Solving the Kolmogorov PDE

by means of deep learning

Abstract

Stochastic differential equations (SDEs) and the Kolmogorov partial differential equations (PDEs) associated to them have been widely used in models from engineering, finance, and the natural sciences. In particular, SDEs and Kolmogorov PDEs, respectively, are highly employed in models for the approximative pricing of financial derivatives. Kolmogorov PDEs and SDEs, respectively, can typically not be solved explicitly and it has been and still is an active topic of research to design and analyze numerical methods which are able to approximately solve Kolmogorov PDEs and SDEs, respectively. Nearly all approximation methods for Kolmogorov PDEs in the literature suffer under the curse of dimensionality or only provide approximations of the solution of the PDE at a single fixed space-time point. In this paper we derive and propose a numerical approximation method which aims to overcome both of the above mentioned drawbacks and intends to deliver a numerical approximation of the Kolmogorov PDE on an entire region without suffering from the curse of dimensionality. Numerical results on examples including the heat equation, the Black-Scholes model, the stochastic Lorenz equation, and the Heston model suggest that the proposed approximation algorithm is quite effective in high dimensions in terms of both accuracy and speed.

1 Introduction

Stochastic differential equations (SDEs) and the Kolmogorov partial differential equations (PDEs) associated to them have been widely used in models from engineering, finance, and the natural sciences. In particular, SDEs and Kolmogorov PDEs, respectively, are highly employed in models for the approximative pricing of financial derivatives. Kolmogorov PDEs and SDEs, respectively, can typically not be solved explicitly and it has been and still is an active topic of research to design and analyze numerical methods which are able to approximately solve Kolmogorov PDEs and SDEs, respectively (see, e.g., [17], [20], [21], [27], [28], [29], [32], [40], [41], [42], [44], [45], [46], [47], [49], [52]). In particular, there are nowadays several different types of numerical approximation methods for Kolmogorov PDEs in the literature including deterministic numerical approximation methods such as finite differences based approximation methods (cf., for example, [7], [8], [23], [43], [58], [56]) and finite elements based approximation methods (cf., for example, [9], [10], [59]) as well as random numerical approximation methods based on Monte Carlo methods (cf., for example, [17], [20]) and discretizations of the underlying SDEs (cf., for example, [21], [27], [28], [29], [32], [40], [41], [42], [44], [45], [46], [47], [49], [52]). The above mentioned deterministic approximation methods for PDEs work quite efficiently in one or two space dimensions but cannot be used in the case of high-dimensional PDEs as they suffer from the so-called curse of dimensionality (cf. Bellman [5]) in the sense that the computational effort of the considered approximation algorithm grows exponentially in the PDE dimension. The above mentioned random numerical approximation methods involving Monte Carlo approximations typically overcome this curse of dimensionality but only provide approximations of the Kolmogorov PDE at a single fixed space-time point.

The key contribution of this paper is to derive and propose a numerical approximation method which aims to overcome both of the above mentioned drawbacks and intends to deliver a numerical approximation of the Kolmogorov PDE on an entire region without suffering from the curse of dimensionality. The numerical scheme, which we propose in this work, is inspired by recently developed deep learning based approximation algorithms for PDEs in the literature (cf., for example, [3], [4], [14], [15], [16], [24], [26], [51], [57]). To derive the proposed approximation scheme we first reformulate the considered Kolmogorov PDE as a suitable infinite dimensional stochastic optimization problem (see items (ii)–(iii) in Proposition 2.7 below for details). This infinite dimensional stochastic optimization problem is then temporally discretized by means of suitable discretizations of the underlying SDE and it is spatially discretized by means of fully connected deep artificial neural network approximations (see (107) in Subsection 2.6 as well as Subsections 2.4–2.5 below). The resulting finite dimensional stochastic optimization problem is then solved by means of stochastic gradient descent type optimization algorithms (see (109) in Subsection 2.6, Framework 2.9 in Subsection 2.7, Framework 2.10 in Subsection 2.8, as well as (124)–(125) in Subsection 3.1). We test the proposed approximation method numerically in the case of several examples of SDEs and PDEs, respectively (see Subsections 3.2–3.6 below for details). The obtained numerical results indicate that the proposed approximation algorithm is quite effective in high dimensions in terms of both accuracy and speed.

The remainder of this article is organized as follows. In Section 2 we derive the proposed approximation algorithm (see Subsections 2.1–2.6 below) and we present a detailed description of the proposed approximation algorithm in a special case (see Subsection 2.7 below) as well as in the general case (see Subsection 2.8 below). In Section 3 we test the proposed algorithm numerically in the case of several examples of SDEs and PDEs, respectively. The employed source codes for the numerical simulations in Section 3 are postponed to Section 4.

2 Derivation and description of the proposed approximation algorithm

In this section we describe the approximation problem which we intend to solve (see Subsection 2.1 below) and we derive (see Subsections 2.2–2.6 below) and specify (see Subsections 2.7–2.8 below) the numerical scheme which we suggest to use to solve this approximation problem (cf., for example, E et al. [14], Han et al. [24], Sirignano & Spiliopoulos [57], Beck et al. [3], Fujii, Takahashi, A., & Takahashi, M. [16], and Henry-Labordere [26] for related derivations and related approximation schemes).

2.1 Kolmogorov partial differential equations (PDEs)

Let , , let and be Lipschitz continuous functions, let be a function, and let be a function with at most polynomially growing partial derivatives which satisfies for every , that and

| (1) |

Our goal is to approximately calculate the function on some subset of . To fix ideas we consider real numbers with and we suppose that our goal is to approximately calculate the function .

2.2 On stochastic differential equations and Kolmogorov PDEs

In this subsection we provide a probabilistic representation for the solutions of the PDE (1), that is, we recall the classical Feynman-Kac formula for the PDE (1) (cf., for example, Øksendal [50, Chapter 8]).

Let be a probability space with a normal filtration , let be a standard -Brownian motion, and for every let be an -adapted stochastic process with continuous sample paths which satisfies that for every it holds -a.s. that

| (2) |

The Feynman-Kac formula (cf., for example, Hairer et al. [22, Corollary 4.17 and Remark 4.1]) and (1) hence yield that for every it holds that

| (3) |

2.3 Formulation as minimization problem

In the next step we exploit (3) to formulate a minimization problem which is uniquely solved by the function (cf. (1) above). For this we first recall the -minimization property of the expectation of a real-valued random variable (see Lemma 2.1 below). Then we extend this minimization result to certain random fields (see Proposition 2.2 below). Thereafter, we apply Proposition 2.2 to random fields in the context of the Feynman-Kac representation (3) to obtain Proposition 2.7 below. Proposition 2.7 provides a minimization problem (see, for instance, (93) below) which has the function as the unique global minimizer.

Our proof of Proposition 2.7 is based on the elementary auxiliary results in Lemmas 2.3–2.6. For completeness we also present the proofs of Lemmas 2.3–2.6 here. The statement and the proof of Lemma 2.3 are based on the proof of Da Prato & Zabczyk [13, Lemma 1.1].

Lemma 2.1.

Let be a probability space and let be an /-measurable random variable which satisfies . Then

-

(i)

it holds for every that

(4) -

(ii)

it holds that there exists a unique real number such that

(5) and

-

(iii)

it holds that

(6)

Proof of Lemma 2.1.

Proposition 2.2.

Let , , let be a probability space, let be a /-measurable function, assume for every that , and assume that the function is continuous. Then

-

(i)

it holds that there exists a unique continuous function such that

(8) and

-

(ii)

it holds for every that .

Proof of Proposition 2.2.

Observe that item (i) in Lemma 2.1 and the hypothesis that ensure that for every function and every it holds that

| (9) |

Fubini’s theorem (see, e.g., Klenke [39, Theorem 14.16]) hence proves that for every continuous function it holds that

| (10) |

The hypothesis that the function is continuous therefore demonstrates that

| (11) | ||||

Hence, we obtain that

| (12) |

Again the fact that the function is continuous therefore proves that there exists a continuous function such that

| (13) |

Next observe that (10) and (12) yield that for every continuous function with

| (14) |

it holds that

| (15) | ||||

Hence, we obtain that for every continuous function with

| (16) |

it holds that

| (17) |

This and again the hypothesis that the function is continuous yield that for every continuous function with

| (18) |

and every it holds that . Combining this with (13) completes the proof of Proposition 2.2. ∎

Lemma 2.3 (Projections in metric spaces).

Let be a metric space, let , , and let be the function which satisfies for every that

| (19) |

Then

-

(i)

it holds for every that

(20) and

-

(ii)

it holds for every that .

Proof of Lemma 2.3.

Throughout this proof let be the function which satisfies for every that

| (21) |

Note that (19) ensures that for every it holds that

| (22) |

This establishes item (i). It thus remains to prove item (ii). For this observe that the fact that the function is continuous ensures that the function is continuous. Hence, we obtain that the function is /-measurable. Next note that item (i) demonstrates that for every , it holds that

| (23) |

Hence, we obtain that for every , it holds that

| (24) |

Moreover, note that (19) ensures that for every , it holds that

| (25) | ||||

Therefore, we obtain that for every , with it holds that

| (26) |

Combining this with (24) yields that for every , with it holds that

| (27) |

Hence, we obtain that for every with it holds that

| (28) |

This and (19) show that for every with it holds that

| (29) |

Combining (21) with the fact that the function is /-measurable therefore demonstrates that for every with it holds that

| (30) | ||||

Hence, we obtain that for every it holds that

| (31) |

Therefore, we obtain that for every it holds that

| (32) | ||||

This establishes item (ii). The proof of Lemma 2.3 is thus completed. ∎

Lemma 2.4.

Let be a separable metric space, let be a metric space, let be a measurable space, let be a function, assume for every that the function is /-measurable, and assume for every that the function is continuous. Then it holds that the function is /-measurable.

Proof of Lemma 2.4.

Throughout this proof let be a sequence which satisfies that , let , , be the functions which satisfy for every , that

| (33) |

and let , , be the functions which satisfy for every , , that

| (34) |

Note that (34) shows that for all , it holds that

| (35) | ||||

Item (ii) in Lemma 2.3 hence implies that for all , it holds that

| (36) | ||||

This proves that for every it holds that the function is /-measurable. In addition, note that item (i) in Lemma 2.3 and the hypothesis that for every it holds that the function is continuous imply that for every , it holds that

| (37) |

Combining this with the fact that for every it holds that the function is /-measurable shows that the function is /-measurable. The proof of Lemma 2.4 is thus completed. ∎

Lemma 2.5.

Let be a probability space, let and be separable metric spaces, let , , be random variables which satisfy for every that

| (38) |

and let be a continuous function. Then it holds for every that

| (39) |

Proof of Lemma 2.5.

Lemma 2.6.

Let , , , , let and be functions which satisfy for every that , let be an at most polynomially growing continuous function, let be a probability space with a normal filtration , let be a continuous uniformly distributed /-measurable random variable, let be a standard -Brownian motion, for every let be an -adapted stochastic process with continuous sample paths which satisfies that for every it holds -a.s. that

| (40) |

and let be an -adapted stochastic process with continuous sample paths which satisfies that for every it holds -a.s. that

| (41) |

Then

-

(i)

it holds for every that the functions and are /-measurable,

-

(ii)

it holds for every , that

(42) -

(iii)

it holds for every that

-

(iv)

it holds that the function is continuous, and

-

(v)

it holds that

(43)

Proof of Lemma 2.6.

Throughout this proof let be a real number which satisfies for every that

| (44) |

let , , be the functions which satisfy for every , that , and let , , , be the functions which satisfy for every , , , , that and

| (45) |

Observe that the fact that the Borel sigma-algebra is generated by the set (cf., for example, Klenke [39, Theorem 21.31]), the hypothesis that for every it holds that is an -adapted stochastic process with continuous sample paths, and the hypothesis that is an -adapted stochastic process with continuous sample paths demonstrate that the functions

| (46) |

and

| (47) |

are /-measurable. Combining this with the fact that the function is /-measurable implies that for every it holds that the functions and are /-measurable. This proves item (i). Next observe that (45), the hypothesis that and are globally Lipschitz continuous, and the fact that for every it holds that ensure that for every it holds that

| (48) |

(cf., for example, Kloeden & Platen [41, Section 10.6]). Next note that (40), (41), (45), the fact that and are locally Lipschitz continuous functions, and e.g., Hutzenthaler & Jentzen [32, Theorem 3.3] ensure that for every , it holds that

| (49) |

and

| (50) |

Combining (46), (47), and, e.g., Hutzenthaler & Jentzen [32, Lemma 3.10] hence demonstrates that for every it holds that

| (51) |

and

| (52) |

This and (48) assure that for every it holds that

| (53) |

Combining (44) and the fact that , therefore demonstrates that for every it holds that

| (54) |

This establishes item (iii). In the next step we observe that (40) ensures that for every , it holds -a.s. that

| (55) |

The triangle inequality hence ensures that for every , it holds -a.s. that

| (56) |

Therefore, we obtain for every , , that

| (57) |

The Burkholder-Davis-Gundy type inequality in Da Prato & Zabczyk [13, Lemma 7.2] hence shows that for every , , it holds that

| (58) |

This demonstrates that for every , , it holds that

| (59) |

Hölder’s inequality hence proves that for every , , it holds that

| (60) |

The fact that therefore shows that for every , , it holds that

| (61) |

Combining the Gronwall inequality (cf., e.g., Andersson et al. [2, Lemma 2.6] (with , , , , in the notation of Lemma 2.6)) and (53) hence establishes that for every , , it holds that

| (62) |

Therefore, we obtain that for every , it holds that

| (63) |

This establishes item (ii). Next observe that item (ii) and Jensen’s inequality imply that for every it holds that

| (64) |

The hypothesis that the function is continuous and Lemma 2.5 hence ensure that for every , with it holds that

| (65) |

Combining (54) with, e.g., Hutzenthaler et al. [35, Proposition 4.5] therefore implies that for every with it holds that

| (66) |

This establishes item (iv). In the next step we observe that (49) and (50) ensure that for every , it holds that

| (67) |

The hypothesis that the function is continuous and Lemma 2.5 therefore demonstrate that for every , it holds that

| (68) |

Next observe that (44) assures that for every , , it holds that

| (69) |

Combining (48) and (53) hence shows that for every it holds that

| (70) |

This, (68), and, e.g., Hutzenthaler et al. [35, Proposition 4.5] imply that for every it holds that

| (71) |

Combining (70) with Lebesgue’s dominated convergence theorem therefore demonstrates that

| (72) |

In addition, observe that (69), (48), and (53) prove that for all it holds that

| (73) |

Next observe that (71) and the fact that and are independent imply that

| (74) | ||||

Combining Fubini’s theorem, (72), and (73) with Lebesgue’s dominated convergence theorem therefore assures that

| (75) | ||||

This establishes item (v). The proof of Lemma 2.6 is thus completed. ∎

Proposition 2.7.

Let , , , , let and be globally Lipschitz continuous functions, let be a function, let be a function with at most polynomially growing partial derivatives which satisfies for every , that and

| (76) |

let be a probability space with a normal filtration , let be a standard -Brownian motion, let be a continuous uniformly distributed /-measurable random variable, and let be an -adapted stochastic process with continuous sample paths which satisfies that for every it holds -a.s. that

| (77) |

Then

-

(i)

it holds that the function is twice continuously differentiable with at most polynomially growing derivatives,

-

(ii)

it holds that there exists a unique continuous function such that

(78) and

-

(iii)

it holds for every that .

Proof of Proposition 2.7.

Throughout this proof let , , be -adapted stochastic processes with continuous sample paths

-

a)

which satisfy that for every , it holds -a.s. that

(79) and

- b)

Note that the assumption that and the assumption that has at most polynomially growing partial derivatives establish item (i). Next note that item (i) and the fact that for every , it holds that

| (80) |

assure that for every it holds that

| (81) |

Item (i), the assumption that for every it holds that the function is continuous, and, e.g., Hutzenthaler et al. [35, Proposition 4.5] hence ensure that the function

| (82) |

is continuous. In the next step we combine the fact that for every it holds that the function is /-measurable, the fact that for every it holds that the function is continuous, and Lemma 2.4 to obtain that the function

| (83) |

is /-measurable. Combining this, (81), (82), and Proposition 2.2 demonstrates

-

A)

that there exists a unique continuous function which satisfies that

(84) and

-

B)

that it holds for every that

(85)

Next note that for every continuous function it holds that

| (86) |

Item (i) hence implies that for every continuous function it holds that

| (87) |

is an at most polynomially growing continuous function. Combining Lemma 2.6 (with for in the notation of Lemma 2.6), (77), item (i), and (79) hence ensures that for every continuous function it holds that

| (88) |

Hence, we obtain that for every continuous function with it holds that

| (89) |

Combining this with (84) proves that for every continuous function with it holds that

| (90) |

Next observe that (88) and (84) demonstrate that

| (91) |

Combining this with (90) proves item (ii). Next note that (76), (85), and the Feynman-Kac formula (cf., for example, Hairer et al. [22, Corollary 4.17]) imply that for every it holds that . This establishes item (iii). The proof of Proposition 2.7 is thus completed. ∎

In the next step we use Proposition 2.7 to obtain a minimization problem which is uniquely solved by the function . More specifically, let be a continuously uniformly distributed /-measurable random variable, and let be an -adapted stochastic process with continuous sample paths which satisfies that for every it holds -a.s. that

| (92) |

Proposition 2.7 then guarantees that the function is the unique global minimizer of the function

| (93) |

In the following two subsections we derive an approximated minimization problem by discretizing the stochastic process (see Subsection 2.4 below) and by employing a deep neural network approximation for the function (see Subsection 2.5 below).

2.4 Discretization of the stochastic differential equation

In this subsection we use the Euler-Maruyama scheme (cf., for example, Kloeden & Platen [41] and Maruyama [44]) to temporally discretize the solution process of the SDE (92).

More specifically, let , let be real numbers which satisfy that

| (94) |

Note that (92) implies that for every it holds -a.s. that

| (95) |

This suggests that for sufficiently small mesh size it holds that

| (96) |

Let be the stochastic process which satisfies for every that and

| (97) |

Observe that (96) and (97) suggest, in turn, that for every it holds that

| (98) |

(cf., for example, Theorem 2.8 below for a strong convergence result for the Euler-Maruyama scheme).

Theorem 2.8 (Strong convergence rate for the Euler-Maruyama scheme).

Let , , , let be a probability space with a normal filtration , let be a standard -Brownian motion, let be a random variable which satisfies that , let and be Lipschitz continuous functions, let be an -adapted stochastic process with continuous sample paths which satisfies that for every it holds -a.s. that

| (99) |

for every let be real numbers which satisfy that

| (100) |

and for every let be the stochastic process which satisfies for every that and

| (101) |

Then there exists a real number such that for every it holds that

| (102) |

2.5 Deep artificial neural network approximations

In this subsection we employ suitable approximations for the solution of the PDE (1) at time .

More specifically, let and let be a continuous function. For every suitable and every we think of as an appropriate approximation

| (103) |

of . We suggest to choose the function as a deep neural network (cf., for example, Bishop [6]). For instance, let be the function which satisfies for every that

| (104) |

(multidimensional version of the standard logistic function), for every , , with let be the function which satisfies for every that

| (105) |

let , assume that , and let be the function which satisfies for every , that

| (106) |

The function in (106) describes an artificial neural network with layers (1 input layer with neurons, hidden layers with neurons each, and output layer with neurons) and standard logistic functions as activation functions (cf., for instance, Bishop [6]).

2.6 Stochastic gradient descent-type minimization

As described in Subsection 2.5 for every suitable and every we think of as an appropriate approximation of . In this subsection we intend to find a suitable as an approximate minimizer of the function

| (107) |

To be more specific, we intend to find an approximate minimizer of the function in (107) through a stochastic gradient descent-type minimization algorithm (cf., for instance, Ruder [53, Section 4], Jentzen et al. [37], and the references mentioned therein). For this we approximate the derivative of the function in (107) by means of the Monte Carlo method.

More precisely, let , , be independent continuously uniformly distributed /-measurable random variables, let , , be independent standard -Brownian motions, for every let be the stochastic process which satisfies for every that and

| (108) |

let , and let be a stochastic process which satisfies for every that

| (109) |

Under appropriate hypotheses we think for every sufficiently large of the random variable as a suitable approximation of a local minimum point of the function (107) and we think for every sufficiently large of the random function as a suitable approximation of the function .

2.7 Description of the algorithm in a special case

In this subsection we give a description of the proposed approximation method in a special case, that is, we describe the proposed approximation method in the specific case where a particular neural network approximation is chosen and where the plain-vanilla stochastic gradient descent method with a constant learning rate is the employed stochastic minimization algorithm (cf. (109) above). For a more general description of the proposed approximation method we refer the reader to Subsection 2.8 below.

Framework 2.9.

Let , , , , , let , let be real numbers with

| (110) |

let and be continuous functions, let be a filtered probability space, let , , be independent continuously uniformly distributed /-measurable random variables, let , , be i.i.d. standard -Brownian motions, for every let be the stochastic process which satisfies for every that and

| (111) |

let be the function which satisfies for every that

| (112) |

for every , , with let be the function which satisfies for every that

| (113) |

let be the function which satisfies for every , that

| (114) |

and let be a stochastic process which satisfies for every that

| (115) |

2.8 Description of the algorithm in the general case

In this subsection we provide a general framework which covers the approximation method derived in Subsections 2.1–2.6 above and which allows, in addition, to incorporate other minimization algorithms (cf., for example, Kingma & Ba [38], Ruder [53], E et al. [14], Han et al. [24], and Beck et al. [3]) than just the plain vanilla stochastic gradient descent method. The proposed approximation algorithm is an extension of the approximation algorithm in E et al. [14], Han et al. [24], and Beck et al. [3] in the special case of linear Kolmogorov partial differential equations.

Framework 2.10.

Let , , let , be functions, let be a filtered probability space, let , , , be independent standard -Brownian motions on , let , , , be i.i.d. /-measurable random variables, let be real numbers with , for every , , let be a function, for every , let be a stochastic process which satisfies for every that and

| (117) |

let be a sequence, for every , let be the function which satisfies for every that

| (118) |

for every , let be a function which satisfies for every , that

| (119) |

let be a function, for every let and be functions, let , , and be stochastic processes which satisfy for every that

| (120) |

| (121) |

Under appropriate hypotheses we think for every sufficiently large and every of the random variable in Framework 2.10 as a suitable approximation of where is a function with at most polynomially growing partial derivatives which satisfies for every , that and

| (122) |

where and are sufficiently regular functions (cf. (1) above).

3 Examples

In this section we test the proposed approximation algorithm (see Section 2 above) in the case of several examples of SDEs and Kolmogorov PDEs, respectively. In particular, in this section we apply the proposed approximation algorithm to the heat equation (cf. Subsection 3.2 below), to independent geometric Brownian motions (cf. Subsection 3.3 below), to the Black-Scholes model (cf. Subsection 3.4 below), to stochastic Lorenz equations (cf. Subsection 3.5 below), and to the Heston model (cf. Subsection 3.6 below). In the case of each of the examples below we employ the general approximation algorithm in Framework 2.10 above in conjunction with the Adam optimizer (cf. Kingma & Ba [38]) with mini-batches of size 8192 in each iteration step (see Subsection 3.1 below for a precise description). Moreover, we employ a fully-connected feedforward neural network with one input layer, two hidden layers, and one one-dimensional output layer in our implementations in the case of each of these examples. We also use batch normalization (cf. Ioffe & Szegedy [36]) just before the first linear transformation, just before each of the two nonlinear activation functions in front of the hidden layers as well as just after the last linear transformation. For the two nonlinear activation functions we employ the multidimensional version of the function . All weights in the neural network are initialized by means of the Xavier initialization (cf. Glorot & Bengio [18]). All computations were performed in single precision (float32) on a NVIDIA GeForce GTX 1080 GPU with 1974 MHz core clock and 8 GB GDDR5X memory with 1809.5 MHz clock rate. The underlying system consisted of an Intel Core i7-6800K CPU with 64 GB DDR4-2133 memory running Tensorflow 1.5 on Ubuntu 16.04.

3.1 Setting

Framework 3.1.

Assume Framework 2.10, let , , , , let , , be the functions which satisfy for every , that

| (123) |

assume for every , that , , , , , assume for every , , , that

| (124) |

and

| (125) |

3.2 Heat equation

In this subsection we apply the proposed approximation algorithm to the heat equation (see (126) below).

Assume Framework 2.10, assume for every , , that , , , , , assume that is continuous uniformly distributed on , and let be an at most polynomially growing function which satisfies for every , that and

| (126) |

Combining, e.g., Lemma 3.2 below with, e.g., Hairer et al. [22, Corollary 4.17 and Remark 4.1] shows that for every , it holds that

| (127) |

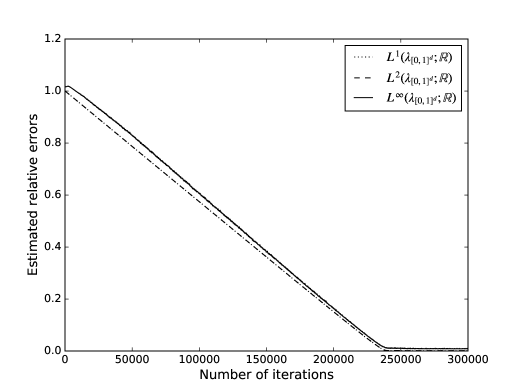

Table 1 approximately presents the relative -approximation error associated to (see (128) below), the relative -approximation error associated to (see (129) below), and the relative -approximation error associated to (see (130) below) against (cf. Python code 2 in Subsection 4.2 below). Figure 1 approximately depicts the relative -approximation error associated to (see (128) below), the relative -approximation error associated to (see (129) below), and the relative -approximation error associated to (see (130) below) against (cf. Python code 2 in Subsection 4.2 below). In our numerical simulations for Table 1 and Figure 1 we calculated the exact solution of the PDE (126) by means of Lemma 3.2 below (see (127) above), we approximately calculated the relative -approximation error

| (128) |

for by means of Monte Carlo approximations with 10240000 samples, we approximately calculated the relative -approximation error

| (129) |

for by means of Monte Carlo approximations with 10240000 samples, and we approximately calculated the relative -approximation error

| (130) |

for by means of Monte Carlo approximations with 10240000 samples (see Lemma 3.5 below). Table 2 approximately presents the relative -approximation error associated to (see (131) below), the relative -approximation error associated to (see (132) below), and the relative -approximation error associated to (see (133) below), against (cf. Python code 2 in Subsection 4.2 below). In our numerical simulations for Table 2 we calculated the exact solution of the PDE (126) by means of Lemma 3.2 below (see (127) above), we approximately calculated the relative -approximation error

| (131) |

for by means of Monte Carlo approximations with 10240000 samples for the Lebesgue integral and 5 samples for the expectation, we approximately calculated the relative -approximation error

| (132) |

for by means of Monte Carlo approximations with 10240000 samples for the Lebesgue integral and 5 samples for the expectation, and we approximately calculated the relative -approximation error

| (133) |

for by means of Monte Carlo approximations with 10240000 samples for the supremum (see Lemma 3.5 below) and 5 samples for the expectation. The following elementary result, Lemma 3.2 below, specifies the explicit solution of the PDE (126) above (cf. (127) above). For completeness we also provide here a proof for Lemma 3.2.

|

|

|

|

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.998253 | 0.998254 | 1.003524 | 0.5 | ||||||||||

| 10000 | 0.957464 | 0.957536 | 0.993083 | 44.6 | ||||||||||

| 50000 | 0.786743 | 0.786806 | 0.828184 | 220.8 | ||||||||||

| 100000 | 0.574013 | 0.574060 | 0.605283 | 440.8 | ||||||||||

| 150000 | 0.361564 | 0.361594 | 0.384105 | 661.0 | ||||||||||

| 200000 | 0.150346 | 0.150362 | 0.164140 | 880.8 | ||||||||||

| 500000 | 0.000882 | 0.001112 | 0.007360 | 2200.7 | ||||||||||

| 750000 | 0.000822 | 0.001036 | 0.007423 | 3300.6 |

|

|

|

|

|

||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1.000310 | 1.000311 | 1.005674 | 0.6 | ||||||||||||||||

| 10000 | 0.957481 | 0.957554 | 0.993097 | 44.7 | ||||||||||||||||

| 50000 | 0.786628 | 0.786690 | 0.828816 | 220.4 | ||||||||||||||||

| 100000 | 0.573867 | 0.573914 | 0.605587 | 440.5 | ||||||||||||||||

| 150000 | 0.361338 | 0.361369 | 0.382967 | 660.8 | ||||||||||||||||

| 200000 | 0.001387 | 0.001741 | 0.010896 | 880.9 | ||||||||||||||||

| 500000 | 0.000883 | 0.001112 | 0.008017 | 2201.0 | ||||||||||||||||

| 750000 | 0.000822 | 0.001038 | 0.007547 | 3300.4 |

Lemma 3.2.

Let , , let be a strictly positive and symmetric matrix, and let be the function which satisfies for every that

| (134) |

Then

-

(i)

it holds that is at most polynomially growing and

-

(ii)

it holds for every , that

(135)

Proof of Lemma 3.2.

Lemma 3.5 below discloses the strategy how we approximatively calculate the -errors in (130) and (133) above. Our proof of Lemma 3.5 employs the elementary auxiliary results in Lemma 3.3 and Lemma 3.4 below. For completeness we also include proofs for Lemma 3.3 and Lemma 3.4 here.

Lemma 3.3.

Let be a probability space and let satisfy that . Then it holds that

| (139) |

Proof of Lemma 3.3.

Observe that the monotonicity of ensures that

| (140) |

Hence, we obtain that for every with it holds that . The Proof of Lemma 3.3 is thus completed. ∎

Lemma 3.4.

Let be a probability space, let , , be random variables, assume for every that , and assume for every that

| (141) |

Then

| (142) |

Proof of Lemma 3.4.

Throughout this proof let be the set given by

| (143) |

Observe that Lemma 3.3 and the hypothesis that for every it holds that assure that for every it holds that

| (144) |

This implies that for every it holds that

| (145) |

The fact that the measure is continuous from above hence demonstrates that

| (146) |

Next note that

| (147) |

Lemma 3.3 and (146) therefore ensure that

| (148) |

Combining this and (141) establishes (142). The proof of Lemma 3.4 is thus completed. ∎

Lemma 3.5.

Let , , , let be a continuous function, let be a probability space, let , , be i.i.d. random variables, and assume that is continuous uniformly distributed on . Then

-

(i)

it holds that

(149) and

-

(ii)

it holds for every that

(150)

Proof of Lemma 3.5.

First, observe that the fact that is a continuous function and the fact that is a compact set demonstrate that there exists which satisfies that . Next note that the fact that for every , it holds that implies that for every it holds that . Hence, we obtain that for every it holds that

| (151) |

Combining this with the fact that ensures that for every , it holds that

| (152) |

In the next step we observe that the fact that is continuous ensures that for every there exists such that for every with it holds that . Combining this and (152) shows that for every there exists such that for every it holds that

| (153) |

Hence, we obtain that for every there exists such that

| (154) |

Next observe that the fact that the random variables , , are i.i.d. ensures that for every , it holds that

| (155) |

In addition, note that the fact that for every it holds that the set has strictly positive -dimensional Lebesgue measure and the fact that is continuous uniformly distributed on ensure that for every it holds that

| (156) |

Hence, we obtain that for every it holds that

| (157) |

Combining this with (155) demonstrates that for every it holds that

| (158) |

This and (154) assure that for every it holds that

| (159) |

Therefore, we obtain that for every it holds that

| (160) |

Combining this with with Lemma 3.4 establishes item (i). It thus remains to prove item (ii). For this note that the fact that is globally bounded, item (i), and Lebesgue’s dominated convergence theorem ensure that for every it holds that

| (161) |

This establishes item (ii). The proof of Lemma 3.5 is thus completed. ∎

3.3 Geometric Brownian motions

In this subsection we apply the proposed approximation algorithm to a Black-Scholes PDE with independent underlying geometric Brownian motions.

Assume Framework 2.10, let , , , ,…, , assume for every , , , that , , , and

| (162) |

assume that is continuous uniformly distributed on , and let be an at most polynomially growing function which satisfies for every , that and

| (163) |

The Feynman-Kac formula (cf., for example, Hairer et al. [22, Corollary 4.17]) shows that for every standard Brownian motion and every , it holds that

| (164) |

Table 3 approximately presents the relative -approximation error associated to (see (165) below), the relative -approximation error associated to (see (166) below), and the relative -approximation error associated to (see (167) below) against (cf. Python code 3 in Subsection 4.3 below). In our numerical simulations for Table 3 we approximately calculated the exact solution of the PDE (163) by means of (164) and Monte Carlo approximations with 1048576 samples, we approximately calculated the relative -approximation error

| (165) |

for by means of Monte Carlo approximations with 81920 samples, we approximately calculated the relative -approximation error

| (166) |

for by means of Monte Carlo approximations with 81920 samples, and we approximately calculated the relative -approximation error

| (167) |

for by means of Monte Carlo approximations with 81920 samples (see Lemma 3.5 above).

|

|

|

|

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1.004285 | 1.004286 | 1.009524 | 1 | ||||||||||

| 25000 | 0.842938 | 0.843021 | 0.87884 | 110.2 | ||||||||||

| 50000 | 0.684955 | 0.685021 | 0.719826 | 219.5 | ||||||||||

| 100000 | 0.371515 | 0.371551 | 0.387978 | 437.9 | ||||||||||

| 150000 | 0.064605 | 0.064628 | 0.072259 | 656.2 | ||||||||||

| 250000 | 0.001220 | 0.001538 | 0.010039 | 1092.6 | ||||||||||

| 500000 | 0.000949 | 0.001187 | 0.005105 | 2183.8 | ||||||||||

| 750000 | 0.000902 | 0.001129 | 0.006028 | 3275.1 |

3.4 Black-Scholes model with correlated noise

In this subsection we apply the proposed approximation algorithm to a Black-Scholes PDE with correlated noise.

Assume Framework 2.10, let , , , ,…, , , , , assume for every , , , , with that , , , , , , , (cf., for example, Golub & Van Loan [19, Theorem 4.2.5]), , , and

| (168) |

assume that is continuous uniformly distributed on , and let be an at most polynomially growing continuous function which satisfies for every , that and

| (169) |

The Feynman-Kac formula (cf., for example, Hairer et al. [22, Corollary 4.17]) shows that for every standard Brownian motion and every , it holds that

| (170) |

Table 4 approximately presents the relative -approximation error associated to (see (171) below), the relative -approximation error associated to (see (172) below), and the relative -approximation error associated to (see (173) below) against (cf. Python code 4 in Subsection 3.4 below). In our numerical simulations for Table 4 we approximately calculated the exact solution of the PDE (169) by means of (170) and Monte Carlo approximations with 1048576 samples, we approximately calculated the relative -approximation error

| (171) |

for by means of Monte Carlo approximations with 81920 samples, we approximately calculated the relative -approximation error

| (172) |

for by means of Monte Carlo approximations with 81920 samples, and we approximately calculated the relative -approximation error

| (173) |

for by means of Monte Carlo approximations with 81920 samples (see Lemma 3.5 above).

|

|

|

|

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1.003383 | 1.003385 | 1.011662 | 0.8 | ||||||||||

| 25000 | 0.631420 | 0.631429 | 0.640633 | 112.1 | ||||||||||

| 50000 | 0.269053 | 0.269058 | 0.275114 | 223.3 | ||||||||||

| 100000 | 0.000752 | 0.000948 | 0.00553 | 445.8 | ||||||||||

| 150000 | 0.000694 | 0.00087 | 0.004662 | 668.2 | ||||||||||

| 250000 | 0.000604 | 0.000758 | 0.006483 | 1119.3 | ||||||||||

| 500000 | 0.000493 | 0.000615 | 0.002774 | 2292.8 | ||||||||||

| 750000 | 0.000471 | 0.00059 | 0.002862 | 3466.8 |

3.5 Stochastic Lorenz equations

In this subsection we apply the proposed approximation algorithm to the stochastic Lorenz equation.

Assume Framework 2.10, let , , , , let be a function, assume for every , , , that , , , , , and

| (174) |

(cf., for example, Hutzenthaler et al. [32], Hutzenthaler et al. [33], Hutzenthaler et al. [34], Milstein & Tretyakov [48], Sabanis [54, 55], and the references mentioned therein for related temporal numerical approximation schemes for SDEs), assume that is continuous uniformly distributed on , and let be an at most polynomially growing function (cf., for example, Hairer et al. [22, Corollary 4.17] and Hörmander [31, Theorem 1.1])for every , that and

| (175) |

Table 5 approximately presents the relative -approximation error associated to (see (176) below), the relative -approximation error associated to (see (177) below), and the relative -approximation error associated to (see (178) below) against (cf. Python code 5 in Subsection 4.5 below). In our numerical simulations for Table 5 we approximately calculated the exact solution of the PDE (LABEL:eq:example_lorenz_kolmogorovPDE) by means of Monte Carlo approximations with 104857 samples and temporal SDE-discretizations based on (174) and 100 equidistant time steps, we approximately calculated the relative -approximation error

| (176) |

for by means of Monte Carlo approximations with 20480 samples, we approximately calculated the relative -approximation error

| (177) |

for by means of Monte Carlo approximations with 20480 samples, and we approximately calculated the relative -approximation error

| (178) |

for by means of Monte Carlo approximations with 20480 samples (see Lemma 3.5 above).

|

|

|

|

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.995732 | 0.995732 | 0.996454 | 1.0 | ||||||||||

| 25000 | 0.905267 | 0.909422 | 1.247772 | 750.1 | ||||||||||

| 50000 | 0.801935 | 0.805497 | 1.115690 | 1461.7 | ||||||||||

| 100000 | 0.599847 | 0.602630 | 0.823042 | 2932.1 | ||||||||||

| 150000 | 0.392394 | 0.394204 | 0.542209 | 4423.3 | ||||||||||

| 250000 | 0.000732 | 0.000811 | 0.002865 | 7327.9 | ||||||||||

| 500000 | 0.000312 | 0.000365 | 0.003158 | 14753.0 | ||||||||||

| 750000 | 0.000187 | 0.000229 | 0.001264 | 21987.4 |

3.6 Heston model

In this subsection we apply the proposed approximation algorithm to the Heston model in (180) below.

Assume Framework 2.10, let , , , , , , let , , be the vectors which satisfy that , , …, , assume for every , , that , , , , and

| (179) |

(cf. Hefter & Herzwurm [25, Section 1]), assume that is continuous uniformly distributed on , and let be an at most polynomially growing function (cf., for example, Alfonsi [1, Proposition 4.1]) which satisfies for every , that and

| (180) |

Table 6 approximately presents the relative -approximation error associated to (see (181) below), the relative -approximation error associated to (see (182) below), and the relative -approximation error associated to (see (183) below) against (cf. Python code 6 in Subsection 4.6 below). In our numerical simulations for Table 6 we approximately calculated the exact solution of the PDE (180) by means of Monte Carlo approximations with 1048576 samples and temporal SDE-discretizations based on (179) and 100 equidistant time steps, we approximately calculated the relative -approximation error

| (181) |

for by means of Monte Carlo approximations with 10240 samples, we approximately calculated the relative -approximation error

| (182) |

for by means of Monte Carlo approximations with 10240 samples, and we approximately calculated the relative -approximation error

| (183) |

for by means of Monte Carlo approximations with 10240 samples (see Lemma 3.5 above).

|

|

|

|

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1.038045 | 1.038686 | 1.210235 | 1.0 | ||||||||||

| 25000 | 0.005691 | 0.007215 | 0.053298 | 688.4 | ||||||||||

| 50000 | 0.005115 | 0.006553 | 0.036513 | 1375.2 | ||||||||||

| 100000 | 0.004749 | 0.005954 | 0.032411 | 2746.8 | ||||||||||

| 150000 | 0.006465 | 0.008581 | 0.051907 | 4120.2 | ||||||||||

| 250000 | 0.005075 | 0.006378 | 0.024458 | 6867.5 | ||||||||||

| 500000 | 0.002082 | 0.002704 | 0.019604 | 13763.7 | ||||||||||

| 750000 | 0.00174 | 0.002233 | 0.012466 | 20758.8 |

4 Python source codes

4.1 Python source code for the algorithm

In Subsections 4.2–4.6 below we present Python source codes associated to the numerical simulations in Subsections 3.2–3.6 above. The following Python source code, Python code 1 below, is employed in the case of each of the Python source codes in Subsections 4.2–4.6 below.

4.2 A Python source code associated to the numerical simulations in Subsection 3.2

4.3 A Python source code associated to the numerical simulations in Subsection 3.3

4.4 A Python source code associated to the numerical simulations in Subsection 3.4

4.5 A Python source code associated to the numerical simulations in Subsection 3.5

4.6 A Python source code associated to the numerical simulations in Subsection 3.6

References

- [1] Alfonsi, A. On the discretization schemes for the CIR (and Bessel squared) processes. Monte Carlo Methods and Applications mcma 11, 4 (2005), 355–384.

- [2] Andersson, Adam and Jentzen, Arnulf and Kurniawan, Ryan. Existence, uniqueness, and regularity for stochastic evolution equations with irregular initial values. arXiv:1512.06899 (2015), 35 pages. Revision requested from J. Math. Anal. Appl.

- [3] Beck, C., E, W., and Jentzen, A. Machine learning approximation algorithms for high-dimensional fully nonlinear partial differential equations and second-order backward stochastic differential equations. arXiv:1709.05963 (2017), 56 pages. Revision requested from J. Nonlinear Sci.

- [4] Becker, S., Cheridito, P., and Jentzen, A. Deep optimal stopping. arXiv:1804.05394 (2018), 18 pages.

- [5] Bellman, R. E. Dynamic Programming. Princeton University Press, 1957.

- [6] Bishop, C. M. Pattern recognition and machine learning. Information Science and Statistics. Springer, New York, 2006.

- [7] Brennan, M. J., and Schwartz, E. S. The valuation of american put options. The Journal of Finance 32, 2 (1977), 449–462.

- [8] Brennan, M. J., and Schwartz, E. S. Finite difference methods and jump processes arising in the pricing of contingent claims: A synthesis. The Journal of Financial and Quantitative Analysis 13, 3 (1978), 461–474.

- [9] Brenner, S., and Scott, R. The mathematical theory of finite element methods, vol. 15. Springer Science & Business Media, 2007.

- [10] Ciarlet, P. G. Basic error estimates for elliptic problems.

- [11] Cox, S., Hutzenthaler, M., and Jentzen, A. Local Lipschitz continuity in the initial value and strong completeness for nonlinear stochastic differential equations. arXiv:1309.5595 (2013), 84 pages.

- [12] Cox, Sonja and Jentzen, Arnulf and Kurniawan, Ryan and Pušnik, Primož. On the mild Itô formula in Banach spaces. arXiv:1612.03210 (2016), 27 pages. Accepted in Discrete Contin. Dyn. Syst. Ser. B.

- [13] Da Prato, G., and Zabczyk, J. Stochastic Equations in Infinite Dimensions. Encyclopedia of Mathematics and its Applications. Cambridge University Press, 2008.

- [14] E, W., Han, J., and Jentzen, A. Deep learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations. Communications in Mathematics and Statistics (2017), 349–380.

- [15] E, W., and Yu, B. The Deep Ritz method: A deep learning-based numerical algorithm for solving variational problems. arXiv:1710.00211 (2017), 14 pages.

- [16] Fujii, M., Takahashi, A., and Takahashi, M. Asymptotic Expansion as Prior Knowledge in Deep Learning Method for high dimensional BSDEs. arXiv:1710.07030 (2017), 16 pages.

- [17] Giles, M. B. Multilevel Monte Carlo path simulation. Oper. Res. 56, 3 (2008), 607–617.

- [18] Glorot, X., and Bengio, Y. Understanding the difficulty of training deep feedforward neural networks. In Proceedings of the thirteenth international conference on artificial intelligence and statistics (2010), pp. 249–256.

- [19] Golub, G. H., and Van Loan, C. F. Matrix computations, fourth ed. Johns Hopkins Studies in the Mathematical Sciences. Johns Hopkins University Press, Baltimore, MD, 2013.

- [20] Graham, C., and Talay, D. Stochastic simulation and Monte Carlo methods, vol. 68 of Stochastic Modelling and Applied Probability. Springer, Heidelberg, 2013. Mathematical foundations of stochastic simulation.

- [21] Gyöngy, I. A note on Euler’s approximations. Potential Anal. 8, 3 (1998), 205–216.

- [22] Hairer, M., Hutzenthaler, M., and Jentzen, A. Loss of regularity for Kolmogorov equations. Ann. Probab. 43, 2 (2015), 468–527.

- [23] Han, H., and Wu, X. A fast numerical method for the black–scholes equation of american options. SIAM Journal on Numerical Analysis 41, 6 (2003), 2081–2095.

- [24] Han, J., Jentzen, A., and E, W. Overcoming the curse of dimensionality: Solving high-dimensional partial differential equations using deep learning. arXiv:1707.02568 (2017), 13 pages.

- [25] Hefter, M., and Herzwurm, A. Strong convergence rates for Cox-Ingersoll-Ross processes—full parameter range. J. Math. Anal. Appl. 459, 2 (2018), 1079–1101.

- [26] Henry-Labordere, P. Deep Primal-Dual Algorithm for BSDEs: Applications of Machine Learning to CVA and IM. 16 pages. Available at SSRN: https://ssrn.com/abstract=3071506.

- [27] Higham., D. J. An Algorithmic Introduction to Numerical Simulation of Stochastic Differential Equations. SIAM Review 43, 3 (2001), 525–546.

- [28] Higham, D. J. Stochastic ordinary differential equations in applied and computational mathematics. IMA journal of applied mathematics 76, 3 (2011), 449–474.

- [29] Higham, D. J., Mao, X., and Stuart, A. M. Strong convergence of Euler-type methods for nonlinear stochastic differential equations. SIAM J. Numer. Anal. 40, 3 (2002), 1041–1063.

- [30] Hofmann, N., Müller-Gronbach, T., and Ritter, K. Optimal approximation of stochastic differential equations by adaptive step-size control. Math. Comp. 69, 231 (2000), 1017–1034.

- [31] Hörmander, L. Hypoelliptic second order differential equations. Acta Math. 119 (1967), 147–171.

- [32] Hutzenthaler, M., and Jentzen, A. Numerical approximations of stochastic differential equations with non-globally Lipschitz continuous coefficients. Mem. Amer. Math. Soc. 236, 1112 (2015), v+99.

- [33] Hutzenthaler, M., Jentzen, A., and Kloeden, P. E. Strong convergence of an explicit numerical method for SDEs with nonglobally Lipschitz continuous coefficients. Ann. Appl. Probab. 22, 4 (2012), 1611–1641.

- [34] Hutzenthaler, M., Jentzen, A., and Wang, X. Exponential integrability properties of numerical approximation processes for nonlinear stochastic differential equations. Math. Comp. 87, 311 (2018), 1353–1413.

- [35] Hutzenthaler, Martin and Jentzen, Arnulf and Salimova, Diyora. Strong convergence of full-discrete nonlinearity-truncated accelerated exponential Euler-type approximations for stochastic Kuramoto-Sivashinsky equations. arXiv:1604.02053 (2016), 40 pages. Accepted in Comm. Math. Sci.

- [36] Ioffe, S., and Szegedy, C. Batch normalization: Accelerating deep network training by reducing internal covariate shift. arXiv:1502.03167 (2015), 11 pages.

- [37] Jentzen, A., Kuckuck, B., Neufeld, A., and von Wurstemberger, P. Strong -error analysis for stochastic gradient descent optimization algorithms. (2018), 51 pages.

- [38] Kingma, D., and Ba, J. Adam: a method for stochastic optimization. Proceedings of the International Conference on Learning Representations (ICLR), 2015.

- [39] Klenke, A. Probability theory, second ed. Universitext. Springer, London, 2014. A comprehensive course.

- [40] Kloeden, P. E. The systematic derivation of higher order numerical schemes for stochastic differential equations. Milan J. Math. 70 (2002), 187–207.

- [41] Kloeden, P. E., and Platen, E. Numerical solution of stochastic differential equations, vol. 23 of Applications of Mathematics (New York). Springer-Verlag, Berlin, 1992.

- [42] Kloeden, P. E., Platen, E., and Schurz, H. Numerical solution of SDE through computer experiments. Springer Science & Business Media, 2012.

- [43] Kushner, H. Finite difference methods for the weak solutions of the kolmogorov equations for the density of both diffusion and conditional diffusion processes. Journal of Mathematical Analysis and Applications 53, 2 (1976), 251 – 265.

- [44] Maruyama, G. Continuous Markov processes and stochastic equations. Rend. Circ. Mat. Palermo (2) 4 (1955), 48–90.

- [45] Milstein, G. N. Approximate integration of stochastic differential equations. Teor. Verojatnost. i Primenen. 19 (1974), 583–588.

- [46] Milstein, G. N. Numerical integration of stochastic differential equations, vol. 313 of Mathematics and its Applications. Kluwer Academic Publishers Group, Dordrecht, 1995. Translated and revised from the 1988 Russian original.

- [47] Milstein, G. N., and Tretyakov, M. V. Stochastic numerics for mathematical physics. Scientific Computation. Springer-Verlag, Berlin, 2004.

- [48] Milstein, G. N., and Tretyakov, M. V. Numerical Integration of Stochastic Differential Equations with Nonglobally Lipschitz Coefficients. SIAM Journal on Numerical Analysis 43, 3 (2005), 1139–1154.

- [49] Müller-Gronbach, T., and Ritter, K. Minimal errors for strong and weak approximation of stochastic differential equations. In Monte Carlo and quasi-Monte Carlo methods 2006. Springer, Berlin, 2008, pp. 53–82.

- [50] Øksendal, B. Stochastic differential equations, sixth ed. Universitext. Springer-Verlag, Berlin, 2003. An introduction with applications.

- [51] Raissi, M. Forward-backward stochastic neural networks: Deep learning of high-dimensional partial differential equations. arXiv:1804.07010 (2018).

- [52] Rößler, A. Runge-Kutta Methods for the Strong Approximation of Solutions of Stochastic Differential Equations. Shaker, Aachen, 2009.

- [53] Ruder, S. An overview of gradient descent optimization algorithms. arXiv:1609.04747 (2016), 14 pages.

- [54] Sabanis, S. A note on tamed Euler approximations. Electron. Commun. Probab. 18 (2013), no. 47, 10.

- [55] Sabanis, S. Euler approximations with varying coefficients: the case of superlinearly growing diffusion coefficients. Ann. Appl. Probab. 26, 4 (2016), 2083–2105.

- [56] Schwartz, E. S. The valuation of warrants: Implementing a new approach. Journal of Financial Economics 4, 1 (1977), 79 – 93.

- [57] Sirignano, J., and Spiliopoulos, K. DGM: A deep learning algorithm for solving partial differential equations. arXiv:1708.07469 (2017), 16 pages.

- [58] Zhao, J., Davison, M., and Corless, R. M. Compact finite difference method for american option pricing. Journal of Computational and Applied Mathematics 206, 1 (2007), 306 – 321.

- [59] Zienkiewicz, O. C., Taylor, R. L., Zienkiewicz, O. C., and Taylor, R. L. The finite element method, vol. 3. McGraw-hill London, 1977.