A General Framework for Bandit Problems Beyond Cumulative Objectives

Abstract

The stochastic multi-armed bandit (MAB) problem is a common model for sequential decision problems. In the standard setup, a decision maker has to choose at every instant between several competing arms, each of them provides a scalar random variable, referred to as a “reward.” Nearly all research on this topic considers the total cumulative reward as the criterion of interest. This work focuses on other natural objectives that cannot be cast as a sum over rewards, but rather more involved functions of the reward stream. Unlike the case of cumulative criteria, in the problems we study here the oracle policy, that knows the problem parameters a priori and is used to “center” the regret, is not trivial. We provide a systematic approach to such problems, and derive general conditions under which the oracle policy is sufficiently tractable to facilitate the design of optimism-based (upper confidence bound) learning policies. These conditions elucidate an interesting interplay between the arm reward distributions and the performance metric. Our main findings are illustrated for several commonly used objectives such as conditional value-at-risk, mean-variance trade-offs, Sharpe-ratio, and more.

Key words: Multi-armed bandit, risk, planning, reinforcement learning, upper confidence bound, optimism principle.

1 Introduction

Consider a sequential decision making problem where at each stage one of independent alternatives is to be selected. When choosing alternative at stage (also referred to as time ), the decision maker receives a reward that is distributed according to some unknown distribution , and is independent of . (Where unambiguous, we avoid indexing with , and leave that implicit; the information will be encoded in the policy that governs said choices, which will be detailed in what follows.) At time , the decision maker has accumulated a vector of rewards . In our setting, performance criteria are defined by a function that maps the reward vector to a real-valued number. As is a random quantity, we consider the accepted notion of expected performance, i.e., , assuming this expectation exists and is finite. An oracle, with full knowledge of the arms’ distributions, will make a sequence of selections based on this information so as to maximize the expected performance criterion. This serves as a benchmark for any other policy which does not have such information a priori, and hence needs to learn it on the fly. The gap between the former (performance of the oracle) and the latter (performance of the policy) represents the usual notion of regret in the learning problem.

The most ubiquitous performance criterion in the literature concerns the long run average reward, which involves the empirical mean, . In this case, the oracle rule, that maximizes the expected value of the above, just samples from the distribution with the highest mean value, namely, it selects . Learning algorithms for such problems date back to Robbins’ paper Robbins (1952) and were extensively studied subsequent to that. In particular, the seminal work of Lai and Robbins (1985) establishes that the normalized (per epoch) regret in this problem, when the arms are “well separated,” cannot be made smaller than , and there exist learning algorithms that achieve this regret by maximizing a confidence bound modification of the empirical mean. (When the arms are not well separated, equivalent statements hold with order-.) Since then, this class of policies has come to be known as UCB, or upper confidence bound policies. Some strands of literature that have emerged from this include Auer et al. (2002) (non-asymptotic analysis of UCB-policies), Maillard et al. (2011) (empirical confidence bounds or KL-UCB), Agrawal and Goyal (2012) (Thompson sampling based algorithms), and various works which consider an adversarial formulation (see, e.g., Auer et al. (1995)).

Main research questions. In this paper we are interested in studying the above problem for more general path dependent objectives that are of interest beyond just the vanilla average. Many of these objectives bear an interpretation as “risk criteria” insofar as they focus on a finer probabilistic nature of the primitive distributions than the mean, and typically relate to the spread or tail behavior. Examples include: the so-called Sharpe ratio, which is the ratio between the mean and standard deviation; value-at-risk () which focuses on the percentile of the distribution (with small); or a close counterpart that integrates (averages) the values out in the tail beyond that point known as the expected shortfall (or conditional value at risk; ). The last example is of further interest as it belongs to the class of coherent risk measures which has various attractive properties from the risk theory perspective. A discussion thereof is beyond the scope of this paper; cf. Artzner et al. (1999) for further details. In our problem setting, the above criteria are applied via the function to the empirical observations, and then the decision maker seeks, as before, to optimize its expected value. A typical example where such criteria may be of interest is that of clinical trials (one of the original motivations for the development of the MAB framework). More specifically, suppose several new drugs are sequentially tested on individuals who share similar characteristics. If we consider average performance, we may conclude that the best choice is a drug with a non-negligible fatality rate but a high success rate. If we wish to control the fatality rate then using for example may be appropriate.

While some of the above mentioned criteria have been examined in the decision making and learning literature (see references below), the analysis tends to be driven by specific properties of the criterion in question, and is very much done on a case-by-case basis. One of the purposes of this paper is to present a more unified approach to a large set of such problems. One of the main obstacles that arises under the non-cumulative criteria is the more complicated structure of the oracle rule. In particular, unlike the case of the mean objective, here the oracle rule need not select the same arm throughout the horizon of the problem. This presents further obstacles in identifying and characterizing a learning policy, as most such blueprints call for minimizing regret by mimicking the oracle rule. To that end, as our analysis will flesh out, under suitable conditions the oracle policy can be approximated (asymptotically) by a simple policy, that is, one that statically selects a single arm. This simplification can be leveraged to address the learning problem which becomes more tractable and amenable to optimism-based design principles. It is therefore of interest to understand and characterize in what instances does this simplified structure exist. This is one of the main thrusts of the paper.

Main contributions of this paper. In this paper we consider a general approach to the analysis of performance criteria where the oracle policy is a simple policy. We identify a class of criteria that we term Empirical Distribution Performance Measures (EDPM). In particular, let be the empirical distribution of the vector , i.e., is the fraction of rewards less or equal to real valued . An EDPM evaluates performance by means of a function , which maps to , i.e., . Alternatively, may also serve to evaluate the distributions of the random variables (). These evaluations may be aggregated to form a different type of performance criteria that we term “pseudo regret,” and consider as an intermediate learning goal. Our main results provide easily verifiable explicit conditions that characterize the asymptotic behavior of the oracle rule, and culminate in a -type learning algorithm with either or normalized regret (depending on the properties of and the arm distributions).

While our framework encompasses many existing performance measures, there are some notable examples that are left out. One is the Maximum Drawdown, which measures the maximum decline from the highest historical peak in the reward sequence. This criterion cannot be expressed by our framework as it depends on the order of the reward sequence. Other criteria such as certain distortion risk measures and cumulative prospect theory can be expressed within our framework, however, they do not satisfy some of its requirements, hence our results are not directly applicable. Whether these could be incorporated into our framework remains open to future work. See further details in Section 6.

Previous works on bandits that concern path-dependent and risk criteria. Sequential performance measures of the type considered here were previously studied in Sani et al. (2012), which considered the Mean-Variance of the sequence and presented the MV-UCB, and MV-DSEE algorithms, and Vakili and Zhao (2016, 2015), which complete the regret analysis of said algorithms and also consider performance under Value at Risk. Zhu and Tan (2020) also consider the Mean-Variance and give a Thompson sampling-based method. Additionally, Agrawal and Devanur (2019) consider a constrained bandit problem with a concave objective. This may, for example, capture the Mean-Variance setting, however, it is not the main focus of the paper and the results are restricted to order regret (or order- normalized regret in our setting).

Other works consider simpler performance measures that are more closely related to our notion of pseudo regret. Galichet et al. (2013) present the MaRaB algorithm which uses in its implementation, however, they analyze the average reward performance, and do so under the assumptions that , and the assumption that the and average optimal arms coincide. Tamkin et al. (2019) also consider and give a sample-wise optimistic algorithm. Bhat and Prashanth (2019) consider the concentration of risk measures and apply it exclusively to bound pseudo regret. It should be noted that some of their findings, and in particular the pseudo regret bound, where previously established in Cassel et al. (2018), which is an antecedent to the present paper. Zimin et al. (2014) consider criteria based on the mean and variance of distributions, and present and analyze the algorithm. We note that these criteria correspond to a much narrower class of problems than the ones considered here. Maillard (2013) presents and analyzes the RA-UCB algorithm which considers the measure of entropic risk with a parameter .

Slightly farther afield, other works consider the best arm identification or simple regret settings. Kagrecha et al. (2019) propose distribution independent algorithms for a linear combination of the mean and measures. L.A. et al. (2020) consider the estimation of for both light and heavy tailed distributions, and provide an algorithm for best arm identification. Tran-Thanh and Yu (2014) consider a general functional of the arm distributions and demonstrate results on Mean-Variance, , and best arm and simple regret. Yu et al. (2017) consider a Mean-Variance best arm identification. David et al. (2018) consider a quantile risk constrained setting for best arm identification.

Finally, we mention two alternative settings that consider quantile-based sequential performance measures such as and . Torossian et al. (2019) consider the convergence of approximate dynamic programming in Markov Decision Processes (MDP), and Jiang and Powell (2018) consider a stochastic optimization setting with bandit feedback. The approach in our paper is quite distinct from these.

Organization. Throughout, all proofs are provided as a sketch that communicates their key ideas, with the full details deferred to the Appendix. In Section 2 we give initial motivation for our suggested class of performance criteria. In Section 3 we formulate the problem setting, oracle rule, and regret metric under non-cumulative criteria. In Section 4 we provide the main results, and in Section 5 we demonstrate them on well-known risk criteria. We also include some negative examples, which illustrate the implications of violation of the proposed conditions, indicating in some way the necessity of such conditions in achieving the unifying theme in our proposed framework.

2 A Motivating Example

In the standard bandit setting, for a sequence of integrable random variables we are interested in designing a policy that maximizes the average reward or, equivalently, minimizes regret compared to an oracle strategy, which is known to pull a single arm throughout the horizon. It is well known that optimistic strategies achieve optimal performance in this setting. Now, suppose we seek to design a policy that maximizes where is the order statistic of . This is known as Conditional Value at Risk () or Expected Shortfall, at percentile level , and is a widely accepted performance measure from the risk literature.

| Question: Can we minimize regret using an optimistic strategy? |

To answer this, we first need to understand what constitutes an optimistic strategy, which in turn requires that we further understand the oracle rule, which is aware of the true distributions of the arms. The current formulation of presents it as a direct function of the reward sequence. While this is very intuitive, it is in fact a sequence of mappings (one for each sample size) that do not naturally share a domain; studying this sequence can be challenging. In lieu of that, we first observe that may be reformulated in terms of a single function that evaluates the sequence of empirical reward distributions , where is the fraction of rewards less than or equal to . Formally, where

is the accepted notion for measuring for a random variable with cumulative distribution function . In Appendix A we show that essentially any performance measure that is invariant to the order of the reward sequence may be reformulated as for some function . Importantly, this captures many well-known performance measures such as Mean-Variance, Entropic Risk, Sharpe Ratio, and more.

Having restricted ourselves to the class of performance measures that can be expressed this way, we have obtained a consistent way to evaluate performance, which is independent of the time . Our study now turns to investigating the properties of the function , in conjunction with the arm distributions, that allow for an optimistic strategy. In the case of , if we only assume sub-Gaussian arm distributions, we find that may be non-smooth, and our framework can only guarantee a regret of using an optimistic strategy. However, if for example the arm distributions have positive density around their percentile then we show that the same strategy only incurs regret. The remainder of this paper will flesh out these ideas and provide a set of easy to verify conditions that yield the results discussed in this section.

3 Problem Formulation

Model and admissible policies.

Consider a standard MAB with the set of arms. Arm is associated with a sequence () of random variables with distribution , the set of all distributions on the real line. When pulling arm for the time, the decision maker receives reward , which is independent of the remaining arms, i.e., the variables (for all ) are mutually independent.

We define the set of admissible policies (strategies) of the decision maker in the following way. Let be the number of times arm was pulled up to time . Let be a random variable over a probability space which is independent of the rewards. An admissible policy is a random process recursively defined by

| (1) | |||

| (2) | |||

| (3) |

We denote the set of admissible policies by , and note that admissible policies are non anticipating, i.e., depend only on the past history of actions and observations, and allow for randomized strategies via their dependence on . Formally, let be the filtration defined by , then is measurable.

Empirical Distribution Performance Measures (EDPM).

The classical bandit optimization criterion centers on the empirical mean, i.e., . We generalize this by considering criteria that are based on the empirical distribution. Formally, the empirical distribution of a real number sequence is obtained through the mapping , given by

| (4) |

where is the indicator function of the interval defined on the extended real line, i.e.

Of particular interest to this work are the empirical distributions of the reward sequence under policy , and of arm . We denote these respectively by,

| (5) | |||

| (6) |

The decision maker possesses a function , which measures the “quality” of a distribution. The resulting criterion is called EDPM, and the decision maker aims to maximize . (Throughout it is assumed implicitly that the class of distributions and performance functions is such that this expectation exists and is finite valued.)

Oracle and regret.

For given horizon , the oracle policy is one that achieves optimal performance given full knowledge of the arm distributions (). Formally, it satisfies

| (7) |

Similar to the classic bandit setting, we define a notion of regret that compares the performance of policy to that of . The expected (normalized) regret of policy at time is given by,

| (8) |

We note that this definition is normalized with respect to the horizon , thus transforming familiar regret bounds such as into . With that convention we simply refer to the above as the “regret” without added qualifiers.

Assumptions.

Beyond the existence and finiteness of expectations, flagged earlier, we make the following assumption throughout. Let the simplex in be

and define the set of all convex combinations of the arms’ reward distributions by

| (9) |

Let be an “optimal” arm. We assume that

| (10) |

While this assumption holds for many known performance measures, and seems crucial for obtaining the improved regret rate, we note that there is some loss of generality here. In Section 6, we give a few examples of known performance measures where 10 does not hold, and discuss how one could potentially address them within our framework. Finally, we note that 10 alone does not immediately imply that playing is optimal or even near-optimal over a finite horizon (for an illustration of this, see Section F.5).

4 Main Results

When defining an objective, it was sufficient to consider as a mapping from (a set) to . Moving forward, our analysis relies on properties such as continuity and differentiability, which requires that we consider as a mapping between seminormed spaces. To that end is a subset of an infinite dimensional vector space for which norm equivalence does not hold. This hints at the importance of using the “correct” (semi)norm for each . As a result, our analysis is done with respect to a general seminorm and its matching seminormed space . We therefore consider EDPMs as mappings .

The goal of this work is to provide a generic analysis of the regret, similar to that of the classical bandit setting, and which culminates in the following result.

Theorem (Informal meta-result).

There exists an efficient algorithm such that:

-

1.

Under suitable regularity conditions obtains regret

-

2.

Under additional smoothness and gap conditions obtains regret

In what follows, we introduce the technical details required to make this statement rigorous. This culminates in Section 4.5, where Theorem 4 gives the desired statement, and where we also explain how the standard bandit setting fits into our framework. Unlike the classical bandit setting, the oracle policy , defined in 7, need not choose a single arm. Since the typical learning algorithms are structured to emulate the oracle rule, we need to first understand the structure of the oracle policy before we can analyze .

4.1 Insights From the Infinite Horizon Oracle

The oracle problem in 7 does not admit a tractable solution, in the absence of further structural assumptions. In this section we consider a relaxation of the oracle problem which examines asymptotic behavior. We provide conditions under which this behavior is “simple” thus suggesting it as a proxy for the finite time performance. More concretely, let be the worst case asymptotic performance of policy , then the infinite horizon oracle satisfies

| (11) |

Note that is well defined as the limit inferior of a sequence of random variables, however (as indicated earlier) we require that its expectation exist for 11 to be well defined.

Simple oracle.

In the traditional multi-armed bandit problem, the oracle policy, which selects a single arm throughout the horizon, is clearly simple. It may seem intuitive that EDPMs always admit such a simple infinite horizon oracle policy. However, in (F.5) we give counter examples, which arise from the “bad behavior” that is still allowed by this objective. The following result gives sufficient conditions for EDPMs to be “well behaved.”

Theorem 1 (EDPM admits a simple oracle policy).

Suppose an EDPM, , is continuous on , and that almost surely . Then the single arm policy that always chooses is an infinite horizon oracle policy, as defined in 11.

Proof sketch. (see full details in Appendix B) First, define the arm pulling ratio and notice that the empirical distribution may be written as Since , which is closed and compact, we have that any subsequence of has a further subsquence, , such that . Next, since we assumed that almost surely, we conclude that Applying the continuity assumption we conclude that We conclude the proof by showing that similar arguments imply that the proposed simple oracle policy achieves this upper bound.

Remark.

Theorem 1 depends not only on but also on the given distributions . Meaning, it may hold for a given only for some distributions, and thus the choice of a seminorm is important in order to get sharp conditions on the viable reward distributions. For example, consider the supremum norm given by . By the Glivenko-Cantelli theorem Van der Vaart (2000), it satisfies the convergence condition for any given distributions , . However, in most cases, continuity holds only if the distributions have bounded support.

4.2 Regret Decomposition

Having gained some understanding of the infinite horizon oracle, we consider a regret decomposition that uses the infinite horizon performance as a benchmark. Let

| (12) |

be the pseudo empirical distribution, where we recall that is the distribution associated with arm , and is such that for all . The regret may now be decomposed as

| (13) |

The term represents what we believe to be the correct notion of pseudo regret in our setting. Unlike the standard bandit pseudo regret which aggregates a policy’s decisions in reward space, here aggregation occurs in distribution space and then evaluates to a reward via . We note that in the standard average reward setting is linear and both notions coincide. However, in the general non-linear setting, the previous notion may underestimate the regret and is thus unsatisfactory.

The remaining terms in 13 may be viewed as a decomposition into error terms that measure discrepancy between distributions via the criterion . As hinted at by our notation, these may be bounded essentially independently of the learning algorithm’s policy . The term measures the difference between the optimal infinite horizon arm pulling mixture, which is a single arm, and that of the finite horizon oracle. Notice that by definition of we always have that . The terms and , which we refer to as horizon gaps, measure the convergence of empirical distributions to their appropriate infinite horizon counterparts, which are given by pseudo empirical distributions. While bounding these proves to be the crux of our problem, we begin by proposing a learning algorithm that minimizes the pseudo regret.

4.3 Learning Algorithm

Theorem 1 presented conditions for understanding the asymptotic behavior of performance. As we now seek a finite time analysis (of the pseudo regret), it stands to reason to employ the following stronger conditions, which quantify the rate of convergence.

Definition 1 (Stable EDPM).

We say that is stable with respect to a seminorm if there exist such that:

-

1.

admits as a local modulus of continuity for all , i.e.,

-

2.

Recalling from 6, we have that for all ,

We note that the constant is treated as a parameter in what follows recognizing that its value depends on the specific choice of norm above, as well as the assumptions made on the arm distributions.

Pseudo regret decomposition.

In the traditional bandit setting, which considers the average reward, the analysis of the regret is well understood. The same analysis extends to any linear EDPM, i.e., when is linear. This follows straightforwardly as such rewards can be formulated as the usual average criterion with augmented arm distributions. Linearity facilitates the regret analysis by providing a decomposition of contributions from each sub-optimal arm. Define the standard single arm sub-optimality gap

where we recall that is the optimal arm. The regret of a linear EDPM is given by, Departing from the simple realm of linearity, we seek a similar decomposition of the pseudo regret. To that end, denote the diameter of and the maximum gap ratio respectively as

| (14) |

where the latter essentially measures how well the chosen seminorm captures the sub-optimality gaps. We provide the following result, which is proved in Appendix C.

Lemma 1 (Pseudo regret decomposition).

Let be a stable EDPM, then is -Lipschitz over with and we have that

Learning algorithm.

We present , a natural adaptation of (see Bubeck and Cesa-Bianchi (2012)) to a stable EDPM. Let,

where are the parameters of Definition 1. The policy is given by,

| (15) |

where for , it samples each arm once as initialization.

Theorem 2 ( Pseudo Regret).

Let be a stable EDPM. If for all , then for defined in Lemma 1 and we have that

Proof sketch.

(see full details in Appendix C) The proof uses standard techniques from the UCB literature and consists of the following steps. First, we show that if at round , the algorithm chooses sub-optimal arm that was pulled more than order- times, then we have significantly overestimated this arm and underestimated the optimal arm. Second, we bound the probability of this estimation failure using standard concentration arguments that are deduced from stability (Definition 1). We conclude that after choosing sub-optimal arm for order- times, the probability of choosing it again is very small, and thus the expected number of sub-optimal arm pulls is order-. Finally, the proof is concluded by plugging this result into the pseudo regret decomposition, given in Lemma 1.

4.4 Bounding the Horizon Gaps

Recall that the horizon gap of a policy is given by . At their core, our bounds on the horizon gaps follow from the convergence of the empirical to pseudo empirical distribution. This convergence is quantified by the following lemma.

Lemma 2 (Empirical Distribution Tail Bound).

Suppose that Requirement 2 of stability holds, then

The proof decomposes the deviation into its contributions from each arm and uses Requirement 2 of stability, single arm concentration of the empirical distribution, and several union bounds to conclude the desired result. See full details in Section D.1. We now present our first bound on the horizon gap, which is uniform over all policies .

Proposition 1 (Uniform horizon gap bound).

Suppose that is a stable EDPM. Then we have that for all

The proof uses Requirement 1 of stability, local modulus of continuity, to get that

| (16) |

and then uses the tail sum formula together with the tail bound in Lemma 2 to obtain the final bound. See full details in Appendix D.

The result of Proposition 1 exhibits a dependence on the time horizon which may be quite loose. To see this, consider a linear . It is relatively easy verify that the left hand side of 16 is zero, while its right hand side behaves as even when .

In order to obtain improved bounds, we require a notion of smoothness. Formally, let be the space of bounded linear functionals on . Assuming is differentiable on , then its differential is well defined, and we denote its (linear) operation on by .

Definition 2 (Smooth EDPM).

An EDPM, is smooth if it is differentiable on , and there exist such that for any satisfying we have that

This definition is a standard notion from optimization, stated for our infinite dimensional function space. The following result shows that “reasonable” policies enjoy a smaller horizon gap under the smoothness assumption.

Theorem 3 (Improved horizon gap bound).

Suppose that is a stable and smooth EDPM with . Letting we have that for any policy and fixed

for all , which is polynomial in problem parameters.

The proof may be found in Appendix D. It explicitly identifies the parameter , and also addresses the case of , which gives an additional low order term. Notice that and thus any policy whose arm pull frequencies converge in expectation at a rate of has horizon gap of . In particular, this clearly holds for .

Proof ((sketch)).

First, a simple calculation shows that Next, since is a linear operator, we conclude that for all . We thus obtain the following decomposition

To bound we use smoothness to get that

and using the tail sum formula together with the tail bound in Lemma 2 bounds .

Finally, to bound we first use the Cauchy–Schwarz inequality together with smoothness to get that

Now, for small deviations we have that

On the other hand, recalling that is the diameter of , we get that

and using the tail sum formula together with Lemma 2, and summing the two inequalities bounds , and concludes the proof.

4.5 Regret Bound

In order to conclude our regret bounds, we require the following definition.

Definition 3 (Linear gap).

We say has a linear gap if there exists such that

This assumption will be seen to hold for our examples, in particular, the following result gives mild sufficient conditions. See proof in Appendix E.

Proposition 2.

Suppose is convex over and for all , then has a linear gap with , where is defined in 14.

Summarizing our observations thus far, the informal statement of our main findings is made concrete by the following result.

Theorem 4 ( regret).

Suppose an EDPM, , is stable, smooth with , and has a linear gap. Letting the regret of running is bounded as

for all , which is polynomial in problem parameters.

For a detailed proof, which includes the exact dependence of on the problem parameters, and an additional low order term when , see Appendix E.

Proof ((sketch)).

First, using Theorem 3 with and large enough we get that

where for we bounded the second term of Theorem 3 using the fact that Theorem 2 actually bounds Second, using the linear gap assumption we get that

Finally, recall that in 13 we decompose the regret as Combining the above and using Theorem 2 to bound concludes the proof.

Remark 1.

Notice that even in the absence of the smoothness and linear gap assumptions, we may still apply Proposition 1 to obtain a weaker regret bound in which the last two terms of Theorem 4 are replaced by In Section 5 we will show that typical examples satisfy Theorem 4, however, we also give two cases where this weaker bound is the best that can be achieved within our framework.

Example: Average Reward

We summarize our approach for the familiar bandit average reward setting that, in our EDPM formulation, is given by Notice that is linear and so the regret decomposition in 13 becomes trivial, i.e., and . For simplicity, suppose that the rewards are constrained to the interval , and consider the seminorm Notice that and thus . Using Hoeffding’s inequality we get that is stable with and thus . Since is linear, it is clearly smooth with and . Plugging all parameters into Theorem 4 we recover the standard regret bound for average reward bandits

| (17) |

Discussion

Our main result demonstrates that the EDPM formulation allows us to convert difficult questions in learning under sequential performance criteria to, essentially, simple questions in functional analysis. Roughly speaking, any quasiconvex function, , that, for an appropriate seminorm, is twice differentiable and grows at most polynomially, can be accommodated by our framework (at least for some arm distributions), i.e., may be learned efficiently. We note that our results focused solely on the time horizon parameter , and we suspect that the dependence on the number of arms can be improved. The main issue there is the squared dependence on in the tail bound of the empirical distribution (Lemma 2), and subsequently in the horizon gap (Theorem 3). It is not clear whether this could be improved uniformly over all policies , or whether this should be done only for near optimal policies. As a motivating example, it is clear that a single arm policy has horizon gap that does not depend on . As the optimal policy is close to a single arm policy, we expect that its dependence on should be weak, perhaps even sub-linear. This would make the horizon gap a low order term compared to the pseudo regret and establish an equivalence between the two notions of regret. We leave this as an open question for future work. So far, we demonstrated how the standard average reward setting fits into our framework. In the following section we use our framework to analyze various well-known performance measures from the risk literature.

5 Illustrative Examples

The purpose of this section is, first and foremost, to show the relative ease with which various performance criteria can be analyzed within the framework developed in the previous sections. To make the exposition more accessible, we forego detailed introductions of the various criteria as well as various other technical details. Our main focus is to show the use of Theorem 4, after which we give some edge cases that demonstrate the subtleties and limitations of our framework. We refer the interested reader to Appendix F for the complete details, and to Table 1 for a summary of the parameter settings of each criterion. We make the following assumption throughout this section.

Assumption 1.

The rewards are restricted to the interval , i.e., the support of is in for all .

This assumption is intended to simplify the exposition and can always be replaced by an appropriate “light tailed” condition.

| Average | 1 | 0 | |||||

|---|---|---|---|---|---|---|---|

| TSV | 1 | 0 | |||||

| Entropic Risk | |||||||

| Variance | 2 | ||||||

| Mean-Variance | |||||||

| Sortino Ratio | |||||||

| —— | —— |

5.1 Linear EDPMs

We begin with with a few examples of linear EDPMs, which are essentially standard stochastic multi-armed bandit settings with augmented arm distributions.

Average reward

is the classic bandit performance criterion, which is given by For a given reward sequence, it is explicitly stated as

Squared reward

is a less typical performance measure on its own but will serve us in what follows. It is given by and in terms of the reward sequence as

Below Target Semi-Variance (TSV)

measures the negative variation from a threshold parameter . The goal here is to minimize the variation and since our setting is expressed in terms of maximization, we state its negation In terms of the reward sequence this stated as

The Analysis

for all linear EDPMs follows in a similar fashion to the average reward demonstrated in Section 4.5, with the only potential change being the value of . More formally, let be any linear EDPM. We define the seminorm which implies that and consequently . Requirement 1 of stability clearly holds with and thus . Recalling the empirical distribution and indicator functions from 4, Hoeffding’s inequality implies Requirement 2 of stability holds with where

is the squared length of the reward interval under , which in the examples above is at most . Since is linear, it is clearly smooth with and . Plugging all parameters into Theorem 4 we recover the standard bandit regret bound given in 17.

5.2 Composite EDPMs

Moving on to more complex performance criteria, we consider compositions of linear EDPMs. Such criteria are often used to state a trade-off between multiple objectives. A partial list of widely used risk metrics which we consider here consists of: Entropic Risk, Variance, Mean-Variance (Markowitz), Sharpe ratio, and Sortino ratio. Formally, we say an EDPM is composite if there exist linear EDPMs and such that

Considering this class under the seminorm where is the norm in , the verification of our framework becomes easy, as seen in the following result.

Lemma 3 (Informal).

Suppose are linear, and stable, then:

-

1.

If admits a polynomial local modulus of continuity, then is stable;

-

2.

If is locally smooth, then is smooth;

-

3.

If is convex then so is .

The formal statement along with its proof may be found in Section F.2. Verifying Lemma 3 is typically very easy, often amounting to bounding the gradient and Hessian of , and yields all the needed properties to invoke Theorem 4 and obtain an regret bound for .

Entropic risk

is a risk assessment measure that uses an exponential utility function with risk aversion parameter . It is given by

where is a linear EDPM and thus is composite with , which is convex. Since the rewards are in , we can bound the derivatives of to conclude that it satisfies Lemma 8 with and .

Variance

measures the empirical squared deviation from the mean reward. As we seek to minimize this deviation, it is given by

and thus , which is convex. It is then easy to verify that Lemma 8 holds with and .

Mean-variance (Markowitz)

measures performance as an additive trade-off between the empirical mean and variance. For it is given by

and thus , which is convex. A simple calculation shows that Lemma 8 holds with and .

Sharpe ratio

measures performance as a ratio between the empirical mean and variance. For and it is given by

and thus The parameter is essentially a threshold for the average reward, while is a regularization parameter. Unlike the previous examples, where was convex, here it is only quasiconvex. While a quasiconvex function could potentially have no linear gap, we show that Sharpe ratio has a linear gap with a slightly worse constant. The calculation is technical and deferred to Appendix F.

Sortino ratio

is Sharpe ratio with variance replaced by below target semi-variance. As such, for and it is given by

and thus Similar to Sharpe ratio, here is also quasiconvex. The resulting analysis is thus similar, if perhaps a bit simpler, and we defer it to Appendix F.

5.3 Non-composite EDPMs

We now consider two examples of non-composite criteria. The first, , is found to be smooth and stable under appropriate conditions. The second, , is stable but appears to be non-smooth. In both cases the resulting conditions possess a more particular nature than those presented for composite EDPMs. (In Appendix F we also include some results for Utility-Based Shortfall Risk (UBSR)).

Conditional Value at Risk ()

is the average reward below percentile level , which is given by

| (18) |

We note that a more explicit expression can be obtained by plugging in the maximizer , which is the Value at Risk of , defined in 21. Now, in order to invoke Theorem 4 we need to show that is convex, stable and smooth.

Convexity is immediate since the expression in 18 is a maximum over linear functions, which is convex. For stability, we use the norm

| (19) |

where is the norm. The two additional terms may be foregone when the rewards are constrained to . The concentration of follows from the Dvoretzky-Kiefer-Wolfowitz inequality (Massart, 1990), while the other two follow from Hoeffding’s inequality. A further technical calculation yields the desired modulus of continuity and thus stability is concluded with parameters Recalling Remark 1, we can now conclude that obtains regret for any bounded reward distributions.

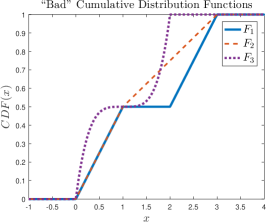

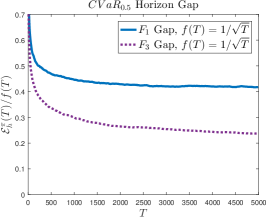

We would like to show that is smooth and thus conclude the requirements for Theorem 4. However, we find that even for bounded distributions, may be non-smooth (see Figure 1). To overcome this limitation, we require that the arm distributions have a positive density around their percentile. Formally, we require that there exist such that

| (20) |

where is the Value at Risk of , defined in 21. This condition is one of the subtleties that arise from our framework. With it, we show that is smooth with and and thus obtain the desired regret bound. Without it, we provide a numerical experiment (see Figure 1), suggesting that the horizon gap truly behaves as as suggested by our framework.

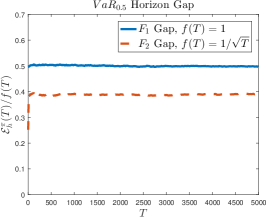

Value at Risk ()

is the reward at percentile , which is given by

| (21) |

We show that is quasiconvex, however, as previously mentioned, we could not find any set of conditions that ensure the smoothness of , and thus we cannot invoke Theorem 4. On a positive note, we show that for distributions satisfying 20, stability holds under the semi-norm in 19 and with parameters We conclude that regret is obtainable by our framework (by means of Remark 1). We conjecture that improved regret is possible for when the arm distributions are also twice differentiable, but it is not clear whether this could be achieved through the smoothness condition.

Notice that the stability issues of are such that even Theorem 1 (single arm infinite horizon oracle) is not satisfied without further assumptions on the arm distributions. Concretely, denote the level set of a function by then Theorem 1 holds if for all . Intuitively, this condition ensures that the arm distributions do not have a flat region at their percentile. If such a flat region exists, then arbitrarily small perturbations to the distribution may change the percentile by a constant, thus causing the instability issue. Interestingly, even in the presence of this instability, we have the following result.

Proposition 3 ( oracle policy).

For , always admits a simple oracle policy , i.e., choosing a single arm throughout the horizon is asymptotically optimal.

5.4 A numerical illustration of an edge case

When considering the existence of simple oracle policies, Proposition 3 essentially means that stability, while a sufficient condition, is not necessary. However, for the purpose of regret analysis, we highlight the importance of stability by means of a simulation. Note that Theorem 4 relies on a suitably fast diminishing horizon gap (see in 13). We calculate this gap in a simple simulation with arms. This is done for three different distributions, each not satisfying a different subset of the previously discussed conditions for stability and or smoothness. Figure 1 displays the simulation results, which show that the obtained rate is slower than the desired which is achieved in Theorem 3.

6 Limitations

While our framework encompasses many known performance measures, it has limitations that make it inapplicable to certain potentially interesting examples. The following outlines some of these limitations and indicates how they may be overcome.

No “single optimal arm”.

While all of the examples in Section 5 satisfy this assumption, formally defined in 10, this is not always the case. For example, consider the performance measure

| (22) |

which is a type of “distorted risk measure” with distortion function . If we take we get that is concave and thus typically obtains its maximum in an interior point. More concretely, suppose we have two arms with Bernoulli distributions with parameters , respectively. Then , the set of convex combinations, is exactly the Bernoulli distributions with parameter . Next, it is easy to see that for a Bernoulli distribution with parameter , we have that , which is strictly concave and obtains its maximum at . We conclude that if then for such that

which contradicts 10. Overall, the above implies that there is no single-arm infinite horizon oracle policy, i.e., one that always chooses a single arm. An example of an infinite horizon oracle in this setting is one that chooses arm with probability and arm otherwise.

The above performance measure is admittedly somewhat contrived: it prefers a Bernoulli distribution with over one with , even though the latter has stochastic dominance over the former. Regardless, it is worth emphasizing here that Proposition 1 holds regardless of 10 and thus it only remains to design a pseudo regret minimization algorithm to obtain regret. We suspect this could be achieved by a similar UCB-type algorithm that optimizes over all convex combinations of the arms. We note that the resulting optimization problem might be difficult to solve and thus may require additional assumptions to make it computationally tractable.

Unstable performance measures.

As seen in the example of in Section 5, some performance measures could be unstable without additional assumptions on the arm distributions. The following is another such example. Consider from 22 with with Bernoulli as before. If then we get that

On the other hand, by the homogeneity of the semi-norm we have that

and thus for any norm, and there exists small enough such that

i.e., does not satisfy Definition 1. This issue could potentially be overcome by weakening the Lipschitz condition in Definition 1 to a Hölder type condition. This type of change will clearly impact the overall performance result.

Heavy-tailed distributions.

This subject is well understood in the classic bandit setting Bubeck and Cesa-Bianchi (2012), and has also been studied for general learning settings under a performance measure Holland and Haress (2020). Our results hold for light-tailed sub-Gaussian arm distributions. We suspect it is possible to extend them to sub-Exponential distributions without significant degradation, but this will not carry over to heavier tails that will likely necessitate a different approach.

7 Open Problems and Future Directions

One main question that we leave open is the dependence of the regret on the number of arms . We conjecture that a finer analysis of the horizon gap may reduce it from our to either or . The subject of lower bounds remains open as well. Future directions may include a more complete taxonomy of performance criteria, or an extension of this framework to different settings (e.g., adversarial or contextual). Additionally, we note that the majority of our proof techniques also apply to non-quasiconvex criteria. If such criteria are found to be of interest then extending the framework to this case may be appealing.

A future direction of great interest is to consider a Markov decision model for the dynamics. The same criteria of interest are still relevant, but now it is unclear whether a simple (Markov) policy could approximate the oracle and if so, at what rate.

Acknowledgments.

A preliminary version of this work appeared at the Conference on Learning Theory, 2018. We thank Ron Amit, Guy Tennenholtz, Nir Baram and Nadav Merlis for helpful discussions of this work, and the anonymous reviewers for their helpful comments. This work was partially funded by the Israel Science Foundation under contract 1380/16 and by the European Community’s Seventh Framework Programme (FP7/2007-2013) under grant agreement 306638 (SUPREL).

References

- Agrawal and Devanur (2019) Shipra Agrawal and Nikhil R Devanur. Bandits with global convex constraints and objective. Operations Research, 67(5):1486–1502, 2019.

- Agrawal and Goyal (2012) Shipra Agrawal and Navin Goyal. Analysis of thompson sampling for the multi-armed bandit problem. In COLT, pages 39–1, 2012.

- Artzner et al. (1999) Philippe Artzner, Freddy Delbaen, Jean-Marc Eber, and David Heath. Coherent measures of risk. Mathematical finance, 9(3):203–228, 1999.

- Auer et al. (1995) Peter Auer, Nicolo Cesa-Bianchi, Yoav Freund, and Robert E Schapire. Gambling in a rigged casino: The adversarial multi-armed bandit problem. In Foundations of Computer Science, 1995. Proceedings., 36th Annual Symposium on, pages 322–331. IEEE, 1995.

- Auer et al. (2002) Peter Auer, Nicolo Cesa-Bianchi, and Paul Fischer. Finite-time analysis of the multiarmed bandit problem. Machine learning, 47(2-3):235–256, 2002.

- Bhat and Prashanth (2019) Sanjay P Bhat and LA Prashanth. Concentration of risk measures: A wasserstein distance approach. In Advances in Neural Information Processing Systems, pages 11762–11771, 2019.

- Bubeck and Cesa-Bianchi (2012) Sébastien Bubeck and Nicolo Cesa-Bianchi. Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Foundations and Trends® in Machine Learning, 5(1):1–122, 2012.

- Cassel et al. (2018) Asaf Cassel, Shie Mannor, and Assaf Zeevi. A general approach to multi-armed bandits under risk criteria. In Conference On Learning Theory, pages 1295–1306, 2018.

- David et al. (2018) Yahel David, Balázs Szörényi, Mohammad Ghavamzadeh, Shie Mannor, and Nahum Shimkin. PAC bandits with risk constraints. In International Symposium on Artificial Intelligence and Mathematics, ISAIM 2018, Fort Lauderdale, Florida, USA, January 3-5, 2018, 2018. URL http://isaim2018.cs.virginia.edu/papers/ISAIM2018_ML_David_etal.pdf.

- Fisher (1992) Evan Fisher. On the law of the iterated logarithm for martingales. The Annals of Probability, pages 675–680, 1992.

- Fournier and Guillin (2015) Nicolas Fournier and Arnaud Guillin. On the rate of convergence in wasserstein distance of the empirical measure. Probability Theory and Related Fields, 162(3):707–738, 2015.

- Galichet et al. (2013) Nicolas Galichet, Michele Sebag, and Olivier Teytaud. Exploration vs exploitation vs safety: Risk-aware multi-armed bandits. In ACML, pages 245–260, 2013.

- Holland and Haress (2020) Matthew J Holland and El Mehdi Haress. Learning with cvar-based feedback under potentially heavy tails. arXiv preprint arXiv:2006.02001, 2020.

- Jiang and Powell (2018) Daniel R Jiang and Warren B Powell. Risk-averse approximate dynamic programming with quantile-based risk measures. Mathematics of Operations Research, 43(2):554–579, 2018.

- Kagrecha et al. (2019) Anmol Kagrecha, Jayakrishnan Nair, and Krishna Jagannathan. Distribution oblivious, risk-aware algorithms for multi-armed bandits with unbounded rewards. In Proceedings of the 33rd International Conference on Neural Information Processing Systems, pages 11272–11281, 2019.

- Klenke (2014) Achim Klenke. Law of the Iterated Logarithm, pages 509–519. Springer London, London, 2014. ISBN 978-1-4471-5361-0. doi: 10.1007/978-1-4471-5361-0˙22. URL http://dx.doi.org/10.1007/978-1-4471-5361-0_22.

- L.A. et al. (2020) Prashanth L.A., Krishna Jagannathan, and Ravi Kolla. Concentration bounds for cvar estimation: The cases of light-tailed and heavy-tailed distributions. In Proceedings of Machine Learning and Systems 2020, pages 3657–3666. PMLR, 2020.

- Lai and Robbins (1985) Tze Leung Lai and Herbert Robbins. Asymptotically efficient adaptive allocation rules. Advances in applied mathematics, 6(1):4–22, 1985.

- Maillard (2013) Odalric-Ambrym Maillard. Robust risk-averse stochastic multi-armed bandits. In International Conference on Algorithmic Learning Theory, pages 218–233. Springer, 2013.

- Maillard et al. (2011) Odalric-Ambrym Maillard, Rémi Munos, and Gilles Stoltz. A finite-time analysis of multi-armed bandits problems with kullback-leibler divergences. In COLT, pages 497–514, 2011.

- Massart (1990) Pascal Massart. The tight constant in the dvoretzky-kiefer-wolfowitz inequality. The Annals of Probability, 18(3):1269–1283, 1990.

- Robbins (1952) Herbert Robbins. Some aspects of the sequential design of experiments. Bulletin of the American Mathematical Society, 58(5):527–535, 1952.

- Sani et al. (2012) Amir Sani, Alessandro Lazaric, and Rémi Munos. Risk-aversion in multi-armed bandits. In Advances in Neural Information Processing Systems, pages 3275–3283, 2012.

- Simonnet (1996) Michel Simonnet. The Strong Law of Large Numbers, pages 311–325. Springer New York, New York, NY, 1996. ISBN 978-1-4612-4012-9. doi: 10.1007/978-1-4612-4012-9˙15. URL http://dx.doi.org/10.1007/978-1-4612-4012-9_15.

- Tamkin et al. (2019) Alex Tamkin, Ramtin Keramati, Christoph Dann, and Emma Brunskill. Distributionally-aware exploration for cvar bandits. NeurIPS 2019 Workshop on Safety and Robustness in Decision Making; RLDM 2019, 2019.

- Torossian et al. (2019) Léonard Torossian, Aurélien Garivier, and Victor Picheny. -armed bandits: Optimizing quantiles, cvar and other risks. In Wee Sun Lee and Taiji Suzuki, editors, Proceedings of Machine Learning Research, volume 101 of Proceedings of Machine Learning Research, pages 252–267, Nagoya, Japan, 17–19 Nov 2019. PMLR. URL http://proceedings.mlr.press/v101/torossian19a.html.

- Tran-Thanh and Yu (2014) Long Tran-Thanh and Jia Yuan Yu. Functional bandits. arXiv preprint arXiv:1405.2432, 2014.

- Vakili and Zhao (2015) Sattar Vakili and Qing Zhao. Mean-variance and value at risk in multi-armed bandit problems. In 2015 53rd Annual Allerton Conference on Communication, Control, and Computing (Allerton), pages 1330–1335. IEEE, 2015.

- Vakili and Zhao (2016) Sattar Vakili and Qing Zhao. Risk-averse multi-armed bandit problems under mean-variance measure. IEEE Journal of Selected Topics in Signal Processing, 10(6):1093–1111, 2016.

- Van der Vaart (2000) Aad W Van der Vaart. Asymptotic statistics, volume 3. Cambridge university press, 2000.

- Yu et al. (2017) Xiaotian Yu, Irwin King, and Michael R Lyu. Risk control of best arm identification in multi-armed bandits via successive rejects. In 2017 IEEE International Conference on Data Mining (ICDM), pages 1147–1152. IEEE, 2017.

- Zhu and Tan (2020) Qiuyu Zhu and Vincent Tan. Thompson sampling algorithms for mean-variance bandits. In Proceedings of Machine Learning and Systems 2020, pages 2645–2654. PMLR, 2020.

- Zimin et al. (2014) Alexander Zimin, Rasmus Ibsen-Jensen, and Krishnendu Chatterjee. Generalized risk-aversion in stochastic multi-armed bandits. arXiv preprint arXiv:1405.0833, 2014.

sectionappendix

Appendix A EDPMs as Permutation Invariant Performance Measures

The following continues the discussion in Section 2 on the motivation behind EDPMs and their relation to permutation invariant performance measures. Let , where is a function that measures the quality of a given reward sequence of length . A decision maker may then wish to maximize the expected performance, i.e., . It makes sense that the preferences of the decision maker remain fixed over time. This means () should, in some sense, be time invariant. However, such an invariance is hard to grasp when the functions do not share a domain. One way of addressing this issue is to assume that is permutation invariant, i.e., it maps all the permutations of its reward sequence to the same value. We provide a formal definition in the proof of the following (known) result.

Lemma 4 (Permutation invariant function representation).

is permutation invariant if and only if, there exists such that, , where is the empirical distribution mapping defined in 4.

The representation given in Lemma 4 suggests as a shared domain thus making it simple to define time invariance. We conclude that EDPMs describe the objectives that are time and permutation invariant.

Proof (of Lemma 4).

We start with a few definitions. Let denote the set of permutation matrices (binary and doubly stochastic). is said to be permutation invariant if for all and . Let, , be the set of empirical distributions created from elements (the image of ). Let,

be the inverse image of at . Let,

be the set of all permutations of . We can now begin the proof.

First direction: Suppose . Notice that is indeed permutation invariant as permuting its input simply reorders its finite sum thus not changing the value. This clearly implies that is permutation invariant.

Second direction: Suppose that is permutation invariant. Below, we prove that for any

| (23) |

Assuming 23 holds true, define in the following way. For any choose arbitrarily . Further define by,

Then by 23 we have that, , and thus there exists , such that . We conclude that,

where the last step uses the permutation invariance of . We now show that 23 holds, thus concluding the proof.

Proof of 23: Let then there exists such that . Since is permutation invariant then,

and so . On the other hand, let , then we have that, . Take such that, , are sorted in ascending order. Suppose in contradiction that and let,

be the first index where and differ. Without loss of generality assume that , then we have that,

where the strict inequality follows since , and if , then the empty sum is in fact zero. This contradicts and so, . Since, permutation matrices are invertible then, . It is well known that is always a permutation matrix. So, and we conclude that , as desired.

Appendix B Proofs of Section 4.1

Denote the fraction of time at which arm was pulled by

| (24) |

where is defined in 2. Recall the definitions of and given in 5 and 6. The following Lemma is the main argument of the proof of Theorem 1.

Lemma 5 ( sub-convergence).

Proof.

We rearrange the expression of such that the sum is over actions and instead of time:

Then we have that

The first and second inequalities follow by the triangle inequality and homogeneity of norms. The third follows by Hölder’s inequality. By the Lemma’s assumption . We show that the same holds for (*). It is enough to show the convergence of the summands in order to conclude the overall convergence of this finite sum. By the Lemma’s assumption we have that

where we used the fact that is non-decreasing and thus always converges. Now since both parts of (*) converge then we have that,

Noticing that

the proof is concluded.

Proof (of Theorem 1).

The remainder of the proof consists of applying Lemma 5. Let be a simple randomized policy that at each turn draws an arm with distribution , i.e., . We begin by proving . Let define the simple policy . Using the strong law of large numbers (Simonnet (1996)) on each coordinate of , we conclude that

Applying Lemma 5 we get that

Since is assumed to be continuous, we have that,

where is the (random) subsequence that achieves the limit inferior. Taking expectation, we conclude that . Now since is compact and is continuous, then by the Weierstrass theorem we have that there exists such that,

| (25) |

We now show that is optimal thus concluding the first part of the proof. Let be a (random) subsequence satisfying the limit inferior. Then we have that

Noticing again that is compact, we have that for any policy , there exist and (both random) satisfying almost surely. Using Lemma 5, 25, and the continuity of we get,

and taking expectation we have for all , i.e., .

Moving on to the second part of the Theorem, notice that is convex, compact and its set of extreme points is also compact (discrete). So, returning to 25 and using the quasiconvexity of , we notice that a maximizer is attained at an extreme point of . Formally, there exists such that

where are the standard unit vectors in . Continuing as before we conclude that as desired.

Appendix C Proofs of Section 4.3

Proof (of Lemma 1).

We begin by proving the Lipschitz property. Using the local modulus of continuity assumed by stability we get that for any

as desired. Next, we show the pseudo regret decomposition. Using quasiconvexity as in the second part of Theorem 1, there exists such that . Using the Lipschitz constant , and the triangle inequality we thus have that,

Proof (of Theorem 2).

The proof uses standard techniques from the UCB literature, and Bubeck and Cesa-Bianchi (2012) in particular. We begin with the following concentration result due to Requirement 2 of stability.

| (26) |

Now, for all and denote the events

and their complements by , respectively. Using the union bound and 26 we have that

The same holds for , and so we obtain

| (27) |

Next, we denote , and show that

| (28) |

Indeed, assume in contradiction that , then noticing that implies we have:

which implies that , thus contradicting our assumption. Finally, denoting

and using 27 and 28 we have that

Combining this with the expression for the pseudo regret given in Lemma 1 we obtain the desired.

Appendix D Proofs of Section 4.4

We first need the following technical lemma whose proof may be found in Section D.1.

Lemma 6.

Suppose that Requirement 2 of stability holds. Then for any integer , policy , and such that , we have that:

-

1.

where ;

-

2.

for all ;

-

3.

for all

Proof (of Proposition 1).

Proof (of Theorem 3).

First, notice that for any . This is easily seen as,

Since is a linear operator, we conclude that

With this in mind, we have the following decomposition

We bound to conclude the proof. For , recalling the parameter in Definition 2 (smoothness), we use smoothness together with the first part of Lemma 6 to get that

Next, we use stability (modulus of continuity) together with part 3 of Lemma 6, which holds due to our assumption on , to get that

where the first step also used the modulus of continuity to bound the Gateaux derivative of . Summing the two inequalities bounds .

Finally, to bound we first use the Cauchy–Schwarz inequality together with smoothness (Definition 2) to get that

Next, let to get that

On the other hand, recalling that is the diameter of , we use part 3 of Lemma 6 to get that

Summing the two inequalities bounds , and concludes the proof.

D.1 Technical Side Lemmas

Proof (of Lemma 2).

We start by using the triangle inequality and the union bound to get,

Now notice that . So we have that,

where the case of is dropped as it is clearly not the maximizer. Using this expression together with the union bound we get that,

Applying Requirement 2 of stability (concentration), we have that

where in the last step we use the fact that maximizes the summands.

Proof (of Lemma 6).

For the first claim, recall that and let be a constant to be determined later. We begin by using the tail sum formula and exchanging variables to get that

| () | ||||

where the last transition used the fact that Next, we use the tail bound in Lemma 2 to get that

Now, choose and using Lemma 7 with to solve this known integral, we get that

This holds for all thus concluding the proof of the first claim.

Next, we prove the second claim by showing that, under the assumption on , the first claim may be bounded by the desired term. To see this notice that

| () | ||||

| () |

Changing sides gives the desired bound, and concludes the proof of the second claim.

Finally, for the third claim, we begin by repeating the first steps of the first claim to get that

where we choose Notice that our choice of ensures that and thus applying Lemma 7 with we get that

where the last step also used the fact that .

Lemma 7.

For any real and integer we have that

If then we also have that

Proof.

Denote and use integration by parts to get that

Now, plugging we get that Finally, it is trivial to verify that the suggested solution satisfies the difference equation as well as the initial condition, thus concluding the first part of the proof. For the second part we use the assumption on to upper bound the expression as

Appendix E Proofs of Section 4.5

Proof (of Proposition 2).

Recall that for any there exists such that . Now, we use convexity to conclude that

where , which is defined in 14, is finite since for all .

Proof (of Theorem 4).

We begin by stating the explicit condition on the time horizon . Letting we require that is large enough such that

| (29) |

which is indeed polynomial in the problem parameters. The first two terms in the minimum are the basic requirements of Theorem 3, and the third term was chosen such that applying Theorem 3 with , we get that

Next, notice that the first step in the decomposition of the pseudo regret, which is given in Lemma 1, is and thus the bound in Theorem 2 together with the left hand side of 29 imply that Applying Theorem 3 with we obtain that

Next, using the linear gap assumption we get that

Finally, recall that in 13 we decompose the regret as Combining the above and using Theorem 2 to bound concludes the proof.

Appendix F Details of Section 5

In this section we provide the missing details from Section 5. For the most part, our goal is to verify stability and smoothness, which are the conditions for Theorem 4. We note that Theorem 1 will typically hold as long as . The exception to this rule is , for which we will require an additional assumption for this to hold. However, we also show that a single arm infinite horizon oracle always exists, even without this assumption.

In what follow we continue to operate under Assumption 1, which bounds the rewards. This is mostly to make the exposition more concise, and we state explicitly the places where it is indeed necessary.

F.1 Linear EDPMs

We expand on the application of Hoeffding’s inequality for the stability of linear EDPMs, and note that this could easily be replaced by a sub-Gaussian type assumption. Recall that for a linear EDPM , we use the seminorm . We thus have that

where the last transition used the definition of the empirical distribution in 6, and the linearity of . Notice that the linearity of also implies that We now have a sum of zero mean random variables that take values in an interval of squared length

and thus invoking Hoeffding’s inequality we get that satisfies Requirement 2 of stability with .

F.2 Composite EDPMs

Recall that an EDPM is composite if there exist and such that

For a set let

be its image under the linear mappings that compose . Lemma 3 is made formal in the following result.

Lemma 8 (Composite EDPM).

Suppose are linear, and stable with parameter . Then:

-

1.

If admits a polynomial local modulus of continuity, i.e., there exist such that

then is stable with the same and ;

-

2.

If is locally smooth, i.e., there exist such that for any satisfying we have that

then is smooth with the same parameters;

-

3.

If is convex then so is .

Proof.

Recall that we consider under the norm

where is the norm on . Starting with Requirement 1 of stability, we use the modulus of continuity assumption on to get that for all and

Next, for Requirement 2 we use the stability of the linear EDPMs to get that

| (union bound) | ||||

thus concluding stability of , which is the first claim.

Now, moving on to smoothness, we use to chain rule to get that for any and

and applying the assumed smoothness of we get that if then

thus concluding the smoothness of , which is the second claim.

Finally, if is convex the is a linear variable on a convex function and as such convex.

F.2.1 Entropic risk

This is the only example where Assumption 1 is indeed necessary for our framework. We note that this could be removed in the future by expanding our analysis to an exponential family of moduli of continuity. Recall that in terms of Lemma 8, we have that , which is convex, and . Bounding the first derivative, we get that

and thus is Lipschitz with this constant and has a modulus of continuity with parameters Next, recalling the second order charachterization of smoothness, we bound the second derivative, to get that

thus proving the desired properties for Lemma 8.

F.2.2 Variance

Here , which is convex. Next, for the modulus of continuity we have that

Since , we can bound Since the reward is also bounded in we further have that , giving us the constant . Finally, for smoothness we may bound the hessian as,

F.2.3 Mean-variance (Markowitz)

Here we have that for , which is convex. Next, for the modulus of continuity we have that

Since , we can bound Since the reward is also bounded in we further have that , giving us the constant . Finally, for smoothness we may bound the hessian as,

F.2.4 Sortino ratio

Here we have that for and

Linear gap: Let and . We need to show that

Denote , , and . Notice that is concave in and so we have that

We conclude that

where and Using the gap ratio defined in 14 we get a linear gap with .

Stability: For and we have that

Since , we can bound Since the reward is also bounded in we further have that , giving us the constants and .

Smoothness: First, we calculate the hessian to get that

Next, we upper bound its spectral norm to get that. Let be such that . Then we have that

Here we cannot take . However, for any we can use the above bound to conclude that the smoothness assumption of Lemma 8 holds with

where under the assumption that the reward is in we further have that .

F.2.5 Sharpe ratio

Here we have that for and

Linear gap: Let and . We need to show that

Denote , , and . Notice that is concave in and so we have that

We conclude that

where and Using the gap ratio defined in 14 we get a linear gap with .

Stability: For and we have that

Since , we can bound Since the reward is also bounded in we further have that , giving us the constants and .

Smoothness: The idea here is to bound the spectral norm of the hessian. This is very similar to previous examples and in particular to Sortino ratio.

F.3 Non-composite EDPMs.

In this section we show the properties of and required by our framework. Unless stated otherwise, we use the norm defined in 19. We recall the definitions of and from 21 and 18, and specifically that we have that

where . Before starting, we require the following technical lemma, proved in Section F.3.3.

Lemma 9 ( and bounds).

F.3.1 Conditional Value at Risk (CVaR)

The following summarizes the properties of required for applying Theorem 4.

Proposition 4 ( properties).

We have that:

-

1.

is convex;

-

2.

is stable with parameters

-

3.

If 20 holds then is smooth with parameters and .

Proof.

As previously mentioned, convexity follows from 18, which expresses as a maximum over linear functions.

Stability. Starting with the easier Requirement 2 of stability, the concentration of follows from the Dvoretzky-Kiefer-Wolfowitz inequality (Massart, 1990) with , and since the other two terms are linear, the same holds for them by Hoeffding’s inequality. As in Lemma 8 (but for max norm), we conclude that Requirement 2 holds with . Next, for Requirement 1, first notice that

and apply this to the second claim of Lemma 9 to get that

Finally, using the first part of Lemma 9 we get that

which is Requirement 1 of stability. Further using Assumption 1, we have that and plugging this into the above gives the desired value for .

Smoothness. Assume that We show that the smoothness condition holds under this assumption, which in turn implies that this assumption must be true (see definition of Frechet derivative). To that end, we use the second and third parts of Lemma 9 to get that for any and satisfying we have that

as desired.

F.3.2 Value at Risk (VaR)

We begin with the following proposition, which proves the needed properties of to get regret, as described in Remark 1.

Proposition 5 ( properties).

We have that:

-

1.

is quasiconvex;

-

2.

If 20 holds then is stable with parameters and

Proof.

Starting with quasiconvexity, let and . Denote , then by the definition of we have that

Using the definition of another time we conclude that

which is one of the characterizations of quasiconvexity.

Stability. Since we use the same norm as , Requirement 2 is proven by Proposition 4. As for Requirement 1, if then using the third part of Lemma 9 we have that

On the other hand, if then using the first part of Lemma 9 we have that

and combining both results we obtain get that stability holds with and

Further using Assumption 1, we have that , which gives the desired value of .

The following result shows when satisfies the conditions of Theorem 1, and thus has a single arm infinite horizon oracle policy. We note that this holds regardless as shown Proposition 3, which uses a different approach that is specific to . Denote the level set of a function by

Proposition 6 ( Theorem 1 conditions).

If for all . Then satisfies then conditions of Theorem 1, and thus has a single arm infinite horizon oracle policy.

Proof.

Unlike the remainder of this section, here we use the norm . By the Glivenko-Cantelli theorem Van der Vaart (2000), the convergence of the empirical distribution required in Theorem 1 is established. It thus remains to show that is continuous on . Our condition on the level set can be interpreted in the following way. For any fixed

| (30) | ||||

| (31) |

Let be given by, We show that is continuous at . is monotone non decreasing and so has left and right limits at . Let and denote,

By the monotonicity of we have that . Using 30 we have that, for any ,

where . So, by the expression of , we have that,

where the second inequality follows by the monotonicity of . So, for all and so . Now take and denote,

A similar set of arguments shows that , and so is continuous at .

By the continuity of , for any , there exists such that for all we have that,

For any satisfying we have that,

We also have,

We conclude that, thus concluding the continuity of on .

Finally, we prove Proposition 3, showing that always has a single arm infinite horizon oracle policy.

Proof (of Proposition 3).

We begin calculating the performance of a single arm policy. We then proceed to show that the performance of any policy is upper bounded by that of the best single arm policy.

Performance of simple policies. Let be the policy that always plays arm . We claim that, If represents a degenerate random variable then the expression holds trivially. Otherwise, let , then there exists , such that, . Using the strong law of large numbers Simonnet (1996) we have that

Let be the event on which the convergence occurs. Then there exists such that , we have that,

This implies that for all . We get that almost surely, and taking the expectation we get . Since this holds for all , then,

| (32) |

On the other hand, using the Law of the iterated logarithm Klenke (2014) we get that

where, since is non-degenerate. We conclude that

and thus

| (33) |

Taking expectation on both sides, we conclude that

which together with 32 proves that Now, recall that in Proposition 5 we showed that is quasiconvex. We thus have that there exists such that for all

| (34) |

Global optimizer. Our purpose will be to show that

| (35) |

Similarly to 33, this implies that

and taking the expectation we conclude that, thus concluding the proof.

By 34, we have that

We thus get that,

| (36) |

where and . We split our remaining analysis into two cases.

The first is when policy chooses some non-degenerate arm infinitely often (i.o). For this case we use the Law of the iterated logarithm for martingales given in Fisher (1992). We use the same notation as in Fisher (1992) aside for denoting the martingale instead of , and its difference sequence by instead of (to avoid confusion with existing notation). We start by showing is a martingale with respect to its natural filtration

where the second equality is the law of total probability in addition to being independent of . Furthermore, , so is a martingale.

Next, let . Since chooses a non-degenerate arm infinitely often then, .

Finally, let denote the first time chooses a non-degenerate arm. So, we can choose in the following way,

Clearly, there exists such that, . Furthermore,

So the conditions of Theorem 1 in Fisher (1992) are met and we conclude that

This means that, infinitely often and substituting into 36 we conclude that 35 holds.

In the second case, any non-degenerate arm is chosen a finite number of times. Let denote the index of the largest degenerate arm and be its value. Clearly,

Denote, . Since non-degenerate arms are pulled a finite number of times then,

where is defined in 24. Since there are finitely many arms, this implies that

Now, since is such that for all , we conclude that

Since , we can clearly conclude 35 holds, thus finishing the proof.

F.3.3 Proof of Lemma 9

We prove the individual claims of Lemma 9.

First claim. We start by showing that for all

| (37) |

Suppose that , then we have that

On the other hand, suppose that , then we have that

thus concluding 37. Using this result, we have that for all

as desired.

Second claim. We have that

and changing sides we get

It therefore suffices to show that

Beginning with the left inequality, we have that

| (38) |

where the final inequality holds since for . Next, for the right hand side inequality we have that

where is obtained by exchanging the roles of and in 38.

Third claim. Consider 20 with , and notice that for any . Then we have that

Using this we get

which by the definition of in 21 implies that

and changing sides we get

| (39) |

On the other hand, consider 20 with , where . Noticing that for any , we have that

and changing sides we get

Using this we get

and using the definition of in 21 and changing sides we get

Notice that the constant may be arbitrarily close to . We thus conclude that

which combined with 39 implies the desired.

F.4 Utility-Based Shortfall Risk (UBSR)