A Novel Mobile Data Contract Design with Time Flexibility

Abstract

In conventional mobile data plans, the data is associated with a fixed period (e.g., one month) and the unused data will be cleared at the end of each period. To take advantage of consumers’ heterogeneous demands across different periods and meanwhile to provide more time flexibility, some mobile data service providers (SP) have offered data plans with different lengths of period. In this paper, we consider the data plan design problem for a single SP, who provides data plans with different lengths of period for consumers with different characteristics of data demands. We propose a contract-theoretic approach, wherein the SP offers a period-price data plan contract which consists of a set of period and price combinations, indicating the prices for data with different periods. We study the optimal data plan contract designs under two different models: discrete and continuous consumer-type models, depending on whether the consumer type is discrete or continuous. In the former model, each type of consumers are assigned with a specific period-price combination. In the latter model, the consumers are first categorized into a finite number of groups, and each group of consumers (possibly with different types) are assigned with a specific period-price combination. We systematically analyze the incentive compatibility (IC) constraint and individual rationality (IR) constraint, which ensure each consumer to choose the data plan with the period-price combination intended for his type. We further derive the optimal contract that maximizes the SP’s expected profit, meanwhile satisfying the IC and IR constraints of consumers. Our numerical results show that the proposed optimal contract can increase the SP’s profit by , comparing with the conventional fixed monthly-period data plan.

Index Terms:

Mobile Data Plan; Time Flexibility; Data Contract Design; Contract Theory1 Introduction

1.1 Background and Motivation

The fast development and wide adoption of smart phones and tablet devices not only drive the explosive growth of mobile data consumption, but also increase the consumption fluctuation over different plan periods [2]. Conventionally, each data plan specifies data cap for a specific period, which is usually one month. The unused data will be cleared at the end of the period, and the overused data will be charged an additional fee. Hence, the consumers with large consumption fluctuation over different periods (e.g., those having frequent trips) will suffer a large utility loss, because the overused data cannot be compensated by the leftover data in the previous periods.

To deal with this problem, researchers in both academia and industry have proposed many data pricing schemes [3, 4, 5, 6, 7, 8, 9]. However, these pricing schemes do not fully take advantage of users’ heterogeneous demands across periods. Seizing this opportunity, some major mobile data service providers (SP) including AT&T [10] and T-mobile [11] have launched a novel data plan called rollover data plan, where unused data from the monthly plan allowance rolls over for one billing period.

The rollover data plan provides customers more time flexibility by decreasing the frequency of clearing unused data from once per month to once every two months. However, the two-month’s time flexibility may not be enough for the consumers with highly varying data demand. In order to provide time flexibility to more types of customers, we propose a new type of data plan, which specifies the length of period. As a simple example, an SP can offer multiple data plans to consumers, e.g., GB for every month with a price of $ per month, GB for every six months (i.e., with average data cap GB per month) with a price of $ per month, and GB for every year (i.e., with average data cap GB per month) with a price of $ per month. Such data plans can benefit different types of consumers. On one hand, the consumers with highly varying data demand may prefer the data plan with a long period (which provides more time flexibility and can potentially reduce the uncertainty of data demand). On the other hand, the consumers with rarely varying data demand may prefer the data plan with a smaller period (which can reduce the total cost due to the lower unit price). In such a scenario, a natural problem for the SP is how to design a proper set of data plans to maximize its expected profit. The problem is challenging due to (a) the information asymmetry between the SP and consumers and (b) the difficulty in discriminating consumers.

1.2 Key Results and Contributions

In the first part of this paper, we propose a contract-theoretic mechanism for a single SP for discrete-consumer-type model. The SP offers a contract consisting of a set of period-price combinations, where each period-price combination is designed for a specific type of consumers with a specific data demand distribution. Contract theory has been widely applied in solving economics, marketing and network problems [12] [13], and is a useful tool in designing incentive compatible (IC) and individual rational (IR) mechanism [14] to elicit the private information of end users. In this work, we adopt the contract theory to solve the SP’s profit maximization problem under information asymmetry. Specifically, we first provide the IC and IR constraints for the feasible contract to guarantee the truthful demand information revelation of consumers, based on which we further derive the optimal contract that maximizes the SP’s expected profit.

In the second part of the paper, we extend our study to a more general mechanism, which is designed for continuous-consumer-type model. In this case, providing a period-price combination for each consumer type is equivalent to providing infinite combinations, which is not realistic and not consumer friendly. Therefore, our mechanism for continuous consumer types includes the procedure of dividing users into groups according to their types. Then, we design limited pairs of period-price combinations, where each combination is designed for a group of consumers. It is very challenging to use a limited period-price combination to model the infinite consumer types, which usually leads to an NP-hard problem [15]. Therefore, an alternative maximizing algorithm is introduced to find a sub-optimal solution. In the algorithm, we alternatively update the period assignments and group boundaries in order to maximize the SP’s total profit. The main challenge of this method lies in the step of updating group boundaries with fixed period assignment due to the non-convexity of the problem. However, by exploiting the unimodal structure of the objective function, we can obtain the sufficient condition for the optimal solution and show that sufficient condition is satisfied for different scenarios.

The main contributions of the paper are as follow.

-

1.

Novel Model: We study the SP’s mobile data plan design problem from the perspective of data period, which provides consumers with more time flexibility. To our best knowledge, this is the first work that systematically studies such a new data plan design perspective.

-

2.

Novel Method: We propose a novel period-price data plan based on the contract theory. Rather than specifying a price for each data cap in conventional data plans, our proposed data plan specifies a data price for each data period. A higher price is associated with a longer data period.

-

3.

Systematic Solution: We first analyze the period-price contract for discrete-consumer-type model, and then extend the analysis to a more general model with continuous-consumer-type. In continuous-consumer-type model, we assume that the consumer type follows a continuous distribution but the SP offers only a limited number of contract items, which is different from traditional continuous modeling in contract theory. In both cases, we analyze the feasibility (incentive compatibility and individual rationality) of the proposed period-price contract systematically, based on which we further derive the optimal contract that maximizes the SP’s profit.

-

4.

Performance Evaluation: We compare our proposed optimal contract with the conventional monthly-period scheme through numerical simulations. Numerical results show that our proposed contract can increase the SP’s profit over .

1.3 Related Literature on Data Pricing Schemes

The survey by Sen et al. in [3] reviewed the past pricing proposals and discussed several potential research problems. There are mainly three categories of methods to alleviate the problem of monthly data plan inflexibility: (1) Shared Data Plan [4] [5] allows sharing data quota among multiple devices or users, and hence to decrease the average unit usage cost. (2) Sponsored Data [6] [7] is offered by the content service providers, to sponsor the end users for the traffic of viewing their content. (3) Secondary Data Trading [8] [9] is proposed by the service providers, which allows users to trade their unused mobile data with each other. However, all the above methods have their own disadvantages. Shared data plan does not fully take advantage of the heterogeneous demands across plan periods, because there exists possibility that everyone in the shared data is in the peak month. Sponsored data is too specific to the contents, because not every content provider is willing to provide this sponsorship. Secondary data trading is not convenient for operation, since the consumer has to buy or sell every time when he is running out of data or has data left unused.

The papers [16, 17, 18, 19, 20] are the pioneer works that study the rollover data plan. Zheng et al. in [16] evaluated the benefits of rollover data for both SPs and users as well as identify the types of users who would upgrade to rollover data plans. Wang et al. in [17] and [18] analyzed the interactions between an SP and its subscribed users under both traditional and rollover data plans. In [19] and [20], they further analyzed the competitive market with multiple SPs offering rollover data plans with fixed rollover period (i.e., one month). However, none of them considers the design of data plans from the dimension of length of period. To the best of our knowledge, this work is the first paper that systematically studies a data plan design regarding the length of period.

The remainder of this paper is organized as follows. We first analyze the optimal contract for discrete-consumer-type model in Section 2 and Section 3. Specifically, we present the system model and formulate the problem in Section 2. We analyze the feasibility of the contract and propose the optimal contract in Section 3. We analyze the generalized contract for continuous-consumer-type model with group division in Section 4. Performance evaluation is illustrated in Section 5. Finally, Section 6 concludes the paper.

2 System Model

2.1 Service Provider Modeling

In the conventional data plans, the SP provides a unique period choice (e.g., one month). In those data plans, each consumer can consume data up to a quantity of during one period. In our proposed data plans, the SP offers multiple data plans with different plan periods, and we denote the length of the period as (). 111 For presentation convenience, in the rest of the paper, we use “period ” to refer to “period with length ”, and use ”unit period” to refer to ”period with length 1”. We assume that can be any positive number, so that it is possible to provide any time flexibility.

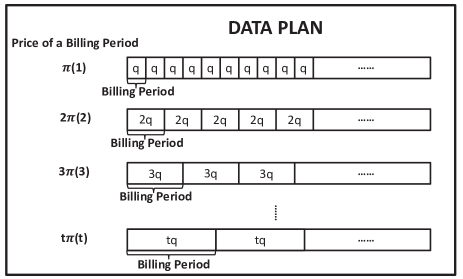

To sharpen the insights of plan periods, we assume that all the data plans are with the same data cap for a unit time period. Figure 1 is an example of the contract of data plans provided by the SP. In the contract, the SP offers a set of combinations, where each combination (also called a contract item) corresponds to one data plan. In each combination, there is a period and a corresponding unit period price . In other words, a consumer who chooses the contract item , needs to pay a price , and can consume data up to a quantity of in a period of . Intuitively, the unit period price is an increasing function of , because a larger period provides more time flexibility for consumers.

We define the cost for the SP as the average expense of providing a data plan of period with data cap . Here, we denote the total expense of a data plan of period as , where the cost (i.e., average expense for one period) is formulated as follows

where is the fixed cost (e.g., the fixed monthly spectrum license fee for providing service and the infrastructure maintenance cost) and is the time-specific cost. We can show that is monotone increasing on . This is because with a smaller , the SP can better predict and hence schedule the demand of consumers. We further assume that grows more rapidly with larger period , which means .222 denotes the first order derivative of with respect to (). and denotes and respectively. Then, we can see and .

The SP’s profit comes from selling data plans with different periods. We use to denote the unit period profit of SP from the data plan , which is the gap between the unit period price and the unit period cost , i.e.,

2.2 Consumer Modeling

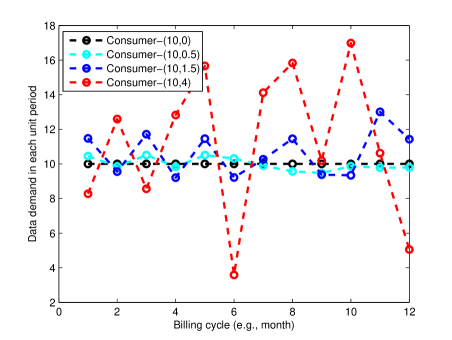

We assume consumer ’s data demand per unit period follows normal distribution with density function , where is the mean and is the standard deviation 333 Normal distribution is widely adopted in modeling consumers’ demand in different areas. For example, [21] applied normal distribution to model consumers’ connectivity of mobile network, while [22] applied normal distribution to model consumers’ demand of electricity.. In our paper, we focus on the demand fluctuation over unit periods, so our design of contract is based on , i.e., standard deviation of consumers’ data demand per unit period. Therefore, in our modeling, we assume that consumers are divided into different groups with different average monthly demand , and we only design contract for a particular group with a certain . Hence, we assume that every consumer has the same and different . For writing convenience, we call a consumer as a type- consumer if the standard deviation of his data demand is . We first assume that the consumer types follow a discrete distribution, and the SP aims to design a specific contract item for each consumer type.444 Mathematically, when we choose a large enough number of types, the discrete-consumer-type model can well approximate a continuous-consumer-type model. In reality, since consumers are heterogeneous, it is more reasonable to assume that consumers’ types follow a continuous distribution [23]. Hence, we will introduce the case of continuous consumer type distribution in Section 4. We denote the set containing all consumer types as . Due to the properties of the normal distribution, when a period of the data plan is changed from unit period to a period of , a consumer’s total data demand within a period still follows normal distribution. The parameters of this normal distribution are as follows: the mean value of the consumer’s total data demand within months is , and the standard deviation is . 555 Intuitively, a consumer with a larger is with a higher data fluctuation, and naturally needs a data plan with higher time flexibility.

We use to denote the valuation of a type- consumer for the contract with period . Similar to [24], for a given period with data cap , we define the unit period valuation as a linear function on the average data consumption per unit period:

| (1) |

where is a predefined parameter, which represents the valuation of unit data, and is identical for all consumers. For writing convenience, we define . We assume the cost of usage exceeding data cap is very large, so that the consumption will not exceed the data cap . Hence, the average data consumption per unit period equals to the consumer’s average data demand , which is the consumer’s maximum average data consumption per unit period, minus average unsatisfied data demand. In a period data plan, the total unsatisfied demand of a type- consumer in a period of is , then the average unsatisfied data demand per unit period is . For example, if a consumer with average data demand GB and standard deviation consume monthly data plan with a quota of GB, and his demands of consecutive two months are GB and GB, then his unsatisfied data demand of these two months are GB and GB, respectively. Since we assume the consumer’s demand per unit period follows normal distribution with and , the average unsatisfied data demand equals to GB, which means his average total data consumption is . As shown in Figure 2, if all the consumers choose the plan of period and , only the consumer with (the black dashed line) can reach an average consumption of . On the contrary, the consumer with (the red dashed line) can satisfy his demand in the , , and periods, but only consumes in the other periods due to the data cap.

From (1), we can find that

and

which means that 1) without considering price, every consumer prefers a larger period and 2) the consumer with larger type has a smaller valuation. Furthermore, is negative through direct calculation, meaning that grows more slowly in a larger period.

The utility of the consumer with type- who accepts the data plan with period is defined as the gap between his valuation and payment of the data plan:

2.3 Contract Formulation

In this paper, we aim to design an optimal contract for the SP to maximize its expected profit. The contract contains a set of combinations, each of which includes a period and a corresponding unit period price . Each consumer can only select one combination. Therefore, for each consumer type , the SP will assign a period with unit period price . The set of period-price combinations shown above is a period-price contract. We denote the contract as .

A feasible contract should satisfy the following two constraints: 1) For any type- consumer, he prefers the contract item with period at the price than any other contract items; 2) The SP should guarantee that the contract designed for any type- consumer leads to non-negative utility so that the consumer is willing to accept the contract designed for him. These two constraints are named as incentive compatibility (IC) constraint and individual rationality (IR) constraint correspondingly. Specifically, we define,

Definition 1.

IC constraint:

Definition 2.

IR constraint:

Any feasible contract satisfies IC and IR constraints, and any contract satisfying IC and IR constraints is feasible. The overall profit of the SP from a feasible contract can be written as:

| (2) |

where is the number of consumers with type-.

| Symbol | Meanings |

|---|---|

| the average data cap per unit period | |

| the time length of the data plan’s period | |

| the unit period price of the data plan | |

| the data item with price | |

| and data quota in a period of | |

| the SP’s unit period expense of offering data plan | |

| with period , i.e., the total expense of a data plan | |

| of period is | |

| the unit period profit of the SP | |

| from the data plan item | |

| consumers’ average data demand in a unit period | |

| In discrete-consumer-type model: | |

| represents the standard deviation | |

| of the unit period data demand of consumer ; | |

| In continuous-consumer-type model: | |

| represents the largest standard deviation | |

| among the unit period data demand | |

| of the consumers in the group | |

| the valuation of a type- consumer | |

| for the contract with period | |

| the total number of consumers | |

| the number of consumers in group | |

| the probability density function | |

| of the distribution of consumer type | |

| the cumulative distribution function | |

| of the distribution of consumer type |

3 Contract Feasibility and Optimality

In this section, we first show the necessary and sufficient conditions for the contract to be feasible. Then we derive the best period assignments and price assignments for the optimal contract that maximizes the SP’s overall profit, which is defined in (2).

According to our assumption in Sec. 2.2, there is a finite number of consumer types . Without loss of generality, we let . Then, we rewrite the period assigned to the type- consumers as , and rewrite the price corresponding to the period as for simplicity. Accordingly, we can rewrite the SP’s profit function and cost function as as and cost function as , respectively. For convenience, we summarize the key notations in Table I.

Therefore, the contract optimization problem can be written as:

Problem 1.

where .

3.1 Feasibility

According to (1), we have the following property: for a given period length increment, the consumers with larger type will have a larger valuation increment than the consumers with smaller type. We call this property as increasing preference (IP) property.666Due to space limit, we put all of the detailed proofs in the online technical report [32].

Proposition 1 (IP property).

For any consumer types and any data plan periods , the following condition holds:

| (3) |

Now, we try to find the necessary and sufficient conditions for the contract to be feasible, i.e., the necessary and sufficient conditions of IC and IR constraints. We show the first necessary condition in the following lemma.

Lemma 1.

For any contract , if it is feasible, then the following condition holds:

Lemma 1 shows that the consumer with larger type should be assigned a longer period.

We show the second necessary condition in the following lemma.

Lemma 2.

For any contract , if it is feasible, then the following condition holds:

Lemma 2 shows that a longer period must be assigned with a higher price. If there is a service with longer period and a lower price, then everyone will select this data plan, and the data plans with shorter periods are meaningless. Together with the observations from Lemma 1, we can find that the data plan with higher price will be assigned to the consumer with larger consumer type (i.e., standard deviation).

From the above two lemmas and IP property, we have the following theorem, which shows the necessary and sufficient conditions for a feasible contract.

Theorem 1 (Necessary and Sufficient conditions for a feasible contract).

For any contract , its IC and IR constraints are equivalent to the following conditions:

| (4) | ||||

| (5) | ||||

| (6) | ||||

| (7) |

The feasible regions of price assignments are then

From IP property, we have . Therefore, the feasible regions of price assignments are not empty.

3.2 Optimality

To solve the contract optimization problem, we first solve the optimal price assignments given the fixed period assignments, and then solve the optimal period assignments by substituting the derived price assignments. From the conditions in Theorem 1, we can get the following lemma, which leads to the optimal price assignments.

Lemma 3.

For any feasible contract with fixed periods , the set of optimal price assignments that maximizes under the conditions in Theorem 1 is given by:

| (8a) | |||

| (8b) | |||

Proof.

Since the period assignments are fixed, the total cost of the SP is fixed. Therefore, if there is another set of price assignments that leads to a larger profit (i.e., ), then there is at least one price . According to Theorem 1, to guarantee the feasibility of the contract, the following constraint on must be satisfied:

| (9) |

From (8) we have

| (10) |

By substituting (10) into (9), we have , which implies . Since , the IR condition is violated. Therefore, there does not exist any set of feasible price assignments with a larger profit than . ∎

From Lemma 3, we can find that for fixed period assignments, the optimal price assignments are:

| (11) |

The maximum overall profit is obtained by solving the following optimization problem

| (12) |

where is the overall profit of the optimal contract with fixed period assignments . By subsituting the derived optimal price assignments (11) into (2), we have:

| (13) |

where and .

We define as and find that is only based on the period , which is designed for type consumers. Therefore, the contract optimization problem can be divided into the following optimization problems.

| (14) |

We use to indicate the period that maximizes , i.e., . Since is concave for all 777It is because both and are negative. , the optimal is either of the boundary points or the critical point (the point satisfying and ).

We can show that if the period assignments are in increasing order, then they are the optimal solution of problem (12). However, it is possible that are not in increasing order, which means that they may not be feasible. Each set of infeasible period assignments must have at least one infeasible sub-sequence, which is defined in the following definition:

Definition 3.

A sub-sequence is an infeasible sub-sequence if it satisfies the following two conditions:

Next, we design a mechanism to replace each infeasible sub-sequence by a feasible sub-sequence. We apply the following proposition to design the mechanism.

Proposition 2.

There are K concave functions and . If , then the optimal solution

| (15) |

satisfies .

The proposition is proved in [25].

Based on Proposition 2, we can see that Algorithm 1, which is an iterative algorithm, can be used to adjust infeasible sub-sequences in into feasible sub-sequences. The details of Algorithm 1 are shown as follows.

4 Continuous-Consumer-Type with Group Division

In general, since consumers are mutually independent, the probability that each two consumers have the same standard deviation (i.e., ) approaches to zero. Therefore, it is more realistic to assume that the consumer types follow a continuous distribution. Under such an assumption, to design a contract item for each consumer type is equivalent to providing infinite contract items, which is not realistic and not consumer friendly. Thus, we propose a novel contract design mechanism for continuous-consumer-type model. The mechanism divides the consumers into limited number of groups according to their types and give a contract item for each group. Specifically, in this mechanism, we optimize the group boundaries as well as the period and price assignments in order to maximize the SP’s overall profit.

4.1 Contract Formulation

We assume that the SP divides the consumers into groups. Instead of designing a distinct contract item for each consumer type, the SP offers a single contract item for each group of consumer types. We denote the set of group indices as , where the minimum consumer type in the () group is denoted as and the maximum consumer type in the group is denoted as . We assume that the consumer type follows a continuous distribution and the probability density function is . We use (where ) and (where ) to denote the minimum and maximum value of the feasible interval, i.e., only when .888 To better illustrate the insights, we assume that for all in this paper. For the case that for some in the feasible interval, we can also show that our following analysis is valid. Without loss of generality, we assume . Since the consumer types follow a continuous distribution, we have for all . The set of variables is named as group boundaries. In this paper, we let for simplicity. We use to denote the total number of consumers, and denote the number of consumers in the group as , where

| (16) |

In (16), is the cumulative distribution function of consumer type , and

In other words, denotes the number of consumers with type less than or equal to .

Similar to our discussion on the contract for discrete-consumer-type model in Sec. 2 and 3, for each consumer group , the SP will assign a combination including a period and a unit period price . We denote the contract for continuous-consumer-type model as . The expected profit of the SP can be written as:

| (17) | ||||

To guarantee the feasibility of the contract, it should satisfy the IC and IR constraints: 1) For any consumer in group , he prefers the contract item that with period at the price than any other contract items; 2) The SP should guarantee that the contract item designed for any consumer group leads to non-negative utility for each consumer in this group so that the consumers are willing to accept the contract designed for them. Specifically, we define,

Definition 4.

IC constraint:

Definition 5.

IR constraint:

Then, the SP’s profit maximization problem becomes finding the optimal group boundaries, period assignments and price assignments, i.e.,

| (18) |

subject to the IC and IR constraints in Definition 4, 5 and the following boundary condition:

| (19) |

First, we can find that IP property in Proposition 1 is still satisfied in continuous-consumer-type model. Then, we try to find the necessary and sufficient conditions for the IC and IR constraints. We show the first necessary condition in the following corollary.

Corollary 1.

For any contract , if it is feasible, then the following condition holds:

Corollary 1 is directly obtained from Lemma 1. Hence, the proof of the corollary is structurally the same as Lemma 1 and is omitted.

The second necessary condition is shown in Lemma 2, which shows that a longer period must be assigned with a higher price.

From Lemma 2, Corollary 1 and IP property, we have the following theorem, which shows the necessary and sufficient conditions of the IC and IR constraints for the contract for continuous-consumer-type model with group division.

Theorem 2.

For any contract , its IC and IR constraints are equivalent to the following conditions:

| (20) | |||

| (21) | |||

| (22) |

4.2 Contract Optimization

According to Theorem 2, we can obtain the optimal price assignments as follows:

which implies

| (23) |

By substituting (23) into (17), the overall profit of the SP can be rewritten as follows

| (24a) | ||||

| (24b) | ||||

| (24c) | ||||

| (24d) | ||||

where and .

| (32) |

| (36) |

4.2.1 Introduction of The Alternative Maximizing Algorithm

Finding the optimal period assignments and group boundaries that can maximize the SP’s overall profit with price assignments in (23) is very challenging because problem (18) is NP-hard [15]. Therefore, we introduce an alternative maximizing algorithm to find a sub-optimal solution. In this algorithm, we divide the variables into two groups, where the first group contains all the period assignments , and the other group contains all the group boundaries . At the beginning of the algorithm, we divide the consumers into groups by randomly generating group boundaries such that . Then, we iterate the following two steps. In the first step, we keep the group boundaries unchanged and maximize the overall profit by tuning period assignments . In the second step, we keep period assignments (which are obtained by solving the problem in the previous step) unchanged and update group boundaries to maximize . For the rest of the paper, we will simply use to denote which is the threshold between group and group .

The details of these two steps are as follows.

-

•

Step I: In this step, we find the optimal period assignments that can maximize the overall profit with fixed group boundaries . Specifically, we have the following problem

(25) We can show that the overall profit in (24c) is structurally similar to the overall profit (13) in Sec. 3. Therefore, this optimization problem can be solved through the same method that solves problem (12).

For writing convenience, we define

(26) where and . Then, we divide the problem (25) into optimization problems

(27) Since is concave for all , the period assignment that can maximize is at the boundary points or at the critical point, i.e.,

(28) where is the solution of .

By denoting the optimal solution of problem (25) as , we can see that if the period assignments from (27) are in increasing order, then for all . However, if are not in increasing order, which means that they may not be feasible, we need to use Algorithm 1 to adjust infeasible period assignments to make them feasible. In the input of the algorithm, we define as in (26) and let .

-

•

Step II: In this step, we find the optimal group boundaries that can maximize the overall profit with fixed period assignments . Specifically, we have the following optimization problem:

(29) By defining as

(30a) (30b) we can find that the overall revenue in (24d) can be represented as the summation of . (30) implies that is only related to , i.e., the group boundary between group and group , and independent of the other group boundaries . Therefore, the best group boundaries for (29), denoted by , can be computed by separately maximizing each of , .

We use to denote the group boundary that maximizes , i.e.,

(31) If the group boundaries obtained by solving (31) are in increasing order, are exactly the solution of (29), i.e., . If are not in increasing order, some further steps are needed to obtain the optimal group boundaries of (29) from .

In order to solve the problem (31), we find the first order derivative of with respect to , which is shown in (32) on the top of this page. Although the form of is complicated, we obtain the unimodality of in the following Theorem.

Theorem 3.

If the distribution of the consumer types satisfies the condition

(33) then with the fixed period assignments, the formula is unimodal with respect to for all .

Proof.

By defining as

(34) the first order derivation of with respect to can be rewritten as:

(35) Since is positive and is a constant for fixed period assignments, is unimodal if is monotonic with respect to .

To study the monotonicity of , we need to find the first order derivative of it with respect to , which is shown in (36) on the top of this page. Before we find the sign of the first order derivation, we first show the following lemma.

Lemma 4.

For any and , we have

(37) In next subsection, we will show that (33) applies for some typical distributions. Then, according to Theorem 3, is an unimodal function with respect to . Therefore, the optimal is at the boundary point or the critical point, i.e.,

(38) where is the solution of .

The group boundaries , which are obtained by separately maximizing each of , may not be in increasing order, which means they may not be feasible. Each set of infeasible group boundaries must have at least one infeasible sub-sequence, which is defined in Definition 3. In order to adjust an infeasible sequence to a feasible sub-sequence, we first show a property of in the following proposition.

Proposition 3.

For any and , the function is a unimodal function with respect to .

Then we apply the following proposition to design a mechanism to deal with the infeasible sub-sequence in .

Proposition 4.

There are unimodal functions and . If , where and , then the optimal solution

satisfies .

The details of the alternative maximizing algorithm are illustrated in Algorithm 2.

4.2.2 Convergence of The Alternative Maximizing Algorithm

In the alternative maximizing algorithm, with arbitrary initialized group boundaries, we alternatively update the period assignments and group boundaries in order to maximize the overall profit .

In each step of the alternative maximizing algorithm, we try to adjust the period assignments or group boundaries to maximize . Hence, the value of is monotonically increasing. Since the value of overall profit is upper bounded, the algorithm will finally converge.

4.3 Analysis of Some Typical Distributions of The Consumer Types

In this subsection, we will show that (33) in Theorem 3 applies for some typical distributions of consumer types, including uniform distribution, exponential distribution and truncated normal distribution.

4.3.1 Uniform Distribution

We first study the case that the consumer types follow a uniform distribution. Specifically, we have

| (39) | |||

| (40) | |||

| (41) |

By substituting (39), (40) and (41) into (i.e., the left hand of (33)), we have

where is from the fact that for all . In conclusion, (33) holds for the case of uniform distribution in consumer types.

4.3.2 Exponential Distribution

Next, we study the case that the consumer types follow an exponential distribution. Specifically, we have

| (42) | |||

| (43) | |||

| (44) |

Here, is the rate parameter of the exponential distribution. By substituting (42), (43) and (44) into , we have

When , we have

| (45) |

where and . Before finding the lower bound of (45), we first derive the following proposition.

Proposition 5.

For , the formula is lower bounded by .

4.3.3 Truncated Normal Distribution

In truncated normal distribution, we can not obtain the expression of the cumulative function in closed-form due to the non-integrability of the formula. Hence, we are not able to show (33) analytically. In this case, we use numerical results to illustrate that (33) holds for various parameters.

When , we have , which means that (33) holds for the case .

When , to simplify the notations, we define a function as

If we can show that for various parameters, which means , then we can see that (33) holds for truncated normal distribution with various parameters.

In our simulation settings, we let the minimum value of truncated normal distribution and the maximum value of truncated normal distribution . We use and to denote the mean and the standard deviation of the corresponding normal distribution.

5 Simulation Results

In the simulation, we first implement the proposed period-price contract in discrete-consumer-type model, and then implement the proposed period-price contract in continuous-consumer-type model. Without loss of generality, we set the predefined parameter and the average data demand per unit period as . We assume the data cap of the unit period data plan is and the cost function of the SP is 999 According to [26, 27, 28], a consumer usually chooses a data plan with monthly data cap larger than his average consumption. Period of data plan helps an SP to manage its network capacity, because an SP should make sure a corresponding network capacity is prepared during the whole period in case that the consumers consume all data quota for the whole period in a very short time. Hence, a larger period requires the SP to prepare more network capacity and will lead to a higher cost. Here for simplicity, we consider a linear-form cost, which has been widely used to model an operator’s operational cost (e.g., [29, 30]). .

5.1 Discrete-Consumer-Type

In discrete-consumer-type model, we assume the number of consumer types . The set of consumer types is .

We run the simulation of the optimal contract in two cases. In Case (1), the numbers of consumers in each type are identical. In Case (2), the numbers are distributed in a mountain shape, which means the probability of medium is large.

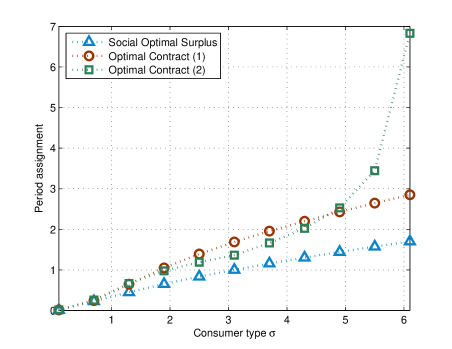

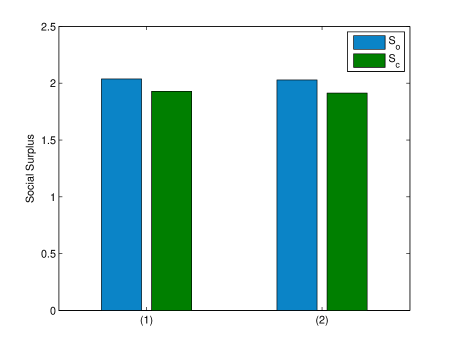

We define the social surplus generated by the contract with period , denoted by , as the aggregate utilities of SP and the consumer with type , i.e.,

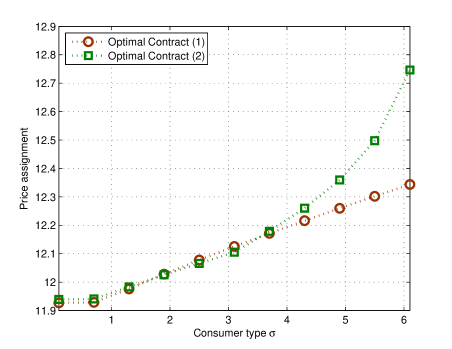

Figure 4 and Figure 5 show the period and price assignments in the optimal contract. The blue curve in Figure 4 presents the social optimal period assignments, which maximize the social surplus. Specifically, we have . From Figure 4, we can see that the social optimal period assignments are always smaller than that in the optimal contract. This is because the optimal contract is aimed to maximize the SP’s overall profit rather than the social surplus. The SP prefers to increase the period assigned to the higher type consumers in order to increase the interest of the lower type consumers in the short period contract items. Hence, by increasing the price of the short period contract items, the SP can increase the profit.

Figure 6 shows the social surplus in the optimal contract and social optimal assignments. The bars denote the social surplus in the social optimal period assignments while the social surplus of our proposed optimal contract is represented by the bars . We can see that is larger than in both Case (1) and Case (2), since the optimal contract is aimed to maximize the SP’s profit rather than social surplus. However, our proposed optimal contract can achieve around of the maximum social surplus.

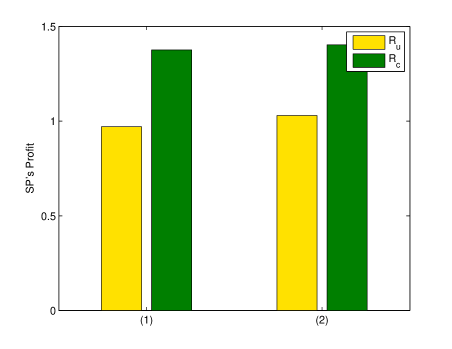

The comparison between our proposed optimal contract and conventional monthly-period scheme in terms of SP’s profit is shown in Figure 7. The bars and denote the profits of the SP in the monthly-period scheme and our optimal contract, respectively. We can see that our optimal contract can increase the SP’s profit by 41% and 37% for Case (1) and Case (2) correspondingly. This is because the optimal contract increases the period assigned to the consumers with larger consumer types in order to increase the interest of the smaller type consumers in the short period contract items. Hence, by increasing the price of the long period contract items and decreasing the period of the short period items, the SP can increase its profit.

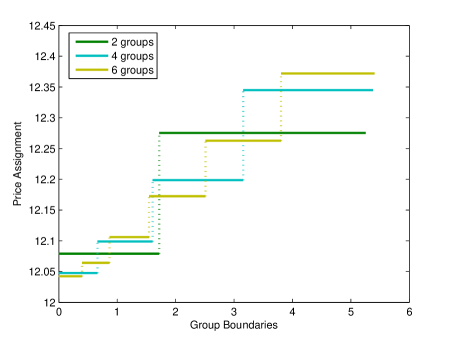

5.2 Continuous-Consumer-Type

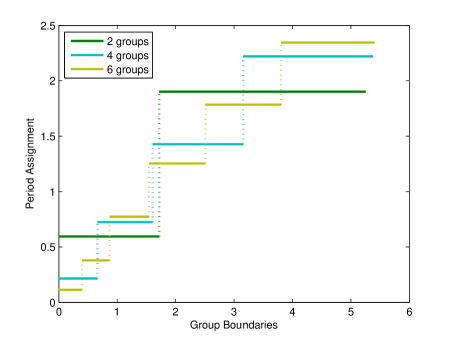

Next, we implement the proposed contract for continuous-consumer-type model. Figure 8 and Figure 9 show the period and price assignments in the contract with different numbers of contract items. The x-axis represents the group boundaries. In these two figures, the distribution of consumer types (i.e., ) follows uniform distribution with and .

From the figures we can find that as the number of group increases, more consumers are under served. From IP Property in Proposition 1, with a given period length increment, the consumers with larger consumer type have a larger valuation increment than the consumers with smaller types. Therefore, with more groups, the SP can serve consumers with a wider range, increase the price of contract item designed for consumers with large types and decrease the cost of serving the consumers with small types by increasing period assigned to consumers with large types and decreasing the period assigned to consumers with small types. In all these ways, the SP can increase its overall profit.

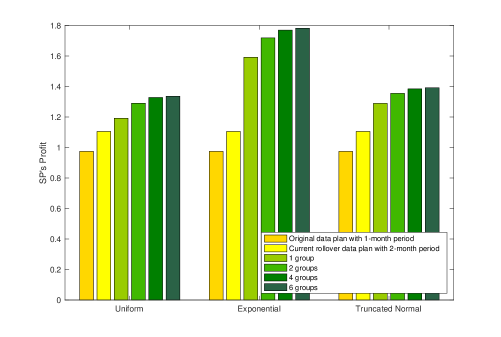

Figure 10 represents the comparison between our proposed contracts with different group numbers and two state-of-art data plans in terms of SP’s profit. They are the original one-month data plan and the rollover data plan provided by AT&T. The rollover scheme can be seen as a contract with period of two months. We run the simulation under the cases of 1) uniformly distributed consumer types, 2) exponentially distributed consumer types and 3) truncated normally distributed consumer types. Comparing with the original data plan with -month period, our contract with groups can increase the SP’s profit by , and in case 1), case 2) and case 3), respectively. Besides, comparing with the rollover data plan with -month period, our contract with groups can increase the SP’s profit by , and in case 1), case 2) and case 3), respectively. From the figure we can find that the SP’s profit is increasing with the number of groups. Specifically, by increasing the number of groups from to , the SP can increase its profit by %, % and % in case 1), case 2) and case 3), respectively; by increasing the number of groups from to , the SP can increase its profit by by %, % and % in case 1), case 2) and case 3), respectively. Therefore, the SP needs to optimize the number of contract items instead of just offering one or two contract items. Moreover, the increment from groups to groups is very small, i.e., the profit of the SP achieved by the contract with groups can reach over of that by the contract with groups. Since more groups will lead to more operation costs and is not consumer friendly, we can conclude that groups is a suitable choice of group numbers, and it is in line with the number of contract items in real life [31].

6 Conclusion

In this paper, we introduce the design of data plans with different lengths of period, in order to provide more time flexibility to consumers and increase the SP’s profit. We design a contract that contains a set of period-price combinations for each of the discrete-consumer-type model and the continuous-consumer-type model. In the discrete-consumer-type model, each combination is intended for a consumer type, while in continuous-consumer-type model, each combination is intended for a range of consumer types. We design the IC and IR constraints of the contracts, under which the consumer will select the contract item designed for him rather than the others. We find the sufficient and necessary conditions of the feasible contract and design an optimal (sub-optimal) contract for the SP to maximize its overall profit in each model. In the future, we will extend this work for two perspectives. The first one is the user mobility. We will consider a city-wise SP, who can deploy service in several cities, then the SP’s price differentiation problem in different cities needs to be considered based on user mobilities. The second one is the multi-dimensional data plan setting. For example, the SP can offer a two-dimensional contract, which includes both the length of the data period and the volume of the data cap.

7 Acknowledgments

This work is supported by the National Natural Science Foundation of China (Grant No. 61771162). Lin Gao is the corresponding author.

References

- [1] Y. Wei, J. Yu, T. M. Lok, and L. Gao, “A novel mobile data plan design from the perspective of data period,” in Proc. of IEEE ICCS, Dec 2016.

- [2] C. Joe-Wong, S. Ha, S. Sen, and M. Chiang, “Do mobile data plans affect usage? results from a pricing trial with isp customers,” in Passive and Active Measurement, pp. 96–108, Springer, 2015.

- [3] S. Sen, C. Joe-Wong, S. Ha, and M. Chiang, “A survey of smart data pricing: Past proposals, current plans, and future trends,” ACM Computing Surveys (CSUR), vol. 46, no. 2, 2013.

- [4] Y. Jin and Z. Pang, “Smart data pricing: To share or not to share?,” in Proc. of IEEE INFOCOM Workshop Smart Data Pricing (SDP), pp. 583–588, April 2014.

- [5] T. Yu, Z. Zhou, D. Zhang, X. Wang, Y. Liu, and S. Lu, “Indapson: An incentive data plan sharing system based on self-organizing network,” in Proc. of IEEE INFOCOM, pp. 1545–1553, April 2014.

- [6] M. Andrews, U. Ozen, M. I. Reiman, and Q. Wang, “Economic models of sponsored content in wireless networks with uncertain demand,” in Proc. of IEEE INFOCOM Workshop Smart Data Pricing (SDP), pp. 345–350, April 2013.

- [7] L. Zhang and D. Wang, “Sponsoring content: Motivation and pitfalls for content service providers,” in Proc. of IEEE INFOCOM Workshop Smart Data Pricing (SDP), pp. 577–582, April 2014.

- [8] L. Zheng, C. Joe-Wong, C. W. Tan, S. Ha, and M. Chiang, “Secondary markets for mobile data: Feasibility and benefits of traded data plans,” in Proc. of IEEE INFOCOM, pp. 1580–1588, April 2015.

- [9] J. Yu, M. H. Cheung, J. Huang, and H. Poor, “Mobile data trading: A behavioral economics perspective,” in Proc. of IEEE WiOpt, pp. 363–370, May 2015.

-

[10]

AT&T, “Rollover data plan.”

[Online]. Available:

https://www.

att.com/shop/wireless/rollover-data.html. - [11] T-Mobile, “T-Mobile rollover data plan.” [Online]. Available: http://www.t-mobile.com/offer/data-stash-data-roll.html.

- [12] L. Duan, L. Gao, and J. Huang, “Cooperative Spectrum Sharing: A Contract-Based Approach,” IEEE Transactions on Mobile Computing, vol. 13, no. 1, pp. 174–187, 2014.

- [13] L. Gao, J. Huang, Y. J. Chen, and B. Shou, “An integrated contract and auction design for secondary spectrum trading,” IEEE Journal on Selected Areas in Communications, vol. 31, no. 3, pp. 581–592, 2013.

- [14] P. Bolton and M. Dewatripont, Contract theory. MIT press, 2005.

- [15] S. Li, J. Huang, and S.-Y. R. Li, “Dynamic profit maximization of cognitive mobile virtual network operator,” IEEE Transactions on Mobile Computing, vol. 13, no. 3, pp. 526–540, 2014.

- [16] L. Zheng and C. Joe-Wong, “Understanding rollover data,” in Proc. of IEEE INFOCOM Workshop Smart Data Pricing (SDP), April 2016.

- [17] Z. Wang, L. Gao, and J. Huang, “Pricing Optimization of Rollover Data Plan,” in Proc. of IEEE WiOpt, May 2017.

- [18] Z. Wang, L. Gao, and J. Huang, “A Contract-Theoretic Design of Mobile Data Plan with Time Flexibility,” in Proc. of ACM NetEcon, June 2017.

- [19] Z. Wang, Lin Gao, and J. Huang, “Multi-Dimensional Contract Design for Mobile Data Plan with Time Flexibility,” in Proc. of ACM MobiHoc, June 2018.

- [20] Z. Wang, Lin Gao, and J. Huang, “Duopoly Competition for Mobile Data Plans with Time Flexibility,” in Proc. of IEEE WiOpt, May 2018.

- [21] Z. Bao, W. Qiu, L. Wu, F. Zhai, W. Xu, B. Li, and Z. Li, “Optimal Multi-Timescale Demand Side Scheduling Considering Dynamic Scenarios of Electricity Demand,” IEEE Transactions on Smart Grid, vol. PP, no. 99, pp. 1–1, 2018.

- [22] J. Ding, R. Xu, Y. Li, P. Hui, and D. Jin, “Measurement-driven Modeling for Connection Density and Traffic Distribution in Large-scale Urban Mobile Networks,” IEEE Transactions on Mobile Computing, vol. PP, no. 99, pp. 1–1, 2018.

- [23] Y. Zhang, L. Song, M. Pan, Z. Dawy, and Z. Han, “Non-Cash Auction for Spectrum Trading in Cognitive Radio Networks: Contract Theoretical Model With Joint Adverse Selection and Moral Hazard,” IEEE Journal on Selected Areas in Communications, vol. 35, no. 3, pp. 643–653, 2017.

- [24] R. T. Ma, “Usage-based pricing and competition in congestible network service markets,” IEEE/ACM Transactions on Networking, vol. 24, no. 5, pp. 3084–3097, 2016.

- [25] L. Gao, X. Wang, Y. Xu, and Q. Zhang, “Spectrum trading in cognitive radio networks: A contract-theoretic modeling approach,” IEEE Journal on Selected Areas in Communications, vol. 29, no. 4, pp. 843–855, 2011.

- [26] W. Dai and S. Jordan, “Design and impact of data caps,” in Proc. of IEEE GLOBECOM, pp. 1650–1656, December 2013.

- [27] W. Dai and S. Jordan, “The effect of data caps upon isp service tier design and users,” ACM Transactions on Internet Technology (TOIT), vol. 15, no. 2, p. 8, 2015.

- [28] X. Wang, R. T. Ma, and Y. Xu, “The role of data cap in two-part pricing under market competition,” in Proc. of IEEE INFOCOM Workshop Computer Communications, April 2015.

- [29] L. Duan, J. Huang, and B. Shou, “Duopoly competition in dynamic spectrum leasing and pricing,” IEEE Transactions on Mobile Computing, vol. 11, no. 11, pp. 1706–1719, 2012.

- [30] Y. Luo, L. Gao, and J. Huang, “An integrated spectrum and information market for green cognitive communications,” IEEE Journal on Selected Areas in Communications, vol. 34, no. 12, pp. 3326–3338, 2016.

-

[31]

CMHK, “Local Service Plan.”

[Online]. Available:

http://www.hk.

chinamobile.com/en/corporate_information/Service_Plans/4.5G

_Service_Plan/4Glocal_serviceplan.html. - [32] Y. Wei, J. Yu, T.-M. Lok, and L. Gao, “A Novel Mobile Data Contract Design with Time Flexibility,” Technical Report, [Online]. Available: http://arxiv.org/abs/1806.07308

![[Uncaptioned image]](/html/1806.07308/assets/x11.png) |

Yi Wei (S’14) received her Ph.D. degree in the Department of Information Engineering at the Chinese University of Hong Kong in 2017. Her research interests include smart data pricing and interference alignment in wireless communication. She is a student member of IEEE. |

![[Uncaptioned image]](/html/1806.07308/assets/x12.png) |

Junlin Yu (S’14) received his Ph.D. degree in the Department of Information Engineering at the Chinese University of Hong Kong in 2017. His research interests include behavioral economical studies in wireless communication networks and optimization in mobile data trading. He is a student member of IEEE. |

![[Uncaptioned image]](/html/1806.07308/assets/x13.png) |

Tat-Ming Lok (SM’03) received the B.Sc. degree in electronic engineering from the Chinese University of Hong Kong, Shatin, Hong Kong, in 1991 and the M.S.E.E. and Ph.D. degrees in electrical engineering from Purdue University, West Lafayette, IN, USA in 1992 and 1995 respectively. He was a Postdoctoral Research Associate with Purdue University. He then joined the Chinese University of Hong Kong, where he is currently an Associate Professor. His research interests include communication theory, communication networks, signal processing for communications, and wireless systems. He has served on Technical Program Committees of different international conferences, including the IEEE International Conference on Communications, IEEE Vehicular Technology Conference, IEEE Globecom, IEEE Wireless Communications and Networking Conference, and IEEE International Symposium on Information Theory. He was a co-chair of the Wireless Access Track of the IEEE Vehicular Technology Conference in 2004. He also served as an Associate Editor for the IEEE TRANSACTIONS ON VEHICULAR TECHNOLOGY from 2002 to 2008. He has been serving as an Editor for the IEEE TRANSACTIONS ON WIRELESS COMMUNICATIONS since 2015. |

![[Uncaptioned image]](/html/1806.07308/assets/x14.png) |

Lin Gao (S’08-M’10-SM’16) is an Associate Professor with the School of Electronic and Information Engineering, Harbin Institute of Technology, Shenzhen, China. He received the Ph.D. degree in Electronic Engineering from Shanghai Jiao Tong University in 2010. His main research interests are in the area of network economics and games, with applications in wireless communications and networking. He was a co-recipient of three Best Paper Awards from WiOpt 2013, 2014, 2015, and one Best Paper Award Finalist from IEEE INFOCOM 2016. He received the IEEE ComSoc Asia-Pacific Outstanding Young Researcher Award in 2016. |

Appendix A Proof of Proposition 1

Appendix B Proof of Lemma 1

We prove the lemma by contradiction. If and hold at the same time, then from the IP property we have:

which violates the IC constraint:

Appendix C Proof of Lemma 2

Proof.

We prove the right direction first and then the left:

-

1.

From the IC constraint, if , we have:

Since and , we can find:

-

2.

From the IC constraint, we have:

If , then

Since and , we can find .

∎

Appendix D Proof of Theorem 1

We first prove the sufficiency of the conditions in Theorem 1 and then the necessity of them.

-

1.

Sufficiency.

We can use mathematical induction to prove the sufficiency of the conditions. We use to denote the subset of contract containing the last contract items, i.e., .

We first prove is feasible. Since there is only one consumer type in this contract, we only need to justify the IR constraint, which can be proved directly from the condition (5) in Theorem 1.

Then, we prove if is feasible, is also feasible. We have the following conditions if is feasible.

(47) (48) (49) From the conditions (6) and (7) of Theorem 1, we have:

(50) (51) With the above conditions and the IP property, we are going to prove that the IC and IR constraints for the contract are satisfied.

IC constraints:

(52) (53) IR constraint:

(54) If the above constrains are satisfied, is feasible.

By adding up (47) and (51), we have:

for all . From the IP property, we have:

for all , since and . By adding up the above two equations, (52) is proved.

-

2.

Necessity.

Appendix E Proof of Theorem 2

Appendix F Proof of Lemma 4

Without loss of generality, we can let , where .

When , we have and the value of is negative. Hence, (37) is satisfied.

When , we rewrite the formula as . The second order derivative of is , which is negative. Hence, the optimal solution that leads to the maximum value of satisfies

Therefore, the maximum value of is . In other words, the maximum value of is and (37) is satisfied.

Appendix G Proof of Proposition 3

The first order derivative of with respect to is

where is defined in (34). Since the first order derivative of is non-positive for all , we have . Hence, crosses zero at most once. Together with the facts that i) is a constant with respect to and ii) is always positive, we have the result that is unimodal with respect to .

Appendix H Proof of Proposition 4

The statement is trivial if , thus we focus on the case of .

The statement can be proved if for arbitrary , we can find a such that . There are two possible cases of : 1) , and 2) .

For the case that . Since is the optimal solution of , we have for any . Since and is a unimodal function, we have for any , which means that . Therefore, by letting , we have .

For the case that , by letting , we have . This is because and is a unimodal function, which implies that 1) for any , and 2) .

Appendix I Proof of Proposition 5

First, we rewrite the formula as

Proposition 5 is proved if . Since the first order derivative of is , which is positive for any , the minimum value of is then lower bounded by .