Bootstrap Based Inference for Sparse High-Dimensional Time Series Models

Abstract

Fitting sparse models to high-dimensional time series is an important area of statistical inference. In this paper we consider sparse vector autoregressive models and develop appropriate bootstrap methods to infer properties of such processes. Our bootstrap methodology generates pseudo time series using a model-based bootstrap procedure which involves an estimated, sparsified version of the underlying vector autoregressive model. Inference is performed using so-called de-sparsified or de-biased estimators of the autoregressive model parameters. We derive the asymptotic distribution of such estimators in the time series context and establish asymptotic validity of the bootstrap procedure proposed for estimation and, appropriately modified, for testing purposes. In particular we focus on testing that large groups of autoregressive coefficients equal zero. Our theoretical results are complemented by simulations which investigate the finite sample performance of the bootstrap methodology proposed. A real-life data application is also presented.

keywords:

arXiv:0000.0000

, and

1 Introduction

Statistical analysis of high-dimensional time series has attracted considerable interest during the last decades. Initiated by developments in the i.i.d., mainly regression, set-up, statistical methods have been proposed to select and to estimate non-zero parameters in the context of sparse high-dimensional time series models by means of regularized-type estimators. To be more specific, consider a dimensional stochastic process , where the random vector is generated via a th order vector autoregressive (VAR()) model,

| (1) |

Here , , are coefficient matrices while the ’s are assumed to be independent and identically distributed (i.i.d.) innovations with , in short, . Assume that the process is stationary and causal, that is for all , where . Model (1) has unknown parameters in the matrices and unknown parameters in the innovation covariance matrix . Hence the total number of unknown parameters is . Suppose that a time series stemming from has been observed. If the number of parameters is small in the sense that , then inference for such processes is a well developed and well understood area in multivariate time series analysis; see among others, Reinsel, (2003); Lütkepohl, (2007); Tsay, (2013) and Kilian and Lütkepohl, (2017).

In this paper we consider the important case where but the VAR(d) model (1) possesses some form of sparse representation, that is many of the parameter coefficients are equal to zero. To elaborate, we first fix some notation. For a random variable we write for , where ; for a vector , , and . Furthermore, for a matrix , , , where denotes the vector with the one appearing in the th position. Denote the largest eigenvalue of a matrix by and . Using this notation, let and be the number of non-zero coefficients in the th row, respectively, in the th column of the matrices , , and, let . In the following we consider the case where the VAR(d) model is sparse, that is the total number of non-zero coefficients within a row or column satisfies . Furthermore, we allow to depend on , that is, can be an increasing function of the dimension of the process under consideration.

In the setting described above, procedures to fit sparse VAR models have been considered by many authors in the literature by means of regularized type estimators; see among others, Song and Bickel, (2011) for -penalized least squares (lasso) estimators, Han et al., (2015) for -penalized Yule-Walker estimators, Kock and Callot, (2015) for oracle type inequalities for adaptive lasso estimators and Davis et al., (2016) for a two step procedure which includes -penalized likelihood estimators. Consistency of -penalized estimators has been established for a specific sparsity setting by Basu and Michailidis, (2015), while Lin and Michailidis, (2017) considered estimation for multi-block high-dimensional VAR models including testing of Granger-causality. However, and despite the progress made in fitting sparse VAR models, statistical inference for such models seems to be a less developed area. This is probably due to the fact that the asymptotic distribution of -penalized estimators is difficult to derive and statistical inference is much more involved and difficult to implement. Notice that even in the i.i.d. regression set-up with fixed dimension, the limiting distribution of regularized lasso estimators has been shown to be nonstandard and one which assigns positive probability mass at zero to the zero coefficients; see Knight and Fu, (2000). This leads, among other things, to inconsistency of standard, model-based bootstrap methods; Chatterjee and Lahiri, (2010); see also Chatterjee and Lahiri, (2011) for a different consistent bootstrap proposal in the high-dimensional i.i.d. regression setting.

In this paper we focus on the development of bootstrap procedures for inferring properties of high-dimensional, sparse VAR() processes. Toward this goal and in order to avoid potential problems associated with nonstandard limiting behaviour of regularized lasso estimators, we propose to bootstrap de-biased or de-sparsified estimators of the VAR parameters. De-sparsified estimators of sparse estimators obtained by lasso regularization, have been introduced and investigated in the i.i.d. regression case by several authors. We refer here to the initial paper by Zhang and Zhang, (2014) and to van de Geer et al., (2014), which investigated such estimators in a much more broader setting and established, under certain regularity conditions, asymptotic optimality in the sense of semi-parametric efficiency. In the same i.i.d. regression set-up, de-sparsified estimators have also been used in the context of model based bootstrap inference; see Dezeure et al., (2017) for a discussion and a recent contribution. De-biased estimators in the context of Gaussian respectively sub-Gaussian VAR processes have also been considered in Chaudhry et al., (2017) and have been used for statistical inference and in particular for testing Granger causality. Furthermore, de-sparsified estimators (or versions of it) were used to do inference for systems of high-dimensional regression equations which included VAR systems. Chernozhukov et al., (2018) show a near oracle inequality for the lasso estimator under a rather general set-up which goes beyond sub-Gaussian innovations. They also do inference by using the bootstrap but they focus on simultaneous equation systems; see in particular Example 2 in Chernozhukov et al., (2018). Thus the inference set-up consider by these authors does not include VAR processes. Neykov et al., (2018) discusses a de-sparsifying approach for Gaussian systems. They construct an influence function by projecting the fitted estimating equations to sparse directions. The resulting de-sparsifying approach is more general in the sense that it can be also applied to nonlinear models. For linear models, like VAR models, estimation of these sparse directions correspond to the CLIME estimator, see Cai et al., (2011). Hence, besides Gaussianity, an important assumption of this approach is that the inverse lag-zero autocovariance matrix of the (stacked) VAR system is sparse. This sparsity is also assumed in Zheng and Raskutti, (2018) who adapt the de-sparsifying approach of Ning et al., (2017) to VAR processes. The innovations are assumed to be componentwise independent, that is, their covariance matrix is diagonal. As we will see in Section 2.1, a sparse VAR system does not necessarily imply that the inverse lag-zero autocovariance matrix is sparse. Hence, such an assumption might be more restrictive in the time series context than it is in the i.i.d. regression set up. We propose here a de-sparsifying approach which makes use of the underlying VAR structure and does not required sparsity of the inverse of the lag-zero autocovariance matrix of the process.

Our work extends and generalizes the aforementioned contributions in many directions. In particular, we consider de-sparsified, respectively de-biased, estimators for the general VAR() process and we derive their limiting distribution under quite general conditions on the process and on the stochastic properties of the, not necessarily Gaussian, innovations. We impose sparsity assumptions only on the VAR coefficient matrices and on the innovation covariance matrix (or on its inverse), but we do not impose sparsity assumptions directly on the autocovariance structure of the VAR() process. Furthermore, we introduce a novel and valid bootstrap procedure for inferring properties of the parameters of the VAR() process. Appropriately modified, this bootstrap procedure also allows, for testing statistical hypotheses about groups of model parameters in a very flexible way, where the total number of hypotheses tested is also allowed to increase to infinity with the sample size .

We first derive the limiting distribution of de-sparsified estimators for the parameters of a general, stationary VAR() process. We show that this limiting distribution is a regular Gaussian distribution which is solely affected by the autocovariance structure of the underlying VAR() process. We then propose a bootstrap procedure to estimate the distribution of the de-sparsified estimators of the VAR parameters. This procedure uses an appropriately thresholded -penalized estimator of the coefficient matrices and a thresholded, sparse estimator of the covariance matrix of the innovations. Thresholding is important in this context, since it guaranties sparsity of the VAR model used in the bootstrap world. The fitted sparse VAR model driven by appropriately generated i.i.d. innovations is then used to generate vector pseudo time series , which appropriately imitate the sparse stochastic structure of the observed time series . We prove consistency of such a bootstrap procedure under general conditions when applied to estimate the distribution of de-sparsified estimators. The results obtained allow for using the bootstrap procedure proposed in order to construct individual or simultaneous confidence intervals and to perform tests of hypotheses about model parameters. In particular, we show how the bootstrap method proposed can be used in order to test the interesting hypothesis that individual or, more importantly, groups of coefficients of the VAR model are equal to zero. For such testing purposes, the bootstrap procedure is appropriately modified so that the sparse VAR model used to generated the pseudo time series satisfies the null hypothesis of interest. Consistency of the bootstrap based testing procedure is established for max-type test statistics. Finally, we demonstrate by means of numerical investigations that the theoretical results established are accompanied by a good finite sample behavior of the bootstrap methodology developed.

The paper is organized as follows. Section 2 introduces de-sparsified estimators for the VAR model parameters and derives their limiting distribution under suitable assumptions on the sparsity of the underlying VAR process and on the consistency properties of the regularized estimators involved. Section 3 introduces the bootstrap procedure proposed and establishes its asymptotic validity for estimating the distribution of de-sparsified estimators and, appropriately modified, for testing hypotheses about model parameters. Asymptotic validity of the bootstrap based test procedure is established. Section 4 is devoted to issues related to the practical implementation and to numerical investigations. We propose a bias correction procedure to improve the finite sample performance of the bootstrap based testing and we present several simulations supporting the good size and power behavior of the bootstrap methodology proposed for difficult inference problems. An application to an interesting real-life data set is also discussed. Auxiliary results and technical proofs are deferred to Section 6.

2 De-Sparsified Estimators of VAR Parameters

2.1 De-sparsified estimators

In this section we present our approach to construct de-biased estimators in the high-dimensional time series context. Towards this we adapt to the time series set-up the basic idea for the introduction of de-sparsified estimators used in the i.i.d. regression context, (see Dezeure et al., (2017)) and make the appropriate modifications. We first fix some additional notation. Let be the matrix obtained from the identity matrix of dimension after deleting its -th row. For a matrix , is its element and its -th row after deleting the element .

Observe first that if , then the standard least squares estimator of obtained by regressing onto , also can be written as

| (2) |

where are the “residuals” obtained as the difference between and its best (in mean square) linear approximation using all other variables contained in the lagged vector . also can be expressed as , where , with the sample covariance matrix of and which is given by , ; see also Lemma 16.

Clearly, in the high-dimensional set-up, that is if , such a construction is not possible since in this case , due to the fact that the row vector is an element of the subspace spanned by To overcome this problem in the i.i.d. regression set-up, the approach followed is to replace the estimator appearing in the definition of the residuals , by some regularized estimator. This approach requires the imposition of sparsity assumptions on the corresponding vector of coefficients , that is on the inverse of the covariance matrix . However, in the sparse VAR time series set-up considered in this paper, such an approach seems not to be appropriate. The reason for this lies in the fact that due to temporal dependence, sparsity of the matrices and respectively , does necessarily imply sparsity of the autocovariance matrices respectively . In fact, even in the simple VAR(1) case, the corresponding model parameter matrices and may be sparse but respectively may not. For the same case observe that if is symmetric then by properties of the Neumann-series it can be shown that for the inverse of the covariance matrix it yields that , which implies certain restrictions on the sparsity conditions one has to impose on and on , respectively , in order to achieve the desired sparsity properties of . Thus imposing, in the sparse VAR time series set-up, sparsity assumptions directly on the autocovariance matrices respectively on its inverse, is difficult to justify and may implicitly restrict the class of VAR(d) processes considered. For these reasons, the sparsity behavior of the VAR(d) process is handled in this paper by imposing sparsity assumptions directly on the process parameter matrices and on , respectively, on . Because of this, and in order to construct de-sparsified estimators, an alternative approach to the one used in the i.i.d. regression set-up has to be followed.

To elaborate, recall that is an estimator of and that if , then least squares leads to the estimation of by the sample covariance . Clearly is not a consistent estimation of (or of its inverse) if . Thus a suitable estimator of has to be used which satisfies certain consistency properties in the high-dimensional sparse time series setting considered. We will discuss later on the construction of such an estimator which we will denote by . Given such an estimator, we can then construct our “residuals” as where now is defined by We then have

Since in the case considered, the “residuals” are not perfectly orthogonal to , the last term above is non-zero. Consequently a bias in the expression for appears which, however, can be estimated using some (regularized) estimator of which satisfies certain consistency properties, to be discussed later on. Given such an estimator, which we denote by , we can then estimate the bias term in the last displayed expression. Subtracting the estimated bias from we obtain the following de-biased estimator of

| (3) |

where . The estimator given above is called a de-biased, respectively, a de-sparsified estimator of since it is a bias corrected version of the initial estimator and it is not sparse anymore.

We now discuss the estimators and used in the above construction of the de-biased estimators . Suitable candidates for in the sparse VAR setting are the adaptive lasso estimator Kock and Callot, (2015); see also Chernozhukov et al., (2018) and the discussion following equation (6) below. Such an estimator for the th row of is obtained as

| (4) |

where are the lasso estimators of obtained as and is a regularized parameter.

Estimation of the covariance matrix is more involved. Recall first that for a stable VAR(1) process with coefficient matrix we have . This expression can be generalized to a VAR(d) process using its stacked VAR(1) representation, i.e., the representation ; see Appendix A for the definition of and . This representation leads to the expression

| (5) |

The above expression suggest that a consistent estimator of can be obtained by plugging in (5) estimators , and of the coefficient matrices , and of the covariance matrix , respectively, provided these estimators satisfy certain consistency properties.

To elaborate on the construction of the estimator , as expression (5) shows, consistency of at a desired rate, requires consistency at an appropriate rate of and of . That is, we need to control the error made in estimating the coefficients in the rows and in the columns of the matrices , , taking into account that the dimension of these matrices is allowed to increase to infinity with . These considerations motivate the following estimator of :

| (6) |

, . Here is the adaptive lasso estimator (4), see also Kock and Callot, (2015), is the regularized Yule-Walker type estimator, see Han et al., (2015) and is a threshold parameter. Notice that the regularized Yule-Walker estimator of the th column of the matrix is obtained as

| (7) |

where , and is a regularization parameter. To further elaborate on the motivation leading to the estimator (6), observe that it is obtained by using the combined support of two initial estimators, that is of and of . This is done in order to achieve a desired row- and columnwise -consistency of the estimator respectively of , . In particular, Kock and Callot, (2015) obtained under some conditions which include Gaussian innovations, that the row-wise -error of the adaptive lasso has the rate . Recall that the adaptive lasso is build up row-wise and therefore, without any further restrictions, the column-wise estimation error cannot be controlled by this estimator. This is why the support of in (6) is also estimated by thresholding the second estimator, . Han et al., (2015) showed that, under some conditions which also include Gaussian innovations, , where this rate refers to the column-wise estimation error. Therefore, estimator (6) allows for the control of both errors made in estimating the coefficients of the parameter matrices , .

To estimate the innovation covariance matrix , several approaches exist which depend on the sparsity assumptions one wants to impose on ; see Pourahmadi, (2013) for a discussion in the i.i.d. setting. If one imposes sparsity assumptions on then Bickel and Levina, (2008), El Karoui, (2008), Cai and Liu, (2011), see also Lemma 14, provide some thresholding-based approaches for estimating . If the sparsity assumptions are imposed on , we refer to Cai et al., (2016), and if one solely requires that , to Ledoit and Wolf, (2012) for approaches to estimate the corresponding covariance matrix.

We elaborate here on the case where sparsity assumptions are imposed on . Let , be the estimated residuals and assume that and . For let and

| (8) |

where denotes the element of ; see Lemma 14 for properties of the estimator and more specifically that this estimator satisfies Assumption 1(iv) of the next section. In particular, it is shown in this lemma, under the assumption of Gaussian innovations , that . The results of Bickel and Levina, (2008), Section 2.3 and El Karoui, (2008), indicate that for the non-Gaussian case slower rates should be expected. However, Cai and Liu, (2011) showed that with a more refined thresholding strategy the same rate can also be obtained in the non-Gaussian i.i.d. case. They suggest using individual thresholding values instead of applying an universal thresholding parameter. A simple modification of (8) taking their considerations into account leads to where .

Note that if the estimators are such that the matrix polynomial has all its roots outside the unit disc, i.e. , and if is positive definite, then is positive definite and the estimator is well defined. Furthermore, given estimators , and , an alternative estimator of the autocovariance matrix of interest can be obtained as

| (9) |

is the spectral density matrix of the estimated VAR(d) process. In the following we will focus on the estimator based on expression (5).

2.2 Asymptotic distribution of de-sparsified estimators

To derive the asymptotic distribution of we first observe that by substituting expression , in (3), that this estimator can be written as,

| (10) | ||||

Representation suggests that asymptotic normality of the de-sparsified estimator, more precisely of can be established, due to the contribution of the second term on the right hand side of (10) and the asymptotic negligibility of the last term since this term depends mainly on the estimation error . Theorem 1 below confirms that this intuition is indeed true. However, to state precisely this theorem, we impose some conditions on the underlying VAR process, on its sparsity as well as on the consistency properties of the estimators involved in the construction of the de-sparsified estimator .

Assumption 1.

-

(i)

, and .

-

(ii)

There exists a such that and for any ,

-

(iii)

The estimator used in estimating the bias term in (3) satisfies

while the estimator used in estimating satisfies the above condition regarding the norm and additionally that

-

(iv)

.

-

(v)

.

-

(vi)

for all for some such that and .

Notice that appearing in the above expressions is an increasing function of the dimension which is allowed to be different from expression to expression.

Some comments on the above assumptions are in order. The first two statements of Assumption 1(i) refer to the sparsity behavior of the coefficient matrices . According to this assumption, is the maximum number of non-zero coefficients that can appear in each row, respectively, in each column of the matrices . This implies that which is a much more flexible sparsity setting for VAR(d) models compared, for instance, to the one used in Basu and Michailidis, (2015) and which requires that . Notice that increasing the dimension of the VAR(d) process means that new time series are included. If none of these new time series is a white noise processes, then the number of non-zero parameters will increase by at least the same order as the dimension of the process increases. Therefore, the requirement that , together with the assumption of Gaussianity, essentially means that only i.i.d. processes can be added to the vector if its dimension increases with . The third statement of Assumption 1(i) refers to the sparsity of the innovation covariance matrix . They have to be modified appropriately if one prefers to put sparsity assumption on the inverse matrix .

Assumption 1 imply that the VAR model considered is stable and further satisfies some kind of uniformity regarding the decay behavior of the coefficient matrices . This assumption seems necessary because the dimension of the process is allowed to increase to infinity with . To elaborate, let for simplicity . Then it is well known that , where are the coefficient matrices appearing in the infinite order causal, moving average representation of . Furthermore, these coefficients decrease exponentially fast to zero, that is , for and for some constants and , which will eventually vary when the dimension of the process changes. This situation is taking care off in Assumption 1(ii) which controls the decay rate of by the same constant .

Assumption 1(iii) states the required row wise consistency rates for the estimator and the row- and column wise consistency rates of . Notice first that as this assumption shows, we can choose to be the same estimator as , where the latter estimator is given in (6). Furthermore, and as we have already mentioned in the discussion following equation (6), under Gaussian assumptions on the innovations , the estimator satisfies by construction the required consistency rates with respect to both norms. Observe that we left unspecified since its particular form depends, among other things, also on the distribution of the i.i.d. innovations. As already mentioned, for Gaussian innovations, Kock and Callot, (2015) showed under standard lasso conditions that the corresponding estimators of satisfy the rates of Assumption 1 with the function given by . Similarly results hold also for the sub-Gaussian case, see Zheng and Raskutti, (2018) and Chernozhukov et al., (2018). If the distribution of the i.i.d innovations possesses has only a limited number of finite moments, Chernozhukov et al., (2018) pointed out that drops to a polynomial rate; see among others Comment 5.4 of the aforementioned paper.

Assumption 1(iv) refers to the consistency rates of the estimator . Notice that as Lemma 14 shows, the thresholded estimator given in (8) satisfies under the imposed sparsity assumptions and for Gaussian innovations the consistency condition stated in this assumption. Assumption 1(v) controls the grow rates of inverse of the stacked covariance matrix . Note that the stacked covariance itself is affected by the increasing number of non-zero elements and but the inverse is also affected by the smallest eigenvalue of . Assumption 1(vi) imposes a moment condition on the innovations and specifies its effect on the allowed growth rates of the sparsity behavior of the VAR process when the dimension of the process increases with .

We now state a result which establishes asymptotic normality of the de-sparsified estimators given in (3).

Theorem 1.

The following lemma deals with the limiting covariance of the same estimators.

Lemma 2.

Under the conditions of Theorem 1 we have for any , and , that as ,

| (12) |

3 Bootstrap Based Inference for Sparse Vector Autoregressions

3.1 Bootstrapping de-sparsified estimators

Due to their regular limiting distribution, de-sparsified estimators can be used as a vehicle for statistical inference for sparse VAR() models. In this section we introduce a bootstrap procedure for this purpose. Note that in contrast to the i.i.d. regression setting, in the VAR() setting considered in this paper, the “regressors” , i.e. the vectors are not fixed; they are dependent random vectors. In order to capture the randomness and the dependence properties of these vectors, an appropriate bootstrap procedure has to be applied, which uses an estimated and sparsified version of the underlying VAR model to generate pseudo time series . This pseudo time series can then be used to infer properties of using the estimated distribution of .

A standard procedure to bootstrap a VAR process in the finite, low dimensional case, is to estimate the model and to generate pseudo time series by using the estimated model structure and by drawing with replacement from the estimated set of residuals. However, this procedure fails in the high-dimensional case. To elaborate, let be the centered, estimated residuals of a VAR fit. If the pseudo innovations are obtained by drawing with replacement from the set , then However, it is well known that the sample covariance matrix is not a valid estimator of in the high-dimensional case. Thus, such a bootstrap approach would fail to appropriately mimic the second-order properties of the time series at hand. To tackle this problem, a different strategy is proposed. To elaborate note first that as Theorem 1 shows, the limiting distribution of the de-sparsified estimators is not affected by the distribution of the ’s but solely by their second order properties, that is by the covariance matrix . Thus, we generate the pseudo innovations as Gaussian random vectors with covariance matrix . The estimator is consistent in the high-dimensional setting which ensures that generated in this way will correctly mimic the second-order properties of the true innovations . Notice that instead of the Gaussian distribution any other distribution could be used as well, provided this distribution possesses at least moments. Furthermore, using the Gaussian distribution to generate the pseudo innovations, does not affect the asymptotic validity of the bootstrap procedure proposed in the sequel, when this procedure is applied to estimate the distribution of the de-sparsified estimators and to perform tests for groups of coefficients.

Apart from using the Gaussian distribution with covariance matrix to generate the pseudo innovations, the thresholded estimators given in (6) are used to generate the pseudo time series. This enables the bootstrap generated pseudo time series to appropriately mimic the dependence and the sparsity properties of the underlying VAR() model. Note that thresholding is important in the sparse high dimensional context since it guarantees sparsity of the VAR model used in the bootstrap world. Using the aforementioned estimators and , the generated pseudo time series stems from a VAR() model which has as its lag-zero autocovariance matrix. Recall that the estimator given in (6), selects the non-zero components of the matrices by means of thresholding two initial estimators. Notice that, as we will see, consistency of this estimator as well as a bounded row- and column-wise support property is sufficient for validity of the bootstrap procedure proposed. More specifically, and as a careful inspection of the proof of Theorem 3 below shows, a full sign recovery, which will require a minimal signal strength condition on the coefficients , is not needed. Notice that under such an additional minimal signal strength condition, consistent estimation of the support of , , also can be established; see Theorem 7 of Kock and Callot, (2015) and Corollary 1 of Han et al., (2015). Lack of such a minimal signal strength condition does not affect the consistency and the aforementioned row- and columnwise boundedness properties of the estimators , which are used for the bootstrap.

The bootstrap algorithm proposed consists of the following four steps.

-

Step 1: Generate i.i.d. pseudo innovations from .

-

Step 2: Generate a pseudo time series using the model equation

and some starting values .

-

Step 3: Let be the same de-sparsified estimator of as the estimator given in , but based on the pseudo time series .

-

Step 4: Approximate the distribution of by that of the bootstrap analogue .

Validity of the bootstrap procedure in approximating consistently the distribution of de-sparsified estimators is established in the following theorem, where Mallow’s metric is used to measure the distance between two distributions. For two random variables and , Mallow’s distance between their distributions is defined as where and denote the cumulative distribution functions of and , respectively; see Bickel and Freedman, (1981).

Theorem 3.

Suppose that Assumption 1 is fulfilled. Then, we have for all and , that as ,

| (13) |

The next corollary establishes validity of the corresponding studentized distributions as well.

Corollary 4.

Under the assumptions of Theorem 3 we have, as , that

| (14) |

where

| (15) |

and

| (16) |

Here and denote the same quantities as and but based on the bootstrap pseudo time series . The estimator is the th diagonal entry of the estimator used in of the bootstrap algorithm.

The last result of this section shows that the bootstrap version of the de-sparsified estimators considered, also can be used to consistently estimate the covariance of the de-sparsified estimators of the coefficients and . Its proof follows along the same lines as the proof of Lemma 2 and uses arguments similar to those applied in the proof of Theorem 3.

Lemma 5.

3.2 Testing statistical hypotheses

Appropriately modified, the bootstrap procedure proposed also can be used in order to test hypotheses of interest regarding the dependence structure of the underlying VAR() model, like for instance, testing that a subset of the parameters of the VAR model is zero. To elaborate, let be a subset of indices and consider the following testing problem:

-

:

, for all .

-

:

There exists at least one such that .

We assume in the following that the restrictions on the parameter space imposed by the above null and alternative hypotheses, do not violate the causality of the underlying VAR() model, that is, we assume that the condition for all , is satisfied under and under .

In order to test the above hypotheses and to avoid problems associated with inverting large scale covariance matrices, we propose to use the max-type test statistic

| (18) |

For small, let be the upper -quantile of the distribution of under the assumption that the null hypothesis is true. is then rejected if . Critical values of the test can be obtained using the model-based bootstrap procedure proposed in this paper. For this, the estimated and sparsified VAR model used to generate the pseudo time series is modified in such a way that it satisfies the null hypothesis. This is important for a good size and power behavior of the bootstrap based test. To achieve this goal, the parameter matrices , , are estimated under the restrictions imposed by the null hypothesis, that is under the constrains for all indices . Using these restrictions on the matrices , the bootstrap algorithm proposed in Section 3.1 is then applied to generate pseudo time series from which the bootstrap analogue of under validity of is calculated and which is given by

| (19) |

Let be the upper -quantile of the distribution of . The bootstrap based test proceeds then by rejecting if . As the following theorem shows, the bootstrap succeeds in consistently estimating the distribution of under the null, justifying, therefore, the use of the bootstrap critical values for performing the test.

Theorem 6.

If Assumption 1 under validity of the null hypothesis is fulfilled then, as ,

| (20) |

where denotes the distribution function of when is true.

We can extent the applicability of the bootstrap procedure proposed also to the case where the set of null hypotheses considered increases to infinity, at an appropriate rate, as increases to infinity. To state this dependence on the sample size, we write for . We then have the following theorem.

Theorem 7.

Let such that . Then under the assumptions of Theorem 6 we have that, as ,

4 Numerical Results

We investigate the finite sample performance of the bootstrap procedure proposed to infer properties of the sparse VAR model by means of simulations and we also discuss a real-life data application. Notice that we can use our bootstrap procedure to construct confidence intervals for the coefficients of the VAR model as well as to perform tests of statistical hypotheses about the VAR parameters. In this section, we focus on the problem of testing hypotheses about groups of model parameters.

All results presented in this section are based on implementations in R, (R Core Team,, 2018), of the procedures proposed in this paper. In the simulations as well as in the real-life data example, the estimator of is based on the adaptive lasso; see Section 4 in Kock and Callot, (2015). To simplify calculations we do not make use of the second estimator appearing in (6). The reason for this is that the adaptive lasso estimates showed a very good finite sample performance regarding both norms, that is the and the norm and no tendency towards an out of scale increasing of the column-wise support has been observed. Moreover, in preliminary simulations we found that the adaptive lasso estimator was not outperformed by the combined estimator (6) and the latter estimator was computationally much more demanding. Thus the estimator used in our simulations, was obtained by thresholding the adaptive lasso estimator with tuning parameter and threshold parameter . The same estimator was used for the construction of the de-sparsified estimators in the bootstrap procedure. The Bayesian Information Criterion (BIC) has been used to select the tuning parameter . More specifically, the adaptive lasso implementation with BIC selection of of the HDeconometrics package, Garcia et al., (2017), which uses the glmnet package, Simon et al., (2011), has been applied. Finally, the covariance matrix of the innovations has been estimated using (8), where the threshold parameter has been chosen by cross-validation and using the implementation of Yan and Lin, (2016).

In our numerical investigations, we have experienced that in situations where the set of hull hypotheses is considerably large, that is, is of the same order as , the bootstrap-based test and despite its consistency, seems to be somehow conservative. This is due to a finite sample bias appearing in estimating the upper percentage point of the distribution of under . To improve the finite sample behavior the bootstrap based test, and inspired by Efron, (1981) for the construction of confidence intervals, see also Efron and Tibshirani, (1993), Section 14.3, we adapt to the testing context a bias correction procedure. This procedure is described in more detail in Appendix B of the Supplement Material and leads to the following bias-corrected bootstrap percentage point , where is the distribution function of the standard normal and . Notice that estimation of the quantity used in this bias correction procedure requires the implementation of a second bootstrap experiment; see Appendix B for more details.

4.1 Simulations

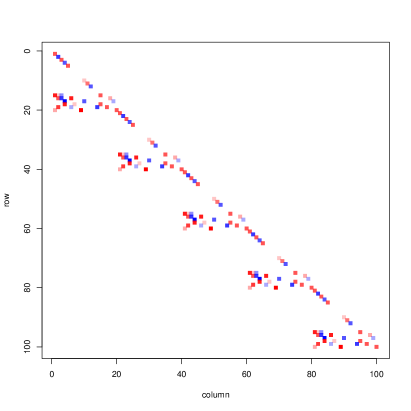

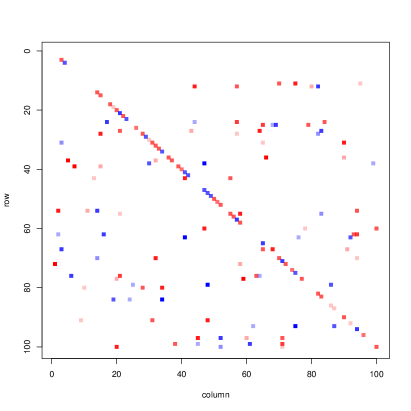

Example 1: We generated time series from the VAR(1) model, , with i.i.d. , where the coefficient matrices and possess a cluster (or block) structure. That is, only the coefficients within a small number of clusters are allowed to be different from zero; see also Han et al., (2015) for the use of such VAR models. Each block is of size and is given by the matrices and in Appendix C. Four entries on the main diagonal of are specified by the choice of the parameter . This parameter controls in some sense the level of dependence of the generated VAR model obtained. Two values and are considered, which lead to the maximal absolute eigenvalues and , respectively, of the coefficient matrix . Note that the information that possesses a cluster structure was not used in the subsequent inference procedure. Therefore, the same results could be obtained for the case where the indices are shuffled randomly; see Figure 1 for an illustration of the matrix and of a randomly shuffled version. The dimension of the VAR process is set equal to and where the case results in a single cluster.

Let be the first set and be a second set of indices which correspond to the upper-right corner of the matrix . Note that while . We consider for , the testing problem,

-

:

for all , against

-

:

There exists such that .

For , corresponds to the case that the time series belonging to the first cluster, that is, are not directly influenced by the set of lagged time series belonging to the last cluster. A similar interpretation occurs for in which corresponds to the case where the first ten time series are not directly influenced by the last ten lagged time series. For only the case is considered since for the corresponding null hypothesis is that is a white noise process. We investigate the performance of the bootstrap based test under the null as well as its power against various alternatives. The alternatives considered refer to the case where only one coefficient in the set is set different to zero and equal to . Notice that corresponds to the null hypothesis. The results obtained for repetitions and bootstrap replications are presented in Table 1 (size) and Table 2 (power).

As Table 1 shows, the bootstrap-based test without the proposed bias correction, seems to be conservative in most of the cases and the differences between the empirical and the nominal level increase as the size of the set increases. The degree of persistence as well as the dimension of the process seem not to affect the size behavior of the test. However, using the bias correction, the behavior of the bootstrap-based test improves considerably for all sizes of the set considered. Table 2 presents the empirical power of the bootstrap based test. As it can be seen, in all settings considered, the bias correction improves the power behavior of the test, where (as expected) the test is more powerful for the set than for the more larger set . Notice that for the sample size of observations, detecting the deviation from the null which is due to the fact that only one out of the elements is set equal to , is a very challenging inference problem. However, even in this case, the test has power and its power improves considerably as the sample size increases. Finally, as in the case of the size, the dimension of the VAR process seems to affect only slightly the power of the test.

| 20 | 100 | 200 | 100 | 200 | |||||||

| 0.05 | 0.10 | 0.05 | 0.10 | 0.05 | 0.10 | 0.05 | 0.10 | 0.05 | 0.10 | ||

| With Bias Correction | |||||||||||

| 128 | 0.7 | 0.04 | 0.08 | 0.05 | 0.11 | 0.03 | 0.07 | 0.05 | 0.11 | 0.03 | 0.06 |

| 0.9 | 0.04 | 0.10 | 0.05 | 0.10 | 0.05 | 0.10 | 0.04 | 0.10 | 0.05 | 0.09 | |

| 200 | 0.7 | 0.04 | 0.10 | 0.05 | 0.11 | 0.06 | 0.09 | 0.04 | 0.10 | 0.06 | 0.11 |

| 0.9 | 0.06 | 0.12 | 0.05 | 0.10 | 0.05 | 0.12 | 0.06 | 0.12 | 0.04 | 0.09 | |

| Without Bias Correction | |||||||||||

| 128 | 0.7 | 0.03 | 0.06 | 0.03 | 0.08 | 0.02 | 0.05 | 0.03 | 0.06 | 0.01 | 0.04 |

| 0.9 | 0.04 | 0.07 | 0.04 | 0.08 | 0.03 | 0.07 | 0.02 | 0.05 | 0.03 | 0.06 | |

| 200 | 0.7 | 0.04 | 0.08 | 0.04 | 0.10 | 0.05 | 0.08 | 0.02 | 0.07 | 0.04 | 0.08 |

| 0.9 | 0.05 | 0.10 | 0.03 | 0.07 | 0.04 | 0.09 | 0.04 | 0.09 | 0.02 | 0.06 | |

| 20 | 100 | 200 | 100 | 200 | |||||||

| 0.05 | 0.10 | 0.05 | 0.10 | 0.05 | 0.10 | 0.05 | 0.10 | 0.05 | 0.10 | ||

| With Bias Correction | |||||||||||

| 128 | 0.7 | 0.61 | 0.75 | 0.64 | 0.77 | 0.62 | 0.79 | 0.27 | 0.43 | 0.28 | 0.43 |

| 0.9 | 0.61 | 0.74 | 0.62 | 0.79 | 0.61 | 0.78 | 0.25 | 0.41 | 0.18 | 0.32 | |

| 200 | 0.7 | 0.95 | 0.99 | 0.95 | 0.97 | 0.96 | 0.98 | 0.83 | 0.90 | 0.82 | 0.88 |

| 0.9 | 0.95 | 0.99 | 0.96 | 0.98 | 0.96 | 0.98 | 0.82 | 0.89 | 0.76 | 0.88 | |

| Without Bias Correction | |||||||||||

| 128 | 0.7 | 0.51 | 0.68 | 0.52 | 0.68 | 0.50 | 0.68 | 0.15 | 0.25 | 0.12 | 0.24 |

| 0.9 | 0.51 | 0.68 | 0.52 | 0.70 | 0.52 | 0.69 | 0.12 | 0.24 | 0.08 | 0.17 | |

| 200 | 0.7 | 0.93 | 0.97 | 0.94 | 0.97 | 0.94 | 0.96 | 0.73 | 0.85 | 0.73 | 0.82 |

| 0.9 | 0.94 | 0.98 | 0.95 | 0.98 | 0.94 | 0.97 | 0.74 | 0.84 | 0.66 | 0.81 | |

4.2 A real-life data example

In Farmer, (2015) the question has been discussed whether the stock market affects the labor market. In the aforementioned paper, the stock market is represented by the S&P 500 index and the labor market by the unemployment rate, that is, a bivariate time series is used to investigate the question of interest. However, restricting the analysis to a bivariate system might be problematic since it implies a loss of information due to the fact that a variety of time series exist which describe the activities in the two different macroeconomic sectors. The corresponding dependence structures might be much more complicated than those captured by the particular bivariate time series considered. Therefore, and in order to get a more detailed and deeper inside into the relations between the labor and the stock market, we consider the Federal Reserve Economic Data (FRED) of St. Louis Fed’s main, which is publicly available at http://research.stlouisfed.org/fred2/. This data set contains time series describing the activities in the labor market and time series describing the stock market. Furthermore, to take into account the fact that other macroeconomic variables may also exist which simultaneously influence the labor and the stock market, all available time series in the aforementioned data set are considered, which refer to a wide range of different economic activities. The entire data set considered contains time series and a complete description of all time series used is given in Appendix B of this paper. The techniques proposed in McCracken and Ng, (2016) have been adopted to transform this set of time series to stationary. Furthermore, to ensure comparability of the data used in our analysis with the data set used by Farmer, (2015), the monthly observations have been aggregated to quarterly data where the time period considered begins by the fourth quarter of 1979 and ends by the first quarter of 2011. The number of available observations is then equal to . As already mentioned, the question of interest is whether the financial sector, that is the stock market, influences the labor market. Following Farmer, (2015), a vector autoregressive model of order has been used and the following hypotheses have been considered:

-

:

for all ,

-

:

There exists such that ,

where is the set containing the indices corresponding to the two economic sectors, that is . Here STOCK denotes the set of indices referring to the time series of the stock market and LABOR to the time series of the labor market. Notice that . To test the above pair of hypotheses, the test statistic described in Section 3.2 with bootstrap replications and bias corrected percentage points have been used.

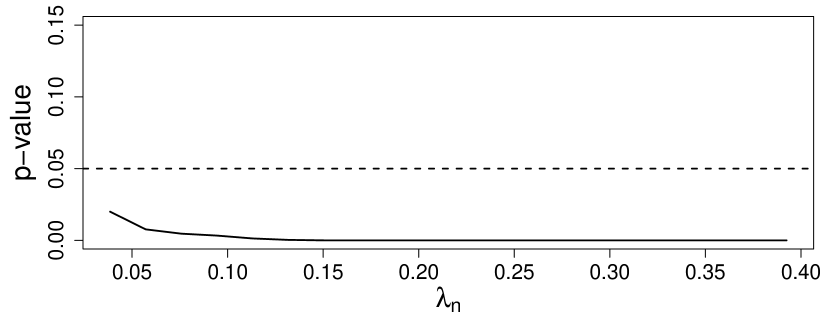

The degree of sparsity obtained depends on the choice of the regularization parameters. As mentioned in the previous section, we use the adaptive lasso with regularization parameter and threshold parameter to estimate the coefficient matrix, while the covariance of the innovations is estimated as in (8), with the threshold parameter chosen by cross-validation. For instance, for we obtain a sparsity in the coefficient matrix of , for the sparsity obtained is and if is chosen by BIC, it leads to a sparsity level of . The p-values of the test seem not to be largely affected by the choice of this regularization parameter. This is demonstrated in Figure 2 where the -values of the bootstrap based test proposed, are shown for different values of the regularization parameter .

As it is seen from this figure, the null hypothesis of interest is rejected at the commonly used level, for all values of considered. If is chosen by BIC, the test gives a p-values of less than . Furthermore, our bootstrap procedure identifies the following coefficients , for and , as different from zero: , , , and . Thus, our analysis leads to the conclusion that the hypothesis that the stock market does not influence the labor market should be rejected. Notice that this conclusion is also supported by the findings reported in Phelps, (1999) and Farmer, (2015).

5 Conclusions

In this paper, high-dimensional and sparse vector autoregressive models have been considered. We have first adopted the concept of de-biasing to the high-dimensional VAR() time series context and have considered de-biased respectively de-sparsified estimators of the autoregressive parameters. The asymptotic distribution of the de-sparsified estimators has been derived under general conditions. Furthermore, a bootstrap procedure has been proposed which is asymptotically able to generate pseudo time series that appropriately imitate the dependence structure and the sparsity properties of the underlying high-dimensional VAR() process. Asymptotic validity of the bootstrap procedure proposed for estimating the distribution of de-sparsified estimators has been established. Furthermore, an appropriately modified version of the bootstrap procedure has been used for testing hypotheses about groups of model parameters. We allow for these groups of model parameters to increase to infinity with sample size. Validity of the bootstrap procedure also has been established for this case. Finally, we have demonstrated by means of numerical investigations, the good finite sample behavior of the bootstrap-based inference procedure proposed and we have analyzed an interesting real-life data set.

6 Proofs

Proofs which are note given in this section are presented in Appendix E of the Supplementary Material.

Lemma 8.

Let be some process generated causally by the i.i.d. processes for some function . Furthermore, denote by the process where is replaced by an i.i.d. copy of it. Furthermore, define the physical dependence coefficients, see Wu, (2005); Zhang and Wu, (2017); Liu et al., (2013), in the following way. Let , , , , and . Furthermore, let .

Lemma 10.

Let be a centered, -dimensional stationary process and let as given in Lemma 8. If

, then

Proof.

Lemma 11.

Proof of Lemma 11.

In order to simplify notation we set . Note that for we have . Using this recursive formula, we obtain Since by Assumption 1(iii), we have .

Since we have by the same arguments . Furthermore, note that Assumption 1(ii) implies and also for We then have .

Using , we have

. For large enough such that , we have

∎

Lemma 12.

Let be the estimator of given by

If , , and for some constant , then , , and .

Proof.

The proof uses ideas similar to those used in the proof of Theorem 1 in Bickel and Levina, (2008). Let , , be the thresholded version of . Since , we have and , which gives the resulting rates for and for , when is thresholded using the thresholding parameter which satisfies . Let be the set of indices for which the entries of the th row of are non-zero. We then have Similarly by the properties of , we have Thus, gives a row-wise and column-wise sparse estimator of . Moreover, The indicator functions ensure that each part consist only of non-zero terms. Due to each non-zero terms is of order and we obtain . In the same way, we obtain and the assertion follows. ∎

Proof.

We proof the assertion for , the other cases can be handled analogously. Denote by a set of indices corresponding to and let for . We have

Proof of Theorem 1: Applying Lemma 13 gives us Furthermore, we have by Lemma 8 that fulfills the conditions of physical dependence, hence . Note further that due to the i.i.d property of we have that is an uncorrelated sequence which gives . Furthermore, Assumption 1(vi) ensures the existence of fourth order moments. Thus a Lyapounov condition can be verified for the sequence , establishing via an extension of the central limit theorem for functional dependent random variables, Theorem 3 of Wu, (2011), to triangular arrays; see also Theorem 27.3 of Billingsley, (1995). Thus the assertion follows by Slutsky’s Lemma.

Proof of Lemma 2: Let and . Note further that due to the i.i.d property of we have that is an uncorrelated sequence. Thus, we have , the assertion follows Lemma 13.

Proof of Theorem 3: Denote by the corresponding quantities in the bootstrap world, that is and . We show that, as , from which the assertion follows by the triangular inequality. To establish the above weak convergence, similar ideas as those used in the proof of Theorem 1 can be applied.

Since and give an sparse estimate, see Lemma 12 and Lemma 14 we have that is a sparse VAR process with Gaussian i.i.d. innovations. Furthermore, due to Assumption 1(ii) and (iii) this process is (asymptotically) causal and we have . Thus, Lemma 9,10, and 8 hold for this processes as well. A regularized estimator similarly as in the construction of but based on the pseudo time series could be used to estimate in the bootstrap world. By Lemma 12 we obtain for , where appears due to the Gaussianity of . Assumption 1(iii) gives . Hence, by the triangular inequality we obtain . Similarly, we obtain by Assumption 1(iv) and Lemma 14. This implies that the estimator which is similarly constructed as in (5) but based on and fulfills by Lemma 11 the rate . This implies Since the Gaussian i.i.d. pseudo innovations fulfill the moment condition of Assumption 1(vi) and the bootstrap analogue of the estimators fulfill the required rates, we obtain by the same arguments as those used in the proof of Theorem 1 that, as , in probability.

Proof of Corollary 4: Follows by Lemma 2 and the arguments used in the proof of Theorem 3 which gives and .

Proof of Theorem 6.

By the Cramér-Wold device and the same arguments as those used in the proof of Theorem 1, it follows that the vector converges weakly to a -dimensional normal distribution with zero mean vector and covariance matrix having components those given in Lemma 2. Then, following the same arguments as those used in the proof of Theorem 3 and by Lemma 5, the same result can be established for the limiting distribution of the bootstrap analogue . The assertion of the theorem follows then by the continuous mapping theorem. ∎

Lemma 14.

Proof.

In order to simplify notation, let . and we assume that we have observations . Note that By Lemma 10 and the convergence rate of , we have that . The same arguments can be applied to . Furthermore, we have by the convergence rate of , that . This establishes (22). In the Gaussian case we have , and from Theorem 1 in Bickel and Levina, (2008) we get that . Note further that . To establish (23), we mainly follow the arguments given in the proof of Theorem 1 in Bickel and Levina, (2008). Since , we have , where denotes the true covariance matrix thresholded with threshold parameter . Let and . Then, Equation (22) and ensures that and . Furthermore, we have for some , that where . Note that and thus, can be bounded analogously as part in the proof of Theorem 1 in Bickel and Levina, (2008). Since , we have . Consequently, and equation (23) follows. Let be the set of indices for which the entries of the th row of are non-zero. Then, for , we have that . ∎

Proof of Theorem 7.

Let and be a set of indices corresponding to . We show this by using first the triangular inequality, thus

where is some appropriate Gaussian process and specified later on. If we can show that the first term is and the second the assertion follows. We begin with the first term. Note that Lemma 13 gives us where . Let . We have where . To see this, note that is an uncorrelated sequence and we have .

Thus, for the process we obtain by Lemma 8 that we have for some , and . For large enough we have . Thus, remark 2 in Zhang and Wu, (2017) can be applied which gives by Theorem 3.2 in Zhang and Wu, (2017) an Gaussian approximation if . This holds by Assumption 1(vi) and the limit on . Applying now Theorem 3.2 in Zhang and Wu, (2017) and using that the other terms are asymptotically negligible we obtain where . In the following we show that Following the arguments used in the proof of Theorem 3 we obtain , and , where the bootstrap analogue of the estimators is denoted by . Hence, Lemma 13 implies , where . Furthermore, we have

if and . Thus, possesses asymptotically the same autocovariance structure as . This implies that Theorem 3.2 in Zhang and Wu, (2017) can be applied in the same way as above to . we obtain ∎

Lemma 15.

Let , where the ’s are i.i.d., and for all . Then, for .

Lemma 16.

Let be some positive definite matrix and , where . Then,

Acknowledgments. The research of the first author was supported by the Research Center (SFB) 884 “Political Economy of Reforms”(Project B6), funded by the German Research Foundation (DFG). Furthermore, the authors acknowledge support by the state of Baden-Württemberg through bwHPC.

References

- Basu and Michailidis, (2015) Basu, S. and Michailidis, G. (2015). Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics, 43(4):1535–1567.

- Bickel and Freedman, (1981) Bickel, P. J. and Freedman, D. A. (1981). Some asymptotic theory for the bootstrap. Ann. Statist., 9(6):1196–1217.

- Bickel and Levina, (2008) Bickel, P. J. and Levina, E. (2008). Covariance regularization by thresholding. The Annals of Statistics, 36(6):2577–2604.

- Billingsley, (1995) Billingsley, P. (1995). Probability and measure. wiley series in probability and mathematical statistics.

- Cai and Liu, (2011) Cai, T. and Liu, W. (2011). Adaptive thresholding for sparse covariance matrix estimation. Journal of the American Statistical Association, 106(494):672–684.

- Cai et al., (2011) Cai, T., Liu, W., and Luo, X. (2011). A constrained l1 minimization approach to sparse precision matrix estimation. Journal of the American Statistical Association, 106(494):594–607.

- Cai et al., (2016) Cai, T. T., Liu, W., Zhou, H. H., et al. (2016). Estimating sparse precision matrix: Optimal rates of convergence and adaptive estimation. The Annals of Statistics, 44(2):455–488.

- Chatterjee and Lahiri, (2010) Chatterjee, A. and Lahiri, S. (2010). Asymptotic properties of the residual bootstrap for lasso estimators. Proceedings of the American Mathematical Society, 138(12):4497–4509.

- Chatterjee and Lahiri, (2011) Chatterjee, A. and Lahiri, S. N. (2011). Bootstrapping lasso estimators. Journal of the American Statistical Association, 106(494):608–625.

- Chaudhry et al., (2017) Chaudhry, A., Xu, P., and Gu, Q. (2017). Uncertainty assessment and false discovery rate control in high-dimensional granger causal inference. In International Conference on Machine Learning, pages 684–693.

- Chen et al., (2013) Chen, X., Xu, M., Wu, W. B., et al. (2013). Covariance and precision matrix estimation for high-dimensional time series. The Annals of Statistics, 41(6):2994–3021.

- Chernozhukov et al., (2018) Chernozhukov, V., Härdle, W. K., Huang, C., and Wang, W. (2018). Lasso-driven inference in time and space. arXiv preprint arXiv:1806.05081.

- Davis et al., (2016) Davis, R. A., Zang, P., and Zheng, T. (2016). Sparse vector autoregressive modeling. Journal of Computational and Graphical Statistics, 25(4):1077–1096.

- Dezeure et al., (2017) Dezeure, R., Bühlmann, P., and Zhang, C.-H. (2017). High-dimensional simultaneous inference with the bootstrap. Test, 26(4):685–719.

- Efron, (1981) Efron, B. (1981). Nonparametric standard errors and confidence intervals. canadian Journal of Statistics, 9(2):139–158.

- Efron and Tibshirani, (1993) Efron, B. and Tibshirani, R. J. (1993). An introduction to the bootstrap. CRC press.

- El Karoui, (2008) El Karoui, N. (2008). Operator norm consistent estimation of large-dimensional sparse covariance matrices. The Annals of Statistics, 36(6):2717–2756.

- Farmer, (2015) Farmer, R. E. (2015). The stock market crash really did cause the great recession. Oxford Bulletin of Economics and Statistics, 77(5):617–633.

- Garcia et al., (2017) Garcia, M. G., Medeiros, M. C., and Vasconcelos, G. F. (2017). Real-time inflation forecasting with high-dimensional models: The case of brazil. International Journal of Forecasting, 33(3):679–693.

- Giacomini et al., (2013) Giacomini, R., Politis, D. N., and White, H. (2013). A warp-speed method for conducting monte carlo experiments involving bootstrap estimators. Econometric theory, 29(3):567–589.

- Han et al., (2015) Han, F., Lu, H., and Liu, H. (2015). A direct estimation of high dimensional stationary vector autoregressions. The Journal of Machine Learning Research, 16(1):3115–3150.

- Kilian and Lütkepohl, (2017) Kilian, L. and Lütkepohl, H. (2017). Structural vector autoregressive analysis. Cambridge University Press.

- Knight and Fu, (2000) Knight, K. and Fu, W. (2000). Asymptotics for lasso-type estimators. The Annals of Statistics, pages 1356–1378.

- Kock and Callot, (2015) Kock, A. B. and Callot, L. (2015). Oracle inequalities for high dimensional vector autoregressions. Journal of Econometrics, 186(2):325–344.

- Ledoit and Wolf, (2012) Ledoit, O. and Wolf, M. (2012). Nonlinear shrinkage estimation of large-dimensional covariance matrices. The Annals of Statistics, 40(2):1024–1060.

- Lin and Michailidis, (2017) Lin, J. and Michailidis, G. (2017). Regularized estimation and testing for high-dimensional multi-block vector-autoregressive models. Journal of Machine Learning Research, 18(1):4188–4236.

- Liu et al., (2013) Liu, W., Xiao, H., and Wu, W. B. (2013). Probability and moment inequalities under dependence. Statistica sinica, pages 1257–1272.

- Lütkepohl, (2007) Lütkepohl, H. (2007). New Introduction to Multiple Time Series Analysis. Springer Berlin Heidelberg.

- McCracken and Ng, (2016) McCracken, M. W. and Ng, S. (2016). Fred-md: A monthly database for macroeconomic research. Journal of Business & Economic Statistics, 34(4):574–589.

- Neykov et al., (2018) Neykov, M., Ning, Y., Liu, J. S., Liu, H., et al. (2018). A unified theory of confidence regions and testing for high-dimensional estimating equations. Statistical Science, 33(3):427–443.

- Ning et al., (2017) Ning, Y., Liu, H., et al. (2017). A general theory of hypothesis tests and confidence regions for sparse high dimensional models. The Annals of Statistics, 45(1):158–195.

- Phelps, (1999) Phelps, E. S. (1999). Behind this structural boom: the role of asset valuations. American Economic Review, 89(2):63–68.

- Pourahmadi, (2013) Pourahmadi, M. (2013). High-dimensional covariance estimation: with high-dimensional data, volume 882. John Wiley & Sons.

- R Core Team, (2018) R Core Team (2018). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Reinsel, (2003) Reinsel, G. C. (2003). Elements of multivariate time series analysis. Springer Science & Business Media.

- Simon et al., (2011) Simon, N., Friedman, J., Hastie, T., and Tibshirani, R. (2011). Regularization paths for cox’s proportional hazards model via coordinate descent. Journal of Statistical Software, 39(5):1–13.

- Song and Bickel, (2011) Song, S. and Bickel, P. J. (2011). Large vector auto regressions. Preprint arXiv:1106.3915.

- Tsay, (2013) Tsay, R. S. (2013). Multivariate time series analysis: with R and financial applications. John Wiley & Sons.

- van de Geer et al., (2014) van de Geer, S., Bühlmann, P., Ritov, Y., and Dezeure, R. (2014). On asymptotically optimal confidence regions and tests for high-dimensional models. The Annals of Statistics, 42(3):1166–1202.

- Wu, (2005) Wu, W. B. (2005). Nonlinear system theory: Another look at dependence. Proceedings of the National Academy of Sciences, 102(40):14150–14154.

- Wu, (2011) Wu, W. B. (2011). Asymptotic theory for stationary processes. Statistics and its Interface, 4(2):207–226.

- Yan and Lin, (2016) Yan, Y. and Lin, F. (2016). FinCovRegularization: Covariance Matrix Estimation and Regularization for Finance. R package version 1.1.0.

- Zhang and Zhang, (2014) Zhang, C.-H. and Zhang, S. S. (2014). Confidence intervals for low dimensional parameters in high dimensional linear models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(1):217–242.

- Zhang and Wu, (2017) Zhang, D. and Wu, W. B. (2017). Gaussian approximation for high dimensional time series. The Annals of Statistics, 45(5):1895–1919.

- Zhang et al., (2018) Zhang, X., Cheng, G., et al. (2018). Gaussian approximation for high dimensional vector under physical dependence. Bernoulli, 24(4A):2640–2675.

- Zheng and Raskutti, (2018) Zheng, L. and Raskutti, G. (2018). Testing for high-dimensional network paramaters in auto-regressive models. arXiv preprint arXiv:1812.03659.

Appendix A: Stacked VAR() processes

In this Appendix we discuss some properties of stacked VAR() processes. The VAR model, , can be written as a VAR model , where

is stable if is stable; see Section 2.1 in Lütkepohl, (2007). Hence, in this case we also have the representation which gives , where . Note that a VAR(1) process with coefficient matrix is stable if , where denotes the maximal absolute eigenvalue of , which is equivalent to for all . A VAR process is stable if for all , see Section 2.1 in Lütkepohl, (2007). Furthermore, this still holds for the stacked VAR process, that is, this process is stable if for all . However, for such a stacked coefficient matrix we may have that ; see Lemma E.2 in Basu and Michailidis, (2015). Furthermore, a stable and causal VAR process, possesses the representation , . For a VAR we have .Note that for a VAR process we have . Thus, .

The following example refers to a VAR(1) process with sparse matrices and which possess a non-sparse lag zero autocovariance matrix .

Example 17.

Consider the VAR(1) process with and where , , , and elsewhere. Then, is sparse and each row contains only one non-zero entry, namely . For , the VAR(1) process is causal. However, all elements of the lag-zero autocovariance matrix are different from zero which also holds for the inverse. Notice that these non-zero entries can be small for large and for the parameter not close to the boundaries respectively . The magnitude of the non-zero entries can be increased for or , if additionally a non-diagonal or is chosen, respectively.

Appendix B: Bias-corrected bootstrap percentage points

Suppose we have data and we want to test against , where is some parameter of interest. Suppose that to perform the test, a test statistic is used which rejects if , where is the upper -percentage point of the distribution of under . A bootstrap-based test works by generating pseudo data under and calculating the upper -percentage point of the distribution of , where is the same statistic as but based on . That is,

| (24) |

where denotes the distribution of function of the standard Gaussian random variable, , the distribution function of and the quantile function of the same random variable.

Suppose now that is a sample of pseudo random variables generated under and using a second bootstrap experiment which is based on . Let be the test statistic of interest calculated using . Assume now that the following assertions are true.

-

1.

There exists a monotone increasing function such that

-

(i)

.

-

(ii)

, (Recall that stems from a bootstrap experiment based on the observed data ).

-

(iii)

, (Recall that stems from a bootstrap experiment based on the bootstrap sample ).

-

(i)

-

2.

It holds true that .

The essential motivation behind the above assumptions is that the second bootstrap experiment which leads to the bootstrap sample , should imitate the same bias as the first bootstrap experiment leading to . If the above relations hold true, then it can be shown that a bias corrected bootstrap percentage point which can be used for performing the bootstrap based test is given by

Notice that if no bias exist, that is if or , respectively, then the standard bootstrap percentage point (24) is obtained. Furthermore, we can estimate all quantities appearing in the expression for without knowledge of the transformation . An estimator of can be obtained using the following algorithm.

-

Step 1: Generate a pseudo time series under the null using the bootstrap procedure described in Section 3.1.

-

Step 2: Based on , compute the test statistic and compute (under the null) the estimators , and .

-

Step 3: Given the estimators , and , generate pseudo time series and compute the test statistic .

-

Step 4: Repeat Step 3 a number of times, say times, and estimate by , where denote the value of the test statistic calculated using the th pseudo time series, .

To reduce the dependence of the above procedure on the initial time series appearing in Step 1, we apply the above algorithm to generated bootstrap time series and average the estimates obtained. As long as the number of trials in Step 4 is large enough, the outcome is not affected considerably. In the numerical examples of this section we use, for computational reasons, repetitions and set . To reduce the computational burden one can apply the idea of Giacomini et al., (2013), that is a good estimate of can also be obtain by using and a larger number of repetitions.

Appendix C: Data description

| 1 | 2 | 3 | 4 | |

|---|---|---|---|---|

| 1 | RPI | PAYEMS | M1SL | EXUSUKx |

| 2 | W875RX1 | USGOOD | M2SL | EXCAUSx |

| 3 | DPCERA3M086SBEA | CES1021000001 | M2REAL | WPSFD49207 |

| 4 | CMRMTSPLx | USCONS | TOTRESNS | WPSFD49502 |

| 5 | RETAILx | MANEMP | BUSLOANS | WPSID61 |

| 6 | INDPRO | DMANEMP | NONREVSL | WPSID62 |

| 7 | IPFPNSS | NDMANEMP | CONSPI | OILPRICEx |

| 8 | IPFINAL | SRVPRD | S.P.500 | PPICMM |

| 9 | IPCONGD | USTPU | S.P..indust | CPIAUCSL |

| 10 | IPDCONGD | USWTRADE | S.P.div.yield | CPIAPPSL |

| 11 | IPNCONGD | USTRADE | S.P.PE.ratio | CPITRNSL |

| 12 | IPBUSEQ | USFIRE | FEDFUNDS | CPIMEDSL |

| 13 | IPMAT | USGOVT | CP3Mx | CUSR0000SAC |

| 14 | IPDMAT | CES0600000007 | TB3MS | CUSR0000SAD |

| 15 | IPNMAT | AWOTMAN | TB6MS | CUSR0000SAS |

| 1 | 2 | 3 | 4 | |

|---|---|---|---|---|

| 16 | IPMANSICS | AWHMAN | GS1 | CPIULFSL |

| 17 | IPB51222S | HOUST | GS5 | CUSR0000SA0L2 |

| 18 | IPFUELS | HOUSTNE | GS10 | CUSR0000SA0L5 |

| 19 | CUMFNS | HOUSTMW | AAA | PCEPI |

| 20 | HWI | HOUSTS | BAA | DDURRG3M086SBEA |

| 21 | HWIURATIO | HOUSTW | COMPAPFFx | DNDGRG3M086SBEA |

| 22 | CLF16OV | PERMIT | TB3SMFFM | DSERRG3M086SBEA |

| 23 | CE16OV | PERMITNE | TB6SMFFM | CES0600000008 |

| 24 | UNRATE | PERMITMW | T1YFFM | CES2000000008 |

| 25 | UEMPMEAN | PERMITS | T5YFFM | CES3000000008 |

| 26 | UEMPLT5 | PERMITW | T10YFFM | UMCSENTx |

| 27 | UEMP5TO14 | AMDMNOx | AAAFFM | MZMSL |

| 28 | UEMP15OV | ANDENOx | BAAFFM | DTCOLNVHFNM |

| 29 | UEMP15T26 | AMDMUOx | TWEXMMTH | DTCTHFNM |

| 30 | UEMP27OV | BUSINVx | EXSZUSx | INVEST |

| 31 | CLAIMSx | ISRATIOx | EXJPUSx | VXOCLSx |

Appendix D: Simulation set-up

Let and where denotes a null matrix of appropriate dimensions and the submatrices , , and are defined as follows.

Appendix E: Additional proofs

Proof of Lemma 8.

Note that and by Assumption (ii) . Such a VAR(1) process possesses the functional dependence measure for every as given by Example 2.2 in Chen et al., (2013). Thus, for and some we obtain and . We obtain due to . Since and is a nonlinear transformation which preserves the functional dependence, see Wu, (2005), these results can be transferred and we obtain 1. Similarly, we obtain 2. Note here that . ∎

Proof of Lemma 15.

We have and is an i.i.d. sequence. Thus, . Since is summable and , can be made arbitrary small. Furthermore, by Rosenthal inequality as in Example 2.2 in Zhang et al., (2018) we obtain . ∎

Proof of Lemma 9.

Let . We have . Furthermore, by Lemma 15 and due to . Furthermore, Lemma (8) implies . This allows us to use Nagaev’s inequality for physical dependent processes, see Theorem 2 in Liu et al., (2013) and their remark below Theorem 2. Hence, we obtain for some

Since , there exists for every an such that the probability is smaller . ∎

Proof of Lemma 16.

Note that . Thus, we have

∎