An MCMC Approach to Empirical Bayes Inference and Bayesian Sensitivity Analysis via Empirical Processes

Abstract

Consider a Bayesian situation in which we observe , where , and we have a family of potential prior distributions on . Let be a real-valued function of , and let be the posterior expectation of when the prior is . We are interested in two problems: (i) selecting a particular value of , and (ii) estimating the family of posterior expectations . Let be the marginal likelihood of the hyperparameter : . The empirical Bayes estimate of is, by definition, the value of that maximizes . It turns out that it is typically possible to use Markov chain Monte Carlo to form point estimates for and for each individual in a continuum, and also confidence intervals for and that are valid pointwise. However, we are interested in forming estimates, with confidence statements, of the entire families of integrals and : we need estimates of the first family in order to carry out empirical Bayes inference, and we need estimates of the second family in order to do Bayesian sensitivity analysis. We establish strong consistency and functional central limit theorems for estimates of these families by using tools from empirical process theory. We give two applications, one to Latent Dirichlet Allocation, which is used in topic modelling, and the other is to a model for Bayesian variable selection in linear regression.

keywords:

[class=MSC]keywords:

arXiv:0000.0000 \startlocaldefs \endlocaldefs

and

t1Supported by NSF Grant DMS-11-06395 and NIH grant P30 AG028740

1 Introduction

This paper is concerned with two related problems. In the first, there is a function , where is a subset of some Euclidean space, and we wish to obtain confidence sets for . For each , the expression for is analytically intractable; however, we have at our disposal a family of functions and a sequence of random variables (these are iid or the initial segment of an ergodic Markov chain) such that the random function satisfies for each . We are interested in how we can use to form both a point estimate and a confidence set for .

This problem appears in empirical Bayes analysis and under many forms in likelihood inference. In empirical Bayes analysis, the application that is the focus of this paper, it arises as follows. Suppose we are in a standard Bayesian situation in which we observe a data vector whose distribution is (with density with respect to some dominating measure) for some . We have a family of potential prior densities , and because the hyperparameter can have a great impact on subsequent inference, we wish to choose it carefully. Selection of is often guided by the marginal likelihood of the data under the prior , given by

| (1.1) |

By definition, the empirical Bayes choice of is . Unfortunately, analytic calculation of is not feasible except for a few textbook examples, and estimation of via Monte Carlo is notoriously difficult—for example, the “harmonic mean estimator” introduced by Newton and Raftery (1994) typically converges at a rate which is much slower than (Wolpert and Schmidler, 2012).

It is very interesting to note that if is a constant, then the information regarding given by the two functions and is the same: the same value of maximizes both functions, and the second derivative matrices of the logarithm of these two functions are identical. In particular, the Hessians of the logarithm of these two functions at the maximum (i.e. the observed Fisher information) are the same and, therefore, the standard point estimates and confidence regions based on and are identical. This is a very useful observation because it turns out that it is usually easy to estimate the entire family for a suitable choice of . Indeed, for any , let denote the posterior corresponding to , let be fixed but arbitrary, and suppose that are either independent and identically distributed according to the posterior , or are the initial segment an ergodic Markov chain with invariant distribution . Let be the likelihood function. Note that given by (1.1) is the normalizing constant in the statement “the posterior is proportional to likelihood times the prior,” i.e.

| (1.2) |

We have

| (1.3) |

in which the first equality follows from (1.2) and cancellation of the likelihood. Let . Since is a fixed constant, as noted above, the two functions and give exactly the same information about . If we let , then —this quantity is computable, since it involves only the priors and not the posteriors—so we have precisely the situation discussed in the first paragraph of this paper. Other examples of this situation arising in frequentist inference, and in particular in missing data models, are given in Sung and Geyer (2007) and Doss and Tan (2014).

In Bayesian applications it is rare that Monte Carlo estimates of posterior quantities can be based on iid samples; in the vast majority of cases they are based on Markov chain samples, and that is the case that is the focus of this paper. We show that under suitable regularity conditions,

| (1.4) |

and

| (1.5) |

where can be estimated consistently. Now, in general, almost sure convergence of to pointwise is not enough to imply that converges to under any mode of convergence, and in fact it is trivial to construct a counterexample in which and are deterministic functions defined on , for every , but does not converge to . To obtain results (1.4) and (1.5) above, some uniformity in the convergence is needed. We establish the necessary uniform convergence and show that (1.4) and (1.5) are true under certain regularity conditions on the sequence , the functions , and the function . Result (1.5) enables us to obtain confidence sets for .

The second problem we are interested in pertains to the Bayesian framework discussed earlier and is described as follows. Suppose that is a real-valued function of , and consider , the posterior expectation of given , when the prior is . Suppose that is fixed but arbitrary, and that is an ergodic Markov chain with invariant distribution . A very interesting and well-known fact, which we review in Section 2.3, is that for any , if we define

then

| (1.6) |

is a consistent estimate of . Clearly is a weighted average of the ’s. Under additional regularity conditions on the Markov chain and the function , we even have a central limit theorem (CLT): , and we can consistently estimate the limiting variance. Thus, with a single Markov chain run, using knowledge of only the priors and not the posteriors, we can estimate and form confidence intervals for for any particular value of . Now in Bayesian sensitivity analysis applications, we will be interested in viewing for many values of . For example, in prior elicitation settings, we may wish to find those aspects of the prior that have the biggest impact on the posterior, so that the focus of the effort is spent on those important aspects. We may also want to determine whether differences in the prior opinions of many experts have a significant impact on the conclusions. (For a discussion of Bayesian sensitivity analysis see Berger (1994) and Kadane and Wolfson (1998).) In these cases we will be interested in forming confidence bands for that are valid globally, as opposed to pointwise.

A common feature of the two problems we study in this paper is the need for uniformity in the convergence: to obtain confidence intervals for we need some uniformity in the convergence of to , and to obtain confidence bands for we need functional CLT’s for the stochastic process . Empirical process theory is a body of results that can be used to establish uniform almost sure convergence and functional CLT’s in very general settings. However, the results hold only under strong regularity conditions; and these conditions are often hard to check in practical settings—indeed the results can easily be false if the conditions are not met. Empirical process theory is fundamentally based on an iid assumption, whereas in our setting, the sequence is a Markov chain. In this paper we show how empirical process methods can be applied to our two problems when the sequence is a Markov chain, and we also show how the needed regularity conditions can be established.

The rest of the paper is organized as follows. In Section 2 we state our theoretical results, the main ones—those that pertain to the Markov chain case—being as follows. Theorem 3 asserts uniform convergence of to when the sequence is a Harris ergodic Markov chain, under certain regularity conditions on the family (the precise details are spelled out in the statement of the theorem), and we show how these regularity conditions can be checked with relative ease in standard settings. We then give a simple result which says that under a mild regularity assumption on , the condition entails . Theorem 4 establishes that under certain regularity conditions, we have asymptotic normality of . Theorem 6 establishes almost sure uniform convergence of to , and also functional weak convergence: the process converges weakly to a mean Gaussian process indexed by . We also show how this result can be used to construct confidence bands for that are valid globally. A by-product is functional weak convergence of to a mean Gaussian process indexed by , and construction of corresponding globally valid confidence bands for . In Section 3 we give two illustrations on Bayesian models in which serious consideration needs to be given to the effect of the hyperparameter and its choice. The first is to the Latent Dirichlet Allocation topic model, where we show how our methodology can be used to do sensitivity analysis, and the second is to a model for Bayesian variable selection in linear regression, where we show how our methodology can be used to select the hyperparameter. In the Appendix we provide the proofs of all the theorems except for Theorem 3; additionally, we show how the regularity conditions in Theorem 1 and Theorem 3 would typically be checked, and we verify these conditions in a simple setting.

2 Convergence of as a Process and Convergence of the Empirical Argmax

This section consists of three parts. Section 2.1 deals with uniform convergence of for the iid case, and introduces the framework that will enable us to obtain results for the Markov chain case; this framework will be used in Section 2.1 and in the rest of the paper. Section 2.2 deals with point estimates and confidence sets for , and Section 2.3 deals with uniform convergence and functional CLT’s for estimates of posterior expectations. Throughout, uniformity refers to a class of functions indexed by .

2.1 Uniform Convergence of

Let be a measurable subset of for some , and let be a probability measure on , where is the Borel sigma-field on . We assume that are independent and identically distributed according to , and we let be the empirical measure that they induce. We assume that is a convex compact subset of for some , and that for each , is measurable. The strong law of large numbers (SLLN) states that

| (2.1) |

Since we will be interested in versions of (2.1) that are uniform in , there will exist measurability difficulties, so we have to be careful in dealing with measurability issues. Before proceeding, we review some terminology and standard facts from the theory of empirical processes. We will use the following standard empirical process notation: for a signed measure on and a -integrable function , denotes . Let be an arbitrary probability measure on , suppose that are independent and identically distributed according to , and let be the empirical measure induced by . If is a class of functions mapping to , and is a signed measure on , we use the notation . We say that is Glivenko-Cantelli if converges to almost surely; sometimes we will say is -Glivenko-Cantelli, to emphasize the dependence on . Let . Our goal is to establish that is -Glivenko-Cantelli, which is exactly equivalent to the statement that the convergence in (2.1) holds uniformly in .

The IID Case

Theorem 1 (Theorem 6.1 and Lemma 6.1 in Wellner (2005))

Suppose that are independent and identically distributed according to . Suppose that is continuous in for -almost all . If is measurable and satisfies , then the class is -Glivenko-Cantelli.

Let and (the subscript to the expectation indicates that ). Then the conclusion of the theorem is the statement .

The integrability condition seems strong, and an even stronger integrability condition is imposed in Theorem 3. We discuss this issue in Remark 1 following the statement of Theorem 3, where we explain that in fact the two conditions are fairly easy to check in practice.

The next theorem also establishes that the class is Glivenko-Cantelli. In the theorem, the integrability condition on is replaced by an integrability condition on (here, is the gradient vector of with respect to , and is Euclidean norm). The condition on the gradient is sometimes easier to check. We include the theorem in part because a component of its proof is a key element in the proofs of Theorems 5 and 6 of this paper.

Theorem 2

Suppose that are independent and identically distributed according to , and that for each , . Assume also that for -almost all , exists and is continuous on . If is measurable and satisfies , then the class is -Glivenko-Cantelli.

The Markov Chain Case

Suppose now that the sequence is a Markov chain with invariant distribution , and that it is Harris ergodic (that is, it is irreducible, aperiodic, and Harris recurrent; see Meyn and Tweedie (1993, chapter 17) for definitions). Suppose also that for all . The best way to deal with the family of averages , is through the use of “regenerative simulation.” A regeneration is a random time at which a stochastic process probabilistically restarts itself; therefore, the “tours” made by the process in between such random times are iid. For example, if the stochastic process is a Markov chain on a discrete state space , and if is any point to which the chain returns infinitely often with probability one, then the times of return to form a sequence of regenerations. This iid structure will enable us to establish uniform convergence of the family . Before we explain this, we first note that for most of the Markov chains used in MCMC algorithms, the state space is continuous, and there is no point to which the chain returns infinitely often with probability one. Fortunately, Mykland et al. (1995) provided a general technique for identifying a sequence of regeneration times that is based on the construction of a minorization condition. This construction is reviewed at the end of this subsection, and gives rise to regeneration times with the property that

| (2.2) |

Suppose now that there exists a regeneration sequence which satisfies (2.2). Such a Markov chain will be called regenerative. For any , consider . Let

| (2.3) |

be the sum of over the tour. Also, let , denote the length of the tour. The ’s do not involve . Note that the pairs are iid. If we run the chain for regenerations, then the total number of cycles is given by

Also, . We have

| (2.4) |

In (2.4), the convergence statement on the left follows from Harris ergodicity of the chain. The convergence statement on the right follows from two applications of the SLLN: By (2.2), and this, together with the convergence statement on the left, entails convergence of . The SLLN then implies that (if then the SLLN implies that with probability one). We conclude that . Note that continuity in of for almost all sequences follows from continuity in of for almost all , since with probability one, is a finite sum. Suppose in addition that is measurable and satisfies . Then by Theorem 1 we have . Since , we obtain

i.e.

| (2.5) |

We summarize this in the following theorem.

Theorem 3

Remark 1

We now discuss the integrability condition , and our discussion encompasses the weaker condition assumed in Theorem 1. Suppose that for all . In the Appendix we show that, because is assumed to be compact, it is often possible to prove that for some ,

| (2.6) |

In this case, since , we obtain

Hence,

which is finite. Thus, checking that reduces to establishing (2.6). In the Appendix we consider the Bayesian framework discussed in Section 1, in which , where is a family of priors, and , the posterior distribution corresponding to the prior , where is fixed. We show that if is an exponential family, then condition (2.6) holds. Therefore, the integrability condition is satisfied in a large class of examples. Moreover, the method we use for establishing (2.6) can be applied to other examples as well.

Remark 2

The idea to transform results for the iid case to the Markov chain case via regeneration has been around for many decades. Levental (1988) also obtained a Glivenko-Cantelli theorem for the Markov chain setting. In essence, the difference between his approach and ours is that his starting point is a Glivenko-Cantelli theorem for the iid case which requires a condition involving the minimum number of balls of radius in that are needed to cover —he is using metric entropy. This condition is very hard to check. By contrast, our starting point is a Glivenko-Cantelli theorem for the iid case which is based on bracketing entropy—in brief, the main regularity condition is implied by the continuity condition in Theorem 3. This continuity condition is trivial to verify: the parametric families that we are working with in our Bayesian setting satisfy it automatically.

The Minorization Construction

We now describe a minorization condition that can sometimes be used to construct regeneration sequences. Let be the transition function for the Markov chain . The construction described in Mykland et al. (1995) requires the existence of a function , whose expectation with respect to is strictly positive, and a probability measure on , such that satisfies

| (2.7) |

This is called a minorization condition and, as we describe below, it can be used to introduce regenerations into the Markov chain driven by . Define the Markov transition function by

Note that for fixed , is a probability measure. We may therefore write

which gives a representation of as a mixture of two probability measures, and . This provides an alternative method of simulating from . Suppose that the current state of the chain is . We generate . If , we draw ; otherwise, we draw . Note that if , the next state of the chain is drawn from , which does not depend on the current state. Hence the chain “forgets” the current state and we have a regeneration. To be more specific, suppose we start the Markov chain with and then use the method described above to simulate the chain. Each time , we have and the process stochastically restarts itself; that is, the process regenerates. Mykland et al. (1995) provided a very widely applicable method, the so-called “distinguished point technique”, for constructing a pair that can be used to form a minorization scheme which satisfies (2.2).

For any fixed , consider now the expression

in (2.4). The bivariate CLT gives

| (2.8) |

where . (We have ignored the moment conditions on and that are needed, but we will return to these conditions in Section 2.3, where we give a rigorous development of a functional version of the CLT (2.8), in which the left side of (2.8) is viewed as a process in .) The delta method applied to the function gives the CLT

where (and is evaluated at the vector of means in (2.8)). Moreover, can be estimated in a simple manner using a plug-in estimate. Whether or not this method gives estimates of variance that are useful in the practical sense depends on whether or not the minorization condition we construct yields regenerations which are sufficiently frequent. Successful constructions of minorization conditions have been developed for widely used chains in many papers (we mention in particular Mykland et al. (1995), Roy and Hobert (2007), Tan and Hobert (2009), and Doss et al. (2014)); nevertheless, successful construction of a minorization condition is the exception rather than the norm. In this context, we point out that here regenerative simulation is notable primarily as a device that enables us to prove the theoretical results in the present paper and to arrive at informative expressions for asymptotic variances, but it may be possible to estimate these variances by other methods; this point is discussed further in Section 2.2.

2.2 A Consistent Estimator and Confidence Sets for

This section pertains to as an estimator of . After establishing that (2.5) entails that is consistent, we show that under additional regularity conditions, (i) is asymptotically normal, and (ii) we can consistently estimate the asymptotic variance. Results (i) and (ii) enable us to form asymptotically valid confidence sets for .

Lemma 1

Suppose that is a compact subset of Euclidean space, and let and be deterministic real-valued functions defined on . Suppose further that is continuous and has a unique maximizer, and that for each the maximizer of exists and is unique. If converges to uniformly on , then the maximizer of converges to the maximizer of .

The proof of Lemma 1 is routine and is given in the Appendix. Consider now and . By Lemma 1, if is continuous and its maximizer is unique, then implies . Thus, under continuity of and uniqueness of its maximizer, any conditions that imply (2.5)—in particular the conditions of Theorems 1, 2, or 3—are also conditions that imply strong consistency of as an estimator of .

Before stating the next theorem, we need to set some notation and assumptions. We assume that each of and has a unique maximizer, and we denote and . For a function , denotes the gradient vector and denotes the Hessian matrix. We will assume that for every , and exist and are continuous for all . Recall that is defined by (2.3). The Markov chain will be run for regenerations, and in the asymptotic results below, . We will use the notation , , , etc. For almost any realization , the random variable is a finite sum, and therefore . Similarly, . We will assume that the family is such that the interchange of the order of integration and either first or second order differentiation is permissible, i.e.

| (2.9) |

For , let

and

Suppose that is a Markov chain on the measurable space and has as an invariant probability measure. Let be the -step Markov transition function. Recall that the chain is called geometrically ergodic if there exist a constant and a function such that for ,

If is a matrix, then a statement of the sort will mean for . We will refer to the following conditions.

-

A1

The chain is geometrically ergodic.

-

A2

For every , there exists such that .

-

A3

The function is twice continuously differentiable and the matrix is nonsingular.

-

A4

is measurable and .

-

A5

is measurable and .

-

A6

is measurable and .

-

A7

is measurable and has finite expectation.

Theorem 4

Remark 4

In the expression for the asymptotic variance given by (2.10), the term is the variance of a certain function of the Markov chain, and the term measures the inverse of the curvature of at its maximum ( is a deterministic function and does not involve the Markov chain): the flatter the surface at its maximum, the higher is the asymptotic variance.

Remark 5

The integrability condition in Assumption A4 was discussed in Remark 1, where we showed that it is satisfied whenever there exist such that for all (cf. (2.6), in which without loss of generality we take the constants to be equal to .) The integrability conditions in A5–A7 are satisfied under (2.13) and (2.14) below, which are very similar to (2.6). To make our explanation notationally less cumbersome and easier to follow, we will assume that , so that , , , and are all scalars. Assume that there exist and constants such that

| (2.13) | ||||

| (2.14) |

The integrability condition in A5, , follows from (2.14) using an argument identical to the one we used to show that the integrability condition in A4 follows from (2.6). Clearly, A6 follows immediately from (2.13).

We now deal with A7 and consider . Let , and let denote the set of indices that comprise the first tour. Since , we have

where the second inequality is from (2.13). Therefore , and hence

| (2.15) |

Now by A2 and the Minkowski inequality, . This integrability condition, together with geometric ergodicity of the chain (cf. A1), enables us to apply Theorem of Hobert et al. (2002) to conclude that which, by (2.15), implies that , which is the integrability condition in A7.

Remark 6

Remark 7

We now step back and put Theorem 4 in the context of frequentist inference. We do not require that the number of components of our data vector goes to infinity, or even that the components are iid. We observe , which induces a marginal likelihood surface , and Theorem 4 pertains to estimation of this surface and its argmax, with the asymptotics referring to the Markov chain length going to infinity. In this regard, it is natural to ask what are the frequentist properties of inference based on this argmax. A very general result, known as the Bernstein-von Mises Theorem, asserts that under certain regularity conditions, if are iid with distribution , and if is the maximum likelihood estimate of based on , then for any , -a.s. Here, denotes the normal distribution with mean vector and covariance matrix , is the Fisher information at , and the subscript TV denotes total variation norm. In particular, the usual Bayesian credible region coincides with the usual confidence region, and therefore has asymptotic frequentist coverage probability equal to . Theorem 1 of Petrone et al. (2014) goes further, and states that the Bernstein-von Mises Theorem holds when we use , the maximum marginal likelihood estimate of . There are regularity conditions; see Petrone et al. (2014), which also contains references for precise statements of the Bernstein-von Mises Theorem. To conclude, if is sufficiently large, credible sets based on have asymptotic frequentist coverage probability equal to .

We now discuss the role of regenerative simulation in our development. Broadly speaking, the existence of regenerative sequences is guaranteed under very general conditions—here we note not only the distinguished point technique of Mykland et al. (1995) mentioned earlier, but also the fact that for any chain satisfying our minimal regularity condition of Harris ergodicity, there exists a such that there is a minorizing pair for the -step Markov transition function (Meyn and Tweedie, 1993, Section 5.2). However, it is often very difficult to construct a useful minorization condition, i.e. one that gives rise to regenerations that are frequent enough so that law of large numbers and CLT approximations are valid for reasonable sample sizes. If we do succeed in obtaining a useful regeneration sequence, then we can estimate variances and construct confidence sets using the estimate given in Part of Theorem 4, and it is widely recognized that estimation of variances using regeneration—when it is feasible—outperforms estimation using other methodologies (Flegal and Jones, 2010). Additionally, it has the advantage that because we start the chain at a regeneration point (i.e. ), the issue of burn-in does not even exist.

It is very interesting to note that we have used regenerative simulation in a theoretical manner: our proof of asymptotic normality of (see (2.12)) requires only the existence of a regeneration sequence, and does not require that we go through a laborious trial and error process to construct one that is useful in the practical sense. Very briefly, to obtain asymptotic results regarding , we need uniformity in the convergence of to . Empirical process theory gives us results on uniformity, but only in the iid setting, and regenerative simulation bridges the gap between the Markov chain setting and the iid setting. Once we have established the asymptotic normality of , we are free to estimate the asymptotic variance and form confidence sets using other methods, for example batching, which we now discuss.

Batching is implemented by breaking up the sequence into consecutive pieces of equal lengths called batches. For , batch is used to produce an estimate in the obvious way. If is fixed, then under the regularity conditions of Theorem 4, (2.12) states that for each , , where . If the batch length is large enough relative to the “mixing time” of the chain, then the ’s are approximately independent. If the independence assumption was exactly true rather than approximately true, then the sample variance of would be a valid estimator of . Standard theoretical results regarding batching deal with the situation in which is a -integrable function, and the Markov chain is used to estimate via . These results, which assume that , state that under regularity conditions which include at a certain rate, the batch-based estimate of is strongly consistent; see Flegal et al. (2008) and also Jones et al. (2006), who recommend using . Our situation is different in that our estimate is not an average, but is the argmax of a function based on . Nevertheless, the method applies, with the minor modification that when we form the “sample variance,” the centering value is based on rather than on the average of the ’s. As is clear from the description above, batch-based estimates of variance are very easy to program. However, it is generally acknowledged that they are outperformed by estimates based on regeneration or spectral methods.

2.3 Convergence of Estimate of Posterior Expectation

This section concerns the Bayesian framework discussed earlier, in which is a family of prior densities on ; for each , is the posterior corresponding to ; is fixed but arbitrary, and is an ergodic Markov chain with invariant distribution . Suppose that is a real-valued function of and consider , the posterior expectation of given , when the prior is . We have

| (2.16) |

in which the first equality follows from (1.2) and cancellation of the likelihood. Therefore,

| (2.17) |

where the convergence of the numerator and the denominator in the expression for follow from (2.16) and (1.3), respectively. In the original expression given in (1.6), is a weighted average of the ’s (with weights all equal to if , and becoming more disparate as and become more dis-similar). The definition of given in (2.17) clearly matches the original expression, so we see that may be represented either as a weighted average or as a ratio of two ordinary averages. To establish almost sure uniform convergence and functional weak convergence results for , we will work with the latter representation, because doing so will enable us to use tools from empirical process theory. With this in mind, recall that in the present framework . We will work with the classes of functions and . We will later assume that the sequence is a Markov chain satisfying certain conditions, and Theorem 6 pertains to that case; however, in order to give an overview of our results, it is convenient to first assume that the ’s form an iid sequence: . Recall that is the empirical measure that gives mass to each of , and that for a signed measure and a function , denotes . In the present specialized Bayesian context, ; thus the norm of is simply . Our goal is to establish that under certain conditions:

-

1.

We have the Glivenko-Cantelli results

-

2.

We have the “Donsker results”

(2.18) where and are mean Gaussian processes indexed by .

By applying the delta method to the function , we then obtain the Glivenko-Cantelli and Donsker results

-

3.

-

4.

(2.19) where is a mean Gaussian process indexed by .

We now give some definitions we will need in order to explain what is meant by (2.18) and (2.19). Define . Let be any set of real-valued functions defined on and let denote the space of bounded functions from to equipped with the supremum norm. Assume that

Under this condition the empirical process can be viewed as a map from into . Any measurable function induces a distribution on . Although the functions we will be working with will in general be measurable, in order to properly state the relevant definitions and theorems from empirical process theory, in our definitions we will deal with functions which are not necessarily measurable. For an arbitrary map from an arbitrary probability space to the extended real line , denotes the outer integral of with respect to . (The outer integral is defined by .) Suppose and are maps into , and that is measurable. We say that converges weakly to , and we write , if for every bounded, continuous, real function on .

We now return to the empirical process . A class is called a Donsker class if in , where the limit is a mean Gaussian process with covariance function

and has paths which are uniformly continuous with respect to the semi-metric on defined by . Sometimes we will say is -Donsker, to emphasize the dependence on .

We say that a class of measurable functions is -measurable if for every and every vector , the function

is measurable on the completion of .

Because and are simply parametric families indexed by , we will slightly abuse terminology and take the two convergence statements in (2.18) to mean in and in , respectively. The limit is a mean Gaussian process indexed by and covariance function

Similarly, is a mean Gaussian process indexed by and covariance function

and we will discuss the covariance function of the limit in (2.19) later. For , let and let .

Before we state the next theorem, we need to lay down preparations for its fourth part, which regards functional weak convergence of the process . Let be the space of all continuous functions , with the topology induced by the sup norm metric : for , . Clearly, functional weak convergence of cannot take place in a space of the type for some set of functions , and in fact, as we will see, the weak convergence will take place in the space . (As usual, if and are probability measures on , we say that if for all functions which are bounded and continuous.)

We now define the expression for the covariance function and give motivation for its form. For any , the multivariate CLT states that

| (2.20) |

where is the matrix given by . Consider the function defined by . Then, if we apply the delta method to (2.20) using , we get

| (2.21) |

where , and (viewed as a matrix) is evaluated at the vector of means . The matrix describes the covariance structure for the process . (Expressions for and are given in Park (2015).)

Theorem 5

Assume that are independent and identically distributed according to .

-

1

-

(a)

Suppose that is continuous in for -almost all . If is measurable and , then is -Glivenko-Cantelli.

-

(b)

Suppose that is continuous in for -almost all . If is measurable and , then is -Glivenko-Cantelli.

-

(a)

-

2

Assume the conditions of Part of the theorem, and also that for every , exists and is continuous on . Then

(2.22) -

3

-

(a)

Suppose that the classes , , and are all -measurable. Assume also that for -almost all , exists and is continuous on . If (1) is measurable and (2) the functions and are all square integrable with respect to , then the class is -Donsker.

-

(b)

Suppose that the classes , , and are all -measurable. Assume also that for -almost all , exists and is continuous on . If (1) is measurable and (2) the functions and are all square integrable with respect to , then the class is -Donsker.

-

(a)

-

4

Under the conditions of Part of the theorem, we have

where is a Gaussian process indexed by with mean and covariance function

Part (a) is, of course, simply a restatement of Theorem 1; we have repeated it here only to clarify the structure of our results. The -measurability conditions cannot be omitted. However, in all the problems we have encountered, the relevant functions are not only measurable, but are actually continuous.

In Remark 8, which follows the statement of Theorem 6, we develop a construction of confidence bands for and we explain why Theorem 6 shows that these bands are valid globally. Theorem 6 pertains to Markov chains, but the same construction and arguments can be applied to the iid case—we use Theorem 5 instead of Theorem 6.

The next result is a version of Theorem 5 that applies to Markov chains. Recall that is the length of the tour and that is defined by (2.3). Similarly, define . Let and . Part of Theorem 6 asserts that under certain conditions the classes and are Donsker, and before stating the theorem, it is necessary to be very clear regarding what these classes are, and what “Donsker” means. Let P be the distribution of the Markov chain . For any , is a function mapping the measure space into . To see this it may be helpful to imagine that we are dealing with the very simple case of a regenerative chain which has an “proper atom” at a singleton. That is, there exists a point which has positive probability under the invariant measure. Thus, with probability one the chain returns to infinitely often, and the times of return to are regeneration times . In this case (with probability one) the sequence itself determines and . Then, is defined by , and we have a similar definition for . Chains which have a proper atom at a singleton are quite rare, and we consider them only for exposition. We remark on the case of a general regenerative Markov chain at the end of the proof of Theorem 6. To clarify, and are classes of functions on , in contrast to and , which are classes of functions on . These classes will be P-Donsker, and we note that P is a distribution on the infinite product space , to be distinguished from , which is a distribution on .

As we will see, Parts and of Theorem 6 are functional CLT’s that concerns certain stochastic processes indexed by . In order to motivate them, we need to first understand the version of these parts of the theorem that pertains to the very simple situation in which we are considering a single value of . Thus, let be fixed. We now consider CLT’s for averages formed from the sequences and . We have and (see (2.4)). Under A1 and the conditions and , the expectations , , and are all finite (Theorem of Hobert et al. 2002). Therefore, the simple multivariate CLT gives

| (2.23) |

where . We apply the delta method to (2.23) three times, using the functions , , and to obtain three CLT’s:

| (2.24) |

With the relationships , , , and the fact that , (2.24) may be restated as

| (2.25) |

(with the understanding that here, is random). Of course, under geometric ergodicity and the moment conditions and , asymptotic normality of the three quantities on the left side of (2.25) is already known (corollary to Theorem 18.5.3 of Ibragimov and Linnik 1971). The point of obtaining (2.25) as we did above is that the method enables us to get functional versions of the three statements in (2.25) (i.e. weak convergence of the three quantities on the left side of (2.25) as processes in ) if we can show that the classes and are Donsker. This is precisely what Part of Theorem 6 asserts. The theorem will refer to the following conditions.

-

B1

For every , there exists such that .

-

B2

For every , there exists such that .

Theorem 6

Assume that is a Harris ergodic Markov chain with invariant distribution for which there exists a regeneration sequence satisfying .

- 1

-

2

Assume the conditions of Part of the theorem, and also that for every , exists and is continuous on . Then

(2.26) -

3

- (a)

- (b)

-

4

Under the conditions of Part of the theorem, we have

(2.27) where is a Gaussian process indexed by with mean and covariance function

Consequently,

(2.28) where is a Gaussian process indexed by with mean and covariance function

In (2.27) is interpreted as , and the limit is as , whereas in (2.28) and the limit are interpreted differently: , and is random.

Remark 8

Here we discuss how to form globally valid confidence bands for (we drop the subscript “” to lighten the notation). We would like to proceed as follows. Having established that , we find the distribution of . If is the -quantile of this distribution, then the band has asymptotic coverage probability equal to . Unfortunately, except for very unusual cases, the distribution of cannot be obtained analytically. Spectral methods can be used for the problem of forming confidence intervals for for a single value of , but not for the problem of forming confidence bands. We know of no way to use regenerative simulation to construct confidence bands. However, the method of batching works, as follows.

For a positive integer , the sequence is broken up into consecutive pieces, each of length (we are ignoring divisibility issues). For , let be the estimate of based on batch , and let

(The difference between and is that the latter is not computable, because it involves the unknown function .) Let be the order statistics of the sequence and, similarly, let be the order statistics of the sequence . Now suppose that in such a way that . Below is the outline of an argument which shows that the band has coverage probability that is asymptotically equal to .

-

1.

For every , we have by Theorem 6, and if the distribution of is continuous, then converges in distribution to , the point mass at .

-

2.

Therefore the (uncomputable) band has coverage probability that converges to .

-

3.

The difference between and is small uniformly in ; more precisely, we have . Therefore the band also has coverage probability that converges to .

Details are given in Park (2015).

Remark 9

We have seen that for any , if is a Markov chain with invariant distribution then, under certain regularity conditions, the estimates and are consistent and asymptotically normal. These estimates can be unstable, however, if is far from , and there may not exist a single value of that gives rise to estimates that are stable for all . Serial tempering (Marinari and Parisi (1992); Geyer and Thompson (1995); see also Geyer (2011) for a review, and Tan (2014) for recent developments) can be very effective in handling this problem. A very brief description of the method in the present context is as follows. We select points ; these should be taken to “cover” in the sense that every in is “close” to at least one of the ’s. Let ; the elements of are called “labels.” For each , let be a Markov transition function with invariant distribution . A Markov chain running on the state space is generated as follows. If the current state of the chain is , a new label is generated, and is generated from the distribution . The mechanism for generating the labels is set up in such a way that the -sequence has invariant distribution , where the ’s are all nearly equal to . From the -sequence, the quantities and can be estimated in a stable manner for any which is “close” to at least one of the ’s, or more precisely, for any such that is “close” to at least one of . The results of this paper do not require that the sequence have invariant distribution equal to for some , and in fact the invariant distribution can be a mixture , for judiciously chosen , as described above, for example.

3 Illustrations

Here we present two illustrations. The first deals with the so-called Latent Dirichlet Allocation model, which is used for organizing and searching electronic documents. The version of the model we discuss is indexed by a two-dimensional hyperparameter. Our focus will be on obtaining globally-valid confidence sets for a certain posterior expectation of interest. For the data set we study, the amount of time it takes to run the Markov chain is a significant issue because each cycle has length . We will use the results of Section 2.3 to determine the minimal Markov chain length that is needed to obtain acceptably narrow confidence regions. The second illustration deals with a model for Bayesian variable selection in linear regression. For this situation our interest will be on hyperparameter selection, and we will use the results of Section 2.2. We will see that for the data set we use, a very modest Markov chain length is all that is needed to produce narrow confidence sets for the empirical Bayes choice of the hyperparameters.

3.1 Sensitivity Analysis in the Latent Dirichlet Allocation Model

Probabilistic topic modelling is an area of machine learning that deals with methods for understanding, summarizing, and searching large electronic archives. Traditional keyword-based searches are very fast, but have important deficiencies. Suppose we are interested in searching for all statistical papers that deal with censored data. A search using the keywords “censored data” will not return papers that use the expression “incomplete data”. In topic-based searches, we do a search based on a concept or topic. A topic is not an expression; it is, by definition, a distribution over a set of expressions. Thus the topic mentioned above gives a lot of mass to expressions like “Kaplan-Meier”, “censored data”, and “incomplete data”, and little mass to expressions like “spectral decomposition”.

Latent Dirichlet Allocation (LDA, Blei et al. 2003) is by far the most used topic model. We will consider the version of the model that deals only with individual words, as opposed to expressions consisting of several words. Suppose we have a corpus of documents, for example a set of articles from The New York Times, and these span several different topics, such as sports, medicine, politics, etc. The words in the documents come from a vocabulary , which is a set consisting of words . For each document, the data we have for that document is a sequence of length consisting of the number of times that word occurs, for . In LDA, we imagine that for each word in each document, there is a latent (i.e. unobserved) variable indicating a topic from which that word is drawn. LDA enables us to make inference on these latent variables, and therefore, on the topics that are covered by each document as a whole. Therefore, LDA enables us to cluster together documents which are similar, i.e. documents which share common topics. By its very nature, LDA is completely automatic in how it defines the topics: these are distributions over the vocabulary, and are themselves latent variables. To be more precise, in LDA there is no such thing as a topic called “sports”. Instead, there is a distribution on which gives most of its mass to words like “homerun”, “marathon”, and “NBA”. A human is then free to call this distribution “sports” if he/she wishes.

We now give more detail. The vocabulary is taken to be the union of all the words in all the documents of the corpus, after removing uninformative words (like “the” and “of”). There are documents in the corpus, and for , document has words, . The order of the words is viewed as uninformative, so is neglected. Each word is represented as an index vector with a at the element, where denotes the term selected from the vocabulary. Thus, document is represented by the vector and the corpus is represented by the vector . The number of topics, , is finite and known. By definition, a topic is a point in , the -dimensional simplex. For , for each word , is an index vector which represents the latent variable that denotes the topic from which is drawn. The distribution of will depend on a document-specific variable which indicates a distribution on the topics for document . We will use to denote the finite-dimensional Dirichlet distribution on the -dimensional simplex. Also, we will use to denote the multinomial distribution with number of trials equal to and probability vector . We will form a matrix , whose row is the topic (how is formed will be described shortly). Thus, will consist of vectors , all lying in . Formally, LDA is described by the following hierarchical model, in which are hyperparameters:

-

1.

.

-

2.

, and the ’s are independent of the ’s.

-

3.

Given , , and the vectors are independent.

-

4.

Given and the ’s, are independently drawn from the row of indicated by .

From the model statement, we see that there is a latent topic variable for every word that appears in the corpus. Thus it is possible that a document spans several topics. However, because there is a single for document , the model encourages different words in the same document to have the same topic. Also note that the hierarchical nature of LDA encourages different documents to share the same topics. This is because is chosen once, at the top of the hierarchy, and is shared among the documents. Let , for , , and let . The model is indexed by the hyperparameter vector . For any given , lines – induce a prior distribution on , which we denote by . Line gives the likelihood. The words are observed, and we are interested in , the posterior distribution of given corresponding to .

The hyperparameter has a strong effect on the distribution of the parameters of the model. For example, when is large, the topics tend to be probability vectors which spread their mass evenly among many words in the vocabulary, whereas when is small, the topics tend to put most of their mass on only a few words. Also, when is large, each document tends to involve many different topics; on the other hand, in the limiting case where , each document involves a single topic, and this topic is randomly chosen from the set of all topics.

In the literature, the following choices for have been presented: , used in Griffiths and Steyvers (2004); , used in Asuncion et al. (2009); and , used in the Gensim topic modelling package (Řehůřek and Sojka, 2010), a well-known package used in the topic modelling community. These choices are ad-hoc, and not based on any principle; nevertheless, they do get used. Blei et al. (2003) propose , as we do, but their approach for estimating is quite a bit different from ours, and involves a combination of the EM algorithm and “variational inference.” Very briefly, is viewed as “observed data,” and is viewed as “missing data.” Because the “complete data likelihood” is available, the EM algorithm is a natural candidate for estimating , since is the “incomplete data likelihood.” But the E-step in the algorithm is infeasible because it requires calculating an expectation with respect to the intractable distribution . Blei et al. (2003) substitute an approximation to this expectation. Unfortunately, because there are no useful bounds on the approximation, and because the approximation is used at every iteration of the algorithm, there are no results regarding the theoretical properties of this method. Determination of the hyperparameter is currently an open problem in LDA modelling (Wallach et al., 2009).

We illustrate our methodology on a corpus of documents from the English Wikipedia, originally created by George (2015). When a Wikipedia article is created, it is typically tagged to one or more categories, one of which is the “primary category.” The corpus consists of documents from the category Leopardus, from the category Lynx, and from Prionailurus, and we took , as in George (2015). There are words in the vocabulary, and the total number of words in the corpus is . The data set is relatively small. However, it is challenging to analyze because the topics are very close to each other, so in the posterior distribution there is a great deal of uncertainty regarding the latent topic indicator variables, and this is why we chose this data set.

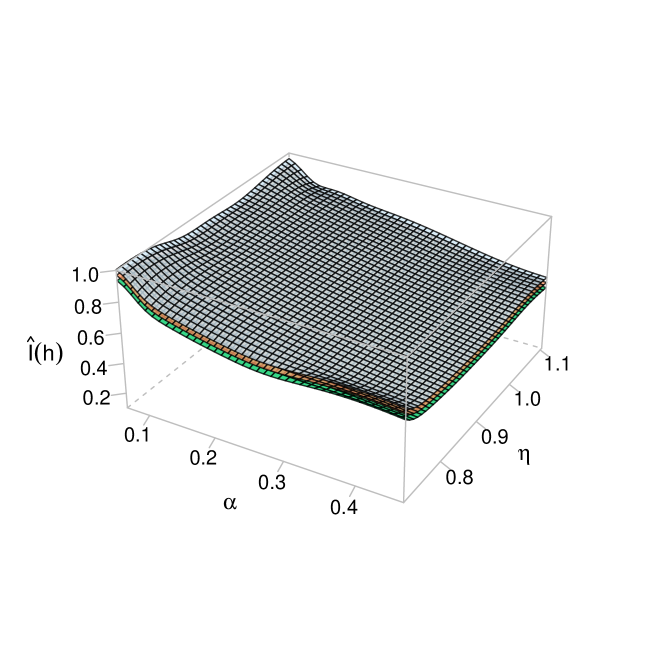

A reader of a given article may wish to look at related articles, so a question of interest is whether the topics for two given documents are nearly the same. One way to word this question precisely is to ask what is the posterior probability that , where and are the indices of the documents in question and is some user-specified small number. Here, denotes ordinary Euclidean distance. This posterior probability will of course depend on , and we would like to view the estimates of the posterior probability as varies, together with (simultaneous) error margins.

To this end, we used the methodology developed in Section 2.3 for simultaneous estimation of posterior expectations (here the posterior expectations of the indicator of a set). The warning given in Remark 9 regarding the high variance of the simple single-chain estimate (1.3) applies, and we use instead a serial tempering chain (cf. Remark 9), the details of which are given in the next paragraph. We consider documents and , which are the articles “Pampas cat” and “Pantanal cat” under the Wikipedia category Leopardus, and we are interested in the posterior probability of the event . Our estimate of is , and the estimate of the posterior probability under the empirical Bayes choice of is . For the other choices of we have , , and , and we see that all three are far from the estimate based on the empirical Bayes choice of . We also calculated the ratio of the marginal likelihood of to the marginal likelihood of each of , , and and noted that each ratio is astronomically large. Therefore, none of these values of are deemed even remotely plausible, and as these choices of do not have any theoretical basis, there is no credibility to posterior probability estimates based on them. Figure 1 gives a plot of the estimate of , together with a globally valid confidence set of level over a relatively small region centered at . The figure shows that the posterior probabilities vary greatly with , ranging from to , even over a small -region, underscoring the fact that the choice of hyperparameter should be made carefully.

Our serial tempering chain is based on the “augmented collapsed Gibbs sampler” developed in George (2015), and which runs on the entire set of latent variables . A single cycle of this Markov chain runs over nodes. To form the confidence region we used the construction described in Remark 8. We took the grid size for the chain (“” in Remark 8) to be , with the reference values evenly spaced over the -region. With this choice the chain gives very stable estimates. The length of the chain was , and the number of batches was (roughly the square root of the chain length). With this chain length the confidence region is adequately narrow, and with a length of only it was not.

3.2 Hyperparameter Choice for Bayesian Variable Selection in Linear Regression

The most commonly used setup for variable selection in Bayesian linear regression is described as follows. We have a response vector and a set of potential predictors , each a vector of length . Every subset of predictors is identified with a binary vector , where if is included in the model and otherwise. For every , we have a model given by

where is the vector of ’s, is the design matrix whose columns consist of the predictor vectors corresponding to , is the vector of coefficients for that subset, and . For this setup, the unknown parameter is , which includes the indicator of the subset of variables that go into the regression model. The prior on is a hierarchy in which we first select the variables that go into the regression model, then a “non-informative prior” is given to , and given and , we choose from some proper distribution. The specific instance of this model that we will consider is indexed by two hyperparameters, and , and is given in detail as follows:

| (3.1a) | ||||||

| (3.1b) | ||||||

| (3.1c) | ||||||

| (3.1d) | ||||||

The prior on given by (3.1d) is the so-called independence Bernoulli prior, in which every variable goes into the model with probability , independently of all the other variables. In (3.1b), is the number of predictors that go in the regression, and the prior on is Zellner’s -prior (Zellner, 1986). Because is given an improper prior (line (3.1c)), the prior on is improper; however, it turns out that the posterior distribution of is proper. Models of the type (3.1) were introduced by Mitchell and Beauchamp (1988) and have been studied in dozens of papers; see Liang et al. (2008) for a review.

The hyperparameter plays a critical role: if is small and is large, the prior concentrates its mass on models with few variables and large coefficients, while if is large and is small, concentrates its mass on models with many variables and small coefficients. (To appreciate the importance of the role played by , note that George and Foster (2000) have shown that for the slightly different version of (3.1) in which is assumed known, can be chosen so that the highest posterior probability model is exactly the best model under the AIC/, BIC, or RIC criteria.) Thus, effectively determines the method that is used to carry out variable selection, so it is important to choose it properly.

Unless is relatively small ( less than or ), the posterior distribution of is intractable, because to compute it we need to calculate integrals (George and Foster, 2000). Smith and Kohn (1996) developed a Markov chain algorithm which runs only on , the other variables being integrated out. Their chain is a simple Gibbs sampler which runs on the vector , updating one component at a time. This chain does not fit into our framework, which requires a Markov chain that runs on . Buta (2010) developed a Markov chain, based on the Smith and Kohn (1996) chain, which runs over . (She proved that for her Markov chain, the rate of convergence to the posterior distribution of is exactly the same as the rate of convergence to the posterior distribution of for the Smith and Kohn (1996) chain, where convergence is in terms of the absolute deviation norm.) We will use the chain developed by Buta (2010) for the analysis below.

To implement the methods of this paper, we need a “ratio of densities ” (cf. equation (1.3)). Note that the prior distributions are not absolutely continuous with respect to the product of counting measure on and Lebesgue measure on (the dimension of is not fixed). The “ratio of densities ” then needs to be replaced by the Radon-Nikodym derivative. To be precise, let be the distribution on induced by (3.1d), (3.1c), and (3.1b). Then (1.3) becomes

The Radon-Nikodym derivative was obtained in Doss (2007) and is given by

where is the density of the -dimensional normal distribution with mean and covariance , evaluated at .

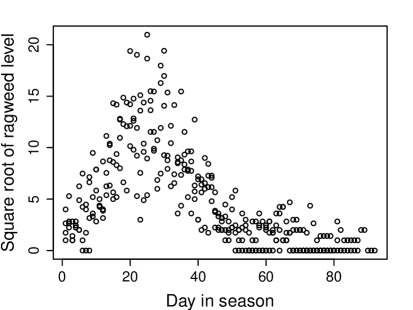

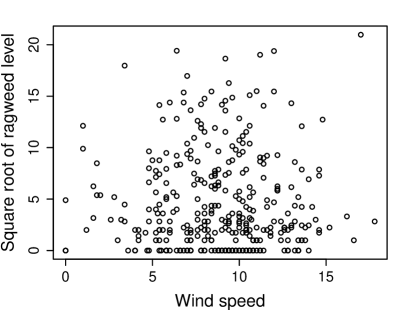

For our illustration we consider the ragweed data of Stark et al. (1997), who were interested in determining how meteorological variables can be used to forecast ragweed pollen levels. The response variable is the ragweed level (grains/m3) for days in Kalamazoo, Michigan, USA. Although the data set contains other predictors, we restrict our analysis to two: day (day number in the current ragweed pollen season) and wind (wind speed forecast in knots for following day). Following Ruppert et al. (2003), we take the square root of the ragweed level as the response. Figure 2 gives separate plots of the response versus each of the two predictors. From the figure we see that the effect of day is certainly nonlinear, but whether wind acts nonlinearly is not clear.

We fit each of the two predictors nonparametrically via cubic regression splines involving equally spaced knots. Hence the model we use has the form

for , where represent the knots for the day explanatory variable, the knots for the wind explanatory variable, and . Note that there are coefficients that could be set to , of which correspond to knots along the domain of the two predictors. Our plan is to carry out the following two steps:

-

1.

We form a point estimate and confidence region for by running a Markov chain.

-

2.

We estimate the posterior distribution of when the prior is , where is the estimate of obtained in Step , by running another Markov chain.

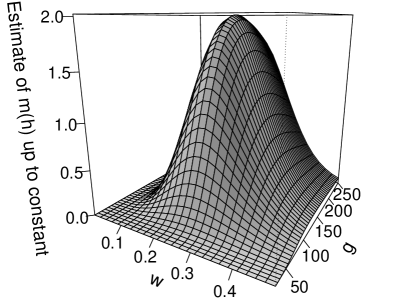

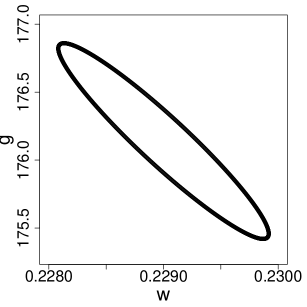

For Step we ran a Markov chain of length , using , from which we formed the surface , shown on the left panel of Figure 3. The argmax of the surface is , and the confidence region for is the ellipse shown in the right panel of Figure 3. For Step , we ran a new Markov chain, of length . For this chain, the highest probability model is the model which selects the variables wind, , , , and . Interestingly, this model is the same as the model selected by the lasso, when we choose the tuning parameter by cross-validation.

Let denote the ellipse. Our theory tells us that we are confident that , so we should run chains with posterior distributions , and determine the highest posterior probability models for all . By checking a few points on the boundary of the ellipse, we saw that the ellipse is narrow enough so that the highest probability model is the same for all . Had this not been the case, we would have run the Step chain for more cycles, getting a ellipse that is more narrow.

The value of that is selected is small, which reflects sparsity: a small model is adequate for fitting the data. We now put our approach in the context of the existing literature. Liang et al. (2008) review methods for selecting in the version of model (3.1) in which is fixed at . The literature has several data-independent choices (e.g. , but these generally do not perform well. As a data-dependent choice, they propose , and to obtain it suggest an EM algorithm in which the model indicator is viewed as missing data. Unfortunately, the M-step in the algorithm involves a sum of terms. Unless is relatively small, complete enumeration is not possible, and Liang et al. (2008) propose summing only over the most significant terms. However, determining which terms these are may be very difficult in some problems. Our approach provides a feasible way of obtaining the maximizer of the likelihood, and this for the model in which both and are unknown.

APPENDIX

Proof of Theorem 2

In order to prove Theorem 2, we need a few definitions and results from empirical process theory. An envelope is any function satisfying for all . For example, is an envelope for the class .

Definition 1 (Definition 2.7 of Pakes and Pollard (1989))

We say that the class is Euclidean for the envelope if there exist positive constants and with the following property: if and if is a measure for which , then there are functions in such that

-

1.

-

2.

The class is covered by the union of the closed balls (in the metric) with radius and centers ; in other words, for each in , there is an , with .

The constants and may not depend on .

Lemma 2 (Lemma 2.8 of Pakes and Pollard (1989))

If is Euclidean for the envelope and if , then converges to almost surely.

Lemma 3 (Lemma 2.13 of Pakes and Pollard (1989))

Let be a class of functions on indexed by a bounded subset of . If there exist an and a nonnegative function such that for and , then is a Euclidean class with the envelope , where is an arbitrary point of and .

Proof of Theorem 2

Recall that we have assumed that for almost all , is continuous in , and that is compact. Therefore, there exists a set , with , such that for all we have . For and any , we have

where lies between and . Let be an arbitrary point of . Define as follows:

where . By Lemma 3 with and , is Euclidean with envelope . We have

since for any , and by assumption. Therefore, by Lemma 2, converges to almost surely, i.e. the class is -Glivenko-Cantelli. ∎

Proof of Lemma 1

Denote and . Let and let be the open ball centered at and with radius . Since is the unique maximizer of , for any , , and since is compact, achieves its maximum on , say at , i.e. . Let . By uniform convergence, there exists such that for all , and in particular, for all . We have

| (A.1) |

At the same time, for all for all . Now if was in , we would have

which contradicts (A.1). Therefore, we conclude that . ∎

Proof of Theorem 4

Proof of Part 1. Recall that is the total number of cycles required to achieve regenerations, and note that implies . We expand around :

where is between and . Since and , we have

Our plan is to show that and that

| (A.2) |

as this will prove the theorem. To show , we first note that

| (A.3) |

Since all the conditions of Theorem 3 are satisfied, , which by Lemma 1 entails , so by continuity of at , we conclude that the second term on the right side of (A.3) converges to almost surely.

We now consider the first term on the right side of (A.3) and we use arguments similar to those used in the proof of Theorem 3 to show that this term converges to almost surely. For any ,

| (A.4) |

where the second equality in (A.4) follows by assumption (2.9). By A5, Theorem 1 implies that

and since , we obtain

i.e. . This shows that the first term on the right side of (A.3) converges to almost surely, which now implies that . Therefore,

| (A.5) |

We now consider the left side of (A.2). We have

Now in view of A1 and A2, Theorem of Hobert et al. (2002) implies that and . Also, . Therefore, by the CLT, , and together with (A.5), this implies (2.11).

Proof of Part 2. That follows by an argument virtually identical to the argument used to show that . Since is nonsingular, we obtain

We now proceed to show that , and we do this by working with quantities and which are the same as and , respectively, except that they do not include the terms and , respectively: Define

and

We will show that , which will show that . To show that , we express as the sum of four differences, and we show that each of these converges to almost surely. As in Remark 5, we will assume that . We do this only for notational simplicity, as all our results and arguments are valid without this restriction.

The first difference is . Letting

we have . By A7, Theorem 1 implies that . Consider now . Clearly . By A7, we may apply the dominated convergence theorem to conclude that , i.e. . Therefore .

The second difference is

We have

in self-defining notation. Consider . From A7, , and together with the SLLN, this gives , i.e.

| (A.6) |

Now

| (A.7) |

by the Cauchy-Schwartz inequality. The first expectation on the right side of (A.7) is finite by A7, and by Theorem of Hobert et al. (2002). Therefore,

| (A.8) |

From (A.6) and (A.8) we see that . From A6 and finiteness of , we may apply dominated convergence to see that , and so conclude that . Let denote the third difference. Since , we have also.

The fourth difference is

We showed earlier that . The SLLN gives (finiteness of is a consequence of Theorem of Hobert et al. (2002)). Therefore . ∎

Before we prove Theorem 5, we need to give some background material on empirical processes. The Pollard-Koltchinskii Theorem (Pollard, 1982; Koltchinskii, 1981), stated as Theorem 7 below, gives sufficient conditions for a class of functions to be Donsker. In order to state it, we need to introduce additional terminology. The covering number is the minimum number of open balls of radius using the norm whose union covers the class . In all of our development we will use the norm or the norm. The uniform entropy integral is

| (A.9) |

where is the set of all finitely discrete probability measures on and .

Theorem 7 (Theorem 8.19 in Kosorok (2008))

Let be a class of measurable functions with envelope and for which . Suppose that the classes and are all -measurable. If is measurable and integrable, then is -Donsker.

The condition in Theorem 7 can be verified by applying a simple upper bound to the covering number (inequality (A.10)) and Lemma 4 below.

Lemma 4

Let be a nonincreasing function. Suppose that for some constants and . Then .

Proof of Lemma 4

We have . Therefore

This convergence implies that there exists such that whenever . Without loss of generality, we suppose that . We have

Let be a set of functions defined on with envelope , let , and let be a probability measure on . Suppose that ; we can then define the norm on given by

Suppose additionally that is Euclidean for , and let and be the positive constants appearing in the definition of Euclidean (Definition 1). If and , then

| (A.10) |

(Nolan and Pollard, 1987, p. 789). We now return to the class . In the proof of Theorem 2 we showed that if for -almost all , exists and is continuous on , then for any point the class is Euclidean with envelope

| (A.11) |

where (recall that is the dimension of ). Thus, by (A.10) with , for , for any probability measure satisfying we have

For any probability measure and we have

Therefore,

so, Lemma 4 with and gives , i.e. the condition in Theorem 7 is satisfied. We summarize this in the following theorem.

Theorem 8

If for -almost all , exists and is continuous on , then the class is Euclidean with envelope given by (A.11), and .

Proof of Theorem 5

- 1.

-

2.

In essence the result is trivial: for -almost every sequence , converges to uniformly in and converges to uniformly in , so in view of the continuity of the function we have

which is assertion (2.22). There is a detail we need to check, namely that is bounded away from . Now by assumption, for every , exists and is continuous in ; so in particular, for every , is continuous in . Therefore, is continuous in by the dominated convergence theorem, and since is compact, .

-

3.

We will show that the class is -Donsker by checking the conditions of Theorem 7. By Theorem 8, the class is Euclidean with envelope given by (A.11), and . Equation (A.11) expresses as a sum of two functions, and . Since each of these is measurable and square-integrable with respect to , we may conclude that is measurable and integrable with respect to . Therefore the conditions of Theorem 7 are all satisfied, and we conclude that the class is -Donsker. The proof that is -Donsker is essentially identical.

-

4.

For -almost every , is continuous in , and as we saw in the proof of Part 2 of the present theorem, is continuous in ; so with probability one, . Because is compact, (a formal proof of this fact is given in Park (2015)). Therefore, weak convergence of in implies weak convergence of in , where is endowed with the sup norm (cf. van der Vaart and Wellner, 1996, Theorem 1.3.10); i.e. in , where is a mean Gaussian process. Similarly, in , where is a mean Gaussian process. Define the map by where, for definiteness, we define . It is not hard to check that is Hadamard differentiable at the point (for a definition of Hadamard differentiability see, e.g., van der Vaart and Wellner (1996, Section 3.9.1))—we use the fact , established in the proof of Part 2. The result now follows from the functional delta method (van der Vaart and Wellner, 1996, Theorem 3.9.4).

Proof of Theorem 6

- 1.

- 2.

-

3.

The proof is analogous to the proof of Part 3 of Theorem 5. For Part (a), we consider and instead of and , respectively. Continuity in of for almost all sequences follows from continuity in of for almost all , since with probability one, is a finite sum. In addition, by A1 and B1, for each . Since is measurable and square integrable with respect to P, by Part 3 of Theorem 5 we see that the class is P-Donsker. The proof of Part (b) is virtually identical. The only changes are that we consider instead of , and obtain finiteness of for all as a consequence of A1 and B2.

-

4.

The proof is entirely parallel to that of Part 4 of Theorem 5.

Prior to the statement of Theorem 6, we noted that when the chain has a proper atom at a singleton, then the sequence itself determines the regeneration times , so that can be viewed as a function mapping to . The minorization condition discussed in Section 2.1 (cf. (2.7)) determines the so-called “split chain” , for which the set is a proper atom (Nummelin, 1984, Section 4.4). The functions may then be viewed as maps , and the situation is the same as the simple situation described earlier.

Verification of Condition (2.6) for Exponential Families in Canonical Form

We now show that if for some fixed , and if is an exponential family and is the canonical parameter, then condition (2.6) holds. It is clearly sufficient to show that

| (A.12) |

(In fact, we can take where . So for example, instead of using a Markov chain with invariant distribution , we can use a serial tempering chain, whose invariant distribution is a mixture of the posteriors for ; see Remark 9.) Recall that denotes the dimension of . We will slightly abuse notation and write instead of , and instead of . This is to avoid notational clashes, e.g. writing and at the same time having . We assume that the ’s form a -parameter exponential family with dominating measure . Thus for , is a density with respect to , having the form , where the ’s and are real-valued functions. The set of all such that is called the natural parameter space, and we assume that is a compact subset of the interior of the natural parameter space. It is well known that is infinitely differentiable in the interior of the natural parameter space, and in particular is continuous there. We will prove (A.12) for the case , the case being no more difficult.

When , we have . We let for notational brevity. Without loss of generality we take the compact set to be . For any fixed , we have

Therefore,

| (A.13) |

for all . Let , which is finite, since is continuous and is compact. Let

By (A.13) we get

Acknowledgments

We thank the referees for their helpful comments.

References

- Asuncion et al. (2009) Asuncion, A., Welling, M., Smyth, P. and Teh, Y. W. (2009). On smoothing and inference for topic models. In Proceedings of the Twenty-Fifth Conference on Uncertainty in Artificial Intelligence. UAI ’09, AUAI Press, Arlington, Virginia, United States.

- Berger (1994) Berger, J. O. (1994). An overview of robust Bayesian analysis (with discussion). Test 3 5–124.

- Blei et al. (2003) Blei, D. M., Ng, A. Y. and Jordan, M. I. (2003). Latent Dirichlet allocation. Journal of Machine Learning Research 3 993–1022.

- Buta (2010) Buta, E. (2010). Computational Approaches for Empirical Bayes Methods and Bayesian Sensitivity Analysis. Ph.D. thesis, University of Florida.

- Doss et al. (2014) Doss, C., Flegal, J. M., Jones, G. L. and Neath, R. C. (2014). Markov chain Monte Carlo estimation of quantiles. Electronic Journal of Statistics 8 2448–2478.

- Doss (2007) Doss, H. (2007). Bayesian model selection: Some thoughts on future directions. Statistica Sinica 17 413–421.

- Doss and Tan (2014) Doss, H. and Tan, A. (2014). Estimates and standard errors for ratios of normalizing constants from multiple Markov chains via regeneration. Journal of the Royal Statistical Society, Series B 76 683–712.

- Flegal et al. (2008) Flegal, J. M., Haran, M. and Jones, G. L. (2008). Markov chain Monte Carlo: Can we trust the third significant figure? Statistical Science 23 250–260.

- Flegal and Jones (2010) Flegal, J. M. and Jones, G. L. (2010). Batch means and spectral variance estimators in Markov chain Monte Carlo. The Annals of Statistics 38 1034–1070.

- George (2015) George, C. P. (2015). Latent Dirichlet Allocation: Hyperparameter Selection and Applications to Electronic Discovery. Ph.D. thesis, University of Florida.

- George and Foster (2000) George, E. I. and Foster, D. P. (2000). Calibration and empirical Bayes variable selection. Biometrika 87 731–747.

- Geyer (2011) Geyer, C. J. (2011). Importance sampling, simulated tempering, and umbrella sampling. In Handbook of Markov Chain Monte Carlo (S. P. Brooks, A. E. Gelman, G. L. Jones and X. L. Meng, eds.). Chapman & Hall/CRC, Boca Raton, 295–311.

- Geyer and Thompson (1995) Geyer, C. J. and Thompson, E. A. (1995). Annealing Markov chain Monte Carlo with applications to ancestral inference. Journal of the American Statistical Association 90 909–920.

- Griffiths and Steyvers (2004) Griffiths, T. L. and Steyvers, M. (2004). Finding scientific topics. Proceedings of the National Academy of Sciences 101 5228–5235.

- Hobert et al. (2002) Hobert, J. P., Jones, G. L., Presnell, B. and Rosenthal, J. S. (2002). On the applicability of regenerative simulation in Markov chain Monte Carlo. Biometrika 89 731–743.

- Ibragimov and Linnik (1971) Ibragimov, I. A. and Linnik, Y. V. (1971). Independent and Stationary Sequences of Random Variables. Wolters-Noordhoff, Groningen.

- Jones et al. (2006) Jones, G. L., Haran, M., Caffo, B. S. and Neath, R. (2006). Fixed-width output analysis for Markov chain Monte Carlo. Journal of the American Statistical Association 101 1537–1547.

- Kadane and Wolfson (1998) Kadane, J. and Wolfson, L. J. (1998). Experiences in elicitation. Journal of the Royal Statistical Society: Series D (The Statistician) 47 3–19.

- Koltchinskii (1981) Koltchinskii, V. I. (1981). On the central limit theorem for empirical measures. Theory of Probability and Mathematical Statistics 24 71–82.

- Kosorok (2008) Kosorok, M. R. (2008). Introduction to Empirical Processes and Semiparametric Inference. Springer, New York.

- Levental (1988) Levental, S. (1988). Uniform limit theorems for Harris recurrent Markov chains. Probability Theory and Related Fields 80 101–118.

- Liang et al. (2008) Liang, F., Paulo, R., Molina, G., Clyde, M. A. and Berger, J. O. (2008). Mixtures of -priors for Bayesian variable selection. Journal of the American Statistical Association 103 410–423.

- Marinari and Parisi (1992) Marinari, E. and Parisi, G. (1992). Simulated tempering: A new Monte Carlo scheme. Europhysics Letters 19 451–458.

- Meyn and Tweedie (1993) Meyn, S. P. and Tweedie, R. L. (1993). Markov Chains and Stochastic Stability. Springer-Verlag, New York, London.

- Mitchell and Beauchamp (1988) Mitchell, T. and Beauchamp, J. (1988). Bayesian variable selection in linear regression. Journal of the American Statistical Association 83 1023–1036.

- Mykland et al. (1995) Mykland, P., Tierney, L. and Yu, B. (1995). Regeneration in Markov chain samplers. Journal of the American Statistical Association 90 233–241.

- Newton and Raftery (1994) Newton, M. and Raftery, A. (1994). Approximate Bayesian inference with the weighted likelihood bootstrap (with discussion). Journal of the Royal Statistical Society, Series B 56 3–48.