Ruin probabilities for risk processes

in a bipartite network

Abstract

This paper studies risk balancing features in an insurance market by evaluating ruin probabilities for single and multiple components of a multivariate compound Poisson risk process. The dependence of the components of the process is induced by a random bipartite network. In analogy with the non-network scenario, a network ruin parameter is introduced. This random parameter, which depends on the bipartite network, is crucial for the ruin probabilities. Under certain conditions on the network and for light-tailed claim size distributions we obtain Lundberg bounds and, for exponential claim size distributions, exact results for the ruin probabilities. For large sparse networks, the network ruin parameter is approximated by a function of independent Poisson variables.

AMS 2010 Subject Classifications: primary: 60G51, 91B30; secondary: 94C15.

Keywords: bipartite network, Cramér-Lundberg model, exponential claim size distribution, hitting probability, multivariate compound Poisson process, ruin theory, Poisson approximation, Pollaczek-Khintchine formula, risk balancing network.

1 Introduction

Consider an insurance risk process in the celebrated Cramér-Lundberg model with Poisson claim arrivals, premium rate and claim sizes , that is, a spectrally positive compound Poisson process given by

where , is a constant, , , are i.i.d. random variables with distribution and finite mean , and is a Poisson process with intensity . For such a process, the ruin probability for a given risk reserve is denoted by and it is given by the famous Pollaczek-Khintchine formula (cf. [1, VIII (5.5)], [2, IV (2.2)] or [10, Eq. (1.10)])

| (1.1) |

whenever the ruin parameter satisfies . Hereby, for every distribution function with , for , we denote the corresponding tail by , the integrated tail distribution function by if the mean is finite, and the -fold convolution by , where and , .

We also recall that, whenever , then for all . Note that the function of the Pollaczek-Khintchine formula (1.1) is a compound geometric distribution tail with parameter . Thus the smaller , the smaller the ruin probability, and for the ruin probability tends to as . More precisely, it is well known that, when the distribution function is light-tailed in the sense that an adjustment coefficient exists; i.e.,

| (1.2) |

then the ruin probability satisfies the famous Cramér-Lundberg inequality (cf. [1, Eq. XIII (5.2)], [2, Eq. I.(4.7)] or [10, Eq. (1.14)])

| (1.3) |

It is easy to see that is a necessary condition for the existence of an adjustment coefficient. Further, if the are exponentially distributed with mean , then and

| (1.4) |

In this paper we derive multivariate analogues to the above classic results in a network setting. More precisely we consider a multivariate compound Poisson process whose dependency structure stems from a random bipartite network which is described in detail in Section 2 below. We investigate the influence to the insurance market of sharing exogeneous losses modelled by the network. Insurance companies or business lines of one insurance company are the agents in the bipartite network of Figure 1, and the portfolio losses, which are the objects, are shared either by different companies or assigned to different business lines within a company. This can also yield useful scenarios for the risk assessment of risk regulators or scenarios of the competitors of a company, when the underlying selection strategy of the agents is unknown.

Our results assess the effect of a network structure on the ruin probability in a Cramér-Lundberg setting. We show that the dependence in the network structure plays a fundamental role for the ruin probability; i.e., the risk within the reinsurance market or within a company. The ruin parameter , which in itself serves as a risk measure, becomes random and its properties depend on the random bipartite network as well as on the characteristics of the claim amount processes. While the network adjacency matrix describes the random selection process of the agents (given by edge indicators), the weights describe how the agents divide the losses among each other.

As a prominent network model, we single out the mixed Binomial network model with conditionally independent Bernoulli edge indicators as defined in Section 2. This includes the (deterministic) complete network where all agents are linked to all objects and vice versa as a special case. We also provide scenarios for the division of the losses. In the network with homogeneous weights, every claim size is equally shared by all agents that are connected to it. The exponential system uses weights which depend on the expected object losses. Notably, for exponentially distributed object claims the exponential system yields an explicit formula for the ruin probability in the network.

Our framework is related to the two-dimensional setting in [3, 4] where it is assumed that two companies divide claims among each other in some prespecified proportions. The main novelty of our setting is that we consider a network of interwoven companies, with emphasis on studying the effects which occur through this random network dependence structure. Our bipartite network model has already been used in [11, 12] to assess quantile-based risk measures for systemic risk.

Our results extend those for multivariate models to a random network situation. Whereas one-dimensional insurance risk processes have been extensively studied since Cramér’s introduction in the 1930s, results for multivariate models (beyond bivariate) are scattered in the literature; for a summary of results see [2, Ch. XIII(9)]. In general dimensions, multivariate ruin is studied e.g. in [7, 15], where dependency between the risk processes is modeled by a Clayton dependence structure in terms of a Lévy copula, which allows for scenarios reaching from weak to strong dependence. Further, in [9, 14], using large deviations methods, multivariate risk processes are treated and so-called ruin regions are studied, that is, sets in which are hit by the risk process with small probability. In contrast, in our setting claims are partitioned and assigned randomly.

The paper is structured as follows. In Section 2 we describe the bipartite network model and present two loss sharing schemes that are characterized by homogeneous or proportional weights. We focus on three ruin situations, namely the ruin of a single agent, the ruin of a risk balanced set of agents, and the joint ruin of all agents. Section 3 derives results for the ruin probabilities of sums of components of the multivariate compound Poisson process with special emphasis on the network influence. Here we derive a network Pollaczek-Khintchine formula for component sums and a network Lundberg bound. In Section 4 we present explicit results for an exponential system. In Section 5 we investigate the bipartite network with conditionally independent edges, and provide a Poisson approximation for the ruin parameter for arbitrary sets of agents. We specialize such networks to the mixed Binomial network and the complete network. Section 6 is dedicated to the joint ruin probability of all agents in a selected group and provides a network Lundberg bound for this ruin event. The proofs are found in Section 7.

2 The bipartite network model

Let be a -dimensional spectrally positive compound Poisson process with independent components given by

such that for all the claim sizes are positive i.i.d. random variables having mean and distribution function . Moreover is a Poisson process with intensity , and the premium rate is constant. The corresponding deterministic constant as in the Pollaczek-Khintchine formula (1.1) is called ruin parameter of component .

Further we introduce a random bipartite network, independent of the multivariate compound Poisson process , that consists of agents , , and objects , , and edges between agents and objects as visualized in Figure 1.

The random edge indicator variables are indicating whether or not there is an edge between agent and object . Here and in the following the variable stands for an agent in , and the variable stands for an object in .

The weighted edges are encoded in a weighted adjacency matrix

| (2.1) |

for random variables , which may depend on the random network and have values in such that

| (2.2) |

The edge indicator variables and weights may depend on each other but are assumed to be independent of the process . We use the degree notation

for all , . For and we abbreviate

We denote by the set of all possible realizations of the weighted adjacency matrix from (2.1).

Every object of the bipartite network is assigned to the corresponding component of the compound Poisson process . Every agent is then assigned to a resulting compound Poisson process, its portfolio, given by

In total, this yields a -dimensional process of all agents given by

| (2.3) |

with as defined above. Hence the components of are no longer independent.

Remarks 2.1.

(i) The independence assumption on the components of entails that claims in different components never happen at the same time. This is no mathematical restriction of the model, since we can disentangle dependence through the introduction of additional objects. For example, we can always write two dependent compound Poisson processes as and , where and have claims only in and , respectively, and is the process of the joint claims. Then are independent. Thus, mathematically, a third object, 3, is introduced, and objects 1 and 2 are altered. There is a caveat in that this procedure introduces preconditions on the network structure: The resulting edge indicator variables to the new objects 1 and 3 will not be independent as implies for any , and the same holds for edges to objects 2 and 3.

(ii) We can easily extend this model to multiple layers, where e.g. the agents are connected to a set of super-agents via another bipartite network that is encoded in a second weighted adjacency matrix .

The resulting process on the top layer is simply obtained by matrix multiplication in (2.3), resulting in , which reduces the problem to the form (2.3).

While many general results in this paper do not require independence of the edge indicator variables in the bipartite network, some of our examples will assume that the edges are conditionally independent, given the value of a random variable which is assumed for convenience to take values in . One could think of as a hidden variable such as an economic indicator or an environmental variable which governs the behaviour of all agents. Given a realisation we then use the notation . The following random bipartite network is of particular interest:

-

•

The mixed Binomial network, where are conditionally independent Bernoulli random variables with random parameter . In case of a degenerate variable a.s., we call the resulting model a Bernoulli network, where are independent Bernoulli random variables with parameter . For a.s. we obtain the complete network, where , that is, all agents are linked to all objects and vice versa.

We also single out two specific models for the weights of the weighted adjacency matrix (2.1), which play a prominent role for the network ruin probability. In both examples, the randomness in arises solely from the randomness of the network; given the network, the weights will be deterministic. Still, our general results apply to any random as long as the resulting matrix is independent of the compound Poisson process and (2.2) holds.

-

•

A natural choice for is given by the homogeneous weights

(2.4) i.e., every object is equally shared by all agents that are connected to it.

-

•

A leading example in our paper (see Section 4) extends the one-dimensional precise ruin probability (1.4) for exponentially distributed claims to the network setting. It relies on proportional weights defined as follows. Fix and set for every agent

(2.5) with some constant . Here is chosen such that

and it can be viewed as the proneness of group to link to objects. The resulting random weighted adjacency matrix encodes that the exposure of agent group to object is inversely proportional to the expected claim size of the process associated to that object, while for a fixed object with mean claim size , all which link to this object share it in equal proportion.

We consider the ruin probability of the sum of a non-empty selected subset of all agents and the probability that these agents face ruin (an and-condition), that is

| (2.6) | ||||

| (2.7) |

for such that .

If we simply denote , while for for we write . Similarly we write for Note that for every ,

3 The ruin probability of aggregated risk processes in the network

We start with for , the ruin probability of a set of agents or the total risk of these agents. We will derive two main results for the bipartite network. First, we generalize the Pollaczek-Khintchine formula of (1.1) and, second, the Lundberg inequality (1.3). The proofs rely on the independence of the risk processes and the network and are obtained by conditioning on the network, carefully taking the network properties into account. We postpone them to Section 7.

3.1 The network Pollaczek-Khinchine formula for component sums

Theorem 3.1.

[Network Pollaczek-Khintchine formula for component sums]

For any the joint ruin probability

for a given risk reserve such that has representation

| (3.1) |

where is defined in (3.3) and

| (3.2) |

is a random integrated tail function depending on the matrix , taking values in the set of cumulative distribution functions on non-negative real numbers.

In the network the random variable, henceforth called the (network) ruin parameter,

| (3.3) | ||||

| (3.4) |

is the random equivalent of in the classical Pollaczeck-Khinchine formula (1.1). Note that given as in the classical case we derive from (3.1) that . While in the classical case, is a cut-off for to trivially equal 1, as is random, in the network a similar cut-off for the ruin probability for or is not available.

Remark 3.2.

The following remark collects some general observations on .

Remark 3.3.

(i) Given it holds that

Thus, if all objects have a ruin parameter , then . Nevertheless can be achieved even if some ruin parameters exceed 1, as long as the others balance this contribution.

(ii) Eq. (3.4) shows that the ruin parameter depends on the weights only through ratios of sums of weights.

Eq. (3.4) implies further that

This bound is an equality when all agents are connected only to one single object. Otherwise the bound may be quite crude. Using the Markov inequality this bound can be used to bound for any :

Example 3.4.

[Equal ruin parameters]

If all are equal, we obtain directly from (3.3) that for any set

and hence for any measurable function on

In particular, if and only if . Comparing this condition to the condition in the non-network case, we see that the presence of the network allows for . The network thus balances the ruin probabilities for single components in the sense that is possible while still ensuring that . Similarly, if we interpret as a risk measure, then , which can be much larger than .

Example 3.5.

[Deterministic weights]

Let be independent of and independent of and , such that (2.2) holds.

Then

The summands in the nominator show that the agents in share the ruin parameters of all objects they are linked to in equal proportion. A small corresponds to a large denominator, hence, to small ’s. Consequently, the agents group would favour risk processes with small ruin parameters.

For illustration purposes we extract from Theorem 3.1 the ruin probability of a single agent in the network.

Example 3.6.

[Network Pollaczek-Khintchine formula for a single agent]

The ruin probability for a given risk reserve of for is given by

where for ,

and

3.2 A Lundberg bound for

As in the classical one-dimensional setting, we expect exponential decay of the ruin probability of sums of agents also in the network setting, provided that the claim size distributions are light-tailed. This is shown in the following theorem.

Note that a similar result for ruin probabilities of sums of components of a multivariate risk process, but without network structure, is derived in [2, Ch. XIII, Proposition 9.3].

In order to find an adjustment coefficient which is independent of the specific realisation of the network, let be deterministic constants such that for all ,

| (3.5) |

Theorem 3.8.

[Network Lundberg bound for component sums]

Let be a set of agents and assume that for all the cumulant generating functions exist in some neighbourhood of zero. Then for fixed ,

| (3.6) |

with

In particular, if for all an adjustment coefficient satisfying (1.2) exists, then

where

| (3.7) |

Note that the general bound in Theorem 3.8 is optimal only in the case that all agents in are only connected to the objects with the heaviest tail in the claim size distribution. For a given network structure (3.6) shows that a Lundberg bound can exist even if some of the claim sizes are heavy tailed in the sense that (1.2) does not hold for all objects .

4 The exponential system

For the one-dimensional ruin model the exponential distribution and mixtures thereof are the only claim size models which allow for an explicit solution of (1.1). Hence, it is not surprising that exponential claim size distributions also play a prominent role in the network model. However, an explicit solution also depends on the network itself. In what follows we work with an exponential system, which is characterized by the proportional weights as in (2.5), identical Poisson intensities and exponential claim sizes with means . For this exponential system we obtain an explicit expression for (3.6).

Theorem 4.1.

[Ruin probability for component sums in the exponential system]

Let be a set of agents and assume the exponential system as defined above.

Then the ruin probability of the sum of all agents in is given by

| (4.1) |

and, regardless of the claim size distribution,

| (4.2) |

In contrast to Theorem 3.1, in this special case the integrated tail distribution from (3.2) is deterministic and exponential,

We may again extract the ruin probability for a single agent in the network as follows.

Example 4.2.

[Ruin probability for a single agent]

Let and assume that the conditions of Theorem 4.1 hold with .

Then the ruin probability of agent for is given by

| (4.4) |

where

The argument in the expectation in (4.4) coincides with (1.4) with random .

For the special situation of equal Pollaczek-Khintchine parameters as in Example 3.4 we obtain the single agent’s ruin probability as

5 The bipartite network with conditionally independent edges

Throughout this section we assume that the edge indicators in the bipartite network are conditionally independent, given the random variable , and that for the realisation we have . In this model, for , also the degrees for different are conditionally independent; in particular,

For fixed this model is a prominent network model (an inhomogeneous random graph, cf. [6]), and we present results for the network ruin parameter as well as the network ruin probability in several situations.

If for , then from Example 3.4 we know that the ruin parameter . In general, calculating and functions thereof as for example in (4.3) is not easy. For sparse networks we therefore give a Poisson approximation for . Here sparseness refers to the sum of the squared edge probabilities being small.

5.1 Poisson approximation of

The results in this subsection are based on the following proposition, which follows from [5, Thm. 10.A] by conditioning; the proof is omitted.

Proposition 5.1.

Assume we are given a bipartite network such that the edge indicators for and are conditionally independent given the value of . For each let be independent Poisson variables for and . Then for any ,

| (5.1) | ||||

If agents pick objects with probability roughly proportional to the number of objects, so that for some fixed , for all as , then the bound (5.1) tends to 0 if .

Proposition 5.2.

Corollary 5.3.

[Homogeneous weights for a single agent]

If , then under the assumptions of Proposition 5.1 the approximating Poisson-based random variable for simplifies to

| (5.4) |

where the Poisson variables are independent with means .

Remark 5.4.

Based on the Poisson approximation, the Delta method can be used to approximate using the expressions in (5.4). For each set

then by conditioning on the value of and of ,

We calculate

where we used Eq. (3.9) in [8] for the last equality. Similarly, by the independence of the Poisson variables and again using the results in [8],

where is the hyperbolic cosine integral, is the hyperbolic sine integral, is the natural logarithm and is the Euler-Mascheroni constant. If each has small variance , then the Delta method combined with Proposition 5.1 yields can be approximated well by If agents pick objects with probability roughly proportional to the number of objects, so that for some fixed , , then if .

Proposition 5.5.

In practical applications the distribution of may not be available. In such a situation a second approximation step could be used, approximating mixed Poisson variables of the type by a Poisson variable with mean . By [5, Thm. 1.C] the approximation error is bounded so that for any , we have Corresponding error terms would then be added to the bounds in this subsection.

5.2 and in the mixed Binomial network

As in the mixed Binomial network all vertices are exchangeable, we can assume without loss of generality that . Further, given , every edge is chosen with the same probability independently, the degree of each agent follows a Binomial distribution with parameters and . Thus, for a.s. we obtain the complete network treated in Section 5.3.

In a general mixed Binomial model the value can take on any positive number. To see this, consider a Bernoulli network with fixed edge probability . Then on the set , in the limit for the set of vertices in will have exactly one edge, and the corresponding neighbour of is chosen uniformly at random in . Hence for we approach a single edge network such that

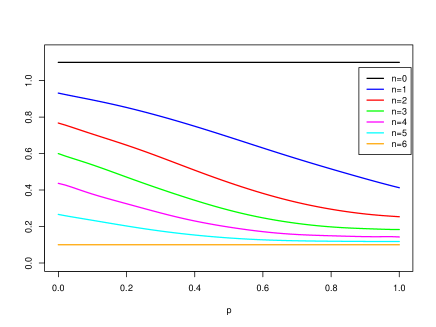

where is uniformly distributed on . This is also illustrated in Figure 2, which shows the varying balancing effect of the network on when the proportion of objects with high and low ruin parameter is changed.

If in the mixed Binomial model for we know from Example 3.4 that and as , we have if and only if . If the distribution of allows for interchanging expectation and the limit , then for we recover the classical condition .

In the following example, we present a family of deterministic weights, such that the randomness of only depends on the random connections of the agents to objects.

Example 5.6.

[Deterministic weights]

Let independent of with independent of and , such that (2.2) holds. Then

For in the Bernoulli network with deterministic parameter , applying Theorem 1 of [8] on we find

and hence

Thus the mean ruin parameter is independent of and equals the arithmetic mean of the ruin parameters of all objects multiplied by .

Similarly, for in a mixed Binomial network with random parameter ,

In particular if follows a Beta distribution with density ,

and again the expected ruin parameter is independent of and proportional to the arithmetic mean of the ruin parameters of all objects.

In the special case where follows a uniform distribution on the above simplifies to

such that for the expected ruin parameter converges from below to the arithmetic mean of the ruin parameters of all objects.

5.3 and in the complete network

The complete network is particularly easy to treat. Here the network ruin parameter from (3.3) equals

In particular, if does not depend on , then is deterministic and does not depend on the choice of the set . This holds true in particular for homogeneous weights (2.4), where every object is equally shared by all agents that connect to it such that for and thus .

For a fixed set of agents and an exponential system with proportional weights as in Theorem 4.1, a complete network implies

which again is deterministic. If , then in the exponential system we find from (4.1)

for such that , which is similar to the one-dimensional case (1.4).

Example 5.7.

To illustrate the effect of the random network and the weights further, assume that the underlying bipartite network is itself a mixture - a complete graph with probability , and the mixed Binomial model considered in Example 5.6 with probability . For a single agent we then have

The expected ruin parameter will be smaller than the ruin parameter of the deterministic network unless the random network is a complete graph almost surely.

In general this monotone behaviour is not the case. For example, in an exponential system with proportional weights as in Theorem 4.1, the same graph mixture gives for a single agent that

Which one of the two summands dominates the expectation depends on the network model and on .

6 The joint ruin probability of a set of agents

In this section we consider as defined in (2.7). Due to the far more complicated structure of the process compared to the sum of components, we do not obtain an explicit form for . Still, we can derive a Lundberg-type bound for using classical martingale techniques.

Recall the bound in (3.5) and write for any and any two vectors

Theorem 6.1.

[Network Lundberg bound for joint ruin probabilities of several agents]

Let be a set of agents and assume that for all the cumulant generating functions exist in some neighbourhood of zero. Then for fixed ,

| (6.1) |

for where

In particular, assume that for all objects the adjustment coefficient satisfying (1.2) exists. Then

with

Remarks 6.2.

[Comparing the bounds for and ]

(i) Assume that all objects have the same adjustment coefficient . Let be a set of agents and assume for the risk reserve for and . Then , which gives the bounds

from Theorem 3.8.

The exponential decay is for both ruin probability bounds the same. The constant in is, however, in general smaller than in .

(ii) For we have and also the bounds obtained in Theorems 3.8 and 6.1 coincide.

7 Proofs

Throughout, we shall denote all realisations of random quantities which are influenced by the realisations of the network structure, by the corresponding tilded letters; e.g., is a specific realisation of the process when the network is fixed.

Proof of Theorem 3.1

By definition of the process we have

such that

For every realisation of the network with the process is a compound Poisson process with intensity, claim size distribution and drift given by

Hence, whenever

for any fixed realisation of it holds that

by the classical Pollaczek-Khintchine formula (1.1). For the ruin probability is obviously . The result now follows by conditioning on the realisations of since and are independent.

Proof of Theorem 3.8

Our proof relies on standard martingale arguments which is why we will only briefly sketch it here. Note first that for any realisation with obviously ruin cannot occur. Thus fix such that . Then the mgf of can be computed as

for any such that the occuring terms are finite. This yields by standard arguments that for all

is a martingale with respect to the natural filtration of . Proceeding as in the classical proof of the Lundberg bound (see e.g. Proposition 3.1 of [2]) we obtain

which yields (3.6) with

To obtain the global bound we have to choose as large as possible such that

for all . This is clearly satisfied if for all and all which leads to the form given in (3.7). Thus

for all , and with

we obtain the result.

Proof of Theorem 4.1

We calculate the random integrated tail distribution as in (3.2),

which is deterministic; we recognise it as the distribution function of the exponential distribution with mean . Hence is an Erlang distribution function with density

Moreover, due to the assumptions on the network, in (3.3) equals (4.2). From (3.1) we obtain for such that ,

| (7.1) |

Now we calculate that

and

Using this expression in (7.1) gives the assertion.

Proof of Proposition 5.2

We write

so that and are independent, as well as and . Recall from Remark 3.2 that in (3.3) the indicator can be omitted. Thus,

Note that for objects and , and are independent for and . Thus is expressed as a function of the edge indicators with the dependence disentangled. While is a non-negative function of the edge indicators, it does not quite fit into the framework of Proposition 5.1 because it may not be bounded by 1. Instead, the deterministic expression serves as upper bound. Using the function with makes Proposition 5.1 applicable. Equivalently, instead of transforming the bound (5.1) can be multiplied by .

Proof of Proposition 5.5

Proof of Theorem 6.1

For notational simplicity the following proof is only given for . The general case can easily be obtained by cutting down the network to a subset of agents. As in the proof of Theorem 3.8 we will follow a standard martingale approach. Note first that, if for one or more agents, then the joint ruin probability is zero, since at least one component of the process is constant. Thus fix any realisation of such that for all . The mgf of can be computed as

for any such that the occuring terms are finite. Hence, for these

is a martingale with respect to the natural filtration of . Proceeding via Doob’s optional stopping theorem as in the classical proof of the (one-dimensional) Lundberg bound (see e.g. Proposition 3.1 of [2]) we obtain for any

which proves (6.1).

For the global bound note that for any such that we have

for all and hence

, . Thus if this yields

and

for any realisation , which gives the result.

References

- [1] S. Asmussen. Applied Probability and Queues. Springer, New York, 2 edition, 2003.

- [2] S. Asmussen and H. Albrecher. Ruin Probabilities. World Scientific, Singapore, 2 edition, 2010.

- [3] F. Avram, Z. Palmowski, and M. Pistorius. Exit problem of a two-dimensional risk process from the quadrant: Exact and asymptotic results. Ann. Appl. Probab., 18:2421–2449, 2008.

- [4] F. Avram, Z. Palmowski, and M. Pistorius. A two-dimensional ruin problem on the positive quadrant. Insurance: Mathematics and Economics, 42:227–234, 2008.

- [5] A.D. Barbour, L. Holst, and S. Janson. Poisson Approximation. Oxford University Press, Oxford, 1992.

- [6] B. Bollobas, S. Janson, and O. Riordan. The phase transition in inhomogeneous random graphs. Random Structures & Algorithms, 31:3–122, 2007.

- [7] Y. Bregman and C. Klüppelberg. Ruin estimation in multivariate models with Clayton dependence structure. Scand. Act. Journal, 2005(6):462–480, 2005.

- [8] M.T. Chao and W.E. Strawderman. Negative moments of positive random variables. JASA, 67(338):429–431, 1972.

- [9] J.F. Collamore. First passage times of general sequences of random vectors: A large deviations approach. Stoch. Proc. Appl., 78(1):97–130, 1998.

- [10] P. Embrechts, C. Klüppelberg, and T. Mikosch. Modelling Extremal Events for Insurance and Finance. Springer, Heidelberg, 1997.

- [11] O. Kley, C. Klüppelberg, and G. Reinert. Systemic risk in a large claims insurance market with bipartite graph structure. Operations Research, 64:1159–1176, 2016.

- [12] O. Kley, C. Klüppelberg, and G. Reinert. Conditional risk measures in a bipartite market structure. Scand. Act. Journal, 2018(4):328–355, 2017. doi: 10.1080/03461238.2017.1350203.

- [13] International Association of Insurance Supervisors (IAIS). Insurance and financial stability, 2011. Available at https://www.iaisweb.org/page/news/other-papers-and-reports//file/34041/insurance-and-financial-stability.

- [14] Y. Pan and K. Borovkov. The exact asymptotics of the large deviation probabilities in the multivariate boundary crossing problem. Adv. Appl. Probab., 51:835–864, 2019.

- [15] S. Ramasubramannian. Multidimensional ruin problem. Communications on Stochastic Analysis, 6(1):33–47, 2012.