*

The Online Saddle Point Problem and Online Convex Optimization with Knapsacks

Abstract

We study the online saddle point problem, an online learning problem where at each iteration a pair of actions need to be chosen without knowledge of the current and future (convex-concave) payoff functions. The objective is to minimize the gap between the cumulative payoffs and the saddle point value of the aggregate payoff function, which we measure using a metric called “SP-Regret”. The problem generalizes the online convex optimization framework but here we must ensure both players incur cumulative payoffs close to that of the Nash equilibrium of the sum of the games. We propose an algorithm that achieves SP-Regret proportional to in the general case, and SP-Regret for the strongly convex-concave case. We also consider the special case where the payoff functions are bilinear and the decision sets are the probability simplex. In this setting we are able to design algorithms that reduce the bounds on SP-Regret from a linear dependence in the dimension of the problem to a logarithmic one. We also study the problem under bandit feedback and provide an algorithm that achieves sublinear SP-Regret. We then consider an online convex optimization with knapsacks problem motivated by a wide variety of applications such as: dynamic pricing, auctions, and crowdsourcing. We relate this problem to the online saddle point problem and establish regret using a primal-dual algorithm.

1 Introduction

In this paper, we study the online saddle point (OSP) problem. The OSP problem involves a sequence of two-player zero-sum convex-concave games which are selected arbitrarily by Nature. In each iteration, player 1 chooses an action to minimize its payoffs, while player 2 chooses an action to maximize its payoffs. Both players choose actions without knowledge of the current and future payoff functions. Our goal is to jointly choose a pair of actions for both players at each iteration, such that each player’s cumulative payoff at the end is as close as possible to that of the Nash equilibrium (i.e. saddle point) of the aggregate game.

More formally, we define the OSP problem as follows. There is a sequence of unknown functions that are convex in and concave in . Here, and are compact convex sets in Euclidean space. As a result, there exists a saddle point such that

At each iteration , the decision makers jointly choose a pair of actions , and then the function is revealed. The goal is to design an algorithm to minimize the cumulative saddle-point regret (SP-Regret), defined as

| (1) |

In other words, we would like to obtain a cumulative payoff that is as close as possible to the saddle-point value if we had known all the functions in advance.

We would like to emphasize an important distinction between the OSP problem and the standard Online Convex Optimization (OCO) problem [31]. In the OCO problem, Nature selects an arbitrary sequence of convex functions , and the decision maker chooses an action before each function is revealed. The objective is to minimize the regret defined as

The objective in the OSP problem is to choose the actions of two players jointly such that the aggregate payoffs of both players are close to the Nash equilibrium payoff. In contrast, OCO involves only an individual player against Nature. The OCO framework can be viewed as a special case of the OSP problem where the action set of the second player is a singleton. Moreover, the standard OCO setting is applicable to the OSP problem when only one of the players’ payoff is optimized at a time. To be specific, we define the individual-regret of players 1 and 2 as

| (2a) | |||

| (2b) | |||

The individual-regret measures each player’s own regret while fixing the other player’s actions. It is easy to see that minimizing individual-regret (2a) or (2b) can be cast as a standard OCO problem.

However, we will show that SP-Regret and individual-regret do not imply one another, so existing OCO algorithms cannot be directly applied to the OSP problem. More surprisingly, we show that any OCO algorithm with a sublinear () individual-regret will inevitably have a linear () SP-Regret in the general OSP problem (see details in §6).

In addition to establishing general results for the OSP problem, we focus on one of its prominent applications: the online convex optimization with knapsacks (OCOwK) problem. Several variants of the OCOwK problem have recently received a lot of attention in recent literature, but we found its connection to the OSP problem has not been well exploited. We show that the OCOwK problem is closely related to the OSP problem through Lagrangian duality; thus, we are able to apply our results for the OSP problem to the OCOwK problem.

In the OCOwK problem, a decision maker is endowed with a fixed budget of resource at the beginning of periods. In each period , the decision maker chooses an action , and then Nature reveals a reward function and a budget consumption function . The objective is to maximize total reward while keeping the total consumption within the given budget.

The OCOwK model also generalizes the standard OCO problem by having an additional budget constraint. Additionally, it also has a wide range of practical applications (see more discussion in [10]), some notable examples include:

-

•

Dynamic pricing: a retailer is selling a fixed amount of goods in a finite horizon. The actions correspond to pricing decisions, the reward is the retailer’s revenue, and the budget represents finite item inventory. The reward functions are unknown initially due to high uncertainty in customer demand.

-

•

Online ad auction: a firm is bidding for advertising on a platform (e.g. Google) with limited daily budget. The actions refer to auction bids, and the reward represents impressions received from displayed ads. The reward function is unknown because the firm is unaware of other firms’ bidding strategies.

-

•

Crowdsourcing: suppose an organization is purchasing labor tasks on a crowdsourcing platform (e.g. Amazon Mechanical Turk). The actions correspond to prices offered for each micro-task, and the budget corresponds to the maximum amount of money to be spent on acquiring these tasks. The reward functions are unknown a priori because of uncertainty in the crowd’s abilities.

1.1 Main Contributions

We first propose an algorithm called SP-FTL (Saddle-Point Follow-the-Leader) for the online saddle point problem when the payoff function is Lipschitz continuous and strongly-convex in and strongly-concave in , the algorithm has a SP-regret that scales as , which is optimal. When the payoff functions are convex-concave we show that a variant of SP-FTL attains a SP-Regret that scales as , which matches the lower bound of up to a logarithmic factor. In the special case where the payoff functions are bilinear and the decision sets are the probability simplex, a setup which we call Online Matrix Games, we show that a variant of SP-FTL can attain SP-Regret that scales almost optimally with and logarithmically with the dimension of the problem. This is in contrast to the general convex-concave case where the SP-Regret scales linearly with the dimension of the problem. We also study Online Matrix Games under bandit feedback. Here the players only observe the loss function evaluated at their decisions instead of observing the whole payoff function, this makes the problem significantly more challenging. For this setting we derive an algorithm that attains sublinear SP-Regret.

In addition, we show that no algorithm can simultaneously achieve sublinear (i.e. ) SP-Regret and sublinear individual-regrets (defined in (1) and (2)) in the general OSP problem. This impossibility result further illustrates the contribution of the SP-FTL algorithm, as existing OCO algorithms designed to achieve sublinear individual-regret are not able to achieve sublinear SP-Regret.

Then, we consider the OCOwK problem. We show that this problem is related to the OSP problem by Lagrangian duality, and a sufficient condition to achieve a sublinear regret for OCOwK is that an algorithm must have both sublinear SP-Regret and sublinear individual-regret for the OSP problem. In light of the previous impossibility result, we consider the OCOwK problem in a stochastic setting where the reward and consumption functions are sampled i.i.d. from some unknown distribution. By applying the SP-FTL algorithm and exploiting the connection between OCOwK and OSP problems, we obtain a regret. We then propose a new algorithm called PD-RFTL (Primal-Dual Regularized-Follow-the-Leader) that achieves an regret bound. The result matches the lower bound for the OCOwK problem in the stochastic setting. We then provide numerical experiments to compare the empirical performances of SP-FTL and PD-RFTL.

2 Literature Review

Saddle point problems emerge from a variety of fields such as machine learning, statistics, computer science, and economics. Some applications of the saddle point problem include: minimizing the maximum of smooth convex functions, minimizing the maximal eigenvalue, -minimization (an important tool in sparsity-oriented Signal processing), nuclear norm minimization, robust learning problems, and two-player zero-sum games [48, 42, 27, 6, 46, 41, 25, 39].

We now discuss some related works that focus on learning in games. [53] study a two player, two-action general sum static game. They show that if both players use Infinitesimal Gradient Ascent, either the strategy pair will converge to a Nash equilibrium (NE), or even if they do not, then the average payoffs are close to that of the NE. A result of similar flavor was derived in [23] for any zero-sum convex-concave game. Given a payoff function , they show that if both players minimize their individual-regrets, then the average of actions will satisfy as , where is a NE. [16] improve upon the result of [53] by proposing an algorithm called WoLF (Win or Learn Fast), which is a modification of gradient ascent; they show that the iterates of their algorithm indeed converge to a NE. [26] further improve the results in [53] and [15] by developing an algorithm called GIGA-WoLF for multi-player nonzero sum static games. Their algorithm learns to play optimally against stationary opponents; when used in self-play, the actions chosen by the algorithm converge to a NE. More recently, [11] studied general multi-player static games and show that by decomposing and classifying the second order dynamics of these games, one can prevent cycling behavior to find NE. We note that unlike our paper, all of the papers above consider repeated games with a static payoff matrix, whereas we allow the payoff matrix to change arbitrarily. An exception is the work by [35], who consider the same setting as our OMG problem; however their paper only shows that the sum of the individual regrets of both players is sublinear and does not study SP-Regret.

Related to the OMG problem with bandit feedback is the seminal work of [29]. They provide the first sublinear regret bound for Online Convex Optimization with bandit feedback, using a one-point estimate of the gradient. The one-point gradient estimate used in [29] is similar to those independently proposed in [54]. The regret bound provided in [29] is , which is suboptimal. In [2], the authors give the first bound for the special case when the functions are linear. More recently, [34] and [18] designed the first efficient algorithms with regret for the general online convex optimization case; unfortunately, the dependence on the dimension in the regret rate is a very large polynomial. Our one-point matrix estimate is most closely related to the random estimator in [8] for linear functions. It is possible to use the more sophisticated techniques from [2, 34, 18] to improve our SP-Regret bound in Section 5.1; however, the result does not seem to be immediate and we leave this as future work.

The Online Convex Optimization with Knapsacks (OCOwK) problem studied in this paper is related to several previous works on constrained multi-armed bandit problems, online linear programming, and online convex programming. We next give an overview of the work related to OCOwK . Agrawal et al. [5] and Agrawal and Devanur [4] consider online linear/convex programming problems. A key difference between the online linear/convex programming problems and the OCOwK problem is that we assume the action must be chosen without knowledge of the function associated with the current iteration. In [5, 4], it is assumed that these functions are revealed before the action is chosen. Related work is that of Buchbinder and Naor [20], where they study an online fractional covering/packing problem, and that of Gupta and Molinaro [30] where they consider a packing/covering multiple choice LP problem in a random permutation model. Another relevant paper is [40] where the authors provide an algorithm to solve convex problems with expectation constraints, such as the benchmark in Section 7. However it is unclear if their optimization algorithm has any sublinear regret properties.

Mannor et al. [45] consider a variant of the online convex optimization (OCO) problem where the adversary may choose extra constraints that must be satisfied. They construct an example such that no algorithm can attain an -approximation to the offline problem. In view of such result, several papers [44, 47, 56] study problems similar to [45] with further restrictions on how constraints are selected by the adversary. The objective in this line of work is to choose a sequence of decisions to achieve the offline optimum while making sure the constraints are (almost) satisfied. In this line of research, the most relevant work to ours is that of [47]. They study OCO with time-varying constraints, the model is similar to that of [45], however in view of the existing 3 negative results they consider three different settings. In the first one, both the cost functions and the constraints are arbitrary sequences of convex functions, however in view of the negative result from [45], the constraints must all be non positive over a common subset of . In the second setting the sequences of loss functions remain adversarially chosen however the constraints are sampled i.i.d. from some unknown distribution. Finally, in the third setting both the sequences of loss functions and constraints are sampled i.i.d. from some unknown distribution. They develop algorithms for all the three different settings that ensure the total loss incurred by the algorithm is not too far from the offline optimum and such that the constraints are almost satisfied. The setup and results are different than ours because they only require the cumulative constraint violation to be sublinear whereas in OCOwK, once the player exceeds the budget it can no longer collect rewards. Closely related is the problem of “Online Convex Optimization with Long Term Constraints”. The setup is similar to that of OCO where the functions are chosen adversarially with the difference that it is not required that the decisions the player makes at each step belong to the set. Instead, it is required that the average decision lies in the set (which is fully known in advance). As the authors explain, this problem is useful to avoid the projection step of online gradient descent (OGD) and it allows to solve problems such as multi-objective online classification [13], and for using the popular online-to-batch conversion. The algorithms they develop consist of simultaneously running two copies of variants of OGD on convex-concave functions. Better rates and slightly different guarantees were obtained for the same problem in [58, 37, 57]. In [50], the authors study a continuous time version of a problem similar to that of [44] and show that a continuous time version of primal-dual online gradient descent in continuous time guarantees small regret. Motivated by an application in low-latency fog computing, [24] consider a problem similar to that in [43] however there is bandit feedback in the loss function. The algorithm proposed in [24] is primal-dual online gradient descent that combines ideas from [29] to deal with bandit feedback.

Most closely related to our model is the Bandits with Knapsacks problem studied by Badanidiyuru et al. [10] and Wu et al. [55]. In this problem, there is a finite set of arms, and each arm yields a random reward and consumes resources when it is pulled. The goal is to maximize total reward without exceeding a total budget. The Bandits with Knapsacks problem can be viewed as a special case of the OCOwK problem, where the reward and consumption functions are both linear. Agrawal and Devanur [3] study a generalization of bandits with concave rewards and convex knapsack constraints. Similar problems have also been studied in specific application contexts, such as online ad auction [12] and dynamic pricing [14, 28]. Recently, [36] study an adversarial version of the multi-armed bandits with knapsack problem. A key part of their algorithm uses a primal-dual approach similar to the one we propose in Section 7.

3 Preliminaries

We introduce some notation and definitions that will be used in later sections. By default, all vectors are column vectors. A vector with entries is written as , where denotes the transpose. Let be any norm of a vector; the ones we will frequently use are .

We say a function is convex-concave if it is convex in , for every fixed , and concave in , for every fixed . A pair is called a saddle point for if for any and any , we have

| (3) |

It is well known that if is convex-concave, and and are convex compact sets, there always exists at least one saddle point (see e.g. [17]).

We say that a function is -strongly convex if for any , it holds that

Here, denotes a subgradient of at . Strong convexity implies that the problem has a unique solution. We say a function is -strongly concave if is -strongly convex.

Furthermore, we say a function is -strongly convex-concave if for any fixed , the function is -strongly convex in , and for any fixed , the function is -strongly concave in . If is -strongly convex-concave, then there exists a unique saddle point.

We say a function is -Lipschitz continuous with respect to norm , if

It is well known that the previous inequality holds if and only if

for all , where is the norm dual to (see Lemma 2.6 in [51]).

Throughout the paper we will use the big notation to hide constant factors. For two functions and , we write if there exists a constant and a constant such that for all ; we write if there exists a constant and a constant such that for all . We use the notation to hide constant factors and poly-logarithmic factors. More specifically, for two functions and , we write if there exists constants , and an integer such that for all .

4 The Online Saddle Point Problem

4.1 The Strongly Convex-Concave Case

We now present algorithms for the OSP problem with guaranteed sublinear SP-Regret. Recall that the SP-regret defined in (1) measures the gap between the cumulative value achieved by an online algorithm and the value of the game under the Nash equilibrium if all functions are known in hindsight.

For simplicity we assume is known in advance (this assumption can be relaxed using the well known doubling trick from [22, 51]). We first consider the case where the functions are strongly convex-concave. We show that the following simple algorithm Saddle-Point Follow-the-Leader (SP-FTL), which is a variant of the Follow-the-Leader (FTL) algorithm by Kalai and Vempala [38], attains sublinear SP-Regret.

The main difference between SP-FTL and FTL is that in SP-FTL both players update jointly and play the (unique) saddle point of the sum of the games observed so far. In contrast, the updates for Follow-the-Leader would be and for and , are arbitrarily chosen from their respective sets and . It is easy to see that the sequence of iterates is in general not the same. In fact, in view of Theorem 6 we will see that FTL can not achieve sublinear when the sequence of functions is chosen arbitrarily.

Theorem 1.

Let be any sequence of -strongly convex-concave, -Lipschitz functions. Then, the - algorithm guarantees

We remark that since Theorem 1 holds against all sequences of functions , this means that the sequence can even be chosen by an adaptive adversary. In particular, this means that can be a function of all the previous iterates .

The proof of Theorem 1 is based on the following two lemmas. We first analyze a quantity that is similar to SP-Regret, but with actions replaced by (Lemma 1). This analysis framework is known as the Follow-the-Leader vs. Be-the-Leader scheme [38]. We then show that consecutive iterates of SP-FTL have distances diminishing proportionally to . The proof heavily utilizes the KKT conditions associated with points and (Lemma 2).

Lemma 1.

Let be an arbitrary sequence of convex-concave functions that are -Lipschitz with respect to norm . Here, , where and are convex compact sets. Let be the iterates of - when run on the sequence of functions . It holds that

| (4) |

Proof.

Proof. We first prove the second inequality, namely

We proceed by induction. The base case holds by definition of :

We now assume the following claim holds for ,

| (5) |

and show it holds for . By definition of , we have

The first inequality holds because is the saddle point of , so is a maximizer for function , see Equation (3). Similarly, the second inequality follows since is the saddle point of . By the induction hypothesis, see Equation (5), and the definition of we have

This proves the second inequality in the lemma.

Using a similar argument, we now show by induction the first inequality in the statement of the lemma, namely that

Indeed, follows from the definition of :

We now assume the following claim holds for ,

| (6) |

and prove it for . By definition of , we have

The first inequality holds because is the saddle point of , so is a minimizer of , see Equation (3). Similarly, the second inequality follows since is the saddle point of so is the maximizer of .

By the induction hypothesis (see Equation (6)) and the definition of , we have

This concludes the proof. ∎

Lemma 2.

Let be an arbitrary sequence of -strongly convex-concave functions (with respect to norm ) which is also -Lipschitz with respect to the same norm. Let be the iterates of - run on the sequence . It holds that

Proof.

Proof. Consider a fixed period . Define

so that is a saddle point of . Since is -strongly convex it holds that for any and any

Plugging in and recalling the KKT condition (see Chapter 2 in [31]), we have that for any

| (7) |

Similarly, since is -strongly concave, for any we have

Together with the KKT condition , we get that for any

| (8) |

Adding up Equations (7) and (8), plugging and , we get

Plugging in the definition of function , we get

Since is the saddle point of , it holds that . Therefore, we have

Additionally, since is the saddle point of , it holds that . This implies

Notice the two summations cancel, thus

Since is -Lipschitz with respect to norm , it holds that

which then implies that

Rearranging the terms of the inequality above, we get

For any , we have , which implies

Therefore, we have

Rearranging the terms, we get

This concludes the proof.

∎

Now we are ready to prove Theorem 1.

4.2 The General Convex-Concave Case

In this section we propose an algorithm to solve the online Saddle Point Problem in the full information setting when the payoff functions are arbitrary convex-concave Lipschitz functions, and the action sets of Player 1 and Player 2 ( and respectively) to be arbitrary convex compact sets.

Let the sequence of convex-concave functions be , which are -Lipschitz with respect to some norm . We propose an algorithm called Saddle Point Regularized Follow the Leader (SP-RFTL), shown in Algorithm 2.

The regularizers are used as input for the algorithm. We will choose regularizers that are strongly convex with respect to norm , and and Lipschitz with respect to norm , which means that for all , and for, all . Finally, we assume for all and for all .

We have the following guarantee for SP-RFTL.

Theorem 2.

Let and be convex and compact sets. Let be any sequence of convex-concave functions. For , let be -Lipschitz with respect to norm . Let , be two strongly convex regularization functions with respect to the same norm, and let be the Lipschitz constants of , . Let be the iterates generated by SP-RFTL when run on the sequence . It holds that

where is the parameter chosen in Algorithm 2.

As a corollary, we have the following result that shows our algorithm guarantees a sublinear SP-Regret.

Corollary 1.

Let and be convex and compact sets containing the origin such that for some . Let and . For , let be -Lipschitz with respect to norm . Setting in SP-RFTL guarantees

where the notation hides an absolute constant.

We note that the bound in Corollary 1 is optimal up to the factor. This is because our setup is a special case of Online Convex Optimization and there is a known lower bound , see Chapter 3 in [31]. In our setup if is bilinear, that is for some matrix with bounded entries, and are unit boxes of dimensions and respectively, we have and so our SP-Regret bound becomes .

Remark 1 (Computational Complexity).

Although the focus of our work is mainly concerned with showing sublinear rate of SP-Regret, it is worth discussing the computation complexity for each iteration of our algorithms. Notice that in each iteration we must solve a strongly convex strongly concave constrained saddle point problem. It is well known that by simultaneously playing two no Individual Regret algorithms for strongly convex functions (such as those in [32] which achieve Individual Regret , one can generate after rounds a solution to the problem that is close to the Nash equilibrium (in terms of the value of the game) (See Theorem 9 in [1]). Recently [1] showed that with additional smoothness assumptions it is possible to obtain linear convergence rates for some static saddle point problems. It is also possible to solve the subproblem for each iteration using the (Stochastic Approximation) Mirror Descent algorithm from [49]. All the previously discussed algorithms are variants of the seminal work of [7].

In the rest of this subsection we will prove Theorem 2. Define . Notice that it is -strongly convex in with respect to norm for all and -strongly concave with respect to norm for all . Additionally, notice that is -Lipschitz with respect to norm . Finally, notice that by nonnegativity of and for , all and all it holds that

| (9) |

The following lemma shows that the value of the convex-concave games defined by and are not too far from each other.

Lemma 3.

Let , be convex and compact sets. Let be any sequence of convex-concave functions where for all . Let

It holds that

Proof.

Proof of Lemma 3.

We will first show that

Plugging in the definition of , we have

where the first inequality holds since is the saddle point of and thus is the minimizer of see Equation (3). The second inequality holds since is a saddle point of , and thus is the maximizer of , see Equation (3). By definition of , we have

where the inequality holds by nonnegativity of .

Using a similar argument we now show that

Plugging in the definition of , we have

where the first inequality holds since is a saddle point of and thus is a maximizer of , see Equation (3). The second inequality holds since is a saddle point of thus is a minimizer of , see Equation (3).

By definition of , we have

where the inequality holds by nonnegativity of . This concludes the proof. ∎

To prove the SP-Regret bound, we note that SP-RFTL is running SP-FTL on functions so the proof will be similar to that of Theorem 1.

Proof.

Proof of Theorem 2. We first prove one side of the inequality.

| since is -Lipschitz | ||

Applying Lemma 2 using and , we have

This completes the proof for one side of the inequality. We now prove the other side of the inequality.

| since is -Lipschitz | ||

Applying Lemma 2 using and , we have

This concludes the proof.

∎

5 Online Matrix Games

In Section 4, we analyzed the OSP problem by treating the payoff functions as general convex-concave functions and the action spaces as general convex compact sets. We explained that, in general, one should expect to achieve SP-Regret which depends linearly in the dimension of the problem (see discussion after Corollary 1).

In this section, we consider a special case of the OSP problem with bilinear payoff functions, which we call Online Matrix Games (OMG). In this setting, player 1 has available actions and player 2 has available actions. At each time step , the payoff of the players will be given by a payoff matrix , where the -th entry specifies the loss of player 1 and the reward of player 2 when they choose actions and respectively. We allow the players to choose probability distributions over their available actions. That is, the decision sets of player 1 and player 2 are the probability simplexes, and , respectively. Here denotes the probability simplex over actions, that is , is defined similarly. Notice that this is a special case of the OSP problem studied in Section 4, where the convex-concave function is defined as , which specifies the expected payoff for the players when they choose distributions .

Our goal in this section is to obtain sharper SP-Regret bounds that scale logarithmically in the dimensions and . This will allow us to solve games that may have exponentially many actions, which often arise in combinatorial optimization settings.

To achieve this goal, we exploit the geometry of the probability simplexes and the bilinear structure of the payoff functions. We use the negative entropy as a regularization function (which is strongly convex with respect to ), that is and where the extra logarithmic terms ensure are nonnegative everywhere in their respective simplexes. Unfortunately, the negative entropy is not Lipschitz over the simplex, so we can not leverage our result from Theorem 2. To deal with this challenge, we will restrict the new algorithm to play over a restricted simplex:111We will also use the notation and to mean the restricted simplex of Player 1 and 2, respectively

| (10) |

The tuning parameter used for the algorithm will be defined later in the analysis. (Notice that when , the set is empty). We have the following result.

Lemma 4.

The function is -Lipschitz continuous with respect to over with .

Proof.

Proof of Lemma 4. We need to find such that for all . Notice that for . Moreover, since for every we have the following sequence of inequalities hold: . It follows that . ∎

The algorithm Online-Matrix-Games Regularized-Follow-the-Leader (OMG-RFTL) is an instantiation of SP-RFTL with a particular choice of regularization functions, which are nonegative and Lipschitz with respect to the norm over the sets , . With this, we can prove a SP-Regret bound for the OMG problem. For the remainder of the section, the regularization functions will be set as follows:

We have the following guarantee for OMG-RFTL.

Theorem 3.

Let be an arbitrary sequence of matrices in . Let be the Lipschitz constant (with respect to ) of for . Let be the iterates of OMG-RFTL and choose such that . By setting in Algorithm 3, it holds that

To prove the theorem, we require a few intermediate results. Since Algorithm 3 selects actions over a restricted simplex, we must quantify the loss in the SP-Regret bound imposed by this restriction. The next two lemmas make this precise.

Lemma 5.

Let define , with . Notice is unique since it is a projection. It holds that .

Proof.

Proof of Lemma 5. Choose , it is easy to see that and ∎

Lemma 6.

Let be an arbitrary sequence of convex-concave functions, , that are -Lipschitz with respect to . It holds that

Proof.

Proof of Lemma 6. Let be any saddle point pair for with . Let be any saddle point pair for with . Let be the projection of onto respectively, using the norm. We first show the second inequality.

Since is a saddle point for over and , and Player 1 deviated to , we have

where the last inequality holds since is a saddle point for over and .

To show the first inequality in the statement of the lemma, by using similar argument, we have

This concludes the proof. ∎

Combining the previous two lemmas and Theorem 2, we can show the SP-Regret bound for OMG-RFTL holds. We are ready to prove Theorem 3.

Proof.

Proof of Theorem 3. For convenience, we define . Let be any saddle point of , and let be the respective projections onto using norm. Using Lemma 5, Lemma 6 and Theorem 2, we have

By Lemma 4, we know that . Our choice of will ensure that , so . Therefore, we have

where the last inequality holds by the choice of .

Notice that . Therefore, we have

The last line follows because , since each entry of is bounded between .

We now prove the other side of the inequality:

where the last inequality holds by the choice of . Again, notice that . We have

The last line follows because , since each entry of is bounded between . This concludes the proof. ∎

5.1 Online Matrix Games with Bandit Feedback

The results we proved for the OMG problem can be extended to a setting with bandit feedback. In the bandit setting, the players observe in every round only the payoff corresponding to the chosen actions. In other words, if Player 1 chooses action , Player 2 chooses action , and the payoff matrix at that time step is , then the players observe only instead of the full matrix . The limited feedback makes the problem significantly more challenging than the full information one, as the players must balance the exploration-exploitation tradeoff. This problem resembles that of Online Bandit Optimization [29, 8, 18, 34], albeit with two players.

For convenience, we define some useful notation. For , let be the collection of standard unit vectors i.e. is the vector that has a in the -th entry and in the rest. Let be the standard unit vector corresponding to the decision made by Player 1 for round , define similarly. Notice that under bandit feedback, in round both players only observe the quantity .

5.1.1 One-Point Estimate for Payoff Function

As explained previously, in each round the players must estimate by observing only one of its entries. To this end, we allow the players to share with each other their decisions and to randomize jointly (a similar assumption is used to define correlated equilibria in zero-sum games, see [9]). The following result shows how to build a random estimate of by observing only one of its entries.

Theorem 4.

Let with and . Sample . Let be the matrix with for all such that and and . It holds that

Proof.

Proof of Theorem 4. Let be the matrix of zeros everywhere except in the entry where it is equal to . We have

∎

5.1.2 Algorithm under Bandit Feedback

We now present an algorithm that ensures sublinear (i.e. ) SP-Regret under bandit feedback for the OMG problem that holds against an adaptive adversary. By adaptive adversary, we mean that the payoff matrices can depend on the players’ actions up to time ; in particular, we assume the adversary does not observe the actions chosen by the players for time period when choosing . We consider an algorithm that runs OMG-RFTL on a sequence of functions , where is the unbiased one-point estimate of derived in Theorem 4. Recall that the iterates of OMG-RFTL algorithm are distributions over the possible actions of both players. In order to generate the estimate , both players will sample an action from their distributions and weigh their observation with the inverse probability of obtaining that observation.

We have the following guarantee for Bandit-OMG-RFTL.

Theorem 5.

Let be any sequence of payoff matrices chosen by an adaptive adversary, where for all . Let be the iterates generated by Bandit-OMG-FTRL. Setting , ensures

where the expectation is taken with respect to all the randomization used in the algorithm.

The full proof of this Theorem will be given shortly. We now present a few lemmas. The total payoff given to each of the players is given by so we must relate this quantity to the iterates of OMG-RFTL when run on sequence of matrices . The following two lemmas will allow us to do so.

Lemma 7.

Let be the sequence of iterates generated by Bandit-OMG-RFTL. It holds that

where the expectation is taken with respect to the internal randomness of the algorithm.

Proof.

Proof of Lemma 7. Let be the expectation of random variable conditioned on all the randomness from time steps .

Since the adversary can can not observe when selecting , and are all independent from each other, thus it holds that . Therefore

Repeating the argument more times yields the result. ∎

Lemma 8.

Let be any sequence of payoff matrices chosen by an adaptive adversary, where for all . Let be generated by Bandit-OMG-FTRL. It holds that

where the expectation is with respect to all the internal randomness of the algorithm.

Proof.

We will then bound the difference between the comparator term and the comparator term Theorem 3 gives us by running OMG-RFTL on functions and sets , . Special care must be taken to ensure this difference holds even against an adaptive adversary. To this end, we use the next two lemmas; as we will see, the proof of Lemma 10 relies heavily on Theorem 4.

Lemma 9.

With probability 1, for any , it holds that

Proof.

Proof of Lemma 9. Let us fist bound for any and with probability 1. For any and we have

This implies that

which implies that

Therefore, it holds that

Thus

Since (the function is convex-concave and the sets and are convex and compact), we have shown that

The other side of the inequality follows from a similar argument. Indeed we know that

The previous inequality implies that

or

Therefore, we have

Since we get the result. ∎

Lemma 10.

Let be any sequence of payoff matrices chosen by an adaptive adversary, where with for all . Let be the sequence of matrices generated by Bandit-OMG-RFTL. For any , it holds that

where the expectation is taken with respect to the internal randomness of the algorithm.

Proof.

Proof of Lemma 10. For any define . We first show that for all such that it holds that . Indeed

where the second to last line follows since

Now, we have

We proceed to bound , the upper bound we obtain will also bound because of the following fact. If the random vector satisfies for some constant c with probability 1 then . Indeed by Jensen’s inequality, we have . Let us omit the subscript for the rest of the proof. Let be the -th row of matrix .

Notice the upper bound can also be obtained by interchanging the summations and repeating the argument. This yields the desired result. ∎

Before we prove Theorem 5, we need the following lemma.

Lemma 11.

Consider a matrix . If the absolute value of each entry of is bounded by , then the function is -Lipschitz continuous with respect to over the sets and , where . The function is also -Lipschitz continuous (over the same sets) with respect to norm , where .

Proof.

Proof of Lemma 11.

We now prove the second part of the claim by bounding .

By Cauchy-Schwarz inequality, for any , we have , since . Similarly, for any . This shows that . ∎

The proof of Theorem 5 follows by combining Lemmas 7 through 10, with careful choice of tuning parameters.

Proof.

The last inequality follows by the same reasoning we used in the proof of Theorem 3. Indeed are the iterates of OMG-RFTL run on the sequence of payoff functions so the same proof holds. By Lemma 11, since the absolute value of all the entries in is bounded above by 1, it holds that

where the last equality holds since we use , .

The last inequality follows by the same reasoning we used in the proof of Theorem 3. Indeed are the iterates of OMG-RFTL run on the sequence of payoff functions so the same proof holds. By Lemma 11, since the absolute value of all the entries in is bounded above by 1, it holds that

The last equality holds since we use , . This completes the proof. ∎

6 Relationship between SP-regret and Individual-regret

We have defined two regret metrics for the OSP problem, namely the SP-regret (1) and the individual-regret (2). In the previous subsection, we proposed an algorithm (SP-FTL) with sublinear SP-regret. We have also mentioned that any OCO algorithm (e.g., online gradient descent, online mirror descent, Follow-the-Leader) can achieve sublinear individual-regret. A natural question is whether there exists a single algorithm that has both sublinear SP-regret and individual-regret. Surprisingly, the answer is negative.

Theorem 6.

A formal proof of the result is shown shortly, but here we give a sketch. The main idea is to construct two parallel scenarios, each with their own sequences of payoff matrices. The two scenarios will be identical for the first periods but are different for the rest of the horizon. In our particular construction, in both scenarios the players play the well known “matching-pennies” game for the first periods, then in first scenario they play a game with equal payoffs for all of their actions and in the second scenario they play a game where Player 1 is indifferent between its actions. One can show that if all three quantities in the statement of the theorem are in the first scenario, then we prove that at least one of them is in the second one which yields the result. This suggests that the machinery for OCO, which minimizes individual regret, cannot be directly applied to the OMG problem.

We note that despite the negative result in Theorem 6, it is possible to achieve both sublinear SP-Regret and individual-regret with further assumptions on the payoff functions .

One such example is where is sampled i.i.d. ; this case is discussed in §7. However, in light of Theorem 6, in the general case where is an arbitrary sequence, the best one can hope for is achieve either SP-Regret or individual-regret, but not both. In §8.1, we include a numerical example to further illustrate the relationship between SP-Regret and individual-regret.

6.1 Proof of the Impossibility Result

We now present a formal proof of the impossibility result.

Proof.

Proof of Theorem 6. We assume there exists an algorithm such that

for all possible sequences of matrices with bounded entries between . We now construct two sequences of functions for which all the three guarantees hold and lead that to a contradiction. Let be divisible by .

In scenario 1: for and for .

In scenario 2: for and for .

It is easy to see that for both scenarios it holds that . Since and we can parametrize any as and any as for some . By assumption, we have

for all sequences of matrices . This implies for scenario 1 that

which also implies that and since is a linear function of and thus its maximum occurs at or .

For scenario 2 reduces to

which implies and . Finally, notice that implies . But from scenario 1, we have since is a contradiction we get the result.

∎

7 Online Convex Optimization with Knapsacks

In this section, we consider the online convex optimization with knapsacks (OCOwK) problem. This problem is motivated by various applications in dynamic pricing, online ad auctions, and crowdsourcing (see [10] and discussion in §1). The OCOwK model generalizes the standard OCO framework by having an additional set of resource constraints. We will show that OCOwK is closely related to the OSP problem studied in §4.

In the OCOwk problem, the decision maker has a set of resources with given budgets . There are time periods. At each time period, the decision maker chooses , where is a convex compact set. After the decision is chosen, Nature reveals two functions: a concave reward function , which is assumed to be -Lipschitz (with respect to ), and a vector-valued resource consumption function , where each entry of is a convex, -Lipschitz function (with respect to ).

The objective is to maximize cumulative reward while satisfying the budget constraints. In particular, we assume that if a decision violates any of the budget constraints, no reward is collected at period . Therefore, the decision maker’s cumulative reward is given by

| (14) |

where denotes the indicator function. In (14), if , the problem reduces to the standard OCO setting. In the special case where and are linear functions, our problem is related to the Bandits with Knapsack (BwK) model studied in [10]. A similar problem with general concave reward and convex constraints is studied by [3]. However, unlike our model, both of these papers assume bandit feedback.

In order to guarantee that the budget constraint can always be satisfied, we assume there exists a “null action” that doesn’t consume any resource or generate any reward.

Assumption 1.

There exists an action such that and for all .

The “null action” assumption is often satisfied in real-world applications of OCOwK. For example, in dynamic pricing, the “null action” is equivalent to charging an extremely high price so there is no customer demand; in online auctions (see [12]), the “null action” corresponds to bidding at $0.

If the reward and consumption functions are chosen arbitrarily, it can be shown that no algorithm can achieve sublinear regret for OCOwK. Intuitively, if the reward and consumption functions shift at , no algorithm can recover the mistake made before in the remaining periods (which is similar to the case in §6). Therefore, we consider the setting where the reward and consumption functions are stochastic.

Assumption 2.

For , the reward function and consumption function are sampled i.i.d. from a fixed and unknown joint distribution.

Notice that even when the reward and consumption distribution is known, the optimal policy for the OCOwK problem is not a static decision, as the optimal decision depends on the remaining time and remaining budget. Therefore, defining the offline benchmark for OCOwK is not as straightforward as in the stochastic OCO setting. However, it has been shown in the literature that the following offline convex problem provides an upper bound of the expected reward of the optimal offline policy under Assumption 2 (see e.g. [10, 14]):

| (15) |

Therefore, we define the expected regret for the OCOwK problem as

where the expectation is taken with respect to the random realizations of functions and .

7.1 Reduction to a Saddle Point Problem

We relate the OCOwK problem to the OSP problem studied in §4 by defining the function

| (16) |

with . Note that is convex in and concave in , so we can treat as a payoff function in the OSP problem. Here, can be viewed as the dual prices associated with the budget constraints in (15), and the function penalizes the payoff if consumption at iteration exceeds the average budget per period.

We let constant be the maximum reward that can be gained by adding one unit of resource (), and define set . Namely, is an upper bound on the dual variables for problem (15). We also define vector . For any sequence of decisions , we claim that the decision maker’s total reward is bounded by

| (17) |

To see this, consider a modified OCOwK problem where resource consumption is allowed to go over the budget, but the decision maker must pay for each additional unit of resource used over . By the definition of , the decision maker’s profit under the modified problem is given by the right-hand side of (17), which can be no more than the reward in the original problem.

We now consider the benchmark (15). By Assumption 1, the Slater condition holds for the convex optimization problem (15); so by using strong duality, we have

Therefore, the expected regret for OCOwK is bounded by

| (18) |

We have bounded the regret of the OCOwK problem by two quantities in a related OSP problem. In particular, the term is equal to the expectation of player 2’s individual-regret (see Eq (2b)), and the second term is related to the SP-Regret.

7.2 Algorithms for OCOwK

Motivated by its connection to the OSP problem, we propose two algorithms for the OCOwK problem. For clarity we defer all proofs to the next two subsections.

First, we consider SP-FTL defined in Algorithm 1. In view of Eq (18), we can bound the regret for OCOwK by the sum of an individual-regret and the SP-Regret. Theorem 2 has already provided a SP-Regret bound for SP-FTL, so we just need to prove a sublinear individual-regret bound. In general, this is impossible due to the negative result in Theorem 6. However, since we made the additional assumption that and are sampled i.i.d., we are able to get a sublinear individual-regret for SP-FTL in the OCOwK problem.

We start by establishing a high probability bound on the individual-regret for the general OSP problem when the payoff function is strongly convex-concave.

Lemma 12.

Let be an i.i.d. sequence of functions that is -strongly convex-concave with respect norm , and -Lipschitz continuous with respect norm . Here . Let be the dimension of , and be some constant such that . SP-FTL run on the sequence of functions guarantees that with probability at least

The proof of Lemma 12 uses a concentration inequality for Lipschitz functions by Shalev-Shwartz et al. [52]. The key step in the proof is to show that the solution of the sample average approximation at step i.e. is close to , the saddle point of the expected game.

However, we cannot directly use Lemma 12 to bound the individual-regret term in (18) because the function is linear in and thus not strongly convex-concave. We add a regularization term to to make it -strongly convex-concave. Notice our choice of the regularization term here is not the same as in Theorem 2, which leads to a bound in the following theorem.

Theorem 7.

Let be a convex compact set. Let be an i.i.d. sequence of concave reward functions with which is -Lipschitz with respect to norm . Let be an i.i.d. sequence of vector-valued functions with where each entry of is convex in and -Lipschitz with respect to norm . Let be defined as in equation (16). Define , where . Applying the SP-FTL algorithm on functions guarantees that with probability at least it holds that

where is defined in the proof of the theorem. Additionally, for the OCOwK problem, with probability at least it holds that

Next, we present an algorithm for OCOwK that improves the regret bound in Theorem 7. The key idea of this algorithm is to update primal variable and dual variable of in parallel. Each variable can be updated using any algorithm for Online Convex Optimization such as Online Gradient Descent [59] or Regularized Follow the Leader [32, 31]. We call this algorithm Primal-Dual Regularized-Follow-the-Leader (PD-RFTL) (see Algorithm 5).

We will bound the regret of PD-RFTL using Eq (18). Before we proceed we state the well known individual-regret guarantee of RFTL.

Lemma 13 (Adapted from [31] Ch. 5).

Let be any sequence of convex and -Lipschitz functions where and is a convex compact set such that . The RFTL algorithm: , guarantees that

Recall that for SP-FTL, it was more challenging to bound the first term and relatively easy to bound the term . For PD-RFTL it is quite the opposite. By defining , the first term can be written as , so we immediately have using the regret bound for Regularized Follow-the-Leader in the OCO setting. To bound the second term , we have the following result.

Theorem 8.

Let be a convex compact set. Let be an i.i.d. sequence of concave reward functions with which is -Lipschitz with respect to norm . Let be an i.i.d. sequence of vector-valued functions with where each entry of is convex in and -Lipschitz with respect to norm . PD-RFTL run with guarantees that

Compared to other algorithms for OCOwK, including the UCB-based algorithm in [10, 3] and Thompson sampling-based algorithm in [28], the proof for Theorem 8 is surprisingly simple, as we are able to exploit the connection between OCOwK and the OSP problem.

The regret bound in Theorem 8 also gives the best possible rate in , since OCO is a special case of OCOwK, and it is well-known that any algorithm must have regret for the general OCO problem. In Section 8.2, we compare the performance of SP-FTL and PD-RFTL in a numerical experiment.

Remark 2.

Our proof for Theorem 8 allows the RFTL subroutine in Algorithm 5 to be replaced with other OCO algorithms with regret. In addition, we can extend Algorithm 5 to the bandit setting of OCOwK, where we only observe the values and after is chosen. By replacing the RFTL subroutine with any Bandit Convex Optimization (BCO) algorithm [19], we can also establish sublinear regret bounds for OCOwK in the bandit setting.

7.3 Proof of SP-FTL for OCOwK

In this section we present the analysis of SP-FTL, applied to the OCOwK problem. The following result from Shalev-Shwartz et al. [52] (Theorem 5) will be useful.

Theorem 9 ([52]).

Let be -Lipschitz in with respect to norm , where is bounded set such that there exists a constant such that . Then with probability at least , for all , it holds that

First, we prove the following lemma.

Lemma 14.

Let be a sequence of i.i.d. functions which are -strongly convex concave with respect and -Lipschitz with respect to norm . Here , where , are convex compact sets. Let be the the iterates of SP-FTL when run on functions . With probability at least , for any it holds that

| (19) |

where is a constant such that and is the dimenssion of .

Proof.

Proof. Define the concentration error at time as

| (20) |

Notice that satisfies all the assumptions of Theorem 9, so with probability at least , for all we have

| (21) |

We now derive some consequences of this fact. Recall that and is the saddle point of . With probability at least .

| by definition of | ||||

| by Equation (21) | ||||

| by definition of |

This implies that

| (22) |

We now show that

| (23) |

Indeed, it holds that

| by Equation (21) | ||||

Now, using the fact that is the saddle point of , which is -strongly convex, we have

It follows that

∎

Proof.

Proof of Lemma 12. For all , it holds that

It follows that

| (by definition of ) | |||

Subtracting in both sides , we get

By Lemma 14, and a simple union bound, we have that with probability at least

Therefore, with probability at least it holds that

Setting yields the result.

∎

We are ready to prove Theorem 7.

Proof.

Proof of Theorem 7. Recall that . If , are constants such that and , it holds that for all ,

| (24) |

Therefore, we have

Thus, by Lemma 12 it holds that with probability at least

Since

we have that with probability at least ,

where we plugged in . This concludes the first part of the proof.

We now prove the second claim. Recall from Eq (18), that

Let

Notice that we already have an upper bound for that holds with high probability, the term can be upper bounded using Theorem 2. Let us upper bound with high probability. As in the proof of Lemma 14 we know that with probability at least it holds that for all . Therefore, with probability at least , we have

This implies that with probability at least

which implies that with probability at least

Therefore it holds that with probability at least

thus we have a high probability bound for . Our high probability bound for scales as , the deterministic bound for scales as , and the high probability bound for scales as . The high probability bounds imply bounds in expectation (please see Lemmas 8 and 9 in [21] that show how to convert high probability bounds into bounds that hold in expectation). It follows that

This concludes the proof. ∎

7.4 Proof of PD-RFTL for OCOwK

In this section we present the analysis of PD-RFTL, applied to the OCOwK problem.

Proof.

Proof of Theorem 8. Notice that PD-RFTL is using two instances of RFTL. One is run on convex functions and another one on concave functions (thus the maximization and the negative sign in the regularizer). Let be the individual-regret guarantee of RFTL on functions from Lemma 13. Let be the individual-regret guarantee of RFTL on functions from Lemma 13. We have

| (25) |

and

| (26) |

Let for any . Let be the saddle point of , satisfying

| (27) |

Notice that

| (28) |

where the expectation is taken with respect to the random draw of functions . Indeed, we have

where the last equality holds since for any it holds that and is deterministic given . We have , repeating the argument more times shows that .

We are ready to prove the statement of the theorem.

By Equation (18), the above inequality implies that . Let us now bound and from above. We start with . To bound , it suffices to bound . Let be the -th entry of vector and be the -th entry of vector valued function , which by assumption is -Lipschitz continuous. We have

The previous line implies that . Let us now upper bound to obtain a bound on . Recall , and therefore we have

Plugging in we get

This concludes the proof.

∎

8 Numerical Experiments

8.1 Individual-Regret and SP-Regret

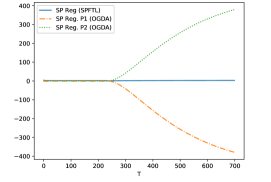

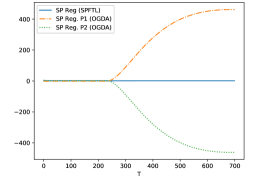

To further illustrate the relationship between SP-regret and individual-regret and the impossibility result of Theorem 6, we compare the performance of two online algorithms numerically. The first algorithm is SP-FTL defined in Algorithm 1. In the second algorithm, which we call OGDA, player 1 applies online gradient descent to function and player 2 applies online gradient ascent to function .

We generated two different instances. In both instances, we assume . The payoff functions in both instances are the same for , given by In Instance 1, for , we define In Instance 2 for , we define Since these functions are strongly convex-concave, when players use OGDA with step size , they are both guaranteed logarithmic individual-regret.

Note. Here we define the SP Regret of Player 1 (SP Reg. P1) as and the SP Regret of Player 2 (SP Reg. P2) as . According to this definition, we have SP Reg. P1SP Reg. P2, and SP-regret of OGDA is equal to SP Reg. P1SP Reg. P2.

In Figure 1, we plot the SP-regret of the two instances. On the left, it can be seen that the SP-regret of OGDA increases significantly after the payoff function switches at , while the SP-regret of SP-FTL remains small throughout the entire horizon.

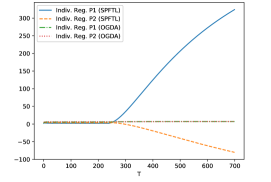

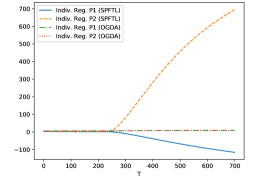

Note. The Individual Regret (Indiv. Reg.) can be negative as we compare a sequence of dynamic decisions against the best fixed decision in hindsight.

From Figure 2, we can observe when both players use the OGDA algorithm, their individual-regrets are small. However, when when they use SP-FTL, at least one player suffers from high individual-regret. Figures 1 and 2 verify Theorem 6, which states that no algorithm can achieve both sublinear SP-regret and sublinear individual-regret.

8.2 SP-FTL and OGDA for the OCOwK problem

In this section, we compare the numerical performance of SP-FTL and OGDA (Online Gradient Descent/Ascent) for solving a OCOwK problem. In OGDA, player 1 applies online gradient descent to function and player 2 applies online gradient ascent to function . The proof for Theorem 8 can also show that OGDA has a regret of (see Remark 2).

We construct a numerical example where for each iteration , the decision maker chooses an action . The reward function is where . There are two types of resources with budgets and . The consumption function for the first resource is given by where , and the consumption function for the is . We assume the budgets are some linear functions of , and respectively. In our simulations and are chosen so that playing the optimal solution to the problem without budgets is no longer optimal.

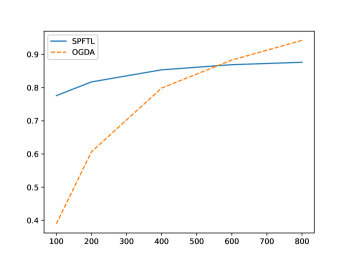

Figure 3 compares the performance of SP-FTL vs OGDA on the OCOwK instance defined above. Performance is measured as the ratio of total reward incurred by the algorithm and the solution to Equation (15) across 25 simulation runs. It can be observed that both algorithms indeed improve their performance as increases. Moreover, it can be observed that while OGDA has worse performance for small values of , the rate at which performance improves is greater than that for SP-FTL, which is consistent with our theoretical results that SP-FTL has regret and OGDA (or PD-FTL) has regret.

9 Conclusion

In this paper we introduced the Online Saddle Point problem. In this problem, we consider two players that jointly play an arbitrary sequence of convex-concave games against Nature. This problem is a generalization of the classical Online Convex Optimization problem, which focuses on a single player. The objective is to minimize the saddle-point regret (SP-Regret), defined as the absolute difference between the cumulative payoffs and the saddle point value of the game in hindsight.

We proposed an algorithm SP-FTL for the Online Saddle Point problem and showed that it achieves SP-Regret for a game with periods. In the special case where the payoff functions are strongly convex-concave, we showed that the algorithm attains SP-Regret. Furthermore, we proved that if the sequence of payoff functions are chosen arbitrarily, any algorithm with regret for the Online Convex Optimization problem may incur SP-Regret in the worst case. We also consider the special case where the payoff functions are bilinear and the decision sets are the probability simplex. In this setting we are able to design algorithms that reduce the bounds on SP-Regret from a linear dependence in the dimension of the problem to a logarithmic one. We also study the problem under bandit feedback and provide an algorithm that achieves sublinear SP-Regret. This implies that all existing algorithms for the Online Convex Optimization problem cannot be applied to the Online Saddle Point problem. Moreover, we showed how our algorithm can be applied to solve the problem of Stochastic Online Convex Optimization with Knapsacks. Finally, we performed some numerical simulations to validate our results.

References

- [1] J. Abernethy, K. A. Lai, K. Y. Levy, and J.-K. Wang. Faster rates for convex-concave games. arXiv preprint arXiv:1805.06792, 2018.

- [2] J. D. Abernethy, E. Hazan, and A. Rakhlin. Competing in the dark: An efficient algorithm for bandit linear optimization. In Proceedings of the 21st Annual Conference on Learning Theory (COLT), 2009.

- [3] S. Agrawal and N. R. Devanur. Bandits with concave rewards and convex knapsacks. In Proceedings of the fifteenth ACM conference on Economics and computation, pages 989–1006, 2014.

- [4] S. Agrawal and N. R. Devanur. Fast algorithms for online stochastic convex programming. In Proceedings of the twenty-sixth annual ACM-SIAM symposium on Discrete algorithms, pages 1405–1424, 2014.

- [5] S. Agrawal, Z. Wang, and Y. Ye. A dynamic near-optimal algorithm for online linear programming. Operations Research, 62(4):876–890, 2014.

- [6] A. Ahmadinejad, S. Dehghani, M. Hajiaghayi, B. Lucier, H. Mahini, and S. Seddighin. From duels to battlefields: Computing equilibria of blotto and other games. Mathematics of Operations Research, 44(4):1304–1325, 2019.

- [7] K. J. Arrow, L. Hurwicz, and H. Uzawa, editors. Studies in linear and non-linear programming. Stanford Unversity Press, 1958.

- [8] P. Auer, N. Cesa-Bianchi, Y. Freund, and R. Schapire. Gambling in a rigged casino: The adversarial multi-armed bandit problem. In Proceedings of the 36th Annual Symposium on Foundations of Computer Science (FOCS), page 322, 1995.

- [9] R. J. Aumann. Correlated equilibrium as an expression of bayesian rationality. Econometrica, pages 1–18, 1987.

- [10] A. Badanidiyuru, R. Kleinberg, and A. Slivkins. Bandits with knapsacks. Journal of the ACM (JACM), 65(3):13, 2018.

- [11] D. Balduzzi, S. Racaniere, J. Martens, J. Foerster, K. Tuyls, and T. Graepel. The mechanics of n-player differentiable games. arXiv preprint arXiv:1802.05642, 2018.

- [12] S. R. Balseiro and Y. Gur. Learning in repeated auctions with budgets: Regret minimization and equilibrium. Management Science, 65(9):3952–3968, 2019.

- [13] A. Bernstein, S. Mannor, and N. Shimkin. Online classification with specificity constraints. In Advances in Neural Information Processing Systems, pages 190–198, 2010.

- [14] O. Besbes and A. Zeevi. Blind network revenue management. Operations Research, 60(6):1537–1550, 2012.

- [15] M. Bowling. Convergence and no-regret in multiagent learning. In Advances in Neural Information Processing Systems, pages 209–216, 2005.

- [16] M. Bowling and M. Veloso. Convergence of gradient dynamics with a variable learning rate. In Proceedings of the Eighteenth International Conference on Machine Learning, pages 27–34, 2001.

- [17] S. Boyd and L. Vandenberghe. Convex optimization. Cambridge University Press, 2004.

- [18] S. Bubeck, Y. T. Lee, and R. Eldan. Kernel-based methods for bandit convex optimization. In Proceedings of the 49th ACM Symposium on Theory of Computing (STOC), pages 72–85, 2017.

- [19] S. Bubeck, Y. T. Lee, and R. Eldan. Kernel-based methods for bandit convex optimization. In Proceedings of the 49th Annual ACM SIGACT Symposium on Theory of Computing, pages 72–85, 2017.

- [20] N. Buchbinder and J. Naor. Online primal-dual algorithms for covering and packing. Mathematics of Operations Research, 34(2):270–286, 2009.

- [21] A. R. Cardoso and H. Xu. Risk-averse stochastic convex bandit. In K. Chaudhuri and M. Sugiyama, editors, Proceedings of Machine Learning Research, volume 89 of Proceedings of Machine Learning Research, pages 39–47. PMLR, 16–18 Apr 2019.

- [22] N. Cesa-Bianchi and G. Lugosi. Prediction, Learning, and Games. Cambridge university press, 2006.

- [23] N. Cesa-Bianchi, Y. Mansour, and G. Stoltz. Improved second-order bounds for prediction with expert advice. Machine Learning, 66(2-3):321–352, 2007.

- [24] T. Chen and G. B. Giannakis. Harnessing bandit online learning to low-latency fog computing. In 2018 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP), pages 6418–6422. IEEE, 2018.

- [25] S. M. Chowdhury, D. Kovenock, and R. M. Sheremeta. An experimental investigation of colonel blotto games. Economic Theory, 52(3):833–861, 2013.

- [26] V. Conitzer and T. Sandholm. Awesome: A general multiagent learning algorithm that converges in self-play and learns a best response against stationary opponents. Machine Learning, 67(1-2):23–43, 2007.

- [27] B. Cox, A. Juditsky, and A. Nemirovski. Decomposition techniques for bilinear saddle point problems and variational inequalities with affine monotone operators. Journal of Optimization Theory and Applications, 172(2):402–435, 2017.

- [28] K. J. Ferreira, D. Simchi-Levi, and H. Wang. Online network revenue management using Thompson sampling. Operations Research, 66(6):1586–1602, 2018.

- [29] A. D. Flaxman, A. T. Kalai, and H. B. McMahan. Online convex optimization in the bandit setting: gradient descent without a gradient. In Proceedings of the sixteenth annual ACM-SIAM symposium on Discrete algorithms, pages 385–394. Society for Industrial and Applied Mathematics, 2005.

- [30] A. Gupta and M. Molinaro. How the experts algorithm can help solve LPs online. Mathematics of Operations Research, 41(4):1404–1431, 2016.

- [31] E. Hazan. Introduction to online convex optimization. Foundations and Trends® in Optimization, 2(3-4):157–325, 2016.

- [32] E. Hazan, A. Agarwal, and S. Kale. Logarithmic regret algorithms for online convex optimization. Machine Learning, 69(2-3):169–192, 2007.

- [33] E. Hazan and S. Kale. Beyond the regret minimization barrier: optimal algorithms for stochastic strongly-convex optimization. The Journal of Machine Learning Research, 15(1):2489–2512, 2014.

- [34] E. Hazan and Y. Li. An optimal algorithm for bandit convex optimization. arXiv preprint arXiv:1603.04350, 2016.

- [35] N. Ho-Nguyen and F. Kılınç-Karzan. The role of flexibility in structure-based acceleration for online convex optimization. Technical report, Carnegie Mellon University, 2016. Technical report.

- [36] N. Immorlica, K. A. Sankararaman, R. Schapire, and A. Slivkins. Adversarial bandits with knapsacks. In 60th Annual Symposium on Foundations of Computer Science (FOCS), pages 202–219. IEEE, 2019.

- [37] R. Jenatton, J. Huang, and C. Archambeau. Adaptive algorithms for online convex optimization with long-term constraints. arXiv preprint arXiv:1512.07422, 2015.

- [38] A. Kalai and S. Vempala. Efficient algorithms for universal portfolios. Journal of Machine Learning Research, 3(Nov):423–440, 2002.

- [39] D. Kovenock and B. Roberson. Coalitional colonel blotto games with application to the economics of alliances. Journal of Public Economic Theory, 14(4):653–676, 2012.

- [40] G. Lan and Z. Zhou. Algorithms for stochastic optimization with expectation constraints. arXiv preprint arXiv:1604.03887, 2016.

- [41] J.-F. Laslier and N. Picard. Distributive politics and electoral competition. Journal of Economic Theory, 103(1):106–130, 2002.

- [42] Z. Lu, A. Nemirovski, and R. D. Monteiro. Large-scale semidefinite programming via a saddle point mirror-prox algorithm. Mathematical Programming, 109(2-3):211–237, 2007.

- [43] M. Mahdavi, R. Jin, and T. Yang. Trading regret for efficiency: online convex optimization with long term constraints. Journal of Machine Learning Research, 13(Sep):2503–2528, 2012.

- [44] M. Mahdavi, T. Yang, and R. Jin. Online decision making under stochastic constraints. In NIPS workshop on Discrete Optimization in Machine Learning, 2012.

- [45] S. Mannor, J. N. Tsitsiklis, and J. Y. Yu. Online learning with sample path constraints. Journal of Machine Learning Research, 10(Mar):569–590, 2009.

- [46] R. B. Myerson. Incentives to cultivate favored minorities under alternative electoral systems. American Political Science Review, 87(4):856–869, 1993.

- [47] M. J. Neely and H. Yu. Online convex optimization with time-varying constraints. arXiv preprint arXiv:1702.04783, 2017.

- [48] A. Nemirovski. Deterministic and randomized first order saddle point methods for large-scale convex optimization, 2010. Technical report.

- [49] A. Nemirovski, A. Juditsky, G. Lan, and A. Shapiro. Robust stochastic approximation approach to stochastic programming. SIAM Journal on Optimization, 19(4):1574–1609, 2009.

- [50] S. Paternain and A. Ribeiro. Online learning of feasible strategies in unknown environments. In American Control Conference (ACC), 2015, pages 4231–4238. IEEE, 2015.

- [51] S. Shalev-Shwartz et al. Online learning and online convex optimization. Foundations and Trends® in Machine Learning, 4(2):107–194, 2012.

- [52] S. Shalev-Shwartz, O. Shamir, N. Srebro, and K. Sridharan. Stochastic convex optimization. Proceedings of the 22nd Annual Conference on Learning Theory, 2009.

- [53] S. Singh, M. Kearns, and Y. Mansour. Nash convergence of gradient dynamics in general-sum games. In Proceedings of the Sixteenth conference on Uncertainty in artificial intelligence, pages 541–548. Morgan Kaufmann Publishers Inc., 2000.

- [54] J. C. Spall. A one-measurement form of simultaneous perturbation stochastic approximation. Automatica, 33(1):109–112, 1997.

- [55] H. Wu, R. Srikant, X. Liu, and C. Jiang. Algorithms with logarithmic or sublinear regret for constrained contextual bandits. In Advances in Neural Information Processing Systems, pages 433–441, 2015.

- [56] H. Yu, M. Neely, and X. Wei. Online convex optimization with stochastic constraints. In Advances in Neural Information Processing Systems, pages 1427–1437, 2017.

- [57] H. Yu and M. J. Neely. A low complexity algorithm with regret and finite constraint violations for online convex optimization with long term constraints. arXiv preprint arXiv:1604.02218, 2016.

- [58] J. Yuan and A. Lamperski. Online convex optimization for cumulative constraints. arXiv preprint arXiv:1802.06472, 2018.

- [59] M. Zinkevich. Online convex programming and generalized infinitesimal gradient ascent. In Proceedings of the 20th International Conference on Machine Learning, pages 928–936, 2003.