Closed-Form Projection Method for Regularizing a Function Defined by a Discrete Set of Noisy Data and for Estimating its Derivative and Fractional Derivative

Abstract

We present a closed-form finite-dimensional projection method for regularizing a function defined by a discrete set of measurement data, which have been contaminated by random, zero mean errors, and for estimating the derivative and fractional derivative of this function by linear combinations of a few low degree trigonometric or Jacobi polynomials. Our method takes advantage of the fact that there are known infinite-dimensional singular value decompositions of the operators of integration and fractional integration.

Keywords: regularization, inverse problem, ill-posed problem, Abel’s integral equation, Volterra integral equation of the first kind, numerical derivative, fractional derivative, singular value decomposition

1 Introduction

In this paper, we present a finite-dimensional spectral projection method for regularizing a smooth function that is defined by a discrete set of noisy data measurements. We also present a related spectral projection method for estimating the derivative and fractional derivative of this function. Our approach takes advantage of known closed-form singular value decompositions of the integral transforms associated with integration and fractional integration.

Our starting point is the Abel transform, an injective compact linear operator which we define by

| (1.1) |

for . Here, is the Euler gamma function, and are weighted real spaces on the bounded interval , with respective weight functions , , and scalar products

| (1.2) |

The problem of inversion of the Abel transform is a Volterra integral equation of the first kind, Abel’s equation, in which the data are given by a function , and the source is a function to be determined. Our goal is to find a smooth approximation of , when is specified only by a finite set of measured values in , which have been contaminated by random, zero-mean measurement errors, with quantified uncertainties.

Abel’s equation arises in a number of important remote sensing applications, including interferometry, seismology, tomography, and astronomy; see, e.g., Craig and Brown [7], Gorenflo and Vessella [13], Anderssen and de Hoog [3], Bracewell [4]. The operator of (1.1) can be interpreted as a fractional integral operator, for [13, Sec. 1.1]. For , it can be shown that [13, Sec. 1.2, 1.A], if is absolutely continuous on , then (1.1) has a unique solution , which is given by

Thus, the inverse of can be interpreted as a fractional derivative operator for [13, Sec. 1.2],

| (1.4) |

If , and in addition , then by partial integration,

| (1.5) |

The presence of the differentiation operator in (1) and (1.5) suggests that there will be difficulties similar to those encountered when trying to estimate the derivative of a function that is specified by noisy data, i.e., in trying to solve

| (1.6) |

for numerically, when is given as a discrete set of data with measurement uncertainties. Like the integration operator [16, Thm. 2.28], the Abel transform is a compact linear operator acting on and into infinite-dimensional Hilbert spaces [13, Thm. 4.3.3]. Therefore, its inverse cannot be continuous [16, Sec. 2.5]. Thus, the problem of inverting the Abel transform is also ill-posed.

Without loss of generality, assume for the moment that in (1.1), and denote its convolution kernel function by , i.e.,

| (1.7) |

Following Craig and Brown [7, Sec. 4.4], we take the Laplace transform of both sides in (1.1), and get that

| (1.8) |

where

| (1.9) |

Let , where is a fixed real number. It follows from (1.9) that, for large , the point spread or filtering property of the kernel behaves like

| (1.10) |

Thus, the closer is to , the more the kernel in (1.1) smoothes high-frequency content in the source function. It follows that if the data function is contaminated by high-frequency noise, it will not lie in the range of the operator , so that the Abel equation becomes more ill-posed as , and the most unstable case is , i.e., numerical differentiation of noisy data.

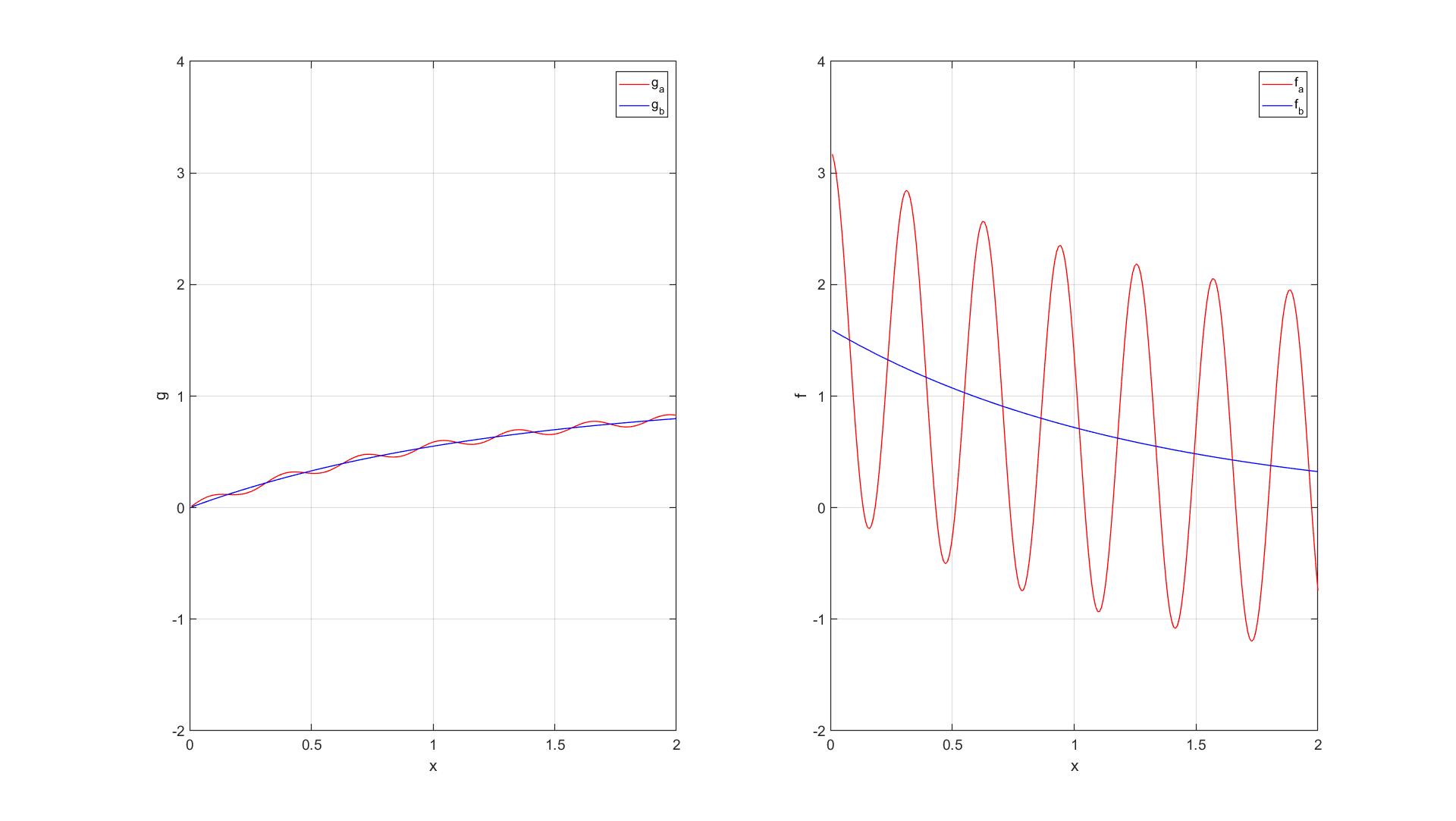

Consider the following example of (1.6) (Craig and Brown [7, Sec. 1.3]),

| (1.11) | |||||

| (1.12) |

for . Denote by and the respective functions (1.11) and (1.12) evaluated with the parameters , , and , and by and the respective functions evaluated with the parameters , , and ; see Fig. 1. Note that, whereas the two functions and differ only by a small-amplitude oscillation of relatively low frequency, corresponding to a maximum pointwise difference of about , the corresponding source functions and differ pointwise by a maximum of more than . Furthermore, whereas the maximum difference between the data functions remains the same as increases, this is not the case for the source functions, where the maximum separation between and increases linearly with . It follows that, for this example, while the forward problem of model fitting, in which source functions are compared as to how well they can predict a given set of measurement data, is insensitive to small high-frequency perturbations in , the inverse problem, of estimating the source function given a set of data measurements, is extremely sensitive to the presence of high-frequency content in the data, even if it is of relatively small amplitude. That this is generally the case for (1.1) and (1.6) follows from the singular value decompositions of the associated integral operators; see Sec. 3. Furthermore, by (1.9), small-amplitude high-frequency content in a set of experimental measurements of the function , that is based on either of the transforms (1.1) or (1.6), for some source , would be expected to correspond to noise, rather than signal, in the data.

As will be discussed in Sec. 2 and 4, our approach to regularizing the data function , i.e., for separating signal from noise in the data, prior to obtaining an estimate of the source function , is based on a global approximation method. The important point that we want to make here is that our approach to smoothing the data is essentially independent of any specific integral equation. The regularization method that we will present is an extension of the work of Rust [19] on the highly ill-posed problem of estimating the source function in Fredholm integral equations of the first kind,

| (1.13) |

with a smooth kernel (see Craig and Brown [7], Wing [23], Kress [16]). Rust developed a global projection method, which is based on the numerical singular value decomposition (SVD) of a discrete version of the operator in (1.13), for the regularization of data, prior to computing an estimate of in (1.13), using a statistical linear regression model, which treats the residual as a realization of a white noise time series.

Rust’s method will be discussed in more detail in the next section. In Sec. 3, we will take advantage of the fact that there are known singular value decompositions for the operators of integration and fractional integration in an infinite-dimensional Hilbert space setting. By approximating in a finite-dimensional subspace of the range of the integral operator, we will show how to obtain a closed-form finite-dimensional estimate for the source function in a finite-dimensional subspace of the domain of the operator. We will then discuss our approach to obtaining a regularized approximation of , prior to estimating , in the context of the infinite-dimensional SVD’s, in Sec. 4. At the end of Sec. 4, we will show how this regularization method can be “decoupled” from the SVD, which will provide a method for separating higher-frequency noise from low-frequency signal in measurement data from more general applications, under the assumption that the process that produces the data is smoothing, so that it preferentially damps higher-frequency content in the data. In Sec. 5, we will present some computational results that show the usefulness of our regularization method. Some discussion and concluding remarks will be given in Sec. 6.

2 Rust’s Regularization Method

As discussed in the Introduction, Rust developed a method for separating signal from noise in noisy data, prior to obtaining an estimate of the source function in an overdetermined linear regression model of a Fredholm integral equation of the first kind. Subsequently, Rust’s method has influenced the work of others on first-kind Fredholm integral equations; see, e.g., [14]. We will show in what follows that this approach to regularization has much wider application to ill-posed problems.

In this section, we will outline Rust’s method by finding an approximate solution of the simple-looking Volterra integral equation of the first kind (see (1.6)),

| (2.1) |

In (2.1), data represented by the function evaluated at are the result of equal contributions from the source function , but only over the subset of its domain of definition. This is in contrast to a Fredholm integral equation of the first kind (1.13), in which the source contributes to the data over the entire interval on which the source is defined.

We assume that the integral equation (2.1) has been nondimensionalized. We also assume that , and that the function is defined by a discrete set of measured values, , corresponding to the mesh, , which have been contaminated by random, zero-mean errors

| (2.2) |

such that

| (2.3) |

Here, is the expectation operator, is the -dimensional zero vector, and is the positive definite variance-covariance matrix for . It is also assumed that the measurement errors are statistically independent, so that

| (2.4) |

where are the estimated standard deviations of the errors. In experimental science, these are an integral part of the measurement process. They are typically reported as or error bars on published plots of data [1]. The need not be equally spaced. We take the point of view that we have no control over the mesh size or the mesh spacing, so that, for example, we may not assume that the are Chebyshev nodes. For simplicity, we will assume that the mesh points are equally spaced.

2.1 Discrete Problem

The inverse problem can then be written as a sequence of integral equations,

| (2.5) |

We fully discretize the problem by approximating the integrals (2.5) using the midpoint rule, and get

| (2.6) |

where , and We assume that is small enough to capture the details of , and that

| (2.7) |

The requirement (2.7) guarantees that the discretization error of the midpoint rule, which is O, is much smaller than the measurement errors. Henceforth, we will neglect the discretization error.

Problem (2.6) can be written as

| (2.8) |

where is the lower-triangular, non-singular matrix

| (2.9) |

In the present case, there is no overdetermined linear regression problem to solve. It is straightforward to verify that the inverse of is given by

| (2.10) |

so that an estimate of the source function is obtained by first-order finite-differencing of the noisy data.

2.2 Need for Regularization

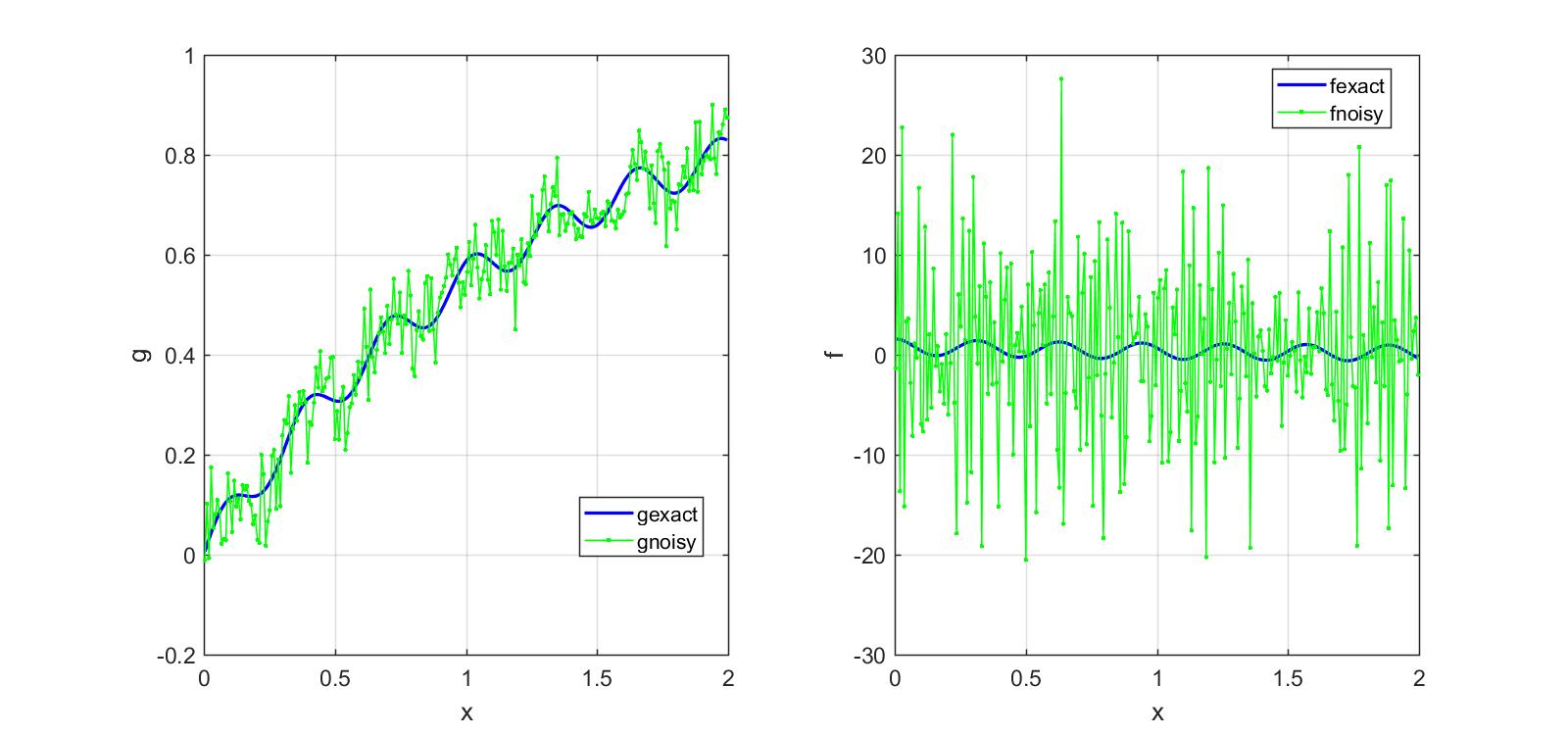

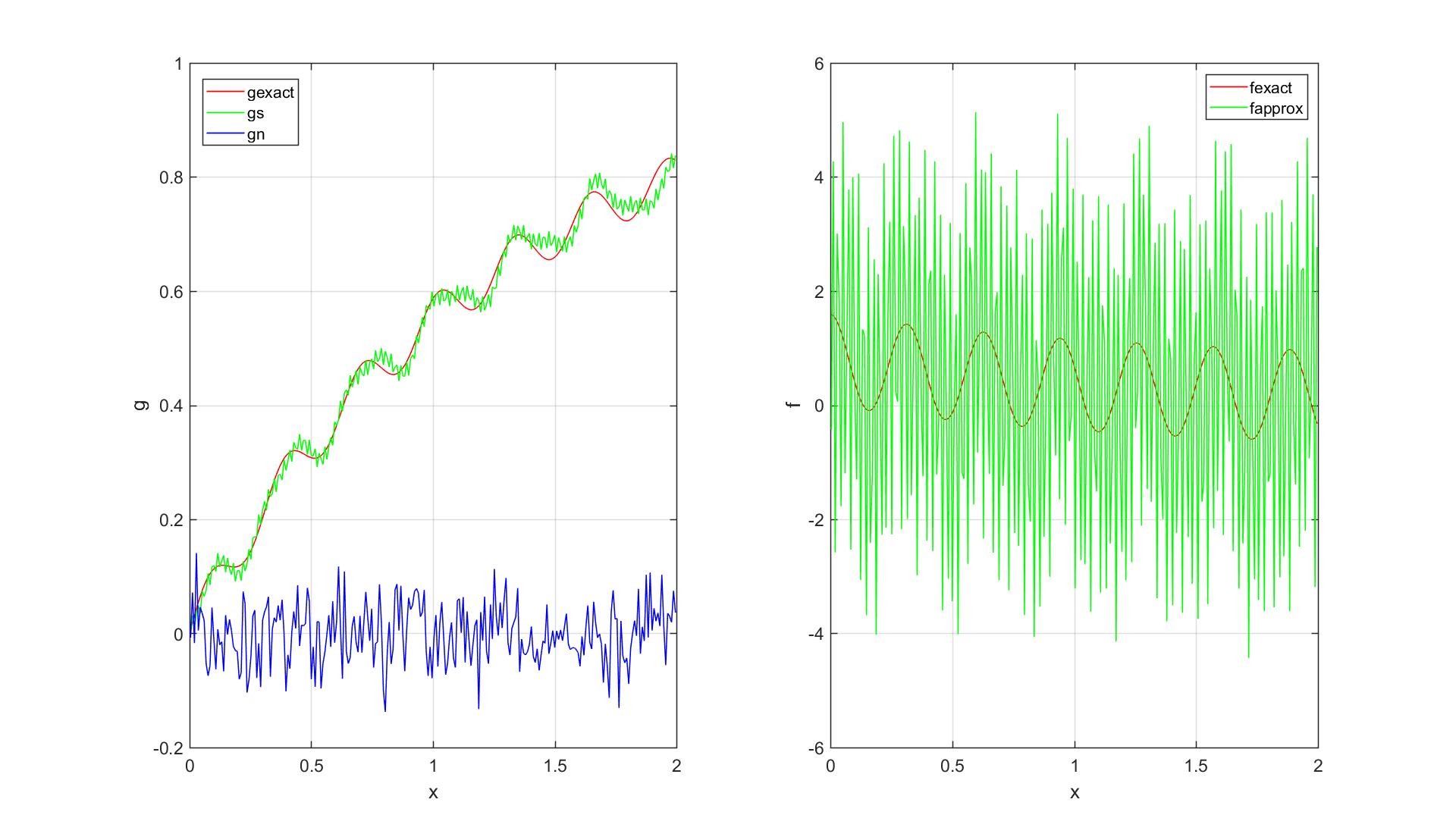

For Case of (1.11)-(1.12) (see Fig. 1), with , , , , and , we perturb each data point as follows. Obtain a pseudorandom sample from a standard normal distribution, using the Matlab function , multiply it by a fixed standard deviation of , and then add this number to . The resulting estimate of is plotted on the right-hand side of Fig. 2. The estimate of the source function is dominated by amplified noise in the data, which is a characteristic feature of an ill-posed problem. It is apparent that some kind of regularization of , i.e., separation of signal from noise in the data, is necessary prior to obtaining an estimate of .

2.3 Scaling the Problem

Rust’s method for regularizing the data begins with scaling the problem. Multiplying both sides of (2.8) by , we get

| (2.11) |

where

| (2.12) |

For the scaled problem (2.11), it follows by a standard theorem of multivariate statistics [2, Thm 2.4.4], that

| (2.13) |

or

| (2.14) |

The considerable advantage that is gained by this scaling can be seen as follows. Let be a discrete estimate of the unknown source function , and let

| (2.15) |

be the corresponding residual vector. Since the regression model can also be written

| (2.16) |

it is clear that an estimate is acceptable only if is a plausible sample from the distribution. An important feature of this approach is that the elements of the residual vector and the true residual vector are considered to be discrete time series, in which the component number is treated as the time variable.

2.4 Diagnostics Based on Statistical Properties of the Residual

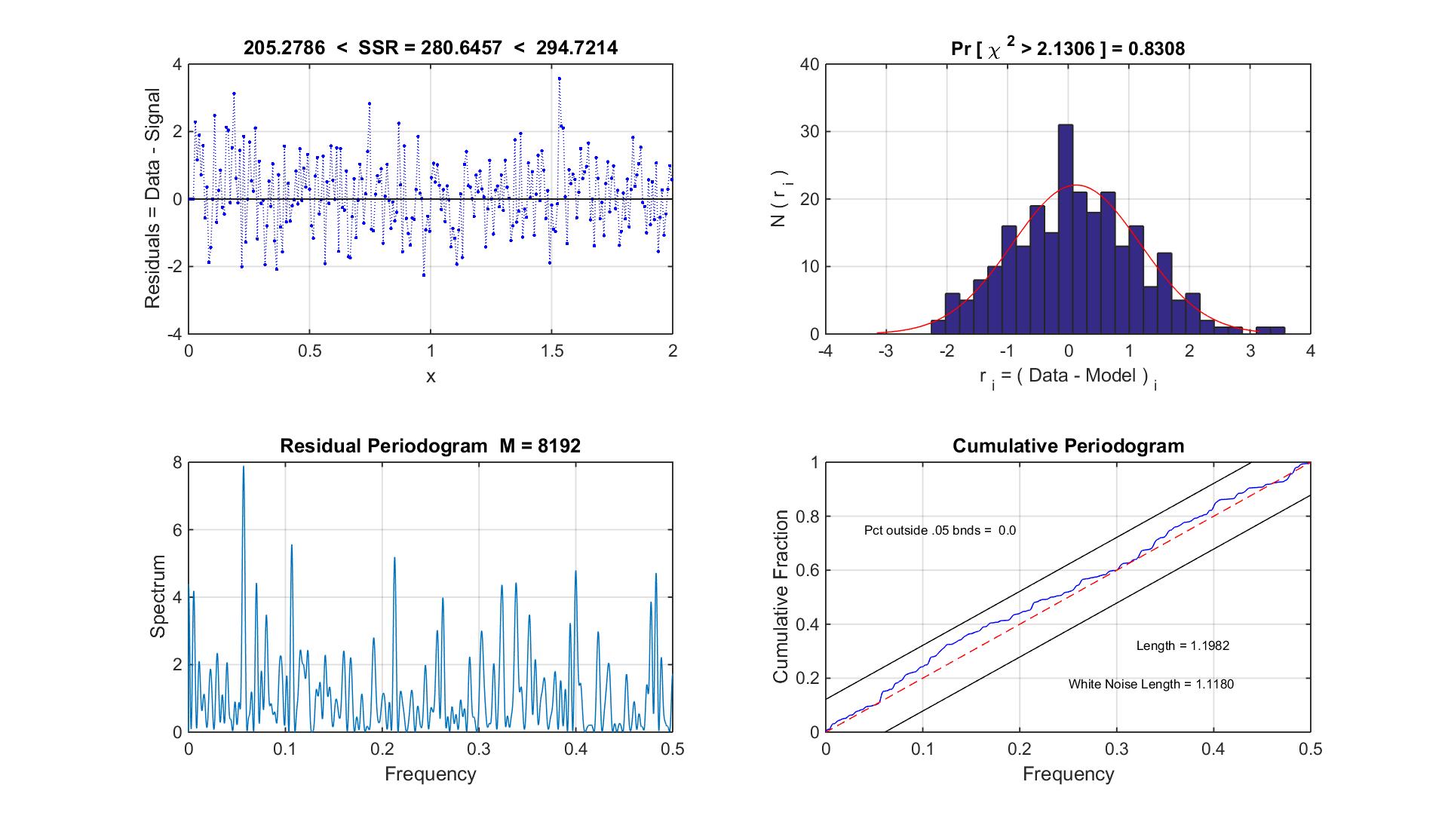

When the source is unknown, the residual vector provides the only objective guide for assessing the quality of an estimate of this function. In the numerical example in Sec. 2.2 (see Fig. 2), , which is much too small. Rust [19] (see also Rust [20], Rust and O’Leary [21]) proposed several diagnostics for judging the acceptability of an estimate with residual . Since the are statistically independent and identically normally distributed, the residuals for an acceptable estimate of the source function should constitute a realization of such a time series.

The first diagnostic is a version of Morozov’s Discrepancy Principle [18], which states that the size of the residual should be comparable to the magnitude of the error in the data. Rust formulated this principle, in the present context, as follows. Since it follows from a standard statistical theorem [15, p 140] that

| (2.17) |

where denotes the chi-square distribution with degrees of freedom. It follows that

| (2.18) |

These two quantities provide rough bounds for the sum of squared residuals that might be expected from a reasonable estimate of . An estimate such that , with , would be quite reasonable, but any whose sum of squared residuals falls outside the bounds with would be suspect. This leads to

Diagnostic 1.

| (2.19) |

Diagnostic 2. The elements of are drawn from a distribution; therefore, a graph of the elements of should look like samples from this distribution. In fact, a histogram of the entries of should look like a bell curve.

A quantititative method for evaluating Diagnostic is the chi-square goodness-of-fit test for a normal distribution [22]. Software for evaluating this criterion is available in the Matlab Statistics toolbox (Matlab function ).

The third diagnostic is based on the periodogram of the residuals, which is an estimate of the spectral density of the residual time series, i.e., it is an estimate of how the total variance in the series is distributed in frequency. A more detailed discussion of this diagnostic is given by Fuller [10, Ch. 7].

To define the periodogram, we first need to define the discrete Fourier transform (DFT). The discrete Fourier transform of the time series data set is defined to be the set of complex numbers , where

where ; the Fourier frequencies , , are harmonics of the fundamental frequency .

The periodogram is defined by

| (2.20) |

where is the smallest integer greater than or equal to . The presence of a sinusoidal cycle in is indicated by a peak in a plot of against the frequencies , , . The amplitude of the peak gives an estimate of the power in that cycle.

The cumulative periodogram is defined by , where , and

| (2.21) |

We note that the are nondecreasing as increases, and that . It can be shown that, for a realization of a white noise time series, a plot of the cumulative periodogram against the frequencies , will fluctuate about the straight line , from to , which corresponds to an ideal white noise series in which the variance is uniformly distributed. This line has length

| (2.22) |

A useful check is to compare with

| (2.23) |

The null hypothesis that the residual series ) represents a realization of white noise can be tested by plotting the two straight lines where is the point for the Kolmogorov-Smirnov statistic for a sample of size . These two lines define a confidence band for white noise.

Diagnostic 3. No more than of the ordinates of a plot of the cumulative periodogram should lie outside the confidence band.

It is convenient to use the FFT algorithm to compute the DFT and the periodogram. We do this by first padding the residual series by zeros, i.e., by choosing to be a convenient power of two, such that , then defining , for , and then re-defining the DFT by

| (2.24) |

so that the new Fourier frequencies are harmonics of the fundamental frequency . The zero-padding increases the density of the frequency mesh, but it does not change the value of the Fourier transform at any given frequency. The periodogram and the cumulative periodogram are computed as before, except that now .

2.5 Separating Signal from Noise in the Data

In the setting of overdetermined least-squares regression, Rust regularized the data by means of a projection method. For the case of the re-scaled problem (2.11) that we consider here, where is an invertible square matrix, the method is as follows. First, compute the singular value decomposition of ,

| (2.25) |

Here, each of the three matrices on the right-hand side is . is orthogonal, and its columns span the range of . In the examples that we have examined, if one plots the corresponding , the vectors appear to become more and more oscillatory as the index increases. In Sec. 4, we will show that this behavior is to be expected for the operators of integration (1.6) and fractional integration (1.1), in an infinite-dimensional Hilbert space setting.

The central matrix in (2.25) is diagonal, . The entries along the main diagonal are the singular values of , all positive numbers, arranged in descending order. is also an orthogonal matrix, with columns that span the domain of .

The next step is to project the data vector onto each of the orthonormal basis vectors of the range of , by multiplying both sides of (2.11) by the matrix , so that

| (2.26) |

Because is an orthogonal matrix, the distribution of each component of the vector is also , and

| (2.27) |

This suggests a practical method for separating signal from noise in the data vector . Project the data vector onto the column vectors of ,

| (2.28) |

where is the standard basis of . To simplify the notation, let

| (2.29) |

Since most experimentalists would be reluctant to claim that a measured value is significantly different from zero if its magnitude does not exceed three standard deviations for the estimated error in the measurement, separate the projected data into signal and noise, respectively, , according to whether or not , for , where .

This is a rule of thumb that we have found to work well in the examples that we have studied. Start with , and then, if necessary, adjust the value of upward or downward, to ensure that Morosov’s discrepancy principle (2.19) is satisfied. We then have the truncation of the scaled data vector,

| (2.30) |

and of the original data vector,

| (2.31) |

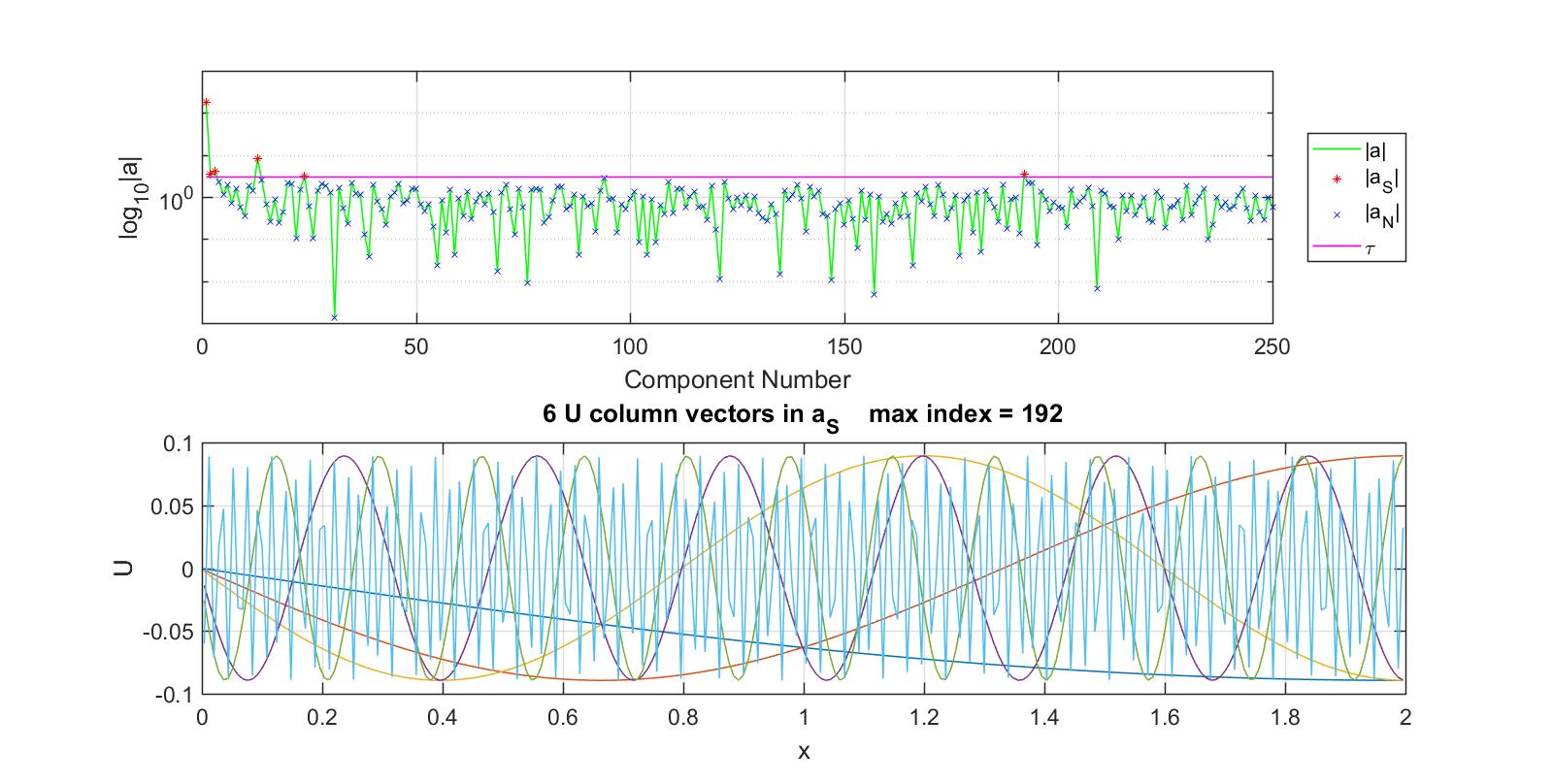

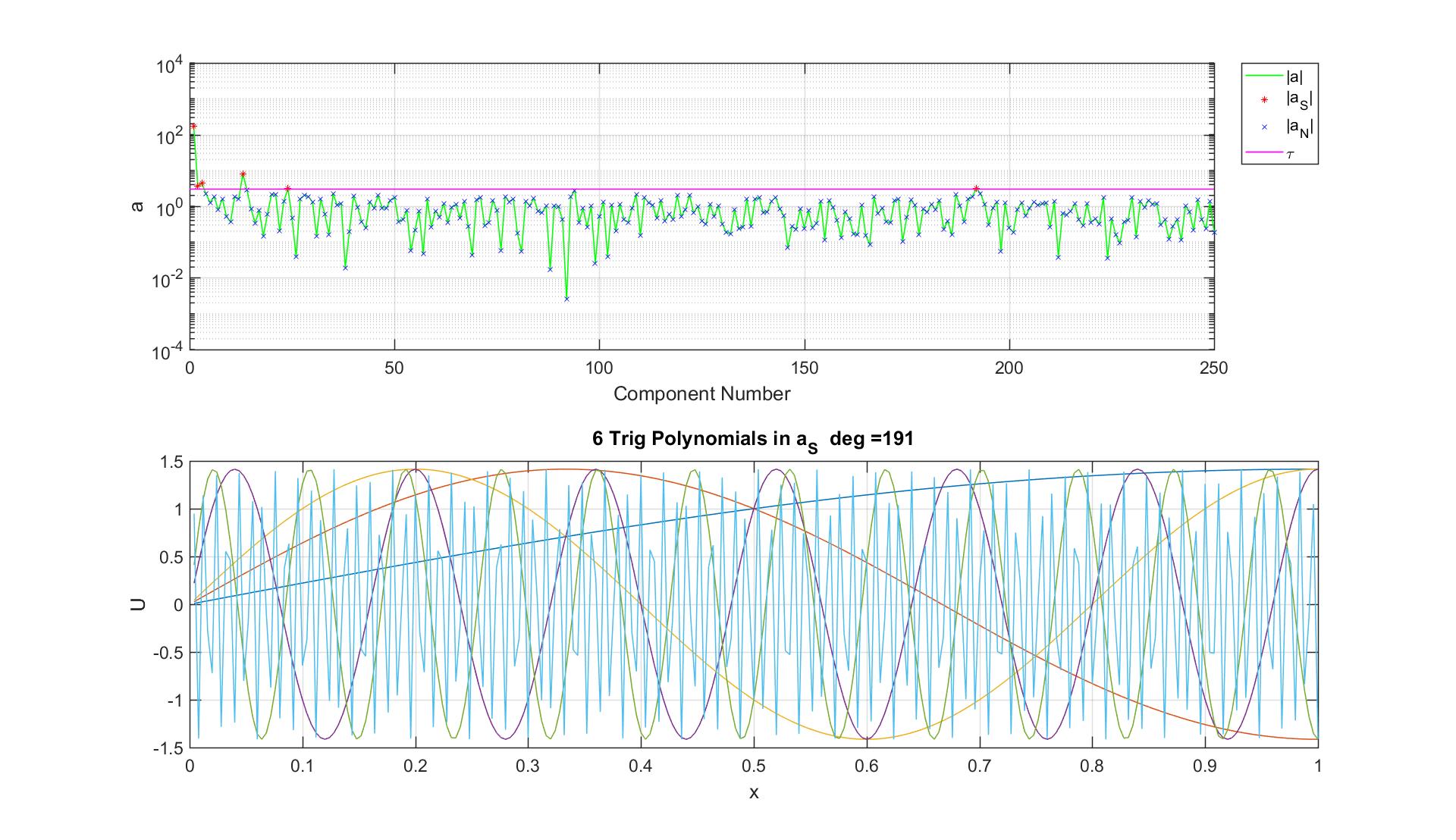

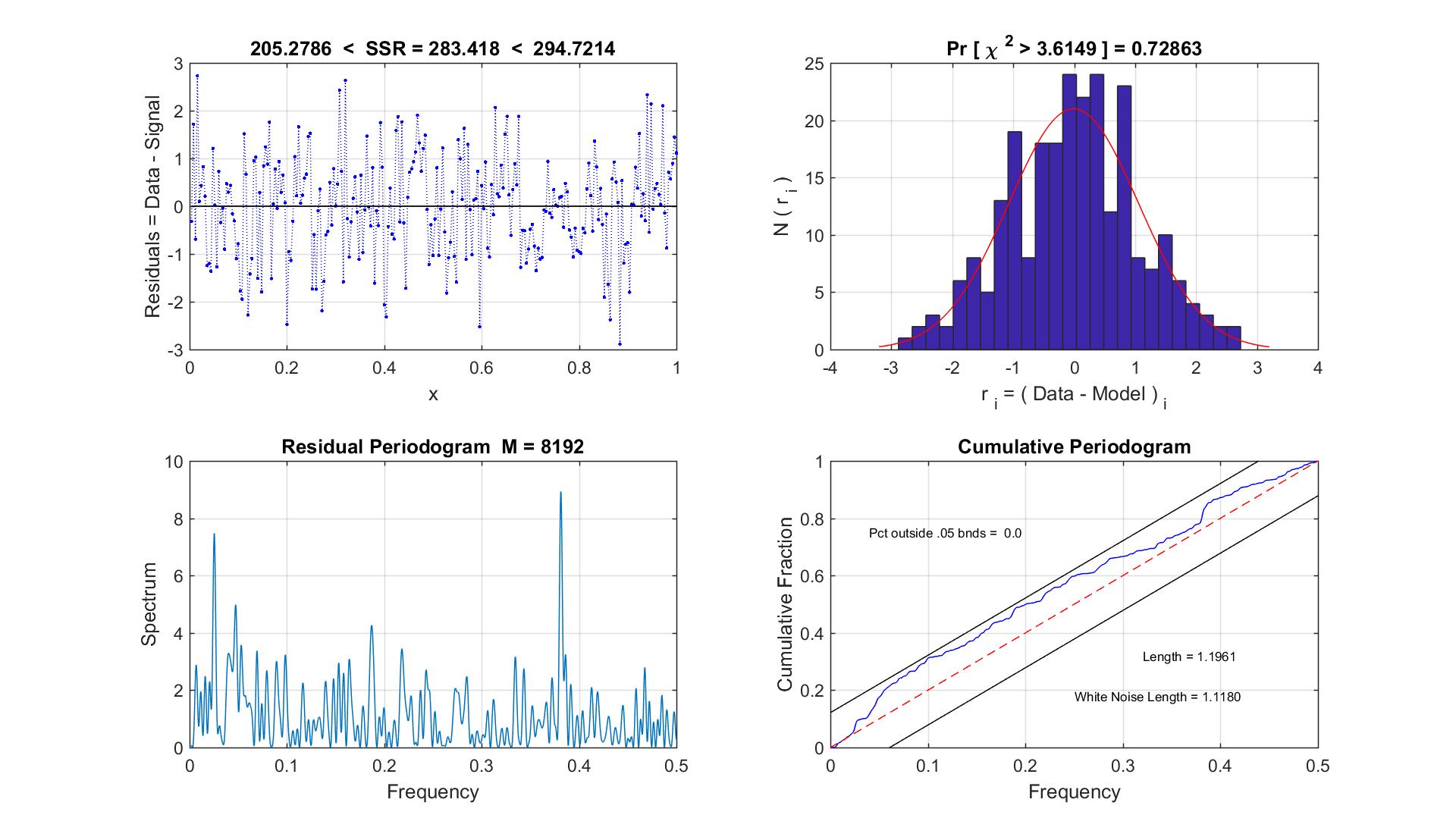

For the problem of Craig and Brown in Fig. 2, with as the boundary between signal and noise in , the lower and upper bounds (2.19) are given by and , respectively. We find that consists of six components, corresponding to the indices and , with the respective values of and ; see Fig. 3. The sum of squared residuals , which satisfies (2.19). It turns out that all of the column vectors of that correspond to the six signal components of are oscillatory. The first five of these oscillate with increasing frequency; see Fig. 3. However, the column of that corresponds to component number oscillates with a much higher frequency than the first five.

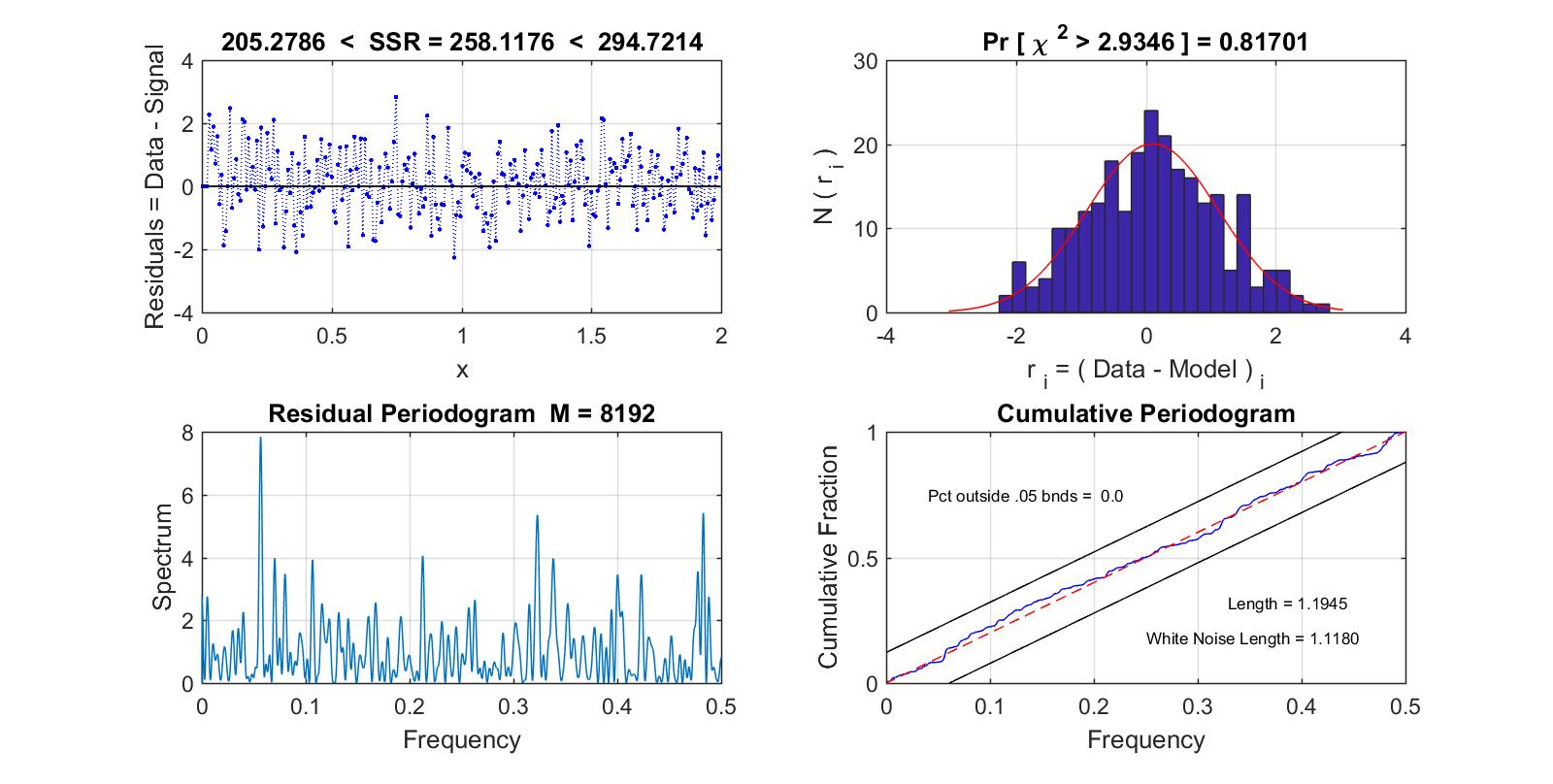

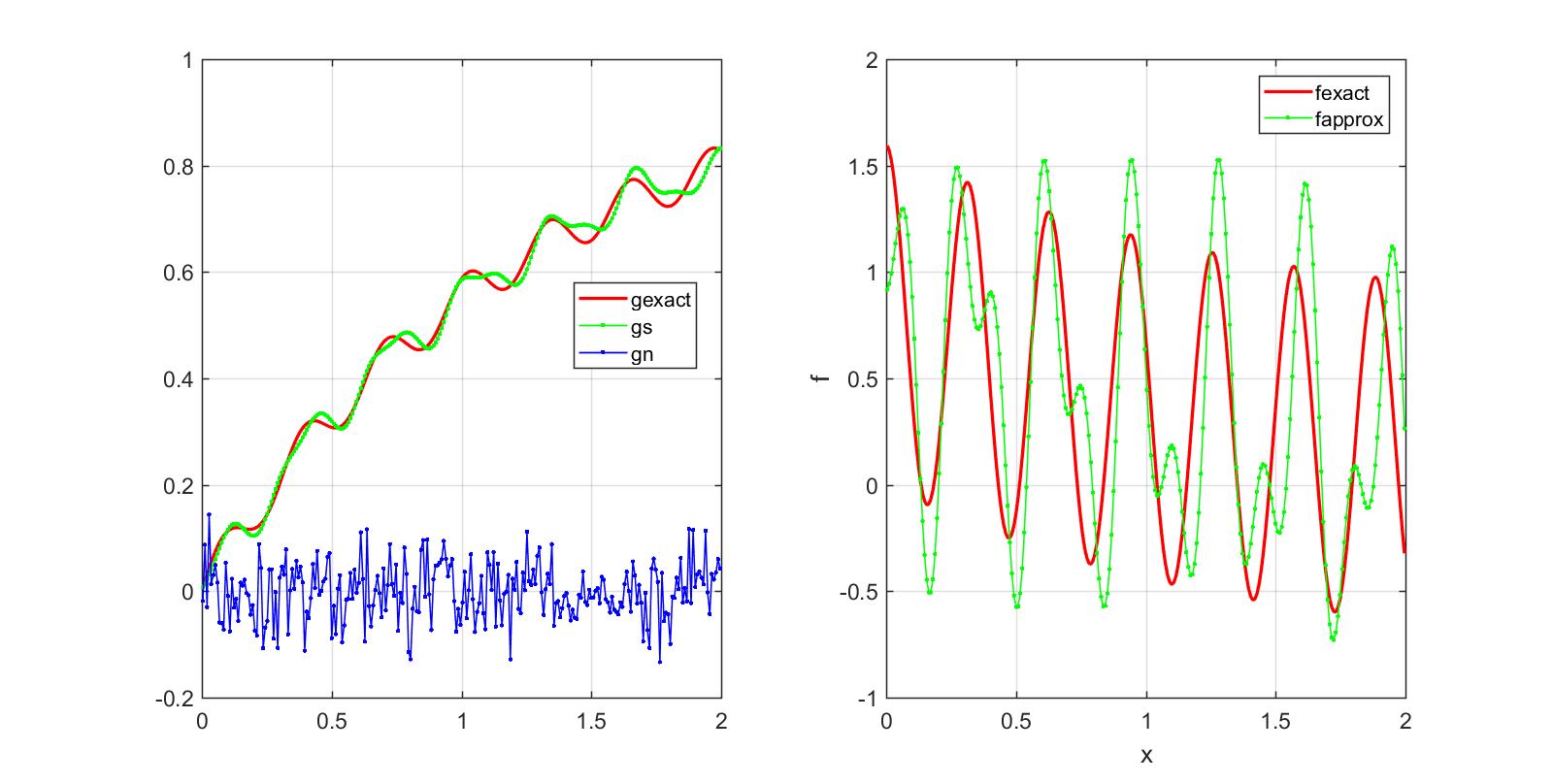

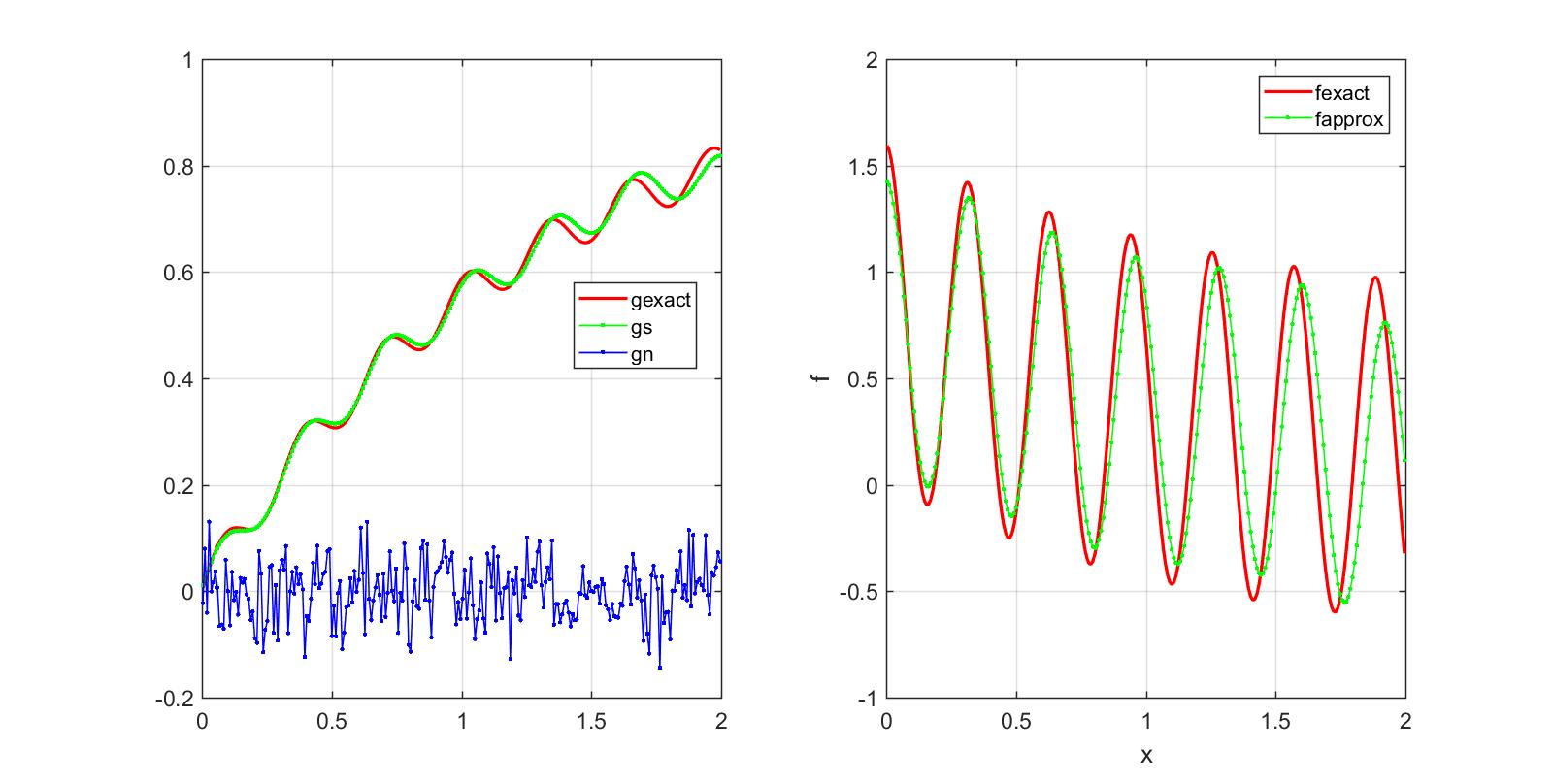

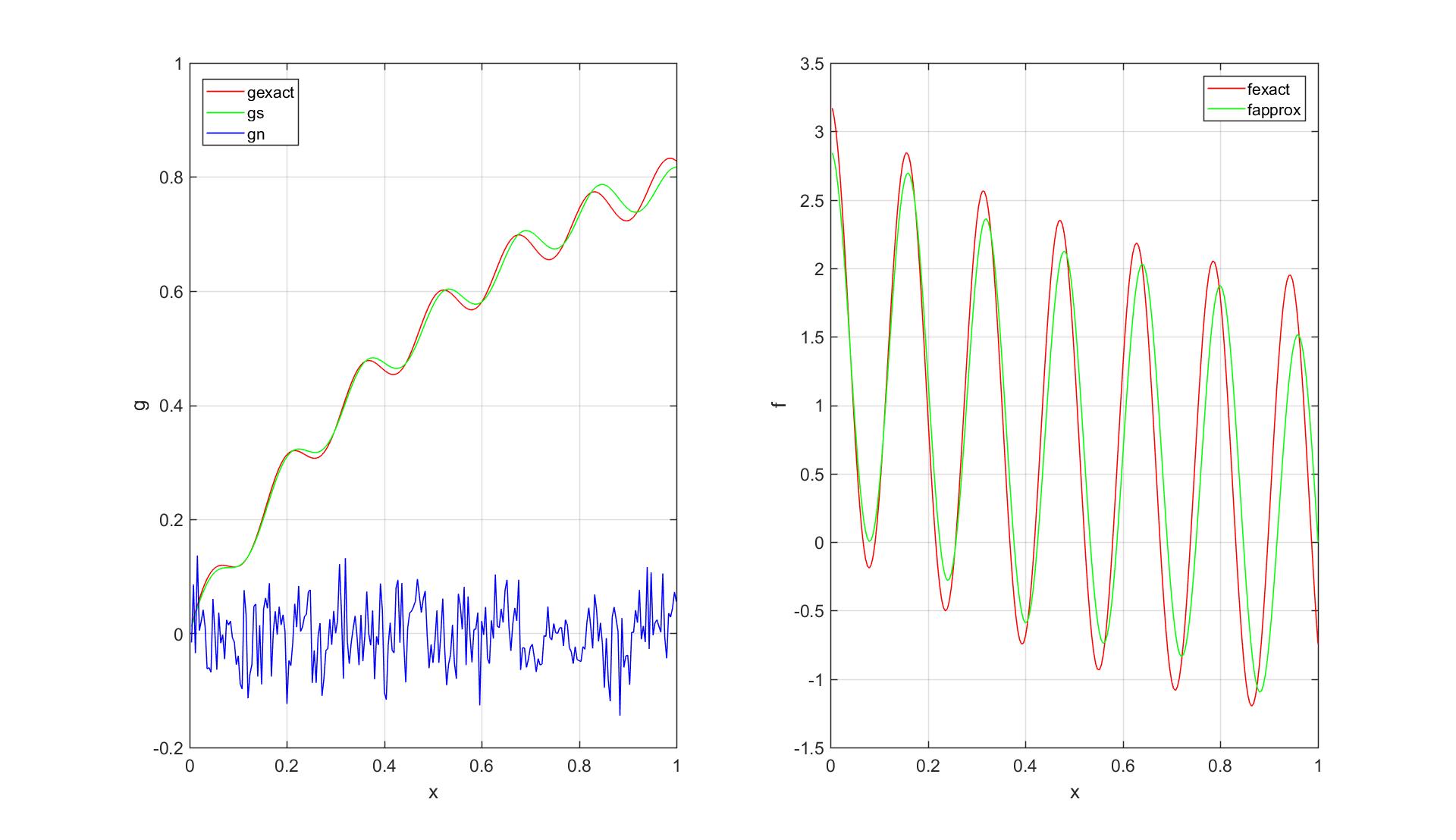

Diagnostics - are summarized in Fig. 4. The three diagnostics indicate that we have found an acceptable truncation of . However, if we just go ahead and estimate the source with high-frequency component included in the signal , we get the results in Fig. 5, which indicate that should have been included in the noise. In fact, in a series of measurements of a standard, normally distributed quantity, a measurement that exceeds three standard deviations will occur roughly once in every terms, which means that the occurrence of one such measurement amongst the higher-frequency components of is not an unlikely event. If we include in , we get the much more satisfactory results in Fig. 6, with the sum of squared residuals now equal to , which still satisfies (2.19). This leads us to add a fourth diagnostic for separating signal from noise in the data.

Diagnostic 4. Even if a higher-frequency component of the projected signal satisfies , include that component in the noise .

Examining the estimate of the source function which corresponds to the regularized data function approximated by the linear combination of columns of , we note that there is a dominant frequency of oscillation, corresponding to , together with an oscillation corresponding to , at almost twice the frequency. Based on the smoothing property (1.10) of the convolution kernel (1.7), we decide also to include in the noise. Alternatively, we could get the same result by adjusting upward to . Including in , we get that the sum of squared residuals is equal to , which still satisfies (2.19). The final results are plotted in Fig. 7 and 8.

In the next section, we will discuss a related projection method for separating signal from noise in a discrete set of noisy data, that is based on closed-form SVD’s of the Hilbert space operators of integration (1.6) and fractional integration (1.1).

3 New Projection Method

In Rust’s method of regularization, as outlined in the preceding section, the orthonormal column vectors of the matrix , which are obtained as part of the discrete SVD (2.25), depend upon the discretization of the infinite-dimensional problem that produces the finite-dimensional full-rank regression matrix . These vectors are ordered by the associated singular values of , , which are listed in order of decreasing size. In this section, for the operators of fractional integration (1.1) and integration (1.6), we will present a different projection method, that will provide a finite-dimensional approximation of , in which the oscillatory behavior of the basis vectors of both the domain and the range of the associated finite-dimensional operator can be characterized in detail. The method is based on the infinite-dimensional version of the SVD for compact linear operators on Hilbert space.

3.1 Singular Value Decomposition

Let and be infinite-dimensional real Hilbert spaces, with respective inner products and , and respective norms and defined by the inner products. Let be an injective compact linear operator, and let be its adjoint. It can be shown [16, Thm. 15.16] that there exists a singular system of the operator , consisting of a nonincreasing sequence of positive numbers with limit as , an orthonormal basis , and a corresponding orthonormal system , such that

| (3.1) |

In addition, for each , we have the Singular Value Decomposition

| (3.2) |

Following Cuer [8], the SVD can be described in “matrix” notation as follows. The action of the operator is a composition of three mappings,

| (3.3) |

such that

| (3.4) |

where is the space of real square-summable sequences, , and

The following theorem is due to Picard [16, Thm. 15.18].

Theorem.

The equation of the first kind

| (3.5) |

is solvable if and only if , and

| (3.6) |

For each satisfying (3.6), the unique solution of is given by

| (3.7) |

Note that the Picard condition (3.6) excludes many functions from , the range of . Suppose that is the solution of (3.5) for some satisfying (3.6). If we add a small perturbation to , , we get that . It follows from (3.7) that can be made arbitrarily large, because the singular values decay to zero as . This demonstrates that equation (3.5) is ill-posed, and it is more ill-posed the faster the singular values of approach zero.

3.2 Projection Method for Integration

It turns out that, for , the singular system for the operator of integration (1.6) has been determined [16, Example 15.19]. It is given by

| (3.8) |

where

| (3.9) |

so that as In this case, the SVD of suggests a natural method for obtaining an approximate solution of .

Define the finite-dimensional subspaces and , as follows,

| (3.10) |

As in Sec. 2, suppose that the smooth function is defined by the noisy data set , corresponding to , and assume that the subspace is unisolvent with respect to these points, i.e., each function in that vanishes at vanishes identically. This is certainly true for the basis functions in in (3.8), so that it is also true for every function in . Then there exists a unique function

| (3.11) |

which is infinitely differentiable on , satisfies , and interpolates the given data,

| (3.12) |

Since is a finite sum, it satisfies (3.6), so that .

The unique set of real coefficients can be determined by solving the matrix equation

| (3.13) |

where

| (3.14) |

so that

| (3.15) |

It follows from (3.7) that an estimate of the source function is given by the finite-dimensional linear combination,

| (3.16) |

which, for the operator of integration (1.6), can be written as follows,

| (3.17) |

where

We are once again faced with the same kind of instability problem that was discussed in Section 2. Because of the ill-posedness of the underlying integral equation, without prior regularization of the data , the estimate (3.17) for the source function would be overwhelmed by amplified high-frequency noise in the data. This amplification results from division of the components in by successively smaller singular values in each case. We will discuss how to resolve these difficulties in Sec. 4. First, however, we want to show how we can use a similar procedure based on the SVD to obtain an estimate for the source function in the case of fractional integration.

3.3 Projection Method for Fractional Integration

It is apparently much less well-known that, for , , , and , Gorenflo and Tuan [12] have determined a family of singular systems for the Abel transform (1.1). In particular, they have shown that, with and , the singular system is given by

| (3.18) |

| (3.19) |

where the are Gegenbauer polynomials of degree , are Jacobi polynomials of degree and

| (3.20) |

We note that

| (3.21) |

where are Legendre polynomials [9, 18.7.9], and that is not differentiable at , .

As before, we determine the unique function that interpolates the data , by solving for the unique set of coefficients , such that

| (3.22) |

This function satisfies , and is smooth on . To do this, we form the analogue of the matrix in (3.14),

| (3.23) |

where , and get

| (3.24) |

For fractional integration, this provides an estimate of the source function , given by the finite linear combination of Legendre polynomials,

| (3.25) |

We must still address the problem of regularizing the noisy data prior to obtaining an estimate of . This will be discussed in the next section.

4 Regularization by Truncated Projection

Our initial goal in this section is to develop a method for separating signal from noise in the data, , which is similar to Rust’s method in Sec. 2, and which also takes advantage of the fact that the SVD’s for integration and fractional integration are known explicitly. We will then show how an extension of this method can be used to regularize discrete sets of data measurements which have been contaminated by random, zero-mean noise, for other applications.

4.1 Regularization Using Closed-Form SVD

As before, we first scale each data point by its estimated standard deviation, and get the scaled data vector . We want to regularize , i.e., we to compute a decomposition , such that captures a sufficient amount of the variance in the data, i.e., such that lies within the bounds (2.19). Rather than do this by computing the discrete singular value decomposition of the matrix in Sec. 3.2 or 3.3 as we did with the matrix in Sec. 2, our approach here is to compute instead its decomposition,

| (4.1) |

Here, is an orthogonal matrix whose columns span , and is an invertible upper triangular matrix. We then project onto the successive orthonormal columns of , and get

| (4.2) |

Because is an orthogonal matrix, . Since the data in vector have been scaled to units of one standard deviation, the same is true of the data in the vector . We proceed as in Sec. 2, and separate into signal and noise, respectively, according to whether or not a component exceeds a specified truncation level, , starting with our rule of thumb, . As we will demonstrate in the next section,

| (4.3) |

is typically significantly smaller than the number of data points .

We thus obtain the decomposition

| (4.4) |

so that we also have the decomposition of the scaled data,

| (4.5) |

and of the original data,

| (4.6) |

We then proceed to construct an estimate (3.16) of the source function, that is based only on . Let

| (4.7) |

A closed-form estimate of the source function is then given by either (3.16) or (3.25).

4.2 Frequency Content of the Data

There is an important consequence of using the factorization (4.1) to separate signal from noise in the scaled, rotated data (4.2), and to determine the coefficients when a closed-form singular system is available for the operator , and the functions and oscillate like orthogonal polynomials of degree on . In this case, each of and has exactly zeros in , so that the number of oscillations of and in increases as increases. As long as we use a decomposition algorithm that does not permute the columns of the original matrix , it follows that, for , each component encodes higher frequency content of the data than the preceding component , as increases. As we will demonstrate in the next section, just as in the example that was presented at the end of Sec. 2, , the signal portion of , is determined by a relatively small subset of the components of , which consists of a few lower-index, lower-frequency components. Since , and , it will follow that the smooth, closed-form function that approximates the data function is formed by a linear combination of only a few lower-index basis functions .

First, however, we want to finish this section by introducing a more general method for regularizing noisy data, that is based on the approach that we have presented in Sec. 4.1, but which does not require the SVD of an operator. This method will provide a smooth, regularized polynomial approximation of a function that is defined by noisy data measurements, with estimated pointwise random errors, for other applications.

4.3 General Method for Regularizing Noisy Data

It is worth noting that, for the purpose of regularizing an unknown smooth function , which is defined only by a finite set of noisy data, the usefulness of having a closed-form SVD for the operator that models the process that produced the data, is that it provides a set of basis functions, which span the range of the operator, and are easy to compute. Using such a basis, for the operators of integration (1.6) and fractional integration (1.1), we have shown in Sec. 4.1 how to construct a smooth, closed-form function , which approximates the unknown data function , in the norm of , for some weight function . We can introduce a different set of smooth basis functions, which will “decouple” our method from any SVD, as follows.

Suppose that we have been given a discrete set of data measurements , corresponding to a subdivision (which does not need to be equally spaced) of , which represent a smooth function . Without loss of generality, we assume that is the interval . Also suppose that the data have been contaminated by random errors , for which it is known that the conditions (2.3) and (2.4) in Sec. 2 are satisfied. Finally, suppose that these data have been generated by some process that smoothes the high-frequency content of the source that produced our data. We can obtain a regularized polynomial approximation of the data function by the following procedure.

Choose a convenient ordered set of Jacobi polynomials of degree , for , which are orthonormal in , where is the appropriate weight function. Denote by the subspace of that is spanned by this set of polynomials. Form the appropriate matrix , as in (3.2) and (3.3), and then compute its factorization. Separate low-frequency signal from higher-frequency noise in the scaled data, by truncating the scaled data, exactly as we have done above, so that we have the decomposition . Then solve for the unique set of coefficients of the -degree polynomial that interpolates the signal portion of the data, .

Without the aid of a singular value decomposition of either a discrete finite-dimensional or a compact infinite-dimensional operator, we have shown how to obtain a smooth, closed-form polynomial function , whose values are easy to compute, and which approximates by interpolating the regularized data on the subdivision . As we will see in the next section, this polynomial is typically of much lower degree than . Furthermore, this method for constructing gives useful information about the frequency content of a given set of measurements. In the next section, we will present the results of some numerical simulations that demonstrate the usefulness of our method of data regularization, and we will also demonstrate the usefulness and simplicity of estimating the source function in (1.6) and (1.1) by means of closed-form singular systems for the respective operators.

5 Numerical Examples

All of the calculations in this paper have been performed on a uniform grid, using the 64-bit Windows version of Matlab (R2017a), and Jacobi polynomials have been evaluated using Matlab software that has been developed by Burkardt [6]. The decompositions have been performed using the Matlab version of Gander’s modification of Rutishauser’s algorithm [11].

Although our focus is on regularizing a function that has been defined by noisy data, we will first study the usefulness of the closed-form SVD expansions for obtaining the derivative of a differentiable function.

5.1 Craig and Brown’s Problem Revisited

As our first example, we revisit Case (a) of the problem of Craig and Brown in Sec. 2. We transform the independent variable , so that the problem is specified on , as follows,

| (5.1) | |||||

| (5.2) |

with the parameter values , , and .

As a check on differentiation using (3.8), we evaluate in (5.1) on the equally-spaced mesh

| (5.3) |

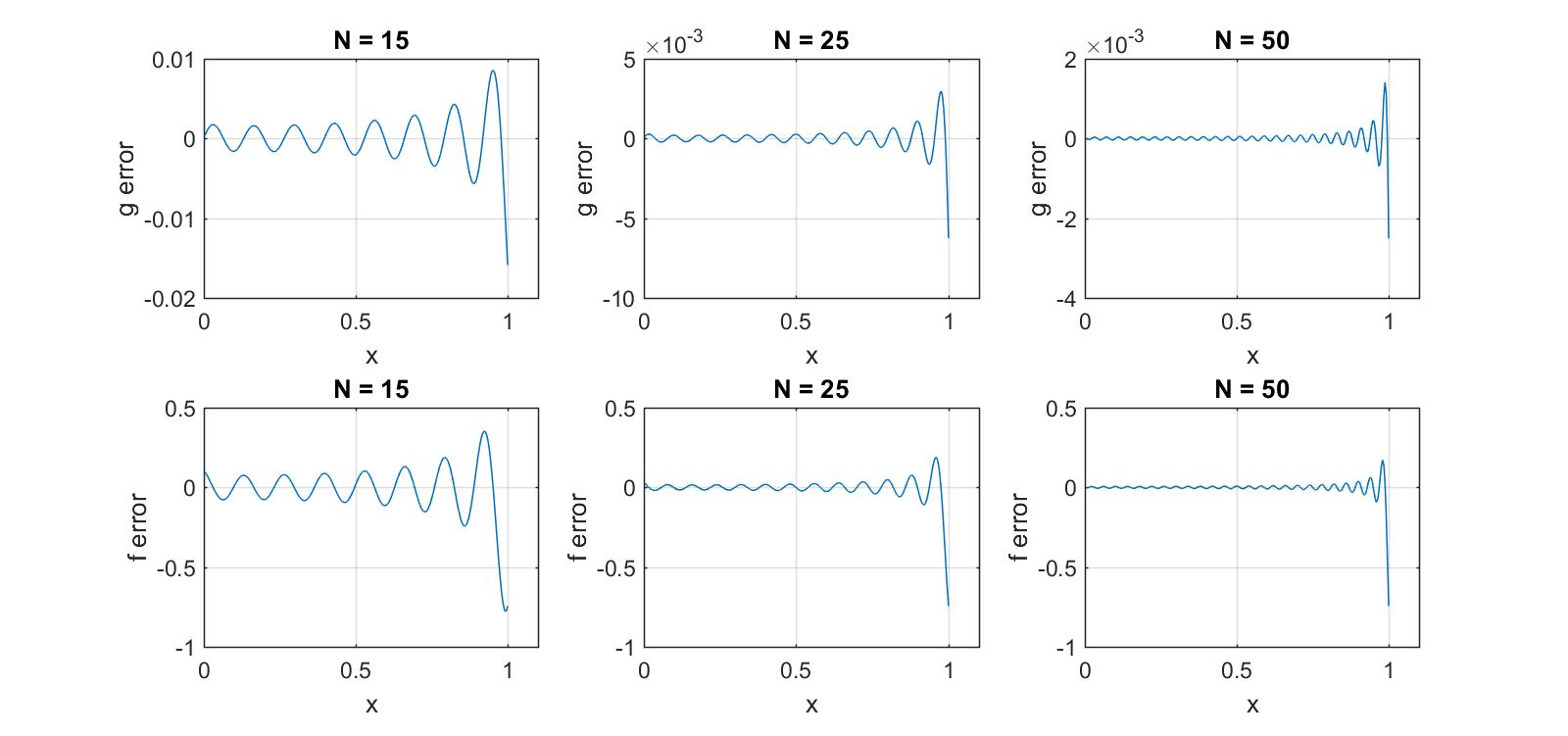

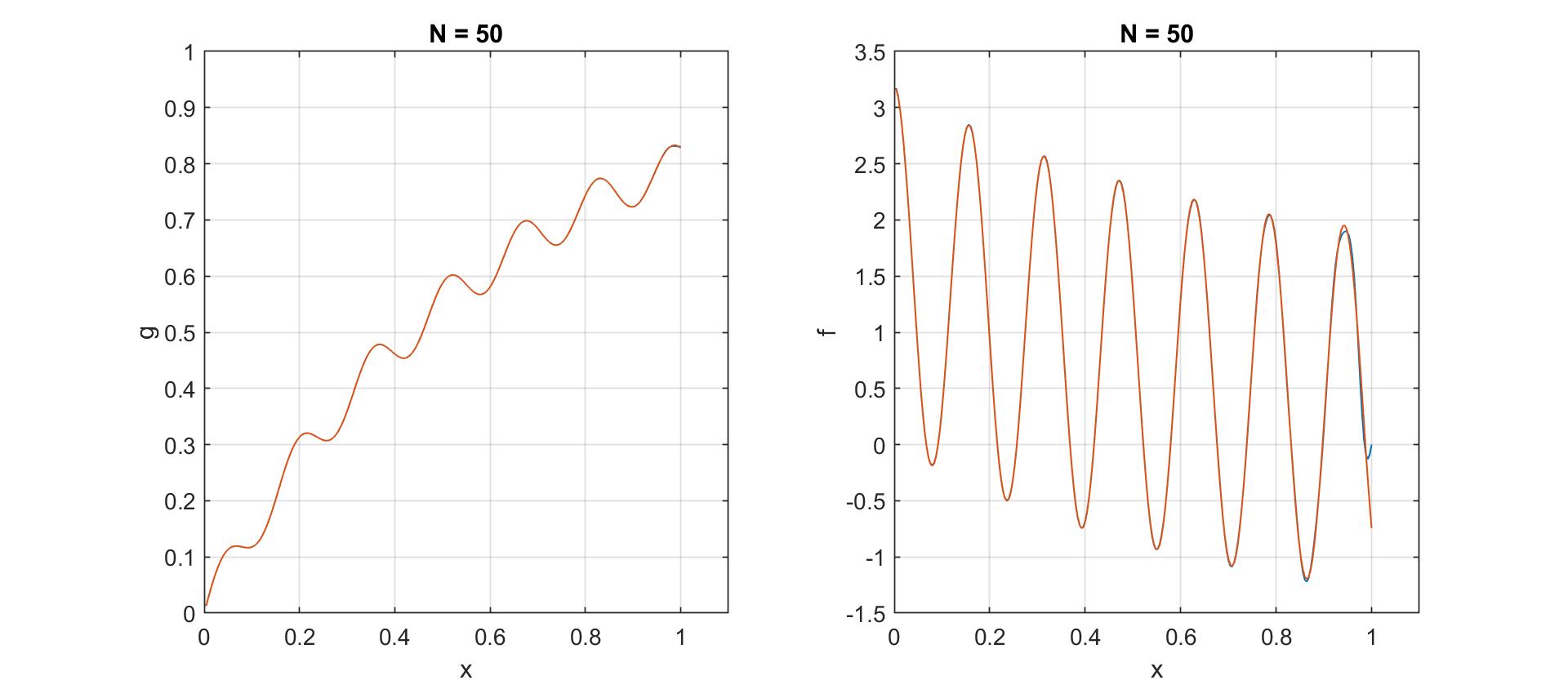

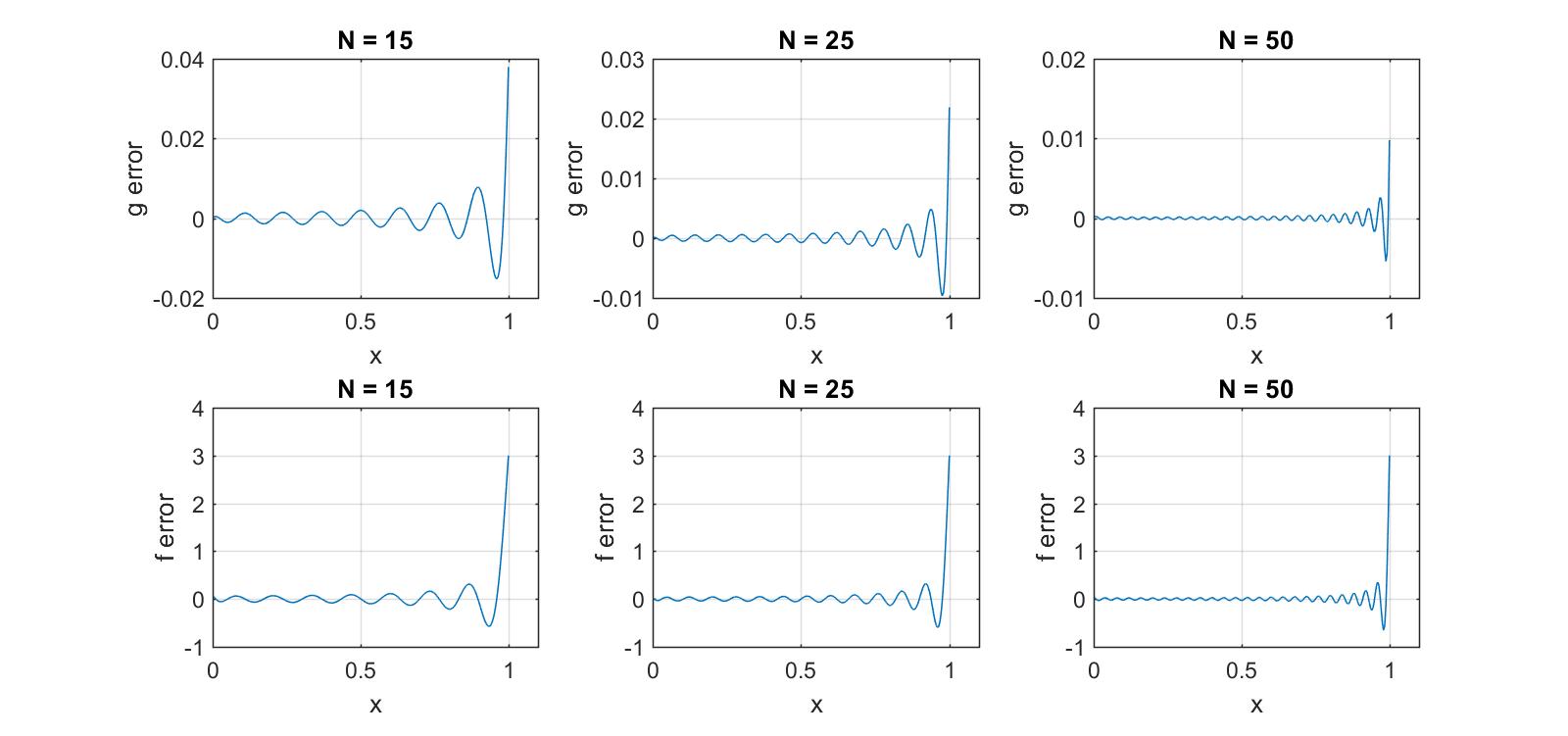

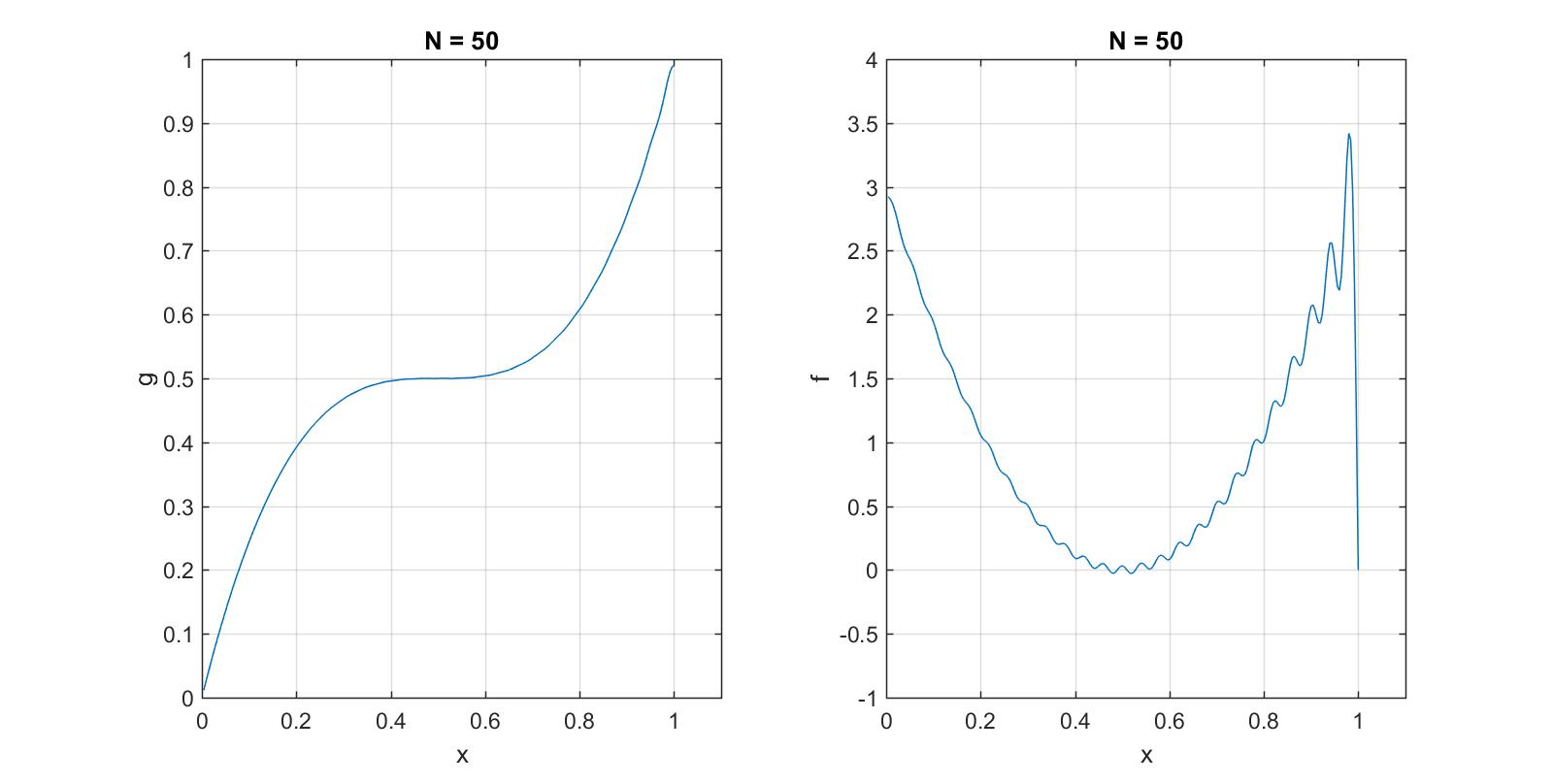

where , for . Note that both and each of the . Furthermore, each of the , and neither nor is periodic on . We interpolate at the points using the first sine functions in (3.8), and then we estimate by , using (3.17) with the first cosine polynomials, for . The corresponding differences between the exact solutions and the polynomial estimates are plotted in Fig. 9. There is nonuniform convergence of the approximation to , and a Gibbs phenomenon in the approximation to , at . By , the approximations are close, except at the right boundary of ; see Fig. 10.

In our second example, just as in Sec. 2, we perturb each data point in the preceding example by obtaining a pseudorandom sample from a standard normal distribution, using the Matlab function , multiplying it by a fixed standard deviation of , and then adding this number to ; the result is depicted on the left-hand side in Fig. 2. We then separate signal from noise in the data, using as the threshold, as described in Sec. 4. The results, which are summarized in Fig. 11, are very similar to those in Fig. 3. Once again, the signal portion of consists of the components , but now the sum of squared residuals is , which is slightly larger than the that was found using the midpoint rule in Sec. 2. We again argue that components should be included in the noise, and we get the results that are summarized in Fig. 12 and 13. Even though the results are similar to those that we have already obtained using the midpoint rule, we have obtained much more information about both the source and the data functions. We now also have simple, closed-form, low-degree trigonometric polynomial approximations for both functions.

5.2 Differentiating a Cubic Function

For our next example, we will estimate the derivative of the cubic function

| (5.4) |

on the same -point grid as before. Before we perturb , we once again check on using the trigonometric SVD expansions for the integration operator, which are given in Sec. 3.2, for and . The differences between the exact and approximate solutions are plotted in Fig. 14. Once again, there is nonuniform convergence in the approximations of , and a Gibbs phenomenon at in the approximations of . Plots of the approximations of and for are given in Fig. 15. Away from the right boundary, the approximation to provides a reasonable approximation of the source function.

If we perturb the data points as above, using the same noise data and as before, we get that the signal components of consist of and ; see Fig. 16. Moving and into the noise, as before, we get approximations of and that consist of the first seven terms in the respective trigonometric polynomial approximations of (3.12) and (3.16). The results are given in Fig. 17. Here, the fact that for each has a significant effect on the estimate of the source function near the right endpoint.

It is interesting to regularize the perturbed data using a different set of basis functions, as has been discussed in Sec. 4.3. We transform Eq. (5.4) to ,

| (5.5) |

and instead of the sine polynomials on that are determined by the SVD of (1.6), we use Legendre polynomials, for the same noise perturbation of the data as above. Again using as a cutoff, we get the separation of signal from noise that is shown in Fig. 19. Here, consists of components and . Once again, we make the decision to include the higher-frequency component in the noise. Since there are closed-form expressions for the derivatives of the Legendre polynomials, we can estimate by simply differentiating the expansion for ,

| (5.6) |

i.e., by computing

| (5.7) |

This gives the results in Fig. 20 and 21. We emphasize two important points here. The first is that regularization of the noisy data function can be treated independently of the associated inverse problem of estimating the source function. The second point is that, once the data have been regularized, there may be better methods for estimating the source function than using the SVD expansion.

5.3 Fractional Differentiation Example

For our next example, we consider an instance of Abel’s equation (1.1) on , with , which is the most frequent case in applications ([7], [13], [3], [4]), for which the exact solution is available [24],

| (5.8) | |||||

| (5.9) |

We note that , and there is a singularity in at . Once again, we begin by checking the SVD expansions for fractional differentiation, as described in Sec. 3.3. The approximations to and using the first terms are essentially indistinguishable; see Fig. 22.

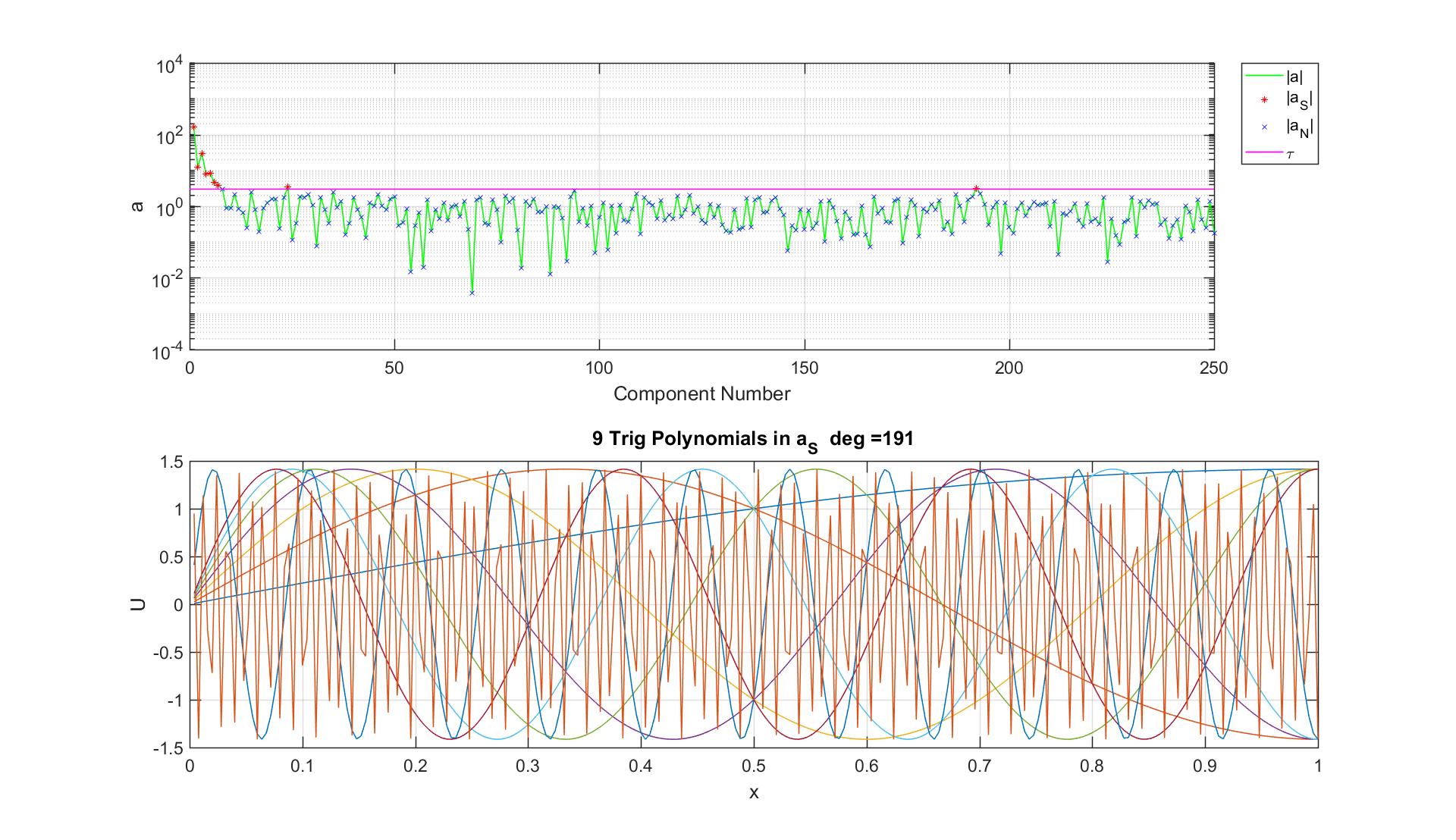

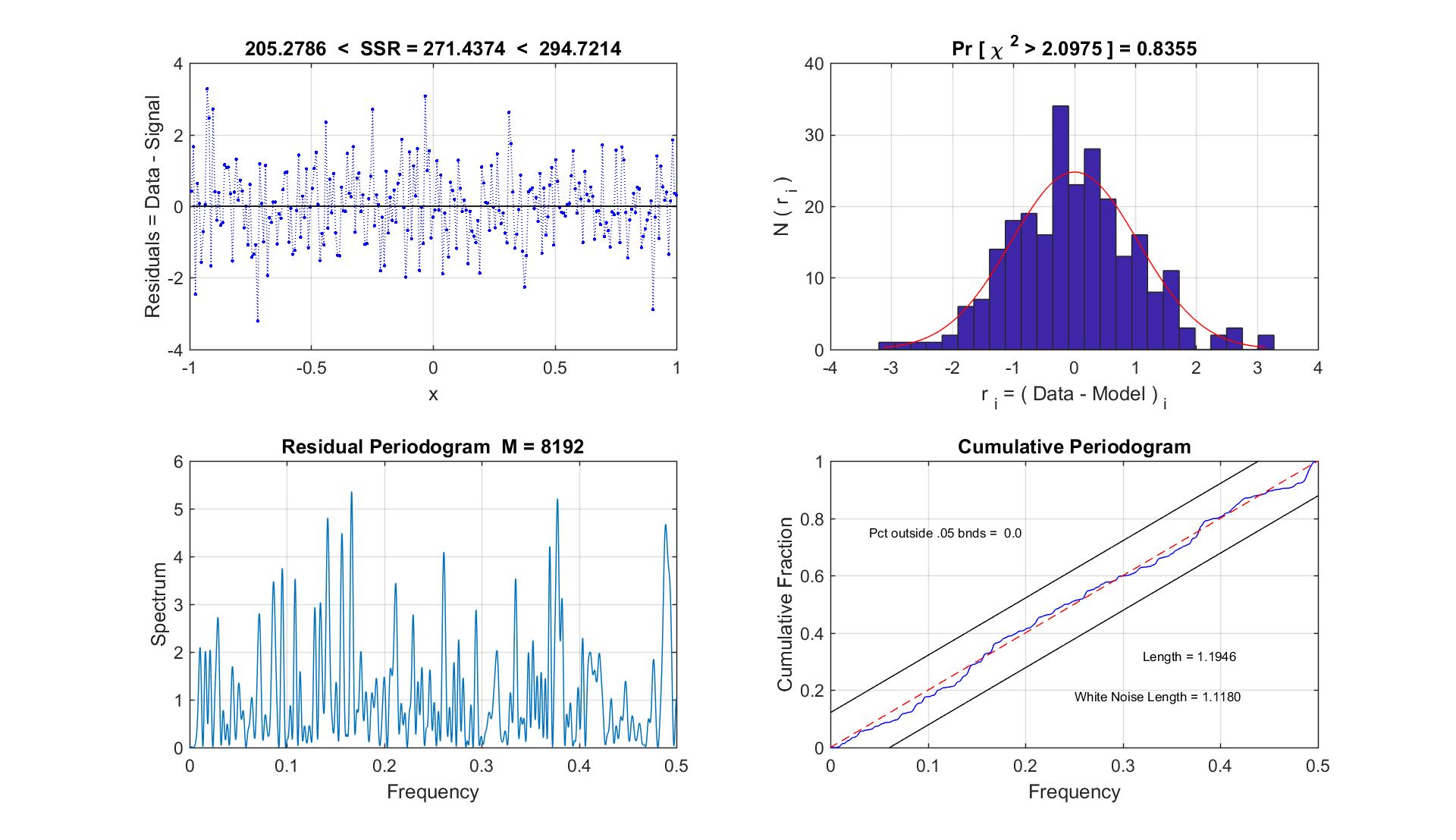

As our last example, we evaluate (5.8) at equally-spaced points , and then we perturb these data at each point, as before, by computing a pseudorandom sample from a standard normal distribution, using the Matlab function , multiplying this number by a fixed standard deviation of , and then adding the result to . Proceeding to separate signal from noise as before, we encounter a difficulty with performing the decomposition of the matrix (3.23), because its condition number blows up as the number of polynomials exceeds about . The workaround we use, which could have been used on all of the earlier examples in which is perturbed by noise, takes advantage of Diagnostic 4 in Sec. 2, which is the assumption that high frequency components of should be included in . Thus, instead of computing the full matrix , we compute the first columns of the matrix, determine the decomposition of this smaller matrix, and then determine the signal components of (see (4.2)) using the resulting smaller matrix, again with the cutoff . The result is summarized in Fig. 23. The signal components identified this way are . Using Diagnostic 4 once more, we decide to include the higher-frequency component in . Using the remaining three components to determine the approximations to and , we get the results in Fig. 24 and 25. Once again, we have determined closed-form approximations, which are easy to compute, for the source and data functions.

As in the case of integration, once the noisy data function has been regularized, there may be a more accurate method for estimating the source function. For example, since we have a closed-form expression for the regularized data function, this function could be evaluated on a denser mesh, that need not be equally spaced, and then a finite-difference estimate could be obtained for (e.g., Linz [17], Brunner and van der Houwen [5]). However, in this case, the estimate would be discrete, and not closed-form.

6 Concluding Remarks

We have presented a new method for regularizing a function that has been defined by a noisy set of measurement data. Our new approach extends a statistical time series method for separating signal from noise in the data that was introduced by Rust, by taking advantage of known closed-form singular value decompositions of the Hilbert space operators of integration and fractional integration. We have shown how to obtain a smooth, closed-form approximation of the data function, in the form of a linear combination of a small number of functions that are either trigonometric polynomials, Jacobi polynomials, or functions which are closely related to Jacobi polynomials, all of low degree. We have also shown how to obtain closed-form estimates of the derivative and fractional derivative of the data function, which are finite linear combinations of trigonometric or Legendre polynomials of low degree.

We would like to acknowledge helpful discussions with Zydrunas Gimbutas and Howard Cohl, and we would like to thank Howard Cohl and Charles Hagwood for detailed comments on the manuscript.

This paper is an official contribution of the National Institute of Standards and Technology and is not subject to copyright in the United States. Commercial products are identified in order to adequately specify certain procedures. In no case does such identification imply recommendation or endorsement by the National Institute of Standards and Technology, nor does it imply that the identified products are necessarily the best available for the purpose.

References

- gum [2008] Guide to the expression of uncertainty in measurement (gum), 2008. URL http://www.bipm.org/en/publications/guides/gum.html.

- Anderson [1958] T. W. Anderson. An Introduction to Multivariate Statistical Analysis. John Wiley and Sons, New York, 1958.

- Anderssen and de Hoog [1990] R. S. Anderssen and F. R. de Hoog. Abel integral equations. In Michael A. Goldberg, editor, Numerical Solution of Integral Equations, chapter 8. Plenum Press, New York, New York, 1990.

- Bracewell [2000] R. N. Bracewell. The Fourier Transform and its Applications. McGraw-Hill, Boston, third edition, 2000.

- Brunner and van der Houwen [1986] H. Brunner and P. J. van der Houwen. The Numerical Solution of Volterra Equations. North-Holland, Amsterdam, New York, 1986.

- Burkardt [2017] J. Burkardt. Matlab source codes, 2017. URL https://people.sc.fsu.edu/~jburkardt/m_src/m_src.html.

- Craig and Brown [1986] I. J. D. Craig and J. C. Brown. Inverse Problems in Astronomy. Adam Hilger, Ltd, Bristol and Boston, 1986.

- Cuer [1987] M. Cuer. An illustrative problem on Abel’s equation. In P. C. Sabatier, editor, Basic Methods of Tomography and Inverse Problems, Malvern Physics Series, 4, pages 643–667. Adam Hilger, Bristol and Philadelphia, 1987.

- [9] DLMF. NIST Digital Library of Mathematical Functions. http://dlmf.nist.gov/, Release 1.0.16 of 2017-09-18. URL http://dlmf.nist.gov/. F. W. J. Olver, A. B. Olde Daalhuis, D. W. Lozier, B. I. Schneider, R. F. Boisvert, C. W. Clark, B. R. Miller and B. V. Saunders, eds.

- Fuller [1976] W. A. Fuller. Introduction to Statistical Time Series. John Wiley and Sons, New York, 1976.

- Gander [1980] W. Gander. Algorithms for the qr-decomposition. Technical Report 80-02, Eidgenoessische Technische Hochschule, Zurich, Switzerland, April 1980.

- Gorenflo and Tuan [1995] R. Gorenflo and K. V. Tuan. Singular value decomposition of fractional integration operators in -spaces with weights. Journal of Inverse and Ill-posed Problems, 3:1–10, 1995.

- Gorenflo and Vessella [1991] R. Gorenflo and S. Vessella. Abel Integral Equations: Analysis and Applications. Lecture Notes in Mathematics (Book 1461). Springer, Berlin, Heidelberg, New York, London, 1991.

- Hansen et al. [2006] P. C. Hansen, M. E. Kilmer, and R. H. Kjeldsen. Exploiting residual information in the parameter choice for discrete ill-posed problems. BIT Numerical Mathematics, 46:41–59, 2006.

- Hogg and Craig [1965] R. V. Hogg and A. T. Craig. Introduction to Mathematical Statistics. Macmillan, New York, second edition, 1965.

- Kress [2014] R. Kress. Linear Integral Equations. Applied Mathematical Sciences. Springer, Berlin, Heidelberg, New York, London, third edition, 2014.

- Linz [1985] P. Linz. Analytical and Numerical Methods for Volterra Equations. SIAM, Philadelphia, Pennsylvania, USA, 1985.

- Morozov [1966] V. A. Morozov. On the solution of functional equations by the method of regularization. Doklady Mathematics, 7(3):414 –417, 1966. ISSN 1064-5624.

- Rust [1998] B. W. Rust. Truncating the singular value decomposition for ill-posed problems. Technical Report NISTIR 6131, National Istitute of Standards and Technology, Gaithersburg, MD, July 1998.

- Rust [2000] B. W. Rust. Parameter selection for constrained solutions to ill-posed problems. Computing Science and Statistics, 32:333–347, 2000.

- Rust and O’Leary [2008] B. W. Rust and D. P. O’Leary. Residual periodograms for choosing regularization parameters for ill-posed problems. Inverse Problems, 24(3):1–30, 2008. doi: 10.1088/0266-5611/24/3/034005.

- Snedecor and Cochran [1989] G. W. Snedecor and W. G. Cochran. Statistical Methods. Iowa State University Press, eighth edition, 1989.

- Wing [1991] G. M. Wing. A Primer on Integral Equations of the First Kind. SIAM, Philadelphia, Pennsylvania, USA, 1991.

- Yousefi [2006] S. A. Yousefi. Numerical solution of Abel’s integral equation by using Legendre wavelets. Applied Mathematics and Computation, 175:574–580, 2006.