Optimality and Sub-optimality of PCA I: Spiked Random Matrix Models

Abstract

A central problem of random matrix theory is to understand the eigenvalues of spiked random matrix models, introduced by Johnstone, in which a prominent eigenvector (or “spike”) is planted into a random matrix. These distributions form natural statistical models for principal component analysis (PCA) problems throughout the sciences. Baik, Ben Arous and Péché showed that the spiked Wishart ensemble exhibits a sharp phase transition asymptotically: when the spike strength is above a critical threshold, it is possible to detect the presence of a spike based on the top eigenvalue, and below the threshold the top eigenvalue provides no information. Such results form the basis of our understanding of when PCA can detect a low-rank signal in the presence of noise. However, under structural assumptions on the spike, not all information is necessarily contained in the spectrum. We study the statistical limits of tests for the presence of a spike, including non-spectral tests. Our results leverage Le Cam’s notion of contiguity, and include:

i) For the Gaussian Wigner ensemble, we show that PCA achieves the optimal detection threshold for certain natural priors for the spike.

ii) For any non-Gaussian Wigner ensemble, PCA is sub-optimal for detection. However, an efficient variant of PCA achieves the optimal threshold (for natural priors) by pre-transforming the matrix entries.

iii) For the Gaussian Wishart ensemble, the PCA threshold is optimal for positive spikes (for natural priors) but this is not always the case for negative spikes.

keywords:

[class=MSC]keywords:

and and and

faThe first two authors contributed equally. t1This work was supported in part by NSF CAREER Award CCF-1453261 and a grant from the MIT NEC Corporation. t2This research was conducted with Government support under and awarded by DoD, Air Force Office of Scientific Research, National Defense Science and Engineering Graduate (NDSEG) Fellowship, 32 CFR 168a. t3A.S.B. was supported by NSF Grants DMS-1317308, DMS-1712730, and DMS-1719545. Part of this work was done while with the MIT Department of Mathematics. t4This work was supported in part by NSF CAREER Award CCF-1453261, NSF Large CCF-1565235, a David and Lucile Packard Fellowship and an Alfred P. Sloan Fellowship.

1 Introduction

One of the most common ways to analyze a collection of data is to extract top eigenvectors of a sample covariance matrix that represent directions of largest variance, often referred to as principal component analysis (PCA). Starting from the work of Karl Pearson, this technique has been a mainstay in statistics and throughout the sciences for more than a century. For instance, genome-wide association studies construct a correlation matrix of expression levels, whereby PCA is able to identify collections of genes that work together. PCA is also used in economics to extract macroeconomic trends and to predict yields and volatility (Litterman and Scheinkman, 1991; Forni et al., 2000; Stock and Watson, 2002; Egloff, Leippold and Wu, 2010), and in network science to find well-connected communities (McSherry, 2001). More broadly, it underlies much of exploratory data analysis, dimensionality reduction, and visualization.

Classical random matrix theory provides a suite of tools to characterize the behavior of the eigenvalues of various random matrix models in high-dimensional settings. Nevertheless, most of these works can be thought of as focusing on a pure noise model (Anderson, Guionnet and Zeitouni, 2010; Bai and Silverstein, 2010; Tao, 2012) where there is not necessarily any low-rank structure to extract. A direction initiated by Johnstone (2001) has brought this powerful theory closer to statistical questions by introducing spiked models that are of the form “signal + noise.” Such models have yielded fundamental new insights on the behaviors of several methods such as principal component analysis (PCA) (Johnstone and Lu, 2004; Paul, 2007; Nadler, 2008), sparse PCA (Amini and Wainwright, 2008; Vu and Lei, 2012; Berthet and Rigollet, 2013a; Ma, 2013; Shen, Shen and Marron, 2013; Cai, Ma and Wu, 2013; Birnbaum et al., 2013; Deshpande and Montanari, 2014a; Krauthgamer, Nadler and Vilenchik, 2015), and synchronization algorithms (Singer, 2011; Boumal et al., 2014; Bandeira, Boumal and Singer, 2014; Boumal, 2016). More precisely, given a true signal in the form of an -dimensional unit vector called the spike, we can define two natural spiked random matrix ensembles as follows:

-

•

Spiked (Gaussian) Wishart: observe the sample covariance , where is an matrix with columns drawn i.i.d. from , in the high-dimensional setting where the sample count and dimension scale proportionally as . We allow .

-

•

Spiked Wigner: observe , where is an random symmetric matrix with entries drawn i.i.d. (up to symmetry) from a fixed distribution of mean and variance .

We adopt a Bayesian viewpoint, taking the spike to be drawn from an arbitrary but known prior. This enables our approach to address structural assumptions on the spike, such as sparsity or an entrywise constraint to , to model variants of sparse PCA or community detection (Deshpande, Abbe and Montanari, 2016).

The Wishart model describes the sample covariance of high-dimensional data. The Gaussian Wigner distribution arises from the Wishart as a particular small- limit (Johnstone and Onatski, 2015). The spiked Wigner model also describes various inference problems where pairwise measurements are observed between entities; this captures, for instance, Gaussian variants of community detection (Deshpande, Abbe and Montanari, 2016) and synchronization (Javanmard, Montanari and Ricci-Tersenghi, 2016).

We will refer to the parameter or as the signal-to-noise ratio (SNR).

In each of the above models, we study the following statistical questions:

-

•

Detection: For what values of the SNR is it possible to consistently test (with probability as ) between a random matrix drawn from the spiked distribution and one from the unspiked distribution?

-

•

Recovery: For what values of the SNR can an estimator achieve correlation with the true spike that is bounded above zero as ?

We primarily study the detection problem, which has previously been explored in various statistical models (Donoho and Jin, 2004; Cai, Jin and Low, 2007; Sun and Nobel, 2008; Ingster, Tsybakov and Verzelen, 2010; Arias-Castro, Candès and Durand, 2011; Arias-Castro, Candès and Plan, 2011; Arias-Castro, Bubeck and Lugosi, 2012; Butucea and Ingster, 2013; Sun and Nobel, 2013; Arias-Castro and Verzelen, 2014; Verzelen and Arias-Castro, 2015).

The spiked random matrix models above all enjoy a sharp characterization of the performance of PCA through random matrix theory. In the complex Wishart case, the seminal work of Baik, Ben Arous and Péché (2005) showed that when an isolated eigenvalue emerges from the Marchenko–Pastur-distributed bulk. Later Baik and Silverstein (2006) established this result in the real Wishart case. In the Wigner case, the top eigenvalue separates from the semicircular bulk when (Péché, 2006; Féral and Péché, 2007; Capitaine, Donati-Martin and Féral, 2009; Pizzo, Renfrew and Soshnikov, 2013). Each result establishes a sharp spectral threshold at which PCA (top eigenvalue) is able to solve the detection problem for the respective spiked random matrix model. Moreover, it is known that above this threshold, the top eigenvector correlates nontrivially with , while the correlation concentrates about zero below the threshold. Despite detailed research on the spectral properties of spiked random matrix models, much less is known about the more general statistical question: can any hypothesis test consistently detect the presence of a spike below the threshold where PCA succeeds? Our main goal in this paper is to address this question in each of the models above, and as we will see, the answer varies considerably across them. Our results shed new light on how much of the accessible information about is not captured by the top eigenvalue, or even by the full spectrum.

Several recent works have examined this question. Onatski, Moreira and Hallin (2013) study the spiked Wishart model where is an arbitrary unknown unit vector (which, by rotational symmetry, is equivalent to drawing from the uniform prior on the unit sphere). They identify the optimal hypothesis testing power (between spiked and unspiked) and in particular show that there is no test to consistently detect the presence of a spike below the spectral threshold. Even more recent work (Onatski, Moreira and Hallin, 2014; Dobriban, 2016; Ke, 2016) elaborates on this point in other spiked models. In the Gaussian Wigner model it has been established by Montanari, Reichman and Zeitouni (2015) and Johnstone and Onatski (2015) that detection is impossible below the spectral threshold, and the former used techniques similar to those of the present paper, which are not fundamentally limited to spherically symmetric models; indeed, these techniques were applied to sparse PCA by Banks et al. (2017).

In another line of work, several papers have studied recovery in structured spiked random matrix models through approximate message passing (Donoho, Maleki and Montanari, 2009; Bayati and Montanari, 2011; Javanmard and Montanari, 2013), Guerra interpolation (Guerra, 2003), and other tools originating from statistical physics. These results span sparse PCA (Deshpande and Montanari, 2014b; Lesieur, Krzakala and Zdeborová, 2015a), non-negative PCA (Montanari and Richard, 2016), cone-constrained PCA (Deshpande, Montanari and Richard, 2014), and general structured PCA (Rangan and Fletcher, 2012; Lesieur, Krzakala and Zdeborová, 2015b; Deshpande, Abbe and Montanari, 2016; Krzakala, Xu and Zdeborová, 2016; Barbier et al., 2016; Lelarge and Miolane, 2016). Methods based on approximate message passing typically exhibit the same threshold as PCA, but above the threshold they obtain better (and often optimal) estimates of the spike. In many cases, the above techniques give the asymptotic minimum mean square error (MMSE) and, in particular, identify the threshold for nontrivial recovery. However, they do not typically address the detection problem (although we expect the detection and recovery thresholds to match), and they tend to be restricted to i.i.d. priors.

We develop a number of general-purpose tools for proving both upper and lower bounds on detection. We defer the precise statement of our results in each model to their respective sections, but for now we highlight some of our main results:

-

•

In the Gaussian Wigner model, detection is impossible below the spectral threshold () for priors such as the spherical prior111 is uniform on the unit sphere in (Corollary 3.14), the Rademacher prior222 is i.i.d. uniform on (Corollary 3.12), and any sufficiently subgaussian prior (Theorem 3.10). We also study sparse Rademacher priors333 is i.i.d. where each entry is 0 with probability and otherwise uniform on , where we see that the spectral threshold is sometimes optimal and sometimes sub-optimal depending on the sparsity level (Section 3.7).

-

•

In the Wigner model with non-Gaussian noise, the spectral threshold is never optimal (subject to mild conditions): there is an entrywise pre-transformation on the observed matrix that exploits the non-Gaussianity of the noise and strictly improves the performance of PCA (Theorem 4.8). This method was first described by Lesieur, Krzakala and Zdeborová (2015b) and we give a rigorous analysis. Moreover we provide a lower bound (Theorem 4.4) which often matches this upper bound.

-

•

In the Wishart model, the PCA threshold is optimal for the spherical prior, both for positive and negative . For the Rademacher prior, PCA is optimal for all positive ; however, in the less-studied case of negative , an inefficient algorithm succeeds below the spectral threshold when is sufficiently large. This exposes a new statistical phase transition that seems to be previously unexplored. For the sparse Rademacher prior, PCA can be sub-optimal in both the positive and negative regimes, but it is always optimal for sufficiently large positive .

We emphasize that when we say PCA is optimal, we refer only to the threshold for consistent detection. In essentially all cases we consider (except the spherical prior), the top eigenvector has sub-optimal estimation error above the threshold; optimal error is often given by an approximate message passing algorithm such as that of Deshpande, Abbe and Montanari (2016). Furthermore, PCA does not achieve optimal hypothesis testing power below the threshold, and in fact no method based on a finite number of top eigenvalues can be optimal in this sense (Onatski, Moreira and Hallin, 2013, 2014; Johnstone and Onatski, 2015; Dobriban, 2016).

All our lower bounds follow a similar pattern and are based on the notion of contiguity introduced by Le Cam (1960). On a technical level, we show that a particular second moment is bounded which (as is standard in contiguity arguments) implies that the spiked distribution cannot be consistently distinguished (with error as ) from the corresponding unspiked distribution. We develop general tools for controlling the second moment based on subgaussianity and large deviations theory that apply across a range of models and a range of different priors on .

While bounds on the second moment do not a priori imply anything about the recovery problem, it follows from results of Banks et al. (2017) that many of our non-detection results imply the corresponding non-recovery results. The value of the second moment also yields bounds on hypothesis testing power (see Proposition 2.5).

Our work fits into an emerging theme in statistics: we indicate several scenarios when PCA is sub-optimal but the only known tests that beat it are computationally inefficient. Such computational vs. statistical gaps have received considerable recent attention (e.g. Berthet and Rigollet (2013b); Ma and Wu (2015)), often in connection with sparsity. We provide evidence for a new such gap in the negatively-spiked Wishart model with the Rademacher prior, offering an example where sparsity is not present.

Outline

In Section 2 we give preliminaries on contiguity and the second moment method. In Section 3 we study the spiked Gaussian Wigner model, in Section 4 we study the spiked non-Gaussian Wigner model, and in Section 5 we study the spiked Wishart model. Some proofs are deferred to appendices in Acknowledgements (included in this document).

2 Contiguity and the second moment method

Contiguity and related ideas will play a crucial role in this paper. First introduced by Le Cam (1960), contiguity is a central concept in the asymptotic theory of statistical experiments, and has found many applications throughout probability and statistics. Our work builds on a history of using contiguity and related tools such as the small subgraph conditioning method to establish fundamental results about random graphs (e.g. Robinson and Wormald (1994); Janson (1995); Molloy et al. (1997); see Wormald (1999) for a survey) and impossibility results for detecting community structure in the sparse stochastic block model (Mossel, Neeman and Sly, 2015; Banks et al., 2016). Contiguity is formally defined as follows:

Definition 2.1 (Le Cam (1960)).

Let distributions , be defined on the measurable space . We say that the sequence is contiguous to , and write , if for any sequence of events,

Contiguity readily implies that the distributions and cannot be consistently distinguished (given a single sample) in the following sense:

Observation 2.2.

If then there is no hypothesis test of the alternative against the null with .

Note that and are not equivalent, but either of them implies non-distinguishability. Also, showing that two (sequences of) distributions are contiguous does not rule out the existence of a test that distinguishes between them with constant error probability (better than random guessing). In fact, such tests do exist for the spiked Wigner and Wishart models, for instance by thresholding the trace of the matrix; optimal tests are discussed by Onatski, Moreira and Hallin (2013) and Johnstone and Onatski (2015).

Our goal in this paper is to show thresholds below which spiked and unspiked random matrix models are contiguous. We will do this through computing a particular second moment, related to the -divergence as , through a classical form of the second moment method:

Lemma 2.3.

Let and be two sequences of distributions on . If the second moment

exists and remains bounded as , then .

All of the contiguity results in this paper will follow through Lemma 2.3 and its conditional variant below. The roles of and are not symmetric, and we will always take to be the unspiked distribution and take to be the spiked distribution, as the second moment is more tractable to compute in this direction. We include the proof of Lemma 2.3 here for completeness:

Proof.

Let be a sequence of events. Using Cauchy–Schwarz,

The first factor on the right-hand side is bounded; so if then also . ∎

There will be times when the above second moment is unbounded but we are still able to prove contiguity using a modified second moment that conditions away from rare ‘bad’ events that would otherwise dominate the second moment. This idea has appeared previously (Arias-Castro and Verzelen, 2014; Verzelen and Arias-Castro, 2015; Banks et al., 2016, 2017).

Lemma 2.4.

Let be an event that occurs with probability under . Let be the conditional distribution of given . If the modified second moment remains bounded as , then .

Proof.

By Lemma 2.3 we have . As we have . ∎

Moreover, given a value of the second moment, we are able to obtain bounds on the tradeoff between type I and type II error in hypothesis testing, which are valid non-asymptotically:

Proposition 2.5.

Consider a hypothesis test of a simple alternative against a simple null . Let be the probability of type I error, and the probability of type II error. Regardless of the test, we must have

assuming the right-hand side is defined and finite. Furthermore, this bound is tight: for any there exist , and a test for which equality holds.

Proof.

Let be the event that the test selects the alternative , and let be its complement.

where the inequality follows from Cauchy–Schwarz. The following example shows tightness: let and let . On input , the test chooses , and on input , it chooses . ∎

Although contiguity is a statement about non-detection rather than non-recovery, our results also have implications for non-recovery. In general, the detection problem and recovery problem can have different thresholds, but such counterexamples are often unnatural. For a wide class of problems with additive Gaussian noise, the results of Banks et al. (2017) imply that if the second moment from above is bounded then nontrivial recovery is impossible. This result applies to the Gaussian Wigner model and the positively-spiked () Wishart model444For the Wishart case, consider the asymmetric matrix of samples, which can be equivalently written as where and is i.i.d. ., and so our non-detection results immediately imply non-recovery results in those settings.

3 Gaussian Wigner models

3.1 Main results

We define the spiked Gaussian Wigner model:

Definition 3.1.

A spike prior is a family of distributions , where is a distribution over . We require our priors to be normalized so that drawn from has (in probability) as .

Definition 3.2.

For and a spike prior , we define the spiked Gaussian Wigner model as follows. We first draw a spike from the prior . Then we reveal

where is drawn from the (Gaussian orthogonal ensemble), i.e. is a random symmetric matrix with off-diagonal entries , diagonal entries , and all entries independent (except for symmetry ). We denote the unspiked model () by .

It is well known that this model admits the following spectral behavior.

Theorem 3.3 (Féral and Péché (2007); Benaych-Georges and Nadakuditi (2011)).

Let be drawn from with any spike prior supported on unit vectors ().

-

•

If , the top eigenvalue of converges almost surely to as , and the top (unit-norm) eigenvector has trivial correlation with the spike: almost surely.

-

•

If , the top eigenvalue converges almost surely to , and estimates the spike nontrivially: almost surely.

It follows that if in probability then the above convergence holds in probability (instead of almost surely). Thus PCA solves the detection and recovery problems precisely when . In the critical case or near-critical case , there is also a test to consistently distinguish the spiked and unspiked models based on their spectra (Johnstone and Onatski, 2015); see Appendix A for details. Our goal is now to investigate whether detection is possible when .

As a starting point, we compute the second moment of Lemma 2.3:

Proposition 3.4.

Let and let be a spike prior. Let and . Let and be independently drawn from . Then

We defer the proof of this proposition until Section 3.2. For specific choices of the prior , our goal will be to show that if is below some critical , this second moment is bounded as (implying that detection is impossible). We will specifically consider the following types of priors.

Definition 3.5.

Let denote the spherical prior: is a uniformly random unit vector in .

By spherical symmetry, the spherical prior is equivalent to asking for a test that works for any unit-norm spike (i.e. no prior). Without loss of generality, any test for the spherical prior depends only on the spectrum.

Definition 3.6.

If is a distribution on with and , let denote the spike prior that samples each coordinate of independently from .

We will give two general techniques for showing contiguity for various priors. We call the first method the subgaussian method, and it is presented in Section 3.3. The idea is that if the correlation between two independent draws from the prior is sufficiently subgaussian, this implies strong tail bounds on which can be integrated to show that the second moment is bounded. For instance, this gives results in the case of an i.i.d. prior where the entrywise distribution is subgaussian.

In Section 3.6 we present our second method, the conditioning method, which uses the conditional second moment method and can improve upon the subgaussian method is some cases. It only applies to finitely-supported i.i.d. priors and is based on a result from Banks et al. (2016).

For certain natural priors, we are able to show contiguity for all , matching the spectral threshold. In particular, this holds for the spherical prior (Corollary 3.14), the i.i.d. Gaussian prior (Corollary 3.11), the i.i.d. Rademacher prior (Corollary 3.12), and more generally for where is strictly subgaussian (Theorem 3.10).

Not all priors are as well behaved as those above. In Section 3.7 we discuss the sparse Rademacher prior, where we see that the PCA threshold is not always optimal.

3.2 Second moment computation

We begin by computing the second moment where and . First we simplify the likelihood ratio:

Now passing to the second moment:

| where and are drawn independently from . We now simplify the Gaussian moment-generating function over the randomness of , and cancel terms, to arrive at the expression | ||||

which proves Proposition 3.4.

3.3 The subgaussian method

In this section we give a general method for controlling the second moment . We will need the concept of a subgaussian random variable.

Definition 3.7.

A -valued random variable is -subgaussian if and, for all , .

The most general form of the subgaussian method is the following.

Proposition 3.8.

Let be any spike prior. Let and . With and drawn independently from , suppose is -subgaussian for some constant . If then is bounded and so .

Proof.

Using the well-known subgaussian tail bound , we have

which is finite (uniformly in ) provided . ∎

We next show that it is sufficient for the prior itself to be (multivariate) subgaussian.

Proposition 3.9.

Let and . Suppose is -subgaussian. If then .

Proof.

Let . We use the conditional second moment method (Lemma 2.4), taking to be the conditional distribution of given the -probability event . With , the conditional second moment is (by Proposition 3.4)

With and , we have that is -subgaussian because for any ,

Choosing small enough so that , the result now follows from Proposition 3.8. ∎

Specializing to i.i.d. priors, it is sufficient for the distribution of each entry to be subgaussian. In this case we can also compute the limit value of the (conditional) second moment.

Theorem 3.10 (subgaussian method for i.i.d. priors).

Let be a mean-zero unit-variance distribution on and let . Let , , and as in the proof of Proposition 3.9. Suppose is -subgaussian. If then and so .

Proof.

Since is -subgaussian, it follows easily from the definition that is -subgaussian and so contiguity follows from Proposition 3.9. To compute the limit value, by the central limit theorem we have that for , converges in distribution to . The same holds for . By the continuous mapping theorem applied to , we also get convergence in distribution . The convergence in expectation follows since the sequence is uniformly integrable; this is clear from the final step of the proof of Proposition 3.8 (which has no dependence on ). ∎

Since , cannot be -subgaussian with . If is -subgaussian (“strictly subgaussian”) then Theorem 3.10 gives a tight result, matching the spectral threshold. For instance, the standard Gaussian distribution is 1-subgaussian, so we have the following.

Corollary 3.11.

If then .

Note that the i.i.d. Gaussian prior is very similar to the spherical prior; in Section 3.5 we show how to transfer the proof to the spherical prior.

3.4 Application: the Rademacher prior

If is a Rademacher random variable (uniform on ) then is the Rademacher prior, which we abbreviate as . This case of the Gaussian Wigner model has been studied by Deshpande, Abbe and Montanari (2016) and Javanmard, Montanari and Ricci-Tersenghi (2016) as a Gaussian model for community detection and synchronization. The former proves that the spectral threshold is precisely the threshold above which nontrivial recovery of the signal is possible. We further show contiguity below this threshold (which, recall, is not implied by non-recovery).

Corollary 3.12.

If then .

Proof.

The Rademacher distribution is 1-subgaussian by Hoeffding’s lemma, so the proof follows from Theorem 3.10. ∎

Perhaps it is surprising that the spectral threshold is optimal for the Rademacher prior because it suggests that there is no way to exploit the structure. However, PCA is only optimal in terms of the threshold and not in terms of error in recovering the spike once . An efficient estimator that asymptotically minimizes the mean squared error is the approximate message passing algorithm of Deshpande, Abbe and Montanari (2016).

3.5 Comparison of similar priors

We show that two similar priors have the same contiguity threshold, in the following sense.

Proposition 3.13.

Let . Let and be spike priors. Suppose that and can be coupled such that where is a random variable with in probability as . Suppose that for each , the second moment remains bounded as . Then for any , .

Proof.

Let and . Let be the conditional distribution of given the -probability event . Letting and , we have

which is bounded provided we choose small enough so that . The result now follows from the conditional second moment method (Lemma 2.4). ∎

We can now show that the spectral threshold is optimal for the spherical prior (uniform on the unit sphere) by comparison to the i.i.d. Gaussian prior; this result was obtained previously by Montanari, Reichman and Zeitouni (2015); Johnstone and Onatski (2015).

Corollary 3.14.

If then .

Proof.

We have shown that for any , the second moment is bounded for a conditioned version of the i.i.d. Gaussian prior (conditioning on ); see Corollary 3.11. This conditioned Gaussian prior can be coupled to the spherical prior as required by Proposition 3.13, due to Gaussian spherical symmetry. The result follows from Proposition 3.13. ∎

A more direct proof for the spherical prior is possible using known properties of the confluent hypergeometric function; see Appendix C.

Another corollary is that any prior (with in probability) and for any , contiguity holds on the level of spectra; this implies that no test depending only on the eigenvalues can succeed below the threshold, even though other tests can in some cases (e.g. the sparse Rademacher prior of Section 3.7).

Corollary 3.15.

Let be any spike prior (with in probability). Let be the joint distribution of eigenvalues of and let be the joint distribution of eigenvalues of . If then .

Proof.

Due to Gaussian spherical symmetry, the distribution of eigenvalues of the spiked matrix depends only on the norm of the spike and not its direction; thus without loss of generality, is a mixture of spherical priors, over a norm distribution converging in probability to 1. The result now follows from Proposition 3.13 and Corollary 3.14. ∎

3.6 The conditioning method

In this section, we give an alternative to the subgaussian method that can give tighter results in some cases. Here we give an overview, with the full details deferred to Appendix D. Throughout this section we require the prior to be where has finite support.

The main idea is that the second moment takes a particular form involving a multinomial random variable; it turns out that this exact form has been studied by Banks et al. (2016) in the context of contiguity in the stochastic block model. Following their work, we apply the conditional second moment method (Lemma 2.4), conditioning on a high-probability ‘good’ event where the empirical distribution of is close to . Proposition 5 in Banks et al. (2016) provides an exact condition (involving an optimization problem over matrices) for boundedness of the conditional second moment. This method improves upon the subgaussian method in some cases (see e.g. Section 3.7).

Let denote the set of nonnegative vectors with row- and column-sums prescribed by , i.e. treating as an matrix, we have (for all ) that row and column of each sum to . Let denote the KL divergence between two vectors: .

Theorem 3.16 (conditioning method).

Let where has mean zero, unit variance, and finite support with . Let and . Define the matrix for . Identify with the vector of probabilities , and define . Let

If then .

3.7 Application: the sparse Rademacher prior

Now consider the case where where is the sparse Rademacher distribution with sparsity : is 0 with probability , and otherwise uniform on . Here we give a summary of our results, with full details deferred to Appendix E.

We know from Corollary 3.12 that when , detection is impossible below the spectral threshold. However, for sufficiently small (roughly 0.054), an exhaustive search procedure is known to perform detection for some range of values below the spectral threshold (Banks et al., 2017). Towards a matching lower bound, we would like to find as small as possible such that PCA is optimal for all .

Using the subgaussian method (Theorem 3.10) it follows that PCA is optimal for all . The conditioning method (Theorem 3.16) improves this constant substantially, to roughly . Using a more sophisticated method that conditions on an event depending jointly on the signal and noise, Perry, Wein and Bandeira (2016) improve the constant further, to roughly . Similar (but quantitatively weaker) results have been obtained by Banks et al. (2017).

Based on heuristics from statistical physics, Lesieur, Krzakala and Zdeborová (2015b) predicted that the exact value at which PCA becomes sub-optimal is given by the replica-symmetric (RS) formula, which yields . It was later proven rigorously that is the exact threshold for nontrivial recovery below , and that if then detection below is possible (by thresholding the free energy) (Krzakala, Xu and Zdeborová, 2016; Barbier et al., 2016; Lelarge and Miolane, 2016). It remains open to show that detection is impossible below for all . Lesieur, Krzakala and Zdeborová (2015b) also conjecture a computational gap: when , no polynomial-time algorithm can perform detection or recovery (regardless of ).

4 Non-Gaussian Wigner models

4.1 Main results

We first define the spiked non-Gaussian Wigner model.

Definition 4.1.

In the general spiked Wigner model , one observes a matrix

with the spike drawn from a spike prior , and the entries of noise matrix drawn independently up to symmetry, with the off-diagonal entries drawn from a distribution and the diagonal entries drawn from a second distribution . For the sake of normalization, we assume that has mean and variance .

Recall that the prior is required to obey the normalization in probability (see Definition 3.1).

The spectral behavior of this model is well understood555Many of the results cited here assume and show almost-sure convergence of various quantities. Since we assume only in probability, the same convergence is true only in probability (which is enough for our purposes). (see e.g. Féral and Péché (2007); Capitaine, Donati-Martin and Féral (2009); Pizzo, Renfrew and Soshnikov (2013); Benaych-Georges and Nadakuditi (2011)). In fact it exhibits universality (see e.g. Tao and Vu (2012)): regardless of the choice of the noise distributions (with sufficiently many finite moments), many properties of the spectrum behave the same as if were a standard Gaussian distribution. In particular, for , the spectrum bulk has a semicircular distribution and the maximum eigenvalue converges almost surely to . For , an isolated eigenvalue emerges from the bulk with value converging to , and (under suitable assumptions) the top eigenvector has squared correlation with the truth.

In stark contrast we will show that from a statistical standpoint, universality breaks down entirely: the detection problem becomes easier when the noise is non-Gaussian. Let be a spike prior, and suppose that through the second moment method, we can establish contiguity between the Gaussian spiked and unspiked models whenever lies below some critical value

The detection threshold for the non-Gaussian Wigner model depends on as well as a parameter (defined below) that depends on the noise distribution .

Recall that if we take the spike prior to be e.g. spherical or Rademacher, we have , implying that our upper and lower bounds match, and thus our pre-transformed PCA procedure achieves the optimal threshold for any noise distribution (subject to regularity assumptions). For reasons discussed later (see Appendix G), we require to be a continuous distribution with a density function . The parameter , which quantifies its difficulty, is the Fisher information of under translation:

Gaussian noise enjoys an extremal value of this Fisher information, qualifying it as the unique hardest noise distribution (among a large class):

Proposition 4.2 (Pitman (1979) p. 37).

Let be a real distribution with a , non-vanishing density function . Suppose . Then , with equality if and only if is a standard Gaussian.

This is effectively a form of the Cramér–Rao inequality, and can be exploited for a proof of the central limit theorem (Brown, 1982; Barron, 1986).

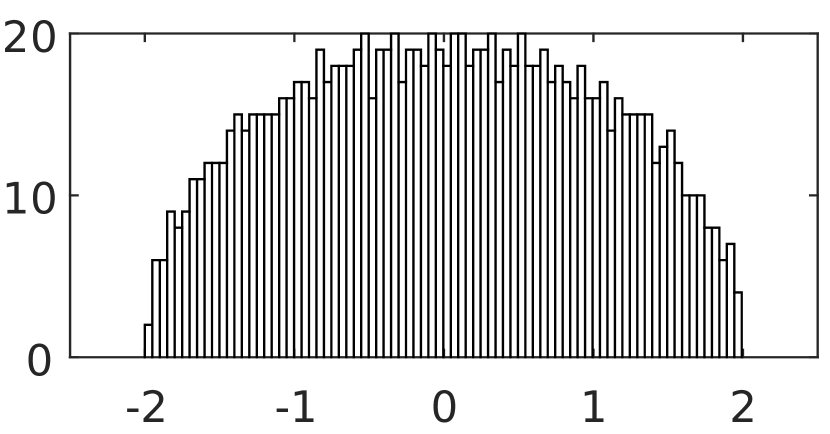

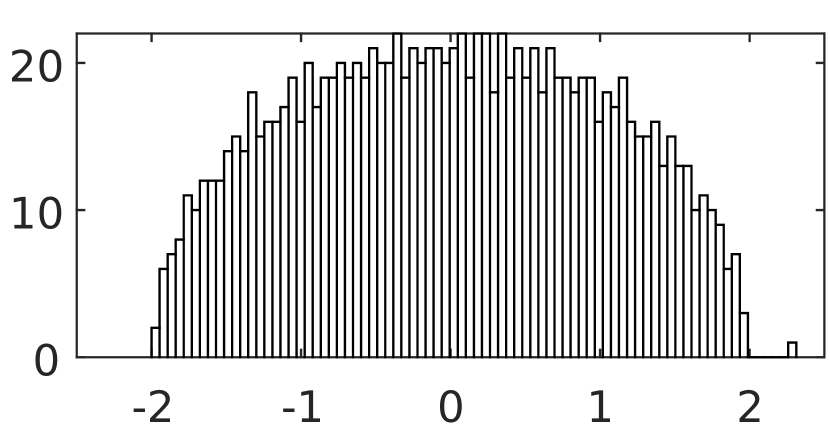

Our upper bound proceeds by a pre-transformed PCA procedure. Define , where is the probability density function of the noise . Given the observed matrix , we apply entrywise to , and examine the largest eigenvalue. This entrywise transformation approximately yields another spiked Wigner model, but with improved signal-to-noise ratio. One can derive the transformation by using calculus of variations to optimize the signal-to-noise ratio of this new spiked Wigner model. This phenomenon is illustrated in Figures 1 and 2:

To intuitively understand why non-Gaussian noise makes the detection problem easier, consider the extreme case where the noise distributions , are uniform on , with mean and variance . Since the noise contribution is entrywise exactly , it is very easy to detect and identify the small signal perturbation , which is entrywise . If there is no spike, all the entries will be (exactly). If there is a spike, each entry will be plus a much smaller offset. One can therefore subtract off the noise and recover the signal exactly. In fact, if we let the noise be a smoothed version of (so that the derivative exists), the entrywise transformation is precisely implementing this noise-subtraction procedure. This justifies the restriction to continuous noise distributions because any distribution with a point mass admits a similar trivial recovery procedure and we will not have contiguity for any ; see Appendix G for details.

The above results on non-Gaussian noise parallel a channel universality phenomenon for mutual information, due to Krzakala, Xu and Zdeborová (2016) (shown for finitely-supported i.i.d. priors). The pre-transformed PCA procedure we use for our upper bound was previously suggested by Lesieur, Krzakala and Zdeborová (2015b) based on linearizing an approximate message passing algorithm, but to our knowledge, no rigorous results have been previously established about its performance in general. Other entrywise pre-transformations have been shown to improve spectral approaches to various structured PCA problems (Deshpande and Montanari, 2014a; Kannan and Vempala, 2016).

4.2 Lower bound

In this section, we state our main statistical lower bound that establishes contiguity in the non-Gaussian Wigner setting. Given a noise distribution , define the translation function

where denotes the translation of distribution by . For instance, the translation function of standard Gaussian noise is .

Assumption 4.3.

-

(i)

The prior satisfies (as usual) in probability, and furthermore is -subgaussian for some constant (see Definition 3.7).

-

(ii)

The prior satisfies high-probability norm bounds: for , there exists a constant for which, with probability over , we have .

-

(iii)

We assume the distributions have non-vanishing density functions , and translation functions that are in a neighborhood of .

Our main lower bound result is the following.

Theorem 4.4.

Under Assumption 4.3, is contiguous to for all .

We defer the proof to Appendix F. In Appendix F we also show that the assumptions on are satisfied for the spherical prior and for reasonable i.i.d. priors; see Propositions 4.5 and 4.6 below. The assumptions on are satisfied by any mixture of Gaussians of positive variance, for example.

Proposition 4.5.

Conditions (i) and (ii) in Assumption 4.3 are satisfied for the spherical prior .

Proposition 4.6.

Consider an i.i.d. prior where is zero-mean, unit-variance, and subgaussian with some constant . Then conditions (i) and (ii) in Assumption 4.3 are satisfied.

4.3 Pre-transformed PCA

In this section we analyze a pre-transformed PCA procedure for the non-Gaussian spiked Wigner model. We need the following regularity assumptions.

Assumption 4.7.

Of the prior we require (as usual) in probability, and we also assume that with probability , all entries of are small: for some fixed . Of the noise , we assume the following:

-

(iv)

has a non-vanishing density function ,

-

(v)

Letting , we have that and its first two derivatives are polynomially-bounded: there exists and an even integer such that for all .

-

(vi)

With as in (ii), has finite moments up to : for all .

The main theorem of this section is the following.

Theorem 4.8.

Let and let satisfy Assumption 4.7. Let where is drawn from . Let denote entrywise application of the function to , except we define the diagonal entries of to be zero.

-

•

If then as .

-

•

If then as and furthermore the top (unit-norm) eigenvector of correlates with the spike: with probability .

Convergence is in probability. Here denotes the maximum eigenvalue.

The proof is deferred to Appendix H, but the main idea is that the entrywise transformation approximately produces another spiked (non-Gaussian) Wigner matrix with a different signal-to-noise ratio , and we can choose to optimize this.

We have set the diagonal entries to zero for convenience, but this is not essential: so long as we define the diagonals of so that the largest (in absolute value) diagonal entry is , the diagonal entries can only change the spectral norm of by and so the result still holds.

5 Spiked Wishart models

5.1 Main results

We first formally define the spiked Wishart model:

Definition 5.1.

Let and . Let be a spike prior. The spiked (Gaussian) Wishart model on matrices is defined as follows: we first draw a hidden spike , and then reveal , where is an matrix whose columns are sampled independently from ; the parameters and scale proportionally with as . If and (so that the covariance matrix is not positive semidefinite), output a failure event .

Recall that spike priors are required to satisfy in probability (Definition 3.1). Our contiguity results will apply even to the case when the sample matrix is revealed.

The spiked Wishart model admits the following spectral behavior. In this high-dimensional setting, the spectrum bulk of converges to the Marchenko–Pastur distribution with shape parameter . By results of Baik, Ben Arous and Péché (2005) and Baik and Silverstein (2006), it is known that the top eigenvalue consistently distinguishes the spiked and unspiked models when . In fact, matching lower bounds are known in the absence of a prior (equivalently, for the spherical prior) due to Onatski, Moreira and Hallin (2013): for , no hypothesis test distinguishes this spiked model from the unspiked model with error. In the case of , a corresponding PCA threshold exists: the minimum eigenvalue exits the bulk when (Baik and Silverstein, 2006), but we are not aware of lower bounds in the literature. The case of is of course invalid, as the covariance matrix must be positive semidefinite. As in the Wigner model, consistent detection is possible in the critical case , at least when ; see Appendix A.

Our goal in this section will be to give lower and upper bounds on the statistical threshold for (as a function of ) for various priors on the spike. We begin with a crude lower bound that allows us to transfer any lower bound for the Gaussian Wigner model into a lower bound for the Wishart model. Recall that denotes the threshold for boundedness of the Gaussian Wigner second moment:

| (1) |

Proposition 5.2.

Let be a spike prior. If then is contiguous to .

The proof can be found in Section 5.5.2. A consequence of the above is that if , so that the spectral method is optimal in the Wigner setting, it follows that the ratio between the above Wishart lower bound () and the spectral upper bound () tends to as . This reflects the fact that the Wigner model is a particular limit of the Wishart model (Johnstone and Onatski, 2015). For , we will later give an even stronger implication from Wigner to Wishart lower bounds (Corollary 5.9).

Although Proposition 5.2 is a strong bound for small , it is rather weak for large (and in particular does not cover the case ). In Section 5.3 we will remedy this by giving a much tighter lower bound (Theorem 5.7) which depends on the rate function of the large deviations of the prior. The proof involves an application of the conditional second moment method whereby we condition away from certain ‘bad’ events depending on interactions between the signal and noise (similarly to Perry, Wein and Bandeira (2016)). One consequence (Corollary 5.9) of our lower bound roughly states that if detection is impossible below the spectral threshold () in the Wigner model, then it is also impossible below the spectral threshold () in the Wishart model for all positive . (This is not true for negative .)

We complement our lower bounds with the following upper bound.

Theorem 5.3.

Let . Let be a spike prior supported on at most points, for some fixed . If

then there is a (inefficient) test that consistently distinguishes between the spiked Wishart model and the unspiked model .

The test that gives this upper bound is based on the maximum likelihood estimator (MLE), computed by exhaustive search over all possible spikes. The proof, which can be found in Appendix I, is a simple application of the Chernoff bound and the union bound. For some priors (such as i.i.d. sparse Rademacher) we can get the most mileage out of this theorem by first conditioning on a -probability event (e.g. has a typical number of nonzeros) in order to decrease the value of .

We will typically not consider the boundary case . Note, however, that if and the prior is finitely-supported (for each ), with almost surely, then detection is possible for any : in the spiked model, the spike is orthogonal to all of the samples; but in the unspiked model, with probability 1 there will not exist a vector in the support of the prior that is orthogonal to all of the samples.

We now summarize the implications of our lower and upper bounds for some specific priors.

-

•

Spherical: For the spherical prior ( is drawn uniformly from the unit sphere), it was known previously that the PCA threshold is optimal for all positive (Onatski, Moreira and Hallin, 2013). We show that the PCA threshold is also optimal for all .

-

•

Rademacher: For the Rademacher prior , we show that the PCA threshold is optimal for all . However, when is negative and sufficiently close to , the MLE of Theorem 5.3 succeeds below the PCA threshold.

-

•

Sparse Rademacher (defined in Section 3.7): If the sparsity is sufficiently small, the MLE beats PCA in both the positive- and negative- regimes. However, for any fixed , if is sufficiently large (and positive) then the PCA threshold is optimal.

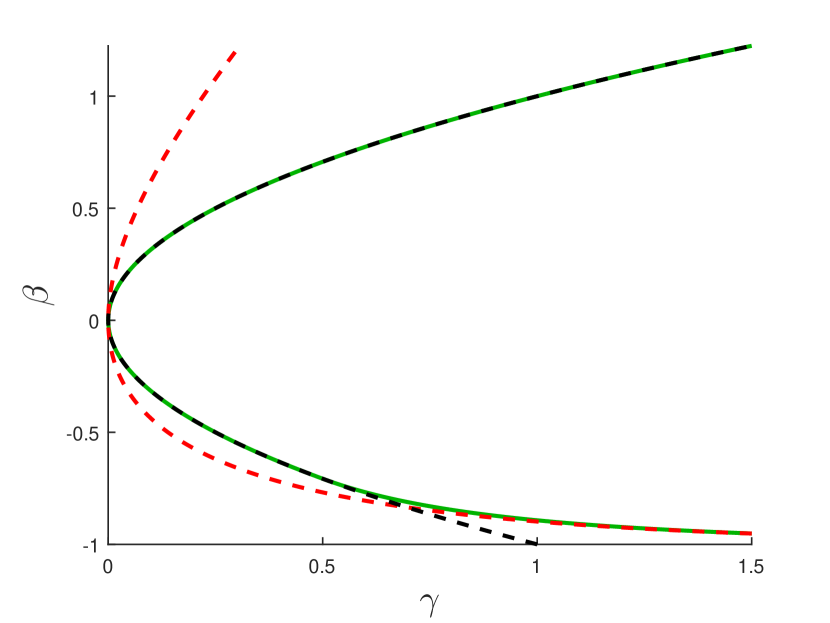

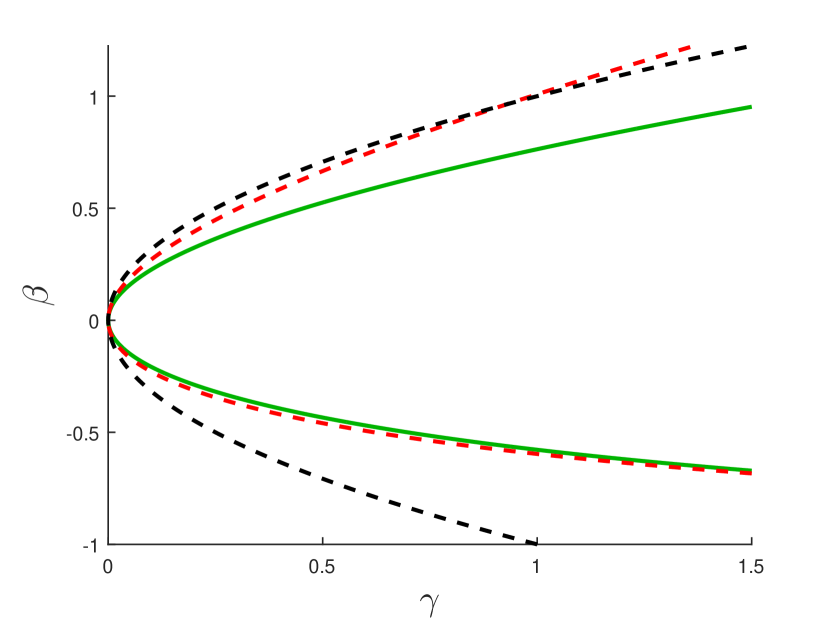

See Appendix N for details on the above results, including how they follow from our general upper and lower bounds (Theorems 5.3 and 5.7). Figure 3 depicts our upper and lower bounds for the Rademacher and sparse Rademacher priors.

As in the Wigner model, our methods often yield the limit value of the (conditional) second moment and thus imply asymptotic bounds on hypothesis testing power via Proposition 2.5; see Appendix B for details.

5.2 Rate functions

Our main lower bound will depend on the prior through tail probabilities of the correlation of two spikes drawn independently from the prior . These tail probabilities are encapsulated by the rate function of the large deviations of , which is intuitively defined by . Formally we define as follows.

Definition 5.4.

Let be a spike prior. For drawn independently from and , let

Suppose we have for some sequence of functions that converges uniformly on to as . Then we call such the rate function of the prior .

Without loss of generality, and is non-decreasing. Note that a tail bound of the form is sufficient to establish that is a rate function.

We now state the rate functions for some priors of interest. It is proven by Perry, Wein and Bandeira (2016) that these indeed satisfy the definition of rate function.

Proposition 5.5 (Perry, Wein and Bandeira (2016)).

We have the following rate functions for the spherical, Rademacher, and sparse Rademacher priors.

-

•

Spherical: .

-

•

Rademacher: .

-

•

Sparse Rademacher666This is for a variant of the sparse Rademacher prior where the sparsity is exactly . See Appendix N for details on how this extends to our variant. with sparsity :

where

Here is the binary entropy, and .

Note that rate functions for general i.i.d. priors can be easily derived from large deviations theory (Cramér’s theorem) since is the sum of i.i.d. random variables; this is how the Rademacher rate function is derived. However, to obtain stronger results in some cases, one may use a variant of the prior that conditions on typical outcomes (similarly to our conditioning method for the Wigner model (Section 3.6) or Appendix A of Banks et al. (2016)); this is how the sparse Rademacher rate function is derived.

We will need the following strengthening of the notion of rate function.

Definition 5.6.

We say that a rate function for a prior admits a local Chernoff bound if there exists and such that for any ,

where and are drawn independently from .

5.3 Main lower bound result

We are now ready to state our main lower bound result. Recall that denotes the Wigner threshold (1).

Theorem 5.7.

Let be a spike prior with rate function . Let and . Suppose that either

-

(i)

, or

-

(ii)

admits a local Chernoff bound (Definition 5.6).

If

| (2) |

where

then is contiguous to for all .

We expect condition (ii) to hold for all reasonable priors; condition (i) yields a weaker result in some cases but is sometimes more convenient. Some basic properties of (2) are discussed in Appendix J. In Appendix M we establish the following monotonicity:

Proposition 5.8.

Let be a spike prior. Fix and . If (2) holds for and then it also holds for any and .

In particular, if (so that , corresponding to the spectral threshold) we have that if Theorem 5.7 shows that the PCA threshold is optimal for some , then the PCA threshold is also optimal for all .

The following connection to the Wigner model is also proved in Appendix M, corresponding to the limit of the monotonicity property above:

Corollary 5.9.

Suppose is -subgaussian (Definition 3.7), where and are drawn independently from . Then for any and any we have .

Recall that the subgaussian condition above implies a Wigner lower bound for all (Proposition 3.8). This means whenever Proposition 3.8 implies that the PCA threshold is optimal for the Wigner model, we also have that the PCA threshold is optimal for the Wishart model for any positive . Conversely, if Theorem 5.7 shows that PCA is optimal for all then it is also optimal for the Wigner model (see Proposition M.2). In light of the above monotonicity (Proposition 5.8), these results makes sense because the Wigner model corresponds to the limit of the Wishart model (Johnstone and Onatski, 2015).

We also show (in Appendix M) that for a wide range of priors, the PCA threshold becomes optimal for sufficiently large :

Proposition 5.10.

Suppose where is a mean-zero unit-variance distribution for which (product of two independent copies of ) has a moment-generating function which is finite on an open interval containing zero. Then there exists such that for any and any we have .

5.4 Lower bound proof summary

The full proof of Theorem 5.7 will be completed in the next section, but we now describe the proof outline and give some preliminary results. We approach contiguity for the spiked Wishart model through the second moment method outlined in Section 2. Note that detection can only become easier when given the original sample matrix (instead of ), so we establish the stronger statement that the spiked distribution on is contiguous to the unspiked distribution. We first simplify the second moment in high generality.

Proposition 5.11.

For any there exists such that the following holds. Let be a spike prior supported on vectors with . In distribution , let a hidden spike be drawn from , and let independent samples , , be revealed from the normal distribution . In distribution , let independent samples , , be revealed from . Then we have

This result has appeared in higher generality (Cai, Ma and Wu, 2015); for completeness we give the proof in Section 5.5.1. The condition will not be an issue because we can always consider a modified prior that conditions on this -probability event (see Lemma 2.4). Note that the above second moment has the curious property of symmetry under replacing with . In contrast, the original Wishart model does not, since for instance is allowed while is not. As a result, the second moment method gives good results for negative but substantially sub-optimal results for positive . To remedy this, we will apply the conditional second moment method (Lemma 2.4), conditioning on an event that depends jointly on the signal and noise (we previously only conditioned on the signal).

The proof of Theorem 5.7 has two parts. In Section 5.5.2 we control the small deviations of the second moment, i.e. the contribution from values at most some small . Here we use either the Wigner lower bound (i) or the local Chernoff bound (ii) (combined with (2)), whichever is provided. This step uses the basic second moment of Proposition 5.11 without conditioning. In Section 5.6 we complete the proof by controlling the remaining large deviations of the conditional second moment. Here we use the condition (2) on the rate function of the prior.

5.5 Proof of lower bound

This section is devoted to proving Theorem 5.7. Along the way we will also prove Propositions 5.11 and 5.2.

5.5.1 Second moment computation: proof of Proposition 5.11

We first compute:

| Note that has eigenvalue on and eigenvalue on the orthogonal complement of . Thus , and we have: | ||||

Passing to the second moment, we compute:

| Over the randomness of , we have , so that the inner expectation can be simplified using the moment-generating function (MGF) of the distribution: | ||||

as desired. Here the MGF step requires

| (3) |

Provided that and are sufficiently close to 1, this is true so long as either (as assumed by Proposition 5.11) or is sufficiently small (as in the small deviations of the next section).

5.5.2 Small deviations and proof of Proposition 5.2

We now show how to bound the small deviations

of the Wishart second moment in terms of the Wigner second moment. (Assume are sufficiently close to 1 and is a sufficiently small constant so that (3) holds). Letting so that , we have

using the convexity of . Note that this resembles the Wigner second moment and so (by definition of ) it is bounded as so long as

| (4) |

Proposition 5.2 now follows by setting for small and conditioning the prior on . (See Section 3.5 for similar arguments; note that the conditioning can only increase the Wigner second moment by a factor.) Furthermore, using the bound we have the following fact that will be used in the proof of Theorem 5.7.

Lemma 5.12.

If then there exists such that is bounded as .

Note that is precisely condition (i) in the statement of Theorem 5.7. If instead condition (ii) holds, we can control the small deviations using the following lemma, deferred to Appendix K:

Lemma 5.13.

If (2) holds and admits a local Chernoff bound, then there exists such that is bounded as .

5.6 Proof of Theorem 5.7

We now prove our main lower bound result using the conditional second moment method. Define and as in Proposition 5.11. For a vector and an matrix , define the ‘good’ event by

where . Note that under (where is the spike and is the Wishart matrix: where the columns of are the samples ), and so occurs with probability . Let be the conditional distribution of given .

For simplicity we now specialize to the case where is supported on unit vectors ; see Appendix L for the general case. Similarly to the proof of Proposition 5.11, we compute the conditional second moment as follows.

and so where

| (5) |

where are defined by and . We will see below that is indeed only a function of .

5.6.1 Interval

Let . Let be a small constant (not depending on ), to be chosen later. First let us focus on the contribution from , i.e. we want to bound

For and with fixed unit vectors, the matrix

follows the Wishart distribution with degrees of freedom and shape matrix

By integrating over and using the PDF of the Wishart distribution, we have

where the integration is over the domain , , and , and denotes the multivariate gamma function.

Using and applying Stirling’s approximation to , we have for ,

where the is uniform in . Letting and solving explicitly for the optimal ,

and has the same sign as .

We now show how to bound the contribution to from positive ; the proof for negative is similar. We have

| Since is strictly increasing on (see Appendix J), we can apply the change of variables to obtain | ||||

5.6.2 Interval

This case needs special consideration because both sides of (2) approach 0 as and so the last step above requires to be bounded away from 0. Since (up to a factor of ) conditioning on only decreases the second moment (for each value of ), we can revert back to the basic second moment: the contribution is bounded by the small deviations from Section 5.5.2. It therefore follows from either Lemma 5.12 or Lemma 5.13 that provided is small enough, is bounded as .

5.6.3 Interval

This case needs special consideration because in the calculations for the interval, certain terms in the exponent blow up at which prevents us from replacing by an error term that is uniformly in . To deal with this case we will bound by its worst-case value .

To see that is the worst case, notice from (5) that up to an factor (which will turn out to be negligible), is proportional to . Since and each follow at distribution (with correlation that increases with ), this probability is maximized when they are perfectly correlated at .

We now proceed to bound . Let , and let be fixed unit vectors with . We have that follows a distribution, with . Similarly to the computation for we obtain

and

Plugging in the rate function, is provided that . This follows from (2) (near ) provided is small enough (since is an increasing function of ).

Acknowledgements

The authors are indebted to Philippe Rigollet for helpful discussions and for many comments on a draft. We thank the anonymous reviewers for many helpful, detailed comments.

Supplement A \stitleOptimality and Sub-optimality of PCA in Spiked Random Matrix Models: Supplementary Proofs \sdescriptionIncluded below as appendices. Contains proofs omitted from this paper for the sake of length.

Appendix A Behavior near criticality

In Gaussian Wigner settings where we have established contiguity for all , it is natural to ask whether the spiked and unspiked models remain contiguous for a sequence with (here may be positive or negative). However, this is never the case; it is possible to consistently distinguish the models in this critical case. By adding additional GOE noise, we can reduce to the case for arbitrary fixed (perhaps taking a tail of the sequence). It is known (Johnstone and Onatski, 2015) that (regardless of the spike prior) the hypothesis testing error (sum of type I and type II errors) in this case tends to as ; thus the minimum hypothesis testing error in the original problem cannot be bounded away from zero.

A similar result for the positively-spiked () Wishart model follows from Onatski, Moreira and Hallin (2013): if is fixed and with then it is possible to consistently distinguish the spiked and unspiked models. (We expect the analogous result to hold for but to the best our knowledge this has not been proven.)

Appendix B Bounds on hypothesis testing

For both the Gaussian Wigner and Wishart models, for the spherical prior (or equivalently, limited to spectral-based tests) the optimal tradeoff curve (power envelope) between type I and type II error is known exactly in the limit (Onatski, Moreira and Hallin, 2013; Johnstone and Onatski, 2015). For other priors, one can apply the optimal spectral-based test from above to obtain an upper bound; however, better tests (which do not depend only on the spectrum) may be possible.

In many cases we can use Proposition 2.5 to obtain lower bounds (which do not match the upper bound above). First note that Proposition 2.5 is still valid (in the limit) in cases when we have used the conditional second moment. (This is because if is obtained from by conditioning on a -probability event, asymptotic hypothesis testing bounds for against imply the same bounds for against .)

For the Gaussian Wigner model, Theorem 3.10 (subgaussian method for i.i.d. priors) and Theorem D.2 (conditioning method) both give the limit value (as ) of the (conditional) second moment, and in fact the value is in both of these cases. Therefore, any time we have used one of those two methods, we obtain asymptotic hypothesis testing bounds from Proposition 2.5. This applies to, for instance, the i.i.d. Gaussian, Rademacher, and sparse Rademacher priors. The same bounds also hold for the spherical prior (although the exact asymptotic power envelope is known in this case) because the comparison method of Proposition 3.13 preserves the value of the second moment.

For the Wishart model, suppose we have a prior for which we know the Wigner second moment has limit value (as above). Furthermore, suppose we have a Wishart lower bound for this prior via Theorem 5.7, using the Wigner second moment to control the small deviations (i.e. condition (i) of Theorem 5.7 holds). From the proof of Theorem 5.7, the limit value of the Wishart (conditional) second moment is determined by the small deviations of Section 5.5.2; the remaining large deviations contribute . We see from Section 5.5.2 that the asymptotic value of the small deviations is bounded by the value of the Wigner second moment with as . Therefore the limsup of the Wishart (conditional) second moment is at most , which yields hypothesis testing bounds via Proposition 2.5.

Appendix C Alternative proof for spherically-spiked Wigner

Here we give an alternative proof of Corollary 3.14. The proof deals with the second moment directly rather than comparing to the i.i.d. Gaussian prior.

Corollary 3.14.

Consider the spherical prior . If then is contiguous to .

Proof.

By symmetry, we reduce the second moment to

where denotes the first standard basis vector. Note that the first coordinate of a point uniformly drawn from the unit sphere in is distributed proportionally to , so that its square is distributed proportionally to . Hence is distributed as . The second moment is thus the moment generating function of evaluated at , and as such, we have

| (6) |

where denotes the confluent hypergeometric function.

Suppose . Equation 13.8.4 from [NIST Digital Library of Mathematical Functions ] grants us that, as ,

| where and is the parabolic cylinder function, | ||||

| by Equation 12.9.1 from [NIST Digital Library of Mathematical Functions ], | ||||

which is bounded as , for all . The result follows from Lemma 2.3. ∎

Appendix D Conditioning method for Gaussian Wigner model

In this section we give the full details of the conditioning method for the Gaussian Wigner model. We assume that the prior is where is a finitely-supported distribution on with mean zero and variance one.

The argument that we will use is based on Banks et al. (2016), in particular their Proposition 5. Suppose is a set of ‘good’ values so that with probability . Let and let . Let be the conditional distribution of given . Let . Our goal is to show , from which it follows that (see Lemma 2.4). If we let be the event that and are both in , our second moment becomes

Let (a finite set) be the support of , and let . We will index by and identify with the vector of probabilities . For , let denote the number of indices for which and (recall is drawn from ). Note that follows a multinomial distribution with trials, outcomes, and with probabilities given by . We have

where is the matrix , and the quadratic form is computed by treating as a vector of length .

We are now in a position to apply Proposition 5 from Banks et al. (2016). Define . Let be the event defined in Appendix A of Banks et al. (2016), which enforces that the empirical distributions of and are close to ; namely,

where (for concreteness) .

Note that (treated as a vector of length ) is in the kernel of because is mean-zero: the inner product between and the row of is

Therefore we have and so we can write our second moment as .

Let denote the set of nonnegative vectors with row- and column-sums prescribed by , i.e. treating as an matrix, we have (for all ) that row and column of each sum to . Let denote the KL divergence between two vectors: . For convenience, we restate Proposition 5 in Banks et al. (2016).

Proposition D.1 (Banks et al. (2016), Proposition 5).

Let be any vector of probabilities. Let be any matrix. Define , , , and as above (depending on ). Let

If then , where . If then .

We apply Proposition D.1 to our specific choice of and :

Theorem D.2 (conditioning method).

Let where has mean zero, unit variance, and finite support with . Let , , and . Define the matrix for . Let

If then and so . Conversely, if then

Note that this is a tight characterization of when the conditional second moment is bounded, but not necessarily of when contiguity holds.

The intuition behind this matrix optimization problem is the following. The matrix represents the ‘type’ of a pair of spikes in the sense that for any , is the fraction of entries for which and . A pair of type contributes the value to the second moment . The probability (when ) that a particular type occurs is asymptotically . Due to the exponential scaling, the second moment is dominated by the worst value: the second moment is unbounded if there is some such that . (This idea is often referred to as Laplace’s method or the saddle point method.) Rearranging this yields the optimization problem in the theorem. The fact that we are conditioning on ‘good’ values of (that have close-to-typical proportions of entries) allows us to add the constraint . If we were not conditioning, we would have the same optimization problem over (the simplex of dimension ), which in some cases gives a worse threshold.

Unfortunately we do not have a good general technique to understand the value of the matrix optimization problem. However, in certain special cases we do. Namely, in Appendix E we show, for the sparse Rademacher prior, how to use symmetry to reduce the problem to only two variables so that it can be easily solved numerically. In other applications, closed form solutions to related optimization problems have been found (Achlioptas and Naor, 2004; Banks et al., 2016).

Above we have computed the limit value of the second moment in the case as follows. Defining as in Proposition D.1 we have where

since is mean-zero and unit-variance, and so

Appendix E Sparse Rademacher prior

In this section we give details for our results on the spiked Gaussian Wigner model with the i.i.d. sparse Rademacher prior: where where is the sparse Rademacher distribution with sparsity :

First we apply the subgaussian method (Theorem 3.10). The subgaussian constant for needs to satisfy

| (7) |

for all so the best (smallest) choice for is

Recall that Theorem 3.10 (subgaussian method) gives contiguity for all . We now show that for sufficiently large , we have , implying that PCA is tight:

Proposition E.1.

When , we have , yielding contiguity for all . On the other hand, if , then .

Proof.

We equivalently consider the following reformulation of (7):

| (8) |

Both sides of the inequality are even functions of , agreeing in value at . When , the inequality fails, by comparing their second-order behavior about . When but , the inequality fails, as the two sides have matching behavior up to third order, but .

It remains to show that the inequality (8) does hold for and . As the left and right sides agree to first order at , and are both even functions, it suffices to show that for all ,

Completing the square for , we have the equivalent inequality:

Note that is bounded below by ; thus for , the underbraced term () is nonnegative, and hence minimized in absolute value when . It then suffices to show the above inequality in the case , so that ; but here the inequality is an equality, by simple algebra. ∎

Using the conditioning method of Section 3.6, we will now improve the range of for which PCA is optimal, although our argument here relies on numerical optimization.

Example E.2.

Let be the sparse Rademacher prior . There exists a critical value (numerically computed) such that if and then is contiguous to . When we are only able to show contiguity when for some .

Details.

Consider the optimization problem of Theorem 3.16 (conditioning method). We will first use symmetry to argue that the optimal must take a simple form. Abbreviate the support of as . For a given matrix, define its complement by swapping and , e.g. swap with and swap with . Note that if we average with its complement, the numerator remains unchanged, the denominator can only decrease, and the row- and column-sum constraints remain satisfied; this means the new solution is at least as good as the original . Therefore we only need to consider values satisfying and . Note that the remaining entries of are uniquely determined by the row- and column-sum constraints, and so we have reduced the problem to only two variables. It is now easy to solve the optimization problem numerically, say by grid search. ∎

Appendix F Proof of non-Gaussian Wigner lower bound

In this section we prove Theorem 4.4, and verify its hypotheses for spherical and i.i.d. priors.

Proof.

We begin by conditioning the prior on the high-probability events that for , and on the event that no entry of exceeds , which is true with high probability by the subgaussian hypothesis; let be this conditioned prior. Hence if is contiguous to then so is . Let , , and .

For convenience, let denote if and if , the density of the noise on the entry. Likewise let denote or as appropriate. We proceed from the second moment:

We will expand and using Taylor’s theorem, using the assumption:

for some remainder function tending to as . As and are entrywise , these remainder terms are as . Note that , so that the non-mixed partials of vanish, and likewise for . We note also that , the Fisher information defined above. Thus,

We can separate these four terms using a weighted AM–GM inequality. For all :

| (9) | ||||

| (10) | ||||

| (11) | ||||

| (12) |

By hypothesis, , implying that we can choose such that . But is dominated as a measure by ; it follows that , and the first term (9) is bounded.

We bound the second term (10) using the subgaussian assumption:

where . We thus have

By subgaussian hypothesis on , the inner expectation over is , so that the overall term (10) is bounded.

We bound the third term (11) using Cauchy–Schwarz:

due to the norm restrictions on prior . This evidently remains bounded as .

The fourth term proceeds similarly:

which likewise remains bounded.

With the overall second moment bounded as , the result follows from Lemma 2.4. ∎

Proof.

Note that one can sample by first sampling and then taking . By Chebyshev, with probability . For , has expectation and variance

Supposing that , which occurs with probability , we have for any that

by Chebyshev. This probability is so long as we take .

The spherical prior is appropriately subgaussian: the inner product is distributed as with , which is known to be -subgaussian (see e.g. Elder (2016)). ∎

Proposition 4.6.

Consider an i.i.d. prior where is zero-mean, unit-variance, and subgaussian with some constant . Then conditions (i) and (ii) in Assumption 4.3 are satisfied.

Proof.

We have where are independent copies of . For ,

| Choose so that , and apply Chebyshev’s inequality: | ||||

Here we needed (which follows from subgaussianity) so that . ∎

Appendix G Non-Gaussian Wigner with discrete noise

In this section we show that in the non-Gaussian Wigner model, if the noise distribution has a point mass then the detection problem becomes easy for any .

Theorem G.1.

Let be a (mean-zero, unit-variance) distribution on with a point mass: for some and some . Let be any distribution on . Let be a spike prior such that for some and , with probability , satisfies both (i) and (ii) . Then for any , there exists a test that consistently distinguishes from .

Here, denotes the norm, i.e. the number of nonzero entries.

Proof.

Let the test statistic be the fraction of entries of that are exactly equal to . Under the unspiked model , we have in probability. Let . Under the spiked model we have with probability that at least entries of lie in the set . With probability , at most of the corresponding entries of take the value (exactly) because by continuity of measure,

Therefore, taking sufficiently small, we have with probability and thus consistently distinguishes the spiked and unspiked models. ∎

Appendix H Proof of pre-transformed PCA

In this section we prove our upper bound for the non-Gaussian Wigner model via pre-transformed PCA. We make the following assumptions on the spike prior and the entrywise noise distribution .

Assumption 4.7.

Of the prior we require (as usual) in probability, and we also assume that with probability , all entries of are small: for some fixed . Of the noise , we assume the following:

-

(iii)

has a non-vanishing density function ,

-

(iv)

Letting , we have that and its first two derivatives are polynomially-bounded: there exists and an even integer such that for all .

-

(v)

With as in (ii), has finite moments up to : for all .

An important consequence of assumptions (ii) and (iii) is the following.

Lemma H.1.

for all and . Likewise for all and .

Proof.

We demonstrate ; then follows identically. Using we have

The main theorem of this section is the following.

Theorem 4.8.

Let and let satisfy Assumption 4.7. Let where is drawn from . Let denote entrywise application of the function to , except we define the diagonal entries of to be zero.

-

•

If then as .

-

•

If then as and furthermore the top (unit-norm) eigenvector of correlates with the spike: with probability .

Convergence is in probability. Here denotes the maximum eigenvalue.

Note that Lemma H.1 implies that the expectation defining is finite.

Proof.

First we justify a local linear approximation of . For , define the error term by

(Define .) We will show that the operator norm of is small: with probability . Apply the mean-value form of the Taylor approximation remainder: for some . Bound the operator norm by the Frobenius norm:

Using the polynomial bound on and the fact , we have

Using finite moments of , it follows that , and so Since , Markov’s inequality now gives the desired result: with probability , and so .

Our goal will be to show that is, up to small error terms, another spiked Wigner matrix. Toward this goal we define another error term: for , let , so that

| (13) |

(Define .) We will show that the operator norm of is small: with probability . Let so that . (Define .) We have because for any unit vector ,

Note that is a Wigner matrix (i.e. a symmetric matrix with off-diagonal entries i.i.d.) and so with probability . This follows from Pizzo, Renfrew and Soshnikov (2013) Theorem 1.1, provided we can check that each entry of has finite fifth moment. But this follows from Lemma H.1:

Now we have with probability as desired.

From (13) we now have that, up to small error terms, is another spiked Wigner matrix:

where (to take care of the diagonal) we define , , and . Note that the final error term is also small: . We now have

and so the theorem follows from known results on the spectrum of spiked Wigner matrices, namely Theorem 1.1 from Pizzo, Renfrew and Soshnikov (2013). We need to check the following details. First note that the Wigner matrix has off-diagonal i.i.d. entries that are centered:

Each off-diagonal entry of has variance The rank-1 deformation has top eigenvalue . Recall that in probability. Also,

and so

Therefore the top eigenvalue of the rank-1 deformation converges in probability to . By Lemma H.1, the entries of have finite fifth moment.

The desired convergence of the top eigenvalue now follows. It remains to show that when , the top eigenvalue of correlates with the planted vector . Let be the top eigenvector of with . From above we have

We know has top eigenvalue and has top eigenvalue , which yields

Appendix I Proof of Theorem 5.3: MLE for Wishart with finite prior

Note the following well-known Chernoff bound for the distribution:

Lemma I.1.

For all ,

Similarly, for all ,

We now prove the following theorem:

Theorem 5.3.

Let . Let be a spike prior supported on at most points, for some fixed . If

then there is a (computationally inefficient) procedure that distinguishes between the spiked Wishart model and the unspiked model , with probability of error.

Proof.

First consider the case . Given a matrix , consider the test statistic

where denotes the support of . Under with true spike , we have that , which converges in probability to (since in probability). Hence, for any , we have that with probability under the spiked model .

Let so that . Under the unspiked model, we have

by Lemma I.1. This is so long as

We can choose such precisely under the hypothesis of this theorem.

Hence, by thresholding the statistic at , we obtain a hypothesis test that distinguishes from , with probability of error of either type.

The proof for the case is similar, using instead the test statistic along with the upper tail bound for . ∎

Appendix J Basic properties of Wishart lower bound