Optimal Portfolio in Intraday Electricity Markets Modelled by Lévy-Ornstein-Uhlenbeck Processes

Abstract.

We study an optimal portfolio problem designed for an agent operating in intraday electricity markets. The investor is allowed to trade in a single risky asset modelling the continuously traded power and aims to maximize the expected terminal utility of his wealth. We assume a mean-reverting additive process to drive the power prices. In the case of logarithmic utility, we reduce the fully non-linear Hamilton-Jacobi-Bellman equation to a linear parabolic integro-differential equation, for which we explicitly exhibit a classical solution in two cases of modelling interest. The optimal strategy is given implicitly as the solution of an integral equation, which is possible to solve numerically as well as to describe analytically. An analysis of two different approximations for the optimal policy is provided. Finally, we perform a numerical test by adapting the parameters of a popular electricity spot price model.

Key words and phrases:

Intraday electricity market, portfolio optimization, additive process, mean-reversion, partial integro-differential equation, approximation.1. Introduction

After power markets have been deregulated worldwide, this financial sector is experiencing profound structural changes. Several interesting issues have triggered a growing interest in models for energy markets. A rigorous mathematical approach may be useful for practitioners and at the same time stimulate the advance in academic research. In this work we consider markets structured as the European Power Exchange (EPEX), which regulates electricity spot trading in Central and Western Europe. In many exchanges, short-term trade is organized in mainly two markets: day-ahead and intraday. While the day-ahead market trades electricity for each hour (or block of hours) to be delivered the next day and is auction-based, the intraday market, which opens after the day-ahead closure, offers the participants the possibility to trade continuously until short time prior to delivery. The intraday market is especially important for renewable energy producers, who can adjust their day-ahead positions due to changes of weather forestcasts [33].

In this work we study a dynamic portfolio optimization problem designed for intraday electricity trading. These markets play an important role in the equilibrium of power grids, since both electricity producers and consumers are allowed to optimize their positions and reduce the risk of imbalance, which entails fees to be paid to system operators. Since the increasing penetration of renewable sources, modelling intraday trading has become particularly important, as well as mathematically interesting. Literature related to this problem is very recent: one of the first paper in this direction is [30], where the author studies how a wind power producer may benefit from trading in intraday markets by taking into account the risk of forecast production errors. [26] study an optimal trade execution problem in order to compensate forecast errors on wind or photovoltaic power production. [2] consider a producer who aims to minimimize the imbalance cost of his residual demand (which is stochastic) by controlling his flexible power production (thermal plants) and his position on the intraday market. Another recent paper [23] studies a stochastic multiperiod portfolio optimization problem in discrete time for hydroassets management and derives, in particular, an optimal intraday trading strategy. In [33] the authors investigate the impact of intraday updated forecasts of wind and photovoltaic on the bidding behavior of market participants, while [45] compare the price drivers in both the EPEX day-ahead and intraday electricity markets. Also, [13] study cross-border effects in intraday prices between interconnected locations and [44] consider a wind energy producer who trades in forward, spot, intraday and adjustment markets and derive optimal trading policies taking into account that his forecast production is imperfect. Our study arises as natural generalization of [20] and takes the perspective of a small agent interested in exploiting the stylized features of intraday prices in order to maximize his expected terminal gains.

We propose a stochastic model for the continuously traded electricity price and formulate an expected profit maximation problem in the language of stochastic control. The price is modeled by additive non-Gaussian Ornstein-Uhlenbeck (OU) processes. Power spot prices are usually described by either geometric [14, 27] or additive mean-reverting processes [7, 11, 34, 35, 36]. In the context of intraday markets, our model choice generalizes both [20], where the authors model the price by Gaussian OU processes, and [33], where the intraday price is an AR(1) process (with regime-switching that we do not consider), which is the discrete time version of the OU process. This class is highly flexible and capable to reproduce both the mean-reverting and the spiky behavior of observed time series. Since we do not perform a logarithmic transformation of the price, as is usually done, negative prices can be reproduced by our model: this is consistent with what has been recently observed since the introduction of renewable energy sources in the power mix (see [21]).

Following the pioneering work of Merton [37, 38], optimal portfolio management has become one of the most popular problems in mathematical finance and has been addressed in several different frameworks. For a general treatment we refer the reader to [39]. Our approach is based on the dynamic programming method and the study of the associated Hamilton-Jacobi-Bellman (HJB) integro-differential equation. Some related works include e.g. [8], where the price evolves as an exponential Ornstein-Uhlenbeck process, known as the Schwartz model, which is ubiquitous in commodity prices modelling. In [32] the authors model the risky assets with exponential Lévy processes and [41] generalize to exponential additive processes. We are inspired by [43, 46] when introducing a transformation for solving the HJB equation. Also, [9] study the same optimization problem for the Barndorff-Nielsen-Shephard model [5], where the volatility is a superposition of non-Gaussian OU processes driven by subordinators.

The problem of finding the value function is not straightforward from the formulation of the HJB equation. We study the case of logarithmic utility in order to disentangle the terms depending on both the wealth process and the strategy, from the ones depending on time and price. This simplification was also observed by [1] for a certain class of jump-diffusion processes. A theoretical study of optimal portfolios in the case of logarithmic utility is performed in [28] and furtherly generalized in [29], where the authors apply martingale methods (see [28, 29] and references therein for details on this approach) to a general semimartingale framework. However, although their analysis provides a characterization of an optimal strategy and its uniqueness, the study of its analytical properties is not explicitly addressed. We reduce the fully nonlinear HJB equation to a linear partial integro-differential equation (PIDE) by applying a logarithmic transformation as in [43]. Even though the optimal strategy is given implicitly as the solution of an integral equation, we are able to show that it is well-defined and satisfies sufficiently regular properties in order to apply the Verification Theorem.

We prove the existence of a classical solution to the HJB equation in two cases of interest: time-inhomogeneous compound Poisson processes with non-degenerate Brownian component and additive pure-jump processes of (possibly) infinite variation. This is done in the first case relying on a result by [42], while in the second case via Feynman-Kač representations. In the latter approach, we follow the idea of [9] and generalize it to time-inhomogeneous processes, which we do not assume to be of finite variation as in [9]. In particular, Danskin’s theorem [18] allows us to prove that the forcing term of the HJB equation, which is defined as the composition of non-differentiable functions, is actually differentiable.

Partial integro-differential equations (PIDE) are in itself of interest and arise across different fields of mathematics. In our paper we consider classical solutions, obtained via probabilistic representations, partly as extensions or complementary contributions of various earlier works. A classical reference for this type of problems is [6], where some existence results are stated under strong regularity assumptions on the coefficients of the equation. In proving the existence of a regular solution for finite Lévy measures with non-degenerate Brownian component, we apply a result of [42]. Nevertheless, this approach is based on classical smoothness results from PDE theory for linear second-order differential equations (cf. [25]), which require the finiteness of the jump measure. Consequently, for more general jump-processes we instead follow [9], where the Feynman-Kač formula yields a candidate, which is proven to be a classical solution of a PIDE very similar to ours. Unfortunately, this approach works only in the first-order case, i.e. with no Brownian component. However, as observed by [17], in order to generate realistic price trajectories, it is sufficient to consider financial models which are either finite activity jump processes combined with a diffusion part, or infinite activity pure-jump models, since the latter behave in a “diffusive” way when frequent small jumps occur.

We then study an approximation of the optimal strategy based on the Taylor expansion of the first-order condition, which is a numerical integral equation. In the case of compound Poisson processes, the center of the polynomial is chosen as the mean jump size. We compare it to the classical Merton ratio [37], which is shown to correspond to a Taylor expansion around zero. This approximation has been studied also in [3, 12, 40, 41] for stochastic volatility price models with jumps. Nevertheless, in their approach the authors start by approximating the HJB equation directly, while we work on the first-order condition. We derive some estimates of the approximation error and perform a numerical test on a power spot price model, specifically the factor model in [10]. Our main finding here is that Merton’s ratio performs poorly in comparison to our jump-based approximation, suggesting that optimal trading in Lévy-driven markets is not well described by this economically meaningful quantity, at least for the specific case of additive mean-reverting prices.

The paper is structured as follows. In Section 2 we introduce the intraday price dynamics and set our stochastic control problem. In Section 3 we describe the properties of our optimal strategy and study the reduced HJB equation for a logarithmic utility. In particular, two existence results of classical solutions to PIDE are given. We conclude this section by applying the Verification Theorem. The approximation study of the optimal strategy is contained in Section 4, while Section 5 presents an exemplary numerical test on the policy approximations. Appendix A includes auxiliary propositions for the existence of a PIDE solution in the first-order case, while in Appendix B we collect some of the most technical proofs.

2. The Optimal Portfolio Problem

We follow the dynamic programming strategy for solving our stochastic optimal control problem (see, for instance, [24]). The purpose is maximizing the expected utility of our portfolio over a set of trading strategies, that is to study the quantity

| (2.1) |

where is a utility function representing the risk profile of the investor, denotes the portfolio value associated to the strategy and is the trading closure time.

Let us introduce the stochastic dynamics driving the market. Denote by a real-valued additive process (for details see e.g. [16, Section 14.1]) defined on the complete filtered probability space by

| (2.2) |

where are continuously differentiable functions, such that for any and and do not vanish at the same time. The process is a standard Brownian motion and is the compensated Poisson random measure associated to a Lévy measure , i.e. a Radon measure on such that . In particular, if and are constant, with , then is a Lévy process. In order to deal with processes with finite second moment, we furtherly assume that satisfies the following integrability condition:

| (2.3) |

Observe that can be decomposed in a deterministic drift part, a Brownian motion with time-varying volatility and a square integrable pure-jump martingale component. We also introduce the following convention.

Remark 2.1 (Jump measure support).

It holds that supp for . We interpret the case formally as the diffusive case, i.e. when has no jump component. If, for instance, , we mean .

We are in a market with one asset (i.e. the continuously traded intraday price of electricity, expressed in Euros per MWh), whose market value evolves in time according to the stochastic differential equation

| (2.4) |

given the initial condition for some and . The constant is positive and represents the mean-reversion rate of . In particular, for any additive process there exists a unique (strong) solution such that in general for some , i.e. the price may assume negative values. Nevertheless, if can have only positive jumps and there is no Brownian component, i.e. it is a time-inhomogeneous subordinator (see e.g. [16]), then a nonnegative initial condition naturally implies that is a.s. nonnegative for each . Therefore, it is possible to consider additive processes taking both positive and negative values, according to one’s modelling preferences. The unique solution of (2.4), with starting condition , can be explicitly written as

| (2.5) |

Since has finite second moment by (2.3), has finite second moment as well.

If represents the amount of shares of the stock (i.e. the amount of energy in MWh), owned by the agent at time , the associated self-financing portfolio dynamics is described by

| (2.6) | |||||

| (2.7) | |||||

where and . We also assume that , so that the agent liquidates the position at the terminal time ; in other words, we are in a pure trading context (see [20, Remark 3.1]). We then define the set of admissible trading strategies and the value function.

Definition 2.2 (Admissible controls).

We call the set of admissible controls, which are defined as real-valued predictable processes on (in the sense of [31, Definition 3.3]) such that the following conditions hold:

- (1)

-

(2)

The associated wealth process is positive, i.e. , -a.s. for each and the final net position is zero: .

Definition 2.3 (Value function).

Following the dynamic programming principle, the Hamilton-Jacobi-Bellman (HJB) equation associated to this optimization problem is

| (2.8) | |||||

| (2.9) |

According to (2.4) and (2.6), the infinitesimal generator of the controlled process acts on a sufficiently regular function as follows

where is the jump measure associated to the two-dimensional process . Since this is a singular two-dimensional measure which coincides with the one-dimensional jump measure on the line , we can rewrite the integral term as

To link the HJB equation to the control problem, we formulate a Verification Theorem in the version of [24, Theorem III.8.1]. The basic tool is the well-known Dynkin formula (see [24, p.122]), which here applies to the controlled process :

| (2.10) |

where denotes the conditional expectation given and is any function for which the expression makes sense.

Theorem 2.4 (Verification Theorem).

Proof.

The proof is classical and follows directly from the Dynkin formula in (2.10). ∎

3. Optimal Control and Value Function for a Logarithmic Utility

In this section we solve the optimization problem in the case of a logarithmic utility, i.e. when the utility function in (2.1) is . Specifically, we find an explicit solution for the HJB equation by means of a logarithmic transform. First, we reduce the fully nonlinear HJB equation to a linear parabolic integro-differential equation for which, under certain assumptions, the existence of a regular solution can be proven. By applying the Verification Theorem of the previous section, we prove it to be equal to the value function of the original maximization problem (Theorem 3.13). We also state the existence and give a representation of an optimal strategy, which is shown to solve an integral equation.

3.1. Optimal strategy

By the properties of logarithmic utility, it holds that, if an optimal strategy exists, it takes the form

| (3.1) |

where is a predictable process that can be implicitly defined in terms of the semimartingale characteristics of , i.e. on the local behavior of the price process (see [28, Theorem 3.1]). This implies that we may explicitly characterize the strategies for which the wealth process is positive. In fact, for an admissible strategy we can rewrite (2.6) as

| (3.2) |

This allows us to have for general an explicit formula for , since it takes the form of a stochastic exponential (cf. [16, Section 8.4]). By Itô’s formula,

Proposition 3.1 (Positivity of the portfolio value).

If , it holds , -a.s., , if and only if

Proof.

From (2.6), if the jump measure at time of , regarded as an additive process, is denoted by , then it holds that supp supp . Then, -a.s., } if and only if { -a.s., }, which is equivalent to { -a.s., -a.e. , }. ∎

Therefore, the portfolio is positive for each strategy of the form such that takes values in a suitably chosen set. This sums up in the following characterization of admissible controls.

Definition 3.2.

Let be a compact set such that

A predictable process is called normalized admissible strategy if there exists an admissible strategy such that

for all , -a.s.

Remark 3.3.

According to the support of the measure , the set consists of

- case A:

-

if and (both positive and negative jumps),

- case B:

-

if and (only positive jumps),

- case C:

-

if and (only negative jumps),

- case D:

-

if (no jumps),

by consistently interpreting where necessary: for instance if , . Observe that in all cases we have . If and , then which makes the problem trivial. Therefore, in order to get rid of this situation, we may assume from now on that at least one between and is finite.

Remark 3.4.

The set is defined according to the jump features of the process (cf. the analogous notion of neutral constraints in [29, Section 2]). On the other hand, we have a certain freedom in the definition of , as we only require that it is a compact subset of . Intuitively, we are restricting the range of possible trading strategies so that the instantaneous portfolio value can not jump to (or below) zero for any admissible (normalized) position .

In order to find a solution to the HJB equation, we make the following ansatz:

This transform, which has been introduced in [20] for the specific case of Gaussian processes, is analogous to the one employed in [43], with the main difference due to the arithmetic nature of our spot price dynamics. We start from the static maximization problem, namely the maximization of the generalized Hamiltonian over all possible values of the strategies . As usual in this approach (see the discussion in [24]) a candidate optimal policy can be found by computing and defining . It is common to refer to the deterministic function as the optimal Markov control policy. Since we are in the case of logarithmic utility (cf. (3.1)), we can write . Simple computations yield

| (3.3) | ||||

Neglecting the terms which do not depend on , we have

where the function is defined as

| (3.4) |

The expression to be maximized with respect to the variable reads as the sum of three terms: a linear term, a strictly concave function and the integral of a strictly concave function. Therefore we are maximizing an overall strictly concave function on a compact set . This ensures the existence of a unique maximizer

| (3.5) |

Remark 3.5.

By adopting this notation we are revealing in advance that corresponds to an optimal strategy, but we have not given a proof yet. The optimality of this candidate will be derived in Theorem 3.13 by applying the Verification Theorem of the previous section.

Recalling that , we can write the HJB equation in reduced form

that is, consistently with our guess ,

After the terms with are collected, the equation reads

| (3.6) |

with terminal condition , where we define by

| (3.7) |

If we interpret (3.6) as an equation in the only unknown , it takes the form of a linear parabolic partial integro-differential equation (PIDE). The analysis of such an equation is typically a delicate task and, to the best of our knowledge, there are not many existence results for regular solutions in literature for this class of problems (see [6, 17, 19, 42] and references therein). Under certain assumptions, we are able to prove the existence and a probabilistic representation formula: we will do this in Propositions 3.11 and 3.12. It is crucial noticing that in the logarithmic case we can solve the HJB equation directly by disentangling the problem of finding and the function . This has been verified by the authors not to be the case for a general CARA or CRRA utility, which makes the issue of solving the HJB equation more difficult as well as interesting (see also [1]). Nevertheless, an approximation of the HJB equation has been proposed in an analogous stochastic framework for CRRA utility in [3, 40].

In order to solve the PIDE, we first have to study the properties of the strategy defined implicitly in (3.5). A straightforward application of the dominated convergence theorem and the finiteness of the second moment of assure that is differentiable for any and . Therefore, if the maximizer is a internal point, it is the unique solution of the first order condition

| (3.8) |

We remark that this is the explicit deterministic counterpart of the third condition appearing in [28, Theorem 3.1].

In the two upcoming propositions, we sum up the properties of the candidate (normalized) optimal policy and of the function appearing in the HJB equation.

Proposition 3.6.

Assume that is a compact interval containing . The static optimization problem in (3.4) and (3.5) admits a unique maximizer with the following properties:

-

(1)

For each , it holds .

-

(2)

The map is continuous and then, in particular, measurable and bounded.

-

(3)

For each , there exists an open interval such that the restrictions are strictly decreasing and smooth, where

- case A:

-

,

- case B:

-

,

- case C:

-

,

- case D:

-

.

Moreover, for any the derivatives of can be extended to .

-

(4)

For each , the map is decreasing on the whole real line and, in particular,

- case A:

-

there exist such that, for any , we have and

- case B:

-

there exists such that, for any , we have and for .

- case C:

-

there exists such that, for any , we have and for .

- case D:

-

we can write down the maximizer explicitly as

for each and such that the above quantity is well-defined and belongs to .

-

(5)

In particular, for all the maps are Lipschitz continuous uniformly in (i.e. with Lipschitz constant independent of ).

Proof.

See Appendix B. ∎

Remark 3.7.

Remark 3.8.

In order to interpret the results of Proposition 3.6, let us suppose for example to be in case A. Recall that in this case we can have both upward and downward jumps in prices (see Remark 3.3) and that the normalized position can take also negative values, so that short-selling is allowed. At each time , a trader who executes optimally takes a net zero position if price reaches the (time-dependent) “equilibrium” level . Furtherly, he goes long if price goes above this level and, accordingly, he goes short when the price is below. The trading allocation increases (with sign) as price decreases and vice versa. Also, (resp. ) consists of a lower (resp. upper) price threshold at which the trader, independently of the time instant, takes the longest (resp. shortest) position possible according to the trading constraints prescribed in .

Proposition 3.9.

The function in (3.7) is continuously differentiable and Lipschitz continuous, with partial derivatives

Furthermore, it grows as a linear function of uniformly in , i.e.

being dependent only on .

Proof.

Recall that by definition

which is a continuously differentiable function in the variable for any , since and are continuously differentiable. Then, by Danskin’s theorem [18, Theorem 1],

is differentiable with partial derivatives

Since they are bounded continuous functions, it follows that and Lipschitz continuous. The linear bound is direct consequence of the definition of and the boundedness of . ∎

3.2. Probabilistic representation and existence of regular solutions

After studying the regularity properties of the forcing term of the reduced HJB equation (3.6), we move on to the problem of existence of solutions. First of all, we clarify the natural notion of classical solution for such a class of integro-differential equations. Tracing through [15, Section 17.4], we say that a function belongs to the set , if it is once continuously differentiable in its first argument and twice continuously differentiable in its second and, furtherly, the following integrability condition holds true: for every and ,

| (3.9) |

Then, a classical solution of the HJB equation is a function belonging to and satisfying the integro-differential equation (3.6).

We now present three results. Firstly, we recall a version of the Feynman-Kač theorem, which gives the probabilistic representation of regular solutions. Then, we state two existence results for classical solutions: the first is valid for additive processes without diffusion part, while the second works for compound Poisson processes and uniformly non-degenerate Brownian component.

Theorem 3.10 (Feynman-Kač formula).

Assume that is a solution of (3.6), satisfying the growth condition:

If, moreover, there exists such that

then we can represent in the following Feynman-Kač type form

| (3.10) |

Proof.

The proof is classical: see [15, Theorem 17.4.10]. ∎

In the upcoming proposition we prove the existence of a classical solution to (3.6) in the case that there is no Brownian component.

Assumption 1.

The diffusion component in (2.2) is identically zero, i.e. .

We follow the idea of [9], where a guess is constructed via the Feynman-Kač formula. Let us remark that we generalize the result in [9] by proving the existence of a classical solution for time-inhomogeneus Lévy processes and possibly infinite variation square integrable Lévy measure. More in detail, we prove that

| (3.11) |

is a well-defined regular function and solves the PIDE in the classical formulation. We need some preliminary propositions, which are collected in Appendix A.

Proposition 3.11 (Pure-jump case).

Under Assumption 1, the function is continuously differentiable in for all and solves the following partial integro-differential equation:

with terminal condition . In particular, . Furthermore, for all and the following integrability condition holds:

Proof.

Fix and apply Itô’s Lemma to from to . Then, we have

Now, divide by and take expectation . Fubini’s theorem gives that

| (3.12) | ||||

By the mean value theorem, since the map is continuous, we have for a that

| (3.13) |

which converges to as approaches . Analogously, for the second term it holds that

for a . Since all the maps in the expectation are continuous, as tends to zero (cf. Lemma A.4), the last term converges to

Moreover,

Finally, the left-hand side can be written as

By the Markov property and the tower rule,

Therefore,

which converges to as goes to zero. Then, we have found that the limit of exists and is equal to

so that exists and it is continuous, being the right-hand term continuous. Also, we get from this expression that solves the integro-differential equation of the statement.

For the last point, as in Lemma A.4, it is sufficient observe that

since is Lipschitz continuous in uniformly in . ∎

In the last proposition, a result by [42] is applied to prove existence and uniqueness in the case that the second-order operator is uniformly elliptic and the jump part of is a compound Poisson process.

Assumption 2.

Assume in (2.2) that for all and is a finite Lévy measure.

Proposition 3.12 (Finite Lévy measure).

Proof.

First of all, observe that, since is the Lévy measure associated to a compound Poisson process, the spaces and coincide (cf. [15, Definition 17.4.9]). Therefore, we only need to verify if the assumptions of [42, Proposition 5.3] are fulfilled. Notice that (H6) there corresponds to assuming that the Lévy jump component is a compound Poisson process. Then, in order to apply [42, Proposition 5.3] it remains to prove that is Lipschitz continuous, which follows from Proposition 3.9. The integrability conditions can be proved as in Lemma A.3. ∎

Finally, we apply the Verification Theorem and state the main results of this section.

Theorem 3.13.

Let be a solution of (3.6) and assume that, for any and , we have the following conditions

where is the solution of

Then, the function , with as in Proposition 3.6, is an optimal Markov control policy, i.e. it induces an admissible strategy in the sense of Definition 2.2 and, for each , we get that .

Proof.

See Appendix C. ∎

4. Estimating the Optimal Strategy: the Merton Ratio and Taylor Approximations

After proving the existence and describing the analytical properties of the optimal strategy, we now study simple ways to compute it by approximation.

4.1. Definition and intuition

In his seminal work on portfolio selection [37], Merton studies the optimal allocation of the investor’s wealth when the risky asset follows a geometric Brownian motion:

and finds that the optimal allocation for a log-utility is111Consistently with our setting, we are assuming that the risk-free interest rate is zero and there is no consumption during the trading period.

which consists of the ratio of the excess return over the local variance of the log-price. Instead, in our framework the price dynamics are

Here, the local variance at time is the sum of the variance of the continuous component and that of the jump part . Then, in this context, it is natural to define the analogue of Merton’s Ratio as

| (4.1) |

This ratio appears naturally when applying a Taylor approximation to (3.8). Recall that the optimal normalized strategy is defined as

where

If the maximum is attained at an interior point (cf. Proposition 3.6), then satisfies the integral equation

| (4.2) |

If we replace the integrand by the second-order Taylor expansion around zero, the integral equation becomes

| (4.3) |

whose unique solution is exactly the strategy à la Merton that we defined in (4.1). A similar Taylor truncation has been introduced in [12] to study approximations of Lévy processes and tested numerically in [41]. Also, [3, 40] arrive at an analogous approximated strategy for stochastic volatility models with jumps, however they start by approximating the HJB directly. The idea is to treat the small jumps as an additional Brownian component (very much in the spirit of [4]) and neglect larger jumps.

Let us now introduce a more accurate approximation in the finite activity case. We assume that , i.e. the jump component of (2.4) is, in fact, a compound Poisson process, which is often the most interesting case for application purposes. Therefore, the Lévy measure takes the form , where is the jump intensity and the jump size distribution. Thanks to our standing assumptions, the distribution admits finite expectation and variance . We remind that the optimal policy is defined through the first order condition in (4.2). Let us write the Taylor polynomial of the integrand around an arbitrary (finite) point . So, we set and compute its derivatives. Writing down its expansion up to the first order, we have

| (4.4) |

Then, (4.2) becomes

| (4.5) |

From this expression it is clear that a significant simplification is given by the choice

since in this case the first-order term just disappears. Besides, by writing the Lévy measure with respect to , we see that corresponds to the mean value of the jump size:

| (4.6) |

We are essentially replacing the integrand with its linear approximation around the integral mean, or, from another point of view, we are approximating a function of the jumps with respect to the jump size mean value. Since here we take into account the jump measure specifications, this is a slightly different approach from the first approximation (where the Taylor polynomial was centered in zero). Hence, from (4.5) we have the following approximated equation for :

| (4.7) |

In the case , it is a second order polynomial in the variable . Consequently, for each we have two (generally) different solutions. However, only one of them is admissible, meaning that for every possible value of . Since the ambiguity comes from the definition domain of the logarithm, we just need to impose the condition . This leads to

where

On the other hand, in a pure jump context (), we get simply

| (4.8) |

for any and for each and such that is well defined and takes values into .

4.2. Error bounds

To estimate the approximation error, we compute the difference between the optimal normalized strategy and the approximated ones and .

Proposition 4.1.

Assume that contains and the finiteness of the third moment of the jumps, that is

and denote . If we are not in case D (no jumps) of Remark 3.3, then for each it holds that

where is a constant which depends on dist , and according to the following different cases:

- case A:

-

- case B:

-

- case C:

-

where .

Proposition 4.2.

Let us assume that we are not in case D of Remark 3.3. Moreover, we suppose and that and are not both identically 0. Then for each it holds that

where , is the square root of the variance of the random jump size and are constants depending on according to the following different cases:

- case A:

-

- case B:

-

- case C:

-

5. Numerical Example

In this section we test our trading strategies on one of the most popular electricity price models, namely the factor model in [10]. There, the authors conduct a critical comparison of three different spot price models for electricity in the context of day-ahead markets. In fact, this is typically an auction market in which the electricity price is fixed for the subsequent day, so that daily averaged prices are taken into account, over a timeline of years. Consequently, our setting concerns different market and price definitions. To recall, we instead take the point of view of an agent in the intraday market, which is the exchange where the electricity is traded continuously for 8-27 hours (depending on the contract) generally in the form of quarterly or hourly forward contracts. However, we aim to exploit the analysis in [10], where the model is calibrated to Nord Pool Spot market data, for mainly two reasons. Firstly, the stylized features of intraday markets are of similar nature as the ones observed in the day-ahead price series, such as spike behavior, high volatility, leptokurtosis (for a more detailed empirical study see, for instance, [20, 33]). Secondly, the factor model is based on a Lévy Ornstein-Uhlenbeck process of the same family as the one in (2.4).

We consider the factor model as in [10], which was originally introduced for electricity price modelling in [7]. The price dynamics are written as

where

is the deseasonalized price and is the seasonal component. The are positive weights while the factors are independent non-Gaussian Ornstein-Uhlenbeck processes described by

being independent càdlàg pure jump additive processes with increasing paths.

As the authors calibrate the model in [10], by comparing the theoretical autocorrelation function to the empirical one, they set the optimal number of factors to . The estimated speeds of mean reversion are and . In the paper these two values are interpreted as, respectively, the base (slowest) and the spike (fastest) signal. We start from here to define our equations. Specifically, their data series ranges from 13/07/2000 to 7/08/2008, which comprises, excluding the weekends, days. The time unit for is 1 day. So, in order to adapt it to our timeline, which covers hours of intraday transactions, first we set one hour as our time unit, that is we do the time variable change . Then, denoting , we set our mean reversion speed in our own model by rescaling in time the spike speed (), i.e. we take . The driving process is a compound Poisson process where the jump intensity, originally adopted in the paper by [27], is seasonally dependent. Also, the jump size distribution is a Pareto(,), with , and density function . Therefore, we are in the case of positive jumps: with the notation of previous sections, , i.e. , , and . The set can be any compact subset of containing .

For our own problem to make sense, another issue to address is to deseasonalize the jump intensity. In details, the form of the intensity is the following

where represents the expected number of spikes per time unit at a spike-clustering time, whereas the seasonal parameters are set by the authors’ calibration procedure , , . We then decide to compute the integral mean of over its time periodicity, that is , obtaining , so that, after rescaling, we have our intensity .

To summarize, the electricity price in our hourly intraday market is described by

| (5.1) |

where is the mean reversion speed and is a compound Poisson process with jump intensity and jump size distribution a Pareto law of parameters and . Therefore, there is no Brownian component in the jumps and the coefficient of the jump volatility is normalized to 1 ( and ). In particular it is important to notice that is a subordinator, which keeps the price positive. The drift value cannot be derived directly from [10], being not part of the spike signal and for this reason it will be discussed later.

Let us write the equation for the exact normalized strategy , defined in the integral equation (3.8), i.e.

or, expressing it in terms of the price level ,

| (5.2) |

where is the density of a Pareto law and the jump intensity of . By using a software to integrate exactly the above expression (we used Mathematica™) and inserting the estimated parameters inside the integral, we get

where is the hypergeometric function. This explicit formula states the value of the price with respect to the optimal strategy . The inverse relation can be computed numerically. As already observed, if we are interested in plotting the functions above, we need to set a value for the drift , being not consistently computable from the analysis in [10]. A quick study of the last expression yields the following.

Proposition 5.1.

Let us recall the definition of the jump measure mean

where is the mean of the jump size distribution . For each , if the drift in the price equation (5.1) is nonpositive, then for any . Furthermore, if the drift is greater than or equal to for , then for any , where denotes the inverse function of (within its range of invertibility).

Proof.

On one hand, the admissible values of the strategy belong to , which is any compact subset of containing 0. On the other hand, the price can take only positive values by construction (recall that is a subordinator). In (5.2) the function is increasing on the positive real line and it holds

Therefore, the first order condition in (5.2) is not satisfied for admissible values of and whenever since

This means that the maximum in (3.5) is attained at the boundary of and more exactly when (cf. Proposition 3.6). The case can be proven along exactly the same reasonings. ∎

Now, we write from (4.1) the first approximated strategy:

A straightforward computation yields . Observe that, in order that condition holds, must be non-negative. Having chosen any compact subset of containing for any , this reads

Finally, from (4.8) we get the second approximation of the optimal strategy:

still with the condition that (cf. Proposition 5.1).

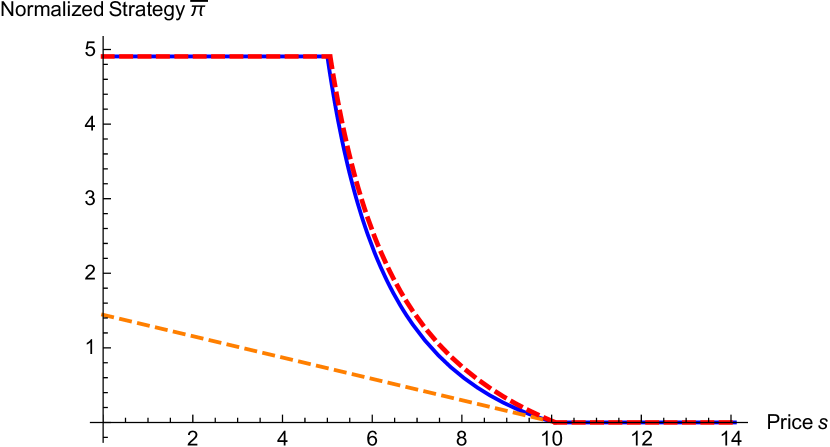

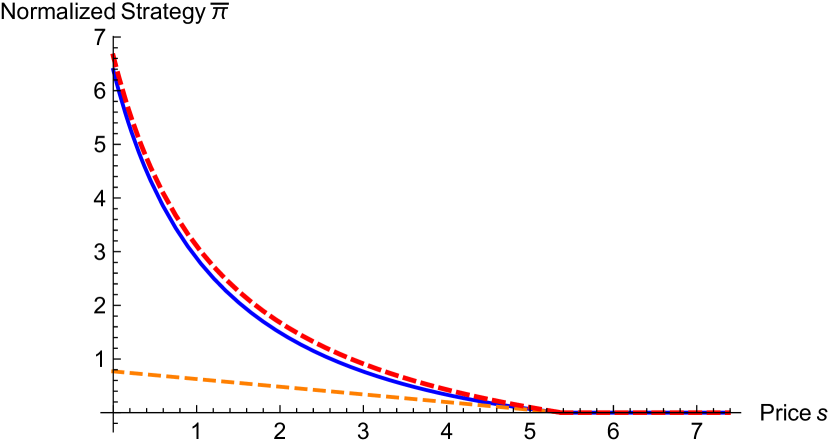

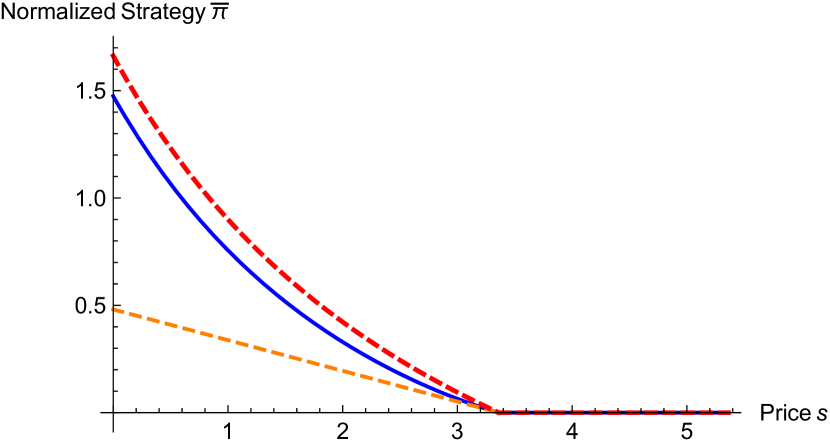

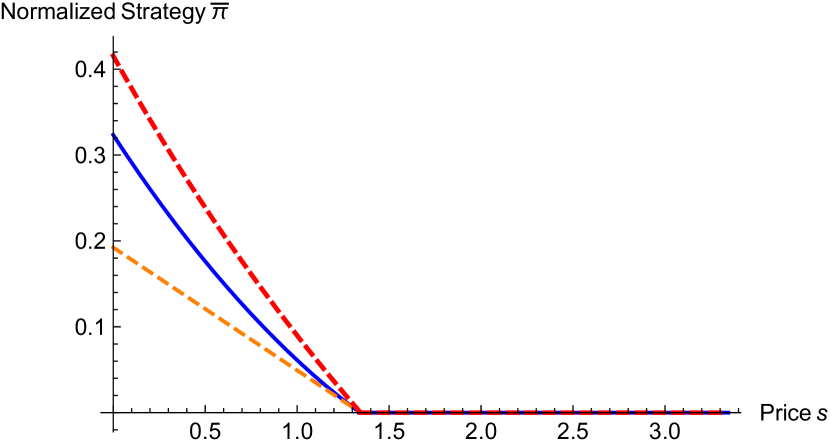

We now plot the different strategies: the exact and the two approximations. In view of Proposition 5.1 we do it for the following values of the drift of . In such a way we can understand their behavior in the most representative cases (see Figure 1). Remind that if , then , and are all identically equal to 0. We observe from our numerical results the following facts:

-

(1)

The order among the strategies: holds.

-

(2)

As approaches (and exceeds) , the second approximation gets much better, until it becomes almost indistinguishable from the exact strategy, while if approaches , the (considerable) error between the first approximation and the exact value decreases. In both cases, the shapes of the two approximations are similar to the one of . For instance, in the latter case the optimal strategy flattens out and looks like a straight line.

-

(3)

The bad performance of may be explained from the fact that it does not satisfy the requirements for the estimate in Proposition 4.1. This happens because the Pareto law estimated by [10] has parameter , which means that it admits finite second moment but not finite third moment (see assumptions of Proposition 4.1). Moreover, this approximation is natural for processes with small jumps, whereas the second one, i.e. , is more consistent with general jump processes since it is constructed around the jump measure mean . What is particularly interesting is that an economically meaningful quantity as the Merton Ratio, that we translated into (see Equation 4.1), performs generally much worse than the Taylor approximation.

-

(4)

As we already mentioned, essentially the same approximation is numerically investigated in [41]. What the authors found there is that it works rather well for three popular price models. The difference from our setting, which could even explain why we observe such an unsatisfactory performance, is that they are in the context of exponentially additive models, while our price dynamics are purely additive and mean-reverting.

Appendix A

The following lemmas are auxiliary results for Proposition 3.11. Let us recall that is described by

and can be written explicitly as

Furthermore, the candidate solution for the PIDE in Proposition 3.11 is defined as

| (A.1) |

Lemma A.1.

For all and , it holds that

Proof.

For , we have

Since

and

we find that

We conclude by Tonelli’s Theorem. ∎

Lemma A.2.

The function in Equation (A.1) is well defined. In particular,

Proof.

Lemma A.3.

The function defined in (A.1) is continuous in the time variable for any fixed and continuously differentiable in for any fixed time with bounded derivative. Specifically,

Furthermore, is Lipschitz continuous in the variable uniformly in .

Proof.

For the continuity observe that

As tends to zero, the second term vanishes by the dominated convergence theorem (cf. Lemma A.2). For the first term observe that

Hence,

which is Lebesgue-integrable for and approaches zero as tends to zero. Then, by the dominated convergence theorem, it holds that

vanishes and that is continuous.

In order to prove differentiability, we apply the classical theorem about differentiation under the integral sign. First, define

Since is continuously differentiable for each with partial derivative dominated by an integrable function:

we have

With the same argument, since

where is differentiable with dominated derivative, we get the statement.

Fix . Since

and is uniformly Lipschitz continuous (cf. Proposition 3.6), we have

where is a constant depending only on , and the Lipschitz constant of (which is independent of ). ∎

Lemma A.4.

For each , and , it holds that

and

are finite.

Proof.

For the first term it is sufficient to observe that

For the second part of the statement, recall from Lemma A.3 that is Lipschitz continuous in uniformly in . Let us denote by the weak derivative of (which is bounded). Therefore, we can write the Taylor expansion of in around the center with integral remainder:

Hence, for all , we have that

As a consequence,

which is finite by our standing assumptions on the Lévy measure . ∎

Appendix B

In this Appendix we collect some of the most technical proofs.

Proof of Proposition 3.6

We prove it for case A, the other cases being analogous. Let us denote , . We already observed, due to the concavity of the function in (3.4), that the map is well defined. Also, from (3.8) we immediately get that .

The continuity of the function relies on a general argument based on the concavity of . If , then . Take a sequence such that as . Then the statement follows from proving that . This is equivalent to saying that each subsequence of admits a subsequence which converges to . Take any subsequence of and denote it by (i.e. we do not rename the indexes). Since , which is compact, it admits a subsequence converging to a limit as . Observe that, for any ,

By definition of , we have that , which implies that . Since this argument is valid for an arbitrary subsequence of , we obtain that itself must converge to as .

Now, fix a . Then, the first order condition can be inverted in the following sense:

so to define the inverse function of from to . By the Inverse Function Theorem (cf. [22, Appendix C.5]), since

we get that, for a fixed , is strictly decreasing and continuously differentiable for any . Observe, in particular, that must be an interval, which we denote by . Also, since is smooth by Lebesgue’s dominated convergence theorem, with -th derivative

| (B.1) |

then is smooth. The boundedness of the derivatives of follows from (B.1) and the fact that, by definition, for each and .

Since as , uniformly with respect to and , there exist independent from and such that, for any and , and

By monotonicity of , it follows that

which proves the fourth statement.

The Lipschitz continuity of follows from the fact that its derivative in is bounded uniformly in and that is constant outside (and the constant is independent of ).

Proof of Theorem 3.13

The admissibility of is immediate consequence of Proposition 3.6. In order to apply the Verification Theorem (Theorem 2.4), which allows us to conclude, we need to prove that satisfies the Dynkin formula (2.10). By Itô’s lemma, for each admissible strategy , we get

Since , we can rewrite it as

Then the validity of Dynkin’s formula boils down to the martingale property of the process

Sufficient conditions are

The first two follow from the definition of (the range of ) and the boundedness of , while the last conditions depend on and are assumed valid in the statement. By standard integrability reasonings (see e.g. [41, Section 3.1] for an argument), we get that is a martingale, and then the result.

Proof of Proposition 4.1

We follow the same lines of reasoning as in Section 4 of [12]. First, let us write from (4.3) for and fixed and :

observing that

Hence,

Now,

By applying the Mean Value Theorem, since takes values in , a compact set whose distance from the boundary of is a certain and , we finally get the above estimate

where is the constant in the statement.

Proof of Proposition 4.2

Define for and fixed and :

being . Then,

and

Coming back to (4.4), observe that

By applying the Mean Value Theorem to :

with, for instance in case A, , since (cf. Proposition 4.1)

Therefore, we have found the following estimate:

Now,

Before applying the Mean Value Theorem again, let us compute

which is negative for each , so that

Finally, denoting , since ,

where is the square root of the variance of the jump size and are the constants in the statement.

References

- [1] K. K. Aase, Optimum portfolio diversification in a general continuous-time model, Stochastic Processes and their Applications 18 (1984), no. 1, 81 – 98.

- [2] R. Aïd, P. Gruet, and H. Pham, An optimal trading problem in intraday electricity markets, Math. Financ. Econ. 10 (2016), no. 1, 49–85.

- [3] M. Ascheberg, N. Branger, H. Kraft, and F. T. Seifried, When do jumps matter for portfolio optimization?, Quantitative Finance 16 (2016), no. 8, 1297–1311.

- [4] S. Asmussen and J. Rosiński, Approximations of small jumps of Lévy processes with a view towards simulation, J. Appl. Probab. 38 (2001), no. 2, 482–493.

- [5] O. E. Barndorff-Nielsen and N. Shephard, Non-Gaussian Ornstein-Uhlenbeck-based models and some of their uses in financial economics, J. R. Stat. Soc. Ser. B Stat. Methodol. 63 (2001), no. 2, 167–241.

- [6] A. Bensoussan and J.-L. Lions, Contrôle impulsionnel et inéquations quasi variationnelles, Méthodes Mathématiques de l’Informatique [Mathematical Methods of Information Science], vol. 11, Gauthier-Villars, Paris, 1982.

- [7] F. E. Benth, J. Kallsen, and T. Meyer-Brandis, A non-Gaussian Ornstein-Uhlenbeck process for electricity spot price modeling and derivatives pricing, Appl. Math. Finance 14 (2007), no. 2, 153–169.

- [8] F. E. Benth and K. H. Karlsen, A note on Merton’s portfolio selection problem for the Schwartz mean-reversion model, Stoch. Anal. Appl. 23 (2005), no. 4, 687–704.

- [9] F. E. Benth, K. H. Karlsen, and K. Reikvam, Merton’s portfolio optimization problem in a Black and Scholes market with non-Gaussian stochastic volatility of Ornstein-Uhlenbeck type, Math. Finance 13 (2003), no. 2, 215–244.

- [10] F. E. Benth, R. Kiesel, and A. Nazarova, A critical empirical study of three electricity spot price models, Energy Economics 34 (2012), no. 5, 1589 – 1616.

- [11] F. E. Benth, M. Piccirilli, and T. Vargiolu, Additive energy forward curves in a Heath-Jarrow-Morton framework, Preprint, 2018.

- [12] F. E. Benth and M. D. Schmeck, Stability of Merton’s portfolio optimization problem for Lévy models, Stochastics 85 (2013), no. 5, 833–858.

- [13] Á. Cartea, M. Flora, G. Slavov, and T. Vargiolu, Optimal cross-border electricity trading, In preparation, 2018.

- [14] Á. Cartea and M. G. Figueroa, Pricing in electricity markets: A mean reverting jump diffusion model with seasonality, Applied Mathematical Finance 12 (2005), no. 4, 313–335.

- [15] S. N. Cohen and R. J. Elliott, Stochastic calculus and applications, second ed., Probability and its Applications (New York), Springer, New York, 2015.

- [16] R. Cont and P. Tankov, Financial Modelling with Jump Processes, Chapman & Hall/CRC Financial Mathematics Series, Chapman & Hall/CRC, Boca Raton, FL, 2004.

- [17] R. Cont and E. Voltchkova, Integro-differential equations for option prices in exponential Lévy models, Finance Stoch. 9 (2005), no. 3, 299–325.

- [18] J. M. Danskin, The theory of , with applications, SIAM J. Appl. Math. 14 (1966), 641–664.

- [19] Ł. Delong and C. Klüppelberg, Optimal investment and consumption in a Black-Scholes market with Lévy-driven stochastic coefficients, Ann. Appl. Probab. 18 (2008), no. 3, 879–908.

- [20] E. Edoli, M. Gallana, and T. Vargiolu, Optimal intra-day power trading with a Gaussian additive process, Journal of Energy Markets 10 (2017), no. 4, 23–42.

- [21] EPEX, Negative Prices, http://www.epexspot.com/en/company-info/basics_of_the_power_market/negative_prices.

- [22] L. C. Evans, Partial differential equations, Graduate Studies in Mathematics, vol. 19, American Mathematical Society, Providence, RI, 1998.

- [23] S. Farinelli and L. Tibiletti, Hydroassets portfolio management for intraday electricity trading from a discrete time stochastic optimization perspective, Tech. report, 2017.

- [24] W. H. Fleming and H. M. Soner, Controlled Markov processes and viscosity solutions, second ed., Stochastic Modelling and Applied Probability, vol. 25, Springer, New York, 2006.

- [25] A. Friedman, Partial differential equations of parabolic type, Prentice-Hall, Inc., Englewood Cliffs, N.J., 1964.

- [26] E. Garnier and R. Madlener, Balancing forecast errors in continuous-trade intraday markets, Energy Systems 6 (2015), no. 3, 361–388.

- [27] H. Geman and A. Roncoroni, Understanding the fine structure of electricity prices, The Journal of Business 79 (2006), no. 3, 1225–1262.

- [28] T. Goll and J. Kallsen, Optimal portfolios for logarithmic utility, Stochastic Processes and their Applications 89 (2000), no. 1, 31 – 48.

- [29] by same author, A complete explicit solution to the log-optimal portfolio problem, Ann. Appl. Probab. 13 (2003), no. 2, 774–799.

- [30] A. Henriot, Market design with centralized wind power management: Handling low-predictability in intraday markets, The Energy Journal 35 (2014), no. 1.

- [31] N. Ikeda and S. Watanabe, Stochastic differential equations and diffusion processes, North-Holland Mathematical Library, vol. 24, North-Holland Publishing Co., Amsterdam-New York; Kodansha, Ltd., Tokyo, 1981.

- [32] J. Kallsen, Optimal portfolios for exponential lévy processes, Mathematical Methods of Operations Research 51 (2000), no. 3, 357–374.

- [33] R. Kiesel and F. Paraschiv, Econometric analysis of 15-minute intraday electricity prices, Energy Economics 64 (2017), 77 – 90.

- [34] S. Koekebakker, An arithmetic forward curve model for the electricity market, Working Paper 2003, Agder University College, Norway, 2003.

- [35] L. Latini, M. Piccirilli, and T. Vargiolu, Mean-reverting no-arbitrage additive models for forward curves in energy markets, Energy Economics. In press. Available online at https://doi.org/10.1016/j.eneco.2018.03.001, 2018.

- [36] J. J. Lucia and E. S. Schwartz, Electricity prices and power derivatives: Evidence from the Nordic power exchange, Review of Derivatives Research 5 (2002), no. 1, 5–50.

- [37] R. C. Merton, Lifetime portfolio selection under uncertainty: The continuous-time case, The Review of Economics and Statistics 51 (1969), no. 3, 247–57.

- [38] by same author, Optimum consumption and portfolio rules in a continuous-time model, J. Econom. Theory 3 (1971), no. 4, 373–413.

- [39] B. Øksendal and A. Sulem, Applied Stochastic Control of Jump Diffusions, Second ed., Universitext, Springer, Berlin, 2007.

- [40] I. Oliva and R. Renò, Optimal portfolio allocation with volatility and co-jump risk that Markowitz would like, Preprint, 2017.

- [41] L. Pasin and T. Vargiolu, Optimal portfolio for CRRA utility functions when risky assets are exponential additive processes, Economic Notes 39 (2010), no. s1, 65–90.

- [42] H. Pham, Optimal stopping of controlled jump diffusion processes: a viscosity solution approach, J. Math. Systems Estim. Control 8 (1998), no. 1, 27 pp. (electronic).

- [43] by same author, Smooth solutions to optimal investment models with stochastic volatilities and portfolio constraints, Appl. Math. Optim. 46 (2002), no. 1, 55–78.

- [44] Z. Tan and P. Tankov, Optimal trading policies for wind energy producer, SIAM Journal on Financial Mathematics 9 (2018), no. 1, 315–346.

- [45] G. Wolff and S. Feuerriegel, Short-term dynamics of day-ahead and intraday electricity prices, International Journal of Energy Sector Management 11 (2017), no. 4, 557–573.

- [46] T. Zariphopoulou, Optimal investment and consumption models with non-linear stock dynamics, Math. Methods Oper. Res. 50 (1999), no. 2, 271–296, Financial optimization.