Causal Bandits with Propagating Inference

Abstract

Bandit is a framework for designing sequential experiments. In each experiment, a learner selects an arm and obtains an observation corresponding to . Theoretically, the tight regret lower-bound for the general bandit is polynomial with respect to the number of arms . This makes bandit incapable of handling an exponentially large number of arms, hence the bandit problem with side-information is often considered to overcome this lower bound. Recently, a bandit framework over a causal graph was introduced, where the structure of the causal graph is available as side-information. A causal graph is a fundamental model that is frequently used with a variety of real problems. In this setting, the arms are identified with interventions on a given causal graph, and the effect of an intervention propagates throughout all over the causal graph. The task is to find the best intervention that maximizes the expected value on a target node. Existing algorithms for causal bandit overcame the simple-regret lower-bound; however, their algorithms work only when the interventions are localized around a single node (i.e., an intervention propagates only to its neighbors).

We propose a novel causal bandit algorithm for an arbitrary set of interventions, which can propagate throughout the causal graph. We also show that it achieves regret bound, where is determined by using a causal graph structure. In particular, if the in-degree of the causal graph is bounded, then , where is the number of nodes.

1 Introduction

Multi-armed bandit has been widely recognized as a standard framework for modeling online learning with a limited number of observations. In each round in the bandit problem, a learner chooses an arm from given candidates , and obtains a corresponding observation. Since observation is limited, the learner must adopt an efficient strategy for exploring the optimal arm . The efficiency of the strategy is measured by regret, and the theoretically tight lower-bound is with respect to the number of arms in the general multi-armed bandit setting. Thus, in order to improve the above lower bound, one requires additional information for the bandit setting. For example, contextual bandit [1, 3] is a well-known class of bandit problems with side information on domain-expert knowledge. For this setting, there is a logarithmic regret bound with respect to the number of arms. In this paper, we also achieve regret bound for a novel class of bandit problems with side information. To this end, let us introduce our bandit setting in detail.

Causal graph [14] is a well-known tool for modeling a variety of real problems, including computational advertising [4], genetics [12], agriculture [19], and marketing [10]. Based on causal graph discovery studies [5, 7, 8, 16], Lattimore et al. [11] recently introduced the causal bandit framework. They consider the problem of finding the best intervention which causes desirable propagation of a probabilistic distribution over a given causal graph with a limited number of experiments . In this setting, the arms are identified as interventions on the causal graph. A set of binary random variables is associated with nodes of the causal graph. At each round of an experiment, a learner selects an intervention which enforces a realization of a variable to when . The effect of the intervention then propagates throughout the causal graph through the edges, and a realization over all nodes is observed after propagation. The goal of the causal bandit problem is to control the realization of a target variable with an optimal intervention.

Figure 1 is an illustrative example of the causal bandit problem. In the figure, the four nodes on the right represent a consumer decision-making model in e-commerce borrowed from [10]. This model assumes that customers make a decision to purchase based on their perceived risk in an online transition (e.g., defective product), the consumer’s trust of a web vendor, and the perceived benefit in e-commerce (e.g., increased convenience). Consumer trust influences perceived risk. Here, we consider controlling customer’s behavior by two kinds of advertising that correspond to adding two nodes (Ad A and Ad B) to be intervened into the model. Ad A can change only the reliability of a website, that is, it can influence the decision of customers in an indirect way through the middle nodes. In contrast, Ad B can change the perceived benefit. The aim is to increase the number of purchases by consumers through choosing an effective advertisement. This is indeed a bandit problem over a causal graph.

The work in [11] considered the causal bandit problem to minimize simple regret and offered an improved regret bound over the aforementioned tight lower-bound [2][Theorem 4] for the general bandit setting [2, 6]. Sen et al. [15] extended this study by incorporating a smooth intervention, and they provided a new regret bound parameterized by the performance gap between the optimal and sub-optimal arms. This parameterized bound comes from the technique developed for the general multi-armed bandit problem [2]. These analyses, however, only work for a special class of interventions with known true parameters. Indeed, they only consider localized interventions.

Main contribution

This paper proposes the first algorithm for the causal bandit problem with an arbitrary set of interventions (which can propagate throughout the causal graph), with a theoretically guaranteed simple regret bound. The bound is , where is a parameter bounded on the basis of the graph structure. In particular, if the in-degree of the causal graph is bounded by a constant, where is the number of nodes.

The major difficulty in dealing with an arbitrary intervention comes from accumulation and propagation of estimation error. Existing studies consider interventions that only affect the parents of a single node . To estimate the relationship between and in this setting, we could apply an efficient importance sampling algorithm [4, 11]. On the other hand, when we intervene an arbitrary node, it can affect the probabilistic propagation mechanism in any part of the causal graph. Hence, we cannot directly control the realization of intermediate nodes when designing efficient experiments.

The proposed algorithm consists of two steps. First, the preprocessing step is devoted to estimating parameters for designing efficient experiments used in the main step. More precisely, we focus on estimation of parameters with bounded relative error. By truncating small parameters that are negligible but tend to have large relative error, we manage to avoid accumulation of estimation error. In the main step, we apply an importance sampling approach introduced in [11, 15] on the basis of estimated parameters with a guaranteed relative error. This step allows us to estimate parameters with bounded absolute error, which results in the desired regret bound.

Related studies

Minimizing simple regret in bandit problems is called the best-arm identification [6, 9] or pure exploration [4] problem, and it has been extensively studied in the machine learning research community. The inference of a causal graph structure is also well-studied, which can be classified into causal graph discovery and causal inference: Causal graph discovery [5, 7, 8, 16] considers efficient experiments for determining the structure of causal graph, while causal inference [13, 14, 17, 18] challenges one to determine the graph structure only from historical data without additional experiments. The causal bandit problem designs experiments without using historical data, which is rather compatible with causal graph discovery studies.

Outline

This paper is organized as follows. We introduce the causal bandit problem proposed in [11] in Section 2. We then present our bandit algorithm and regret bound in Section 3. The proof of the bound is presented in Section 4. We offer experimental evaluation of our algorithm in Section 5.

2 Causal bandit problem

This section introduces the causal bandit problem proposed by [11].

Let be a directed acyclic graph (DAG) with a node set and a (directed) edge set . Let denote an edge from to . Without loss of generality, we suppose that the nodes in are topologically sorted so that no edge from to exists if . For each , let denote the index set of the parents of , i.e., . We then define .

Each node is associated with a random variable , which takes a value in . The distribution of is then influenced by the variables associated with the parents of (unless is intervened, as described below). For each , the parameter defined below characterizes the distribution of given the realizations of its parents:

That is to say, if the parents for are realized as , then with probability , and with probability .

Together with a DAG, we are also given a set of interventions. Each intervention is identified with a vector , where implies that is intervened and that the realization of is fixed as . Let . Given an intervention and realizations over the parents , the probability that holds is then determined as follows:

This equality together with the adjacency of the causal graph completely determines the joint distribution over the variables , under an arbitrary intervention .

In the causal bandit problem, we are given a DAG and a set of interventions. However, the parameters () are not known. Our ideal goal is then to find an intervention that maximizes the probability of realizing , where is defined by

for each .

For this purpose, we discuss the following algorithms. First, they estimate () from experimental trials. Each experiment consists of the application of an intervention and the observation of a realization over all nodes. Let denote the estimate of . Second, the algorithm selects the intervention that maximizes . We evaluate the efficiency of such an algorithm with the simple regret defined as follows:

Note that, even if an algorithm is deterministic, includes stochasticity since the observations obtained in each experiment are produced by a stochastic process.

In this paper, we assume that and for ease of technical discussion.

3 Proposed Algorithm

We propose an algorithm for the causal bandit problem, and present regret bound of the proposed algorithm in this section. The proofs of the bound are presented in the next section. Let for each , and . For and , let denote the restriction of onto .

3.1 Outline of the proposed algorithm

Recall that the purpose of the causal bandit problem is to identify an intervention that maximizes . This task is trivial if is known for all , because can then be calculated for all . Let , and for , let denote the set of nodes in which are not intervened by ; . can then be represented as

Therefore, for computing approximately, our algorithm estimates ().

In order to estimate efficiently, we are required to manipulate the random variables associated with the parents of . More concretely, to estimate for , we require samples with realization satisfying over the parents of . For , , and , we thus introduce the additional quantities that denote the probability of realizing with under a given intervention . More precisely, we define

Our algorithm consists of two phases. The first phase estimates (), and the second phase estimates . The algorithm requires experiments in the first phase, and experiments in the second phase. In the rest of this section, we first explain those phases and present a regret bound on the algorithm.

3.2 First Phase: Estimation of

Here, we introduce the estimation phase of for all . The pseudo-code of this phase is described in Algorithm 1. Algorithm 1 requires a positive number as a parameter, which will be set to . We perform experiments in this phase.

Before explaining the details of Algorithm 1, we note that can be calculated from . For , let

| (1) |

denote the set of realizations over that is consistent with the realization over and the intervention . If , then is then described as

| (2) |

Algorithm 1 consists of iterations. The -th iteration computes the following objects:

-

•

an estimate of ,

-

•

for each ,

-

•

an estimate of , and

-

•

.

We remark that in Algorithm 1 are used only for computing an estimate and are not used for estimating . An estimate of is computed in the next phase of our algorithm.

At the beginning of the -th iteration, we compute for each and by (2) substituting for ;

| (3) |

Let us confirm that this can be computed if () are available.

For each , then, we identify an intervention that attains . Using , we compute as follows, where is an extension of onto . We conduct experiments with . Let be the number of experiments in those experiments in which the obtained realization satisfies for each . Let be the number of experiments counted in , where also holds. We then compute using the equation

| (4) |

The vector is added to if

| (5) |

where is defined as

This reserves such that is too small to estimate with sufficient accuracy. Then is determined by replacing with for :

| (6) |

This replacement contributes to reducing the relative estimation error of in subsequent steps ().

After iterating for all , the algorithm computes and () defined by

| (7) | ||||

| (8) |

This contributes to bound the absolute error of the estimation of for . The algorithm returns an estimate and the family .

3.3 Second Phase: Estimation of

In this phase, our algorithm computes an estimate of for all . The pseudo-code for this phase is given in Algorithm 2. As an input, it receives and from Algorithm 1.

Algorithm 2 consists of two parts. The first part conducts experiments with (computed from , ) for each and . This is the same process used to compute in Algorithm 1. Let

where is the extension of onto with . Let us define a constant for each and . In the second part, the algorithm solves the following optimization problem:

| s.t. | (9) |

Note that, for each , only if according to Line 20 of Algorithm 1. Thus the denominator is positive for every , and the above optimization problem is well-defined. Let be an optimal solution for (9). Consider the distribution over that generates with a probability of . For times, the second part samples an intervention according to and uses it to conduct experiments.

For each and , the algorithm counts the number (resp., ) of experiments that result in with (resp., and ). Then, (, ) is defined by

| (10) |

The output defined by

| (11) |

3.4 Regret bound

Pseudo-code of our entire algorithm is provided in Algorithm 3. It computes an estimate of by Algorithm 1 and then computes by Algorithm 2. It then computes an estimate of by

| (12) |

for each . The algorithm returns an intervention that maximizes .

Let us define as the optimum value of the following problem:

| s.t. | (13) |

The regret bound of Algorithm 3 is parameterized by the optimum value :

Theorem 1.

The regret of Algorithm 3 satisfies

The notation is used here under the assumption that is sufficiently small with respect to but not negligible. The optimum value is bounded as follows. Let denote the number of nodes intervened by , i.e., :

Proposition 2.

It holds that .

Since the lower-bound for the general best-arm identification problem is [2][Theorem 4], our algorithm provides a better regret bound when the number of interventions is large compared to , which is only dependent on the causal graph structure.

Remark 3.

We present Algorithms 1, 2, and 3 for the setting that every is unknown. However, our algorithms can be applied even when is known for some and by incorporating minor modifications. In this case, we denote the number of unknown as . The modified algorithm just skips experiments for estimating the known , and we can define for such and . We then redefine by replacing corresponding with in (3.4), and our bound in Theorem 1 is valid for this reduced . In particular, we can recover the regret bound considered in [11][Theorem 3] as follows:

Corollary 4.

Suppose that is known for every and . Then the regret of Algorithm 3 satisfies , where

| s.t. |

Remark 5.

Our problem setting is often called hard intervention, which directly controls the realization of a node as . In contrast, Sen et al. [15] introduced the soft intervention model on a node where an intervention changes the conditional probability of a node . They in fact considered a simple case where a graph has a single node such that , whose conditional probability can be controlled by soft intervention. In their model, we are given a discrete set as the set of soft interventions. For and , define

as the probability of realizing under the soft intervention and the condition for . The goal is then to maximize the following probability:

Sen et al. [15] proved parameterized regret bound assuming that is known in advance.

We here remark that their model can be implemented by the hard intervention model as follows. Regard as the set of indices, and we add nodes for each to the graph. Every has only one adjacent edge from to . Observe that is the set of indices of nodes which are the parents of in the new graph. For , we define by

We consider the set of hard interventions , where each intervention is indexed by , and fixes the realization of the node as . More concretely,

Then the joint distribution over the nodes under the soft intervention is equal to the distribution under the corresponding hard intervention , and thus the soft intervention model is reduced to the hard intervention model.

4 Proofs

This section is devoted to proving Theorem 1. We introduce a series of well-known technical lemmas together with a novel variant of Hoeffding’s inequality in Section 4.1. In Sections 4.2 and 4.3, we ensure the accuracy of estimation in Algorithms 1 and 2, respectively, which are presented formally as Propositions 10 and 14. Section 4.4 then proves Theorem 1 and Proposition 2, whose statements are presented in the previous section.

4.1 Technical lemmas

We introduce Hoeffding’s inequality, Chernoff’s bound, and Hoeffding’s lemma as follows.

Proposition 6 (Hoeffding’s inequality).

For every , suppose that is an independent random variable over . We define and . Then for any we have

Proposition 7 (Chernoff’s bound).

For every , suppose that is an independent random variable over . We define and . Then we have

Proposition 8 (Hoeffding’s lemma).

Suppose that is a random variable over , and define . Then for any it holds that

The following statement is a variant of Hoeffding’s inequality, which is proven on the basis of Hoeffding’s lemma.

Lemma 9 (Variant of Hoeffding’s inequality).

For every and , let be a random variable over . For each , we assume that the variables in are independent and has the identical mean (i.e., for all ) under the condition that the variables in are fixed. For , let be a random variable over which is independent of if . Let be a finite set, and let , , and be arbitrary numbers given for each and . Then we have

Proof.

Let be the indicator function. For each , we introduce positive numbers , which will be optimized later. We note that holds if and only if

| (14) |

holds. Hence,

| (16) | |||

| (20) | |||

| (22) | |||

| (24) | |||

| (25) |

For bounding the first term of the right-hand side, by Markov’s inequality we have

| (26) |

for every . For every and , let us define a random variable

Then the right-hand side of (26) is equal to , and for each , it holds that

We bound inductively, as

where the first inequality follows from Proposition 8 by putting . Thus, by induction, we have

which implies

Putting

for each , we have

Thus the first term of (25) is bounded above by

| (27) |

4.2 Accuracy of Algorithm 1

For , let and be the stochastic estimates computed in Algorithm 1, and be the action determined from the estimate .

Let be defined by . Using , we define and as follows. For each and , we define by

For each , , and , we define by

| (28) |

Thus is obtained from by truncating its values if , and is defined from . We define and in the same way. Since , we observe that . Similarly, for , we define by

| (29) |

The following proposition demonstrates the error bound for outputs and from Algorithm 1.

Proposition 10.

Let and be the outputs of Algorithm 1 with parameter . Then the following holds with a probability of at least : for every , with , and :

| (30) | |||

| (31) | |||

| (32) | |||

| (33) |

We prepare the following three lemmas to prove Proposition 10. Let be the indicator function. The first lemma is an application of Chernoff’s bound, which bounds the relative estimation error on :

Lemma 11.

Let , , and .

(i) If , then the following holds with a probability of at least :

(ii) If , then the following holds with a probability of at least :

Proof.

The cases and are symmetric, and thus without loss of generality we can assume that . If , then for any and thus (i) immediately holds. Therefore the following discussion assumes that . Let be the obtained realization over experiments in Algorithm 1 with . Then we define i.i.d. random variables for by

Observe that for . We also define a random variable by

Then it holds that

| (34) |

Given for and , we define i.i.d. random variables for as follows: Let be the indices such that and for . Then, for each , a variable is defined by

Observe that . In addition, we define a random variable by

Then it holds that

| (35) |

and

| (36) |

(i) Let us define

Since , we have

| (37) |

Below we prove that

| (38) | |||

| (39) | |||

| (40) |

where the details of each transformation will be explained as follows.

(38) follows from the following equivalence:

Here, the first equivalence follows from (36), and the last equivalence follows from (35) and the definition of .

For (40), we first observe that since and . If , then Lemma 11 (i) is trivial. Hence we may assume that . Then,

| (41) |

Observe that

Here, the first inequailty is obtained by applying Proposition 7 to with , and the second inequality follows from (41). Then we have

Since and by (37), the right-hand side of this inequality is at least

The first inequality holds since and . This completes the proof of (i).

(ii) Putting , we prove that

| (42) | |||

| (43) | |||

| (44) | |||

| (45) |

where the details of each transformation will be explained as follows.

The second lemma bounds the gap produced by truncation of that is conducted for introducing and . We use the notation .

Lemma 12.

(i) Let and . For every , it holds that

(ii) For every , it holds that

Proof.

For , let be defined by

We define and by replacing by in the definition of and , respectively. By definition, we see and . Then it holds that

| (46) |

(i) We prove that

| (47) |

for every . This and (46) directly imply the desired bound (i). For and , observe that and differ only when and , which implies that and .

If , then it holds that

Suppose that the following holds for each :

| (48) |

Then we have (47) as follows:

Thus it suffices to prove (48) for every and .

Let and . Let us define

For , observe that

where is the concatenation of the three vectors with respective dimensions , , and . Thus it holds that

| (49) |

The second equality holds since for each , the sum in the above parenthesis is equal to . The inequality (48) and thus (i) hold.

(ii) For any and , we can apply the discussion for proving (49) to show

| (50) |

For , let be defined by

We define and by replacing by and in the definition of , respectively. Then it holds that

For the first term, observe that

The first inequality follows from (50). Thus we have

For the second term, since , we have

The first inequality follows from (50). Thus we have (ii). ∎

The third lemma bounds the relative error of . This statement can be proven by induction on the basis of Lemma 11.

Lemma 13.

The following holds for every , with , and with a probability of at least :

| (51) | |||

| (52) | |||

| (53) |

Proof.

We suppose that (51), (52), and (53) hold for every , , and , and will prove that, for and a single with ,

-

•

(51) holds for all ,

- •

Since , this indicates that (51), (52), and (53) hold for all combinations of , , and with probability at least .

For (51), observe that implies . Thus by (52) and (53), the following holds for every and , irrespective of whether or not:

| (54) |

Then for every , we have

The first inequality holds from (54), and the second inequality holds since and if . Thus the right inequality of (51) holds. Since , the left inequality is shown in the same way. Thus (51) holds for and all .

Proof of Proposition 10.

(31) also directly follows from the contraposition of (52), which states that: if , then . Recall that we are claiming (31) only for . Since , indicates . Hence the contraposition of (52) implies (31) for .

To prove (32), first we show that for every , , and it holds that

| (55) |

We prove the contraposition. Suppose that . Since by (53), we have

and thus .

By Lemma 12 (i), it holds that

Thus it suffices for proving (32) to show that, for , and

| (56) |

where denotes . Since the former follows from (51), (56) remains to be proven.

Observe that by (51) and the definition of . Then the following holds for every by (55):

| (57) |

Since , it holds that

| (58) |

Since , we have . Hence, Line 20 of Algorithm 1 implies that , which is equivalent to

| (59) |

4.3 Accuracy of Algorithm 2

This subsection bounds the gap between the true value and its estimate given by Algorithm 2, assuming that the input of Algorithm 2, which is output of Algorithm 1, satisfies the conditions in Proposition 10.

Proposition 14.

Recall that for . For and , let . For and , we define by

Observe that is given by replacing by for in the definition (29) of . Recall that is given by replacing in the definition of by for all . Based on these relationships, we have the following lemma:

Lemma 15.

For , it holds that:

| (63) |

Proof.

The first equality directly follows from the definition of . For the second,

The second equality holds by the binary expansion of . ∎

For , let . We provide probabilistic bounds for the linear terms () and super-linear terms () in (63), separately.

Lemma 16.

(i) The following holds with a probability of at least :

(ii) The following holds with a probability of at least :

Proof.

For , let be the intervention applied in the -th experiment in Algorithm 2, and be the corresponding realizations. For each , , and , we define a random variable by

We also define a random variable .

Let and . If the -th experiment adapts , then holds. Among the first experiments done in the algorithm, at least experiments adapt . Moreover, if , then the -th experiment adapts sampled from according to the probability . Hence holds for each . These imply that

| (64) |

holds, where

| (65) |

From (, , ), we define a random variable as follows for each : let be the indices such that for ; then

Let .

Let (resp., ) be the extension of such that (resp., ). Then it holds that

| (66) |

We also introduce by

| (67) |

where the inequality follows from (64). If , then or holds. Then by (31), (64), and (65), it holds that

since and by the assumption. Applying Proposition 7 to with , we have for ,

| (68) |

for and .

(i) First we prove that the following holds for every with probability :

| (69) |

For , define

| (70) | ||||

Since for any , we have

The fifth equality holds since implies . Let us define for by

Let us consider a unique correspondence between indices in Lemma 9 and pairs of elements where and , satisfying the following condition: if , , and , then it holds that . Under this relationship, the random variables and , respectively corresponding to and in Lemma 9, and the set of random variables satisfies the conditional independence assumption of Lemma 9. Thus we apply Lemma 9 with constants and for , , and , it holds that

The last inequality holds since (68) holds with a probability of at least for each and , where the number of such pair is at most . If

| (71) |

then it holds that

which and (67) show the probabilistic bound (69). Thus it is suffices to prove (71).

Recall that, for , , and , defined in (1) is the set of realizations which coincides with and . Since

it holds for that

| (72) |

This implies (71).

We now prove (i) on the basis of (69). Let be the optimum solution corresponding to . Then the RHS of (69) can be bounded as:

| (73) |

The first equality holds by the definition (65) of . The last inequality follows from the fact and (30), which implies , , and . Observe then that, removing the square root and ignoring the coefficient , (73) coincides with the subject of minimization in (9), whose optimum solution is . Thus the replacement of by provides an upper-bound, and we have

| (74) | ||||

The second inequality follows from the application of (32) to the denominator, and the third inequality follows from (30) again, as . Since holds for every , we have the last inequality. Then (74) is the subject of minimization in (3.4), whose optimum solution is with optimum value . Thus we have the last equality, and the proof of (i) is complete.

(ii) We first show that

| (75) |

holds for every and with a probability of at least . Since the number of such pair is , it suffices to show that for each , (75) holds with a probability of at least . If , which implies , then the above is trivial. If , then (31) holds. Similarly to the discussion as Lemma 11 (ii), the following holds for each with probability :

In fact, by (34), (64), and (65), the expected number of samples available for estimating in Algorithm 2 is larger than that for in Algorithm 1, and thus the same probabilistic bound on estimation error holds. Thus, whichever or not, (75) holds with a probability of at least for a pair of .

Suppose that the inequality (75) holds for every and , which is attained with a probability of at least . Observe that

| (76) |

The first equality follows from the definition of , and the second and the third equalities follow from suitable arrangement of indices for summations. Since (75) holds for every and , the value in the parenthesis in (76) can be bounded by

The last inequality holds since . Putting this into (76), we have

| (77) |

The second equality follows from the definition (70) of , and the third equality holds since for and for every and . The inequality follows from (72). The last equality then follows from the definition of and (66). Since , by applying Proposition 6 to independent variables for over with , it holds that

| (78) |

Thus, by (77) and (78), the following holds for every with probability at least :

The second inequality follows from (67), the third inequality follows from (65). Since by (30), we have

The last inequality holds since and . Thus, if (75) holds for every and , which is attained with a probability of at least , then the desired probabilistic bound (ii) holds with a probability of at least . This directly implies that the bound (ii) holds with a probability of at least . ∎

The above two lemmas imply Proposition 14 as follows.

4.4 Proof of Theorem 1 and Proposition 2

Proof of Theorem 1.

We put . From Propositions 2, 10, and 14, the following holds for every with probability at least :

Let us define and . It then holds that

| (79) | ||||

| (80) | ||||

| (81) |

The first inequality holds since is the maximizer of and thus . Thus the difference between and is bounded by (81) with a probability of at least , which implies the desired regret bound:

∎

We conclude this section by proving Proposition 2, whose proof is independent of the above series of discussions.

Proof of Proposition 2.

We first show the left inequality. It holds that

The last inequality holds by letting , noting that

For each and the minimization problem with respect to is a convex optimization problem, where the minimum is attained when . Hence the above lower bound is equal to

This proves the left inequality.

We next prove the right inequality. For each and , let be an intervention that attains . Note that, if such is not unique, then we choose one of them. Consider the solution such that for each . Let us confirm that, since the number of pairs is exactly equal to , it holds that , and thus is in fact a feasible solution for the minimization problem. For each , it holds that , and thus we have

Hence it holds that

Also, consider for all . Then, since for any , it holds that

Thus we have the statement. ∎

5 Experiments

We now demonstrate the performance of the proposed algorithm through experimental evaluations and compare it with a baseline algorithm [2] which was proposed for the general best arm identification problem and thus cannot take advantage of given side-information of causal graph structure.

5.1 Instances

We evaluated the algorithms on both synthetic and real-world instances. Recall that an instance of the causal bandit problem consists of a DAG , an intervention set , and .

In the synthetic instances, the DAG is defined as a directed complete binary tree of height , where each edge is oriented toward the root. From this construction, the number of nodes is , which consists of leaves (nodes without incoming edges) and non-leaves. Then the number of uncertain parameter is in these instances.

In the real-world instances, the DAG is constructed from the Alarm and the Water data sets in a Bayesian Network Repository111http://www.cs.huji.ac.il/~galel/Repository/. The numbers of nodes in the DAGs constructed from Alarm and Water data sets are 37 and 32, respectively. We consider interventions on nodes that have no incoming edge. for the instances with Alarm data set, and for the instances with the Water data set.

For each , we consider interventions over all leaves which fixes exactly nodes as and the others as . We call this parameter budget, and the number of intervention is then controlled by the budget. In both of the synthetic and the real-world instances, the budget varies among . In the synthetic instances, the numbers of interventions are 120, 1820, and 12870 for , respectively. In the instances with the Alarm data set, the numbers of interventions are 78, 793, and 3796 for , respectively. In the instances with the Water data set, the numbers of interventions are 36, 126, and 256 for , respectively.

For each and , we generate from the uniform distribution over .

For each of those instances, we executed the algorithms 10 times and compared their average regrets.

5.2 Implementation of the proposed algorithm

Our algorithm given in Section 3 is designed conservatively to obtain the theoretical regred bound (Theorem 1), and there is a room to modify the algorithm to be more efficient in practice although the theoretical regret bound may not hold for it. In our implementation, we introduced the following three modifications into the proposed algorithm. First, while Algorithm 2 discards samples obtained for computing in Algorithm 1 to maintain the independence between and , we use all of them also in Algorithm 2 in our implementation. Next, we ignore the truncation mechanism of Algorithm 1 by setting . We expect these two modifications make the estimates of the algorithm more accurate. Finally, instead of solving (9), we set by if for some and , and otherwise. Since it is time-consuming to solve (9), this modification makes the algorithm faster.

5.3 Experimental results

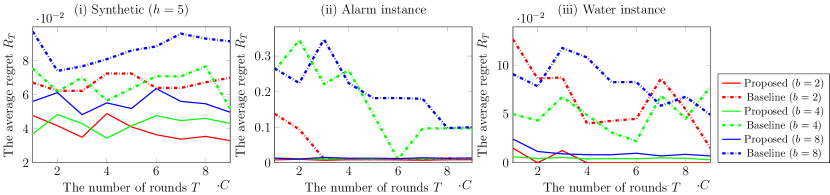

Figure 2(i) shows the average regrets over the synthetic instances against the number of rounds . Figures 2(ii) and (iii) respectively illustrate the average regrets for the real-world instances constructed from the Alarm and the Water data sets.

The results show that the proposed algorithm outperforms the baseline in every instance. In particular, the gap is remarkably large () in the Alarm data set (ii) with a large number of interventions (, corresponding to , respectively,) and a small number of samples (). In these cases, the baseline cannot apply every intervention at least once. On the other hand, the regret of the proposed algorithm only grows slowly with respect to the number of arms , in all instances. Thus the proposed algorithm provides effective regret, even when the number of interventions is times larger than the number of experiments .

6 Conclusion

In this paper, we proposed the first algorithm for the causal bandit problem, where existing algorithms could deal with only localized interventions, and proved a novel regret bound which is logarithmic with respect to the number of arms. Our experimental result shows that the proposed algorithm is applicable to systems where the number of interventions is much larger than . One important future research direction would be to prove the gap-dependent bound as [15] has proven for localized interventions. Another research direction, which is mentioned in [11], would include incorporation of a causal discovery algorithm to enable the estimation of the structure of a causal graph, which is currently assumed to be known in advance.

References

- [1] Alekh Agarwal, Daniel Hsu, Satyen Kale, John Langford, Lihong Li, and Robert Schapire. Taming the monster: A fast and simple algorithm for contextual bandits. In International Conference on Machine Learning, pages 1638–1646, 2014.

- [2] Jean-Yves Audibert and Sébastien Bubeck. Best arm identification in multi-armed bandits. In The 23rd Conference on Learning Theory, pages 41–53, 2010.

- [3] Peter Auer, Nicolo Cesa-Bianchi, Yoav Freund, and Robert E Schapire. The nonstochastic multiarmed bandit problem. SIAM Journal on Computing, 32(1):48–77, 2002.

- [4] Léon Bottou, Jonas Peters, Joaquin Quiñonero-Candela, Denis X Charles, D Max Chickering, Elon Portugaly, Dipankar Ray, Patrice Simard, and Ed Snelson. Counterfactual reasoning and learning systems: The example of computational advertising. The Journal of Machine Learning Research, 14(1):3207–3260, 2013.

- [5] Frederick Eberhardt, Clark Glymour, and Richard Scheines. On the number of experiments sufficient and in the worst case necessary to identify all causal relations among n variables. In Proceedings of the Twenty-First Conference on Uncertainty in Artificial Intelligence, pages 178–184. AUAI Press, 2005.

- [6] Victor Gabillon, Mohammad Ghavamzadeh, and Alessandro Lazaric. Best arm identification: A unified approach to fixed budget and fixed confidence. In Advances in Neural Information Processing Systems, pages 3212–3220, 2012.

- [7] Alain Hauser and Peter Bühlmann. Two optimal strategies for active learning of causal models from interventional data. International Journal of Approximate Reasoning, 55(4):926–939, 2014.

- [8] Huining Hu, Zhentao Li, and Adrian R Vetta. Randomized experimental design for causal graph discovery. In Advances in Neural Information Processing Systems, pages 2339–2347, 2014.

- [9] Emilie Kaufmann, Olivier Cappé, and Aurélien Garivier. On the complexity of best-arm identification in multi-armed bandit models. The Journal of Machine Learning Research, 17(1):1–42, 2016.

- [10] Dan J Kim, Donald L Ferrin, and H Raghav Rao. A trust-based consumer decision-making model in electronic commerce: The role of trust, perceived risk, and their antecedents. Decision Support Systems, 44(2):544–564, 2008.

- [11] Finnian Lattimore, Tor Lattimore, and Mark D Reid. Causal bandits: Learning good interventions via causal inference. In Advances in Neural Information Processing Systems, pages 1181–1189, 2016.

- [12] Nicolai Meinshausen, Alain Hauser, Joris M Mooij, Jonas Peters, Philip Versteeg, and Peter Bühlmann. Methods for causal inference from gene perturbation experiments and validation. Proceedings of the National Academy of Sciences, 113(27):7361–7368, 2016.

- [13] Joris M Mooij, Jonas Peters, Dominik Janzing, Jakob Zscheischler, and Bernhard Schölkopf. Distinguishing cause from effect using observational data: methods and benchmarks. The Journal of Machine Learning Research, 17(1):1103–1204, 2016.

- [14] Judea Pearl. Causality. Cambridge university press, 2009.

- [15] Rajat Sen, Karthikeyan Shanmugam, Alexandros G Dimakis, and Sanjay Shakkottai. Identifying best interventions through online importance sampling. In International Conference on Machine Learning, pages 3057–3066, 2017.

- [16] Karthikeyan Shanmugam, Murat Kocaoglu, Alexandros G Dimakis, and Sriram Vishwanath. Learning causal graphs with small interventions. In Advances in Neural Information Processing Systems, pages 3195–3203, 2015.

- [17] Shohei Shimizu, Takanori Inazumi, Yasuhiro Sogawa, Aapo Hyvärinen, Yoshinobu Kawahara, Takashi Washio, Patrik O Hoyer, and Kenneth Bollen. Directlingam: A direct method for learning a linear non-gaussian structural equation model. Journal of Machine Learning Research, 12(Apr):1225–1248, 2011.

- [18] Peter Spirtes and Clark Glymour. An algorithm for fast recovery of sparse causal graphs. Social Science Computer Review, 9(1):62–72, 1991.

- [19] Jerzy Splawa-Neyman, Dorota M Dabrowska, and TP Speed. On the application of probability theory to agricultural experiments. essay on principles. section 9. Statistical Science, pages 465–472, 1990.