25mm30mm30mm30mm

Fast Hybrid Schemes for Fractional Riccati Equations

(Rough is not so Tough)

Abstract

We solve a family of fractional Riccati equations with constant (possibly complex) coefficients. These equations arise, e.g., in fractional Heston stochastic volatility models, that have received great attention in the recent financial literature thanks to their ability to reproduce a rough volatility behavior. We first consider the case of a zero initial value corresponding to the characteristic function of the log-price. Then we investigate the case of a general starting value associated to a transform also involving the volatility process. The solution to the fractional Riccati equation takes the form of power series, whose convergence domain is typically finite. This naturally suggests a hybrid numerical algorithm to explicitly obtain the solution also beyond the convergence domain of the power series. Numerical tests show that the hybrid algorithm is extremely fast and stable. When applied to option pricing, our method largely outperforms the only available alternative, based on the Adams method.

2010 Mathematics Subject Classification. 60F10, 91G99, 91B25.

Keywords: fractional Brownian motion, fractional Riccati equation, rough Heston model, power series representation.

1 Introduction and Motivation

Stochastic volatility models have received great attention in the last decades in the financial community. The most celebrated model is probably the one introduced by Heston (1993), where the asset price has a diffusive dynamics with a stochastic volatility following a square root process driven by a Brownian motion partially correlated with the one driving the underlying. This correlation is important in order to capture the leverage effect, a stylized feature observed in the option market that translates into a skewed implied volatility surface. The Heston model is also able to reproduce other stylized facts, as fat tails for the distribution of the underlying and time-varying volatility. What is more, the characteristic function of the asset price can be computed in closed form, so that the Heston model turns out to be highly tractable insofar option pricing as well as calibration can be efficiently performed through Fourier methods. This analytical tractability is probably the main reason behind the success of the Heston model among practitioners.

Recently, there has been an increasing attention in the literature to some roughness phenomena observed in the volatility behaviour of high frequency data, which suggest that the log-volatility is very well modeled by a fractional Brownian motion with Hurst parameter of order , see e.g. El Euch and Rosenbaum (2019), Jaisson and Rosenbaum (2016), Gatheral et al. (2018). From a practitioner’s perspective, rough volatility models would in principle allow for a good fit of the whole volatility surface, in a parsimonious way. Nevertheless, being the fractional Brownian motion non-Markovian, mathematical tractability might be a challenge. The idea of introducing a fractional Brownian motion in the volatility noise is not new and it goes back, to the best of our knowledge, to Comte and Renault (1998), where the authors extend the Hull and White (1987) stochastic volatility model to the case where the volatility displays long-memory, in order to capture the empirical evidence of persistence of the stochastic feature of the Black Scholes implied volatilities, when time to maturity increases. Long-memory is associated to a Hurst index greater than , while the classic Brownian motion case corresponds to a Hurst parameter equal to 0.5. As the debate on the empirical value for the Hurst index is still controversial in the literature, in our paper we will consider settings which include the complete range of the Hurst coefficient, namely .

A fractional adaptation of the classical Heston model has come under the spotlight (see e.g. the papers El Euch and Rosenbaum (2019), Gatheral et al. (2018) and Jaisson and Rosenbaum (2016)), since, in this case, pricing of European options is still feasible and hedging portfolios for vanilla options are explicit. In addition, the fractional version of the Heston model is able to reproduce the slope of the skew for short term expiring options without the need of introducing jumps as in the classical Heston model.

When extending the Heston model to the case where the volatility process is driven by a fractional Brownian motion, one faces some challenges due to the fact that the model is no longer Markovian, due to the presence of memory in the volatility process. On the one hand, the model keeps the affine structure, so that the computation of the characteristic function of the log-price is still associated to the solution of a quadratic ODE as in the classic Heston case. On the other hand, such Riccati ODE involves fractional derivatives and their solution is no longer available in closed form. The Adams discretization scheme (see e.g. Diethelm et al. (2002), Diethelm et al. (2004)) is the standard numerical method to deal with fractional ODEs. As an alternative, a rational approximation, based on Padé approximants, has been recently proposed in Gatheral and Radoicic (2019), who started from the short time expansion of the solution as developed in Alòs et al. (2020). Unfortunately, they considered only a very specific set of parameters (and only one value for the argument of the Fourier transform) and they did not provide a detailed analysis of the error and the computational time, so that it seems difficult to benchmark to their results. From a numerical viewpoint, algorithms based on the Adams method, which is basically an Euler scheme of the equation, are not well performing due to the presence of a discrete time convolution induced by the fact that the fractional derivative is not a local operator. In this respect, Runge-Kutta schemes do not seem to be appropriate. On the contrary, the Richardson-Romberg extrapolation method is easy to implement since it consists of a linear combination of solutions of Euler schemes with coarse and refined steps, so that the same accuracy can be obtained with a dramatic reduction of the computation time (see Talay and Tubaro (1990) and Pagès (2007) who developed and popularized the same paradigm in a stochastic environment). One can reach and even outperform in the multi-step case the rate obtained by Euler schemes for regular ODEs, which is known to be proportional to the inverse of the complexity.

In this paper we study the efficient computation of the solution of the fractional Riccati ODEs arising from the (fractional) Heston model with constant coefficients for a general Hurst index ranging in . It is also worth mentioning paper Gerhold et al. (2019), where the authors exploited the Volterra integral representation for the solution to the Riccati ODE, with null initial condition, in order to find upper and lower bounds for its explosion time. In the specific case of the rough Heston model, they tried a fractional power series ansatz for the solution to the Riccati and, via the Cauchy-Hadamard formula they proposed an approximation of the explosion time (see Theorems 7.5 and 7.6 therein).

We show that it is possible to represent the solution as a power series in a neigbourhood of and we determine upper and lower bounds for its convergence domain. It is important to notice that the existence domain of the solution does not always coincide with the convergence domain of the power series (we will see that this typically happens when the coefficients of the fractional Riccati ODE have different signs), in analogy with the fact that the function is well defined on , despite the convergence domain of its power series expansion is only defined for . From a computational point of view, the expansion we propose is extremely efficient compared with the Richardson-Romberg extrapolation method on its domain of existence. If the solution is needed at a date which is beyond the convergence interval, we propose a hybrid numerical scheme that combines our series expansion together with the Richardson-Romberg machinery. The resulting algorithm turns out to be flexible and still very fast, when compared with the benchmark available in the literature, based on the Adams method.

The fractional Riccati ODE associated to the characteristic function of the log-asset price is very special insofar it starts from zero. More general transforms (including the characteristic function of the volatility process) lead to non zero initial conditions, see e.g. Abi Jaber et al. (2019), where the authors extend the results of El Euch and Rosenbaum (2019) to the case where the volatility is a Volterra process, which includes the (classic and) fractional Heston model for some particular choice of the kernel. The extension of our results to the case of a general (non-null) initial condition is not straightforward and requires additional care. Nevertheless, we will show that it is still possible to provide bounds for the convergence domain of the corresponding power series expansion, at the additional cost of extending the implementation of the algorithm to a doubly indexed series, in the spirit of Guennon et al. (2018).

Notation.

denotes the modulus of the complex number and and its real and imaginary part respectively.

, .

, and , . We will use extensively the classical identities and .

denotes the set of all Lebesgue measurable functions such that , for .

for , denotes the space of absolutely continuous functions on . A function is absolutely continuous if for any there exists a such that for any finite set of pairwise nonintersecting intervals , , such that we have .

, for and for , denotes the space of continuous functions which have continuous derivatives up to order on , with .

2 The Problem

We start by recalling the fractional version of the Heston model, where the pair of the stock (forward) price and its instantaneous variance has the dynamics

| (2.1) |

where are positive real numbers and the correlation between the two Brownian motions and is . The parameter plays a crucial role (see Remark 2.1 below). Notice that the classical Heston (1993) model corresponds to the case .

Remark 2.1.

The smoothness of the volatility trajectories is governed by . Recall that the fractional Brownian motion , where is the Hurst exponent, admits the Manderlbrot-Van Ness representation

where the Hurst parameter plays a crucial role in the path’s regularity of the kernel . In particular, when the Brownian integral has Holder regularity and it allows for a rough behavior (see El Euch and Rosenbaum (2019)). So, defining and taking in the dynamics (2.1) leads to a rough behavior of the trajectories of .

The starting point of our work is the key Theorem 4.1 in El Euch and Rosenbaum (2019), which has been extended by Abi Jaber et al. (2019) (see Theorem 4.3 and Example 7.2 therein) to the class of affine Volterra processes. More precisely, El Euch and Rosenbaum (2019) showed that the characteristic function of the log-price , for and , reads

| (2.2) |

where

| (2.3) |

and solves the fractional Riccati equation for

| (2.4) |

where and denote, respectively, the Riemann-Liouville fractional derivative of order and the Riemann-Liouville integral of order .

Here we briefly recall both definitions, inspired by (Samko et al., 1993, Chapter 2). For any and in , the Riemann-Liouville fractional integral of order is defined as follows

| (2.5) |

Note that we skip in the above fractional integral, thus avoiding the classical notation .

For , we now define the Riemann-Liouville fractional derivative of order of as follows:

| (2.6) |

A sufficient condition for its existence is . In the case when we have

| (2.7) |

A sufficient condition for its existence is .

Remark 2.2.

When , obviously coincides with the regular differentiation operator and the above Riccati equation reduces to the classic one.

Notice that the fractional derivative is also defined for a general as follows:

| (2.8) |

A sufficient condition for its existence is .

More generally, Abi Jaber et al. (2019) in their Example 7.2 proved that for ,

| (2.9) |

where are defined as before and solves the same fractional Riccati equation (2.4) with a different initial condition:

| (2.10) |

This transform can be useful in view of pricing volatility products, as it involves the joint distribution of the asset price and the volatility. Obviously, once the characteristic function is known, option pricing can be easily performed through standard Fourier techniques.

Our first aim in this paper is to solve the fractional Riccati ODE (2.4) with constant coefficients when . From now on, we relabel the coefficients as follows

| (2.11) |

where , , and , are complex numbers (when we use ).

We will propose an efficient numerical method to compute the solution, with a special emphasis on the case where and the initial condition is equal to zero, corresponding to the characteristic function of the log-asset price.

Remark 2.3.

a) Being the Hurst coefficient , the case contains the rough volatility modeling whereas the case contains the long memory modeling and corresponds to the framework of Comte and Renault (1998).

b) We refer, respectively, to El Euch and Rosenbaum (2019) and to Abi Jaber et al. (2019) for existence and uniqueness of the solution to the Riccati equation (2.4), respectively with null initial condition and with initial condition (2.10). Our approach will prove the existence of a solution in a (right) neighbourhood of .

One checks that, under appropriate integrability conditions on the function , , so that the Fractional Riccati equation can be rewritten equivalently in a fractional integral form as follows

| (2.12) |

with , and

| (2.13) |

with , . The consistency of such initial conditions follows in both cases from the fact that , for .

The starting strategy of our approach is to establish the existence of formal solutions to as fractional power series expansions and then prove by a propagation method of upper/lower bounds that the convergence radius of such series is non zero (and possibly finite). Indeed, this is strongly suggested by the elementary computation of the fractional derivative of a power function , :

| (2.14) |

Similarly

| (2.15) |

In particular, note that this last property justifies why a natural starting value for is of the form since its -derivative is and its -integral antiderivative is owing to the above formulas. On the other hand, the fractional derivative of a constant is not zero and reads:

| (2.16) |

Remark 2.4.

When , obviously coincides with the regular differentiation operator and the above Riccati equation is simply the regular Riccati equation with quadratic right-hand side, for which a closed form solution is available.

In the first part of this paper we will mostly distinguish two cases:

- •

-

•

the case and , which can be seen as a special case of the more general results presented in Abi Jaber et al. (2019),

and in a second part, we well investigate the more general case where , which requires more care.

The property (2.14) shows that the -fractional differentiation preserves the fractional monomials , . This property strongly suggests to solve the above equation as fractional power series, at least in the neighborhood of . Usually the fractional power series has a finite convergence radius but this does not mean that the solution does not exist outside the interval defined by this radius. This will lead us to design a hybrid numerical scheme to solve this equation.

3 Solving as a Power Series

As preliminary remarks before getting onto technicalities, note that:

-

•

if , then the solution to the equation is clearly by a uniqueness argument.

-

•

If , the Equation becomes linear and, as we will see on the way, the unique solution is expandable in a fractional power series with an infinite convergence radius.

As a consequence, henceforth we will work, except specific mention, under the following

Assumption 3.1.

We assume that .

3.1 The Algorithm

The starting idea is to proceed by verification: we search for a solution as a fractional power series:

| (3.17) |

where the coefficients , , are complex numbers. We will show that the coefficients are uniquely defined and we will establish that the convergence radius of is non-zero.

Assume that . First note that, for

with the Cauchy coefficients of the discrete time convolution given by

It follows from (2.14) that

On the other hand, from the Riccati equation we have

| (3.18) |

so that the sequence satisfies (by identification of the two expansions for ) the discrete time convolution equation:

| (3.19) |

Remark 3.2.

As a consequence of , note that the discrete convolution reads

| (3.20) |

3.2 The Convergence Radius

Let us recall that the convergence radius of the fractional power series (3.17) is given by Hadamard’s formula:

| (3.21) |

The fractional power series is absolutely converging for every and diverges outside . (We will not discuss the possible extension on the negative real line of the equation.) It may also be semi-convergent at if the are real numbers with an alternate sign and decreasing in absolute value.

The maximal solution of the equation may exist beyond this interval: we will see that this occurs for example when the parameters , , satisfy and . The typical example being the function solution to , defined on but only expandable (at ) on . This has to do with the existence of poles on the complex plane of the meromorphic extension of the expansion.

However, if the , , are all non-negative, one at least being non zero, then the domain of existence of the maximal solution is exactly . Its proof is postponed to Section B.

The theorem below, which is the first key result of this paper, provides explicit bounds for the convergence radius for the equation .

Theorem 3.3.

Let and let , , , . We denote by the function defined by (3.17) where the coefficients satisfy .

General lower bound of the radius We have

| (3.22) |

where .

Upper-bound for the radius If and (resp. and ), then

with . Moreover, is increasing (resp. decreasing) and so that the existence domain of is .

If and , then (with obvious notations) , , so that . Moreover if the sequence decreases for large enough, then the expansion of converges at .

If , then for every and the sequence , , is solution to the recursive equation

| (3.23) |

where the squared convolution is still defined by (3.20) (the equation is consistent since only involves terms , ).

Remark 3.4.

(a) The lower bound is not optimal since, if and , it is straightforward that

(b) In particular the theorem shows that, if , , there exist real constants , only depending on , such that

(c) When , and , the maximal solution of lives on the whole positive real line, even if its expansion only converges for .

(d) In Table 2 in Section 5.1 we will provide the values of the convergence domain in some realistic scenarios.

As already mentioned in the introduction, the domain of existence of the solution to may be strictly wider than that of the fractional power series. Hence, it is not possible to rely exclusively on this expansion of the solution to propose a fast numerical method for solving the equation. The aim is to take optimally advantage of this expansion to devise a hybrid numerical scheme which works to approximate the solution of the equation everywhere on its domain of existence.

3.3 Controlling the “Remainder” Term

In order to control the error induced by truncating the fractional series expansion (3.17) at any order , we need some errors bounds. In practice we do not know the exact value of the radius . However, we can rely on our theoretical lower bound given by the right-hand side of (3.22).

An alternative to this theoretical choice is to compute for large enough where satisfies . The value turns out to be a good approximation of , but may of course overestimate it, which suggests to consider with .

In both cases, in what follows we assume that .

In the proof of Theorem 3.3, see Section B, we will show by induction that the sequence satisfies

where or, equivalently, and is given by .

Case : The function is decreasing on the positive real line.

| (3.24) |

Note that for every since so that . Hence, we deduce that

Case . Note that the function is now only decreasing over so that (3.24) only holds for (which can be very large if is close to ). In practice this means that, to compute one should at least consider terms!

To get an upper-bound we perform an integration by part which shows that

where in the second line we used that since and . Plugging this in (3.24) with and yields the following formula which holds true for every ,

If is estimated empirically, the propagation property can be no longer used. Similar bounds, though less precise, can be obtained using that .

In practice, we will favor this second approach over the use of , as provides a too conservative lower estimate of .

4 Hybrid Numerical Scheme for ,

The idea now is to mix two approaches to solve the above fractional Riccati equations (2.11) on an interval , , supposed to be included in the domain on which is defined. We will focus on the first equation (with as initial value) for convenience.

The aim here is to describe a hybrid algorithm to compute the triplet

at a given time where is solution to (see Equation (2.11)). By hybrid we mean that we will mix (and merge) two methods, one based on the fractional power series expansion of and its two integrals and one based on a time discretization of the equation satisfied by and the integral operators.

On the top of that, we will introduce a Richardson-Romberg extrapolation method based on a conjecture on the existence of an expansion of the time discretization error. We refer to Talay and Tubaro (1990) and Pagès (2007) for a full explanation of the Richardson-Romberg extrapolation method and its multistep refinements.

As established in Section 3, the solution can be expanded as a (fractional) power series on , . Namely, for every

| (4.25) |

As a consequence, it is straightforward that

| (4.26) |

and, using (2.15), that

| (4.27) |

We will now proceed in four steps.

4.1 Step 1: radius of the power series expansion

A preliminary step consists in computing enough coefficients of the fractional power extension of , say , and estimating its convergence radius by

The radius is also that of the two other components of , so a more conservative approach in practice is to estimate using the larger coefficients , , coming out in (4.27), i.e. consider

This estimate of the radius is lower than what would be obtained with the sequence , which is in favor of a better accuracy of the scheme (see further on).

Then we decide the accuracy level we wish for the approximation of these series: let denote this level, typically or . If we consider some close to (or at least its estimate), we will need to compute too many terms of the series to achieve the prescribed accuracy, so we define a threshold and we decide that the above triplet will be computed by their series expansion only on . Then the prescribed accuracy is satisfied if the above fractional power series expansions are truncated into sums from up to with

provided . If , it suffices to invert the above formula where is replaced by to determine the resulting accuracy of the computation.

4.2 Step 2: hybrid expansion-Euler discretization scheme

We assume in what follows that to preserve the accuracy of the computations of the values of by the fractional power expansion.

Case . One computes the triplet by truncating the three fractional power extensions as explained above.

Case . This is the case where we need to introduce the hybrid feature of the method.

Phase I: Power series computation. We will use the power series expansion until and then an Euler scheme with memory (of course) of the equation in its integral form

First we consider a time step of the form where is an integer (usually a power of ). We denote by the Euler discretization scheme with step . Set

so that . Note that may be equal to .

Remark 4.1.

The values are not computed as an Euler scheme (in spite of the notations) but using the fractional power expansion (4.25) truncated at .

Phase II: Plain Euler discretization. Then, given the definition (2.5) of the fractional integral operator , one has, for every

so that the values of for are computed by induction for every by

| (4.28) |

where

To approximate the other two components and of , we proceed as follows:

-

•

For the regular antiderivative : we first decompose the integral into two parts by additivity of regular integral

The first integral is computed by integrating the fractional power series expansion (4.25)

while the second one is computed using a classical trapezoid method, namely

-

•

For the fractional antiderivative : first note that we could take advantage of the fact that leading to

so that, for every ,

This reduces the problem to the numerical computation of a standard integral, but with an integrand containing the square of the function .

However, numerical experiments (not reproduced here) showed that a direct approach is much faster, especially when the ratio is large. This led us to conclude that a standard Euler discretization of the integral would be more satisfactory. Consequently, we have

(4.29) where and , .

Remark 4.2.

The rate of convergence of the Euler scheme of the fractional Riccati equation with our quadratic right-hand side is not a consequence of standard theorems on ODEs, even in the regular setting , since the standard Lipschitz condition is not satisfied by the polynomial function .

4.3 Step 3: extrapolated Hybrid method

Let and

with an obvious (abuse of) notation. Numerical experiments – not yet confirmed by a theoretical analysis – strongly suggest (see the Example 4.5 below) that the first component of the vector , i.e. the solution to the Riccati equation itself, satisfies

| (4.30) |

Taking advantage of this error expansion (4.30), one considers, for even, the approximator – known as Richardson-Romberg (RR) extrapolation – defined by

which satisfies

We analogously perform the same extrapolation with the two other components and of and we may reasonably guess that

Note that if , then , which dramatically reduces the complexity and makes the scheme rate of decay (inverse-)linear in the complexity.

4.4 Step 4: multistep extrapolated Hybrid method

Here we make the additional assumption that the following second-order expansion holds on the triplet

We define the weights by (for a reference on this multistep extrapolation we may cite Pagès (2007))

and taking as a multiple of and set

So, we define the multistep extrapolation

| (4.31) |

An easy computation shows that satisfies

4.5 Example

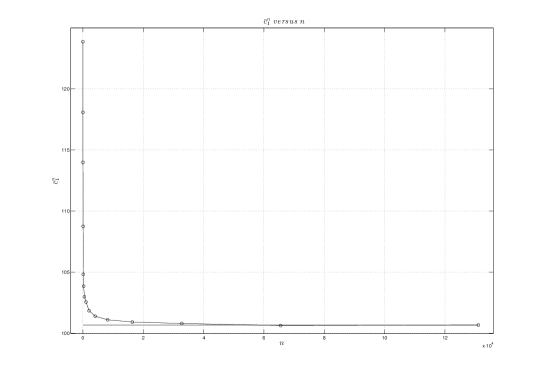

Testing the convergence rate. Here we test on an example whether our guess on the rate of convergence is true. We take the fractional Riccati equation (2.11) with ( Hurst coefficient ), with null initial condition and (real valued) parameters (these parameters are in line with the one in Section 5, which were calibrated in El Euch and Rosenbaum (2019) using a real data set; here we humped the parameter in order to gain convexity in the quadratic term of the Riccati, which is more challenging from the numerical point of view. )

We focus on short maturities, supposed to be numerically more demanding, and we set (corresponding to one trading day). Numerically speaking, one may proceed as follows (with the notations introduced for the Richardson-Romberg extrapolation): if the rate (4.30) is true, it becomes clear that the sequence

| (4.32) |

converges to as .

In Table 1 we display the values of the constant coefficient appearing in (4.30) for different values of ranging in .

| [8–16] | 123.8478 | [256–512] | 103.8532 | [8 192–16 384] | 101.1105 |

|---|---|---|---|---|---|

| [16–32] | 118.0696 | [512–1 024] | 102.9883 | [ 16 384–32 768] | 100.9268 |

| [32–64] | 113.9827 | [1 024–2 048] | 102.5672 | [32 768–65 536 ] | 100.8097 |

| [64–128] | 108.7523 | [2 048–4 096] | 101.8524 | [65 536–131 072 ] | 100.6396 |

| [128–256] | 104.8304 | [4 096–8 192] | 101.3989 | [131 072–262144 ] | 100.5652 |

We take in Formula (4.30) as a reference value, obtained with an accuracy level and .

|

|

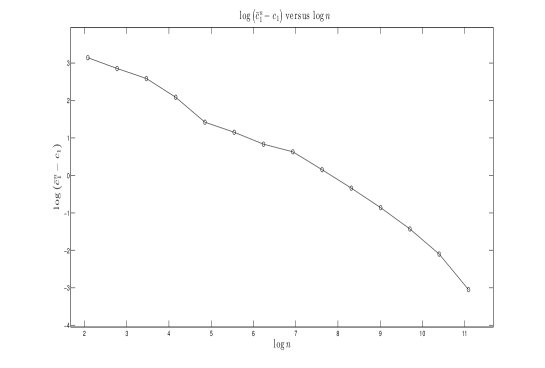

Figure 1 (left hand side) strongly supports the existence of a first order expansion, whereas Figure 1 (right hand side) is quite consistent with the existence of a second order expansion. Unfortunately, Figure 1 (right hand side) suggests that the higher order expansion does exist but rather of the form

where seems to depend on the value of the parameters , and . When we consider the regression coefficient in the - plot of versus , we find a slope of . Hence, we do not find an expansion of the form , since which suggests a second term . The numerical test seems to suggest that the exponent of this second term of the expansion varies as increases. In order to avoid the calibration of this additional parameter, we set , which numerically yields by far the most stable and accurate results (see also Section 5). Hence, in all our numerical tests we use the “regular” extrapolation formula of order three (4.31).

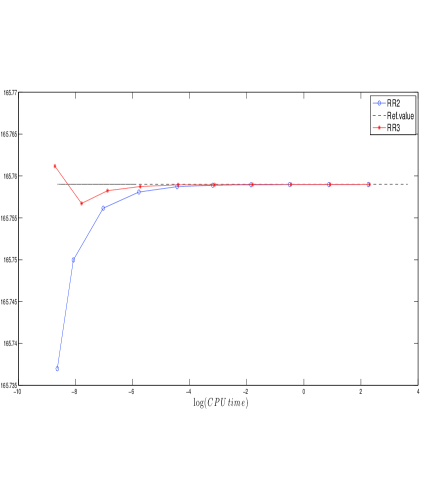

Testing the efficiency of the Richardson-Romberg meta-schemes. Let us now turn our attention to the convergence of the hybrid scheme. To evaluate its efficiency we proceed as follows: we artificially introduce the hybrid scheme by setting

which differs from the original by the factor. As a consequence, the series expansion is only used approximately between and and the time discretization scheme is used between and . This artificial switch is applied to each of the three scales , and of the extrapolated meta-scheme implemented.

As a benchmark for the triplet we use the value obtained via the fractional power series expansion with , namely

In the numerical test reproduced in Figure 2 below, the convergence of both the and the “regular” (namely, associated to error expansion in the scale , ) Richardson-Romberg meta-schemes (which were introduced, respectively, in Sections 4.3 and 4.4) is tested, by plotting and as functions of and of the computational time.

Although we could not exhibit through numerical experiments the existence of a third order expansion of the error at rate – corresponding to – as mentioned above, it turns out that the weights resulting from this value of , i.e. the “regular” extrapolation formula (4.31) in the third order Richardson-Romberg extrapolation (RR3) yields by far the most stable and accurate results (see also Section 5).

|

|

Remark 4.3.

When , the computation is performed exclusively via the series expansion and is extremely faster than that involving the meta-schemes.

We end this subsection by highlighting that in all numerical experiments that follow we will adopt, in our hybrid algorithm, the “regular” third order extrapolation meta-scheme (4.31).

We provide in the short section that follows further technical specifications of the hybrid scheme.

4.6 Practitioner’s Corner

-

Complexity reduction. To significantly reduce the complexity of the computations, one may note that if is solution to then is solution to . Solving directly allows to cancel all multiplications by throughout the numerical scheme, at the price of a unique division by at the end.

-

Calibration of . Numerical experiments carried out with (one trading day) suggest that, at least for small values of , the optimal threshold is a function of the time discretization step . The coarser is, the lower should be to minimize the execution time. It seems that for , whereas for , . This leads us to set, when ,

5 Numerical performance in the rough Heston model

In this section we test the performance of our results in solving the homogeneous fractional Riccati equation in (2.11) that we recall for the reader’s convenience:

We apply our methodology to the fractional Riccati equation arising in the Rough Heston pricing model considered in El Euch and Rosenbaum (2019).

We test the series approximation and the hybrid procedure we introduced in two steps: first we consider the power series approximation to the Riccati solution, which reveals to be extremely fast. Then we consider the hybrid method, i.e., the series combined with the Richardson-Romberg extrapolation method, in order to allow for horizons beyond the convergence radius of the power series representation. Remarkably, we find that also the hybrid method is very fast and stable when compared with the only competitor in the literature, represented by the Adams method. All the test have been obtained in C++ using a standard laptop endowed with a 3.4GHz processor.

5.1 Testing the Fractional Power Series Approximation

Let us consider the fractional power series expansion representation (3.17) .

We would like to use the calibrated parameters in El Euch and Rosenbaum (2019), namely we would like to work in the following setting (for clarity, we add a subscript in the parameters below)

| (5.33) |

where are positive real numbers. We take the following values

| (5.34) |

where denotes the correlation between the two Brownian motions and .

The fractional Riccati equation to be solved in the setting of El Euch and Rosenbaum (2019) is:

| (5.35) |

so that the correspondence for the fractional Riccati coefficients is as follows:

Of course, the parameters for the fractional Riccati will depend on the frequency of the Fourier-Laplace transform. To provide more insight into the convergence domain of the series solution studied in Section 3.2, we show in Table 2 the value introduced in Equation (3.22) for the specified parameters and for different values of (recall that this bound is conservative, in that it is not optimal).

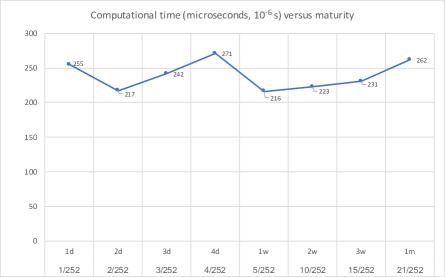

In order to give an idea of the computational time required by the fractional power series solution, we set (in the pricing procedure we will consider several values for , as we shall integrate over this parameter in order to compute the inverse Fourier transform) and we fix the dampening factor , in line with the Fourier approach of Carr and Madan (1999). Finally, we focus on short term maturities (namely month), in order to test the pure series expansion.

In Figure 3 we plot the computational time required to obtain the solution when . We stress the fact that this time is expressed in microseconds, i.e., in seconds. The corresponding convergence radius is equal to , which is beyond . Namely, with the notation of Section 4, and so is approximated via the fractional power series (4.25) truncated into sums from to . Figure 3 confirms that the power series representation is extremely fast and the computational time is basically constant with respect to small maturities .

5.2 The Hybrid Algorithm at Work

We now test the performance of our hybrid method presented in Section 4 when applied to the option pricing problem. We consider a book of European Call options on , in a Heston-like stochastic volatility framework, where the volatility exhibits a rough behaviour (the so-called fractional Heston model) as in El Euch and Rosenbaum (2019), with maturities ranging from day till years and strikes in the interval in the moneyness. The model parameters are those specified in Section 5.1, i.e., the same parameters calibrated by El Euch and Rosenbaum (2019). In order to obtain the prices we use the Carr-Madan inversion technique, namely the one presented in (Carr and Madan, 1999, Section 3), with dampening factor . In the numerical inversion of the Fourier transform in Equation (2.2), we integrate with respect to the real part of the frequency parameter . Here, we consider varying as follows (the choice of turns out to be a good tradeoff between the stability of the results and the computational time)

That is, we compute times a Fourier transform. Notice that, in general, the maturities of the options can go beyond the convergence radius of the power series representation. In other words, when computing the triplet

one can be forced to switch to the hybrid method in order to get the solution of the fractional Riccati, since . In this case, we set (recall Section 4, Step 2, Phase I), which turns out to be a value leading to stable results, in the sense that for larger values of the prices do not change.

| day | week | month | months | year | years | ||

|---|---|---|---|---|---|---|---|

| Strike | price(CT) | price(CT) | price(CT) | price(CT) | price(CT) | price(CT) | |

| Hybrid | |||||||

| Adams | |||||||

| Hybrid | |||||||

| Adams | |||||||

| Hybrid | |||||||

| Adams | |||||||

| Hybrid | |||||||

| Adams | |||||||

| Hybrid | |||||||

| Adams | |||||||

| Hybrid | E-05 | ||||||

| Adams | E-04 | ||||||

| Hybrid | E-05 | E-05 | |||||

| Adams | E-03 | E-05 | |||||

| Hybrid | E-05 | E-09 | |||||

| Adams | E-03 | E-07 | |||||

| Hybrid | E-05 | E-13 | E-04 | ||||

| Adams | E-03 | E-7 | E-04 |

In Table 3 we display the prices together with the computational times (in milliseconds) obtained by our hybrid method for the entire book of options. A quick look at the Table 3 shows that our method is extremely fast. In fact, all prices are computed in less than one second. Moreover, one can easily verify that using a larger value for (which here is set to ) does not change the prices. Therefore, our hybrid method is also very stable and can be used as the benchmark.

Now we compare the performance of our hybrid algorithm with the (only) other competitor present in the literature, namely the fractional Adams method, a numerical discretization procedure described e.g. in El Euch and Rosenbaum (2019) (see their Section 5.1). As for any discretization algorithm, also for the Adams method one should select the discretization step, and according to this choice the corresponding price can be different. Of course, the smaller the time step in the discretization procedure, the longer will take the pricing procedure. As we consider our hybrid method as the benchmark, now we look for the discretization step for the Adams method that leads to prices that are close enough to ours, according to a given tolerance. Here, the error is measured in terms of the difference of the corresponding implied volatilities associated to the prices generated by the two methods. We fix for example a maximal difference of . Notice that this maximal error is very large, as for the calibration of the classic Heston model one can typically reach an average for the RESNORM (sum of the squares of the differences) around E-05.

First of all, let us focus our attention on the very short term maturities in Table 3, namely 1 day and 1 week. It turns out that, apart from a couple of situations for 1 week, the Adams method is also very fast. However, we notice that Adams prices can lead to some arbitrage opportunities. In fact, for example, for the maturity of 1 day and strike , Adams method leads to a price smaller than the intrinsic value of the Call (recall that the interest rate here is set to be zero). We put in the table when this situation occurs. Also, one can check that in many cases it is not possible to find the discretization step for the Adams method in order to generate a price within the tolerance. We put for the cases where the error is greater than the tolerance, regardless the choice of the discretization step (we pushed the discretization till 150 steps without observing any relevant change). The reason for this phenomenon is quite intuitive: if the maturity is very short, adding discretization steps in the procedure does not necessarily produce different prices because the process has not enough time to move. On the other hand, our hybrid method takes benefit of the fractional power series expansion that works extremely well mostly for very short maturities. In conclusion, our method is very fast, stable and accurate in the short maturities when compared to the Adams method.

Now let us consider the other maturities till 2 years. Here, in order to get prices close to our benchmark, we are forced to choose an ad hoc discretization grid for the Adams method, including a number of steps ranging from 10 to 150, depending on the particular maturity and strike. As a consequence, the corresponding computational time turns out to be much higher than ours, to the point that for 2 years the computation of prices for the Adams method require about 4 minutes with 150 discretization steps, while our hybrid algorithm still takes less than one second. In conclusion, we can state that our hybrid algorithm dominates the Adams method for all maturities.

We end this subsection by reproducing the analogue of Figure 5.2 in El Euch and Rosenbaum (2019), namely the term structure of the at-the-money skew, that is the derivative of the implied volatility with respect to the log-strike for at-the-money Calls.

Figure 4 confirms the results in El Euch and Rosenbaum (2019): in particular, for the Rough Heston model we see that the skew explodes for short maturities, while it remains quite flat for the classic Heston model, which is well known to be unable to reproduce the slope of the skew for short-maturity options.

6 The Non-Homogeneous Fractional Riccati Equation

In this section, we consider the more general case where the fractional Riccati equation has a non zero starting point. The fractional Riccati ODE arising in finance and associated to the characteristic function of the log-asset price is very special insofar it starts from zero. Recently, Abi Jaber et al. (2019) extended the results of El Euch and Rosenbaum (2019) to the case where the volatility is a Volterra process, which includes the (classic and) fractional Heston model for some particular choice of the kernel. Such extension leads to a fractional Riccati ODE but with a general (non-zero) initial condition. This case is mathematically more challenging and requires additional care. Nevertheless, in this section we prove that it is still possible to provide bounds for the convergence domain of the corresponding power series expansion, at the additional cost of extending the implementation of the algorithm to a doubly indexed series, in the spirit of Guennon et al. (2018).

For the reader’s convenience, first of all we recall the general Riccati equation (see (2.11))

where , , and , are complex numbers. Our aim is to find a solution as a fractional power series as we did in Section 3 in the case , and , . This leads us to deal with the integral form (2.13) of this equation. However, the solution will be in this more general setting a doubly index series based on the fractional monomial functions . Of course, we will again take advantage of the fact that for every and every ,

We now state the result of this section, which represents the main mathematical contribution of the paper.

Theorem 6.1.

Equation admits a solution expandable on a non-trivial interval , , as follows

| (6.36) |

where the coefficients and, for every , denotes the valuation of . Moreover, the above doubly indexed series is normally convergent on any compact interval of .

Case : we have if , , if and for if . In particular, one always has .

The coefficients are recursively defined as follows: , , and, for every and every ,

| (6.37) |

where

| (6.38) |

Note that , , and , .

The constructive proof of this result is divided into several steps and is provided in full details in Appendix C. A full numerical illustration of the general case is beyond the scope of our paper. Here, we just mention that the computation of the solution through the doubly index fractional power series representation turns out to be still extremely fast as in the previous single-index case. In practice very few -layers are needed to compute for a standard accuracy, say or . Also, a hybrid algorithm based on Richardson-Romberg extrapolation can also be devised in order to allow for maturities longer than the convergence radius of the above double index series. We skip the details for sake of brevity.

7 Conclusion

In this paper, motivated by recent advances in Mathematical Finance, we solved a family of fractional Riccati differential equations, with constant (and possibly complex) coefficients, whose solution is the main ingredient of the characteristic function of the log-spot price in the fractional Heston stochastic volatility model. We first considered the case of a zero initial condition and we then analyzed the case of a general starting value, which is closely related to the theory of affine Volterra processes.

The solution to the fractional Riccati equation with null initial condition takes the form of power series, whose coefficients satisfy a convolution equation. We showed that this solution has a positive convergence domain, which is typically finite. In order to allow for maturities that are longer than the convergence domain of the fractional power series representation, we provide a hybrid algorithm based on a Richardson-Romberg extrapolation method that reveals to be very powerful. Our theoretical results naturally suggest an efficient numerical procedure to price vanilla options in the Rough Heston model that is quite encouraging in terms of computational performance, when compared with the usual benchmark, represented by the Adams method.

In the case of a non-null initial condition, the solution takes the form of a double indexed series and, working with additional technical care, we provided error bounds for its convergence domain.

In the last years, Deep Neural Networks(DNN)-based algorithms have been massively adopted in finance in order to solve long-standing problems like robust calibration and hedging of large portfolios, see e.g. Stone (2019), Horvath et al. (2019), Bayer and Stemper (2019) and references therein. Thanks to their flexibility and extremely fast execution time, DNN represent nowadays the standard in the banking industry. However, any deep neural network requires a learning phase, which typically takes a lot of time and needs the pricing technology to feed the network. Our methodology, in view of pricing, is useful in order to speed up the learning phase. In this sense, our results should not be seen in competition with DNN since, on the contrary, they are a useful and efficient ingredient to feed the DNN with. So our work is a prerequisite for any DNN based algorithm.

Appendix A Toolbox: Riemann Sums, Convexity and Kershaw’s Inequalities

A.1 Riemann sums, convexity

We will extensively need the following elementary lemma on Riemann sums.

Lemma A.1.

Let be a function, non increasing on and symmetric, i.e. such that , hence convex. Assume that . Then, and:

| (A.39) |

In particular, it follows that, for every ,

so that

| (A.40) |

Proof.

The lower bound is a straightforward consequence of the convexity of the function since for every ,

with equality if and only if . Let us consider now the upper bounds.

Case even. We consider separately the half sums from to and from to .

For , for , while for , for . Therefore

On the other hand, for the second half sum, if , for , while for , for .

Therefore

Summing up both sums yields “even part” of (A.39).

Case odd. One shows likewise that

for the first half sum, while

for the second one. Summing up gives the“odd part” of (A.39). ∎

A.2 Kershaw inequalities

We also rely on these inequalities (see Kershaw (1983)) controlling “ratios of close terms” of the Gamma function. For , and every ,

| (A.41) |

For this double inequality becomes an equality.

Appendix B Proof of Theorem 3.3

B.1 Proof when

B.1.1 Lower Bound for the Radius by Upper-Bound Propagation (Claim )

We first want to prove by induction the following upper-bound of the coefficients , namely

| (B.42) |

for some and (note that ). We assume the (with : this condition will be double-checked later) and we want to propagate this inequality by induction. Assume that (B.42) holds for some . Plugging this bound in (3.19) yields

| (B.43) |

As (see (3.20)), we have

| (B.44) |

where denotes the Beta function (note that ).

From the Kershaw inequality (B.45), we obtain in particular that, for every and every ,

| (B.45) |

Now set and . We get

since . Plugging successively this inequality and (B.44) into (B.43) yields for every ,

| (B.46) |

Keeping in mind that we want to get , we rearrange the terms as follows

| (B.47) |

where we used that and we recall the notation .

Finally, the propagation of Inequality (B.42) is satisfied for every by any couple satisfying

It is clear that that, the lower is, the higher our lower bound for the convergence radius of the series will be. Consequently, we need to saturate both inequalities which leads to the system

or, equivalently, using both identities and ,

The positive solution of the above quadratic equation in is given by

| (B.48) |

Consequently, setting , we finally find that

| (B.49) |

so that the convergence radius of the function satisfies

A slight improvement of the theoretical lower bound is possible by imposing the constraints and and using that when in (B.47).

B.1.2 Upper-Bound for the Radius via Lower Bound Propagation, , , , (Claims , , )

In this subsection, we assume that the parameters , , are real numbers. We will prove a comparison result between the case and .

The case of can be reduced to the case owing to the next Section B.1: we will see that the triplets () and lead to solutions as fractional power series having the same convergence radius.

Proposition B.1.

Let . Let and be solutions to and respectively, where are real numbers.

For every , and . Moreover, the sequence defined for every by is solution of the recursive equation

| (B.50) |

where the squared convolution is still defined by (3.20) (the equation is consistent since only involves terms , ).

Assume and , , . Then for every , , so that .

Assume . If and , then (with obvious notations) , so that . Moreover if the non-negative sequence decreases for large enough , then the expansion of converges at .

Note that claim is that of Theorem 3.3 and claim is claim .

Proof. We proceed again by induction on . If , and . Assume , , then

It is clear that either or is even. Consequently, so that and

Let us look first at the convolution at an odd even index. As for even index , one has

Plugging this in at index yields (B.50).

Notice that, by induction, for every if , , (in particular as well).

We proceed by induction on . It holds as an equality for : . Assume , . Then, using (3.20),

so that, using that ,

Let . It is clear that

(also obvious by setting and replacing by in former computations). Consequently, and

so that is solution to . In particular, if we set formally

then

so that both expansions of and have the same convergence radius . See also the comments further on.

Remark B.2.

Note that when the coefficients so that . As a consequence, the definition domain of the solution of the Riccati equation on the positive real line is .

By contrast, the series with terms is most likely alternate ( the absolute value of the generic term decreases toward for large enough). This implies that the series will still converge at i.e.

This explains the highly unstable numerical behavior observed near the explosion time compared to the case where all , but also that the solution of the Riccati equation may be defined beyond , as already mentioned in the introduction.

Now, we are in position to prove claim (lower bound of the radius). In the same manner as we proceed for upper bound, we aim this time at propagating a lower bound for the non-zero subsequence of i.e. the sequence , namely

Keeping in mind that the function is convex since ,

Using Kershaw’s Inequality with and

Plugging the above two lower bounds for and into (B.50) yields

where

Consequently the propagation holds if

If we saturate the left inequality by setting , then the right condition boils down to One checks that which yields

Now,

which finally leads to the announced upper-bound

Remark. From the upper-bound result, we know that

In particular we have established that, if , , there exist real constants , only depending on , such that

with and .

B.2 Proof when

B.2.1 Upper-Bound of the Radius by Lower Bound Propagation (Claim )

We start from the same the equation (see (3.19)). If , then we may write

By Kershaw’s Inequality we have, by setting and ,

so that

since . Now, using the concavity of the function over since , we derive by Jensen’s Inequality that

Consequently, assuming that for every , we derive that

where we used that and . Hence, the propagation of the upper-bound holds if and only if

Following the lines of the case , we derive that propagation does hold when

| (B.51) |

so that the convergence radius of satisfies

Remark. It is the same formula as (B.48) except for the term which replaces since . This is due to the inversion of the convexity of the function when switches from to .

B.2.2 Upper Bound of the Radius by Lower Bound Propagation (Claim )

As a preliminary task, we note that the function defined on is strictly concave when , is symmetric with respect to and attains its maximum at . Hence, satisfies the assumptions of Lemma A.1, so that

which finally yields, after easy manipulations, that, for every ,

| (B.52) |

Notice that the positivity of simply follows from the strict concavity of .

We assume that , , and that, for , for some real constant .

As in the case , we will focus on the sequence since Lemma B.1 still applies.

As for the factor , we may proceed as follows, still using Kershaw’s Inequality, this time with and :

with

One checks that this sequence decreases toward , so that . Following the lines of the case yields

whereas . Hence, the propagation of the lower bound is satisfied if

Finally, the lowest solution to this system is corresponding to .

Appendix C Proof of Theorem 6.1

We now focus on the two separate cases on the next two subsections.

C.1 Proof of Theorem 6.1 (Case )

Step 1 Induction formula and propagation principle. Let be formally defined by (C.2) and let be the valuation of the sequences .

The induction equation (6.37) is obvious by identification. Note that satisfies the recursion (3.19) of the case , so that if and otherwise. The main point is to determine the valuation when .

We start with the fact that (corresponding to the expansion when ) and due to the presence of the fractional monomial .

Let . A term comes in (C.2) for the -fractional integration of a term , which itself comes either directly, either from the expansion at the same level of or from a product with and induced by the convolution term. Hence, and, for every ,

It is clear that this minimum cannot be attained at or , since it leads to a non-sense. Then we can check that the formula

is solution to the above minimization problem. Finally, , . This justifies the definition of (C.2) and the double index discrete convolution (6.37).

To show the existence of a positive convergence radius shared by all the fractional series at all the levels, we will prove that he coefficients satisfy the following upper bound for every level and every :

| (C.53) |

(with ). The method of proof consists in propagating this bound by a nested induction on the index and through the levels .

Step 2 Propagation of the initial value across the levels . Following (C.53), we want to propagate by induction the bound

| (C.54) |

keeping in mind that , and . The levels yield direct conditions to be used later. Let .

Applying the induction formula (6.37) with , we obtain

First note that since and . Moreover,

so that we get the following induction formula for the starting values , :

Let . Assume that (C.54) is satisfied by for every lower level . Then

It follows from Kershaw’s Inequality (B.45), applied with and , and the elementary identity that

Hence

| (C.55) |

since one easily checks (e.g. with the use of Mathematica) that the maximum is achieved at . The condition on and for propagation hence reads

| (C.56) |

where the first two inequalities come from the initial values at levels and the third one ensures the propagation of the upper-bound in (C.55). These three inequalities are in particular satisfied if

where

| (C.57) |

so that

| (C.58) |

Step 3 Propagation through a level . Let . Assume that the above bound holds for every couple such that level and or and .

owing (twice) to Lemma A.1 since . Now, as by defintion of the valuation, we deduce that

so that

If , so that the above right inequality still holds by replacing by . Now, combining these inequalities yields

As for the ratio of Gamma functions, one has, using and Kershaw’s inequality (B.45),

For every and ,

Now, we note that

Combining the above inequality with this identity and the elementary inequality between non-negative real numbers

| (C.59) |

we obtain (once noted that )

Now, still using that ,

However, if , this bound is infinite. Coming back to the original ratio yields, for every ,

Finally, collecting the above ienqualities, we obtained that, for every and every ,

with .

Consequently, propagation inside a level boils down to

| (C.60) |

We combine now this constraint on with those on and coming the propagation across initial values, that is (C.58) i.e. , where is given by (C.57) and (C.58). The constraint (C.60) reads

| (C.61) |

where

| (C.62) |

Then all the constraints are fulfilled by parameters satisfying

where is given by (C.58) and

is the positive solution of the equation associated to Inequation (C.61). In what follows we consider the admissible pair . We derive that the convergence radii of the functions all satisfy

Now we have to ensure the summability of the functions . It suffices to consider the levels , so that . Let , where . Elementary computations using the upper bound (C.53) for the coefficients and a change of index show that

where does not depend neither on nor on and is uniformly bounded on any compact interval of .

To ensure the summability of the functions for every , we note that

Since as , it is clear that so there exists such that . Hence

owing to the continuity of . As is non-increasing in , yields the highest admissible value for so that

in the sense that the doubly indexed series (C.2) that defines the function is normally converging on any compact interval of .

The following proposition establishes a semi-closed form for the starting values at each level .

Proposition C.1 (Closed form for the starting values).

For every ,

with and for ,

| (C.63) |

Proof.

We prove the identity by induction: for it is obvious. Assume now it holds for . Then

since (keep in mind that ). Now, we rely on (6.38). First note that , if both . Hence implies and consequently , . If , so that which implies . As is always by construction, we finally obtain

Therefore

where is given by (C.63) (at level ). The conclusion follows by induction. ∎

C.2 Proof of Claim of Theorem 6.1 (Case )

We still search for a function of the form (C.2), more precisely

where the valuation is specified in the Lemma below. We set for convenience for .

Lemma C.2.

Valuation. When , then satisfies

If , or , as defined above is still admissible as a lower bound in the above sum.

Induction formula. The coefficients still satisfy the doubly indexed recursion (6.37), this time with , , and , . Note that for every .

Closed form for the starting values. For every ,

| (C.64) | ||||

| (C.65) |

Remark C.3 (Case ).

When , one checks that , and, then, by induction, that for every . As a second step, one shows by induction that, actually, for every level , , so that, like in the former case, the solution appears in the much simpler form

Proof. The fact that for is obvious. For , it is clear by adapting the analogous proof in Step 1 of the former case that is solution to the same recursive optimization problem

| (C.66) |

with the former initial values (keeping in mind that ). This time the only admissible solution is .

This is straightforward.

We proceed by induction. First of all, it follows from Equation (6.37) that

| (C.67) |

which agrees with the Formula (C.64). Assume now the formula valid for and let us check for . One checks by inspecting successively the cases , and that

whereas . Likewise

which agrees with (C.65). Therefore we get

which also agrees with Formula (C.64). One proceeds likewise for .

Now we are in position to prove Theorem 6.1. Our aim in this proof is to propagate an upper-bound of the form

| (C.68) |

Step 1 Propagation for the initial value across the levels . On checks by inspecting successively the cases , and that

whereas . Consequently, it follows from (6.38) and the fact that , that, for every ,

By Kershaw’s Inequality (B.45) used with and , we deduce that

since . We assume now that (C.68) is satisfied at levels , in particular for , . Then

One checks that, for every , and . Consequently, if we set

we obtain

Consequently, keeping in mind that , the propagation condition on the initial values reads

or, equivalently,

| (C.69) |

Step 2 Propagation across the levels . We assume that the bound to be propagated holds for every couple such that level and or and .

We first focus on the discrete time convolution. Let

where we used Lemma A.1 in the penultimate line and (see (C.66)). Now note that, if ,

owing to Lemma A.1. If , the above inequality still holds since . Now, combining these inequalities yields

| (C.70) |

where is defined in (C.62).

First note, by inspecting the four cases and , that

Now, using and Kershaw’s Inequality (B.45) with and , we obtain

| (C.71) |

As for every , we deduce that

Now note that

and that

Hence, using (C.59), we deduce

Finally, one notes that to deduce

where

Plugging Inequalities (C.70), (C.71) and the estimate for into (6.37) yields

where we used that . We deduce that the propagation of the bound holds as soon as

| (C.72) |

Step 3 Synthesis. If we saturate the left-hand side of inequality (C.69) and plug it in (C.72), we obtain the inequality

The minimal solution is given by

where is given by the right-hand side of inequality (C.69) and

Now, we focus on the convergence of the series (keeping in mind that the first three levels have no influence on the result) so that we may use that , . Set and . One checks that for every ,

where is normally convergent on every compact interval of the open interval . Then, for every ,

Hence, the series is absolutely convergent if .

As , one shows that the function satisfies so that we may set

Finally, one checks that the doubly indexed series is normally convergent on .

Acknowledgments.

We thank Omar El Euch and Mathieu Rosenbaum for useful discussions on the first part of the paper. We are also grateful to Elia Smaniotto and Giulio Pegorer for valuable comments.

References

- Abi Jaber et al. (2019) Abi Jaber, E., Larsson, M., and Pulido, S. (2019). Affine volterra processes. Annals of Applied Probability, 29(5):3155–3200.

- Alòs et al. (2020) Alòs, E., Gatheral, J., and Radoicic, R. (2020). Exponentiation of conditional expectations under stochastic volatility. Quantitative Finance, 20(1):13–27.

- Bayer and Stemper (2019) Bayer, C. and Stemper, B. (2019). Deep calibration of rough stochastic volatility models. Preprint, ArXiV https://arxiv.org/abs/1810.03399.

- Carr and Madan (1999) Carr, P. and Madan, D. B. (1999). Option Valuation Using the Fast Fourier Transform. Journal of Computational Finance, 2(4):61–73.

- Comte and Renault (1998) Comte, F. and Renault, E. (1998). Long memory in continuous-time stochastic volatility models. Mathematical Finance, 8(4):291–323.

- Diethelm et al. (2002) Diethelm, N., Ford, J., and Freed, A. (2002). A predictor-corrector approach for the numerical solution of fractional differential equations. Nonlinear Dynamics, 29(1–4):3–22.

- Diethelm et al. (2004) Diethelm, N., Ford, J., and Freed, A. (2004). Detailed error analysis for a fractional Adams method. Numerical Algorithms, 36(1):31–52.

- El Euch and Rosenbaum (2019) El Euch, O. and Rosenbaum, M. (2019). The characteristic function of rough Heston models. Mathematical Finance, 29(1):3–38.

- Gatheral et al. (2018) Gatheral, J., Jaisson, T., and Rosenbaum, M. (2018). Volatility is rough. Quantitative Finance, 18(6):933–949.

- Gatheral and Radoicic (2019) Gatheral, J. and Radoicic, R. (2019). Rational approximation of the rough Heston solution. International Journal of Theoretical and Applied Finance, 22(3):13–27.

- Gerhold et al. (2019) Gerhold, S., Gerstenecker, C., and Pinter, A. (2019). Moment explosions in the rough Heston model. Decisions in Economics and Finance, 42(2):575–608.

- Guennon et al. (2018) Guennon, H., Jaquier, A., Roome, P., and Shi, F. (2018). Asymptotic behaviour of the fractional Heston model. SIAM Journal on Financial Mathematics, 9(3):1017–1045.

- Heston (1993) Heston, S. L. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud., 6:327–343.

- Horvath et al. (2019) Horvath, B., Muguruza, A., and Tomas, M. (2019). Deep learning volatility. preprint, ArXiV https://arxiv.org/abs/1901.09647.

- Hull and White (1987) Hull, J. and White, A. (1987). The pricing of options on assets with stochastic volatilities. Journal of Finance, 3:281–300.

- Jaisson and Rosenbaum (2016) Jaisson, T. and Rosenbaum, M. (2016). Rough fractional diffusions as scaling limits of nearly unstable heavy tailed Hawkes processes. The Annals of Applied Probability, 26(5):2860–2882.

- Kershaw (1983) Kershaw, D. (1983). Some extensions of W. Gautschi’s inequalities for the Gamma function. Math. Comp., 41(164):607–611.

- Pagès (2007) Pagès, G. (2007). Multi-step Richardson-Romberg extrapolation: remarks on variance control and complexity. Monte Carlo Methods Appl., 13(1):37–70.

- Samko et al. (1993) Samko, S., Kilbas, A., and Marichev, O. (1993). Fractional integrals and derivatives. Theory and Applications, Gordon and Breach, Yverdon.

- Stone (2019) Stone, H. (2019). Calibrating rough volatility models: a convolutional neural network approach. Quantitative Finance, to appear.

- Talay and Tubaro (1990) Talay, D. and Tubaro, L. (1990). Expansion of the global error for numerical schemes solving stochastic differential equations. Stoch. Anal. and App., 8:94–120.