Robust Inference Under Heteroskedasticity

via the Hadamard Estimator

Abstract

Drawing statistical inferences from large datasets in a model-robust way is an important problem in statistics and data science. In this paper, we propose methods that are robust to large and unequal noise in different observational units (i.e., heteroskedasticity) for statistical inference in linear regression. We leverage the Hadamard estimator, which is unbiased for the variances of ordinary least-squares regression. This is in contrast to the popular White’s sandwich estimator, which can be substantially biased in high dimensions. We propose to estimate the signal strength, noise level, signal-to-noise ratio, and mean squared error via the Hadamard estimator. We develop a new degrees of freedom adjustment that gives more accurate confidence intervals than variants of White’s sandwich estimator. Moreover, we provide conditions ensuring the estimator is well-defined, by studying a new random matrix ensemble in which the entries of a random orthogonal projection matrix are squared. We also show approximate normality, using the second-order Poincaré inequality. Our work provides improved statistical theory and methods for linear regression in high dimensions.

1 Introduction

Drawing statistical inferences from large datasets in a way that is robust to model assumptions is an important problem in statistics and data science. In this paper, we study a central question in this area, performing statistical inference for the unknown regression parameters in linear models.

1.1 Linear models and heteroskedastic noise

The linear regression model

| (1) |

is widely used and fundamental in many areas. The goal is to understand the dependence of an outcome variable on some covariates . We observe such data points, arranging their outcomes into the vector , and their covariates into the matrix . We assume that depends linearly on , via some unknown parameter vector . The noise vector consists of independent random variables.

A fundamental practical problem is that the structure of noise affects the accuracy of inferences about the regression coefficient . If the noise level in an observation is very high, that observation contributes little useful information. Such an observation could bias our inferences, and we should discard or down-weight it. The practical meaning of large noise is that our model underfits the specific observation. However, we usually do not know the noise level of each observation. Therefore, we must design procedures that adapt to unknown noise levels, for instance by constructing preliminary estimators of the noise. This problem of unknown and unequal noise levels, i.e., heteroskedasticity, has long been recognized as a central problem in many applied areas, especially in finance and econometrics.

In applied data analysis, and especially in the fields mentioned above, it is a common practice to use the ordinary least-squares (OLS) estimator as the estimator of the unknown regression coefficients, despite the potential of heteroskedasticity. The OLS estimator is still unbiased, and has other desirable properties—such as consistency—under mild conditions. For statistical inference about , the common practice is to use heteroskedasticity-robust confidence intervals.

Specifically, in the classical low-dimensional case when the dimension is fixed and the sample size grows, the OLS estimator is asymptotically normal with asymptotic covariance matrix , with

| (2) |

Here the covariance matrix of the noise is a diagonal matrix To form confidence intervals for individual components of , we need to estimate diagonal entries of . White (1980), in one of highest cited papers in econometrics, studied the following plug-in estimator of , which simply estimates the unknown noise variances by the squared residuals:

| (3) |

Here is the vector containing the residuals from the OLS fit. This is also known as the sandwich estimator, the Huber-White, or the Eicker-Huber-White estimator. White showed that this estimator is consistent for the true covariance matrix of , when the sample size grows to infinity, , with fixed dimension . Earlier closely related work was done by Eicker (1967); Huber (1967). In theory, these works considered more general problems, but White’s estimator was explicit and directly applicable to the central problem of inference in OLS. This may explain why White’s work has achieved such a large practical impact, with more than 34,000 citations at the time of writing.

However, it was quickly realized that White’s estimator is substantially biased when the sample size is not too large—for instance when we only have twice as many samples as the dimension. This is a problem, because it can lead to incorrect statistical inferences. MacKinnon and White (1985) proposed a bias-correction that is unbiased under homoskedasticity. However, the question of forming confidence intervals has remained challenging. Despite the unbiasedness of the MacKinnon-White estimate in special cases, confidence intervals based on it have below-nominal probability of covering the true parameters in low dimensions (see e.g., Kauermann and Carroll, 2001). It is not clear if this continues to hold in the high-dimensional case. In fact in our simulations we observe that these confidence intervals (CIs) can be anti-conservative in high dimensions. Thus, constructing accurate CIs in high dimensions remains a challenging open problem.

In this paper, we propose to construct confidence intervals via a variance estimator that is unbiased even under heteroskedasticity. Since the estimator (described later), is based on Hadamard products, we call it the Hadamard estimator. This remarkable estimator has been discovered several times (Hartley et al., 1969; Chew, 1970; Cattaneo et al., 2018), and the later works do not always appear to be aware of the earlier ones. The estimator does not appear to be widely known by researchers in finance and econometrics, and does not appear in standard econometrics textbooks such as Greene (2003), or in recent review papers such as Imbens and Kolesar (2016). We came upon the Hadamard estimator in 2017 while studying the bias of White’s estimator, and were surprised to find out about how early it was discovered. We emphasize that the papers above did not study many of the important properties of this estimator. For instance, it is not even clear based on these works under what conditions this estimator exists.

In our paper, we start by showing how to solve five important problems in the linear regression model using the Hadamard estimator: constructing confidence intervals, estimating signal-to-noise ratio (SNR), signal strength, noise level, and mean squared error (MSE) in a robust way under heteroskedasticity (Section 2.1). To use the Hadamard estimator, we need to show the fundamental result that it is well-defined (Section 2.2). We prove matching upper and lower bounds on the relation between the dimension and sample size guaranteeing that the Hadamard estimator is generically well-defined. We also prove well conditioning. For this, we study a new random matrix ensemble in which the entries of a random partial orthogonal projection matrix are squared. Specifically, we prove sharp bounds on the smallest and largest eigenvalues of this matrix. This mathematical contribution should be of independent interest.

Next, we develop a new degrees-of-freedom correction for the Hadamard estimator, which gives more accurate confidence intervals than several variants of the sandwich estimator (Section 2.3). Finally, we also establish the rate of convergence and approximate normality of the estimator, using the second-order Poincaré inequality (Section 4). We also perform numerical experiments to validate our theoretical results (Section 5). Software implementing our method, and reproducing our results, is available from the authors’ GitHub page, http://github.com/dobriban/Hadamard.

Notation. For a positive integer , we denote . For a vector , let be the Euclidean norm. For any matrix , let or stand for the operator norm, defined by . The Frobenius norm is defined by ; and the infinity norm is .

2 Main Results

2.1 Solving five problems under heteroskedasticity

Under heteroskedasticity, some fundamental estimation and inference tasks in the linear model are more challenging than under homoskedasticity. As we will see, the difficulty often arises from a lack of a good estimator of the variance of the OLS estimator. For the moment, assume that there is an unbiased estimator of the coordinate-wise variances of the OLS estimator. That is, we consider a vector satisfying under heteroskedasticity, where is defined through equation (2). To define this unbiased estimator, we collect some useful notation as follows, though the estimator itself shall be introduced in detail in Section 2.2. Let be the matrix used in defining the ordinary least-squares estimate, and be the projection into the orthocomplement of the column space of . Here is the identity matrix. Let us denote by the Hadamard—or elementwise—product of a matrix or vector with itself.

Among others, the following five important applications demonstrate the usefulness of the unbiased variance estimator .

Constructing confidence intervals.

A first fundamental problem is inference for the regression coefficients. Assuming the noise in the linear model (1) follows a heteroskedastic normal distribution for a diagonal covariance matrix , the random variable follows the standard normal distribution. We replace the unknown variance of the OLS estimator by its approximation and focus on the distribution of the following approximate pivotal quantity

| (4) |

The distribution of this random variable is approximated by a distribution in Section 2.3 and this plays a pivotal role in constructing confidence intervals and conducting hypothesis testing for the coefficients. More generally, our inference result handles any linear combination—contrast—of , see the result in Section 4.

Estimating the SNR.

Recall that is the Euclidean norm of a vector . The signal-to-noise ratio (SNR)

of the linear model (1) is a fundamental measure that quantifies the fraction of variability explained by the covariates of an observational unit. In genetics, the SNR corresponds to heritability if the response denotes the phenotype of a genetic trait (Visscher et al., 2008). Existing work on estimating this important ratio in linear models, however, largely focuses on the relatively simple case of homoskedasticity (see, for example, Dicker (2014); Janson et al. (2017)). Without appropriately accounting for heteroskedasticity, the estimated SNR may be unreliable.

As an application of the estimator , we propose to estimate the SNR using

| (5) |

where recall that is the vector of residuals in the linear model, and denotes a column vector with all entries being ones. Above, denotes the inverse of the Hadamard product of with itself (we will later study this invertibility in detail). The numerator and denominator of the fraction in (5) are unbiased for the signal part and noise part, respectively, as we show in the next two examples. As shown in Section A.12, this estimator is ratio-consistent.

Estimating signal squared magnitude.

A further fundamental problem is estimating the magnitude of the regression coefficient . From the identity , it follows that an unbiased estimator of is . Thus, an unbiased estimator of the squared signal magnitude is .

Estimating the total noise level.

As an intermediate step in the derivation of the unbiased estimator , we obtain the identity

| (6) |

That is, the vector of the entries of can be written as a matrix-vector product in the appropriate way. As a consequence of this, we can use to estimate in an unbiased way. In addition, we can use as an unbiased estimate of the total noise level .

Estimating the MSE.

An important problem concerning the least-squares method is estimating its mean squared error (MSE). Let be the MSE. Consider the estimator As in the part “Estimating signal squared magnitude,” it follows that is an unbiased estimator of the MSE. Later in Section 5 we will show in simulations that this estimator is more accurate than the corresponding estimators based on White’s and MacKinnon-White’s covariance estimators.

2.2 The Hadamard estimator and its well-posedness

This section specifies the variance estimator . This estimator has appeared in Hartley et al. (1969); Chew (1970); Cattaneo et al. (2018), and takes the following form of matrix-vector product

where the matrix is

| (7) |

Here is the usual matrix inverse of and recall that both and denote the Hadamard product. As such, is henceforth referred to as the Hadamard estimator. In short, this is a method of moments estimator, using linear combinations of the squared residuals.

While the Hadamard estimator enjoys a simple expression, there is little work on a fundamental question: whether this estimator exists or not. More precisely, in order for the Hadamard estimator to be well-defined, the matrix must be invertible. Without this knowledge, all five important applications in Section 2.1 would suffer from a lack of theoretical foundation. While the invertibility can be checked for a given dataset, knowing that it should hold under general conditions gives us a confidence that the method can work broadly.

As a major thrust of this paper, we provide a deep understanding of under what conditions should be expected to be invertible. The problem is theoretically nontrivial, because there are no general statements about the invertibility of matrices whose entries are squared values of some other matrix. In fact, is an rank-deficient projection matrix of rank . Therefore, itself is not invertible, and it is not clear how its rank behaves when the entries are squared. However, we have the following lower bound on for this invertibility to hold.

Proposition 2.1 (Lower bound).

If the Hadamard product is invertible, then the sample size must be at least

| (8) |

This result reveals that the Hadamard estimator simply does not exist if is only slightly greater than , (say ), though the OLS estimator exists in this regime. The proof of Proposition 2.1 comes from a well-known property of the Hadamard product, that is, if a matrix is of rank , then the rank of is at most (e.g., Horn and Johnson, 1994). For completeness, a proof of this property is given in Section A.2. Using this property, the invertibility of readily implies

which is equivalent to (8).

In light of the above, it is tempting to ask whether (8) is sufficient for the existence of the Hadamard estimator. In general, this is not the case. For example, let for any orthogonal matrix . Then, is not invertible as is a diagonal matrix whose first diagonal entries are 0 and the remaining are 1. This holds no matter how large is compared to . However, such design matrices that lead to a degenerate are very “rare” in the sense of the following theorem. Recall that .

Theorem 1.

Therefore, the lower bound in Proposition 2.1 is sharp. Roughly speaking, , for , is sufficient for the invertibility of . The proof of this result is new in the vast literature on the Hadamard matrix product. In short, our proof uses certain algebraic properties of the determinant of and employs a novel induction step. Section 3 is devoted to developing the proof of Theorem 1 in detail. To be complete, Cattaneo et al. (2018) show high-probability invertibility when for Gaussian designs. Our invertibility result is more broadly applicable.

Up to now, we have conditioned on , working in a fixed design setting. To better appreciate the theoretical contributions of our paper, we consider a random matrix in the following corollary, which ensures that the Hadamard estimator is well-defined almost surely for popular random matrix ensembles of such as the Wishart ensemble.

Corollary 2.2.

Under the same conditions as in Theorem 1, if is sampled from a distribution that is absolutely continuous with respect to the Lebesgue measure on (put simply, has a density), then is invertible almost surely.

Although is invertible under very general conditions, our simulations reveal that the condition number of this matrix can be very large for close to due to very small eigenvalues. This is problematic, because the estimator can then amplify the error. Our next result shows that is well-conditioned under some conditions if . We will show that this holds for certain random design matrices .

Suppose for instance that the entries of are i.i.d. standard normal, . Then, each diagonal entry of is relatively large, of unit order. The off-diagonal entries are of order . When we square the entries, the off-diagonal entries become of order , while the diagonal ones are still of unit order. Thus, it is possible that the matrix is diagonally dominant, so the diagonal entries are larger than the sum of the off-diagonal ones. This would ensure well-conditioning. We will show rigorously that this is true under some additional conditions.

Specifically, we will consider a high-dimensional asymptotic setting, where the dimension and the sample size are both large. We assume that they grow proportionally to each other, with . This is a modern setting for high-dimensional statistics, and it has many connections to random matrix theory (see e.g., Bai and Silverstein, 2010; Paul and Aue, 2014; Yao et al., 2015).

We will provide bounds on the largest and smallest eigenvalues. We can handle correlated designs , where each row is sampled i.i.d. from a distribution with covariance matrix . Let be the symmetric square root of .

Theorem 2 (Eigenvalue bounds for the Hadamard product with a random design).

Suppose the rows of are i.i.d. and have the form , where have i.i.d. entries with mean zero, unit variance and uniformly bounded -th moment. Suppose that is invertible. Then, as such that for , we have , the matrix with satisfies the following eigenvalue bounds for any fixed and sufficiently large :

and

with probability at least for some positive constant not depending on .

See Section A.3 for a proof. Hence, if , then almost surely

Practically speaking, the above result states that the condition number of is at most with high probability. Our invertibility results are stronger than those of Cattaneo et al. (2018). Specifically, we show generic invertibility in finite dimensional designs with probability one, and condition number bounds on non-Gaussian correlated designs that go beyond those considered in their work.

While Corollary 2.2 proves invertibility for continuous distributions, in practice some columns of can be discrete.222We thank a referee for raising this point. In that case, we can still obtain invertibility or condition number bounds by applying Lemma A.2 used in the proof of Theorem 2. That result which has no assumptions on the continuity of and provides non-asymptotic bounds for the eigenvalues of the matrix.

As an illustration, we study an ANOVA design. For two integers , we write Consider a sequence . Consider the ANOVA design where for , for , and so on, until for . It is readily verified that if . If , then and . Hence, we obtain a bound on the condition number of .

2.3 Degrees-of-freedom adjustment

To obtain a confidence interval for , we propose to approximate the distribution of the approximate pivot in (4) by a -distribution. The key is to find a good approximation to the degrees of freedom. Let us denote by , the expected value of . Suppose the degrees of freedom of are . Using the second moment properties of the variable, these degrees of freedom should obey that

Consequently, we formally define

| (9) |

To proceed, we need to evaluate . The following proposition gives a closed-form expression of this vector assuming homoskedasticity. Let us denote

| (10) |

Recall that .

Proposition 2.3 (Degrees of freedom).

If the noise has i.i.d. normal entries, we have that the vector of degrees of freedom of , defined in equation (9), has the form

| (11) |

where the division is understood to be entrywise.

See Section A.6 for a proof.

We call the inference method based on approximating by a -distribution with the degrees of freedom specified by (11) the Hadamard-t method. This result also leads to a useful degrees of freedom heuristic. If the degrees of freedom are large, this suggests that inferences for are based on a large amount of information. On the other hand, if the degrees of freedom are small, this suggests that the inferences are based on little information, and may thus be unstable.

In our case, the -distribution is still a heuristic, because the numerator and denominator are not independent under heteroskedasticity. However, the degree of dependence can be bounded as follows:

| (12) | |||||

In the first line, we have used that . Hence, . Indeed,

For this reason, we can add a constant times in the second step. Then, we can use the inequality for any two conformable matrices .

In (12), we have chosen , where and denote the maximal and minimal entries of , respectively. Moreover, we have also used that , while .

Now, for designs of aspect ratios that are not close to 1, and with i.i.d. entries with sufficiently many moments, it is known that is of the order . This suggests that the covariance between and is small. Hence, this heuristic suggests that the -approximation should be accurate. Moreover when in probability, and under the conditions in Section 4.1, we also have that the limiting distribution is standard normal.

2.4 Hadamard estimator with

As a simple example, consider the case of one covariate, when . In this case, we have , where are -vectors. Assuming without loss of generality that , the OLS estimator takes the form . Its variance equals , where is the variance of , and are the entries of .

The Hadamard estimator takes the form

which is well-defined if all coordinates are small enough that . See section A.7 for the argument. The unbiased estimator is not always nonnegative. To ensure nonnegativity, we need in this case. In practice, we may enforce non-negativity by using instead of , but see below for a more thorough discussion.

For comparison, White’s variance estimator is while MacKinnon-White’s variance estimator (MacKinnon and White, 1985) can be seen to take the form

We observe that each variance estimator is a weighted linear combination of the squared residuals, where the weights are some functions of the squares of the entries of the feature vector . For White’s estimator, the weights are simply the squared entries. For MacKinnon-White’s variance estimator, the weights are scaled up by a factor . As we know, this ensures the estimator is unbiased under homoskedasticity. For the Hadamard estimator, the weights are scaled up more aggressively by , and there is an additional normalization step. In general, these weights do not have to be larger—or smaller—than those of the other two weighting schemes.

A critical issue is that the Hadamard estimator may not always be non-negative. It is well known that unbiased estimators may fall outside of the parameter space (Lehmann and Casella, 1998). When , almost sure non-negativity is ensured when the coordinates of are sufficiently small. It would be desirable, but seems non-obvious, to obtain such results for general dimension .

In addition, the degrees of freedom from (11) simplifies to This can be as large as , for instance when all . The degrees of freedom can only be small if the distribution of is very skewed.

2.5 Bias of classical estimators

As a byproduct of our analysis, we also obtain explicit formulas for the bias of the two classical estimators of the variances of the ordinary least-squares estimator, namely the White and MacKinnon-White estimators. This can in principle enable us to understand when the bias is small or large.

The estimator proposed by MacKinnon and White (1985), which we will call the MW estimator, is:

| (13) |

where . This estimator is unbiased under homoskedasticity, that is, . It is denoted as HC2 in the paper MacKinnon and White (1985). The same estimator was also proposed by Wu (1986), equation (2.6).

Proposition 2.4 (Bias of classical estimators).

Consider White’s covariance estimator defined in (3) and MacKinnon-White’s estimator defined in (13). Their bias for estimating the coordinate-wise variances of the OLS estimator equals, respectively

| (14) |

for White’s covariance estimator, and

| (15) |

for MacKinnon-White’s estimator. Here is the vector of diagonal entries of , the covariance of the noise.

See Section A.8 for a proof. In particular, MacKinnon-White’s estimator is known to be unbiased under homoskedasticity, that is when (MacKinnon and White, 1985). This can be checked easily using our explicit formula for the bias. Specifically suppose that . Then, , the vector of all ones. Therefore, , the vector of squared Euclidean norms of the rows of . Since is a projection matrix, , so . Therefore we see that

so that MacKinnon-White’s estimator is unbiased under homoskedasticity.

2.6 Some related work

There has been a lot of related work on inference in linear models under heteroskedasticity. Here we can only mention a few of the most closely related works, and refer to Imbens and Kolesar (2016) for a review. In the low-dimensional case, Bera et al. (2002) compared the Hadamard and White-type estimators and discovered that the Hadamard estimator lead to more accurate coverage, while the White estimators have better mean squared error.

As a heuristic to improve the performance of the MacKinnon-White (MW) confidence intervals in high dimensions, Bell and McCaffrey (2002) have a similar approach to ours, with a degrees of freedom correction. Simulations in the very recent review paper by Imbens and Kolesar (2016) suggest this method is the state of the art for heteroskedasticity-consistent inference, and performs well under many settings. However, this correction is computationally more burdensome than the MW method, because it requires a separate computation for each regression coefficient, raising the cost to . In contrast, our method has computational cost only. In addition, the accuracy of their method typically does not increase substantially compared to the MW method. We think that this could be due to the bias of the MW method under heteroskedasticity.

In this work, we have used the term “robust” informally to mean insensitivity to assumptions about the covariance of the noise. Robust statistics is a much larger field which classically studies robustness to outliers in the data distribution (e.g., Huber and Ronchetti, 2011). Recent work has focused, among many other topics, on high-dimensional regression and covariance estimation (e.g., El Karoui et al., 2013; Chen et al., 2016; Donoho and Montanari, 2016; Zhou et al., 2018; Diakonikolas et al., 2017, etc).

3 Existence of Hadamard estimator

In this section we develop the novel proof of the existence of the Hadamard estimator. We begin by observing that Theorem 1 is equivalent to the proposition below. This is because the Lebesgue measure admits an orthogonal decomposition using the SVD.

Proposition 3.1.

Assume . Denote by the set of all projection matrices of rank and let be the Lebesgue measure on . Then, the set has zero- measure.

We take the following lemma as given for the moment.

Lemma 3.2.

Under the same assumptions as Proposition 3.1, there exists a such that .

Proof of Proposition 3.1.

Let . Consider the map from (ignoring the zero-Lebesgue measure set where is not of rank ) to :

It is easy to see that the map is a surjection and the preimage of this map for every is rotationally equivalent to each other. Hence, it suffices to show that the set of where the Hadamard product of is degenerate is measure zero.

We observe that the determinant takes the form

where and are polynomials in the variables . As a fundamental property of polynomials, one and exactly one of the following two cases holds:

-

(a)

The polynomial for all .

-

(b)

The roots of are of zero Lebesgue measure.

Lemma 3.2 falsifies case (a). Therefore, case (b) must hold. Recognizing that the set of where the Hadamard product of is not full rank is a subset of the roots of , case (b) confirms the claim of the present lemma.

∎

Now we turn to prove Lemma 3.2. For convenience, we adopt the following definition.

Definition 3.3.

For a set of vectors , write the rank of the vectors each taking the form for .

First, we give two simple lemmas.

Lemma 3.4.

Suppose two sets of vectors and are linearly equivalent, meaning that one can be linearly represented by the other. Then,

Lemma 3.5.

For any matrix that takes the form for some vectors , we have

Making use of the two lemmas above, Lemma 3.2 is validated once we show the following.

Lemma 3.6.

There exist vectors such that if .

To see this point, we apply the Gram–Schmidt orthonormalization to considered in Lemma 3.6, and get orthonormal vectors . Write , which belongs to . Since and are linearly equivalent, Lemmas 3.4 and 3.5 reveal that

Now we aim to prove Lemma 3.6.

Proof of Lemma 3.6.

We consider a stronger form of Lemma 3.6: for generic , any combination of vectors from for have full rank. Here generic means that this statement does not hold only for a set of zero Lebesgue measure.

We induct on . The statement is true for . Suppose it has been proven true for . Let denote an arbitrary subset of with cardinality . Write .

It is sufficient to show that is generically nonzero. As earlier in the proof of Proposition 3.1, it suffices to show that is not always zero. Without loss of generality, let be the first column of . Expressing the determinant of in terms of its minors along the first column, we see that is an affine function of , with the leading coefficient being the determinant of a minor matrix that results from by removing the first row and the first column. The induction step is complete if we show that this minor matrix, denoted by is nonzero generically. Write the vector in formed by removing the first entry from for . Then, each of the column of takes the form for some . Since the induction step has been validated for , it follows that the determinant of is nonzero in the generic sense.

∎

Proof of Lemma 3.4.

Since can be linearly represented by , each can be written as for constants . Using the representation, the Hadamard product between two vectors reads

This expression for suggests that is in the linear span of for . As a consequence of this, it must hold that

Likewise, we have . Taking the two inequalities together leads to an identity between the two ranks.

∎

4 Rate of Convergence

We now turn to studying the rates of convergence of estimators analyzed in this paper. For this, we need to introduce some additional notation. We use and for the standard big-O and little-o notation. For two positive sequences , , we say if there exists a universal positive constant such that . The condition number of a square matrix is denoted by . Convergence in probability and convergence in distribution are denoted as and , respectively.

We next give a fundamental result characterizing the sampling properties of the Hadamard estimator. This result bounds the relative error for estimating the vector of variances of all the entries of the OLS estimator. It shows that the estimation error is smaller when the aspect ratio is small. We write for the vector of the diagonal elements of .

Theorem 3 (Rate of convergence).

Under the conditions of Theorem 2, assume in addition that the fourth moment of the entries , is less than a constant times the squared variance of the entries. Let denote the vector of variances of the entries of the OLS estimator. Then, under high-dimensional asymptotics as such that , we have for any constant and some constant that for all large enough,

See Section A.9 for a proof.

4.1 Asymptotic normality

We already know that the estimator is unbiased for the variances of the coordinates of the OLS estimator , and in the previous section we have seen an inequality bounding the error . In this section, we aim to study an estimator of for a sequence of vectors . This represents the variance of , and taking to be the -th canonical basis vectors in , for all , it reduces to . The analysis will later be further used to derive an inferential method for .

We use the coordinate-wise case of estimating for some , to illustrate the idea. To study the asymptotic distribution of , where is the -th row of , we consider the noise to be linear combination of a vector of sufficiently smooth functions of a Gaussian random vector, specified by the conditions in Theorem 4 below. In that case, we can express the residuals as .

Thus, we see that the estimator , a linear combination of squared entries of , can be written as a symmetric quadratic form in . In particular, if , its distribution is a weighted linear combination of chi-squared random variables. For general , the above discussion still applies by replacing with . For a linear combination of chi-squared random variables, we expect that it is close to a normal distribution if none of the weights is too large. This is formalized by a so-called second order Poincaré inequality (Chatterjee, 2009). We will use this result to obtain the approximation to the normality of the variance estimator, given in the following result, proved in Section A.10. Let denote total variation distance. For a function , is the sup-norm.

Theorem 4 (Approximate normality).

Assume where consists of independent entries that have means zero, variances one, and fourth moments bounded by . Further suppose that for all , , where , and are twice-differentiable functions such that for all , and for some positive constants .

Let For a sequence of vectors , where for all , of unit norm, we have that

| (16) |

where

| (17) |

and .

We do not necessarily require , , to have unit variances, since we can normalize them and absorb the constants into . It is also possible to allow , and to grow to infinity, which allows for some heavy-tailed distributions for . In addition, as a special case of this theorem, taking to be the -th canonical basis vectors in , for all , leads to

where

In principle, this result could justify using normal confidence intervals for inference on as soon the upper bound provided is small. Moreover, the upper bound in Theorem 4 can be simplified as follows. Denote . We have the upper bound and the lower bound Therefore, the upper bound simplifies to

This bound decouples as the product of a term depending on the unknown covariance matrix , and the known design matrix . Therefore, in practice one can evaluate the second term. Thus, the deviation from normality only depends on the unknown through its condition number.

The subsequent proposition further characterizes conditions on the design matrix that lead to , thereby resulting in the asymptotic normality of the variance estimator of . We also verify that the random design matrix specified in Theorem 2 satisfies these conditions with probability tending to one. See Section A.11 for the proof.

Proposition 4.1 (Conditions for asymptotic normality).

For , let be the -th column of . Consider the following conditions, where and are two positive constants:

-

1.

.

-

2.

-

3.

Then, for from (17), we have

In particular, and thus the total variation from (16) vanishes asymptotically. Moreover, for a random design matrix satisfying the conditions in Theorem 2, if is bounded, the above conditions hold with probability tending to one; and thus is asymptotically normal.

After this detailed analysis of and its estimator , we discuss inference for . This task crucially relies on the first conclusion in the following ratio-consistency lemma, which is a simple consequence of several bounds obtained in Proposition 4.1. The second conclusion in this lemma shows that although —the unbiased estimator of —can be negative with a small probability, all , for , are simultaneously positive with probability tending to one. This finding is consistent with our numerical experiments. The proof of Lemma 4.2 is in Section A.13.

Lemma 4.2 (Ratio-consistency).

We have the following ratio-consistency results:

The following result provides an inferential method for contrasts . Its proof is built on Lemma 4.2, and is included in Section A.13.

Theorem 5 (Inference for contrasts).

Condition 18 can be viewed as a delocalization property, where none of the coordinates of the vector dominate.

5 Numerical Results

In this section, we present several numerical simulations supporting our theoretical results. We consider the following cases:

-

Case 1: Take to have i.i.d. standard normal entries, and the noise to be , where has i.i.d. standard normal entries. The noise covariance matrix is the diagonal matrix of eigenvalues of an AR-1 covariance matrix , with .

-

Case 2: Take to have i.i.d. entries, and the noise to be where has i.i.d. standard normal entries. The noise covariance matrix is the diagonal matrix consisting of the coordinates of where .

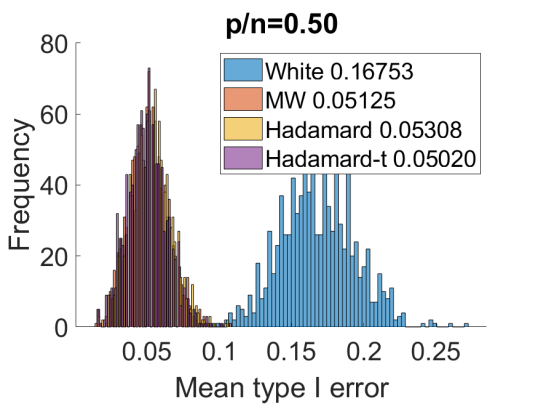

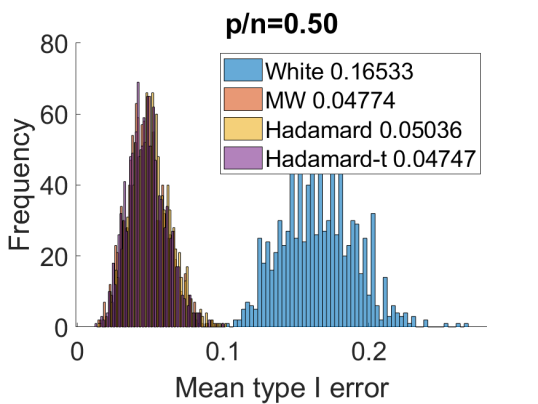

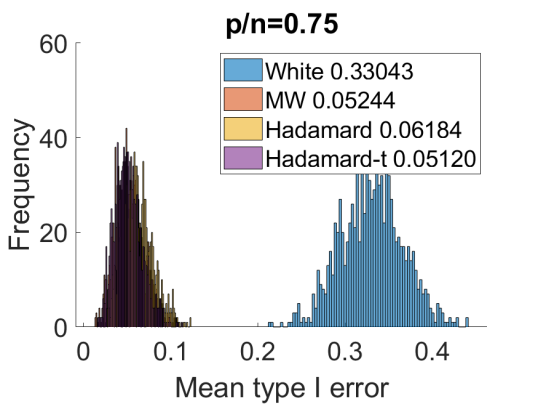

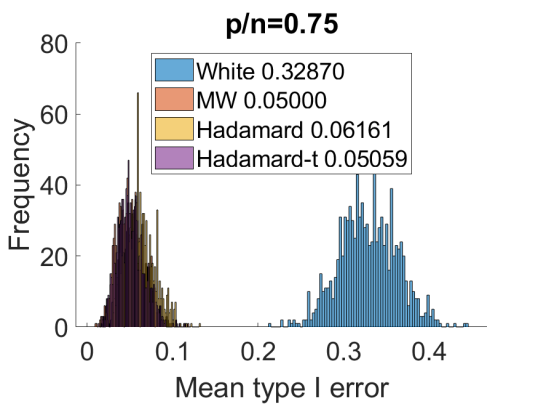

5.1 Mean type I error over all coordinates

We show the mean type I error of the normal confidence intervals based on the White, MacKinnon-White, and Hadamard methods over all coordinates of the OLS estimator.

|

|

|

|

|---|---|---|

|

|

|

|

|

|

|

|

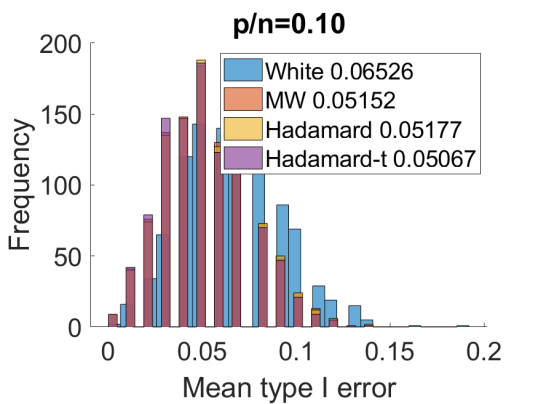

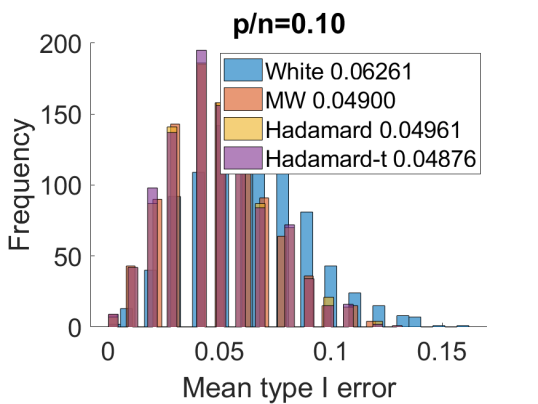

In Figure 1, we show the results for Case 1. We take , and three aspect ratios, , varying . We consider (homoskedasticity), and (heteroskedasticity). We draw one instance of , and draw 1000 Monte Carlo repetitions of .

We observe that the CIs based on White’s covariance matrix estimator are inaccurate for the aspect ratios considered. They have inflated type I error rates. All other estimators are more accurate. The MW confidence intervals are quite accurate for each configuration. The Hadamard estimator using the degrees of freedom correction is comparable, and noticably better if the dimension is high.

5.2 Coordinate-wise type I error

The situation is more nuanced, however, when we look at individual coordinates. In Table 1, we report the empirical type I error of the methods for the first coordinate in Case 1, where the average is over the Monte Carlo trials. In this case, the MW estimator can be either liberal or conservative, while the Hadamard estimator is closer to having the right coverage.

| White | MW | Hadamard | Hadamard-t | |

|---|---|---|---|---|

| 0.5 | 0.172 | 0.045 | 0.042 | 0.039 |

| 0.75 | 0.347 | 0.059 | 0.053 | 0.047 |

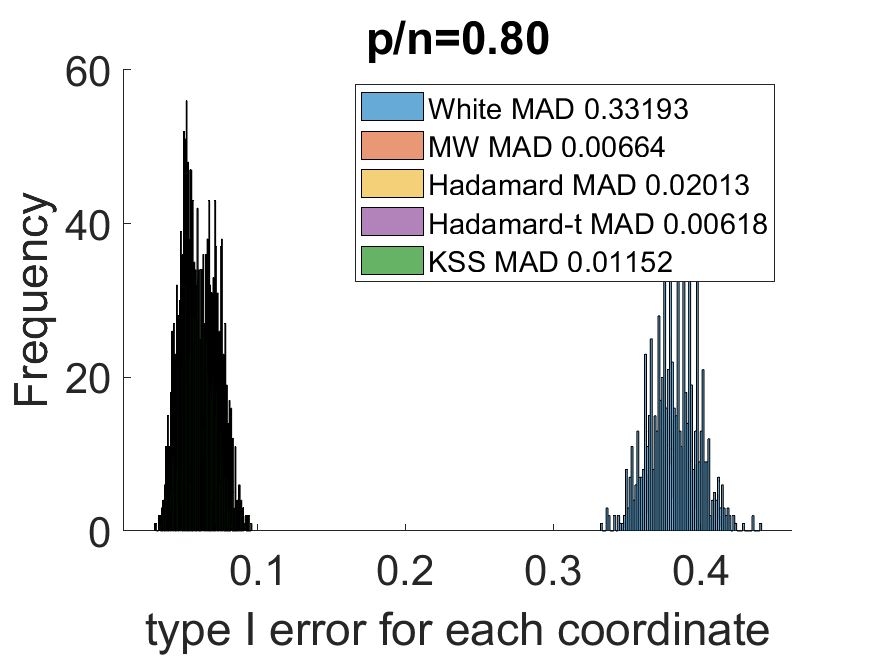

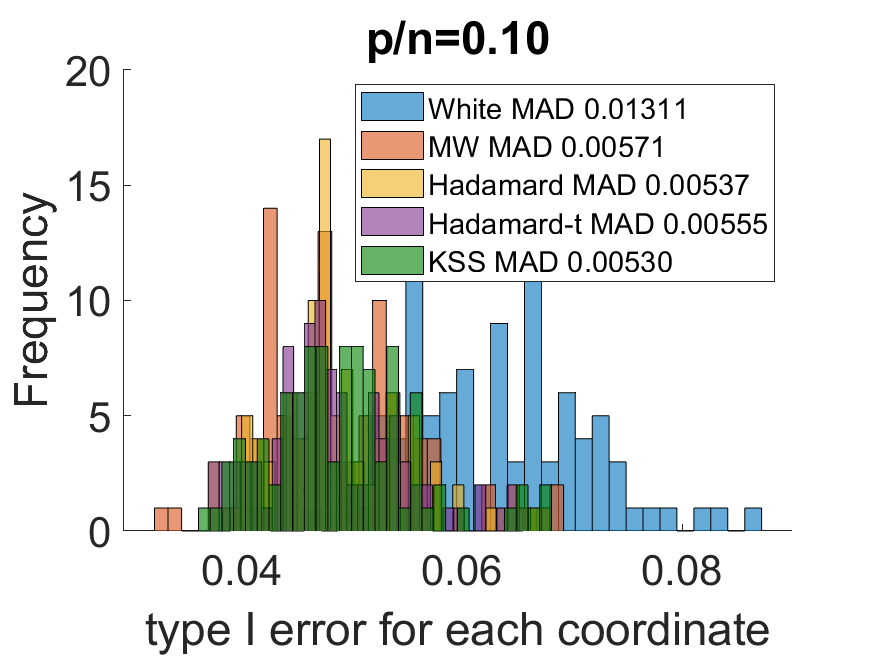

Figure 2 displays the mean type I error of each coordinate in Case 2. We also compare with the leave out (KSS) estimator developed in Kline et al. (2020). The results for Case 1 are in Section B of the appendix. To measure the overall accuracy, we also report the mean absolute deviation where refers to the type I error for the -th coordinate. The White estimator has inflated type I errors especially for larger . We also observe that although the MAD of the Hadamard estimator is large when , the degrees-of-freedom adjustment significantly improves the performance and achieves performance comparable to the MW estimator. The performance of the KSS estimator resembles that of the Hadamard-t estimator.

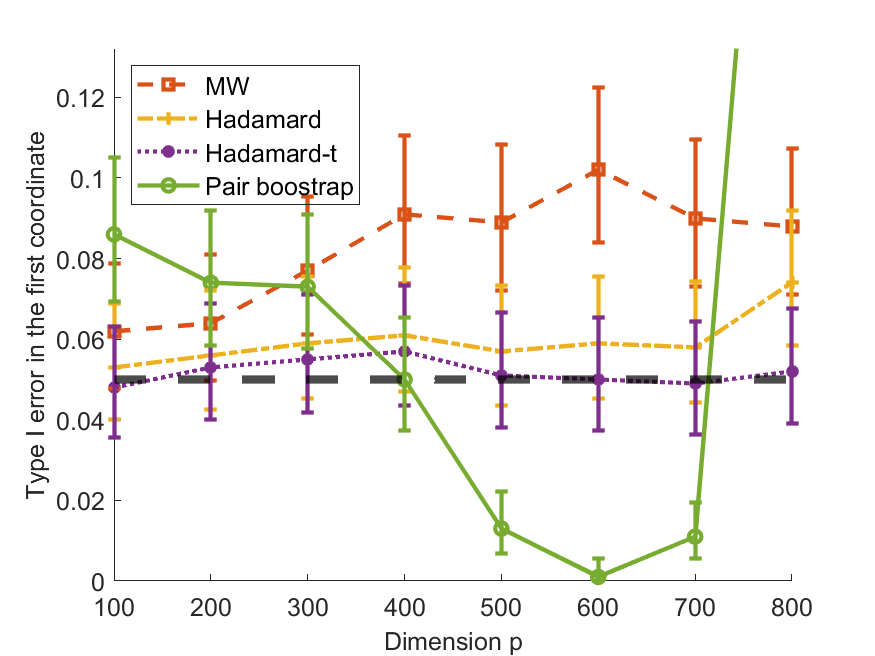

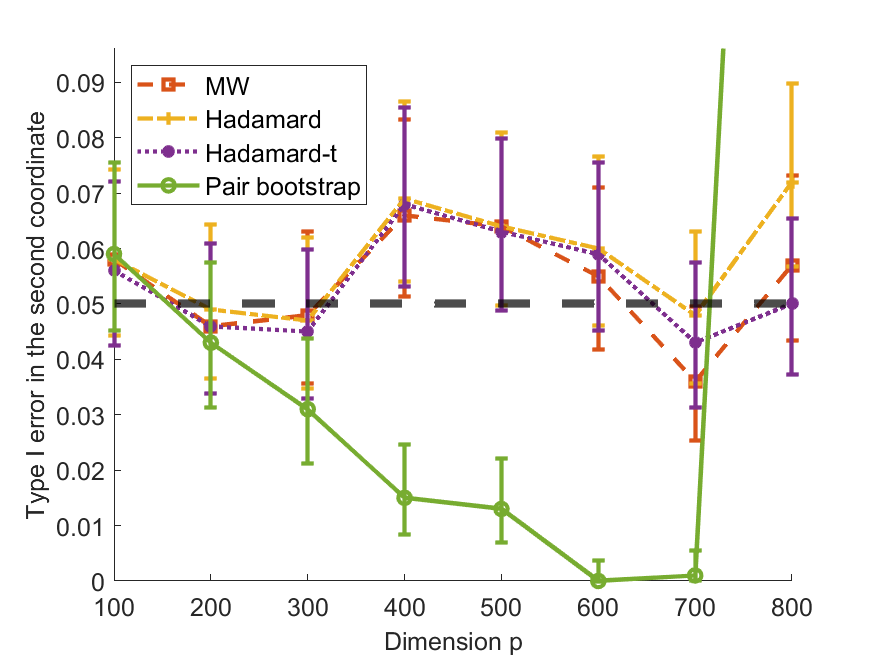

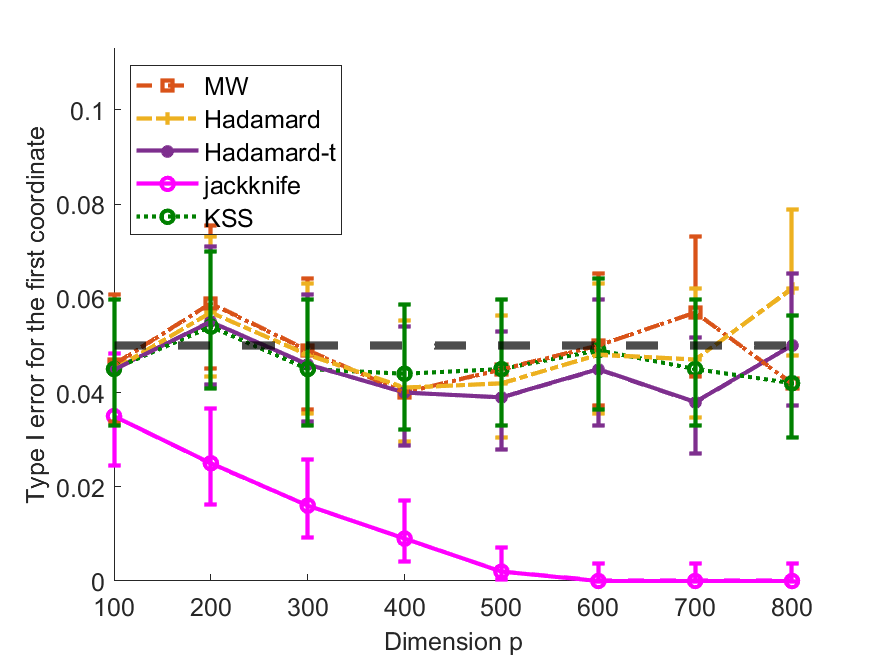

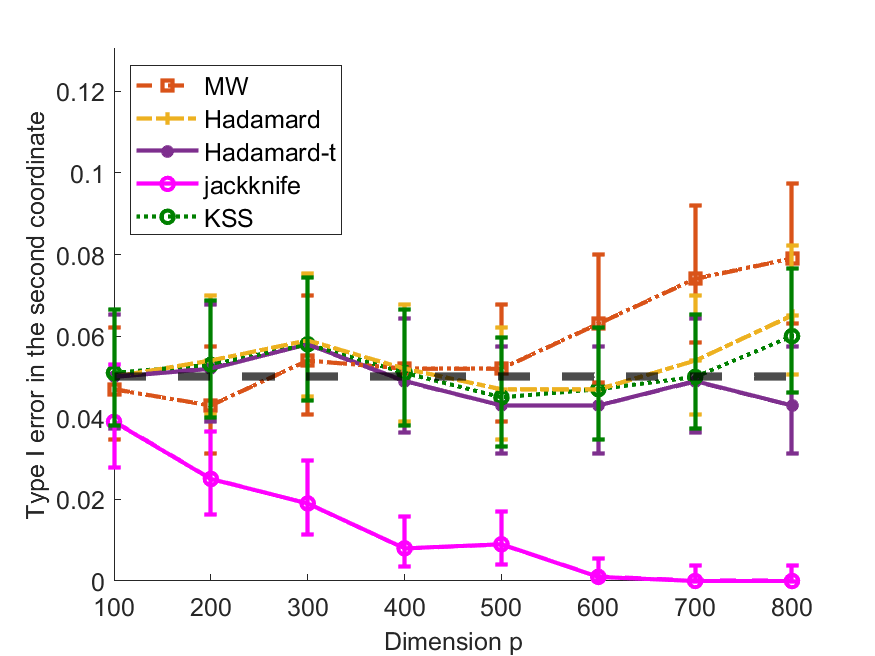

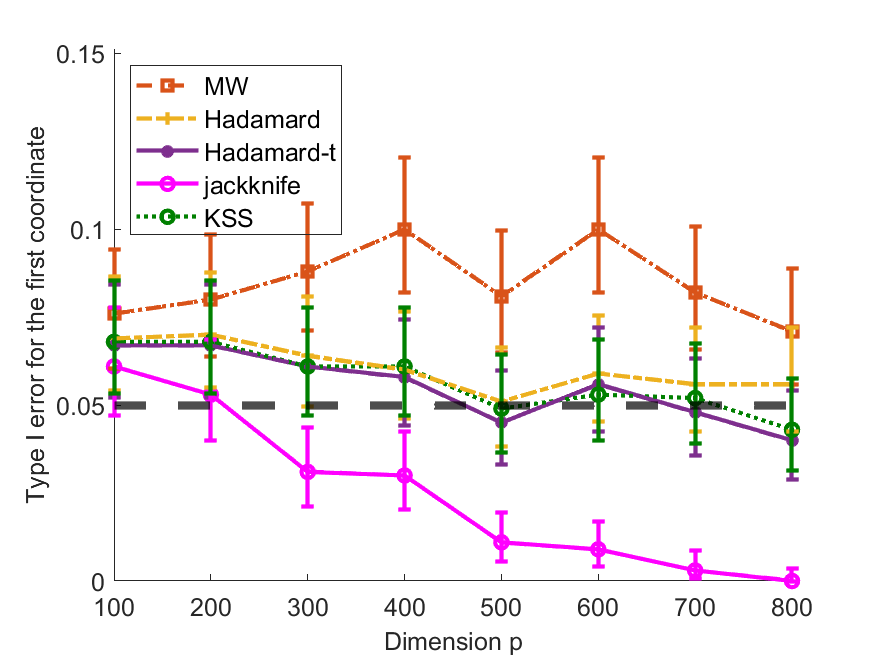

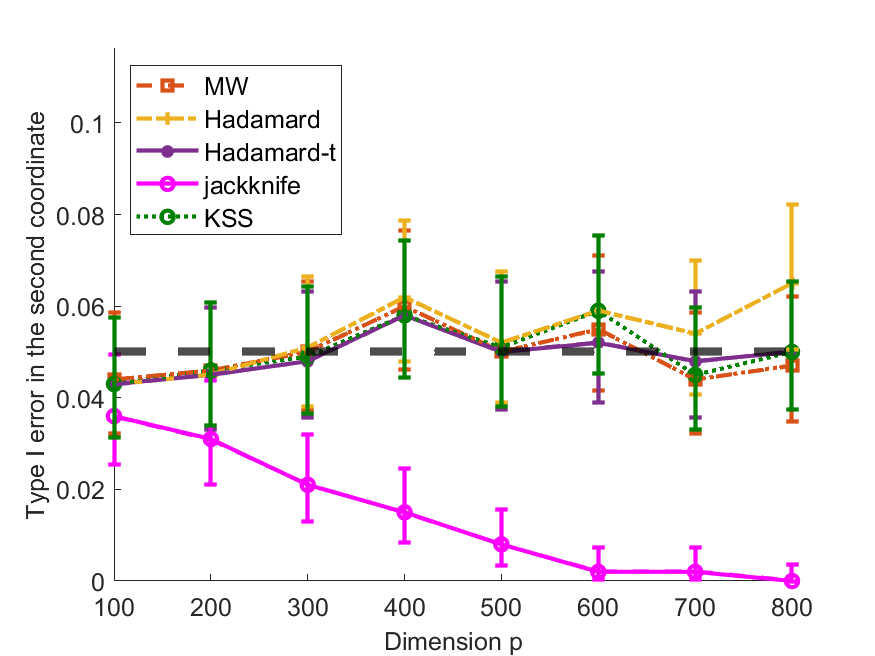

To further compare with other methods, we plot the mean type I error as a function of by taking equally spaced from 100 to 800 with gaps of 100, see Figure 3. The results including the KSS estimator and for Case 1 are reported in Section B of the appendix. We observe that the MW estimators are liberal for the first coordinate but accurate for the second coordinate. The CI based on the Hadamard estimator has a slightly inflated type I error for both coordinates for larger , but the Hadamard-t estimator is accurate.

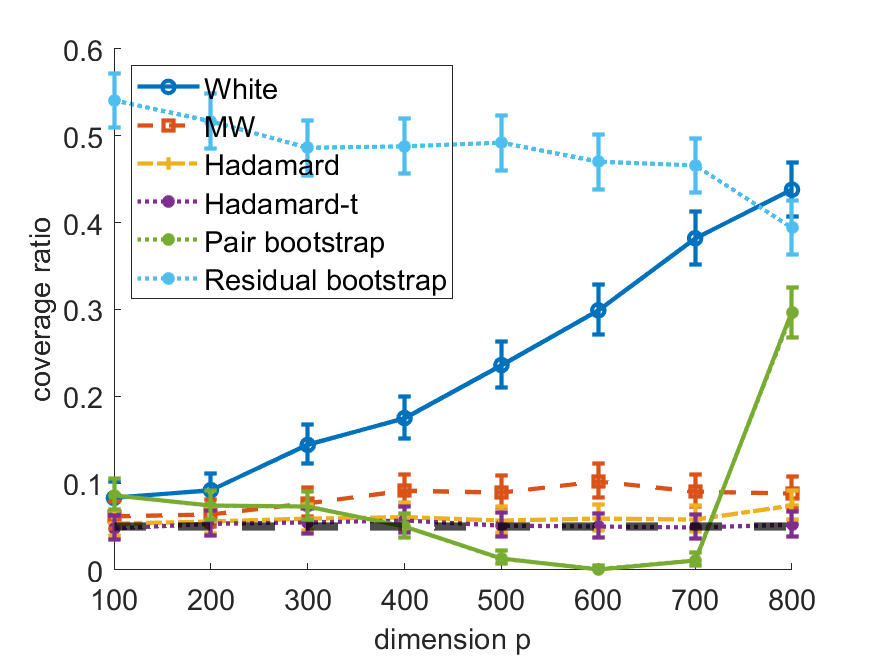

For comparison, we also conduct experiments using two variants of the bootstrap. First, we use the pairs bootstrap (Freedman, 1981), where each observation of the bootstrap sample is sampled randomly with replacement from the rows of , see Figure 3. We also include the residual bootstrap, which samples with replacement the residuals , and adds them to to get the new . Intuitively, this method is justified if the error terms are independent and identically distributed (see e.g., MacKinnon (2006) for a discussion). The corresponding results are in Figure 8.

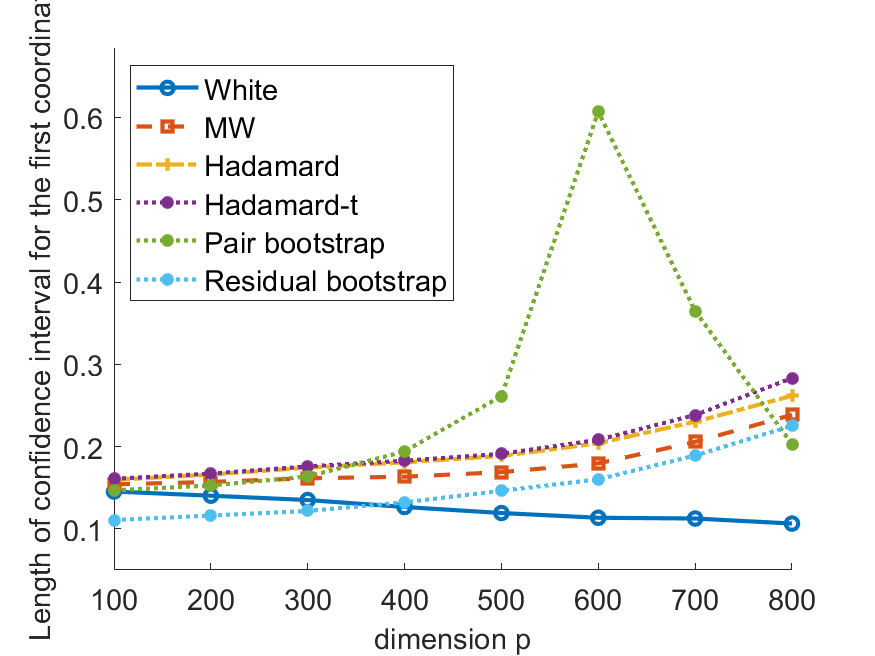

Since the rows are sampled with replacement for the pairs bootstrap, when is close to , the resampled may be ill-conditioned or non-invertible. Figure 3 shows the results where the matrix inversion is done using a pseudoinverse when . This leads to unstable confidence intervals, coverage and length. The lengths of the confidence intervals are in the right panel of Figure 8.

We also conduct experiments using the jackknife (or equivalently HC3 in MacKinnon and White (1985)), and see from Figures 7 and 9 that the jackknife is not accurate. This can be explained by the fact that the expression for the jackknife estimator therein was derived for a relatively small dimension .

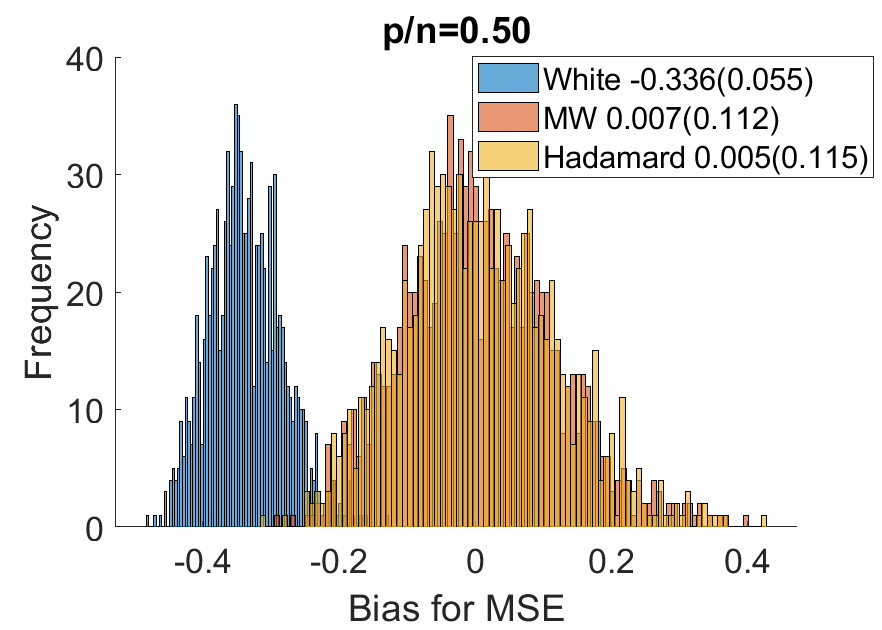

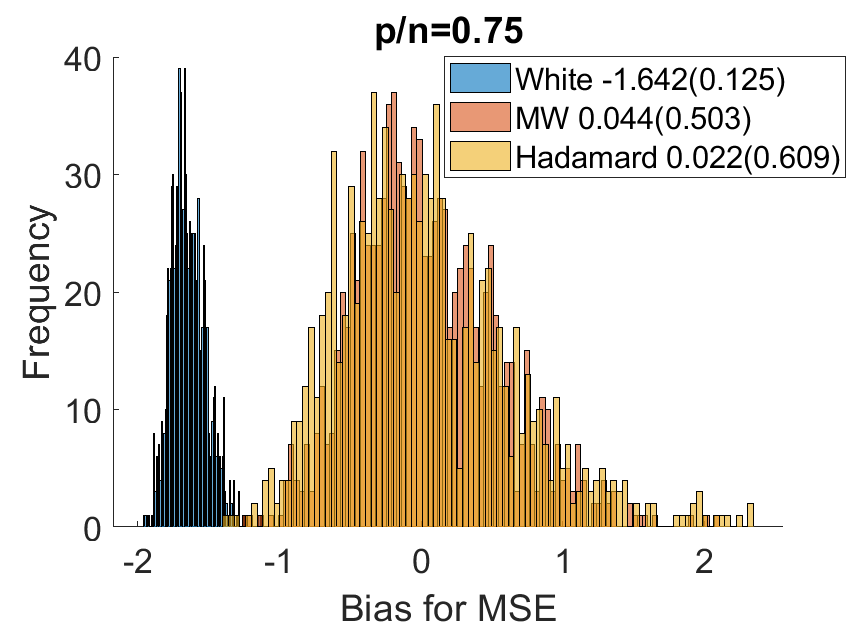

5.3 Estimating the MSE

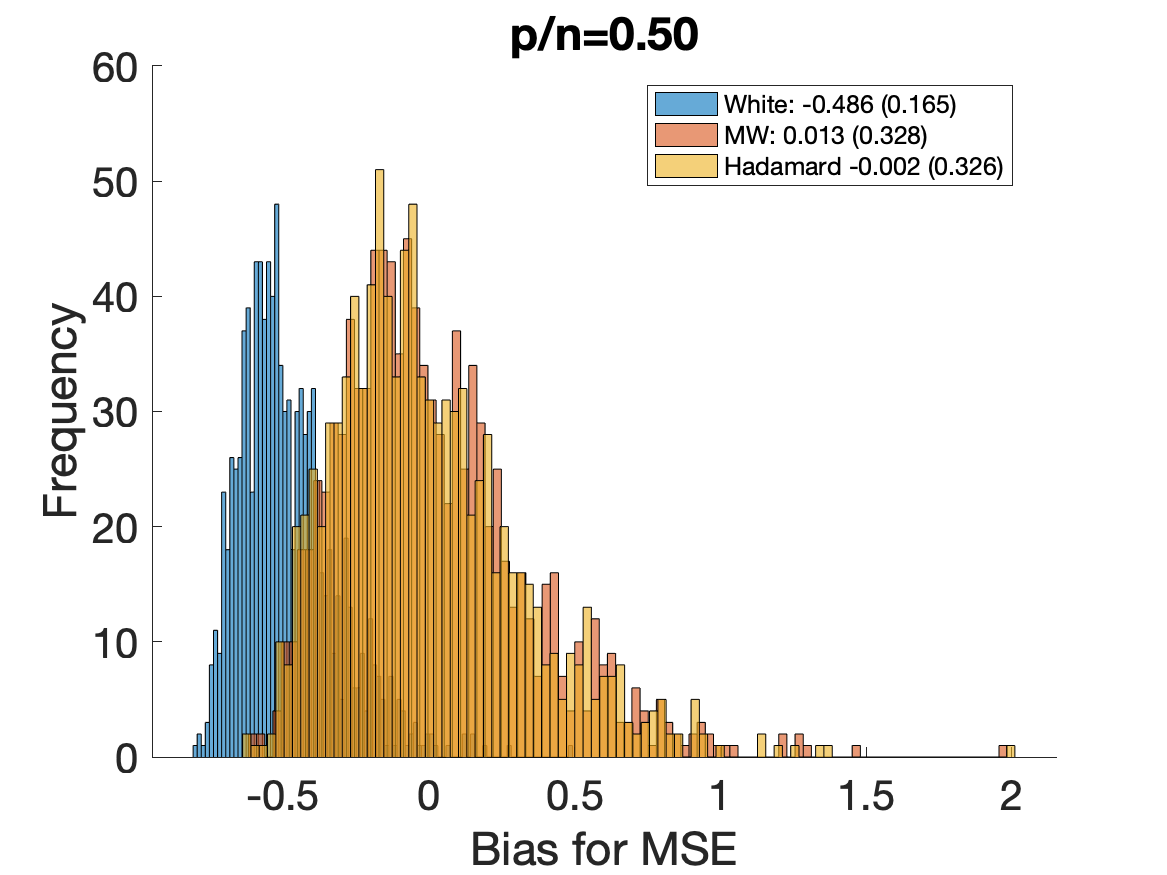

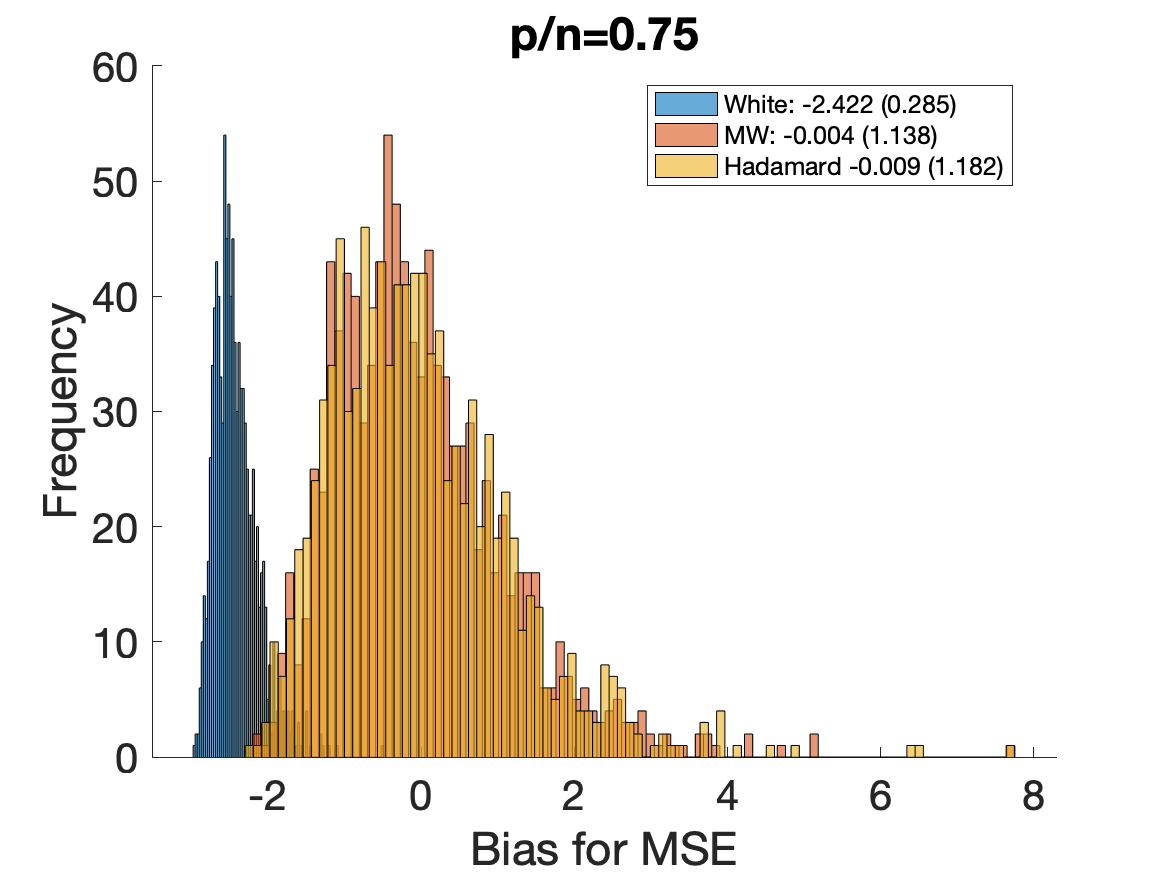

In Figure 4, we show the bias in estimating the MSE of the OLS estimator in Case 1 for the three methods where the numbers outside the bracket correspond to the mean biases of the 1000 Monte Carlo runs and the numbers inside the bracket stand for the standard deviation. For each method, we use the estimator which equals the sum of the variances of the individual component estimators.

The results are in line with those from the previous sections. Both MacKinnon-White’s and the Hadamard estimator perform much better than the White estimator. In addition, the Hadamard estimator is usually comparable to MacKinnon-White’s. More results for Case 2 are included in Section B of the Appendix.

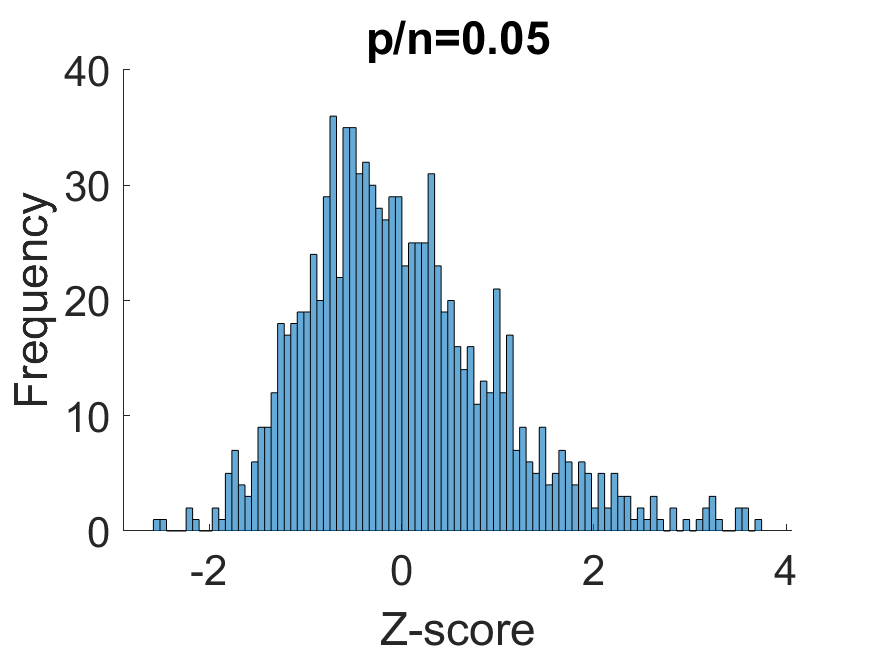

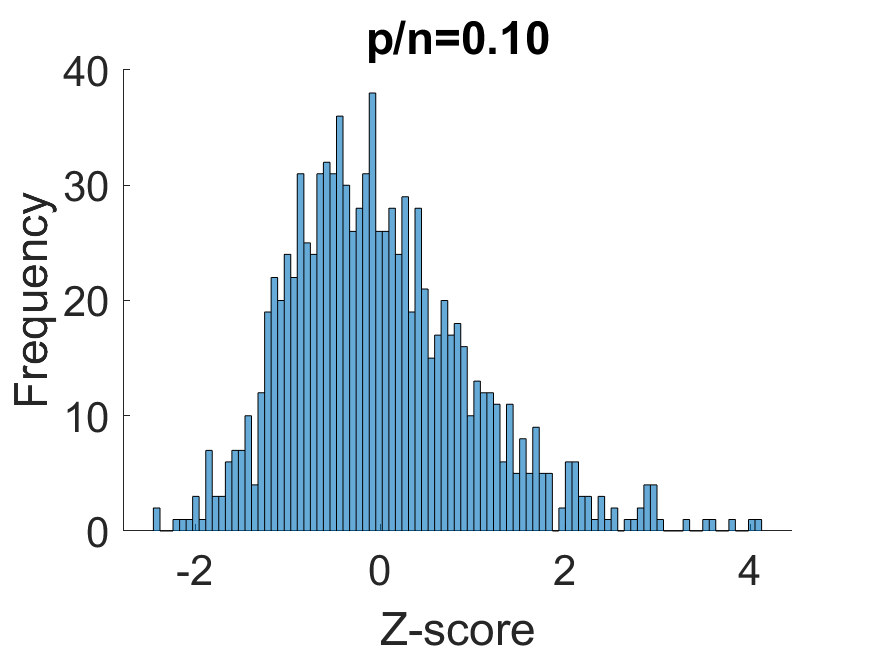

5.4 Approximate Normality

In Figure 5, we show the distribution of -scores of a fixed coordinate of the Hadamard estimator in Case 1. We use a similar setup to the previous sections, but we choose a larger sample size , and also smaller aspect ratios and . We observe a relatively good fit to the normal distribution, but it is also clear that a chi-squared approximation may lead to a better fit.

6 Discussion and Future Work

In this paper, we have provided several fundamental theoretical results for the Hadamard estimator, which can be used to construct confidence intervals for the OLS estimator of coefficients in a linear model under heteroskedasticity. We showed that the Hadamard estimator is well-defined and well-conditioned for certain random design models. There are several important directions for future research. Can one develop similar results for nonlinear models? Is it possible to establish the non-negativity of the Hadamard estimator, possibly with some regularization? Is it possible to show approximate coverage results for our -confidence intervals based on the degrees of freedom correction as given in (11)? Such results have been obtained in the low-dimensional case by Kauermann and Carroll (2001), for instance. However, establishing such results in high dimensions seems to require different techniques.

Beyond our current investigations, an important direction is the development of tests for heteroskedasticity. White’s original paper proposed such a test based on comparing his covariance estimator to the usual one under homoskedasticity. There are many other well-known proposals (Dette and Munk, 1998; Azzalini and Bowman, 1993; Cook and Weisberg, 1983; Breusch and Pagan, 1979; Wang et al., 2018). Perhaps most closely related to our work, Li and Yao (2019) have proposed tests for heteroskedasticity with good properties in low and high dimensional settings. Their tests rely on computing measures of variability of the estimated residuals, including the ratio of the arithmetic and geometric means, as well as the coefficient of variation. Their works and follow-ups such as Bai et al. (2016, 2018) show central limit theorems for these test statistics. They also show an improved empirical power compared to some classical tests for heteroskedasticity. It would be of interest to see if our covariance matrix estimator could be used to develop new tests for heteroskedasticity.

An important extension of the heteroskedastic model is the clustered observations model. Liang and Zeger (1986) proposed estimating equations for such longitudinal/clustered data. They allowed arbitrarily correlated observations for any fixed individual (i.e., within each cluster), and proposed a consistent covariance estimator in the low-dimensional setting. Can one extend our ideas to the clustered case?

Another important direction is to develop covariance estimators that have good performance in the presence of both heteroskedasticity and autocorrelation. The most well-known example is possibly the popular Newey-West estimator (West and Newey, 1987), which is a sum of symmetrized lagged autocovariance matrices with decaying weights. Is it possible to develop new methods inspired by our ideas suitable for this setting?

Our paper does not touch on the interesting but challenging regime where . In that setting, Buhlmann, Dezeure, Zhang, (Dezeure et al., 2017) proposed bootstrap methods for inference with the lasso under heteroskedasticity, under the limited ultra-sparse regime, where the sparsity of the regression parameter is . These methods are limited as they apply only to the lasso, and because they only concern the ultra-sparse regime. It would be interesting to understand this regime better.

It is possible that one could sometimes get better confidence intervals by adding some regularization to the starting estimator, such as starting with an regularized regression estimator. However, note that this would come at the cost of introducing some bias, so that each confidence interval would not be centered at the true parameter anymore. It is possible that by an appropriately small regularization, one could achieve a favorable “bias-variance” tradeoff for confidence intervals. However, the specific details are likely complex (e.g., how to tune the regularization) and deserve a separate investigation.

7 Acknowledgements

The authors thank Matias Cattaneo and Jason Klusowski for valuable discussions and feedback on an earlier version of the manuscript. We are grateful to the referees, whose valuable suggestions have lead to many improvements to the paper. This work was supported in part by the NSF grant DMS 2046874.

References

- Azzalini and Bowman (1993) A. Azzalini and A. Bowman. On the use of nonparametric regression for checking linear relationships. Journal of the Royal Statistical Society. Series B (Methodological), 55(2):549–557, 1993.

- Bai and Silverstein (2010) Z. Bai and J. W. Silverstein. Spectral analysis of large dimensional random matrices. Springer, 2010.

- Bai et al. (2016) Z. Bai, G. Pan, and Y. Yin. Homoscedasticity tests for both low and high-dimensional fixed design regressions. arXiv preprint arXiv:1603.03830, 2016.

- Bai et al. (2018) Z. Bai, G. Pan, and Y. Yin. A central limit theorem for sums of functions of residuals in a high-dimensional regression model with an application to variance homoscedasticity test. Test, 27:896–920, 2018.

- Bell and McCaffrey (2002) R. M. Bell and D. F. McCaffrey. Bias reduction in standard errors for linear regression with multi-stage samples. Survey Methodology, 28(2):169–182, 2002.

- Bera et al. (2002) A. K. Bera, T. Suprayitno, and G. Premaratne. On some heteroskedasticity-robust estimators of variance–covariance matrix of the least-squares estimators. Journal of Statisticsistical Planning and Inference, 108(1-2):121–136, 2002.

- Breusch and Pagan (1979) T. S. Breusch and A. R. Pagan. A simple test for heteroscedasticity and random coefficient variation. Econometrica: Journal of the Econometric Society, 47(5):1287–1294, 1979.

- Cattaneo et al. (2018) M. D. Cattaneo, M. Jansson, and W. K. Newey. Inference in linear regression models with many covariates and heteroscedasticity. Journal of the American Statistical Association, 113(523):1350–1361, 2018.

- Chatterjee (2009) S. Chatterjee. Fluctuations of eigenvalues and second order poincaré inequalities. Probability Theory and Related Fields, 143(1-2):1–40, 2009.

- Chen et al. (2016) M. Chen, C. Gao, and Z. Ren. A general decision theory for huber’s epsilon-contamination model. Electronic Journal of Statistics, 10(2):3752–3774, 2016.

- Chew (1970) V. Chew. Covariance matrix estimation in linear models. Journal of the American Statistical Association, 65(329):173–181, 1970.

- Cook and Weisberg (1983) R. D. Cook and S. Weisberg. Diagnostics for heteroscedasticity in regression. Biometrika, 70(1):1–10, 1983.

- Dette and Munk (1998) H. Dette and A. Munk. Testing heteroscedasticity in nonparametric regression. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 60(4):693–708, 1998.

- Dezeure et al. (2017) R. Dezeure, P. Bühlmann, and C.-H. Zhang. High-dimensional simultaneous inference with the bootstrap. Test, 26:685–719, 2017.

- Diakonikolas et al. (2017) I. Diakonikolas, G. Kamath, D. M. Kane, J. Li, A. Moitra, and A. Stewart. Being robust (in high dimensions) can be practical. In International Conference on Machine Learning, pages 999–1008. PMLR, 2017.

- Dicker (2014) L. H. Dicker. Variance estimation in high-dimensional linear models. Biometrika, 101(2):269–284, 2014.

- Donoho and Montanari (2016) D. Donoho and A. Montanari. High dimensional robust m-estimation: Asymptotic variance via approximate message passing. Probability Theory and Related Fields, 166(3-4):935–969, 2016.

- Eicker (1967) F. Eicker. Limit theorems for regressions with unequal and dependent errors. In Proceedings of the fifth Berkeley symposium on mathematical statistics and probability, volume 1, pages 59–82, 1967.

- El Karoui et al. (2013) N. El Karoui, D. Bean, P. J. Bickel, C. Lim, and B. Yu. On robust regression with high-dimensional predictors. Proceedings of the National Academy of Sciences, 110(36):14557–14562, 2013.

- Freedman (1981) D. A. Freedman. Bootstrapping regression models. The Annals of Statistics, 9(6):1218–1228, 1981.

- Greene (2003) W. H. Greene. Econometric analysis. Pearson, 2003.

- Hartley et al. (1969) H. Hartley, J. Rao, and G. Kiefer. Variance estimation with one unit per stratum. Journal of the American Statistical Association, 64(327):841–851, 1969.

- Horn and Johnson (1990) R. A. Horn and C. R. Johnson. Matrix analysis. Cambridge University Press, 1990.

- Horn and Johnson (1994) R. A. Horn and C. R. Johnson. Topics in matrix analysis. Cambridge University Press, 1994.

- Huber (1967) P. J. Huber. The behavior of maximum likelihood estimates under nonstandard conditions. In Proceedings of the fifth Berkeley symposium on mathematical statistics and probability, volume 1, pages 221–233. Berkeley, CA, 1967.

- Huber and Ronchetti (2011) P. J. Huber and E. M. Ronchetti. Robust statistics. Wiley, 2011.

- Imbens and Kolesar (2016) G. W. Imbens and M. Kolesar. Robust standard errors in small samples: Some practical advice. Review of Economics and Statistics, 98(4):701–712, 2016.

- Janson et al. (2017) L. Janson, R. F. Barber, and E. Candès. Eigenprism: inference for high dimensional signal-to-noise ratios. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 79(4):1037–1065, 2017.

- Kauermann and Carroll (2001) G. Kauermann and R. J. Carroll. A note on the efficiency of sandwich covariance matrix estimation. Journal of the American Statistical Association, 96(456):1387–1396, 2001.

- Kline et al. (2020) P. Kline, R. Saggio, and M. Sølvsten. Leave-out estimation of variance components. Econometrica, 88(5):1859–1898, 2020.

- Lehmann and Casella (1998) E. Lehmann and G. Casella. Theory of point estimation. Springer Texts in Statistics, 1998.

- Li and Yao (2019) Z. Li and J. Yao. Testing for heteroscedasticity in high-dimensional regressions. Econometrics and Statistics, 9:122–139, 2019.

- Liang and Zeger (1986) K.-Y. Liang and S. L. Zeger. Longitudinal data analysis using generalized linear models. Biometrika, 73(1):13–22, 1986.

- MacKinnon (2006) J. G. MacKinnon. Bootstrap methods in econometrics. Economic Record, 82:S2–S18, 2006.

- MacKinnon and White (1985) J. G. MacKinnon and H. White. Some heteroskedasticity-consistent covariance matrix estimators with improved finite sample properties. Journal of econometrics, 29(3):305–325, 1985.

- Paul and Aue (2014) D. Paul and A. Aue. Random matrix theory in statistics: A review. Journal of Statisticsistical Planning and Inference, 150:1–29, 2014.

- Visscher et al. (2008) P. M. Visscher, W. G. Hill, and N. R. Wray. Heritability in the genomics era—concepts and misconceptions. Nature reviews genetics, 9(4):255–266, 2008.

- Wang et al. (2018) H. Wang, P.-S. Zhong, and Y. Cui. Empirical likelihood ratio tests for coefficients in high-dimensional heteroscedastic linear models. Statistica Sinica, 28(4):2409–2433, 2018.

- West and Newey (1987) K. D. West and W. K. Newey. A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica, 55(3):703–708, 1987.

- White (1980) H. White. A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica, 48(4):817–838, 1980.

- Wu (1986) C.-F. J. Wu. Jackknife, bootstrap and other resampling methods in regression analysis. The Annals of Statistics, 14(4):1261–1295, 1986.

- Yang (2020) F. Yang. Linear spectral statistics of eigenvectors of anisotropic sample covariance matrices. arXiv preprint arXiv:2005.00999, 2020.

- Yao et al. (2015) J. Yao, Z. Bai, and S. Zheng. Large Sample Covariance Matrices and High-Dimensional Data Analysis. Cambridge University Press, 2015.

- Zhou et al. (2018) W.-X. Zhou, K. Bose, J. Fan, and H. Liu. A new perspective on robust M-estimation: Finite sample theory and applications to dependence-adjusted multiple testing. Annals of Statistics, 46(5):1904, 2018.

Appendix

Notation. For two positive sequences , , we write if for some positive constant .

Appendix A Proofs

A.1 Proof of unbiasedness of the Hadamard estimator

We consider estimators of the vector of variances of of the form where is a matrix, and is the element-wise (or Hadamard) product of the vector or matrix with itself. Our goal is to find such that , where . Here the operator returns the vector of diagonal entries of the matrix , that is .

Recall that is a matrix. We have that . Since , we have that Thus, our goal is to find unbiased estimates of the diagonal of this matrix. The following key lemma re-expresses that diagonal in terms of Hadamard products:

Lemma A.1.

Let be a zero-mean random vector, and be a fixed matrix. Then,

In particular, let be a diagonal matrix. and let be the vector of diagonal entries of . Then

Alternatively, let be a vector. Then

Proof.

Suppose has rows, and denote them by , . Let also . Then, for any , the -th entry of the left hand side equals, with denoting the number of columns of ,

The -th entry of the right hand side equals Thus, the two sides are equal, which proves the first claim of the lemma. The second claim follows directly from the first claim, from the special case when the covariance of is diagonal. The third claim is simply a restatement of the second one.

∎

We now apply the lemma as follows.

-

1.

Let us use the lemma for and . Notice that we have is diagonal, so the right hand side of the lemma is , where the equality follows from our calculation before the lemma. Moreover, the left hand side is , where we vectorize , writing . The equality follows because is diagonal. Thus, by the lemma, we have

-

2.

Let us now use the lemma for a second time, with and . This shows that . By linearity of expectation, we obtain

-

3.

Finally, let us use the lemma for the third time, with and . As in the first case, the left hand side equals . The right hand side equals , where we used that is a symmetric matrix. Now, . Thus, we conclude .

Putting these conclusions together, we obtain that is unbiased, namely , if This system of linear equations holds for any if and only if If is invertible, then we have (7). This shows that the original estimator has the required form, finishing the proof.

For a sequence , we can also estimate , the variance of . Since we can use to estimate in an unbiased way, and considering that is diagonal, an unbiased estimator of is .

A.2 Proof of Proposition 2.1

To prove the lower bound, we first claim that for any symmetric matrix ,

Therefore, in order for to be invertible, we need By solving the quadratic inequality, this is equivalent to .

To prove the claim about ranks, let be the rank of , and let be its eigendecomposition. Here are orthogonal, but not necessarily of unit norm. Then,

This shows that the rank of is at most , as desired.

A.3 Proof of Theorem 2

Our first step is to reduce to the case . Indeed, we notice that we can write , where is the matrix with rows . Hence, Therefore, we can take .

The next step is to reduce the bounds on eigenvalues to bounds on certain quadratic forms. For all , let us define the matrices . See Section A.4 for a proof of the following result.

Lemma A.2 (Reduction to quadratic forms).

We have the following two bounds on the eigenvalues of with :

and

To bound these expressions, we will use the following well-known statement about concentration of quadratic forms; its short proof is provided in Section A.5.

Lemma A.3 (Concentration of quadratic forms, consequence of Lemma B.26 in Bai and Silverstein (2010)).

Let be a random vector with i.i.d. entries and , for which and for some and . Moreover, let be a random symmetric matrix independent of , with uniformly bounded eigenvalues. Then

Proceeding with the proof of Theorem 2, we can scale so that the variances of the entries of are . Define the following events:

We obtain from Lemma A.3 and by taking a union bound over . Next, we will verify that . Then by Lemma A.2, and applying the inequality with , , the proof will be concluded.

Now to bound , according to the rank inequality, see Theorem A.43 of Bai and Silverstein (2010), we can equivalently show for sufficiently large . We further define

Since for , it can be checked that by Chebyshev’s inequality and taking a union bound. To bound , by the argument from Section 9.12.5 of Bai and Silverstein (2010), it can be readily checked that for any fixed . Then by taking large enough, .

Let be a small positive constant, and take . Denoting the imaginary unit by , define the rectangular region

in the complex plane.

For any in , let , and be the solution to the self-consistent equation whose imaginary part has the same sign as that of . This equation has a unique solution (Bai and Silverstein, 2010).

By Cauchy’s integral formula, we have

| (19) |

Defining , we have for any fixed . This is a consequence of the averaged local law from random matrix theory, see Theorem 3.5 of Yang (2020) for instance. Specifically, we apply their result for and . Note that for defined in their equation (2.10), thus with from their equation (3.10) and some small , . Additionally, the bounded support condition in their equation (3.15) is satisfied on . Then (3.21) in their Theorem 3.5 implies our desired bound.

By taking large enough, . Therefore, combining the above bounds for the probabilities of and by (19), we have

This finishes the argument.

A.4 Proof of Lemma A.2

We need to bound the smallest and largest eigenvalues of . Now, for all , , where and is the Kronecker delta which equals unity if , and zero otherwise. We will use the following well-known rank-one perturbation formula for an invertible matrix and a vector of conformable size:

We will also use a “leave-one-out” argument which has roots in random matrix theory (see e.g., Bai and Silverstein, 2010; Paul and Aue, 2014; Yao et al., 2015). For any , letting , we have For all , the quantity that is squared in the -th entry of is thus

Also, for all , we have so that the diagonal terms are

By the Gershgorin disk theorem (Horn and Johnson, 1990, Thm 6.1.1), we have Thus,

Now, the sum in the numerator can be written as . Thus, the upper bound simplifies to Similarly, for the smallest eigenvalue, by the Gershgorin disk theorem (Horn and Johnson, 1990, Thm 6.1.1), we have We can express for all

Hence finishing the proof.

A.5 Proof of Lemma A.3

We will use the following Lemma quoted from Bai and Silverstein (2010).

Lemma A.4 (Trace Lemma, Lemma B.26 of Bai and Silverstein (2010)).

Let be a p-dimensional random vector of i.i.d. elements with mean zero. Suppose that for all , and let be a fixed matrix. Then for any ,

for some constant that only depends on .

Proof.

Under the conditions of Lemma A.3, the operator norms are bounded by a constant , thus and . Consider now a random vector with the properties assumed in the present lemma. For and with , using that and the other the conditions in Lemma A.3, Lemma A.4 thus yields

or equivalently . By Markov’s inequality applied to the -th moment of , we obtain as required that for , ∎

A.6 Proof of Proposition 2.3

We need to evaluate . Note that this vector is the diagonal of , which is equal to

Note that , since the residuals . Using this expression and recognizing that has i.i.d. entries, for any , the -th element of is

To proceed, we recognize that is the -th element of

and is the -th element of .

A.7 Calculation for the case when

We compute each part of the unbiased estimator in turn. We start by noticing that is a vector. We continue by calculating , where . Thus,

Denoting , and , we can write Now, the estimator takes the form . Hence, we need to calculate . We use the rank-one perturbation formula In our case,

and has entries for . This leads to the desired final answer:

Next, since , we have for from (10) that . Finally, for from (11), since , , and , so that , we find

as desired.

A.8 Proof of Proposition 2.4

To compute the bias of White’s estimator defined in (3), we proceed as follows. First we need to compute its expectation,

As we saw, Thus,

Again, as we saw, Therefore, the bias of White’s estimator is as in (14).

To compute the bias of MacKinnon-White’s estimator, we proceed similarly, starting with its expectation:

In this equation, the expression is interpreted as the diagonal matrix whose entries are those on the diagonal of . Thus,

Thus the bias is as in (15), finishing the proof.

A.9 Proof of Theorem 3

We aim to bound , where denotes usual Euclidean vector norm. Recalling that and , where , we have

| (20) |

We will find upper bounds for each term in the above product.

- 1.

- 2.

-

3.

To bound , we can express , where for all , From the earlier unbiasedness argument, , and thus . A simple calculation shows that, with for all , we have

Now for all , the excess kurtosis can be bounded as . Therefore, we can bound by Markov’s inequality:

According to Theorem 2, holds with probability for some positive constant and any constant . Hence

In conclusion, we have for sufficiently large and with that

This proves the required result.

A.10 Proof of Theorem 4

For the given , any matrices and any vector , we find

Taking , , above, we find that

| (21) |

where is defined in (17).

Recall the following claim from e.g., Bai and Silverstein (2010). Let , where , , are i.i.d. real random variables with mean zero and variance one. Let be a real symmetric matrix. Then we have

| (22) |

Let be defined for all by . By the moment assumptions on the entries of , we have

| (23) |

To use the second order Poincaré inequality, see Chatterjee (2009), Theorem 2.2, we need to bound the following quantities:

In the following, we denote for all by the -th row of , and omit the dependence on for simplicity. A direct calculation yields

We have

where we use (22) in the last step. Then . We also have and

Therefore, we have

This proves the desired claim.

A.11 Proof of Proposition 4.1

Proof.

We consider first. For any vector , we find that

| (24) | ||||

where we use condition 3 in the first step, and in the second last step.

Recall that for , is the -th column of . Then

| (25) | ||||

Substituting into (24), by the above bound, and by the conditions and , we conclude that

The upper bound for is obtained by

where the second step uses condition 3 and , and the third step uses conditions 1 and 2.

In the remainder, we show that the first two conditions hold probability tending to one under the random design satisfying the conditions of Theorem 2. In a matrix form, write with the -th row being for all , where has independent entries with zero mean, unit variance and finite -th moment. The bound for in condition 1 holds with probability tending to one, as a consequence of Theorem 2.

Next we verify condition 2. For any sequence of deterministic vectors with a bounded norm, we have

where in the first step we use the Sherman–Morrison formula

and in the second step we use the moment bound for any . This moment bound can be checked by applying Lemma A.4 with and using .

Therefore

We further find where we use and that is bounded. Then we find

This shows the validity of condition 2 with probability tending to one. ∎

A.12 Consistency of the SNR estimator

The following result shows that the SNR estimator given in (5) is ratio-consistent.

Proposition A.5 (Ratio-consistency of SNR estimator).

Proof.

We already know that the numerator and the denominator of are unbiased estimators for and , respectively. The conclusion follows by applying Slutsky’s theorem if we can show

| (26) |

and

| (27) |

We show (26) first by verifying that . We have a decomposition for , given as . By the assumptions , , and , we find

| (28) | ||||

For , using (21) with and summing over , we find . Then

where in the second step we use (24) with . By and , we have . Therefore, combining this with (28) and , we conclude (26).

Then we verify (27) by checking that the variance of the left term tends to zero. Writing we obtain

where in the second step we use (24). Since , we conclude (27).

∎

A.13 Proof of Lemma 4.2 and Theorem 5

A.13.1 Proof of Lemma 4.2

We start with the first conclusion. By (23) and the conclusion from Proposition 4.1, we have

| (29) |

This and yield

To show the second conclusion, it suffices to prove that for ,

| (30) |

This together with implies that for any ,

By (21) and using Lemma A.4, we have for some positive constant . Then we bound and for any of unit norm. Recalling the lower bound in (25), we have the upper bound for given as

where the last step uses condition 2 of Proposition 4.1. Then using (24) we can check that

Using —concluded from Proposition 4.1—we have for any of unit norm that . Combining these bounds with for , we conclude (30). ∎

A.13.2 Proof of Theorem 5

Appendix B Additional simulation results

This section includes additional simulation results mentioned in Section 5.

B.1 Case 1

Figure 6 displays the mean type-I error for each coordinate over 1000 simulations in Case 1. It exhibits a similar pattern to that shown in Figure 2. We also plot the mean type-I error in the first and second coordinates over 1000 simulations in Figure 7. Compared with case 2 shown in Figure 3, where MW has an inflated type-I error for the first coordinate, here the MW estimator is more accurate, though still performing slightly worse than the Hadamard-t estimator. We also observe that the Hadamard-t estimator is more accurate compared with the MW estimator for larger , as also reflected by MAD reported in Figure 6.

B.2 Case 2

It is observed from Table 2 and Figure 9 that the jackknife estimator performs poorly. The performance of KSS is similar to that of the Hadamard-t estimator.

| Method \ Dimension | 100 | 200 | 300 | 400 | 500 | 600 | 700 | 800 |

|---|---|---|---|---|---|---|---|---|

| MW | 0.072 | 0.080 | 0.088 | 0.100 | 0.081 | 0.100 | 0.082 | 0.071 |

| Hadamard | 0.067 | 0.070 | 0.064 | 0.060 | 0.051 | 0.059 | 0.0560 | 0.056 |

| Hadamard-t | 0.063 | 0.067 | 0.061 | 0.058 | 0.045 | 0.056 | 0.048 | 0.040 |

| jackknife | 0.061 | 0.053 | 0.031 | 0.030 | 0.011 | 0.009 | 0.003 | 0.000 |

Figure 10 illustrates the bias in estimating the MSE of the OLS estimators in Case 2. We observe the same pattern as in Case 1, where the MW and Hadamard estimator have comparable performance and both are much better than the White estimator.