Quantum Risk Analysis

Abstract

We present a quantum algorithm that analyzes risk more efficiently than Monte Carlo simulations traditionally used on classical computers. We employ quantum amplitude estimation to evaluate risk measures such as Value at Risk and Conditional Value at Risk on a gate-based quantum computer. Additionally, we show how to implement this algorithm and how to trade off the convergence rate of the algorithm and the circuit depth. The shortest possible circuit depth - growing polynomially in the number of qubits representing the uncertainty - leads to a convergence rate of . This is already faster than classical Monte Carlo simulations which converge at a rate of . If we allow the circuit depth to grow faster, but still polynomially, the convergence rate quickly approaches the optimum of . Thus, for slowly increasing circuit depths our algorithm provides a near quadratic speed-up compared to Monte Carlo methods. We demonstrate our algorithm using two toy models. In the first model we use real hardware, such as the IBM Q Experience, to measure the financial risk in a Treasury-bill (T-bill) faced by a possible interest rate increase. In the second model, we simulate our algorithm to illustrate how a quantum computer can determine financial risk for a two-asset portfolio made up of Government debt with different maturity dates. Both models confirm the improved convergence rate over Monte Carlo methods. Using simulations, we also evaluate the impact of cross-talk and energy relaxation errors.

I Introduction

Risk management plays a central role in the financial system. Value at risk (VaR) (Glasserman et al., 2000), a quantile of the loss distribution, is a widely used risk metric. Examples of use cases include the Basel III regulations under which banks are required to perform stress tests using VaR Basel Committee on Banking Supervision (2009) and the calculation of haircuts applied to collateral used in security settelement systems García Cañizares and Gençay (2006). A second important risk metric is conditional value at risk (CVaR, sometimes also called expected shortfall), defined as the expected loss for losses greater than VaR. By contrast to VaR, CVaR is more sensitive to extreme events in the tail of the loss distribution.

Monte Carlo simulations are the method of choice to determine VaR and CVaR of a portfolio (Glasserman et al., 2000). They are done by building a model of the portfolio assets and computing the aggregated value for different realizations of the model input parameters. VaR calculations are computationally intensive since the width of the confidence interval scales as . Many different runs are needed to achieve a representative distribution of the portfolio value.

Quantum computers process information using the laws of quantum mechanics Nielsen and Chuang (2010). This has opened up novel ways of addressing some problems, e.g. in quantum chemistry (Peruzzo et al., 2014), optimization (Moll et al., 2017), or machine learning (Biamonte et al., 2017). Amplitude estimation is a quantum algorithm used to estimate an unknown parameter and converges as , which is a quadratic speed-up over classical algorithms like Monte Carlo Brassard et al. (2000). It has already been shown how amplitude estimation can be used to price options with the Black-Scholes model Black and Scholes (1973); Rebentrost et al. (2018).

In Section II of this paper we show how to use amplitude estimation to calculate expectation, variance, VaR and CVaR of random distributions. Section III discusses how to construct the corresponding quantum circuits. In Sections IV and V we show how to apply our algorithm to portfolios made up of debt issued by the United States Treasury (US Treasury), which as of December 2016 had 14.5 trillion USD in outstanding marketable debt held by the public The Bureau of the fiscal service (2017). This debt is an actively traded asset class with typical daily volumes close to 500 billion USD Federal reserve bank of New York (2016) and is regarded as high quality collateral Federal Reserve Bank of New York (2018). Additionally, government debt typically lacks some of the more complex features that other types of fixed-income securities have. These features make US Treasuries a highly relevant asset class to study whilst allowing us to use simple models to illustrate our algorithm. In Section IV we introduce a very simple portfolio made up of one T-Bill analyzed on a single period of a binomial tree. We demonstrate amplitude estimation and can approximate the expected value of the T-Bill on a real quantum computer. In Section V we show a more comprehensive two asset portfolio and simulate the presented algorithms assuming a perfect as well as a noisy quantum computer. We discuss our results as well as next steps in Sec. VI.

II Quantum Risk Analysis

In this section, we introduce amplitude estimation and explain how it can be used to estimate properties of random distributions such as risk measures.

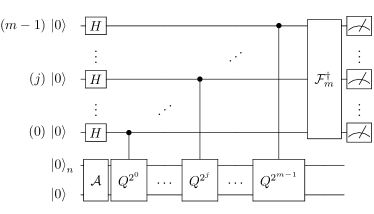

Suppose a unitary operator acting on a register of qubits such that for some normalized states and , where is unknown. Amplitude estimation allows the efficient estimation of , i.e., the probability of measuring in the last qubit Brassard et al. (2000). This is done using an operator (formally introduced in Appendix A), based on , and Quantum Phase Estimation (Kitaev, 1995) to approximate certain eigenvalues of . This requires additional qubits and applications of . The qubits are first put into equal superposition by applying Hadamard gates. Then, they are used to control different powers of . And last, after an inverse Quantum Fourier Transform has been applied, their state is measured, see the circuit in Fig. 1. This results in an integer , which is classically mapped to the estimator . The estimator satisfies

| (1) | |||||

| (2) |

with probability of at least . This represents a quadratic speedup compared to the convergence rate of classical Monte Carlo methods (Glasserman et al., 2000).

We now explain how to use amplitude estimation to approximate the expected value of a random variable (Abrams and Williams, 1999; Montanaro, 2017). Suppose a quantum state

| (3) |

where the probability of measuring the state is , with , and . The state is one of the possible realizations of a bounded discrete random variable , which, for instance, can represent a discretized interest rate or the value of a portfolio.

We consider a function and a corresponding operator

| (4) |

for all , acting on an ancilla qubit. Applying to leads to the state

Now we can use amplitude estimation to approximate the probability of measuring in the last qubit, which equals and thus also . Choosing allows us to estimate and hence . If we choose we can efficiently estimate which yields the variance . In the remainder of this section we extend this technique and show how to evaluate risk measures such as VaR and CVaR.

For a given confidence level , can be defined as the smallest value such that . To find on a quantum computer, we define the function if and otherwise, where . Applying , i.e. the operator corresponding to , to leads to the state

| (5) |

The probability of measuring for the last qubit is . Therefore, with a bisection search over we can find the smallest level such that in at most steps. The smallest level is equal to . This allows us to estimate as before with accuracy , which again is a quadratic speedup compared to classical Monte Carlo methods.

is the conditional expectation of restricted to , where we compute as before. To estimate CVaR we apply the operator that corresponds to the function to , which leads to the state

| (6) |

The probability of measuring for the last qubit equals , which we approximate using amplitude estimation. However, we know that does not sum up to one but to as evaluated during the VaR estimation. Therefore we must normalize the probability of measuring to get

| (7) |

We also multiplied by , otherwise we would estimate . Even though we replace by an estimation, the error bound on CVaR, computed in Appendix C, shows that we still achieve a quadratic speed up compared to classical Monte Carlo methods.

We have shown how to calculate the expected value, variance, VaR and CVaR of . However, if we are instead interested in properties of , for a given function , , , we can apply an operator and use the previously introduced algorithms on the second register. Alternatively, as long as we can efficiently perform the bisection search on for , we can spare the second register and combine and and apply all algorithms directly.

III Quantum Circuits

In this section, we show how the algorithms discussed in Sec. II can be mapped to quantum circuits.

We start with the construction of as introduced in Eq. (3), representing the probability distribution of a random variable mapped to . In general, the best known upper bound for the number of gates required to create is (Mottonen et al., 2004). However, approximations with polynomial complexity in are possible for many distributions, e.g., log-concave distributions Grover and Rudolph (2002). In the remainder of this section, we assume a given operator such that .

If we are interested in properties of , as discussed in the previous section, then, depending on , we can use basic arithmetic operations to construct the operator . Numerous quantum algorithms exist for arithmetic operations (Vedral et al., 1995; Draper, 2000; Cuccaro et al., 2004; Draper et al., 2004; Bhaskar et al., 2015) as well as tools to translate classical logic into quantum circuits (Green et al., 2013a, b). However, since the latter are not necessarily efficient, the development of new and improved algorithms is ongoing research.

Approximating using amplitude estimation requires the operator for , defined in Eq. (4). In general, representing for the expected value or for the CVaR either requires an exponential number of gates or additional ancillas to pre-compute the (discretized) function into qubits, using quantum arithmetic, before applying the rotation (Mitarai et al., 2018). The exact number of ancillas depends on the desired accuracy of the approximation of . Another approach consists of piecewise polynomial approximations of (Häner et al., 2018). However, this also implies a significant overhead in terms of the number of ancillas and gates. In the following, we show how to overcome these hurdles by approximating without ancillas using polynomially many gates, at the cost of a lower - but still faster than classical - rate of convergence. Note that the operator required for estimating VaR is easier to construct and we can always achieve the optimal rate of convergence as discussed later in this section.

Our contribution rests on the fact that an operator , for a given polynomial of order , can be efficiently constructed using multi- controlled Y-rotations, as illustrated in Fig. 2. Single qubit operations with control qubits can be exactly constructed, e.g., using gates and ancillas or gates without any ancillas. They can also be approximated with accuracy using gates (Barenco et al., 1995). For simplicity, we use gates and ancillas. Since the binary variable representation of , illustrated in Fig. 2, leads to at most terms, the operator can be constructed using gates and ancillas.

For every analytic function , there exists a sequence of polynomials such that the approximation error converges exponentially fast to zero with increasing order of the polynomials (Trefethen, 2013). Thus, for simplicity, we assume that is a polynomial of order .

If we can find a polynomial such that , then we can set , and the previous discussion provides a way to construct the operator . Since the expected value is linear, we may choose to estimate instead of for a parameter , and then map the result back to an estimator for . The rationale behind this choice is that . Thus, we want to find such that is sufficiently well approximated by . Setting the two terms equal and solving for leads to

| (8) |

and we choose as a Taylor approximation of Eq. (8) around . Note that Eq. (8) defines an odd function around , and thus the even terms in the Taylor series equal zero. The Taylor approximation of order leads to a maximal approximation error for Eq. (8) of

| (9) |

for all , as shown in Appendix B.

Now we consider the resulting polynomial of order . The number of gates required to construct the corresponding circuit scales as . The smallest scenario of interest is and , i.e., both, and , are linear functions, which leads to a circuit for where the number of gates scales quadratically as the number of qubits representing grows linearly.

Thus, using amplitude estimation to estimate leads to a maximal error

| (10) |

where we ignore the higher order terms in the following. Since our estimation uses , we also need to analyze the scaled error , where denotes the resulting estimation error for . Setting Eq. (10) equal to and reformulating it leads to

| (11) |

Maximizing the left-hand-side with respect to , i.e. minimizing the number of required samples to achieve a target error , results in . Plugging into Eq. (11) gives

| (12) |

Translating this into a rate of convergence for the estimation error with respect to the number of samples leads to For , we get , which is already better than the classical convergence rate of . For increasing , the convergence rate quickly approaches the optimal rate of .

For the estimation of the expectation we exploited . For the variance we apply the same idea but use . We employ this approximation to estimate the value of and then, together with the estimation for , we evaluate . The resulting convergence rate is again equal to .

The previous discussion shows how to build quantum circuits to estimate and more efficiently than possible classically. In the following, we extend this to VaR and CVaR.

Suppose the state corresponding to the random variable on and a fixed . To estimate VaR, we need an operator that maps to if and to otherwise, for all . Then, for the fixed , amplitude estimation can be used to approximate , as shown in Eq. (6). With ancillas, adder-circuits can be used to construct using gates (Cuccaro et al., 2004), and the resulting convergence rate is . For a given level , a bisection search can find the smallest such that in at most steps, and we get .

To estimate the CVaR, we apply the circuit for to an ancilla qubit and use this ancilla qubit as a control for the operator used to estimate the expected value, but with a different normalization, as shown in Eq. (6). Based on the previous discussion, it follows that amplitude estimation can then be used to approximate with the same trade-off between circuit depth and convergence rate as for the expected value.

IV T-Bill on a single period binomial tree

Our first model consists of a zero coupon bond discounted at an interest rate . We seek to find the value of the bond today given that in the next time step there might be a rise in . The value of the bond with face value is

| (13) |

where and denote the probabilities of a constant interest rate and a rise, respectively. This model is the first step of a binomial tree. Binomial trees can be used to price securities with a path dependency such as bonds with embedded options Black et al. (1990).

The simple scenario in Eq. (13) could correspond to a market participant who bought a 1 year T-bill the day before a Federal Open Markets Committee announcement and expects a -points increase of the Federal Funds Rate with a probability and no change with a probability 111The investor would also have to assume that there is a perfect correlation between one year T-Bills and the Federal Funds Rate. This situation also implies that the market does not expect a change in the Federal Funds Rate to occur..

We show how to calculate the value of the investor’s T-bill using the IBM Q Experience by using amplitude estimation and mapping to such that and correspond to and , respectively.

Here, we only need a single qubit to represent the uncertainty and the objective and we have , where , and thus, .

For the one-dimensional case, it can be easily seen that the amplitude estimation operator , where denotes the corresponding Pauli operator (Nielsen and Chuang, 2010). We discuss this in more detail in Appendix A. In particular, this implies , which allows us to construct the amplitude estimation circuit efficiently to approximate the parameter .

Although a single period binomial tree is a very simple model, it is straight-forward to extend it to multi-period multi-nomial trees with path-dependent assets. Thus, it represents the smallest building block for interesting scenarios of arbitrary complexity.

Results from real quantum hardware

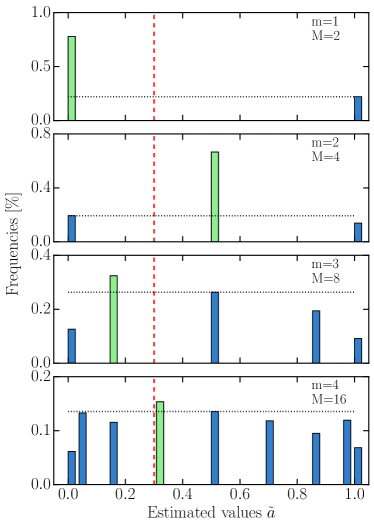

We run several experiments in which we apply amplitude estimation with a different number of evaluation qubits corresponding to samples, respectively, to estimate . This requires at most five qubits and can be implemented and run on the IBM Q 5 Yorktown (ibmqx2) quantum processor with five qubits accessible via the IBM Q Experience (ibm, a). As disussed in Sec. II, the success probability of amplitude estimation is larger than , but not necessarily , and the real hardware introduces additional errors. Thus, we repeat every circuit times (i.e., the maximal number of shots in the IBM Q Experience) to get a reliable estimate. This implies a constant overhead, which we ignore in the comparison of the algorithms. The quantum circuit for compiled to the IBM Q 5 quantum processor is illustrated in Fig. 3. The connectivity of the IBM Q 5 quantum processor, shown in Appendix G, requires swapping two qubits in the middle of the circuit between the application of the controlled operators and the inverse Quantum Fourier Transform. The results of the algorithm are illustrated in Fig. 4 where it can be seen that the most frequent estimator approaches the real value and how the resolution of the algorithm increases with . The quantum algorithm presented in this paper outperforms the Monte Carlo method already for samples (i.e. evaluation qubits), which is the largest scenario we performed on the real hardware, see Fig. 5. The details of this convergence analysis are discussed in Appendix E.

V Two asset portfolio

We now illustrate how to use our algorithm to calculate the daily risk in a portfolio made up of one-year US Treasury bills and two-year US Treasury notes with face values and , respectively. We chose a simple portfolio in order to put the focus on the amplitude estimation algorithm applied to VaR. The portfolio is worth

| (14) |

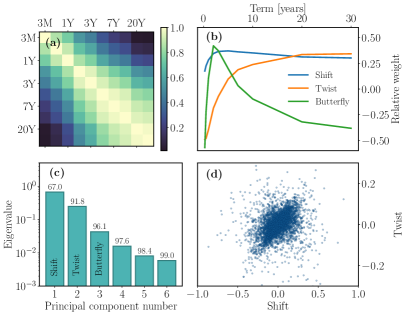

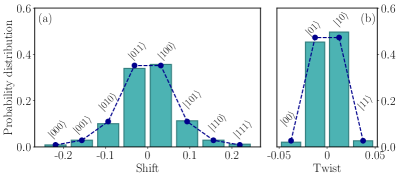

where is the coupon rate paid every six months by the two-year treasury note and and are the yield to maturity of the one-year bill and two-year note, respectively. US Treasuries are usually assumed to be default free Nippani et al. (2001). The cash-flows are thus known ex ante and the changes in the interest rates are the primary risk factors. Therefore, a proper understanding of the yield curve suffices to model the risk in this portfolio. In this work we use the Constant Maturity Treasury (CMT) rates to model the uncertainty in and , see Appendix F for a description of the data. To calculate the daily risk of our portfolio we study the difference in the CMT rates from one day to the next. These differences are highly correlated (as are the initial CMT rates), see Fig. 6(a), making it unnecessary to model them all when simulating more complex portfolios. A principal component analysis reveals that the first three principal components, named shift, twist and butterfly account for 96% of the variance Colin et al. (2006); Vannerem and Iyer (2010), see Fig. 6(b)-(d). Therefore, when modeling a portfolio of US Treasury securities it suffices to study the distribution of these three factors. This dimensionality reduction also lowers the amount of resources needed by our quantum algorithm.

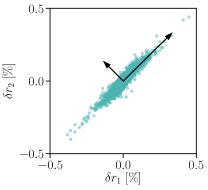

To study the daily risk in the portfolio we write where is the yield to maturity observed today and the random variable follows the historical distribution of the one day changes in the CMT rate with maturity . For our demonstration we set , , , and in Eq. (14). We perform a principal component analysis of and and retain only the shift and twist components. Figure 7 illustrates the historical data as well as and , related to by

| (15) |

The correlation coefficient between shift and twist is . We thus assume them to be independent and fit discrete distributions to each separately, see Fig. 8. We retained only the first two principal components to illustrate the use of principal component analysis despite the fact that, in this example, there is no dimensionality reduction. Furthermore, this allows us to simulate our algorithm in a reasonable time on classical hardware by keeping the number of required qubits low. We expect that all three components would be retained when running this algorithm on real quantum hardware for larger portfolios.

V.1 Uncertainty representation in the quantum computer

We use three qubits, denoted by , to represent the distribution of , and two, denoted by , for . As discussed in Sec. III, the probability distributions are encoded by the states and for and , which can thus take eight and four different values, respectively. We use more qubits for than for since the shift explains a larger part of the variance. Additional qubits may be used to represent the probability distributions at a higher resolution. The qubits naturally represent integers via binary encoding and we apply the affine mappings

| (16) | |||||

| (17) |

Here and denote the integer representations of and , respectively. Given the almost perfect symmetry of the historical data we fit symmetric distributions to it. The operator that we define prepares a quantum state , illustrated by the dots in Fig. 8, that represents the distributions of and , up to the aforementioned affine mapping.

V.2 Portfolio model on the quantum computer

Next, we show how to construct the operator to translate the random variables and into a portfolio value. Equations (14) through (17) allow us to define the portfolio value in terms of and , instead of and . For simplicity, we use a first order approximation

| (18) |

of around the mid points and . From a financial perspective, the first order approximation of corresponds to studying the portfolio from the point of view of its duration Martellini et al. (2003). Higher order expansions, e.g. convexity could be considered at the cost of increased circuit depth.

To map the approximated value of the portfolio to a function with target set we compute , where and , i.e., the minimum and maximum values can take for the considered values of and . This leads to

| (19) |

The approach, illustrated in Fig. 2, allows us to construct an operator corresponding to for a given scaling parameter .

V.3 Results from simulations of an ideal quantum computer

We simulate the two-asset portfolio for different numbers of sampling qubits to show the behavior of the accuracy and convergence rate. We repeat this task twice, once for a processor with all-to-all connectivity and once for a processor with a connectivity corresponding to the IBM Q 20 chip, see Appendix G. This highlights the overhead imposed by a realistic chip connectivity. For a number samples, we need a total of qubits for expected value and VaR, and qubits for CVaR. Five of these qubits are used to represent the distribution of the interest rate changes, see Sec. V.1, one qubit is needed to create the state in Eq. (4) used by amplitude estimation, and six ancillas are needed to implement the controlled operator. For CVaR we need one more ancilla for the comparison to the level as discussed in Sec. III. Once the shift and twist distributions are loaded into the quantum computer, using the circuit shown in Fig. 8(c) and (d), we apply the operator to create the state defined in Eq. (4).

We compare the quantum estimation of risk to the exact VaR level of . When taking into account the mapping of Sec. V.2, this classical VaR corresponds to 0.093, shown by the verticle line in Fig. 9. The quantum estimation of risk rapidly approaches this value as is increased, see Fig. 9. With sample qubits the difference between the classical and quantum estimates is 9%. The number of CNOT gates needed to calculate VaR approximately doubles each time a sample qubit is added, see Tab. 1, i.e. it scales as with a resulting error of .

We find that the connectivity of the IBM Q 20 chip increases the number of CNOT gates by a factor when compared to a chip with all-to-all connectivity 222These results are based on QISKit 0.5, future version might be able to further reduce the CNOT overhead, cf. Qis (2018).

| #CX | |||||

|---|---|---|---|---|---|

| m | M | #qubits | all-to-all | IBM Q 20 | overhead |

| 1 | 2 | 13 | 795 | 1’817 | 2.29 |

| 2 | 4 | 14 | 2’225 | 5’542 | 2.49 |

| 3 | 8 | 15 | 5’085 | 12’691 | 2.50 |

| 4 | 16 | 16 | 10’803 | 26’457 | 2.45 |

| 5 | 32 | 17 | 22’235 | 55’520 | 2.50 |

V.4 Results from simulations of a noisy quantum computer

Computing risk for the two-asset portfolio requires a long circuit. However, it suffices for amplitude estimation to return the correct state with the highest probability, i.e. measurements do not need to yield this state with 100% probability. We now run simulations with errors to investigate how much imperfections can be tolerated before the correct state can no longer be identified.

We study the effect of two types of errors: energy relaxation and cross-talk, where the latter is only considered for two-qubit gates (CNOT gates). We believe this to be a sufficient approximation to capture the leading error sources. Errors and gate times for single qubit gates are in general an order of magnitude lower than for two-qubit gates Sheldon et al. (2016); Gustavsson et al. (2013); International Business Machines Corporation (2016). Furthermore, our algorithm requires the same order of magnitude in the number of single and two-qubit gates, see Tab. 1. Energy relaxation is simulated using a relaxation rate such that after a time each qubit has a probability of relaxing to Qis (2018). We set the duration of the CNOT gates to and assume that the single qubit gates are done instantly and are thus exempt from errors. We also include qubit-qubit cross-talk in our simulation by adding a error-term in the generator of the CNOT gate

| (20) |

Typical cross-resonance Rigetti and Devoret (2010) CNOT gate rates are of the order of whilst cross-talk on IBM Q chips are of the order of International Business Machines Corporation (2016). We thus estimate a reasonable value of , i.e. the strength of the cross-talk, to be and simulate its effect over the range .

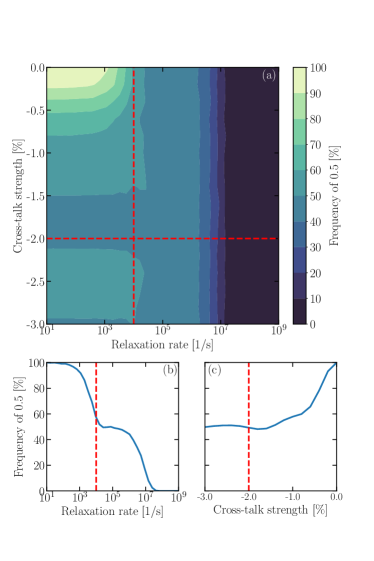

We illustrate the effect of these errors by computing the expected value of the portfolio. Since the distributions are symmetric around zero and mapped to the interval we expect a value of , i.e. from one day to the next we do not expect a change in the portfolio value. This simulation is run with sample qubits since this suffices to exactly estimate . The algorithm is successful if it manages to identify 0.5 with a probability greater than 50%. With our error model this is achieved for relaxation rates and cross-talk strength , see Fig. 10(a)-(c), despite the 4383 gates needed. A generous estimation of current hardware capabilities with (loosely based on ) and , shown as red lines in Fig. 10, indicates that this simulation may be possible in the near future as long as other error sources (such as measurement error and unitary errors resulting from improper gate calibrations) are kept under control.

VI Conclusion

We developed a quantum algorithm to estimate risk, e.g. for portfolios of financial assets, resulting in a quadratic speedup compared to classical Monte Carlo methods. The algorithm has been demonstrated on real hardware for a small model and the scalability and impact of noise has been studied using a more complex model and simulation. Our approach is very flexible and straight-forward to extend to other risk measures such as semi-variance.

More qubits are needed to model realistic scenarios and the errors of actual hardware need to be reduced. Although the quadratic speedup can already be observed for a small number of samples, more is needed to achieve a practical quantum advantage. In practice, Monte Carlo simulations can be massively parallelized, which pushes the border for a quantum advantage even higher.

Our simulations of the two-asset portfolio show that circuit depth is limited for current hardware. In order to perform the calculation of VaR for the two asset portfolio on real quantum hardware it is likely that qubit coherence times will have to be increased by several orders of magnitude and that cross-talk will have to be further suppressed.

However, approximating, parallelizing, and decomposing quantum phase estimation is ongoing research and we expect significant improvements in this area not only through hardware, but also algorithms (Dobsicek et al., 2006; O’Loan, 2010; Svore et al., 2014). This can also help to shorten the required circuit depths, and thus, to reduce the requirements on the hardware to achieve a quantum advantage. Circuit depth can also be shortened by using a more versatile set of gates. For instance, the ability to implement SWAP gates directly in hardware would circumvent the need to synthesize them using CNOT gates Egger et al. (2018); Sjöqvist et al. (2012). In addition, techniques such as error mitigation Kandala et al. (2018) could be applied to cope with the noisy hardware of the near future.

Another question that has only briefly been addressed in this paper is the loading of considered random distributions or stochastic processes. For auto-correlated processes this can be rather costly and needs to be further investigated. Techniques known from classical Monte Carlo, such as importance sampling (Tokdar and Kass, 2010), might be employed here as well to improve the results or reduce the circuit depth.

Acknowledgements.

We want to thank Lior Horesh for his insights and the stimulating discussions. IBM and IBM Q are trademarks of International Business Machines Corporation, registered in many jurisdictions worldwide. Other product or service names may be trademarks or service marks of IBM or other companies.Appendix A -Operator

For a given circuit acting on qubits, the corresponding -operator used in amplitude estimation is defined as (Brassard et al., 2000)

where denotes the identity operator. If , as e.g. considered in Sec. IV, the reflections defining reduce to the Pauli -operators and simplifies to . In addition, if then it can be easily seen that .

Appendix B Error bound for approximation

Suppose denotes the Taylor approximation of Eq. (8) of order . Then, the error bound is derived from the next coefficient in the Taylor series (plus higher order terms). Therefore, we analyze the Taylor series

for . The Taylor series can be derived by first taking the derivative, using the corresponding Taylor series, and integrating the different terms independently. Replacing by for and the fact that the extreme values are assumed for leads to a bound on the individual terms for a particular given by

where we used . For a Taylor approximation of order , the error bound is given by the bound on the next Taylor coefficient in the series, i.e. for .

Appendix C CVaR Error Bound

Since is replaced by an estimation, we cannot directly apply the amplitude estimation error bound for CVaR. Assume two unknowns and their estimates , , where for . The first order Taylor approximation of with respect to and around zero can be used to derive

| (21) |

where we ignore higher order terms of and .

Setting and , multiplying everything with and replacing by leads to the following bound for the approximation error of :

| (22) | |||||

| (23) |

where again we omit higher order terms. Thus, the quantum estimation of CVaR also achieves a quadratic speedup compared to classical Monte Carlo methods.

Appendix D , single qubit rotations

Appendix E Convergence Analysis

For the Monte Carlo simulation we consider a -confidence interval. To enable a fair comparison despite the small number of samples, we compute an optimistic bound and assume the exact standard error , where denotes the success probability of the Bernoulli random variable. For and a confidence level, the resulting confidence interval is given by .

For the quantum algorithm we exploit the error bound given in Eq. (10).

Although the exact value of is supposed to be unknown, we can use the estimated value to compute an error bound.

The algorithm results in an integer which is classically mapped to , and we assume is the most probable result of the quantum algorithm.

The theory says that for , defined through , it holds that .

Then, the interval for can be mapped to an interval for , whose width is compared to the confidence interval from the Monte Carlo simulation.

Since the mapping from to is non-linear, the error bound is not symmetric around and we consider the maximum.

Appendix F Data used in this work

In this work we use the Constant Maturity Treasury rates obtained from the U.S. Department of the Treasury U.S. Department of the Treasury (2018). The data is made up of 1/4, 1/2, 1, 2, 3, 5, 7, 10, 20 and 30 year rates resulting from an interpolation of the daily yield curve obtained from the bid yield of actively traded treasury securities at market close. We only consider periods where all rates are available and ignore the others. In total, we use more than data points.

Appendix G Topology of IBM Q 5 and IBM Q 20 quantum processor

Figures 11 and 12 show the topologies of the IBM Q 5 (ibm, a) and IBM Q 20 (ibm, b) quantum processors. The lines indicate the connectivity, i.e., the pairs of qubits that allow the application of CNOT gates.

References

- Glasserman et al. (2000) P. Glasserman, P. Heidelberger, and P. Shahabuddin, in Mastering Risk (2000), vol. 2, pp. 5–18.

- Basel Committee on Banking Supervision (2009) Basel Committee on Banking Supervision, Revisions to the basel ii market risk framework (2009).

- García Cañizares and Gençay (2006) A. García Cañizares and R. Gençay, SSRN Electronic Journal (2006).

- Nielsen and Chuang (2010) M. A. Nielsen and I. L. Chuang, Quantum Computation and Quantum Information (2010), ISBN 9780511976667.

- Peruzzo et al. (2014) A. Peruzzo, J. McClean, P. Shadbolt, M. H. Yung, X. Q. Zhou, P. J. Love, A. Aspuru-Guzik, and J. L. O’Brien, Nature Communications 5 (2014), ISSN 20411723.

- Moll et al. (2017) N. Moll, P. Barkoutsos, L. S. Bishop, J. M. Chow, A. Cross, D. J. Egger, S. Filipp, A. Fuhrer, J. M. Gambetta, M. Ganzhorn, et al., arXiv:1710.01022 (2017).

- Biamonte et al. (2017) J. Biamonte, P. Wittek, N. Pancotti, P. Rebentrost, N. Wiebe, and S. Lloyd, Nature 549, 195 (2017), ISSN 14764687.

- Brassard et al. (2000) G. Brassard, P. Hoyer, M. Mosca, and A. Tapp, arXiv:0005055 (2000).

- Black and Scholes (1973) F. Black and M. Scholes, Journal of Political Economy 81, 637 (1973).

- Rebentrost et al. (2018) P. Rebentrost, B. Gupt, and T. R. Bromley (2018), eprint arXiv:1805.00109.

- The Bureau of the fiscal service (2017) The Bureau of the fiscal service, Monthly statment of the public debt of the united states (2017).

- Federal reserve bank of New York (2016) Federal reserve bank of New York, US Treasury Trading Volume (2016).

- Federal Reserve Bank of New York (2018) Federal Reserve Bank of New York, Federal reserve collateral guidelines (2018).

- Kitaev (1995) A. Y. Kitaev (1995), eprint arXiv:9511026.

- Abrams and Williams (1999) D. S. Abrams and C. P. Williams (1999), eprint arXiv:9908083.

- Montanaro (2017) A. Montanaro (2017), eprint arXiv:1504.06987.

- Mottonen et al. (2004) M. Mottonen, J. J. Vartiainen, V. Bergholm, and M. M. Salomaa, Quant. Inf. Comp. 5, 4 (2004), ISSN 15337146, eprint 0407010.

- Grover and Rudolph (2002) L. Grover and T. Rudolph (2002), eprint arXiv:0208112.

- Vedral et al. (1995) V. Vedral, A. Barenco, and A. Ekert (1995), eprint arXiv:9511018v1.

- Draper (2000) T. G. Draper (2000), ISSN 16136829, eprint arXiv:0008033.

- Cuccaro et al. (2004) S. A. Cuccaro, T. G. Draper, S. A. Kutin, and D. P. Moulton (2004), eprint arXiv:0410184.

- Draper et al. (2004) T. G. Draper, S. A. Kutin, E. M. Rains, and K. M. Svore, pp. 1–21 (2004), ISSN 1533-7146, eprint arXiv:0406142.

- Bhaskar et al. (2015) M. K. Bhaskar, S. Hadfield, A. Papageorgiou, and I. Petras (2015), ISSN 15337146, eprint arXiv:1511.08253.

- Green et al. (2013a) A. S. Green, P. L. Lumsdaine, N. J. Ross, P. Selinger, and B. Valiron (2013a), eprint arXiv:1304.3390.

- Green et al. (2013b) A. S. Green, P. L. Lumsdaine, N. J. Ross, P. Selinger, and B. Valiron, in Lecture Notes in Computer Science (including subseries Lecture Notes in Artificial Intelligence and Lecture Notes in Bioinformatics) (2013b), vol. 7948 LNCS, pp. 110–124, ISBN 9783642389856, ISSN 03029743, eprint arXiv:1304.5485.

- Mitarai et al. (2018) K. Mitarai, M. Kitagawa, and K. Fujii (2018), eprint arXiv:1805.11250.

- Häner et al. (2018) T. Häner, M. Roetteler, and K. M. Svore (2018), eprint arXiv:1805.12445.

- Barenco et al. (1995) A. Barenco, C. H. Bennett, R. Cleve, D. P. Divincenzo, N. Margolus, P. Shor, T. Sleator, J. A. Smolin, and H. Weinfurter, Physical Review A 52, 3457 (1995), ISSN 10502947, eprint arXiv:9503016.

- Trefethen (2013) L. N. L. N. Trefethen, Approximation theory and approximation practice (2013), ISBN 1611972396.

- Black et al. (1990) F. Black, E. Derman, and W. Toy, Financial Analysts Journal 46, 33 (1990), ISSN 0015198X.

- ibm (a) IBM Q 5 (ibmqx2), https://github.com/QISKit/qiskit-backend-information/blob/master/backends/yorktown/V1/README.md, accessed: 2018-05-22.

- Nippani et al. (2001) S. Nippani, P. Liu, and C. T. Schulman, The Journal of Financial and Quantitative Analysis 36, 251 (2001).

- Colin et al. (2006) A. Colin, M. Cubilié, and F. Bardoux, The Journal of Performance Measurement 10 (2006).

- Vannerem and Iyer (2010) P. Vannerem and A. S. Iyer, MSCI Barra Research Insights (2010).

- Martellini et al. (2003) L. Martellini, P. Priaulet, and S. Priaulet, Fixed-Income Securities (Wiley and Sons, 2003), ISBN 0-470-85277-1.

- Sheldon et al. (2016) S. Sheldon, E. Magesan, J. M. Chow, and J. M. Gambetta, Phys. Rev. A 93, 060302 (2016).

- Gustavsson et al. (2013) S. Gustavsson, O. Zwier, J. Bylander, F. Yan, F. Yoshihara, Y. Nakamura, T. P. Orlando, and W. D. Oliver, Phys. Rev. Lett. 110, 040502 (2013).

- International Business Machines Corporation (2016) International Business Machines Corporation, IBM Q Experience (2016), URL https://quantumexperience.ng.bluemix.net/qx/experience.

- Qis (2018) Quantum Information Software Kit (QISKit) (2018), URL https://qiskit.org/.

- Rigetti and Devoret (2010) C. Rigetti and M. Devoret, Phys. Rev. B 81, 134507 (2010).

- Dobsicek et al. (2006) M. Dobsicek, G. Johansson, V. Shumeiko, and G. Wendin, Science 2, 2 (2006), eprint arXiv:0610214.

- O’Loan (2010) C. J. O’Loan, Journal of Physics A: Mathematical and Theoretical 43 (2010), ISSN 17518113, eprint arXiv:0904.3426.

- Svore et al. (2014) K. M. Svore, M. B. Hastings, and M. Freedman, Quantum Information & Computation 14, 306 (2014), ISSN 1533-7146, eprint arXiv:1304.0741v1.

- Egger et al. (2018) D. J. Egger, G. Ganzhorn, Marc Salis, A. Fuhrer, P. Mueler, P. K. Barkoutsos, N. Moll, I. Tavernelli, and S. Filipp (2018), eprint arXiv:1804.04900.

- Sjöqvist et al. (2012) E. Sjöqvist, D. M. Tong, L. M. Andersson, B. Hessmo, M. Johansson, and K. Singh, New J. Phys. 14 (2012).

- Kandala et al. (2018) A. Kandala, K. Temme, A. D. Corcoles, A. Mezzacapo, J. M. Chow, and J. M. Gambetta (2018), eprint arXiv:1805.04492.

- Tokdar and Kass (2010) S. T. Tokdar and R. E. Kass, Wiley Interdisciplinary Reviews: Computational Statistics 2, 54 (2010), ISSN 19395108.

- U.S. Department of the Treasury (2018) U.S. Department of the Treasury, Daily treasury yield curve rates (2018).

- ibm (b) IBM Q 20, https://quantumexperience.ng.bluemix.net/qx/devices, accessed: 2018-05-22.