Time Series Modeling on Dynamic Networks

J. Krampe1

1 University of Mannheim and TU Braunschweig

Abstract

This paper focuses on modeling the dynamic attributes of a dynamic network with a fixed number of vertices. These attributes are considered as time series which dependency structure is influenced by the underlying network. They are modeled by a multivariate doubly stochastic time series framework, that is we assume linear processes for which the coefficient matrices are stochastic processes themselves. We explicitly allow for dependence in the dynamics of the coefficient matrices as well as between these two stochastic processes. This framework allows for a separate modeling of the attributes and the underlying network. In this setting, we define network autoregressive models and discuss their stationarity conditions. Furthermore, an estimation approach is discussed in a low- and high-dimensional setting and how this can be applied to forecasting. The finite sample behavior of the forecast approach is investigated. This approach is applied to real data whereby the goal is to forecast the GDP of economies.

1 Introduction

Consider a vertex-labeled dynamic and weighted network with a fixed number of vertices given by the set . The weights are within the interval . Such a dynamic and weighted network with a fixed number of vertices can be described by a time dependent adjacency matrix, here denoted by , where is - valued. If no edge is present at time , a zero weight is considered. Thus, gives the weight of an edge at time from vertex to vertex . It is considered that the network is driven by some random process, hence, the corresponding adjacency matrix process is a stochastic process.

The vertices are considered as actors (e.g. people, countries), and a network could describe a relationship structure among these actors. A (weighted) edge between two actors describes some connection between them. The weights can be interpreted as the strength of the connection. For example, consider economies as actors where a possible relationship between two economies could be given by their relative trade volume at a given time point. Further examples are social networks, see [10, 23]. The actors in such networks often possess attributes. These attributes can be static (e.g a person’s name or birthday) or dynamic (e.g. personal income, time a person does sports, or political views). In the example with the economies and their trade volume as a relationship between them, dynamic attributes of interest are macroeconomic measures such as inflation rate or gross domestic product (GDP). These attributes may be affected by the attributes of other actors, especially by actors with which the considered actor is strongly connected. In this work, the dynamic attributes are denoted by a time series . To simplify the notation, we focus on the case that each actor has only one attribute, meaning that is d-dimensional. Nevertheless, this framework can also handle multiple attributes per actor, see Section 2 for details.

In this work, the dynamic attributes are denoted by a -dimensional time series , where each component of the time series is assigned to a vertex (actor) of the underlying network. In the social-economical literature, the influence of connected actors on the attributes is denoted as peer effect, see [8, 20].

This work focuses on the dynamic attributes and not on the network itself. Consequently, this work is not about modeling a dynamic network. For modeling these dynamic networks, many models for static networks have been extended to the dynamic case as done by [9, 15] for the Exponential Random Graph Models (ERGM), see Section 6.5 in [14], or by [38, 39] for the stochastic block model (SBM). By contrast, this work gives a framework which models the dynamic attributes, that means modeling a time series on a dynamic network, in which the weighted edges influence the dependency of the time series. [12, 42] have modeled these attributes for non-random edges, which mainly cover static networks. In the context of a static network, attributes can be considered as standard multivariate time series with additional information and can be modeled by using vector autoregressive (VAR) models with constraints, see Lütkepohl, [19, Chapter 2 and 5]. However, VAR models have many parameters, which is why [12, 42] focus on how to use the network structure to reduce the number of parameters so that high dimensions, meaning a large number of vertices, become feasible. By contrast, this work deals with a random network structure, and consequently, the process cannot be modeled appropriately by using VAR models. Instead, we adopt a multivariate doubly stochastic time series framework, meaning two stochastic processes drive the time series. On the one hand, there is the innovation process of the time series. On the other hand, the coefficient matrices in linear processes or autoregressive models are stochastic processes themselves. Doubly stochastic time series models were introduced in Tjøstheim, [31], Pourahmadi, [27, 28], and these authors assume that the two processes driving the time series are independent. That would mean the network could influence the attributes but not the other way around. This assumption could be too restrictive for most application. In the example where the GDP is the attribute and the trade volume defines the underlying network, the influence goes in both directions. To capture such behavior, we allow dependency between both processes, see Section 2 for details. Hence, the network, in form of the edges, can influence the attributes, and the attributes can influence the edges.

Knight et al., [11] extended the model of [12] to dynamic networks. Their model can be considered as a special case of the model considered in this paper, see Section 2 for details. They present an R-package to estimate their model, however, they present theoretical results only for the case of a static network such that the attributes can be written as a VAR model with constraints. Thus, they do not derive theoretical results for the dynamic case. This gap is filled in this work.

This paper is structured as follows. In Section 2, time series on dynamic networks are defined and some basic properties are given. In Section 3, the focus is on statistical results of network autoregressive processes, and their applications to forecasting are discussed. Some of the forecasting results are underlined by a simulation study which is given in Section 4. In Section 5, we apply this setup to forecast the GDP using the trade volume between economies as an underlying network. Proofs can be found in Section 7.

2 Time Series Modeling on Dynamic Networks

To elaborate, we first fix some notation. For a random variable , we write for , where ; for a vector , , and . Furthermore, for a matrix , , , , where denotes the vector with the one appearing in the th position. Let be a vector of ones. For a matrix , the absolute value evaluated component-wise is denoted by . Denote the largest eigenvalue of a matrix by and . The -dimensional identity matrix is denoted by . Furthermore, for two matrices the Kronecker product of and is denoted by , see among others Appendix A.11 in [19]. Let denote the component-wise multiplication of and , i.e. the Hadamard product. denotes the signum function, , and they are evaluated component-wise for matrix arguments. Let denote a -dimensional identity matrix without the rows and . An empty product denotes the neutral element, meaning . For a vector-valued times series , we write , and for a matrix-valued time series , we write .

With this, we can define a network linear process as follows.

Definition 2.1.

Let be a -valued, strictly stationary stochastic process, and let be measurable functions. Furthermore, let be an i.i.d. sequence of -valued random vectors with (positive definite and ). and are independent for all . If the following -limes exists,

| (1) |

we denote the process given by a (generalized) network linear process (GNLP).

Let and be measurable functions. A process fulfilling equation is denoted as a (generalized) network autoregressive moving average process of order (GNARMA)

| (2) |

In this work, the focus is on the following network autoregressive process of order given by

| (3) |

where are coefficient matrices, are some known measurable functions. Since (3) is a special case of (2), where the functions appearing in (2) have a particular form, we drop the term generalized. Note that the causal solution of (3) fits into the framework (1), see Lemma 2.2. Since for an adjacency matrix we have that gives the number of paths with length from node to node , examples for are polynomials. E.g., if for some lag the direct neighbors as well as the neighbors of these neighbors should have a direct impact, then can be chosen as Denote a vertex as a -stage neighbor of if there is a path from to of length but no shorter one. That means a direct neighbor is a -stage neighbor and a neighbor’s neighbor which is not a direct neighbor a -stage one. Given an adjacency matrix , the -stage neighborhood matrix is given by , where the ones in indicate the -stage neighbors of vertex .

For direct edges, two natural concepts occur; the concept that the influence goes in the direction of the edge and vice versa. Definition 1 can handle both concepts. E.g., if is used in (3), one can switch between both concepts. If not specified otherwise, the concept that the influence goes in the direction of the edge is used in this work. That means the easiest function for in model (3) is given by .

An NAR model can be written as a stacked NAR process in the following way. Let . Then, the stacked NAR process corresponding to (3) is given by

and

are the corresponding matrices of the stacked NAR process. The process is denoted by .

It is also possible to handle more than one attribute at a time by simply enlarging . For two different attributes we can replace by the following matrix , where and describe the (time-dependent) relationship between the different attributes. E.g, if there shall only be an influence between the different attributes of the same actor, we set , or if the different attributes shall influence each other in the same way as they are influenced by their own kind, we set .

Model (3) is inspired by [12]. Let be the order number for lag , which denotes the maximal stage neighbors included for lag . Let be a static adjacency matrix and denote by the -stage neighbors of vertex . Then, for component , their autoregressive model is given in the following way

| (4) |

Note that -stage neighborhood sets are disjoint for different . Thus, the above model fits into the framework (1) in the following way

| (5) |

Knight et al., [11] extended the model (4) to dynamic networks with potential covariates and edge weights. Apart from the covariates, their extended model fits also in the framework (3). As mentioned in the case of a static network, model (3) can be considered as a vector autoregressive model with parameter constraints. For this case, Knight et al., [11] give conditions for stationarity and showed consistency of the least square approach. However, they give no theoretical results for the case of a dynamic network. In this work, the focus is on the dynamic case. Note that for this case model (3) cannot be considered as a VAR model with constraints anymore.

The condition that and are independent for all ensures that (1) is a meaningful and causal representation. This condition allows that there could be an interaction between network and in a way that the network at time can be influenced by . That means an underlying network given by the adjacency process has to fulfill only this condition, strictly stationarity and later on some dependence measure conditions on the dynamic behavior, but we assume nothing about the inner structure of the network. Thus, it does not matter if its a sparse or dense network, or if it has properties like the small-world-phenomenon. Hence, it gives the flexibility that the time series and the underlying dynamic network can be modeled separately. One is not fixed to a specific network model as it would be the case for a joint modeling approach. Instead, the idea is that the approach described here is used to model the time series , and one of the several models for dynamic networks can be used to model the network .

If is a deterministic sequence, the GNARMA model is closely related to time-varying ARMA models, which, for instance, are used in the locally stationary framework; see [6, 32]. Furthermore, if is i.i.d., this framework reduces to the framework of random coefficient models, see for instance [25] and for the multivariate setting [24]. However, assuming independence between different time-points for the process seems to be inappropriate in the framework of dynamic networks. Some form of influence of the recent history seems to be more reasonable, see among others [10].

Assumption 1 gives conditions which implies that (3) possesses a causal, stationary solution, see the following Lemma 2.2 for details. Assumption 1a) imposes only conditions on , but no restrictions on the underlying dynamic network are required. If more about the underlying network is known, e.g. its weights and sparsity setting, one may work with Assumption 1b) which is more general but harder to verify without knowledge about the network. In Section 3.2, a simplified model is considered in which Assumption b) can be verified under simple conditions.

Assumption 1.

In (3) let for and let further one of the following hold

-

a)

for all ,

-

b)

, where denote the corresponding quantities of the stacked process.

Lemma 2.2.

The autocovariance as well as the mean of is affected by the dynamic behavior of the underlying network. In order to get a better understanding on how the dynamic dependency of the network affects the time series, the following Lemma 2.3 presents the autocovariance structure in the more simple case that and are mutually independent. Note that Assumption 1 implies for model (3) the conditions (ii),(iii) of the following Lemma.

Lemma 2.3.

Let be a generalized network linear process as defined in . If

-

i)

and are mutually independent,

-

ii)

for all (component-wise)

-

iii)

(component-wise),

hold, then converges component-wise in the -limit, and the autocovariance function is given by , and

| (7) |

and the mean function by .

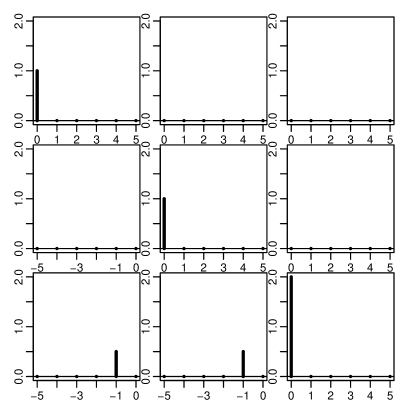

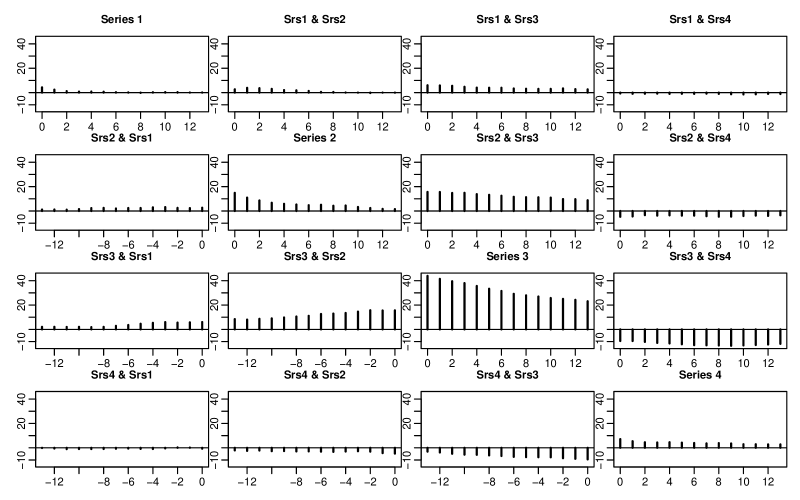

The latter term of the autocovariance function, , comes only into play for non-centered innovations and is driven by the linear dependency structure of the network. Consequently, it can be seen that the linear dependency of the network directly influences the linear dependency of the process . As a consequence, even a network moving average process of order may possess a nonzero autocovariance for lags higher than . In order to better understand this, consider a small toy example with three vertices and two possible edges, and , and only one edge is present at a time. Let be i.i.d. random variables with uniform distribution on , i.e., . Which edge is present at time is given by the random variables in the following way. If , then if , then else . If (that means ), then if , then else . Consequently, we flip in this network between the edges and , and if one edge is present at time , it is more likely (with probability ) that it is present at time than flipping to the other edge. We have dependency between different time points as well as between edges. and . Let be given by

| (8) |

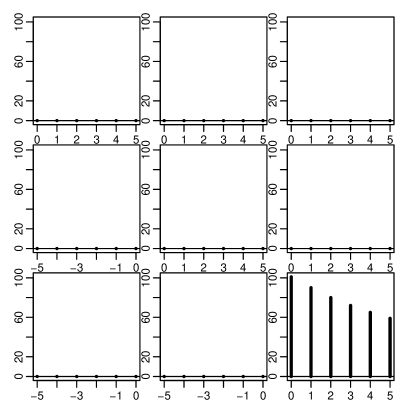

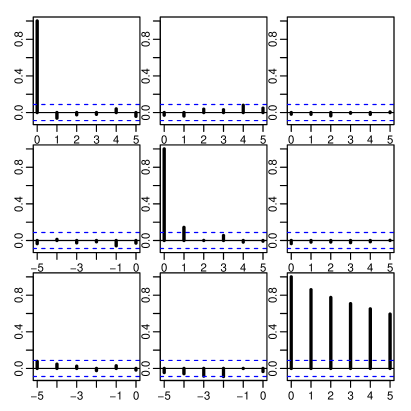

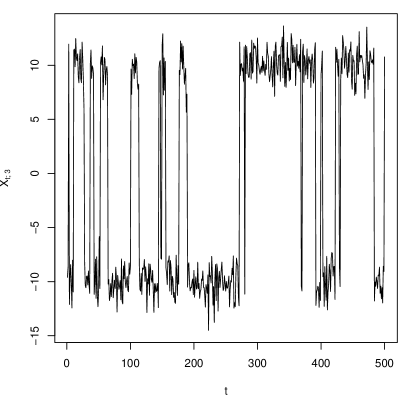

Thus, is a network moving average process of order , and the influence goes in the direction of the edges. Since no edge goes into vertex or , and are white noise. This can be also seen in the autocovariance function, which is displayed in its two parts in Figure 1. The left-hand side figures display the first part; . The dependency of the network has no influence on the first part, thus, this part would remain the same if a static model was considered where is replaced by its expected value. That is why this part of the autocovariance function has the structure one expects from a vector moving average (VMA) process of order . The right-hand side figures display the second part of the autocovariance function in Lemma 2.3, . As already mentioned, this part is completely driven by the linear dependence structure of the network. For the two edges, we have the following linear dependency: . This explains the geometric decay in the autocovariance function of the third component of , whereas the magnitude of the autocovariance function of the third component is mainly given by the difference of the mean of the innovations of the first two components. Hence, a greater difference of the innovations mean makes it harder to identify the linear dependency, which means the first part of the autocovariance function in Lemma 2.3, between components and , or and respectively. In this particular example with mean , no linear dependency between the different components can be identified for moderate sample sizes. A sample autocorrelation function as well as a realization of the third component of is displayed in Figure 2 for a sample size . Instead, looking from the perspective of the classical time series analysis, the sample autocorrelation function looks like we have three uncorrelated components where the first two components are white noises and the third could be an AR process. Hence, this examples gives two important aspects to keep in mind: firstly, the linear dependency of the network can influence the linear dependency of the time series directly. Secondly, the problem that the autocovariance function may not suffice to identify network linear processes such as network autoregressive models should be kept in mind.

3 Statistical results

In this section we focus on the estimation of model (3). As seen in the example in Section 2, the autocovariance function is not helpful to identify such models. Note further that even if is Markovian, an NAR process can generally not be written as a Hidden Markov model (HMM). This is because given is not a sequence of conditionally independent variables and cannot be written as a noisy functional of only, which is required by a HMM, see among others [2] for details on HMM. Consequently, techniques used for HMM cannot be applied here. Instead, the same setting as in Knight et al., [12, 11], Zhu et al., [42] is considered. Thus, the process as well as the network is observed leading to observations and . In such a setting, the consistency of a least square estimate as well as asymptotic normality for model (3) is shown in the first subsection. The results are presented under general assumptions and the asymptotic setting that is fixed and . Later on, we give dependence measure conditions for the underlying dynamic network such that the general assumptions hold. In the second subsection, a simplified version of model (3) is considered. This simplified model is suited for high-dimensional cases, and consequently, the theoretical estimation results are presented nonasymptotically.

3.1 Network autoregressive models

Networks usually come together with some form of sparsity, see among others Section 3.5 in [14]. This means that a vertex has only a connection to a limited number of other vertices and could have some zero entries or might even be a sparse matrix. Thus, might be sparse matrices as well. That means the number of parameters of model (3) is given by and depends on the sparsity of the underlying network. Let be a set of indices corresponding to the non-zero coefficients of and is the corresponding population quantity. Note that for all . Only parameters corresponding to indices of the set are well defined in the sense that they have an influence on the process. We set the other parameters, meaning those corresponding to indices of the set , to zero. Recall that denotes a -dimensional identity matrix without rows and Let for and

Then for and we can write (3) as

| (9) |

Thus, and can be estimated by using the following least square approach given by For component , this leads to the following linear system:

| (10) |

We show the consistency of the least square estimators under general assumptions. Later on, we specify a dependence concept for the underlying network which ensures these general assumptions, see Lemma 3.2.

Assumption 2.

For all we have, as ,

-

1.

, and , ,

-

2.

and

-

3.

For all and .

Assumption 3.

For all we have, as ,

where .

Theorem 3.1.

The results of Theorem 3.1 can be used to forecast the process . If is observed, then let and a one-step ahead forecast of is given by Since is i.i.d. and are consistent, we have . If is not observed, itself needs to be predicted first. This could be done by fitting a dynamic network model to and using this model to predict . An -step ahead forecast can be done recursively, which means performing a one-step ahead forecast based on the observations and the results of the -step ahead forecasts.

Assumption 2 mainly requires a conversion rate of the first and second sample moments of . An absolutely summable autocovariance function of is sufficient for the convergence of the first sample moments. As pointed out in Lemma 2.2 and Lemma 2.3, the autocovariance of depends on the dependency structure of . For simplicity, consider the following network moving average process where and are independent. Following Lemma 2.3, we obtain . Hence, even for this simple moving average process, a summmable autocovariance function can be obtained only if possesses some sort of short-range dependence. Several general dependency concepts exists which could describe a short-range dependency structure such as mixing[3], some weak dependency concepts[7] or physical dependence[33, 35, 37, 17]. Since the concept of physical dependence works well also in the high-dimensional case, see among others [40, 41], this concept is used to quantify the dependence structure of .

To elaborate, let be a sequence of i.i.d. random vectors of dimension such that is also an i.i.d. sequence. Furthermore, let , where is some measurable function to . Denote by an i.i.d. copy of and let for some where is a coupled version of with in the latter being replaced by . Since is a function to , for . Furthermore, let The process is denoted as -stable if . This property still holds for some nonlinear transformations, see [33, 34]. E.g. consider a polynomial transformation given by . Note that for some matrices we have . If , then . Without assuming any sparsity, an upper bound is given by . This dependency concept covers a wide range of processes among them many nonlinear time series, see [33, 35, 37] for examples. Furthermore, this concept includes nonlinear Markov chains, meaning can be given by . Zhang et al., [41] pointed out that a stable process is obtained if possesses some form of Lipschitz-continuity. Then, for some , see Example 2.4 in [41] or Example 2.1 in [5] for details. A stable vector autoregressive process possesses also such geometrically decaying physical dependence coefficients, see among others Example 2.2 in [5]. Note that many dynamic network models, e.g. Temporal ERGMs [9], are Markovian.

3.2 Network autoregressive models for large dimension

The number of parameters in model (3) is of size . If the underlying network is not very sparse, a reasonable estimate could be only obtained if . Hence, in order to handle high-dimensional cases, meaning is of the same order as or even larger, we follow Knight et al., [11] and simplify model (3). For each component, the influence of the own lagged components is modeled separately, thus, we set for all . Then, the simplified model is given by

| (11) |

where and . Hence, this simplified model possesses in total only parameters or more precisely only parameters for each component of the time series independently of the dimension. The parameter quantifies the linear influence of the same component and the linear influence of the other components. Note that model (11) can be written as

| (12) |

and consequently fits into the framework (3). We denote the process as Large Network AutoRegression (LNAR) and the coefficient matrices occurring in (12) by . Since a LNAR is an NAR process, a stationary solution is given by Lemma 2.2 if for all or . If no restrictions on the underlying network are imposed, then the first condition implies that in order to obtain a stationary solution, the parameter space depends on . This is not the case we would like to consider here, which is why conditions on the underlying network are imposed. We require that , which means that the sum of weights of the edges going into a vertex does not grow with the dimension . To simplify notation, we bound the sum of weights by . Knight et al., [11] require a similar condition in the case of a static network. Under this condition, we obtain a stationary solution if , see the following Lemma 3.3. Note that under the same conditions Knight et al., [11] obtain a stationary solution in the case of a static network.

Lemma 3.3.

If for and , then (11) fulfills Assumption 1b) and possesses a stationary solution. The solution takes the form

| (13) |

where

Furthermore,

For component , let and . Then, (11) can be written as . This is the same framework as in Section 3.1, and the linear system (3.1) gives a least square estimate. To cover a high-dimensional setting, we study the theoretical properties of this estimator in a nonasymptotic framework as it is done in the high-dimensional vector autoregressive case, see among others [1]. We make use of the Nagaev inequality for dependent variables, see Theorem 2 in [18], to formulate nonasymptotic error bounds. Again, the physical dependency concept is used to quantify the dependency structure of , see the following Assumption 4.

Assumption 4.

For let and let be -stable with , where is some constant. Furthermore, let and . The constants appearing here do not depend on the dimension .

Note that and implies . Furthermore, we have a bound for the largest eigenvalue , see the proof of Lemma 3.3. If where and for all , then . If possesses geometrically decaying physical dependence coefficients, then .

This Assumption implies that as well as are -stable and their physical dependency quantity can be bounded independently from the dimension , see Lemma 3.4 for details.

Lemma 3.4.

With this results, we can formulate the nonasymptotic error bounds. In order to handle a high-dimensional setting an import result is to obtain an error bound which grows only moderately with , the dimension of the process. Note that in contrast to the estimation of a high-dimensional VAR system, e.g. [13], the dimension of the parameter vector does not depend on . This enables us to obtain an error bound which does not depend on at all, see the following Theorem 3.5 for details.

Theorem 3.5.

For , the error tends to zero but the probability still faces with increasing . This rate is independent of the dimension . This enables us to use LNAR for forecasting in a high-dimensional framework. The forecasting procedure is analogue to the one for the NAR approach, see the end of the previous subsection.

4 Numerical Examples

In this section, the forecasting performance of the models presented in Section 2 is investigated in finite samples. For a low-dimensional example and a high-dimensional example, we forecast based on observations and , where . The performance is measured by computing the mean squared error (MSE) averaged over all components via a Monte Carlo simulation using repetitions, meaning

where denotes the th component of the th observation of the th Monte Carlo sample. In the following, we denote the approach using model (3) as NAR and the approach using model (11) as LNAR. As a benchmark, we use a vector autoregressive model given by , where . This approach is denoted by VAR. The three models considered have a tuning parameter which specifies the lag order. For all three models, the Bayesian Information Criterion (BIC) is used to automatically choose the lag-order , see among others Section 5.5 in [4].

The approaches NAR and LNAR make use of the underlying network structure. That means in order to compute , the approaches NAR and LNAR require an observation or at least an estimate of the underlying network structure. Both cases are considered here, in the first case we forecast based on the observations , and in the second case we assume that is observed. In order to distinguish between these two cases, we denote the forecast of approach NAR based on an estimated network by NAR and the forecast based on a known network structure by NAR. An analogue notation is used for LNAR.

All computations are done in R [29] using the additional packages tergm, BigVAR, markovchain [16, 26, 30].

In the first example, a network with vertices is considered. The adjacency matrix process is a Markovian process and the edges are independent from each other. The process is given by

| (16) |

The process is an NAR process and is given by

| (17) |

where .

[width=loop=TRUE,autoplay=TRUE]1MarkovNetwork_d_4

A realization of the network, the time series, and the sample autocovariance function are displayed in Figure 3. The edges and have a coefficient of , hence, whether they are present or not, they do not influence the time series .

The model structure of is used to compute a forecast of . Thus, for each component of , a discrete Markov chain is fitted to , and this Markov chain is then used to obtain a forecast for . For this the R-package markovchain was used.

The mean squared errors for the forecast horizons are displayed in Table 1. Note that an optimal one-step ahead forecast for this process would possess a forecast error of . This can be nearly achieved by NAR with a known network structure and moderate sample size. If the underlying network structure is unknown, NAR outperforms the other approaches for the forecast horizons up to . For forecast horizons further ahead, VAR performs slightly better. This drop in performance for horizons further ahead is mainly caused by the estimate of the underlying network structure. The approach used here causes that is identical for all horizons . This estimate gets poorer, the larger is.

| n | |||||

|---|---|---|---|---|---|

| NAR | 1.24 | 1.42 | 1.53 | 1.61 | |

| NAR | 1.47 | 2.80 | 3.67 | 4.14 | |

| 50 | LNAR | 1.89 | 2.32 | 2.62 | 2.91 |

| LNAR | 2.00 | 3.18 | 4.04 | 4.63 | |

| VAR | 2.83 | 3.56 | 4.08 | 4.35 | |

| NAR | 1.07 | 1.19 | 1.23 | 1.25 | |

| NAR | 1.20 | 2.76 | 3.56 | 4.13 | |

| 100 | LNAR | 1.78 | 2.18 | 2.35 | 2.47 |

| LNAR | 1.83 | 3.08 | 3.86 | 4.49 | |

| VAR | 2.65 | 3.40 | 3.80 | 4.08 | |

| NAR | 1.01 | 1.12 | 1.14 | 1.16 | |

| NAR | 1.11 | 2.63 | 3.55 | 4.09 | |

| 200 | LNAR | 1.71 | 2.04 | 2.20 | 2.30 |

| LNAR | 1.74 | 2.88 | 3.71 | 4.30 | |

| VAR | 2.63 | 3.30 | 3.69 | 4.01 | |

| NAR | 1.01 | 1.11 | 1.14 | 1.15 | |

| NAR | 1.13 | 2.66 | 3.41 | 4.10 | |

| 500 | LNAR | 1.69 | 2.00 | 2.14 | 2.23 |

| LNAR | 1.73 | 2.91 | 3.60 | 4.32 | |

| VAR | 2.60 | 3.27 | 3.60 | 3.92 |

In the second example, a Separable Temporal Exponential Random Graph Model (STERGM) is considered, see Krivitsky and Handcock, [15] and also [16] for the used R package tergm. The network is generated using simulate.stergm of the R-package tergm with dissolution coefficient , formation coefficient , and a mean density of . Networks of the sizes , and are considered, and for each network size the sample sizes , and . For , such a network has about edge changes from to . Let be the adjacency matrix of such a network at time and let be a diagonal matrix, where is defined as . This defines the function and let . This means apportions equally the weight among the in-going edges to vertex at time , and we have . Then, the process is given by the following LNAR(1) model

| (18) |

where and and is a banded matrix with ones on the diagonal and on the first off diagonal. The function is considered as known, meaning is observed.

Two approaches are used to obtain a forecast for . The first approach fits a STERGM model to and then generates by simulating the fitted model with as a starting value. This forecast is denoted as . The second approach fits for each component independently a discrete Markov chain and uses this to forecast . The second approach is denoted as .

Since a standard VAR model cannot be applied well to a high-dimensional setting, the VAR estimation is modified by adding sparsity constraints, meaning a coefficient is set to zero for if . This is motivated by the fact that in model (18) if , then do not directly influence . Furthermore, forecasts given by the R-package BigVAR are included as additional benchmarks, see [26]. There the idea is that the underlying VAR model is sparse but the sparsity structure is unknown. It can be estimated by using a LASSO approach, see among others [1, 13]. The forecast obtained by a such a model of order is denoted by BigVAR, where .

The mean squared errors of the forecasts are displayed in Table 3 to Table 4. Note that an optimal one-step ahead forecast would possess a forecast error of . With a known network structure at hand, LNAR is nearly able to achieve such optimal results independently of the dimension. Is the future network unknown, then the forecasting performance of NAR and LNAR drop considerably. Especially for LNAR, the loss of performance due to an unknown network structure seems to increase with the dimension of the process. Of the two approaches used to forecast the network, a better performance is given by the network forecasting approach for NAR as well as LNAR. Given the network forecast , both approaches still outperform all others namely VAR and BigVAR. As mentioned, VAR uses the underlying network structure to set sparsity constraints such that the number of parameters can be reduced. In all settings considered, VAR outperforms BigVAR. This indicates that for this process the network induced sparsity constraints are more helpful than a free but unknown sparsity setting as given in BigVAR. However, note that the amount of parameters which are estimated for the approaches NAR and VAR depend on the set and we have for . This could explain why these two approaches do not gain immediately from an increasing sample size for larger dimensions.

In order to get a better overview of the results, we set the MSE of the approach VAR as basing point, meaning all MSE values are divided by the corresponding VAR’s MSE. An average over all sample sizes and forecast horizons leads to Table 2. These aggregated results support the argument that the approaches NAR and LNAR benefit from the underlying network structure and even when the future network structure is unknown and needs to be estimated itself, there is still a benefit. For higher dimensions, only LNAR performs well whereas the performance of all others drop dramatically, meaning that the network induced sparsity does not seem to be sufficient to obtain good estimation results in this setting.

| 10 | 33 | 100 | 500 | |

|---|---|---|---|---|

| NAR | 0.35 | 0.33 | 0.44 | 0.51 |

| NAR | 0.71 | 0.74 | 0.78 | 0.77 |

| NAR | 0.84 | 0.93 | 0.95 | 0.96 |

| LNAR | 0.27 | 0.04 | 0.01 | |

| LNAR | 0.66 | 0.60 | 0.56 | 0.53 |

| LNAR | 0.80 | 0.85 | 0.81 | 0.80 |

| VAR | 1.00 | 1.00 | 1.00 | 1.00 |

| BigVAR | 2.99 | 5.35 | 6.35 | 7.88 |

| BigVAR | 3.24 | 5.71 | 6.68 | 8.09 |

| Model | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| NAR | 6.9E+00 | 1.1E+01 | 1.5E+01 | 1.9E+01 | 3.4E+01 | 7.2E+01 | 1.1E+02 | 1.6E+02 | |

| NAR | 9.7E+00 | 1.8E+01 | 2.7E+01 | 3.6E+01 | 5.6E+01 | 1.3E+02 | 2.1E+02 | 2.9E+02 | |

| NAR | 1.2E+01 | 2.3E+01 | 3.2E+01 | 4.3E+01 | 7.5E+01 | 1.6E+02 | 2.5E+02 | 3.4E+02 | |

| LNAR | 5.1E+00 | 7.1E+00 | 8.5E+00 | 9.6E+00 | 5.3E+00 | 7.2E+00 | 8.5E+00 | 9.4E+00 | |

| 100 | LNAR | 8.3E+00 | 1.6E+01 | 2.3E+01 | 3.1E+01 | 4.1E+01 | 1.0E+02 | 1.7E+02 | 2.4E+02 |

| LNAR | 1.1E+01 | 2.1E+01 | 2.9E+01 | 3.8E+01 | 6.7E+01 | 1.5E+02 | 2.3E+02 | 3.1E+02 | |

| VAR | 1.3E+01 | 2.7E+01 | 4.1E+01 | 5.5E+01 | 6.9E+01 | 1.8E+02 | 3.2E+02 | 4.9E+02 | |

| BigVAR | 4.4E+01 | 6.8E+01 | 8.8E+01 | 1.0E+02 | 5.4E+02 | 7.3E+02 | 8.9E+02 | 1.0E+03 | |

| BigVAR | 4.8E+01 | 7.2E+01 | 9.1E+01 | 1.1E+02 | 5.7E+02 | 7.6E+02 | 9.2E+02 | 1.0E+03 | |

| NAR | 5.9E+00 | 8.8E+00 | 1.1E+01 | 1.3E+01 | 2.9E+01 | 5.7E+01 | 8.5E+01 | 1.1E+02 | |

| NAR | 9.4E+00 | 1.8E+01 | 2.8E+01 | 3.7E+01 | 5.7E+01 | 1.2E+02 | 1.9E+02 | 2.6E+02 | |

| NAR | 1.1E+01 | 2.2E+01 | 3.2E+01 | 4.2E+01 | 7.6E+01 | 1.5E+02 | 2.4E+02 | 3.2E+02 | |

| LNAR | 5.2E+00 | 7.2E+00 | 8.3E+00 | 9.2E+00 | 5.1E+00 | 6.9E+00 | 8.0E+00 | 8.7E+00 | |

| 200 | LNAR | 8.9E+00 | 1.7E+01 | 2.6E+01 | 3.5E+01 | 4.2E+01 | 9.3E+01 | 1.5E+02 | 2.2E+02 |

| LNAR | 1.1E+01 | 2.1E+01 | 3.0E+01 | 4.0E+01 | 6.6E+01 | 1.4E+02 | 2.2E+02 | 3.0E+02 | |

| VAR | 1.3E+01 | 2.6E+01 | 4.0E+01 | 5.3E+01 | 6.2E+01 | 1.5E+02 | 2.7E+02 | 4.1E+02 | |

| BigVAR | 5.2E+01 | 8.1E+01 | 1.0E+02 | 1.2E+02 | 6.9E+02 | 9.3E+02 | 1.1E+03 | 1.2E+03 | |

| BigVAR | 6.0E+01 | 9.0E+01 | 1.1E+02 | 1.3E+02 | 7.5E+02 | 9.8E+02 | 1.2E+03 | 1.3E+03 | |

| NAR | 5.1E+00 | 7.3E+00 | 8.8E+00 | 9.9E+00 | 1.9E+01 | 3.6E+01 | 5.2E+01 | 6.5E+01 | |

| NAR | 9.1E+00 | 1.7E+01 | 2.6E+01 | 3.3E+01 | 4.9E+01 | 1.1E+02 | 1.8E+02 | 2.5E+02 | |

| NAR | 1.1E+01 | 2.0E+01 | 2.9E+01 | 3.8E+01 | 6.5E+01 | 1.4E+02 | 2.2E+02 | 3.0E+02 | |

| LNAR | 5.0E+00 | 7.0E+00 | 8.3E+00 | 9.2E+00 | 5.0E+00 | 6.7E+00 | 7.8E+00 | 8.4E+00 | |

| 500 | LNAR | 9.0E+00 | 1.7E+01 | 2.6E+01 | 3.3E+01 | 3.9E+01 | 9.5E+01 | 1.6E+02 | 2.3E+02 |

| LNAR | 1.1E+01 | 2.0E+01 | 2.9E+01 | 3.7E+01 | 5.7E+01 | 1.3E+02 | 2.1E+02 | 2.9E+02 | |

| VAR | 1.2E+01 | 2.3E+01 | 3.5E+01 | 4.5E+01 | 5.4E+01 | 1.4E+02 | 2.5E+02 | 3.6E+02 | |

| BigVAR | 5.0E+01 | 8.6E+01 | 1.1E+02 | 1.3E+02 | 5.1E+02 | 8.6E+02 | 1.1E+03 | 1.3E+03 | |

| BigVAR | 5.6E+01 | 9.2E+01 | 1.2E+02 | 1.3E+02 | 5.7E+02 | 9.2E+02 | 1.2E+03 | 1.3E+03 | |

| Model | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| NAR | 2.6E+02 | 5.7E+02 | 9.5E+02 | 1.4E+03 | 5.5E+03 | 1.2E+04 | 2.0E+04 | 2.7E+04 | |

| NAR | 4.2E+02 | 9.5E+02 | 1.5E+03 | 2.1E+03 | 9.5E+03 | 2.3E+04 | 3.7E+04 | 5.1E+04 | |

| NAR | 5.7E+02 | 1.2E+03 | 1.8E+03 | 2.5E+03 | 1.4E+04 | 3.0E+04 | 4.6E+04 | 6.1E+04 | |

| LNAR | 5.2E+00 | 7.3E+00 | 8.4E+00 | 9.3E+00 | 5.3E+00 | 7.2E+00 | 8.3E+00 | 9.1E+00 | |

| 100 | LNAR | 2.8E+02 | 7.3E+02 | 1.2E+03 | 1.8E+03 | 6.9E+03 | 1.8E+04 | 3.1E+04 | 4.4E+04 |

| LNAR | 4.8E+02 | 1.1E+03 | 1.7E+03 | 2.4E+03 | 1.2E+04 | 2.8E+04 | 4.3E+04 | 5.9E+04 | |

| VAR | 4.8E+02 | 1.4E+03 | 2.6E+03 | 4.3E+03 | 1.2E+04 | 3.5E+04 | 7.0E+04 | 1.2E+05 | |

| BigVAR | 5.1E+03 | 6.4E+03 | 7.3E+03 | 8.1E+03 | 1.7E+05 | 1.9E+05 | 2.1E+05 | 2.2E+05 | |

| BigVAR | 5.3E+03 | 6.4E+03 | 7.4E+03 | 8.2E+03 | 1.7E+05 | 1.9E+05 | 2.1E+05 | 2.2E+05 | |

| NAR | 3.1E+02 | 6.5E+02 | 9.7E+02 | 1.3E+03 | 6.6E+03 | 1.5E+04 | 2.5E+04 | 3.7E+04 | |

| NAR | 5.0E+02 | 1.1E+03 | 1.7E+03 | 2.3E+03 | 1.1E+04 | 2.5E+04 | 4.0E+04 | 5.8E+04 | |

| NAR | 6.8E+02 | 1.4E+03 | 2.1E+03 | 2.8E+03 | 1.4E+04 | 3.0E+04 | 4.8E+04 | 6.8E+04 | |

| LNAR | 5.1E+00 | 6.9E+00 | 8.0E+00 | 8.5E+00 | 5.2E+00 | 6.9E+00 | 7.9E+00 | 8.7E+00 | |

| 200 | LNAR | 3.0E+02 | 7.3E+02 | 1.3E+03 | 1.9E+03 | 7.3E+03 | 1.8E+04 | 3.1E+04 | 4.5E+04 |

| LNAR | 5.6E+02 | 1.2E+03 | 1.9E+03 | 2.5E+03 | 1.2E+04 | 2.6E+04 | 4.2E+04 | 5.8E+04 | |

| VAR | 4.8E+02 | 1.3E+03 | 2.5E+03 | 3.9E+03 | 1.1E+04 | 3.3E+04 | 6.3E+04 | 1.0E+05 | |

| BigVAR | 7.8E+03 | 9.4E+03 | 1.1E+04 | 1.1E+04 | 2.2E+05 | 2.4E+05 | 2.5E+05 | 2.7E+05 | |

| BigVAR | 8.3E+03 | 9.8E+03 | 1.1E+04 | 1.2E+04 | 2.3E+05 | 2.5E+05 | 2.6E+05 | 2.7E+05 | |

| NAR | 2.6E+02 | 5.7E+02 | 8.1E+02 | 1.0E+03 | 5.6E+03 | 1.4E+04 | 3.2E+04 | 1.1E+05 | |

| NAR | 4.6E+02 | 1.1E+03 | 1.7E+03 | 2.2E+03 | 7.9E+03 | 2.1E+04 | 4.3E+04 | 1.3E+05 | |

| NAR | 5.8E+02 | 1.3E+03 | 1.9E+03 | 2.5E+03 | 1.1E+04 | 2.8E+04 | 5.3E+04 | 1.4E+05 | |

| LNAR | 5.1E+00 | 6.7E+00 | 7.6E+00 | 8.2E+00 | 5.0E+00 | 6.8E+00 | 7.6E+00 | 8.3E+00 | |

| 500 | LNAR | 3.0E+02 | 8.1E+02 | 1.3E+03 | 1.8E+03 | 6.6E+03 | 1.7E+04 | 2.9E+04 | 4.3E+04 |

| LNAR | 4.7E+02 | 1.1E+03 | 1.7E+03 | 2.3E+03 | 1.2E+04 | 2.7E+04 | 4.2E+04 | 5.7E+04 | |

| VAR | 4.3E+02 | 1.2E+03 | 2.2E+03 | 3.2E+03 | 1.0E+04 | 2.9E+04 | 5.3E+04 | 8.4E+04 | |

| BigVAR | 5.6E+03 | 8.1E+03 | 9.8E+03 | 1.1E+04 | 2.0E+05 | 2.5E+05 | 2.7E+05 | 2.8E+05 | |

| BigVAR | 6.2E+03 | 8.6E+03 | 1.0E+04 | 1.1E+04 | 2.1E+05 | 2.4E+05 | 2.7E+05 | 2.8E+05 | |

5 Real Data Example

In this section, we investigate further the example in which the actors are economies, their gross domestic product is the attribute of interest and their trade volume defines the underlying network. To elaborate, we consider the data set of [22]. This data set contains economic data of economies in the time period from 1980-2016. The economies cover more than of world GDP, see Table 6 for a list of included economies. The economies are considered as actors, and the relationship between these actors is given by the IMF (International Monetary Fund) Direction of Trade statistics, see data.imf.org/DOT and also the trade matrix in [22]. For time , the connection from actors to actor given by is defined as the sum of exports and imports between actor and at time divided by the sum of all exports and imports of actor at time . The data set considered contains for each economy attributes such as real GDP (log transform), inflation rate, short/long-term interest rate. Note that these attributes are given quarterly whereas the trade relations are only given annually. We assume here that the trade relations do not change within a year and perform the analysis on the quarterly sampling level. The focus here is on the attribute real GDP, and based on the data from 1980Q1-2014Q4 the goal is to forecast the GDP for the period 2015Q1-2016Q4. The indices denote the time period 1980Q1-2014Q4 and the time period 2015Q1-2016Q4. To perform a forecast, we use the models presented here, namely NAR given by (3) and LNAR given by (11), and include a VAR model as a benchmark. It is a solid benchmark, since Marcellino, [21] compared a VAR model GDP forecast with various nonlinear alternatives and pointed out that even though a VAR model is a “simple” linear model, it can hardly be beaten if it is carefully specified. Let be the real GDP (log transform) of the economies. Unit root tests applied to suggest that real GDP itself may not be stationary. We follow here the economic literature, see among others [21], and model instead the GDP growth rate given by . This transformation can be inverted, and we obtain a forecast for by , where denote forecasts of . The three models considered have a tuning parameter which specifies the lag order. For all three models, the Bayesian Information Criterion (BIC) is used to choose automatically the lag-order . The models NAR and LNAR require a forecast of the underlying network. A simple approach for this is used, namely is used as a forecast. We obtain for a forecast the forecast error . The squared error and the absolute error is used to measure the forecast performance. In Table 5, the sum of all squared and absolute errors is displayed, meaning and . Over all forecast horizons and economies, the additional network structure improves the forecast, and NAR performs best. NAR’s forecast error is for the squared error and for the absolute error smaller than VAR’s forecast error.

| VAR | LNAR | NAR | |

|---|---|---|---|

| Square error | 0.23 | 0.21 | 0.17 |

| Absolute error | 5.21 | 4.87 | 4.39 |

Table 6 breaks the forecast error down into economies, and Table 7 breaks it down into forecast horizons. The performance gap between NAR and LNAR is small for small , and it increases with increasing . Since for LNAR and VAR almost have the same performance and NAR outperforms both, it seems that LNAR performs worse with increasing . Taking a closer look at Table 6, we cannot identify a clear winner. For the listed economies VAR performs independently of the used error measure 11 times best, LNAR 6 times and NAR 16 times.

To sum up, the trade network delivers useful information for the GDP forecast. The models presented in this paper are able to benefit from these additional information such that they can outperform the VAR approach. Note that an NAR model possesses the same amount of parameters as a VAR model. Thus, the additional information can be used without estimating additional parameters.

| Squared error (100) | Absolute error | |||||

|---|---|---|---|---|---|---|

| VAR | LNAR | NAR | VAR | LNAR | NAR | |

| USA | 0.114 | 0.147 | 0.033 | 0.079 | 0.095 | 0.044 |

| UNITED KINGDOM | 0.057 | 0.107 | 0.079 | 0.062 | 0.088 | 0.067 |

| AUSTRIA | 0.133 | 0.211 | 0.404 | 0.096 | 0.124 | 0.165 |

| BELGIUM | 0.094 | 0.097 | 0.085 | 0.079 | 0.077 | 0.077 |

| FRANCE | 0.087 | 0.039 | 0.004 | 0.074 | 0.050 | 0.016 |

| GERMANY | 0.032 | 0.056 | 0.329 | 0.048 | 0.062 | 0.148 |

| ITALY | 0.045 | 0.004 | 0.038 | 0.054 | 0.016 | 0.046 |

| NETHERLANDS | 0.010 | 0.035 | 0.013 | 0.024 | 0.048 | 0.026 |

| NORWAY | 0.701 | 0.508 | 0.155 | 0.217 | 0.179 | 0.096 |

| SWEDEN | 0.185 | 0.250 | 0.134 | 0.106 | 0.127 | 0.090 |

| SWITZERLAND | 0.188 | 0.268 | 0.477 | 0.118 | 0.140 | 0.184 |

| CANADA | 0.401 | 0.449 | 0.146 | 0.168 | 0.179 | 0.104 |

| JAPAN | 0.101 | 0.013 | 0.085 | 0.078 | 0.030 | 0.076 |

| CHINA | 1.099 | 0.905 | 0.321 | 0.257 | 0.235 | 0.131 |

| FINLAND | 0.268 | 0.153 | 0.036 | 0.142 | 0.110 | 0.047 |

| SPAIN | 0.086 | 0.043 | 0.939 | 0.078 | 0.054 | 0.246 |

| TURKEY | 0.326 | 0.450 | 1.330 | 0.123 | 0.182 | 0.248 |

| AUSTRALIA | 0.098 | 0.069 | 0.038 | 0.074 | 0.059 | 0.046 |

| NEW ZEALAND | 0.055 | 0.095 | 0.441 | 0.056 | 0.073 | 0.157 |

| SOUTH AFRICA | 0.711 | 1.063 | 0.059 | 0.210 | 0.254 | 0.064 |

| ARGENTINA | 0.486 | 0.782 | 0.981 | 0.176 | 0.207 | 0.233 |

| BRAZIL | 6.896 | 8.437 | 7.244 | 0.683 | 0.748 | 0.700 |

| CHILE | 0.977 | 1.180 | 0.382 | 0.240 | 0.251 | 0.149 |

| MEXICO | 0.049 | 0.019 | 0.184 | 0.058 | 0.034 | 0.111 |

| PERU | 0.057 | 0.017 | 1.143 | 0.058 | 0.028 | 0.271 |

| SAUDI ARABIA | 0.286 | 0.243 | 0.357 | 0.145 | 0.116 | 0.164 |

| INDIA | 0.060 | 0.093 | 0.085 | 0.064 | 0.079 | 0.074 |

| INDONESIA | 0.006 | 0.059 | 0.037 | 0.020 | 0.061 | 0.048 |

| KOREA | 1.700 | 0.256 | 0.008 | 0.334 | 0.129 | 0.019 |

| MALAYSIA | 0.510 | 0.404 | 0.122 | 0.184 | 0.160 | 0.071 |

| PHILIPPINES | 1.442 | 0.868 | 0.424 | 0.302 | 0.225 | 0.154 |

| SINGAPORE | 4.251 | 2.714 | 0.315 | 0.544 | 0.427 | 0.156 |

| THAILAND | 1.020 | 0.767 | 0.367 | 0.260 | 0.228 | 0.163 |

| Squared error (100) | Absolute error | |||||

| VAR | LNAR | NAR | VAR | LNAR | NAR | |

| 1 | 0.23 | 0.17 | 0.15 | 0.20 | 0.18 | 0.17 |

| 2 | 0.95 | 0.69 | 0.68 | 0.40 | 0.35 | 0.34 |

| 3 | 1.31 | 1.05 | 0.98 | 0.48 | 0.41 | 0.40 |

| 4 | 2.18 | 1.87 | 1.49 | 0.63 | 0.55 | 0.50 |

| 5 | 2.87 | 2.58 | 2.07 | 0.70 | 0.66 | 0.58 |

| 6 | 3.81 | 3.69 | 2.75 | 0.82 | 0.80 | 0.68 |

| 7 | 5.27 | 4.95 | 4.40 | 0.98 | 0.93 | 0.85 |

| 8 | 5.90 | 5.79 | 4.28 | 1.00 | 0.99 | 0.87 |

6 Conclusions

This paper models dynamic attributes of the vertices of a dynamic network. The attributes are modeled such that the underlying network structure can influence the attributes and vice versa. A linear time series framework is adopted and network linear processes and network autoregressive processes were defined. This framework gives flexibility in the sense that the attributes and the underlying network can be modeled separately. The physical dependence framework is used to quantify the dependency structure of the underlying network such that this framework becomes feasible and statistical results can be derived in a low- and high-dimensional setting. These results can be used to do forecasting, and, as can be seen in the numerical examples as well as in the real data example, the benefit of using the additional structure can be quite large.

Acknowledgments. The author is grateful to the editor, an associate editor and one referee for their valuable and insightful comments that led to a considerably improved manuscript. The research of the author was supported by the Research Center (SFB) 884 “Political Economy of Reforms”(Project B6), funded by the German Research Foundation (DFG). Furthermore, the author acknowledges support by the state of Baden-Württemberg through bwHPC.

7 Proofs

Proof of Lemma 2.2.

Under Assumption 1a), we have that implies , where denotes the corresponding quantity of the stacked processes. Thus, for and , we have . The condition for all implies for all , which gives component-wise summability of the sequence , see Appendix A.6 and A.9 in [19]. Under Assumption 1b), we have also by the results of A.9 in [19] that is absolutely component-wise summable.

Proof of Lemma 2.3.

Proof of Theorem 3.1.

Proof of Lemma 3.2.

To simplify notation, let . Since Assumption 1a) gives a causal representation, see Lemma 2.2, we have for component that for some measurable function . Note that and for all . Denote by ∗ a coupled version with being replaced by an i.i.d. copy . Then, . We have by triangular inequality and Cauchy-Schwarz for

Let . Since is -stable, we have that . Note that is a causal process and for all . Furthermore, we have by Assumption 1a)

With this, we have further

Similarly, we obtain Furthermore, let . Since the components are absolutely summable, see Lemma 2.2, we have . This gives us

Hence, the assertion that is -stable follows.

Let . Since is stationary and -stable, we have , where is the indicator function, meaning if is true and zero otherwise. This implies, as , Consequently, for large enough, we have . Suppose in the following that this hold.

A -stable implies that is -stable. To see this, let . Then, and . Since is a causal process, and and are independent for all , we have that and are independent for all and . Hence, the i.i.d. structure of implies that is -stable and centered. This ensures that Theorem 3 in [35] can be applied, see also Proposition 3 in [36]. This gives us that Assumption 2(2.) follows.

Proof of Lemma 3.3.

We have

Suppose is an eigenvector of to eigenvalue . Due to the special structure of we have the following equations and . Following the proof of Theorem 1 in [11] we obtain . We have . Hence, we obtain for an eigenvalue . Since this implies . Furthermore, note that this implies Assumption 1b), which gives stationarity by Lemma 2.2. ∎

Proof of Lemma 3.4.

To simplify notation, let . Similarly as in the proof of Theorem 3.2, we have

Note that for , we have . This gives us . Note that for all . Hence,

due to , , and . Hence,

Since the constants do not depend on , this is finite and is -stable for any .

For , we have for and . Hence, for we have

Note that . Thus, we have for

∎

Proof of Theorem 3.5.

Let and . Furthermore, let and . Note that is a dimensional vector with independently from the dimension . Let further and Then, the linear system (3.1) gives

Hence, . We use the Nagaev inequality for dependent random variables, see Theorem 2 in [18], to bound and . For some process , let

Note that for some vector with , we have . Hence, . Furthermore, we have . Hence, Since and , we have .

We have by Theorem 2 in [18] and the remark thereafter for some vector and some

where are constants depending on only. Similarly, we obtain , , and .

Let . We have Note that . Thus, we have for

Since , we have ∎

References

- Basu and Michailidis, [2015] Basu, S. and Michailidis, G. (2015). Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics, 43(4):1535–1567.

- Bickel et al., [1998] Bickel, P. J., Ritov, Y., Ryden, T., et al. (1998). Asymptotic normality of the maximum-likelihood estimator for general hidden markov models. The Annals of Statistics, 26(4):1614–1635.

- Bradley, [2007] Bradley, R. (2007). Introduction to Strong Mixing Conditions. Kendrick Press, ISBN 0-9740427-9-X.

- Brockwell and Davis, [1991] Brockwell, P. and Davis, R. A. (1991). Time Series: Theory and Methods (2nd edition). Springer, New York.

- Chen et al., [2013] Chen, X., Xu, M., Wu, W. B., et al. (2013). Covariance and precision matrix estimation for high-dimensional time series. The Annals of Statistics, 41(6):2994–3021.

- Dahlhaus et al., [1999] Dahlhaus, R., Neumann, M. H., Von Sachs, R., et al. (1999). Nonlinear wavelet estimation of time-varying autoregressive processes. Bernoulli, 5(5):873–906.

- Doukhan and Louhichi, [1999] Doukhan, P. and Louhichi, S. (1999). A new weak dependence condition and applications to moment inequalities. Stochastic Processes and their Applications, 84(2):313–342.

- Goldsmith-Pinkham and Imbens, [2013] Goldsmith-Pinkham, P. and Imbens, G. W. (2013). Social networks and the identification of peer effects. Journal of Business & Economic Statistics, 31(3):253–264.

- Hanneke et al., [2010] Hanneke, S., Fu, W., Xing, E. P., et al. (2010). Discrete temporal models of social networks. Electronic Journal of Statistics, 4:585–605.

- Hanneke and Xing, [2007] Hanneke, S. and Xing, E. (2007). Discrete temporal models of social networks. Statistical Network Analysis: Models, Issues, and New Directions.

- Knight et al., [2019] Knight, M., Leeming, K., Nason, G., and Nunes, M. (2019). Generalised Network Autoregressive Processes and the GNAR package. Journal of Statistical Software.

- Knight et al., [2016] Knight, M., Nunes, M., and Nason, G. (2016). Modelling, detrending and decorrelation of network time series. arXiv preprint arXiv:1603.03221.

- Kock and Callot, [2015] Kock, A. B. and Callot, L. (2015). Oracle inequalities for high dimensional vector autoregressions. Journal of Econometrics, 186(2):325–344.

- Kolaczyk, [2009] Kolaczyk, E. D. (2009). Statistical Analysis of Network Data: Methods and Models. Springer Publishing Company, Incorporated, 1st edition.

- Krivitsky and Handcock, [2014] Krivitsky, P. N. and Handcock, M. S. (2014). A separable model for dynamic networks. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(1):29–46.

- Krivitsky and Handcock, [2016] Krivitsky, P. N. and Handcock, M. S. (2016). tergm: Fit, Simulate and Diagnose Models for Network Evolution Based on Exponential-Family Random Graph Models. The Statnet Project. R package version 3.4.0.

- Liu and Lin, [2009] Liu, W. and Lin, Z. (2009). Strong approximation for a class of stationary processes. Stochastic Processes and their Applications, 119(1):249–280.

- Liu et al., [2013] Liu, W., Xiao, H., and Wu, W. B. (2013). Probability and moment inequalities under dependence. Statistica sinica, pages 1257–1272.

- Lütkepohl, [2007] Lütkepohl, H. (2007). New Introduction to Multiple Time Series Analysis. Springer Berlin Heidelberg.

- Manski, [1993] Manski, C. F. (1993). Identification of endogenous social effects: The reflection problem. The review of economic studies, 60(3):531–542.

- Marcellino, [2008] Marcellino, M. (2008). A linear benchmark for forecasting GDP growth and inflation? Journal of Forecasting, 27(4):305–340.

- Mohaddes and Raissi, [2018] Mohaddes, K. and Raissi, M. (2018). Compilation, Revision and Updating of the Global VAR (GVAR) Database, 1979Q2-2016Q4. University of Cambridge: Faculty of Economics (mimeo).

- Morris and Kretzschmar, [1997] Morris, M. and Kretzschmar, M. (1997). Concurrent partnerships and the spread of HIV. Aids, 11(5):641–648.

- Nicholls and Quinn, [1981] Nicholls, D. and Quinn, B. (1981). Multiple autoregressive models with random coefficients. Journal of Multivariate Analysis, 11(2):185 – 198.

- Nicholls and Quinn, [1982] Nicholls, D. F. and Quinn, B. G. (1982). Random Coefficient Autoregressive Models: An Introduction, volume 1. Springer Science & Business Media.

- Nicholson et al., [2019] Nicholson, W., Matteson, D., and Bien, J. (2019). BigVAR: Dimension Reduction Methods for Multivariate Time Series. R package version 1.0.4.

- Pourahmadi, [1986] Pourahmadi, M. (1986). On stationarity of the solution of a doubly stochastic model. Journal of Time Series Analysis, 7(2):123–131.

- Pourahmadi, [1988] Pourahmadi, M. (1988). Stationarity of the solution of and analysis of non-gaussian dependent random variables. Journal of Time Series Analysis, 9(3):225–239.

- R Core Team, [2019] R Core Team (2019). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Spedicato, [2017] Spedicato, G. A. (2017). Discrete Time Markov Chains with R. The R Journal. R package version 0.6.9.7.

- Tjøstheim, [1986] Tjøstheim, D. (1986). Some doubly stochastic time series models. Journal of Time Series Analysis, 7(1):51–72.

- Wiesel et al., [2013] Wiesel, A., Bibi, O., and Globerson, A. (2013). Time varying autoregressive moving average models for covariance estimation. IEEE Trans. Signal Processing, 61(11):2791–2801.

- Wu, [2005] Wu, W. B. (2005). Nonlinear system theory: Another look at dependence. Proceedings of the National Academy of Sciences, 102(40):14150–14154.

- Wu, [2006] Wu, W. B. (2006). Unit root testing for functionals of linear processes. Econometric Theory, 22(1):1–14.

- Wu, [2011] Wu, W. B. (2011). Asymptotic theory for stationary processes. Statistics and its Interface, 4(2):207–226.

- Wu et al., [2007] Wu, W. B. et al. (2007). Strong invariance principles for dependent random variables. The Annals of Probability, 35(6):2294–2320.

- Wu and Zhou, [2011] Wu, W. B. and Zhou, Z. (2011). Gaussian approximations for non-stationary multiple time series. Statistica Sinica, pages 1397–1413.

- Xing et al., [2010] Xing, E. P., Fu, W., Song, L., et al. (2010). A state-space mixed membership blockmodel for dynamic network tomography. The Annals of Applied Statistics, 4(2):535–566.

- Xu, [2015] Xu, K. (2015). Stochastic block transition models for dynamic networks. Artificial Intelligence and Statistics, pages 1079–1087.

- Zhang et al., [2017] Zhang, D., Wu, W. B., et al. (2017). Gaussian approximation for high dimensional time series. The Annals of Statistics, 45(5):1895–1919.

- Zhang et al., [2018] Zhang, X., Cheng, G., et al. (2018). Gaussian approximation for high dimensional vector under physical dependence. Bernoulli, 24(4A):2640–2675.

- Zhu et al., [2017] Zhu, X., Pan, R., Li, G., Liu, Y., Wang, H., et al. (2017). Network vector autoregression. The Annals of Statistics, 45(3):1096–1123.