∎

Wellington 6140, New Zealand

22email: thuong.nguyen@vuw.ac.nz

Distribution free goodness of fit tests for regularly varying tail distributions

Abstract

We discuss in this paper a possibility of constructing a whole class of asymptotic distribution-free tests for testing regularly varying tail distributions. The idea is that we treat the tails of distributions as members of a parametric family and using MLE to estimate the exponent. No matter what the exponent’s estimator is, we are able to transform the whole class into a specific distribution with a prefix exponent so that we are free from choosing any functional of the tail empirical process as a distribution-free test statistic. The asymptotic behaviour of some new tests, as examples from the whole class of new tests, are demonstrated as well.

Keywords:

Regularly varying distribution free goodness of fit testunitary transformation.1 Introduction

Suppose that we have a random sample of a random variable following some unknown distribution . No matter how behaves, we are mainly interested in the right tail behavior of , i.e., in when . Among the class of heavy-tail distributions, regularly varying tail distributions has been attracted most attention due to its various applications. Briefly, a distribution is said to be regularly varying in tail if

| (1) |

for all where is called the index or exponent of regular variation. By this definition, regularly varying tail distributions are often indicated as Pareto-type distributions.

Regular variation of the tail of a distribution often appears as a natural condition in various theoretical results of probability theory. The most typical example is that it is the condition for the distribution of the partial maxima to belong to the domain of attraction of extreme value distributions. This could be found in various references, we refer to books of de Haan and Ferreira deHaanbook and Resnick Resnick among others. Moreover, regular variation naturally arises as a common phenomenon in numerous practical case studies such as finance, insurance, physics, geology, hydrology and engineering, etc. Therefore, detecting and testing regular variation plays an important role in probabilistic areas as well as in practical applications.

The problem of estimating the exponent has a very rich literature. Among various studies, the Hill estimator is the most common one, see Hill Hill . Recall that the Hill estimator of the exponent essentially takes on the following form

| (2) |

where is a certain sample fraction, in an appropriate way and denotes the upper order statistics of the sample . Many other estimators was proposed, most of them is also based on the upper order statistics and is not too difficult to compute. These include, to name a few, popular estimators introduced by Dekkers et. al. Dekkersetal , de Haan and Resnick DeHaan , Pickands Pickands , Teugels Teugels among others. The rate of the convergence of an estimator was also discussed, for example, in Hall and Welsh Hall84 .

In contrast to the numerous number of approaches to estimate the exponent , using goodness of fit (gof) for testing regular variation has been addressed in a modest number of studies. Not long ago, Beirlant et al. Beirlantetall modified the Jackson statistic - which was originally proposed as a gof for testing exponentiality - for testing Pareto-type data. Koning and Peng Koning examined the Kolmogorov-Smirnov, Berk-Jones and the estimated score tests and compare them in terms of Bahadur efficiency. In that paper, the Berk-Jones and estimated score tests, which are not based on the empirical process, were shown to perform better than the Kolmogorov-Smirnov test.

Note that regularly varying tail distributions are members of the family of the generalized Pareto distribution (GPD), which is of the form

| (3) |

where and are shape and scale parameters and . To test the fit of data to a GDP, there has been several studies such as Davison and Smith Davison , Choulakian and Stephens Choulakian . In these papers, the critical values for Cramer-von Mises statistic and Anderson-Darling statistic, which is a weighted Cramer-von Mises statistic, were given.

In this paper, we will introduce a wide class of asymptotically distribution free gof tests for testing regularly varying tail distributions. Our approach follows a new method introduced in Khmaladze Estate2 . In that paper, the author proposed a unitary transformation which enables us to create a class of gof tests for both simple and parametric hypothesis testing problems. The method for the latter will be adopted for our problem, which we will present in Section 2.2. Briefly speaking, we will use exactly the same transformation in Estate2 to derive a modification of the empirical process. Only this time, the assumption that belongs to a parametric family of distributions is no longer available and the fact is that the right tail just partially describes the distribution . Hence, we can only consider the tail empirical process and transform it. The transformed tail empirical process, under the hypothesis of interest, possesses a limit in distribution asymptotically free from any underlying distribution as well as the unknown index/exponent of the regular variation. Therefore, any appropriate functionals of the transformed process could be used as asymptotically distribution free test statistics. Section 2.1 will be devoted for the main literature of the empirical process based on the tail.

Some simulation results will be documented in Section 3. Namely, we will take the Kolmogorov-Smirnov (KS), Cramer-von Mises () and Anderson-Darling () tests as examples from the new class of asymptotically distribution free gof tests for demonstration. The asymptotically distribution free property of these test statistics will be illustrated for different choices of the original distribution .

2 Main results

2.1 Overall review

Suppose that from a random sample we are only considering excesses over a certain threshold which is considerably large. Let us denote the subsample of all observations exceeding by . Generally, the choice of as well as the sample fraction may require some educated guessing. Hill Hill suggested be chosen as an adaptive, data-analytic basis. Several methods for choosing or based on survey data could be found in Drees and Kaufmann Drees , Danielsson et al. Danielsson and Guillou and Hall Guillou . Nevertheless, there has existed various research assuming that is known such that as but . With this assumption and some prior knowledge about the underlying distribution function , Haeusler and Teugels Haeusler derived a general condition which can be used to determine the optimal value explicitly. Hall Hall82 also considered having a deterministic value and a quite common estimate of the exponent was introduced. Throughout this paper, our approach will be based on the same such assumption, that also means fixed.

Our main aim is to create a class of gof test for testing the hypothesis “ is a regularly varying tail distribution” against the alternative “ is not a regularly varying tail distribution”. It is sensible that the exponent needs to be estimated based on the right tail only. Specifically, we only consider observed values , which now should be looked at as a sample of a different random variable, let say, .

Denote and . Under the hypothesis of interest and by the definition of the regular variation, the survival distribution of conditional on the specified large value is

| (4) |

Then, the distribution of the positive continuous random variable under the null hypothesis is

| (5) |

Clearly, the density function is Viewing as a new random variable, we can define the tail empirical process in a similar way as of the standard empirical process, i.e., we have

| (6) |

The tail parametric empirical process is

| (7) |

where is an estimator of calculated from the subsample (or ). Assume that the true unknown exponent under the hypothesis is . Let be the maximum likelihood estimator (MLE), then it is the solution of the equation

| (8) |

That yields

| (9) |

which actually coincides with the Hill estimator . This estimator was proved to be consistent in the sense that

| (10) |

under the condition that as such that . The proof of this convergence could be found in Mason Mason . Regarding the asymptotic normality of the estimator, we refer to Haeusler and Teugels Haeusler , Geluk et al. Geluketal. , de Haan and Resnick deHaanRes among various others.

We will spend few more lines here to review the property of the limit in distribution of the process because it is essential for the method we present below. For all the concepts and terminologies, we follow and keep the same as in Estate2 . For the sake of lucidity, we extract and represent the method only for our particular problem.

Consider the space . Recall that a function is integrable with respect to if and square integrable if . The space consists of all square integrable functions with respect to . The inner product and norm in are defined as usual. That is, for any we have

Denote by a function-parametric -Brownian motion where is a square integrable function in . That means, for each is a Gaussian random variable with expected value and variance This also implies that the covariance between and is

If then is simply the Brownian motion in time As usual, a linear transformation of which is of the form is the Brownian bridge in time

Assuming that under the null hypothesis the true unknown exponent of the regular variation is . Denote by the usual tail empirical process, that is,

| (11) |

Let us stress that, since we assumed is known, the limit in distribution of , as a conditional tail empirical process, is similar to that of the standard empirical process, which is the Brownian bridge . For a full description on the property of general tail empirical process, we refer to Einmahl Einmahl90 ; Einmahl92 . It was proved in these papers that if such process is unconditional on , the limit in distribution of is a Brownian motion in time . On a recent approach on distribution free gof test for testing tail copula by Can et al. Canetal , the tail empirical process - constructed on tail copula, was mapped to a standard Brownian motion. Their construction based on the innovative martingale method in Khmaladze Estate1 which is known as the Khmaladze transformation. Our approach here use a different Khmaladze transformation in Estate2 , and so let us call it Khmaladze-2.

Considers the function-parametric version of the tail empirical process

| (12) |

where is a function in . In a similar way to achieve the limit of , the limit in distribution of with some proper restriction on functions is called a function-parametric -Brownian bridge. Specifically,

| (13) |

where stands for the function identically equals to .

We can also say more about the asymptotic behavior of the tail parametric empirical process where is the MLE which is also the Hill’s estimator. It is well-known since long ago that under some usual and mild constraints, MLE possesses the asymptotic property

| (14) |

where denotes the hypothetical density and its derivatives in . Denote by

| (15) |

the Fisher information. Then it is easy to check that As a consequence of (14), we can expand the process as

| (16) |

where

| (17) |

denotes the normalized score function. This expression represents the limit in distribution of the process , that is, an orthogonal projection of the process parallel to the normalized score function . Note that by its definition is of unit norm in the space . Moreover, functions and are orthogonal. Therefore, from (2.1) we have the limit in distribution of the process is

| (18) |

This implies that is an orthogonal projection of the function-parametric -Brownian motion parallel to the subspace generated by 2 functions . The process depends not only on the true unknown exponent but also the score function . In the terminology of Estate2 , the process is called a -projected H-Brownian motion.

2.2 Method

Our approach follows the method in Khmaladze Estate2 for parametric family of distributions. The main idea can be briefly explained as follows: Under the null hypothesis, the empirical process (see (7) and (12)) constructed on the tail of an unknown distribution , from a fixed threshold , possesses an “unspecified” limit in distribution (see (2.1)). “Unspecified” here means that the limit depends on some unknown parameter. We will map the process into another process (see (22)) whose limit in distribution is specified. The mapping procedure is one-to-one to guarantee that no statistical information is lost.

We chose to be the exponential distribution simply by preference with some reasons. That is, both and are members of the GPD family (see (3)). The distribution is the limiting distribution of the GPD as and scaled by . A research by Davison and Smith Davison employed Kolmogorov-Smirnov and Anderson-Darling statistics to test the fit of the GPD to data using the critical value derived from an exponential distribution for the purpose. They discussed that the approach may be suspect since the exponential distribution is just a member of the whole family though.

It is obvious that distributions and are equivalent or in other words, mutually absolutely continuous. It is also easy to check that the Fisher information of is . Put

then this function belongs to . In addition, if then and Note that when and are equivalent, it is known that a transformation from a -Brownian motion into a -Brownian motion is straightforward by multiplication. Namely, is a G-Brownian motion in . However, mapping a Brownian bridge such as or to another Brownian bridge is not that straightforward any more. The fact is that depends on both and and so does .

Consider a subspace of generated by four functions . These functions are of unit norm in . More explicitly, the score functions and are

| (19) |

For any function and in , define the unitary operator as

where is the identity function. This unitary operator will turn the function into and reversely to and any function which is orthogonal to and in the subspace into itself.

Step into the method, we first consider the unitary operator

| (20) |

This operator will map to and to Next, consider the image of the function via , which is

Then consider the operator defined as

Set , then this unitary operator will map to and to . The non-uniqueness of such unitary operator like was discussed thoroughly in Khmaladze Estate2 , Section 3.4. Nevertheless, we believe that this operator is simple enough for practical purpose, especially with only one parameter.

The main result for testing composite hypothesis was stated as Theorem 7 in Estate2 , it is essential so we restate it here accordingly to our notations.

Theorem 2.1

(Restatement of Theorem 7 in Estate2 )

If is a -projected -Brownian motion and is absolutely continuous with respect to , then

| (21) |

is a -projected G-Brownian motion.

As a consequence, transform the function-parametric tail empirical process by , we obtain another process

| (22) |

which has as a limit in distribution.

Let

be series of indicator functions defined on depending on . Let runs from to . From Theorem 2.1, we know that the limit in distribution of the process is a -projected G-Brownian motion in . Hence, any statistic as an appropriate function based on will be asymptotically distribution free. Denote by the image of via the operator , that is,

For practical purpose, the form of is

| (23) | ||||

Applying the unitary operator on the process we have

| (24) |

Here denotes the expected value with respect to the distribution . That means, for any integrable function . As a result of the Theorem 2.1, the limit in distribution of process is - a projected -Brownian motion. We demonstrate in the next Section that any functionals of is asymptotically distribution free.

3 Simulation results

The main purpose of this section is to show the asymptotically distribution free property of the new test statistics based on the transformed empirical process . To do so, we will take some prevalent gof tests as examples, namely the Kolmogorov-Smirnov (KS), the Cramer-von Mises and the Anderson-Darling tests. These test statistics are some specific functionals of the transformed process . Namely, an analogue version of the Kolmogorov-Smirnov test statistic is

| (25) |

The Cramer-von Mises statistics should be of the form

| (26) |

and its weighted version called Anderson-Darling statistic is

| (27) |

As shown in Section 2.2, the limit in distribution of the process is a projected Brownian motion in time . Hence, theoretically these test statistics are asymptotically distribution free. Especially, it makes sense that we integrate with respect to nothing else but in order to get the and tests. In principle, runs from to infinity. However, we choose since hence we practically just need as the maximum value for . The and tests can be approximated as follows:

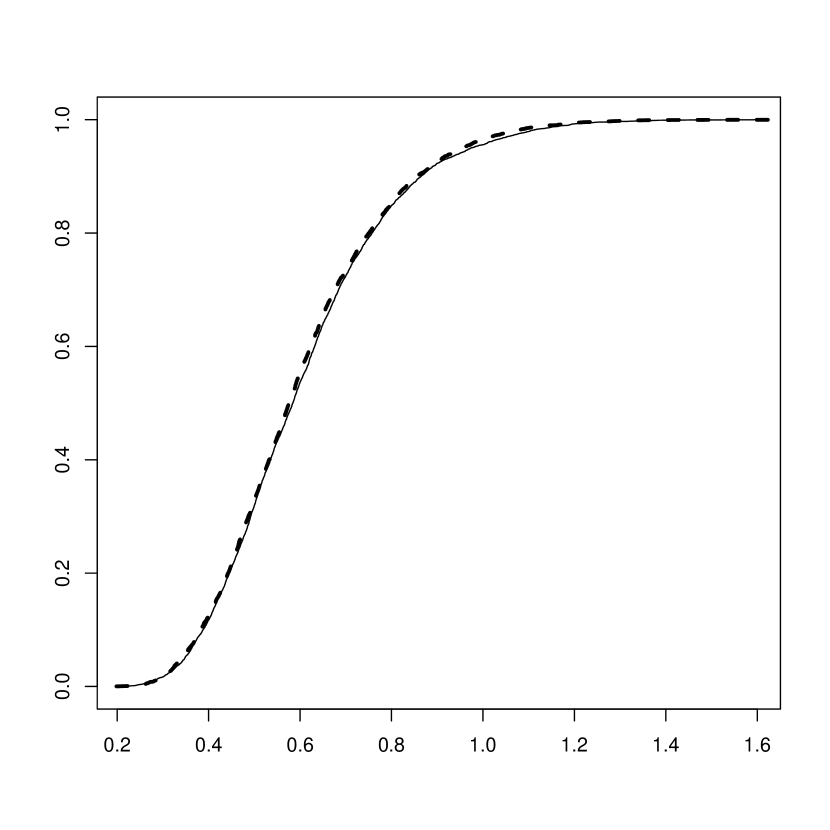

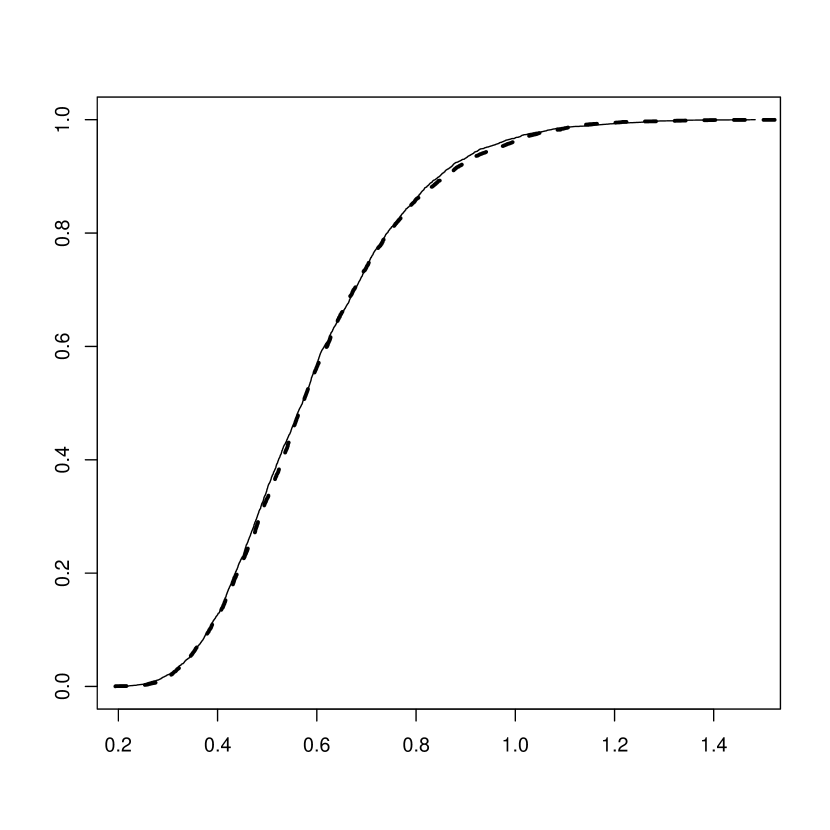

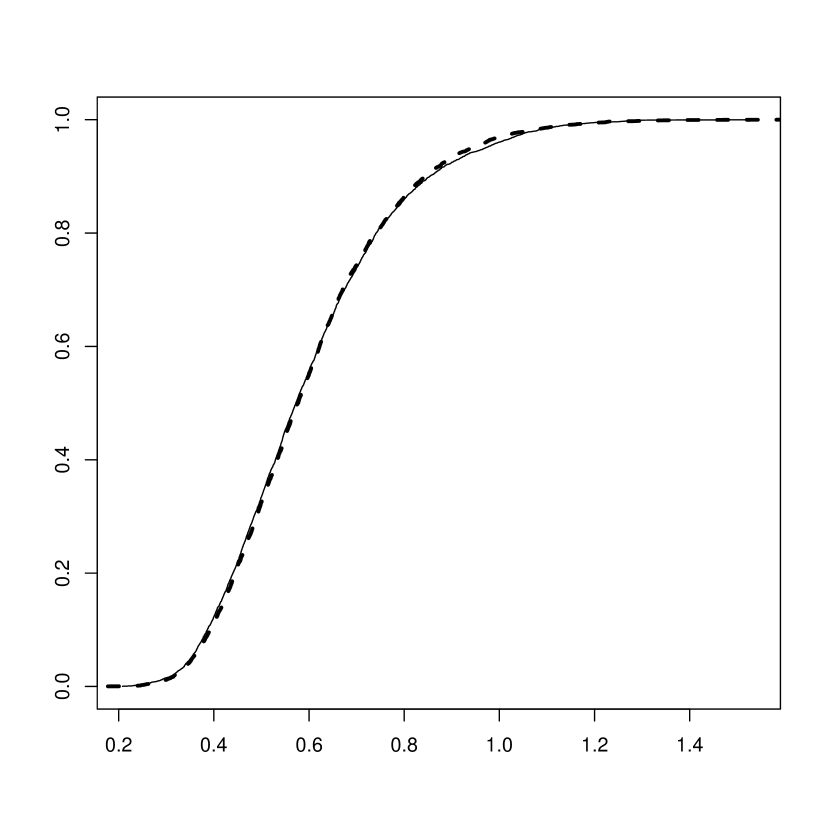

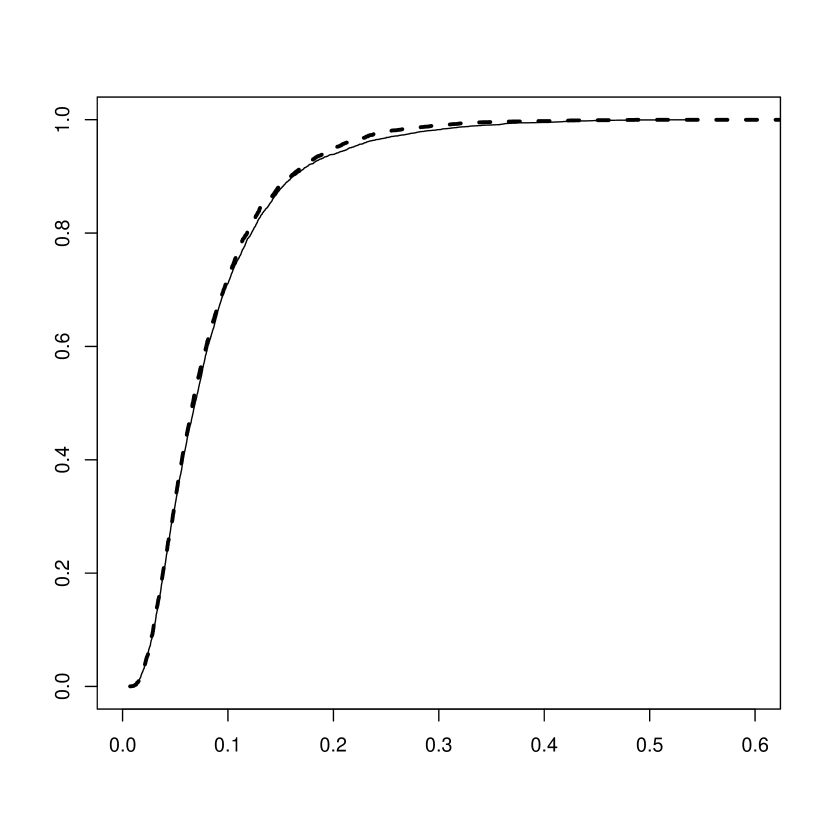

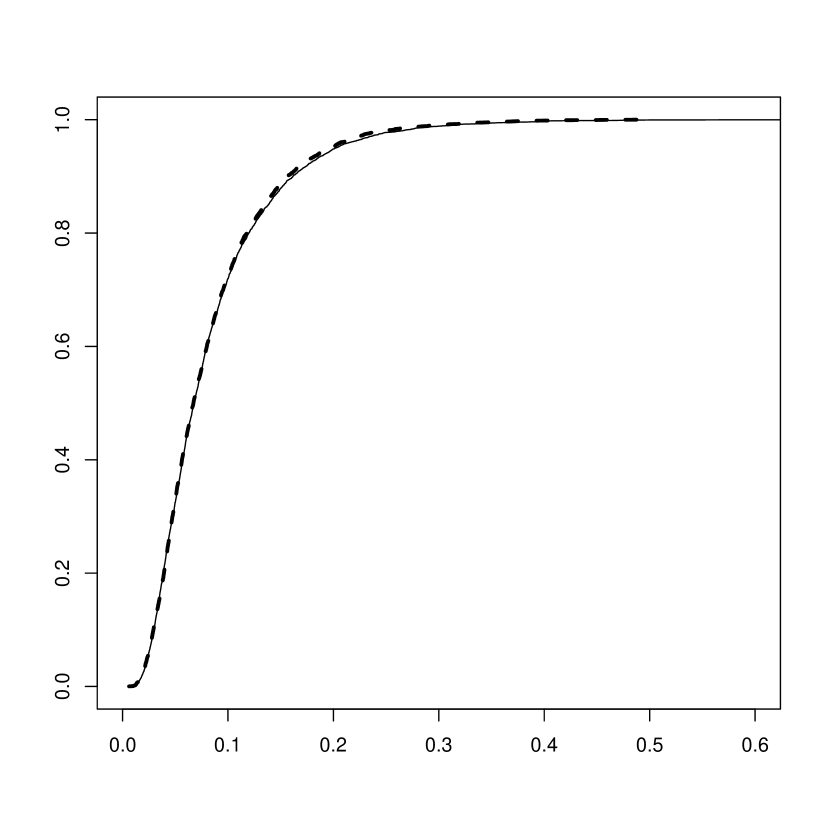

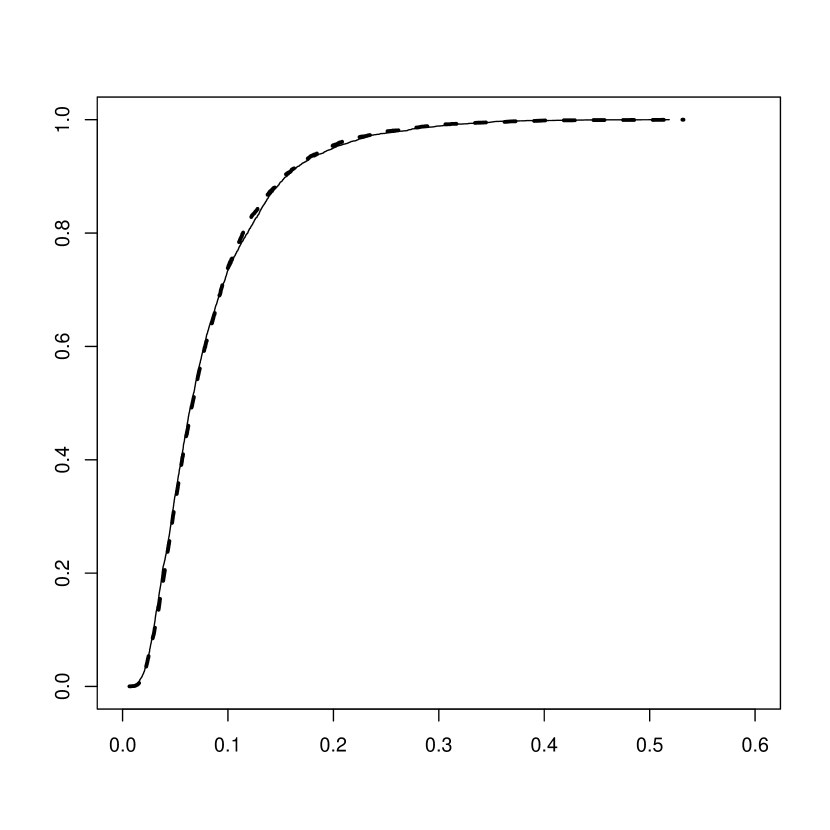

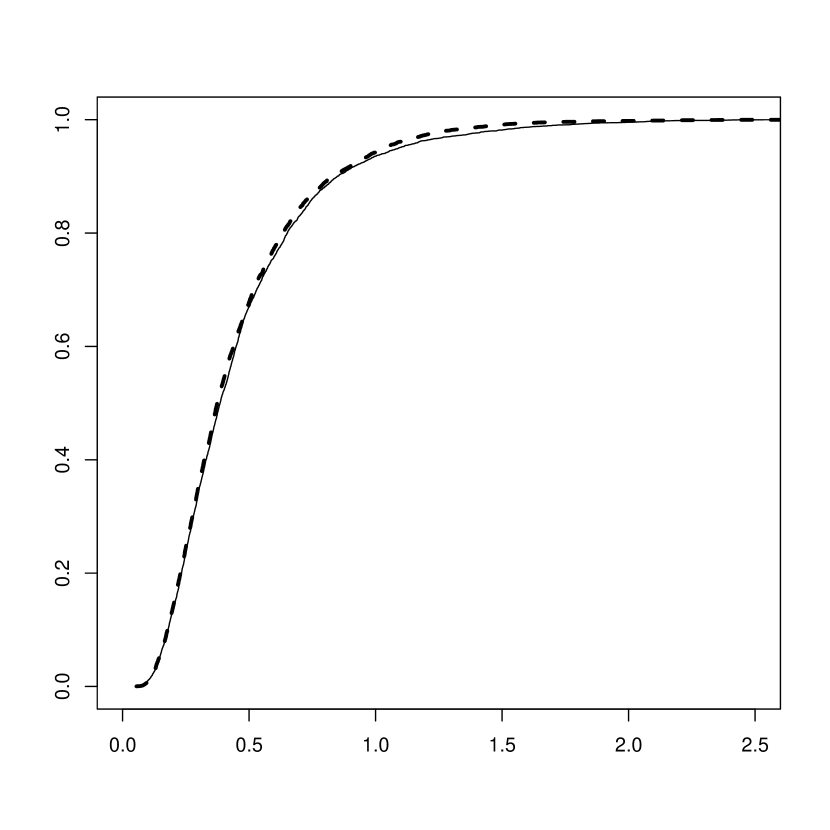

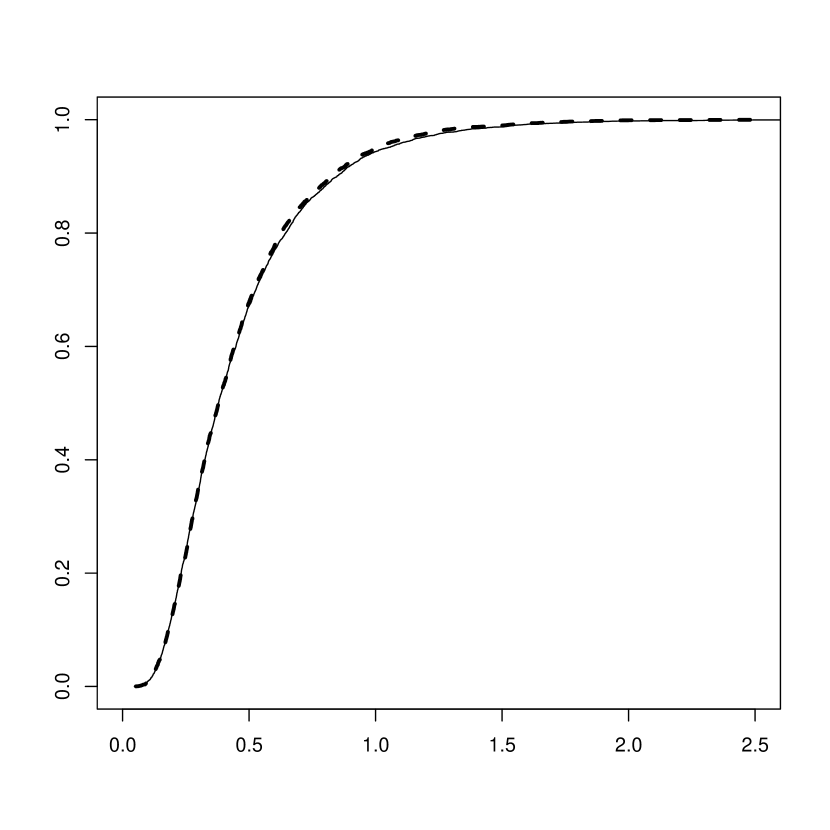

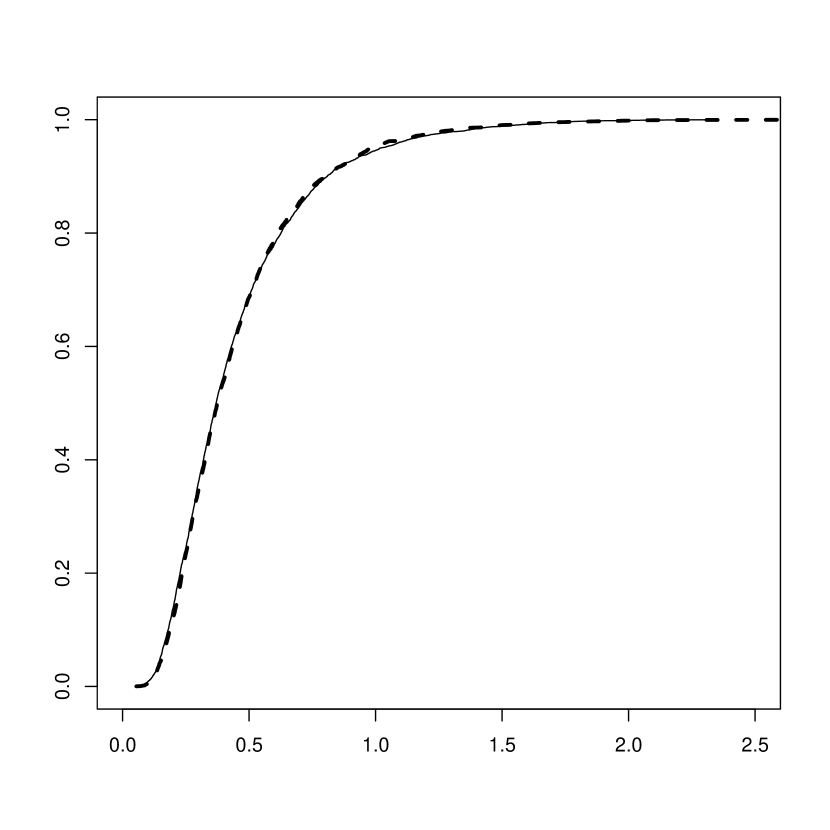

To create the curves of the cumulative distributions of the new tests, we choose Pareto and Cauchy distributions as the underlying distributions. It is known that the tail of the Cauchy distribution is regularly varying with the exponent . For the Pareto distributions, the exponent is arbitrarily selected and positive. We did choose some ranging from to . Sample size for simulation needs to be large to guarantee that the tail is sufficiently big, namely, is not less than . Hence, we chose at least equals . We also chose different threshold , namely . Usually, each curve is produced by iterations of simulation.

Figures 1, 2 and 3 show the plots of the cumulative functions for test statistics respectively with different choices of the threshold , different sample sizes and different underlying distributions. As we can see in these figures, the two curves of the cumulative distribution functions in each plot are not distinguishable, which practically demonstrate the asymptotically distribution free property of the new test statistics. Moreover, as we notice, for different , the difference between these curves is also very minor.

Regarding the time of the procedure, it took approximately hour to create the cumulative distribution functions with and sample size by iterations for two different original distributions . Therefore, we believe that the method is easy to implement and also quick.

4 Discussion

It is possible to extend this approach to testing multidimensional regularly varying tail distributions. As long as we are able to find a transparent expression for the class of regularly varying tail distributions with an explicit parametric family form, we are able to transform the whole family into a specific distribution, from that we can build up a whole class of asymptotic distribution-free test statistics.

Acknowledgements

The author is greatly indebted to Professor Estate Khmaladze for his invaluable suggestion for approaching this problem and many useful discussions during this research. This research was conducted during the author’s doctorate of philosophy degree, so the author would also like to thank Victoria University of Wellington for providing the doctoral scholarship to conduct this research.

References

- (1) Beirlant, J., de Wet, T. and Goegebeur, Y., A goodness of fit statistic for Pareto-type behaviour, Journal of Computational and Applied Mathematics, 186, pp. 99-116, (2006)

- (2) Can, S. M, Einmahl, J. H. J, Khmaladze, E. V and Laeven, R. J. A., Asymptotically distribution-free goodness-of-fit testing for tail copulas, Ann. Statist., 43 (2), pp. 878-902, (2015)

- (3) Choulakian, V. and Stephens, M. A., Goodness of fit tests for the generalized Pareto distribution, Technometrics, 43, No. 4, pp. 478-484, (2001)

- (4) Danielsson, J., de Haan, L., Peng, L. and de Vries, C. G., Using a bootstrap method to choose the sample fraction in tail index estimation, Journal of Multivariate Analysis, 76, No. 2, pp. 226-248, (2001)

- (5) Davison, A. C., Smith, R. L., Models for exceedances over high threshold, J. Roy. Statist. Soc. Ser. B: Methodological 52 (3), pp. 393-442, (1990)

- (6) De Haan, L. and Resnick, S. I., A simple asymptotic estimate for the index of a stable distribution, J. R. Statist. Soc. B, 42, pp. 83-88, (1980)

- (7) De Haan, L. and Resnick, S. I., On asymptotic normality of the Hill estimator, Comm. Statist. Stochastic Models, 14(4), pp. 849-866, (1998)

- (8) De Haan, L. and Ferreira, A., Extreme value theory, Springer, (2006)

- (9) Dekkers, A. L. M., Einmahl, J. H. J. and de Haan, L., A moment estimator for the index of an extreme value distribution, Ann. Statist., 17, pp. 1833-1855, (1989)

- (10) Dietrich, D., de Haan, L. and Husler, J., Testing extreme value conditions, Extremes, 5, 71-85, (2002)

- (11) Drees, H. and Kaulfmann, E., Selecting the optimal sample fraction in univariate extreme value estimation, Stochastic Processes and their Applications, 75, No. 2, pp. 149-172, (1998)

- (12) Drees, H., de Haan, L., Li, D., Approximations to the tail empirical distribution function with application to testing extreme value conditions, J. Statist. Plann. Inference, 136, pp. 3498-3538, (2006)

- (13) Einmahl, J. H. J, The empirical distribution functions as a tail estimator, Statist. Neerlandica, 44, pp.79-82, (1990)

- (14) Einmahl, J. H. J, Limit theorems for tail processes and application to intermediate quantile estimation, J. Statistical Planning and Inference, 32, pp. 137-145, (1992)

- (15) Hall, P., On some simple estimates of an exponent of regular variation, J. R. Statist. Soc. B, Vol. 44, No. 1, pp. 37-42, (1984)

- (16) Hall, P. and Welsh, A. H., Best attainable rates of convergence for estimates of parameters of regular variation. Annals of Statistics, 12(3), pp. 1079-1084, (1984)

- (17) Haeusler, E. and Teugels, J. L., On asymptotic normality of Hill’s estimator for the exponent of regular variation. Annals. Statist., 13(2), pp. 743-756, (1985)

- (18) Hill, B. M., A simple general approach to inference about the tail of a distribution. Annals. Math. Statist., 3, pp. 1163-1174

- (19) Geluk, J., de Haan, L., Resnick, S. and Starica, C., Second-order regular variation, convolution and the central limit theorem, Stochastic Processes and their applications, 69(2), pp. 139-159, (1997)

- (20) Guillou, A. and Hall, P., A diagnostic for selecting the threshold in extreme value analysis. Journal of Royal Statistical Society, Series B: Methodology, 63, No. 2, pp. 293-305, (2001)

- (21) Khmaladze, E., Goodness of fit problem and scanning innovation martingales, Annals of Statistics, 21, pp. 798–829, (1993)

- (22) Khmaladze, E., Note on distribution free testing for discrete distribution, Annals of Statistics, 41, pp. 2979–2993, (2013)

- (23) Khmaladze, E., Unitary transformations, empirical processes and distribution free testing, Bernoulli, 22, pp. 563–588, (2016)

- (24) Mason, D., Law of large numbers for sums of extreme values, Ann. Prob., 10, pp. 754-764, (1982)

- (25) Pickands, III J., Statistical inference using extreme order statistics, Ann. Statist., 3, pp. 119-131, (1975)

- (26) Koning, A. J. and Peng, L., Goodness of fit tests for heavy tailed distribution, Journal of Statistical Planning and Inference, 138, pp. 3960-3981, (2008)

- (27) Resnick, S. I., Extreme values, regular variation and point process, Springer-Verlag, New York (1987)

- (28) Smith, R. L., Estimating tails of probability distributions, Annals of Statistics, 15, pp. 1174-1207, (1987)

- (29) Teugels, J. L., Limit theorems on order statistics, Annals. Prob., Vol. 9, No. 5, pp. 868-880, (1981)