On Distributionally Robust Chance Constrained Programs with Wasserstein Distance

Abstract

This paper studies a distributionally robust chance constrained program (DRCCP) with Wasserstein ambiguity set, where the uncertain constraints should be satisfied with a probability at least a given threshold for all the probability distributions of the uncertain parameters within a chosen Wasserstein distance from an empirical distribution. In this work, we investigate equivalent reformulations and approximations of such problems. We first show that a DRCCP can be reformulated as a conditional value-at-risk constrained optimization problem, and thus admits tight inner and outer approximations. We also show that a DRCCP of bounded feasible region is mixed integer representable by introducing big-M coefficients and additional binary variables. For a DRCCP with pure binary decision variables, by exploring the submodular structure, we show that it admits a big-M free formulation, which can be solved by a branch and cut algorithm. Finally, we present a numerical study to illustrate the effectiveness of the proposed formulations.

1 Introduction

1.1 Setting

We study distributional robust chance constrained programs (DRCCPs) of the form:

| (1a) | ||||

| (1b) | ||||

| (1c) | ||||

In (1), the vector denotes the decision variables; the vector denotes the objective function coefficients; the set denotes deterministic constraints on ; and the constraint (1c) is a chance constraint involving uncertain constraints specified by the random vectors supported on set for each with a joint probability distribution from a family , termed “ambiguity set”. We let for any positive integer , and for each uncertain constraint , and denote affine mappings of such that and with parameters , , and , respectively. For notational convenience, we let and . Note that (i) for any and , the random vectors and can be correlated; and (ii) we use to differentiate whether (1c) involves left-hand uncertainty (i.e., ), right-hand uncertainty (i.e., ) or both-side uncertainty (i.e., ).

The distributionally robust chance constraint (DRCC) (1c) requires that all uncertain constraints are simultaneously satisfied for all the probability distributions from ambiguity set with a probability at least , where is a specified risk tolerance. We call (1) a single DRCCP if and a joint DRCCP if . Also, (1) is termed a DRCCP with right-hand uncertainty if and a DRCCP with left-hand uncertainty if . For a joint DRCCP, if , we call (1) as a two-sided DRCCP.

We denote the feasible region induced by DRCC (1c) as

| (2) |

1.2 Assumptions

In this paper, we consider Wasserstein ambiguity set , i.e., we make the following assumption on the ambiguity set .

-

(A1)

The Wasserstein ambiguity set is defined as

(3) where Wasserstein distance is defined as

and denotes a discrete empirical distribution of generated by i.i.d. samples from the true distribution , i.e., its point mass function is , and denotes the Wasserstein radius. We assume that is a totally bounded Polish (separable complete metric) space with distance metric , i.e., for every , there exists a finite covering of by balls with radius at most .

Note that the Wasserstein metric measures the distance between true distribution and empirical distribution and is able to recover the true distribution when the number of sampled data goes to infinity [18]. The fact that the convergence result is not affected by the support motivates us to consider relaxing the support , which provides us better reformulation power. That is, we make the following assumption about the support .

-

(A2)

The support , i.e., and .

We remark that

- •

- •

-

•

The interdependence between different random vectors can be inherited implicitly from the empirical distribution. For example, suppose that in the true distribution , we have for some and , then for any empirical sample , we must have with probability one. Since the empirical distribution will converge to the true distribution according to Lemma 3.7 [17] (i.e., when , ), thus Wasserstein Ambiguity set (3) will eventually pick up the fact that . However, this process might require many more samples than that without Assumption (A2);

- •

1.3 Related Literature

There are significant works on reformulation, convexity and approximations of set under various ambiguity sets [9, 23, 24, 27, 43, 46]). For a single DRCCP, when consists of all probability distributions with given first and second moments, the set is second-order conic representable [9, 16]. Similar convexity results hold for single DRCCP when also incorporates other distributional information such as the support of [13], the unimodality of [23, 30], or arbitrary convex mapping of [43]. For a joint DRCCP, [24] provided the first convex reformulation of in the absence of coefficient uncertainty, i.e., , when is characterized by the mean, a positively homogeneous dispersion measure, and conic support of . For the more general coefficient uncertainty setting, [43] identified several sufficient conditions for to be convex (e.g., when is specified by only one moment constraint), and [42] showed that is convex for two-sided DRCCP when is characterized by the first two moments.

When DRCC set is not convex, many inner convex approximations have been proposed. In [11], the authors proposed to aggregate the multiple uncertain constraints with positive scalars in to a single constraint, and then use conditional value-at-risk () approximation scheme [34] to develop an inner approximation of . This approximation is shown to be exact for single DRCCP when is specified by first and second moments in [51] or, more generally, by convex moment constraints in [43]. In [45], the authors provided several sufficient conditions under which the well-known Bonferroni approximation of joint DRCCP is exact and yields a convex reformulation.

Recently, there are many successful developments on data-driven distributionally robust programs with Wasserstein ambiguity set (3) [20, 17, 49]. For instance, [20, 17] studied its reformulation under different settings. Later on, [6, 19, 29, 38] applied it to the optimization problems related with machine learning. Other relevant works can be found [5, 22, 28, 33]. However, there is very limited literature on DRCCP with Wasserstein ambiguity set. In [44], the authors proved that it is strongly NP-hard to optimize over the DRCC set with Wasserstein ambiguity set and proposed a bicriteria approximation for a class of DRCCP with covering uncertain constraints (i.e., is a closed convex cone and for each ). In [14], the authors considered two-sided DRCCP with right-hand uncertainty and proposed its tractable reformulation, while in [25], the authors studied CVaR approximation of DRCCP. While this paper was under review, we became aware of the independent works [12, 26], which developed approximations and exact reformulations DRCCP with Wasserstein ambiguity set. Similar to this paper, in [12], the authors also derived exact mixed integer programming reformulations for single DRCCP and DRCCP with right-hand uncertainty using a different proof technique. In [26], the authors provided exact reformulations for single DRCCP under discrete support (i.e., ) and approximations for single DRCCP under continuous support.

1.4 Contributions

In this paper, we study approximations and exact reformulations of DRCCP under Wasserstein ambiguity set. In particular, our main contributions are summarized as below.

-

1.

We derive a deterministic equivalent reformulation for set and show that this reformulation admits a conditional value-at-risk () interpretation, i.e.,

where is defined in Theorem 1.

-

2.

We show that set , once bounded, is mixed integer representable with big-M coefficients and additional binary variables.

-

3.

We derive inner and outer approximations based upon interpretation. We develop compact formulations for these approximations and compare their strengths.

-

4.

When the decision variables are pure binary (i.e., ), we first show that the nonlinear constraints in the reformulation can be recast as submodular knapsack constraints. Then, by exploiting the polyhedral properties of submodular functions, we propose a new big-M free mixed integer linear reformulation, which can be effectively solved by a branch and cut algorithm.

The remainder of the paper is organized as follows. Section 2 presents exact reformulations of DRCC set . Section 3 provides inner and outer approximations of set and compares their strengths. Section 4 studies binary DRCCP (i.e., ), develops a big-M free formulation. Section 5 numerically illustrates the proposed methods. Section 6 concludes the paper.

Notation: The following notation is used throughout the paper. We use bold-letters (e.g., ) to denote vectors or matrices, and use corresponding non-bold letters to denote their components. We let be the all-ones vector, and let be the th standard basis vector. Given an integer , we let , and use and . Given a real number , we let . Given a finite set , we let denote its cardinality. We let denote a random vector with support and denote one of its realization by . Given a set , the characteristic function if , and , otherwise, while the indicator function =1 if , and 0, otherwise. For a matrix , we let denote th row of and denote th column of . Additional notation will be introduced as needed. Given a subset , we define an -dimensional binary vector as .

2 Exact Reformulations

In this section, we will show that DRCC set admits a conditional-value-at-risk () interpretation and is mixed integer representable. This reformulation also allows us to derive tight inner and outer approximations in next section.

2.1 Reformulation

In this subsection, we will reformulate the set into its deterministic counterpart with respect to empirical distribution. The main idea of this reformulation is that we first use the strong duality result from [7, 20] to formulate the worst-case chance constraint into its dual form, and then break down the indicator function according to its definition.

Theorem 1.

Set is equivalent to

| (4a) | ||||

| (4b) | ||||

where

| (5) |

and if and , otherwise, and characteristic function if and 0, otherwise.

Proof.

We separate the proof into three steps, where the first step is to apply strong duality result for distributionally robust optimization, the second step is to break down the indicator function, and the third step is to replace the dual variable with its reciprocal.

-

(i)

Note that

is equivalent to

Since

and the indicator function is always bounded and upper semi-continuous, therefore, according to Theorem 1 in [20] or Theorem 1 in [7], is equivalent to

(6a) Thus, set becomes

(6b) -

(ii)

Next, we break down the indicator function in the infimum of (6b) by discussing the conditions under which it is equal to zero or one and reformulate it as below.

Claim 1.

For given and , we have

(6c) Proof.

We first note that . Thus,

Therefore, we only need to show that for any ,

(6d) According to Claim 1 and the fact that

set becomes

(6e) -

(iii)

Finally, let denote the set in the right-hand side of (4) , we only need to show that .

∎

Please note that in the proof, we use the fact that from Assumption (A1), and the formulation (4) does not hold if .

An interesting corollary of Theorem 1 is that set can be reformulated as a conditional-value-at-risk () constrained set. Before showing this interpretation, let us first introduce the following two definitions. Given a random variable , let and be its probability distribution and cumulative distribution function, respectively. Then -value at risk (VaR) of is

while its -conditional value-at-risk (CVaR) [37] is defined as

With the definitions above, we observe that set in (4) has a interpretation.

Corollary 1.

Proof.

First, we observe that the constraint in (4) directly implies , thus the nonnegativity constraint of can be dropped, i.e., equivalently, we have

Next, in the above formulation, letting and replacing the existence of by finding the best such that the constraint still holds, we arrive at

which is equivalent to (7).∎∎

In the following sections, we will derive the inner and outer approximations mainly based upon formulation in Corollary 1.

2.2 Exact Mixed Integer Program Reformulation

In this subsection, we show that set is mixed integer representable. To do so, we first observe that the reformulation of set in Theorem 1 can be further simplified as a disjunction of a nonconvex set and a convex set.

Proposition 1.

Set , where

| (8a) | ||||

| (8b) | ||||

| (8c) | ||||

| (8d) | ||||

| (8e) | ||||

and

| (9) |

Proof.

We need to show that and .

-

.

Given , we have , thus (defined in (5)) is . Thus, let . Clearly, satisfies all the constraints in (4), i.e., . Hence, .

-

.

Similarly, given , there exists which satisfies constraints in (4). Suppose that , then we must have for all , otherwise, we have for all . Then (4a) is equivalent to

a contradiction that . Hence, we must .

From now on, we assume that . Let us define , and for each . Clearly, satisfies constraints in (8), i.e., . ∎

∎

We make the following remarks about the disjunctive formulation of set .

Remark 1.

-

(i)

Set is trivial:

-

•

For DRCCP with left-hand uncertainty (i.e., ), we have

-

•

For DRCCP with right-hand uncertainty or two-side uncertainty (i.e., ), we have .

-

•

- (ii)

We observe that set can be formulated as a mixed integer set when it is bounded, i.e., we can use binary variables to represent the nonlinear constraints (8b) as mixed integer linear ones. This result has been observed independently by [12] (see their Proposition 1) for single DRCCP.

Theorem 2.

Suppose there exists an such that

for all . Then is mixed integer representable, i.e.,

| (10a) | ||||

| (10b) | ||||

| (10c) | ||||

| (10d) | ||||

| (10e) | ||||

| (10f) | ||||

Proof.

Usually, we can derive the big-M coefficients by inspection; for example, suppose that , then for each , we can find in the following way: (i) rewrite for each , (ii) define sets and , and (iii) let be

There are various methods introduced in literature [36, 39] to further tighten big-M coefficients.

2.3 A Special Case: DRCCP with Right-hand Uncertainty

In this subsection, we consider DRCCP with right-hand uncertainty, i.e., . We first observe that when , in Theorem 1, set of DRCCP with right-hand uncertainty has a more compact representation.

Corollary 2.

For DRCCP with right-hand uncertainty (i.e., ), set is equivalent to the following mathematical program:

| (11a) | ||||

| (11b) | ||||

| (11c) | ||||

Proof.

The result directly follows from Theorem 1.∎∎

The differences between this result and the one in Proposition 1 are: (i) for DRCCP with right-hand uncertainty, we do not need to reformulate set as a disjunction of two sets, and (ii) compared to set in (8), there is no need to introduce additional positive variable in the formulation (11).

Following the similar derivation in Theorem 2, we can also reformulate the set in (11) as a mixed integer program as below. This result has been observed independently by [12] (see their Proposition 2).

Corollary 3.

For DRCCP with right-hand uncertainty (i.e., ), suppose that there exists an such that

for all . Then set is mixed integer representable, i.e.,

| (12a) | ||||

| (12b) | ||||

| (12c) | ||||

| (12d) | ||||

| (12e) | ||||

Proof.

The proof is similar as that of Theorem 2, thus is omitted. ∎∎

Similar to Theorem 2, suppose that , then for each , one possible can be derived as below:

where and .

3 Outer and Inner Approximations

In this section, we will introduce one outer approximation and three different inner approximations by exploiting the exact reformulations in the previous section. The outer approximation can provide a lower bound for DRCCP, while inner approximations can provide good-quality feasible solutions. Our numerical study in Section 5 will demonstrate that together these approximations, we can obtain better solutions than those from the exact mixed integer programming model in the previous section, in particular, for large-sized instances.

3.1 Outer Approximation

Note from [37] that for any random variable , we have

Therefore, in Corollary 1, if we replace by , then we have the following outer approximation of set .

Theorem 3.

Set can be outer approximated by

| (13) |

Proof.

Note that

and if , otherwise, . Thus we further have

Using the fact that , we arrive at (13).∎∎

We make the following remarks about outer approximation .

- (i)

-

(ii)

A particular interpretation of formulation (13) is that in order to enforce the robustness, we further penalize the left-hand side of uncertain constraints by the dual norm ; and

-

(iii)

Suppose that the empirical distribution will converge to the true distribution (cf., Lemma 3.7 [17]), i.e., as . Then as .

This final remark is summarized below.

Proposition 2.

Suppose that the empirical distribution will converge to the true distribution . Then with probability one, we have as .

Recently, there are several works [3, 4, 21, 41] on distributionally robust optimization with Wasserstein ambiguity set, and set is in fact equal to the feasible region induced by DRCC with Wasserstein ambiguity set.

Proposition 3.

Consider Wasserstein ambiguity set defined as

| (14) |

where Wasserstein distance is defined as

Then set is equivalent to

Proof.

Let us denote set . Let minus both sides of the inequalities, and we have Note that

According to Theorem 5 in [3], is equivalent to

Using the fact that , set is equivalent to

Clearly,

Thus,

∎

This result demonstrates that set indeed can be viewed as a deterministic counterpart of DRCCP with Wasserstein ambiguity set. Thus, in practice, it can serve as an alternative for the set .

For the completeness of this paper, we present the mixed integer program formulation of outer approximation set . The proof is omitted as it directly follows the proof of Theorem 2.

Corollary 4.

Suppose that there exists an such that

for all . Then is mixed integer representable, i.e.,

| (15a) | ||||

| (15b) | ||||

| (15c) | ||||

Similar to Theorem 2, suppose that , then for each , one possible can be derived as below:

where and .

3.2 Inner Approximation I- Robust Scenario Approximation

We also observe that for any random variable , we have

Thus, in Corollary 1, if we replace by , then we have the following inner approximation of set .

Theorem 4.

Set can be inner approximated by

| (16) |

Proof.

Since , and is a discrete random vector, therefore, set can be inner approximated by

Using the definition of and the fact that , we arrive at (16). ∎∎

We remark that set in (16) is very similar to scenario approach to regular chance constrained program [8, 10, 35]. That is, we generate i.i.d. samples and enforce all the sampled constraints to hold. It has been shown in [8, 10, 35] that if is larger than a threshold, it guarantees with high probability that the solution of scenario approach is feasible to the regular chance constrained program.

Different from scenario approach, in formulation (16), we add a penalty to the sampled constraints, which can be viewed as a “robust” scenario approach to the regular chance constrained problem. That is, if the sample size is not sufficiently large (i.e., is smaller than the threshold given by [8, 10, 35]), one might want to add a penalty to enforce that set is indeed a subset of the feasible region induced by a regular chance constraint.

3.3 Inner Approximation II- An Inner Chance Constrained Programming Approximation

Next we propose an inner chance constrained programming approximation of set by constructing a feasible in (4).

Theorem 5.

Set is inner approximated by

| (17) |

Proof.

We remark that this result together with set shows that the DRCC set can be inner and outer approximated by sets induced by regular chance constraints with empirical distribution .

We also observe that (i) set is a special case of set by letting , thus, we must have ; (ii) there are disjoint intervals that belong to, that is,

Suppose that for some . Since for all , thus the chance constraint in (18) is equivalent to

The feasible region induced by the above chance constraint increases if we decrease the value of to . Therefore, to optimize over set , we only need to enumerate these different values of and choose the one which yields the smallest objective value; (iii) for each given , the chance constraint in (17) is mixed integer program representable. These three results are summarized below.

Corollary 5.

Let set be defined in (18), then

-

(i)

;

-

(ii)

set , where set is defined as

(19) for each ; and

-

(iii)

suppose that there exists an such that

for all , then set is mixed integer representable, i.e.,

(20a) (20b) (20c)

Similar to Theorem 2, suppose that , then for each and , one possible in Corollary 5 can be derived as below:

where and .

According to Corollary 5, to solve the inner approximation of DRCCP (i.e., ), we can solve for each and choose the smallest value.

Finally, suppose that the empirical distribution will converge to the true distribution with an exponential rate (cf., Theorem 3.4 [17]), i.e., if , then with rate , where are positive constant. Then with probability one, as . Indeed, suppose that is sufficiently large such that . In (19), let . Clearly, as , we have and

where the inequality is due to and . This observation is summarized below.

Proposition 4.

Suppose that the empirical distribution will converge to the true distribution with an exponential rate. Then with probability one, we have as .

We make the following two remarks:

-

•

According to [17], any light-tail distribution (e.g., Gaussian distribution) satisfies the assumption in above proposition; and

-

•

Sets and together build up a hierarchy of regular chance constrained programs, which converges to DRCC set as and preserves the outer and inner approximations, i.e., for all and and as .

3.4 Inner Approximation III- Approximation

In this subsection, we will study a well-known convex approximation of a chance constraint, which is to replace the nonconvex chance constraint by a convex constraint defined by (cf., [34]). For DRCC set , the resulting approximation is

| (21) |

Set (21) is convex and is an inner approximation of set . The following results show a reformulation of set . We would like to acknowledge that this result has been independently observed by a recent work in [25]. Thus, the proof is omitted.

Theorem 6.

Set is equivalent to

| (22a) | ||||

| (22b) | ||||

| (22c) | ||||

| (22d) | ||||

| (22e) | ||||

Remark 2.

Since , by replacing with , then function is lower bounded by

Thus, set can be inner approximated by the following set

By introducing additional variables to linearize the nonlinear function , we arrive at

This set can be proven to be exactly equal to set by discussing whether or not:

-

(i)

if , then replace and by and ;

-

(ii)

if , since and , according to the pigeonhole principle, we must have for some , which implies that for all .

This observation inspires us that if . In fact, if , then we must have for all , which implies that .

Proposition 5.

Suppose that , then .

Proof.

We note that , where and are defined in (8) and (9), respectively. We note that set . Indeed, suppose that , i.e., for each , then let and for each . Clearly, satisfies the constraints in (22). Hence, .

Thus, it is sufficient to show that . Indeed, given , there exists such that satisfies the constraints in (8). We only need to show that for each . Suppose that there exists a such that . Then according to (8a), we have

where the second inequality is due to and , a contradiction that . Therefore, in (8b), we must have

for each . Hence, satisfies the constraints in (22), i.e., . ∎∎

The result in Proposition 5 shows that if the risk parameter is small enough (i.e., less than or equal to ), then set is convex and is equivalent to its approximation.

3.5 Formulation Comparisons

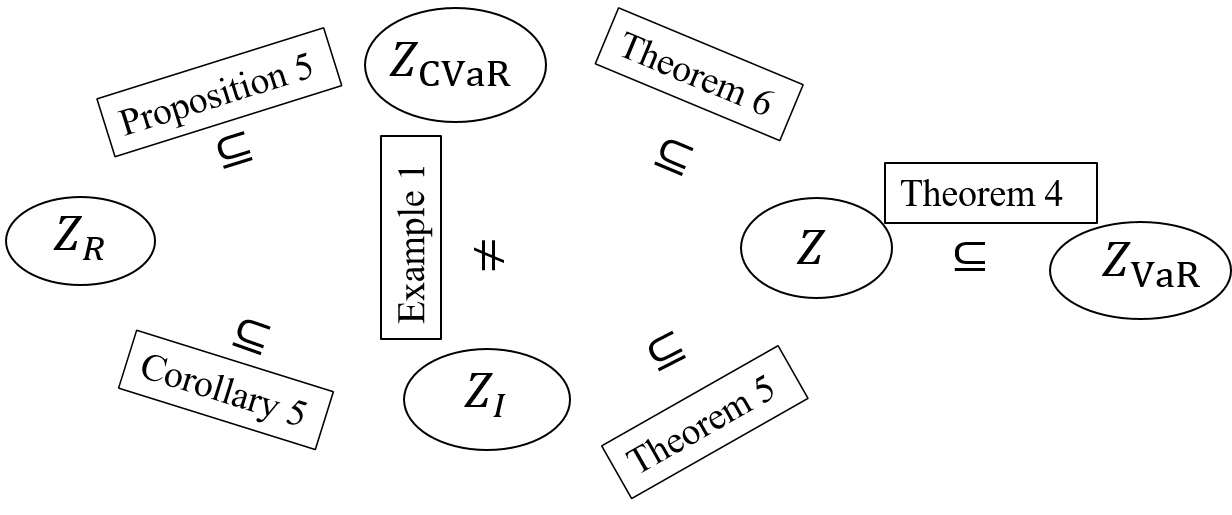

First, we would like to compare sets . Indeed, we can show that , i.e., set is at least as conservative as approximation .

Proof.

Given , we only need to show that . Indeed, let us consider , for all , then we see that satisfies the constraints in (22), i.e., .∎

∎

The following example illustrates sets and their inclusive relationships.

Example 1.

Suppose and . Then, (2) becomes:

| (23) |

Finally, the theoretical inclusive relationships of sets are shown in Figure 2 and their reformulations are summarized in Table 1.

4 DRCCP with Pure Binary Decision Variables

In this section, we will study DRCCP with pure binary decision variables , i.e., we assume that . If is a bounded integer set, we can use binary expansion to reformulate an equivalent binary set (c.f., [50]). For binary DRCCP, we will show that the reformulations in the previous section can be improved.

4.1 Polyhedral Results of Submodular Functions: A Review

Our main derivation of stronger formulations is based upon some polyhedral results of submodular functions, which will be briefly reviewed in this subsection.

We first briefly introduce the definition of submodularity and interested readers are referred to [15, 31] for more details.

Definition 1.

(Submodularity) Let be the power set of . Then a set function is “submodular” if and only if it satisfies the following condition:

-

•

for every with and every , we must have .

We first begin with the following lemmas on submodular functions.

Lemma 1.

Given , function is submodular over the binary hypercube.

Proof.

Since is a nondecreasing submodular function and is a nonincreasing concave function, the submodularity of their composition follows by Table 1 in [40].∎∎

Lemma 2.

Given , function with is submodular over the binary hypercube.

Proof.

This is because , and is a submodular function if is a concave function (cf., [47]). ∎∎

Next, we will introduce polyhedral properties of submodular functions. For any given submodular function with , let us denote to be its epigraph, i.e.,

Then the convex hull of is characterized by the system of “extended polymatroid inequalities” (EPI) [2, 47], i.e.,

| (24) |

where denotes a collection of all permutations of set and for each with and .

In addition, although there are number of inequalities in (24), these inequalities can be easily separated by a greedy procedure.

From Lemma 3, we see that to separate a point from , we only need to sort the coordinates of in a descending order, i.e., . Then can be the separated by the constraint from . The time complexity of this separating procedure is .

4.2 Reformulating a Binary DRCCP by Submodular Knapsack Constraints: Big-M free

In this section, we will replace the nonlinear constraints defining the feasible region of a binary DRCCP (i.e., set ) by submodular knapsack constraints. These constraints can be equivalently described by the system of EPI in (24). Therefore we obtain a big-M free mixed integer representation of set .

First, we introduce auxiliary variables complementing binary variables , denoted by , i.e., for each . With these additional variables, we can reformulate function as

| (25) |

for each such that . Indeed, since and , in (25), we can choose

for each .

Thus, from above discussion, we can formulate (recall that set according to Proposition 1) as the following mixed integer set with submodular knapsack constraints.

Theorem 7.

Suppose that . Then , where

| (26a) | ||||

| (26b) | ||||

| (26c) | ||||

| (26d) | ||||

| (26e) | ||||

| (26f) | ||||

| (26g) | ||||

and

| (27) |

Proof.

According to Proposition 1, equalities (25) and the fact that with constant , constraints (8b) and (8d) are equivalent to (26b) and (26d). Thus, we only need to show that . There are two cases.

-

Case 1.

If , then we must have , then . We are done.

-

Case 2.

If , then we must have . For any , we need to show that . If , then the constraints (8) become

Since , thus by the pigeonhole principle, we must have for some . This implies that for each . Together with , we must have .

Now suppose that . Note that , therefore, implies that , thus, . Thus, .∎

∎

From the proof of Theorem 7, we note that if for each , then we have . Thus, .

Corollary 6.

Suppose that and for each . Then .

Proof.

We note that the left-hand sides of constraints (26b) and (26d) are submodular functions according to Lemma 1 and Lemma 2. Therefore, equivalently, we can replace these constraints with the convex hulls of epigraphs of their associated submodular functions. Thus, we arrive at the following equivalent representation of set .

Corollary 7.

Suppose that and is norm with . Then

| (28a) | ||||

| (28b) | ||||

| (28c) | ||||

| (28d) | ||||

| (28e) | ||||

| (28f) | ||||

where

| (29a) | ||||

| (29b) | ||||

| and can be described by the system of EPI in (24). | ||||

Note that the optimization problem can be solved by a branch and cut algorithm. In particular, at each branch and bound node, denoted as , there might be too many (i.e., ) valid inequalities to add, since in (28b) and (28d), there are convex hulls of epigraphs (i.e., ) to be separated from. Therefore, instead, we can first check and find the epigraphs of (e.g., in our numerical study) most violated constraints in (26b) and (26d), i.e., find the epigraphs corresponding to the largest values in the following set

Finally, we can generate and add valid inequalities by separating from the convex hulls of these epigraphs according to Lemma 3.

5 Numerical Demonstration

In this section, we present a series of numerical studies to demonstrate the effectiveness of the proposed formulations and also show how to use cross validation to choose a proper Wasserstein radius .

For the demonstration purpose, we will study distributionally robust multidimensional knapsack problem (DRMKP) [13, 39, 43] with continuous decision variables (i.e., continuous DRMKP) or binary decision variables (i.e., binary DRMKP). In a DRMKP, there are items and knapsacks. Additionally, represents the value of item for all , represents the vector of random item weights in knapsack , and represents the capacity limit of knapsack , for all . The decision variable represents the proportion of th item to be picked. In a continuous DRMKP, we let , and for a binary DRMKP, we let . We use the Wasserstein ambiguity set under Assumptions (A1) and (A2) with - norm as distance metric. With the notation above, DRMKP is formulated as

| (30) |

where the chance constraint here is to guarantee that the worst-case probability that each knapsack’s capacity should be satisfied is at least .

In the following subsections, we generated different random instances to test the proposed formulations. All the instances were executed on a MacBook Pro with a 2.80 GHz processor and 16GB RAM with a call of the commercial solver Gurobi (version 7.5, with default settings). We set the time limit of solving each instance to be 3600 seconds.

5.1 Continuous DRMKP: Numerical Demonstration of Exact Formulation, Outer and Inner Approximations

In this subsection, we use continuous DRMKP (i.e., in (30)) to numerically demonstrate the exact formulation in Theorem 2, outer approximation in Corollary 4, approximation in Theorem 6 and inner chance constrained programming approximation in Corollary 5. To test the proposed formulations, we generated 10 random instances with and , indexed by . For each instance, we generate empirical samples from a uniform distribution over a box . For each , we independently generated from the uniform distribution on the interval , while for each , we set . We tested these 10 random instances with risk parameter and Wasserstein radius .

The numerical results with sample size are displayed in Table 2, where we use BigM Model, Model, Model and ICCP Model denote exact formulation in Theorem 2, outer approximation in Corollary 4, approximation in Theorem 6 and inner chance constrained programming approximation in Corollary 5, respectively. We also use “Opt.Val” to denote the optimal value , “Value” to denote the best objective value output from an approximation model and “Time” to denote the computational time in seconds. Additionally, since we can solve exact BigM Model to the optimality, we use GAP denote the optimality gap of an approximation model, which is computed as

We also let denote the best found in ICCP Model. In BigM Model (10), we chose a lower bound of as . We chosen the big-M coefficients in BigM Model, Model, and ICCP Model according to the remarks after Theorem 2, Corollary 4, and Corollary 5, respectively, where . From Table 2, we see that all the models can be solved to the optimality within 2 minutes, where BigM Model and ICCP Model often take the longest time to solve, and for each instance, Model can be solved within a second. This might be because (i) Model is a second order conic program and does not involve any binary variables; (ii) on the contrary, the BigM Model not only has binary variables but also involves the most number of auxiliary variables, while to solve ICCP Model, one needs to solve regular chance constrained programs. In terms of approximation accuracy, we see that VaR Model is usually 2-3% away from the true optimality, Model is 1-2% away from the true optimality, while ICCP Model nearly finds the true optimal solution. This demonstrates that all of the proposed approximation models can find near-optimal solutions.

The numerical results with sample size are displayed in Table 3, where similarly, we use BigM Model, Model, Model and ICCP Model denote exact formulation in Theorem 2, outer approximation in Corollary 4, approximation in Theorem 6 and inner chance constrained programming approximation in Corollary 5, respectively. We use “UB” to denote the best upper bound found by BigM Model or Model, “LB” to denote the best lower bound found by BigM Model, Model, or ICCP Model, and “Time” to denote the computational time in seconds. Additionally, since we cannot solve the BigM Model to optimality, we use GAP denote its optimality gap, which is computed as

To evaluate the effectiveness of approximation models, we use Improvement to denote the percentage of differences between the bounds of approximation models and bounds of BigM Model, i.e., for the Model,

while for the Model or ICCP Model,

where Approximation Model here is either Model or ICCP Model. We found that ICCP Model is difficult to solve these instances to optimality, and thus we chose a particular in ICCP Model. Similarly, in BigM Model (10), we chose a lower bound of as , and the big-M coefficients in BigM Model, Model, and ICCP Model were computed according to the remarks after Theorem 2, Corollary 4, and Corollary 5, respectively, where . From Table 3, we see that Model can be solved to optimality within 2 seconds, while all the other models cannot be solved within the time limit. In terms of approximation accuracy, we see that VaR Model consistently provides better upper bounds and can help close more 10% optimality gap on average compared to BigM Model, Model often provides slightly better feasible solutions than BigM Model, while, ICCP Model yields the best feasible solutions. This demonstrates that all of the proposed approximation models are useful, to some extent, to improve the exact bigM model. In particular, Model provides a better upper bound, which helps evaluate the solution quality more accurately, Model and ICCP Model often provide better feasible solutions. Also, we notice that mixed integer programs Model and ICCP Model outperform BigM Model, which might be because (i) the BigM Model requires more auxiliary variables than Model or ICCP Model; (ii) the naive big-M coefficients of the BigM Model are typically larger than the other two. In practice, it is worthy of trying all the BigM Model, ICCP Model, and CVaR Model first, then choose the best solution from three models and use the outer approximation- VaR Model to provide a numerical optimality guarantee on how good the solution quality is.

| Insta- nces | BigM Model | Model | Model | ICCP Model | ||||||||||

| Opt.Val | Time | Value | GAP | Time | Value | GAP | Time | Value | GAP | Time | ||||

| 0.05 | 0.01 | 1 | 54.93 | 6.11 | 56.37 | 2.62% | 3.37 | 54.30 | 1.14% | 0.06 | 54.93 | 0.03 | 0.00% | 9.43 |

| 2 | 47.69 | 5.24 | 48.79 | 2.29% | 2.04 | 47.16 | 1.11% | 0.05 | 47.69 | 0.03 | 0.00% | 7.90 | ||

| 3 | 50.73 | 4.44 | 51.43 | 1.38% | 4.43 | 50.38 | 0.70% | 0.05 | 50.73 | 0.02 | 0.00% | 8.64 | ||

| 4 | 53.97 | 3.61 | 54.98 | 1.87% | 4.75 | 52.72 | 2.32% | 0.06 | 53.97 | 0.03 | 0.00% | 8.16 | ||

| 5 | 54.96 | 6.99 | 56.44 | 2.68% | 4.20 | 52.88 | 3.79% | 0.05 | 54.96 | 0.03 | 0.00% | 7.42 | ||

| 6 | 56.03 | 6.46 | 57.40 | 2.44% | 2.64 | 54.97 | 1.89% | 0.05 | 56.03 | 0.03 | 0.00% | 6.35 | ||

| 7 | 54.17 | 6.69 | 55.04 | 1.62% | 3.68 | 53.26 | 1.67% | 0.05 | 54.12 | 0.02 | 0.08% | 7.92 | ||

| 8 | 55.40 | 5.81 | 56.55 | 2.09% | 3.19 | 54.15 | 2.26% | 0.05 | 55.40 | 0.03 | 0.00% | 6.86 | ||

| 9 | 57.63 | 4.91 | 58.95 | 2.29% | 4.20 | 57.07 | 0.96% | 0.05 | 57.62 | 0.02 | 0.02% | 10.80 | ||

| 10 | 56.31 | 4.34 | 57.15 | 1.50% | 4.71 | 55.95 | 0.63% | 0.06 | 56.31 | 0.02 | 0.00% | 8.62 | ||

| Average | 5.46 | 2.08% | 3.72 | 1.65% | 0.05 | 0.01% | 8.21 | |||||||

| 0.05 | 0.02 | 1 | 53.97 | 3.94 | 55.92 | 3.63% | 3.27 | 53.83 | 0.24% | 0.05 | 53.94 | 0.02 | 0.05% | 9.95 |

| 2 | 47.05 | 3.63 | 48.42 | 2.92% | 3.20 | 46.79 | 0.53% | 0.04 | 47.04 | 0.02 | 0.01% | 8.64 | ||

| 3 | 50.12 | 5.26 | 51.02 | 1.79% | 4.48 | 49.96 | 0.33% | 0.05 | 50.11 | 0.01 | 0.03% | 8.88 | ||

| 4 | 52.98 | 5.14 | 54.49 | 2.84% | 4.83 | 52.28 | 1.33% | 0.06 | 52.98 | 0.02 | 0.00% | 9.41 | ||

| 5 | 54.10 | 3.76 | 55.95 | 3.41% | 3.67 | 52.44 | 3.07% | 0.05 | 54.05 | 0.02 | 0.09% | 9.55 | ||

| 6 | 55.16 | 6.02 | 56.90 | 3.16% | 3.33 | 54.52 | 1.17% | 0.05 | 55.14 | 0.02 | 0.04% | 7.58 | ||

| 7 | 53.41 | 3.91 | 54.55 | 2.13% | 3.81 | 52.83 | 1.08% | 0.05 | 53.38 | 0.02 | 0.06% | 7.59 | ||

| 8 | 54.47 | 2.77 | 56.09 | 2.98% | 3.34 | 53.71 | 1.39% | 0.06 | 54.43 | 0.02 | 0.07% | 6.63 | ||

| 9 | 56.85 | 3.40 | 58.44 | 2.79% | 4.00 | 56.59 | 0.46% | 0.05 | 56.84 | 0.01 | 0.02% | 9.39 | ||

| 10 | 55.65 | 5.47 | 56.71 | 1.90% | 4.90 | 55.53 | 0.22% | 0.06 | 55.65 | 0.01 | 0.00% | 9.29 | ||

| Average | 4.33 | 2.76% | 3.88 | 0.98% | 0.05 | 0.04% | 8.69 | |||||||

| 0.1 | 0.01 | 1 | 56.47 | 25.78 | 57.71 | 2.19% | 10.01 | 55.14 | 2.36% | 0.05 | 56.47 | 0.06 | 0.00% | 35.61 |

| 2 | 48.82 | 66.63 | 49.87 | 2.16% | 6.51 | 48.00 | 1.68% | 0.06 | 48.79 | 0.06 | 0.06% | 25.94 | ||

| 3 | 51.58 | 102.52 | 52.56 | 1.89% | 10.35 | 50.93 | 1.26% | 0.06 | 51.58 | 0.07 | 0.00% | 54.93 | ||

| 4 | 55.28 | 15.06 | 56.20 | 1.66% | 8.26 | 53.97 | 2.37% | 0.05 | 55.28 | 0.06 | 0.00% | 35.40 | ||

| 5 | 56.94 | 22.07 | 58.51 | 2.75% | 4.82 | 54.28 | 4.68% | 0.06 | 56.94 | 0.07 | 0.00% | 31.10 | ||

| 6 | 57.50 | 23.31 | 58.94 | 2.51% | 9.04 | 55.92 | 2.74% | 0.07 | 57.50 | 0.06 | 0.00% | 29.69 | ||

| 7 | 55.21 | 24.96 | 56.51 | 2.35% | 5.15 | 54.24 | 1.77% | 0.06 | 55.19 | 0.06 | 0.04% | 27.51 | ||

| 8 | 56.64 | 15.43 | 57.96 | 2.33% | 3.80 | 55.42 | 2.15% | 0.06 | 56.60 | 0.06 | 0.08% | 29.52 | ||

| 9 | 59.18 | 23.14 | 60.47 | 2.19% | 8.79 | 58.01 | 1.98% | 0.08 | 59.14 | 0.07 | 0.07% | 46.42 | ||

| 10 | 57.20 | 29.34 | 58.02 | 1.44% | 10.08 | 56.50 | 1.21% | 0.07 | 57.19 | 0.07 | 0.00% | 48.08 | ||

| Average | 34.83 | 2.15% | 7.68 | 2.22% | 0.06 | 0.03% | 36.42 | |||||||

| 0.1 | 0.02 | 1 | 55.93 | 77.63 | 57.45 | 2.72% | 9.50 | 54.89 | 1.85% | 0.05 | 55.92 | 0.05 | 0.01% | 36.73 |

| 2 | 48.47 | 20.09 | 49.66 | 2.47% | 2.77 | 47.82 | 1.34% | 0.06 | 48.42 | 0.05 | 0.09% | 27.42 | ||

| 3 | 51.14 | 110.17 | 52.34 | 2.35% | 14.61 | 50.72 | 0.81% | 0.07 | 51.06 | 0.04 | 0.14% | 54.71 | ||

| 4 | 54.68 | 73.17 | 55.96 | 2.35% | 12.99 | 53.74 | 1.71% | 0.06 | 54.67 | 0.06 | 0.01% | 43.06 | ||

| 5 | 56.11 | 16.04 | 58.25 | 3.81% | 3.98 | 54.05 | 3.67% | 0.06 | 56.11 | 0.07 | 0.00% | 34.82 | ||

| 6 | 56.93 | 18.81 | 58.66 | 3.05% | 3.61 | 55.68 | 2.19% | 0.06 | 56.90 | 0.05 | 0.05% | 33.87 | ||

| 7 | 54.67 | 37.46 | 56.26 | 2.90% | 6.57 | 54.00 | 1.22% | 0.05 | 54.61 | 0.06 | 0.12% | 33.40 | ||

| 8 | 56.15 | 15.48 | 57.71 | 2.77% | 4.54 | 55.20 | 1.70% | 0.05 | 56.09 | 0.05 | 0.11% | 26.77 | ||

| 9 | 58.51 | 18.82 | 60.21 | 2.91% | 10.79 | 57.76 | 1.28% | 0.06 | 58.48 | 0.04 | 0.05% | 47.85 | ||

| 10 | 56.76 | 33.72 | 57.80 | 1.84% | 12.03 | 56.29 | 0.83% | 0.07 | 56.71 | 0.05 | 0.08% | 44.74 | ||

| Average | 42.14 | 2.72% | 8.14 | 1.66% | 0.06 | 0.07% | 38.34 | |||||||

| Insta- nces | BigM Model | Model | Model | ICCP Model | |||||||||||||||

| UB | LB | GAP | Time | UB |

|

Time | LB |

|

Time | LB |

|

Time | |||||||

| 0.05 | 0.01 | 1 | 66.45 | 53.02 | 25.32% | 3600 | 57.71 | 13.15% | 3600 | 52.94 | -0.15% | 0.72 | 53.47 | 0.025 | 0.84% | 3600 | |||

| 2 | 64.48 | 52.18 | 23.57% | 3600 | 57.07 | 11.50% | 3600 | 52.51 | 0.62% | 0.61 | 52.57 | 0.025 | 0.74% | 3600 | |||||

| 3 | 69.55 | 54.02 | 28.75% | 3600 | 62.21 | 10.54% | 3600 | 54.45 | 0.81% | 1.00 | 55.13 | 0.025 | 2.06% | 3600 | |||||

| 4 | 68.02 | 53.91 | 26.18% | 3600 | 61.60 | 9.45% | 3600 | 54.23 | 0.58% | 1.01 | 54.60 | 0.025 | 1.28% | 3600 | |||||

| 5 | 68.39 | 56.75 | 20.52% | 3600 | 61.25 | 10.44% | 3600 | 56.80 | 0.09% | 0.65 | 57.12 | 0.025 | 0.65% | 3600 | |||||

| 6 | 69.66 | 56.15 | 24.05% | 3600 | 60.74 | 12.81% | 3600 | 56.32 | 0.29% | 0.84 | 56.00 | 0.025 | -0.28% | 3600 | |||||

| 7 | 74.45 | 57.95 | 28.47% | 3600 | 66.33 | 10.91% | 3600 | 58.11 | 0.29% | 1.08 | 58.65 | 0.025 | 1.21% | 3600 | |||||

| 8 | 74.91 | 57.42 | 30.45% | 3600 | 66.42 | 11.33% | 3600 | 57.86 | 0.75% | 0.93 | 58.04 | 0.025 | 1.07% | 3600 | |||||

| 9 | 65.84 | 51.64 | 27.49% | 3600 | 56.72 | 13.85% | 3600 | 51.85 | 0.41% | 0.51 | 52.16 | 0.025 | 1.01% | 3600 | |||||

| 10 | 66.26 | 50.94 | 30.06% | 3600 | 56.11 | 15.32% | 3600 | 51.43 | 0.96% | 0.62 | 51.37 | 0.025 | 0.85% | 3600 | |||||

| Average | 26.49% | 3600 | 11.93% | 3600 | 0.46% | 0.80 | 0.94% | 3600 | |||||||||||

| 0.05 | 0.02 | 1 | 72.24 | 53.22 | 35.74% | 3600 | 60.48 | 16.27% | 3600 | 53.10 | -0.22% | 0.90 | 53.54 | 0.05 | 0.62% | 3600 | |||

| 2 | 68.90 | 52.53 | 31.15% | 3600 | 60.68 | 11.94% | 3600 | 52.88 | 0.65% | 1.18 | 53.10 | 0.05 | 1.07% | 3600 | |||||

| 3 | 57.60 | 46.77 | 23.14% | 3600 | 51.53 | 10.53% | 3600 | 46.94 | 0.35% | 0.95 | 47.16 | 0.05 | 0.83% | 3600 | |||||

| 4 | 57.05 | 46.13 | 23.67% | 3600 | 52.25 | 8.40% | 3600 | 46.56 | 0.93% | 0.82 | 46.41 | 0.05 | 0.61% | 3600 | |||||

| 5 | 60.61 | 48.11 | 25.99% | 3600 | 54.86 | 9.49% | 3600 | 48.12 | 0.02% | 1.13 | 48.61 | 0.05 | 1.04% | 3600 | |||||

| 6 | 62.30 | 47.24 | 31.89% | 3600 | 55.74 | 10.53% | 3600 | 47.92 | 1.45% | 1.49 | 48.00 | 0.05 | 1.61% | 3600 | |||||

| 7 | 61.50 | 48.76 | 26.12% | 3600 | 53.23 | 13.44% | 3600 | 49.11 | 0.72% | 0.51 | 49.44 | 0.05 | 1.39% | 3600 | |||||

| 8 | 60.38 | 48.39 | 24.77% | 3600 | 52.77 | 12.59% | 3600 | 48.70 | 0.64% | 0.57 | 48.62 | 0.05 | 0.46% | 3600 | |||||

| 9 | 65.20 | 49.94 | 30.56% | 3600 | 57.51 | 11.80% | 3600 | 50.36 | 0.84% | 1.05 | 50.63 | 0.05 | 1.39% | 3600 | |||||

| 10 | 64.73 | 49.71 | 30.22% | 3600 | 57.68 | 10.90% | 3600 | 50.15 | 0.88% | 1.08 | 50.28 | 0.05 | 1.16% | 3600 | |||||

| Average | 28.33% | 3600 | 11.59% | 3600 | 0.63% | 0.97 | 1.02% | 3600 | |||||||||||

| 0.1 | 0.01 | 1 | 68.21 | 51.92 | 31.39% | 3600 | 57.01 | 16.43% | 3600 | 51.99 | 0.14% | 0.62 | 52.38 | 0.025 | 0.88% | 3600 | |||

| 2 | 67.75 | 51.22 | 32.26% | 3600 | 57.75 | 14.75% | 3600 | 51.57 | 0.68% | 0.66 | 51.55 | 0.025 | 0.63% | 3600 | |||||

| 3 | 70.55 | 53.00 | 33.11% | 3600 | 62.53 | 11.37% | 3600 | 53.24 | 0.44% | 0.78 | 53.93 | 0.025 | 1.75% | 3600 | |||||

| 4 | 70.47 | 52.49 | 34.26% | 3600 | 60.78 | 13.75% | 3600 | 53.02 | 1.01% | 0.87 | 53.35 | 0.025 | 1.64% | 3600 | |||||

| 5 | 64.24 | 51.29 | 25.27% | 3600 | 55.59 | 13.47% | 3600 | 51.38 | 0.18% | 0.53 | 51.78 | 0.025 | 0.96% | 3600 | |||||

| 6 | 63.74 | 50.69 | 25.75% | 3600 | 54.92 | 13.84% | 3600 | 50.95 | 0.52% | 0.61 | 50.90 | 0.025 | 0.42% | 3600 | |||||

| 7 | 66.93 | 52.90 | 26.52% | 3600 | 58.97 | 11.89% | 3600 | 52.75 | -0.29% | 1.31 | 53.35 | 0.025 | 0.84% | 3600 | |||||

| 8 | 66.56 | 52.42 | 26.97% | 3600 | 59.37 | 10.80% | 3600 | 52.53 | 0.20% | 1.14 | 52.84 | 0.025 | 0.80% | 3600 | |||||

| 9 | 69.74 | 56.43 | 23.59% | 3600 | 61.97 | 11.15% | 3600 | 56.23 | -0.35% | 0.75 | 56.83 | 0.025 | 0.71% | 3600 | |||||

| 10 | 67.45 | 55.72 | 21.05% | 3600 | 60.87 | 9.76% | 3600 | 55.78 | 0.11% | 0.66 | 55.94 | 0.025 | 0.39% | 3600 | |||||

| Average | 28.02% | 3600 | 12.72% | 3600 | 0.26% | 0.79 | 0.90% | 3600 | |||||||||||

| 0.1 | 0.02 | 1 | 75.06 | 58.30 | 28.75% | 3600 | 67.10 | 10.60% | 3600 | 57.67 | -1.08% | 0.93 | 58.39 | 0.05 | 0.15% | 3600 | |||

| 2 | 75.79 | 57.11 | 32.72% | 3600 | 65.20 | 13.97% | 3600 | 57.43 | 0.56% | 0.96 | 57.87 | 0.05 | 1.34% | 3600 | |||||

| 3 | 71.66 | 55.49 | 29.13% | 3600 | 59.52 | 16.93% | 3600 | 55.21 | -0.51% | 0.50 | 55.69 | 0.05 | 0.36% | 3600 | |||||

| 4 | 67.30 | 54.31 | 23.92% | 3600 | 59.01 | 12.31% | 3600 | 54.74 | 0.80% | 0.56 | 54.78 | 0.05 | 0.87% | 3600 | |||||

| 5 | 73.91 | 57.35 | 28.88% | 3600 | 65.21 | 11.77% | 3600 | 56.72 | -1.09% | 0.89 | 57.37 | 0.05 | 0.04% | 3600 | |||||

| 6 | 72.05 | 56.71 | 27.04% | 3600 | 64.56 | 10.39% | 3600 | 56.48 | -0.41% | 1.00 | 56.88 | 0.05 | 0.29% | 3600 | |||||

| 7 | 70.33 | 56.87 | 23.67% | 3600 | 60.52 | 13.94% | 3600 | 56.25 | -1.09% | 0.59 | 57.03 | 0.05 | 0.29% | 3600 | |||||

| 8 | 66.69 | 55.88 | 19.34% | 3600 | 60.25 | 9.65% | 3600 | 55.76 | -0.22% | 0.77 | 56.08 | 0.05 | 0.35% | 3600 | |||||

| 9 | 73.51 | 58.36 | 25.94% | 3600 | 65.38 | 11.05% | 3600 | 57.99 | -0.64% | 0.89 | 58.77 | 0.05 | 0.69% | 3600 | |||||

| 10 | 73.98 | 57.51 | 28.65% | 3600 | 66.01 | 10.78% | 3600 | 57.73 | 0.38% | 1.16 | 58.18 | 0.05 | 1.17% | 3600 | |||||

| Average | 26.80% | 3600 | 12.14% | 3600 | -0.33% | 0.83 | 0.55% | 3600 | |||||||||||

5.2 Choosing a Wasserstein Radius using Cross Validation

In this subsection, we use continuous DRMKP (i.e., in (30)) to numerically demonstrate how to use cross validation to choose a proper Wasserstein radius and also test the effects of the correlation of the random vectors . We suppose that , and , and for each , where are independent uniform random vectors over the box , and . Clearly, as grows, the correlation among random vectors increases. Our numerical instances were generated as follows. We first generated i.i.d. samples from a uniform distribution over a box , and i.i.d. samples from a uniform distribution over a box , where and . Next, we constructed 11 instances with empirical samples as

for each and , and . For each , we independently generated from the uniform distribution on the interval , while for each , we set . We also suppose that the possible Wasserstein radii are from .

The cross validation procedure was done in the following manner: (i) for each , we solved continuous DRMKP to the optimality using exact formulation in Proposition 1; (ii) we generated samples of the random vectors and used these samples to estimate the violation probability of uncertain constraints with respect to the optimal solution found at step (i). We repeated this procedure 10 times and output the 90-percentile of these estimated violation probabilities, denoted as 90-percentile violation; and (iii) we chose the best Wasserstein radius as the smallest such that its 90-percentile violation is below the target violation, i.e., less than or equal to , which implies that approximately with probability at least 0.9, the DRMKP solution will be feasible to its regular CCP Model.

For the comparison purpose, we also solve a regular chance constrained programming counterpart of DRMKP (30) with respect to the empirical samples and used the same procedure to compute its 90-percentile violation. The numerical results are displayed in Table 4, where we use “CCP Model” to denote the chance constrained programming counterpart of DRMKP, and “Opt.Val” to denote the optimal value of a corresponding model.

From Table 2, we see that for the optimal solutions from CCP Model often have much higher probability of violating the uncertain constraints than the target risk parameter . On the other hand, for DRMKP Model, by choosing Wasserstein radius properly, its probability of violating the uncertain constraints is often smaller than the target risk parameter, and its optimal value is often very close to that of CCP Model. This demonstrates the robustness and accuracy of the proposed DRMKP Model. We also note that when grows, i.e., the correlation between among random vectors increases, the best Wasserstein radius does not tend to decrease or increase. This result demonstrates that Assumption (A2) does not cause too much over-conservatism of the proposed DRCCP models. In fact, we note that the best Wasserstein radius is positively correlated with the 90-percentile violation of CCP Model, i.e., tends to be bigger if CCP Model has a larger 90-percentile violation value. In practice, we suggest solving regular CCP Model first and then choose a proper range of for the cross validation. Finally, if the cross validation takes too much time due to the difficulty of solving MILPs, then we can reduce the running time via warm start. That is, we suggest solving the cross validation instances in the descending order of possible values, and when solving a cross validation instance, since the optimal solution from previous instance is feasible to the current one, thus, we can input this solution to the solver as a starting point.

| DRMKP Model | CCP Model | Target Violation () | ||||||

|---|---|---|---|---|---|---|---|---|

| Opt.Val |

|

Opt.Val |

|

|||||

| 0 | 0.03 | 53.76 | 0.04154 | 56.99 | 0.13461 | 0.05 | ||

| 0.1 | 0.02 | 50.06 | 0.04431 | 52.67 | 0.08698 | |||

| 0.2 | 0.03 | 52.37 | 0.03133 | 55.11 | 0.15273 | |||

| 0.3 | 0.01 | 56.94 | 0.03905 | 58.33 | 0.09624 | |||

| 0.4 | 0.02 | 53.38 | 0.02801 | 55.89 | 0.12054 | |||

| 0.5 | 0.02 | 50.25 | 0.03249 | 52.13 | 0.09629 | |||

| 0.6 | 0.01 | 59.38 | 0.04671 | 60.98 | 0.08015 | |||

| 0.7 | 0.03 | 54.60 | 0.04742 | 57.77 | 0.12871 | |||

| 0.8 | 0.03 | 62.51 | 0.04678 | 66.39 | 0.11837 | |||

| 0.9 | 0.03 | 52.82 | 0.0364 | 56.90 | 0.13221 | |||

| 1 | 0.02 | 59.51 | 0.03998 | 62.09 | 0.09496 | |||

5.3 Binary DRMKP: Strength of Big-M Free Formulation

In this subsection, we present a numerical study to compare the big-M formulation in Theorem 2 with big-M free formulation in Corollary 7 on solving binary DRMKP (i.e., in (30)). To test the proposed formulations, we generated 10 random instances with and , indexed by . For each instance, we generated empirical samples from a uniform distribution over a box . For each , we independently generated from the uniform distribution on the interval , while for each , we set . We tested these 10 random instances with risk parameter and Wasserstein radius . Also, in BigM Model (10), we chose

and a lower bound of as . In the branch and cut implementation described in the end of Section 4, each time we added EPI inequalities.

The results are displayed in Table 5. We use BigM Model and BigM-free Model to denote the big-M formulation in Theorem 2 and big-M free formulation in Corollary 7, respectively. In addition, we use UB, LB, GAP, Opt.Val and Time to denote the best upper bound, the best lower bound, optimality gap, the optimal objective value, and the total running time in seconds, respectively.

| Instances | BigM Model | BigM-free Model | ||||||||

| UB | LB | Time | GAP | Opt.Val | Time | |||||

| 0.05 | 0.1 | 1 | 20 | 10 | 93 | 86 | 3600.0 | 7.5% | 89 | 49.3 |

| 2 | 20 | 10 | 97 | 90 | 3600.0 | 7.2% | 95 | 30.6 | ||

| 3 | 20 | 10 | 95 | 84 | 3600.0 | 11.6% | 90 | 387.0 | ||

| 4 | 20 | 10 | 84 | 74 | 3600.0 | 11.9% | 78 | 275.7 | ||

| 5 | 20 | 10 | 87 | 81 | 3600.0 | 6.9% | 82 | 140.4 | ||

| 6 | 20 | 10 | 97 | 85 | 3600.0 | 12.4% | 88 | 972.5 | ||

| 7 | 20 | 10 | 89 | 75 | 3600.0 | 15.7% | 84 | 169.6 | ||

| 8 | 20 | 10 | 100 | 88 | 3600.0 | 12.0% | 96 | 80.5 | ||

| 9 | 20 | 10 | 96 | 78 | 3600.0 | 18.8% | 92 | 59.3 | ||

| 10 | 20 | 10 | 93 | 93 | 3542.7 | 0.0% | 93 | 18.2 | ||

| Average | 3594.3 | 10.4% | 218.3 | |||||||

| 0.1 | 0.1 | 1 | 20 | 10 | 100 | NA | 3600.0 | NA | 92 | 172.9 |

| 2 | 20 | 10 | 106 | NA | 3600.0 | NA | 99 | 164.0 | ||

| 3 | 20 | 10 | 105 | 87 | 3600.0 | 17.1% | 93 | 569.1 | ||

| 4 | 20 | 10 | 92 | 67 | 3600.0 | 27.2% | 82 | 600.5 | ||

| 5 | 20 | 10 | 95 | NA | 3600.0 | NA | 86 | 332.0 | ||

| 6 | 20 | 10 | 109 | NA | 3600.0 | NA | 94 | 1852.4 | ||

| 7 | 20 | 10 | 96 | NA | 3600.0 | NA | 88 | 279.8 | ||

| 8 | 20 | 10 | 108 | 82 | 3600.0 | 24.1% | 100 | 133.2 | ||

| 9 | 20 | 10 | 102 | NA | 3600.0 | NA | 94 | 389.3 | ||

| 10 | 20 | 10 | 103 | 96 | 3600.0 | 6.8% | 96 | 149.7 | ||

| Average | 3600.0 | 18.8% | 464.3 | |||||||

| 0.05 | 0.2 | 1 | 20 | 10 | 87 | 87 | 665.8 | 0.0% | 87 | 8.5 |

| 2 | 20 | 10 | 88 | 88 | 2473.2 | 0.0% | 88 | 19.3 | ||

| 3 | 20 | 10 | 86 | 86 | 1391.3 | 0.0% | 86 | 70.4 | ||

| 4 | 20 | 10 | 74 | 74 | 2881.7 | 0.0% | 74 | 102.5 | ||

| 5 | 20 | 10 | 78 | 78 | 1553.5 | 0.0% | 78 | 26.9 | ||

| 6 | 20 | 10 | 86 | 86 | 2776.2 | 0.0% | 86 | 442.7 | ||

| 7 | 20 | 10 | 83 | 83 | 1413.9 | 0.0% | 83 | 17.1 | ||

| 8 | 20 | 10 | 92 | 92 | 297.7 | 0.0% | 92 | 21.0 | ||

| 9 | 20 | 10 | 90 | 90 | 148.5 | 0.0% | 90 | 14.6 | ||

| 10 | 20 | 10 | 90 | 90 | 1074.2 | 0.0% | 90 | 8.9 | ||

| Average | 1467.6 | 0.0% | 73.2 | |||||||

| 0.1 | 0.2 | 1 | 20 | 10 | 96 | 85 | 3600.0 | 11.5% | 92 | 34.3 |

| 2 | 20 | 10 | 103 | 88 | 3600.0 | 14.6% | 99 | 16.5 | ||

| 3 | 20 | 10 | 98 | 93 | 3600.0 | 5.1% | 93 | 175.4 | ||

| 4 | 20 | 10 | 86 | 82 | 3600.0 | 4.7% | 82 | 243.5 | ||

| 5 | 20 | 10 | 90 | NA | 3600.0 | NA | 86 | 84.7 | ||

| 6 | 20 | 10 | 101 | 81 | 3600.0 | 19.8% | 94 | 524.6 | ||

| 7 | 20 | 10 | 90 | 88 | 3600.0 | 2.2% | 88 | 93.1 | ||

| 8 | 20 | 10 | 103 | NA | 3600.0 | NA | 100 | 53.4 | ||

| 9 | 20 | 10 | 97 | 94 | 3600.0 | 3.1% | 94 | 75.5 | ||

| 10 | 20 | 10 | 99 | 89 | 3600.0 | 10.1% | 96 | 14.1 | ||

| Average | 3600.0 | 8.9% | 131.5 | |||||||

∗ The NA represents that no feasible solution has been found within the time limit

From Table 5, we observe that the overall running time of BigM-free Model significantly outperforms that of BigM Model, i.e., almost all of the instances of BigM-free Model can be solved within 10 minutes, while the majority of the instances of BigM Model reach the time limit. The main reasons are two-fold: (i) BigM Model involves binary variables and continuous variables, while BigM-free Model only involves binary variables and continuous variables; and (ii) BigM Model contains big-M coefficients, while BigM-free Model does not. We also observe that, as the risk parameter increases or Wasserstein radius decreases, both formulations take longer time to solve, but BigM-free Model still significantly outperforms BigM Model. These results demonstrate the effectiveness of our proposed BigM-free Model.

6 Conclusion

In this paper, we studied a distributionally robust chance constrained problem (DRCCP) with Wasserstein ambiguity set. We showed that a DRCCP could be formulated as a conditional value-at-risk constrained optimization, thus admits tight inner and outer approximations. Once the feasible region is bounded, we showed that a DRCCP could be mixed integer representable with big-M coefficients and additional binary variables, i.e., a DRCCP can be formulated as a mixed integer conic program. We also compared various inner and outer approximations and proved their corresponding inclusive relations. We further proposed a big-M free formulation for a binary DRCCP and a branch and cut solution algorithm. The numerical studies demonstrated that the proposed formulations are quite promising.

Acknowledgments

The author would like to thank Professor Shabbir Ahmed (Georgia Tech) for his helpful comments on an earlier version of the paper. Valuable comments from the editors and three anonymous reviewers are gratefully acknowledged.

References

- [1] S. Ahmed, J. Luedtke, Y. Song, and W. Xie. Nonanticipative duality, relaxations, and formulations for chance-constrained stochastic programs. Mathematical Programming, 162(1-2):51–81, 2017.

- [2] A. Atamtürk and V. Narayanan. Polymatroids and mean-risk minimization in discrete optimization. Operations Research Letters, 36(5):618–622, 2008.

- [3] D. Bertsimas, S. Shtern, and B. Sturt. A data-driven approach for multi-stage linear optimization. Available at Optimization Online, 2018.

- [4] D. Bertsimas, S. Shtern, and B. Sturt. Two-stage sample robust optimization. arXiv preprint arXiv:1907.07142, 2019.

- [5] J. Blanchet, L. Chen, and X. Y. Zhou. Distributionally robust mean-variance portfolio selection with Wasserstein distances. arXiv preprint arXiv:1802.04885, 2018.

- [6] J. Blanchet, Y. Kang, and K. Murthy. Robust Wasserstein profile inference and applications to machine learning. arXiv preprint arXiv:1610.05627, 2016.

- [7] J. Blanchet and K. R. Murthy. Quantifying distributional model risk via optimal transport. arXiv preprint arXiv:1604.01446, 2016.

- [8] G. C. Calafiore and M. C. Campi. The scenario approach to robust control design. IEEE Transactions on Automatic Control, 51(5):742–753, 2006.

- [9] G. C. Calafiore and L. El Ghaoui. On distributionally robust chance-constrained linear programs. Journal of Optimization Theory and Applications, 130(1):1–22, 2006.

- [10] M. C. Campi, S. Garatti, and M. Prandini. The scenario approach for systems and control design. Annual Reviews in Control, 33(2):149–157, 2009.

- [11] W. Chen, M. Sim, J. Sun, and C.-P. Teo. From CVaR to uncertainty set: Implications in joint chance-constrained optimization. Operations research, 58(2):470–485, 2010.

- [12] Z. Chen, D. Kuhn, and W. Wiesemann. Data-driven chance constrained programs over Wasserstein balls. arXiv preprint arXiv:1809.00210, 2018.

- [13] J. Cheng, E. Delage, and A. Lisser. Distributionally robust stochastic knapsack problem. SIAM Journal on Optimization, 24(3):1485–1506, 2014.

- [14] C. Duan, W. Fang, L. Jiang, L. Yao, and J. Liu. Distributionally robust chance-constrained approximate AC-OPF with Wasserstein metric. IEEE Transactions on Power Systems, 33(5):4924–4936, 2018.

- [15] J. Edmonds. Submodular functions, matroids, and certain polyhedra. In Combinatorial Optimization-Eureka, You Shrink!, pages 11–26. Springer, 2003.

- [16] L. El Ghaoui, M. Oks, and F. Oustry. Worst-case value-at-risk and robust portfolio optimization: A conic programming approach. Operations Research, 51(4):543–556, 2003.

- [17] P. M. Esfahani and D. Kuhn. Data-driven distributionally robust optimization using the Wasserstein metric: Performance guarantees and tractable reformulations. Mathematical Programming, 171(1-2):115–166, 2018.

- [18] N. Fournier and A. Guillin. On the rate of convergence in Wasserstein distance of the empirical measure. Probability Theory and Related Fields, 162(3-4):707–738, 2015.

- [19] R. Gao, X. Chen, and A. J. Kleywegt. Wasserstein distributional robustness and regularization in statistical learning. arXiv preprint arXiv:1712.06050, 2017.

- [20] R. Gao and A. J. Kleywegt. Distributionally robust stochastic optimization with Wasserstein distance. arXiv preprint arXiv:1604.02199, 2016.

- [21] R. Gao and A. J. Kleywegt. Distributionally robust stochastic optimization with dependence structure. arXiv preprint arXiv:1701.04200, 2017.

- [22] G. A. Hanasusanto and D. Kuhn. Conic programming reformulations of two-stage distributionally robust linear programs over Wasserstein balls. Operations Research, 66(3):849–869, 2018.

- [23] G. A. Hanasusanto, V. Roitch, D. Kuhn, and W. Wiesemann. A distributionally robust perspective on uncertainty quantification and chance constrained programming. Mathematical Programming, 151:35–62, 2015.

- [24] G. A. Hanasusanto, V. Roitch, D. Kuhn, and W. Wiesemann. Ambiguous joint chance constraints under mean and dispersion information. Operations Research, 65(3):751–767, 2017.

- [25] A. R. Hota, A. Cherukuri, and J. Lygeros. Data-driven chance constrained optimization under Wasserstein ambiguity sets. arXiv preprint arXiv:1805.06729, 2018.

- [26] R. Ji and M. Lejeune. Data-driven distributionally robust chanceconstrained optimization with Wasserstein metric. Avaiable at Optimization Online, 2018.

- [27] R. Jiang and Y. Guan. Data-driven chance constrained stochastic program. Mathematical Programming, 158:291–327, 2016.

- [28] R. Kiesel, R. Rühlicke, G. Stahl, and J. Zheng. The wasserstein metric and robustness in risk management. Risks, 4(3):32, 2016.

- [29] J. Lee and M. Raginsky. Minimax statistical learning and domain adaptation with Wasserstein distances. arXiv preprint arXiv:1705.07815, 2017.

- [30] B. Li, R. Jiang, and J. L. Mathieu. Ambiguous risk constraints with moment and unimodality information. Mathematical Programming, 173(1):151–192, Jan 2019.

- [31] L. Lovász. Submodular functions and convexity. In Mathematical Programming The State of the Art, pages 235–257. Springer, 1983.

- [32] J. Luedtke and S. Ahmed. A sample approximation approach for optimization with probabilistic constraints. SIAM Journal on Optimization, 19(2):674–699, 2008.

- [33] F. Luo and S. Mehrotra. Decomposition algorithm for distributionally robust optimization using Wasserstein metric. arXiv preprint arXiv:1704.03920, 2017.

- [34] A. Nemirovski and A. Shapiro. Convex approximations of chance constrained programs. SIAM Journal on Optimization, 17(4):969–996, 2006.

- [35] A. Nemirovski and A. Shapiro. Scenario approximations of chance constraints. In Probabilistic and randomized methods for design under uncertainty, pages 3–47. Springer, 2006.

- [36] F. Qiu, S. Ahmed, S. S. Dey, and L. A. Wolsey. Covering linear programming with violations. INFORMS Journal on Computing, 26(3):531–546, 2014.

- [37] R. T. Rockafellar and S. Uryasev. Optimization of conditional value-at-risk. Journal of risk, 2:21–42, 2000.

- [38] S. Shafieezadeh-Abadeh, P. M. Esfahani, and D. Kuhn. Distributionally robust logistic regression. In Advances in Neural Information Processing Systems, pages 1576–1584, 2015.

- [39] Y. Song, J. R. Luedtke, and S. Küçükyavuz. Chance-constrained binary packing problems. INFORMS Journal on Computing, 26(4):735–747, 2014.

- [40] D. M. Topkis. Minimizing a submodular function on a lattice. Operations research, 26(2):305–321, 1978.

- [41] W. Xie. Tractable reformulations of distributionally robust two-stage stochastic programs with Wasserstein distance. Available at Optimization Online, 2018.

- [42] W. Xie and S. Ahmed. Distributionally robust chance constrained optimal power flow with renewables: A conic reformulation. IEEE Transactions on Power Systems, 33(2):1860–1867, 2018.

- [43] W. Xie and S. Ahmed. On deterministic reformulations of distributionally robust joint chance constrained optimization problems. SIAM Journal on Optimization, 28(2):1151–1182, 2018.

- [44] W. Xie and S. Ahmed. Bicriteria approximation of chance constrained covering problems. Operations Research, 2019.

- [45] W. Xie, S. Ahmed, and R. Jiang. Optimized bonferroni approximations of distributionally robust joint chance constraints. Available at Optimization Online, 2017.

- [46] W. Yang and H. Xu. Distributionally robust chance constraints for non-linear uncertainties. Mathematical Programming, 155:231–265, 2016.

- [47] J. Yu and S. Ahmed. Polyhedral results for a class of cardinality constrained submodular minimization problems. Discrete Optimization, 24:87–102, 2017.

- [48] Y. Zhang, R. Jiang, and S. Shen. Ambiguous chance-constrained binary programs under mean-covariance information. SIAM Journal on Optimization, 28(4):2922–2944, 2018.

- [49] C. Zhao and Y. Guan. Data-driven risk-averse two-stage stochastic program with -structure probability metrics. Available at http://www.optimization-online.org/DB_FILE/2015/07/5014.pdf, 2015.

- [50] J. Zou, S. Ahmed, and X. A. Sun. Stochastic dual dynamic integer programming. Mathematical Programming, 175(1):461–502, 2019.

- [51] S. Zymler, D. Kuhn, and B. Rustem. Distributionally robust joint chance constraints with second-order moment information. Mathematical Programming, 137:167–198, 2013.