Simulation of particle systems interacting through hitting times

Abstract

We develop an Euler-type particle method for the simulation of a McKean–Vlasov equation arising from a mean-field model with positive feedback from hitting a boundary. Under assumptions on the parameters which ensure differentiable solutions, we establish convergence of order in the time step. Moreover, we give a modification of the scheme using Brownian bridges and local mesh refinement, which improves the order to . We confirm our theoretical results with numerical tests and empirically investigate cases with blow-up.

Keywords: McKean-Vlasov equations, particle method, timestepping scheme, Brownian bridge.

1 Introduction

There has been a recent surge in interest in mean-field problems, both from a theoretical and applications perspective. We focus on models where the interaction derives from feedback on the system when a certain threshold is hit. Application areas include electrical surges in networks of neurons and systemic risk in financial markets. As analytic solutions are generally not known, numerical methods are inevitable, but still lacking.

We therefore propose and analyse numerical schemes for the simulation of a specific McKean–Vlasov equation which exhibits key features of these models, namely

| (1) | |||||

| (2) | |||||

| (3) | |||||

where , a standard Brownian motion on a probability space , on which is also given an -valued random variable independent of . The non-linearity arises from the dependence of in (1) on the law of . More specifically, if has a derivative , which is then the density of the hitting time of zero,

so that the drift depends on the law of the path of .

Theoretical properties of (1)–(3) have been studied in Hambly et al., (2018), who prove the existence of a differentiable solution up to an ‘‘explosion time’’ . Conversely, they show that cannot be continuous for all for above a threshold determined by the law of . Such systemic events where discontinuities occur are also referred to as ‘‘blow-ups’’ in the literature.

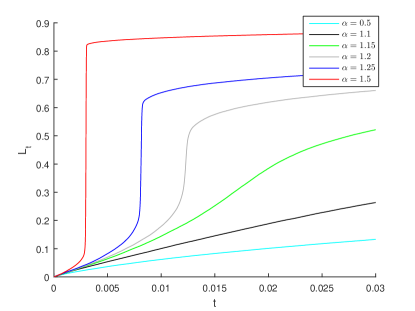

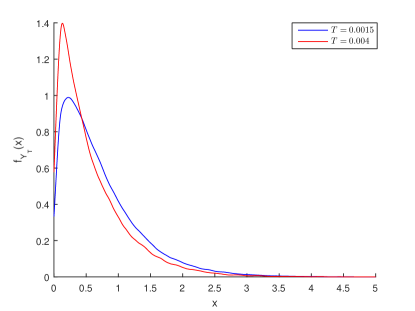

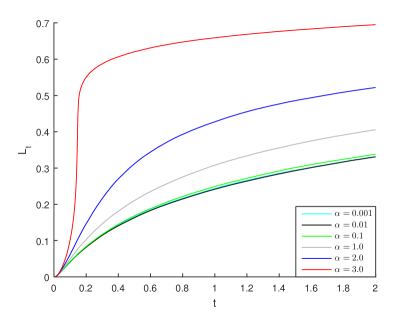

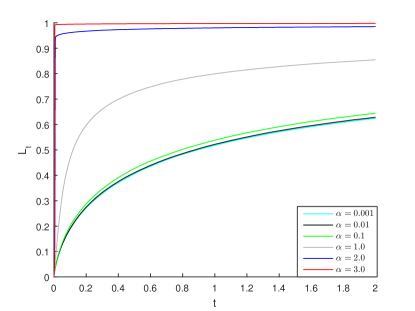

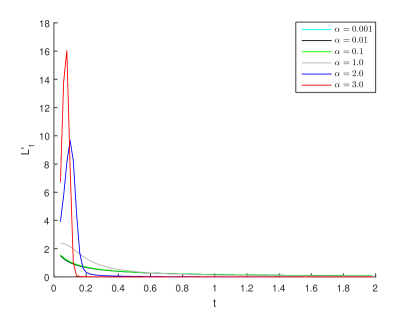

The question of the constructive solution, however, remained open. Examples of a numerical solution computed with Algorithm 1 introduced in Section 2 are shown in Figure 1. The left plot shows the formation of a discontinuity in the loss function for increasing , with . The density of for before and after the shock is displayed in the right panel.

A similar model has been studied in Nadtochiy and Shkolnikov, (2017), where the authors consider instead of in (1). Our numerical scheme can be applied in principle to this problem, but we concentrate the analysis on (1)–(3) in this paper.

One motivation for studying these equations comes from mathematical finance, in particular, systemic risk. A large interconnected banking network can be approximated by a particle system with interactions by which the default of one firm, modeled as the hitting of a lower default threshold of its value, causes a downward move in the firm value of others. More details can be found in Hambly et al., (2018) and Nadtochiy and Shkolnikov, (2017). This model can also be viewed as the large pool limit of a structural default model for a pool of firms where interconnectivity is caused by mutual liabilities, such as in Lipton, (2016).

An earlier version this problem is found in neuroscience, where a large network of electrically coupled neurons can be described by McKean–Vlasov type equations (Cáceres et al., (2011); Carrillo et al., (2013); Delarue et al., 2015b ; Delarue et al., 2015a ). If a neuron’s potential reaches some fixed threshold, it jumps to a higher potential level and sends a signal to other neurons. This feedback leads to the following equations

| (4) | |||||

| (5) |

where a.s. The similarity to (1)–(3) is seen by noticing that and in (5) is constant between hitting times, however, while in (4) an upper boundary is hit and after that the value resets to zero, in our model we are interested in hitting the zero boundary (from above), and after hitting the particle’s value remains zero.

While McKean–Vlasov equations are an active area of current research, to our knowledge, there is only a fairly small number of papers where their simulation is studied rigorously and none of these encompass the models above.

Early works include Bossy and Talay, (1997), which proves convergence (with order 1/2 in the timestep and inverse number of particles) of a particle approximation to the distribution function for the measure of in the classical McKean-Vlasov equation

| (6) |

with sufficient regularity. The proven rate in the timestep is improved to 1 in Antonelli et al., (2002) using Malliavin calculus techniques.

More recently, multilevel simulation algorithms have been proposed and analysed: Ricketson, (2015) considers the special case of an SDE whose coefficients at time depend on and the expected value of a function of ; Szpruch et al., (2017) study a method based on fixed point iteration for the general case (6). An alternative variance reduction technique by importance sampling is given in Reis et al., (2018).

The system (1)–(3) above does not fall into the setting of (6) due to the extra path-dependence of the coefficients through the hitting time distribution. In this paper, we therefore propose and analyse a particle scheme for (1)–(3) with an explicit timestepping scheme for the nonlinear term. We simulate exchangeable particles at discrete time points with distance , whereby at each time point we use an estimator of from the previous particle locations to approximate (3). We prove the convergence of the numerical scheme up to some time as the time step goes to zero and number of particles goes to infinity. The scheme can be extended up to the explosion time under certain conditions on the model parameters. The order in for this standard estimator is 1/2. Next, we use Brownian bridges to better approximate the hitting probability, similar to barrier option pricing (Glasserman, (2013)). In this case, the convergence rate improves to , where is the Hölder exponent of the density of the initial value (e.g., 0.5 in the example from Figure 8). The order can be improved to 1 by non-uniform time-stepping.

A main contribution of the paper is the first provably convergent scheme for equations of the type (1)–(3). The analysis uses a direct recursion of the error and regularity results proven in Hambly et al., (2018). This has the advantage that sharp convergence orders – i.e., consistent with the numerical tests – can be given, but also means that it seems difficult to apply the analysis directly to variations of the problem where such results are not available. Nonetheless, the method itself is natural and applicable in principle to other settings such as those outlined above.

The rest of the paper is organized as follows. In Section 2 we list the running assumptions and state the main results of the paper; in Sections 3.1 and 3.2 we prove the uniform convergence of the discretized process; in Section 3.3, we show the convergence of Monte Carlo particle estimators with an increasing number of samples; in Section 3.4 we prove the convergence order for the scheme with Brownian bridge; in Section 4 we give numerical tests of the schemes; finally, in Section 5, we conclude.

2 Assumptions and main results

We begin by listing the assumptions. The first one, Hölder continuity at 0 of the initial density, is key for the regularity of the solution. The Hölder exponent will also limit the rate of convergence of the discrete time schemes.

Assumption 1.

We assume that has a density supported on such that

| (7) |

for some .

Under Assumption 1, we can refer to Theorem 1.8 in Hambly et al., (2018) for the existence of a unique, differentiable solution for (1)–(3) up to time

and a corresponding such that for every

| (8) |

This estimate admits a singularity of the rate of losses at time 0, however, what is actually observed in numerical studies (see Figure 1, left) is that the loss rate is bounded initially but then has a sharp peak for small (and then especially for large ).

The following assumption will be used to control the propagation of the discretisation error, by bounding the density (especially at 0) of the running minimum of and its approximations.

Assumption 2.

In the following, we assume that Assumptions 1 and 2 hold. Consider a uniform time mesh , where , and a discretized process, for ,

| (11) | |||||

| (12) | |||||

| (13) |

We extend to by setting for .

The first theorem, proven in Section 3.1, shows that converges uniformly to .

Theorem 1.

Theorem 2.

For all ,

| (15) |

Next, we improve our scheme by using a Brownian bridge strategy to estimate the hitting probabilities. In order to do this, we consider the process

| (16) | |||||

| (17) | |||||

| (18) |

Then, for each Brownian path , we compute in , where is an -sample estimator of given below. Hence, using Brownian bridges, we compute

Thus, a natural choice for is

| (19) |

As a result, the new algorithm with the Brownian bridge modification is the following.

Theorem 3.

We will later give a result with variable time steps which achieves rate 1 for all .

3 Convergence results

3.1 Convergence of the timestepping scheme

In this section we prove Theorem 1. Then, in Section 3.2, under a modification of Assumption 2, we formulate and prove an improvement of this theorem which extends the applicable time interval.

The proof is based on induction on the error bound over the timesteps, which requires an error estimate of the hitting probability after discretisation (Lemmas 1 and 2), a sort of consistency, plus a control of the resulting misspecification of the barrier through a bound on the density of the running minimum (Lemma 3), a kind of stability.

As we have crude estimates on the densities, using only Assumption 1 but no sharper bound on, and regularity of, , or any regularity of the distribution of or its approximations, the time until which the numerical scheme is shown to converge will by no means be sharp. Indeed, in our numerical tests (see Section 4) we did not encounter any difficulties for any , even .

We first formulate these auxiliary results which we will use to prove Theorems 1, 3, and 4. The proofs are given in Appendix A.

First, we modify Proposition 1 from Asmussen et al., (1995), where an analogous result is shown for standard Brownian motion, i.e., without the presence of and (i.e., ).

Lemma 1.

Define and . Then, as ,

| (21) |

and

| (22) |

The next lemma deduced the convergence rate of the hitting probabilities on the mesh.

Lemma 2.

Consider the processes and . Then, for any there exist , independent of and , such that

| (23) |

and

| (24) |

Finally, we bound the probability that the running minimum is close to the boundary.

Lemma 3.

We are now in a position to prove Theorem 1.

Proof of Theorem 1.

We split the error into two contributions,

We can use Lemma 2, (23), for the second term. Now we shall proceed by induction to estimate . For , we have . Assume we have shown for , where as . Then,

where and are the CDF and pdf of .

Then, using Lemma 3, we have

as . As a result, we have the following inequality for ,

hence is bounded independent of and by Assumption 2. By induction we get (14).

∎

3.2 Extension of the result in time

The following result extends the applicability of Theorem 1 up to the explosion time under certain conditions on the parameters, as specified precisely in (27) below.

We shall adapt Theorem 1 in Borovkov and Novikov, (2005), which states: For a Lipschitz function with Lipschitz constant , and such that ,

By Remark 2 in Borovkov and Novikov, (2005), this result can be improved for a non-decreasing function . Indeed, retracing the steps in their proof and using monotonicity, one finds easily the slightly better bound

In our case, we cannot directly apply the result with and as is not guaranteed to be Lipschitz at . But, along the lines of the proof of Theorem 1 in Borovkov and Novikov, (2005), the above result can be modified as follows:

Lemma 4.

For a non-decreasing function which is Lipschitz with constant on , and a function such that for and ,

| (26) |

Theorem 4.

Proof.

We first split again the error by

| (28) |

The second term can be estimated from Lemma 2, (24). Again, we shall then proceed by induction. We have already shown that for according to Theorem 1.

Consider . Assume we have shown that for . We want to derive such that and where all are bounded independent of . First, consider an intermediate point , then

with the Lipschitz constant of , and thus

| (29) |

Now we show that . Consider

and . Then,

| (30) |

To estimate the first term, we can write

where we have used in the second line that since for , hitting after does not affect the difference. For , . Then, using Theorem 1,

For the second term in (30), is Lipschitz on with and we can apply (26). Thus,

| (31) | |||

| (32) |

using (29). Moreover, by (24) and (32), (28) can be written as

where .

As a result, we have the following inequality for ,

Hence, because of (27), is bounded independent of , and by induction we get the result.

∎

3.3 Monte Carlo simulation of discretized process

In this section, we prove the convergence in probability of

in Algorithm 1 to as . We note that we cannot directly apply the law of large numbers, as the summands are dependent through . However, we see below that the dependence diminishes (i.e., the covariance goes to zero) as , which easily gives convergence, albeit without a Central Limit Theorem-type error estimate or a rate for the variance.

First, we formulate an auxiliary lemma.

Lemma 5.

Consider . Assume for all

| (33) |

Then,

| (34) | |||||

| (35) |

The proof is given in Appendix B. Now we can deduce the convergence instantly.

3.4 Brownian bridge convergence improvement

In this section, we prove Theorem 3, which ascertains the uniform convergence (in ) of to at the improved rate.

Proof of Theorem 3.

We shall proceed by induction. Assume we have shown that for all with some , and we want to estimate . First, we have

since . Now consider

where is the density of .

∎

The proof of Theorem 3 indicates that the order is limited by the behaviour of for small . The next result shows that a locally refined time mesh achieves convergence order 1 for all .

Corollary 1.

Consider a non-uniform time mesh for with . Then, there exists , independent of , such that

Proof.

The proof follows by repeating all the steps of the proof of Theorem 3. ∎

4 Numerical experiments

In this section, we demonstrate that the proven convergence orders in the timestep of , , and 1 for the different methods are indeed sharp in the case of regular solutions; that the empirical variance of -sample estimators is ; and that the method also converges experimentally in the presence of blow-up. To show this, we study three test cases with varying regularity of the initial data and of the loss function.

4.1 Lipschitz initial data and no blow-up

In our first experiment, we choose such that , which guarantees that the density decays exponentially near zero. We take in our experiments, and pick the parameters in (1) to be , . The solution is found to be continuous.

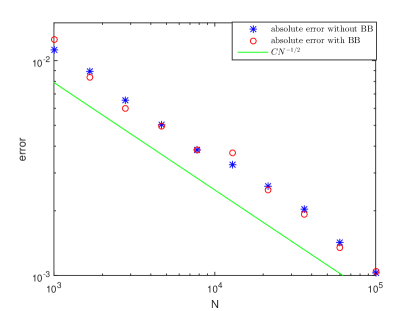

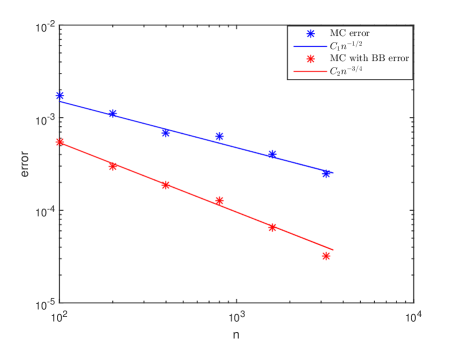

We perform numerical simulations using Algorithms 1 and 2 with particles and different time meshes varying from to points. To estimate the error, we consider the difference between the solutions with and timesteps, respectively, computed with the same paths. The results, presented in Figure 2, agree with the theory: for Algorithm 1, we get the convergence rate , and for Algorithm 2, the rate is , because the initial distribution is regular enough around , i.e. in (1).

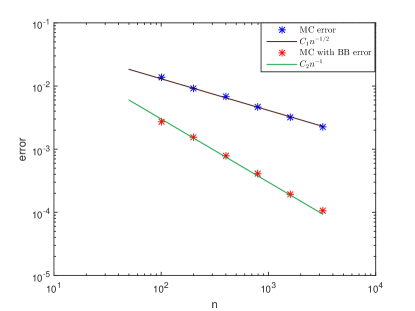

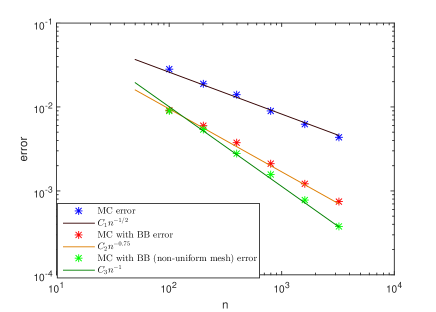

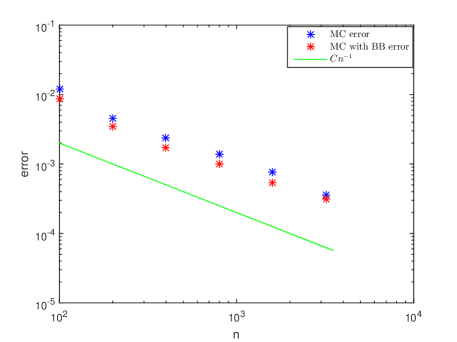

We also investigate the convergence rate of to and to empirically. In order to compute the benchmark solution, we used particles. From the results we conclude that both Algorithm 1 and 2 have the convergence rate in .

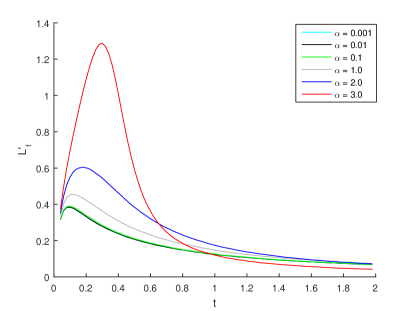

To illustrate the dependence on the parameter , we include plots for and for different values of . We evaluate numerically using a central finite difference approximation. In order to reduce the Monte Carlo noise, we increase to and reduce to .

4.2 Hölder initial data and no blow-up

In another example we again consider and , but choose , such that we have that for and some . We choose . The solution is again found to be continuous.

We perform numerical simulations using Algorithm 1, and Algorithm 2 on uniform and non-uniform meshes varying from to points and with particles. The results are presented in Figure 4. As predicted by the theory, for Algorithm 1 we get the convergence rate , for Algorithm 2 on uniform meshes rate , and for Algorithm 2 on non-uniform meshes rate .

As in the previous example, we also investigate the convergence rate in empirically. These results also confirm convergence rate in for both Algorithms 1 and 2. In Figure 5 we present the dependence of and on the parameter . As in the previous example, we use and .

4.3 Hölder initial data and blow-up

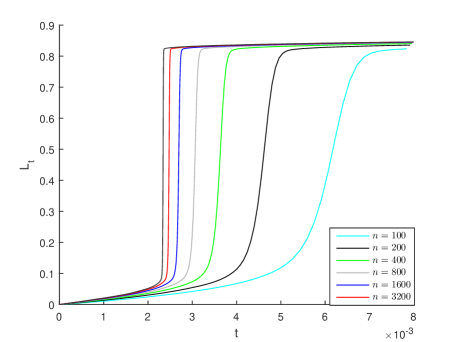

In our third example, we illustrate possible jumps arising in the solution for sufficiently large values of . We consider , and choose as in the previous example, . Note that the blow-up happens already for very small due to the interplay of the mass close to 0 for and the relatively large .

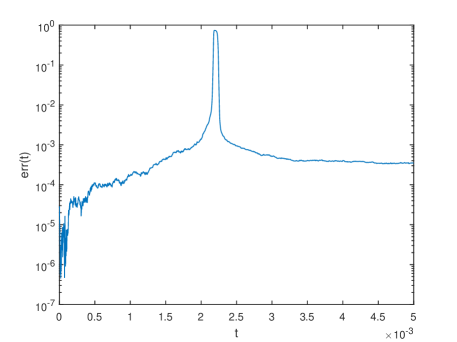

With the lack of convergence theory for discontinuous , we apply Algorithms 1 and 2, and empirically estimate the error. In Figure 6 (a) we show computed using Algorithm 1 for different ; in Figure 6 (b) the numerical error as a function of for specific ; and in Figure 7 (a) and (b) we estimate the convergence rate for different .

Figure 6 (a) shows that a fairly fine resolution is needed to capture the discontinuity and its timing, but that all meshes predict the size of the jump well. This is further illustrated in Figure 6 (b), which shows the build-up of the error before the jump, the lack of uniform convergence due to the displacement of the jump on different meshes, and the relatively constant error after the jump.

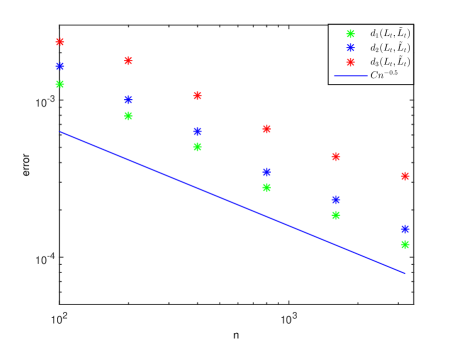

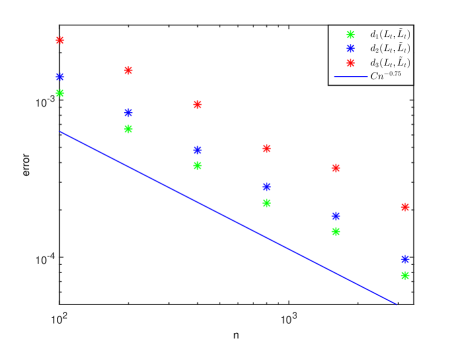

In Figure 7 (a) we estimate the convergence order at , i.e. before the jump. By regression, we get for Algorithm 1 and for Algorithm 2, where the 95% confidence interval is in brackets, which agrees with the theory for continuous . In Figure 7 (b), for the error at , i.e. after the jump, we get for Algorithm 1 and for Algorithm 2. The faster convergence may result from the almost constancy of the losses after the jump.

To get an overall picture of the accuracy, we suggest the following metrics to measure the ‘‘closeness’’ of the computed solutions to :

-

1.

. This is practically computed by numerical integration.

-

2.

, where and are the jump times for and , respectively. They are approximated by the points with the steepest gradient .

-

3.

, where and are the corresponding inverse functions. The inverse functions are found by the chebfun toolbox (Driscoll et al., (2014)), which automatically splits functions into intervals of continuity.

In the absence of the exact , we use again the difference between quantities computed using and points, for the same Monte Carlo paths, as a proxy.

We present the results in Figure 8 (a) for Algorithm 1 and in Figure 8 (b) for Algorithm 2. For metric 1 we have convergence rate and , for metric 2 we have and , and for metric 3 we have and for Algorithms 1 and 2, respectively, where the 95% confidence interval are in brackets. We observe that the convergence rate for Algorithm 1 is somewhat better than , while for Algorithm 2 it is around for all three metrics.

5 Conclusions

We have developed particle methods with explicit timestepping for the simulation of (1)-(3). Convergence with a rate up to 1 in the timestep is shown under a condition on the model parameters and time horizon, when the loss function is differentiable. Experimentally, the method also converges in the blow-up regime, and the variance of estimators is inversely proportional to the number of samples.

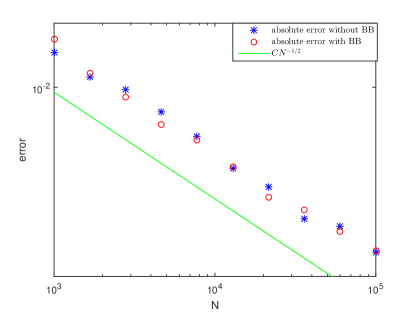

This opens up several theoretical and practical questions. The efficiency of the method could be significantly improved by a simple application of multilevel simulation (Szpruch et al., (2017); Ricketson, (2015)). If the variance can be shown to behave on the finer levels as suggested by the numerical tests, combined with the proven result on the time stepping bias, the computational complexity for root-mean-square error would be brought down to , from as observed presently ( from the number of samples and from the number of timesteps).

For the particular system (1)–(3), it is conceivable to apply a particle method without time stepping of the form

where and are i.i.d. copies of and , and , , is the order statistic of the hitting times of zero. Then, for , conditional on the information up to , the law of for those particles which have not yet hit, is identical to that of independent standard Brownian motions with constant drift . So if we simulate those independent hitting times of for each and then take the smallest one to be , this inductive construction satisfies the correct law. The complexity is then , and combined with the observed variance of , this gives a complexity of for error . Another disadvantage is that this method with exact sampling is restricted to the constant parameter case, while the time stepping scheme can easily be extended to variable coefficients.

Theoretically, one would like guaranteed convergence also in the blow-up regime. This requires the choice of an appropriate metric – the Skorokhod distance may be suitable, considering the analysis in Delarue et al., 2015b and the tests in Section 4.3. It also requires verification that the limit in the case of blow-up is a so-called ‘‘physical solution’’ as defined in Hambly et al., (2018); Nadtochiy and Shkolnikov, (2017); Delarue et al., 2015b , which on the one hand results from a specific sequential realisation of the losses in the case of blow-up (Nadtochiy and Shkolnikov, (2017); Delarue et al., 2015b ), and on the other hand is the right-continuous solution with the smallest jump size (Hambly et al., (2018)).

Lastly, it would be interesting to investigate the extension to the models in Nadtochiy and Shkolnikov, (2017) and Delarue et al., 2015b in more detail.

Acknowledgements

We thank Alex Lipton, Andreas Søjmark, and Sean Ledger for useful comments and interesting discussion. We assume full responsibility for any remaining mistakes.

Appendix A Proof of Lemmas in Section 3.1

A.1 Proof of Lemma 1

A.2 Proof of Lemma 2

Proof of Lemma 2.

Consider the first term. Using Markov’s inequality

for any .

Using Lemma 1,

thus

For the second term

where and are the CDF and PDF of the process . We also note that is bounded according to Lemma 3.

Combining both terms, we have

Minimising the right-hand side over , we find with . As a result, choosing , we get that for any , there exists , such that

For (24), we use identical steps and the corresponding estimates in Lemma 1 and Lemma 3 for instead of .

∎

A.3 Proof of Lemma 3

Proof of Lemma 3.

We can rewrite , where . As and are independent, using convolution, we have

Using the fact that and (7), we have

| (36) |

where is the CDF of . It is obvious that for all . Indeed, .

Since , for all the function is concave and, using Jensen’s inequality for the proper probability measure on ,

| (37) |

where as . Since is non-decreasing, inserting ,

| (38) | ||||

By simple integration of the density of the running minimum of Brownian motion,

| (39) |

and, taking , we get from (38) for ,

and, similarly, for ,

Combing the last two equations, we finally get (25) for .

Using similar arguments for and , using and , respectively, we get the analogous estimates for and , and hence (25). ∎

Appendix B Proof of Lemma 5, Section 3.3

Proof of Lemma 5.

We can write

and estimate

| (40) |

We evaluate left- and right-hand side of the last equation separately. We start with the right-hand side, and define for brevity . Consider some .Then,

where is the pdf of , which is bounded according to Lemma 3.

Using (33) and properties of convergence in probability, we have

Thus, the last term goes to with . Considering , we get

| (41) |

Similar, denote by , then

where is the pdf of , which is bounded according to Lemma 3. Thus,

| (42) |

Consider now the variance

| (43) |

The covariance can be estimated by

| (44) |

As above and because of exchangeability, for the second term of the last expression,

| (45) |

Now we consider the first term of (44). Similar to above, it can be estimated by

| (46) |

Similar to (41) and (42), one can show that

Hence,

| (47) |

Thus, combining (45) and (47), we get

Considering the first term of (43), it is easy to see that each variance is bounded by 1. As a result, we have

∎

References

- Antonelli et al., (2002) Antonelli, F., Kohatsu-Higa, A., et al. (2002). Rate of convergence of a particle method to the solution of the McKean–Vlasov equation. The Annals of Applied Probability, 12(2):423–476.

- Asmussen et al., (1995) Asmussen, S., Glynn, P., and Pitman, J. (1995). Discretization error in simulation of one-dimensional reflecting Brownian motion. The Annals of Applied Probability, 5(4):875–896.

- Borovkov and Novikov, (2005) Borovkov, K. and Novikov, A. (2005). Explicit bounds for approximation rates of boundary crossing probabilities for the Wiener process. Journal of Applied Probability, 42(1):82–92.

- Bossy and Talay, (1997) Bossy, M. and Talay, D. (1997). A stochastic particle method for the McKean-Vlasov and the Burgers equation. Mathematics of Computation, 66(217):157–192.

- Cáceres et al., (2011) Cáceres, M. J., Carrillo, J. A., and Perthame, B. (2011). Analysis of nonlinear noisy integrate & fire neuron models: blow-up and steady states. The Journal of Mathematical Neuroscience, 1(1):7.

- Carrillo et al., (2013) Carrillo, J. A., González, M. d. M., Gualdani, M. P., and Schonbek, M. E. (2013). Classical solutions for a nonlinear Fokker–Planck equation arising in computational neuroscience. Communications in Partial Differential Equations, 38(3):385–409.

- (7) Delarue, F., Inglis, J., Rubenthaler, S., and Tanré, E. (2015a). Global solvability of a networked integrate-and-fire model of McKean–Vlasov type. The Annals of Applied Probability, 25(4):2096–2133.

- (8) Delarue, F., Inglis, J., Rubenthaler, S., and Tanré, E. (2015b). Particle systems with a singular mean-field self-excitation. Application to neuronal networks. Stochastic Processes and their Applications, 125(6):2451–2492.

- Driscoll et al., (2014) Driscoll, T. A., Hale, N., and Trefethen, L. N. (2014). Chebfun guide. Pafnuty Publ.

- Glasserman, (2013) Glasserman, P. (2013). Monte Carlo methods in financial engineering, volume 53. Springer Science & Business Media.

- Hambly et al., (2018) Hambly, B., Ledger, S., and Sojmark, A. (2018). A McKean–Vlasov equation with positive feedback and blow-ups. arXiv preprint arXiv:1801.07703.

- Lipton, (2016) Lipton, A. (2016). Modern monetary circuit theory, stability of interconnected banking network, and balance sheet optimization for individual banks. International Journal of Theoretical and Applied Finance, 19(06). doi: 10.1142/S0219024916500345.

- Nadtochiy and Shkolnikov, (2017) Nadtochiy, S. and Shkolnikov, M. (2017). Particle systems with singular interaction through hitting times: application in systemic risk modeling. arXiv preprint arXiv:1705.00691.

- Reis et al., (2018) Reis, G. d., Smith, G., and Tankov, P. (2018). Importance sampling for McKean-Vlasov SDEs. arXiv preprint arXiv:1803.09320.

- Ricketson, (2015) Ricketson, L. (2015). A multilevel Monte Carlo method for a class of McKean–Vlasov processes. arXiv preprint arXiv:1508.02299.

- Szpruch et al., (2017) Szpruch, L., Tan, S., and Tse, A. (2017). Iterative particle approximation for McKean–Vlasov SDEs with application to Multilevel Monte Carlo estimation. arXiv preprint arXiv:1706.00907.