Generic Conditions for Forecast Dominance††thanks: We thank Werner Ehm, Tilmann Gneiting, Malte Knüppel, Sebastian Lerch, Melanie Schienle and seminar and conference participants at the Heidelberg Institute for Theoretical Studies, Statistische Woche (Linz, 2018), the University of Cologne and QFFE (Marseille, 2019) for helpful discussions, and Yoon-Jae Whang for making program code related to Linton et al., (2005) available via his website. Johanna F. Ziegel gratefully acknowledges financial support from the Swiss National Science Foundation.

Abstract

Recent studies have analyzed whether one forecast method dominates another under a class of consistent scoring functions. While the existing literature focuses on empirical tests of forecast dominance, little is known about the theoretical conditions under which one forecast dominates another. To address this question, we derive a new characterization of dominance among forecasts of the mean functional. We present various scenarios under which dominance occurs. Unlike existing results, our results allow for the case that the forecasts’ underlying information sets are not nested, and allow for uncalibrated forecasts that suffer, e.g., from model misspecification or parameter estimation error. We illustrate the empirical relevance of our results via data examples from finance and economics.

Key words: loss function, model comparison, prediction

1 Introduction

Forecasts of a random variable (such as the inflation rate, a financial volatility measure, or the sale price of a house) play an important role in economics. Recent technological advances have contributed to an ever increasing array of data sources and forecasting techniques, which necessitates statistically principled comparisons of forecast quality. Here we focus on the typical task of predicting the mean of . It is well known that squared error loss sets the incentive to correctly forecast the mean, conditional on a certain information set. This basic insight underlies the use of squared error for estimating regression models. However, Savage, (1971) shows that there are infinitely many other scoring (or loss) functions that are also consistent with the goal of forecasting the mean. Consider, for example, the task of modeling and forecasting the mean of a binary variable , which is simply the probability that . In this case, squared error is often referred to as the ‘Brier score’ (following Brier,, 1950). While squared error can be used to construct consistent parameter estimators in regression models and to evaluate probability forecasts out-of-sample, there is a continuum of other scoring functions that can be used as well (see e.g. Buja et al.,, 2005). The Bernoulli log likelihood function, which corresponds to maximum likelihood estimation, is arguably the most popular of these choices. In the general case where is not restricted to be binary, squared error continues to be a popular scoring function, and can be motivated as the (negative) log likelihood function of a Gaussian density with known variance. Log likelihood functions corresponding to other single-parameter families (such as Poisson or Exponential) can be employed as well; Table 1 below provides examples.

The non-uniqueness of consistent scoring functions is challenging, in that rankings of two forecast methods by average scores may depend on the specific function used for out-of-sample evaluation. Ehm et al., (2016), Ehm and Krüger, (2018), Yen and Yen, (2018), Ziegel et al., (2018) and Barendse and Patton, (2019) therefore propose graphical tools and hypothesis tests to analyze the robustness of empirical forecast rankings. In their terminology, one forecast method dominates another if it performs better in terms of every consistent scoring function.

Adopting a theoretical perspective, Holzmann and Eulert, (2014) show that a correctly specified forecast method dominates a competitor that is based on a smaller (nested) information set. However, forecasts based on diverse and thus non-nested information sets play a major role in applications, and are often encouraged by designers of forecast surveys and contests. For example, the European Central Bank’s ‘Survey of Professional Forecasters’ features private and public-sector, financial and non-financial institutions from all over Europe (European Central Bank,, 2018). Patton, (2018) demonstrates that non-nested information sets may lead to lack of forecast dominance, i.e., to forecast rankings that fail to be robust across consistent scoring functions. This issue has been tackled for probability forecasts of a binary variable (DeGroot and Fienberg,, 1983; Krzysztofowicz and Long,, 1990), but results for more general situations are available only under specific assumptions. Furthermore, all existing theoretical results assume that the forecasts under comparison specify the correct expectation of , given some information set. As illustrated by Patton, (2018), this assumption is often violated in applications, which may lead to non-robust forecast rankings.

The present paper sheds new light on the theoretical conditions under which forecast dominance occurs. An understanding of these conditions is useful to interpret empirical results of (non-)robust forecast rankings, and to identify desiderata of forecasting methods that may inspire improvements of existing methods. Unlike previous studies, we derive conditions that allow for non-nested information sets. Furthermore, we allow for various types of forecast imperfections resulting, amongst others, from model misspecification and parameter estimation error (if forecasts are generated by statistical methods) or cognitive biases (if forecasts are judgmental, generated by humans). These phenomena are ubiquitous in practice but have not been tackled by the existing theoretical literature on forecast dominance.

The paper is structured as follows. Section 2 presents our main technical result, a new characterization of dominance among mean forecasts. We then discuss alternative sets of assumptions that yield natural conditions for dominance. Section 3 considers the case of auto-calibrated forecasts, which means that the forecast matches the conditional expectation of , given the forecast itself. Under this condition, which allows for non-nested information sets, the forecast which is more variable in the sense of convex order (see e.g. Shaked and Shanthikumar,, 2007; Levy,, 2016) dominates the other. This result generalizes the result of Holzmann and Eulert, (2014) mentioned above, and thus provides weaker sufficient conditions for forecast dominance. Section 4 drops the auto-calibration assumption, but instead requires joint normality of each forecast with the predictand. Alternatively, Section 5 assumes that both forecasts are based on the same information set , but yield imperfect approximations of the conditional expectation of the predictand given . Our results in Sections 4 and 5 demonstrate that there can well be dominance relations among two uncalibrated (i.e., not auto-calibrated) forecasts. In Section 6, we illustrate our theoretical results via data examples from finance and economics. Section 7 concludes with a discussion of the results and open problems. All proofs are deferred to the appendix. An online appendix presents additional analytical examples and details on hypothesis testing in our data examples.

2 A Characterization of Forecast Dominance

Savage, (1971) considers scoring functions of the form

| (1) |

where is a forecast, is a realization, and is a convex function with subgradient . Here, a scoring function assigns a negatively oriented penalty, such that a smaller value of corresponds to a better forecast. Functions of the form given in (1) are consistent for the mean (Gneiting,, 2011): If has cumulative distribution function (CDF) , then

| (2) |

Here is the mean of (which we always assume to exist and be finite), and denotes expectation. Equation (2) states that a forecaster minimizes their expected score when stating the mean of as their forecast. The scoring function is strictly consistent if equality in (2) implies . Strict consistency corresponds to a strictly convex function in (1). Under some additional assumptions (see Gneiting,, 2011, Theorem 7), the scoring functions given at (1) are the only consistent scoring functions for the mean. Note that the additive term in (1) is included to enforce the convention that . However, the term does not depend on , and is hence irrelevant in terms of optimal forecasting. Table 1, which is a modified version of Yen and Yen, (2018, Table 1), presents examples of strictly consistent scoring functions for the mean.

| Range | Range | |||

|---|---|---|---|---|

| of | of | Comment(s) | ||

| squared error | ||||

| negative log likelihood of | ||||

| Bernoulli dist. | ||||

| negative log likelihood of | ||||

| exponential dist.; equal to | ||||

| QLIKE loss (Patton,, 2011) | ||||

| negative log likelihood of | ||||

| Poisson dist. |

Consider two generic forecasters (or forecasting methods) A and B who issue forecasts and of the mean of . We treat these forecasts as random variables and consider their joint distribution with , the random variable to be predicted. We assume throughout that , and are integrable. The random variables are defined on the probability space whereby the point forecasts are measurable with respect to information sets ; see Ehm et al., (2016, Section 3.1) for a detailed discussion. This setup includes the case of a binary predictand , in which the mean forecasts quote the probability that , conditional on their respective information sets. We emphasize that the setup is consistent with the case that is a time series and are associated forecasts. The only requirement is that the joint distribution of the forecasts and the predictand is strictly stationary, such that the objects that we use in the following (notably expectations and CDFs) are well defined and do not depend on time. See Strähl and Ziegel, (2017, Definition 2.2) for a formal probability space setup involving time series of forecasts and realizations, and Example 3.3 for an illustration. The following notion of forecast dominance is central to this paper.

Definition 2.1 (Forecast dominance).

The preceding definition implies that the better performance of compared to is robust across all consistent scoring functions . Theorem 1b and Corollary 1b of Ehm et al., (2016) imply that forecast dominance holds if and only if for all , where

| (3) |

is the so-called elementary score for the mean indexed by the parameter , up to a term that does not depend on and is thus irrelevant in terms of forecast rankings (see Lemma A.3 for details). Building upon the elementary score, we next present a novel characterization of forecast dominance.

Theorem 2.1.

Let and be forecasts for the mean. Then dominates if and only if for all , where

The function appearing in Theorem 2.1 is the expected value of the random variable , where has been defined at (3). Theorem A.4 in Appendix A is a more general version of Theorem 2.1, covering forecast dominance for expectiles at level . Expectiles are an asymmetric generalization of the mean which is the expectile at level (Newey and Powell,, 1987). While the representation of forecast dominance in Ehm et al., (2016) is an important prerequisite for our Theorems A.4 and 2.1, our derivation of an analytical expression for the expected score is novel, and is crucial in order to establish forecast dominance (or lack thereof) in theoretical scenarios. The two summands of the function separate the influence of the variability (first summand) and the calibration (second summand) of the forecast. Roughly speaking, calibration refers to the statistical compatibility of forecasts and observations; see Section 3 for details. Variability of a forecast may or may not be desirable depending on the calibration properties; see Theorem 3.1 and Proposition 4.1. In the remainder of this paper, we derive various interpretable scenarios under which the technical condition of Theorem 2.1 is satisfied.

3 Auto-Calibrated Forecasts

Definition 3.1 (Auto-calibration).

is an auto-calibrated forecast of if almost surely.

The definition implies that the forecast of can be used ‘as is’, without any need to perform bias correction. The prefix ‘auto’ indicates that is an optimal forecast relative to the information set generated by itself. Patton, (2018, Proposition 2) also considered this notion of auto-calibration in the context of forecast dominance. In the literature on forecasting binary probabilities, which are mean forecasts and thus nested in the current setting, the same notion is often simply called ‘calibration’, see e.g. Ranjan and Gneiting, (2010, Section 2.1). Furthermore, the definition coincides with the null hypothesis of the popular Mincer and Zarnowitz, (1969, henceforth MZ) regression, given by

| (4) |

the null hypothesis corresponds to being an auto-calibrated forecast of .

Auto-calibration relates to the joint distribution of the forecast and the realization . Below we make use of the concept of convex order that compares univariate distributions.

Definition 3.2 (Convex order).

A random variable is greater than in convex order if , for all convex functions such that the expectations exist.

By Strassen,’s (1965) theorem, is greater than in convex order if and only if there are random variables , on a joint probability space such that , and . Here, denotes equality in distribution. If is greater than in convex order then , where denotes variance. The converse is generally false; however, in the special case that and are both Gaussian with the same mean, implies that is greater in convex order than .

If is greater than in convex order, then second-order stochastically dominates . (A random variable second-order stochastically dominates another random variable if for all non-decreasing and concave functions ; see Levy, (2016, Section 3.6). Note that this definition is weaker than convex order since the latter involves both increasing and decreasing functions .) Furthermore, writing with , we obtain . In the economic literature, is sometimes referred to as being equal in distribution to ’ plus noise’ (Rothschild and Stiglitz,, 1970; Machina and Pratt,, 1997). The term ‘noise’ for suggests that the variation in is undesirable. Indeed, if and represent two investments with stochastic monetary payoffs, then every risk-averse decision maker with concave utility function will prefer to . We avoid the ‘noise’ terminology since the negative connotation of the term is not justified in the present context; by contrast, the following result indicates that being more volatile is highly desirable in the context of auto-calibrated mean forecasts.

Theorem 3.1.

Assume that and are both auto-calibrated mean forecasts. Then, dominates if and only if is greater than in convex order.

According to Theorem 3.1, it is desirable for a forecast to be large in convex order: Given the assumption that forecasts are auto-calibrated, being large in convex order implies that the forecast is more variable and is based on a ‘larger’ information set . Without the assumption of auto-calibration, a forecast could be more variable simply because of erratic variation (see Sections 4 and 5 below). In the case that is binary and are discretely distributed with finite support, Theorem 3.1 coincides with DeGroot and Fienberg, (1983, Theorem 1). However, Theorem 3.1 is much more widely applicable since it imposes no assumptions on the distributions of , and .

Example 3.1.

Let , where are independent and identically distributed random variables with mean zero. The distribution may be non-Gaussian, may involve skewness and excess kurtosis, or could be discrete. Now let and , such that both and are auto-calibrated for , and is greater than in convex order. By Theorem 3.1, dominates . This setup includes the example of Ehm et al., (2016, p. 557) where are all standard normal and dominance is established via calculations that exploit normality.

Example 3.2.

Suppose that and are both auto-calibrated and normally distributed. If , then normality implies that is greater than in convex order, so that dominates by Theorem 3.1. This example generalizes Patton, (2018, Proposition 2) since it is based on slightly weaker assumptions and establishes dominance under all consistent scoring functions instead of a subclass called exponential Bregman loss.

Proposition 3.2.

For , let where . Then and are both auto-calibrated and is greater than in convex order.

Examples 3.1 and 3.2 both feature non-nested information sets. Proposition 3.2 establishes that two forecasts with nested information sets satisfy the auto-calibration and convex order conditions that underlie Theorem 3.1. The latter then states that dominates , as would be expected given that has access to a larger information set and both forecasts are correctly specified. The result of Holzmann and Eulert, (2014, final line of Corollary 2) uses the same setup as Proposition 3.2 above, and is thus a special case of Theorem 3.1. Hence, Theorem 3.1 provides sufficient conditions for forecast dominance that are weaker than the ones by Holzmann and Eulert,. However, the result of Holzmann and Eulert, applies to general functionals, whereas we focus on the mean functional. The following example concerns forecasts made at different points in time, which is an important special case of nested information sets in practice.

Example 3.3.

Let where and is independent and identically distributed with mean zero and variance , and let be the information set generated by observations until time . Suppose and for some . Then and are all strictly stationary time series, and . Proposition 3.2 thus implies that both forecasts are auto-calibrated, and that is greater than in convex order. Hence, the variance of exceeds that of , which also follows from Corollary 2 of Patton and Timmermann, (2012).

Finally, the following corollary describes a simple implication of Theorem 3.1 that is closely related to empirical practice in econometrics.

Corollary.

4 Forecast Dominance under Normality

Auto-calibration essentially rules out uninformative variation (‘noise’) in a forecast that may result from an overfitted statistical model, for example.

Example 4.1.

Let where and are independently standard normal. Suppose forecaster quotes as a mean forecast for , and forecaster quotes where , independently of and . One obtains easily that , which implies that forecast is uncalibrated.

In Example 4.1, intuition suggests that is a better forecast than since the latter simply adds the noise term on top of the former. Theorem 3.1 cannot be used to derive this statement since is uncalibrated. In this section and in Section 5, we dispense with the auto-calibration assumption. In order to arrive at interpretable conditions, we investigate the scenario in which the forecast and the realization follow a bivariate normal distribution, such that

| (5) |

where is the correlation between and .

The Gaussian setup is similar to Satopää et al., (2016) who motivate joint normality of forecasts and realizations from a situation in which forecasters observe small bits (’particles’) of the information that generates the predictand; see their Section 3.2.

Forecast dominance does not depend on the dependence structure between the forecasts. Hence Equation (5) refers to the pair only; the joint distribution of is left unspecified, and may be non-Gaussian. The distribution in (5) is an unconditional one, and does not specify the dependence (or independence) across forecast instances. See Example A.1 in the Online Appendix for a stationary time series illustration that fits into the Gaussian framework.

We assume that , which means that forecasts and correctly assess the unconditional mean of . This simplifies our analysis but does not seem restrictive in most applications. The setup in Equation (5) allows for a wide range of scenarios in terms of forecast accuracy. In particular, the correlation parameter may be positive or negative, and there is no prespecified relation between the variance parameters and . This modeling approach hence is capable of describing the behavior of imperfect forecasts.

Proposition 4.1.

By Ehm et al., (2016, Theorem 1b and Corollary 1b), dominates if the left hand side of (6) is non-negative for all . The expression in (6) yields several sets of sufficient conditions for forecast dominance, where we use the notation to denote the population slope coefficient in a MZ regression of on as in Equation (4). The condition is necessary and sufficient for auto-calibration.

- Case 1

-

Let , and assume that . Then dominates .

- Case 2

-

Let .

- Case 2a

-

Assume that . If , then dominates .

- Case 2b

-

If , then dominates .

- Case 3

-

Suppose that , and that either or . Then the forecast for which is smaller dominates the other.

- Case 4

-

If , the forecast for which is higher dominates the other.

Justification of these claims is given in the Appendix. For two auto-calibrated forecasts (), Case 1 implies that the one with higher variance is dominant, which echoes the statement of Theorem 3.1. (Since both forecasts are Gaussian with the same mean, having higher variance is the same as being greater in convex order.) However, Case 1 does not require auto-calibration. It implies that there may be dominance relations among two uncalibrated forecasts, or dominance of an auto-calibrated forecast over an uncalibrated competitor, or vice versa. Case 2a describes a situation in which has lower variance than , but at the same time has higher covariance with . This suggests that has a more favorable signal-to-noise ratio than , explaining dominance of over . In Case 2b, is a particularly poor forecast, featuring high variance and negative correlation with . Case 3 describes situations in which both forecasts have the same correlation with , and both are uncalibrated. In these situations, the forecast that comes closer to being auto-calibrated is dominant. Finally, Case 4 describes a simple condition for dominance if both forecasts have the same variance.

Proposition 4.1 yields a simple necessary condition for forecast dominance: For to dominate , it must hold that . (This can be seen by evaluating the expected score difference in Proposition 4.1 at .) If the forecast parameters satisfy this necessary condition but can not be classified into one of the four cases presented above, it is unclear whether a dominance relation exists. In this situation, one can use the result of Proposition 4.1 for an informal numerical check of dominance; see Example A.2 in the Online Appendix for an illustration.

A major implication of the Gaussian case is that auto-calibration – which underlies Section 3, as well as all of the previous literature – is not generally required to establish forecast dominance. In particular, there may well be dominance relations among forecasts generated from mis-specified statistical models; see Section 5.

5 Forecasts based on a Common Information Set

The results in Section 4 do not require auto-calibration, but require joint Gaussianity of forecasts and realizations. In this section, we present a result that requires neither auto-calibration nor Gaussianity, but assumes that both forecasts can be represented as plus noise, where the information set is common across forecasting methods. The forecast methods can be viewed as different ways of exploiting , based on statistical models using alternative estimation algorithms or functional form assumptions, for example.

Theorem 5.1.

Let be a -algebra, and let

where , and is conditionally independent of given . Assume that, conditionally on , the distributions of and are both symmetric around zero and are such that is smaller than with respect to first order stochastic dominance. Then A dominates B.

Conditional independence of and says that, given the information , must not contain information about . This requirement seems natural given our interpretation of as a modeling error. The assumptions about and imply that the former is less variable (Shaked and Shanthikumar,, 2007, Section 3.D). In the special case that , the condition is satisfied if . The assumption that implies that modeling errors are unsystematic, which seems plausible in the context of overfitted statistical models, for example. The theorem nests the case that almost surely for one model .

In contrast to Theorem 3.1 and Proposition 4.1, the conditions of Theorem 5.1 are not directly testable for empirical data. However, we present testable implications.

Proposition 5.2.

Under the conditions of Theorem 5.1, the following statements hold:

-

(a)

.

-

(b)

for that is, both forecasts attain a slope coeffient in MZ regressions.

-

(c)

for all .

Theorem 5.1 has implications for out-of-sample prediction in linear models.

Example 5.1.

Let

where is a -dimensional vector of regressors, and is an error term satisfying . Suppose that forecast is based on some estimator for , obtained from training data . We seek to make predictions for a new observation , where and are independent of the training data. We have that , where is the estimator underlying forecast , and represents the approximation error of forecast . Setting , we can apply Theorem 5.1. By assumption, (which is generated from training data) is independent of such that is conditionally independent of given . For large training samples, it is natural to assume multivariate normality of for with mean zero and covariance matrix . Under this assumption, dominance of over occurs if , for all , which is equivalent to being positive semi-definite. This is the standard notion of being a more precise estimator of (Lehmann and Casella,, 1998, Equation 4.4).

6 Data Examples

6.1 Forecasting the volatility of financial asset returns

Following Andersen et al., (2003), a large literature is concerned with modeling and forecasting realized measures of asset return volatility. Here we consider forecasting , where is a realized kernel estimate (Barndorff-Nielsen et al.,, 2008) for the Dow Jones Industrial Average on day . The two forecast specifications we compare are of the form

where is a sequence of predictor variables. This functional form follows Corsi, (2009), and provides a simple way of capturing the temporal persistence in that is typical of financial volatilities. For forecast , corresponds to the daily logarithmic value of the VIX index, an implied volatility index computed from financial options. For forecast , corresponds to the logarithmic value of the absolute index return on day . We estimate both specifications using ordinary least squares, based on a rolling window of observations. Data on the realized kernel measure and daily returns are from the Oxford-Man Realized library at https://realized.oxford-man.ox.ac.uk/; data on the VIX are from the FRED database of the Federal Reserve Bank of St. Louis (https://fred.stlouisfed.org/series/VIXCLS). The sample obtained from merging both data sources covers daily observations from January 4, 2000 to May 10, 2018. The initial part of the sample is reserved for estimating the model. We evaluate forecasts for an out-of-sample period ranging from February 13, 2004 to May 10, 2018 ( observations).

To illustrate the conditions for Theorem 3.1 empirically, we first consider MZ regressions for both forecasts, based on the out-of-sample period. For forecast (based on VIX), we obtain the estimate

| + error; | ||||

the of the regression is , and standard errors that are robust to autocorrelation and heteroscedasticity are reported in brackets. The standard errors are computed using the function NeweyWest from the R package sandwich (Zeileis,, 2004), which implements the Newey and West, (1987, 1994) variance estimator. For forecast (based on absolute returns), we obtain

| + error, | ||||

with an of . In both regressions, a Wald test of the hypothesis of auto-calibration (corresponding to an intercept of zero and a slope of one) cannot be rejected at conventional significance levels.

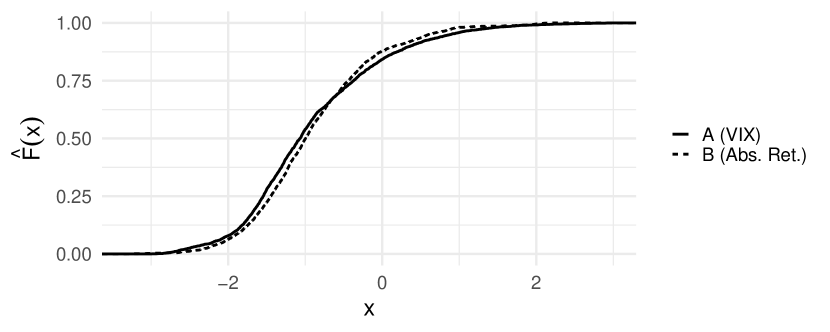

To assess the convex order condition empirically, let denote the CDF of forecast . Then is greater than in convex order if and only if

| (7) |

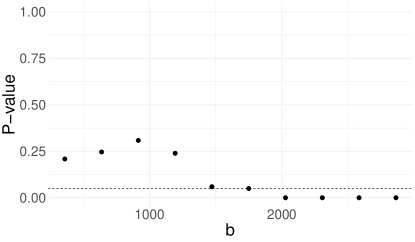

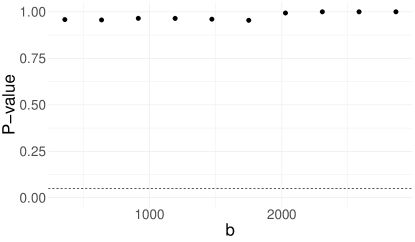

for every , and equality holds in the limit as (see the proof of Theorem 3.1 in Appendix B). Figure 2 plots the empirical CDFs of both forecasts. Visual inspection suggests that the integral condition in Equation 7 is plausible in the current example. In order to provide a more formal assessment, we use the subsampling based test by Linton et al., (2005) to investigate the hypothesis that one distribution is smaller than another in convex order. (Linton et al., (2005) test for second order stochastic dominance (SOSD). Under the assumption of auto-calibration, both forecasts have the same expected value, so that SOSD and convex order coincide, except for a differential sign convention.) We abbreviate the hypothesis of interest as ‘ is CO-smaller than ’ in the following discussion. Since the test depends on a tuning parameter (the size of the subsamples) that is hard to select in practice, Linton et al., (2005, Section 5.2) suggest to plot the test’s -value against , and select from within a range over which is stable; see Online Appendix B.1 for details. Figure 1 shows the test results. The hypothesis that is CO-smaller than is rejected at the five percent levels for a range of over which the -values are stable. By contrast, the right panel of Figure 1 shows no evidence against the hypothesis that is CO-smaller than , with large -values for all values of . In summary, the test thus reinforces the impression that a convex ordering (with being greater than ) is plausible in the present example.

| smaller than in convex order | smaller than in convex order |

|---|---|

|

|

Hence both conditions of Theorem 3.1 seem plausible, and forecast appears to be more informative than forecast . Thus, we expect to dominate . In order to test dominance empirically, we use the bootstrap-based test by Ziegel et al., (2018) which we modify to cover the class of Bregman scoring functions at (1), instead of the class of scoring functions related to Expected Shortfall that is used by Ziegel et al., (2018). Following their implementation, we use a stationary bootstrap with block length drawn from a geometric distribution with mean where is the size of the forecast evaluation sample. We use bootstrap iterations; see Online Appendix B.2 for further details. In line with the implication of Theorem 3.1, the hypothesis that dominates is not rejected by the test, with a bootstrap -value of one. In contrast, the hypothesis that dominates is rejected with a bootstrap -value below one percent.

6.2 Forecasting US inflation

We illustrate the results of the normally distributed case from Section 4 with inflation forecasts from the Survey of Professional Forecasters (SPF), a widely used survey of macroeconomic experts. We compare the survey against two simple forecasting schemes: A random walk forecast (RW) that states the latest realization available to SPF participants, and a rolling mean forecast (RM) considering the four latest available observations (Atkeson and Ohanian,, 2001). Given their simplicity, these methods act as minimal benchmarks for more sophisticated competitors, and are routinely included in practical forecast comparisons (see e.g. Faust and Wright,, 2013, Section 2.5). Our analysis is based on real-time data published by the Federal Reserve Bank of Philadelphia at https://www.philadelphiafed.org/research-and-data/real-time-center. We focus on inflation as measured by the GDP deflator; the relevant series codes are PGDP (SPF forecasts) and P (realizations). We compare the forecasts against the second vintages of the realizations data. We further center the forecasts and realizations at zero in order to enforce the common mean assumption made in Section 4 (); however, our results are very similar if we omit this centering step.

We first assess the assumption that forecasts and realizations follow a bivariate normal distribution. To this end, we implement the test by Lobato and Velasco, (2004) for the null hypothesis that a univariate stationary time series is unconditionally Gaussian. The test is appealing in that it is free of tuning parameters. We apply the test to the forecasts , the outcome and the forecast errors , all of which are normally distributed if and are jointly normal. Repeating this procedure for three different forecast methods (SPF, random walk and rolling mean) and at five forecast horizons (ranging from zero to four quarters ahead), we obtain -values above in all but one case. These results indicate that there is little evidence against pairwise bivariate normality of forecasts and realizations. Analogous tests for other macroeconomic variables (GDP growth and consumer price inflation) yielded clear rejections of normality, which is why we do not consider these variables here.

As a simple summary measure of forecast performance, Table 2 presents the methods’ mean squared error (MSE) at various forecast horizons. The SPF attains the smallest MSE among the three methods, with the rolling mean method performing similarly well at some horizons. The random walk method attains the largest MSE at all horizons. In order to assess the plausibility of various dominance scenarios (see below Proposition 4.1), Table 2 presents some relevant statistics related to the covariance matrix of . We check whether these statistics match any of the scenarios under which dominance may occur. Consider, for example, the comparison of SPF versus RW at horizon in the first column of Table 2. The SPF forecasts have a smaller empirical standard deviation than the random walk forecasts (). At the same time, the SPF’s MZ regression coefficient () exceeds that of the random walk (). These findings indicate that the SPF forecasts have a better signal-to-noise ratio than the random walk. Indeed, the point estimates satisfy the conditions of Case 2a in Section 4, with the SPF taking the role of the dominant forecast .

The left panel of Table 3 summarizes the outcomes of similar comparisons for all forecast horizons . This analysis is based on the empirical point estimates, and can hence be thought of as calibrating the theoretical results of Section 4 to empirical data. The table reports a ‘’ entry whenever the parameters in Table 2 belong to one of the sufficient conditions for dominance presented in Section 4 (Case 1-4). The SPF forecasts are dominant in six instances, all of which satisfy the conditions of Case 2a. These findings hence indicate that the SPF forecasts tend to contain less noise and more signal than the simple time series methods. Furthermore, according to the parameter estimates, the RM forecast dominates the RW forecast at the three shortest horizons, with the parameters again belonging to Case 2a in each case.

The right panel of Table 3 reports bootstrap -values for various possible dominance relations. The bootstrap implementation is analogous to the one in Section 6.1. The bootstrap is nonparametric, contrasting the Gaussian setup of the theory in Section 4. In comparing the left and right panels of Table 3, one can see a fairly close correspondence between the theoretical implications and the empirical test results. In particular, instances where theory predicts dominance (symbol in left panel) correspond to high bootstrap -values in the right panel, such that there is no evidence against dominance. Cases where theory rules out dominance (symbol X in left panel) tend to go along with low bootstrap -values in the right panel, corresponding to evidence against dominance.

The preceding analysis shows that our theoretical results under normality can inform empirical forecast comparisons. In addition, the comparisons between the two simple time series methods (RW and RM) are also in line with the theoretical conditions of Theorem 5.1: First, both methods are based on the same information set generated by observations up until time . Second, the theorem’s testable implications in Proposition 5.2 all seem plausible here; compare the coefficients , and reported in Table 2. The theorem then predicts dominance of RM over RW. As shown in Table 3, this conclusion is broadly in line with empirical nonparametric bootstrap tests.

| MSESPF | 0.665 | 0.778 | 0.862 | 0.920 | 1.001 |

|---|---|---|---|---|---|

| MSERW | 1.412 | 1.535 | 1.497 | 1.348 | 1.538 |

| MSERM | 0.886 | 0.917 | 0.991 | 1.103 | 1.201 |

| 1.160 | 1.160 | 1.160 | 1.160 | 1.160 | |

| 0.916 | 0.917 | 0.967 | 1.008 | 1.012 | |

| 1.156 | 1.161 | 1.176 | 1.213 | 1.221 | |

| 0.924 | 0.935 | 0.950 | 0.971 | 0.987 | |

| 0.903 | 0.834 | 0.755 | 0.706 | 0.665 | |

| 0.471 | 0.425 | 0.441 | 0.496 | 0.432 | |

| 0.766 | 0.741 | 0.692 | 0.624 | 0.570 | |

| 2.088 | 2.220 | 2.488 | 3.172 | 2.813 | |

| 5.393 | 5.383 | 5.515 | 6.506 | 6.534 | |

| 1.895 | 1.932 | 2.028 | 2.234 | 2.354 |

| Theory implications | Bootstrap -values | |||||||||||

| 0 | 1 | 2 | 3 | 4 | 0 | 1 | 2 | 3 | 4 | |||

| SPF RW | ? | 1.000 | 1.000 | 1.000 | 0.968 | 0.798 | ||||||

| RW SPF | X | X | X | X | X | 0.031 | 0.043 | 0.050 | 0.030 | 0.056 | ||

| SPF RM | ? | ? | ? | 0.911 | 0.650 | 0.723 | 0.441 | 0.736 | ||||

| RM SPF | X | X | X | X | X | 0.435 | 0.255 | 0.160 | 0.291 | 0.225 | ||

| RW RM | X | X | X | X | X | 0.032 | 0.014 | 0.027 | 0.473 | 0.298 | ||

| RM RW | ? | ? | 1.000 | 1.000 | 0.999 | 0.760 | 0.919 | |||||

7 Discussion

Patton, (2018) identifies three reasons why forecast dominance may not hold in practice: Non-nested information sets, misspecification, and estimation error. Motivated by this assessment, the present paper provides a theoretical analysis of forecast dominance that relates to each of these situations. Under the assumption that forecasts are auto-calibrated, our results in Section 3 provide a novel characterization of the role played by information sets that may or may not be nested. Misspecification and estimation error are likely to lead to uncalibrated forecasts for which no analytical results are available in the existing literature on forecast dominance. Our results in Sections 4 and 5 cover this case in detail, based on two distinct sets of assumptions that allow us to arrive at interpretable conditions.

Conceptually, our results indicate that the notion of forecast dominance may be less strong than suggested by Patton, (2018), Nolde and Ziegel, (2017, Section 2.3), and others. In particular, there can be dominance relations among two forecasts that are both highly imperfect. From a more technical perspective, an interesting question is whether similar conditions for forecast dominance can be derived for functionals other than the mean. As starting points of the analysis, our Theorem A.4 specifies conditions for dominance for the expectile functional (which includes the mean as a special case), and we treat quantiles in Online Appendix C. An open challenge are full distributional forecasts.

References

- Andersen et al., (2003) Andersen, T. G., Bollerslev, T., Diebold, F. X., and Labys, P. (2003). Modeling and forecasting realized volatility. Econometrica, 71:579–625.

- Atkeson and Ohanian, (2001) Atkeson, A. and Ohanian, L. E. (2001). Are Phillips curves useful for forecasting inflation? Federal Reserve Bank of Minneapolis Quarterly Review, 25:2–11.

- Barendse and Patton, (2019) Barendse, S. and Patton, A. (2019). Comparing predictive accuracy in the presence of a loss function shape parameter. Working Paper, Duke University, November 2019.

- Barndorff-Nielsen et al., (2008) Barndorff-Nielsen, O. E., Hansen, P. R., Lunde, A., and Shephard, N. (2008). Designing realized kernels to measure the ex post variation of equity prices in the presence of noise. Econometrica, 76:1481–1536.

- Brier, (1950) Brier, G. W. (1950). Verification of forecasts expressed in terms of probability. Monthly Weather Review, 78:1–3.

- Buja et al., (2005) Buja, A., Stuetzle, W., and Shen, Y. (2005). Loss functions for binary class probability estimation and classification: Structure and applications. Working Paper, University of Washington, November 2005.

- Corsi, (2009) Corsi, F. (2009). A simple approximate long-memory model of realized volatility. Journal of Financial Econometrics, 7:174–196.

- DeGroot and Fienberg, (1983) DeGroot, M. H. and Fienberg, S. E. (1983). The comparison and evaluation of forecasters. The Statistician, 32:12–22.

- Ehm et al., (2016) Ehm, W., Gneiting, T., Jordan, A., and Krüger, F. (2016). Of quantiles and expectiles: Consistent scoring functions, Choquet representations and forecast rankings (with discussion and rejoinder). Journal of the Royal Statistical Society: Series B, 78:505–562.

- Ehm and Krüger, (2018) Ehm, W. and Krüger, F. (2018). Forecast dominance testing via sign randomization. Electronic Journal of Statistics, 12:3758–3793.

- European Central Bank, (2018) European Central Bank (2018). ECB survey of professional forecasters (documentation). Available at https://www.ecb.europa.eu/stats/ecb_surveys/survey_of_professional_forecasters/html/index.en.html, accessed: September 17, 2018.

- Faust and Wright, (2013) Faust, J. and Wright, J. H. (2013). Forecasting inflation. In Handbook of Economic Forecasting, volume 2, pages 2–56. Elsevier, Amsterdam.

- Gneiting, (2011) Gneiting, T. (2011). Making and evaluating point forecasts. Journal of the American Statistical Association, 106:746–762.

- Holzmann and Eulert, (2014) Holzmann, H. and Eulert, M. (2014). The role of the information set for forecasting–with applications to risk management. Annals of Applied Statistics, 8:595–621.

- Krzysztofowicz and Long, (1990) Krzysztofowicz, R. and Long, D. (1990). Fusion of detection probabilities and comparison of multisensor systems. IEEE Transactions on Systems, Man, and Cybernetics, 20:665–677.

- Lehmann and Casella, (1998) Lehmann, E. L. and Casella, G. (1998). Theory of Point Estimation. Springer, New York, 2 edition.

- Levy, (2016) Levy, H. (2016). Stochastic Dominance: Investment Decision Making Under Uncertainty. Springer, New York, 3 edition.

- Linton et al., (2005) Linton, O., Maasoumi, E., and Whang, Y.-J. (2005). Consistent testing for stochastic dominance under general sampling schemes. Review of Economic Studies, 72:735–765.

- Lobato and Velasco, (2004) Lobato, I. N. and Velasco, C. (2004). A simple test of normality for time series. Econometric Theory, 20:671–689.

- Machina and Pratt, (1997) Machina, M. and Pratt, J. (1997). Increasing risk: Some direct constructions. Journal of Risk and Uncertainty, 14:103–127.

- Mincer and Zarnowitz, (1969) Mincer, J. A. and Zarnowitz, V. (1969). The evaluation of economic forecasts. In Mincer, J. A., editor, Economic Forecasts and Expectations: Analysis of Forecasting Behavior and Performance, pages 3–46. Columbia University Press, New York.

- Müller and Rüschendorf, (2001) Müller, A. and Rüschendorf, L. (2001). On the optimal stopping values induced by general dependence structures. Journal of Applied Probability, 38:672–684.

- Newey and Powell, (1987) Newey, W. K. and Powell, J. L. (1987). Asymmetric least squares estimation and testing. Econometrica, 55:819–847.

- Newey and West, (1987) Newey, W. K. and West, K. D. (1987). A simple, positive semi-definite, heteroscedasticity and autocorrelation consistent covariance matrix. Econometrica, 55:703–708.

- Newey and West, (1994) Newey, W. K. and West, K. D. (1994). Automatic lag selection in covariance matrix estimation. Review of Economic Studies, 61:631–653.

- Nolde and Ziegel, (2017) Nolde, N. and Ziegel, J. F. (2017). Elicitability and backtesting: Perspectives for banking regulation (with discussion and rejoinder). Annals of Applied Statistics, 11:1833–1874.

- Patton, (2011) Patton, A. J. (2011). Volatility forecast comparison using imperfect volatility proxies. Journal of Econometrics, 160:246–256.

- Patton, (2018) Patton, A. J. (2018). Comparing possibly misspecified forecasts. Journal of Business & Economic Statistics. Forthcoming.

- Patton and Timmermann, (2012) Patton, A. J. and Timmermann, A. (2012). Forecast rationality tests based on multi-horizon bounds. Journal of Business & Economic Statistics, 30:1–17.

- Ranjan and Gneiting, (2010) Ranjan, R. and Gneiting, T. (2010). Combining probability forecasts. Journal of the Royal Statistical Society. Series B, 72:71–91.

- Rothschild and Stiglitz, (1970) Rothschild, M. and Stiglitz, J. E. (1970). Increasing risk: I. A definition. Journal of Economic Theory, 2:225 – 243.

- Satopää et al., (2016) Satopää, V. A., Pemantle, R., and Ungar, L. H. (2016). Modeling probability forecasts via information diversity. Journal of the American Statistical Association, 111:1623–1633.

- Savage, (1971) Savage, L. J. (1971). Elicitation of personal probabilities and expectations. Journal of the American Statistical Association, 66:783–801.

- Shaked and Shanthikumar, (2007) Shaked, M. and Shanthikumar, J. G. (2007). Stochastic Orders. Springer, New York.

- Strähl and Ziegel, (2017) Strähl, C. and Ziegel, J. F. (2017). Cross-calibration of probabilistic forecasts. Electronic Journal of Statistics, 11:608–639.

- Strassen, (1965) Strassen, V. (1965). The existence of probability measures with given marginals. Annals of Mathematical Statistics, 36:423–439.

- Yen and Yen, (2018) Yen, T.-J. and Yen, Y.-M. (2018). Testing forecast accuracy of expectiles and quantiles with the extremal consistent loss functions. Working Paper, National Chengchi University, July 2018.

- Zeileis, (2004) Zeileis, A. (2004). Econometric computing with HC and HAC covariance matrix estimators. Journal of Statistical Software, 11:1–17.

- Ziegel et al., (2018) Ziegel, J. F., Krüger, F., Jordan, A., and Fasciati, F. (2018). Robust forecast evaluation of Expected Shortfall. Journal of Financial Econometrics. Forthcoming.

Appendix

Appendix A Result for Dominance of Expectile Forecasts

We state and prove a more general version of Theorem 2.1. We consider the expectile functional of at level (Newey and Powell,, 1987). The expectile is the unique value that satisfies

where is the CDF of . The mean functional is obtained as a special case for . As shown by Gneiting, (2011), the class of consistent scoring functions for the expectile at level is given by

| (8) |

where is a convex function with subgradient . The relevant class for the mean (see Equation 1) emerges for . Analogously to Definition 2.1, we then have the following definition of forecast dominance for expectiles.

Definition A.1 (Forecast dominance for expectiles).

Lemma A.1.

For any Borel set ,

Proof.

By Fubini’s theorem, we obtain

where denotes the conditional CDF of given , and denotes the CDF of . The proof of the second equality is analogous. ∎

Lemma A.2.

Let be two random variables such that exists and is finite. Then,

| (9) |

where , , are the joint and marginal CDFs of , and , respectively.

Proof.

For a random variable , we can write

where , are the positive and the negative part of , respectively. Therefore,

| (10) |

Taking the expectation in (10) and using Fubini’s theorem, we obtain

and, similarly, with ,

Lemma A.3.

The elementary scoring function for expectiles in Ehm et al., (2016, Equation 12) is identical to the function

| (11) |

up to a difference of which does not depend on .

Proof.

Adjusting the notation in Equation (12) of Ehm et al. (2016) (using the symbol instead of for the expectile level), we have

Since and , the score can be rewritten as

Subtracting the term (which does not depend on ) and rearranging, we get

Theorem A.4.

Let and be forecasts for the -expectile. Then dominates if and only if , for all , where

Proof.

By Ehm et al., (2016, Corollary 1b), A dominates B if and only if for all , where is given at (11), see Lemma A.3. Note that is integrable if is integrable, . We apply Lemma A.2 to the random variables and . We have ,

Therefore, the first integral on the right hand side of (9) is

Similarly, we can compute the third integal on the right hand side of (9) to obtain

The second and the fourth integral on the right hand side of (9) are zero because and are zero for . Using a change of variables, we obtain

We can rewrite this as

where the second equality holds because for and for , for . The last equality follows from Lemma A.1 with . ∎

Appendix B Proofs and Technical Details

Proof of Theorem 2.1.

The result follows from Theorem A.4 with because and , where the second equality uses the law of iterated expectations. ∎

Proof of Theorem 3.1.

Under auto-calibration, holds almost surely. In view of Theorem 2.1, Theorem 3.1 then follows from Müller and Rüschendorf, (2001, Corollary 4.1) which shows that is greater than in convex order if and only if for all , and

| (12) |

To see why (12) holds, note that

where the first equality follows from Müller and Rüschendorf, (2001, Proposition 4.1.(a)(iii)), and the second equality follows from auto-calibration. ∎

Proof of Proposition 3.2.

Auto-calibration of holds because and where the first equality uses the tower property of conditional expectation. To show that is greater than in convex order, note that where the second equality again uses the tower property, together with the fact that . Strassen,’s 1965 characterization mentioned in Section 2 thus implies that is greater than in convex order.∎

Proof of Corollary at the end of Section 3.

Due to auto-calibration, for where Cov denotes covariance. The convex order condition implies that , and hence that where Cor denotes correlation and is the from the Mincer-Zarnowitz regression for forecast . ∎

Proof of Proposition 4.1.

Suppose that follow a bivariate normal distribution. We compute defined in Theorem 2.1 for . We have that , and hence

where we define for , . Then,

| (13) |

Using the assumption that and the fact that Equation (13) yields that

| (14) |

Notes on Cases 1 to 4.

Case 1 holds because, for each , we have where has been defined at (14). Case 2a can be shown by re-parametrizing , and differentiating with respect to . Case 3 can be shown by differentiating with respect to . Cases 2b and 4 are immediate. ∎

Proof of Theorem 5.1.

Denote the CDF of , conditional on , by , for . By Shaked and Shanthikumar, (2007, Theorem 3.D.1), the assumptions of Theorem 5.1 imply that

| (15) |

By Ehm et al., (2016, Corollary 1b), A dominates B if and only if for all , where is given at (3). The random variable is integrable if is integrable. Define , and let . Then,

Hence, (15) implies

Proof of Proposition 5.2.

Parts (a) and (b) are immediate given the setup of Theorem 5.1. Regarding (c), we have the following inequality for any strictly increasing function :

| (16) |

where the inequality follows from (15) in the proof of Theorem 5.1.

Now let such that . For terms of the form , with and being odd integers, it holds that where the last equality follows from symmetry of around zero. For terms of the form , with and being even integers, it holds that where the inequality follows from (16). Part (b) of Theorem 5.1 then follows from the binomial theorem. ∎