Optimal sustainable harvesting of populations in random environments

Abstract.

We study the optimal sustainable harvesting of a population that lives in a random environment. The novelty of our setting is that we maximize the asymptotic harvesting yield, both in an expected value and almost sure sense, for a large class of harvesting strategies and unstructured population models. We prove under relatively weak assumptions that there exists a unique optimal harvesting strategy characterized by an optimal threshold below which the population is maintained at all times by utilizing a local time push-type policy. We also discuss, through Abelian limits, how our results are related to the optimal harvesting strategies when one maximizes the expected cumulative present value of the harvesting yield and establish a simple connection and ordering between the values and optimal boundaries. Finally, we explicitly characterize the optimal harvesting strategies in two different cases, one of which is the celebrated stochastic Verhulst Pearl logistic model of population growth.

Key words and phrases:

Ergodic control; stochastic harvesting; ergodicity; stochastic logistic model; stochastic environment2010 Mathematics Subject Classification:

92D25, 60J70, 60J601. Introduction

When trying to establish the best harvesting policy of a certain species, one needs to take into account both the biological and economic implications. It is well known that overharvesting might lead to the extinction of whole populations (see [Cla10, Gul71, Pri06, LES95]). Many species of animals (birds, mammals, and fish) are endangered because of unrestricted harvesting or hunting. In some instances people have overestimated the population density of a certain species, and since it takes a while for a harvested population to recover to previous levels, this has led to either local or global extinctions. However, if we underharvest a species, this can lead to the loss of valuable resources. We are therefore presented with a conundrum: should we overharvest and gain economically but possibly drive a species extinct or should we underharvest to make sure extinction is less likely but lose precious resources? We present a model and a harvesting method which give us, based on a rigorous mathematical analysis, the best possible sustainable harvesting policy that does not drive the species extinct.

We study a population whose dynamics is continuous in time and that is affected by both biotic (competition) and abiotic (rainfall, temperature, resource availability) factors. Since the abiotic factors are affected by random disturbances, we look at a model that has environmental stochasticity. This transforms a system that is modeled by an ordinary differential equation (ODE) into a system that is modeled by a stochastic differential equation (SDE). We refer the reader to [Tur77] for a thorough discussion of environmental stochasticity.

We build on the results from [AES98, AE01] and [HNUW18]. Suppose that in an infinitesimal time we harvest a quantity where is any adapted, non-negative, non-decreasing, and right continuous process. We determine the optimal harvesting strategy maximizing the expected average asymptotic yield

of harvested individuals. As in [HNUW18], and in contrast to what happens in a significant part of the literature (see [LES94, LES95, AES98, LØ97]), the optimal strategy will be such that the population is never depleted and cannot be harvested to extinction. This is clear since if in some sense then in the above equation. Our main result is that the optimal harvesting strategy is of the local time reflection type: the population is kept in the interval at all times by first harvesting and then harvesting only when the population hits the boundary just enough to maintain the population density below . This result was conjectured in [HNUW18] where the authors showed that if the harvesting rate is bounded the optimal strategy is of bang-bang type i.e. there is a threshold such that if the population size is under there is no harvesting while if the population size is above we harvest according to the maximal rate . If one works with discounted yields like in [AES98], then interestingly the optimal harvesting strategy is also of this local time reflection type. In our setting the diffusion governing the unharvested population is much more general than the one from [AES98] and [HNUW18] where the authors mostly work with a stochastic Verhulst-Pearl diffusion or its generalization. In the current paper we present a unifying result that encompasses a large variety of stochastic models.

Another advantage of our framework is that it does not depend on parameters that are hard to be quantified empirically. Many papers from the literature (see [AES98]) work with a time discounted yield in order to capture the opportunity cost of capital. However, it is a difficult question to come up with a good value for the discount factors (see [DS87]). Moreover, as [LES94] state in their influential paper focusing on the relationship between discounting and extinction risk:

“Thus, even when the discount rate is less than the critical value predicted by deterministic models, the economically optimal strategy will often be immediate harvesting to extinction. These results make a powerful a argument that, for the common good, economic discounting should be avoided in the development of optimal strategies for sustainable use of biological resources.”

Our model does not involve any discount factors. We generalize the setting of [HNUW18] where the authors assumed the harvesting rate was bounded by some parameter . This corresponds to having total control over the harvested population. Moreover, it also side-steps needing to know the parameter which could be hard to estimate realistically.

The paper is organized as follows. In Section 2 we introduce the model and prove the main results. Section 3 showcases how our model relates to the discounted model from [AES98, AE01]. In particular we show that by letting the discount rate go to zero, , we can recover in a sense the results of this paper. In Section 4 we look at two explicit applications of our results. As a first application we look at the Verhulst-Pearl diffusion model studied in [AES98, HNUW18]. The second model we analyze is the one studied in [AE00, LØ97]. Finally, Section 5 is dedicated to a discussion of our results.

2. Model and Results

We consider a population whose density at time follows, in the absence of harvesting, the stochastic differential equation (SDE)

| (2.1) |

where is a standard one dimensional Brownian motion. This describes a population with per-capita growth rate given by and infinitesimal variance of fluctuations in the per-capita growth rate given by when the density is . We make the following standing assumption throughout the paper.

Assumption 2.1.

The functions are continuous and satisfy the Engelbert-Schmidt conditions:

These conditions ensure the existence and uniqueness of weak solutions to (2.1) (see for example [ES91]). In addition, we want the population to persist in the absence of harvesting and to not explode to infinity (which would be absurd from a biological point of view). To this end we will assume throughout our analysis that the boundaries of the state space of the population density are unattainable (i.e. either natural or entrance) for in the absence of harvesting. This means that even though the process may tend towards a boundary it will never attain it in finite time. We refer the reader to Section II.6 from [BS15] for a thorough discussion of the boundary classification of one-dimensional diffusions.

We denote the density of the scale function of by

| (2.2) |

where is an arbitrary constant. The density of the speed measure is, in turn, denoted by

| (2.3) |

The second order differential operator

| (2.4) |

is the infinitesimal generator of the underlying diffusion .

For most harvesting applications it is sufficient to make the following assumption.

Assumption 2.2.

-

(A1)

The function is nonincreasing and fulfills the limiting conditions and for some .

-

(A2)

The function has a unique maximum point so that is increasing on and decreasing on .

-

(A3)

for .

Remark 2.1.

It is worth pointing out that assumption (A1) guarantees that the per-capita growth rate vanishes at some given point . In typical population models this point coincides with the carrying capacity of the population. We naturally have that .

Condition (A3) is needed for the existence of a stationary distribution for the process . Under our boundary assumptions, it guarantees that is repelling for and the condition , for , is satisfied (cf. p. 234 in [KT81]).

A stochastic process taking values in is said to be an admissible harvesting strategy if is non-negative, nondecreasing, right continuous, and adapted to the filtration generated by the driving Brownian motion . We denote the class of all admissible harvesting strategies (or controls) by . Assume that and that at time we harvest in the infinitesimal period an amount . Then our harvested population’s dynamics is given by

| (2.5) |

We consider the following ergodic singular control problem:

| (2.6) |

We are interested (as in [HNUW18]) in the maximization of the expected asymptotic harvesting yield (also called the expected average cumulative yield) of the population.

Before presenting our main findings on the optimal ergodic harvesting strategy and the maximal expected average cumulative yield we first establish the following auxiliary verification lemma.

Lemma 2.1.

Let be a given positive constant and assume that is a twice continuously differentiable function satisfying the inequalities and for all . Then

for all .

Proof.

Applying the generalized Itô-Döblin (see [Har85]) change of variable formula to the nonnegative function yields

where denotes the continuous part of an arbitrary admissible harvesting strategy , , and is a sequence of finite stopping times converging to as . Reordering terms and taking expectations shows that

Imposing now the inequalities and demonstrates that

Letting and applying Fatou’s lemma then finally yields

from which the alleged results follow. ∎

It is natural to ask if there is a function and a constant satisfying the conditions of Lemma 2.1. In order to show that the answer to this question is positive, we now follow the seminal paper [Kar83] and investigate the following question: can we find two constants and a twice continuously differentiable function satisfying the conditions

| (2.7) | ||||

Using (2.4) we get

The last equality, together with the boundary condition , yields that

| (2.8) |

Invoking the twice continuous differentiability of across the boundary , and noting that then shows that the constants are the solutions of the system

| (2.9) |

We can now establish the following.

Lemma 2.2.

Proof.

We first show that the optimality conditions (2.9) have a unique solution under our assumptions. To this end we investigate the behavior of the continuous function defined by

Making use of Assumption (A3) guarantees that

Therefore, we can express as

It is clear that and

demonstrating, using the intermediate value theorem, that has at least one root . To prove that the root is unique, we notice that if , then

Hence, if then proving that is strictly decreasing on . If, in turn, then proving that is strictly increasing on . Combining these observations with the continuity of and the fact that then proves that the root is unique and, consequently, that a unique pair exists. Moreover, since

we get that

and

Remark 2.2.

Lemma 2.2 also shows that the function satisfying the considered free boundary value problem is concave on . This property is later shown to be the principal determinant of the sign of the impact of increased volatility on the optimal harvesting policy and the expected average cumulative yield.

Lemma 2.2 essentially shows that if there is an admissible harvesting strategy resulting into a value satisfying the variational inequalities of Lemma 2.1, then the value of that policy dominates the value of the maximal expected average cumulative yield. Naturally, if we could determine an admissible policy yielding precisely the value characterized in Lemma 2.2 then that policy would automatically constitute the optimal harvesting policy. This is accomplished in the following theorem summarizing our main result on the optimal sustainable harvesting policy.

Theorem 2.1.

Suppose Assumptions 2.1 and 2.2 hold and . The optimal harvesting strategy is

| (2.10) |

where is the local time push of the process at the boundary (cf. [Har85, Kar83, SLG84]). The optimal harvesting boundary as well as the maximal expected average asymptotic yield are the solutions of the optimality conditions

Moreover,

Proof.

It is clear that the proposed harvesting strategy is admissible. Our objective is now to show that this policy attains the maximal expected average cumulative yield and is, therefore, optimal. To show that this is indeed the case, we first notice that the harvesting policy is continuous on , increases only when , and maintains the process in for all ([Har85, Kar83, SLG84]). In this case (2.5) can be re-expressed as

The continuity of the diffusion coefficient now guarantees that is bounded for all and, therefore, that

Consequently,

Since we notice that the process is ergodic and has an invariant probability measure (cf. [BS15], pp. 37-38). Hence,

demonstrating the optimality of the proposed policy. ∎

Remark 2.3.

It is worth noticing that since (cf. pp. 36–38 in [BS15])

our findings are in line with observations based on renewal theoretic approaches to ergodic control (cf. Chapter 5 in [Har85]). On the other hand we also observe that

where denotes the population density in the absence of harvesting and as . Consequently, the same conclusion could be obtained by focusing on the ergodic limit of the process controlled by .

Theorem 2.1 demonstrates that the optimal harvesting policy is of the standard local time push type in the ergodic control setting as well. Consequently, under the optimal harvesting policy the population is maintained below an optimal threshold by harvesting (in an infinitely intense fashion) only at instants when the population hits the optimal boundary. Below the critical threshold the population is naturally left unharvested.

One may wonder wether the findings of Theorem 2.1 could be extended further to a setting focusing on the almost sure maximization problem

| (2.11) |

This is an almost sure statement, compared to the maximization from (2.6) which deals with expected values. In order to delineate general circumstances under which the almost sure maximization problem admits a local time push type solution, we initially analyze the problem by focusing solely on this type of harvesting policies. Our main findings on that class is established in the next proposition.

Proposition 2.1.

Let be an arbitrary local time push type harvesting policy maintaining the population density on for all . Then, for any

| (2.12) |

Consequently,

| (2.13) |

Proof.

Let be an arbitrary finite boundary and consider the policy maintaining the population density in for all . As in the case of Theorem 2.1, the policy is continuous on and increases only when . Moreover,

| (2.14) |

Since for all one trivially has

| (2.15) |

with probability . Since the controlled process is ergodic on and has an invariant probability measure . Invoking the ergodic results from [BS15] (pp. 37-38) shows that almost surely

| (2.16) |

Let . Then is a local martingale with quadratic variation . By the ergodic results from [BS15], one has that almost surely

This combined with the Law of Large Numbers for local martingales (see Theorem 1.3.4 from [Mao97]) yields that almost surely

| (2.17) |

Using (2.15), (2.16) and (2.17) in (2.14) we get that (2.12) holds almost surely. (2.13) then follows from Lemma 2.2. ∎

Proposition 2.1 shows that the local time push controls affect the dynamics of the controlled population density in a way where the almost sure asymptotic average cumulative harvest can be computed explicitly in terms of the exogenous harvesting boundary. Since this representation is valid for all local time push controls, we find that choosing the threshold according to the rule maximizing the long run expected average cumulative harvest results in a maximal representation in this setting as well. Given the generality of admissible harvesting strategies, it is a challenging task to prove a general verification lemma analogous to Lemma 2.1. Fortunately, there is a relatively large class of processes for which the desired result is valid. To see that this is indeed the case, we first establish the following auxiliary result.

Lemma 2.3.

Proof.

This is a modification of the arguments from the seminal papers [Yam73] and [IW77] for the comparison of one-dimensional diffusions and the paper [Yan86] for the comparison of semimartingales. For small define the process via

Assume that . By [IW77] we see that almost surely

By the pathwise uniqueness of solutions of (2.1), combined with the continuity of we have almost surely that

We note that the semimartingales and satisfy the assumptions of Theorem 1 from [Yan86]. Therefore, if , we have that almost surely

Taking the limit as we get

which finishes the proof. ∎

Remark 2.4.

We make two remarks on the assumptions needed in Lemma 2.3. First of all, sufficient conditions for pathwise uniqueness of solutions can be found, for example, in [IW89, Kal02, Mao97]. Second, for most models of natural resources for some . In those cases the required growth condition is satisfied by simply taking .

Lemma 2.3 states a set of conditions under which the solution of the uncontrolled dynamics (2.1) dominates the solution of the dynamics subject to harvesting (2.5). It is worth pointing out that similar comparison results have been previously established for Lipschitz-continuous coefficients (see Theorem 54 in [Pro05]). However, that result does not directly apply to our setting, since most applied population models have only locally Lipschitz-continuous coefficients. Given our findings in Lemma 2.3 we can now establish the following Theorem which extends our results on the expected average cumulative yield to the almost sure setting.

Theorem 2.2.

Assume that Assumptions 2.1 and 2.2 hold, that (2.1) has pathwise unique solutions, that there exists an increasing function such that and , and that

-

(1)

The process from (2.1) has a unique invariant probability measure on .

-

(2)

One can find a twice continuously differentiable function satisfying the variational inequalities and for all .

-

(3)

The function is non-decreasing and square-integrable with respect to the speed measure of .

Then for any admissible strategy and any

| (2.18) |

Moreover,

| (2.19) |

for all and all .

Proof.

It is clear that for any admissible policy we have

| (2.20) |

The local martingale

has quadratic variation

By our assumptions and Lemma 2.3 we have almost surely that

Then, almost surely

By the ergodic results from [BS15] and the assumptions of the proposition, one has that almost surely

The Law of Large Numbers for local martingales (see Theorem 1.3.4 from [Mao97]) yields that almost surely

If we combine this with (2.20) we get

Finally, inequality (2.19) follows from (2.18) and (2.13). ∎

Remark 2.5.

We make the following three remarks on the assumptions (1)-(3) needed in Theorem 2.2.

-

(a)

If are unattainable and not attracting, i.e. for any we have , and then has a unique invariant probability measure with density on . In terms of boundary behavior the points can be entrance or natural, and the natural boundaries have to be non-attracting.

-

(b)

We note that the function defined in (2.8) satisfies and .

-

(c)

Checking condition (6) reduces to looking at the function

(2.21) verifying that it is non-decreasing, and then checking whether .

Remark 2.6.

Our work is related to [JZ06] where the authors consider the more general case where there are two controls. Consider the controlled diffusion

where is a right-continuous process with left limits that has finite variation and is adapted. Fix a starting point . The paper [JZ06] is concerned with the the minimization of

and the almost sure minimization of

Here is a given function that models the running cost resulting from the system’s operation, while are given functions penalizing the expenditure of control effort. We note that one of their assumption is that , which is more restrictive than what we have since in most population models .

Our main result on the sign of the relationship between volatility and the optimal harvesting strategy is summarized in the following.

Theorem 2.3.

Increased volatility increases the optimal harvesting threshold and decreases the long run average cumulative yield .

Proof.

Denote by the optimal harvesting threshold and by the maximal expected average cumulative yield associated with the more volatile dynamics characterized by the diffusion coefficient for all and let

denote the differential operator associated with the more volatile process. Let be the solution of the free boundary problem (2.7). Because we get

for all . Since we also have we notice by combining Theorem 2.1 and Lemma 2.2 that . However, since , , and the optimal harvesting threshold is on the set where the drift is decreasing, we find which completes the proof of our claim. ∎

3. Discounting and Harvesting: Connecting the Harvesting Problems

The previous section focused on the optimal ergodic harvesting policy maximizing the expected (or almost sure) long-run average cumulative yield. It is naturally of interest to analyze in which way the optimal policy differs form the optimal policies suggested by models maximizing the expected present value of the cumulative yield. To this end, let (cf. [AE01])

| (3.1) |

denote the value of the harvesting policy maximizing the expected present value of the cumulative yield. Our objective is to characterize how the different problems are connected by relying on an Abelian limit result first developed within singular stochastic control in the seminal paper [Kar83] (see also [Wee07] for a generalization).

In order to present our main findings on the connection between the two different approaches we first have to make a set of assumptions guaranteeing that the harvesting policy maximizing the expected present value of the cumulative yield is nontrivial. Define the function by

where denotes the prevailing discount rate. In addition to our assumptions on the boundary behavior of the population dynamics stated in Section 2 we now assume the following.

Assumption 3.1.

The function satisfies

-

(B1)

and , where

-

(B2)

the function attains a unique maximum at , where .

As was established in [AE01], one gets

| (3.2) |

The quantity denotes the increasing fundamental solution of the differential equation . The optimal harvesting boundary is the unique root of the ordinary first order optimality condition which can be re-expressed as

| (3.3) |

The value of the optimal harvesting policy is monotonically increasing, concave, and twice continuously differentiable. Moreover, increased volatility decreases the value of the optimal policy and expands the continuation region where harvesting is suboptimal by increasing the optimal harvesting boundary .

Under the optimal harvesting policy the population density converges in law to its unique stationary distribution. In other words, as . The random variable is distributed on according to the density

We can now establish the following limiting result

Lemma 3.1.

Proof.

The monotonicity of the admissible harvesting strategy guarantees that increased discounting decreases the value of the optimal policy. To see that it also accelerates harvesting by decreasing the optimal harvesting boundary we first observe that under our assumptions the conditions of Lemma 3.1 in [AE04] are met and, therefore,

| (3.4) |

for all . Reordering terms shows that (3.4) can be re-expressed as

| (3.5) |

On the other hand, if denotes the first hitting time to , then the identity (cf. p. 18 in [BS15])

guarantees that if then

for all . Since

we notice that

for all . Consequently, for all . Since and for all we notice that

implying that

and, therefore, that . This shows that higher discounting accelerates harvesting by decreasing the optimal threshold.

According to Lemma 3.1 higher discounting accelerates harvesting and results into a lower expected asymptotic population density. Interestingly, the optimal harvesting threshold approaches the one from the average cumulative yield setting as . It is clear that the same conclusion is not directly valid for the value of the optimal policy . However, there exists an Abelian limit connecting the value of the two seemingly different control problems. This connection is established in the following.

Theorem 3.1.

Under our assumptions,

for all .

4. Applications

4.1. Verhulst-Pearl diffusion

Assume that the unharvested population follows the standard Verhulst-Pearl diffusion

| (4.1) |

where is the per-capita growth rate at low densities, is the carrying capacity, and is the infinitesimal variance of fluctuations in the per-capita growth rate. In this case

and

Moreover, if is satisfied, then

We note that in this case Assumptions 2.1, 2.2 and the conditions of Theorem 2.2 hold (see [EHS15] for a thorough investigation of (4.1)). Consequently,

The optimal boundary reads as , where is the unique root of the equation

This shows that the optimal harvesting boundary is directly proportional to the carrying capacity.

As was shown in [AES98], in this case the harvesting boundary maximizing the expected present value of the cumulative yield constitutes the root of the equation , where denotes the prevailing discount rate,

denotes the Kummer confluent hypergeometric function,

and

We notice again that as in the ergodic setting, the optimal threshold is directly proportional to the carrying capacity.

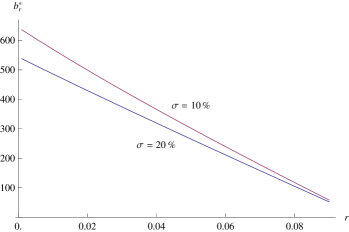

The optimal harvesting threshold is illustrated for two different volatilities as a function of the discount rate in Figure 1 under the assumptions that .

4.2. Logistic Diffusion

An alternative logistic population growth model was studied in [LØ97] and in [AE00]. The dynamics is characterized by the stochastic differential equation

| (4.2) |

As was established in [LØ97], this SDE has a unique strong solution defined for all . In this case we know that

and

Moreover, if is satisfied, then for any

where denotes the incomplete beta-function. One can see that in this setting Assumptions 2.1, 2.2 and the conditions of Theorem 2.2 hold. Consequently,

demonstrating that the optimal harvesting boundary is directly proportional to the carrying capacity in this case as well. Standard differentiation now shows that the harvesting threshold maximizing the expected average cumulative yield is where constitutes the unique root of the equation

As was shown in [AE00], in this case the harvesting boundary maximizing the expected present value of the cumulative yield is the unique solution of , where

is the standard hypergeometric function,

and

We notice again that, as in the ergodic setting, the optimal threshold is directly proportional to the carrying capacity.

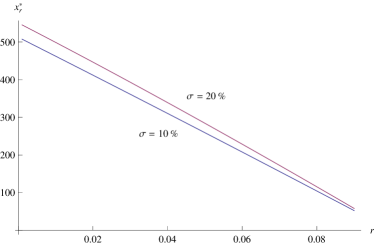

The optimal harvesting threshold is illustrated for two different volatilities as a function of the discount rate in Figure 2 under the assumptions that .

5. Discussion

We investigated the optimal ergodic harvesting strategies of a population whose dynamics is given by a general one-dimensional stochastic differential equation. The theory we develop for optimal sustainable harvesting includes the risks of extinction from evironmental fluctuations (environmental stochasticity) as well as from harvesting. However, in contrast to most of the literature, we do not work with discount factors (see [LES94, LES95, AES98, LØ97, AE00]) or maximal harvesting rates (see [HNUW18]). Instead, we concentrate on policies aiming to the maximization of the average cumulative yield. We proved that the optimal policy is of the same local time push type as in the discounted setting. Since the optimal threshold at which harvesting becomes optimal is a decreasing function of the prevailing discount rate, our results unambiguously demonstrate that policies based on ergodic (sustainable) criteria are more prudent and imply higher population densities than models subject to discounting. Our results show higher stochastic fluctuations negatively impact the population densities – this provides rigorous mathematical support for the arguments developed in [LES94] based on approximation arguments.

There are at least two directions in which our analysis could be extended. As was originally established in [Kar83] in a model based on controlled Brownian motion, the value of the optimal ergodic policy is associated with the value of the finite horizon control problem

where is a known fixed finite time horizon. It would be of interest whether an analogous limiting result connects to in the general setting.

The present analysis focuses on the harvesting of a single unstructured population. It would relevant to increasing the dimensionality of the considered model and introduce interactions into the dynamics governing the evolution of the population stock (see for example the population dynamics models from [HN18a, HN18b, SBA11]). In light of the studies [LOk01, ALOk16] this latter problem seems to be very challenging and is left for future considerations.

References

- [AE00] L. H. R. Alvarez E., Singular stochastic control in the presence of a state-dependent yield structure, Stochastic Process. Appl. 86 (2000), no. 2, 323–343. MR 1741811

- [AE01] Luis H. R. Alvarez E., Singular stochastic control, linear diffusions, and optimal stopping: a class of solvable problems, SIAM J. Control Optim. 39 (2001), no. 6, 1697–1710.

- [AE04] L. H. R. Alvarez E., A class of solvable impulse control problems, Applied Mathematics and Optimization 49 (2004), 265–295.

- [AES98] L. H. R. Alvarez E. and L. A. Shepp, Optimal harvesting of stochastically fluctuating populations, J. Math. Biol. 37 (1998), no. 2, 155–177. MR 1649508

- [ALOk16] Luis H. R. Alvarez, Edward Lungu, and Bernt Ø ksendal, Optimal multi-dimensional stochastic harvesting with density-dependent prices, Afr. Mat. 27 (2016), no. 3-4, 427–442.

- [BS15] A. N. Borodin and P. Salminen, Handbook of brownian motion-facts and formulae, Birkhäuser, 2015.

- [Cla10] C. W. Clark, Mathematical bioeconomics, third ed., Pure and Applied Mathematics (Hoboken), John Wiley & Sons, Inc., Hoboken, NJ, 2010, The mathematics of conservation. MR 2778605

- [DS87] J. Drèze and N. Stern, The theory of cost-benefit analysis, Handbook of public economics 2 (1987), 909–989.

- [EHS15] S. N. Evans, A. Hening, and S. J. Schreiber, Protected polymorphisms and evolutionary stability of patch-selection strategies in stochastic environments, J. Math. Biol. 71 (2015), no. 2, 325–359. MR 3367678

- [ES91] H. J. Engelbert and W. Schmidt, Strong markov continuous local martingales and solutions of one-dimensional stochastic differential equations (part iii), Mathematische Nachrichten 151 (1991), no. 1, 149–197.

- [Gul71] J. A. Gulland, The effect of exploitation on the numbers of marine animals, Proc. Adv. Study, Inst. Dynamics Numbers Popu (1971), 450–468.

- [Har85] J. M. Harrison, Brownian motion and stochastic flow systems, Wiley, New York, 1985.

- [HN18a] A. Hening and D. Nguyen, Coexistence and extinction for stochastic Kolmogorov systems, Annals of Applied Probability 28 (2018), no. 3, 1893–1942.

- [HN18b] by same author, Stochastic Lotka-Volterra food chains, J. Math. Biol. 77 (2018), no. 1, 135–163.

- [HNUW18] A. Hening, D. H. Nguyen, S. C. Ungureanu, and T. K. Wong, Asymptotic harvesting of populations in random environments, Journal of Mathematical Biology (2018), to appear.

- [IW77] N. Ikeda and S. Watanabe, A comparison theorem for solutions of stochastic differential equations and its applications, Osaka Journal of Mathematics 14 (1977), no. 3, 619–633.

- [IW89] N. Ikeda and S. Watanabe, Stochastic differential equations and diffusion processes, North-Holland Publishing Co., Amsterdam, 1989.

- [JZ06] A. Jack and M. Zervos, A singular control problem with an expected and a pathwise ergodic performance criterion, Journal of Applied Mathematics and Stochastic Analysis (2006), 1–19.

- [Kal02] O. Kallenberg, Foundations of modern probability, Springer, 2002.

- [Kar83] I. Karatzas, A class of singular stochastic control problems, Advances in Applied Probability 15 (1983), no. 2, 225–254.

- [KT81] Samuel Karlin and Howard M. Taylor, A second course in stochastic processes, Academic Press, Inc. [Harcourt Brace Jovanovich, Publishers], New York-London, 1981.

- [LES94] R. Lande, S. Engen, and B.-E. Sæther, Optimal harvesting, economic discounting and extinction risk in fluctuating populations, Nature 372 (1994), 88–90.

- [LES95] by same author, Optimal harvesting of fluctuating populations with a risk of extinction, The American Naturalist 145 (1995), no. 5, 728–745.

- [LØ97] E. M. Lungu and B. Øksendal, Optimal harvesting from a population in a stochastic crowded environment, Math. Biosci. 145 (1997), no. 1, 47–75. MR 1478875

- [LOk01] Edward Lungu and Bernt Ø ksendal, Optimal harvesting from interacting populations in a stochastic environment, Bernoulli 7 (2001), no. 3, 527–539.

- [Mao97] X. Mao, Stochastic differential equations and their applications, Horwood Publishing Series in Mathematics & Applications, Horwood Publishing Limited, Chichester, 1997. MR 1475218

- [Pri06] R. B. Primack, Essentials of conservation biology, Sunderland, Mass: Sinauer Associates, 2006.

- [Pro05] Philip E. Protter, Stochastic integration and differential equations, Stochastic Modelling and Applied Probability, vol. 21, Springer-Verlag, Berlin, 2005, Second edition. Version 2.1, Corrected third printing.

- [SBA11] S. J. Schreiber, M. Benaïm, and K. A. S. Atchadé, Persistence in fluctuating environments, J. Math. Biol. 62 (2011), no. 5, 655–683. MR 2786721

- [SLG84] S.E. Shreve, J.P. Lehoczky, and D.P. Gaver, Optimal consumption for general diffusion with absorbing and reflecting barriers, SIAM Journal on Control and Optimization 22 (1984), 55–75.

- [Tur77] M. Turelli, Random environments and stochastic calculus, Theoretical Population Biology 12 (1977), no. 2, 140–178.

- [Wee07] Ananda Weerasinghe, An abelian limit approach to a singular ergodic control problem, SIAM J. Control Optim. 46 (2007), no. 2, 714–737.

- [Yam73] Toshio Yamada, On a comparison theorem for solutions of stochastic differential equations and its applications, J. Math. Kyoto Univ. 13 (1973), 497–512.

- [Yan86] J. Yan, A comparison theorem for semimartingales and its applications, Séminaire de Probabilités, XX, Lecture Notes in Mathematics 1204 (1986), 349–351.