Distributed Statistical Inference for Massive Data

Abstract

This paper considers distributed statistical inference for a general type of statistics that encompasses the U-statistics and the M-estimators in the context of massive data where the data can be stored at multiple platforms at different locations. In order to facilitate effective computation and to avoid expensive data communication among different platforms, we formulate distributed statistics which can be computed over smaller data blocks. The statistical properties of the distributed statistics are investigated in terms of the mean square error of estimation and their asymptotic distributions with respect to the number of data blocks. In addition, we propose two distributed bootstrap algorithms which are computationally effective and are able to capture the underlying distribution of the distributed statistics. Numerical simulation and real data applications of the proposed approaches are provided to demonstrate the empirical performance.

Keywords: Distributed bootstrap, distributed statistics, massive data, pseudo-distributed bootstrap

1 Introduction

Massive data with rapidly increasing size are generated in many fields of scientific studies that create needs for statistical analyzes. Not only the size of the data is an issue, but also a fact that the data are often stored in multiple locations, where each contains a subset of the data which can be massive in its own right. This implies that a statistical procedure that involves the entire data has to involve data communication between different storage facilities, which can slow down the computation. For statistical analyzes involving massive data, the computational and data storage implications of a statistical procedure should be taken into consideration in additional to the usual criteria of statistical inference.

Two methods have been developed to deal with the challenges with massive data. One is the so-called “split-and-conquer” (SaC) method considered in Zhang, Duchi and Wainwright (2013), Chen and Xie (2014) and Battey et al. (2015); and the other is the resampling-based methods advocated by Kleiner et al. (2014) and Sengupta, Volgushev and Shao (2016). From the estimation point of view, the SaC first partitions the entire data into blocks with smaller sizes, performs the estimation on each data block and then aggregate the estimators from these blocks to form the final estimator. SaC has been used in different settings under the massive data scenario, for instance the M-estimation by Zhang, Duchi and Wainwright (2013), the generalized linear models by Chen and Xie (2014), see also Huang and Huo (2015), Battey et al. (2015) and Lee et al. (2015).

The other method involves making the bootstrap procedure adaptive to the massive data setting in order to obtain standard errors or confidence intervals for statistical inference. As the bootstrap resampling of the entire dataset is not feasible due to its being computationally too expensive, Kleiner et al. (2014) introduced the bag of little bootstrap (BLB) that incorporates subsampling and the out of bootstrap to assess the quality of estimators for various inference purposes. Sengupta, Volgushev and Shao (2016) proposed the subsampled double bootstrap (SDB) method that combines the BLB with a fast double bootstrap (Davidson and MacKinnon, 2002; Chang and Hall, 2015) that has computational advantages over the BLB. However, both the BLB and SDB have some limitations. Firstly, the core idea of the BLB and SDB is to construct subsets of small size from the entire dataset, and then resample these small subsets to obtain resamples. The computational efficiency of the BLB and SDB heavily rely on that the estimator of interest admits a weighted subsample representation (Kleiner et al., 2014), which is usually satisfied for linear statistics. Secondly, the SDB requires resampling from the entire dataset, which can be computationally expensive to accomplish when the data are stored in different locations.

In this paper, we consider distributed statistical inference for a class of symmetric statistics (Lai and Wang, 1993), which are more general than linear statistics. We first carry out the SaC step for a distributed formulation of the statistics for better computational efficiency. Estimation efficiency and distribution approximation for the distributed statistics are studied relative to the full sample formulation. We propose computationally efficient bootstrap algorithms to approximate the distribution of the distributed statistics: a distributed bootstrap (DB) and a pseudo-distributed bootstrap (PDB) . Both strains of the bootstrap method can be implemented distributively and are suitable for parallel and distributed computing platforms, while maintaining sufficient level of statistical efficiency and accuracy in the inference.

The paper is organized as follows. Aspects of symmetric statistics are introduced in Section . The distributed statistics are formulated in Section together with its statistical efficiency. Section concerns computationally complexity and the selection of the number of data blocks. In Section , asymptotic distributions of the distributed statistics are established for both non-degenerate and degenerate cases. Bootstrap procedures designed to approximate the distribution of the distributed statistics are discussed in Section . Section provides simulation verification to the theoretical results. An application on the airline on-time performance data is presented in Section . Proofs, more technical details and some simulation results are reported in the supplementary materials.

2 Symmetric statistics

Let be a sequence of independent random vectors taking values in a measurable space with a common distribution . A statistic for a parameter , that is invariant under any data permutations, admits a general non-linear form

| (2.1) |

where and are known functions, and is a remainder term of the expansion that constitutes the first three terms on the right side.

The statistic encompasses some commonly used statistics, for example, the U- and L-statistics, and the smoothed functions of the sample means. The form (2.1) was introduced in Lai and Wang (1993) while Edgeworth expansions for were studied in Jing and Wang (2010). In these two papers, it is assumed that is non-lattice distributed and is of smaller order of the quadratic term involving . For instance, can be a U-statistic with and terms to be the first and second order terms in the Hoeffding’s decomposition (Hoeffding, 1948; Serfling, 1980). In this case, and . Here, we relax the conditions that is non-lattice and is of a small order in Lai and Wang (1993) and Jing and Wang (2010) such that includes more types of statistics. The linear term involving can vanish, for instance in the case of the degenerate U-statistics. The M-estimators are included in (2.1) with having certain order of magnitude depending on the forms of the score functions. When the score function of the M-estimator is twice differentiable and its second derivative is Lipschitz continuous, the M-estimator can be expressed in the form of (2.1) with an explicit and the remainder term . However, when the score function is not smooth enough, the M-estimator may not be expanded to the second-order term. In this situation, we can absorb the quadratic term into , which is often of order (He and Shao, 1996). We assume the following regarding and .

Condition C1.

The functions and , depending on , are known measurable functions of and , satisfying and , and is symmetric in and such that and .

3 Distributed statistics

To improve the computation of , we divide the full dataset into data blocks. Let be the -th data block of size , for . Such division is naturally available when is stored over storage facilities. Otherwise, the blocks can be obtained by random sampling.

Condition C2.

There exist finite positive constants and such that , and can be either finite or diverging to infinity as long as it satisfies that as .

Condition C2 implies that are of the same order and the number of data blocks should be of a smaller order of .

For , let be a version of , but is based on the -th data block such that , where is the remainder term specific to the -th block.

By averaging the block-wise statistics, we arrive at the distributed statistic

| (3.1) |

which can be expressed as

| (3.2) |

where . It is clear that the first two terms of and are the same. The difference between them occurs at the terms involving and the remainders.

The distributed statistics for non-degenerate U-statistics were considered in Lin and Xi (2010). The authors suggested the “aggregated U-statistic” which is just when is a U-statistic. They showed that the aggregated U-statistic is asymptotically equivalent to the corresponding U-statistic. In this paper, we consider a more general class of statistics with different assumptions on , and without the limitation of non-degenerate statistics. In addition, we study distributed bootstrap strategies to approximate the distribution of , that was not considered in Lin and Xi (2010).

To facilitate analyzes on the statistical efficiency of , we assume the following.

Condition C3.

If and for some , and , then for some and , for .

Condition C3 prescribes a divisible property of in its first two moments with respect to the sample size . That is, inherits the properties of ’s first two moments with substituted by .

We first present results concerning to provide benchmarks for our analyzes.

Proposition 1.

Under Condition C1, if for some , , and , then and

The bias of is determined by the expectation of . In the variance expression, we keep the term involving the covariance between and as it may not be negligible in a general case. For the special case when is uncorrelated with , which is the case of U-statistics, the covariance term vanishes.

According to Proposition 1, the mean square error (MSE) of is

| (3.3) |

The bias and variance of is given in the following theorem.

If is an unbiased estimator of , namely , is also unbiased so that . Thus the distributed approach can preserve the unbiasedness of the statistics. For the biased case of , as is under Condition C2, the bias is enlarged by a factor of for relative to that of . This indicates that the data blocking accumulates the biases from each data block, leading to an increase in the bias of the distributed statistic. For the more common case that the bias of is at the order of , the bias of is of order .

For the variance, there is an increase by a factor of in the term that involves due to the data blocking. For the covariance term in and , under the conditions of Theorem 3.1, as and , by Cauchy-Schwarz inequality. Similarly, . Thus, an increase by a factor of occurs in the covariance term. Moreover, the covariance term in is always a smaller order of as . However, it may be a larger order of . For the case of , the variance inflation happens in the second order term without altering the leading order term. For the degenerate case of , but , the variance inflation appears in the leading order via a factor of .

Combining the bias and variance from Theorem 3.1, we have

| (3.4) |

To compare the MSEs of and , we first consider the non-degenerate case of . By comparing (3) with (3), if

| (3.5) |

then , and and share the same leading order term . We note that is an increasing function of , ranging from () to (). For the case of when has a bias of order , the number of blocks is required to be at a smaller order of such that maintains the same leading MSE as . The increase in the variance due to the data blocking is reflected in the MSE, although it is of the second order in the non-degenerate case.

If is degenerate ( but ), besides the increase in the bias, an increase by a factor of occurs in the variance of . This indicates that the distributed statistic can not maintain the same efficiency as in the degenerate case.

In summary, we see that the data blocking increases the bias and variance of the distributed statistic . This may be viewed as a price paid to gain computational scalability for massive data. Despite this, there is room to select properly to minimize the increases. For instance, by choosing to satisfy (3.5), the increase in the bias and variance are confined in the second order for the non-degenerate case.

4 Computing issues and selection of

The rationale for carrying out the distributed formulation is in reducing time for computing and data communication in the context of massive data while maintaining certain level of estimation accuracy given a computation budget. Suppose that the computational complexity of calculating is at the order of with , then computing only needs , that is steps. So calculating is a factor of faster than computing directly. Similar statement can be made from Theorem 5 in Chen and Xie (2014).

In addition to saving computing cost, the distributed approach requires less memory space. Suppose the memory needed for computing is for some . Then for , the requirement on the size of memory is at the order of . This means a memory saving by a factor of when , or when .

Now we use the U-statistics as an example to demonstrate the computational advantages of the distributed approach. Consider a U-statistic of degree with a symmetric kernel function such that

| (4.1) |

where , ,

and is the remainder term satisfying and under the condition that . The representation in (4) is the Hoeffding’s decomposition of U-statistics (Hoeffding, 1948, 1961).

If steps are needed to calculate the function, then the computing cost of is , which is at the order of . Assume that the entire dataset of size is divided evenly into subsets with each of size . Denote as the U-statistic using data in the -th block. Notice that the number of computing steps for is , which is of order . Thus, the computing steps of the distributed U-statistic is a factor less than that of the full sample based .

Now we consider the problem of selecting . As discussed earlier, using a larger reduces the computing burden and makes computation more feasible. However, the mean square error of is an increasing function of , which indicates a loss in the estimation accuracy for using a large . Hence, in practice, the selection of should be chosen as a compromise between the statistical accuracy and the computational cost and feasibility.

Suppose that is a hard requirement to meet the memory and storage capacity. As the mean square error of is increasing with respect to , so the minimum mean square error we can get is , which is achieved at . In practice, we may have a fixed time budget. In this situation, denote the computing cost as and the fixed time budget as . It is reasonable to assume that the computing cost is a decreasing function of . Denote , then the optimal is . This suggests selecting the smallest that meet the limits of memory, storage and computation budget, to attain the best statistical efficiency possible.

5 Asymptotic distribution of

We investigate the asymptotic distribution of under different assumptions on and , and compare it with that of . First, we have the following theorem on the asymptotic distribution of when .

Theorem 5.1.

Under Condition C1 and , if , then as ,

It is noted that the requirement that can be met by many statistics and one sufficient assumption for it is .

When discussing the statistical efficiency of in Section 3, the conditions on the first two moments of the remainder term are assumed in Theorem 3.1 in order to get a better insight into the MSE of . However, for some statistics in the form of , the orders of ’s first two moments can be hard to achieve. Instead, is known to be at a certain stochastic order. Thus, we have an alternative assumption to Condition C3 on and .

Condition C3′.

If for some , then for .

The following theorem concerns the asymptotic distribution of .

Theorem 5.2.

(i) If and for some and , then under Condition C3, as , .

(ii) If for some , then under Condition C3′, as , .

The condition indicates that, under Conditions C1, C2, C3 (or C3′) and , the smaller order is, the higher can be, so that can attain the same asymptotic normal distribution as . Thus, the requirement on is determined by the order of . It is noted that the above condition on coincides with the requirement on in (3.5) in order that and have the same leading order term.

We need the following assumption on to attain the uniform convergence of the distribution of to that of , which is commonly used in obtaining the uniform convergence, see for instance in Petrov (1998).

Condition C4.

There exists a positive constant such that .

Theorem 5.3.

It is noted that the uniform convergence requires for , which is slightly stronger than assumed in Theorem 5.2.

To sum up the results for the case of , we note that as long as the number of data blocks does not diverges too fast, can maintain the same estimation efficiency as and the same asymptotic normal distribution. Thus, is a good substitute of as an estimator of for the non-degenerate case.

For the degenerate case of , an increase by a factor of in the variance has been shown in Theorem 3.1. This means that can not achieve the same efficiency as . It is noticed that when and ,

| (5.1) |

Before studying the asymptotic distributions of and , we introduce notations used in the spectral decomposition of . As is symmetric in its two arguments, when it has finite second moment, there exist a sequence of eigenvalues and eigenfunctions such that admits expansion (Dunford and Schwartz, 1963; Serfling, 1980):

| (5.2) |

in the sense that . Here satisfy , for all and

Theorem 5.4.

Under Condition C1, and , if , then as , where are independent random variables.

From (5), can be viewed as a weighted average of independent random variables, the asymptotic behavior of degenerate is given in the following theorem.

Theorem 5.5.

(i) if is finite and , then as , where are independent random variables;

(ii) if , there exists a constant such that , and , then as .

Here, we get two different limiting distributions for depending on whether is finite or diverging. This is easy to interpret as is an average of independent random variables. Thus, with the data divided into increasingly many data blocks, the distribution of is asymptotically normal. When is finite, the condition is a directly result of , . When diverges to infinity, if for some , and , then under Condition C3 which prescribes the divisibility of with respect to the sample size , and . Thus, in order for , it requires that is This is a slower growth rate for comparing to the non-degenerate case. If with , which means that is not achievable in this case. Similarly, if for some , then under Condition C3′, it is necessary such that is satisfied.

It is of interest to mention that when , the normalizing factor is of order , which is of smaller order of , the normalizing factor for . This reflects the variance increase of as revealed in Theorem 3.1.

6 Bootstrap procedures

An important remaining issue is how to approximate the distribution of under different conditions on and . This motivates our consideration of the bootstrap method, which has been a powerful tool for statistical analyzes, especially in approximating distributions, see Efron (1979); Hall (1992); Shao and Tu (1995). In this section, we will first investigate the properties of the conventional bootstrap when applied to the distributed statistics, followed by reviews of the bag of little bootstrap (BLB) and the subsampled double bootstrap (SDB). Then, we propose two distributed bootstrap algorithms which are particularly designed for the distributed statistics under the massive data scenario.

We first outline the entire sample bootstrap for the distributed statistics to offer a benchmark for our discussions in this section, despite the method is not computationally feasible for massive data. To approximate the distribution of , this version of the bootstrap generates resampled data blocks from the entire sample for constructing resampled distributed statistics. By recognizing the distributed character of , the entire-sample bootstrap has the following resampling procedure.

Step 1. For , randomly sample a data subset from with replacement and compute the corresponding statistic .

Step 2. Obtain the distributed statistic on the resampled data subsets

This two-step procedure ensures that the resampled subsets are conditionally independently and identically distributed from , the empirical distribution of . Repeat Steps 1 to 2 times, bootstrap distributed statistics, denoted as , are obtained. The empirical distribution of is used to approximate that of , where is the analog of under .

The drawback of the entire-sample bootstrap is in requiring a rather large data communication expenditure should the data are stored in multiple locations. Furthermore, has the same computational complexity as . Thus, we do not pursue this version of the bootstrap algorithm further in this paper.

6.1 BLB and SDB

The bag of little bootstrap (BLB) (Kleiner et al., 2014) and the subsampled double bootstrap (SDB) (Sengupta, Volgushev and Shao, 2016) are two existing resampling-based methods for massive data inference. Suppose is an estimator of based on the sample . Let be an inferential quantity concerning , and be its sampling distribution, which is unknown due to its dependence on the underlying distribution . One is interested in a quantity on certain aspect of . For example, if , may be the expectation of representing the bias of . Similarly, can be the mean square error of or a confidence interval of .

For massive data, calculating and its resampled version with the entire-sample bootstrap can be computationally expensive. Kleiner et al. (2014) proposed BLB to obtain computationally “cheaper” estimates of . To avoid calculating the full sample and , BLB first generates data subsets of smaller sizes, say subsets of size (often for some ) by sampling from the original dataset without replacement (these subsets can be predefined disjoint subsets of ). Denote the -th data subset as , its empirical distribution as , and as the estimator of , which is relatively cheap to compute due to its smaller size.

The second step of BLB is in constructing inflated resample of full size by repeated sampling with replacement from the smaller data subset . The inflated resample can be efficiently produced via generating resampling weights for elements of from the multinomial distribution as elaborated in Kleiner et al. (2014).

Let be the empirical distribution of the inflated resample . BLB calculates the estimator and for B inflated resamples of , namely for . Then, the empirical distribution of , denoted as , is used to estimate and to obtain for the -th data subset . Finally, the BLB estimator of is . Kleiner et al. (2014) proved that under some conditions, converges to in probability as .

Sengupta, Volgushev and Shao (2016) proposed the SDB that combines the idea of the BLB and a fast double bootstrap (Davidson and MacKinnon, 2002; Chang and Hall, 2015). SDB first generates a large number of random subsets of size from the original full sample, which is similar to BLB’s first step. However, the SDB selects subsets from the entire dataset by sampling with replacement, while the BLB can sample subsets without replacement in the creation of the small subsets . Hence in the SDB, the sampled subsets are denoted as with to highlight the resampling features, whereas in BLB the symbol is not used in as it may be viewed as true subsets of the original sample. For each , SDB generates only one inflated resample of the full size using the same approach as in the BLB. So for each , only one is obtained, where and , and are the empirical distributions of and , respectively. The empirical distribution of , denoted as , is used to estimate and obtain , the SDB’s estimate of .

It is noted that SDB only generates one double bootstrap resample for each and the estimate of is based on the over different subsets . Thus, SDB requires . In contrast, the number of subsets in the BLB can be either finite or diverging. In addition, SDB requires resampling from the entire dataset to get the random subsets , while the BLB can choose predefined disjoint subsets . Thus, for massive datasets stored in different locations, SDB requires more data communications as a trade-off for having only one double bootstrap resample.

The attraction of BLB and SDB is in avoiding resampling from the original full data sample but rather from smaller size subsamples, which is facilitated by obtaining the sampling weights from the multinomial distribution. Indeed, both BLB and SDB have computational advantages when the underlying estimator can be calculated via a weighted empirical function representation, which is the case for the general M-estimators or other liner-type statistics. In those cases, the amount of computation for is scaled in rather than . However, for non-linear estimators like the symmetric statistics considered in this paper, the computational advantages of BLB and SDB via a weighted empirical function representation may not be available.

As noted in Sengupta, Volgushev and Shao (2016), BLB uses a small number of subsets (i.e. small ) but a large number of resamples for each subset (i.e. large ), which may lead to only a small portion of the full dataset being covered. Another issue is that using too many resamples for each subset can increase the computational burden too. For the SDB, it can not be implemented distributively as it requires to conduct the first level resampling from the entire data. We propose two versions of a distributed bootstrap method that overcomes these issues.

6.2 Distributed bootstrap

Our aim is in approximating the distribution of by avoiding resampling from the entire dataset. By recognizing the distributive nature of the statistics, we consider resampling within each data subset.

Suppose the entire data are divided into subsets: . For , let be the empirical distribution of , and be i.i.d. samples drawn from . Repeat this procedure times, one obtains resampled data subsets . Compute the corresponding statistic for each resampled subset. Averaging them over the subsets leads to

for . Let be the analogy of under . Define , then the empirical distribution of is used to approximate the distribution of . The algorithm is outlined in Table S2 in the supplementary material.

We call the above the distributed bootstrap (DB) because the resampling is fulfilled within each data subset without the sample inflation as BLB. For each data subset in each iteration, we can calculate and locally avoiding data communication between different data subsets. These make the approach suitable for the massive data.

To explore the theoretical properties of the distributed bootstrap, we need some notations and assumptions. Specifically, is assumed to admit

| (6.1) |

where and are analogues of and under . Then can be written as

| (6.2) |

where and . Here, and are the empirical versions of and , which we regulate in the following condition. Let first denote as the support of .

Condition C5.

For , and satisfy , is symmetric in and , for any . In addition, as , and

Condition C5 indicates that for with distribution , and for any . Moreover, it requires that and are uniformally consistent to and . The next theorem, inspired by Hall (1986, 1988) and Lai and Wang (1993), establishes the consistency of the distributed bootstrap for the non-degenerated case of .

Theorem 6.1.

Theorem 6.1 gives theoretical support for the distributed bootstrap for the non-degenerate case. For specific statistics, we need to check if satisfies the conditions in Theorem 6.1. Section B.1 in the supplementary material provides details checking on the conditions for the U-statistics. The distributed bootstrap works for both finite and infinite , as long as is of an appropriate order of . The requirement on is hidden in the assumption that

For a distributed U-statistic of degree two as discussed in the supplementary material, that is equivalent to satisfying and , for . Thus, the consistency of the distributed bootstrap for the distributed U-statistics is ensured as long as for a positive .

Theorem 6.1 ensures that the distributed bootstrap can be utilized in a broad range by combining it with the continuous mapping theorem and delta method, for instance in the variance estimation and confidence intervals. Specifically, let be the sample variance of . Then is a consistent estimator of , which is a consistent estimator of . In addition, denote as the lower quantile of the empirical distribution of , then an equal-tail two-sided confidence interval for with level can be constructed as

For degenerate statistics, the distributed bootstrap can be adapted by replacing with for each data block. Similar to Theorem 5.5, the consistency of the distributed bootstrap for the degenerate case needs to be discussed separately for being finite or . When is fixed, the conditional distribution of is consistent to the distribution of if . When and , that conditional distribution of can approximate the distribution of can be established. In the next subsection, we will propose a pseudo-distributed bootstrap that works for both degenerate and non-degenerate cases.

6.3 Pseudo-distributed bootstrap

Although the distributed bootstrap lead to substantial computational saving due to its distributive nature, it is still computationally involved when the size of the data is massive since the distributed statistics need to be re-calculated for each bootstrap replication. To further reduce the computational burden, we consider another way to approximate the distribution of under the case of diverging .

The idea comes from the expression

which indicates that is the average of independent random variables. Hence, when is large, approximating the distribution of is similar to that of the sample mean of independent but not necessary identically distributed samples. This leads us to propose directly resampling rather than the original data.

We first consider the non-degenerate case of . As different subsets of data may have different sample sizes, we need to scale before the resampling. Let

and be the empirical distribution of . To estimate the distribution of , we draw independent resamples for from . Let , then the empirical distribution of is used to estimate the distribution of . We call this algorithm the pseudo-distributed bootstrap (PDB) and its procedure is summarized in Table S3 in the supplementary material.

The PDB is the conventional bootstrap carried out on the scaled subset-wise statistics , which are independent but not necessary identically distributed. The bootstrap procedures under non-i.i.d. models has been studied in Liu (1988). The following theorem establishes the asymptotic properties of the PDB for the non-degenerate case.

Theorem 6.2.

Under the conditions of Theorem 5.3. Suppose that is an i.i.d. sample from and . If , , and as , then with probability , as ,

Theorem 6.2 shows that under moderate conditions on , and the moments of , the PDB is asymptotic consistent when . As we have mentioned earlier, the subset based statistics need to be re-scaled first by their respective sample sizes. The condition ensures that the size of each subset should not be too different from each other.

Compared to the distributed bootstrap, besides computing saving, an appealing property of the PDB is that it does not require the bootstrap distributed statistics admitting form (6.2) as assumed in Theorem 6.1. This makes the PDB more versatile and easier to verify, although it does requires that diverges.

Another advantage of the PDB is that it can be applied for the degenerate case. Indeed, when but , is still an average of independent random variables. One only needs to rescaled with a different scaling factor such that for , followed by the same procedures as those for the non-degenerate case. The next theorem gives theoretical support for the PDB under degeneracy.

Theorem 6.3.

Compared to the case of , stronger conditions are needed for degenerate case. This is reflected firstly in that needs to be strictly larger than such that can be dominated by the quadratic term involving . Secondly, is assumed to be the same for all subsets and is required to have a slower growth rate to . Lastly, a stronger moment condition is needed for . That its applicable for both non-degenerate and degenerate statistics reveals the versatility of the PDB.

Before concluding this section, we compare the distributed bootstrap (DB), the PDB, BLB and SDB in approximating the distribution of . First, we compare them regarding their computational complexity. To make our discussion more straightforward, we assume that the entire data are divided evenly into blocks such that .

| Methods | Computing Complexity | Distributed or Not | Requirement on |

|---|---|---|---|

| DB | distributed | finite or diverging | |

| PDB | distributed | diverging | |

| BLB | distributed | finite or diverging | |

| SDB | not distributed | finite or diverging |

Table 3 reports the computational complexity of the four methods together with specification on their distributive nature and the requirement on the total number of subsets . Suppose that the time cost for calculating the statistic in (2.1) on a sample of size is , then the computing time of BLB with resamples and subsets is , where is the size of the smaller subset . For SDB with random subsets of size , its computational complexity is . If we generate resamples in the distributed bootstrap, its computational cost would be for the distributed bootstrap. In addition, the PDB requires time to fulfill its implementation with pseudo resamples. Thus, the PDB is the fastest among the four methods. The distributed bootstrap and the SDB have similar computational cost if is close to . However, the SDB can not be implemented distributively, while the other three methods can. For the BLB, its computational complexity depends on both and . Furthermore, only the PDB requires diverges, while the other three work for both being finite or diverging.

7 Simulation studies

In this section, we report simulation studies to evaluate the performance of the proposed distributed approaches and the associated bootstrap algorithms. In particular, we compare the proposed bootstrap methods to the BLB and SDB approaches. The statistic we considered was the Gini’s mean difference

It is an unbiased estimator of a dispersion parameter which measures the variability of a distribution. In addition, is a U-statistic of degree two and can be expanded to the form (2.1). Suppose the entire data are divided into data blocks with the -th having size . For each subset, denote as the Gini’s mean difference obtained from the -th data block, then the distributed Gini’s mean difference estimator is .

When , we can use the jackknife (Efron and Stein, 1981) to estimate , denoted as where which can be written in the form of (2.1) with the quadratic term absorbed in the remainder term (Callaert and Veraverbeke, 1981). As an estimator of , has a bias of order . Because , the MSE of is of order .

Three distributions of were experimented: (I) ; (II) and (III) . The true values of and can be calculated algebraically for the first two distributions. For the Poisson distribution, they can be well approximated (Lomnicki, 1952). We chose the sample size . For the sake of convenience, we randomly divided the entire dataset into blocks of equal size. The number of blocks . All the simulation results were based on replications. All the simulation experiments were conducted in R with a single Intel(R) Core(TM) i7 4790K @4.0 GHz processor.

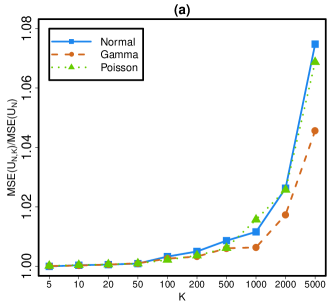

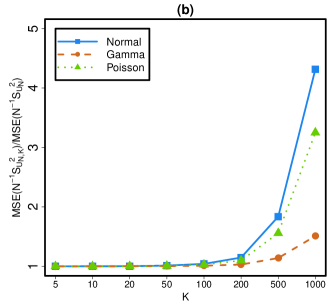

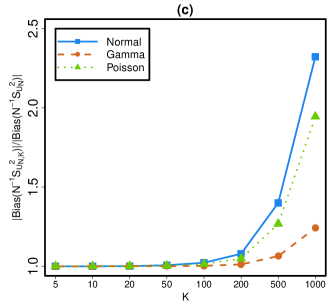

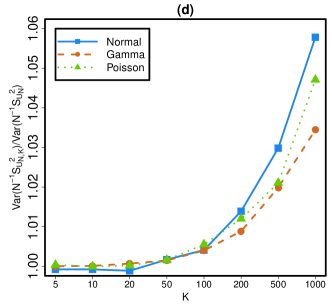

Figure 1 summarizes the empirical performance of and for the three distributions relative to those of and based on the full sample, respectively. The figure presents the relative MSE of , and the relative MSE, bias and variance of with respective to their full sample counterparts.

Figure 1 shows that the relative increased quite slowly as was increased before being too large. This indicated that the distributed estimator was almost as good as for relatively small , which coincided with our theoretical results that is unbiased and the variance increase occurs only in the second order term. From the plot we can also see that even was as large as , the relative increases in the MSEs were all less than for all three distributions. Thus, was a reasonable substitute of as an estimator of in these situations. Figure 1 shows that the MSEs of was comparable to that of for relatively small . However, increased rapidly when was lager than , which confirmed the theoretical result that increases at the order of when diverges. In addition, Figures 1 and 1 depict the variations of the absolute bias and variance of , which both contribute to its mean square error. By comparing Figure 1 to Figure 1, we see that the increment in the mean square error of was mainly due to the increase in the bias when was relatively large.

Now we turn to the performance of the distributed bootstrap (DB) and the pseudo-distributed bootstrap (PDB), and compare them with the BLB and SDB. In the simulations, we constructed the equal-tailed confidence intervals for based on with . For each simulated dataset and , each method was allowed to run for seconds in order to mimic the fixed time budget scenario. For the BLB, we fixed as in Kleiner et al. (2014) and Sengupta, Volgushev and Shao (2016); and the -th subset had size . For the SDB, the size of was also . Table 2 summarized the number of iterations completed for each method within the second budget for different . The table shows that the pseudo-distributed bootstrap (PDB) was the fastest that had the most completed iterations among the four methods. The BLB was the slowest. For , the BLB could not finish one iteration with the time budget of seconds. The distributed bootstrap (DP) and SDB had similar performance. However, it is worth mentioning that these results did not take the time expenditure in data communication among different data blocks into account.

| K | ||||||

|---|---|---|---|---|---|---|

| DB | ||||||

| PDB | ||||||

| BLB | ||||||

| SDB | ||||||

We next evaluate the inference offered by these four bootstrap methods under a fixed time budget of 10 seconds. We tried to run simulation replications which produced the coverage probabilities and widths of the confidence intervals for in Table 3 for the Gaussian scenario, while the results for Gamma and Poisson distributions can be found in Tables S4 and S5 in the supplementary material. Table 3 shows that there was some under-coverage for the confidence intervals by all four methods for relatively small . For , the smallest number of data blocks considered in the simulation, the reason for the DP and SDB not having good coverage performance was that they completed too few bootstrap iterations to ensure good accuracy. As the pseudo-distributed bootstrap (PDB) is based on the assumption that diverges, the coverage probability was not good when even it can complete enough iterations in seconds. As the number of subsets increased, and the computational burden was alleviated, the performances of the distributed bootstrap (DP), PDB and SDB all got better with comparable to coverage and width. The best coverage appeared to be reached at . BLB could not produce any result for as it could not complete a single bootstrap run. For larger , the coverage probabilities of the BLB were slightly less comparable to the other three methods. It is interesting to see that the PDB was able to take advantage of its speedy computation to complete more runs of the bootstrap resampling that led to its producing very comparable coverage levels and width of the confidence intervals.

| K | ||||||

|---|---|---|---|---|---|---|

| DB | ||||||

| PDB | ||||||

| BLB | NA | |||||

| (NA) | ||||||

| SDB | ||||||

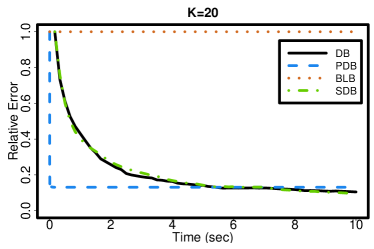

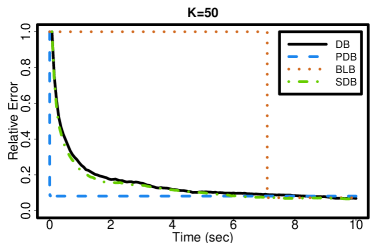

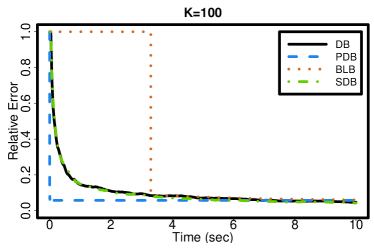

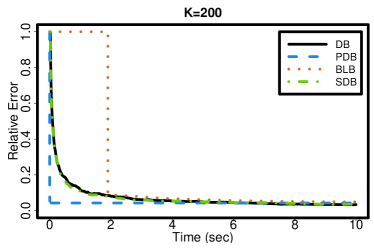

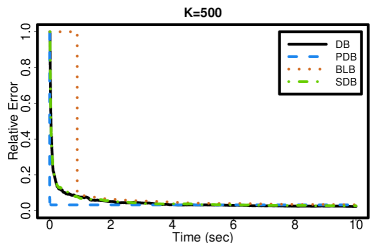

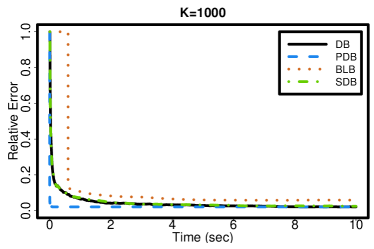

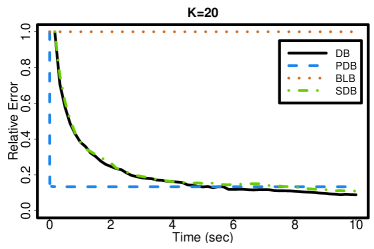

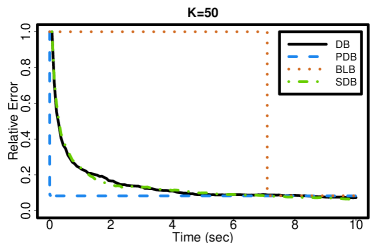

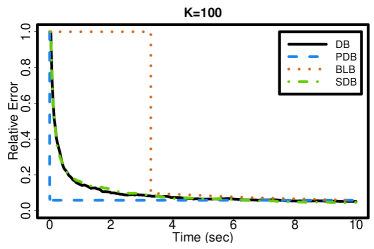

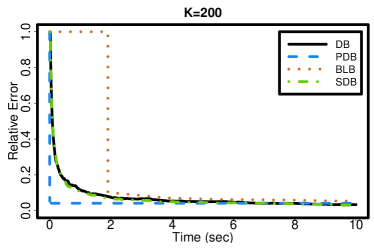

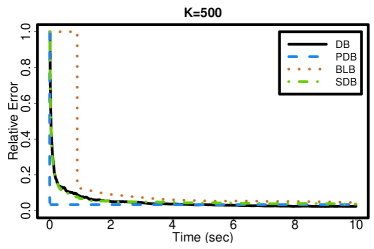

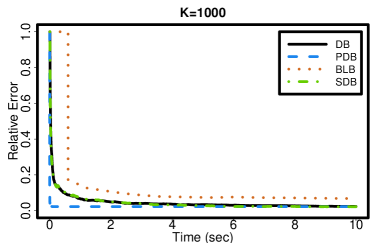

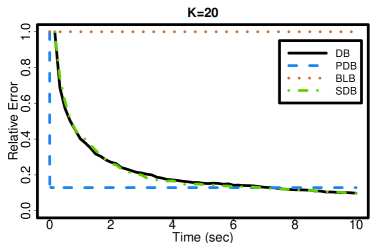

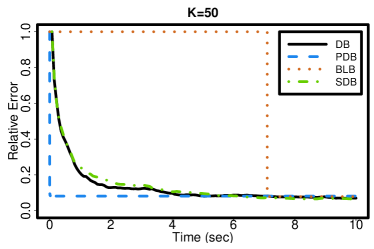

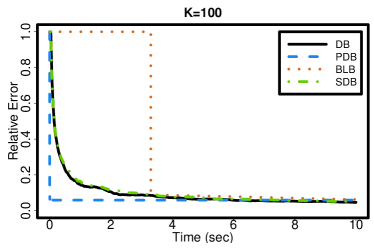

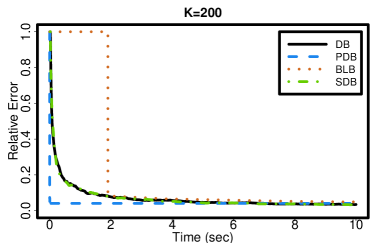

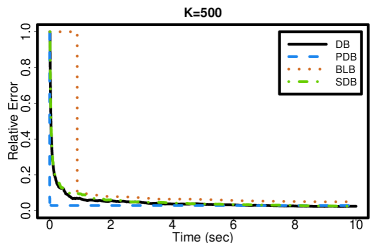

Next we evaluate the relative errors of the confidence interval widths for each method. Let be the true width, be the width of the confidence interval by one of the four methods, and the relative error is . The exact width was obtained by simulations for each distribution. The relative errors were averaged over the simulation replications. Follow the strategy in Sengupta, Volgushev and Shao (2016), these four methods are compared with respect to the time evolution of relative errors under the fixed budget of 10 seconds. This was to explore which method can produce more precise result given a fixed time budget. For the BLB and SDB, one iteration means the completion of estimation procedure for one subset. The relative error was initially assigned to be before the first iteration was completed.

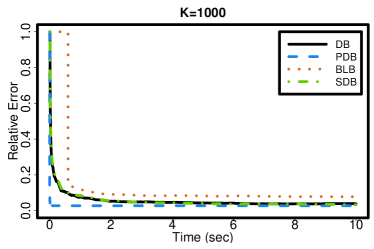

Figure 2 displays the evolution of the relative errors in the widths of the confidence intervals with respect to time for the four methods with different number block size for Gaussian data. We note that the pseudo-distributed bootstrap (PDB) was the fastest method to converge for all . BLB’s relative error was severely affected by its rather limited completion rates of the bootstrap iteration when and . When , the distributed bootstrap (DB) and SDB had smaller relative errors than the PDB after seconds. This is expected as the convergence rate of the PDB relies on a larger . However, as was increased to larger than 200, the relative errors of the PDB quickly decreased to an acceptable rate and became comparable to those of the DB and SDB towards the 10 seconds. DB and SDB had similar performance and they could produce stable results with a sufficient time budget. Results for Gamma and Poisson scenarios were similar and are reported in Figures S2 and S3 in the supplementary material.

In conclusion, with a small time budget, the pseudo-distributed bootstrap (PDB) had better performance than the other three resampling strategies. When is relatively large, PDB has advantage in computing and can produce reasonable estimators. However, the convergence of PDB is limited by the order of . With a sufficient time budget, the distributed bootstrap (DB) and SDB can work for a wide range of and obtain better estimator than the pseudo-distributed bootstrap (PDB) in some situation.

8 Real data analysis

In this section, we analyze an airline on-time performance data to illustrate the proposed distributed inference for massive data. The data are available from the Bureau of Transportation Statistics website (https://www.bts.gov/), which consist of the arrival and departure details for passenger flights within the USA in . We are interested in the arrival delay (ARR_DELAY) variable which is the difference in minutes between the scheduled and the actual arrival times. After removing missing values, which corresponded to the canceled flights, there are flight entries in the dataset.

Each sample point consists of features that are potentially related to the arrival delay. These features along with descriptions of their meanings are listed in Table S6 in the supplementary material. It is expected that departure delay (DEP_DELAY) tends to result in late arrival. Hence, the variable DEP_DELAY should be highly correlated with ARR_DELAY. The variable DIF_ELAPS is the difference between actual (ACT_ELAPS) and scheduled elapsed time (CRS_ELAPS) in the computer reservation system (CRS). Thus, DEP_DELAY and DIF_ELAPS together determine the ARR_DELAY. One question is, how much of the arrival delay is due to the departure delay or the difference between actual and scheduled elapsed time? In addition, TAXI_OUT records the time between departure from the gate and wheels off, while TAXI_IN is the time differences between wheels down and arrival at the gate. DISTANCE provides the flight distance, while MONTH, DAY_OF_WEEK and DAY_OF_MONTH provide month and date information of each flight.

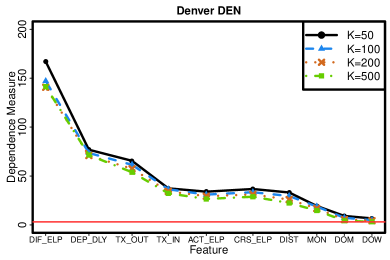

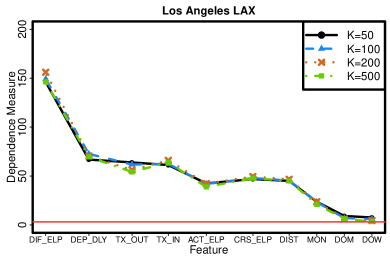

Our goal is to find out which variables were more dependent with ARR_DELAY and to characterize the dependence with respect to different airports. We only considered the airports with at least flight arrivals in . This led to four airports: ATL (Atlanta International Airport), ORD (Chicago O’Hare), DEN (Denver) and LAX (Los Angeles), which had , , , flight arrivals in 2016, respectively.

We use the distance covariance introduced in Székely, Rizzo and Bakirov (2007) to quantify the dependence. Suppose and are two random vectors having finite first moments and taking values in and , respectively. The population distance covariance between and is

where , and are the characteristic functions of , and , respectively, and is a weight function with , is the Gamma function. It is clear that equals zero if and only if and are independent. Suppose is a sample from , where for . Define and for . Then, the empirical distance covariance (Székely and Rizzo, 2014) is

which is a U-statistic of degree and an unbiased estimator of .

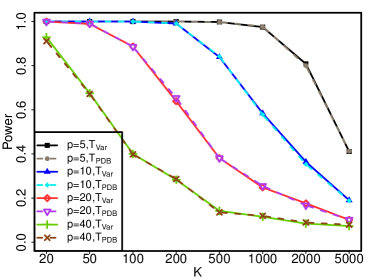

Because of the sizes of these datasets, the distance covariance encounters heavy computational burden. We utilized the distributed version of the distance covariance, see Section B.3 in the supplementary material for details. We divided the data of each airport randomly into subsets of equal size where was chosen in a set . As discussed in the supplementary material, for two random vectors and , is asymptotic normal with unit variance regardless and are independent or not. Here, is the distributed distance covariance based on subsets, and is a consistent estimator of . So, can be used to measure the dependence between and . The larger is, the more dependence between and is. Also we can compare with the critical values from the standard normal distribution to test for the significance of the dependence between and .

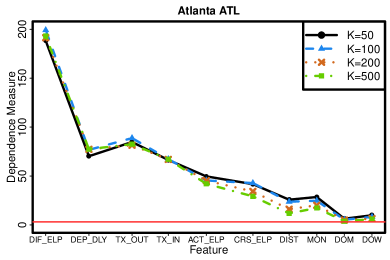

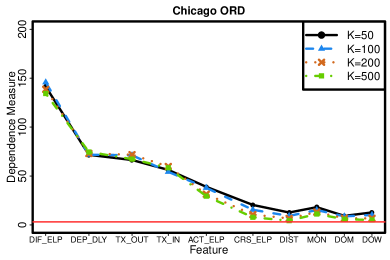

Figure 3 reports the standardized dependence measures between the arrival delay and each of the feature variables for the four airports with the block size . It shows that all test statistics were above the critical value lines, which indicated significant dependence between the arrival delay and the ten features for the four airports. Here, we deliberately use a rather small critical value to account for any multiplicity in the testing. Figure 3 clearly shows that the amount of dependence as quantified by for being the ten features were very consistent across different values. The largest variation with respect to was observed for the CRS_ELP and Distance for Atlanta.

This implied that the distributed inference would produce stable results with respect to different . This is attractive as using a larger benefits the computing.

As expected, DIF_ELAPS and DEP_DELAY were the most dependent with the arrival delay for all airports. The only exception was Atlanta, where TAXI_OUT was more dependent with the arrival delay than DEP_DELAY. Besides DIF_ELAPS and DEP_DELAY, TAXI_OUT and TAXI_IN both had strong dependence on the arrival delay than the other six features for the four airports. The DAY_OF_MONTH and DAY_OF_WEEK were the least dependent with the arrival delay. For the feature DISTANCE, the result varied with different airports. For DEN and LAX, the dependence between DISTANCE and the arrival delay was stronger than those at ATL and ORD. It is observed that different data block size had less bearings on the distance measure for almost all the features at all four airports, except for the Distance and CRS_ELP features at ATL, ORD and DEN.

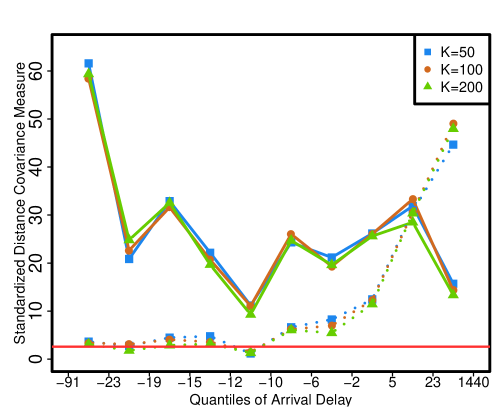

We carried out further analysis to give a clearer vision of the impact of DIF_ELAPS and DEP_DELAY on the arrival delay. Take Atlanta ATL as an illustration, we split the data of ATL into equal sized subsets according to the quantiles of its arrival delay. Figure 4 plots the standardized distance dependence between ARR_DELAY and DIF_ELAPS and DEP_DELAY, respectively, for different quantile ranges of ARR_DELAY with the subset size . For each subset with ARR_DELAY within each quantile range, the standardized dependence measures were plotted with respect to . Figure 4 shows that the results were consistent for different in all cases, which was assuring for the distributed inference.

9 Conclusion

The paper has investigated distributed inferences for massive data with a focus on a general symmetric statistics given in (2.1), which is designed to make the computation scalable. We have provided detailed analyzes on the statistical properties of the distributed statistics as well as their asymptotic distributions when the number of subsets is either fixed or diverging and the statistics is non-degenerate or otherwise. Two bootstrap methods are proposed and studied theoretically, which are showed to have aspects of computational advantages over the BLB and SDB in the context of massive data.

An important practical issue for the distributed inference is the choice of the number of blocks . As showed in our analysis, an increasing would decrease the computational cost, but lead to a loss in statistical efficiency. This topic has been touched in Section 4, where storage and memory requirement are considered. However, it is still an issue on how to select in practice that balances the computing time and statistical efficiency. Instead of considering a fixed time budget, another way of consideration is to minimize computing time subject to attaining certain statistical efficiency. This is similar as the sample size determination problem. We leave its analysis in future study. It is also of interest to study higher order correctness and convergence rates of our proposed distributed approaches.

References

- Arcones and Giné (1992) Arcones, M. A. and Giné, E. (1992). On the bootstrap of U and V statistics. Ann. Statist. 20, 655-674.

- Battey et al. (2015) Battey, H., Fan, J., Liu, H., Lu, J. and Zhu, Z. (2015). Distributed estimation and inference with statistical guarantees. arXiv preprint arXiv:1509.05457.

- Chang and Hall (2015) Chang, J. and Hall, P. (2015). Double-bootstrap methods that use a single double-bootstrap simulation. Boimetrika 102(1), 203-214.

- Chen and Xie (2014) Chen, X. and Xie, M. (2014). A split-and-conquer approach for analysis of extraordinarily large data. Statistica Sinica, 24, 1655-1684.

- Davidson and MacKinnon (2002) Davidson, R. and MacKinnon, J. G. (2002). Fast double bootstrap tests of nonnested linear regression models. Econometric Reviews, 21(4), 419-429.

- Dunford and Schwartz (1963) Dunford, N. and Schwartz, J. T. (1963). Linear Operators. Wiley-Interscience, New York.

- Efron (1979) Efron, B. (1979). Bootstrap methods: another look at the jackknife. Ann. Statist. 7, 1-16.

- Efron and Stein (1981) Efron, B. and Stein, C. (1981). The jackknife estimate of variance. Ann. Statist. 9, 586-596.

- Hall (1986) Hall, P. (1986). On the bootstrap and confidence intervals. Ann. Statist. 14, 1431-1452.

- Hall (1988) Hall, P. (1988). Theoretical comparison of bootstrap confidence intervals. Ann. Statist. 16, 927-953.

- Hall (1992) Hall, P. (1992). The Bootstrap and Edgeworth Expansion. Springer-Verlag, New York.

- He and Shao (1996) He, X. and Shao, Q.-M. (1996). A general Bahadur representation of M-estimators and its application to linear regression with nonstochastic designs. Ann. Statist. 24, 2608-2630.

- Hoeffding (1948) Hoeffding, W. (1948). A class of statistics with asymptotically normal distribution. Ann. Math. Statist. 19, 293-325.

- Hoeffding (1961) Hoeffding, W. (1961). The strong law of large numbers for U-statistics. University of North Carolina Institute of Statistics Mimeo Series, No. 203.

- Huang and Huo (2015) Huang, C. and Huo, X. (2015). A Distributed One-Step Estimator. arXiv preprint arXiv:1511.01443.

- Jing and Wang (2010) Jing, B.-Y. and Wang, Q. (2010). A unified approach to Edgeworth expansions for a general class of statistics. Statistica Sinica, 20, 613-636.

- Kleiner et al. (2014) Kleiner, A., Talwalkar, A., Sarkar, P. and Jordan, M. I. (2014). A scalable bootstrap for massive data. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76, 795-816.

- Lai and Wang (1993) Lai, T. L. and Wang, J. Q. (1993). Edgeworth expansions for symmetric statistics with applications to bootstrap methods. Statistica Sinica, 3, 517-542.

- Lee et al. (2015) Lee, J. D., Liu, Q., Sun, Y. and Taylor, J. E. (2015). Communication-efficient sparse regression: a one-shot approach. arXiv preprint arXiv:1503.04337.

- Lin and Xi (2010) Lin, N. and Xi, R. (2010). Fast surrogates of U-statistics. Computational Statistics and Data Analysis, 54, 16-24.

- Liu (1988) Liu, R. Y. (1988). Bootstrap procedures under some non-i.i.d. models. Ann. Stat. 4, 1696-1708.

- Lomnicki (1952) Lomnicki, Z. A. (1952). The standard error of Gini’s mean difference. The Annals of Mathematical Statistics, 23, 635-637.

- Petrov (1998) Petrov, V. V. (1998). Limit Theorems of Probability Theory: Sequences of Independent Random Variables. Oxford University Press Inc., New York.

- Sengupta, Volgushev and Shao (2016) Sengupta, S., Volgushev, S. and Shao, X. (2016). A subsampled double bootstrap for massive data. Journal of the American Statistical Association, 111 1222-1232.

- Serfling (1980) Serfling R. J. (1980). Approximation Theorems of Mathematical Statistics. John Wiley Sons, Inc.

- Shao and Tu (1995) Shao, J. and Tu, D. (1995). The Jackknife and Bootstrap. Springer-Verlag New York, Inc.

- Székely and Rizzo (2014) Szkely and G. J., Rizzo, M. L. (2014). Partial distance correlation with methods for dissimilarities. Ann. Stat., 42 2382-2412.

- Székely, Rizzo and Bakirov (2007) Szkely, G. J., Rizzo, M. L. and Bakirov N. K. (2007). Measuring and testing dependence by correlation of distance. Ann. Stat., 35 2769-2794.

- Zhang, Duchi and Wainwright (2013) Zhang, Y., Duchi, J. C. and Wainwright, M. J. (2013). Communication-efficient algorithms for statistical optimization. Journal of Machine Learning Research, 14, 3321-3363.

Supplementary material for “Distributed Statistical Inference for Massive Data”

Song Xi Chen and Liuhua Peng

The supplementary materials including technical details, proofs of main theorems and additional simulation studies, are organized as follows. Section A presents important lemmas and proofs of theorems in the paper. Section B introduces distributed distance covariance along with other technical discussions. More simulation results are reported in Section C.

A Proofs

In this section, we present the proofs of main theorems in this paper. Before that, we give several lemmas that will be frequently used. The first lemma is a generalization of Esseen’s inequality which we may refer to Theorem 5.7 in Petrov (1998).

Lemma 1.

Let be independent random variables. For , and for some positive . Then

where and is a positive constant.

The second lemma is a modified version of Marcinkiewicz-Zygmund strong law of larger numbers (SLLN) and its proof can be found in Liu (1988).

Lemma 2.

Let be independent random variables with for some positive , , and . Then as ,

almost surely, where if and otherwise.

A.1 Proof of Theorem 5.3

A.2 Proof of Theorem 5.5

Proof.

(i) When is finite, the result can be easily obtained by the independence between each subset and the classic limit theorem for degenerate U-statistics (Serfling, 1980).

(ii) When , without loss of generality, assume . Denote where . Under the condition that , it is sufficient to prove that converges to as , here . Rewrite

where satisfies and for . As are independent, it is enough to check the Lindeberg condition for . Note that , then for every ,

The next-to-last line is from the moment inequalities of U-statistics (Koroljuk and Borovskich, 1994) and is a positive constant. Thus we finish the proof of Theorem 5.5. ∎

A.3 Proof of Theorem 6.1

Proof.

According to the proof of Theorem 5.3, under the conditions in Theorem 5.3, we have

thus, it is sufficient to show that under the conditions assumed in the theorem

| (A.1) |

We proceed to show that is bounded in probability for . Note that

for some positive constant . By the condition that and the strong law of large numbers, we have for . Similarly, we can show that in probability.

Thus, under the condition , by carrying out similar procedures in the proof of Theorem 5.3, we can prove (A.1) which leads to the result that

In addition,

∎

A.4 Proof of Theorem 6.2

Proof.

Let . Denote

and for , then

Denote , then , are i.i.d. from . Since , and , we have . This immediately results in

with probability for some satisfies (Lemma 2). Define

then where . Denote and

then implies that

almost surely. According to Lemma 1,

almost surely as . It has been shown in the proof of Theorem 5.3 that

Combine this with the fact that with probability 1, we complete the proof of this corollary.

∎

A.5 Proof of Theorem 6.3

Proof.

Use similar techniques as in the proof of Theorem 6.2, let , denote and for , then and .

Under the conditions that and , we obtain , which in turn implies that

where .

Denote , then , are i.i.d. from . As , this immediately results in

with probability and satisfies (Lemma 2). Define

then . Denote , then

which convergence to almost surely. According to Lemma 1,

almost surely as , thus we finish the proof of Theorem 6.3.

∎

B Technical details

B.1 U-statistics as an example

We show that the conditions in Theorem 6.1 are satisfied by U-statistics. Suppose is a U-statistic of degree with a symmetric kernel function , that is,

| (B.1) |

where , , , and is the remainder term. Obviously, is in the form of (2.1). Under the condition that , it can be shown that and meet Condition C1 with and satisfies and (Hoeffding, 1948; Serfling, 1980). Let be the corresponding U-statistic obtained from the -th data block, , then the remainder terms of satisfy Condition C3 with . Thus the distributed U-statistic is

where satisfies and under Condition C2. If and for some positive and , then as ,

Now we consider the distributed bootstrap version of the distributed U-statistic. For , let be an i.i.d. sample from and , then

where ,

, and . Thus, is in the form of (6.2) with and remainder term . Represent and in term of and , we have

By simple algebra, it is checked that , is symmetric in and , and for any . Furthermore, according to the condition and , and are easily verifiable by law of large numbers.

B.2 Discussions on the convergence rate of the pseudo-distributed bootstrap

Under the conditions in Theorem 6.2, we assume that are of small order such that they can be omitted in the following discussion. Assume is non-lattice, and , by Theorem 5.18 of Petrov (1998),

uniformly in where . Mentioned that

this clearly implies

According to the proof of Theorem 5.3,

it follows that

This result indicates that the convergence rate of the pseudo-distributed bootstrap is at the order of .

B.3 Distributed distance covariance

Distance covariance, introduced in Székely, Rizzo and Bakirov (2007), is a method that measures and tests dependence between two random vectors. In this section, we introduce the distributed distance covariance and its usage in testing independence for massive data.

Suppose and are two random vectors having finite first moments and taking values in and , respectively. The population distance covariance between and is

where , and are the characteristic functions of , and , respectively, and is a weight function with . It is clear that equals zero if and only if and are independent. This property makes the distance variance more versatile in detecting dependence than the classic Pearson’s correlation. If ,

where and are independent copies of .

Suppose is a sample from , where for . Define and for . Then the -centered empirical distance covariance (Székely and Rizzo, 2014; Yao, Zhang and Shao, 2017) is

which is a U-statistic of degree and an unbiased estimator of .

The computing complexity and memory requirement of the distance covariance are both at the order of , limit its usage when is large. The proposed distributed version of the distance covariance has much to offer under the massive data scenario. Suppose the entire data are divided into sub-samples with the -th subset of size for . Denote as the empirical distance covariance based on . Then the distributed distance covariance is defined as

It is easy to see that is also an unbiased estimator of , and it enjoys computational advantage over . Specially, the memory requirement of computing is only , which makes more feasible when the size of the data is huge. Now we consider testing independence between and using the distance covariance. That is to test the hypothesis

| (B.2) |

Under the null hypothesis that and are independent, if , the empirical distance covariance is a degenerate U-statistic that has the following representation (Yao, Zhang and Shao, 2017):

where with and , and is the remainder term satisfies and . It is easy to verify that under the null hypothesis, and .

If is used to test (B.2), we need to obtain a reference distribution for using the bootstrap (Arcones and Giné, 1992) or random permutation (Székely, Rizzo and Bakirov, 2007) on the entire dataset. For massive dataset, computing itself is a big issue. Moreover, the bootstrap and random permutation on the entire dataset are both computationally expensive as we need to re-calculate the statistic for each resample or permuted sample. Thus we consider using the distributed distance covariance . According to Theorem 5.5, we have the following asymptotic result concerning .

Corollary B.3.

Under Condition C2, assume there exists a constant such that , then under the null hypothesis that and are independent,

We need to estimate in order to implement the test. Mentioned that , and , an distributed version of unbiased estimator for under the null is

The consistency of the variance estimator is established in the next theorem.

Theorem B.3.

Under the conditions in Corollary B.3, if , then,

Proof.

Under the null hypothesis, , thus it is sufficient to show that as . Mentioned that

Since and are both U-statistics of degree , under the condition that , and , these immediately lead to and the proof is complete.

∎

By Slutsky’s theorem, converges to standard normal distribution under the null. Thus, a consistent test with nominal significant level reject if

| (B.3) |

where is the -th upper-quantile of the standard normal distribution.

Remark B.1.

When and are dependent and is non-degenerate, still converges to a normal distribution under certain moment conditions (Theorem 5.2). That is,

as . In addition, we can use the pseudo-distributed bootstrap to approximate the distribution of and get a consistent estimator of when .

Next we consider the special case when each data block has the same size . Define

According to the proof of Theorem 6.3, is a consistent estimator of under the conditions in Corollary B.3. Thus is asymptotic standard normal under the null. Therefore, a consistent test with nominal significant level reject if

| (B.4) |

Remark B.2.

When each data block has the same size, even when is non-degenerate, is still a consistent estimator of if (proof of Theorem 6.2). Thus is asymptotic normal with unit variance regardless is degenerate or not. Therefore, we can use to measure the dependence between and for massive data. The larger is, the more dependent and are.

C Simulations on distributed distance covariance

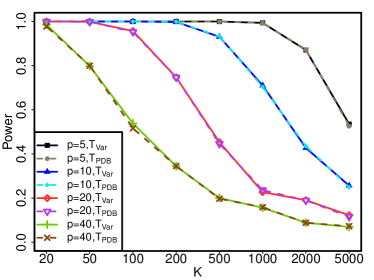

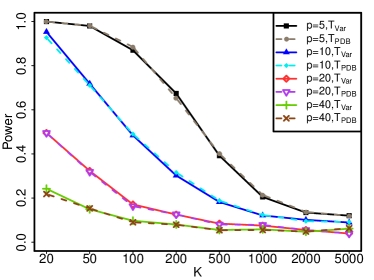

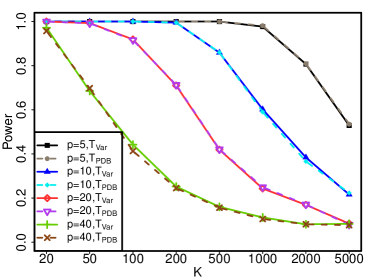

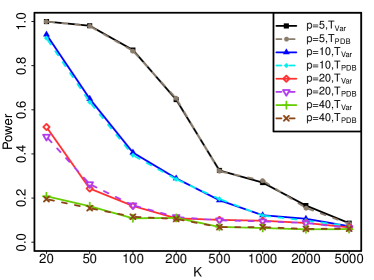

The distributed version of distance covariance and its usage in testing independence between two multivariate random vectors has been studied in Section B.3. In this section, we investigate the performance of the distributed distance covariance in testing independence by numerical studies. All simulation results in this section are based on iterations with the nominal significant level at . The sample size is fixed at and the number of data blocks is selected in the set .

For the null hypothesis, we generated i.i.d. samples and independently from distributions and , respectively. Three different combinations of and were considered: (I) and are both , where is the -dimensional identity matrix; (II) is , for , its components are i.i.d. from student- distribution with degrees of freedom; (III) For both and , their components are i.i.d. from student- distribution with degrees of freedom. The dimension was chosen as , , and for each scenario.

Table S1 reports the empirical sizes of and , which stand for the testing procedures based on (B.3) and (B.4), respectively. Table S1 shows that the empirical sizes of both methods are close to the nominal level for all combinations of and under all three scenarios. Thus, these two test procedures both have good control of Type-I error for a wide range of . In addition, the performance of these two methods is very comparable to each other. However, for relatively large , has slightly better control of the empirical sizes than .

| scenario I | ||||||||

| scenario II | ||||||||

| scenario III | ||||||||

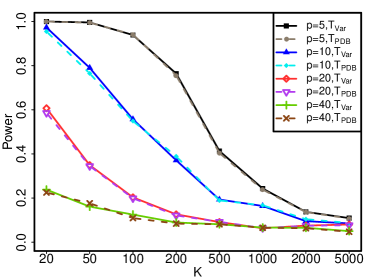

To compare the powers of these two tests, we generated i.i.d. samples , , and the same three different combinations of and were considered as before. For and under each scenario, we simulated for and , were considered. Under these setups, and are dependent with each other. Figure S1 gives the empirical powers of and .

From Figure S1, it is clear that the empirical powers of these two tests decrease as the dimension increases. In addition, as the number of data blocks increases, the empirical powers of the tests also decrease. This is due to the increase in the variance of when increases. This is the price we need to pay for using the distributed distance covariance. The computing time and memory requirement can be reduced by increasing the number of data blocks, however, this will result in the power loss of the tests.

C.1 Additional tables and figures

| Input: data ; , number of subsets; , subset sizes; |

|---|

| , number of Monte Carlo iterations; , function deriving statistic |

| Output: an estimate of the distribution of |

| For to do |

| compute |

| for to do |

| generate resample from |

| compute |

| end |

| End |

| Compute |

| For to do |

| compute |

| compute |

| End |

| Input: data ; , number of subsets; , subset sizes; |

|---|

| , number of Monte Carlo iterations; , function deriving statistic |

| Output: an estimate of the distribution of |

| For to do |

| compute |

| compute |

| End |

| Compute |

| For to do |

| generate resample from |

| compute |

| End |

| For to do |

| compute |

| End |

| K | ||||||

|---|---|---|---|---|---|---|

| PDB | ||||||

| DB | ||||||

| BLB | NA | |||||

| (NA) | ||||||

| SDB | ||||||

| K | ||||||

|---|---|---|---|---|---|---|

| PDB | ||||||

| DB | ||||||

| BLB | NA | |||||

| (NA) | ||||||

| SDB | ||||||

| Feature Variable | Description |

|---|---|

| DIF_ELAPS (DIF_ELP) | Difference in minutes between actual and scheduled elapsed |

| time. () | |

| DEP_DELAY (DEP_DLY) | Difference in minutes between scheduled and actual |

| departure time. | |

| TAXI_OUT (TX_OUT) | Difference in minutes between departure from the origin |

| airport gate and wheels off. | |

| TAXI_IN (TX_IN) | Differences in minutes between wheels down and arrival at |

| the destination airport gate. | |

| ACT_ELAPS (ACT_ELP) | Actual elapsed time between departure from the origin airport |

| gate and arrival at the destination airport gate in minutes. | |

| CRS_ELAPS (CRS_ELP) | Scheduled elapsed time between departure and arrival in |

| minutes, CRS is short for Computer Reservation System. | |

| DISTANCE (DIST) | Distance between departure and arrival airports in miles. |

| MONTH (MON) | Month of flight. |

| DAY_OF_MONTH (DOM) | Day of month. |

| DAY_OF_WEEK (DOW) | Day of week. |

References

- Arcones and Giné (1992) Arcones, M. A. and Giné, E. (1992). On the bootstrap of U and V statistics. Ann. Statist. 20, 655-674.

- Callaert and Veraverbeke (1981) Callaert, H. and Veraverbeke, N. (1981). The order of the normal approximation for a studentized U-statistic. Ann. Statist. 1, 194-200.

- Efron and Stein (1981) Efron, B. and Stein, C. (1981). The jackknife estimate of variance. Ann. Statist. 9, 586-596.

- Kleiner et al. (2014) Kleiner, A., Talwalkar, A., Sarkar, P. and Jordan, M. I. (2014). A scalable bootstrap for massive data. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 76, 795-816.

- Koroljuk and Borovskich (1994) Koroljuk, V. S. and Borovskich, Yu. V. (1994). Theory of U-statistics. Kluwer Academic Publishers.

- Liu (1988) Liu, R. Y. (1988). Bootstrap procedures under some non-i.i.d. models. Ann. Stat. 4, 1696-1708.

- Petrov (1998) Petrov, V. V. (1998). Limit Theorems of Probability Theory: Sequences of Independent Random Variables. Oxford University Press Inc., New York.

- Sengupta, Volgushev and Shao (2016) Sengupta, S., Volgushev, S. and Shao, X. (2016). A subsampled double bootstrap for massive data. Journal of the American Statistical Association, 111 1222-1232.

- Serfling (1980) Serfling R. J. (1980). Approximation Theorems of Mathematical Statistics. John Wiley Sons, Inc.

- Székely and Rizzo (2014) Szkely and G. J., Rizzo, M. L. (2014). Partial distance correlation with methods for dissimilarities. Ann. Stat., 42 2382-2412.

- Székely, Rizzo and Bakirov (2007) Szkely, G. J., Rizzo, M. L. and Bakirov N. K. (2007). Measuring and testing dependence by correlation of distance. Ann. Stat., 35 2769-2794.

- Yao, Zhang and Shao (2017) Yao, S., Zhang, X. and Shao, X. (2017). Testing mutual independence in high dimension via distance covariance. arXiv preprint arXiv:1609.09380.