Product matrix processes as limits of random plane partitions

Abstract.

We consider a random process with discrete time formed by singular values of products of truncations of Haar distributed unitary matrices. We show that this process can be understood as a scaling limit of the Schur process, which gives determinantal formulas for (dynamical) correlation functions and a contour integral representation for the correlation kernel. The relation with the Schur processes implies that the continuous limit of marginals for q-distributed plane partitions coincides with the joint law of singular values for products of truncations of Haar-distributed random unitary matrices. We provide structural reasons for this coincidence that may also extend to other classes of random matrices.

Key words and phrases:

Products of random matrices, multi-level determinantal point processes, Schur processes, random plane partitions1. Introduction

It was observed by many researchers that probability distributions from random matrix theory appear as limit laws in a variety of problems in statistical mechanics and combinatorics. Probably, the most known examples of this phenomenon are Ulam’s problem for increasing subsequences of random permutations and domino tilings of the Aztec diamond. We refer the reader to the book by Baik, Deift, and Suidan [6] and references therein for a detailed analysis of these two examples.

In both these problems, distributions of certain key quantities converge to limiting distributions of random matrix theory (in an appropriate scaling limit as the size of random matrices tends to infinity), in particular to the Tracy-Widom distribution [44]. However, there are situations where not only limiting random matrix distributions play a role. It can happen that joint laws of eigenvalues (or singular values) corresponding to finite size random matrix ensembles arise as scaling limits in a combinatorial or statistical mechanics problem that has no a priori relation with random matrices.

One example is the GUE-corners process investigated by Johansson, Nordenstam [32] and Okounkov, Reshetikhin [40]. It is easy to define the corners process: start with an infinite random matrix picked from the Gaussian Unitary Ensemble (GUE) and consider the eigenvalues of its principal corner submatrices. As was discovered in [32], [40], the GUE-corners process can be obtained as a scaling limit in tiling models. Okounkov and Reshetikhin further suggested a (heuristic) argument towards the universal appearance of this process. Following this prediction, GUE–corners process was found in more general tilings models by Gorin, Panova [23] and the six–vertex model by Gorin [22] and Dimitrov [18]. It can be also linked to the last passage percolation, see Baryshnikov [7], Gravner, Tracy, Widom [26], O’Connell, Yor [37], Bougerol, Jeuli [14], Adler, van Moerbeke, Wang [1], and references therein.

The GUE–corners process is a determinantal (see, e.g., Borodin [9]) point process with discrete time obtained using random matrices. If, instead of cutting out corners of a single matrix, one starts adding independent GUE matrices, then the eigenvalues of the sums also form a determinantal process, and the number of matrices in the sum plays the role of discrete time, see Eynard, Mehta [19]. Another class of (dynamical) determinantal processes with discrete time can be constructed from products of random matrices, see Strahov [43], Akemann and Strahov [5]. (Determinantal processes in products of random matrices were first discovered in Akemann and Burda [2]). Such processes are called product matrix processes, and they are formed by the squared singular values of random matrix products. We can use independent complex Gaussian matrices to obtain a simple example of such processes. Namely, let , , be independent matrices with standard i.i.d. complex Gaussian entries. Assume that is of size , , , , , and for each denote by , , the squared singular values of the partial product . The configuration

of all these squared singular values generates a random point process on . It was shown in Strahov [43] that this process is determinantal (and it can be viewed as a determinantal process with discrete time). Paper [43] gives a contour integral representation for the correlation kernel, together with its hard edge scaling limit, and generalizes results obtained in Akemann, Kieburg, and Wei [3], Akemann, Ipsen, and Kieburg [4], Kuijlaars and Zhang [31] to the multi-level situation. A more general class of product matrix processes related to certain multi-matrix models was introduced and studied in Akemann and Strahov [5]. In this class the matrices in the products are no longer independent, but in spite of that the product matrix processes are still determinantal.

From a different viewpoint, various matrix corners processes studied by Johansson, Nordenstam [32], Okounkov, Reshetikhin [40], Adler, van Moerbeke, Wang [1], Forrester, Rains [21], Borodin, Gorin [12] were shown to be continuous limits of special Schur processes of Okounkov and Reshetikhin [38], [39]. The discrete time determinantal process formed by the eigenvalues of sums of independent GUE matrices can be understood as a limit of a special Schur process as well. It is natural to ask whether product matrix processes also have this property. Motivated by this question, we construct in this paper a product matrix process using corners of independent Haar distributed unitary matrices (or truncated unitary matrices). We demonstrate that this process is a scaling limit of a certain Schur process, which implies determinantal formulas for (dynamical) correlation functions. Moreover, starting from the general Okounkov-Reshetikhin formula [39] for the correlation kernels of Schur processes, we derive a double contour integral representation for the correlation kernel of the product matrix process formed by truncated unitary matrices. The formula for the correlation kernel we derive in this paper can be understood as a time-dependent generalization of the result obtained in Kieburg, Kuijlaars, and Stivigny [28] for the squared singular values of matrix products with truncated unitary matrices.

The fact that the product matrix process formed by truncated unitary matrices is a continuous limit of the Schur process enables us to prove Theorem 2.9 below, that says that the continuous limit of marginals for -distributed (skew) plane partitions coincides with the joint law of squared singular values for products of corners of Haar-distributed unitary matrices, see Figure 1 for one particular case of the theorem. We consider Theorem 2.9 as the main result of the present paper. It demonstrates that, similarly to the corners process, the time-dependent determinantal processes constructed from products of truncated unitary matrices appear as scaling limits in a model of statistical mechanics of a combinatorial nature. To the best our knowledge, the present paper is the first work relating products of random matrices with scaling limits of models that have no a priori relation to random matrices.

It is also natural to ask about conceptual reasons for such a coincidence. Why should random matrices be directly related to statistical mechanics models? For the GUE–corners process, Okounkov and Reshetikhin [40] suggested the following heuristic argument: If we start with a discrete model of statistical mechanics satisfying a certain Gibbs (i.e., conditional uniformity) property, then one expects the same property to survive in the continuous limit. Olshanski and Vershik [42] classified all such Gibbs measures on triangular arrays of reals, and out of them only the GUE–corners process agrees with the growth conditions implied by the Law of Large Numbers (limit shape behavior) of the discrete model.

For the products of random matrices we do not dispose of an analogue of the Okounkov–Reshetikhin argument. However, let us explain the path that led us to the understanding that a similar connection with combinatorial statistical mechanics is possible. The following fact [21], [12] is easy to prove by comparing the explicit formulas for the distributions: If is a corner of Haar-random unitary matrix, then the eigenvalues of (this is often called Jacobi or MANOVA ensemble) are distributed as a continuous limit of a Schur measure with two principal specializations. One could argue that this is an instance of the semiclassical asymptotics common in representation theory. Next, we need to understand what happens with these eigenvalues when is multiplied by another similar matrix. It is known that multiplication of (real/complex/quaternion at ) matrices is intimately linked to multiplication of corresponding Jack (=zonal) polynomials, which become Schur polynomials in the case of the complex field () that we discuss here. This is discussed by Macdonald [34, Chapter VII], Forrester [20, Section 13.4.3], and more recently used, e.g., by Kieburg, Kosters [29] and by Gorin, Marcus [24]. If we consider a version of the multidimensional Fourier transform for the Schur measures (the appropriate version was introduced by Gorin, Panova [23], Bufetov, Gorin [16] under the name Schur generating functions), then being a Schur measure or its continuous limit is equivalent to the factorization of this transform into a product of one variable functions. Since such factorization is preserved under multiplication, the squared singular values of products of random matrices have to be described by the Schur processes.

We detail how this argument works in the simplest case of matrices in Section 8. For the proof of our main statements, Proposition 2.6 and Theorem 2.9, we choose in Sections 2-7 another path, which is more direct (and leads to a more general result) but, perhaps, more mysterious. Let us remark that while the arguments of Section 8 admit an immediate generalization to products of real and quaternion matrices, yielding their representation as limits of Macdonald processes, for the proofs of Sections 2-7 such a generalization is unclear.

The paper is organized as follows. In Section 2 we introduce notation and present the main results. In particular, Proposition 2.4 gives a formula for the correlation kernel of the product matrix process associated with truncated unitary matrices, Proposition 2.6 shows that this product matrix process can be understood as a continuous limit of a special Schur process, and Theorem 2.9 presents our result on convergence of marginals of -distributed plane partitions to this product matrix process. Sections 2-7 contain the proofs of our statements. In Section 8 we sketch another way to prove our main results by exploiting symmetric functions and zonal polynomials. Finally, Appendix gives a second proof of Proposition 2.4 based on the Eynard-Mehta theorem.

Acknowledgements. We are very grateful to Mario Kieburg and Leonid Petrov for discussions. All three authors were partially supported by the NSF grant DMS-1664619. A.B. was partially supported by the NSF grant DMS-1607901. V.G. was partially supported by the by NEC Corporation Fund for Research in Computers and Communications and by the Sloan Research Fellowship.

2. Notation and statement of results

2.1. Product matrix processes with truncated unitary matrices

Let , , be matrices with random complex entries, and assume that each matrix , , is of size . Set

If , then for each , , are random matrices of the same size . Denote by the th largest eigenvalue of . The configuration of all these eigenvalues,

| (2.1) |

forms a point process on . This point process is called the product matrix process associated with the random matrices , , , .

Here we consider a product matrix process constructed from a collection of truncated unitary matrices. Namely, let , , , ,, be independent Haar distributed unitary matrices. We assume that the size of each matrix , , is equal to . Recall that if is a matrix, and the integers , are chosen such that , the submatrix of defined by

is called a truncation of . Now, for let be the truncation of of size . We agree that , and assume that the positive integers , , , are chosen in such a way that the conditions

| (2.2) |

and

| (2.3) |

are satisfied. Denote by the vector of the squared singular values of the product matrix , and for denote by the vector of the squared singular values of the product matrix . Configurations form a point process on . We will refer to this point process as to the product matrix process associated with truncated unitary matrices. We say that the product matrix determines the initial conditions of the product matrix process associated with truncated unitary matrices. The numbers , , will be called the parameters of the product matrix process associated with truncated unitary matrices.

Proposition 2.1.

Consider the product matrix process associated with truncated unitary matrices, and let ; denote the set of the squared singular values of the product matrix . The joint probability distribution of is given by

| (2.4) |

where , the Vandermonde determinant is defined by , for we write , is a normalization constant, and is a sequence of weight functions. The normalization constant can be written explicitly as

| (2.5) |

Here stands for the Pochhammer symbol. The function can be expressed as a Meijer -function,

| (2.6) |

In this formula denotes a positively oriented contour in the complex -plane that starts and ends at and encircles the negative real axis. The constant in the formula for can be written as

| (2.7) |

Remark 2.2.

The Meijer -function in equation (2.6) is equal to zero for . Correspondingly, we set the weight functions to zero for .

Remark 2.3.

Our next result provides explicit formulae for the correlation functions of the product matrix process associated with truncated unitary matrices.

Proposition 2.4.

The product matrix process with truncated unitary matrices is a determinantal process on . Its correlation kernel, (where , and ) can be written as

| (2.8) |

where is a closed contour in the complex -plane encircling the interval once in the positive direction, is a positively oriented closed contour in the complex -plane encircling once an interval containing all the points , , ; ; , , , which does not intersect . In the formula above it is understood that .

We note that at and the formula for the correlation kernel stated in Proposition 2.4 turns into that derived in Kieburg, Kuijlaars, and Stivigny [28], Proposition 2.7.

In what follows we will give two proofs of Proposition 2.4. The first proof will use the fact that the process defined by equation (2.4) can be understood as a continuous limit of a special Schur process, see Proposition 2.6 below. Since the Schur processes are determinantal, this will imply determinantal formulae for the correlation functions. As for the explicit formula for the correlation kernel (see equation (2.8)), it will be obtained from the general Okounkov-Reshetikhin formula [39] for correlation kernels of the Schur processes by a certain limiting procedure in Section 6. The second proof will be based on the observation that the density of the product matrix process with truncated unitary matrices can be written as a product of determinants. This will enable us to apply the result by Eynard and Mehta [19], and to give a formula for the correlation functions, see the Appendix. This second argument is similar to the proof of Borodin and Rains [13] of the determinantal structure of Schur processes.

2.2. Convergence of the Schur process

Let be the algebra of symmetric functions in countably many variables . We use two sets of generators of : power sums and complete homogeneous symmetric functions , , defined through

We recall that the Schur functions form a basis of when varies over all Young diagrams (or partitions). We also use skew Schur functions labeled by two Young diagrams and .

A specialization of is an algebra homomorphism of to . A specialization of is called nonnegative if it takes non-negative values on the Schur functions, see, e.g., Borodin [10], Section 1 for a detailed discussion of nonnegative specializations of the algebra of symmetric functions. The application of a specialization to will be denoted as . The trivial specialization of takes value at the constant function , and takes value at any homogeneous of degree . In particular unless , and unless .

In this paper we will only use the simplest Schur positive specializations parameterized by arbitrary and –tuple of positive reals . We denote it and set

Equivalently, this specialization can be encoded by its generating function:

where the second identity is the algebraic relation between generators and .

The specializations that we use are often given by geometric series . When , the geometric series is empty and becomes the trivial specialization.

Definition 2.5.

Let be a natural number, and let be nonnegative specializations of . The Schur process of rank is a probability measure on sequences of Young diagrams

parameterized by Schur-positive specializations of the algebra of symmetric functions given by

| (2.9) |

Here is a normalization constant.

Since unless , the Schur process lives on the following configurations of Young diagrams

For skew Schur functions we have the following summation formulae

| (2.10) |

and

| (2.11) |

see Macdonald [34], Section I.5, equation (5.9), and Example I.5.26(1). Here

and the values of the symmetric functions under the union specialization are determined by the power sum values given by

Hence, for specializations we have

Proposition 2.6.

Consider the Schur process defined by the probability measure (2.9). Assume that the specializations , , of the Schur process are defined by

| (2.12) |

| (2.13) |

| (2.14) |

The specialization is defined by

| (2.15) |

and all the other specializations , , are trivial. With these specializations the Schur process lives on the point configurations

| (2.16) |

and each , has at most nonzero parts almost surely. Set

| (2.17) |

Then the Schur process induces a point process on , and this process is formed by the configurations

| (2.18) |

As , the point process formed by configurations (2.17) converges to the product matrix process associated with truncated unitary matrices, as defined in Section 2.1.

Remark 2.7.

We prove Proposition 2.6 only under the assumption of (2.2). Although it is very plausible that the statement is true without this condition, we do not address the more general case in this text. A technical difficulty is that without (2.2) we cannot use the result of Proposition 2.1 directly; in particular, the constant of (2.7) is infinite.

2.3. Random skew plane partitions, and products of truncated unitary matrices

Let and be two natural numbers, and denote by the rectangle. Let be a Young diagram such that . A skew plane partition with support is a filling of all boxes of such that and for all meaningfull values of and . Here we assume that is located in the row and column of . The volume of a skew plane partition is defined by

| (2.19) |

Given a parameter , define a probability measure on the set of all plane partitions with support by setting

| (2.20) |

For a skew plane partition we define Young diagrams , , through

Note that . Also, define

This is a subset of containing points, and all such subsets are in bijection with the Young diagrams (or partitions) contained in the box .

It is not hard to see that the set of all skew plane partitions with support consists of sequences with

| (2.21) |

where notation means that and interlace, that is

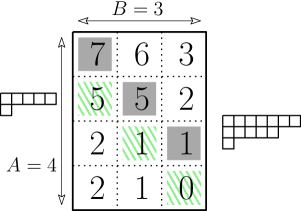

We refer to Figure 1 for an illustration of , , case. Moreover, we have

where denotes the number of boxes in the Young diagram .

The probability measure on the set of all skew plane partitions with support and defined by equation (2.20) induces a probability measure on sequences . It is known (see Okounkov and Reshetikhin [39, 41]) that this probability measure can be understood as the Schur process defined in Section 2.2 by equation (2.9) with the rank , and nonnegative specializations , defined by

Note that for any two neighboring specializations , defined above at least one is trivial, and each coincides either with or . The only nontrivial specializations are one variable specializations with . A basic property of skew Schur functions is that unless ; this implies interlacing conditions (2.21).

Let . The set enumerates the intersections of the boundary of the skew diagram with the square grid, as shown on Figure 2. Denote by the number of vertical segments of of the boundary of the skew diagram .

Let be a subset of , where the numbers , , parameterize the vertical segments of the boundary of the skew diagram , see Figure 3. For example, for the Young diagram on Figure 2 we have , , , , , , and . Now, assume that , and pick numbers , , such that , see Figure 3.

Consider the sequence of random Young diagrams associated with a random skew plane partition whose support is , and whose weight is proportional to . By assigning to this sequence the point configuration

| (2.22) |

we obtain a random point process on .

Proposition 2.8.

The probability of the point configuration (2.22) is determined by the probability measure

| (2.23) |

where is a normalization constant.

Now we are ready to state the main result of the present work. Let be a random skew partition with support whose weight is determined by equation (2.20). Let be a sequence of Young diagrams associated with . Consider the subsequence of , where the indexes , , are chosen as it is described above. By assigning to this subsequence the point configuration (2.22) we obtain a random point process on . Set , , and define

Theorem 2.9.

As , the point process formed by configurations

converges to the product matrix process associated with truncated unitary matrices, described in Section 2.1, and defined by probability distribution (2.4). The parameters of the relevant product matrix process are given by

-

•

.

-

•

for , and for .

-

•

, for , and for .

The truncated unitary matrices forming the product matrix process in Theorem 2.9 are shown schematically on Figure 4.

Remark 2.10.

The condition reads as

| (2.24) |

The conditions (where ) can be rewritten as

and

(where ), and are satisfied automatically.

Remark 2.11.

The choice of the parameters , is not unique. Namely, we need to identify the geometric series in (2.12) with geometric series in the last two lines of (2.23) and there are ways to do so. Formally, our proof goes through only for the choices which agree with the condition of (2.2), see, however, Remark 2.7.

Example 2.12.

Consider the particular case in which , as in Figure 1. In this situation , , , and the parameters , , take values in . As a limit, we obtain the product matrix process with truncated unitary matrices whose parameters ; , , ; , , are given by

-

•

;

-

•

, and for ;

-

•

for .

3. Proof of Proposition 2.1

In order to prove Proposition 2.1 we will use two results obtained in Kieburg, Kuijlaars, and Stivigny [28]. Namely, Corollary 2.6 in Kieburg, Kuijlaars, and Stivigny [28] implies that the probability distribution of (which is the vector of the squared singular values of ) can be written as

The second result concerns the density of squared singular values for a product of a nonrandom and a truncated unitary matrix. Namely, assume that is a Haar distributed unitary matrix of size , and let be an truncation of . In addition, let be a nonrandom matrix of size , and impose the following constraints for the parameters , , , and :

Denote by the vector of squared singular values of , and by the vector of squared singular values of . If are pairwise distinct and nonzero, then the vector has density

| (3.1) |

see Kieburg, Kuijlaars, and Stivigny [28], Theorem 2.1. Now assume that . Applying the results stated above we immediately obtain that the probability distribution of is proportional to the product of determinants as in equation (2.4). In order to compute the normalization constant we use the Andrief integral identity (see, for instance, De Bruijn [15]), and the recurrence relation

see Kieburg, Kuijlaars, and Stivigny [28], equation (2.22). The integration over , , gives

Changing the integration variable , we rewrite the integral inside the determinant above as

| (3.2) |

As a result of integration over the variables , , ; ; , , we find

Applying the Andrief integral identity again, we obtain

The integral inside the determinant can be computed explicitly in terms of Gamma functions. Namely, formula (5.6.1.1) in Luke [33] gives

| (3.3) |

and we find

The following formula for the determinant with Gamma functions entries is known

| (3.4) |

see equation (4.11) in Normand [35]. Using this formula we obtain

This gives

Since

we can rewrite the normalization constant in the same form as in the statement of the Proposition 2.1. ∎

4. Limits of symmetric functions

The aim of this Section is to obtain certain asymptotic formulae for the Schur functions, and for the skew Schur functions, see Proposition 4.1 and Proposition 4.3 below. We will need these formulae in the proofs of our main results (Proposition 2.6 and Theorem 2.9).

Proposition 4.1.

Let be a Young diagram with rows, and assume that . Set

where . Then

| (4.1) |

The convergence is uniform in ’s.

Proof.

Homogeneity of the Schur polynomials implies

| (4.2) |

Moreover, the principal specialization of the Schur polynomials (see Macdonald [34], 3, Example 1) gives

| (4.3) |

The product in the right-hand side of the expression above can be written as

| (4.4) |

Taking the limit , and using the fact that

| (4.5) |

we obtain the formula in the statement of the Proposition. ∎

Lemma 4.2.

Let , be two positive integers. Assume that . If , and , then we have

| (4.6) |

where is the th complete homogeneous symmetric function, , , and . The convergence is uniform in , .

Proof.

We start by noting that the right-hand side of (4.6) has no singularity at . Indeed, this follows from the observation that for positive we have .

Proposition 4.3.

Let , be two Young diagrams, . Set

where , and . Then we have

| (4.8) |

The convergence is uniform in ’s and ’s.

Proposition 4.4.

Let be a Young diagram with rows. Set , , . We have, uniformly for ,

| (4.9) |

where the parameters , are those specified in Section 2.1.

Proof.

The proof is by induction over . Assume that . Then equation (4.9) takes the form

| (4.10) |

As follows from equations (2.20)-(2.25) in Kieburg, Kuijlaars, and Strivigny [28],

We see that equation (4.10) turns into equation (4.1) (with , ), and conclude that Proposition 4.4 holds true for .

Assume that the statement of Proposition 4.4 holds true for certain natural . Let us prove this statement for . Equation (2.11) implies

| (4.11) |

Here we can assume that the sum is over Young diagrams with at most rows. Set

If

then Proposition 4.3 (with , , and ) implies that

converges to

and the convergence is uniform in ’s and ’s. Moreover, by our assumption

converges to

uniformly for . Since , we conclude that the right-hand side of equation (4.11) multiplied by

converges to

and the convergence is uniform in . The expression above can be rewritten as

where we have used equations (2.6), (2.7) to rewrite the Meijer -function in terms of the corresponding weight function . By the Andrief identity, and by the same calculations as in the proof of Proposition 2.1 it can be shown that (4) is equal to

Rewriting the weight function in terms of the corresponding Meijer -function we obtain that

| (4.12) |

uniformly for . ∎

5. Convergence of the Schur process to the product matrix process with truncated unitary matrices. Proof of Proposition 2.6

Now we begin to investigate the convergence of the Schur process to the product matrix process with truncated unitary matrices. We start with the case where the initial conditions are defined by a single truncated matrix , see Proposition 5.1 below. Then (using Proposition 4.4) we generalize Proposition 5.1 to the case where the initial conditions are specified by a product of truncated matrices , and prove Proposition 2.6. We remark that, in principle, the second part can be avoided, as the general case can be obtained from the case by restriction of a distribution to a subset of matrices. In particular, in this way the consistency of Proposition 2.1 between different values of can be used to produce an alternative proof of Proposition 4.4.

Consider the Schur process defined in Section 2.2. Define the specializations , , , , , of the algebra of symmetric functions as follows

-

•

The specialization is defined by

All other , , are trivial.

-

•

The specializations , , are defined by

With these specializations the Schur process lives on the point configurations

| (5.1) |

Set

| (5.2) |

The above Schur process induces a point process on , and this process is formed by the configurations

| (5.3) |

Proposition 5.1.

Proof.

Since specializations , , are trivial, the Schur process turns into the probability measure

| (5.4) |

where

Now we use the asymptotic formulae for the Schur functions obtained in Section 4. In particular, Proposition 4.1 gives

| (5.5) |

as . In addition, Proposition 4.3 implies that as ,

| (5.6) |

where . Besides, Proposition 4.1 also gives

| (5.7) |

Let us find the asymptotics of the normalization constant (defined by equation (5.4))111This is not strictly necessary as the uniform convergence of the configuration weights implies the convergence of the normalization constants. We perform this limit transition for the sake of completeness.. We have

where . Therefore,

| (5.8) |

Taking into account that

we find that the probability measure on , ,, turns into the probability measure

| (5.9) |

This probability measure can be interpreted as the product matrix process associated with truncated unitary matrices, see Proposition 2.1. The initial conditions of this process are defined by the single truncated unitary matrix , which corresponds to in the definition of this product matrix process in Section 2.1. ∎

Proposition 5.2.

Consider the Schur measure

| (5.10) |

which is the projection222For a discussion of projections of Schur processes see Borodin [10], Section 2. of the Schur process (equation (5.4)) to the Young diagram . If

then as the probability measure defined by equation (5.10) converges to

| (5.11) |

The probability measure defined by expression (5.11) can be understood as the ensemble of squared singular values of the product matrix (where , , are the truncated unitary matrices defined in Section 2.1).

Proof.

We already know that the Schur process defined by equation (5.4) converges to the product matrix process defined by the probability distribution (2.4). The Schur measure defined by expression (5.10) is the projection of this Schur process to the Young diagram , and the probability measure defined by expression (5.11) can be understood as the projection of the product matrix process defined by the probability distribution (2.4) to . The result follows. ∎

Proof of Proposition 2.6.

Proposition 2.6 is a generalization of Proposition 5.1 to the situation where the initial conditions are defined by a product of truncated matrices (and not by a single truncated matrix).

For the specializations specified in the statement of Proposition 2.6 the Schur process turns into the probability measure

| (5.12) |

where is a normalization constant. The rest of the proof of Proposition 2.6 follows the same line as that of Proposition 5.1. The only essential difference is that we use equation (4.9) instead of equation (5.4) for the asymptotics of the relevant Schur function

as . ∎

6. Convergence of the correlation functions and the proof of Proposition 2.4

Consider the Schur process defined by probability measure (2.9). Assume that the specializations , , of the Schur process are defined by equations (2.12)- (2.14), and that the specialization is defined by equation (2.15). Let us agree that all other , , are trivial. With these specializations the Schur process can be understood as a point process on formed by point configurations (2.16). Denote by the correlation functions of this Schur process, and by the correlation kernel of this Schur process.

Proposition 2.6 says that the Schur process under consideration converges to the product matrix process with truncated unitary matrices. This implies convergence of the correlation functions. Namely, if denotes the correlation function of the product matrix process with truncated unitary matrices defined by probability measure (2.4), then we must have

where the denominator came from the coordinate change. This limiting relation between the correlation functions would naturally follow from the limiting relation between the correlation kernels,

| (6.1) |

where denotes the correlation kernel of the product matrix process with truncated unitary matrices, and where stands for a kernel equivalent to . 333Recall that two kernels of a determinantal process are called equivalent if they define the same correlation functions. In what follows we will choose in such a way that the limit in the righthand side of equation (6.1) will exist.

The Okounkov-Reshetikhin formula for the correlation kernel is

| (6.2) |

see Theorem 2.2 in Ref. [13]. The choice of the integration contours and depends on the time variables and , and will be specified below. In the formula for the correlation kernel above we have used the notation

The specializations , , , , , of the algebra of symmetric functions are specified by equations (2.12)-(2.15).

For simplicity, let us consider the case corresponding to . The proof of Proposition 2.4 for a general is essentially the same.

We find

and

Therefore, we can write

| (6.3) |

Assume that . According to Theorem 2.2 in Ref. [13], we can choose as a counterclockwise circle contour with its center at , whose radius is larger than 1. Moreover, should be chosen in such a way that all the points , , ; ; , , of the complex -plane will be situated outside of the circle on its right. So we define the contour by

where .

In addition, we can choose as a counterclockwise circle with its center at , such that for all , for all , and such that the points , , , of the complex -plane are situated outside of . So we define by

where .

Let us consider the integral over in (6.3). Since , the residue at infinity of the integrand is equal to zero. Moreover, since , the singular point is situated inside the contour , for every . This enables us (without changing the integral in the right-hand side of equation (6.3)) transform through the extended -complex plane into an integration contour which encircles all the points , , ; ; , , once in the clockwise direction, and leaves on its left. The contour can be viewed as an image of a contour in the complex -plane under the transformation . The contour can be chosen in such a way that will be a clockwise oriented closed contour encircling all the points , , ; ; , , of the negative real axis, and leaving on its right.

Now let us consider the integral over in formula (6.3). We note that , so the residue of the integrand at infinity is zero. Moreover, since , and since leaves on its left, the singular point is situated inside , for every . Thus we can deform through the extended complex plane into a new contour encircling the points , , , of the complex -plane once in the clockwise direction, and this deformation will not affect the integral. The contour can be obtained from a clockwise oriented contour by the transformation . Clearly, can be chosen in such a way that will encircle the interval , and will not intersect .

We make the change of integration variables,

and set

This gives

| (6.4) |

where the integration contours are chosen as in the statement of Proposition 2.4.

Set

| (6.5) |

As , the function converges uniformly (with respect to on , and with respect to on ) to

| (6.6) |

as .

Now we define

Clearly, the kernels and are equivalent. Let us consider the limit

| (6.7) |

The fact that converges uniformly (with respect to on , and with respect to on ) to expression (6.6) enables us to interchange the limit and the integrals, and to compute (6.7) explicitly. By formula (6.1) this limit is equal to . Thus we have

| (6.8) |

where . We rewrite the products inside the integrals above in terms of Gamma functions as follows

| (6.9) |

| (6.10) |

and

| (6.11) |

Taking this into account we see that the righthand side of equation (6.8) can be rewritten as that of equation (2.8). This proves Proposition 2.4 for (and ).

Assume that . In this case we can choose both and as counterclockwise circle contours whose centers are at , and whose radii are less than 1, see Theorem 2.2 in Ref. [13]. Let us agree that for all , and . In addition, we will choose in such a way that all the points , , ; ; , , will be situated inside .

We will deform the contour through the extended complex plane into a new contour encircling all the points , , ; ; , , in the clockwise direction, and leaving the points , outside. As we deform into , we should pick up the contribution at the residue at . Thus we rewrite equation (6.3) as

| (6.12) |

Denote by the first term in the right-hand side of the above equation, and by the second term, so that

| (6.13) |

and

| (6.14) |

In the formula for we deform the contour through the extended complex plane into a new contour encircling the points , , , in the clockwise direction. Since we agree that all the points , , ; , , are situated inside , the contour can be chosen such that this deformation will not affect the value of . The contours and can be viewed as images of contours , under the transformations , and , and the contours , will be those described in the statement of the Proposition.

Set

and

After the change of variables we find

| (6.15) |

where is defined by equation (6.5). We thus have

| (6.16) |

where again we have used the uniform convergence of to take the limit inside the integrals. Note that (as in the case ) the right-hand side of equation (6.16) can be written as the second term in the righthand side of equation (2.8).

Now consider the formula for given by (6.13). Assume that . In this case the residue at infinity is equal to zero, and all finite poles are situated inside the contour . This implies that is equal to zero for . If , then the residue at is equal to , and we can deform into a contour encircling the poles , , ; , , once in the counterclockwise direction, and leaving on the left. The contour can be viewed as an image of a contour under the transformation , where will be that described in the statement of the Proposition. After the change of variables we find that

| (6.17) |

where . We have

| (6.18) |

where . As follows from equations (2.22), (2.23) and (2.24) in Kieburg, Kuijlaars, and Stivigny [28], the function

is equal to for . Therefore, equation

| (6.19) |

holds true for as well. Finally, formula (6.1), equations (6.16) and (6.18) give the desired formula for the correlation kernel in the case . ∎

7. Proof of Proposition 2.8 and Theorem 2.9

Proof of Proposition 2.8

In order to compute the probability of the point configuration (2.22), we need to compute the projection

of the Schur process associated with a skew plane partition to the diagrams , ,.

It is convenient to obtain first the projection on , , , , ,,

see Figure 3.

Using equation (2.11) we find

| (7.1) |

Equations (2.10) and (2.11) enable us to sum over the Young diagrams , , , , and . The result is

| (7.2) |

Taking into account the homogeneity of the Schur polynomials, and noting that , we see that the expression above can be rewritten

as in the statement of the Proposition 2.8.

∎

Proof of Theorem 2.8.

Proposition 2.8 says that the probability of the point configuration

can be written as a product of skew Schur functions, see equation (2.23). If , the parameters ; ; , , are related with parameters , ; ; , , ; , , as in the statement of Theorem 2.9, and , , are identified with , then the probability measure defined by equation (5.12) turns into the probability measure defined by equation (2.23). Application of Proposition 2.6 gives the result. ∎

8. Alternative proof through symmetric functions and zonal polynomials

In this section we sketch an alternative path to derive Proposition 2.6. For the clarity of the exposition we only detail one simplest case. At the end of the section we outline ways for generalizations.

Simplest case: product of two matrices. Let and be two independent Haar-distributed random unitary complex matrices. Let and be principal corners of and , respectively. Our aim is to link the distribution of the squared singular values of to a Schur measure.

First, note that and are almost surely non-degenerate. The squared singular values of are eigenvalues of . Since eigenvalues are preserved under conjugations, they are the same as the eigenvalues of . Since, and have the same distribution, we can further rewrite the law of interest as the distribution of eigenvalues for the matrix .

Set and . The (ordered) eigenvalues of are real numbers distributed with probability density

| (8.1) |

This computation is a particular case of the identification of singular values of a corner of ф a random unitary matrix with Jacobi ensemble, see [17] and references therein. This is also the case in Proposition 2.1. The eigenvalues of , have the same distribution.

Next, we fix and consider a distribution on pairs of integers with weight

| (8.2) |

On one hand, (8.2) is a particular case of the Schur measure. On the other hand, the explicit evaluations

imply that upon the change of variables , , in the limit , (8.2) becomes (8.1). The same computation works for matrices of arbitrary size and for any values of the random matrix parameter , see [21, Section 3.1], [12, Theorem 2.8].

The next step is to use the Cauchy–Littlewood identity (see [34, Chapter I])

| (8.3) |

Equation (8.2) and the identity (8.3) lead to the expectation evaluation

| (8.4) |

Here and can be any complex numbers such that the series defining the expectation absolutely converges. We make a particular choice, for two integers . Then, using the label–variable duality (which is an immediate consequence of the definition of the Schur polynomials as ratios of two determinants)

| (8.5) |

we get

| (8.6) |

Note that as one varies , the left–hand side of (8.6) uniquely determines all the moments of –random vector . Indeed, since , it is enough to consider only symmetric linear combinations of moments, and those are finite combinations of Schur polynomials. Since is supported inside , the moments uniquely determine the distribution . The conclusion is that (8.6) is equivalent to the definition (8.2). Further, the same equivalency holds in the limit , as . Equation (8.6) becomes

| (8.7) |

We can now describe what is happening with expectations (8.4), (8.6), (8.7), when we multiply the matrices. The computation relies on the following integral identity:

| (8.8) |

In (8.8), the integration goes over the group of unitary complex matrices, and are two fixed complex matrices with eigenvalues and , respectively, and by we mean the Schur polynomial evaluated on two eigenvalues of the matrix . When and are unitary, the relation (8.8) is known as the functional equation for the characters of . More generally, (8.8) is the identification of zonal polynomials of the symmetric space with Schur polynomials, see [34, Chapter VII], [20, Section 13.4.3]. For real and quaternion matrices, an analogue of (8.8) holds with Schur polynomials replaced by the Jack polynomials. Using in also plays no special role in (8.8) and the identity extends to all .

Coming back to , the matrices and are independent, and the distribution of each of them is –invariant, with respect to the action by conjugation. In other words, while the eigenvalues have a specific distribution (8.1), the eigenvectors are chosen uniformly at random (in the set of all possible pairs of orthogonal unit vectors in ). Thus, if we plug , into (8.8) and take expectation with respect to and , we get

Combining with (8.7), this implies

which is (again by (8.3) and (8.5)) precisely the limit of

for the integral vector distributed according to the Schur measure

| (8.9) |

We conclude that the eigenvalue distribution for is the limit of distributed according to the Schur measure (8.9).

Generalizations. Let us discuss how to see the structure of the full Schur processes, rather than just its slices given by the Schur measures. Note that the transition between of (8.2) and of (8.9) can be seen as one step of Markov chain on two-row Young diagrams with transition probabilities found from the decomposition

| (8.10) |

Summing (8.10) using (8.4), we get . In the limit, the same structure of the Markov chain can be seen for the projection of the joint law of and onto their eigenvalues; this is again a corollary of (8.8).

Comparison of (8.10) with the skew Cauchy identity (see, e.g., [34, Section I.5, Example 26]) yields that is given by the fomula

| (8.11) |

Combining the definition of with (8.11), we conclude that the two times Markov chain with initial state , transitional probability (and final state ) is the Schur process. Sending , we see that that the joint law of squared singular values of and is the continuous limit of this Schur process.

At this moment we can generalize the argument to products of more matrices. Each additional factor gives another time step of the Markov chain. These transition probabilities generalize (8.11) and therefore, the link to Schur processes persists. Let us make a remark about the sizes of the matrices that are being multiplied. The computation leading to (8.1) and its connection to (8.2) can be generalized to rectangular corners of random unitary matrices of arbitrary sizes (and we can also deal with real/squaternion cases). The identity (8.8) has similar extensions. However, when we start iterating (8.8) it is convenient to assume that all the involved matrices have the same square size, as then the present arguments extend word-for-word. This is less general than the setting of Proposition 2.6. It is plausible that the arguments of this section can be adapted to the changing sizes as well,444When we pass between a rectangular matrix and its square counterpart encapsulating the singular values, the following distinction becomes important: the matrices and have the same non-trivial eigenvalues, but additional s show up because of different sizes. One needs to translate this into the language of Schur processes and expectations (8.4), (8.6). but we will not pursue this direction.

Finally, one can go beyond corners of unitary matrices and consider factors with more complicated unitarily–invariant distributions. We refer to [25] for a progress in this direction.

9. Appendix. Measures given by products of determinants, the Eynard-Mehta theorem, and the second proof of Proposition 2.4

The aim of this Appendix is to give another, more direct proof of Proposition 2.4 based on an application of the Eynard-Mehta theorem [19]. The starting point of this proof is the fact that the density of the product matrix process under considerations is given by a product of determinants, see Proposition 2.1. This enables us to apply the Eynard-Mehta theorem to the product matrix process with truncated unitary matrices. Although, the proof below is similar to the arguments of [13] and [43], we decided to reproduce it in the present setting for pedagogical reasons.

9.1. The Eynard-Mehta theorem

Let us first recall the formulation of the Eynard-Mehta theorem. Let be two fixed natural numbers, and let , be two given sets. Let be a complete separable metric space, and consider a probability measure on given by

| (9.1) |

In the formula above, is the normalization constant, the functions , are given intermediate one-step transition functions, is a given initial one-step transition function, and is a given final one-step transition function. Also,

the vectors

are fixed initial and final vectors, and

Here is a given Borel measure on . Given two transition functions and set

The theorem below is the Eynard-Mehta theorem.

Theorem 9.1.

The probability measure given by equation (9.1) defines a determinantal point process on . The correlation kernel of this determinantal point process, (where , and , is given by the formula

| (9.2) |

The functions , and the matrix (where ) are defined in terms of transition functions as follows

| (9.3) |

and

| (9.4) |

Remark 9.2.

In what follows the functions

will be called initial transition functions, and the functions

will be called final transition functions. In addition, the functions of the form

will be called intermediate transition functions. Finally, the function

will be called the total transition function.

9.2. Explicit formulae for the transition functions

In our situation , , . The initial one-step transition function is defined by

The final one-step transition function is defined by

In addition, the intermediate transition functions can be written as

where .

For the initial transition functions we obtain the following recurrence relation

| (9.5) |

This is the recurrence relation for (where ), see Kieburg, Kuijlaars, and Stivigny, equation (2.23).

The total transition function can be written as

| (9.6) |

where is defined by equation (2.7). The Mellin transform of a Meijer -function is

| (9.7) |

This gives an expression of the total transition function in terms of Gamma functions

| (9.8) |

Similar calculations give us the formula for the final transition functions. In particular, we can write

| (9.9) |

The change of the integration variable gives

| (9.10) |

Repeating this calculation, we arrive to a general formula for the final transition function

| (9.11) |

9.3. The inverse of

Here we find an explicit formula for in the formula for the correlation kernel in Theorem 2.4. If , then is equal to the total transition function given by equation (9.8). We need to find the inverse of the matrix defined by

Proposition 9.3.

For and , the matrix

is invertible and its inverse matrix is given by

| (9.15) |

Proof.

See Theorem 10 in Zhang and Chen [45]. ∎

9.4. The contour integral representation for

Using explicit formula for the final transition function (see equation (9.11)) we rewrite as

| (9.21) |

The Residue Theorem gives the following contour integral representation for :

| (9.22) |

where is a closed contour encircling the interval once in the positive direction, and where .

9.5. The contour integral representation for

Equation (9.20) together with the formula for the initial transition functions obtained in Section 9.2 give

| (9.23) |

The contour integral representation for the Meijer -function inside the sum above is

| (9.24) |

where the contour is a positively oriented curve in the complex -plane that starts and ends at , and encircles the negative real axis. In equation (9.23) the resulting sum is

The Pfaff-Saalschltz Theorem says that

if the balanced condition, , is satisfied, see, for example, Ismail [27], Section 1.4. In our case

and the balanced condition is satisfied. Thus we have

Taking into account that

we obtain the formula

| (9.25) |

9.6. Derivation of the correlation kernel

Equation (9.14) gives the first term in equation (9.2) for the correlation kernel. To write explicitly the second term in equation (9.2) we insert the formulae for (equation (9.22)), and (equation (9.25)) into equation (9.18). After simplifications we see that the second term in equation (9.2) can be written as

| (9.26) |

The sum inside the integral is the same as that in Kuijlaars, Stivigny [30] (see the proof of Proposition 4.4 in Kuijlaars, Stivigny [30]), and the rest of the proof is the same as that of Proposition 4.4 and Theorem 4.7 in Kuijlaars, Stivigny [30]. ∎

References

- [1] Adler, M.; van Moerbeke, P.; Wang, D. Random matrix minor process related to percolation theory. Random Matrix Theory Appl. 2 (2013), no. 4, 1350008.

- [2] Akemann, G.; Burda, Z. Universal microscopic correlation functions for products of independent Ginibre matrices. J. Phys. A: Math. Theor. 45 (2012) 465201.

- [3] Akemann, G.; Kieburg M.; Wei, L. Singular value correlation functions for products of Wishart random matrices. J. Phys. A. 46 (2013) 275205.

- [4] Akemann, G.; Ipsen, J.; Kieburg M. Products of rectangular random matrices: singular values and progressive scattering. Phys. Rev. E 88 (2013) 052118.

- [5] Akemann, G.; Strahov, E. Product matrix processes for coupled multi-matrix models and their hard edge scaling limits. arXiv:1711.01873

- [6] Baik, J.; Deift, P.; Suidan, T. Combinatorics and Random Matrix Theory. Graduate Studies in Mathematics, 172.

- [7] Baryshnikov, Yu. M. GUEs and queues, Probability Theory and Related Fields, 119(2):256–274, 2001.

- [8] Beals, R.; Szmigielski, J. Meijer G-functions: a gentle introduction. Notices Amer. Math. Soc. 60 (2013), no. 7, 866–872.

- [9] Borodin, A. Determinantal point processes, in Oxford Handbook of Random Matrix Theory, Oxford University Press, 2011. arXiv:0911.1153.

- [10] Borodin, A. Schur dynamics of the Schur processes. Adv. Math. 228 (2011), no. 4, 2268–-2291

- [11] Borodin, A.; Gorin, V. Lectures on integrable probability. Probability and statistical physics in St. Petersburg, 155–214, Proc. Sympos. Pure Math., 91, Amer. Math. Soc., Providence, RI, 2016.

- [12] Borodin, A.; Gorin, V. General beta Jacobi corners process and the Gaussian Free Field, Communications on Pure and Applied Mathematics, 68, no. 10, 1774–1844, (2015). arXiv:1305.3627.

- [13] Borodin, A.; Rains, E. M.; Eynard-Mehta theorem, Schur process, and their Pfaffian analogs. J. Stat. Phys. 121 (2005), no. 3–4, 291–317.

- [14] Bougerol, P.; Jeulin, T.; Paths in Weyl chambers and random matrices, Probability Theory and Related Fields, 124, no. 4 (2002), 517–543.

- [15] De Bruijn, N. G. On some multiple integrals involving determinants, J. Indian Math. Soc. (N.S.) 19 (1955), 133 -151.

- [16] Bufetov, A.; Gorin, V.; Fourier transform on high–dimensional unitary groups with applications to random tilings, arXiv:1712.09925.

- [17] Collins, B.; Product of random projections, Jacobi ensembles and universality problems arising from free probability, Probability Theory and Related Fields, 133, no. 3 (2005), 315–344, arXiv:math/0406560.

- [18] Dimitrov, E.; Six-vertex models and the GUE-corners process, International Mathematics Research Notices, rny072, arXiv:1610.06893.

- [19] Eynard, B.; Mehta, M. L. Matrices coupled in a chain. I. Eigenvalue correlations. J. Phys. A 31 (1998), no. 19, 4449–4456.

- [20] Forrester, P.J.; Log-Gases and Random Matrices, Princeton University Press, 2010.

- [21] Forrester, P.; Rains, E.; Interpretations of some parameter dependent generalizations of classical matrix ensembles, Probability Theory and Related Fields, 131, no. 1 (2005), 1–61. arXiv:math-ph/0211042

- [22] Gorin,V.; From Alternating Sign Matrices to the Gaussian Unitary Ensemble, Communications in Mathematical Physics, 332, no. 1 (2014), 437–447, arXiv:1306.6347.

- [23] Gorin, V; Panova.G; Asymptotics of symmetric polynomials with applications to statistical mechanics and representation theory, Annals of Probability, 43, no. 6, (2015) 3052–3132. arXiv:1301.0634.

- [24] Gorin,V; Marcus, A.W.; Crystallization of random matrix orbits, International Mathematics Research Notices, rny052, arXiv:1706.07393.

- [25] Gorin, V; Sun, Y; In preparation.

- [26] Gravner, J.; Tracy, C.A.; Widom, H.; Limit Theorems for Height Fluctuations in a Class of Discrete Space and Time Growth Models, J. of Statistical Physics 102 (2001), 1085–1132, arXiv:math/0005133

- [27] Ismail, M. E. H. Classical and quantum orthogonal polynomials in one variable. Encyclopedia of Mathematics and its Applications, 98. Cambridge University Press, Cambridge, 2009.

- [28] Kieburg, M.; Kuijlaars, A. B. J.; Stivigny, D. Singular value statistics of matrix products with truncated unitary matrices. Int. Math. Res. Not. IMRN 2016, no. 11, 3392–3424.

- [29] Kieburg, M.; Kosters, H; Products of Random Matrices from Polynomial Ensembles, arXiv:1601.03724.

- [30] Kuijlaars, A. B. J.; Stivigny, D. Singular values of products of random matrices and polynomial ensembles. Random Matrices Theory Appl. 3 (2014), no. 3, 1450011.

- [31] Kuijlaars, A.B.J.; Zhang, L. Singular values of products of Ginibre random matrices, multiple orthogonal polynomials and hard edge scaling limits. Commun. Math. Phys. 332 (2014) 759–781.

- [32] Johansson, K.; Nordenstam, E. Eigenvalues of GUE Minors. Electron. J. Probab. 11 (2006), 1342–1371.

- [33] Luke, Y.L. The special functions and their approximations. Academic Press, New York 1969.

- [34] Macdonald, I. G. Symmetric functions and Hall polynomials. Second edition. With contributions by A. Zelevinsky. Oxford Mathematical Monographs. Oxford Science Publications. The Clarendon Press, Oxford University Press, New York, 1995.

- [35] Normand, J.-M. Calculation of some determinants using the s-shifted factorial. J. Phys. A 37 (2004), no. 22, 5737–5762.

- [36] Jiang, T. Approximation of Haar distributed matrices and limiting distributions of eigenvalues of Jacobi ensembles, Probab. Theory Related Fields 144 (2009) 221–246.

- [37] O’Connell,N; Yor,M; A Representation for Non-Colliding Random Walks, Electron. Commun. Probab. Volume 7 (2002), paper no. 1, 1–12.

- [38] Okounkov, A. Infinite wedge and random partitions. Selecta Mathematica 7 (2001), 57–81. arXiv:math/9907127.

- [39] Okounkov, A.; Reshetikhin, N. Correlation function of Schur process with application to local geometry of a random 3-dimensional Young diagram. J. Amer. Math. Soc. 16 (2003), no. 3, 581–603.

- [40] Okounkov, A. Yu.; Reshetikhin, N. Yu. The birth of a random matrix, Moscow Mathematical Journal, 6, no. 3 (2006), 553–566

- [41] Okounkov, A.; Reshetikhin, N. Random Skew Plane Partitions and the Pearcey Process, Communications in Mathematical Physics, 269, no. 3 (2007), 571–609.

- [42] Olshanski, G.; Vershik, A. Ergodic unitarily invariant measures on the space of infinite Hermitian matrices. Contemporary mathematical physics, 137–175, Amer. Math. Soc. Transl. Ser. 2, 175, Amer. Math. Soc., Providence, RI, 1996, arXiv:math/9601215

- [43] Strahov, E. Dynamical correlation functions for products of random matrices. Random Matrices Theory Appl. 4 (2015), no. 4, 1550020.

- [44] Tracy, C.; Widom, H. Level-spacing distributions and the Airy kernel, Communications in Mathematical Physics, 159, no. 1 (1994), 151–174.

- [45] Zhang, R.; Chen, Li-Chen. Matrix inversion using orthogonal polynomials. Arab J. Math. Sci. 17 (2011), no. 1, 11–30.