Improved Sample Complexity for Stochastic Compositional Variance Reduced Gradient

Tianyi Lin, Chenyou Fan, Mengdi Wang and Michael I. Jordan

Tianyi Lin is with Department of IEOR, UC Berkeley. Chenyou Fan is with Google. Mengdi Wang is with Department of ORFE, Princeton University. Michael I. Jordan is with Department of EECS and Statistics, UC Berkeley. Email: {darren_lin@, jordan@cs}berkeley.edu, fanchenyou@gmail.com, mengdiw@princeton.edu

Abstract

Convex composition optimization is an emerging topic that covers a wide range of applications arising from stochastic optimal control, reinforcement learning and multi-stage stochastic programming. Existing algorithms suffer from unsatisfactory sample complexity and practical issues since they ignore the convexity structure in the algorithmic design. In this paper, we develop a new stochastic compositional variance-reduced gradient algorithm with the sample complexity of where is the total number of samples. Our algorithm is near-optimal as the dependence on is optimal up to a logarithmic factor. Experimental results on real-world datasets demonstrate the effectiveness and efficiency of the new algorithm.

I Introduction

We consider the convex composition optimization model:

(1)

where is convex with and being continuously differentiable but possibly nonconvex, is an extended real-valued closed convex function on and is a convex set. Problem (1) is highly structured but also quite general; indeed, various special cases have been studied in a host of applications, including stochastic optimal control [2], multi-stage stochastic programming [10] and portfolio mean-variance optimization [8]. A typical example is on-policy reinforcement learning [11]: given a controllable Markov chain with states , a policy space , a discount factor , a collection of transition probability matrices and from a simulator and a loss function , the problem of solving the Bellman equation in a black-box simulation environment resorts to solving an optimization model:

This is equivalent to problem (1) with , and for all .

Despite the popularity, problem (1) is more computationally challenging than its noncompositional counterpart; i.e., problem (1) with . Both stochastic gradient descent (SGD) and stochastic variance reduced gradient (SVRG) [1] deteriorate because they suffer from very high computational burden for computing at each iteration. In response to this, a number of efficient variants of compositional SGD (SCGD) [13, 14] and compositional SVRG (SCVRG) [4, 15, 3] have been developed for solving problem (1). The current state-of-the-art sample complexity in terms of optimality gap for convex composition optimization is achieved by the VRSC-PG algorithm [3]; see Table I.

There has been abundant recent work on compositional SVRG for solving compositional optimization problems with strongly convex objectives [4, 15] and nonconvex objectives [3]. However, there has been relatively little investigation of convex (but not strongly convex) objectives which indeed cover various application problems in high-dimensional statistical learning [12]. In particular, the following important case has been neglected: the composition function is convex while some of the composition terms are nonconvex. Perhaps counterintuitively, it has been observed in that the average of loss functions can be convex even if some loss functions are nonconvex [9]. This occurs when some of the loss functions are strongly convex. In the SVRG setting, Allen-Zhu [1] has shown that the optimal dependence of the sample complexity on can be established when the objective is convex. What remains unknown is whether this conclusion holds true in the compositional setting. Thus, it is natural to ask:

Can an algorithm achieve optimal dependence on for convex composition optimization?

In this paper, we provide an affirmative answer to this question by developing an algorithm with a sample complexity of in terms of the optimality gap. The algorithm is intuitive and has an efficient implementation. The proof technique is new and of independent interest.

The rest of the paper is organized as follows. In Section II, we discuss the notation, definitions and assumptions. In Section III, we describe the algorithm and discuss its differences from the algorithms in Table I. In Section IV, we provide the sample complexity analysis. We place some technical detail in the Appendix. In Section V, we present numerical results on real-world datasets.

TABLE I: Sample Complexity of Candidate Algorithms.

Notation. Vectors are denoted by bold lower case letters. denotes the -norm and the matrix spectral norm. For two sequences , we write if for some constant . We denote the gradient111We refer to the gradient of at , not the gradient of at . of at as , where is the Jacobian matrix of . refers to expectation conditioned on .

Goals in stochastic composition optimization: We wish to find a point that globally minimizes the objective .

In general, finding such global optimal solution is NP-hard [5] but standard for convex optimization. To this end, we make the following assumption throughout this paper.

Assumption 1

The objective and are both convex:

where is a subgradient of at and the constraint set is bounded. The proximal mapping of , defined by

can be efficiently computed for any and any .

Assumption 1 is not restrictive since is an indicator function of a convex and bounded set in many applications [7]. Furthermore, a minimal set of conditions that have become standard in the literature [4, 15, 3] are as follows.

Assumption 2

is -Lipschitz and -gradient Lipschitz on , i.e.,

Also, is -Lipschitz and -Jacobian Lipschitz on :

Given that is bounded, Assumption 2 is not restrictive but requires that and are continuously differentiable. Assumption 2 also implies that

We define an -optimal solution in stochastic optimization via a relaxation of the global optimality condition.

Definition 2

is an -optimal solution to problem (1) if where is an optimal solution.

Throughout this paper, the algorithm efficiency is quantified by sample complexity, i.e., the number of sampled or for , or sampled or for , required to achieve an -optimal solution in Definition 2.

With these definitions in mind, we ask if an algorithm can achieve a near-optimal sample complexity for convex composition optimization.

III Algorithm

In this section, we present our algorithm and discuss its differences from the algorithms in Table I. We first choose a reference point with , , and

(2)

(3)

(4)

Then we update with a step size :

(5)

and choose the reference point for the next epoch as the averaging iterates. Computing a full gradient vector and a full Jacobian matrix once requires samples and the sample complexity for the th epoch is .

Input: , first epoch length , step size , the number of epochs and sample size .

Initialization: and .

fordo

.

.

.

.

.

fordo

Uniformly sample with replacement a subset with , and update by (2) and (3).

Uniformly sample with replacement a subset with , and update by (4). .

Finally, we discuss the differences between Algorithm 1 and existing algorithms. Indeed, AGD is deterministic and SCGD/ASC-PG are compositional variants of SGD while Algorithm 1 is a compositional variant of SVRG. Algorithm 1 also differs from other existing compositional variants of SVRG [4, 15, 3] since the number of inner loops is a constant in these algorithms while increasing in Algorithm 1. Intuitively, Algorithm 1 gradually increases the number of inner loops as the iterate approaches the optimal set and yields an improved sample complexity by reducing the number of computations of the full gradient vector and Jacobian matrix.

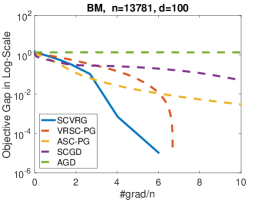

(a) Book-to-Market

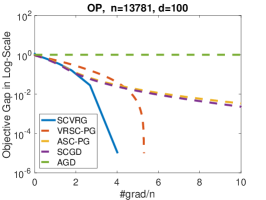

(b) Operating Profitability

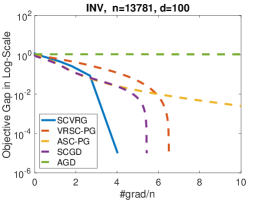

(c) Investment

Figure 1: The Performance of All Methods on three Large 100-Portfolio Datasets

Let be an optimal solution, be a small tolerance and let satisfy and where . The first epoch length and the number of epochs and satisfy

The sample sizes satisfy

Then the number of samples required to return such that is upper bounded by .

Remark 4

We discuss the results presented in Table I. Indeed, the sample complexity of AGD, VRSC-PG and Algorithm 1 depend on while that of SCGD and ASC-PG is independent at the expense of worse dependence on . The advantage of Algorithm 1 is that is independent of up to a logarithmic factor. Compared to VRSC-PG, Algorithm 1 is better if for . Compared to ASC-PG, Algorithm 1 is better than if for . This explains why Algorithm 1 performs better in many applications. For example, is a common choice in practice to avoid over-fitting the training data, while many real-world learning problems have number of samples.

Remark 5

Algorithm 1 benefits from using adaptive , which is crucial to the effectiveness and robustness of the algorithms when a huge number of iterations are required.

V Experiments

In this section, we present numerical results on real-world datasets222http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/Data_Library/, including 3 large 100-portfolio datasets and 15 medium 25-portfolio datasets as shown in Table II.

Given assets and the reward vectors at time points, the goal of sparse mean-variance optimization [8] is to maximize the return of the investment as well as to control the investment risk:

(6)

Problem (6) is exactly problem (1) with , , for and , and is a bounded set. This problem satisfies Assumption 1 and 2 and serves as a typical example of the problem studied in this paper.

TABLE II: Statistics of CRSP Real Datasets

Size

Problems

Large

13781

100

Book-to-Market (BM)

Operating Profitability (OP)

Investment (INV)

Medium

7240

25

BM: Asia, Europe, Global, Japan, America

OP: Asia, Europe, Global, Japan, America

INV: Asia, Europe, Global, Japan, America

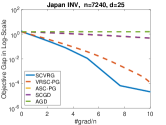

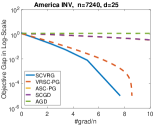

We denote Algorithm 1 as SCVRG and compare it with a line of existing algorithms. The implementations of baseline algorithms are provided by their authors with default parameters. We exclude the algorithm in [4, 15] since problem (6) is neither smooth nor strongly convex. We set and , and choose by cross validation. We use the number of samples used divided by for the -axis and on a log scale for the -axis333 is achieved by running Algorithm 1 until convergence to a highly accurate solution..

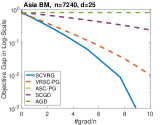

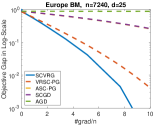

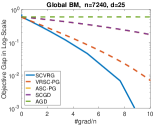

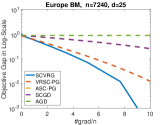

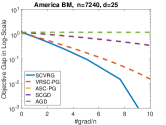

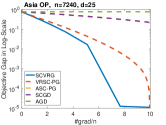

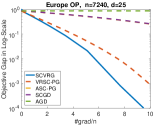

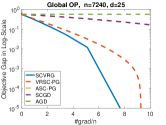

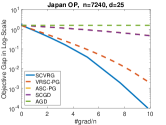

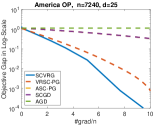

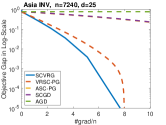

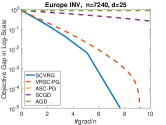

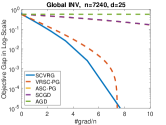

Figure 1 shows that SCVRG outperforms other algorithms on large datasets. In particular, SCVRG and VRSC-PG are more robust than SCGD and ASC-PG, demonstrating the superiority of variance reduction and constant stepsizes. AGD performs the worst because of the highest per-iteration sample complexity on large datasets. Figures 2-4 show that SCVRG outperforms other algorithms on these datasets. This is consistent with the better complexity bound of SCVRG. Furthermore, VRSC-PG is less robust than SCVRG possibly because the number of inner loops in SCVRG is increasing which provides flexibility in handling different dataset sizes. Overall, SCVRG has the potential to be a benchmark algorithm for convex composition optimization.

(a) Asia

(b) Europe

(c) Global

(d) Japan

(e) America

Figure 2: The Performance of All Methods on five 25-Portfolio Book-to-Market Datasets

(a) Asia

(b) Europe

(c) Global

(d) Japan

(e) America

Figure 3: The Performance of All Methods on five 25-Portfolio Operating Profitability Datasets

(a) Asia

(b) Europe

(c) Global

(d) Japan

(e) America

Figure 4: The Performance of All Methods on five 25-Portfolio Investment Datasets

VI Conclusions

We propose a stochastic compositional variance gradient algorithm for convex composition optimization with an improved sample complexity. Experiments on real-world datasets demonstrate the efficiency of our new algorithm. Future research could establish a lower bound for the sample complexity of convex composition optimization.

APPENDIX

We define an unbiased estimate of as

Lemma 6

We have the following inequality,

Proof.

Using (4) and Cauchy-Schwarz inequality, we have

(7)

where . Using the Cauchy-Schwarz inequality again, we have

Taking the expectation of (16), summing it over and dividing the final inequality by yields that

Rearranging the above inequality yields that

By the convexity of and the definition of , we have

Putting these pieces together with , and yields that where

Telescoping the inequality over and rearranging yields the desired inequality.

Proof of Theorem 3: Let , we have and and . Note that satisfies and

Therefore, Lemma 9 holds true. By the definition of , , and and the fact that , we have

Therefore, we conclude that the sample complexity is

This completes the proof.

References

[1]

Z. Allen-Zhu and Y. Yuan.

Improved SVRG for non-strongly-convex or sum-of-non-convex

objectives.

In ICML, pages 1080–1089, 2016.

[2]

D. P. Bertsekas and J. N. Tsitsiklis.

Neuro-dynamic programming: an overview.

In CDC, volume 1, pages 560–564. IEEE, 1995.

[3]

Z. Huo, B. Gu, J. Liu, and H. Huang.

Accelerated method for stochastic composition optimization with

nonsmooth regularization.

In AAAI, 2018.

[4]

X. Lian, M. Wang, and J. Liu.

Finite-sum composition optimization via variance reduced gradient

descent.

In AISTATS, pages 1159–1167, 2017.

[5]

K. G. Murty and S. N. Kabadi.

Some NP-complete problems in quadratic and nonlinear programming.

Mathematical Programming, 39(2):117–129, 1987.

[6]

Y. Nesterov.

Introductory Lectures on Convex Optimization: A Basic Course,

volume 87.

Springer Science & Business Media, 2013.

[7]

N. Parikh and S. Boyd.

Proximal algorithms.

Foundations and Trends® in Optimization,

1(3):127–239, 2014.

[8]

P. Ravikumar, J. Lafferty, H. Liu, and L. Wasserman.

Sparse additive models.

Journal of the Royal Statistical Society. Series B, Statistical

Methodology, pages 1009–1030, 2009.

[9]

S. Shalev-Shwartz.

SDCA without duality, regularization, and individual convexity.

In ICML, pages 747–754, 2016.

[10]

A. Shapiro, D. Dentcheva, and A. Ruszczyński.

Lectures on Stochastic Programming: Modeling and Theory.

SIAM, 2009.

[11]

R. S. Sutton and A. G. Barto.

Reinforcement Learning: An Introduction, volume 1.

MIT press Cambridge, 1998.

[12]

M. J. Wainwright.

High-dimensional Statistics: A Non-asymptotic Viewpoint,

volume 48.

Cambridge University Press, 2019.

[13]

M. Wang, E. X. Fang, and H. Liu.

Stochastic compositional gradient descent: algorithms for minimizing

compositions of expected-value functions.

Mathematical Programming, 161(1-2):419–449, 2017.

[14]

M. Wang, J. Liu, and E. X. Fang.

Accelerating stochastic composition optimization.

Journal of Machine Learning Research, 18:1–23, 2017.

[15]

Y. Yu and L. Huang.

Fast stochastic variance reduced admm for stochastic composition

optimization.

In IJCAI, pages 3364–3370. AAAI Press, 2017.