Predicting the Last Zero of a Spectrally Negative Lévy Process

Erik J. Baurdoux111Department of Statistics, London School of Economics and Political Science. Houghton street, London, WC2A 2AE, United Kingdom. E-mail: e.j.baurdoux@lse.ac.uk & J. M. Pedraza 222Department of Statistics, London School of Economics and Political Science. Houghton street, London, WC2A 2AE, United Kingdom. E-mail: j.m.pedraza-ramirez@lse.ac.uk

Abstract

Last passage times arise in a number of areas of applied probability, including risk theory and degradation models. Such times are obviously not stopping times since they depend on the whole path of the underlying process.

We consider the problem of finding a stopping time that minimises the -distance to the last time a spectrally negative Lévy process is below zero. Examples of related problems in a finite horizon setting for processes with continuous paths are Du Toit et al., (2008) and Glover and Hulley, (2014), where the last zero is predicted for a Brownian motion with drift, and for a transient diffusion, respectively.

As we consider the infinite horizon setting, the problem is interesting only when the Lévy process drifts to which we will assume throughout. Existing results allow us to rewrite the problem as a classic optimal stopping problem, i.e. with an adapted payoff process. We use a direct method to show that an optimal stopping time is given by the first passage time above a level defined in terms of the median of the convolution with itself of the distribution function of . We also characterise when continuous and/or smooth fit holds.

In recent years last exit times have been studied in several areas of applied probability, e.g. in risk theory (see Chiu et al., (2005)). Consider the Cramér–Lundberg process, which is a process consisting of a deterministic drift plus a compound Poisson process which has only negative jumps (see Figure 1) which typically models the capital of an insurance company. A key quantity of interest is the time of ruin , i.e. the first time the process becomes negative. Suppose the insurance company has funds to endure negative capital for some time. Then another quantity of interest is the last time that the process is below zero. In a more general setting we may consider a spectrally negative Lévy process instead of the classical risk process. We refer to Chiu et al., (2005) and Baurdoux, (2009) for the Laplace transform of the last time before an exponential time a spectrally negative Lévy process is below some level.

Figure 1: Cramér–Lundberg process with the moment of ruin and the last zero.

Last passage times also appear in financial modeling. In particular, Madan et al., 2008a ; Madan et al., 2008b showed that the price of a European put and call option for certain non-negative, continuous martingales can be expressed in terms of the probability distributions of last passage times.

Another application is in degradation models. Paroissin and Rabehasaina, (2013) proposed a spectrally positive Lévy process as a degradation model. They consider a subordinator perturbed by an independent Brownian motion. The presence of a Brownian motion can model small repairs of the component or system and the jumps represents major deterioration. Classically, the failure time of a component or system is defined as the first hitting time of a critical level which represents a failure or a bad performance of the component or system. Another approach is to consider instead the last time that the process is under . Indeed, for this process the paths are not necessarily monotone and hence when the process is above the level it can return back below it later.

The main aim of this paper is to predict the last time a spectrally negative Lévy process is below zero. More specifically, we aim to find a stopping time that is closest (in sense) to the above random time. This is an example of an optimal prediction problem. Recently, these problems have received considerable attention, for example, Bernyk et al., (2011) predicted the time at which a stable spectrally negative Lévy process attains its supremum in a finite time horizon. A few years later, the infinite time horizon version was solved in Baurdoux and Van Schaik, (2014) for a general Lévy process with an infinite time horizon. Glover et al., (2013) predicted the time of its ultimate minimum for a transient diffusion processes. Du Toit et al., (2008) predicted the last zero of a Brownian motion with drift and Glover and Hulley, (2014) predicted the last zero of a transient difussion. It turns out that the problems just mentioned are equivalent to an optimal stopping problem, in other words, optimal prediction problems and optimal stopping problems are intimately related.

The rest of this paper is organised as follows. In Section 2 we discuss some preliminaries and some technicalities to be used later. Section 3 concerns main result, Theorem 3.4. Section 4 is then dedicated to the proof of Theorem 3.4. In the final Section we consider specific examples.

2 Prerequisites and formulation of the problem

Formally, let be a spectrally negative Lévy process drifting to infinity, i.e. , starting from defined on a filtered probability space where is the filtration generated by which is naturally enlarged (see Definition 1.3.38 in Bichteler, (2002)). Suppose that has Lévy triple where , and is the so-called Lévy measure concentrated on satisfying . Then the characteristic exponent defined by take the form

Moreover, the Lévy–Itô decomposition states that can be represented as

where is an standard Brownian motion, is a Poisson random measure with intensity and the process is a square-integrable martingale. Furthermore, it can be shown that all Lévy processes satisfy the strong Markov property.

Let and the scale functions corresponding to the process (see Kyprianou, (2014) or Bertoin, (1998) for more details). That is, is such that for , and is characterised on as a strictly increasing and continuous function whose Laplace transform satisfies

and

where and are, respectively, the Laplace exponent and its right inverse given by

for .

Note that is zero at zero and tends to infinity at infinity. Moreover, it is infinitely differentiable and strictly convex with (since drifts to infinity). The latter directly implies that .

We know that the right and left derivatives of exist (see Kyprianou, (2014) Lemma 8.2). For ease of notation we shall assume that has no atoms when is of finite variation, which guarantees that . Moreover, for every the function is an analytic function on .

If is of finite variation we may write

where necessarily

With this notation, from the fact that for and using the dominated convergence theorem we have that

(1)

For all , the function may have a discontinuity at zero and this depends on the path variation of : in the case that is of infinite variation we have that , otherwise

(2)

There are many important fluctuations identities in terms of the scale functions and (see Bertoin, (1998) Chapter VII or Kyprianou, (2014) Chapter 8). We mention some of them that will be useful for us later on. Denote by the first time the process is below the zero, i.e.

We then have for

(5)

where denotes the law of started from .

Let us define the -potential measure of killed on exiting for as follows

The potential measure has a density (see Kuznetsov et al., (2011) Theorem 2.7 for details) which is given by

(6)

In particular, will be useful later. Another pair of processes that will be useful later on are the running supremum and running infimum defined by

The well-known duality lemma states that the pairs and have the same distribution under the measure . Moreover, with an independent exponential distributed random variable with parameter , we deduce from the Wiener–Hopf factorisation that the random variables and are independent. Furthermore, in the spectrally negative case, is exponentially distributed with parameter . From the theory of scale functions we can also deduce that is a continuous random variable with

(7)

for .

Denote by as the last passage time below , i.e.

(8)

When we simply write .

Remark 2.1.

Note that from the fact that drifts to infinity we have that -a.s. Moreover, as is a spectrally negative Lévy process, and hence the case of a compound Poisson process is excluded, the only way of exiting the set is by creeping upwards. This tells us that and that -a.s.

Clearly, up to any time the value of is unknown (unless is trivial), and it is only with the realisation of the whole process that we know that the last passage time below has occurred. However, this is often too late: typically one would like to know how close is to at any time and then take some action based on this information. We search for a stopping time of that is as “close” as possible to . Consider the optimal prediction problem

(9)

where is the set of all stopping times.

3 Main result

Before giving an equivalence between the optimal prediction problem (9) and an optimal stopping problem we prove that the random times for have finite mean. For this purpose, let be the first passage time above , i.e,

Lemma 3.1.

Let be a spectrally negative Lévy process drifting to infinity with Lévy measure such that

(10)

Then for every .

Proof.

Note that by the spatial homogeneity of Lévy processes we have to prove that for all .

Then it suffices to take . From Baurdoux, (2009) (Theorem 1) or Chiu et al., (2005) (Theorem 3.1) we know that for a spectrally negative Lévy process such that the Laplace transform of for and is given by

Then, from the well-known result which links the moments and derivatives of the Laplace transform (see Feller, (1971) (section XIII.2)), the expectation of is given by

We know that for any the function is analytic, therefore the first term in the last expression is finite. Hence has finite second moment if and are finite. Recall that the function is zero at zero and tends to infinity at infinity. Further, it is infinitely differentiable and strictly convex on . Since drifts to infinity we have that for any .

We deduce that is strictly increasing in and the right inverse is the usual inverse for . From the fact that is strictly convex we have that for all .

We then compute

and

From the Lévy–Itô decomposition of we know that

where the last inequality holds by assumption (10) and from the fact that since is a Lévy measure. Then we have that and hence for all .

∎

Now we are ready to state the equivalence between the optimal prediction problem and an optimal stopping problem mentioned earlier. This equivalence is mainly based on the work of Urusov, (2005).

Lemma 3.2.

Consider the standard optimal stopping problem

(11)

where the function is given by for . Then the stopping time which minimises (9) is the same which minimises (11). In particular,

(12)

Proof.

Fix any stopping time of . We then have

From Fubini’s Theorem we have

Note that due to Remark 2.1, the event is equal to (up to a -null set). Hence, since is -measurable,

where for . From the Markov property for Lévy processes we have that is a Lévy process with the same law as , independent of . We therefore find that

where .

Note that the event is equal to where . Hence, by the spatial homogeneity of Lévy processes

where the last equality holds by identity (5) and the fact that . Therefore,

Hence,

∎

To find the solution of the optimal stopping problem (11) we will expand it to an optimal stopping problem for a strong Markov process with starting value . Specifically, we define the function as

(13)

Thus,

Remark 3.3.

Note that the distribution function of is given by

Hence the function can be written in terms of as .

Let us now give some intuition about the optimal stopping problem (13). For this define as the lowest value such that , i.e.

(14)

We know that is continuous and strictly increasing on and vanishes on . Moreover, we have that (since is a distribution function). As a consequence we have that is a strictly increasing and continuous function on such that for and . In the same way as , may have a discontinuity at zero depending of the path variation of . From the fact that for and the definition of given in (14) we have that .

The above observations tell us that, to solve the optimal stopping problem (13), we are interested in a stopping time such that before stopping, the process spent most of the time in those values where is negative, taking into account that can pass some time in the set and then return back to the set .

It therefore seems reasonable to think that a stopping time which attains the infimum in (13) is of the form,

for some .

The following theorem is the main result of this work. It confirms the intuition above and links the optimal stopping level with the median of the convolution with itself of the distribution function of .

Theorem 3.4.

Suppose that is a spectrally negative Lévy process drifting to infinity with Lévy measure satisfying

Then there exists some such that an optimal stopping time in (13) is given by

The optimal stopping level is defined by

(15)

where is the convolution of with itself, i.e.,

Furthermore, is a non-decreasing, continuous function satisfying the following:

If is of infinite variation or finite variation with

(16)

then is the median of the distribution function , i.e. is the unique value which satisfies the following equation

(17)

The value function is given by

(18)

Moreover, there is smooth fit at i.e. .

If is of finite variation with then and

In particular, there is continuous fit at i.e. and there is no smooth fit at i.e. .

Remark 3.5.

Note that since corresponds to the distribution function of , can be interpreted as the distribution function of where is an independent copy of . Moreover, can be written in terms of scale functions as

Using Fubini’s Theorem the value function takes the form

(20)

Note that in the case that is of finite variation the condition is equivalent to (since and ) so the condition given in tells us that the drift is much larger than the average size of the jumps. This implies that the process drifts quickly to infinity and then we have to stop the first time that the process is above zero. In this case, concerning the optimal prediction problem, the stopping time which is nearest (in the sense) to the last time that the process is below zero is the first time that the process is above the level zero.

If is of finite variation with then we have that the average of size of the jumps of are sufficiently large such that when the process crosses above the level zero the process is more likely (than in ) that the process jumps again below and spend more time in the region where is negative. This condition also tells us that the process drifts a little slower to infinity that in the . The stopping time which is nearest (in the sense) to the last time that the process is below zero is the first time that the process is above the level .

4 Proof of Main Result

In the next section we proof Theorem 3.4 using a direct method. Since proof is rather long, we break it into a number of lemmas.

In particular, we will use the general theory of optimal stopping (see Peskir and Shiryaev, (2006)) to get a direct proof of Theorem 3.4. First, using the Snell envelope we will show that an optimal stopping time for (13) is the first time that the process enters to a stopping set , defined in terms of the value function . Recall the set

We denote as the set of all stopping times.

The next Lemma is standard in optimal stopping and we include the proof for completeness.

Lemma 4.1.

Denoting by the stopping set, we have that for any the stopping time

attains the infimum in , i.e. .

Proof.

From the general theory of optimal stopping consider the Snell envelope defined as

and define the stopping time

Then we have that the stopping time is is optimal for

(21)

On account of the Markov property we have

where the last equality follows from the spatial homogeneity of Lévy processes and from the definition of . Therefore . So we have

Thus

where the third equality holds since is optimal for (21) and the fourth follows from the spatial homogeneity of Lévy processes. Therefore the stopping time is the optimal stopping time for for all .

∎

Next, we will prove that is finite for all which implies that there exists a stopping time such that the infimum in (13) is attained. Recall the definition of in (14).

Lemma 4.2.

The function is non-decreasing with for all . In particular, for any .

Proof.

From the spatial homogeneity of Lévy processes,

Then, if we have since is a non-decreasing function (see the discussion before Theorem 3.4). This implies that and is non-decreasing as claimed. If we take the stopping time , then for any we have . Let and let then and from the fact that for all , we have

where the last inequality holds due to and then .

Now we will see that for all . Note that holds for all and thus

where the last inequality holds since if then .

From Lemma 3.1 we have that . Hence for all we have and due to the monotonicity of , for all .

∎

Next, we derive some properties of which will be useful to find the form of the set .

Lemma 4.3.

The set is non-empty. Moreover, there exists an such that

Proof.

Suppose that . Then by Lemma 4.1 the optimal stopping time for (13) is . This implies that

Let be the median of , i.e.

and let the last time that the process is below the level defined in (8). Then

(22)

Note that from the fact that is finite and has finite expectation (see Lemma 3.1)) the first term on the right-hand side of (22) is finite. Now we analyse the second term in the right-hand side of (22). With , since is non-negative for all we have

Then letting and using the monotone convergence theorem we deduce that which leads to a contradiction. From the fact that is a non-decreasing function and the set we have that there exists a sufficiently large such that for all .

∎

Lemma 4.4.

The function is continuous.

Proof.

From the previous lemma we know that there exists an such that for all . As is a spectrally negative Lévy process drifting to infinity we have that -a.s. and thus

Using the strong Markov property of and the fact that we have

Note that the process is continuous. Then we have that

where the last quantity is finite since we know that for a spectrally negative Lévy process

and then calculating derivatives with respect to and evaluating at zero (see Feller, (1971) (section XIII.2)) we obtain that

Then from the general theory of optimal stopping time we have that the infimum in

(23)

is attained, say . Note that from the definition of and we have that . Now we check the continuity of . As is continuous in we have that is uniformly continuous in the interval . Now take , then there exists some such that for all it holds when . Then we have

where the first inequality holds since is not necessarily optimal for and the last inequality follows since is always positive and from .

Recall that we have a possible discontinuity for in zero, and for . Thus

(24)

Note that the first term in (4) is zero. Now we analyse the second term. Using the monotonicity of , Fubini’s Theorem and the density of the potential measure of killed on exiting given in (6) we have

where the final inequality follows since is strictly increasing and . Finally we inspect the third term in (4), using the finiteness of the moment of we obtain

Hence

and the continuity holds.

∎

From Lemmas 4.3 and 4.4 we have that the set for some . From Lemma 4.1 we know that for some

attains the infimum in . As is a spectrally negative Lévy process we have that -a.s. and hence is an optimal stopping time for (13) for some . Then we just have to find the value of which minimises the right hand side of (13) with . So in what follows we will analyse the function

(25)

and find the value which minimises the function for a fixed . We could then conclude that and is an optimal stopping time.

Using the Wiener–Hopf factorisation we find an a explicit form of in terms of the convolution of the function with itself.

Lemma 4.5.

For , and for ,

(26)

Proof.

It is clear that for , since if the process begins above the level , then the first passage time above is zero and the integral inside of the expectation in (25) is again zero. Now suppose that , then using Fubini’s Theorem twice,

where is the running supremum. Denote by an exponential distribution with parameter independent of , then using the dominated convergence theorem we obtain

From the Wiener–Hopf factorisation (see for example Kyprianou, (2014) Theorem 6.15) we know that is independent of and that is exponentially distributed with parameter . Thus we have

where the last equality follows since for all . From the expression of the density of given in equation (7) we deduce that

where the last equality follows by the dominated convergence theorem, is an analytic function and . Now recall that and that for all

and the proof is complete.

∎

Now we characterise the value at which the function achieves its minimum value. Recall that is smallest value in which the function is positive, i.e.

Lemma 4.6.

For all the function achieves its minimum value in which does not depend on the value of . The value is characterised as in Theorem 3.4.

Proof.

We know that the function is given for

then is differentiable and for sufficiently small

Recall that is a continuous function in and for all then we can write

Due to monotone convergence we see that is a continuous function in and

where the last equality follows since is a distribution function. Moreover we have that for and

Hence in the case that is of infinite variation we have that and thus . Meanwhile in the case that is of finite variation if and only if . Hence, if is of infinite variation or is of finite variation with there exists a value such that and this occurs if and only if

In the case that that is of finite variation with we have that and then we define . Therefore we have the following: there exists a value such that for , and for it holds that . This implies that the behaviour of is as follows: for , is a decreasing function, and for , is increasing. Consequently reaches its minimum value uniquely at . That is, for all

It only remains to prove that . Recall that the definition of is

We know from the definition of that which implies that

where in the last inequality we use that . Therefore we have that .

∎

We conclude that for all ,

where is characterised in Theorem 3.4. All that remains is to show now is the necessary and sufficient conditions for smooth fit to hold.

Lemma 4.7.

We have the following:

If is of infinite variation or finite variation with (16) then there is smooth fit at i.e. .

If is of finite variation and (16) does not hold then there is continuous fit at i.e. . There is no smooth fit at i.e. .

so . The left and right derivative of at are given by

Therefore in this case only the continuous fit at is satisfied. If is of infinite variation or finite variation with

we have from Lemma 4.5 that . Its derivative for is

Since satisfies we have that

Thus we have smooth fit at .

∎

Remark 4.8.

The main result can also be deduced using a classical verification-type argument. Indeed, it is straightforward to show

that if is a candidate optimal strategy for the optimal stopping problem (13) and , , then the pair is a solution if

1.

for all ,

2.

the process is a -submartingale for all .

With it can be shown that the first condition is satisfied. The submartingale property can also be shown to hold using Itô’s formula. However, the proof of this turns out to be rather more involved than the direct approach, as it requires some technical lemmas to derive the necessary smoothness of the value function, as well as the required inequality linked to the submartingale propery.

5 Examples

We calculate numerically (using the statistical software R Core Team, (2017)) the value function for some values of . The models used were Brownian motion with drift, Cramér–Lundberg risk process with exponential claims and a spectrally negative Lévy process with no Gaussian component and Lévy measure given by .

5.1 Brownian motion with drift

Let be a Brownian motion with drift, i.e., is of the form

where . Since there is absence of positive jumps and we have a positive drift, is indeed a spectrally negative Lévy process drifting to infinity. In this case the expressions for the Laplace exponent and scale functions are well known (see for example Kuznetsov et al., (2011), Example 1.3). The Laplace exponent is given by

For the scale function is

Letting and using that we get that

That is, , which implies that corresponds to the distribution function of a (see Remark 3.5 ). Therefore corresponds to the median of the aforementioned Gamma distribution. In other words, is given by

and then is the solution to

Moreover, is given by

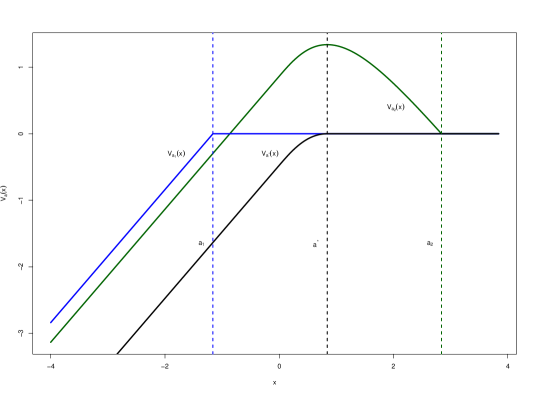

In Figure 2 we sketch a picture of defined in (26) for different values of . The parameters chosen for the model are and .

Figure 2: Brownian motion with drift. Function for different values of . Blue: ; green: ; black: .

5.2 Cramér–Lundberg risk process

We consider as the Cramér–Lundberg risk process with exponential claims. That is is given by

where , is a Poisson process with rate and is a sequence of independent and identically exponentially distributed random variables with parameter . Due to the presence of only negative jumps we have that is a spectrally negative Lévy process. It can be easily shown that is a finite variation process. Moreover, since we need the process to drift to infinity we assume that

The Laplace exponent is given by

It is well known (see Hubalek and Kyprianou, (2011), Example 1.3 or Kyprianou, (2014), Exercise 8.3 iii)) that the scale function for this process is given by

This directly implies that

and then is given by

Hence, when we have that and

For the case , is the solution to the equation and the value function is given by

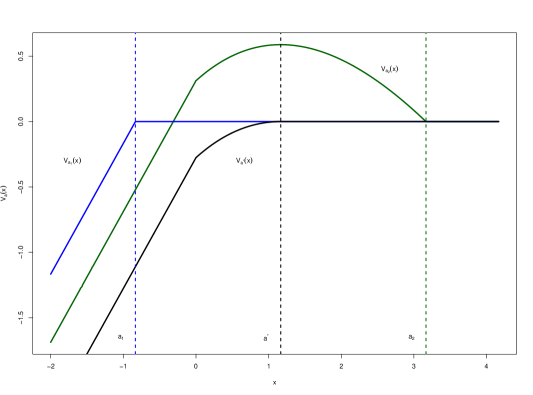

In Figure 3 we calculate numerically the value of for the parameters , and and different values of . In particular, the numerical value for the latter integral corresponds to .

Figure 3: Cramér–Lundberg risk process. Function for different values of . Blue: ; green: ; black: .

5.3 An infinite variation process with no Gaussian component

In this subsection we consider a spectrally negative Lévy process related to the theory of self-similar Markov processes and conditioned stable Lévy processes (see Chaumont et al., (2009)). This process turns out to be the underlying Lévy process in the Lamperti represetantion of a stable Lévy process conditioned to stay positive. Now we describe the characteristics of this process (which can also be found in Hubalek and Kyprianou, (2011)).

We consider as a spectrally negative Lévy process with Laplace exponent

where . This process has no Gaussian component and the corresponding Lévy measure is given by

This process is of infinite variation and drifts to infinity. Its scale function is given by

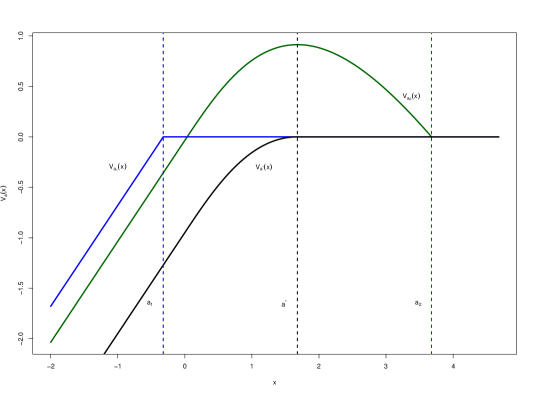

Taking the limit when goes to infinity on we easily deduce that and thus . For the case we calculate numerically the function and then the value of the number as well as the values of the function see Figure 4. We also included the values of the function (defined in (26)) for different values of (including ).

We close this section with a final remark. Using the empirical evidence from the previous examples we make some observations about whether the smooth fit conditions holds.

Remark 5.1.

Note in Figures 2, 3 and 4 that the value is the unique value for which the function exhibits smooth fit (or continuous fit) at . When we choose , the function is not differentiable at . Moreover, there exists some such that . Similarly, If the function is also not differentiable at .

Figure 4: Spectrally negative Lévy process with Lévy measure . Function for different values of . Blue: ; green: ; black: .

References

Baurdoux, (2009)

Baurdoux, E. J. (2009).

Last exit before an exponential time for spectrally negative lévy

processes.

Journal of Applied Probability, 46(2):542–558.

Baurdoux and Van Schaik, (2014)

Baurdoux, E. J. and Van Schaik, K. (2014).

Predicting the time at which a lévy process attains its ultimate

supremum.

Acta Applicandae Mathematicae, 134(1):21–44.

Bernyk et al., (2011)

Bernyk, V., Dalang, R. C., and Peskir, G. (2011).

Predicting the ultimate supremum of a stable lévy process with no

negative jumps.

The Annals of Probability, pages 2385–2423.

Bertoin, (1998)

Bertoin, J. (1998).

Lévy processes, volume 121.

Cambridge university press.

Bichteler, (2002)

Bichteler, K. (2002).

Stochastic integration with jumps, volume 89.

Cambridge University Press.

Chaumont et al., (2009)

Chaumont, L., Kyprianou, A. E., and Pardo, J. C. (2009).

Some explicit identities associated with positive self-similar markov

processes.

Stochastic Processes and Their Applications, 119(3):980–1000.

Chiu et al., (2005)

Chiu, S. N., Yin, C., et al. (2005).

Passage times for a spectrally negative lévy process with

applications to risk theory.

Bernoulli, 11(3):511–522.

Du Toit et al., (2008)

Du Toit, J., Peskir, G., and Shiryaev, A. (2008).

Predicting the last zero of brownian motion with drift.

Stochastics: An International Journal of Probability and

Stochastics Processes, 80(2-3):229–245.

Feller, (1971)

Feller, W. (1971).

An Introduction to probability theory and its applications, Vol.

II.

Wiley, New York, 2nd edition.

Glover and Hulley, (2014)

Glover, K. and Hulley, H. (2014).

Optimal prediction of the last-passage time of a transient diffusion.

SIAM Journal on Control and Optimization, 52(6):3833–3853.

Glover et al., (2013)

Glover, K., Hulley, H., Peskir, G., et al. (2013).

Three-dimensional brownian motion and the golden ratio rule.

The Annals of Applied Probability, 23(3):895–922.

Hubalek and Kyprianou, (2011)

Hubalek, F. and Kyprianou, E. (2011).

Old and new examples of scale functions for spectrally negative

lévy processes.

In Seminar on Stochastic Analysis, Random Fields and

Applications VI, pages 119–145. Springer.

Kuznetsov et al., (2011)

Kuznetsov, A., Kyprianou, A., and Rivero, V. (2011).

The theory of scale functions for spectrally negative lévy

processes. lévy matters ii.

Kyprianou, (2014)

Kyprianou, A. E. (2014).

Fluctuations of Lévy Processes with Applications:

Introductory Lectures.

Springer Science & Business Media, 2 edition.

(15)

Madan, D., Roynette, B., and Yor, M. (2008a).

From black-scholes formula, to local times and last passage times for

certain submartingales.

Prépublication IECN, 14:2008.

(16)

Madan, D., Roynette, B., and Yor, M. (2008b).

Option prices as probabilities.

Finance Research Letters, 5(2):79–87.

Paroissin and Rabehasaina, (2013)

Paroissin, C. and Rabehasaina, L. (2013).

First and last passage times of spectrally positive lévy

processes with application to reliability.

Methodology and Computing in Applied Probability, pages 1–22.

Peskir and Shiryaev, (2006)

Peskir, G. and Shiryaev, A. (2006).

Optimal stopping and free-boundary problems.

Springer.

R Core Team, (2017)

R Core Team (2017).

R: A Language and Environment for Statistical Computing.

R Foundation for Statistical Computing, Vienna, Austria.

Urusov, (2005)

Urusov, M. A. (2005).

On a property of the moment at which brownian motion attains its

maximum and some optimal stopping problems.

Theory of Probability & Its Applications, 49(1):169–176.