of the two equations

| (14) | ||||

| (15) |

Moreover, . For these, we define through

and through

Then, for any initial positions , the strategies

| (16) |

form a Nash equilibrium for mean-variance optimization in and a Nash equilibrium for CARA utility maximization in .

In the preceding theorem, we have assumed that . In the general case, the following result will follow immediately from the proof of Theorem 2.11.

Proposition 2.12.

As a matter of fact, we conjecture that in the situation of Proposition 2.12 (b), no Nash equilibrium exists unless holds. The situation is very similar to the one of Theorem 4.5 in [20], where a continuous-time version of the game for and was analyzed. It was shown there that a continuous-time Nash equilibrium can exist only if or . In both situations, the underlying intuition for the nonexistence of Nash equilibria results from the possibility of trading infinitely often, either in continuous time or over an infinite time horizon. This shows that the idealization of admitting infinitely many trades is not as harmless as it might seem, an observation that has also been made, for instance, in the context of the FTAP.

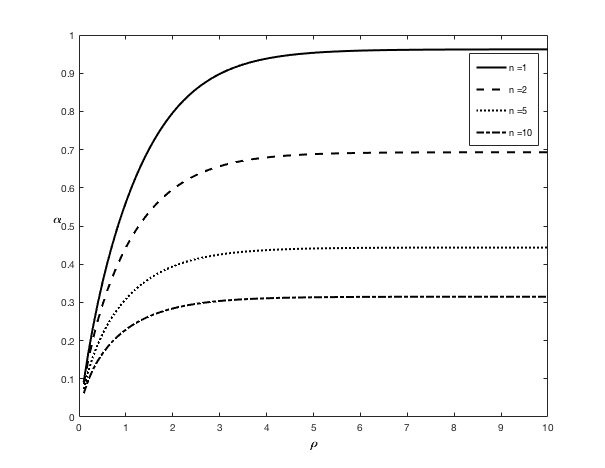

The qualitative behavior of the respective solutions and of (14) and (15) is plotted in Figures 7 and 8. In case , we have the following explicit result.

Proposition 2.13.

If , then the solution of (14) is given by

| (17) |

3 Proofs

Lemma 3.1.

An admissible strategy given all the competitors’ strategies with has the following mean-variance functional:

| (18) |

Proof.

Since all strategies are deterministic,

Since is a martingale,

Moreover, using matrix notation,

and

Using again that are deterministic and the martingale property of ,

By substituting the preceding results into (5), we obtain the desired formula:

∎

We will use the convention of saying that an -matrix is positive if for all nonzero , which makes sense also if is not necessarily symmetric. Clearly, for a positive matrix there is no nonzero for which , and so is invertible.

Lemma 3.2.

For all and , the matrices , , and are positive.

Proof.

By Lemma 3.2 in [22], the matrices , , , and are positive. Since is the covariance matrix of the random variables, , it is nonnegative definite. It follows that and are positive as well. Hence, is also positive. ∎

Lemma 3.3.

For a given time grid and initial values , there exists at most one Nash equilibrium for mean-variance optimization.

Now we are ready to prove Theorem 2.4.

Proof of Theorem 2.4.

By Definition 2.2 and Lemma 3.1, we have the following linear-quadratic optimization problem: for all ,

The constraint can be re-written as the linear equality constraint .

To solve this problem, we use the Lagrange multiplier theorem [4, pp. 276-283] to obtain for such that the optimal strategies satisfy the following necessary conditions:

| (19) |

We will show below that these equations are also sufficient for our optimization problem. Summing over in the first line of (19) yields

By Lemma 3.2, is an invertible matrix. Thus,

| (20) |

where we have used the second condition from (19) in the final step.

Now consider the first conditions in (19). Pick the equation, multiply by , and then subtract the other equations from it. We get

Further simplifications show that

The matrix is invertible by Lemma 3.2. If follows that

| (21) |

where .

Now we show that the equations (19) are sufficient for the minimization of our mean-variance functional. To this end, we rewrite the objective mean-variance functional as follows:

where . Next, for , we consider arbitrary . Then, by (19),

| (22) |

with equality if and only if . Altogether, we obtain that (10) defines the unique Nash equilibrium in .

Now we turn to CARA utility maximization. We first note that the cost functional is a Gaussian random variable if is a Bachelier model and the strategies are deterministic. Therefore, for ,

For , we clearly have

Therefore, mean-variance optimization and CARA utility maximization are equivalent when performed over the class of deterministic strategies. Next, suppose that the strategies are deterministic. Then it follows as in Theorem 2.1 of [19] that the maximizer of the functional over the class of all adapted strategies is deterministic. That is, the maximization of over is equivalent to the maximization over . Therefore, it now follows as in the proof of Corollary 2.1 of [21] that the strategies (10) form a Nash equilibrium for CARA utility maximization.∎

Proof of Proposition 2.9.

Let us define a vector by for and . Then the assertion will follow if

| (23) |

with . To this end, we note that, with denoting the Kronecker delta,

Since , we have

This proves (23) and hence the assertion. ∎

Now we prepare for the proof of Theorem 2.11.

Lemma 3.4.

For , the following equation has a unique positive solution ,

| (24) |

Moreover, .

Proof.

By rearranging equation (24) we get

| (25) |

Clearly, when , then . Therefore, if a zero of exists, it must be within . One easily sees that

Hence, admits at least one zero in . Moreover,

and so the zero must be unique. ∎

Lemma 3.5.

Suppose that and . Then the following equation has a unique positive solution ,

| (26) |

Proof.

Let

Clearly,

| (27) |

Hence, there exists at least one zero in . Next, we look at

Note that if

Here, is strictly decreasing and bounded below by because for all ,

and because by L’Hôpital’s Rule,

Therefore, we have two cases to consider:

-

1.

when , we have that for all . It follows that there exists a unique such that ;

-

2.

when , we can always find a unique such that for and for . In other words, is the global maximum of on . Now suppose . We know that is strictly decreasing on , then for all , , which contradicts (27). Therefore, , and for all , which implies a zero cannot exist in . Since is strictly increasing on , it follows that there exists a unique such that .

In either case, there exists a unique positive solution that solves (26). ∎

Proof of Theorem 2.11.

Next, let be as provided by Lemma 3.4 and define a vector by

We will now show that

| (28) |

where is the sequence . Using our assumption , we get that

Expanding the center term gives,

Thus,

where we have used and our equation (24) in the final step. This establishes (28). Now we can define

which satisfies the equivalent of (8) in our setting with infinite time horizon.

Let us now deal with the vector . To this end, we take as provided by Lemma 3.5 and define by . Then

It follows that we can define

which satisfies the equivalent of (9) in our setting with infinite time horizon.

Finally, if initial positions are given, and we define via (16), then it is straightforward to verify that of the first-order conditions (19) are verified with our current choices for , , , and . As in (22), these yield that form a Nash equilibrium for mean-variance optimization. As in the proof of Theorem 2.4, one then concludes that this is also a Nash equilibrium for CARA utility maximization. ∎

References

- [1] A. Alfonsi, A. Fruth, and A. Schied. Constrained portfolio liquidation in a limit order book model. Banach Center Publications, 83:9–25, 2008.

- [2] A. Alfonsi, A. Schied, and A. Slynko. Order book resilience, price manipulation, and the positive portfolio problem. SIAM J. Financial Math., 3:511–533, 2012.

- [3] R. Almgren and N. Chriss. Optimal execution of portfolio transactions. Journal of Risk, 3:5–39, 2000.

- [4] D. P. Bertsekas. Nonlinear programming. Athena Scientific Optimization and Computation Series. Athena Scientific, Belmont, MA, second edition, 1999.

- [5] D. Bertsimas and A. Lo. Optimal control of execution costs. Journal of Financial Markets, 1:1–50, 1998.

- [6] M. K. Brunnermeier and L. H. Pedersen. Predatory trading. Journal of Finance, 60(4):1825–1863, August 2005.

- [7] B. I. Carlin, M. S. Lobo, and S. Viswanathan. Episodic liquidity crises: cooperative and predatory trading. Journal of Finance, 65:2235–2274, 2007.

- [8] R. Carmona. Lectures on BSDEs, stochastic control, and stochastic differential games with financial applications, volume 1 of Financial Mathematics. Society for Industrial and Applied Mathematics (SIAM), Philadelphia, PA, 2016.

- [9] R. A. Carmona and J. Yang. Predatory trading: a game on volatility and liquidity. Preprint, 2011.

- [10] P. Casgrain and S. Jaimungal. Algorithmic trading with partial information: A mean field game approach. arXiv:1803.04094, 2018.

- [11] CFTC-SEC. Findings regarding the market events of May 6, 2010. Report, 2010.

- [12] J. Gatheral. No-dynamic-arbitrage and market impact. Quant. Finance, 10:749–759, 2010.

- [13] J. Gatheral and A. Schied. Dynamical models of market impact and algorithms for order execution. In J.-P. Fouque and J. Langsam, editors, Handbook on Systemic Risk, pages 579–602. Cambridge University Press, 2013.

- [14] G. Huberman and W. Stanzl. Price manipulation and quasi-arbitrage. Econometrica, 72(4):1247–1275, 07 2004.

- [15] J. Lorenz and R. Almgren. Mean-variance optimal adaptive execution. Appl. Math. Finance, 18(5):395–422, 2011.

- [16] C. C. Moallemi, B. Park, and B. Van Roy. Strategic execution in the presence of an uninformed arbitrageur. Journal of Financial Markets, 15(4):361 – 391, 2012.

- [17] A. Obizhaeva and J. Wang. Optimal trading strategy and supply/demand dynamics. Journal of Financial Markets, 16:1–32, 2013.

- [18] G. Pólya. Remarks on characteristic functions. In J. Neyman, editor, Proceedings of the Berkeley Symposium of Mathematical Statistics and Probability, pages 115–123. University of California Press, 1949.

- [19] A. Schied, T. Schöneborn, and M. Tehranchi. Optimal basket liquidation for CARA investors is deterministic. Applied Mathematical Finance, 17:471–489, 2010.

- [20] A. Schied, E. Strehle, and T. Zhang. High-frequency limit of Nash equilibria in a market impact game with transient price impact. SIAM J. Financial Math., 8(1):589–634, 2017.

- [21] A. Schied and T. Zhang. A state-constrained differential game arising in optimal portfolio liquidation. Math. Finance, 27(3):779–802, 2017.

- [22] A. Schied and T. Zhang. A market impact game under transient price impact. Mathematics of Operations Research, 44(1):102–121, 2019.

- [23] T. Schöneborn. Trade execution in illiquid markets. Optimal stochastic control and multi-agent equilibria. Doctoral dissertation, TU Berlin, 2008.

- [24] T. Schöneborn and A. Schied. Liquidation in the face of adversity: stealth vs. sunshine trading. SSRN Preprint 1007014, 2009.

- [25] E. Strehle. Optimal execution in a multiplayer model of transient price impact. Market Microstructure and Liquidity, 3(4):1850007, 2017.

- [26] W. H. Young. On the Fourier series of bounded functions. Proceedings of the London Mathematical Society (2), 12:41–70, 1913.