Reconstruction methods for networks:

the case of economic and financial

systems

Abstract

The study of social, economic and biological systems is often (when not always) limited by the partial information about the structure of the underlying networks. An example of paramount importance is provided by financial systems: information on the interconnections between financial institutions is privacy-protected, dramatically reducing the possibility of correctly estimating crucial systemic properties such as the resilience to the propagation of shocks. The need to compensate for the scarcity of data, while optimally employing the available information, has led to the birth of a research field known as network reconstruction. Since the latter has benefited from the contribution of researchers working in disciplines as different as mathematics, physics and economics, the results achieved so far are still scattered across heterogeneous publications. Most importantly, a systematic comparison of the network reconstruction methods proposed up to now is currently missing. This review aims at providing a unifying framework to present all these studies, mainly focusing on their application to economic and financial networks.

keywords:

entropy maximization , network reconstruction , statistical inference , economic and financial networks , systemic risk evaluationPACS:

02.50.Tt , 89.65.Gh , 89.70.Cf , 89.75.HcThe study of truth requires a considerable effort

which is why few are willing to undertake it out of love of

knowledge

— Thomas Aquinas, Summa Contra Gentiles

List of the symbols employed in the review

Throughout this work we shall employ top-hatted letters (e.g., , , , etc.) for the measured values of the empirical networks to be reconstructed, while we shall use the same letters (e.g., , , , etc.) without any addition to indicate the same quantities when considered as (deterministic or stochastic) variables. In particular:

-

: the (observed) network to reconstruct;

-

: ensemble of network configurations used to reconstruct ;

-

: (fixed) number of nodes of (and of all networks in the ensemble );

-

: a generic network configuration belonging to ;

-

: probability measure on the ensemble of configurations ;

-

: information content of the configuration ;

-

: network Hamiltonian of the configuration , i.e. linear combination of the constraints determining its probability ;

-

: Shannon entropy;

-

: Lagrangian functional, i.e., the constrained Shannon entropy;

-

: number of constraints (excluding normalization) in ;

-

: -th constraint;

-

: -th Lagrange multiplier, controlling for the -th constraint;

-

: estimation of the -th Lagrange multiplier for ;

-

: log-likelihood of given the Lagrange multipliers defining ;

-

: expected value over the ensemble of a generic quantity of interest ;

-

: ensemble standard deviation of a generic quantity of interest ;

-

: estimate of quantity by the algorithm “name”;

-

: number of links in a network;

-

: density of links in a (directed) network, defined as the fraction of possible connections in the network that are actually realized;

-

: weighted adjacency matrix representing a network, with generic element denoting the weight of the link from node to node ;

-

: adjacency matrix representing a binary version of , with generic element if (and 0 otherwise);

-

and : out-strength and in-strength of node , or equivalently the marginal row and column sums of ;

-

and : out-degree and in-degree of node , or equivalently the marginal row and column sums of ;

1 Introduction

Networks: the why and how of a theory

There is nowadays an overwhelming evidence that a large deal of complex systems around us can be successfully described by means of complex networks [1, 2, 3]. Graph theory, from which complex networks theory originates, was firstly developed in the XVIII century as an application of discrete mathematics to the well-known “Königsberg bridge problem” [4] and for many years it remained relegated to merely solving puzzling topological problems [5].

A new burst of activity was registered in 1920, to provide mathematical support to the analysis of social networks [6, 7]. This laid the foundation for “sociometry”, a discipline characterized by a mathematical description of social sciences111A similar approach coupled to modern technology constitutes the core of a newborn field, “computational social science” [8], where mathematics is employed to analyze the huge amount of data generated by online social networks.. Later on, the seminal papers of Erdős and Rényi [9, 10], lately extended to combinatorics by Bollobás [11], opened the field of “random graph theory” [12].

Only after the digital revolution, complex networks became part of everybody’s life. Indeed current technology has made the presence of personal computers pervasive and also constantly reduced the cost of backup memories. These two features have produced immense databases, collecting information about a wide range of relationships. Just to name a few we have: the Internet wiring [13, 14, 15], the set of WWW connections [16, 17], e-mail exchanges [18, 19] [20], mobile communication networks [21, 22, 23], online social networks [24, 25, 26, 27], protein-protein interactions [28, 29, 30], food-webs and ecological networks [31, 32, 33], production activities [34, 35, 36, 37, 38, 39], financial exchanges and stock investments [40, 41, 42].

The network representation clearly highlights qualitative universal behaviors, irrespectively from the specific case-studies [43]. In what follows we name some of the features shared by many real-world networks:

- 1.

-

2.

a small-world effect [45]: distances are distributed around a characteristic average value, usually “very small”, (i.e. ) and scaling as the logarithm of the system size;

-

3.

a large clustering [46]: we spot the presence of densely-connected subgraphs in many complex networks. The small-world and the large clustering effects co-exist thanks to presence of the so-called “weak-ties” in the social networks literature, allowing for “long-range” interconnections without affecting the locally large density of links;

-

4.

a distinct centrality structure [47] implying that some nodes appear to have a higher importance than others;

-

5.

a well-defined assortativity structure [48]: the neighbors of each node have a degree that is either positively or negatively correlated to the degree of the node itself (more intuitively, “my” neighbors have a degree that is either very similar or very different from mine). In the case of bipartite networks, a well-defined nestedness structure has been observed, mainly in ecological and economic contexts [49, 50, 51].

The problem of missing information

After an initial activity aimed at determining the structure of real-world networks by measuring standard topological quantities, a more theoretical activity was started, aiming at both defining new quantities and devising proper models to explain observations [45, 44, 52, 53, 54]. Given the complexity that can arise even from a simple mathematical model based upon graphs, researchers have recently focused on the development of a topological theory: loosely speaking, topological quantities are employed to define statistical models, rather than reproduced from microscopic dynamical rules [55, 56, 57, 58, 59].

Unfortunately, when moving to the validation of such models a common problem arises: very often, the data available on the real network are either incomplete or imprecise (or both). This problem is particularly evident in the case of economic and financial networks: in this case, data collection suffers from the problem of partial accounting and the presence of disclosure requirements. In order to illustrate the importance of such an issue, let us think of a bipartite, financial network whose node sets represent investors and the investments they do. Although the knowledge of the whole network structure could help regulators to take immediate countermeasures to stop the propagation of financial distress, this information is seldom available (the knowledge of the whole network of investments would pose immense problems of privacy), thus hindering the possibility of providing a realistic estimate of the extent of the contagion. As confirmed by the analysis of the various papers reported in this review, the incompleteness of network instances seems to be unavoidable [60, 61]: since addressing the problem of estimating the resilience of financial networks cannot be addressed without knowing the structural details of national and cross-countries interbank networks, information theory seems indeed to provide the right framework to tackle this kind of problems.

Finance is not the only domain affected by limitedness of information about nodes interdependencies: biological and ecological systems also exist (e.g., cell metabolic networks and ecological webs) whose interaction network is often only partially accessible due either to experimental limitations or observational constraints222In these cases, one is often more interested in the reconstruction of individual links from partial local information, a problem known as “link prediction” [62, 63]..

Approaching network reconstruction

In order to deal with the problem of missing information, many different approaches have been attempted so far. Some reconstruction procedures are based on a measured (or expected) statistical self-similarity of the network topology [64]. In this case, the observed behavior of a given topological property (e.g., the degree distribution) is supposed to be induced by some non-topological property assigned to nodes (e.g., a node “fitness”[52]) obeying the same behavior.

More often, the fundamental assumption grounding network reconstruction is statistical homogeneity. This means that the structure of the network observed are representative of statistical properties not depending on that specific portion. In the jargon of statistics, supposing that from similar observations we can infer similar regularities is equivalent to requiring that the information available is representative of the whole network structure. This is particularly relevant when only limited information is available, and constitutes the physical reason to be confident that the efforts to define a statistically-grounded network reconstruction algorithm can indeed be successful. By using this “symmetry” it is then possible to provide some likely estimates of the missing quantities of the network under analysis. Clearly, while the homogeneity assumption minimizes the bias introduced by adopting arbitrary assumptions not supported by the available information (and, in principle, untestable), it also limits the accuracy of the reconstruction of real networks showing, instead, strong structural heterogeneity.

Given these premises, entropy maximization provides the unifying concept underlying all the reviewed methods. Entropy maximization is, in fact, an ubiquitous prescription for obtaining the least biased probability distribution consistent with some imposed constraints (i.e., a probability distribution not encoding other information than that represented by the constraints themselves [65, 66]). This principle has not only found hundreds of applications in statistical mechanics, information theory and statistics [67], but it has been also argued to represent an evolutionary drive of out-of-equilibrium systems [68] (e.g., a relationship has been suggested between the dynamics of intelligent systems and entropy maximization [69]).

The outline of this report is the following. In section 2, Information theory as a basis for network reconstruction, we present the tools that can be derived from classical approaches in statistical physics and information theory, mainly Gibbs’ ensembles theory, Shannon’s works on entropy and Jaynes’ interpretation of statistical mechanics. Moving from these theoretical premises, in section 3, Reconstruction methods, we present an overview of the different reconstruction methods, dividing them into a) dense reconstruction methods, b) density-tunable reconstruction methods, c) exact-density methods, d) alternative approaches. In section 4, Testing the network reconstruction, we present in detail a number of indicators and metrics that can be used to test the accuracy of the achieved reconstruction; more specifically, we have distinguished three classes of indicators, of statistical, topological and dynamical nature, respectively aiming at testing the accuracy in reconstructing the microscopic details, the macroscopic topological features and the dynamical properties of a given network. Concerning dynamical indicators, we put particular emphasis on the possibility of estimating the resilience of the system to processes of shocks propagation. In the financial context this is know as systemic risk, i.e., the likelihood that a consistent part of a given financial network may collapse (go bankrupt) as a consequence of a local failure. In section 5, Model selection criteria, we describe some of the existing criteria to compare different models and the corresponding recipes for how to choose the most appropriate one. The report ends with section 6, Conclusions and perspectives, where we describe future possible applications of the reviewed algorithms.

As a general remark, we would like to stress that almost every paper reviewed here has its own nomenclature for the (often similar) quantities of interest. Since we wanted to present the different contributions within a unified framework, our presentation might not reflect the original derivation of the results.

2 Information theory as a basis for network reconstruction

Information theory provides the theoretical basis of our formalism [70]. The concept of information plays a fundamental role in network reconstruction, since reconstructing a network ultimately means making optimal use of the available, partial, information. Otherwise stated, our task is that of inferring as much as possible about the system under analysis from the available data, while limiting the number of unsupported assumptions.

As stated before, real data are very often partial: thus, any data-driven inference procedure is bound to consider an enlarged set of plausible configurations, i.e., all configurations that are compatible with the available information. In the language of statistical mechanics, this set is called ensemble. Enlarging the set of allowable configurations means, in turn, increasing the degree of uncertainty about the actual one; the description, thus, becomes necessarily probabilistic: a probability value must be assigned to each configuration compatible with the known information, that is, to all configurations belonging to the ensemble.

The degree of plausibility of a given configuration can be unambiguously quantified by recalling the concept of surprise. Since a “surprising” event (deemed as highly improbable) is assumed to convey a large amount of information [65]. An operative definition of surprise should encode a (negative) correlation with the probability of realization of the event under consideration. The content of information of a given outcome out of the set of possible outcomes can be thus quantified as

| (1) |

a definition pointing out that the occurrence of an event that is certain (i.e., characterized by ) brings no information and comes with no surprise, whereas, the occurrence of an (almost) impossible event (i.e., characterized by ) conveys an (almost) infinite amount of information and causes an (almost) “infinite” amount of surprise [65]. The average degree of surprise which accompanies the events belonging to the set can be then quantified by averaging over the ensemble itself. Such an operation leads to the basic concept of the Shannon entropy:

| (2) |

Another interpretation of eq. (2) comes from information theory [71, 72]. Given an alphabet of symbols (as a language) to be transmitted across a channel, shorter codes should be assigned to symbols met with larger frequency, while longer codes should be employed for symbols met with smaller frequency (see Appendix A). Looking for the average code length needed to transmit a given message leads to as well.

From an axiomatic point of view, Shannon entropy is the only functional that satisfies a number of properties known as the Shannon-Khinchin axioms [66]:

-

1.

Shannon entropy is a continuous functional of all its arguments: this ensures that small deformations of the probability distribution induce small changes in ;

-

2.

Shannon entropy attains its maximum in correspondence of the uniform distribution over the set of possible configurations;

-

3.

Shannon entropy is invariant under the addition of events with zero probability;

-

4.

For a system composed by two independent subsystems and , whose ensembles of possible configurations and have probability measures and , the entropy is additive: , i.e.the entropy of the whole system is the sum of the entropies of the two subsystems333In [73] this axiom is replaced by the so-called “composition law”.. On the other hand, if the two subsystems are not independent, , with indicating the probability measure for the configurations of the subsystem , conditioned to the realization of subsystem .

In other words, Shannon entropy is a functional of the probability distribution of an arbitrary set of random variables (in our case, the configurations within the aforementioned ensemble ) and quantifies the (un)evenness of the distribution itself [74]. As an example, if no information on the system is available, uncertainty about it is maximal and Shannon entropy prescribes to assign a uniform distribution over . By converse, any statistical information gained on the system reduces the uniform character of the probability distribution, which becomes progressively more peaked in correspondence of the configurations conveying the given information.

2.1 Setting the problem: constraining Shannon entropy

E. T. Jaynes first pointed out the possibility of using Shannon entropy to define a novel inference procedure [73], by extending the recipe proposed by Gibbs in the context of statistical mechanics. Jaynes proposed to carry out a constrained maximization of Shannon entropy, i.e., to maximize the functional

| (3) |

with the quantities that sum up the available knowledge on the system acting as constraints to be satisfied by the probability distribution itself. Maximizing Shannon entropy ensures that our ignorance about the system to be reconstructed is maximized, except for what is known or, equivalently, that the number of unjustified assumptions about the system itself is minimized. Indeed, it can be proven that the probability distribution that maximizes Shannon entropy is maximally non-committal with respect to the unknown information [73] (see Appendix B).

Since constrained Shannon entropy maximization represents a sort of “guessing” process about the unknown information, characterized by the least amount of statistical bias, it can be viewed as an updated version of the Laplace principle of insufficient reason [73]. The latter states that in absence of any information about the system under analysis, there is no reason to prefer any particular configuration which, thus, is equiprobable to any other. This principle is nothing else than a particular case of eq. (3) with no constraints but the normalization condition—which actually leads to the uniform distribution over the ensemble . As already mentioned, Shannon entropy attains its maximum in this situation.

The framework sketched above is general enough to allow physical systems as well as networks to be analyzed. While in the first case the constraints represent physical quantities (e.g., the mean energy of the system), in the second case they represent purely topological quantities as nodes degrees, the network’s reciprocity, and so on. We would also like to stress that the Gibbs-Jaynes approach has been originally defined within the realm of equilibrium statistical mechanics, and this is also the spirit that has guided its application to networks. Generally speaking, however, networks do not satisfy the equilibrium conditions valid for thermodynamic systems. Consequently, in the networks realm the adoption of an entropy-maximization approach for the reconstruction of higher-order statistical properties from lower-order constraints is rather justified by the minimization of arbitrary statistical assumptions on the network structure not supported by the available information.

Let us now explicitly consider as the set of all possible network configurations with vertices. In most cases we consider networks that are both weighted and directed, which implies that the interlinkages characterizing them can be represented by an asymmetric matrix with real entries:

| (4) |

where represents the weight of the link from node to node . Matrix induces a second matrix , known as the adjacency matrix of the network. Formally, the generic element of is equal to 1 if , and 0 otherwise. In other words, the matrix simply indicates the presence/absence of connections between node pairs.

The problem of network reconstruction arises whenever the weights of an empirical network are not directly observable, and instead only aggregate (marginal) information on the network is accessible. More precisely, only the sum of the rows and/or the columns are typically known:

| (5) |

Note that rows and column sums of , namely the out-degree and in-degree of each node are typically unknown.

In the financial context, typically represents a matrix of interbank exposures, also named liability matrix. The entries of this matrix are the loans and borrowings between banks, protected by privacy issues, while marginals are publicly released in balance sheets. then quantifies the total interbank assets of node , and its total interbank liabilities (see section 4.3.1). Another classical example is the World Trade Network (WTN), where these quantities represent the total export and import of countries.

Generally speaking, any algorithm aimed at reconstructing a weighted directed network outputs two matrices, and : while the generic entry of the first matrix describes the probability that any two nodes and are connected, the generic entry of the second matrix provides an estimate of the weight of the corresponding link. We can say that, in certain conditions, the probabilities and weights estimates of the methods considered in the present review are functions of the accessible information and can, in general, be written as and . As a consequence, the entries can be interpreted as Bernoulli variables that are with a certain probability and otherwise.

Since the number of available data in the cases we consider here is ( if only out- and in-strengths are known), the problem of reconstructing an adjacency matrix of real numbers is under-determined. In what follows, we shall review methods that adopt a probabilistic approach to tackle these kinds of problems, making use of tools and concepts developed within the information-theoretic framework introduced in the previous subsection.

2.2 Exponential Random Graphs

Exponential Random Graphs (ERG) [55, 59] occupy a central role in most of network reconstruction algorithms. Indeed, ERG are defined as the ensemble of graphs whose probability is obtained by maximizing of the constrained entropy functional of eq. (3). More specifically, solving the functional differential equation with respect to leads to the following formula:

| (6) |

that describes an exponential distribution (whence the name of the formalism) over the set of all possible network configurations. Notice that the coefficients are nothing else than the Lagrange multipliers in eq. (3), whose values are fixed by the set of equations

| (7) |

, where sets the normalization condition

| (8) |

Using the above relation, we can eliminate and obtain the standard expression of the ERG probability distribution that is analogous to that of the canonical ensemble in statistical physics:

| (9) |

The quantity at the exponent is called graph Hamiltonian and is the partition function, which properly normalizes the probability distribution. It can be easily shown that eq. (6) not only makes the first functional derivative of vanish, but also makes the second derivative negative definite, so that is indeed a maximum of (see Appendix C).

The ERG formalism can be fruitfully used to analyze real-world networks by supposing that a given observed configuration has been drawn from and, as such, can be consistently assigned the probability coefficient . However, we still need a recipe to set the mean values or, equivalently, the Lagrange multipliers , in an optimal way. To this aim, we can invoke the maximum-likelihood principle, prescribing to maximize as a function of , or equivalently the log-likelihood function

| (10) |

Using eqs. (7) and (9), it is possible to show that the set of values satisfying the set of equations are those ensuring that

| (11) |

, namely that the ensemble averages of constraints match their values observed in . [58]. Remarkably, likelihood maximization consistently prescribes that the only information usable to make inference is the one we have access to. Moreover, it is simple to show that the same choice makes the Hessian of negative definite, implying that the position in eq. (11) corresponds to a maximum of the likelihood.

The whole ERG recipe can be thus summarized as joining two optimization principles:

-

1.

entropy maximization, which guarantees that the derived probability distribution encodes information only from the chosen constraints;

-

2.

likelihood maximization, which guarantees that the value of the imposed constraints matches the observed one, without any statistical bias.

In what follows, we shall dwell into the details of various network reconstruction methods. Note however that, generally speaking, the ERG formalism can be also fruitfully used for a second purpose, i.e., analyzing known real-world networks in order to detect the level of randomness affecting their topological structure. Indeed, suppose to have an empirical network whose structure is completely known. We can then ask whether this network is a “typical” configuration of a particular ERG derived from imposing an arbitrary set of network observables . In other words, we can check if the network is “maximally random”—the level of randomness being determined by the chosen constraints, so that the information brought by any other network observable can be reduced to the information encoded in the constraints. We shall briefly discuss this approach in subsection 4.2.3. 444Entropy-maximization can be also used to assign probabilities to (dynamical) pathways. In such a context, the principle is known as maximum-caliber [67]. An application of this principle concerns the so-called origin-destination networks, i.e., graphs defined by an origin node, a destination node and a set of connections linking them, representing the pathways along which information flows [75].

3 Reconstruction methods

The reconstruction methods reviewed in the present work can be classified according to the link density of the output configurations. Indeed, the reconstructed networks can be fully connected (or, at least, very dense), with a tunable density, or exactly reproducing the observed number of links.

3.1 Dense reconstruction methods

3.1.1 The MaxEnt algorithm

The MaxEnt algorithm [76, 77] represents the simplest and, probably, the best known method for reconstructing networks. It prescribes to maximize the functional

| (12) |

under the constraints represented by eqs. (5). Equation (12) defines a particular kind of entropy in which the random variables are the matrix entries themselves. However, the absence of a proper normalization condition prevents eq. (12) from returning a genuine probability distribution. The solution to the aforementioned constrained maximization problem is, in fact,

| (13) |

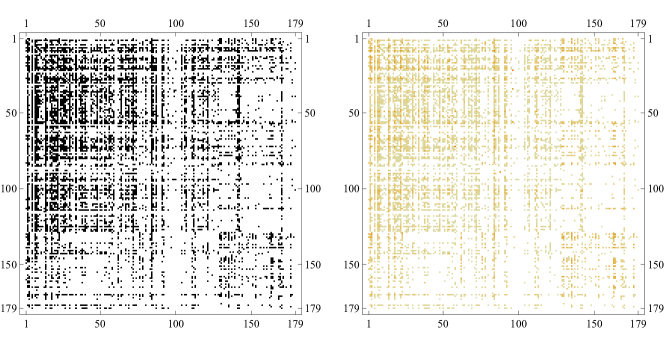

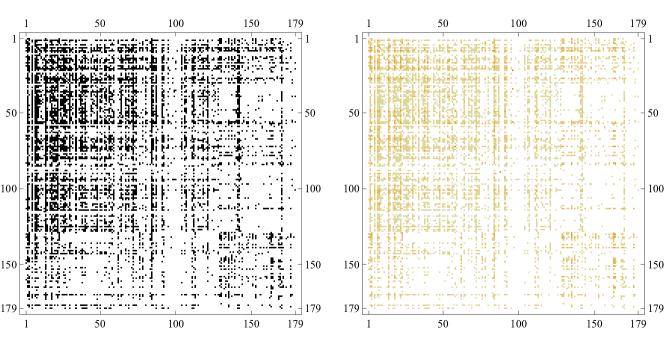

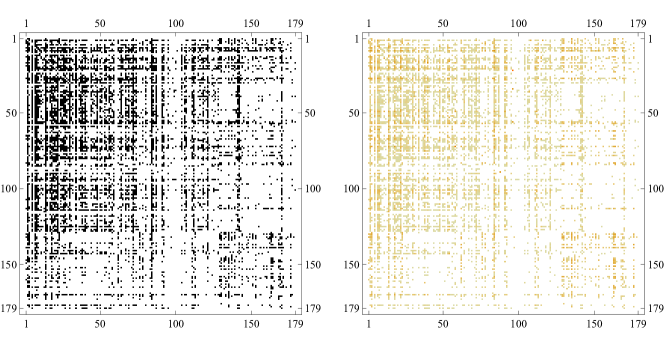

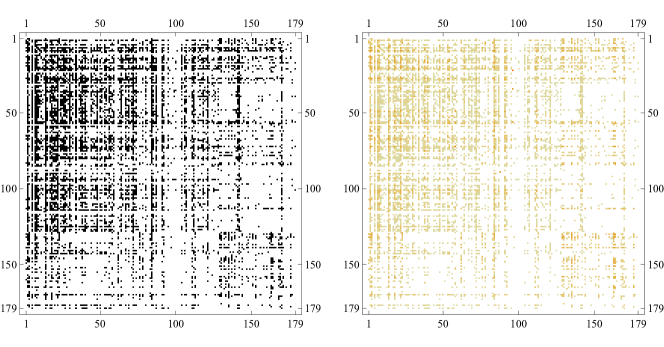

where is the total weight of the observed network . It is easy to verify that the constraints are satisfied, since and . The summation index, however, has to run over all values , including the ones corresponding to the diagonal entries. Note that eq. (13) implies that, unless either or for some nodes, no entries can be zero and the resulting matrix is fully connected (see fig. 1 where this algorithm has been applied to a snapshot of the Italian electronic market for interbank deposits eMID [40]). This feature represents the main limitation of the method, for a twofold reason. The first one is that real-world networks are often very sparse, and thus MaxEnt cannot possibly reproduce their topology. The second one is that systemic risk is underestimated in dense networks [78, 79]. Yet, the MaxEnt prescription provides quite accurate estimates whenever only the magnitude of weights are considered [80, 81]. The latter is the reason why MaxEnt is widely used in economics—the simple gravity model (without distance) has the same functional form of the MaxEnt estimate [82], and in finance—where it takes the same form of the capital asset pricing model (CAPM) [83, 84]. As a final remark, we stress that the MaxEnt algorithm generates a unique reconstructed configuration, thus being classifiable as a deterministic algorithm.

3.1.2 Overcoming the problem of missing connections: the IPF algorithm

A first step in the description of networks which are not fully connected (i.e., characterized by some null entries of the corresponding adjacency matrix) is given by the iterative proportional fitting (IPF) procedure. It is a simple recipe to obtain a matrix that

Let us call the matrix satisfying these conditions. In the case of null diagonal entries, the method formally defines as:

| (14) |

i.e., the matrix that minimizes the Kullback-Leibler (KL) divergence [85] between a generic non-negative with null diagonal entries and . The KL divergence is an asymmetric measure of “distance” between any two probability distributions and quantifies the amount of information lost when is approximated by .

A numerical recipe guaranteeing that the three requests above are met is provided by the iterative process whose basic steps at the -th and -th iterations are

| (15) |

so that , and represents the matrix used to initialize the algorithm. In a nutshell, the IPF algorithm iteratively distributes the known matrix marginals across the non-zero entries of the initial matrix. As long as this initial matrix is irreducible (meaning that it cannot be permuted into a block upper triangular matrix, or equivalently that the network is represents is strongly connected), eqs. (15) always yield a unique matrix that satisfies the marginals [86]. As a first consistency check, let us consider the case in which the initial matrix is defined by . Without restricting the sum to the non-diagonal terms, we would obtain . As a second check, let us consider the case in which the initial matrix is taken to be , a position that is equivalent to immediately maximizing the functional in eq. (13). We obtain and , hence the MaxEnt estimation is correctly recovered after just two iterations.

3.1.3 The Directed Weighted Configuration Model

Like MaxEnt, the IPF has the major drawback of generating a single deterministic configuration, so that it is difficult to statistically evaluate the accuracy of the provided reconstruction. A more rigorous statistical method to evaluate the probability that nodes and are connected by a link is the ERG-based approach known as Directed Weighted Configuration Model (DWCM) [58]. The method constrains the out-strength and in-strength (defined as in eqs. (5)) of each node of the network, and the Hamiltonian takes the form

| (16) |

Substituting the definitions of and in eq. (16) leads to a probability distribution which factorizes into the product of pair-specific distributions

| (17) |

In the simple case of weights taking only non-negative integer values, the probability distribution governing the behavior of the random variable is geometric [58]:

| (18) |

where and . From eq. (18), we immediately find that

| (19) |

and, by definition, the probability that a directed link from node to is present is , which in view of eq. (18) becomes:

| (20) |

Finally, the Lagrange multipliers are found by solving the corresponding equations deriving from the likelihood-maximization principle: , and .

The DWCM falls into the category of dense reconstruction methods because the observed marginals are usually so large that the induced link probability between any two nodes and becomes very close to 1. However, differently from the MaxEnt and the IPF, the DWCM algorithm produces a whole ensemble of networks, by treating link as independent variables and drawing the corresponding weights from the geometric distributions described by eq. (19).

3.1.4 Combining MaxEnt and ERG frameworks

An approach combining the MaxEnt and the ERG frameworks has been recently developed, under the name of Maximum Entropy CAPM (MECAPM) [84]. The idea is to maximize the Shannon entropy constraining not the expected values of the matrix marginals, but rather the expected value of each link weight. Similarly to the case of the DWCM, this leads to

| (21) |

where is the Lagrange multiplier controlling for the weight of the link from to . This framework can be used for network reconstruction provided that the imposed expected weights depend only on the matrix marginals, which is the only information available on the system. This is naturally achieved by the MaxEnt recipe, hence:

| (22) |

a position allowing for the Lagrange multipliers to be readily estimated as the link probabilities:

| (23) |

This algorithm falls into the category of dense reconstruction methods, since the MaxEnt weights are usually sufficiently large to induce . And as the DWCM, the MECAPM algorithm produces a whole ensemble of networks.

3.2 Density-tunable reconstruction methods

The MaxEnt, the DWCM and the MECAPM methods suffer from the same limitation: the predicted configurations are often too dense to faithfully describe real-world networks. Therefore other reconstruction methods have been proposed. The rationale driving the algorithms described below is to produce configurations that are sparser than the ones obtained through the aforementioned algorithms.

3.2.1 The IPF algorithm: generic formulation

As we have seen, the IPF algorithm basically acts by distributing the known marginals across the positive entries of the matrix. Hence, it requires that the position of the null entries is known in advance. This limitation is the reason why the method is often used in combination with other algorithms that estimate the positions of the zeros. Once these positions are known, the IPF algorithm adjusts the positive entries (typically initialized as MaxEnt estimates) to match the constraints.

Indeed, the freedom to choose the topological details turns out to be fundamental whenever an algorithm able to generate realistic configurations is needed. The general formulation of the IPF algorithm give us this freedom. Indeed, in order to account for either known or guessed subsets of entries (which do not necessarily need to be zero), it is enough to i) subtract them from the known marginals and , and ii) modify eqs. (14) and (15) by using these rescaled marginals and explicitly excluding known entries from the sums at the denominator [86]. In the most general case, the IPF estimation can be written as the infinite product

| (24) |

where and .555The IPF algorithm is also known with the name of RAS algorithm, because the form of the solution devised in [87] is written as the product of three matrices whose symbols are , , . More specifically, and , with being the initial adjacency matrix and , being the two diagonal matrices , being the two diagonal matrices and .

3.2.2 The Drehmann & Tarashev approach

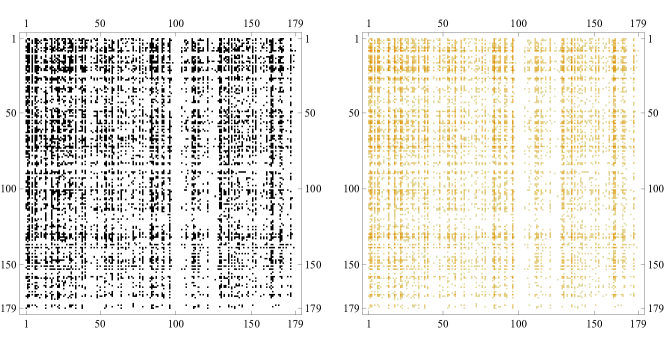

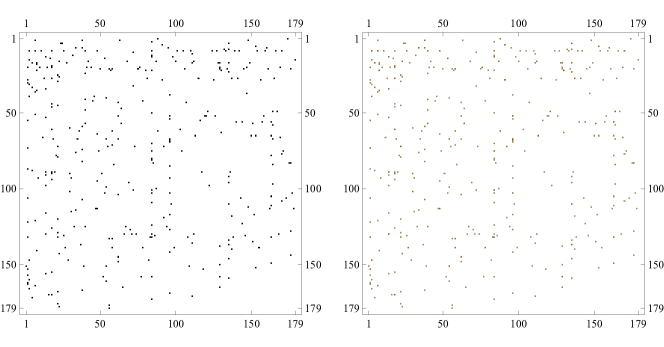

In the absence of a clear recipe to estimate the network density, a number of algorithms exploring the whole range of possible density values have been proposed. Drehmann & Tarashev devise a simple approach [88] to perturb the MaxEnt matrix and obtain sparse network, following three steps:

-

1.

choosing a random set of off-diagonal entries to be zero, thus manually setting a desired link density;

-

2.

treating the remaining non-zero entries as random variables, uniformly distributed between zero and twice their MaxEnt estimated value:

(25) (so that the expected value of weights under this distribution coincides with the MaxEnt estimates );

-

3.

running the IPF algorithm to correctly restore the value of the marginals.

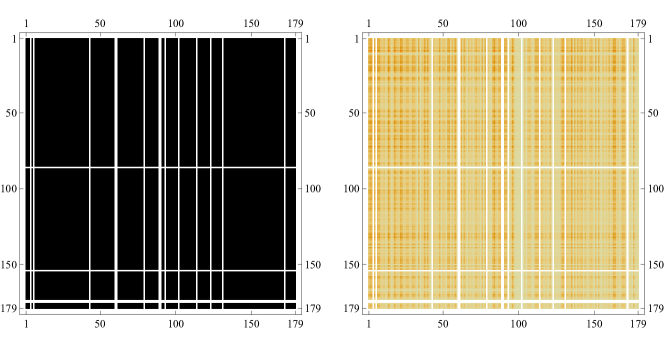

The value of the network density can be tuned to generate arbitrarily sparse configurations. Yet a drawback of the method lies in the completely random nature of the obtained topological structure(s) (see fig. 2).

3.2.3 The Mastromatteo, Zarinelli & Marsili approach

Another approach to generate reconstructed networks with an arbitrary density of links has been formulated in [79]. This method consists in sampling uniformly the set of network configurations that are compatible with the constraints defined by eqs. (5) and have a given value of the density. Two additional assumptions are made on the matrix : i) the entries larger than a certain threshold (supposed to be at most of order ) are considered to be known—an hypothesis that in the case of financial networks meets the recent disclosure policies adopted for some markets [89]); ii) the unknown entries are rescaled by the threshold itself, and thus become bounded in the range . Known entries can be completely omitted in the description of the method, and the focus can be kept only on the ensemble generated by the variability of the unknown entries.

The fundamental question the authors tackle is the following: given an arbitrary value of , how many matrices exist that satisfy eqs. (5) and whose density matches the chosen one? Clearly, while the maximum density value allowing for (at least) one configuration to exist is (the MaxEnt algorithm always satisfies eqs. (5)), finding for a given value of the constraints is non-trivial. The measure introduced in [79] to fairly sample the space of binary adjacency matrices that are compatible with a given is , where is a normalization constant, is the number of links in and the parameter sets the average density

| (26) |

to a desired value (notice that the sum runs over the compatible configurations only).

However, when it is hard to analytically evaluate the sampling probability distribution . Consequently, an approximated probability distribution is introduced:

| (27) |

where . The parameter plays the role of the fugacity in statistical physics and fixes the mean value of the density over the whole set of adjacency matrices. Since the unknown entries of range between 0 and 1, the number of out-going (in-coming) links of each node in any compatible configuration with the chosen density value is always larger than its out-strength (in-strength): this brings to the condition . Conversely, the probability of any infeasible configuration (i.e., with ) to appear is suppressed by a coefficient which vanishes as . Since an analytical treatment of the distribution in eq. (27) is also infeasible, the authors implement a message-passing algorithm [79] to calculate the marginal link probabilities, which are then independently sampled to build a candidate binary network. And once the binary topology is obtained, weights are inferred via the IPF algorithm.

As the authors explicitly notice [79], being able to tune the network density implies being able to consider a whole range of structures characterized by (potentially) different degrees of robustness to, e.g., financial shocks. However, as a result of the authors’ “compatibility analysis”, no allowable configurations can be found below a certain value of the network density. And while the MaxEnt method produces configurations believed to maximize the network robustness, sparser configurations may, on the other hand, provide lower bounds to it.

3.2.4 The Moussa & Cont approach

Another algorithm that combines the MaxEnt and the ERG frameworks is the one presented in [90], where the authors propose two different versions of their method—both similar to the entropy-based approaches described in the previous subsections. The major difference lies in the amount of available information required, which is now substantially larger: namely, the out- and in-degree distributions of the network, as well as the out- and in-strength distributions, all of them supposedly well-described by power-laws (whose parameters are tuned to reproduce stylized facts of financial networks). In a nutshell, the method generates a whole ensemble of different binary network configurations (i.e., the prior configurations), whose topological structure is then “adjusted” a posteriori to match the constraints represented by eqs. (5).

The “exact” approach

The first version of the method is designed to meet the constraints exactly in each configuration of the ensemble. Prior configurations are characterized by the same degree distributions but different topological structures (the algorithm used to generate the ensemble is the generalization of the preferential attachment algorithm to directed networks [91]). Once a binary configuration is generated, the IPF algorithm is used to assign weights to the realized links. The problem can thus be formally stated as that of determining, for each binary configuration in the ensemble, the set of weights such that

| (28) |

where the sum runs over the set of non-zero entries of any configuration in the ensemble (for all null entries we trivially have ). Using a normalization condition that the entries to be estimated satisfy , the solution to the optimization problem above can be formally written as

| (29) |

where and are, respectively, the Lagrange multipliers related to the constraints on nodes out- and in-strengths, found by solving and .

The “average” approach

However, as the authors explicitly notice, dealing with too sparse matrices may prevent the IPF algorithm to converge, because a solution of the IPF algorithm exists and is unique if and only if the matrix is irreducible (i.e., the network is strongly connected) [86]. Moreover, there is no guarantee that the numerical values of weights assigned by IPF are distributed according to some empirical observations (e.g., following a power law) [90].

For this reason, a second version of the algorithm is proposed. The ensemble of configurations is now composed by weighted networks for which both degrees and weights distributions are specified. The probability distribution on this set of configurations, however, is not uniform: each configuration is, in fact, characterized by a statistical weight such that the constraints represented by eqs. (5) are satisfied on average. The ensemble probability distribution is derived by minimizing its KL divergence from the uniform distribution

| (30) |

under the constraints and (where and are the out- and in-strengths for the configuration in the ensemble). Similar calculations to those used for eq. (29) lead to the analytical expression of the probability coefficients

| (31) |

with . As usual, the numerical value of the Lagrange multipliers can be found by solving the constraints equations and . The estimation of any quantity of interest is then carried out by computing the ensemble average of the quantity itself.

3.3 Exact density methods

The reconstruction algorithms described in the previous sections are attempts to circumvent the lack of information on the actual network density and, most importantly, to avoid predicting too dense configurations. The methods described below, instead, explicitly require the knowledge of the observed network density or, at least, the link density for a subset of nodes. This is because, as shown in [92, 81, 93], adding this piece of information can dramatically increases the performance of a reconstruction algorithm. We now introduce a series of algorithms of this kind, all strictly following the ERG formalism introduced in Section 2.2.

3.3.1 The density-corrected DWCM

The first example of ERG-based reconstruction method we have met in subsection 3.1.3 is the DWCM, obtained by constraining the out-strength and in-strength sequences. As we have seen, the DWCM-induced ensemble is basically characterized by fully-connected configurations, with a density of links which cannot be tuned independently from the distribution of weights (see eq. (20). So the outcome of the DWCM is very close to that of the MaxEnt method, and indeed the DWCM can be seen a sort of stochastic generalization of MaxEnt. In order to overcome this limitation, the authors of [81] propose a density-corrected version of the DWCM, defined by constraining the total number of links beside the out-strength and in-strength sequences:

| (32) |

In analogy with the DWCM, also in this case links turn out to be statistically independent. When weights can assume only positive integer values, the weight probability distribution can be written as

| (33) |

where

| (34) |

in which and are defined as in the DWCM and (thus, for we recover the standard DWCM). Notice that eq. (33) defines a composition of a single Bernoulli trial, controlling for the existence of a link between any two nodes and , and a geometric distribution for its weight, whose mean value reads

| (35) |

Finally the Lagrange multipliers are fixed as in the DWCM, while is obtained by .

This method ideally refines the DWCM by explicitly adding to the recipe a piece of topological information. By doing so, the occurrence probability of a network in the ensemble still depends on the marginals, but also on the imposed number of links, hence very dense configurations become highly improbable.

3.3.2 The Directed Enhanced Configuration Model

Beyond the total number of links, also the degree heterogeneity can be explicitly taken into account. The Directed Enhanced Configuration Model (DECM) [94] is defined by:

| (36) |

and encompasses many ERG-based models as special cases (for instance, the degree-corrected DWCM is obtained when , ). The DECM probability distribution can be written as:

| (37) |

with

| (38) |

and

| (39) |

(where , , and ). Notice that from eq. (38) it is simple to evaluate the average value of the generic link weight as

| (40) |

Lagrange multipliers are as usual found by solving the corresponding equations derived from the likelihood-maximization principle: , , , , .

As for the density-corrected DWCM, eq. (38) can be interpreted as a combination of a Bernoulli trial, with probability , and a drawing from a geometric distribution, with parameter ; in this case, however, the link probability depends also on the degrees of nodes and .

The DECM method has a simple interpretation when a specific economic system is considered, namely the World Trade Network (WTN). In economic terms, the two aforementioned processes respectively describe the tendency of a generic country either to establish a new export towards country (with probability ) or to reinforce an existing one (with probability , by rising the exchanged amount of goods of, so to say, “one unit” of trade). In order to understand which process is more probable, we can study the behavior of the ratio . Whenever this quantity is greater than 1, country would probably establish a new export relation towards , and at the same time experience a certain resistance to reinforce it; otherwise, country would experience a certain resistance to start exporting to , but once such relation were established it would be characterized by a relatively low “friction”, inducing the involved partners to strengthen it [95]. Note that the case implies reducing eq. (38) to eq. (18) of the DWCM. In other words, the DWCM does not discriminate between the first link and the subsequent ones, reducing to a simple geometric distribution. As shown in [94], the DWCM fails in reproducing the observed properties of the WTN precisely because it cannot give the right importance to the very first link, which is treated as a simple unit of weight. This observation hints at the importance of the information encoded into nodes degrees, to be considered as a fundamental ingredient (together with nodes strengths) for a faithful reconstruction of real-world networks.

3.3.3 Simplifying the DECM: a two-step model

A simplified version of the DECM can be derived by noticing that the estimation of the topological structure of a network can be, in some circumstances, disentangled from the estimation of its weighted structure. This observation rests upon the evidence that the link probabilities of the DECM show a large (positive) correlation with the analogous probabilities of a much simpler ERG model, namely the Directed Binary Configuration Model (DBCM) obtained by constraining only the out- and in-degree sequences [95]. The DBCM is thus defined by the Hamiltonian

| (41) |

which leads to the connection probability

| (42) |

with and , determined via the usual equations and , .

| (43) |

which defines a “two-step” version of the DECM, and whose Lagrange multipliers are found by imposing, , and first and then and .

3.3.4 Fitness-induced Exponential Random Graphs

Despite the previous findings, we note that it is impossible to use either the DECM or its two-step version when the degrees of nodes are not known, which is unfortunately a rather common situation. Nevertheless, these cases can be treated by resorting to the fitness ansatz, which states that the link probability between any two nodes depends on non-topological features of the involved nodes, typical of the system under analysis. More precisely, it is assumed that the “activity” of each node in the network is summed up by an “intrinsic” quantity, called fitness[52], which is directly related to the Lagrange multiplier controlling the degree of that node through a monotone functional relation. Note that such relation between fitness values and degrees lies at the basis of the the so-called good-gets-richer mechanism, according to which “better” nodes (those characterized by a higher fitness value) have more chances to “attract” connections [52].

For instance, in the case of the (undirected) WTN, where nodes represent countries and links represent trade relationships between them, a strong linear correlation can be observed between the Lagrange multipliers of nodes’ degrees and the Gross Domestic Product (GDP) values of the respective countries: [96, 57]. Consequently, the link probability between nodes and can be rewritten as

| (44) |

where UBCM stands for Undirected Binary Configuration Model. Similar fitness ansatzs have been successfully tested for financial networks, such as interbank markets [97, 98, 92] and shareholding networks [99, 100],

The validity of the fitness ansatz has profound implications on the kind of information that is necessary to have in order to accurately reconstruct a network, but in general leads to face the problem of finding node observables that are correlated with degrees. Remarkably, strengths often work well as fitnesses [101], a “stylized fact” implying that the DBCM Lagrange multipliers can be expressed as and . As the many empirical analyses of economic and financial systems mentioned above have pointed out, the functional form and with exponent is often accurate enough for all practical purposes.

Estimating the degrees

The above assumption of linear proportionality allows to estimate the unknown degrees in a straightforward way. Indeed, connection probabilities or the fitness-induced DBCM assume the form

| (45) |

so that the only variable left is the proportionality constant .666Note that the MECAPM connection probabilities defined in eq. (23) are recovered here by the particular choice . The latter can be simply estimated provided that the total number of links of the empirical network is known. Imposing in fact means solving only one equation

| (46) |

which has a single solution [98, 92]. Once is found, the degrees of any node in the network can be estimated as

| (47) |

An estimate of can be obtained also using the information on the connectivity of a subset of nodes, for instance the total number of links internal to , or the degrees of all nodes belonging to [102, 80]. In both cases, in fact, the likelihood-maximization principle leads to an equation similar-in-spirit to eq. (46). In the first case, we have

| (48) |

while in the second case it is

| (49) |

As shown in [103], the way a specific subset of nodes is selected does matter. Whenever a faithful estimation of the network density is needed, nodes must be sampled according to a random selection scheme [80], any other procedure being biased towards larger or smaller density values.

3.3.5 Combining fitness-induced DBCM and IPF

An reconstruction method combining the fitness-induced ERG formalism and the IPF recipe is proposed in [104]. Here, the authors assume to know only the out- and in-strengths and the total number of links . The algorithm then consists of two steps:

- 1.

-

2.

the weights are placed on each generated binary configuration according to the IPF algorithm, and hence the constraints of eqs. (5) are always met exactly.

3.3.6 Combining fitness-induced DBCM and DECM

A more rigorous way to assign weights to the fitness-induced ERG formalism consists in solving “bootstrapped” version of the DECM [92]. More precisely, the system of equations to be solved to find the Lagrange multipliers of the DECM becomes

| (50) |

where is defined in eq. (39) and and are the fitness-induced DBCM estimates defined by eqs. (47). The name bootstrapped DECM comes from the double role played by node out- and in-strengths, which are first used to estimate the degrees, and then imposed as complementary constraints.

3.3.7 The degree-corrected gravity model

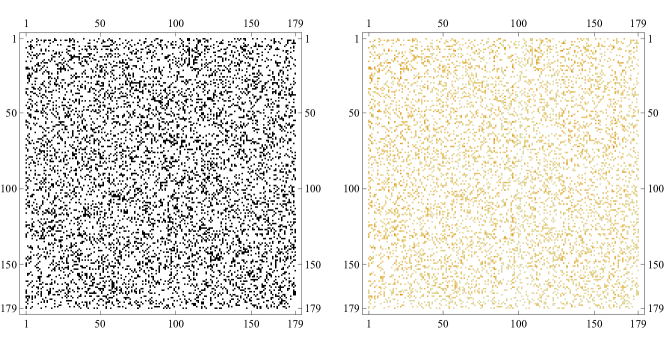

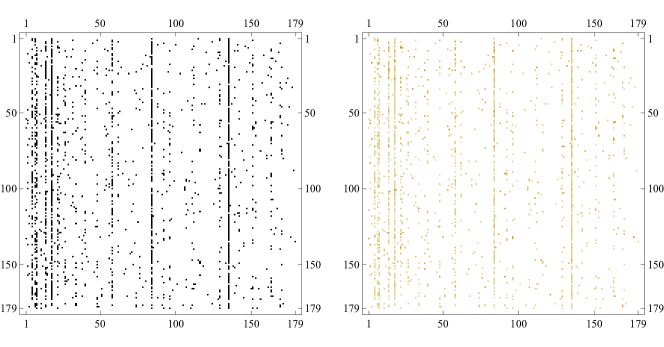

Although the DECM (both in its original and “bootstrapped” versions) represents a very accurate reconstruction method [94, 92], its numerical resolution can represent a computationally-demanding task777It should, however, be noticed that the estimation procedure leading to eqs. (47) has a regularizing effect on the values of degrees, which become smooth monotonic functions of the strengths [98]. This, in turn, may lead to a smaller computational effort to solve eqs. (50).. Building upon the MaxEnt recipe, economics provides the main inspiration for a simpler alternative. Indeed, although the MaxEnt method performs poorly in reproducing the topological structure of many real-world networks, the observed weights are nicely reproduced by eq. (13) [80, 81]. A straightforward way to both retain the explanatory power of the gravity model and avoid ending up with a complete network is provided by the heuristic recipe of the “degree-corrected gravity model” (dcGM) [98]:

| (51) |

This equation “corrects” the MaxEnt recipe by placing the weight only with probability (i.e., conditional to the existence of the link), and rescaled in order to have . In this way, both the network marginals and the link density are correctly reproduced on average (see fig. 3). However, as for the original MaxEnt, this happens only if non-zero diagonal entries are considered as well. Otherwise, by restricting the sums over , the expected values of the strengths obtained from the dcGM would require an extra-term to reproduce the observed marginals: , we would get and , and the missing term would be precisely the expected diagonal weight .

The authors in [80] devise a procedure, inspired by the IPF algorithm, to redistribute the diagonal terms across the non-diagonal entries of the network. Precisely, the correction term to be added to the second line of eq. (51) at the -th iteration of the IPF-like algorithm is defined as

| (52) |

and where the algorithm is initialized at . Once the asymptotic corrections are determined, the heuristic recipe of eq. (51) is replaced by

| (53) |

For all practical purposes, a small number of iterations is often enough to achieve a satisfactory degree of accuracy. Here we explicitly report the functional form of the first three iterations:

| (54) | |||||

A bipartite degree-corrected gravity model

The degree-corrected gravity model can be straightforwardly extended to the case of bipartite (undirected) networks [100]. It is in fact enough to adapt eq. (46) and eq. (51) to the new problem setup. In particular, the equation to determine the unknown coefficient relating the known and the expected total number of links is

| (55) |

with and denoting the cardinality of the two layers of the network, and and indicating the known strength sequences of nodes belonging to the first and second layer, respectively. Notably, correction terms as the ones defined by eqs. (3.3.7) are no longer needed, since diagonal terms are now absent by definition.

3.3.8 Reconciling ERG and gravity models

Remarkably, the ERG framework allows the “economic” information defining gravity models to be translated into opportunely-defined fitnesses. Equation (44) provides a clear example. Another example is provided by the following definition

| (56) |

where is an increasing function of the geographic distance between countries and . The simplest functional form comes from considering the Hamiltonian

| (57) |

with . The latter term quantifies to what extent the topological structure of the network fills the geometric space in which the network itself is embedded [105]. As usual, the unknown parameters must be estimated by solving the equations and . In a sense, eq. (56) defines the closest network-based model to traditional gravity models.

The main difference between the approach proposed here and the traditional economic one becomes evident upon sketching the derivation of the so-called zero-inflated gravity models (ZIGM) [106]. In order to prevent this model from predicting a fully-connected network (the same limitation of the MaxEnt recipe), a probability coefficient reading

| (58) |

is assumed to control for the presence of a link between any two nodes and . The vector of unknowns is estimated by considering the elements of the adjacency matrix to be the dependent variables, and the quantities usually employed to fit a gravity model (as the countries GDP, their geographic distances, etc.—i.e., a whole vector of quantities for each pair of nodes) to play the role of explanatory variables. Both are then used to define the likelihood function for the actual network configuration , which is as usual maximized with respect to . Once a matrix of probability coefficients is obtained, only the nodes pairs satisfying the condition (where is the known density of links) are actually linked [106].

Zero-inflated gravity models and network-based gravity models differ in the amount of information needed to be fully specified. While the former require the whole adjacency matrix of a given (economic) network to be fully specified, the latter only require the knowledge of global (marginal) information. Remarkably, despite the much smaller amount of information needed, network-based gravity models perform much better than zero-inflated gravity models [106].

3.3.9 A remark on the ensemble methods

One of the reasons of the attractiveness of the “ensemble methods” lies in the possibility they offer to generate different topological structures that satisfy the same (weighted) constraints. This feature can be used to disentangle the impact of marginals such as the balance sheets of a financial system and of network structural details on the outcome of a dynamical process like the spreading of financial distress [93].

In order to generate realistic scenarios, however, some kind of topological information must be accessible. In the optimal case, the whole degree sequence of a real network would be available (and, thus, used as additional constrain beside the weighted marginals, via the DECM or its two-step version). Otherwise, if a more aggregate knowledge on the system is available (like the total number of links, or the degrees of a particular subset of nodes), an additional assumption is needed to make the best use out of such information. From the many attempts done so far, it seems that a preliminary estimation of the degree sequence (as in the bootstrapped DECM scheme) enhances the performance of a given reconstruction method, an evidence that explains the superiority of the algorithm in [98] with respect to, e.g., the algorithm in [84]—although both are defined by exactly the same information [81]. From a quantitative point of view, providing a realistic estimate of the degrees of nodes from aggregate information implies having a good fitness ansatz and a realistic estimate of the whole network density. The latter requirements ultimately means having an estimate for the parameter to be used in eq. (45).

3.4 Shannon-like approaches to reconstruction

The reconstruction algorithms presented in the previous subsections build on the constrained maximization of Shannon entropy, or closely-related functionals like the KL divergence. Shannon entropy is however only one out of many possible functionals that can be taken to extremes under the constraints representing the accessible information.

3.4.1 Spectral entropy

Among Shannon-like functionals, entropic measures exist that are inspired by quantum physics. Spectral entropy, also known as Von Neumann entropy, deserves a special mention [107]. It is defined as

| (59) |

i.e., as the Shannon entropy of a probability distribution induced by the eigenvalues of the matrix . In quantum physics, the density matrix describes a system that can be found in one of a set of pure states with different probabilities (precisely defined by the eigenvalues of ): in order to employ this concept in network theory, the density matrix has to be re-expressed in terms of network quantities. A network-based version of the density matrix satisfying the properties of positive semi-definiteness and trace unitarity has been defined as [108]888Other proposals like do not satisfy the (sub)additivity property [108].:

| (60) |

where is the Laplacian matrix ( is a diagonal matrix of nodes degrees) with elements and .

This approach ultimately boils down to the calculation of the divergence between the spectral density of an operator associated with the empirical graph and that of the corresponding operator associated with a graph model [108]. In principle this allows to optimize the parameters of the model using a sort of quantum analogue of the method described in section 2.2.

3.4.2 The Cressie-Read family of power divergences

A whole family of functionals to be extremized to reconstruct partially known networks, generalizing the usual Shannon entropy or Kullback-Leibler divergence (see subsection 3.1.2), is represented by the so-called Cressie-Read power divergences. The latter can be compactly written as

| (61) |

with the real parameter indexing the members of the family. Equation (61) generalizes the KL divergence and provides an alternative measure of “distance” between any two probability distributions and . Notice that even if is not a proper metric distance for all values of , the properties it satisfies are nonetheless useful for quantifying the extent to which any two distributions differ [109]. More specifically,

-

1.

is a continuous function of all its arguments , ;

-

2.

, with equality if and only if ;

-

3.

is invariant under the addition of events with zero probability;

-

4.

is log-additive999The log-additivity property reads with and indicating the tensor product of the two involved probability distributions [110].;

-

5.

the functionals indexed by values of the parameter satisfy the triangle inequality;

-

6.

the only functional representing a proper metric distance (related to the Matusita distance) is the one characterized by .

Since is often intended as summarizing the prior information about the system, the prescription to search for the probability distribution which is maximally non-committal with respect to the missing information can be translated into the request of minimizing the divergence from to . In the case constraints are present, this (first) optimization step leads to recover an expression for which depends on a vector of unknown Lagrange multipliers:

| (62) |

the second step of the whole procedure prescribes to substitute the recovered expression of into itself and optimize with respect to the unknown parameters [109].

Equation (62) generalizes the two principles lying at the basis of the ERG formalism introduced in the previous sections. As varies, the functional describing the divergence between and varies as well. Two noteworthy examples are retrieved by solving the following limits

| (63) | |||||

| (64) |

i.e., the KL divergence between and and between and . Whenever the maximally uninformative prior is adopted, , the well-known expressions

| (65) | |||||

| (66) |

are recovered, respectively defining (up to a sign) the Shannon entropy functional and the likelihood functional [109]. Notice that, for , minimizing consistently translates into maximizing Shannon entropy, thus retrieving the procedure described previously.

In order to use the framework described above for reconstruction purposes, the most general problem of inferring the entries of a rectangular matrix by using the information provided by marginals and must be restated in probabilistic terms. As illustrated in table 1, upon introducing the variables , and further dividing all entries by (thus inducing the definitions and ), providing a numerical estimate of the table entries translates into estimating the entries of the matrix appearing within the set of linear equations

| (67) |

Indeed the entries of can be formally interpreted as probability coefficients, defined as fractions of marginals. This position, in turn, allows a problem formally analogous to the one stated in eq. 62 to be defined as

| (68) |

and a solution of the form to be found. Notice that choosing and a maximally uninformative prior reduces to the usual exponential form coming from the minimization of the KL divergence101010This solution is formally equivalent to the MaxEnt one. However, since this approach is typically used to infer election percentages or estimate the purchases of a basket of commodities (i.e., to reconstruct tables where zero entries are practically never observed), the evidence that non-zero marginals cannot induce zero entries does not constitute a problem [75].

| (69) |

Other choices, instead, lead to coefficients described by different functional forms. As an example, adopting the functional induced by the choice leads to the expression

| (70) |

In general, for an arbitrary choice of the exponent , the functional form of the entries of induced by the functional differs substantially from the “usual” exponential one shown in eq. (69). This, in turn, induces a reconstruction procedure whose performance is potentially very different from that of the KL-based approach.

3.4.3 Other entropic families

Just like the Cressie-Read functionals provide a generalization of the Kullback-Leibler divergence, generalizations of the Shannon entropy are provided by Renyi entropies [112] and Tsallis entropies [113]. These entropies depend on a free parameter and include Shannon entropy as a limiting case. More specifically, Renyi entropies are defined as

| (71) |

(with being a non-negative parameter, different from 1) and satisfy the additivity property111111The additivity property reads with indicating the tensor product of the two involved probability distributions..

Tsallis entropies can be axiomatically defined upon generalizing the fourth Shannon-Khinchin axiom (see section 2). While this axiom unambiguously identifies Shannon entropy, substituting it with the requirement that leads to the only functional that satisfies such a new set of axioms121212The parameter quantifies the degree of non-extensivity of such a functional.:

| (72) |

Remarkably, can be employed to define a non-extensive version of the ERG formalism, whose derivation proceeds along similar lines. For example, imposing only the normalization condition leads to the functional which is maximized by the uniform distribution . Imposing less trivial constraints, however, has not been attempted yet: as a consequence, a thorough comparison between the goodness of the reconstruction performances induced by extensive and non-extensive entropies is still missing.

3.5 Beyond Shannon entropy: alternative approaches to reconstruction

After having revised the existing Shannon-based and Shannon-like approaches to reconstruction, we now review algorithms that are not based on the maximization of Shannon-inspired functionals.

3.5.1 The “copula” approach

The first “alternative” approach to entropy-based reconstruction is, actually, the closest one to traditional MaxEnt. The “copula” method, in fact, adopts the same philosophy and uses the entries of a given matrix to define the support of a probability distribution to be estimated; at the same time, however, it provides a more general solution to the problem.

The MaxEnt prescription represents the simplest method for estimating a bivariate probability distribution , given the two marginal distributions and . Indeed, maximizing the Shannon entropy

| (73) |

under the constraints represented by normalization and the two marginal distributions and leads precisely to the MaxEnt-like estimation

| (74) |

The recipe above, however, can be generalized by introducing the so-called copula functions. The rationale for employing copulas is provided by Sklar’s theorem, which states that every multivariate cumulative distribution function (CDF) can be expressed in terms of its marginal CDFs131313Sklar’s theorem requires the marginals to be continuous. Whenever discrete datasets are considered, the results described here can be thought as being applied to the kernel density estimations of the corresponding (discrete) CDFs. (say, , , etc.) and a copula function which, as the name suggests, “couples” them:

| (75) |

In our case, the marginal CDFs are those of the constraints (defined by eqs. (5)) to be estimated from data. The choice of the particular copula function, on the other hand, is completely arbitrary141414Notably, a maximum-entropy recipe for estimating copulas has been recently proposed [114].. The authors in [115] use the Gumbel copula, defined as

| (76) |

where the only parameter quantifies the dependence between the marginals. Remarkably, the parameter estimation can be carried out by maximizing the likelihood-like function

| (77) |

with respect to . Once the model parameter has been estimated, a matrix whose entries are (interpreted as) probability coefficients is obtained. Finally, the IPF method is employed to readjust the sums along rows and columns and recover the observed marginals.

Note that if the so-called “independent” copula function, defined by , is used, then the MaxEnt estimation is recovered. And as for MaxEnt, the copula approach cannot reproduce the topological structure of sparse networks [115].

3.5.2 A Bayesian approach to network reconstruction

The major difference between likelihood-based methods (as those described in the previous sections) and Bayesian methods lies in the role played by model parameters. Very broadly speaking, while likelihood-based methods provide a recipe for estimating the unknown parameters on the basis of the observations, Bayesian approaches treat the unknown parameters as (additional) random variables, described by properly-defined prior probability distributions, whose parameters (called meta-parameters) are chosen a priori.

The first example of this second kind of approach to network modeling is provided by the fitness model [52], resting upon the same ideas lying at the basis of the ERG approach:

-

1.

each node is described by a hidden variables , representing its “fitness”; generally speaking, this is a real numbers supposedly quantifying the importance of that node in the network, and is drawn from a given probability distribution ;

-

2.

any two nodes and establish a connection according to a coupling function that, for undirected networks, is symmetric in the hidden variables assigned to nodes and .

The main difference with respect to the ERG approach lies in the a priori choice of both the functional form of the coupling function and the distribution from which fitnesses are drawn. The fitness model can be straightforwardly implemented by adapting the discrete formulas derived within the ERG framework to the continuous case. For instance, in the undirected case, the Bayesian derivation of the nodes degrees and of the total number of links reads

| (78) |

| (79) |

where the integrations over the support of the distribution are necessary to account for the fitness variability.

Remarkably, several combinations of and lead to recover power-law degree distributions. In particular, both the intuitive combination

| (80) |

and the highly non-trivial combination

| (81) |

lead to . This result points out that a number of topological properties believed to arise only as a consequence of microscopic dynamic processes (as the one described by the preferential attachment mechanism and its variants) can, instead, be replicated also via a static model [52]. In other words, whenever preferential attachment does not represent a plausible mechanism, it is reasonable to imagine that any two vertices establish a connection when the link creates a mutual benefit, depending on some intrinsic node property.

The aforementioned approach has been recently extended to account also for weights, through an algorithm which is not dissimilar in spirit from the DECM. More specifically, the model introduced in [116] is described by the following probability distribution for link weights:

| (82) |

(with ). Hence, as in the DECM, distinct links are independent, and while the presence of the link is described by a Bernoulli trial, the value of its weight is set according to an exponential distribution. Note that the latter is the continuous version of the geometric distribution, which is obtained by ERG-based models upon assuming discrete weights. The philosophy of the fitness model is then encoded into the choice of functional forms reading

| (83) |

In these expressions, is the quantile function of the Gamma distribution with positive shape and scale parameters and , drawn from an a prior distribution , while fitnesses are drawn from the distribution and is defined as in [116] such that the degree distribution exhibits a power law. An homogeneous version of the model has been also introduced, defined by the choices and .

Since this model induces an entire ensemble of networks, the expected value of the quantities of interest can be computed only after introducing a sampling procedure on the ensemble. The authors of [116] adopt a Gibbs sampler working as follows.

-

1.

The sampler is initialized with a matrix . When considering the homogeneous version, the initial matrix is generated via the Erdős-Rényi model whose only parameter is required to match the observed average degree. Since the initial configuration is required to satisfy the conditions and , the maximum-flow algorithm [117] is employed to obtain a matrix matching the constraints exactly.

-

2.

The whole ensemble of configurations is obtained by “perturbing” . Such perturbations generalize the local rewiring algorithm according to the following rules: 1) the dimension of the sub-matrices to be updated is chosen and a set of pairs of indices is selected; 2) the entries of are updated according to the rule

(84) with indicating the -th pair of indices (e.g., the -th row and the -th column) and .

Such a sampling process does not leave unexplored regions of the space of configurations: the existence of a sequence of Gibbs moves allowing for a transition from any matrix compatible with the given constraints to any other is, in fact, guaranteed [116]). And although the algorithm allows one to generate networks characterized by different topological structures, every configuration satisfies the constraints defined by eqs. (5) exactly.

An “empirical” Bayesian approach to network reconstruction

3.5.3 A comment on the Bayesian approaches to reconstruction

Although the three aforementioned algorithms have been labeled as Bayesian, they share features of both likelihood-based and genuinely Bayesian methods. All of them are, in fact, characterized by the presence of one, or more, free parameters not to be drawn from a priori distributions, but to be estimated via properly-defined likelihood conditions.

For what concerns the model in [52], the only free parameter is fixed by imposing the condition , i.e., by substituting either eq. (80) or eq. (81) into eq. (79) and solving the resulting equation for . A main difference with the fitness-induced ERG formalism [98] remains in the way fitnesses are dealt with. In a sense, the fitness-induced ERG formalism represents the likelihood-based analogue of the Bayesian approach discussed here: there, the information on the fitness distribution is completely ignored and just a point-estimation is carried out; here, the fitness variability is completely accounted for.