[table]capposition=top \newfloatcommandcapbtabboxtable[][\FBwidth]

A Generalized Matrix Splitting Algorithm

Abstract

Composite function minimization captures a wide spectrum of applications in both computer vision and machine learning. It includes bound constrained optimization, norm regularized optimization, and norm regularized optimization as special cases. This paper proposes and analyzes a new Generalized Matrix Splitting Algorithm (GMSA) for minimizing composite functions. It can be viewed as a generalization of the classical Gauss-Seidel method and the Successive Over-Relaxation method for solving linear systems in the literature. Our algorithm is derived from a novel triangle operator mapping, which can be computed exactly using a new generalized Gaussian elimination procedure. We establish the global convergence, convergence rate, and iteration complexity of GMSA for convex problems. In addition, we also discuss several important extensions of GMSA. Finally, we validate the performance of our proposed method on three particular applications: nonnegative matrix factorization, norm regularized sparse coding, and norm regularized Dantzig selector problem. Extensive experiments show that our method achieves state-of-the-art performance in term of both efficiency and efficacy.

Index Terms:

Matrix Splitting Algorithm, Nonsmooth Optimization, Convex Optimization, Convergence Analysis.1 Introduction

In this paper, we focus on the following composite function minimization problem:

| (1) |

where , is a symmetric positive semidefinite matrix, and is a piecewise separable function (i.e. ) but not necessarily convex. Typical examples of include the bound constrained function and the and norm functions. We assume that is bounded below for any feasible solution .

The optimization in (1) is flexible enough to model a variety of applications of interest in both computer vision and machine learning, including compressive sensing [9], nonnegative matrix factorization [20, 22, 11], sparse coding [21, 1, 2, 35], support vector machine [15], logistic regression [47], subspace clustering [10], to name a few. Although we only focus on the quadratic function , our method can be extended to handle general non-quadratic composite functions by considering a Newton approximation of the objective [42, 50] and to solve general linear constrained problems by using its associated augmented Lagrangian function of the problem [12, 13].

The most popular method for solving problem (1) is perhaps the proximal gradient method [31, 3]. It considers a fixed-point proximal iterative procedure based on the current gradient . Here the proximal operator can often be evaluated analytically, is the step size with being the local (or global) Lipschitz constant. It is guaranteed to decrease the objective at a rate of , where is the iteration number. The accelerated proximal gradient method can further boost the rate to . Tighter estimates of the local Lipschitz constant leads to better convergence rate, but it scarifies additional computation overhead to compute . Our method is also a fixed-point iterative method, but it does not rely on a sparse eigenvalue solver or line search backtracking to compute such a Lipschitz constant, and it can exploit the specified structure of the quadratic Hessian matrix .

The proposed method is essentially a generalization of the classical Gauss-Seidel (GS) method and Successive Over-Relaxation (SOR) method [8, 37]. In numerical linear algebra, the Gauss-Seidel method, also known as the successive displacement method, is a fast iterative method for solving a linear system of equations. It works by solving a sequence of triangular matrix equations. The method of SOR is a variant of the GS method and it often leads to faster convergence. Similar iterative methods for solving linear systems include the Jacobi method and symmetric SOR. Our proposed method can solve versatile composite function minimization problems, while inheriting the efficiency of modern linear algebra techniques.

Our method is closely related to coordinate gradient descent and its variants such as randomized coordinate descent [15, 34], cyclic coordinate descent [39], block coordinate descent [30, 4, 14], randomized block coordinate descent [36, 26], accelerated randomized coordinate descent [30, 23, 25] and others [24, 18, 52]. However, all these work are based on gradient-descent type iterations and a constant Lipschitz step size. They work by solving a first-order majorization/surrogate function via closed form updates. Their algorithm design and convergence result cannot be applied here. In contrast, our method does not rely on computing the Lipschicz constant step size, yet it adopts a triangle matrix factorization strategy, where the triangle subproblem can be solved by an alternating cyclic coordinate strategy.

We are aware that matrix splitting algorithm has been considered to solve symmetric linear complementarity problems [27, 28, 17] and second-order cone complementarity problems [53] in the literature. However, we focus on minimizing a general separable nonsmooth composite function which is different from theirs. In addition, our algorithm is derived from a novel triangle operator mapping, which can be computed exactly using a new Gaussian elimination procedure. It is worthwhile to mention that matrix splitting has been extended to operator splitting recently to solve multi-term nonsmooth convex composite optimization problems [38].

Contributions. (i) We propose a new Generalized Matrix Splitting Algorithm (GMSA) for composite function minimization (See Section 2). Our method is derived from a novel triangle proximal operator (See Subsection 2.1). We establish the global convergence, convergence rate, and iteration complexity of GMSA for convex problems (See Subsection 2.2). (ii) We discuss several important extensions of GMSA (see Section 3). First, we consider a new correction strategy to achieve pointwise contraction for the proposed method (See Subsection 3.1). Second, we discuss using Richardson extrapolation technique to further accelerate GMSA (See Subsection 3.2). Third, we extend GMSA to solve nonconvex problems with global convergence guarantee (See Subsection 3.3). Fourth, we discuss how to adapt GMSA to minimize non-quadratic functions (See Subsection 3.4). Fifth, we show how to incorporate GMSA into the general optimization framework of Alternating Direction Method of Multipliers (ADMM) (See Subsection 3.5). (iii) Our extensive experiments on nonnegative matrix factorization, sparse coding and Danzig selectors have shown that GMSA achieves state-of-the-art performance in term of both efficiency and efficacy (See Section 4). A preliminary version of this paper appeared in [49].

Notation. We use lowercase and uppercase boldfaced letters to denote real vectors and matrices respectively. The Euclidean inner product between and is denoted by or . We denote , , and as the spectral norm (i.e. the largest singular value) of . We denote the element of vector as and the element of matrix as . is a column vector formed from the main diagonal of . and indicate that the matrix is positive semidefinite and positive definite, respectively. Here is not necessarily symmetric 111. We denote as a diagonal matrix of and as a strictly lower triangle matrix of 222For example, when , and take the following form:

. Thus, we have . Throughout this paper, denotes the value of at -th iteration if is a variable, and denotes the -th power of if is a constant scalar. We use to denote any solution of the optimal solution set of (1). For notation simplicity, we denote:

2 Proposed Algorithm

This section presents our proposed Generalized Matrix Splitting Algorithm (GMSA) for solving (1). Throughout this section, we assume that is convex and postpone the discussion for nonconvex to Section 3.3.

Our solution algorithm is derived from a fixed-point iterative method based on the first-order optimal condition of (1). It is not hard to validate that a solution is the optimal solution of (1) if and only if satisfies the following nonlinear equation (“” means define):

| (2) |

where and denote the gradient of and the sub-gradient of in , respectively. In numerical analysis, a point is called a fixed point if it satisfies the equation , for some operator . Converting the transcendental equation algebraically into the form , we obtain the following iterative scheme with recursive relation:

| (3) |

We now discuss how to adapt our algorithm into the iterative scheme in (3). First, we split the matrix in (2) using the following strategy:

| (4) |

Here, is a relaxation parameter and is a parameter for strong convexity that enforces . These parameters are specified by the user beforehand. Using these notations, we obtain the following optimality condition which is equivalent to (2):

Then, we have the following equivalent fixed-point equation:

| (5) |

For notation simplicity, we denote as since can be known from the context.

We name the triangle proximal operator, which is novel in this paper333This is in contrast with Moreau’s proximal operator [33]: , where the mapping is called the resolvent of the subdifferential operator .. Due to the triangle property of the matrix and the element-wise separable structure of , the triangle proximal operator in (5) can be computed exactly and analytically, by a generalized Gaussian elimination procedure (discussed later in Section 2.1). Our generalized matrix splitting algorithm iteratively applies until convergence. We summarize our algorithm in Algorithm 1.

In what follows, we show how to compute in (5) in Section 2.1, and then we study the convergence properties of Algorithm 1 in Section 2.2.

2.1 Computing the Triangle Proximal Operator

We now present how to compute the triangle proximal operator in (5), which is based on a new generalized Gaussian elimination procedure. Notice that (5) seeks a solution that satisfies the following nonlinear system:

| (6) |

By taking advantage of the triangular form of and the element-wise/decomposable structure of , the elements of can be computed sequentially using forward substitution. Specifically, the above equation can be written as a system of nonlinear equations:

If satisfies the equations above, it must solve the following one-dimensional subproblems:

This is equivalent to solving the following one-dimensional problem for all :

| (7) |

Note that the computation of uses only the elements of that have already been computed and a successive displacement strategy is applied to find .

We remark that the one-dimensional subproblem in (7) often admits a closed form solution for many problems of interest. For example, when with denoting an indicator function on the box constraint , the optimal solution can be computed as: ; when (i.e. in the case of the norm), the optimal solution can be computed as: .

Our generalized Gaussian elimination procedure for computing is summarized in Algorithm 2. Note that its computational complexity is , which is the same as computing a matrix-vector product.

2.2 Convergence Analysis

In what follows, we present our convergence analysis for Algorithm 1.

The following lemma characterizes the optimality of the triangle proximal operator for any .

Lemma 1.

For all , it holds that:

| (8) |

| (9) | ||||

| (10) |

Proof.

(i) Using the optimality of in (6), we derive the following results: , where step uses and step uses the definition of in (2).

(ii) Since is convex, we have:

| (11) |

Letting , we derive the following inequalities: , where step uses (8).

(iii) Since is a quadratic function, we have:

| (12) |

We naturally derive the following results: , where step uses the definition of ; step uses (12) with and ; step uses (9).

∎

Remarks. Both (8) and (9) can be used to characterize the optimality of (1). Recall that we have the following sufficient and necessary conditions for the optimal solution: . When occurs, (8) and (9) coincide with the optimal condition and one can conclude that is the optimal solution.

Theorem 1.

(Proof of Global Convergence) We define and let be chosen such that . Algorithm 1 is globally convergent.

Proof.

(i) First, the following results hold for all :

| (13) |

where we have used the definition of and , and the fact that .

We invoke (10) in Lemma 1 with and combine the inequality in (1) to obtain:

| (14) |

(ii) Second, summing (14) over , we have:

where step uses the fact that . Note that is bounded below. As , we have , which implies the convergence of the algorithm. Invoking (8) in Lemma 1 with , we obtain: . The fact that implies that is the global optimal solution of the convex problem.

Note that guaranteeing can be achieved by simply choosing and setting to a small number. ∎

Remarks. (i) When is empty and , Algorithm 1 reduces to the classical Gauss-Seidel method () and Successive Over-Relaxation method (). (ii) When contains zeros in its diagonal entries, one needs to set to a strictly positive number. This is to guarantee the strong convexity of the one dimensional subproblem and a bounded solution for any in (7). The introduction of the parameter is novel in this paper and it removes the assumption that is strictly positive-definite or strictly diagonally dominant, which is used in the classical result of GS and SOR method [37, 8].

We now prove the convergence rate of Algorithm 1. We make the following assumption, which characterizes the relations between and for any .

Assumption 1.

If is not the optimum of (1), there exists a constant such that .

Remarks. Assumption 1 is similar to the classical local proximal error bound assumption in the literature [29, 42, 41, 51], and it is mild. Firstly, if is not the optimum, we have . This is because when , we have (refer to the optimal condition of in (8)), which contradicts with the condition that is not the optimal solution. Secondly, by the boundedness of and , there exists a sufficiently large constant such that .

We now prove the convergence rate of Algorithm 1.

Theorem 2.

(Proof of Convergence Rate) We define and let be chosen such that . Assuming that is bound for all , we have:

| (15) | |||

| (16) |

where .

Proof.

Invoking Assumption 1 with , we obtain:

| (17) |

We derive the following inequalities:

| (18) | |||

| (19) |

where step uses (10) in Lemma 1 with ; step uses the fact that and ; step uses and the inequality that which is due to (1); step () uses the Cauchy-Schwarz inequality and the norm inequality ; step () uses (17); step uses the descent condition in (14); step uses the definition of .

Rearranging the last inequality in (19), we have , leading to: . Solving this recursive formulation, we obtain (15). In other words, the sequence converges to linearly in the quotient sense. Using (14), we derive the following inequalities: . Therefore, we obtain (16).

∎

The following lemma is useful in our proof of iteration complexity.

Lemma 2.

Suppose a nonnegative sequence satisfies for some constant . It holds that: .

Proof.

The proof of this lemma can be obtained by mathematical induction. We denote . (i) When , we have . (ii) When , we assume that holds. We derive the following results: . Here, step uses ; step uses the inequality that ; step uses .

∎

We now prove the iteration complexity of Algorithm 1.

Theorem 3.

(Proof of Iteration Complexity) We define and let be chosen such that . Assuming that for all , we have:

where , , , and is some unknown iteration index.

Proof.

We have the following inequalities:

| (20) |

where step uses (18); step uses the fact that ; step uses the Cauchy-Schwarz inequality and the norm inequality; step uses the fact that ; step uses (14); step uses the definition of and .

Now we consider the two cases for the recursion formula in (20): (i) for some (ii) for some . In case (i), (20) implies that we have and rearranging terms gives: . Thus, we have: . We now focus on case (ii). When , (20) implies that we have and rearranging terms yields:. Solving this quadratic inequality, we have: ; solving this recursive formulation by Lemma 2, we obtain .

∎

Remarks. The convergence result in Theorem 3 is weaker than that in Theorem 2, however, it does not rely on Assumption 1 and the unknown constant .

We now derive the convergence rate when is strongly convex.

Theorem 4.

(Proof of Convergence Rate when is Strongly Convex) We define and let be chosen such that . Assuming that is strongly convex with respect to such that with and for all , we have:

| (21) | |||

| (22) |

where .

Proof.

We notice that the right-hand side in (4) is concave. Maximizing over , we obtain:

| (24) |

Putting (4) into (4), we further derive the following inequalities:

where step uses the norm inequality ; step uses (14); step uses the definition of . Finally, we obtain: . Solving the recursive formulation, we obtain the result in (21).

Using the similar strategy for deriving (16), we have:

| (25) |

Finally, we derive the following inequalities:

where step uses (4); step uses the fact that ; step uses the norm inequality. Therefore, we obtain:

∎

3 Extensions

This section discusses several extensions of our proposed generalized matrix splitting algorithm.

3.1 Pointwise Contraction via a Correction Strategy

This section considers a new correction strategy to achieve pointwise contraction for the proposed method to solve (1). One remarkable feature of this strategy is that the resulting iterated solutions of always satisfy the monotone/contractive property that for all if is not the optimal solution. We summarize our new algorithm in Algorithm 3.

We provide detailed theoretical analysis for Algorithm 3. The following lemmas are useful in our proof.

Lemma 3.

Assume that is convex. For all , it holds that:

Lemma 4.

Assume . For all , it holds that:

Proof.

Using the variable substitution that , we have the following equivalent inequalities: . Clearly, these inequalities hold since .

∎

The following theorem provides important theoretical insights on choosing suitable parameters to guarantee convergence of Algorithm 3.

Theorem 5.

We define and let be chosen such that . Assuming that is convex and generated by Algorithm 3 is not the optimal solution, we have the following results: (i)

| (27) | |||

(ii) If we choose a global constant , we have and .

(iii) If we choose a local constant , we have .

Proof.

(i) First of all, we derive the following inequalities:

| (28) |

where step () uses the fact that ; step () Lemma 3 with ; step uses the fact that ; step uses Lemma 4. We then have the following results:

where step uses Pythagoras relation that ; step uses the update rule for ; step uses the fact that ; step uses (5); step uses the definition of .

(ii) We have the following inequalities:

| (29) |

where uses the definition of in (27); step uses ; step uses the fact that ; step uses the fact that , which is due to (1). Then we derive the following inequalities:

where step uses (29); step uses the choice that .

(iii) We define . Minimizing the right-hand side of (27) over the variable , we obtain (30).

| (30) |

Setting the gradient of quadratic function to zero, we obtain the optimal solution for . We obtain . Therefore, we have .

∎

Remarks. (i) The iterated solutions generated by Algorithm 3 satisfy the monotone/contractive property. Therefore, the convergence properties in Theorem 5 are stronger than the results in Theorem 2 and Theorem 3. (ii) There are two methods to decide the value of in Algorithm 3. One method is to use the global constant as indicated in part (ii) in Theorem 5, and another method is to use a local constant parameter as shown in part (iii) in Theorem 5. We remark that a local constant is more desirable in practice since it provides a better estimation of the local structure of the problem and does not require any sparse eigenvalue solver.

3.2 Acceleration via Richardson Extrapolation

This subsection discusses using Richardson extrapolation to further accelerate GMSA.

We introduce a parameter and consider the following iterative procedure:

| (31) | ||||

Note that the SOC update rule is not a special case of this formulation. Values of are often used to help establish convergence of the iterative procedure, while values of are used to speed up convergence of a slow-converging procedure which is also known as Richardson extrapolation [43]. Such strategy is closely related to Nesterov’s extrapolation acceleration strategy [3, 31].

The following proposition provides important insights on how to choose the parameter .

Proposition 1.

We define:

The optimal solution of (1) can be computed as . In addition, if , there exists a constant such that .

Remarks. (i) The assumption also implies that is not the optimal solution since it holds that and when is not the optimal solution. (ii) The step size selection strategy is attractive since it guarantees contractive property for . However, it is not practical since the optimal solution is unknown.

In what follows, we consider the following solution. Since is the current available solution which is the closest to , we replace with , and with . We obtain the follow update rule for :

We summarize our accelerated generalized matrix splitting algorithm in Algorithm 4. Note that we set in the first iteration () and introduce two additional parameters and to avoid to become arbitrarily small or large. Since the strategy in (31) is expected to achieve acceleration when , we set and as the default parameters for Algorithm 4.

3.3 When h is Nonconvex

When is nonconvex, our theoretical analysis breaks down in (11) and the exact solution to the triangle proximal operator in (6) cannot be guaranteed. However, our Gaussian elimination procedure in Algorithm 2 can still be applied. What one needs is to solve a one-dimensional nonconvex subproblem in (7). For example, when (e.g. in the case of the norm), it has an analytical solution: ; when and , it admits a closed form solution for some special values [45, 7], such as or .

Our generalized matrix splitting algorithm is guaranteed to converge even when is nonconvex. Specifically, we present the following theorem.

Theorem 6.

(Proof of Global Convergence when is Nonconvex) We define and let be chosen such that . Assuming the nonconvex one-dimensional subproblem in (7) can be solved globally and analytically, we have: (i)

| (34) |

(ii) Algorithm 1 is globally convergent.

Proof.

(i) Due to the optimality of the one-dimensional subproblem in (7), for all , we have:

Letting , we obtain:

Since , we obtain the following inequality:

By denoting and , we have: , , and . Therefore, we have the following inequalities:

where step () uses , since is a Skew-Hermitian matrix; step () uses , since . Thus, we obtain the sufficient decrease inequality in (34).

(ii) Based on the sufficient decrease inequality in (34), we have: is a non-increasing sequence, , and if . We note that (8) can be still applied even is nonconvex. Using the same methodology as in the second part of Theorem 1, we obtain that , which implies the convergence of the algorithm.

Note that guaranteeing can be achieved by simply choosing and setting to a small number.

∎

3.4 When q is not Quadratic

This subsection discusses how to adapt GMSA to solve (1) even when is not quadratic but it is convex and twice differentiable. Following previous work [42, 50], we keep the nonsmooth function and approximate the smooth function around the current solution by its second-order Taylor expansion:

where and denote the gradient and Hessian of at , respectively. In order to generate the next solution that decreases the objective, one can minimize the quadratic model above by solving

| (35) |

And then one performs line search by the update: for the greatest descent in objective (as in the damped Newton method). Here, is the step-size selected by backtracking line search.

| (36) |

In practice, one does not need to solve the Newton approximation subproblem in (35) exactly and one iteration suffices for global convergence. We use to denote one iteration of GMSA with the parameter . Note that both and are changing with . We use to denote the associated matrices of using the same splitting strategy as in (4). In some situation, we drop the superscript for simplicity since it can be known from the context. We summarized our algorithm to solve the general convex composite problem in Algorithm 5.

Algorithm 5 iteratively calls Algorithm 1 for one time to compute the next point . Based on the search direction , we employ Armijo’s rule and try step size with a constant decrease rate until we find the smallest with such that satisfies the sufficient decrease condition. A typical choice for the parameters is .

In what follows, we present our convergence analysis for Algorithm 5. The following lemma is useful in our proof.

Lemma 5.

Proof.

It is not hard to notice that GMSA reduces to the following inclusion problem:

Using the definition that and , we have:

| (37) |

We further derive the following inequalities:

where step uses the fact that ; step uses the convexity of ; step uses (37) and . Rearranging terms we finish the proof of this lemma.

∎

Theorem 7.

We define and let be chosen such that . Assuming that the gradient of is -Lipschitz continuous, we have the following results: (i) There always exists a strictly positive constant such that the descent condition in (36) is satisfied. (ii) The sequence is nonincreasing and Algorithm 5 is globally convergent.

Proof.

For simplicity, we drop the iteration counter as it can be inferred from the context. First of all, for all , we have:

| (38) |

where step uses the definition of that and the fact that ; step uses ; step uses the fact that is positive semidefinite for convex problems.

For any , we have the following results:

where step uses the fact that which is due to the convexity of ; step uses the inequality with ; step uses the definition of in Algorithm 5; step uses Lemma (5) that which is due to (7); step uses the choice that .

(ii) We obtain the following inequality:

and the sequence is non-increasing. Using the same methodology as in the second part of Theorem 1, we have as . Therefore, any cluster point of the sequence is a stationary point. Finally, we have . From (8) in Lemma (1), we obtain: . Therefore, we conclude that is the global optimal solution.

∎

3.5 Adapting into ADMM Optimization Framework

This subsection shows how to adapt GMSA into the general optimization framework of ADMM [12, 13] to solve the following structured convex problem:

| (39) |

where and are decision variables, and are given. We assume that is positive semidefinite and is simple and convex (may not necessarily be separable) such that its proximal operator can be evaluated analytically. We let be the augmented Lagrangian function of (39):

where is the multiplier associated with the equality constraint , and is the penalty parameter.

We summarize our algorithm for solving (39) in Algorithm 6. The algorithm optimizes for a set of primal variables at a time and keeps the other primal and dual variables fixed, with the dual variables updating via gradient ascent. For the -subproblem, it admits a closed-form solution. For the -subproblem, since the smooth part is quadratic and the nonsmooth part is separable, it can be solved by Algorithm 1. Algorithm 6 is convergent if the -subproblem is solved exactly since it reduces to classical ADMM [12]. We remark that similar to linearized ADMM [12], Algorithm 6 also suffices for convergence empirically even if we only solve the -subproblem approximately.

3.6 When x is a Matrix

In many applications (e.g. nonegative matrix factorization and sparse coding), the solutions exist in the matrix form as follows: , where . Our matrix splitting algorithm can still be applied in this case. Using the same technique to decompose as in (4): , one needs to replace (6) to solve the following nonlinear equation: , where . It can be decomposed into independent components. By updating every column of , the proposed algorithm can be used to solve the matrix problem above. Thus, our algorithm can also make good use of existing parallel architectures to solve the matrix optimization problem.

4 Experiments

This section demonstrates the efficiency and efficacy of the proposed Generalized Matrix Splitting Algorithm (GMSA) by considering three important applications: nonnegative matrix factorization (NMF) [20, 22], norm regularized sparse coding [32, 35, 21], and norm regularized Danzig selectors. We implement our method in MATLAB on an Intel 2.6 GHz CPU with 8 GB RAM. Only our generalized Gaussian elimination procedure is developed in C and wrapped into the MATLAB code, since it requires an elementwise loop that is quite inefficient in native MATLAB. We consider and as our default parameters for GMSA in all our experiments. Some Matlab code can be found in the authors’ research webpages.

4.1 Convergence Behavior of Different Methods

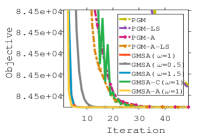

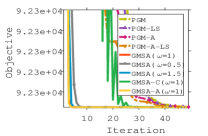

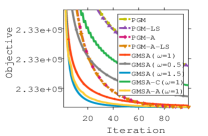

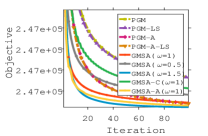

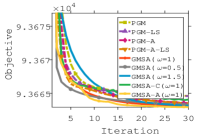

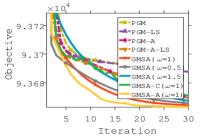

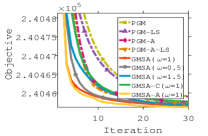

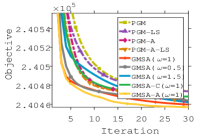

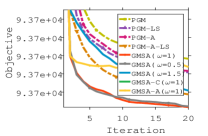

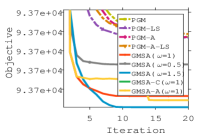

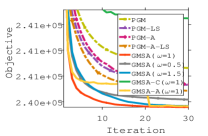

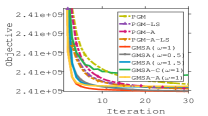

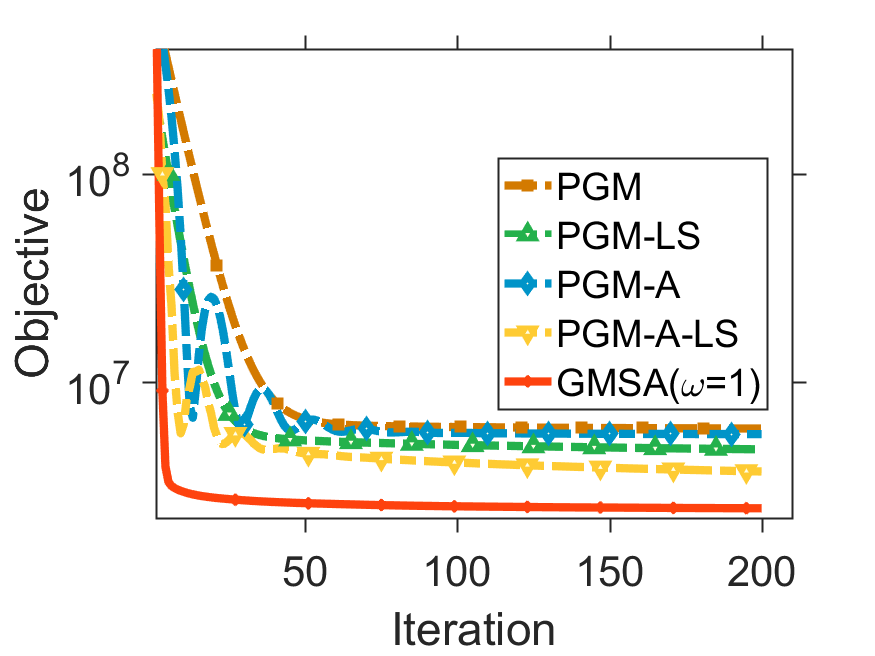

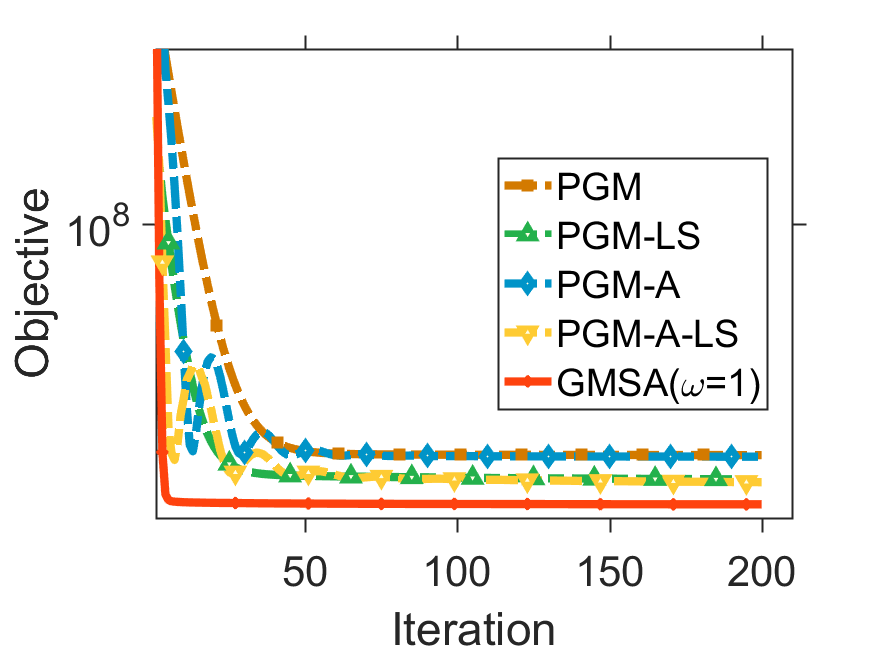

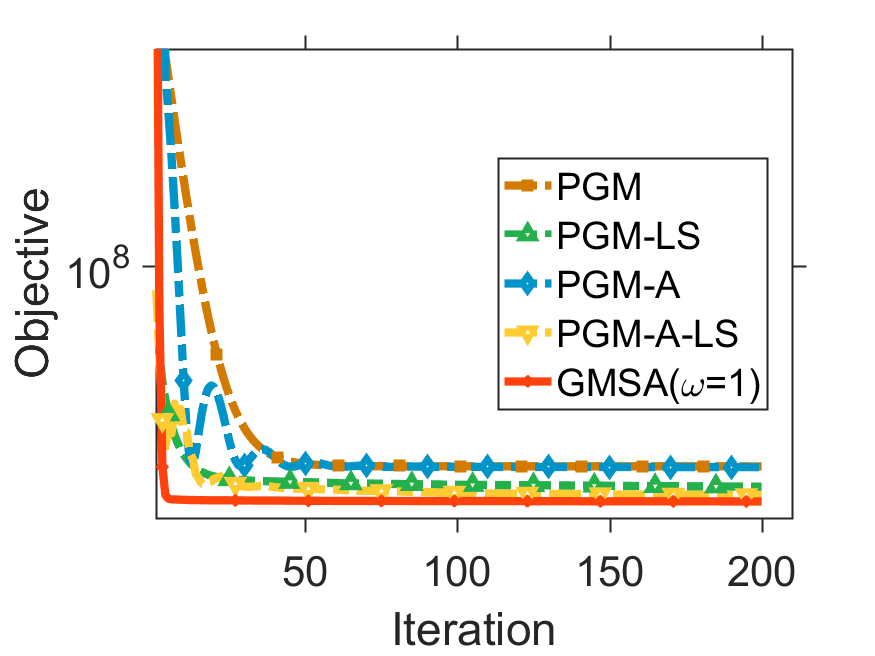

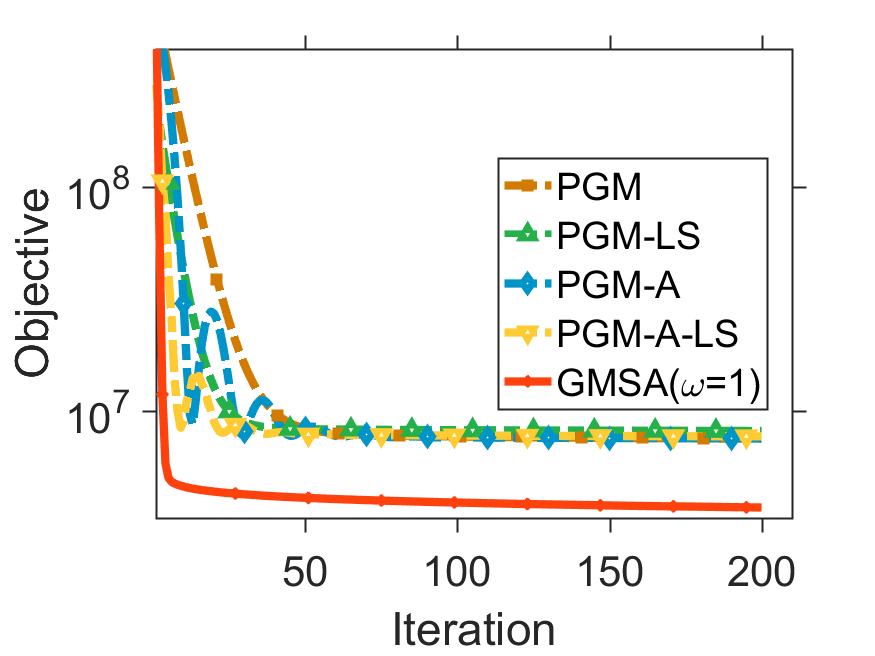

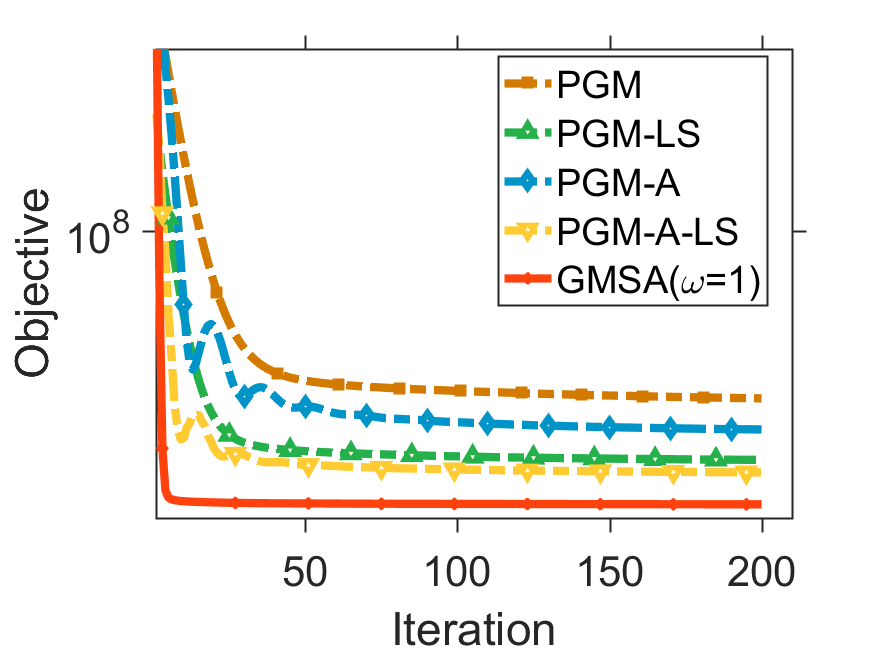

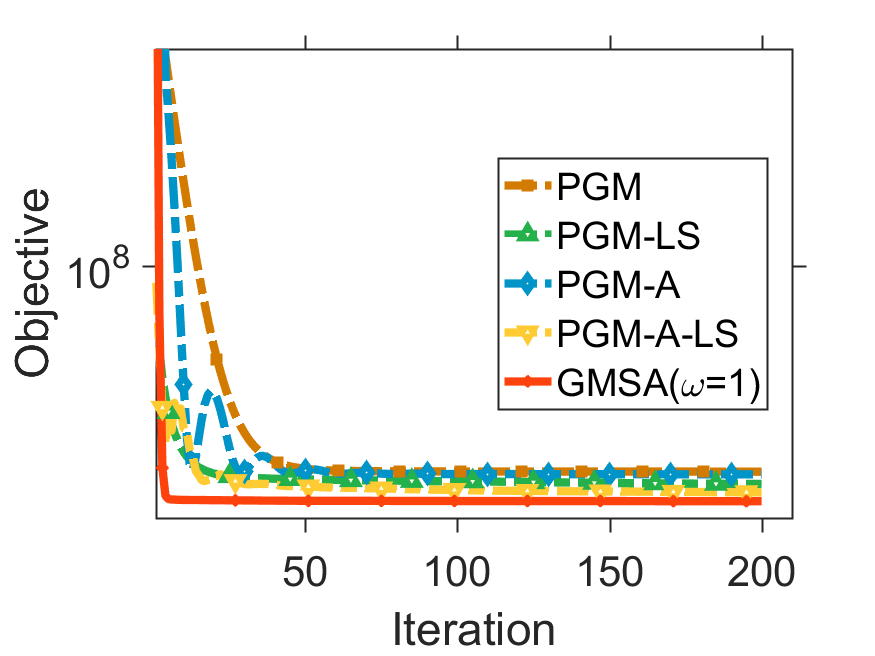

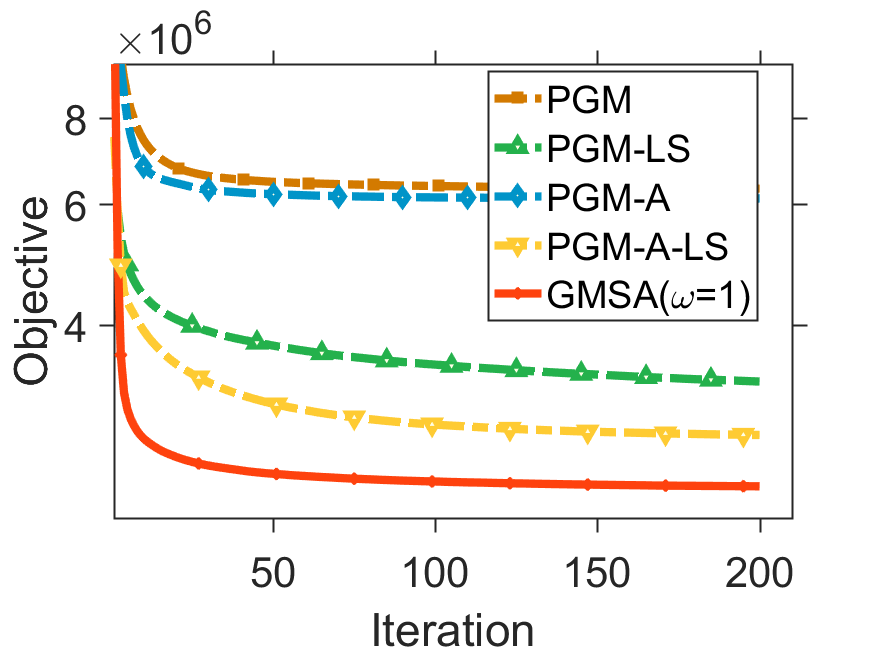

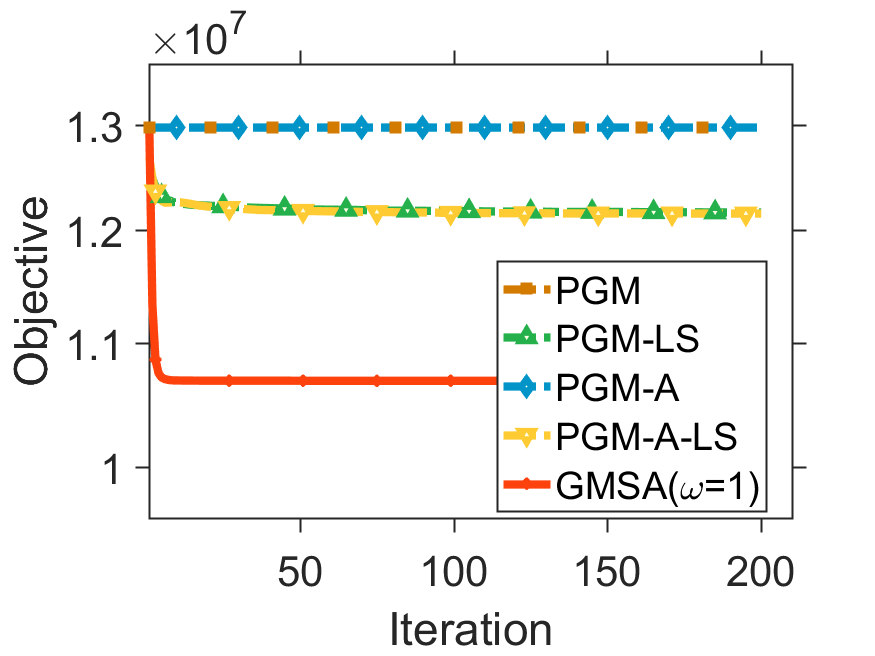

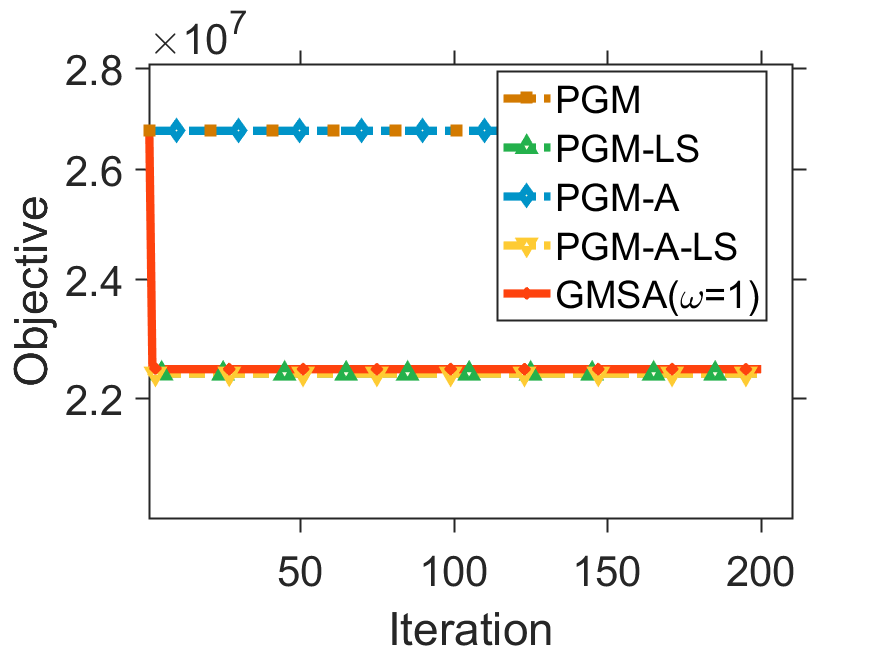

We demonstrate the convergence behavior of different methods for solving random least squares problems. We compare the following methods. (i) PGM: classical proximal gradient method with constant step size [31]; (ii) PGM-LS: classical PGM with line search [3]; (iii) PGM-A: accelerated PGM with constant step size [31]; (iv) PGM-A-LS: accelerated PGM with line search [3, 31]; (v) GMSA : generalized matrix splitting algorithm with varying the parameter described in Algorithm 1; (vi) GMSA-C: generalized matrix splitting algorithm with correction step described in (3), where a local constant for computing the step size is used; (vii) GMSA-A: generalized matrix splitting algorithm with Richardson extrapolation acceleration described in (4). We report the objective values of the comparing methods for each iteration when they are applied to solve non-negative/ norm regularized/ norm regularized least squares problems in Figure 1. Note that all the methods have the same computational complexity for one iteration.

We have the following observations. (i) GMSA with the default parameters and significantly outperforms proximal gradient method and its variants. (ii) GMSA gives better performance than GMSA for solving non-negative least squares problem but it gives worse performance than GMSA for solving norm regularized least squares problem. The choice of the parameter seems to be sensitive to the specific data. (iii) GMSA-C converges slower than GMSA but faster than PGM, PGM-LS. (iv) GMSA-A generally outperforms the other methods in the convex problems. (v) GMSA generally presents the best performance in the nonconvex problems.

Since (i) GMSA with the choice and gives comparable performance to its variants, and (ii) GMSA-A is not necessarily a monotonic algorithm (although it achieves acceleration upon GMSA), we only report the results for GMSA with and in our following experiments.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

4.2 Nonnegative Matrix Factorization

Nonnegative matrix factorization [20] is a very useful tool for feature extraction and identification in the fields of text mining and image understanding. It is formulated as the following optimization problem:

where and . Following previous work [19, 11, 22, 16], we alternatively minimize the objective while keeping one of the two variables fixed. In each alternating subproblem, we solve a convex nonnegative least squares problem, where our GMSA is used. We conduct experiments on three datasets 444http://www.cad.zju.edu.cn/home/dengcai/Data/TextData.html 20news, COIL, and TDT2. The size of the datasets are , respectively. We compare GMSA against the following state-of-the-art methods: (1) Projective Gradient (PG) [22, 5] that updates the current solution via steep gradient descent and then maps a point back to the bounded feasible region 555https://www.csie.ntu.edu.tw/~cjlin/libmf/; (2) Active Set (AS) method [19] and (3) Block Principal Pivoting (BPP) method [19] 666http://www.cc.gatech.edu/~hpark/nmfsoftware.php that iteratively identify an active and passive set by a principal pivoting procedure and solve a reduced linear system; (4) Accelerated Proximal Gradient (APG) [11] 777https://sites.google.com/site/nmfsolvers/ that applies Nesterov’s momentum strategy with a constant step size to solve the convex sub-problems; (5) Coordinate Gradient Descent (CGD) [16] 888http://www.cs.utexas.edu/~cjhsieh/nmf/ that greedily selects one coordinate by measuring the objective reduction and optimizes for a single variable via closed-form update. Similar to our method, the core procedure of CGD is developed in C and wrapped into the MATLAB code, while all other methods are implemented using builtin MATLAB functions.

We use the same settings as in [22]. We compare objective values after running seconds with varying from 20 to 50. Table I presents average results of using 10 random initial points, which are generated from a standard normal distribution. While the other methods may quickly lower objective values when is small (), GMSA catches up very quickly and achieves a faster convergence speed when is large. It generally achieves the best performance in terms of objective value among all the methods.

4.3 Norm Regularized Sparse Coding

Sparse coding is a popular unsupervised feature learning technique for data representation that is widely used in computer vision and medical imaging. Motivated by recent success in norm modeling [48, 2, 46], we consider the following norm regularized (i.e. cardinality) sparse coding problem:

| (40) |

with and . Existing solutions for this problem are mostly based on the family of proximal point methods [31, 2]. We compare GMSA with the following methods: (1) Proximal Gradient Method (PGM) with constant step size, (2) PGM with line search, (3) accelerated PGM with constant step size, and (4) accelerated PGM with line search.

We evaluate all the methods for the application of image denoising. Following [1, 2], we set the dimension of the dictionary to . The dictionary is learned from image patches randomly chosen from the noisy input image. The patch size is , leading to . The experiments are conducted on 16 conventional test images with different noise standard deviations . We tune the regularization parameter and compare the resulting objective values and the Signalto-Noise Ratio (SNR) values for all methods. We do not include the comparison of SNR values here. Interested readers can refer to Section 4.2 of the conference version of this paper [49].

We compare the objective values for all methods by fixing the variable to an over-complete DCT dictionary [1] and only optimizing over . We compare all methods with varying regularization parameter and different initial points that are either generated by random Gaussian sampling or the Orthogonal Matching Pursuit (OMP) method [40]. In Figure 2, we observe that GMSA converges rapidly in 10 iterations. Moreover, it often generates much better local optimal solutions than the compared methods.

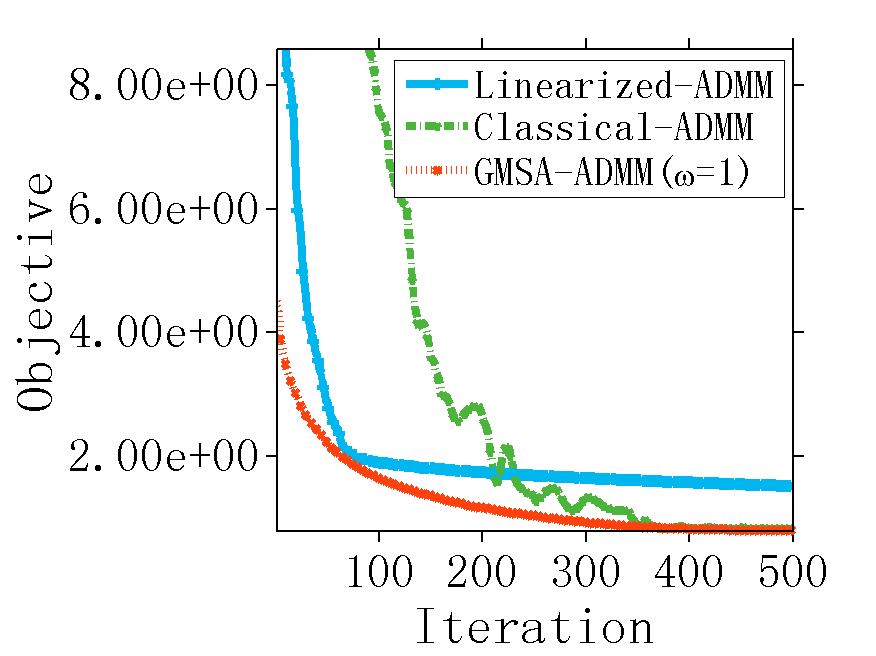

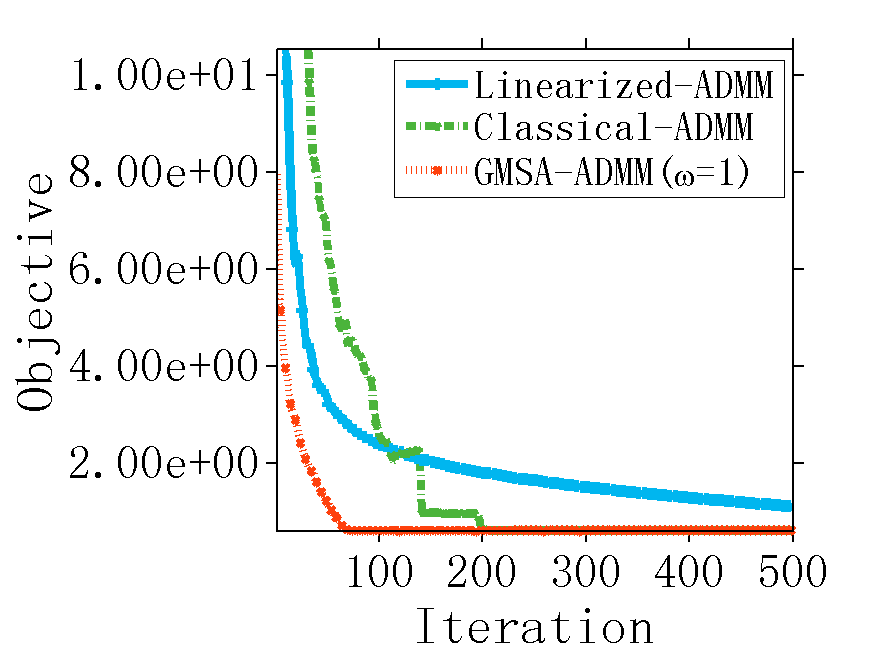

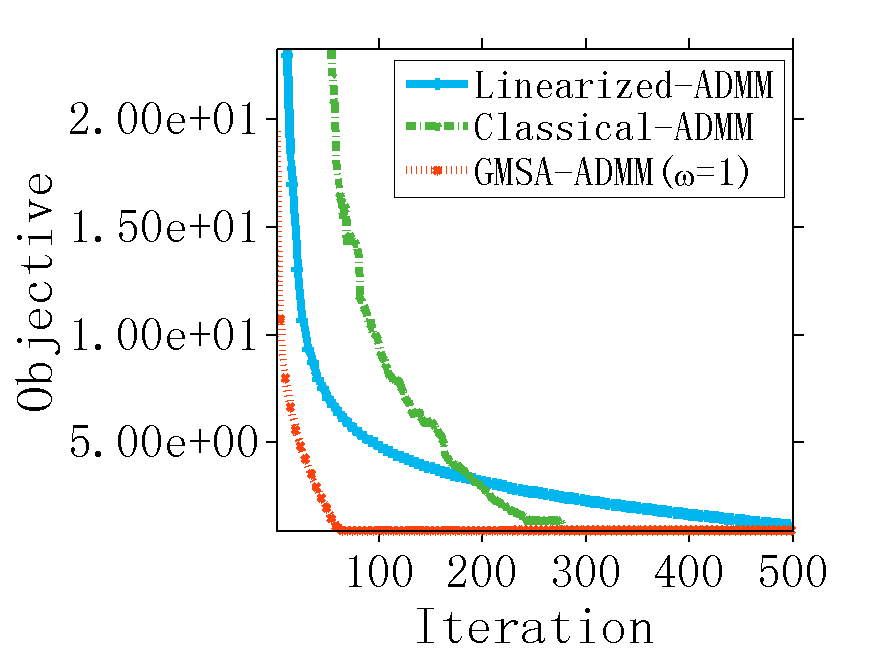

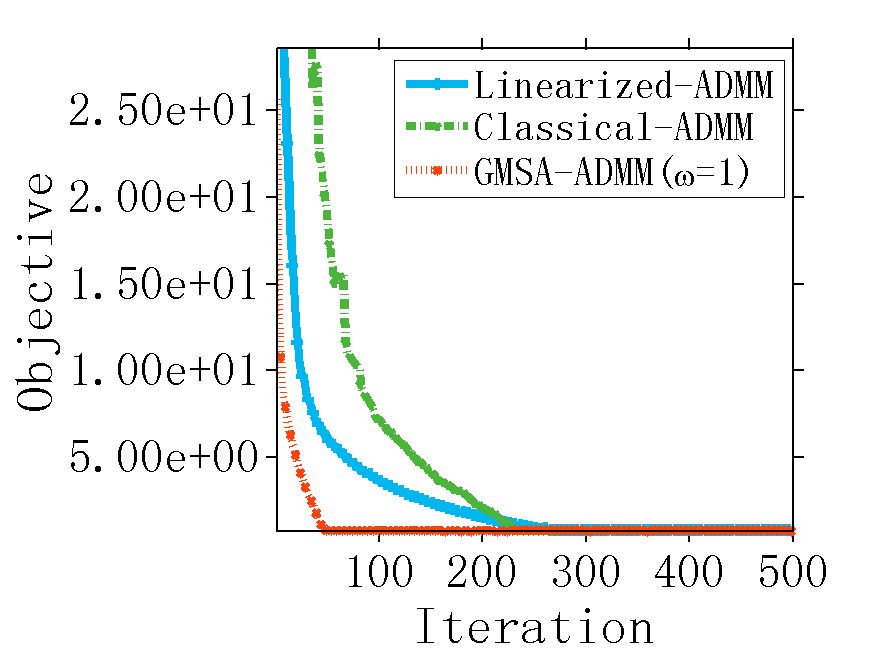

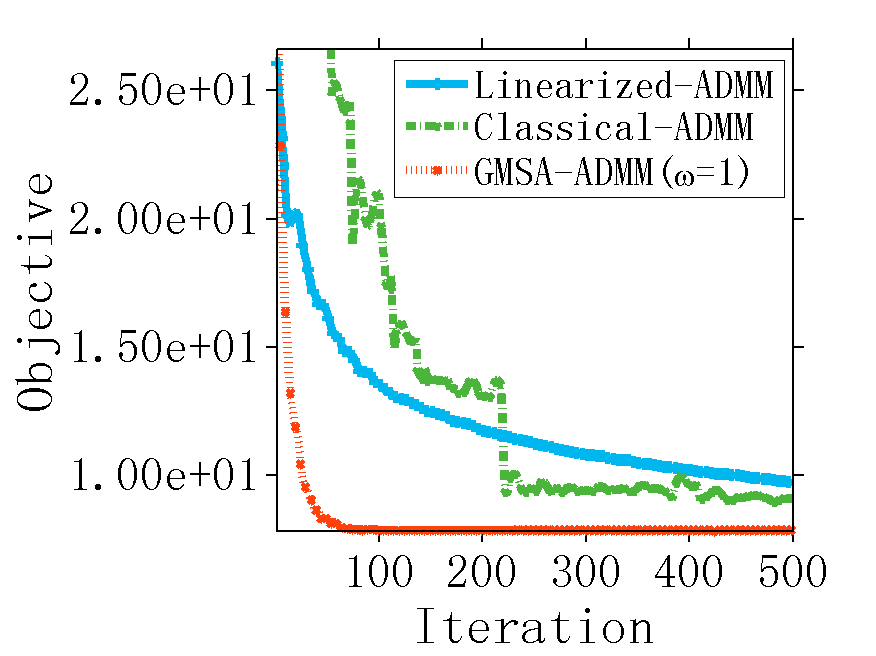

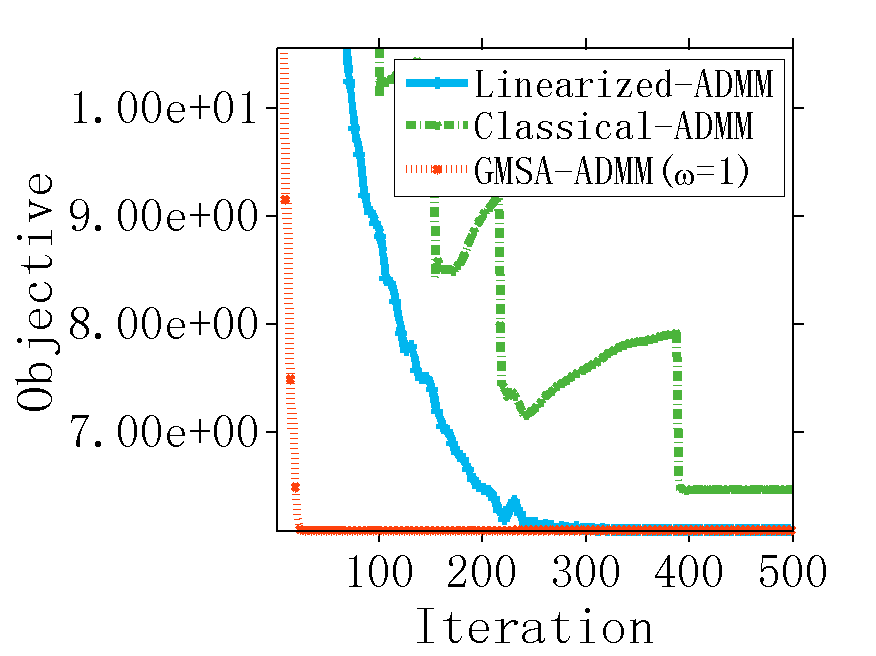

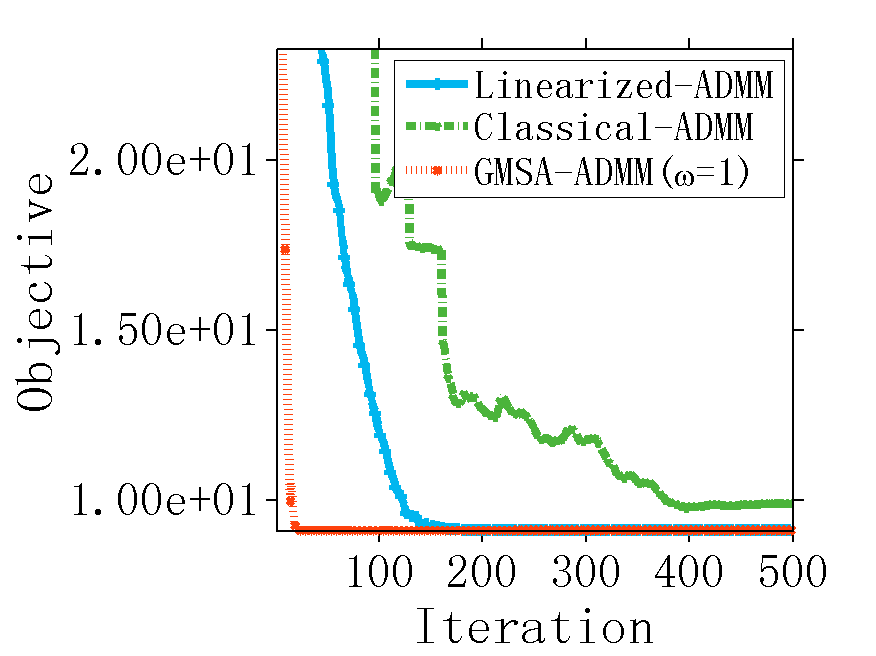

4.4 Norm Regularized Danzig Selectors

Danzig selectors [6] can be formulated as the following optimization problem: , where , and is the diagonal matrix whose diagonal entries are the norm of the columns of . For the ease of discussion, we consider the following equivalent unconstrained optimization problem:

| (41) |

with , and .

We generate the design matrix via sampling from a standard Gaussian distribution. The sparse original signal is generated via selecting a support set of size 20 uniformly at random and set them to arbitrary number sampled from standard Gaussian distribution. We set . We fix and consider different choices for and .

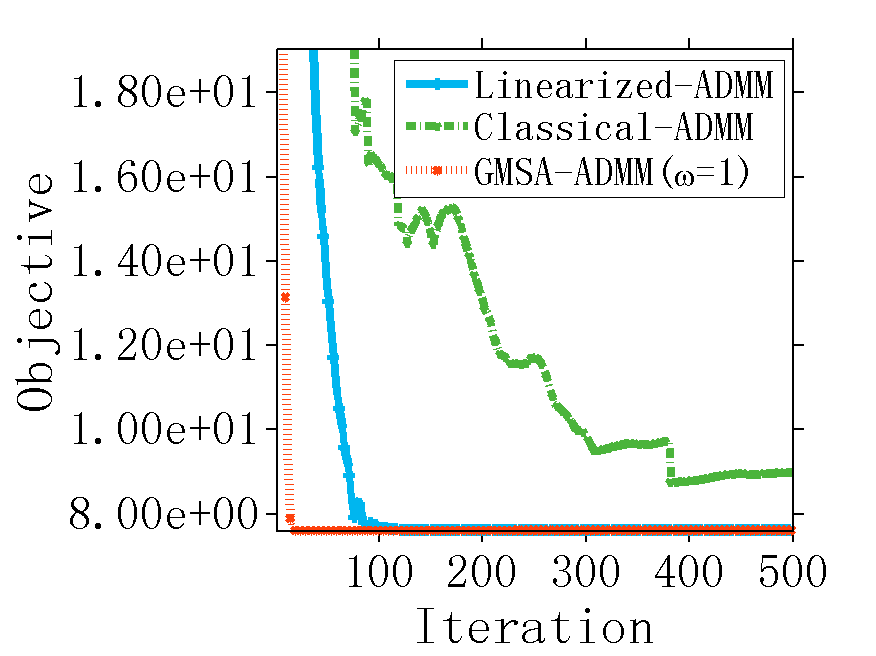

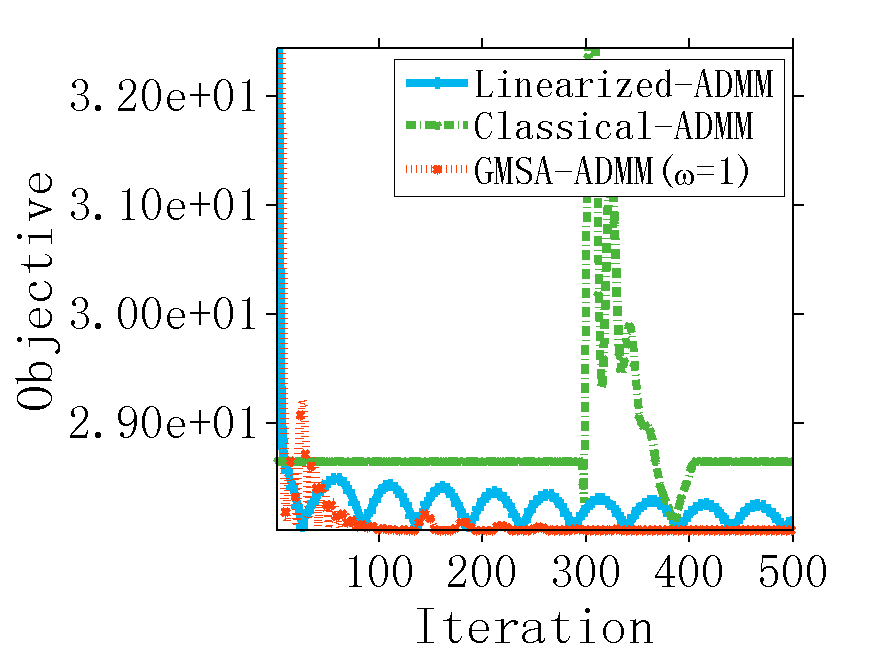

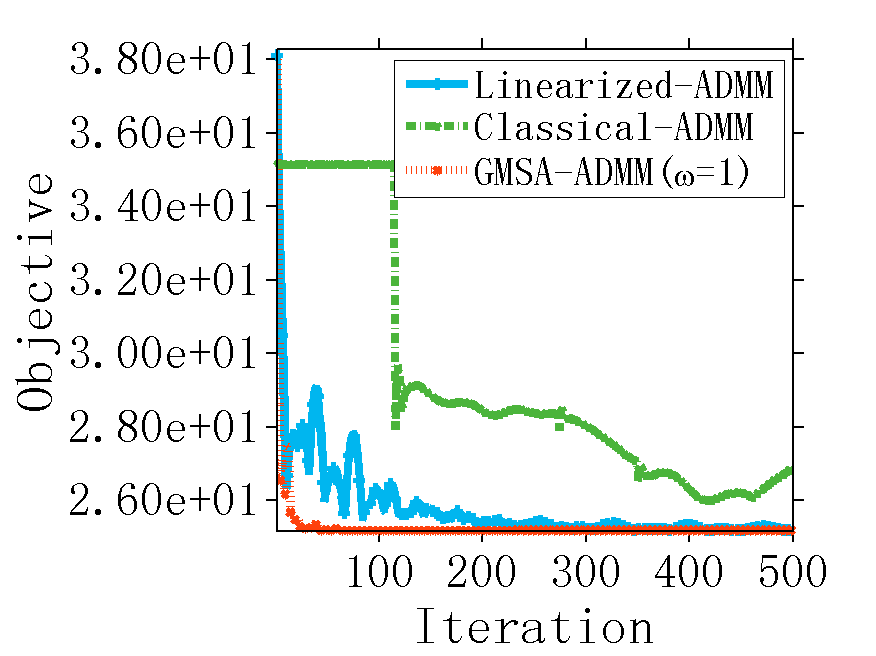

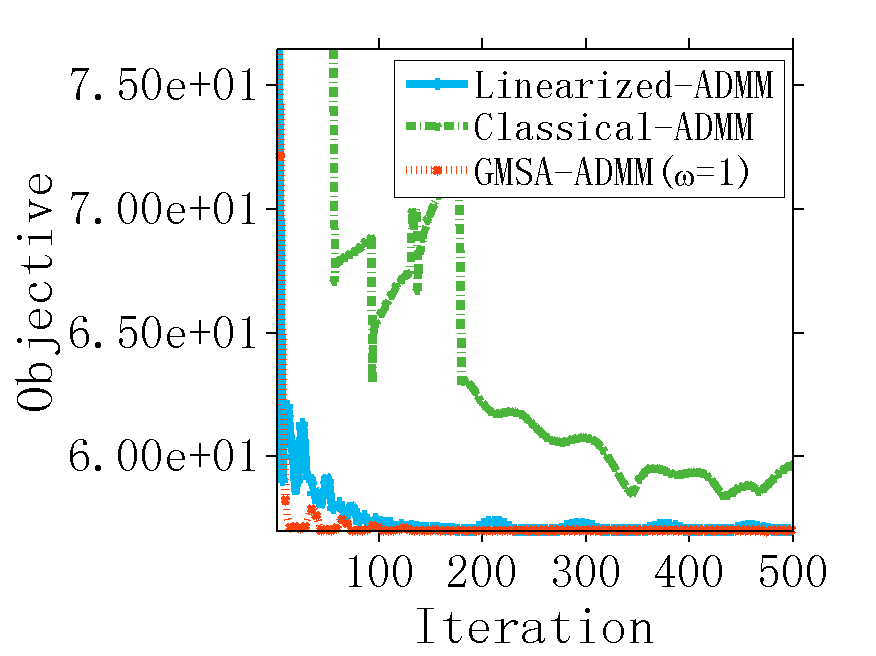

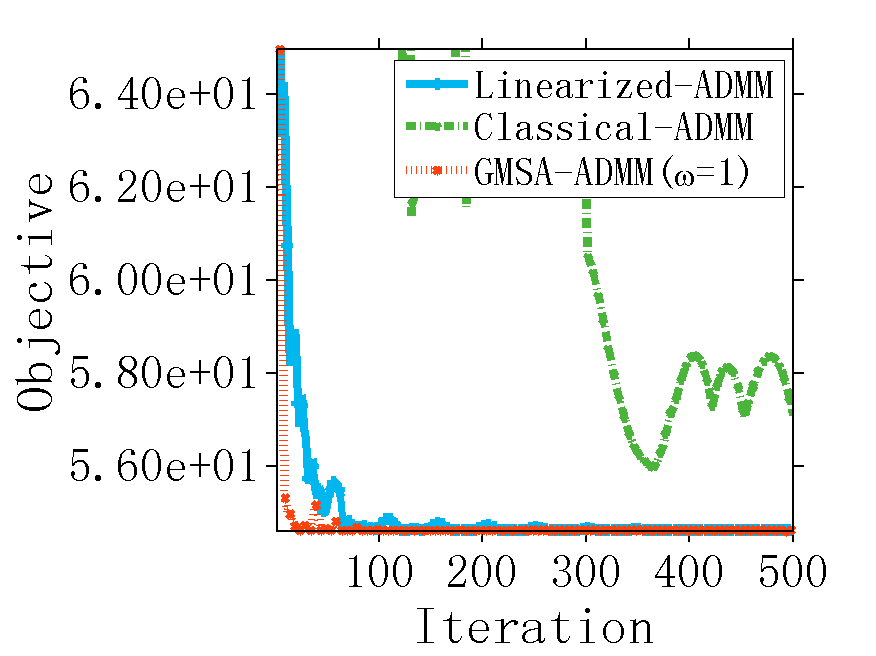

We compare the proposed method GMSA-ADMM against linearized ADMM algorithm and classical ADMM algorithm. The penalty parameter is fixed to a constant with . For linearized ADMM, we use the same splitting strategy as in [44]. For classical ADMM, we introduce addition two variables and rewrite (41) as: to make sure that the smooth subproblem of the resulting augmented Lagrangian function is quadratic and can be solved by linear equations. For GMSA-ADMM, we do not solve the -subproblem exactly using GMSA but solve it using one GMSA iteration. We demonstrate the objective values for the comparing methods. It can be been in Figure 3 that our GMSA-ADMM significantly outperforms linearized ADMM and classical ADMM.

5 Conclusions

This paper presents a new generalized matrix splitting algorithm for minimizing composite functions. We rigorously analyze its convergence behavior for convex problems and discuss its several importance extensions. Experimental results on nonnegative matrix factorization, norm regularized sparse coding, and norm regularized Danzig selector demonstrate that our methods achieve state-of-the-art performance.

Acknowledgments

This work was supported by the King Abdullah University of Science and Technology (KAUST) Office of Sponsored Research. This work was also supported by the NSF-China (61772570, 61472456, 61522115, 61628212).

References

- [1] Michal Aharon, Michael Elad, and Alfred Bruckstein. K-svd: An algorithm for designing overcomplete dictionaries for sparse representation. IEEE Transactions on Signal Processing, 54(11):4311–4322, 2006.

- [2] Chenglong Bao, Hui Ji, Yuhui Quan, and Zuowei Shen. Dictionary learning for sparse coding: Algorithms and convergence analysis. IEEE Transactions on Pattern Analysis and Machine Intelligence (TPAMI), 38(7):1356–1369, 2016.

- [3] Amir Beck and Marc Teboulle. A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM Journal on Imaging Sciences (SIIMS), 2(1):183–202, 2009.

- [4] Amir Beck and Luba Tetruashvili. On the convergence of block coordinate descent type methods. SIAM journal on Optimization (SIOPT), 23(4):2037–2060, 2013.

- [5] Dimitri P Bertsekas. Nonlinear programming. Athena scientific Belmont, 1999.

- [6] Emmanuel Candes, Terence Tao, et al. The dantzig selector: Statistical estimation when p is much larger than n. The Annals of Statistics, 35(6):2313–2351, 2007.

- [7] Wenfei Cao, Jian Sun, and Zongben Xu. Fast image deconvolution using closed-form thresholding formulas of regularization. Journal of Visual Communication and Image Representation, 24(1):31–41, 2013.

- [8] James W Demmel. Applied numerical linear algebra. SIAM, 1997.

- [9] David L. Donoho. Compressed sensing. IEEE Transactions on Information Theory, 52(4):1289–1306, 2006.

- [10] Ehsan Elhamifar and Rene Vidal. Sparse subspace clustering: Algorithm, theory, and applications. IEEE Transactions on Pattern Analysis and Machine Intelligence (TPAMI), 35(11):2765–2781, 2013.

- [11] Naiyang Guan, Dacheng Tao, Zhigang Luo, and Bo Yuan. Nenmf: an optimal gradient method for nonnegative matrix factorization. IEEE Transactions on Signal Processing, 60(6):2882–2898, 2012.

- [12] Bingsheng He and Xiaoming Yuan. On the o(1/n) convergence rate of the douglas-rachford alternating direction method. SIAM Journal on Numerical Analysis, 50(2):700–709, 2012.

- [13] Bingsheng He and Xiaoming Yuan. On non-ergodic convergence rate of douglas-rachford alternating direction method of multipliers. Numerische Mathematik, 130(3):567–577, 2015.

- [14] Mingyi Hong, Xiangfeng Wang, Meisam Razaviyayn, and Zhi-Quan Luo. Iteration complexity analysis of block coordinate descent methods. Mathematical Programming, pages 1–30, 2013.

- [15] Cho-Jui Hsieh, Kai-Wei Chang, Chih-Jen Lin, S Sathiya Keerthi, and Sellamanickam Sundararajan. A dual coordinate descent method for large-scale linear svm. In International Conference on Machine Learning (ICML), pages 408–415, 2008.

- [16] Cho-Jui Hsieh and Inderjit S Dhillon. Fast coordinate descent methods with variable selection for non-negative matrix factorization. In ACM SIGKDD International Conference on Knowledge Discovery and Data Mining (SIGKDD), pages 1064–1072, 2011.

- [17] Alfredo N. Iusem. On the convergence of iterative methods for symmetric linear complementarity problems. Math. Program., 59(1):33–48, March 1993.

- [18] Rie Johnson and Tong Zhang. Accelerating stochastic gradient descent using predictive variance reduction. In Advances in Neural Information Processing Systems (NIPS), pages 315–323, 2013.

- [19] Jingu Kim and Haesun Park. Fast nonnegative matrix factorization: An active-set-like method and comparisons. SIAM Journal on Scientific Computing (SISC), 33(6):3261–3281, 2011.

- [20] Daniel D Lee and H Sebastian Seung. Learning the parts of objects by non-negative matrix factorization. Nature, 401(6755):788–791, 1999.

- [21] Honglak Lee, Alexis Battle, Rajat Raina, and Andrew Y Ng. Efficient sparse coding algorithms. In Advances in Neural Information Processing Systems (NIPS), pages 801–808, 2006.

- [22] Chih-Jen Lin. Projected gradient methods for nonnegative matrix factorization. Neural Computation, 19(10):2756–2779, 2007.

- [23] Qihang Lin, Zhaosong Lu, and Lin Xiao. An accelerated randomized proximal coordinate gradient method and its application to regularized empirical risk minimization. SIAM Journal on Optimization (SIOPT), 25(4):2244–2273, 2015.

- [24] Ji Liu and Stephen J Wright. Asynchronous stochastic coordinate descent: Parallelism and convergence properties. SIAM Journal on Optimization (SIOPT), 25(1):351–376, 2015.

- [25] Zhaosong Lu and Lin Xiao. Randomized block coordinate non-monotone gradient method for a class of nonlinear programming. arXiv preprint, 2013.

- [26] Zhaosong Lu and Lin Xiao. On the complexity analysis of randomized block-coordinate descent methods. Mathematical Programming, 152(1-2):615–642, 2015.

- [27] Zhi-Quan Luo and Paul Tseng. On the convergence of a matrix splitting algorithm for the symmetric monotone linear complementarity problem. SIAM Journal on Control and Optimization, 29(5):1037–1060, 1991.

- [28] Zhi-Quan Luo and Paul Tseng. Error bound and convergence analysis of matrix splitting algorithms for the affine variational inequality problem. SIAM Journal on Optimization, 2(1):43–54, 1992.

- [29] Zhi-Quan Luo and Paul Tseng. Error bounds and convergence analysis of feasible descent methods: a general approach. Annals of Operations Research, 46(1):157–178, 1993.

- [30] Yu Nesterov. Efficiency of coordinate descent methods on huge-scale optimization problems. SIAM Journal on Optimization (SIOPT), 22(2):341–362, 2012.

- [31] Yurii Nesterov. Introductory lectures on convex optimization: A basic course, volume 87. Springer Science & Business Media, 2013.

- [32] Bruno A Olshausen et al. Emergence of simple-cell receptive field properties by learning a sparse code for natural images. Nature, 381(6583):607–609, 1996.

- [33] Neal Parikh, Stephen P Boyd, et al. Proximal algorithms. Foundations and Trends in optimization, 1(3):127–239, 2014.

- [34] Andrei Patrascu and Ion Necoara. Iteration complexity analysis of random coordinate descent methods for regularized convex problems. arXiv preprint, 2014.

- [35] Yuhui Quan, Yong Xu, Yuping Sun, Yan Huang, and Hui Ji. Sparse coding for classification via discrimination ensemble. In IEEE Conference on Computer Vision and Pattern Recognition (CVPR), June 2016.

- [36] Peter Richtárik and Martin Takáč. Iteration complexity of randomized block-coordinate descent methods for minimizing a composite function. Mathematical Programming, 144(1-2):1–38, 2014.

- [37] Y. Saad. Iterative Methods for Sparse Linear Systems. Society for Industrial and Applied Mathematics, Philadelphia, PA, USA, 2nd edition, 2003.

- [38] Li Shen, Wei Liu, Ganzhao Yuan, and Shiqian Ma. GSOS: gauss-seidel operator splitting algorithm for multi-term nonsmooth convex composite optimization. In International Conference on Machine Learning (ICML), pages 3125–3134, 2017.

- [39] Ruoyu Sun and Mingyi Hong. Improved iteration complexity bounds of cyclic block coordinate descent for convex problems. In Advances in Neural Information Processing Systems (NIPS), pages 1306–1314, 2015.

- [40] Joel A Tropp and Anna C Gilbert. Signal recovery from random measurements via orthogonal matching pursuit. IEEE Transactions on Information Theory, 53(12):4655–4666, 2007.

- [41] Paul Tseng. Approximation accuracy, gradient methods, and error bound for structured convex optimization. Mathematical Programming, 125(2):263–295, 2010.

- [42] Paul Tseng and Sangwoon Yun. A coordinate gradient descent method for nonsmooth separable minimization. Mathematical Programming, 117(1-2):387–423, 2009.

- [43] Richard S. Varga and J. Gillis. Matrix Iterative Analysis. Prentice-Hall, 1962.

- [44] Xiangfeng Wang and Xiaoming Yuan. The linearized alternating direction method of multipliers for dantzig selector. SIAM Journal on Scientific Computing, 34(5), 2012.

- [45] Zongben Xu, Xiangyu Chang, Fengmin Xu, and Hai Zhang. L1/2 regularization: A thresholding representation theory and a fast solver. IEEE Transactions on Neural Networks and Learning Systems (TNNLS), 23(7):1013–1027, 2012.

- [46] Yingzhen Yang, Jiashi Feng, Nebojsa Jojic, Jianchao Yang, and Thomas S. Huang. -sparse subspace clustering. European Conference on Computer Vision (ECCV), 2016.

- [47] Hsiang-Fu Yu, Fang-Lan Huang, and Chih-Jen Lin. Dual coordinate descent methods for logistic regression and maximum entropy models. Machine Learning, 85(1-2):41–75, 2011.

- [48] Ganzhao Yuan and Bernard Ghanem. : A new method for image restoration in the presence of impulse noise. In IEEE Conference on Computer Vision and Pattern Recognition (CVPR), pages 5369–5377, 2015.

- [49] Ganzhao Yuan, Wei-Shi Zheng, and Bernard Ghanem. A matrix splitting method for composite function minimization. In IEEE Conference on Computer Vision and Pattern Recognition (CVPR), pages 5310–5319, 2017.

- [50] Xiao-Tong Yuan and Qingshan Liu. Newton greedy pursuit: A quadratic approximation method for sparsity-constrained optimization. In IEEE Conference on Computer Vision and Pattern Recognition (CVPR), pages 4122–4129, 2014.

- [51] Sangwoon Yun, Paul Tseng, and Kim-Chuan Toh. A block coordinate gradient descent method for regularized convex separable optimization and covariance selection. Mathematical Programming, 129(2):331–355, 2011.

- [52] Jinshan Zeng, Zhimin Peng, and Shaobo Lin. GAITA: A gauss-seidel iterative thresholding algorithm for regularized least squares regression. Journal of Computational and Applied Mathematics, 319:220–235, 2017.

- [53] Lei-Hong Zhang and Wei Hong Yang. An efficient matrix splitting method for the second-order cone complementarity problem. SIAM Journal on Optimization, 24(3):1178–1205, 2014.

![[Uncaptioned image]](/html/1806.03165/assets/x13.png) |

Ganzhao Yuan was born in Guangdong, China. He received his Ph.D. in School of Computer Science and Engineering, South China University of Technology in 2013. He is currently a research associate professor at School of Data and Computer Science in Sun Yat-sen University. His research interests primarily center around large-scale mathematical optimization and its applications in computer vision and machine learning. He has published technical papers in ICML, SIGKDD, AAAI, CVPR, VLDB, IEEE TPAMI, and ACM TODS. |

![[Uncaptioned image]](/html/1806.03165/assets/x14.png) |

Wei-Shi Zheng was born in Guangdong, China. He is now a Professor at Sun Yat-sen University. He has now published more than 90 papers, including more than 60 publications in main journals (TPAMI, TIP, TNNLS, PR) and top conferences (ICCV, CVPR, IJCAI). His research interests include person/object association and activity understanding in visual surveillance. He has joined Microsoft Research Asia Young Faculty Visiting Programme. He is a recipient of Excellent Young Scientists Fund of the NSFC, and a recipient of Royal Society-Newton Advanced Fellowship. |

![[Uncaptioned image]](/html/1806.03165/assets/x15.png) |

Li Shen was born in Hubei, China. He received his Ph.D. in School of Mathematics, South China University of Technology in 2017. He is currently a research scientist at Tencent AI Lab, Shenzhen. His research interests include algorithms for nonsmooth optimization, and their applications in statistical machine learning, game theory and reinforcement learning. He has published several papers in ICML and AAAI. |

![[Uncaptioned image]](/html/1806.03165/assets/x16.png) |

Bernard Ghanem was born in Betroumine, Lebanon. He received his Ph.D. in Electrical and Computer Engineering from the University of Illinois at Urbana-Champaign (UIUC) in 2010. He is currently an assistant professor at King Abdullah University of Science and Technology (KAUST), where he leads the Image and Video Understanding Lab (IVUL). His research interests focus on designing, implementing, and analyzing approaches to address computer vision problems (e.g. object tracking and action recognition/detection in video), especially at large-scale. |