This paper develops an inferential theory for state-varying factor models of large dimensions. Unlike constant factor models, loadings are general functions of some recurrent state process. We develop an estimator for the latent factors and state-varying loadings under a large cross-section and time dimension. Our estimator combines nonparametric methods with principal component analysis. We derive the rate of convergence and limiting normal distribution for the factors, loadings and common components. In addition, we develop a statistical test for a change in the factor structure in different states. We apply the estimator to U.S. Treasury yields and S&P500 stock returns. The systematic factor structure in treasury yields differs in times of booms and recessions as well as in periods of high market volatility. State-varying factors based on the VIX capture significantly more variation and pricing information in individual stocks than constant factor models.

Keywords: Factor Analysis, Principal Components, State-Varying, Nonparametric, Kernel-Regression, Large-Dimensional Panel Data, Large and

JEL classification: C14, C38, C55, G12

1 Introduction

Factor models provide an appealing way to summarize information from large data sets. In factor models, a small number of latent common factors explain a large portion of the co-movements. They have been successfully used in finance, e.g. Ross (1976), Chamberlain and Rothschild (1983) and Ludvigson and Ng (2009), and in macro-economics, e.g. Stock and Watson (2002) and Jurado, Ludvigson, and Ng (2015). Large dimensional factor models typically assume that the underlying factor structure does not change over time, that is, the factor loadings capturing the exposure to factors are assumed to be constant over time as for example in Bai and Ng (2002), Bai (2003) and Fan, Liao, and Mincheva (2013).111Extensions of the constant loading model include sparse and interpretable latent factors in Pelger and Xiong (2020), estimation from incomplete data sets in Xiong and Pelger (2020) and including additional moments to estimate weak factors as in Lettau and Pelger (2020a, b). However, since financial and macroeconomic data sets often span a long time period, it can be overly restrictive to assume a constant exposure to factors. Over a long time horizon, domestic and foreign policies change, business cycles occur, technology progresses, and agents’ preferences switch (Stock and Watson, 2009). Ignoring these changes can lead to a misspecified model with false inference and prediction (Breitung and Eickmeier, 2011).

This paper presents an inferential theory for state-varying factor models of large dimensions. Unlike constant-loading factor models, the loadings are general functions of some recurrent state process. We develop an estimator for the latent factors and state-varying loadings for a large number of cross-sectional and time observations. Our estimator combines nonparametric methods with principal component analysis (PCA). We derive the rate of convergence and asymptotic normal distribution for the estimated factors, loadings, and common components. We also develop a statistical test for the change of the loadings in different states.

Our state-varying model achieves two important goals: First, we can estimate the systematic factor structure conditioned on the outcome of a state variable. For example, we can estimate how the factor structure in asset prices depends on the business cycle.222Pelger (2020) provides empirical evidence for time-variation in latent factor models that is related to recessions. In particular, we can obtain the loadings as a general function of the state variable and use this insight for building economic models. Second, we can capture time variation in the systematic factor structure. The loadings in our model are time-varying because the state process changes over time. The dynamics of the state process and the functional form of loadings as a function of the state process jointly determine the dynamics of loadings over time. We allow for very general dynamics of the state process that include smooth processes but also discontinuous processes. Hence, our approach allows the loadings to change many times rapidly, but also covers the cases of a small number of large changes or many gradual changes. As we consider a very general functional form for the loading function, the loadings can vary more for particular state outcomes or even be constant for other outcomes of the state process.

Our approach combines kernel methods with PCA. The underlying idea is to estimate a large-dimensional covariance matrix conditioned on a recurrent state process and to analyze its spectral decomposition. For this purpose, we apply a kernel projection in the time dimension on a particular state value.333Fan, Liao, and Wang (2016) model loadings as non-linear functions of time-varying features of the cross-sectional units. Their estimation approach applies PCA to the data matrix that is projected in the cross-section on the subject-specific covariates. We also apply PCA to a projected data matrix, but our projection is applied in the time dimension. PCA is then applied to the projected data. Our estimator is easy to use and simple to implement. The inferential theory depends in a complex way on the kernel approximation and the number of cross-sectional and time-series observations.444In this paper, we consider a scalar state process and leave the extension to multivariate state processes to future research. We expect multivariate state processes to lead to lower convergence rates due to the “curse of dimensionality” inherent in higher-dimensional kernel projections. An additional challenge is that many multivariate state processes do not have the recurrence property. The theoretical framework for the factor estimation is closely related to Bai (2003)’s and Su and Wang (2017)’s inferential theory of the PCA estimator. While Bai (2003) applies PCA to the unconditional covariance matrix, Su and Wang (2017) use the spot covariance matrix conditioned on a particular point in time. Our approach conditions on a particular realization of the state process. Conditioning on a state with a kernel projection significantly complicates the analysis as it leads to additional bias terms and a complex interplay between the number of time and cross-sectional observations and the kernel bandwidth. We characterize the general conditions that are sufficient for asymptotic consistency and a conditional normal distribution of the loadings, factors, and common components under the assumptions of an approximate factor model that has a similar level of generality as Bai (2003)’s framework.555Wang, Peng, Li, and Leng (2019) also study a state-dependent latent factor model. Their focus is the estimation of a large dimensional state-dependent covariance matrix, while we derive the inferential theory for the factors and conditional loadings.

We develop a novel test for changes in the loadings. Our test statistic allows us to answer the important question in which states loadings are different. The challenge comes from the fact that factor models can only be identified up to invertible linear transformations, and hence we cannot directly compare the loadings estimated for different states with each other. Our test statistic is based on a generalized correlation statistic, which measures how close the two vector spaces spanned by loadings in two states are.666Generalized correlations or canonical correlations have been studied in Anderson (1958), Yuan and Bentler (2000), Bai and Ng (2006), Pelger (2019) and Andreou, Gagliardini, Ghysels, and Rubin (2019) Testing the null hypothesis of the same loadings in two different state realizations turns out to be a “corner case” similar to unit root test statistics with a faster convergence rate than under the alternative hypothesis. The test statistic is non-standard and requires a novel bias correction, which we provide. We believe that the novel technique that we develop for our test statistic can also be easily adopted to the gradual change or high-frequency PCA models and will encourage further developments.777Our test differs from the existing tests, such as those of Breitung and Eickmeier (2011), Chen, Dolado, and Gonzalo (2014), Han and Inoue (2015), and Yamamoto and Tanaka (2015), which check the stability of the moments of factor loadings or common factors, but do not take invertible transformations into account. Our test takes a “micro” view to compare loadings in any two states, while Su and Wang (2017) takes a “global” view to test whether loadings change in the whole time dimension.

Our method can estimate the functional relationship between a time-varying state process and structural changes in the loadings, which adds additional economic interpretability to the model. We do not require a parametric form for the loadings as a function of the state process, which is potentially misspecified, but allow for a general functional relationship. Our approach allows us to study questions such as how a macroeconomic factor structure depends on the business cycle, while other approaches are more limited to study these types of questions: First, the magnitude of the changes might be too smooth to be captured as a large structural break. Second, there might not be sufficient local observations that are required in the local smoothing framework, which ignores the information that is contained in similar states of the business cycle.

Our framework generalizes the conventional constant loading factor models and allows for a more parsimonious representation of the data. Under certain assumptions, a factor model with state-dependent loadings can be approximated by a constant loading model with a larger number of latent factors. A more complex functional form of the state-dependent loadings typically requires more basis functions to approximate them and results in a larger number of latent factors in the constant loading approximation. Our state-varying factor model can require significantly fewer factors than a constant loading model to explain the same or more variation in the data. In this sense, our model provides a more parsimonious model. Furthermore, our estimator can be valid even if we observe the state process with noise or omit a relevant state. Our inferential theory is robust to moderate noise contamination in the state process. Even if we miss a relevant state or the noise contamination in the state process is more severe, our estimator can still dominate the conventional factor model approach. We only need to condition on a state process that depends on the source of variation in the loadings. We confirm this result in our simulation and empirical studies.

We show a strong state-dependent time variation in the factor structure of U.S. Treasury yields and S&P 500 stock returns. The yields of bonds with different maturities are well-explained by the three PCA factors commonly labeled as level, slope, and curvature factors.888See Diebold, Piazzesi, and Rudebusch (2005), Diebold and Li (2006), Cochrane and Piazzesi (2005) and Cochrane and Piazzesi (2009). We show that this factor structure depends on state variables such as recession and boom indicators, the stock market’s expectation of volatility (VIX), or the unemployment rate. We show that during recessions, in times of high volatility, or in times of a high unemployment rate, the first PCA factor, typically labeled as a level factor, becomes less dominant and shifts to longer-term bonds. However, the second and third PCA factors, labeled as slope and curvature factors, both shift more towards shorter-term bonds. These changes are statistically and economically significant and show that the economic interpretation of “level”, ”slope” and “curvature” has to be used with caution, as for different economic states, the PCA factors will be different. In the second application on individual stock returns, we show that a state-varying factor model with the VIX as the state variable is more parsimonious in explaining variation and captures more pricing information than the constant loading model. A constant loading model requires five more factors to explain the same amount of variation as our state-dependent factor model. At the same time, an optimal portfolio based on the state-varying factors earns out-of-sample a five times higher risk-adjusted return than the corresponding portfolio based on a constant loading model. Hence, even if we might not capture all time-variation in the loadings with the proposed state variable, we still obtain a model that explains the correlations structure and mean returns better than a constant loading model.

Our paper is complementary to the literature on structural breaks and local PCA estimation that pursue a related but different objective. Our goal is to provide a parsimonious model that allows for time variation due to an observable time-varying state process. The literature on structural breaks focuses on detecting and modeling a small number of large breaks in the latent factor structure. It includes Andrews (1993), Chen, Dolado, and Gonzalo (2014), Breitung and Eickmeier (2011), Cheng, Liao, and Schorfheide (2016), Baltagi, Kao, and Wang (2020), Bai, Han, and Shi (2020), Ma and Su (2018) and Barigozzi, Cho, and Fryzlewicz (2018).999Breitung and Eickmeier (2011) develop three test statistics for structural breaks. Chen, Dolado, and Gonzalo (2014) study the detection of large breaks in loadings through a two-stage procedure. Han and Inoue (2015) test for structural breaks by studying the stability in second moments. Yamamoto and Tanaka (2015) generalize Breitung and Eickmeier (2011)’s test. Cheng, Liao, and Schorfheide (2016) propose a test where both the factor loadings and the number of factors change simultaneously. Baltagi, Kao, and Wang (2020) and Bai, Han, and Shi (2020) estimate structural breaks with pseudo factors, Ma and Su (2018) propose a three-step approach with local estimates and Barigozzi, Cho, and Fryzlewicz (2018) estimate structural breaks with wavelets. A factor structure, that depends on a state process that jumps, exhibits structural breaks that we can detect reliably. Modeling a one-time large structural break may be inappropriate if changes happen smoothly, for example, policy changes or business cycles can lead to gradual changes. Moreover, the large structural break models are limited to a small number of changes. Re-occurring events, for example, changes in the business cycle and economic conditions, can lead to a large number of changes in the factor structure. The alternative approach is to model changes smoothly with a local estimator. Su and Wang (2017) and Eichler, Motta, and Von Sachs (2011) use a local kernel estimator in the time dimension to study gradual changes. This approach excludes sudden large changes and exploits only the data in a local neighborhood of a particular time observation. This problem can be overcome by using high-frequency data as in Pelger (2019, 2020), Ait-Sahalia and Xiu (2019, 2017), Kong (2017, 2018) and Kong and Liu (2018), that allows to make general statements about time-variation in large dimensional latent factor models. The idea is similar to the local PCA estimators, but the high-frequency data provides sufficient information to detect more rapid changes. However, appropriate high-frequency data is only available for a limited number of applications, e.g., high-frequency trading data for U.S. equity in the recent past. We show that if we have additional information about a state process, we can reliably model structural breaks or a local time-variation in a uniform framework. In fact, in this case, we can explain more structure in the data than the models based only on structural breaks or a local time-variation that are not taking advantage of this additional information. Importantly, neither the large structural break models nor the gradual change models provide a direct economic link of the change to underlying economic variables.

2 Model Overview

2.1 Setup

Assume a panel data set of time-series observations and cross-sectional observations, denoted as , has a factor structure with common factors. Let be the value of a state process at time , the cross-sectional observation at time , the latent factors at time , and the factor loadings of the cross-sectional unit when the state value is :

or in vector notation,

We observe and and want to estimate and in an asymptotic setup where and are both large. This model generalizes the large dimensional factor model in Bai and Ng (2002) and Bai (2003) and allows factor loadings to change over time. The loadings in our model are time-varying because the state process changes over time. The loadings are deterministic general functions of the state process that satisfy some smoothness conditions. The random state process itself has a continuous distribution.101010In contrast to other time-varying factor models, e.g., Bates, Plagborg-Møller, Stock, and Watson (2013), Cheng, Liao, and Schorfheide (2016), and Su and Wang (2017), our model directly incorporates the driving forces for the changes in loadings. Park, Mammen, Härdle, and Borak (2009) study a similar semiparametric factor model but require cross-sectional variation in the loadings to come from observable covariates, this means they estimate a function of observable covariates where is the same function for all . They apply B-splines to estimate the unknown loading function and estimate the factors with a Newton-Raphson algorithm. Our approach is based on a simple-to-implement PCA method, which allows us to derive an inferential theory.

2.2 Estimation Problem

We want to estimate the factor model conditioned on the state outcome . Before providing formal arguments, we will describe the intuition behind our approach. If the idiosyncratic component is conditionally uncorrelated with the factors, then the conditional second moment matrix equals

We will assume that the factors are systematic in the sense that they affect many cross-sectional units captured by a full rank assumption of for . Furthermore, the idiosyncratic component has conditionally only a weak dependency structure modeled by a sparsity assumption on the conditional residual covariance matrix. Hence, the largest eigenvalues of should come from the systematic part and the corresponding eigenvectors will be linked to the loadings . This motivates the application of PCA to the conditional second moment matrix to estimate the factor and loadings.111111If has a conditional mean of zero, PCA is applied to the conditional covariance matrix. The essential identification condition is the full rank of the conditional second moment matrix of the factors and of the limit loading matrix .

The conditional second moment matrix is estimated by a kernel projection of the data that puts higher weights on time observations where the state process takes values in a neighborhood of , i.e. we analyze with an appropriate diagonal matrix of kernel weights and bandwidth .121212The PCA estimation can either be applied to , in which case the eigenvectors are related to the transformed factors, or to , which relates the eigenvectors to the transformed loadings. The analysis is inherently complicated by the bias arising in any kernel estimation from using observations from nearby states. In more detail, the observations can be written as

The bias term behaves like an additional error term that requires a different treatment than the idiosyncratic error.

2.3 Identification Assumption

Unlike the conventional constant loading factor model there are two sources of time-variation in our model: the time-series of the factors and of the state process. This poses the inherent identification problem what is a factor and what is a state? We impose the identification assumption that the second factor moment does not depend on the state process to separate the state process from the latent factors. We denote the conditional and unconditional second factor moment by and respectively. is the implied stochastic process.

Assumption 1.

Identification Assumption: For all in the support of we assume that the conditional second factor moment does not depend on the state process and is positive definite: .

Note that the identification assumption is not limiting the generality of our model. Replacing the factors by and loadings by we can ensure that for any conditional factor model the assumption is satisfied. It is possible to relax the full-rank assumption, i.e. the number of systematic factors in different states can differ.

As in any PCA estimation problem the factors and state-varying loadings are only identified up to an invertible matrix which in our case can be state-varying, i.e. . We estimate the factors as the eigenvectors of the conditional second moment matrix. Our estimates coincide with the factors if and is diagonal. In the general case, the conditional eigenvectors estimate where is uniquely determined. This is a generalization of the standard assumption in the unconditional factor models that the estimated factors are the eigenvectors of the unconditional second moment and the estimated loadings are orthogonal.

We illustrate how Assumption 1 identifies the factors with a number of examples. For simplicity we consider in these examples only a one-factor model, but the extensions to more factors are straightforward. Assume that the cross-section is modeled by

We can either view this as a constant loading model () or a state-varying factor model. Both formulations are equally valid and will explain the same amount of variation. With the identification Assumption 1 we obtain the model (). It simplifies to () if is independent of .

If the systematic component of is a function of and , we can formulate it as

for some function . Assume that can be approximated well by a second-order Taylor approximation, i.e. we will model as a second-order polynomial function:

Thus, we can either formulate the model as a constant loading model with 6 factors or a state-varying loading model with 3 factors. Both formulations are equivalent in terms of explaining variation, but the state-varying model is more parsimonious. Assumption 1 separates the state process from the latent factor in the above formulation.

Next, we consider the same model but assume that is a third-order polynomial function based on a Taylor expansion:

Assumption 1 identifies a state-varying four-factor model which can equivalently be written as a 10 factor model with constant loadings. Hence, for a more complex functional relationship, the state-varying model is more parsimonious compared to the constant loading model. Note, that in the examples the loadings are a linear function of a finite number of transformations of the state process. Our focus is on the relevant model where we have a continuum of state outcomes and a non-linear loading function that requires a large number of basis functions for its approximation. In this case there exists in general no multi-factor representation with constant loadings.

2.4 Robustness to Misspecification

Our framework allows us to study conditional latent factors. The purpose can be to understand how the systematic dependency structure changes with some specific state variable or to have a parsimonious factor model that allows for time variation. In the second case, it is important to find the state variable that is the source of the time variation in the factor model. In practice, we might not know which state process attributes to changes in the loadings. In the Internet Appendix, we show that our results are still valid if we use a noisy approximation of the source of change:

The term is the time-varying component of the loading coefficient that cannot be explained by the state process . It can, for example, be due to a measurement error in the state process or an omitted additional state process that affects only a small number of loadings. We show that under mild assumptions, the term can be treated like an additional non-systematic error term that will not affect our results. In this sense, our model is robust to mild misspecification.

More generally, missing a relevant systematic state can be accounted for by including more latent factors. In this sense our model is also robust to more severe misspecification as we illustrate with the following example. Assume there are two state processes and that have a systematic effect, i.e. . If is a second order polynomial we have

which has equivalent representations as a 10-factor constant loading model, a 7-factor model conditioned on and a 3-factor model conditional on and . Hence, even if we do not condition on all relevant states or use a noisy approximation, the state-varying factor model can provide a more parsimonious representation than the constant loading version. We formalize this idea in the Internet Appendix.

3 Estimation

We estimate the factor model conditional on the realization of the state process . Our approach generalizes the conventional PCA estimator by using projected data. We first apply a kernel projection to calculate the second moment matrix conditioned on the state outcome . Second, we use PCA on the conditional second moment matrix to obtain the estimated factors and loadings for the state outcome . The estimated factors are the eigenvectors of the conditional second moment matrix. Loadings in state are the regression coefficients of the projected data on the estimated factors.

We estimate factors and loadings by minimizing the following criterion function

where and . can be interpreted as the effective number of time observations used to estimate the factor structure conditioned on a state value. denotes a kernel function. is a bandwidth parameter, which depends on how much information we want to use from the neighboring states and our prior knowledge about the smoothness of the loadings as a the function of the state process. We can think of as the average loss function conditioned on the state outcome . We reformulate the problem as a conventional least squares problem by projecting the data, factors and idiosyncratic components in the time dimension on the kernel: , and . The objective function can then be expressed as

where , ,

is a quadratic and convex loss function. Factors and loadings can be estimated up to some invertible rotation.131313If and are a solution minimizing , then which are invertible, and also minimize . After normalizing and concentrating out the loadings, the objective function becomes a conventional PCA problem:

The estimator equals times the eigenvectors of the largest eigenvalues of the matrix . is the diagonal matrix with diagonal elements equal to the largest eigenvalues in decreasing order of the matrix . The conditional loadings are estimated as , and the unconditional factors can be estimated for each state outcome as .

4 Assumptions

Let denote a generic constant. The matrix norm below is the Frobenius norm . We condition on the state outcome which is in the support of the distribution of the state process .

Assumption 2.

State and kernel function:

-

1.

The state process at time is observed and positive recurrent. is the stationary probability density function (PDF) of . is continuous and has first order bounded derivative.

-

2.

The kernel function is a symmetric, continuously differentiable and nonnegative function that has a compact support and exists.141414Many common kernels satisfy this Assumption: 1. Gaussian kernel . 2. Uniform kernel . 3. Epanechnikov kernel . 4. Biweight kernel (). 5. Triweight kernel ()). 6. Many higher order kernels obtained by multiplying them by a higher order polynomial in .

Under Assumption 2, is positive recurrent, implying the existence of a stationary distribution. The assumptions that is continuous and has first-order bounded derivative, implies a continuous state space for . For simplicity we assume that follows its stationary distribution for all , but it is straightforward to relax this assumption. It is sufficient that there exists a with such that . As a result it holds for all that . In the remainder of this paper, we estimate the factor model in the state with a stationary density greater than zero. Intuitively, this means that a neighborhood of any state can be visited infinitely many times in an infinite time horizon. Under this assumption, we show consistency for and jointly going to infinity. If the stationary distribution is continuous and has bounded first-order derivative, together with the kernel’s property, we can estimate the stationary distribution nonparametrically, which is as and .

This assumption implies that the state process can take infinitely many values, but it does not make an assumption about the dynamics of the state process.151515Many relevant state processes in economics and finance can be modeled with a continuous state space, e.g., inflation rates, growth rates, volatility processes or return processes. In this case, the state process takes infinitely many values. The state process can be a slowly changing process, or it can be an abruptly changing process, even with many jumps.

On the other hand, if the state process takes only finitely many values, we can separate the data by state values and estimate a factor model for each state with stationary probability greater than 0. This would be a special case of estimating the factor model from the data projected by a kernel, which has an indicator term, such as the uniform kernel, and picks an appropriate bandwidth . With some modifications of the proofs, the theorems hold.

Because the kernel function is symmetric and continuously differentiable, the bias in the nonparametric density estimator is of order , which is smaller than obtained from a non-symmetric kernel. In addition, the existence of a fourth moment of the kernel implies that the tail in the kernel cannot be too heavy. When we estimate the factor model in , we also use data in other states weighted by the kernel, which results in some biases in the estimator. Assumption 2.2 ensures that the bias can be controlled by the kernel weight and will not dominate in the limiting distribution of the estimators.

Assumption 3.

Conditional Factors: It holds , , where is the filtration of the state process, and as for some positive definite matrix .

Assumption 3 is the state-conditional version of assumption A in Bai (2003). The fourth moment of the factor is bounded both without and with the state filtration, which makes it possible to have asymptotic results for both unconditional and conditional estimated factors. This assumption implies that given any realization of the state process, the fourth moment of the factor cannot explode. The conditional covariance matrix of the factors needs to be positive definite, which implies that no factor is degenerated after being projected on a particular state outcome.

Assumption 4.

Factor Loadings:

-

1.

Factor loadings are deterministic functions of the state process. Furthermore, and , for some positive definite matrix .

-

2.

is deterministic and Lipschitz continuous in : There exist some constant , , and .

Assumption 4 ensures that, in every state, each factor has a nontrivial contribution to the variance of the data. The loadings are deterministic functions of the state process, which is a stochastic process. Therefore, the unconditional loadings are random, but conditional on the outcome of the state process, they are deterministic. The loadings are Lipschitz continuous with respect to the state, e.g., a differentiable function of the state with bounded first-order derivative. If the state process is bounded, most differentiable loading functions can satisfy this assumption. This assumption, together with the kernel assumption, guarantee that the bias generated from using data in neighboring states is not a leading term in the limiting distribution of the estimators.

Assumption 5.

Time and Cross Sectional Dependence and Heteroskedasticity:

There exists a positive constant such that for all and :

-

1.

. . and are independent.

-

2.

Weak time-series dependence: . , , and .

-

3.

Weak cross-sectional dependence: , with for some and for all .

-

4.

Weak total dependence: and .

-

5.

Bounded cross-sectional fourth moment correlation:

For every (t,u), . -

6.

Weak dependence between factors and idiosyncratic components:

-

(a)

Define . Then , and

and . -

(b)

Define . Then and

and .

-

(a)

Assumption 5 allows the unconditional idiosyncratic components to have weak time-series and cross-sectional dependences. Our model is an approximate static factor model similar to Bai and Ng (2002) and Bai (2003). For simplicity, we also assume the state process is independent of the idiosyncratic components. This assumption, together with weak time-series and cross-sectional unconditional dependence in the idiosyncratic components, implies that the idiosyncratic components can have weak time-series and cross-sectional dependence conditional on the state process. The last part assumes weak unconditional and conditional correlation between factors and idiosyncratic components. We state them separately because the factors and state process may be dependent.

Assumption 6.

Moments and Central Limit Theorem (CLT): There exists an , such that for any and for all , , and that satisfy , , , and ,

-

1.

Projected factors and idiosyncratic components:

,

where . -

2.

Projected factors, loadings and idiosyncratic components:

,

where . -

3.

CLT for loadings and idiosyncratic components:

where .

-

4.

CLT for projected factors and idiosyncratic components:

where ,

and -

5.

Loadings and projected idiosyncratic components:

, where

.

Assumption 6 are moment conditions and central limit theorems, which are satisfied by mixing processes of factors, loadings, and idiosyncratic components projected by the kernel function of the state process. This assumption is required only for asymptotic distribution results. The CLT for loadings and idiosyncratic components will be used to show the limiting distribution for estimated factors and common components. The CLT for projected factors and idiosyncratic components will be used to show the limiting distribution for estimated loadings and common components. Assumption 6.1, 6.2 and 6.5 allow for a weak conditional dependency between the idiosyncratic component and the factors and loadings. It is trivially satisfied if the idiosyncratic components are independent of the factors and loadings. The bandwidth parameter appears in the assumptions, which is used to balance the term in the denominator of the second moment of the kernel function. Intuitively, for a smaller bandwidth , we are using information from a smaller portion of the data, which lowers the convergence rate. We will discuss the rate conditions on , , and in more detail in the next section.

Assumption 7.

The eigenvalues of the matrix are distinct.

Factors and loadings can be estimated up to some rotation matrix, and this matrix can be uniquely determined by Assumption 7.161616In general, our approach allows the relative importance of factors to switch in the support of the state process. and its eigenvalues are continuous in . Thus, Assumption 7 does not allow factors to switch their relative importance in the neighborhood of the state that we condition on. In this case, there exists some state value for which has repeated eigenvalues. The individual factors are not identified for this particular state outcome. Nevertheless, the common component is still identified.

5 Asymptotic Results

Under appropriate rate conditions, we can consistently estimate the factors, loadings, and common components and obtain an asymptotic normal distribution. The rate conditions are similar to the results in Bai (2003), but replace by the effective number of time observations . However, the kernel bias term requires additional rate restrictions.

We assume that the number of factors has been consistently estimated. A possible consistent estimator for the number of factors is proposed in Bai and Ng (2002) and based on an information criterion. In the Internet Appendix, we generalize this estimator to our setup, which allows us to estimate the number of factors conditional on a specific state outcome. This estimator selects the number of factors by trading off the amount variation explained in a specific state and a penalty function based on an information criterion. This penalty function essentially replaces the rate by in the estimator of Bai and Ng (2002). In the Internet Appendix, we also discuss how to use a cross-validation approach to determine the number of factors.

Theorem 1.

are estimates of the projected factors . The factors can be identified up to some rotation matrix, , which depends on the state. The convergence rate is the smaller of and , denoted as , as and . As expected, the bandwidth parameter interacts with , but not with , as the kernel projection is equivalent to weighting data differently in the time dimension.

The additional restriction is due to the kernel bias. In more detail, the projected observations can be written as

| (3) |

Factors are estimated as eigenvectors from the projected data, i.e.

| (4) |

Plugging Equation (3) into Equation (4) we obtain

where and . The three terms, , , are bias terms from using observations in nearby states.171717Although Su and Wang (2017) also uses a PCA estimator with a kernel method to estimate a time-varying factor model, they do not take these bias terms into consideration. The bias terms are controlled by the Lipschitz condition in Assumption 4 and the assumptions on the kernel function. We show that the bias terms are negligible for . In particular, a candidate bandwidth to satisfy the rate assumptions is .

Theorem 2.

This theorem shows the asymptotic normality of the estimated factors up to the some of rotation of true factors for the times when the state process is equal to the target outcome .181818Instead of conditioning only on the times when we could allow for the times when satisfies . Since is an estimate of the projected , dividing both sides by , results in an estimate of . A valid bandwidth for the case is for some small .

Note that the convergence rate is the same as in the constant loading factor model (see Theorem 1 in Bai (2003)). The variance is equal to that of an ordinary least square regression (OLS) of the panel on the unknown population loadings.

Theorem 3.

This theorem shows the asymptotic normality of the estimated conditional loadings up to some rotation. has some error and bias terms, including a leading bias term for the time average of . We show in the appendix that . Therefore, when , the bias terms are sufficiently small relative to the error term. A candidate bandwidth to satisfy the assumptions is when .

As expected the convergence rate is , which is slower than the convergence rate in the constant loading factor model (see Theorem 2 in Bai (2003)). The variance is equal to an OLS regression of the projected data on the projected unknown population factors. The smaller the bandwidth , the slower the convergence rate and the smaller the bias. The variance of is and the bias of is . The optimal bandwidth to balance variance and bias and satisfy the assumptions in the asymptotic distribution is for some small .

We denote the common component by and its estimator by .

Theorem 4.

The estimated common components converge to an asymptotic normal distribution that combines the results of the previous two theorems. Note that the systematic part is identified without a rotation. The variance in the asymptotic distribution is determined by two components, factor and loading distributions. The first component is from the asymptotic distribution of estimated factors . The second component comes from the asymptotic distribution of estimated loadings . It depends on the relationship between and , which one dominates. If and have similar scales, both , and play a role in the variance of the asymptotic distribution. However, if , the asymptotic distribution of the loadings dominates (which allows us to drop the additional assumption on the times ), while if , the factor distribution dominates.

6 Generalized Correlation Test for Change in Loadings

We derive a test statistic to detect if and for which states loadings are different. This is distinct from a “global” test if loadings change at some time without guidance when the change actually happens. We provide an answer to the relevant economic question for which specific times and states loadings are different.191919 Su and Wang (2017) provide a “global” test for the constancy of factor loadings over time. Similar arguments could be applied to our framework. The proof would go through with some modification about controlling the bias from using data in other states. In a similar spirit, Kong (2018) provide a global test in a high-frequency setup. Pelger (2020) illustrates in an empirical study that it is important to identify when and how time-varying loadings change as this can provide valuable economic insights.

Since the loadings can be estimated up to some rotation matrix, the test statistic needs to be invariant to invertible linear transformations. A candidate measure is the total generalized correlation, which measures how close the two vector spaces spanned by loading vectors in two states are. The total generalized correlation ranges from 0 to the number of factors . 0 means that two spaces are orthogonal, while represents that two spaces are the same.

It is worth noting that it is insufficient to test if the loading vectors for individual factors are different in different states. For example, it is possible that the first factor explains less variation in another state and switches with the second factor. In this case, measuring the correlation of the loadings of the first factor for different state outcomes would indicate a change in loadings, while the factor structure itself actually does not change. Thus, it is crucial to study the harder problem if the span of all factor loadings changes with the state.

We consider the two state outcomes and with the corresponding loadings and . Note that our state process still has a continuous support. Testing the constancy of factor loadings for the particular state realizations and is equivalent to testing whether there exists an invertible matrix , such that . We use a slightly modified estimator for the loadings and estimators that will simplify the notation. Instead of normalizing the projected factors to be orthonormal, we apply this normalization to the loadings. This means we use and . All results are valid for the modified estimator under the same assumptions as for the estimators introduced in the previous section. has the same asymptotic distribution as except that it replaces the asymptotic variance by that of multiplied by on the left and and on the right. Similarly, has the same asymptotic distribution as , except that the asymptotic variance is multiplied on the left and on the right.212121In order to study and , we need to redefine , , where , and 202020 here is the same as the in theorem 3, since the eigenvalues of are the same as those of are eigenvalues of , is the corresponding eigenvector matrix such that . Under the same assumption as Theorem 4, the asymptotic distribution of is , where is the same as the in Theorem 4. Let and , then we have under the same assumptions as in Theorem 4.

The generalized correlation test statistic requires some mildly stronger assumptions.

Assumption 8.

Moments and Central Limit Theorem: There exists an , such that and , for any

-

1.

Double-sum factors, loadings and projected idiosyncratic components in two states:

-

2.

Double-sum loadings and projected idiosyncratic components in two states:

-

3.

Projected factors, loadings and idiosyncratic components in two states:

-

4.

Define and let . It holds222222Here we denote by the vectorization operator. Inevitably the matrix is singular due to the symmetric nature of the covariance and a proper formulation uses vech operators and elimination matrices.

(8)

Assumption 8 is closely related to Assumption 6, but Assumption 8 involves loadings in two states, and . Assumptions 8.1 and 8.2 are similar to Assumption 6.5, but these two assumptions are averaged twice in the cross-sectional dimension. Assumption 8.3 generalizes Assumption 6.2 and it is identical to Assumption 6.2 when . Assumption 8.4 is a joint central limit theorem for the cross-sectional and time-series average of the residuals.

In order to simplify notation, we denote and . We define the estimated total generalized correlation as

and the population counterpart as .

Testing if is some linear rotation of is equivalent to

If we multiple any full rank square matrix to the right of or , does not change and the same holds for . Note that if , then it holds , where is an identity matrix. Hence, it is equivalent to test232323Here we use the following result:

Lemma 1.

Let and . Assume , and , let , then we have .

Theorem 5 provides the inferential statistic for a one-sided test of the null hypothesis .242424Note that our generalized correlation test statistic would also work when the dimensions of the loading spaces change with the state.

Theorem 5.

Under Assumptions 1-8 and under the null hypothesis , if , , , , and , then

| (9) |

The matrix and a consistent plug-in estimator are given in the Internet Appendix. is a bias correction term.

Let and . Assume there are only finitely many non-zero elements in each row of and and we know the sets and of nonzero indices.

A consistent estimator of the bias correction term is

and

where and and with components

where and . The feasible test statistic

is asymptotically distributed under and diverges to with probability 1 under .

There are two surprising results. First, the test statistic for the null hypothesis is super-consistent, i.e. converges at the higher rate . Under the assumption , a simple delta-method argument applied to the trace shows that the convergence rate is slower at as stated in Lemma 4 in the Internet Appendix. Second, the special case of requires a bias correction in contrast to where the bias can be ignored. The bias arises because the higher rate of convergence does not allow us to ignore certain higher-order terms in the asymptotic expansion of . Note that by construction (see Lemma 1), we have . Theorem 5 shows that under the null hypothesis, is distributed asymptotically normal around which implies that the bias term is negative.

Let . All rate conditions in Theorem 5 can be reduced to , , . If (equivalent to ), there exists combinations of and that satisfy the rate conditions. For example, if , then the rate conditions can be reduced to and . The rate conditions are more stringent than Theorem 1-4, because converges at the faster rate . The strong condition , equivalent to is needed to neglect the bias term. Simulations suggest that the distribution result is still a good approximation even if the rate conditions are not satisfied.

In order to obtain a consistent estimator of the bias term, we assume that the residual covariance matrix is sparse similar to Fan, Liao, and Mincheva (2013). Our sparsity assumption imposes that there are only finitely many nonzero elements in each row of the covariance matrix of the errors and similarly in the autocovariance matrix . For simplicity, we assume that we know the set of nonzero indices. This assumption could be relaxed, and we could estimate the nonzero elements with a thresholding approach similar to Fan, Liao, and Mincheva (2013) under additional assumptions.

7 Simulation

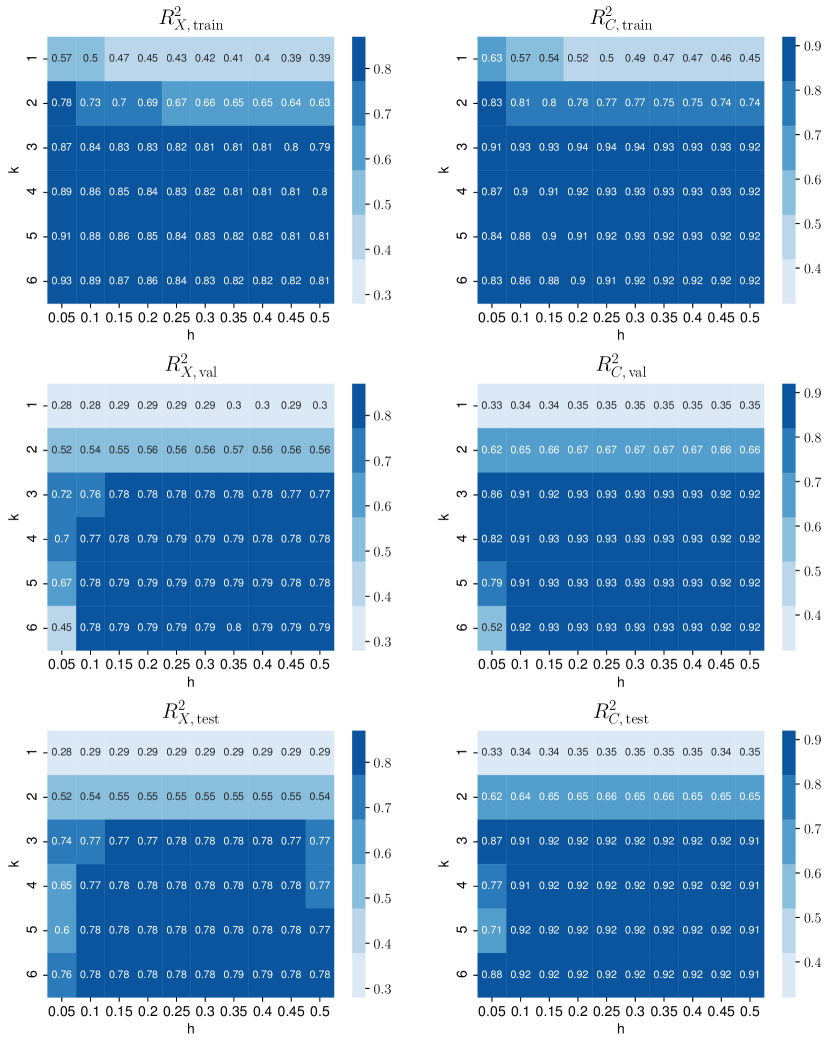

We study the finite sample properties of our estimators with Monte-Carlo simulations. First, we show that the simulated distributions of the estimated loadings, factors, and common components converge to the asymptotic distributions. Second, we show that the functional form of the loadings as a function of the state can be reliably recovered. Third, we verify the good size and power properties of our test statistic. Fourth, we test the performance of our estimator for a misspecified state process. The Internet Appendix contains a validation study for selecting the number of factors and bandwidth and shows the good performance of our estimator relative to existing estimation approaches based on structural breaks or local PCA estimation.

7.1 Asymptotic Distribution Theory of Estimators

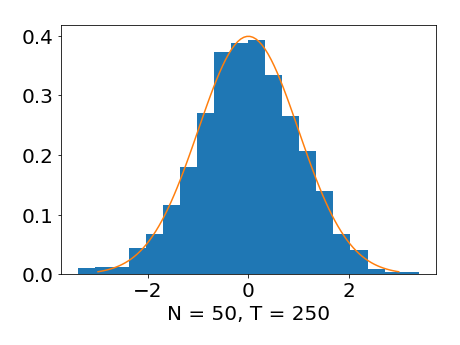

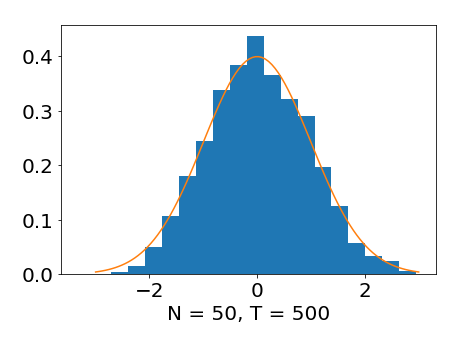

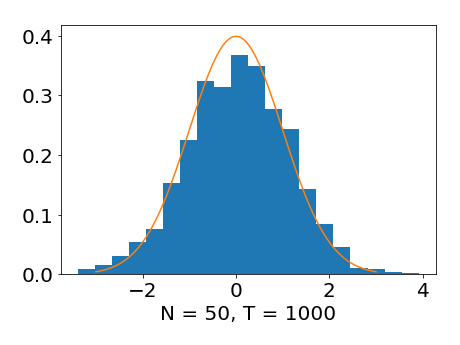

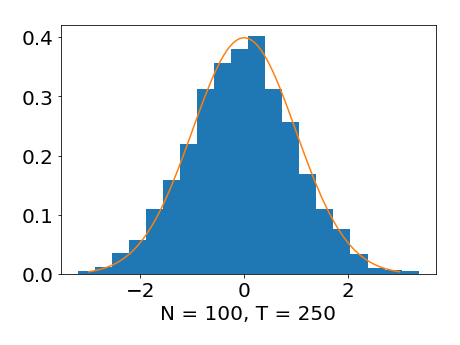

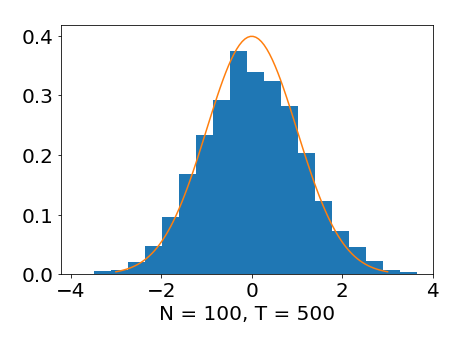

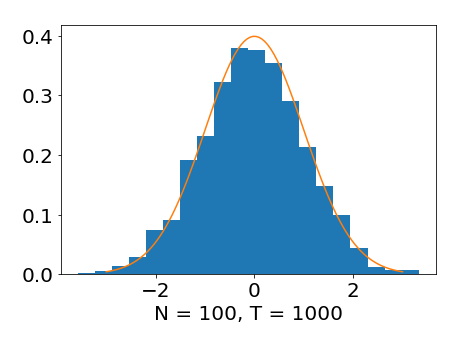

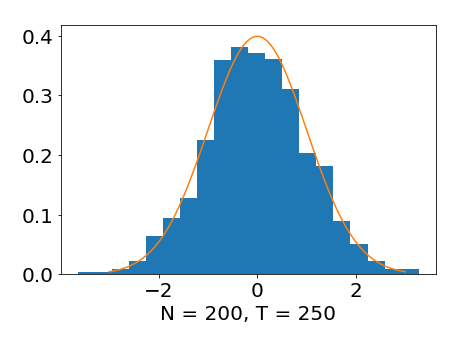

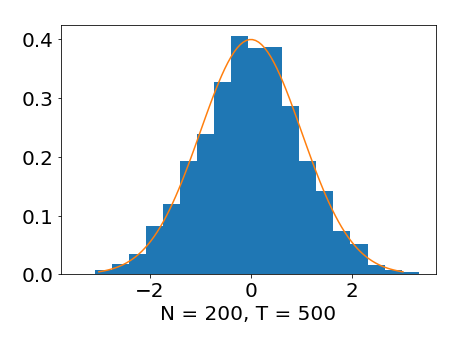

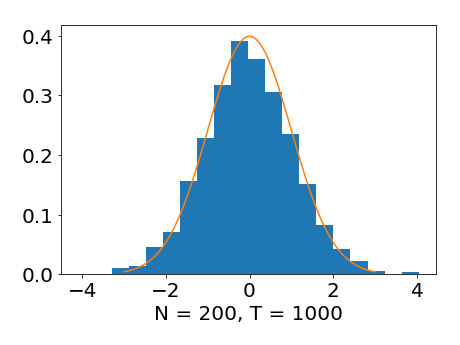

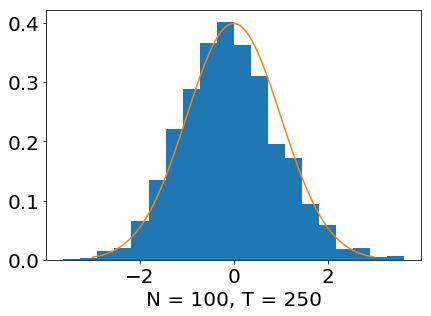

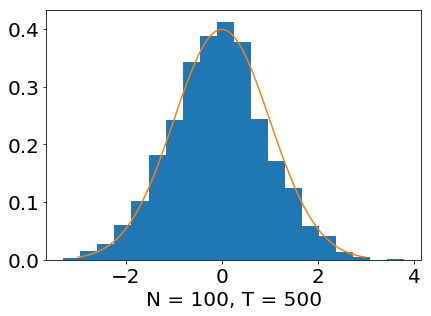

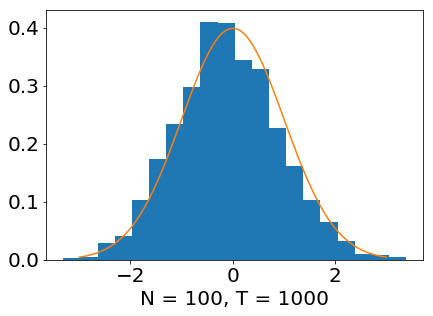

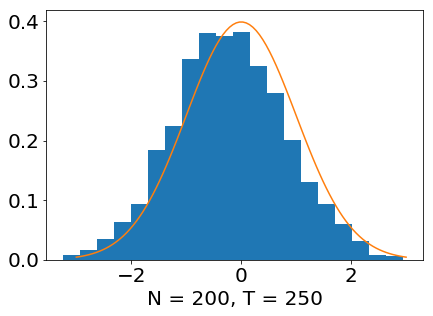

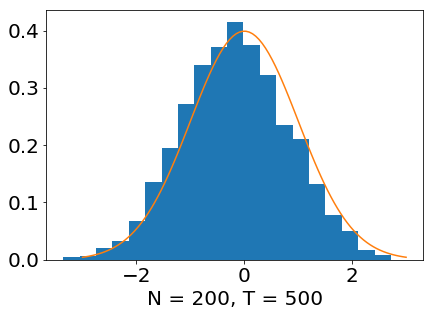

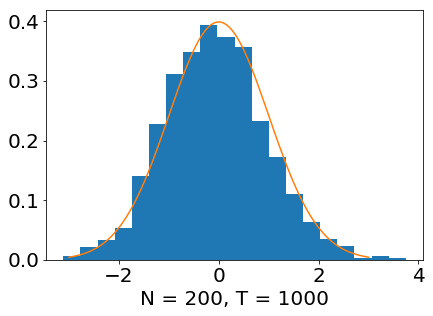

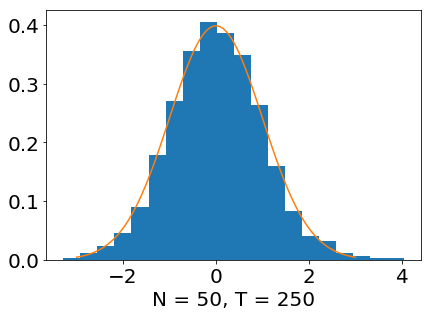

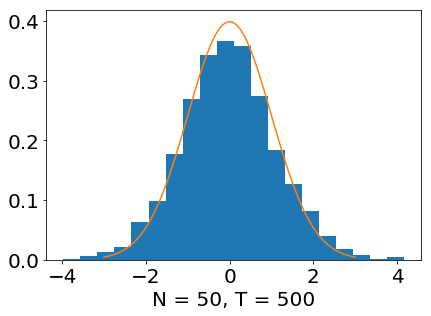

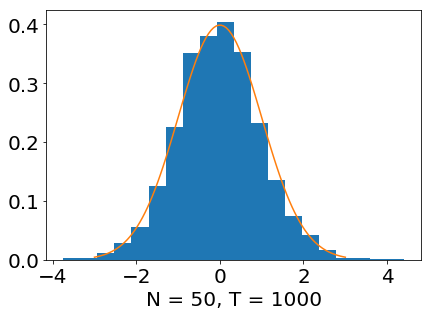

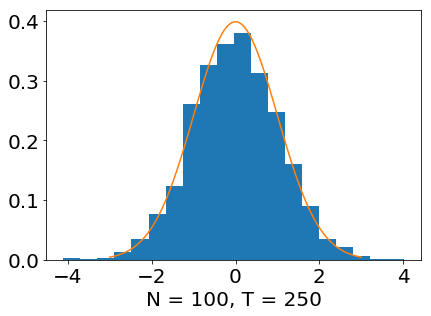

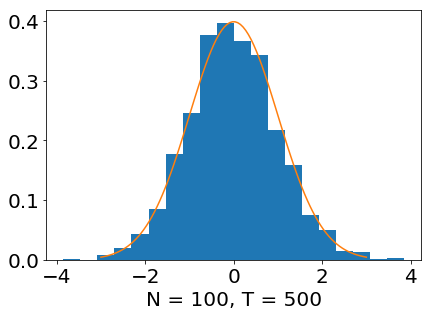

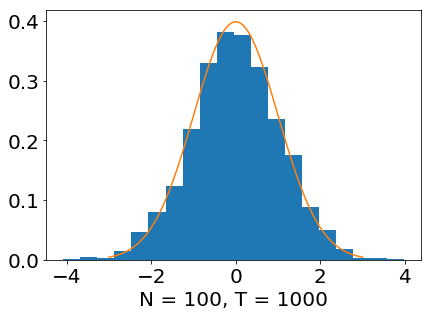

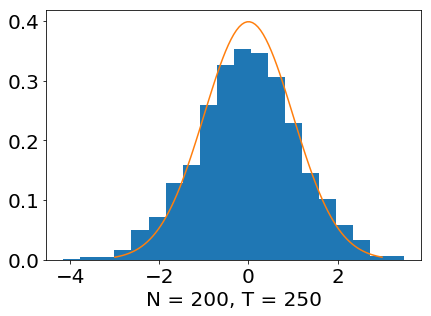

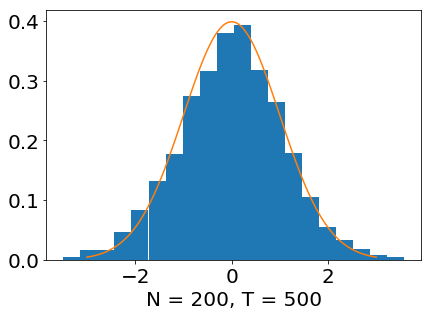

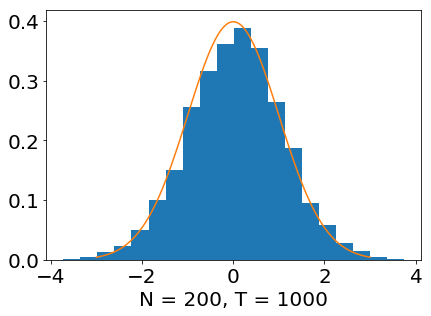

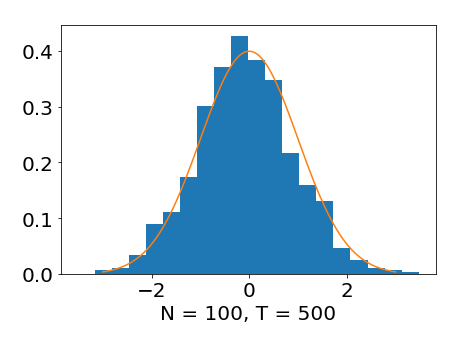

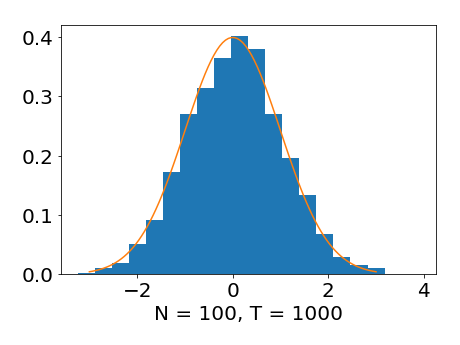

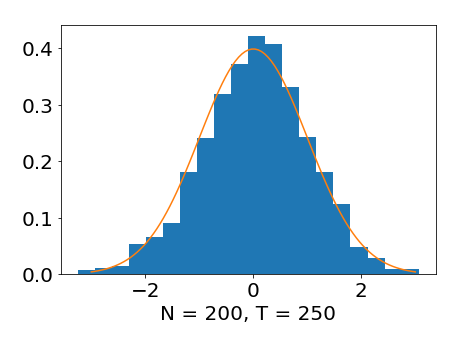

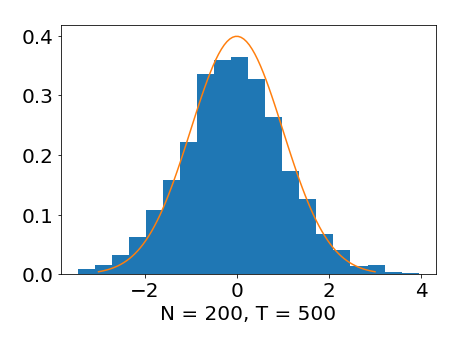

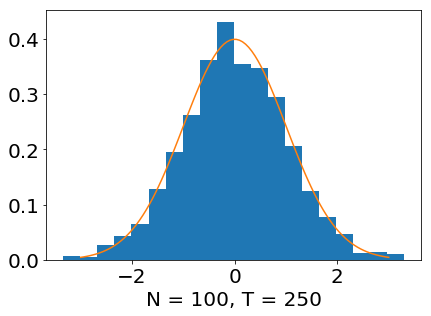

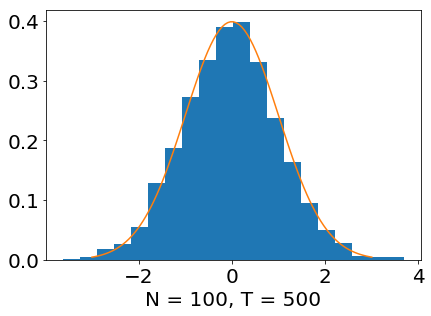

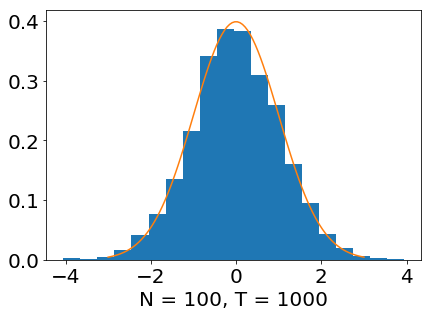

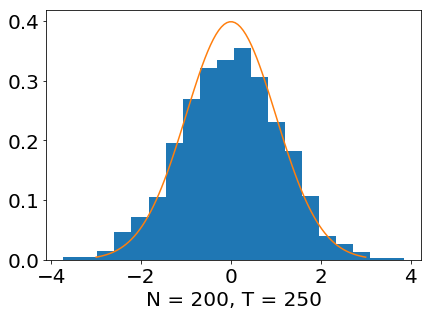

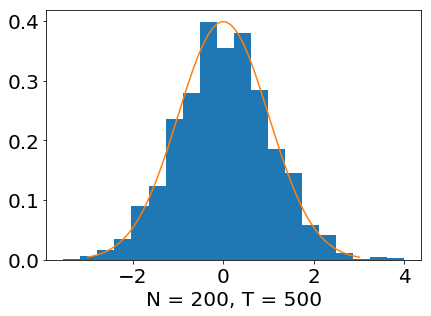

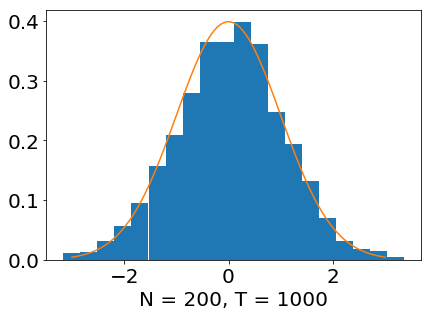

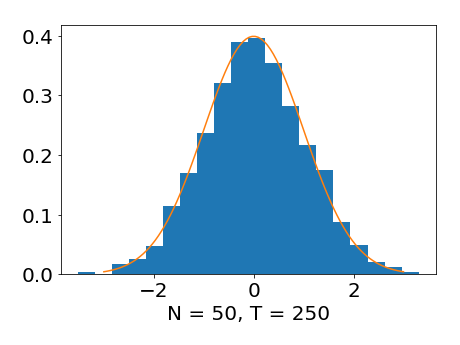

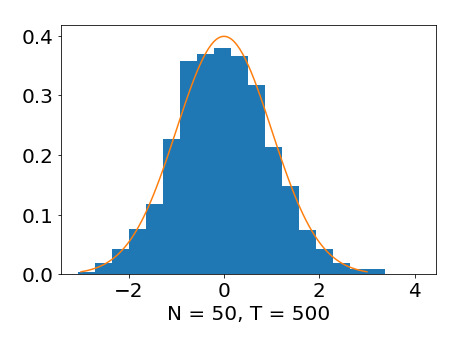

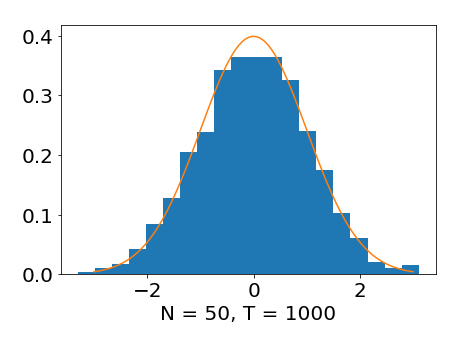

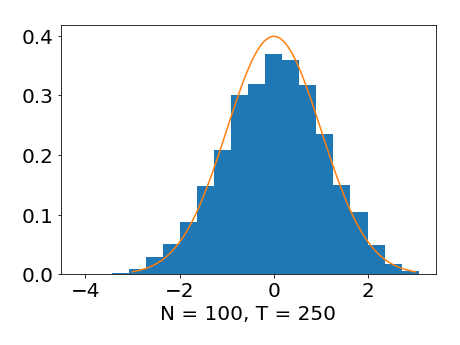

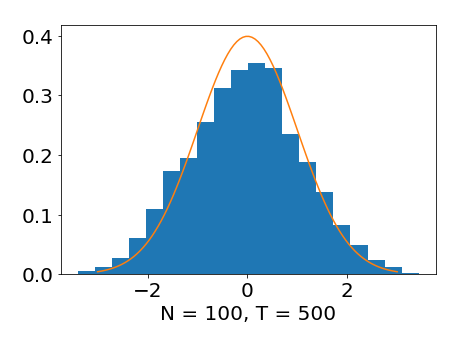

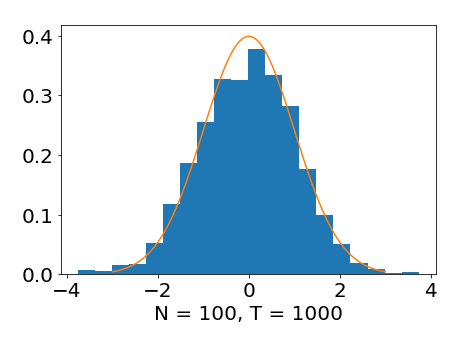

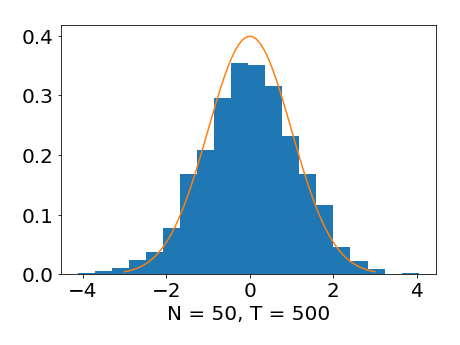

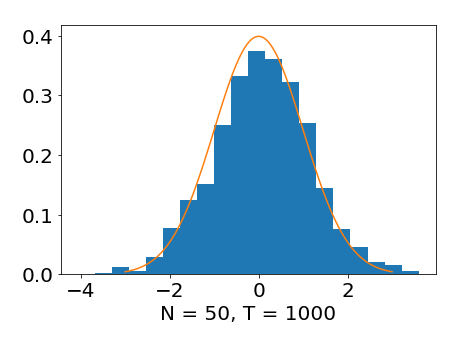

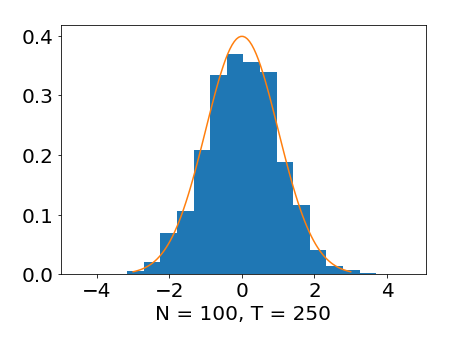

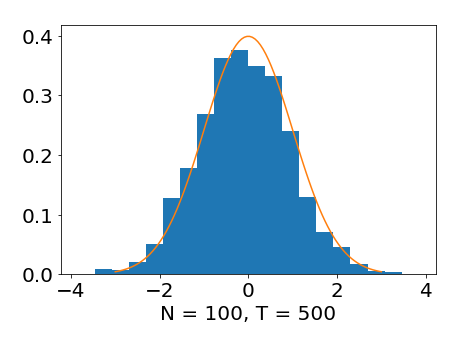

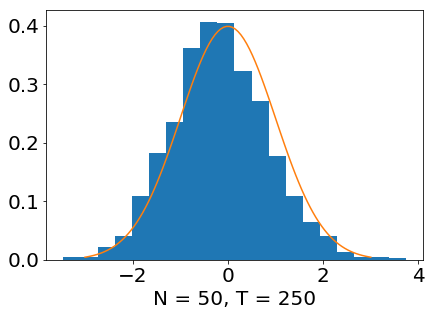

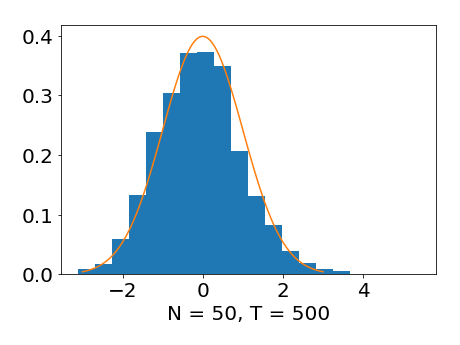

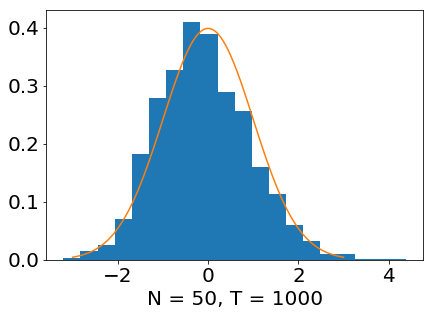

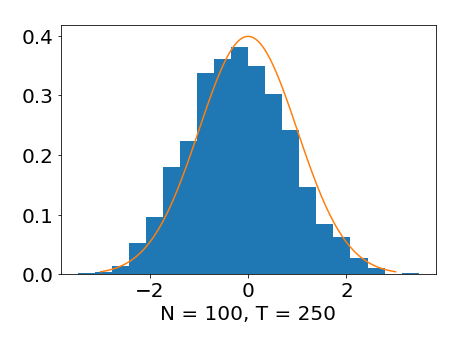

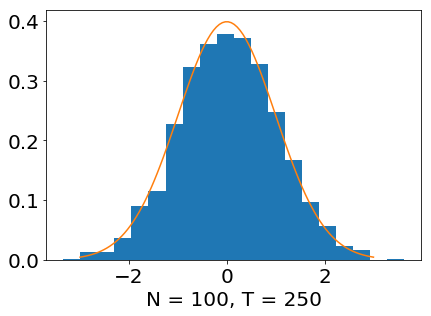

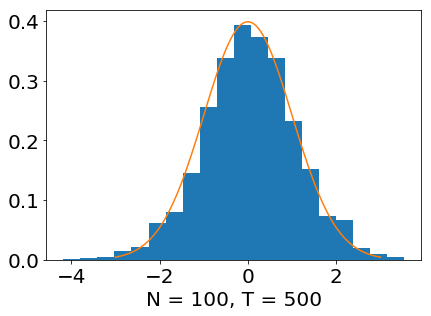

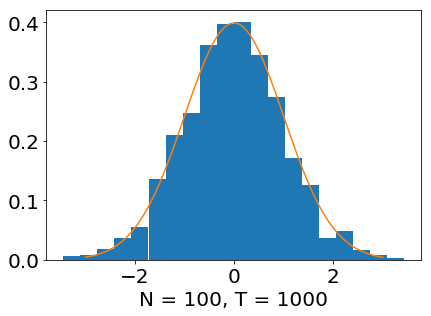

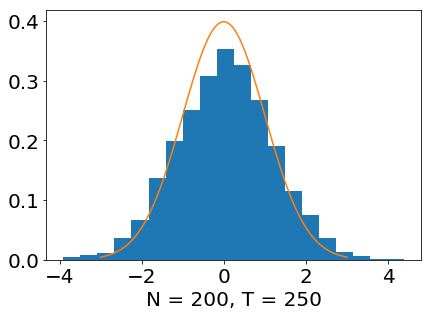

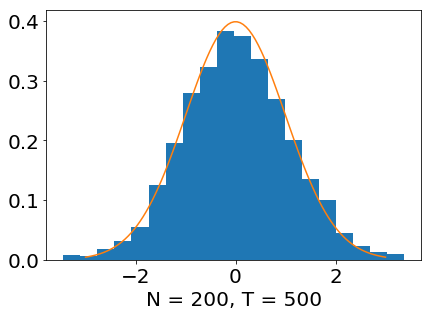

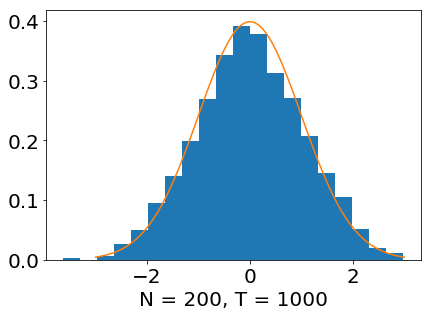

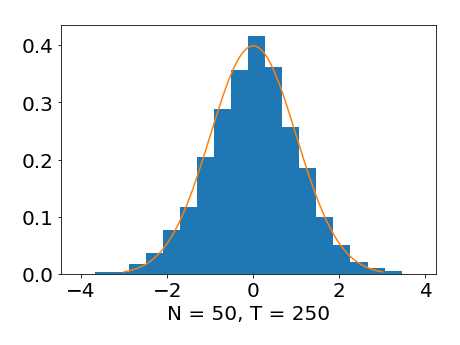

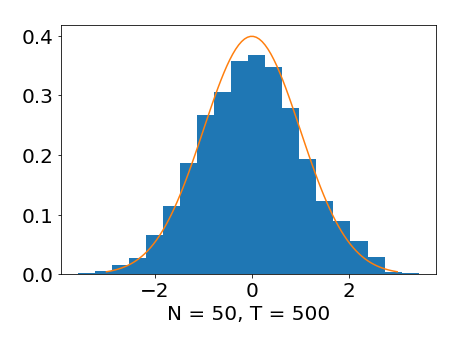

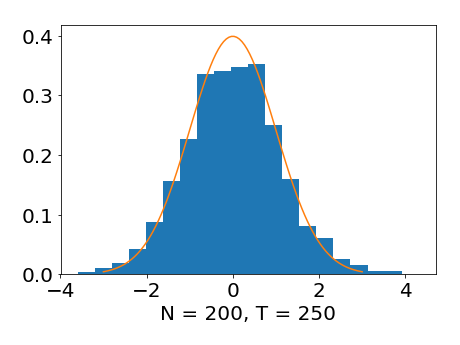

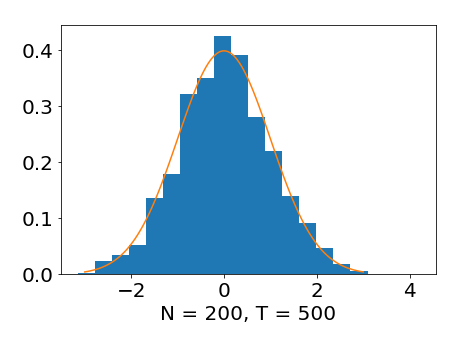

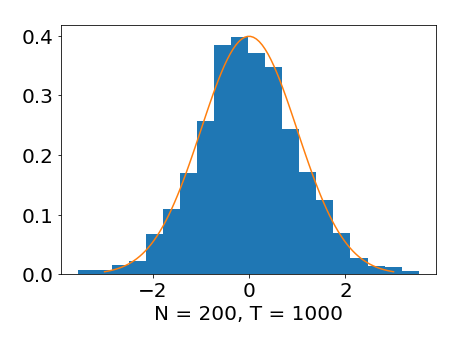

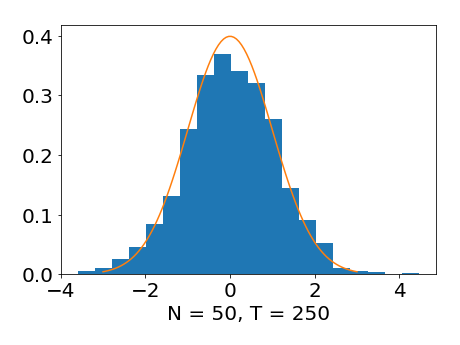

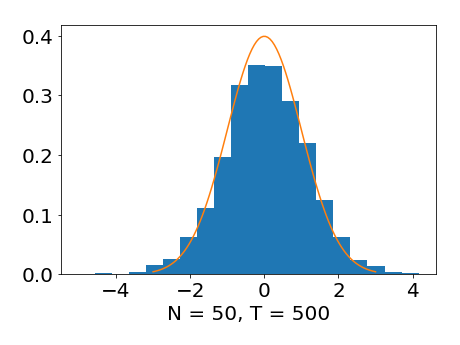

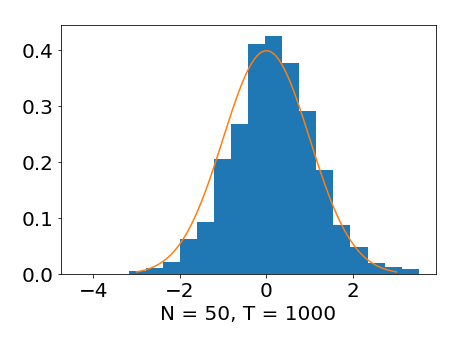

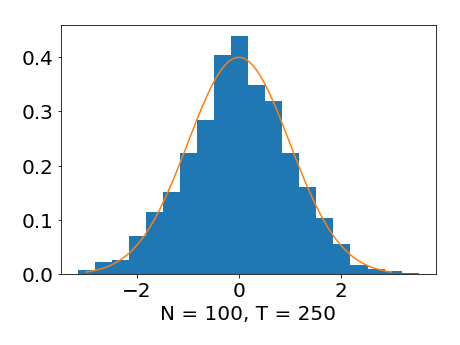

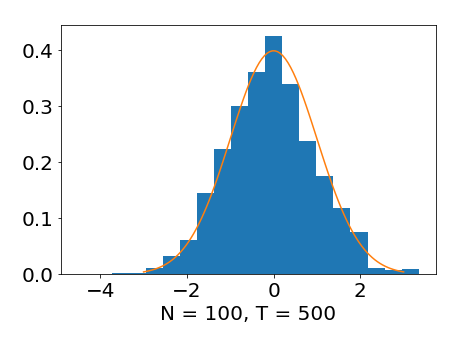

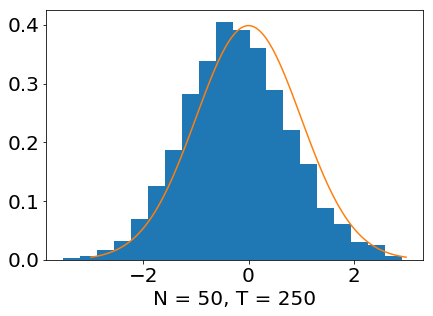

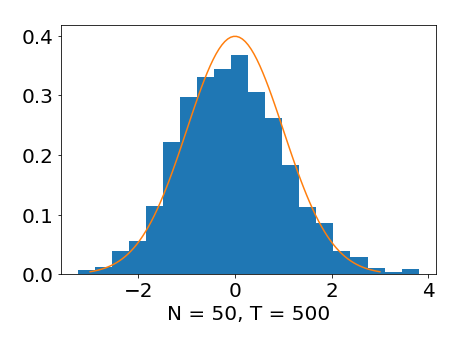

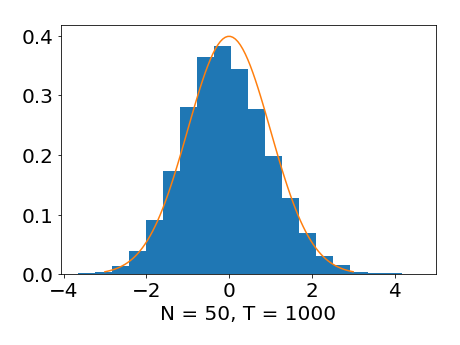

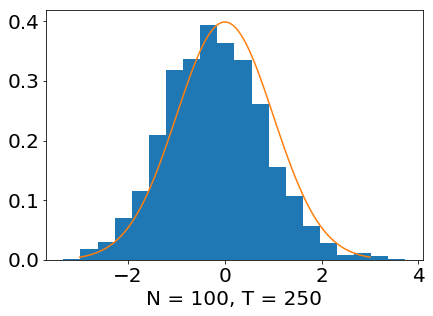

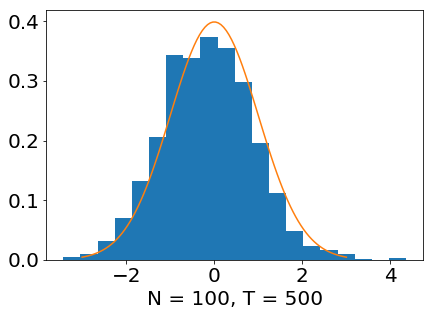

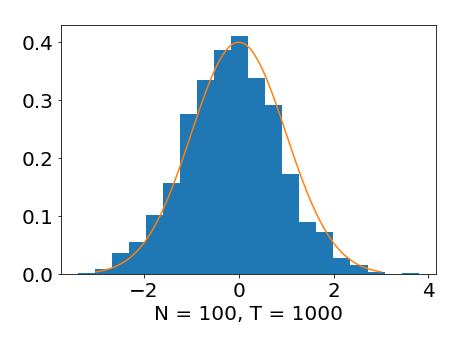

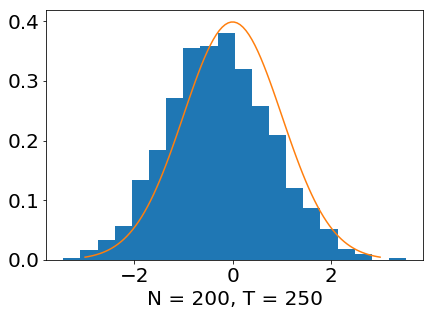

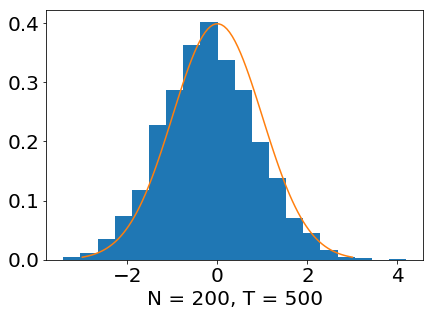

In the baseline model, we generate data from a one-factor model , where . The state process is an Ornstein-Uhlenbeck (OU) process which is a mean-reverting process with stationary distribution. In more detail, we simulate the state process as , where , , and and its stationary distribution has mean and variance . The OU process is popular for modeling stochastic volatility in financial data, which is aligned with the volatility index as state process in our empirical applications. The loadings are cubic functions of the state process, , where . The functional form of the loading function is motivated by our empirical findings. The loadings as a function of volatility change non-linearly, and the changes are larger for state values that deviate more from its mean. The coefficients in the cubic, quadratic and linear terms are chosen to guarantee that loadings will not be completely dominated by the state realizations with the largest absolute values, which is again in line with our empirical findings. We generate three different idiosyncratic processes: (1) i.i.d. , (2) heteroskedastic and (3) cross sectional dependent , with .

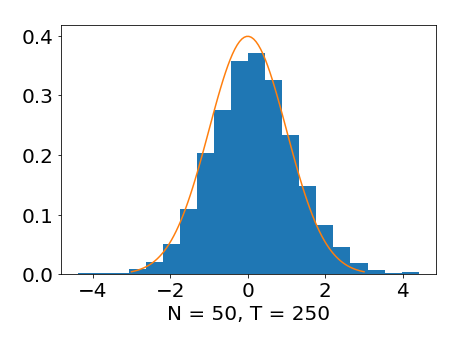

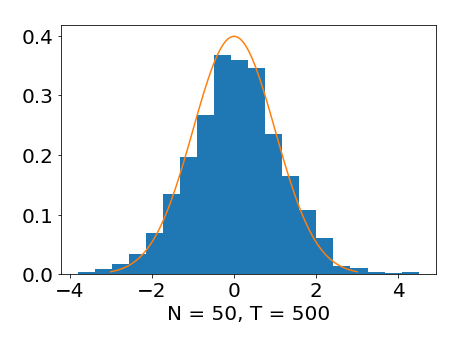

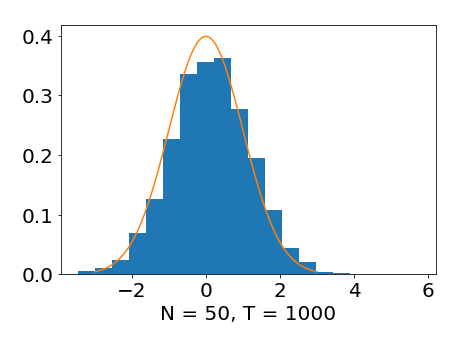

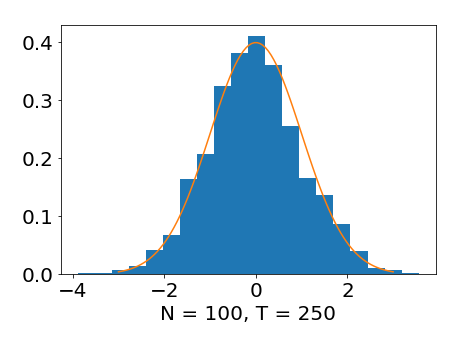

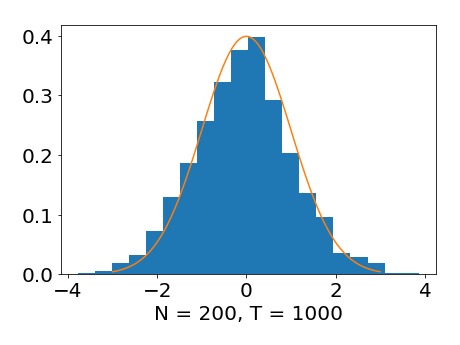

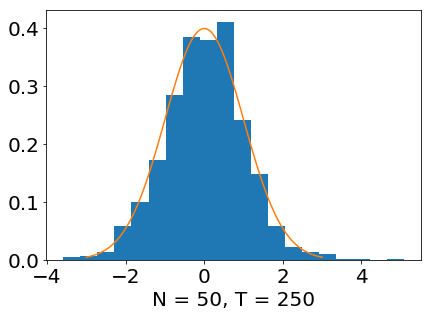

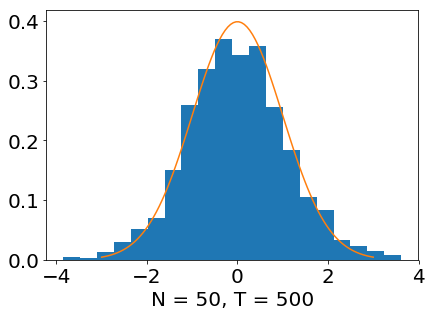

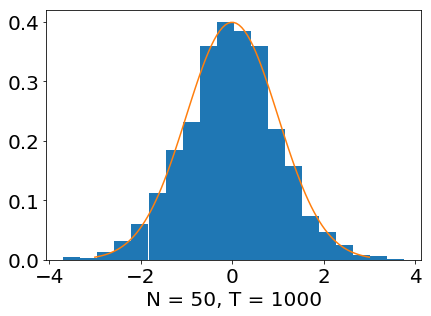

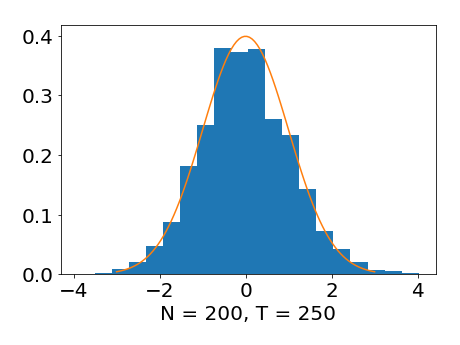

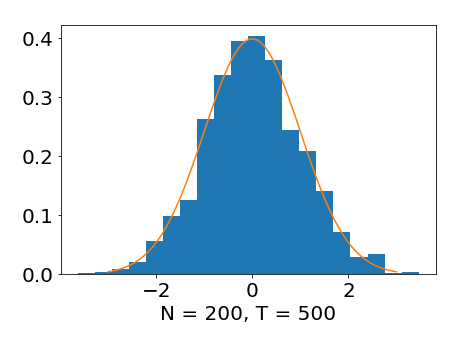

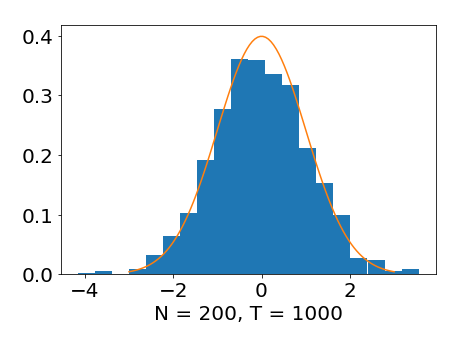

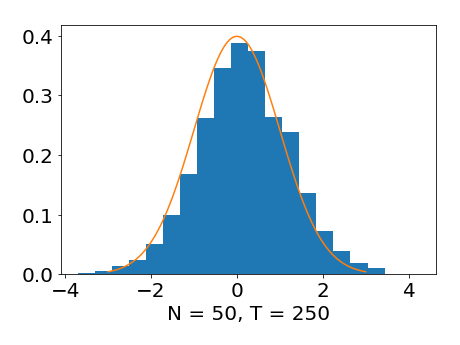

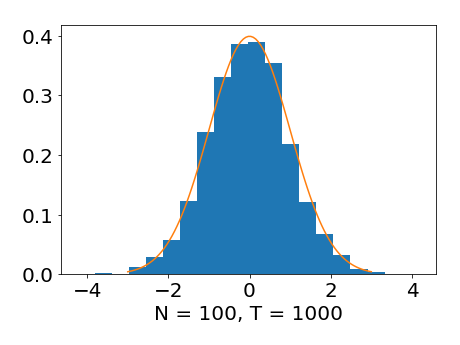

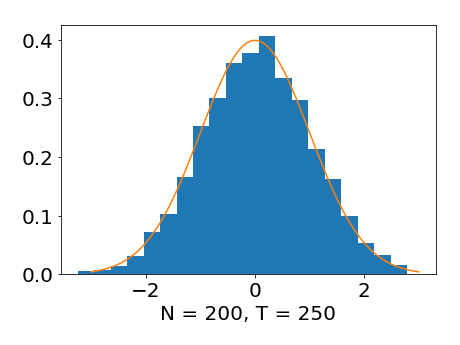

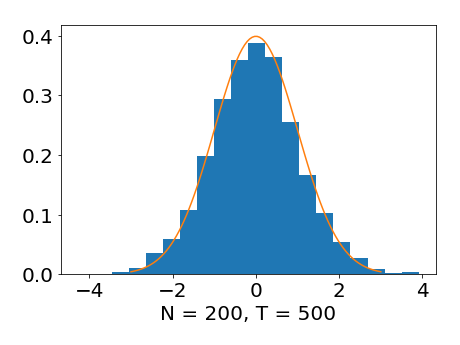

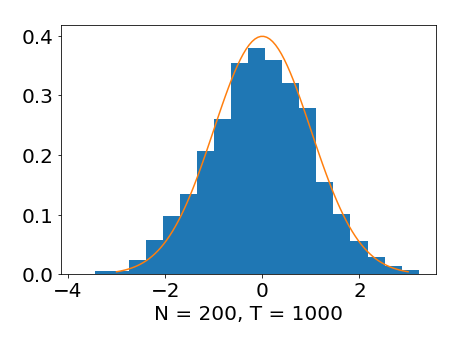

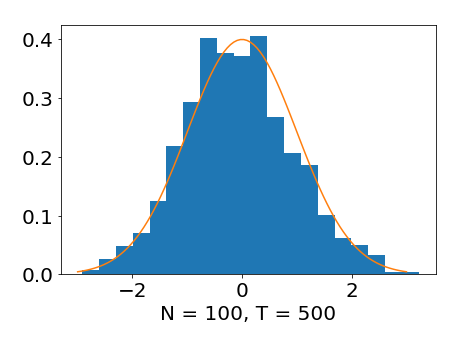

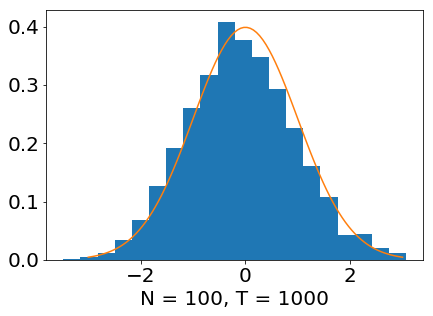

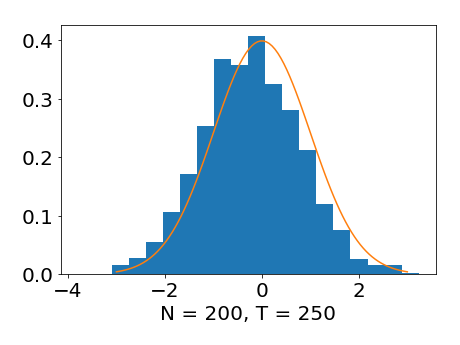

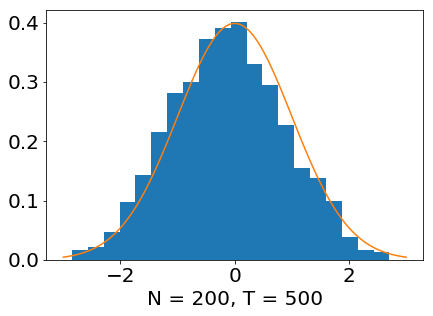

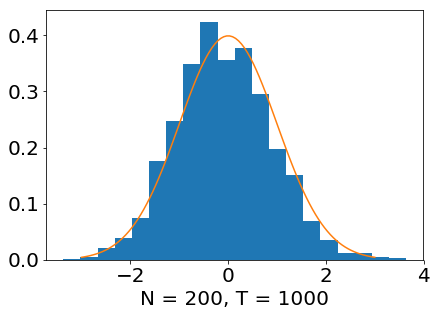

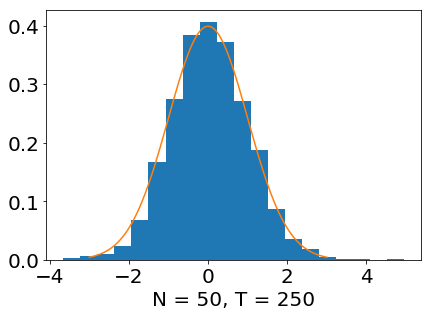

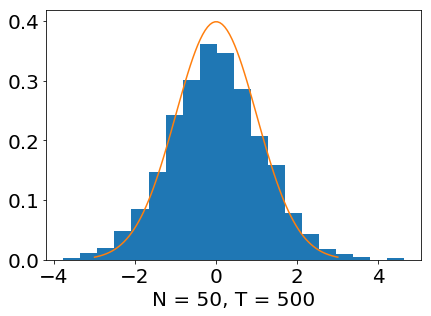

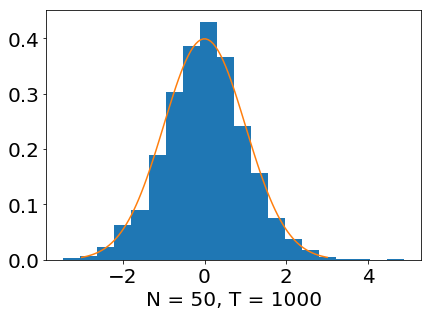

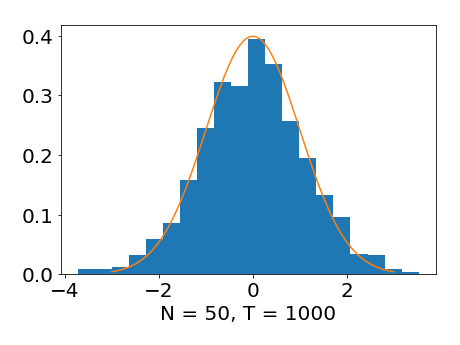

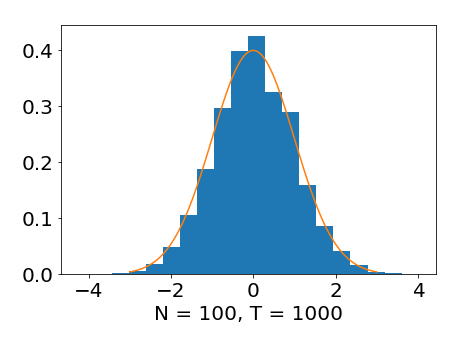

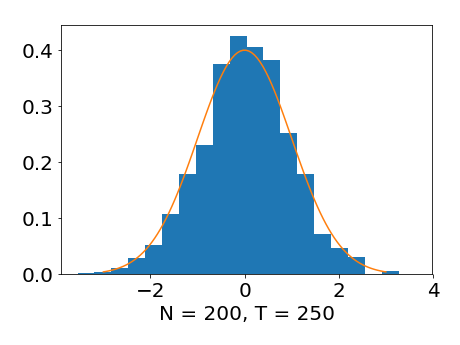

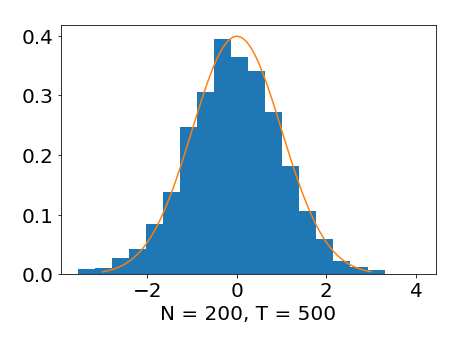

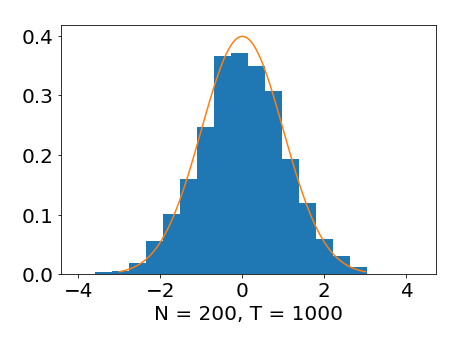

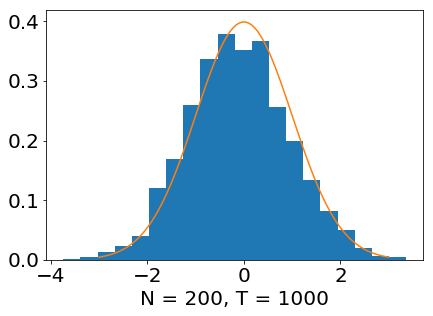

Figure 1 shows histograms of the standardized estimated loadings for different and . The estimates are centered and standardized using consistent estimates of the theoretical mean and standard deviation. We set the state outcome to and bandwidth to to balance the bias and variance inherited in the nonparametric method.252525The squared error of the nonparametric method is . In order for the results in Section 5 and 6 to hold, we have , , and . This gives us a guideline for selecting the bandwidth in the simulation and empirical studies and suggests range of 0.1 to 0.5. The Internet Appendix collects the results for various bandwidth and shows that our findings are robust to the choice of . The Internet Appendix collects the results for the estimated factors and common components and includes the cases of heteroskedastic and cross-sectionally dependent errors. The results are virtually identical, and we find that the simulated data is very well approximated by the theoretically implied normal distribution. Thus, our results are robust to heteroskedastic or cross-sectionally dependent errors.

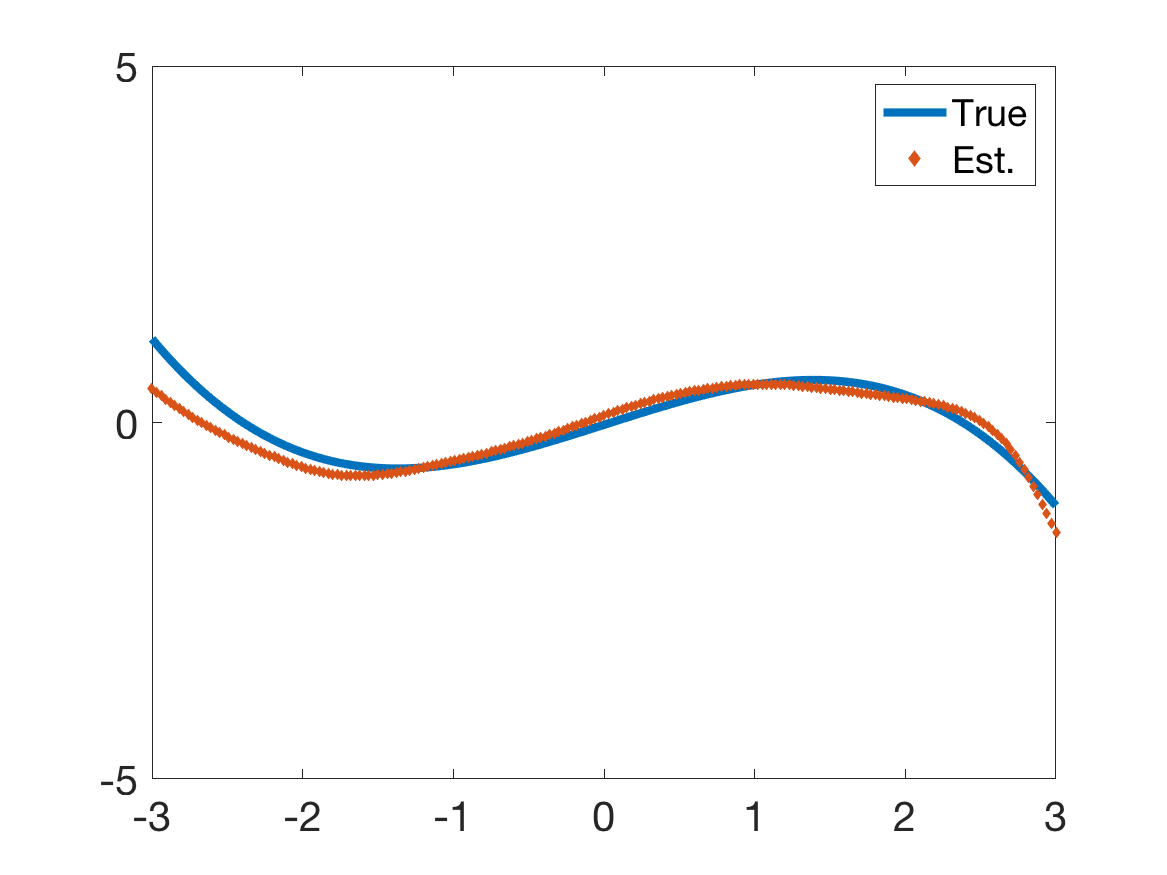

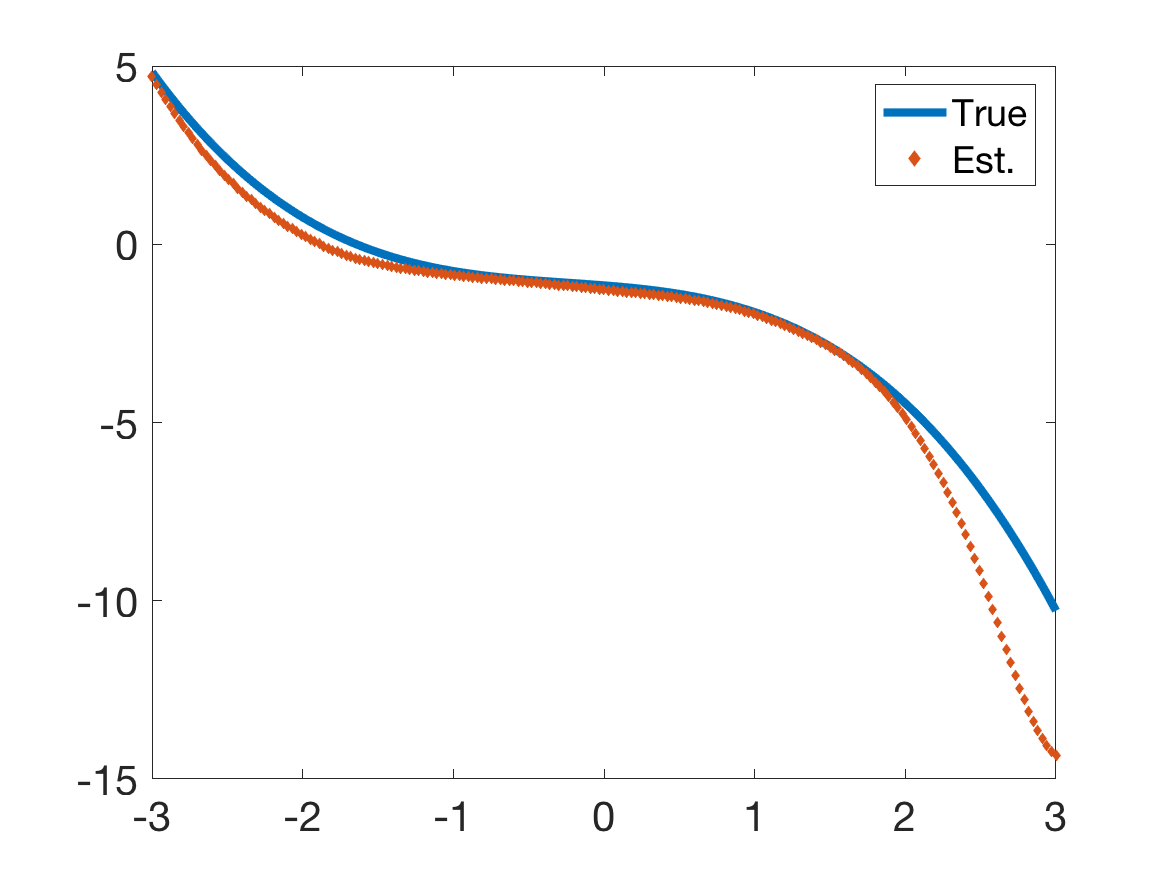

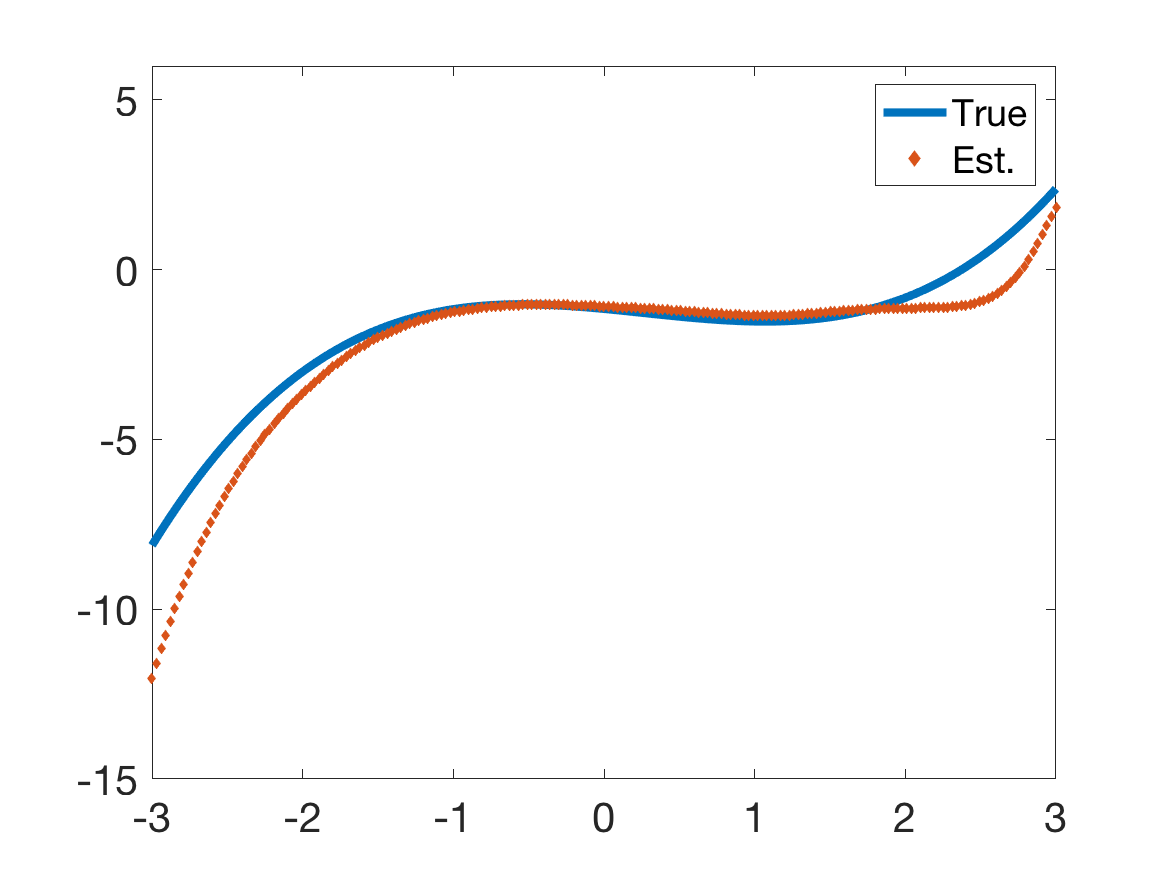

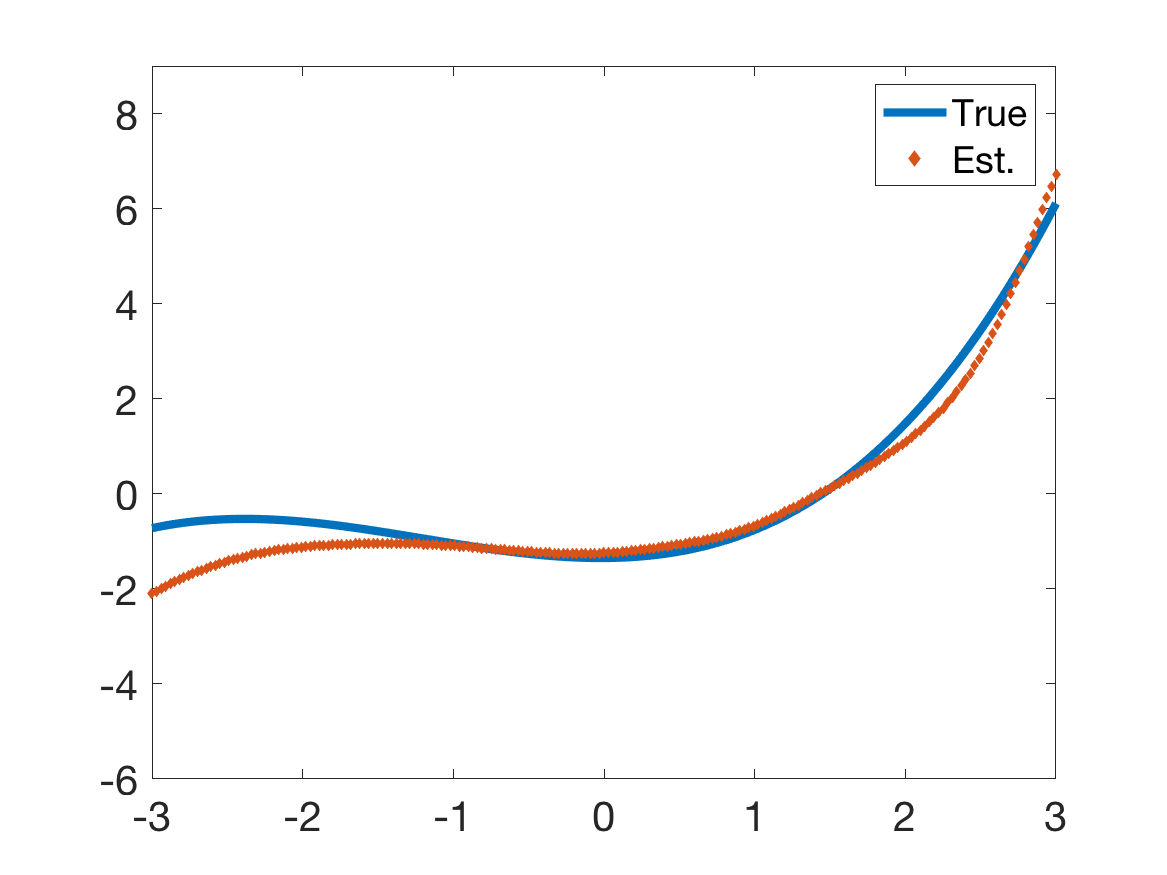

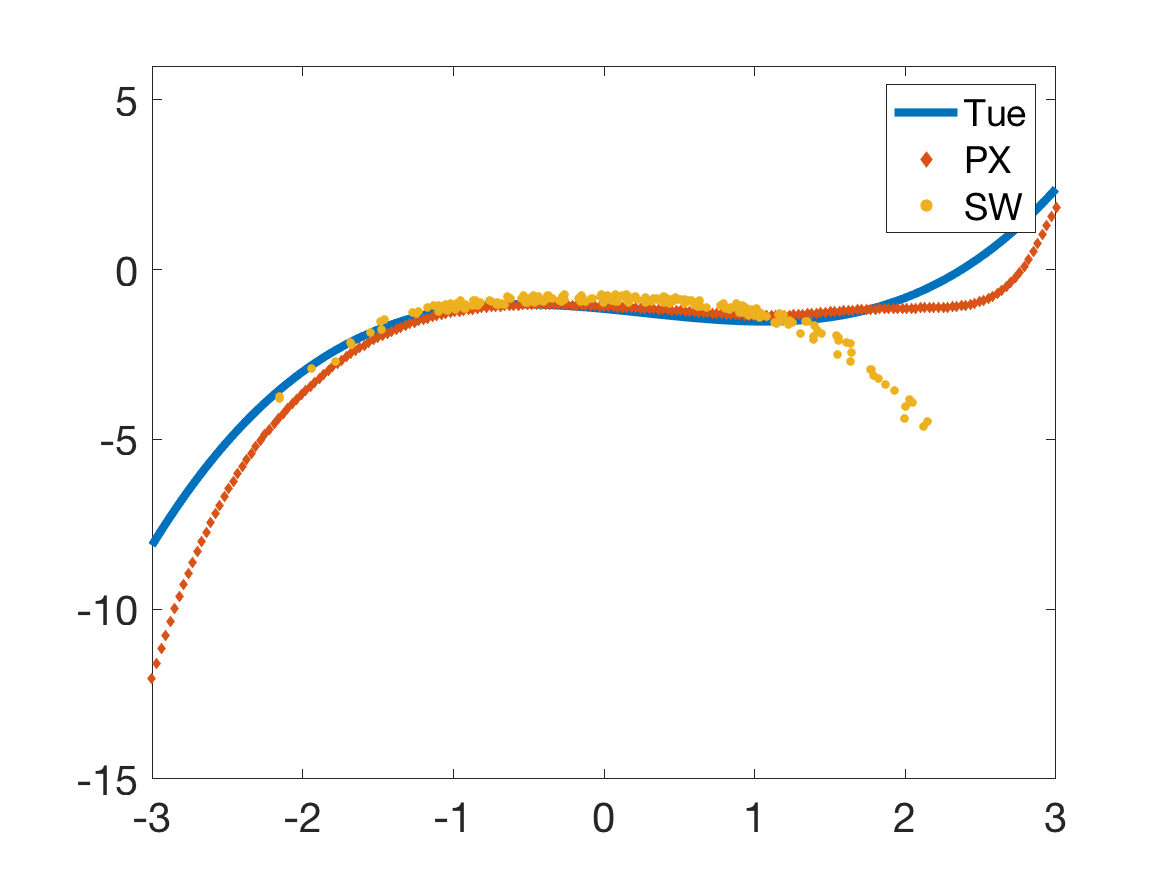

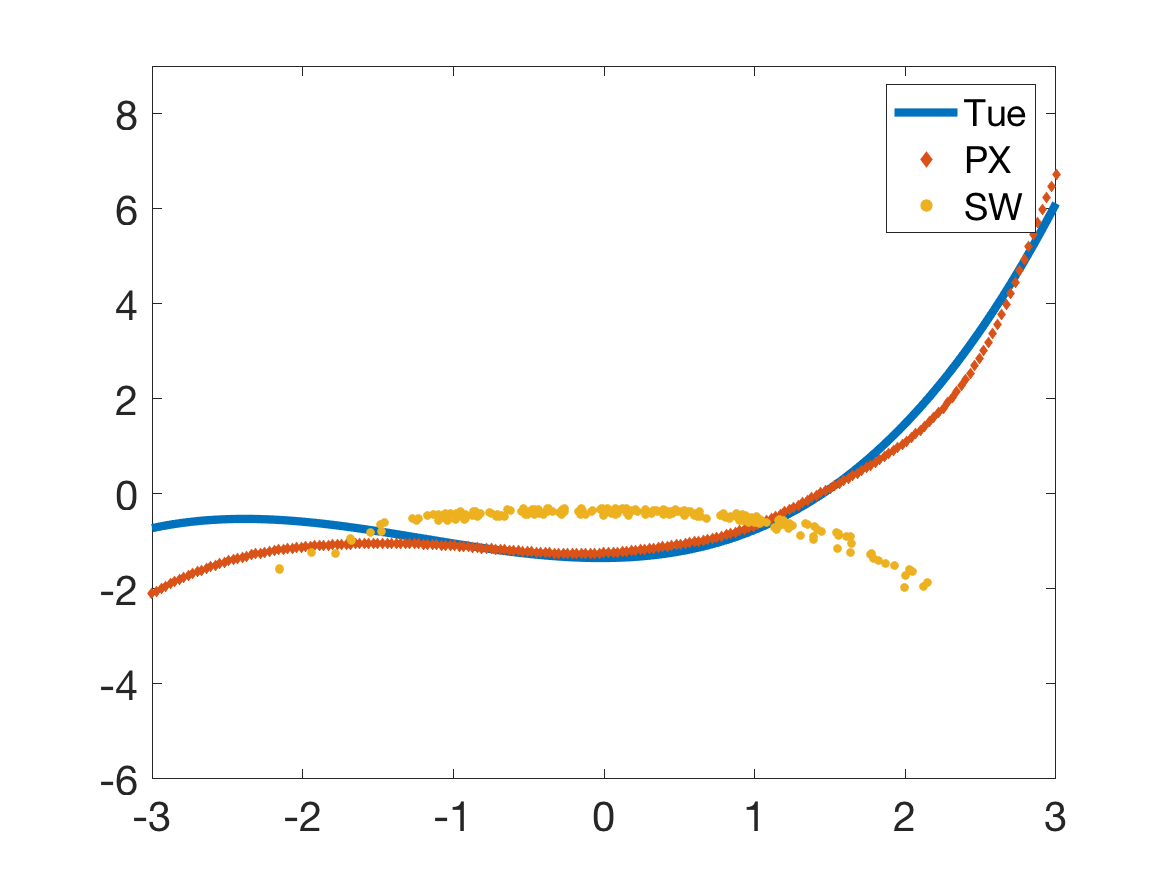

We can estimate well the functional form of the loadings depending on the state. Figure 2 compares the estimated functional form with the true functional form of the loadings of four randomly selected cross-section units. The factor model is estimated in every possible state between -3 and 3. The estimated functional form of the loadings matches the true functional form very well.262626In Figure IA.15 in the Internet Appendix, we compare the estimation results of our state-varying factor model with the local time-varying model of Su and Wang (2017) under the same simulation setup. Our state-varying factor model can recover the correct functional form while the local window estimator fails.

7.2 Generalized Correlation Test

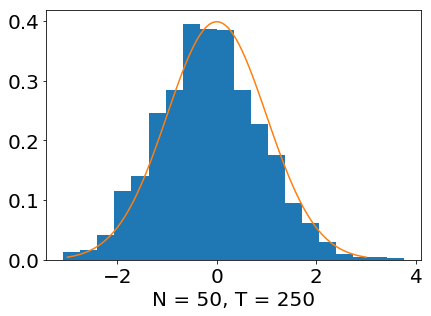

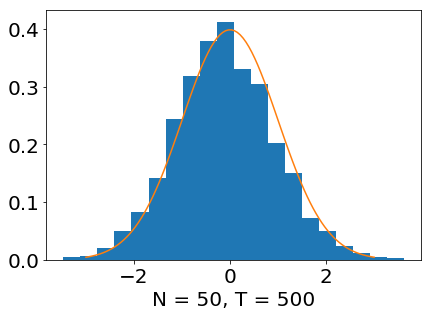

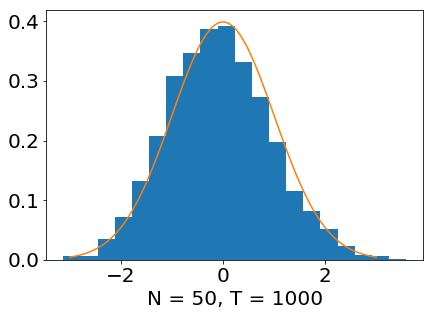

The data generating process is similar to the data generating process in Section 7.1, except that we use constant loadings to generate the data for all states. Figure 3 is generated by keeping the realization of the single factor, loadings, and state fixed and simulating the i.i.d. errors. The histograms for heteroscedastic errors and cross-sectionally dependent errors are in the Internet Appendix. Without loss of generality, we select the two-state outcomes and to calculate the generalized correlation . We compare the empirical distribution of standardized by the consistent estimators of its theoretical mean and deviation with a standard normal distribution. Figure 3 shows that the standardized generalized correlation is very well approximated by a normal distribution.272727Although we correct for the bias, the empirical distribution is still slightly shifted to the left. Our bias correction term only takes into account the dominant bias term. We believe that correcting for higher-order bias terms can correct the remaining minor bias. Note that the remaining minor bias makes our test statistic more conservative, i.e., we are more likely to reject the null hypothesis.

Figure 4 shows the p-values and t-values of any paired state outcomes when the loadings are constant. From the subplot of p-values, we would conclude that the loadings are constant for almost all paired loadings. As we face a multiple testing problem, there exists, as expected, a small number of false rejections for a given significance level.

Simulations show the good power properties of the generalized correlation test. We assume the true underlying model has constant loadings in one interval and state-varying loadings in another interval. More specifically, data is generated such that loadings are constant in and linearly or quadratically depend on the state in . Table 1 shows the acceptance probability for the null hypothesis for a 95% significance level. When loadings in two states are different, the power of the generalized correlation test increases as or increases. The power is close to when the data size is at least .

| Loading linear in state | Loading quadratic in state | |||||

|---|---|---|---|---|---|---|

| (0.1, 0.9) | (0.25, 0.75) | (0.90, 0.95) | (0.1, 0.9) | (0.25, 0.75) | (0.90, 0.95) | |

| (50, 250) | 0.328 | 0.424 | 0.942 | 0.128 | 0.220 | 0.918 |

| (50, 500) | 0.014 | 0.044 | 0.938 | 0.000 | 0.002 | 0.932 |

| (50, 1000) | 0.002 | 0.000 | 0.952 | 0.000 | 0.000 | 0.970 |

| (100, 250) | 0.084 | 0.124 | 0.948 | 0.022 | 0.024 | 0.934 |

| (100, 500) | 0.000 | 0.002 | 0.954 | 0.002 | 0.002 | 0.938 |

| (100, 1000) | 0.000 | 0.000 | 0.954 | 0.000 | 0.000 | 0.954 |

| (200, 250) | 0.014 | 0.014 | 0.942 | 0.002 | 0.000 | 0.940 |

| (200, 500) | 0.000 | 0.000 | 0.934 | 0.000 | 0.000 | 0.964 |

| (200, 1000) | 0.000 | 0.000 | 0.946 | 0.000 | 0.000 | 0.946 |

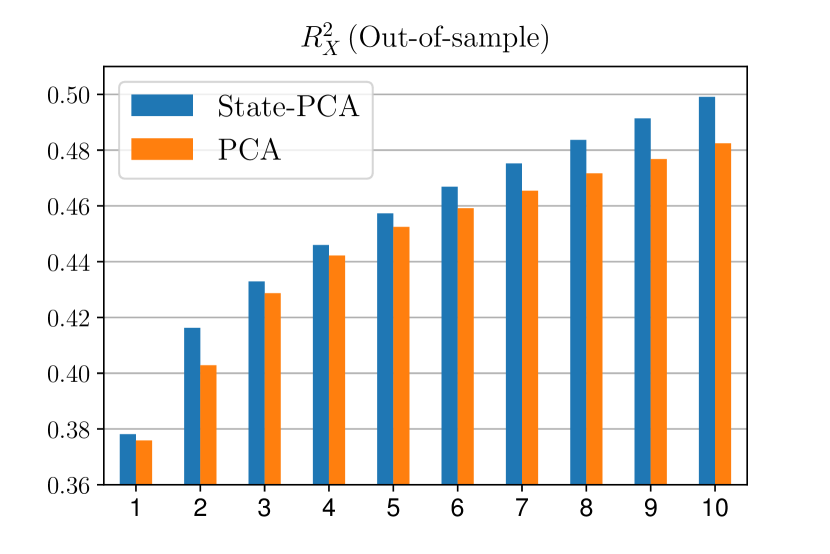

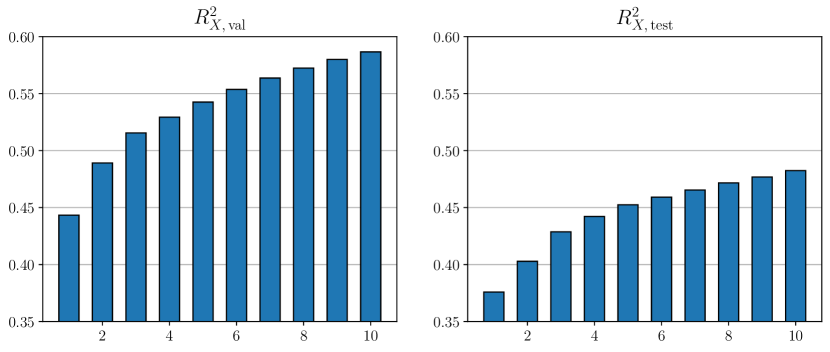

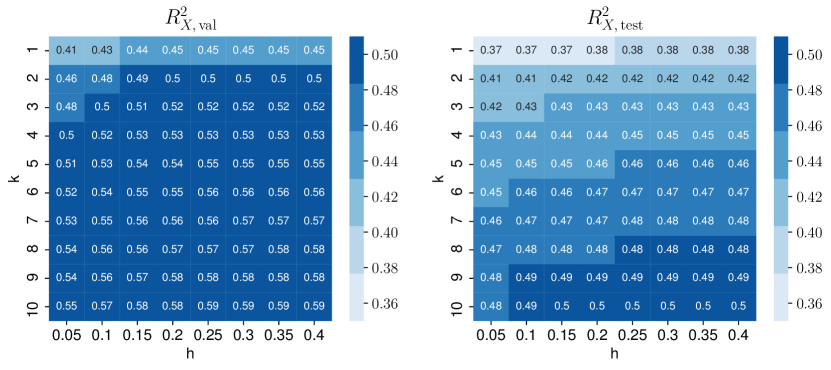

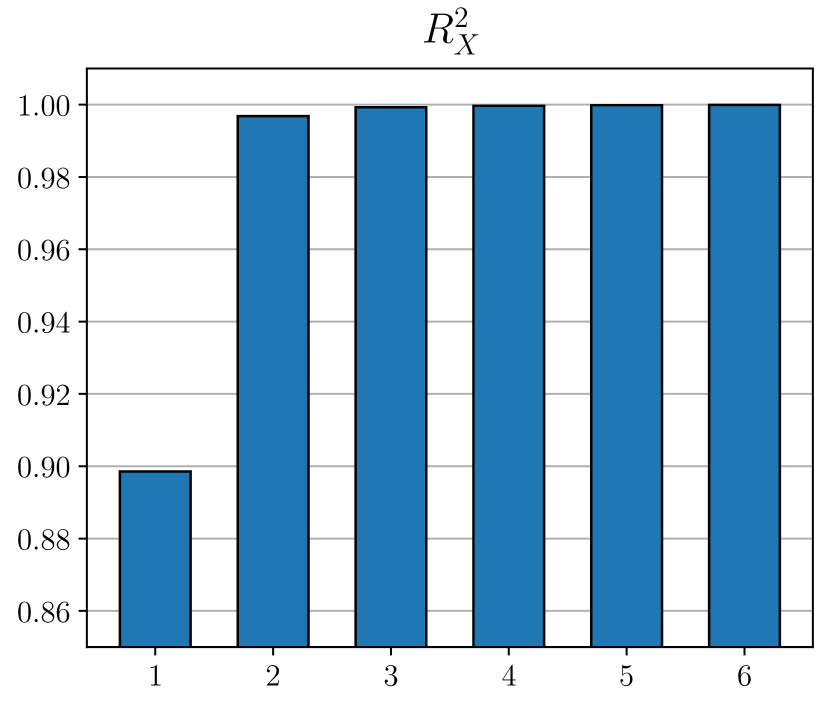

7.3 Variation Explained by Factor Models

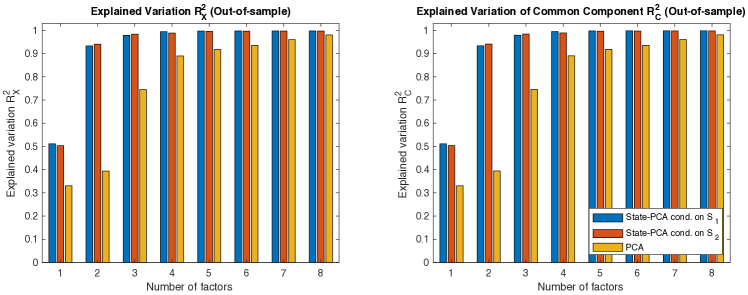

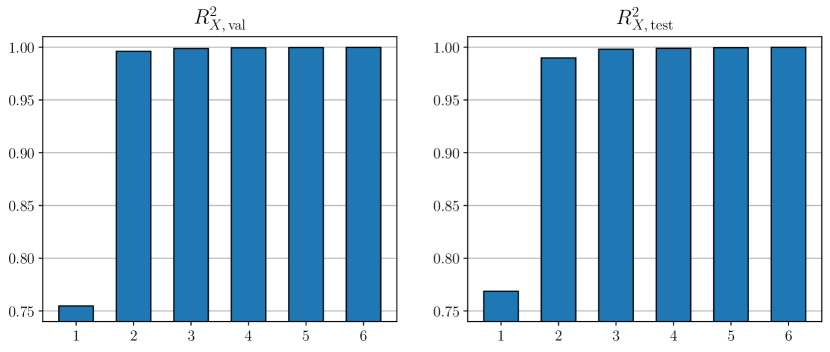

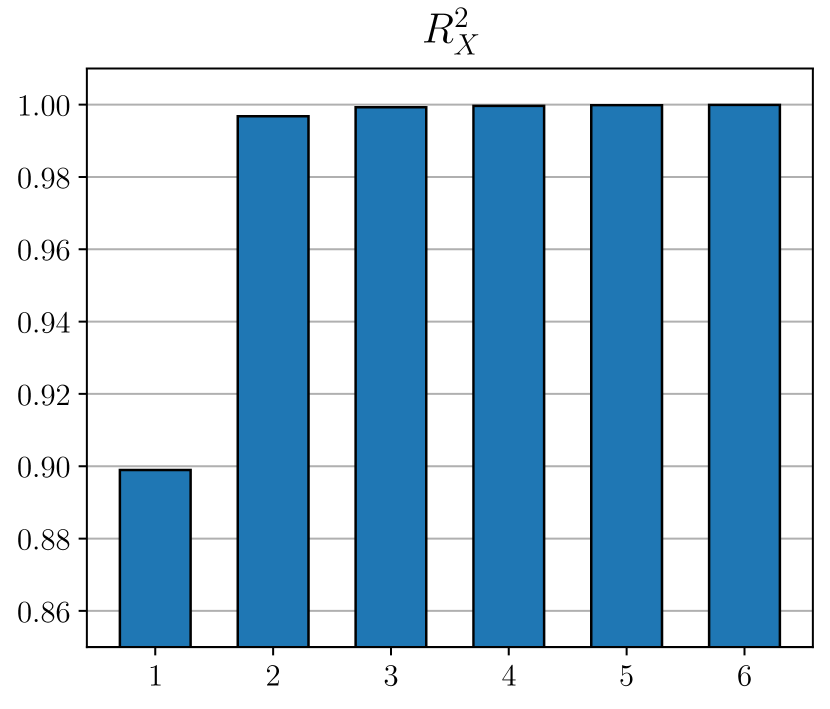

We compare the amount of explained variation for the constant and state-varying factor model under misspecification. We consider a state observed with noise and a missing relevant state. Our simulation results confirm that our estimator is robust to noise in the observed state process and provides a more parsimonious model than a constant loading model as long as we condition on a process that is related to the underlying state process.

We compare the in- and out-of-sample explained variation of and the common component for different factor estimators. The explained variation labeled as and is defined as

where the common component is either based on a state-varying or constant loading model. The out-of-sample common component projects the loading functions estimated in-sample on the out-of-sample observations, i.e. . For the out-of-sample results we use the first time-series observations to estimate the loadings and test the model out-of-sample on the second observations.

Table 2 reports the explained variation for a noisy state process. This model can also be interpreted as a missing state process. Even when the noise has the same magnitude as the state process, the explained variation is very close to the case of using the true state. In contrast, the constant loading model explains one third less of the variation with the same number of factors.

| In-sample | Out-of-sample | |||

|---|---|---|---|---|

| State-Varying Model: | 0.677 | 0.987 | 0.643 | 0.982 |

| State-Varying Model: | 0.676 | 0.985 | 0.642 | 0.980 |

| State-Varying Model: | 0.653 | 0.952 | 0.611 | 0.934 |

| State-Varying Model: | 0.616 | 0.894 | 0.559 | 0.856 |

| State-Varying Model: | 0.569 | 0.818 | 0.490 | 0.749 |

| Constant Loading Model | 0.442 | 0.650 | 0.427 | 0.653 |

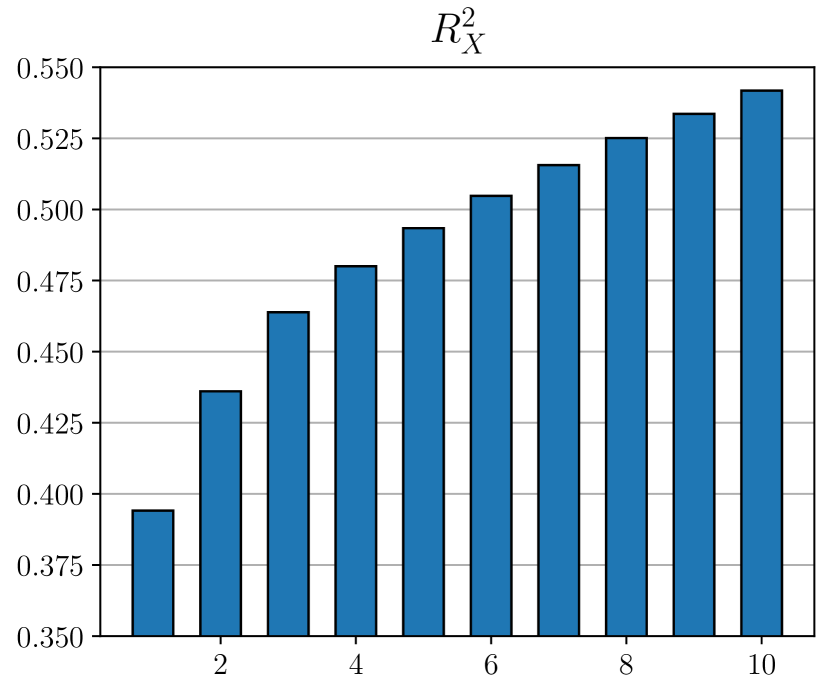

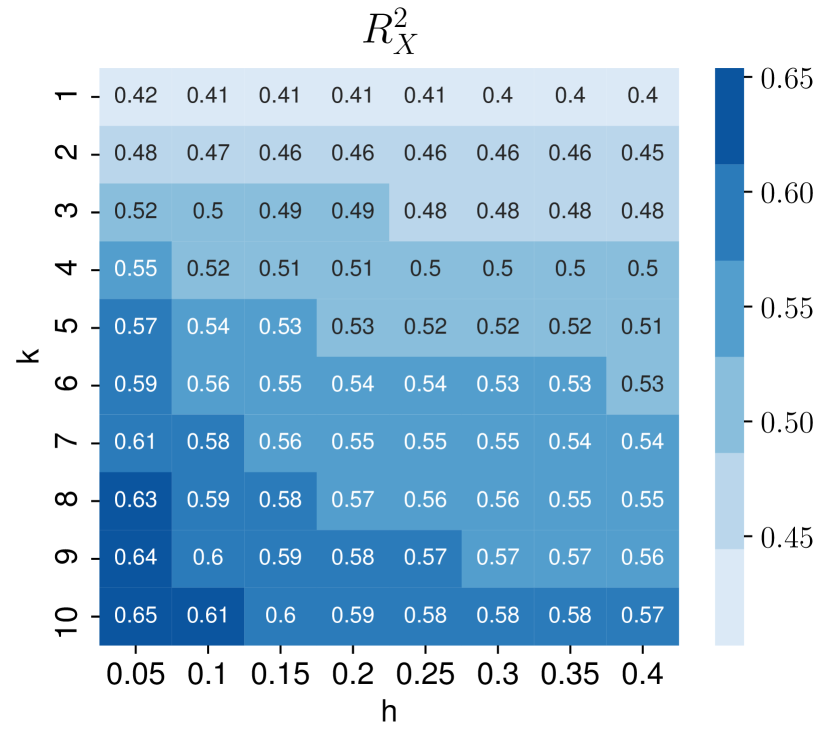

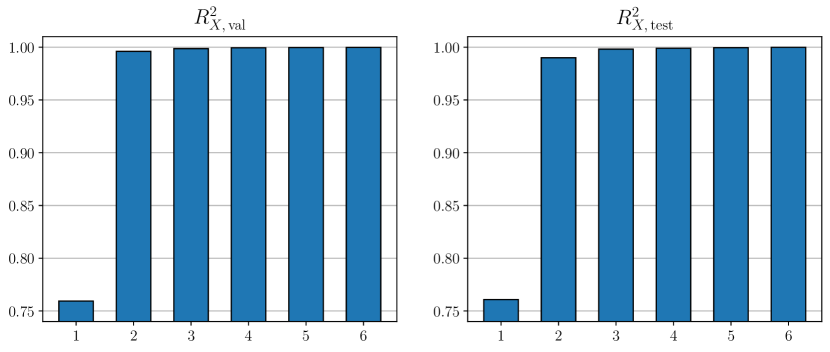

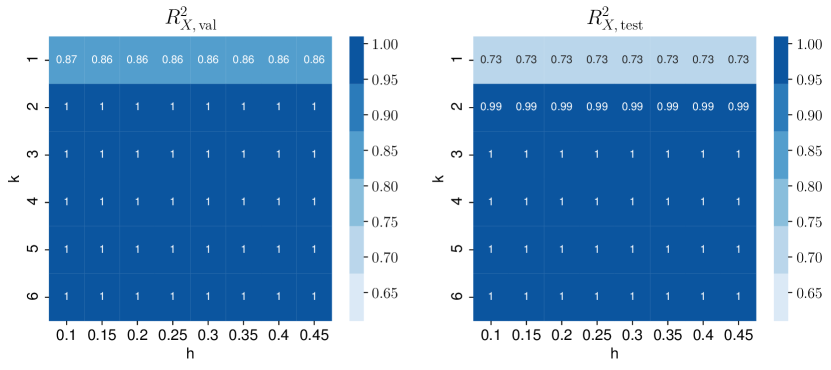

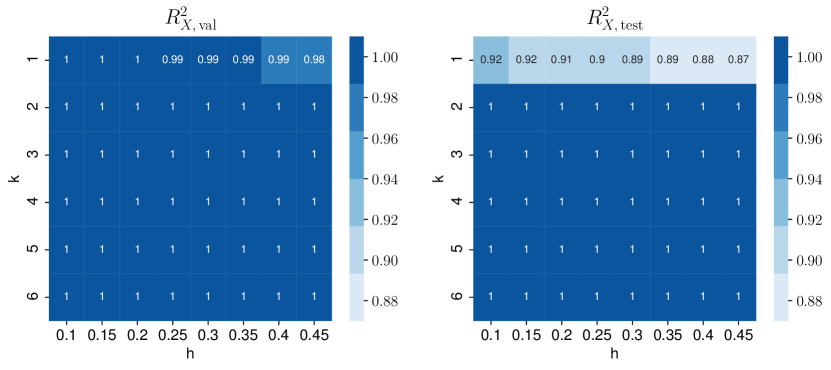

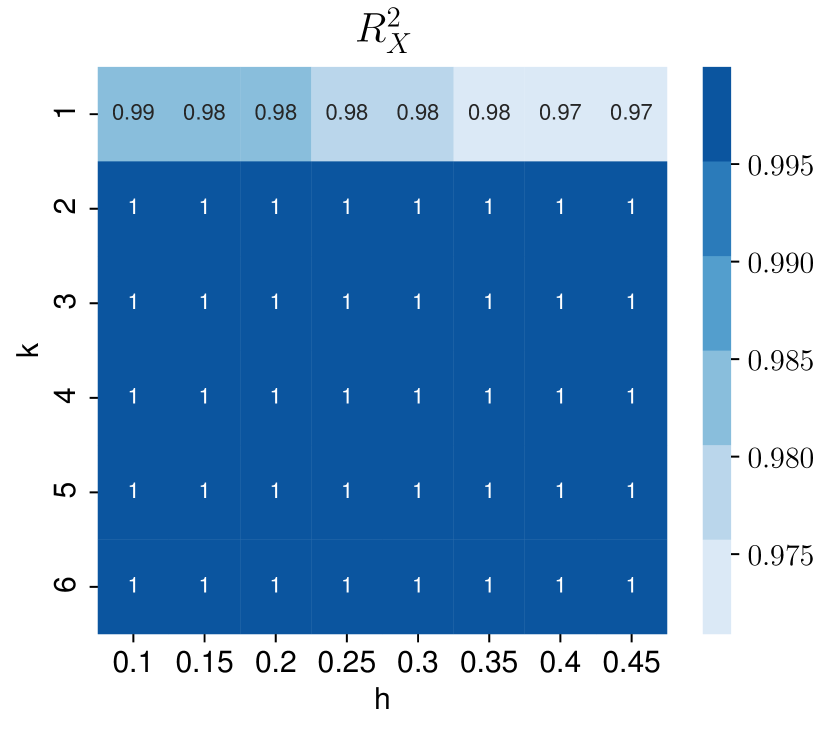

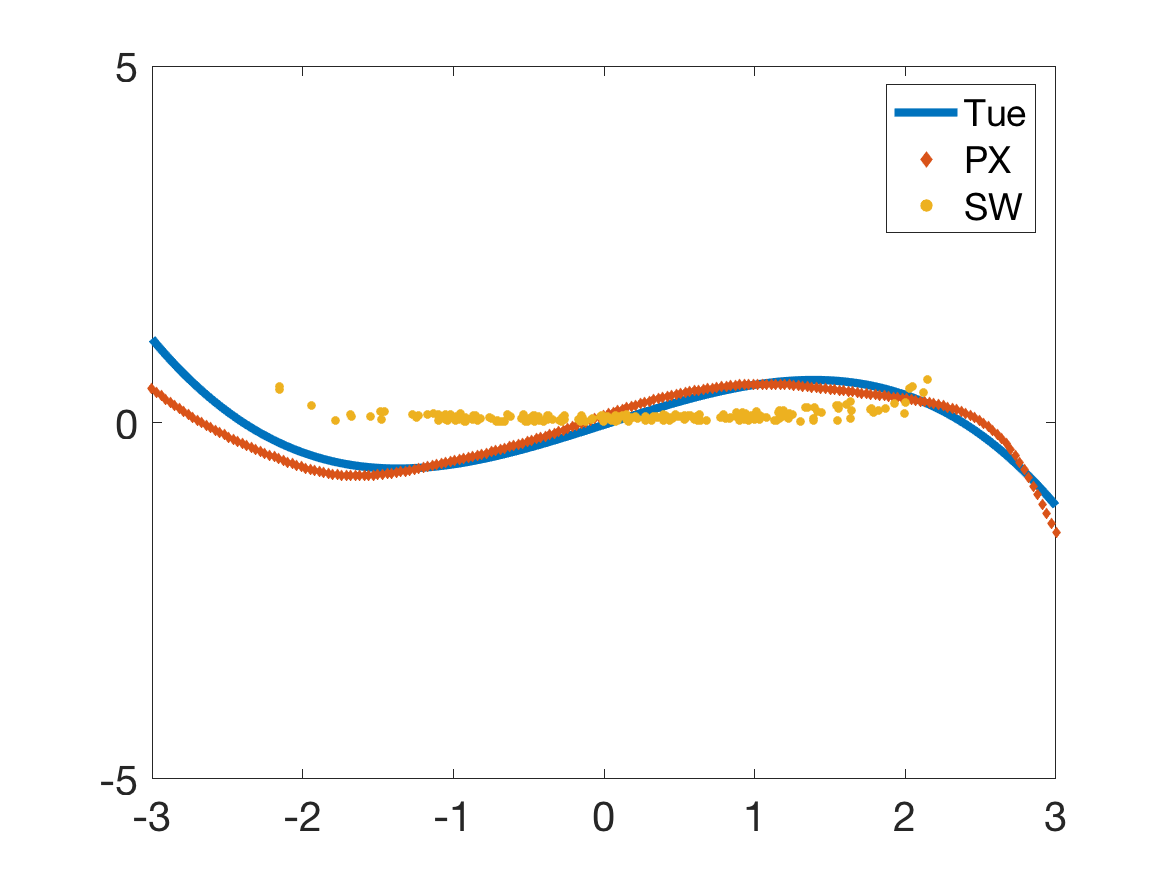

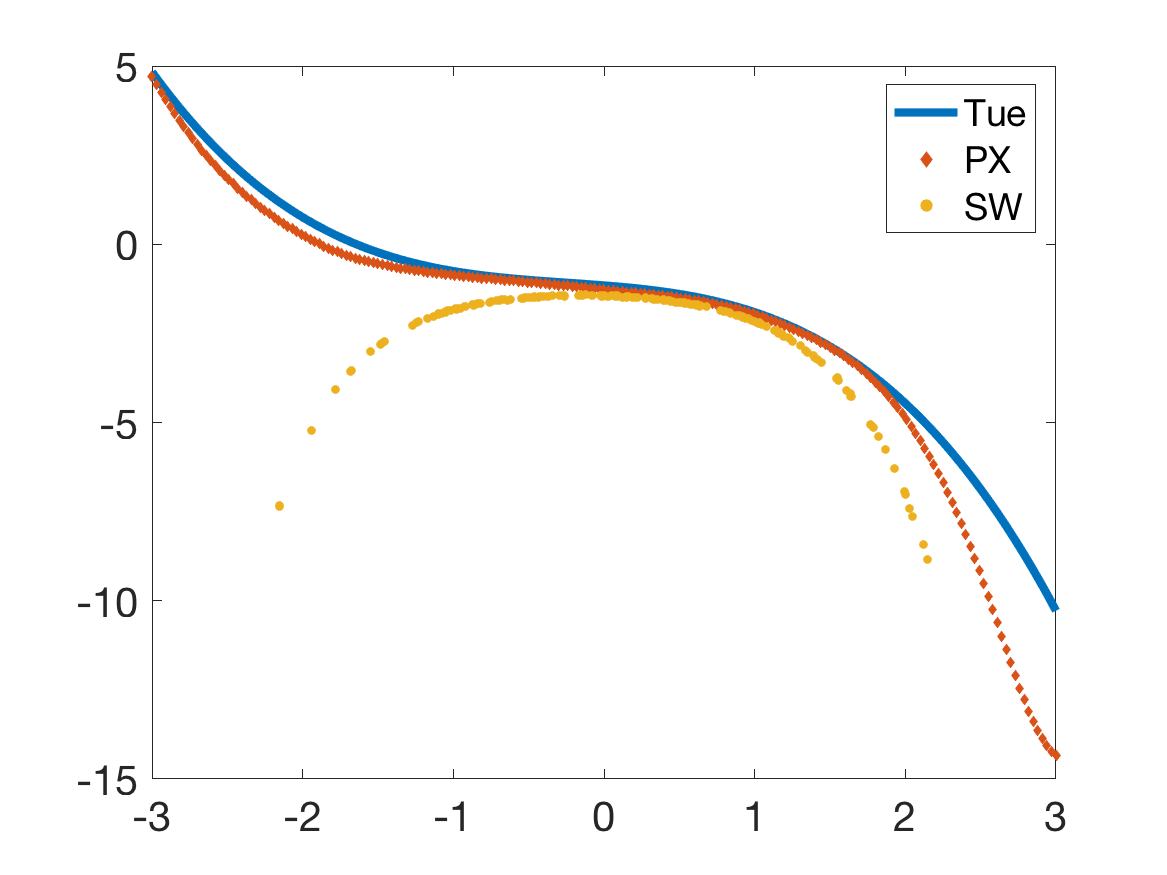

Figure 5 considers missing a systematically relevant state in a non-linear state function. In this case, both the state-varying and constant loading model are misspecified. The loading function is modeled as where the two independent states follow the same distribution as in Section 7.1. We condition only on one state process and calculate the explained variation in and the common component out-of-sample. As before, we estimate the model on the first half of the data to obtain the out-of-sample fit on the second half. Conditioning on both state variables should yield a model with a high explained variation with only one factor. Both the state-dependent model with one state and the constant loading model do not explain a large amount of variation with one factor. However, the state-varying loading model with two factors can almost perfectly explain the variation out-of-sample. In contrast, the constant loading model requires eight factors to capture the same amount of variation as a misspecified state-dependent model with two factors. This is exactly the same pattern that we observe in our empirical analysis of stock returns.

8 Empirical Application to U.S. Treasury Securities

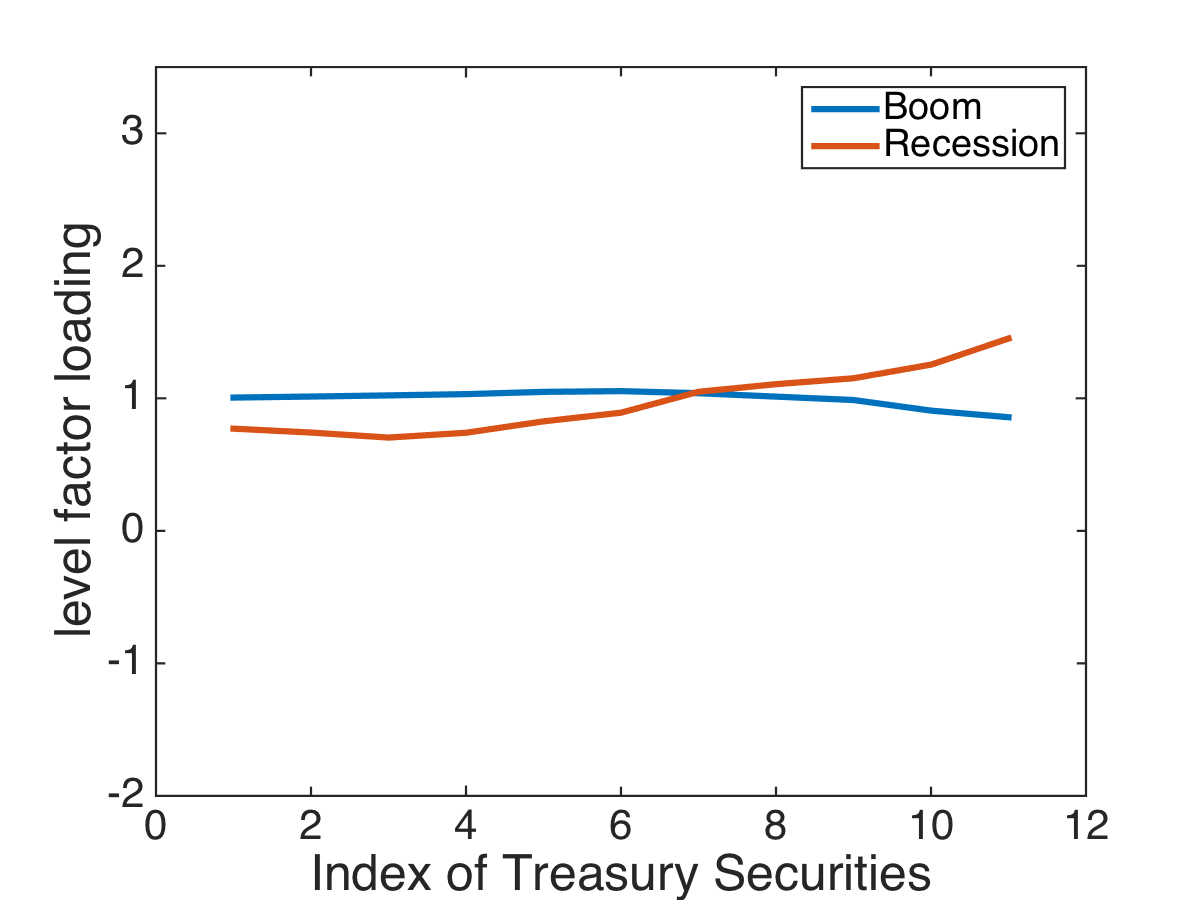

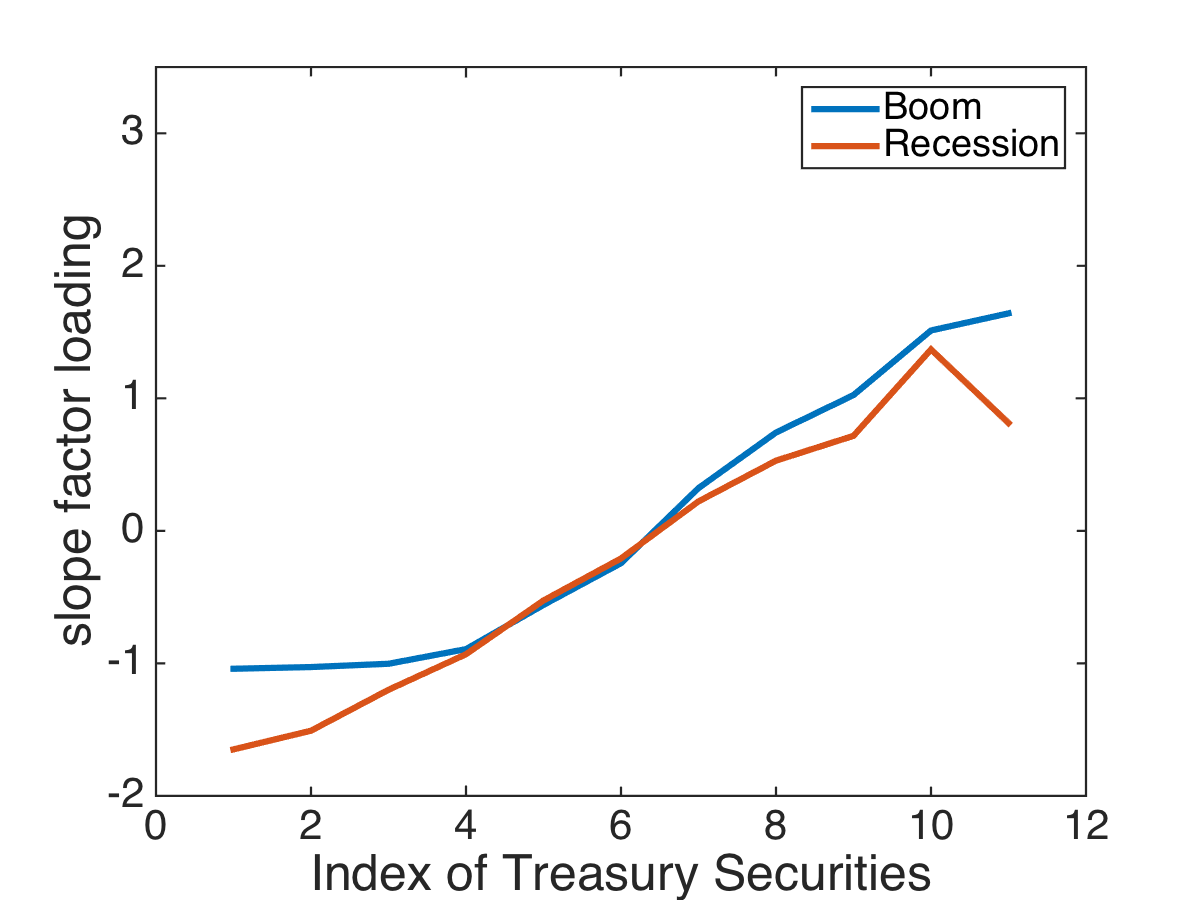

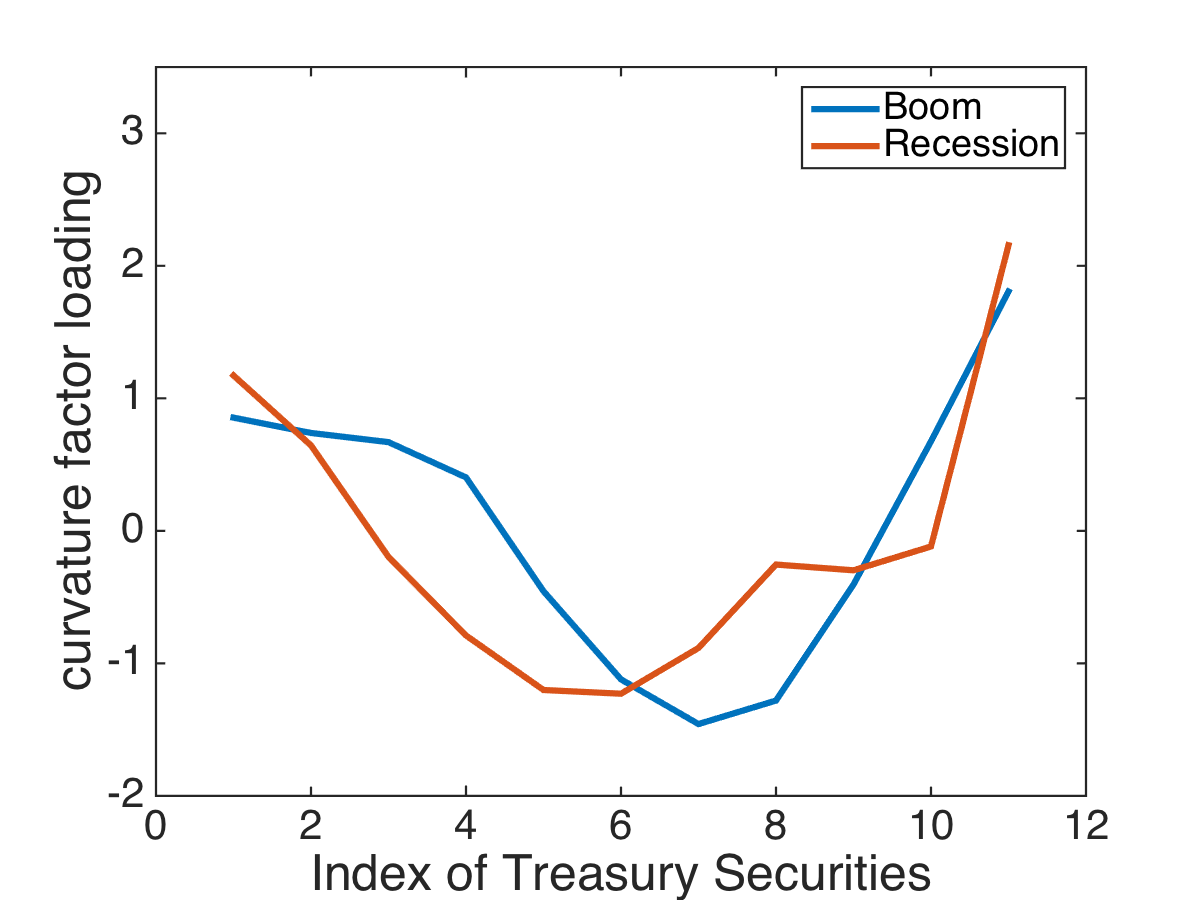

We apply our approach to the treasury securities market and show that the factor structure changes with economic conditions. The U.S. Treasury yield structure has been shown to be well explained by the first three principal components.282828See Diebold, Piazzesi, and Rudebusch (2005), Diebold and Li (2006), Cochrane and Piazzesi (2005) and Cochrane and Piazzesi (2009). The first three PCA factors are commonly referred to as the level (the long rate), slope (a long minus short rate), and curvature factor (a short and long rate average minus a mid-maturity) and can characterize the yield curves for different maturity bonds. We analyze how these three factors are influenced by three different macro-economic state variables. First, we use an NBER-based boom and recession indicator as a discrete state process. Second, we condition on the CBOE Volatility Index (VIX). Third, we model macro-economic conditions using the U.S. unemployment rate. Our findings strongly support a time-varying factor structure.

The data set is daily data of the U.S. Treasury Securities Yields from 07/31/2001 to 12/01/2016. The terms range from 1, 3, 6 months to 1, 2, 3, 5, 7, 10, 20, 30 years. We first separate the data into booms and recessions based on NBER-based recession indicators and estimate a factor model for each state. Figure 6 shows the loadings for the first three factors. The level, slope, and curvature patterns of loadings versus bond terms persist in the loadings in the boom and in the loadings in the recession. However, there are differences in the values of the loadings, or the composition weights in the factors in the two different states.

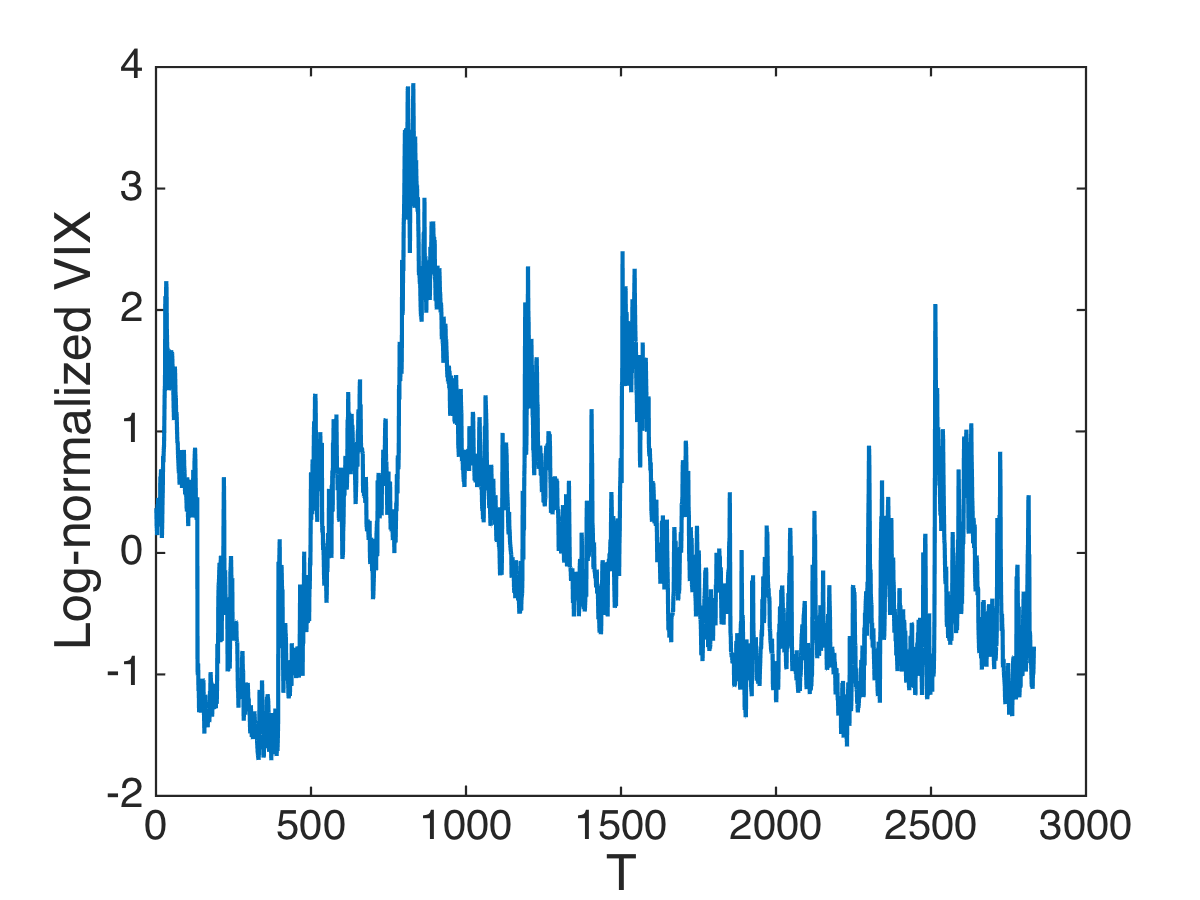

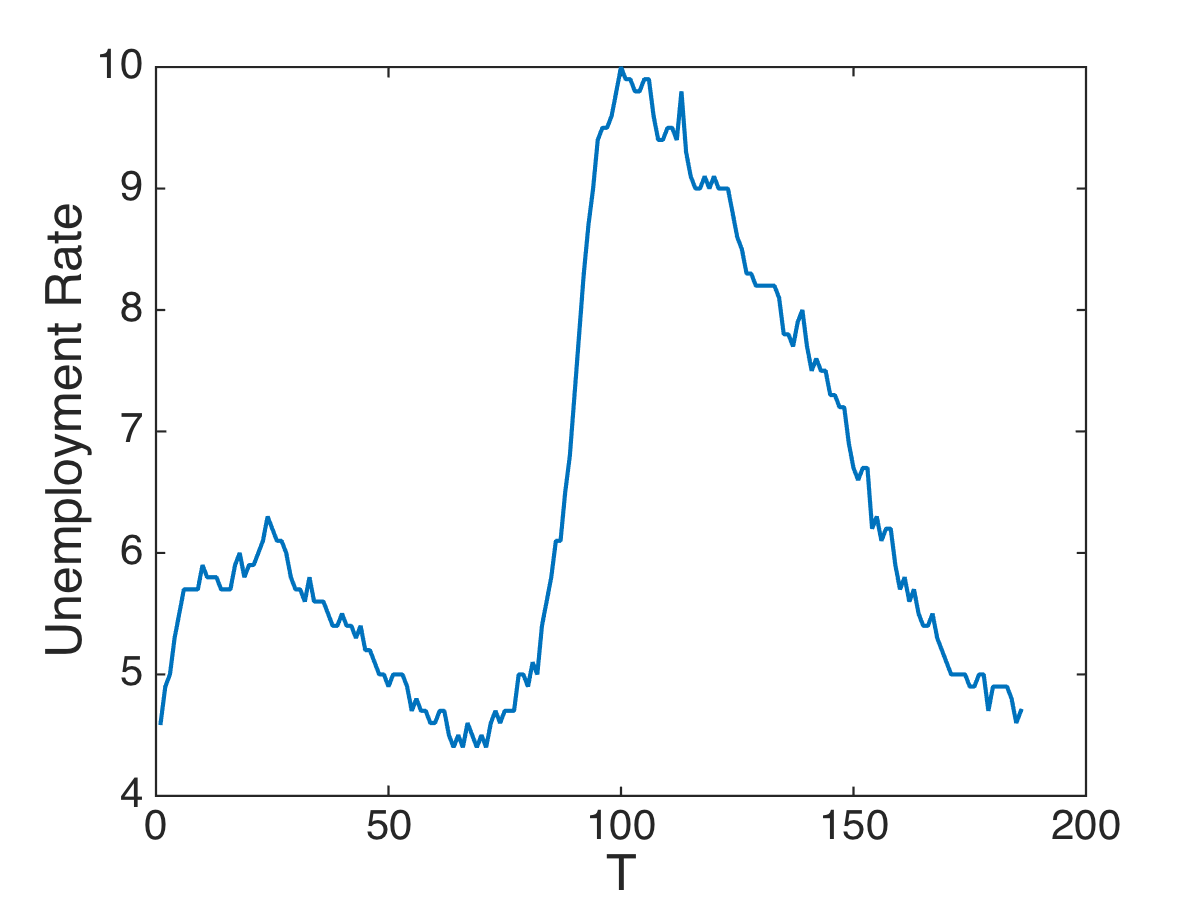

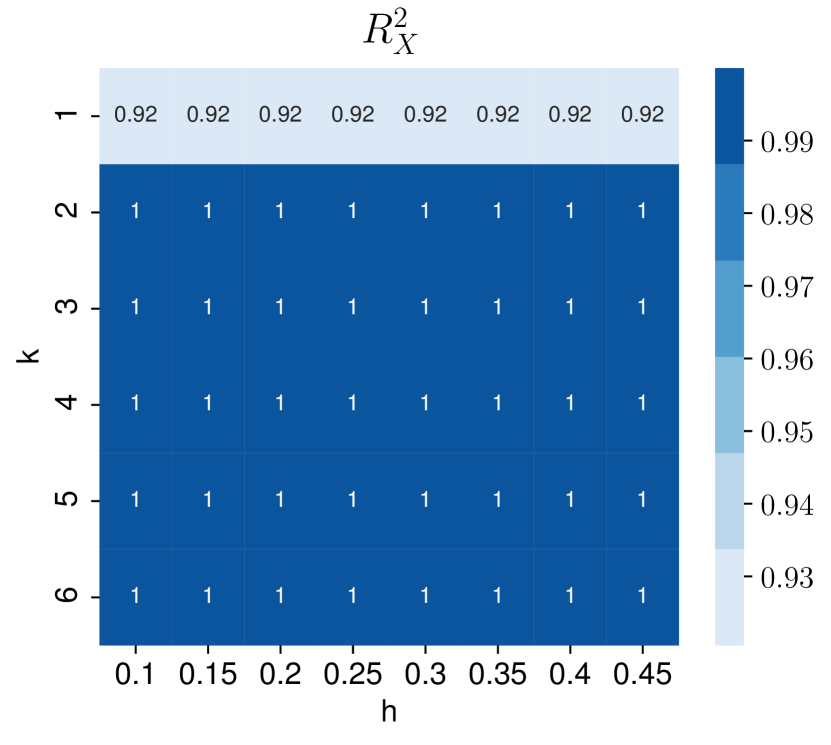

It is coarse to characterize macro-economic conditions by only two state outcomes. The volatility index VIX and the unemployment rate can be viewed as continuous state processes that will provide a more refined analysis of the state-dependency. The CBOE Volatility Index (VIX) is a measure of the implied volatility of S&P 500 index options. A higher VIX indicates a more volatile market. Typically a recession coincides with a high VIX. We use the standard convention of logarithmic VIX values to account for its heavy tails on the right. Figure 7(a) shows that the log-normalized VIX seems to be recurrent, as required by our methodology.

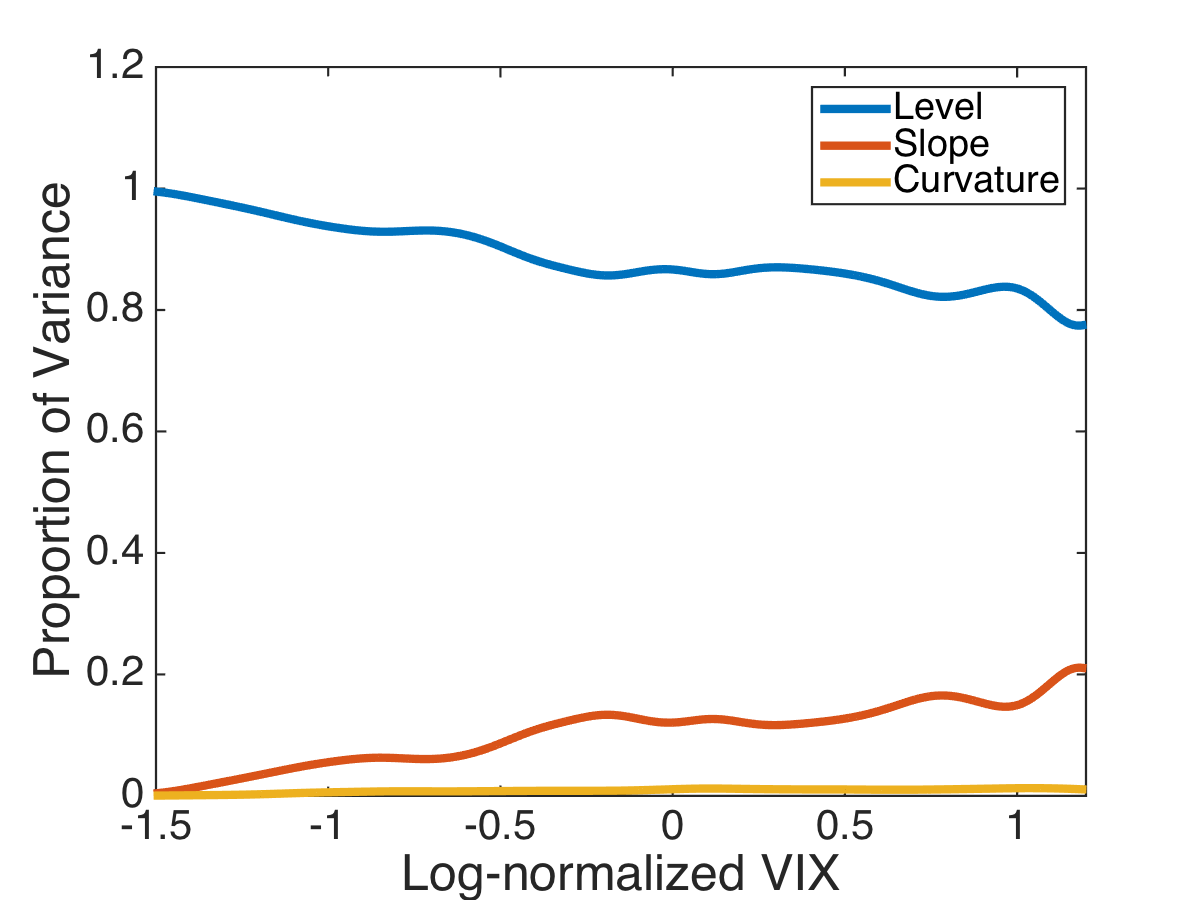

We estimate a factor model conditional on every possible log-normalized VIX value. We choose the bandwidth and confirm in the Internet Appendix that our results are robust to this choice. Figure 7(b) shows the variance explained by the first three factors. The level factor becomes less dominant as VIX goes up. Meanwhile, the slope factor becomes more important as the VIX increases. In a more volatile market, more yield movements are explained by the long minus short rate changes.

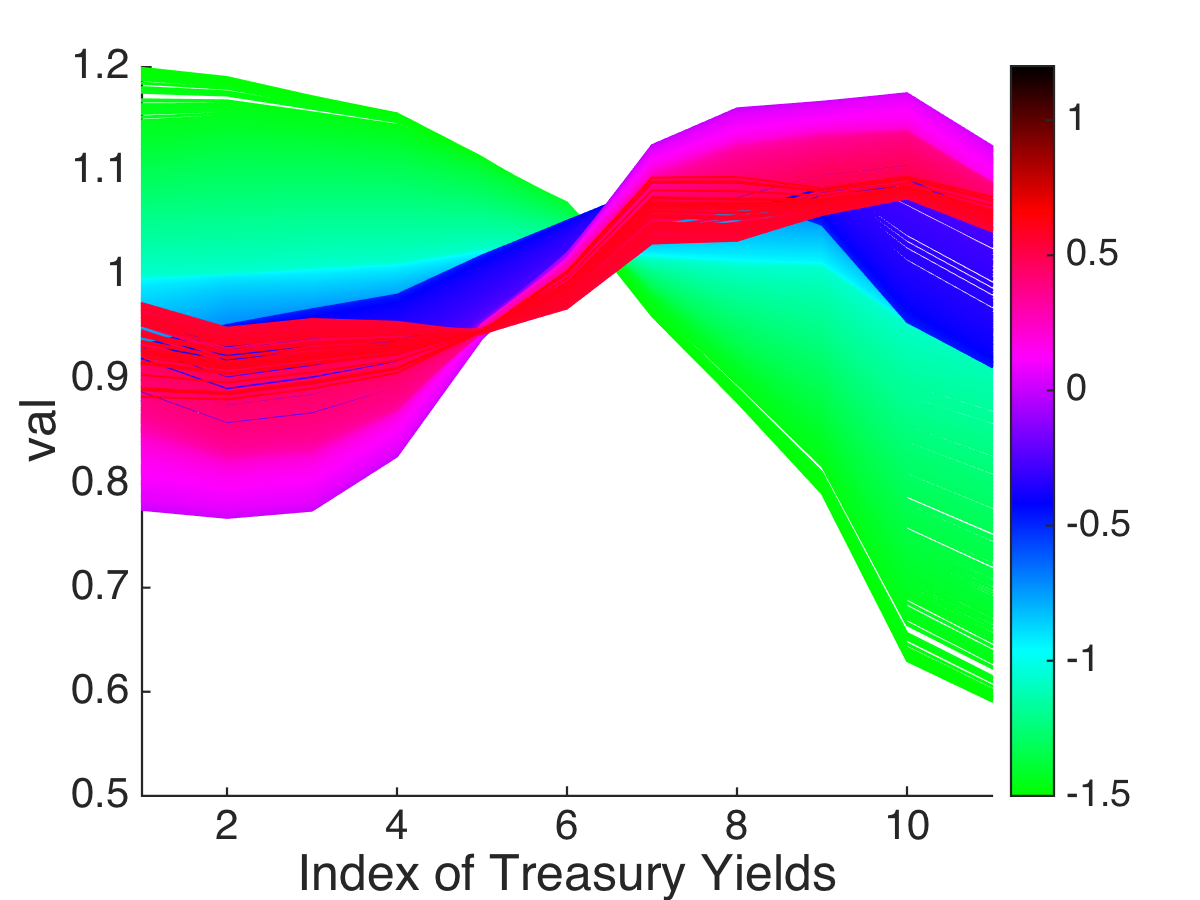

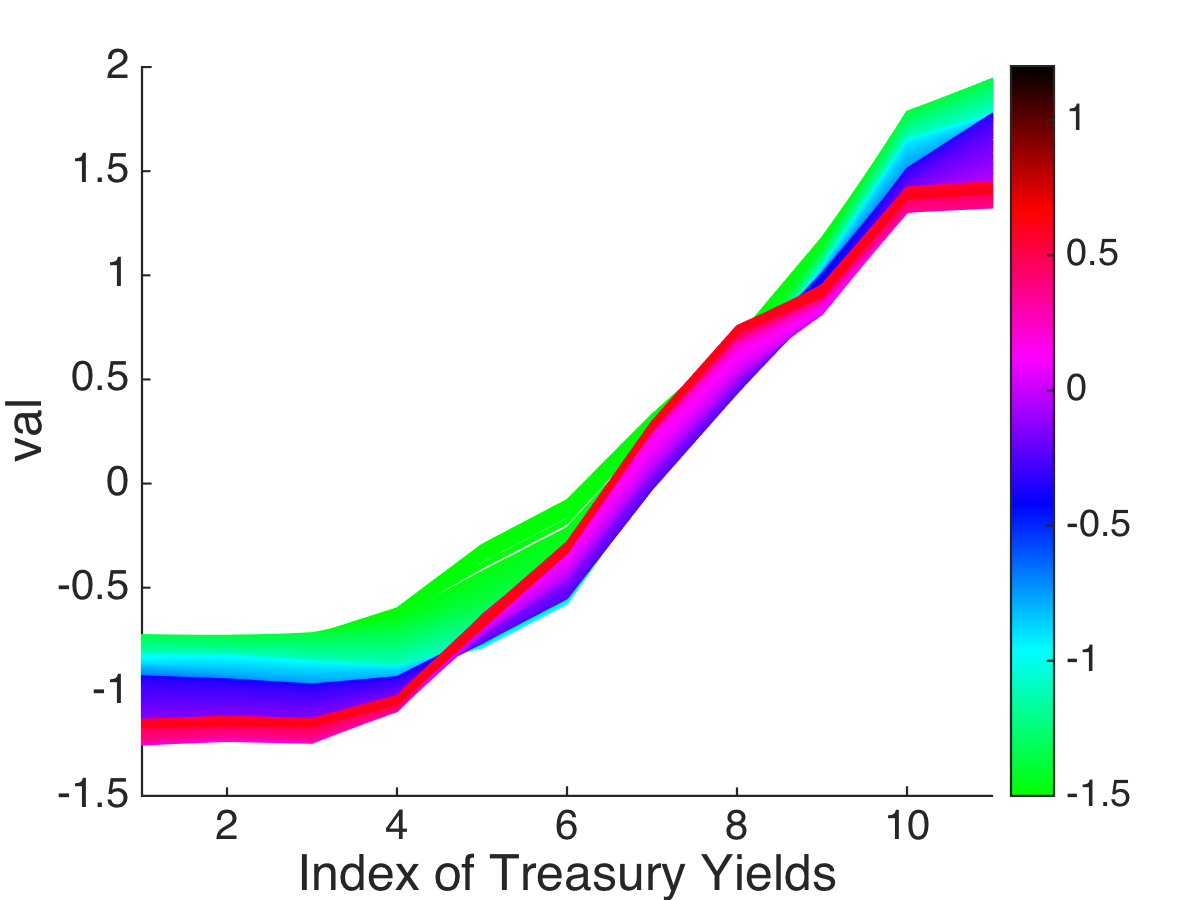

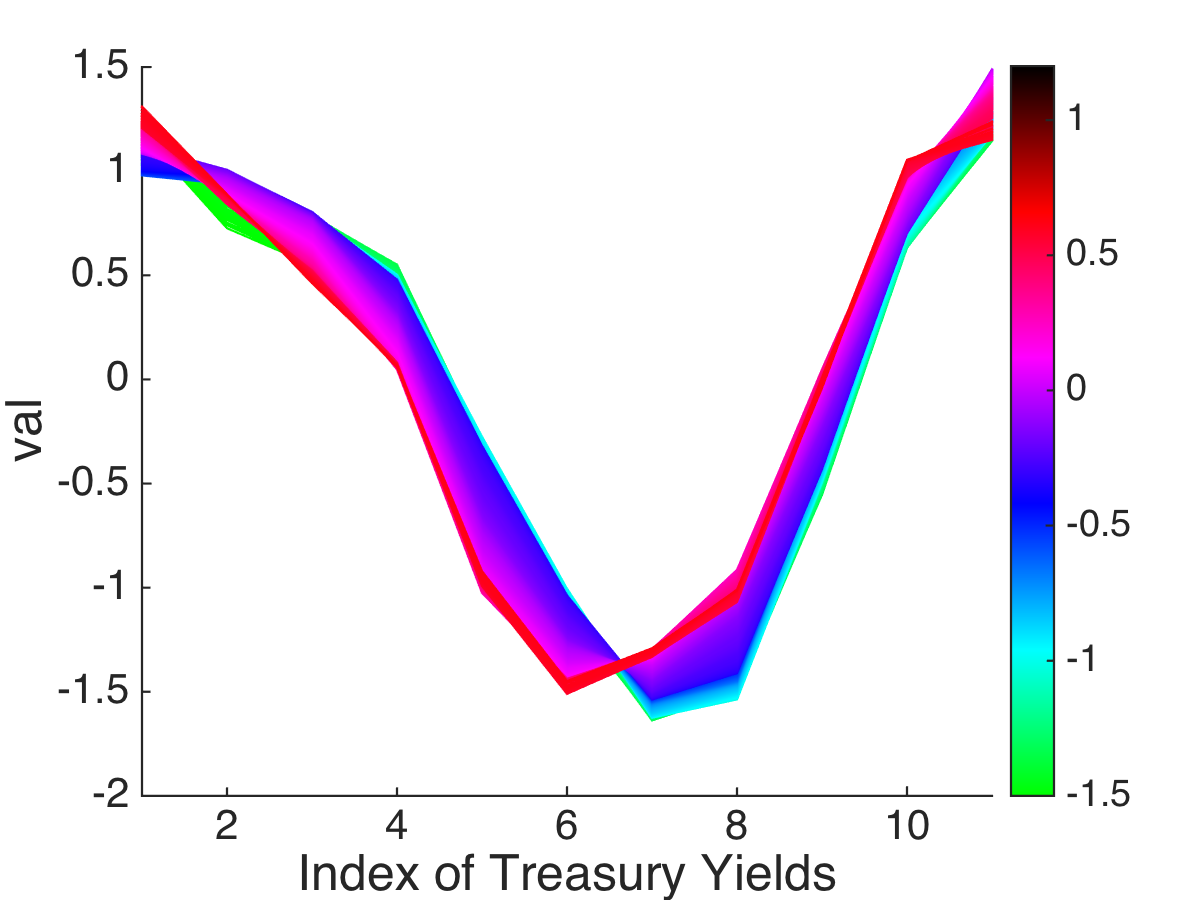

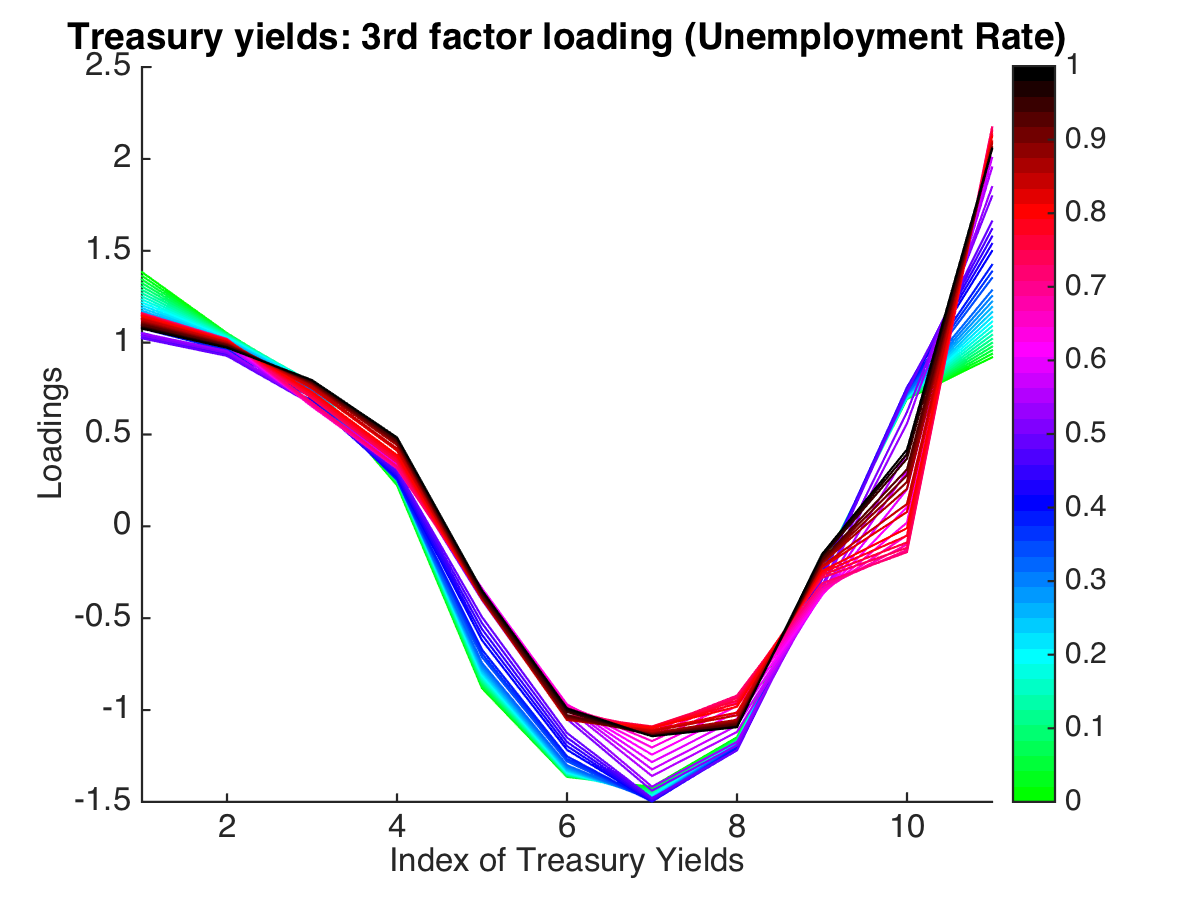

Figure 8 shows how the loadings change with the VIX. The color bar indicates the log-normalized VIX value. Green curves represent loadings in low VIX states. Purple and red curves represent loadings in high VIX states. Even though the level, slope, and curvature patterns persist in all states, changes in the state variables lead to shifts in the curves of loadings versus bond terms, implying the changes of the compositions of level, slope, and curvature factors. For the level factor, longer-term bonds increase in weights as the VIX goes up. The loadings of the second factor, the slope factor, shift towards shorter maturities in more volatile markets. The curvature factor has a clear parallel shift to the left with increasing VIX. These results are consistent with the factor model conditioned on booms and recessions.

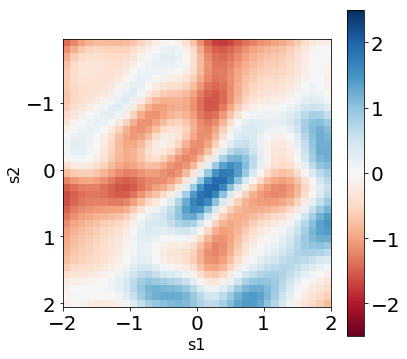

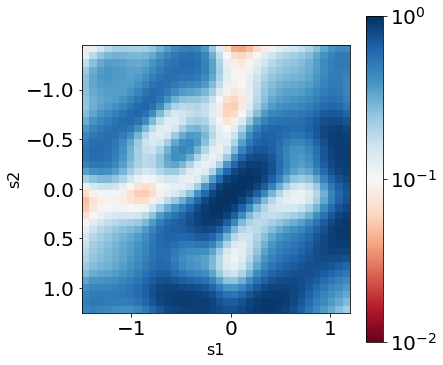

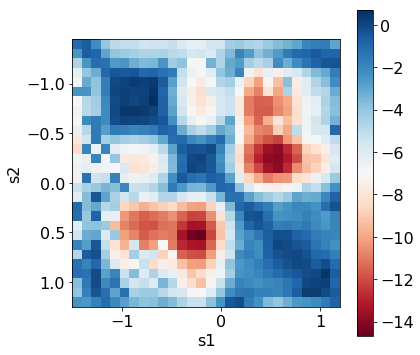

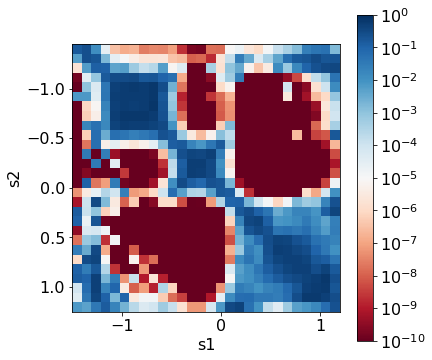

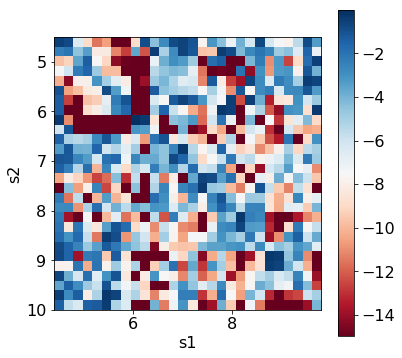

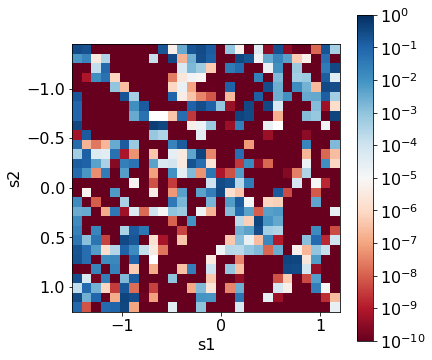

We use the generalized correlation approach to test for which states the factor structure changes. The previous results indicate that each of the first three eigenvectors changes with the VIX. However, it could be possible that the span of the eigenvectors does not change, i.e. it is possible that the factor structure is stable over time. Figure 9 shows the results for the generalized correlation test statistic and its p-values for any combination of two states and . As expected, the diagonal values take the largest values implying that the factor structure is very “close” for these paired states. The red regions represent changes in the factor structure. Apparently, the loading space is different in states with positive values (high VIX) from states with negative values (low VIX).292929Our test-statistic is not a global test for changes in the factor structure, but aims at comparing two specific states. In order to use our results for a global test the p-values would need to be adjusted to account for multiple hypothesis testing.

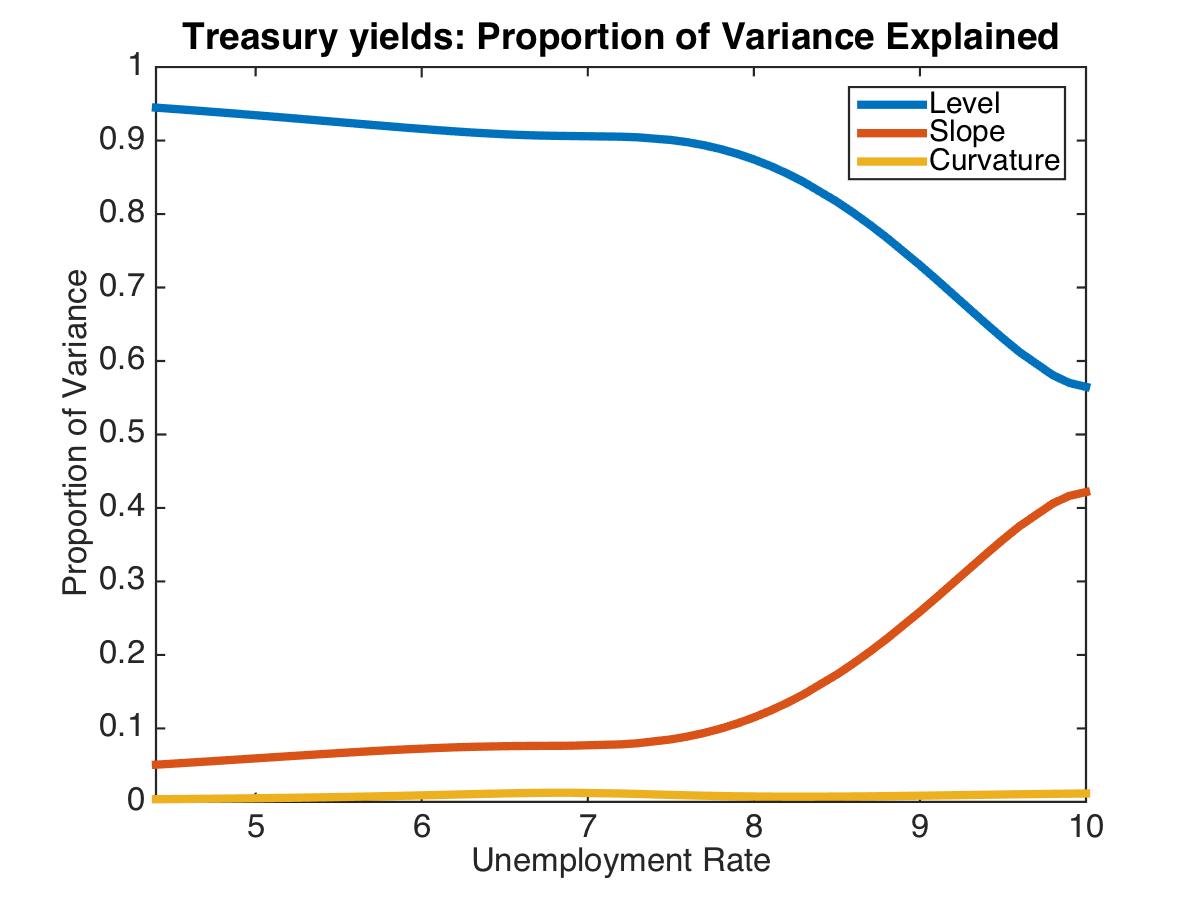

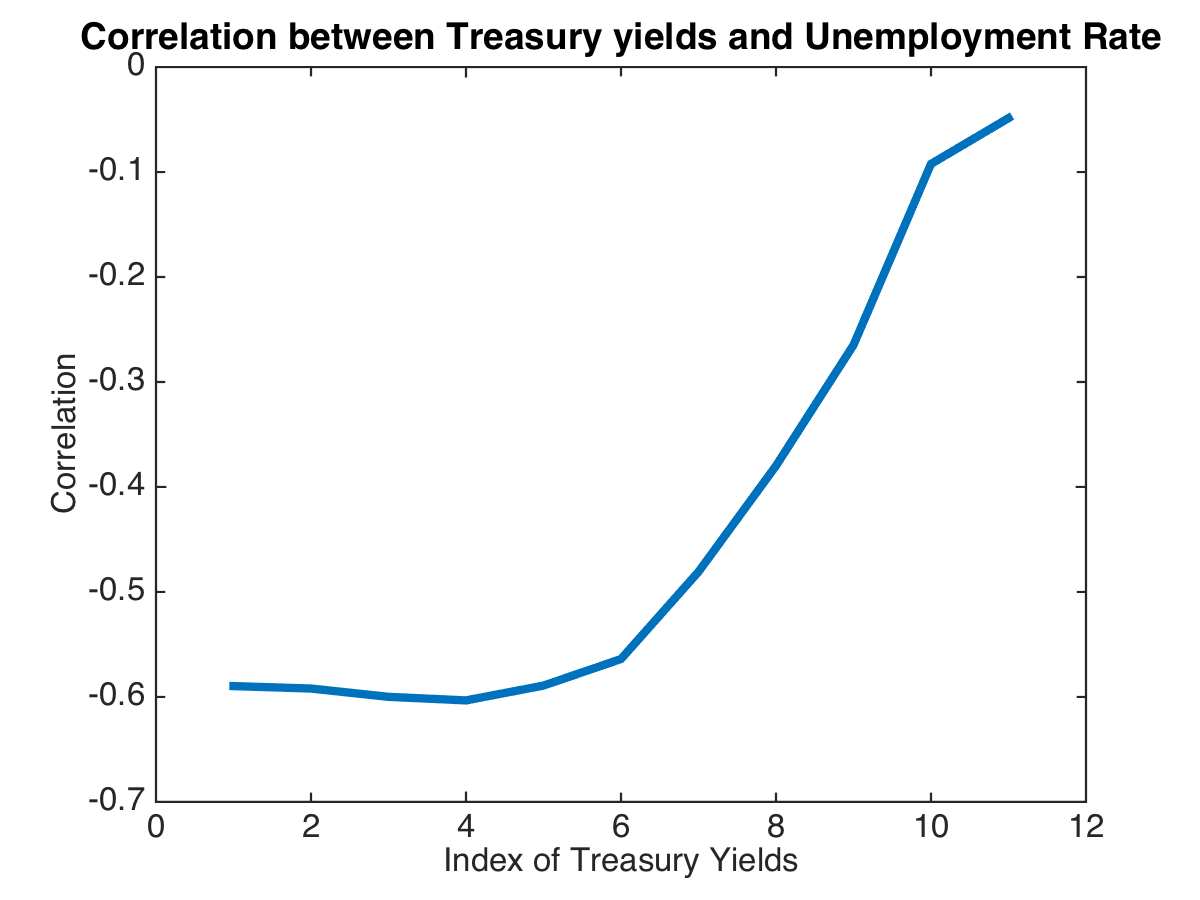

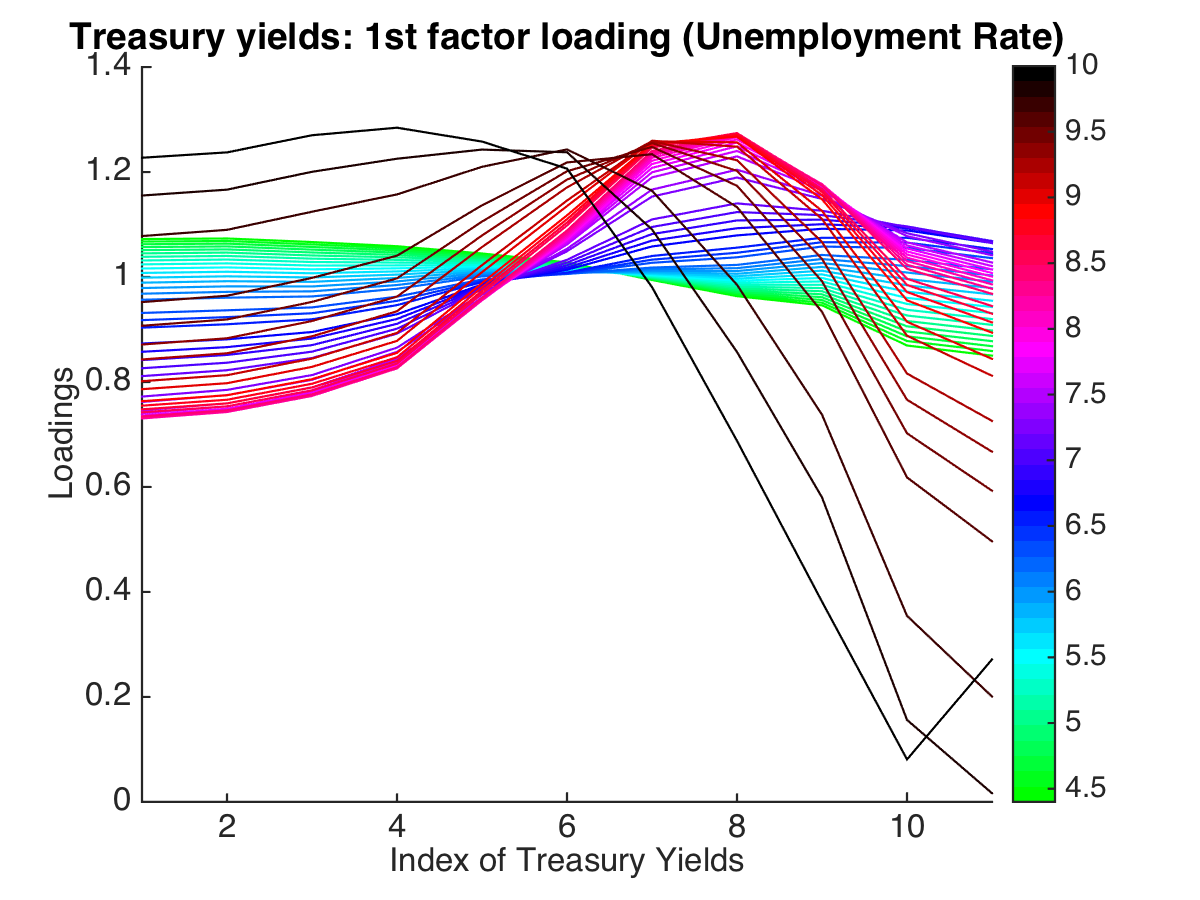

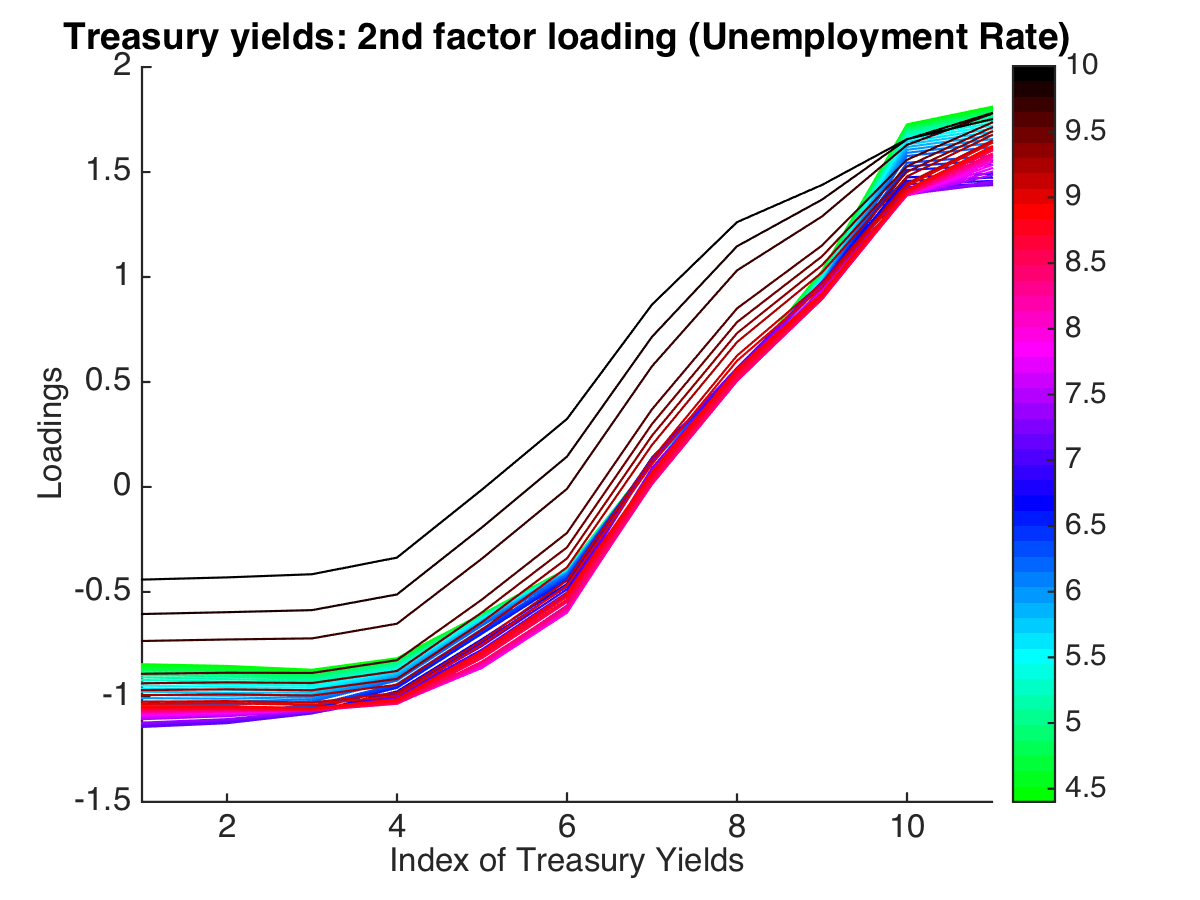

Furthermore, we use the U.S. unemployment rate as the third state variable. The results are very similar to the VIX as the state variable and delegated to the Internet Appendix. In the Internet Appendix, we also compare the amount of variation explained by different factor models. Treasury yields are somewhat special in the sense that their variation can almost perfectly be explained by three factors. The state-varying factor model with three factors explains slightly more variation, comparable to a four-factor model with constant loadings. However, if the goal is to explain variation, both a time-varying and a constant three-factor models perform well. The takeaway from this empirical application is to understand that the economic interpretation of “level”, “slope” and “curvature” has to be used with caution. Depending on the economic conditions, the first PCAs are different. The next application to individual stock returns shows that in other asset classes, the state-varying model can actually explain a significant larger amount of variation than its constant counterpart.

9 Empirical Application to Stock Returns

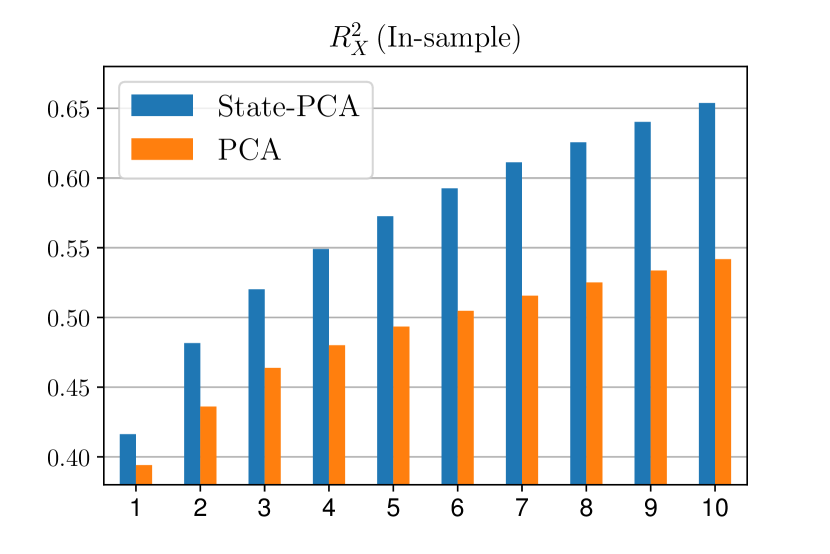

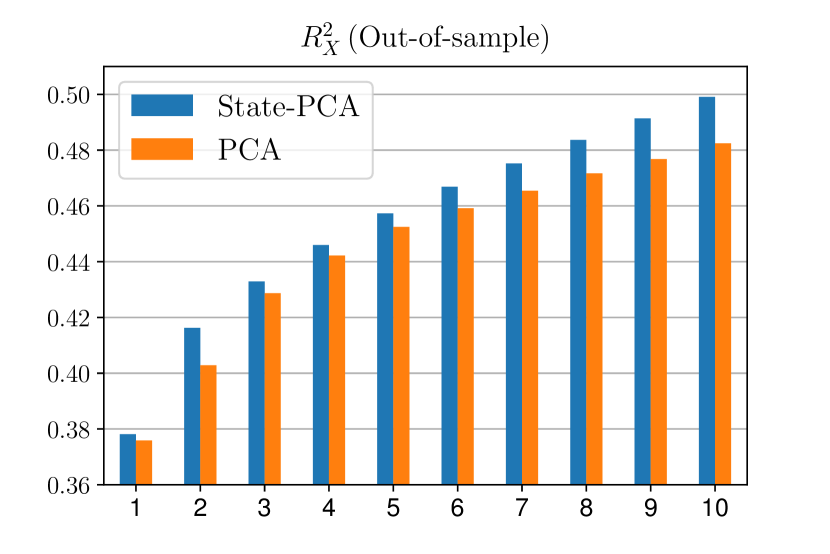

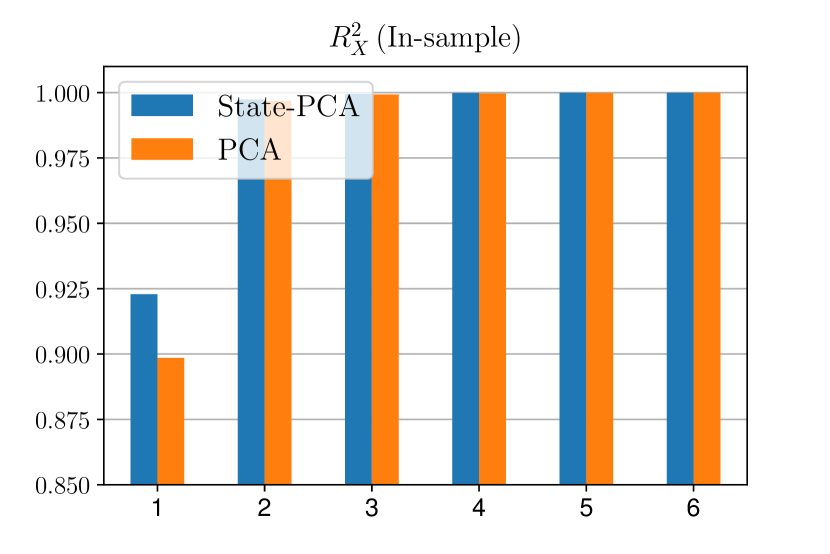

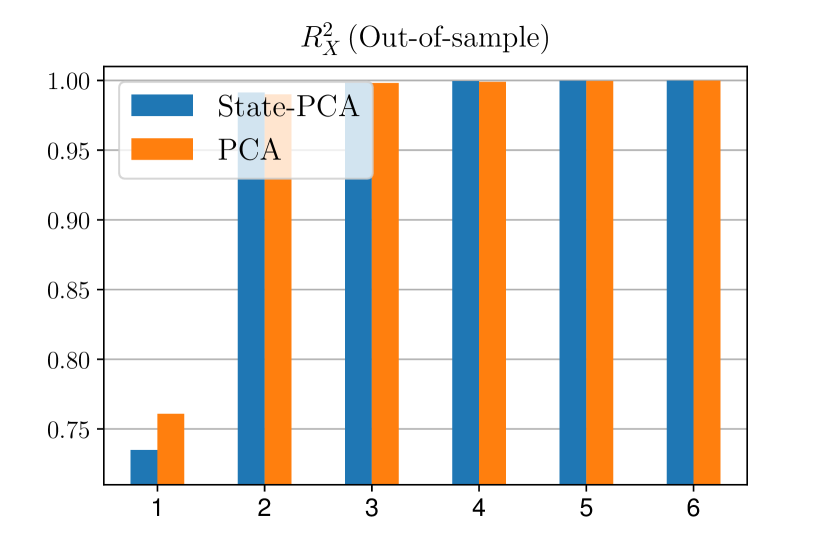

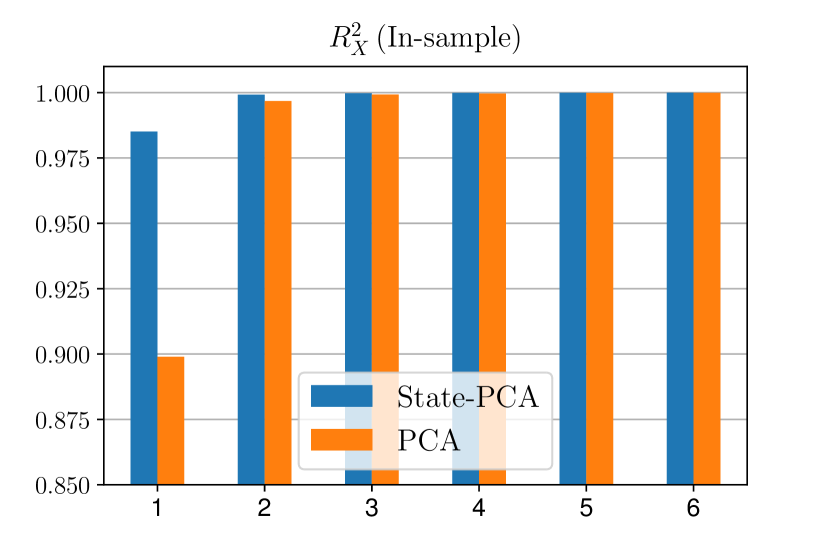

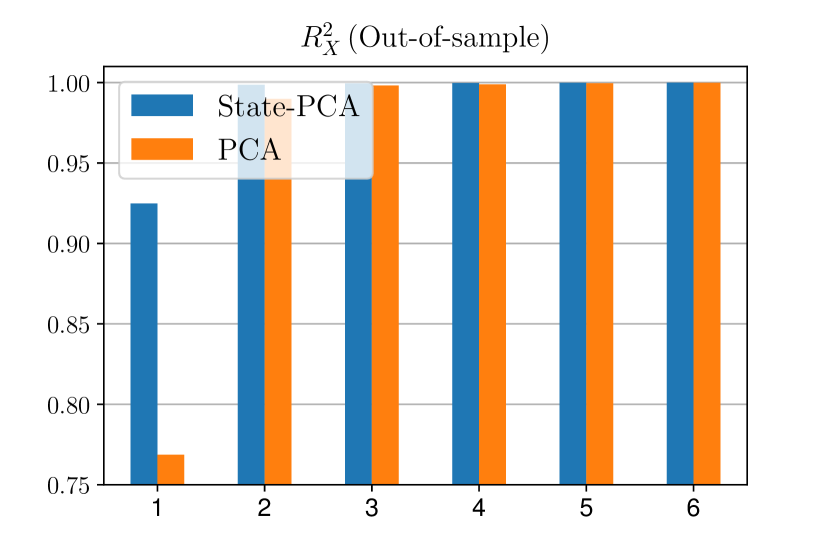

We estimate the latent factor structure in individual stock returns and show that the state-varying factor model is more parsimonious in explaining variation and captures more pricing information than the constant loading model. Our data set is the same as in Pelger (2020) and consists of the daily stock returns for the balanced panel of S&P 500 stocks from January 1st 2004 to December 31st 2016. We include only stocks with returns available for the full-time horizon, which leaves us with a panel of and . We supplement the data with the daily risk-free rate from Kenneth French’s website. As before, we condition on the log normalized VIX. We study the amount of variation explained by different factor models, the loadings for different states, and the optimal portfolio strategies implied by the factor models.

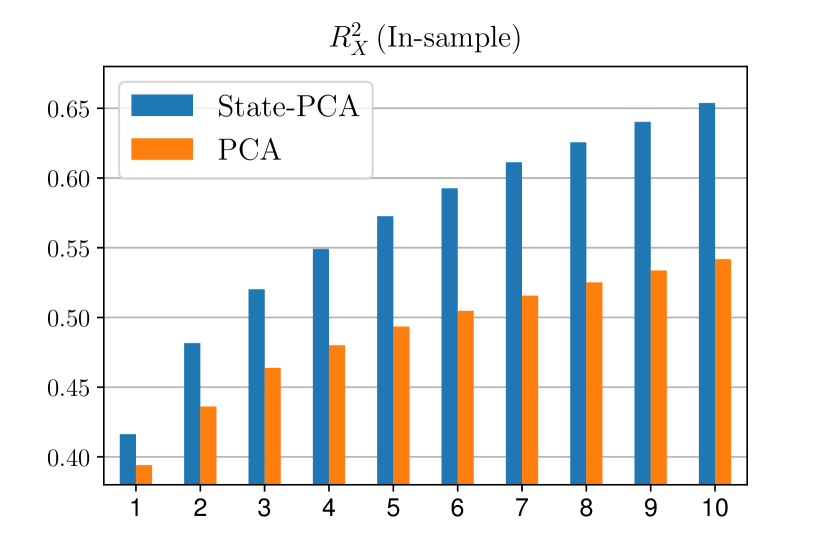

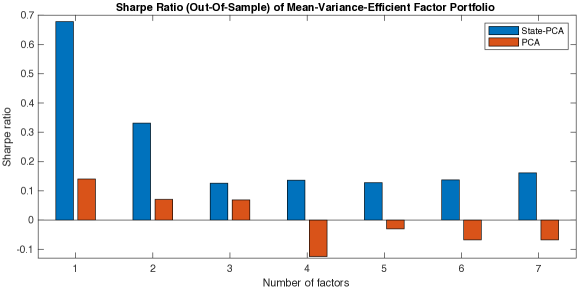

Figure 10 reports the explained variation in- and out-of-sample for the state-varying and constant loading model. For the out-of-sample results, we first estimate the loadings on the first three years of data and then update the loadings estimates on an expanding window to obtain the out-of-sample systematic component for the next ten years. Obviously, the state-varying factor model explains more variation than the constant loading model in- and out-of-sample for the same number of factors. Therefore, conditioning on the VIX results in a more parsimonious factor model to explain the co-movement in stock returns. Our results do not depend on a prior on the number of factors. In particular, it implies that stock returns do not follow a constant loading model and that the VIX is related to the source of time-variation. We do not require that the VIX explains all the time-variation in the loadings, but we show the conditional model provides a better description of the data than the unconditional one.

Figure IA.4 shows the test results for the generalized correlation test for the combination of any two state outcomes of the VIX. We use a five-factor model motivated by the five factors of Fama and French (2015) and Lettau and Pelger (2020b). The span of the loadings drastically changes with the realization of the VIX, which confirms the previous results. The Internet Appendix shows that, even in a one-factor model, the span of the state-varying loadings is different from a constant factor model and studies the portfolio implications of the time-varying factors.

10 Conclusion

The exposure of financial or macro-economic variables to factors may change with policies, macroeconomic environment, and technology innovation. Failing to correctly model the exposure may result in misspecifying factors and potentially inflating the number of factors identified in the model. We model these driving forces as a state process to build a state-varying factor model. We combine a nonparametric kernel projection with PCA to estimate the factor model in a particular state. Our model allows for general time-variation in the loadings for a given state. Asymptotic properties of estimated factors, loadings, and common components are presented. We develop a test for detecting changes in loadings at different states based on a generalized correlation statistic. Simulations show the good finite sample properties of our estimators and test statistic.

The analytical analysis is challenging for both the kernel estimator of the loadings, factors, and the test statistic because we have to take into account bias terms. We show under which conditions these bias terms can be neglected or how to estimate and correct for this bias. In turns out that our test statistic for changes in the loadings is non-standard with a super-consistent rate.

We believe that the proposed estimator and test statistic have wide applications in macro-economics and finance. In two empirical studies, we apply our estimators to U.S. Treasury securities and individual stock returns. In the first case, we use a recession indicator, the VIX, and the unemployment rate as state variables. In recessions, times of high volatility or times of high unemployment rate, the level factor explains less variance in the data and becomes less important, while the slope factor gains importance. In particular, the composition of the slope and curvature factors is shifted to shorter maturities in bad or volatile times. Based on our generalized correlation test, we identify the states for which the factor structure changes. The takeaway is that the economic interpretation of “level”, ”slope” and “curvature” has to be used with caution, as for different economic states, the PCA factors will be different. In the second application on individual stock returns, we show that the state-varying factor model with the VIX as state variable is more parsimonious in explaining variation and captures more pricing information than the constant loading model. Hence, even if we do not capture all time-variation in the loadings with the proposed state variable, we still obtain a model that explains the correlations structure and mean returns better than a constant loading model.

References

- (1)

- Ait-Sahalia and Xiu (2017) Ait-Sahalia, Y., and D. Xiu (2017): “Using principal component analysis to estimate a high dimensional factor model with high-frequency data,” Journal of Econometrics, 201(2), 384–399.

- Ait-Sahalia and Xiu (2019) Ait-Sahalia, Yacine, Y., and D. Xiu (2019): “Principal component analysis of high-frequency data,” Journal of the American Statistical Association, 114(525), 287–303.

- Anderson (1958) Anderson, T. W. (1958): An introduction to multivariate statistical analysis, vol. 2. Wiley New York.

- Andreou, Gagliardini, Ghysels, and Rubin (2019) Andreou, E., P. Gagliardini, E. Ghysels, and M. Rubin (2019): “Inference in Group Factor Models with an Application to Mixed Frequency Data,” .

- Andrews (1993) Andrews, D. (1993): “Tests for Parameter Instability and Structural Change with Unknown Change Point,” Econometrica, 61(4), 821–56.

- Bai (2003) Bai, J. (2003): “Inferential theory for factor models of large dimensions,” Econometrica, 71(1), 135–171.

- Bai, Han, and Shi (2020) Bai, J., X. Han, and Y. Shi (2020): “Estimation and inference of change points in high-dimensional factor models,” Journal of Econometrics.

- Bai and Ng (2002) Bai, J., and S. Ng (2002): “Determining the number of factors in approximate factor models,” Econometrica, 70(1), 191–221.

- Bai and Ng (2006) Bai, J., and S. Ng (2006): “Confidence intervals for diffusion index forecasts and inference with factor-augmented regressions,” Econometrica, 74(4), 1133–1150.

- Bai, Ng, et al. (2008) Bai, J., S. Ng, et al. (2008): “Large dimensional factor analysis,” Foundations and Trends® in Econometrics, 3(2), 89–163.

- Baltagi, Kao, and Wang (2020) Baltagi, B. H., C. Kao, and F. Wang (2020): “Estimating and testing high dimensional factor models with multiple structural changes,” Journal of Econometrics.

- Barigozzi, Cho, and Fryzlewicz (2018) Barigozzi, M., H. Cho, and P. Fryzlewicz (2018): “Simultaneous multiple change-point and factor analysis for high-dimensional time series,” Journal of Econometrics, 206(1), 187–225.

- Bates, Plagborg-Møller, Stock, and Watson (2013) Bates, B. J., M. Plagborg-Møller, J. H. Stock, and M. Watson (2013): “Consistent factor estimation in dynamic factor models with structural instability,” Journal of Econometrics, 177(2), 289–304.

- Breitung and Eickmeier (2011) Breitung, J., and S. Eickmeier (2011): “Testing for structural breaks in dynamic factor models,” Journal of Econometrics, 163(1), 71–84.

- Chamberlain and Rothschild (1983) Chamberlain, G., and M. Rothschild (1983): “Arbitrage, factor structure, and mean-variance analysis on large asset markets,” .

- Chen, Dolado, and Gonzalo (2014) Chen, L., J. J. Dolado, and J. Gonzalo (2014): “Detecting big structural breaks in large factor models,” Journal of Econometrics, 180(1), 30–48.

- Cheng, Liao, and Schorfheide (2016) Cheng, X., Z. Liao, and F. Schorfheide (2016): “Shrinkage estimation of high-dimensional factor models with structural instabilities,” The Review of Economic Studies, 83(4), 1511–1543.

- Cochrane and Piazzesi (2005) Cochrane, J. H., and M. Piazzesi (2005): “Bond risk premia,” American Economic Review, 95(1), 138–160.

- Cochrane and Piazzesi (2009) (2009): “Decomposing the yield curve,” .

- Diebold and Li (2006) Diebold, F. X., and C. Li (2006): “Forecasting the term structure of government bond yields,” Journal of Econometrics, 130(2), 337–364.

- Diebold, Piazzesi, and Rudebusch (2005) Diebold, F. X., M. Piazzesi, and G. D. Rudebusch (2005): “Modeling bond yields in finance and macroeconomics,” American Economic Review, 95(2), 415–420.

- Eichler, Motta, and Von Sachs (2011) Eichler, M., G. Motta, and R. Von Sachs (2011): “Fitting dynamic factor models to non-stationary time series,” Journal of Econometrics, 163(1), 51–70.

- Fama and French (2015) Fama, E. F., and K. R. French (2015): “A five-factor asset pricing model,” Journal of financial economics, 116(1), 1–22.

- Fan, Liao, and Mincheva (2013) Fan, J., Y. Liao, and M. Mincheva (2013): “Large covariance estimation by thresholding principal orthogonal complements,” Journal of the Royal Statistical Society: Series B (Statistical Methodology), 75(4), 603–680.

- Fan, Liao, and Wang (2016) Fan, J., Y. Liao, and W. Wang (2016): “Projected principal component analysis in factor models,” Annals of statistics, 44(1), 219.

- Franklin (2012) Franklin, J. N. (2012): Matrix theory. Courier Corporation.

- Han and Inoue (2015) Han, X., and A. Inoue (2015): “Tests for parameter instability in dynamic factor models,” Econometric Theory, 31, 1117–1152.

- Hansen (2007) Hansen, C. B. (2007): “Asymptotic properties of a robust variance matrix estimator for panel data when T is large,” Journal of Econometrics, 141(2), 597–620.

- Jurado, Ludvigson, and Ng (2015) Jurado, K., S. C. Ludvigson, and S. Ng (2015): “Measuring uncertainty,” American Economic Review, 105(3), 1177–1216.

- Kong (2017) Kong, X.-B. (2017): “On the number of common factors with high-frequency data,” Biometrika, 104(2), 397–410.

- Kong (2018) (2018): “On the systematic and idiosyncratic volatility with large panel high-frequency data,” Annals of Statistics, 46(3), 1077–1108.

- Kong and Liu (2018) Kong, X.-B., and C. Liu (2018): “Testing against constant factor loading matrix with large panel high-frequency data,” Journal of Econometrics, 204(2), 301–319.

- Lettau and Pelger (2020a) Lettau, M., and M. Pelger (2020a): “Estimating Latent Asset Pricing Factors,” Journal of Econometrics, 218(1), 1–31.

- Lettau and Pelger (2020b) (2020b): “Factors that Fit the Time-Series and Cross-Section of Stock Returns,” Review of Financial Studies, 33(5), 2274–2325.

- Ludvigson and Ng (2009) Ludvigson, S. C., and S. Ng (2009): “A factor analysis of bond risk premia,” Discussion paper, National Bureau of Economic Research.

- Ma and Su (2018) Ma, S., and L. Su (2018): “Estimation of large dimensional factor models with an unknown number of breaks,” Journal of econometrics, 207(1), 1–29.

- Newey and West (1994) Newey, W. K., and K. D. West (1994): “Automatic lag selection in covariance matrix estimation,” The Review of Economic Studies, 61(4), 631–653.

- Park, Mammen, Härdle, and Borak (2009) Park, B. U., E. Mammen, W. Härdle, and S. Borak (2009): “Time Series Modelling With Semiparametric Factor Dynamics,” Journal of the American Statistical Association, 104(485), 284–298.

- Pelger (2019) Pelger, M. (2019): “Large-Dimensional Factor Modeling Based on High-Frequency Observations,” Journal of Econometrics, 208(1), 23–42.

- Pelger (2020) Pelger, M. (2020): “Understanding Systematic Risk: A High-Frequency Approach,” Journal of Finance, 75(4), 2179–2220.

- Pelger and Xiong (2020) Pelger, M., and R. Xiong (2020): “Interpretable Sparse Proximate Factors for Large Dimensions,” Working paper.

- Ross (1976) Ross, S. A. (1976): “The arbitrage theory of capital asset pricing,” Journal of Economic Theory, 13(3), 341–360.

- Stewart (1990) Stewart, G. W. (1990): “Matrix perturbation theory,” .

- Stock and Watson (2002) Stock, J. H., and M. Watson (2002): “Macroeconomic Forecasting Using Diffusion Indexes,” Journal of Business & Economic Statistics, 20, 147–162.

- Stock and Watson (2009) Stock, J. H., and M. Watson (2009): “Forecasting in dynamic factor models subject to structural instability,” The Methodology and Practice of Econometrics. A Festschrift in Honour of David F. Hendry, 173, 205.

- Su and Wang (2017) Su, L., and X. Wang (2017): “On time-varying factor models: Estimation and testing,” Journal of Econometrics, 198(1), 84–101.

- Wang, Peng, Li, and Leng (2019) Wang, H., B. Peng, D. Li, and C. Leng (2019): “Nonparametric Estimation of Large Covariance Matrices with Conditional Sparsity,” Working paper.

- Xiong and Pelger (2020) Xiong, R., and M. Pelger (2020): “Large Dimensional Latent Factor Modeling with Missing Observations and Applications to Causal Inference,” Working paper.

- Yamamoto and Tanaka (2015) Yamamoto, Y., and S. Tanaka (2015): “Testing for factor loading structural change under common breaks,” Journal of Econometrics, 189(1), 187–206.

- Yuan and Bentler (2000) Yuan, K.-H., and P. M. Bentler (2000): “Three likelihood-based methods for mean and covariance structure analysis with nonnormal missing data,” Sociological methodology, 30(1), 165–200.

Internet Appendix for

State-Varying Factor Models of Large Dimensions

The Internet Appendix collects the proofs and additional results that support the main text. The additional theoretical results include a detailed description of special cases and related models and an extension to noisy and misspecified state processes. We also provide an estimator for the number of factors. The additional empirical results consider alternative state processes and discuss the choice of tuning parameters. We also study a portfolio application of our state-varying factors. The extensive simulation section compares the performance relative to alternative latent factor models that allow for time-variation and studies the choice of bandwidth and number of factors with cross-validation arguments. Lastly, we collect the detailed proofs for all the theoretical statements.

Keywords: Factor Analysis, Principal Components, State-Varying, Nonparametric, Kernel-Regression, Large-Dimensional Panel Data, Large and

JEL classification: C14, C38, C55, G12

IA.A Overview