Parametric versus nonparametric: the fitness coefficient

Abstract

The fitness coefficient, introduced in this paper, results from a competition between parametric and nonparametric density estimators within the likelihood of the data. As illustrated on several real datasets, the fitness coefficient generally agrees with p-values but is easier to compute and interpret. Namely, the fitness coefficient can be interpreted as the proportion of data coming from the parametric model. Moreover, the fitness coefficient can be used to build a semiparamteric compromise which improves inference over the parametric and nonparametric approaches. From a theoretical perspective, the fitness coefficient is shown to converge in probability to one if the model is true and to zero if the model is false. From a practical perspective, the utility of the fitness coefficient is illustrated on real and simulated datasets.

Keywords: Goodness-of-fit; Density estimation; Semiparametric methods; Kernel smoothing; Likelihood methods.

1 Introduction

A challenge of data analysis is to assess the quality of a model. The traditional approach relies on goodness-of-fit tests where, loosely speaking, the ability of a model to fit the data is measured through distances between the observed values and the values expected under the model. Examples include the classical Pearson’s chi-squared test [2], the Kolmogorov or Cramer-von-Mises goodness-of-fit tests [3, 8, 10], or likelihood-ratio based statistics [5, 6, 50] (see [5] for an empirical likelihood approach).

In this context, p-values have emerged as natural instruments to measure the amount of evidence in favor of the model. However, the use of p-values is subjected to several difficulties: (i) their calculation might require computationally intensive strategies as the bootstrap [21, 24, 45]; (ii) interpretation is notoriously difficult [29, 38] as emphasized again in a recent ASA statement [52]; (iii) whenever some evidence has been found against the model, no information is delivered to improve inference.

In this paper, we introduce the fitness coefficient, a new criterion for simultaneously measuring the amount of evidence of a model and improving inference. Our goal is to provide an alternative approach to the use of p-values in goodness-of-fit testing that is no longer sensitive to the difficulties (i)-(iii).

Let be independent -variate observations with common density . Let be a family of probability density functions representing the model. Given the maximum likelihood estimator (based on the model), and the standard kernel density estimator (free from the model) with kernel and bandwidth , define the fitness coefficient as

| (1) |

where is called the leave-and-repair (LR) kernel estimate of and is given by

| (2) |

with and . The LR estimate is a modification of the well-known leave-one-out (LOO) estimate usually employed in cross-validation procedures [18] and semiparametric estimation [9].

The fitness coefficient has the following advantages.

(i) The fitness coefficient is easy to compute.

It is the minimizer of a simple one dimensional concave function.

(ii) The fitness coefficient is a measure of model quality.

As seen in (1), the fitness coefficient follows from a competition between the parametric and the nonparametric approach so as to maximize the likelihood of the observations. Hence, whenever the model is sufficiently true, we expect a value of relatively close to one. This is because the parametric estimator is likely to be more accurate than the nonparametric one. On the opposite, whenever the model is wrong, we expect a value of close to zero. Because is a mixture distribution between the parametric and the nonparametric estimates, the fitness coefficient is interpreted as the proportion of data distributed under the model. For instance, if one draws a bootstrap sample from the combination then the fitness coefficient is the proportion of data drawn from the fitted model . Therefore, the less the value of , the less the bootstrap sample shall be “contaminated” by the nonparametric part of the combination.

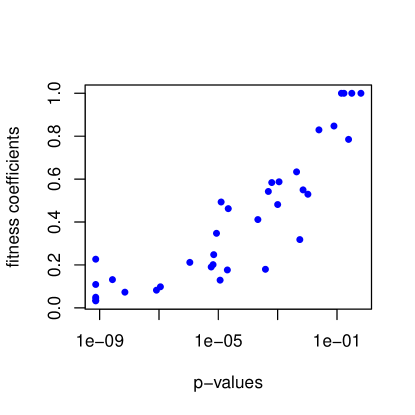

To show the capability of the fitness coefficient, we compare it to p-values on a real data example. Consider the problem of testing whether a given sample comes from a normal distribution. Specifically, we have 38 samples each consisting of financial returns of a company from the French stock market CAC40 and we wish to measure the quality of the normal model for each of these samples. On the one hand a goodness-of-fit test based on the Cramer-Von-Mises statistic [8] is carried out. On the other hand the fitness coefficient defined by (1) is computed with a Gaussian kernel , , where is the density of a Student-t distribution with degrees of freedom, and given by [42] (p. 48). In Figure 1, we plotted the values of the fitness coefficient against the p-values on a logarithmic scale. We can see a clear positive dependence relationship: large values for the fitness coefficient correspond to large p-values. This suggests that, if one had used p-values to assess the fitness of the normal model, he or she could have done so with the fitness coefficient.

The quality criterion induced by the fitness coefficient is different than that of information criteria [4, 7] such as the Akaike information criterion [1] or the Bayesian information criterion [40] which focus on the relative performances between models. Note that convex parametric combinations recently have been proposed in the Bayesian literature [23] to assess the fitness of a certain parametric model against another.

(iii) The fitness coefficient is useful to get robust semiparametric estimators.

The fitness coefficient offers a natural semiparametric alternative for estimating the probability density function of the observations. The idea of forming such a convex combination to get an estimator robust to misspecification while retaining a performance comparable to parametric estimators when the true density is close to the model was originally developed by Olkin and Spiegelman [33]. Their method, referred to as the OS method, consists of computing

| (3) |

where is the standard kernel density estimator. The OS method and the LR method given in (1) differ in the choice of the nonparametric estimator in the combination. The OS method was noticed to be sensitive to the choice of the bandwidth [12, 36].

Rather than considering the likelihood of the observations, some authors [25, 36, 43] investigate strategies based on the mean squared error between the combination and the true density , but then the solution depends on the unknown distribution and hence heavy bootstrap methods need to be employed.

To improve inference, there exist also other approaches than that of forming a convex combination between the parametric and nonparametric estimators. The locally parametric nonparametric estimation is developed for instance in [19, 20, 46], but is less appealing from the point of view of model quality assessment because they do not provide any “fitness coefficient”.

Main contributions.

By introducing the fitness coefficient, we provide a new measure for assessing the quality of a model and an alternative to the OS method to get robust semiparametric estimators. Under mild conditions, the fitness coefficient is shown to converge in probability to one if the model is true and zero otherwise, a property called consistency. Even if the fitness coefficient is maximizing some objective function (over ), classical results from M-estimation theory does not apply because, when the model is true, the limiting objective function is independent from . The proposed approach follows from a fine comparison between the rates of convergence of and . We moreover provide examples of densities that satisfy our set of assumptions. Using some real data as well as extensive simulations, we observed that the LR approach is more stable than the OS approach and leads to more accurate inference. This is in agreement with our theoretical analysis, which cannot include the OS method as an example.

Outline.

In Section 2, we introduce some quantities of interest and motivate the use of the LR estimator to compute the fitness coefficient . The consistency of the fitness coefficient is stated in Section 3 where some examples are given. In Section 4, numerical experiments are designed to measure the robustness of the fitness coefficient and the performance of the corresponding density estimators. All the proofs are postponed to the Appendix.

2 The leave-and-repair estimator

The aim of this section is to define and motivate the use of the leave-and-repair (LR) estimator (2) introduced in the definition of the fitness coefficient (1). Compared with the OS method given in (3), the use of the LR estimator might seem irrelevant at first view but in fact plays an important role to ensure the good behavior of the fitness coefficient.

The kernel density estimator of at is given by

For any , define the function as the convolution product between and , that is, , . Note that is the expected value of . In other words, . But since , we see that has a positive -dependent bias when estimating , conditionally on . When studying the estimator decomposition, this bias term spreads to the diagonal terms of some -statistics and gives rise, in the end, to some non-negligible terms. This phenomenon is common in semiparametric statisitcs, and has been noticed for instance in Remark 4 in [35].

To overcome the undesirable effects caused by this bias term, the leave-one-out (LOO) estimator of , given by

has been successfully used in several cross-validation procedures aiming at selecting the bandwidth, either based on the likelihood [17, 26, 18] or on the mean squared error [37, 44] (see [27] for a comparison). Since then, LOO estimators have been frequently used in semiparametric studies [9].

The LR estimator proposed in this paper is inspired, but different, from the LOO estimator. In view of (2), the LR estimator satisfies

If the LR estimator is equal to the LOO estimator. If and the LR estimator is equal to . In general, one can think of as of order and as a density, yielding that has probability .

The heuristic for using the LR estimator instead of the LOO estimator is as follows. It is well-known that the Kullback-Leibler divergence of kernel density estimates depends crucially on the tails of the true distribution [18, 39]. As shown in [18], if the tail is too heavy and the kernel vanishes too quickly as becomes large then the Kullback-Leibler divergence associated to the kernel density estimate goes to minus infinity. This is because some of the , , might have very small values (possibly zero), leading to very large values (possibly infinite) for some of the . These values are involved in the computation of the Kullback-Liebler divergence and play an important role in our proofs when dealing with the likelihood of the nonparametric estimate. We built the LR estimator to overcome this issue by simply adding to the LOO estimator. We coined the term leave-and-repair because the term repairs the LOO estimator. Since , the LR estimator is not subjected to the difficulties of the LOO estimator. By adding the term in (2), however, a biais is introduced: now one has . Thus, there is a biais-variance tradeoff controlled by the sequence that must go to zero slowly enough to keep away from zero but also fast enough to keep the biais as small as possible. The right compromise is given in the conditions in Theorem 2 (for instance is one possibility).

Concerning the parametric estimator , we follow [33] by considering the maximum likelihood estimator. Let be the parametric model where is such that for each , is a measurable function satisfying . The maximum likelihood estimator of based on and is where (when it exists; this is further assumed) is defined as

The good behaviour of the maximum likelihood estimator is subjected to the assumption that , that is, there exists such that .

To conclude the section, we consider existence and uniqueness of the fitness coefficient . The existence follows from the use of the LR estimator . Uniqueness of is obtained under the mild requirement that the parametric and nonparametric estimators are distinguishable on the observed data.

Proposition 1.

Suppose that a.s. and for at least one . Then the fitness coefficient exists and is unique.

The proof is given in Appendix A.

3 Consistency of the fitness coefficient

Recall that consistency of the fitness coefficient means in probability if and if , where is the true underlying density and is the parametric model. Section 3.1 and Section 3.2 contain the main consistency theorem and some examples satisfying our set of assumptions, respectively.

3.1 Assumptions and main result

Let be the Euclidean norm and for any set and any function , define the sup-norm as . Denote by the Lebesgue measure on . Introduce the density level sets

We shall assume the following.

-

(H1)

The density is bounded and continuous on and the gradient of is bounded on , and satisfies, for every and ,

where is positive, bounded, integrable and .

-

(H2)

The kernel function integrates to and takes one of the two following forms,

where is a bounded function of bounded variation. The sequence is such that , .

Whereas (H1) and (H2) are rather classical in the kernel smoothing littereature (see the remarks just below Theorem 2), the following assumption is specific to our approach. We shall see in Section 3.2 that this is satisfied for densities with classical tails.

-

(H3)

The function is bounded, integrable, and satisfies . There exist and such that as . For any , , there exists such that, as ,

For the sake of clarity, the (classical) assumptions dealing with the parametric model are postponed to the appendix: (A1) and (A2). They are taken from the monographs [48] and [31], and they mainly ensure the asymptotic normality of whenever .

Theorem 2.

Appendix B is dedicated to the proof of Theorem 2. We did not follow the approach used in [33], which, we believe, is unsatisfactory because they do not consider the case when lies in the border of . Actually, this is not straightforwardly remedied as the event or has a non-negligible probability (as illustrated in the numerical experiments in section 4.1). The smoothness assumption stated in (H1) and the symmetries in the kernel function ensure a control of order of the bias , uniformly in (see Lemma B.7 stated in Appendix B.5). Such a rate could be improved by using higher order kernels but this is not necessary here. Assumption (H2), (a) and (b), are borrowed from the empirical process literature; see among others [32, 15, 11]. They permit to bound, uniformly in , the variance term . The fact that the kernel has a compact support can be alleviated at the price of additional technicalities in the proof and assuming that the tails of the kernel are light enough. We did not include this analysis in the paper for reasons of clarity.

For any dimension , there exists a couple of sequences that fulfills the restrictions (i), (ii) of Theorem 2 and (H2). For instance, the optimal bandwidth , which minimizes the asymptotic mean integrated squared error [51, equation (2.5)], and , is one such sequence. This means that, in practice, one can choose the bandwidth according to the various methods of the literature, see e.g. [42].

An interesting point in Theorem 2 is the two opposite roles played by the sequence in (i) and (ii), respectively. The consistency when requires to be as small as possible whereas when , must not be too close to . In the proof, the case (leave-one-out) as well as (OS method) need to be excluded, suggesting that these other options are not consistent under our set of assumptions.

3.2 Distributions and bandwidth sequences satisfying (H3)

For densities with unbounded supports, the verification of Assumption (H3) only depends on some tail function associated to the density . The meaning of this is made precise in the following proposition.

Proposition 3.

Suppose that for any , and that there exists a function such that as . Suppose that obeys . If there exist and such that

and if for any , , there exists , such that

| (4) |

as , then (H3) is valid for with the same value of .

The proof of Proposition 3 is given in Appendix A. The function in Proposition 3, not necessarily a proper density function, represents the rate of decrease of as .

Example 1 (Mixture of densities).

Let . Let , , , , where and are densities such that as . Take . Then, as ,

Hence the verification of (H3) by only depends on the component .

Putting (the symbol stands for proportionality) in Proposition 3 amounts to check (H3) directly, which is done in the following examples.

Example 2 (Gaussian tails).

Example 3 (Exponential tails).

Example 4 (Polynomial tails).

Let and with , . For simpicity, as in the Gaussian example, we focus on . We find that . For , we have

Finally, since , a sufficient condition on guaranteeing (4) is that .

The three examples considered above are informative on the interplay between the tails of and the choice of . For distribution with light enough tails, including Gaussian, exponential and polynomials with , the conditions on required by (H3) are already fulfilled when assuming (H2). Consequently, the optimal bandwidth which has order is included by our set of assumptions. In contrast, as soon as in the polynomial case, we have the additional condition that .

4 Numerical illustrations

In all the simulation experiments, we have set

, and where is the density of a Student-t distribution with degrees of freedom, and . With such a large variance and heavy tails, this choice of is non informative. We made and vary but the results were very similar, suggesting that the choice for has little effect in practice (at least for light-tailed distribution). In all the experiments but those in Section 4.1, the bandwidth was chosen according to the well known rule of thumb given in [42] (p. 48, equation (3.31)). The choice of the bandwidth is discussed in Section 4.1. In Section 4.2, we study the behavior of the fitness coefficient and the performance

of the estimators with respect to the amount of evidence of the model.

In Section 4.3, we use the LR method for protection against misspecification.

All the numerical experiments were carried out with the R software.

4.1 Sensitivity to the bandwidth: comparison of the fitness coefficient and the OS coefficient

In this section, we study how a change in the bandwidth affects the fitness coefficient and the OS coefficient. We reanalyze the data of Olkin and Spiegelman [33], consisting of yearly wind speed maxima taken in the north direction in Sheridan, Wyoming. There are 20 observations for the years 1958 to 1977: 70, 61, 61, 60, 61, 63, 61, 67, 61, 62, 47, 67, 61, 49, 55, 65, 57, 51, 47, 56. The parametric model is a Gumbel model, that is, , where , is a real location parameter and a dispersion parameter obeying and , where is the Euler-Mascheroni constant. The maximum likelihood estimator is given by .

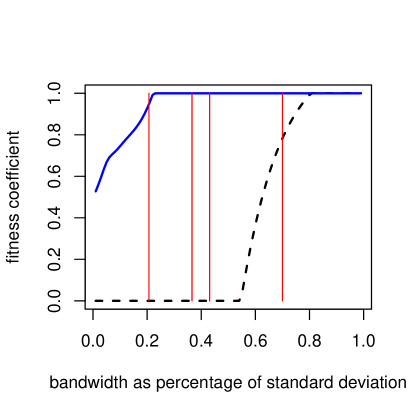

Let denote the bandwidth. In [33], it was arbitrarily chosen , where is the standard deviation of the data. This yields . But if or then one gets . All the above values for are grounded by well-known bandwidth selection methods, see the textbook [42] (p. 47, eqn (3.30) and p. 48, eqn (3.31)) and [41]. By contrast, the fitness coefficient yields . These findings are summarized in Figure 2 LABEL:sub@fig:subfig:robustness , where the coefficients are represented as functions of . We see that the OS coefficient is sensitive to the choice of the bandwidth: a slight difference in can yield a large difference in especially in the range . On the opposite, the fitness coefficient is more robust: the estimated value for remains close to one in a large range for . In Figure 2 LABEL:sub@fig:subfig:robustness, the fitness coefficient and the OS coefficient contradict each other and no more credit can be given to any one of them because the ground truth is unknown.

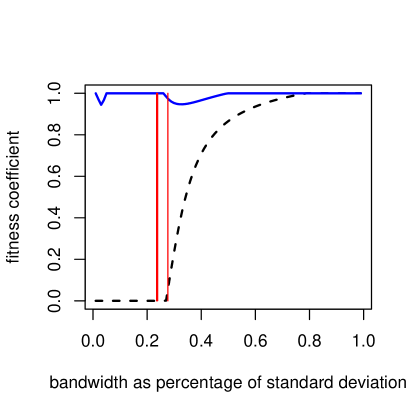

To observe the behavior of the coefficients when the model is known to be true, we simulated observations according to a Gumbel distribution with mean and standard deviation equal to those of the wind speed data, that is, 59.1 and 6.55 respectively. The results are shown in Figure 2 LABEL:sub@fig:subfig:touchup. One has whatever while for all chosen by the bandwidth selection methods of the literature. These results tend to indicate that the fitness coefficient is consistent but the OS coefficient is not. Let us note that Figure 2 LABEL:sub@fig:subfig:robustness and LABEL:sub@fig:subfig:touchup are similar, making the Gumbel model plausible. The difference spotted in the range can be explained by the ties of the wind speed data. (When is small, one can see that (1) is close to the likelihood of a Bernouilli trials experiment, the maximizer of which is given by the proportion of untied observations, here one half.)

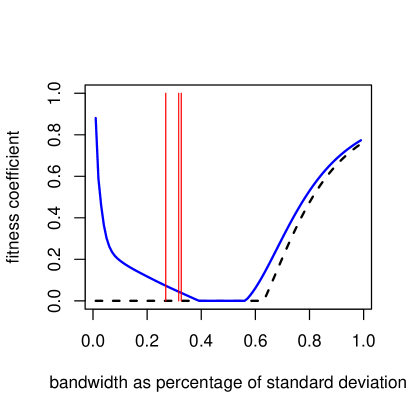

Whenever the model is wrong, we found on simulations that for most reasonable (that is, found in the literature as above) values of , the values of the coefficients are close to zero, as expected. This is illustrated in Figure 2 LABEL:sub@fig:subfig:touchdown: the model is still Gumbel, but the data points were generated according to a Gaussian distribution with mean 59.1 and standard deviation 6.55.

4.2 Performance of the methods when the model and the truth intertwine

Parametric estimators perform better than kernel density estimators when the model is approximately true, but worse otherwise. Can the semiparametric combination be uniformly best? Does the fitness coefficient goes to unity as the model approaches the truth?

To get some insight, the following numerical experiment was done. We generated samples of size according to a density , for several values in a certain index set, representing the “distance” between and the model. Two settings have been tested.

- Setting 1

-

The parametric model is given by and the curve of true distributions is given by . The intersection between the model and the family is given by ; that is, .

- Setting 2

-

The parametric model is given by and the curve of true distributions is given by . The intersection between the model the family is given by a as well.

For each , we compute the maximum likelihood estimator, the standard kernel density estimator, the fitness coefficient, the OS coefficient, and the semiparametric density estimator. The semiparametric density estimator is the combination between the maximum likelihood estimator and the kernel density estimator where the mixing coefficient can be either the fitness coefficient (LR method) or the OS coefficient (OS method). To assess the performances of the estimators, we compute the L2-distance to . The above procedure is repeated 500 times so that the errors are averaged over the repetitions.

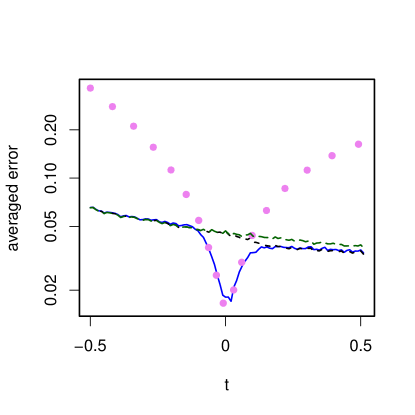

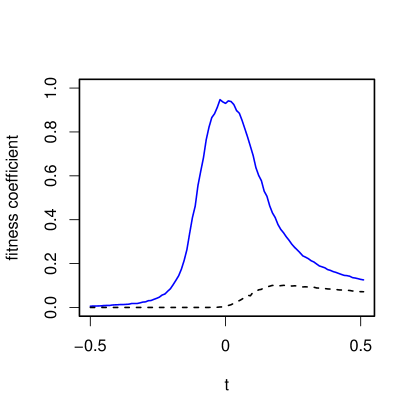

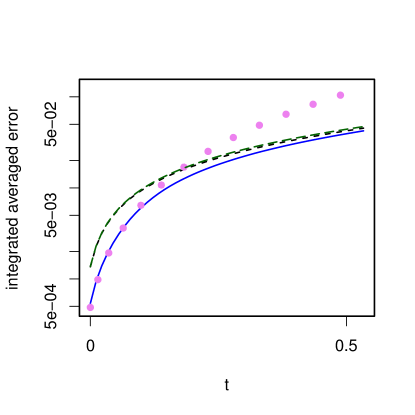

Figure 3 summarizes the results for the first setting. The errors for the parametric estimator, shown in Figure 3 LABEL:sub@fig:subfig:errors-n400nrep500setting1seed1, shrink sharply as the model and the truth intersect. The error for the nonparametric estimator is approximately constant. We see that the OS method performs poorly: it fails to give accurate estimates near the truth. This behavior is explained in Figure 3 LABEL:sub@fig:subfig:mixingCoefficients-n400nrep500setting1seed1, where we see that the values of the OS coefficient barely exceed 0.1. This is not the case for the fitness coefficient; the values stretch entirely the range and are consistent with the proximity between the truth and the parametric model. As a consequence, coming back to Figure 3 LABEL:sub@fig:subfig:errors-n400nrep500setting1seed1, the error of the LR method is near the minimum of the parametric and nonparametric errors. This means that, in practice, however close our parametric model is to the truth, we never lose by choosing the LR method. Even more interestingly is the fact that in the region where the parametric and the nonparametric estimators perform similarly, the LR method performs better: this corresponds to the values and . This fact is clearly seen in Figure 3 LABEL:sub@fig:subfig:integratedErrors-n400nrep500setting1seed1 which pictures the averaged error integrated in the interval : the LR method always has the lowest curve.

The results for and for setting 2 are similar and not shown here to limit the length of the paper.

4.3 Application to multivariate density estimation

It is well known that building accurate multivariate parametric models is an uncertain and difficult task. One way of addressing this problem consists of decomposing the target density into a copula and the marginal densities , that is,

(here the stand for the distribution functions). This decomposition, also known as Sklar’s theorem, is unique provided that the are continuous; for more details about copulas, see e.g. [13] or the books [30, 22]. The copula is assumed to belong to a parametric model and the true underlying parameter is estimated [14] by

where is the rank of among and stands for the -th coordinate of the -th observation. The marginals are estimated in a separate step. If one of the marginals is misspecified, the estimation of the joint distribution is biased. In the following, a computer experiment illustrates that the LR method can help to reduce this bias by avoiding misspecification.

We have generated datasets of size with a copula of the form (a so-called Gumbel copula)

| (5) |

with and marginals , where is an exponential distribution with mean and is a Weibull distribution with shape and scale , that is,

For each of the simulated datasets, the copula parameter was estimated as mentioned above and the marginals were estimated under three scenarios. In the first scenario we estimate them nonparametrically with the standard kernel density estimator. In the second scenario we do as if both marginals were exponentially distributed and compute the maximum likelihood estimator. In the third scenario we form the convex combination with the maximum likelihood estimator and the standard kernel density estimators, where the mixing coefficient is the fitness coefficient (LR method).

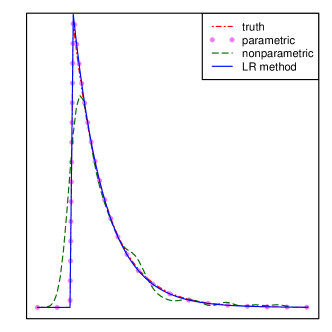

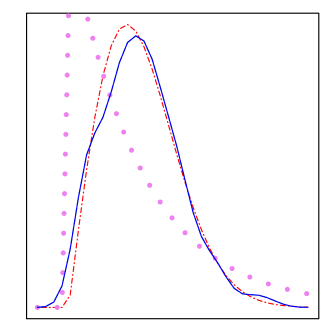

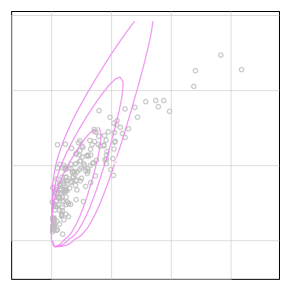

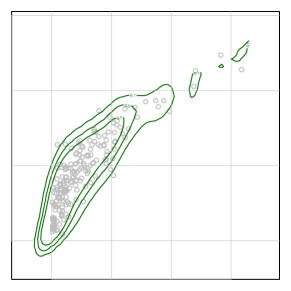

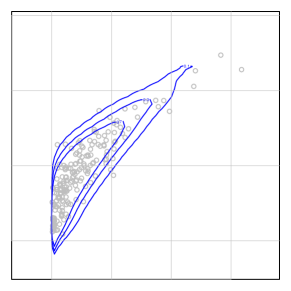

The results for and marginal estimation are shown in Figure 4. Figure 4 LABEL:sub@fig:subfig:n200-script4-marginal1 pictures the estimated densities with the parametric, nonparametric and semiparametric methods for the first marginal, that is, when the parametric model is well specified. We see only two lines because the parametric, semiparametric and the true densities are very similar, indicating that . Figure 4 LABEL:sub@fig:subfig:n200-script4-marginal2 corresponds to the misspecified second marginal. Here this is the nonparametric and the semiparametric estimates which are nearly identical, indicating that .

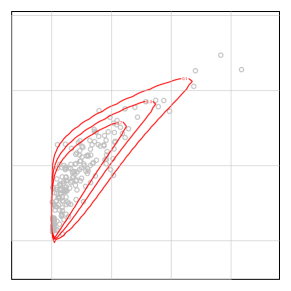

Figure 5 shows the estimation for the bivariate joint density. In Figure 5 LABEL:sub@fig:subfig:n200-script4-para we see that one marginal misspecification led to a poor estimation of the joint density, especially in the joint tails. Figure 5 LABEL:sub@fig:subfig:n200-script4-nonpara shows the estimated joint density with the nonparametric strategy for the marginals. Drawbacks of nonparametric estimation are easily spotted: the estimated density is multimodal and assumes positive values where it should be null. Visually, the best performance is achieved with the semiparametric strategy in Figure 5 LABEL:sub@fig:subfig:n200-script4-semi. The figures for are similar and not shown to limit the length of the paper.

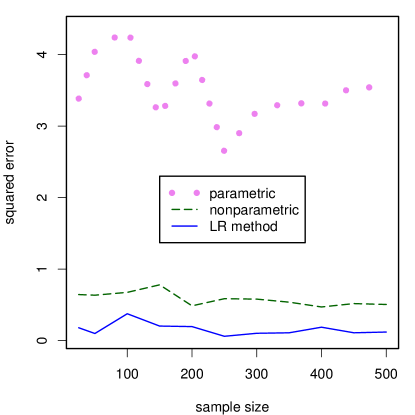

The squared L2-distances between the true joint density and the estimators are shown in Figure 6. The semiparametric strategy performs best for all sample sizes.

Appendix A Proofs of the propositions

We define the mixture likelihood function as

The fitness coeficient in (1) is then defined as a maximizer of over .

A.1 Proof of Proposition 1

The presence of in allows for for all . If for all , , i.e., , then is continuos on and the extreme value theorem yields the existence of . Else, if , there exists such that , meaning that the maximum is over and exists in virtue of the extreme value theorem. Whenever is not identically equal to for all , the function is strictly concave and so comes the unicity.

∎

A.2 Proof of Proposition 3

Let . By assumption, there exists , such that for all , we have

For small enough (i.e., taking any implies that , or equivalently that ), it holds

Consequently, we obtain that .

Suppose that . By enlarging (i.e., taking ), we have, for all and ,

Let and . As soon as ,

Otherwise,

We conclude by remarking that the previous is bounded, by . ∎

Appendix B Proof of Theorem 2

Theorem 2 follows from the application of two high-level results, corresponding respectively to the well-specified and misspecified case. Both high-level results take place in the following general framework: given a triangular sequence of non-negative real numbers , , we consider the mixture likelihood function given by

Here the sequence is left unspecified in order to highlight the assumptions that we need on the nonparametric part. This random sequence could be the non-parametric estimator evaluated at , i.e., , the LOO estimate or the LR estimate with . In this slightly new context, we define as

In both cases, respectively, the misspecified and well-specified case, the approach taken is similar. We compare the empirical likelihood of the mixture to the one of the parametric estimate (in the well-specified case) or the nonparametric estimate (in the misspecified case).

In the proofs below, it is convenient to introduce the normalized version of , given by

where, for any real valued function , we have introduced the short-cut notation for .

B.1 Case (i) : the model is well-specified

We are based on some restricted mean quadratic error

and some averaged linear error

The proof of the following theorem is given in Section B.3.1.

Theorem B.1.

Suppose that and let and be such that for all , . If the following convergences hold in probability, as ,

| (6) | ||||

| (7) |

then, as , in probability.

We now verify the conditions of the previous theorem when is the LR sequence and when (H1), (H2), (H3), (A1), (A2) and are fulfilled.

Condition (6).

The first convergence in (6) holds in virtue of (21) established in Section C. For the second one, it holds that

Applying the first statement of Proposition C.1 in [35] (which is a consequence of Theorem 2.1 in [15]), we have, under (H1) and (H2), that

Together with Lemma B.9, we obtain that . Consequently, we get

| (8) |

The latter bound indeed goes to , in probability, as .

Condition (7).

We proceed as follows, with :

B.2 Case (ii) : the model is misspecified

When the model is misspecified, i.e., , the following high-level conditions are enough to ensure the convergence in probability . These conditions are easily implied by (A1), (H1), (H2), (H3) and as demonstrated below. The proof of this theorem is given in Section B.3.2.

Theorem B.2.

Suppose that and , that the class is Glivenko-Cantelli (i.e., (20) holds) with compact, that the envelop is such that , and that for every , is a continuous function defined on . Suppose that there exists and such that, as , , and such that , a.s., and

then, , as , in probability.

B.3 Proofs of the high-level Theorems

B.3.1 Proof of Theorem B.1

Because , it holds that for all , which guarantees the existence of a maximizer (as explained in the proof of Proposition 1). By definition of , . Consequently, and for every , the event implies that . Thus, let , the proof will be completed by showing that with probability going to ,

A useful notation in the following is

A useful technical detail is there exists a sequence such that the event

has probability going to as . This is a consequence of (6). As we are establishing a result in probability, we can further suppose that this event is realized.

A key step in our approach is the following inequality, reminiscent of the Taylor development of the logarithm around ,

which might be derived by studying the concerned function. This kind of inequality is commonly used for studying likelyhood methods [16, 28]. Applied to , it gives

Note that whenever , because it holds , we have (for small enough) that . This means that, for all , , and it follows

where

Bounding the right-hand side with respect to gives

By assumption, we have that in probability. From the Cauchy-Schwartz inequality we get that , leading to , in probability. Consequently, we obtain that

The term between brackets goes to , in probability, implying that for every , with probability going to ,

Hence it remains to note that, by (7), with probability going to , .

∎

B.3.2 Proof of Theorem B.2

Note that exists because for all , as explained in the proof of Proposition 1. Let . The proof requires to show that with probability going to , . This event is realized as soon as . We analyse both terms separately. First we show that

in probability, and then that there exists such that, with probability going to ,

| (9) |

Let , and . We assume further that and . We have

The expectation of the term in the middle is bounded by of order , by assumption. The corresponding term goes to , as is arbitrarily small. The expectation of the term in the right is smaller than , which goes to because and are integrable. Hence it remains to obtain that the term in the left goes to . The mean-value theorem gives

Now we establish (9) by obtaining one-sided inequalities. Take , suppose that , and use the monotonicity of the logarithm, to get that

Taking the expectation, we find a bound in which goes to as in virtue of the Lebesgue dominated convergence theorem. Then, taking , it holds that

The first term in the right-hand side is decomposed according to

By the mean value theorem, the term on the left is bounded by

which goes to , by assumption. For the term on the right, notice that is Glivenko-Cantelli with envelop . Then applying Theorem 3 in [47], the class formed by is still Glivenko-Cantelli. Since for all , ,

the function is an integrable envelop. Using again Theorem 3 in [47], the class formed by , , , , is still Glivenko-Cantelli with the same envelop. This implies that

The integrability of the envelop and the fact that implies that

It remains to use the inequality to obtain that

where . Since

we get, using that , , ,

Using standard results about the Hellinger distance [34] (chapter 3) we obtain

Since and by the continuity assumption on , it holds that . Then, as is arbitrary, the proof of (9) is complete.

∎

B.4 Linear and quadratic error of parametric and nonparametric estimate

Important tools for dealing with the terms involving are coming from -statistic theory. We call -statistic of order with kernel , any quantity of the kind

where the summation is taken over the subset formed by the such that , . The number of terms in the summation is then . When the kernel is such that, for every , , it is called a degenerate -statistic. In the proofs, we shall rely on the so-called Hajek decomposition [48, Lemma 11.11].

To establish the two following lemmas, Lemma B.3 and Lemma B.4, we are based on (H1), (H2) and (H3). One might note that the expressions (a) or (b) in (H2) on the kernel are not used in any of these lemmas.

Lemma B.3.

Proof.

Note that

The proof follows from the decomposition

where

We will show that , in probability and that , in probability. This will be enough as , almost surely.

Proof that in probability.

Introduce the notation, for any ,

Developing, we find

where is as short-cut for . We treat relying on the Hajek projection of -statistics. Up to a centering term, , the -statistic is a degenerate -statistic. In the following we voluntary introduce this centering term in the summation to handle separately a degenerate U-statistic and another summation with less indices. By introducing, for any ,

we obtain

| (10) |

Treatment of the first term in (10). Note that defines a degenerate -statistic, i.e.,

Note that

where is the symmetrized version of , i.e., for any triplet of where the sum is over all the possible permutations of the set . Using that the -statistic with kernel is degenerate, some algebra gives that

We have, using Minkowski’s inequality and the definition of the conditional expectation, that

Consequently, in virtue of (15) in Lemma B.7, we have shown that

The previous rate, multiplied by , goes to , hence, this term is negligible.

Treatment of the second term in (10). We continue the study of by considering

The first term is a degenerate -statistic of order whose order moments satisfy

This is obtained by following exactly the same lines as in the treatment of the -statistic and using (18) in Lemma B.7. As , the previous term is negligible. The second term is a sum of centred independent random variables with variance smaller than, in virtue of (14) in Lemma B.7,

This is the same rate as the rate obtained for the (negligible) -statistic of order with kernel .

Treatment of the third term in (10). The study of continues by considering

The term associated with double summation over and is a degenerate -statistic, as . Consequently, following the same lines as in the treatment of the first term of , and using (19) in Lemma B.7, we get

which goes to , when multiplied by . The remaining term is a sum of independent and identically distributed random variables. We have, by computing the variance of the centred average,

where the first term, using (17) in Lemma B.7, is which goes to when multiplied by . The dominating term is in fact the last one, as by Lemma B.8, it holds that .

Proof that in probability.

We are based on similar decompositions as for involving -statistics. Let and note that in virtue of Lemma B.9, it holds

Then

with . The term on the left is a degenerate -statistic for which it holds

Using (13) in Lemma B.7 and the previous bound for , we find

where is defined in (12). The previous bound multiplied by goes to . Using that and (16), the variance of the term on the right in is smaller than

which, multiplied by , goes to by hypothesis. Hence , in probability and the proof is complete. ∎

Proof.

The decomposition is as follows

| (11) |

The expectation of the last term is which goes to by assumption. We can now focus on the first and second term of the decomposition.

Treatment of the second term in (11). Using that , the considered term is a centred empirical sum. Using Lemma B.9, its variance is then bounded by

which goes to .

Treatment of the first term in (11). Using that , one can verify that it is a degenerate -statistic. Here the variance can not be computed directly because the leading term is not necessarily finite. Hence we decompose according to the in and the others, with where is given in (H3) and . We introduce

and define the linear operator as

Because for all , one sees that

Because the summation over is a degenerate -statistics, we get that

Defining the kernel and , we obtain

For the term with , we obtain that

From Lemma B.10, we deduce that . To conclude, we have shown that there exists a constant such that

Invoking (H3) and because is arbitrarily small, the limit as is . ∎

Proof.

Proof.

In virtue of (A2), the map is differentiable at , for -almost every with derivative (this is obtained in [48], in the proof of Theorem 5.39). Using stability properties for the composition, the map is differentiable at , for -almost every with derivative . We are in position to apply Lemma 19.31 in [48], with and . From the mentioned lemma, as is tight, defining

we obtain

Actually, recalling that , we find that, for all , . Hence, we obtain

where the first term is a . ∎

B.5 Auxiliary results

Recall some definitions, for any ,

| (12) | ||||

as well as the short-cut for .

Lemma B.7.

Proof.

Remark that because is bounded and , we have , for any . Note that, for every ,

We obtain (14) by writing

To establish (15), note that

For (16), write

Inequality (17) follows from the lines

To show (18), write

Using that , we obtain

For (19), we have

We develop and compute bounds for each term. The larger term will be the one associated with the product of the kernels. We have, by Jensen’s inequality, for any ,

Then we obtain

Moreover, as

and

we finally obtain the result. ∎

Proof.

Write

The right-hand side is bounded by , hence its participation in the stated limit is . For the left-hand side term, use and write

It remains to note that the term in the right goes to , as , in virtue of the Lebesgue dominated convergence theorem. ∎

Proof.

Appendix C Parametric maximum likelihood estimator

In this section are reported some classical results on the maximum likelihood estimator of the density. When the model is well-specified, we need the consistency and the asymptotic normality of the estimated parameter .

-

(A1)

The set is compact. The model , a collection of densities on , is identifiable, i.e., for every in , and the envelop is such that . There exists an -valued measurable function with for every , for every and in ,

There exists such that the function is bounded.

It follows from (A1) that the class of functions is Glivenko-Cantell [49, Theorem 2.7.11], i.e.,

| (20) |

Whenever , it holds that , in probability [31, Theorem 2.1] or [48, Lemma 5.35]. For now, asking the above Lipschitz condition to guarantee the Glivenko-Cantelli might seem a bit restrictive [31, Lemma 2.4], but this condition will also be required to derive asymptotic normality of as well as to obtain uniform convergence (over ) of to . Indeed, we have that for any , with probability going to , . Hence, using the mean-value theorem, we find

| (21) |

for every . Conclude using that is bounded and the convergence in probability of to .

-

(A2)

The true parameter an interior point of . The model is differentiable in quadratic mean at , i.e., there exists a measurable vector-valued function , with , such that

The matrix is invertible.

As a consequence of the previous set of conditions [48, Lemma 5.39], we have

| (22) |

where . In particular, it holds that .

Acknowledgments.

The authors are grateful to Ingrid Van Keilegom, Anouar El Ghouch and Sylvie Huet for useful comments and references. The authors are also grateful to Christian Robert for some motivating remarks at the very beginning of this work.

References

- [1] H. Akaike. A new look at the statistical model identification. Automatic Control, IEEE Transactions on, 19(6):716–723, 1974.

- [2] M. G. Akritas. Pearson-type goodness-of-fit tests: the univariate case. Journal of the American Statistical Association, 83(401):222–230, 1988.

- [3] N. H. Anderson, P. Hall, and D. M. Titterington. Two-sample test statistics for measuring discrepancies between two multivariate probability density functions using kernel-based density estimates. Journal of Multivariate Analysis, 50(1):41–54, 1994.

- [4] K. P. Burnham and D. R. Anderson. Model selection and multimodel inference: a practical information-theoretic approach. Springer Science & Business Media, 2003.

- [5] S. X. Chen and I. Van Keilegom. A goodness-of-fit test for parametric and semi-parametric models in multiresponse regression. Bernoulli, 15(4):955–976, 2009.

- [6] G. Claeskens and N. L. Hjort. Goodness of fit via non-parametric likelihood ratios. Scandinavian Journal of Statistics, 31(4):487–513, 2004.

- [7] G. Claeskens and N. L. Hjort. Model selection and model averaging, volume 330. Cambridge University Press Cambridge, 2008.

- [8] R. B. D’Agostino and M. A. Stephens. Goodness-of-Fit Techniques. Marcel Dekker Inc., New York, 1986.

- [9] M. Delecroix, M. Hristache, and V. Patilea. On semiparametric M-estimation in single-index regression. Journal of Statistical Planning and Inference, 136(3):730–769, 2006.

- [10] J. Durbin. Weak convergence of the sample distribution function when parameters are estimated. The Annals of Statistics, 1(2):279–290, 1973.

- [11] U. Einmahl and D. M. Mason. An empirical process approach to the uniform consistency of kernel-type function estimators. J. Theoret. Probab., 13(1):1–37, 2000.

- [12] J. Faraway. Implementing semiparametric density estimation. Statistics and Probability Letters, 10(2):141–143, 1990.

- [13] C. Genest and A. Favre. Everything you always wanted to know about copula modeling but were afraid to ask. Journal of Hydrologic Engineering, 12(4):347–368, 2007.

- [14] C. Genest, K. Ghoudi, and L. P. Rivest. A semiparametric estimation procedure of dependence parameters in multivariate families of distributions. Biometrika, 82(3):543–552, 1995.

- [15] E. Giné and A. Guillou. Rates of strong uniform consistency for multivariate kernel density estimators. Ann. Inst. H. Poincaré Probab. Statist., 38(6):907–921, 2002.

- [16] U. Grenander. Abstract inference. John Wiley & Sons, Inc., New York, 1981.

- [17] J. Habbema, J. D. F. Hermans and K. Van Den Broeck. A stepwise discriminant analysis program using density estimation. Physica Verlag, Vienna, 1974.

- [18] P. Hall. On Kullback-Leibler loss and density estimation. The Annals of Statistics, 15(4):1491–1519, 1987.

- [19] N. L. Hjort and M. C. Jones. Locally parametric nonparametric density estimation. The Annals of Statistics, pages 1619–1647, 1996.

- [20] N. L. Hjort, I. W. McKeague, and I. Van Keilegom. Hybrid combinations of parametric and empirical likelihoods. To appear in statistica sinica, 2017.

- [21] M. a. D. Jiménez-Gamero and J. C. Pardo-Fernández. Empirical characteristic function tests for GARCH innovation distribution using multipliers. J. Stat. Comput. Simul., 87(10):2069–2093, 2017.

- [22] H. Joe. Dependence Modeling with Copulas. Chapman & Hall, 2014.

- [23] K. Kamary, K. Mengersen, C. P. Robert, and J. Rousseau. Testing hypotheses via a mixture estimation model. arXiv preprint arXiv:1412.2044, 2014.

- [24] I. Kojadinovic and J. Yan. Goodness-of-fit testing based on a weighted bootstrap: a fast large-sample alternative to the parametric bootstrap. Can J Statistics, 40(3):480–500, 2012.

- [25] S. S. M. Lee and M. Soleymani. A simple formula for mixing estimators with different convergence rates. Journal of the American Statistical Association, 110(512):1463–1478, 2015.

- [26] J. S. Marron. An asymptotically efficient solution to the bandwidth problem of kernel density estimation. The Annals of Statistics, 13(3):1011–1023, 1985.

- [27] J. S. Marron. A comparison of cross-validation techniques in density estimation. The Annals of Statistics, 15(1):152–162, 1987.

- [28] S. A. Murphy. Consistency in a proportional hazards model incorporating a random effect. The Annals of Statistics, 22(2):712–731, 1994.

- [29] P. A. Murtaugh. In defense of p values. Ecology, 95(3):611–617, 2014.

- [30] R. B. Nelsen. An introduction to copulas. Springer, 2006.

- [31] W. K. Newey and D. McFadden. Large sample estimation and hypothesis testing. Handbook of econometrics, 4:2111–2245, 1994.

- [32] D. Nolan and D. Pollard. -processes: rates of convergence. The Annals of Statistics, 15(2):780–799, 1987.

- [33] I. Olkin and C. H. Spiegelman. A semiparametric approach to density estimation. Journal of the American Statistical Association, 82(399):858–865, 1987.

- [34] D. Pollard. Asymptopia. Unpublished book, 2000.

- [35] F. Portier and J. Segers. On the weak convergence of the empirical conditional copula under a simplifying assumption. arXiv preprint arXiv:1511.06544, 2015.

- [36] M. Rahman, R. J. Beaver, and D. V. Gokhale. A note on estimating the combining constant in semiparametric density estimation. Brazilian Journal of Probability and Statistics, 11(1):37–50, 1997.

- [37] M. Rudemo. Empirical choice of histograms and kernel density estimators. Scandinavian Journal of Statistics, 9(2):65–78, 1982.

- [38] M. J. Schervish. P values: what they are and what they are not. The American Statistician, 50(3):203–206, 1996.

- [39] E. F. Schuster and G. G. Gregory. On the nonconsistency of maximum likelihood nonparametric density estimators. In Computer Science and Statistics: Proceedings of the 13th Symposium on the Interface, pages 295–298. Springer, 1981.

- [40] G. Schwarz. Estimating the dimension of a model. The Annals of Statistics, 6(2):461–464, 1978.

- [41] S. J. Sheather and M. C. Jones. A reliable data-based bandwidth selection method for kernel density estimation. Journal of the Royal Statistical Society series B, 53(3):683–690, 1991.

- [42] B. W. Silverman. Density estimation for statistics and data analysis. Chapman & Hall, 1998.

- [43] M. Soleymani and S. M. S. Lee. A bootstrap procedure for local semiparametric density estimation amid model uncertainties. Journal of Statistical Planning and Inference, 153:75–86, 2014.

- [44] C. J. Stone. An asymptotically optimal window selection rule for kernel density estimates. The Annals of Statistics, 12(4):1285–1297, 1984.

- [45] W. Stute, W. G. Manteiga, and M. P. Quindimil. Bootstrap based goodness-of-fit-tests. Metrika, 40(1):243–256, 1993.

- [46] M. Talamakrouni, A. El Ghouch, and I. Van Keilegom. Parametrically guided local quasi-likelihood with censored data. Electronic Journal of Statistics, 11(2):2773–2799, 2017.

- [47] A. van der Vaart and J. A. Wellner. Preservation theorems for Glivenko-Cantelli and uniform Glivenko-Cantelli classes. In High dimensional probability II, pages 115–133. Springer, 2000.

- [48] A. W. van der Vaart. Asymptotic statistics. Cambridge University Press, Cambridge, 1998.

- [49] A. W. van der Vaart and J. A. Wellner. Weak convergence and empirical processes. With applications to statistics. Springer-Verlag, New York, 1996.

- [50] Q. H. Vuong. Likelihood ratio tests for model selection and non-nested hypotheses. Econometrica, 57(2):307–333, 1989.

- [51] M. P. Wand and M. C. Jones. Multivariate plug-in bandwidth selection. Computational Statistics, 9(2):97–116, 1994.

- [52] R. L. Wasserstein and N. A. Lazar. The ASA’s statement on p-values: context, process, and purpose, 2016.