Babier et al.

Learning to Optimize Contextually Constrained Problems

Learning to Optimize Contextually Constrained Problems for Real-Time Decision-Generation

Aaron Babier1, Timothy C. Y. Chan1, Adam Diamant2, Rafid Mahmood1

\AFF

1Mechanical & Industrial Engineering, University of Toronto, Toronto, Canada, \EMAIL{ababier, tcychan, rmahmood}@mie.utoronto.ca

2Schulich School of Business, York University, Toronto, Canada, \EMAILadiamant@schulich.yorku.ca

The topic of learning to solve optimization problems has received interest from both the operations research and machine learning communities. In this work, we combine techniques from both fields to address the problem of learning to generate decisions to instances of continuous optimization problems where the feasible set varies with contextual features. We propose a novel framework for training a generative model to estimate optimal decisions by combining interior point methods and adversarial learning, which we further embed within a data generation algorithm. Decisions generated by our model satisfy in-sample and out-of-sample optimality guarantees. Finally, we investigate case studies in portfolio optimization and personalized treatment design, demonstrating that our approach yields advantages over predict-then-optimize and supervised deep learning techniques, respectively.

1 Introduction

Advances in machine learning have led to a growing interest in solving contextual optimization problems whose objective and/or constraints depend on input context features that vary from instance to instance. For example, consider a medical decision making application where the context is a patient’s medical history, current diagnosis, and the results of recent clinical tests, all of which influence the design of a personalized treatment. In this paper, we study contextual optimization problems characterized by three distinct attributes: (i) a large universe of contexts where the relationship between each context and the feasible set requires estimation; (ii) a set of complicating constraints that are controlled by the contexts and make the problem challenging to solve; and (iii) decision-makers or end-users that require high-quality solutions to be generated quickly for incoming contexts. Below, we provide two concrete examples.

Portfolio Optimization. Automated brokers are increasingly used to recommend personalized investment portfolios over web or mobile interfaces (Capponi et al. 2021). (i) A user of the service possesses unique demographic characteristics and risk tolerances that affect the types of portfolios that can be recommended (Bansal and Pachamanova 2019, Li 2020). (ii) The feasible set for each user’s optimization problem may be complex, e.g., containing non-convex cardinality constraints to restrict the number and type of investments that can be held (Kim et al. 2019). (iii) Recommended investment portfolios must be of certifiable quality (Ban et al. 2018) since users receiving unsuitable recommendations may churn. Finally, to be deemed user-responsive, modern web services require low latencies when producing recommendations. For instance, Google estimates each 500 ms delay corresponds to a traffic loss for their mobile applications (Wang et al. 2012).

Personalized Cancer Treatment. Radiation therapy is a widely used cancer treatment modality where treatment quality is typically evaluated on whether it meets target thresholds for a set of clinical performance metrics or criteria (Delaney et al. 2005). Since not all criteria can be satisfied simultaneously in general, oncologists aim to design treatments that satisfy a personalized subset of them. (i) Each patient’s clinical history and medical images are used as context to determine which criteria should be used as constraints in treatment design (Kearney et al. 2018, Babier et al. 2019). (ii) The most commonly used clinical criteria are akin to Value-at-Risk and thus, induce non-convex constraints. (iii) High-quality treatments are essential in achieving good clinical outcomes. Additionally, treatment design needs to be efficient to minimize the delay until treatment initiation, since poor initial designs undergo time-consuming re-planning iterations.

In contextual optimization problems, contexts are often integrated following the ‘predict-then-optimize’ paradigm, which uses machine learning to map a context to an input parameter of an optimization model (see Chan et al. 2012, Angalakudati et al. 2014, Ferreira et al. 2015 for examples and Mišić and Perakis 2020 for a modern survey). However, predict-then-optimize frameworks may be challenging to solve due to the presence of parametric complicating constraints that inhibit efficient solution methods (Campbell and Savelsbergh 2004, Conejo et al. 2006, Boyd et al. 2007). Given the large universe of contexts, solving such optimization problems on-demand can be slow and sensitive to poor estimates of the constraint parameters (Bertsimas et al. 2011). An alternative is to use deep neural networks that learn from context-solution pairs to directly generate solutions to contextual optimization problems without having to solve mathematical programs (see Bengio et al. 2020 and Mazyavkina et al. 2020 for recent surveys). Such approaches benefit from fast decision generation and the ability to estimate complex relationships between contexts and the feasible sets of the corresponding optimization problems, but they also require large data sets for training and often do not provide theoretical guarantees on solution quality (Kotary et al. 2021).

In this paper, we develop an alternative learning-based methodology to solve contextual optimization problems with a linear objective and context-dependent complicating constraints. To accommodate complex relationships between the large number of contexts and their corresponding constraint sets, as well as the need to produce decisions in near real-time, we employ the machine learning paradigm of generating solutions directly from contexts. Our approach consists of:

-

•

A binary classification model (classifier) that, given an input decision and context vector, predicts whether that decision is feasible or infeasible.

-

•

A generative model (generator) that outputs optimal decisions given an input context that is trained using the classifier as a regularizer to penalize the generation of infeasible decisions.

-

•

An active learning loop that uses the outputs of the generative model, which are labeled via a feasibility oracle, to iteratively refine the classifier and generator during training.

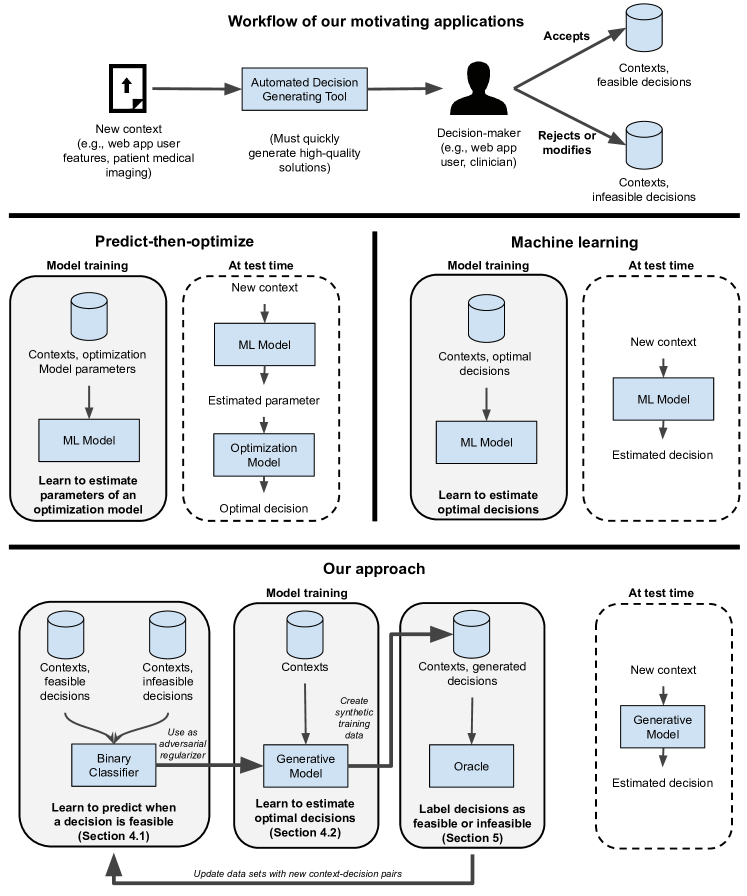

Figure 1 describes our motivating applications, the existing predict-then-optimize and machine learning paradigms, as well as our proposed learning algorithm.

In our approach, we first train a classifier using data on infeasible and feasible solutions to learn a mapping between a contextual input and the feasible region of the corresponding optimization problem. We then use this trained classifier as a regularizer when training a generative model to learn to generate optimal decisions when given a context vector as input. Because learning high-dimensional feasible sets may require large amounts of data, we augment our learning approach by actively generating synthetic decision data using the contexts available in our training set. This synthetic training data is evaluated and labeled as either feasible or infeasible using an “oracle of feasibility”, which can be a look-up-table that uses explicit information on the constraint structure and past feasible decisions as a reference, human decision-makers in-the-loop that manually assess the outputs of the model during training, or a model-based algorithmic labeler. Thus, the classifier and generator are embedded in an active learning loop that ensures the generator learns to produce progressively better solutions for all contexts. After training, our framework will have learned a data-driven representation of the feasible region and how it varies with the contextual input; furthermore, the generator will then be able to quickly generate optimal decisions.

The learning algorithm used to train the generator is analogous to those used for Interior Point Methods (IPMs) in that the classifier acts as a barrier function that penalizes infeasibility. Because the classifier is data-driven, it may not be a perfect representation of the feasible region, which means that classical results on the quality of IPM-generated solutions do not apply. Consequently, we first derive new results in IPM theory by considering barrier functions that are defined over a relaxation of a feasible set; we call these barrier functions -barriers, where refers to the approximate size of this relaxed feasible set. We then develop a new -optimality guarantee for optimization problems that employ -barriers and generalize key properties of IPM algorithms to this setting. Because the classifier is used as a substitute for the -barrier function when training the generator, we prove that the generator inherits in-sample guarantees on prediction accuracy associated with this -optimality property and provide a generalization bound on the out-of-sample -optimality gap of our framework. Finally, we show that our active learning-based algorithm (which we call Interior Point Methods with Adversarial Networks, or IPMAN) produces progressively tighter -optimal solutions by iteratively growing the training data set.

To illustrate the effectiveness of IPMAN, we apply this method to two case studies representing the examples above. In the portfolio optimization application, we collect asset data from multiple exchanges and create a synthetic data set of the demographic characteristics, preferences, and feasible/infeasible decisions made by retail investors. In practice, this set would be collected by deploying a baseline model for a trial group of investors and then observing whether they use the baseline recommendations or reject them. The recorded preferences are also used to create an oracle that labels the decisions generated during training within the active learning loop. We compare IPMAN to an idealized predict-then-optimize baseline, where we predict investor preferences with perfect accuracy and then optimize the portfolio. Our experiments show that IPMAN generates portfolio recommendations with competitive objective function values in an order-of-magnitude less time than a commercial optimization solver. Further, we show that IPMAN is more robust to parameter estimation error compared to the predict-then-optimize baseline.

In the personalized treatment design application, real imaging data and dose distributions are obtained for 217 patients with head-and-neck cancer. By cross-referencing which clinical targets were met by delivered treatments versus those that our models generate during training, we can define a look-up-table-based oracle to evaluate the quality of the generated treatment plans. We compare against two state-of-the-art neural network dose prediction models as baselines and show that IPMAN learns to generate radiation therapy doses that better satisfy clinical constraints as compared to the baseline. We also show that IPMAN can adapt to out-of-sample settings without data by demonstrating that it continues to perform well if the clinical criteria used to evaluate treatment quality change. This analysis models the situation of domain shift where IPMAN is trained on one clinic’s data but applied to patients from a new clinic.

The paper is organized as follows. In Section 3, we present an IPM-based theory for relaxed barrier functions which we call -barriers. In Section 4, we develop our classification and generative models, and establish bounds on the quality of in-sample solutions produced by our generator when using a classifier-based -barrier as a regularizer. Section 5 describes the active learning framework and how feasible and infeasible data are synthesized to iteratively improve the performance of the classifier and generator. We prove a generalization bound on out-of-sample performance in Section 6 and numerically validate IPMAN in Section 7 on the two examples discussed above. We conclude in Section 8 by discussing the nuances of our approach and propose several potential extensions.

1.1 Relationship to Prior Work

In the optimization literature, complicating constraints are typically addressed via decomposition techniques (e.g., Langrangian relaxation, Benders algorithms). Given the generality of the effect that a context may have on the formulation of an optimization problem, there is no guarantee that an optimal solution can be obtained in real-time. Alternatively in our data-driven framework, the feasible set is learned and provably optimal solutions are generated quickly. Active learning iteratively creates new data points which allows the algorithm to explore the feasible region (Settles 2009). Thus, our approach relaxes the mathematical representation of the constraint set and replaces it with a data-driven model trained on past feasible and infeasible decisions.

Our framework uses two predictive models, one to evaluate and one to generate decisions; this is common in reinforcement learning (e.g., actor-critic methods, Konda and Tsitsiklis 2000) and deep learning (e.g., generative adversarial networks, Goodfellow et al. 2014). The objective used to train the generative model is derived from IPMs (Nesterov and Nemirovskii 1994) and our learning guarantees extend previous Rademacher complexity results (Bartlett and Mendelson 2002) for data-driven optimization. Finally, the design of a model to generate decisions is related to the estimation of distribution algorithms commonly used in the black-box optimization literature (Pelikan et al. 2002). We summarize the most relevant related work below.

Interior Point Methods. These algorithms are among the most popular techniques for solving constrained optimization problems (Nesterov and Nemirovskii 1994). IPMs have been primarily applied to linear and quadratic optimization problems where they quickly converge to optimal solutions (Gondzio 2012). Recent results on barriers for arbitrary convex sets have renewed interest in IPMs for general convex optimization (Badenbroek and de Klerk 2018, Bubeck and Eldan 2019). IPMs also exist for non-convex problems (Vanderbei and Shanno 1999, Benson et al. 2004, Hinder and Ye 2018). These papers all assume access to explicit constraints or a barrier that is well-defined for the entire feasible set. Here, we construct a barrier function (i.e., our classifier) that approximates a relaxation of the feasible set and develop an IPM theory for this setting.

Contextual Optimization. The most common approach is the ‘predict-then-optimize’ paradigm, i.e., to construct a parametric optimization model of the decision-making problem and use machine learning to predict parameters from context-dependent inputs (Angalakudati et al. 2014, Ferreira et al. 2015, Elmachtoub and Grigas 2017). A non-parametric alternative is to directly estimate the effect of the context in terms of a conditional stochastic optimization model. For example, a stochastic objective that is conditioned on the context may be characterized by embedding a machine learning model to estimate probability weights on the objective (Kao et al. 2009, Hannah et al. 2010, Ban and Rudin 2018, Bertsimas and Kallus 2019, Bertsimas and McCord 2018).

Our work is most similar to Ban and Rudin (2018) who use Empirical Risk Minimization (ERM) to construct a predictor for the optimal solution to a Newsvendor problem. Because their optimization model is only constrained by the non-negativity of the decision variables, we generalize their result to an arbitrary set of restrictions by incorporating constraint satisfaction via a binary classifier. Bertsimas and Kallus (2019) remark on the challenges of constraint satisfaction when using ERM, and instead, propose a weighted learning framework that estimates the weights (i.e., conditional probability terms) in a sample-average optimization problem. They also prove several generalization results that arise from ERM theory. We extend their generalization bounds to out-of-sample -optimality guarantees, and in particular, to problems where the feasible set depends on the contexts via a relationship that must be estimated.

Deep Learning for Constrained Optimization. Recent advances have spurred interest in using neural networks to solve constrained optimization problems (Bengio et al. 2020). These task-specific models are trained via customized learning algorithms and include supervised learning with a data set of contexts and optimal solutions (Vinyals et al. 2015, Larsen et al. 2018), reinforcement learning (Bello et al. 2017, Kool et al. 2019), and task-based learning (Donti et al. 2017).

Generating a solution via the function call of a neural network is typically faster than solving an optimization problem (see Nair et al. 2018, Kool et al. 2019, for numerical studies). However, a trained model may not guarantee that predicted solutions can satisfy every constraint. There are several potential approaches that address this issue. For instance, training a supervised learning technique on a large data set may help make predictions more accurate (Larsen et al. 2018). An increasingly popular approach is to use a customized class of neural network layers which can directly learn to satisfy first-order KKT conditions for solving a convex problem (Amos and Kolter 2017, Agrawal et al. 2019). Finally, the loss function may be customized to encourage constraint satisfaction (Donti et al. 2017). We train a prediction model using a loss function motivated by IPM theory. This allows us to prove optimality guarantees on the generated solutions. We also relax the assumption that training data must solely consist of optimal solutions for different contexts.

Active Learning. Many operational applications are characterized by data that is scarce or expensive to obtain (Gupta and Rusmevichientong 2020). However, training models with high-dimensional data (e.g., decision vectors in ) requires large data sets (Sun et al. 2017). An increasingly popular approach for learning with limited data is to synthetically generate and label new data (Bastani et al. 2018, Zhang et al. 2021a, b); this is also known as active learning by membership query synthesis (Angluin 1988, Wang et al. 2015). For classification problems, given a means of generating artificial unlabeled data and a labeling oracle, one can iteratively synthesize a training set and re-train a model until it meets a desired performance level (Settles 2009). In our setting, the unlabeled data are context-decision tuples and the labels are feasible/infeasible.

In practice, the oracle can be a heuristic (Zhang et al. 2021b), a black-box (Bastani et al. 2018), or even human decision-makers in-the-training-loop (Castrejon et al. 2017, Emmanouilidis et al. 2019). Note that our use of oracles or humans in-the-loop differs from conventional decision-making settings (Melançon et al. 2021), where they guide an algorithm when solving an optimization problem for a new context. In active learning, oracles are used in model training; at test time, we directly generate a context-dependent decision. Since oracles must label up to thousands of data points during training, we automate rule-based oracles by leveraging prior optimization structure.

2 Problem Definition

In this paper, vectors are denoted in bold and sets in calligraphic. The interior, boundary, and closure of a set are , , and , respectively. The exclusion of from is denoted while . We denote probability distributions with and their supports with . Finally, denotes the -norm.

Let be a decision vector, be a cost vector (we assume without loss of generality that ), and be a context vector (e.g., customer demographics, patient information, decision-maker preferences) from a context space . We consider the problem

where is a feasible set that depends on the context vector via some relationship that must be estimated. Solving this optimization problem is challenging because: (i) the relationship between and must be learned; and (ii) the corresponding context-dependent constraints may induce an optimization problem that is difficult to efficiently solve.

Let be an optimal solution to . Our goal is to train a machine learning model such that given a context vector , it can generate a decision satisfying

| (1) |

for some . To facilitate this learning, we assume access to the following:

-

•

A data set of context vectors .

-

•

A training data set of feasible decisions , where and for all . This data consists of decisions that were implemented in the past by domain experts or recommended by heuristic models and may include multiple decisions for each .

-

•

A training data set of infeasible decisions , where . This data could consist of decisions that were previously proposed but not implemented.

-

•

A polyhedron whose interior bounds all context-dependent feasible sets, i.e., for all . We refer to as bounding constraints.

Knowledge of , which is a relaxation of any feasible set, does not sacrifice the generality of problem . For instance, one can often define a bounding box such that for all if is sufficiently large. A tighter may improve the learning rate of the algorithm. Finally, we make the following assumption on and , to ensure that will always have an optimal solution .

[Compactness] For all , the feasible set is compact and has a non-empty interior. Furthermore, is compact and has a non-empty interior.

3 Interior Point Methods with Approximate Feasible Sets

Before addressing our learning problem, we first develop an optimization theory for solving by extending IPMs to the case where the barrier function may not exactly characterize the feasible region. Consider the problem for a single context vector . We define a barrier function that approximates the feasible region with some error and then propose a barrier optimization problem that produces a solution to with an optimality guarantee. We use this result to provide in-sample and out-of-sample optimality guarantees for our learning approach in Section 4.

For intuition, suppose first that . Here, the feasible set is is a fully-specified polyhedron and we can construct a canonical log-barrier, i.e., , to solve via an IPM (see Nesterov and Nemirovskii 1994). However, when , this log-barrier may incorrectly return finite values for . Thus, to generalize the concept of a barrier over a relaxation of the feasible set, we define a class of functions, which we call -barriers, that are strictly positive for all and are zero for all that are sufficiently far from .

Definition 3.1

For some , let be a neighborhood of . A -barrier is a continuous function that satisfies

A -barrier is a function whose support is a bounded superset of , where relates to the size of this superset. We visualize this and the below properties in Figure 2 (Left).

Remark 3.2

The term is an upper bound on the Hausdorff distance between the feasible set and the support of a function , where this support is a superset of ,

| (2) |

Remark 3.3

Given the set , we can always construct a -barrier for . For instance, let be a normalization factor and consider the function

| (3) |

This function is always bounded between and has support equal to , which is a bounded superset of . Thus, is a -barrier where .

Suppose we have a -barrier for some . Let be a constant corresponding to a regularization parameter and consider the unconstrained barrier optimization problem

| (4) |

We now show that the optimal value of is bounded by the optimal value of .

Theorem 3.4

For any , has an optimal solution . Furthermore, this solution is -optimal for :

| (5) |

where with being a positive constant.

The -optimality inequalities in Theorem 3.4 generalize the classical -optimality (Nesterov and Nemirovskii 1994) to problems where we only possess a relaxation of the feasible set. When , the bounding set is tight and (5) reduces to the classical -optimality bound . The proof of Theorem 3.4 does not require the classical IPM assumptions of coerciveness and self-concordance; the former is replaced with continuity and a compact feasible set, while the latter is only required for polynomial-time optimality guarantees. Similar to classical IPMs, the -optimality of solutions to can be controlled by tuning . Because for a fixed , as goes to , so does . However, is a property characterizing the approximation error of the barrier function and does not change with .

Figure 2 (Right) shows a sequence of solutions for a decreasing set of regularization values . Intuitively, we may expect that when is large (i.e., is also large), may also have a large objective function value and be sub-optimal for . When and are small, may have a small objective function value and could be infeasible for . Although counterexamples may exist if the -barrier has a pathological structure, we show in Section 10 that given a regularity assumption on the -barrier function, we can guarantee that is feasible for a sufficiently large and that as decreases, becomes infeasible. This leads to an interior point algorithm using -barriers that is analogous to classical IPMs.

4 Learning to Optimize with Data-Driven Barrier Functions

The previous section assumes that (i) we have access to a -barrier; and (ii) we optimize over a single context vector . We now relax both assumptions in order to address our core problem of learning to generate for any input . We first develop a function, i.e., a binary classifier, that serves as a data-driven -barrier for any given context vector . We then develop a generative model, or generator, that uses this trained classifier to learn to generate -optimal solutions to for any given .

4.1 Learning a -Barrier Using Classification

Suppose we possess a data set of feasible and infeasible decisions. To create a function that can act as a data-driven -barrier for any , we train a classifier to predict whenever the input decision-context tuples are feasible, i.e., , and otherwise i.e., . After training, the classifier will output larger values when and smaller values when . If for a fixed , the trained classifier outputs positive values for all , and zero for all sufficiently far from , then this function is supported over a relaxation of and is a -barrier for . Figure 3 (Left) visualizes this intuition.

There exists a plethora of models and learning algorithms for developing binary classifiers including logistic regression, decision trees, random forests, and neural networks. We note two main considerations for our task. First, we want the classifier to be differentiable, since later in Section 4.2, we will use it as a -barrier to learn to solve a barrier problem via gradient descent. Second, to produce good approximations of the -barrier for any , we require a model class that can express complex shapes. Given these needs, we employ a neural network classifier.

The most popular approach to training neural network classifiers is by gradient descent and minimizing the Binary Cross Entropy (BCE) loss function (Goodfellow et al. 2016). Therefore, we define the Feasibility Classification Problem as a BCE optimization problem wherein we train to predict as feasible and as infeasible:

| (6) |

In (6), the classifier output (i.e., the estimated likelihood of a decision being feasible) is compared to whether the decision is actually feasible. The objective falls to if the model incorrectly predicts or for any point in or , respectively, but it is maximized when and for all points in and , respectively. Let be a classifier trained by solving .

In addition to BCE being an easy-to-implement approach to training a neural network classifier, we also provide an expectation-level argument as to why this loss function is appropriate. Let be a distribution of feasible pairs (i.e., where ) and let be a distribution of infeasible pairs (i.e., where ) corresponding to empirical data distributions. Then, consider the stochastic version of the Feasibility Classification Problem:

Lemma 4.1

Assume that and have closed and disjoint supports and that includes all continuous functions mapping .

-

1.

There exists a continuous function of where for all and for all that achieves an optimal value of for .

-

2.

If , then for any , the product is a -barrier with .

The first statement is a variation of a result by Arjovsky and Bottou (2017, Theorem 2.1), which demonstrates that an optimal binary classifier trained by minimizing BCE will produce a continuous function that is equal to and over the distributions for each respective class. The second statement indicates that a product of classifiers can be used as a -barrier when trained with a probability distribution over feasible decisions.

Although the Lemma is stated in terms of expected risks over true data distributions, the assumption of closed and disjoint supports is satisfied with empirical data distributions and thus, the lemma holds without loss of generality. Further, Lemma 4.1 assumes that the model class contains all continuous mappings of . This assumption is a sufficient rather than a necessary condition. Finally, although we theoretically require neural networks of infinite size in order to approximate any continuous function classifier (see Hornik 1991), in practice, we simply train a large but finite neural network with a large data set of different contexts and multiple feasible/infeasible decisions per context. Our numerical results show that neural network models with sufficiently high capacity can be trained as high-quality classifiers to approximate -barriers.

4.2 Learning to Generate Solutions to the Data-Driven Barrier Problem

Given a classifier that approximates a -barrier for , we now develop an algorithm for training a generator to learns to output -optimal solutions for any context . Let denote a model class of generators. Let denot a series of steps and let be a regularization parameter where for all . Recall that solving for a decreasing sequence of can produce a sequence of solutions that slowly improve the objective function value until they become infeasible for sufficiently small values of . In an analogous fashion, we train a set of generators over a decreasing sequence of . The sequence of generators for should progressively produce decisions with lower objective function values, but for a sufficiently small value of , the generator may produce infeasible decisions, i.e., . Figure 3 (Right) visualizes this intuition.

Let be the classifier trained in Section 4.1 and be the canonical barrier from (3). We now define the Generative Barrier Problem as an empirical risk minimization problem:

| (7) |

The above equation is the machine learning analogue of (4). The first term is a linear cost with respect to training set decisions outputted by the generator, i.e., the objective of . The second term is the data-driven -barrier, as determined by (6). Similarly to the log-barrier term in (4), it penalizes the objective by discouraging solutions that are far from the feasible set. Thus, the generator learns to produce low-cost decisions that the classifier would predict to be feasible.

We solve for steps to produce different generators similar to IPMs, where we would solve a barrier problem over different steps to obtain solutions with different optimality bounds (see 10 for details on the optimization theory). However, we only need a single model to generate decisions at test time. Once training is complete, we select a particular generator that most often predicts feasible decisions with low objective function values by using a decision maker as an oracle to cross-validate the feasibility of decisions outputted by each model for a hold-out set of context vectors. Thus, can be interpreted as a tuneable regularization parameter.

For each , let be an optimal generator trained by minimizing . To further simplify the above equation, denote as a -barrier defined as the product of two barrier functions. Note that the support of is bounded since is assumed to be compact. This property is needed to prove an in-sample optimality bound below.

To justify training these models via empirical risk minimization of the barrier problem, we show that for a fixed , optimizing ensures that for all in-sample context vectors , the error between the solution generated by and the optimal value of is bounded. That is, the generative model outputs decisions satisfying the optimality guarantee given by (1).

Theorem 4.2

For , let and be the trained generator and product barrier, respectively. For any , let be an optimal solution to . Then, there exists such that

| (8) |

Theorem 4.2 ensures that for any generated decision from an in-sample context vector , the optimality gap is bounded above by the sum of two terms: (i) the empirical error between the optimal solution to and as given in Theorem 3.4; and (ii) a -optimality bound. The value of this bound, and hence the quality of the trained generator , depends on the quality of the classifier. Recall that is effectively a regularization parameter for training . If the classifier is a -barrier for , then selecting an appropriate ensures that the trained generator produces a solution that is arbitrarily close to the optimal value for .

Note that Theorem 4.2 holds independently of Lemma 4.1, meaning that we do not necessarily need a perfect -barrier to achieve a specified bound. However, as the proof of Theorem 4.2 demonstrates, a classifier that satisfies Lemma 4.1 can reduce the size of the term. The proof also demonstrates that, similar to Theorem 3.4, can be calculated using known quantities. However, is a property of the classifier and the feasible set which may not be fully characterized by the barrier function. As a consequence, we may not know the exact value of . The next result demonstrates that we can bound this value as a function of the data set.

Corollary 4.3

For any , in (8) is bounded by .

Corollary 4.3 reveals the key challenge of our learning approach. While we may generate decisions that bound the optimal value by , the size of is dependent on the available training data. Indeed, in order to appropriately train a classifier to be used as a -barrier, we require a significant amount of data that includes both feasible and infeasible decisions. While this setup is typical of many deep learning applications (e.g., the FaceNet system described in Schroff et al. (2015) uses more than samples to train a neural network to verify and recognize faces), many operational applications do not have data sets of this magnitude. Thus, in the next section, we embed the classifier and generator in an active learning framework, which allows us to augment the data used to train our machine learning models.

5 Active Learning with Data-Driven Barrier Functions

The quality of the generator depends on the tightness of , and therefore, on the quality of the classifier . Given data sets of limited size, we can improve our classifier using active learning by iteratively generating synthetic training data, labeling it, and then re-training the model (Zhang et al. 2021b). In our problem, the unlabeled data consists of decision-context pairs . Thus, we must be able to (i) easily label incoming decisions (as either feasible or infeasible decisions for their corresponding context vectors); and (ii) synthesize new decision-context pairs.

Creating and labeling synthetic data is a challenging problem in general. To simplify our task, we leverage the available context vectors and only synthesize new decision vectors using the existing generators trained in Section 4.2. Thus, our synthetic data consists of pairs for each and we need only to determine whether a decision generated for a context is feasible. We first discuss how to create a labeling oracle by leveraging a priori knowledge of . We then present our active learning-based algorithm previewed in Figure 1 (Bottom).

5.1 Constructing a Labeling Oracle

Given a trained generator and , we require a means of determining whether is feasible or infeasible, i.e., a function that gives if and otherwise for any and . From the active learning literature, the most intuitive choice for is to employ human labelers. For example, AI companies building image classifiers will use Mechanical Turks to label image data (Liao et al. 2021). However, due to the amount of data that is labeled in active learning, it is often advantageous to use automated labeling techniques via heuristics or black-box functions (Wu et al. 2015, Zhang et al. 2021b, Bastani et al. 2018).

While our learning approach does not assume any specific structure for , we can leverage structural knowledge of the constraints and feasible decision data set to construct an automated, data-driven labeling function. We discuss two examples, which are later used in our case studies, that assume is composed of a set of inequality constraints, where the left-hand-side, , are a priori known functions of the decision , but the right-hand-side, , are functions of the context that must be estimated. Note that both and may be non-convex functions of and , respectively. In our portfolio optimization case study (Section 7.1), is the expected risk of a portfolio , while represents the risk tolerance of an investor characterized by demographic features .

Example 5.1 (Look-Up-Table Constraints)

To collect , , and , we may deploy a baseline generator for a small trial group of users and observe whether they accept or reject the produced decisions (see Figure 1 Top). At the end of the trial period, we query these users to collect their specific values for with respect to the constraint functions . Then during model training, we can label generated for via the following look-up table:

Alternatively, in our personalized cancer treatment case study (Section 7.2), can be a clinical performance measure or criterion of a treatment protocol, while represents how important the criterion is given the particular patient context.

Example 5.2 (On-off constraints)

Suppose we know a priori that for all , where . For instance, this can represent scenarios where a constraint is either “on” () or “off” () depending on the context. Given a context-decision pair , we can estimate by evaluating whether satisfies . That is, for any such that there exists , a labeling oracle can determine feasibility for a new by evaluating

The oracles presented above leverage the general structure of to automatically determine whether a decision is feasible. The primary advantage of using this approach is that because oracles can be called a large number of times during training, labeling can be performed efficiently. One disadvantage is that these oracles may mislabel the synthetic data points. While we develop theory assuming a perfect feasibility oracle, we demonstrate in our numerical experiments that our approach is robust to erroneous or noisy oracles that may misclassify artifically generated points.

5.2 Interior Point Methods with Adversarial Networks (IPMAN)

We now present the complete learning algorithm shown in Figure 1 (Bottom), which leverages active learning in conjunction with the Feasibility Classification and Generative Barrier Problems. In each iteration of the IPMAN algorithm, we train a classifier and a generator in succession as described in Section 4. Then, for each context , we use the trained generator to produce decisions. These new data points are labeled and then added to the existing data sets of feasible and infeasible decisions. Let index the -th iteration of training and let superscript index the model and data sets after the conclusion of the -th iteration (see Algorithm 1).

In the -th iteration, the classifier is trained with feasible and infeasible data sets and , respectively, which are larger than the data sets and due to the labeling procedure described in Section 5.1. Because of this data augmentation step, the optimal solution set of the Feasibility Classification Problem can be shown to contract after each iteration, i.e., represents a tighter approximation to than .

Proposition 5.3

Assume that contains all continuous functions mapping . For any , let be the optimal solution set of . Then, .

Proposition 5.3 demonstrates that by iteratively increasing the amount of available data using the oracle, we can contract the optimal solution set. Because the sets are augmented with correctly labeled data (assuming a perfect oracle), data augmentation removes classifiers whose supports are looser approximations to the different . Intuitively, it allows the classifier to correct regions it had previously mislabeled as feasible and reinforce regions it had correctly labeled so that it does not incorrectly mislabel them in future iterations. Figure 4 visualizes this behavior; the black classifier is a tighter approximation of than the gray classifier due to the additional points.

Proposition 5.3 assumes that all synthetic data is correctly labeled (i.e., a perfect oracle of feasibility), whereas it is possible that oracles may mislabel new data points. If is a noisy oracle, our data sets and may contain noisy labels for classification. We briefly remark that we can use algorithms from the deep learning literature on classification with noisy labels, which modify the BCE loss in to account for this (Natarajan et al. 2013, Li et al. 2017, Han et al. 2019). Furthermore, our numerical experiments evaluate of the effect of a noisy oracle to show that our generative model is robust to a modest degree of misclassification.

6 Generalization of -Optimality to Out-of-sample Instances

In this section, we analyze the potential of IPMAN, or any machine learning model used to generate solutions to contextually constrained optimization problems, to obtain -optimal solutions when given an out-of-sample context vector . To this end, we assume there exists a probability distribution over context vectors and that the data set of context vectors is sampled i.i.d. according to . We then use Rademacher complexity theory to obtain a probabilistic bound on the empirical error from an out-of-sample input (Bartlett and Mendelson 2002).

Definition 6.1 (Bertsimas and Kallus (2019))

Let be a function class and be an i.i.d. data set. The empirical multivariate Rademacher complexity of is

where is an -dimensional vector of i.i.d. Rademacher variables. The multivariate Rademacher complexity of is .

In statistical learning theory, Rademacher complexities are used to generate risk bounds that are dependent on the class of learning model that is used and the training data (Bartlett and Mendelson 2002). Bertsimas and Kallus (2019) apply the theory to develop generalization bounds for producing decisions to problems with a conditional stochastic optimization objective. We extend their work by providing a probabilistic bound on -optimality when the feasible set is estimated. Typically, more complex model classes are required to learn more complex relationships. The IPMAN algorithm is agnostic to the class of model used. However, if we need a tight generalization bound, we should use a model class with a tightly bounded Rademacher complexity.

Remark 6.2

Although the literature mostly focuses on the univariate Rademacher complexity, Maurer (2016) and Bertsimas and Kallus (2019) prove bounds for linear multivariate classes (e.g., ). In general, if , then , where and is the -th identity vector. Then, decomposes to a sum of univariate complexities. We refer to Bartlett and Mendelson (2002) for bounds on linear and tree models and Bartlett and Mendelson (2002), Neyshabur et al. (2015) and Foster et al. (2018) for neural networks.

For the ease of theory, we assume that our generator is trained by minimizing with a -barrier for some . Note that since we are using a fixed data set , there is no guarantee that will be feasible or even satisfy for an arbitrary . Because is available, however, we can always project any generated solution to the polyhedron to ensure that the generated decisions are bounded. {assumption} Consider a -barrier and generator trained via . We use projections at test time.

Our generalization bound follows from Bertsimas and Kallus (2019). While they derive an empirical risk bound on an unconstrained stochastic optimization problem, we focus on -optimality for a constrained continuous optimization problem (see 11 for the proof and discussion).

Theorem 6.3

Let satisfy Assumption 6, and be sufficiently large positive constants, and fix . Then, for any , the following inequality holds

with probability at least with respect to the sampling of .

Theorem 6.3 bounds the -optimality of a random context vector. Given a and , it computes the probability that the model will predict a -optimal solution for an out-of-sample context vector . The first term , is the empirical error associated with solving versus for all . It effectively measures how well the model performs in-sample. The second term is dependent on the constants and and scales with . Thus, as the size of the data set increases, the smaller this term becomes. The third term is dependent the Rademacher complexity of , where the greater the representative capacity of the learning model, the larger its Rademacher complexity. The summation of these terms is a lower bound on the probability of producing optimal decisions for unseen instances and holds with probability at least . Thus, in order to obtain a tight bound, we must balance the trade-off between a model class with high complexity versus obtaining a model with low error.

7 Case Studies

In this section, we perform two numerical case studies where we compare IPMAN to state-of-the-art optimization and deep learning baselines, respectively. In the first set of experiments, we consider an online automated investment service whose users require investment strategies with personalized risk tolerances and investment quotas (Vielma et al. 2017, Swezey and Charron 2018, Li 2020, Bertsimas and Cory-Wright 2022). First-time investors, who represent the target market of these services, may not be able to accurately identify their ideal investment preferences and incorporate them as parameters into a portfolio optimization problem. The conventional solution is to estimate the parameters from user profiles or questionnaires and then solve an optimization problem. However, online services typically require latencies of less than 500 milliseconds (Wang et al. 2012, Crankshaw et al. 2015, Zhao et al. 2018), and a mobile service employing mathematical programming for real-time user interfacing will likely be too slow, especially if the optimization problem has complicating constraints. Instead, we train IPMAN to generate decisions that replicate the performance of an industrial-strength optimization solver such as Gurobi (Gurobi Optimization 2020). This model can then be deployed by an online service to produce high-quality solutions to a contextual, non-convex optimization problem in milliseconds. We find that:

-

1.

IPMAN-trained models generate portfolios in approximately 130 ms, while a predict-then-optimize baseline often requires up to 100 s. Moreover, on average, the portfolios generated by IPMAN are within a optimality gap of a predict-then-optimize baseline that perfectly predicts parameters for every context. Thus, we find that IPMAN is competitive with optimistic optimization baselines that are tuned to quickly generate solutions.

-

2.

The quality of decisions produced by predict-then-optimize approaches are sensitive to estimation errors in the prediction of the constraint parameters. Those solutions are often infeasible with respect to the true constraints even for small deviations from the true parameters. However, even with an similarly noisy labeling oracle, we demonstrate that IPMAN can generate decisions that are more robust to labeling errors.

In the second case study, we investigate a treatment design problem. Radiation therapy (RT) is a cancer treatment procedure in which high-energy x-rays deliver radiation to a patient to destroy a tumor (Delaney et al. 2005). Treatment plans are evaluated using a set of non-convex, pass-fail constraints that vary from clinic to clinic. Since not all constraints can be simultaneously satisfied in general, treatment planners manually tune parameters in the treatment optimization software and re-solve the problem until an oncologist approves the treatment plan for delivery. Modern treatment planning methods have moved towards machine learning to automate the planning process and reduce manual re-planning iterations (Kaderka et al. 2021). This involves generating a dose distribution that satisfies a relevant subset of the pass-fail constraints that an oncologist would have deemed acceptable for the patient. The current state-of-the-art uses deep learning models trained on medical images from previous patients with approved treatment plans (Kearney et al. 2018, Babier et al. 2019). Instead, by treating the constraints satisfied by previous oncologist-approved doses as a set of patient-specific complicating constraints, IPMAN can generate doses that better meet contextually relevant clinical constraints while simultaneously delivering lower radiation to healthy tissue. We find that:

-

1.

Compared to supervised learning baselines, IPMAN-trained models yield dose distributions that are feasible more often and result in less radiation to healthy tissue.

-

2.

IPMAN demonstrates better generalization. That is, by encoding clinical policies as constraints, IPMAN-trained models can produce treatments that better meet a new clinic’s metrics when trained using approved treatments from another clinic. This suggests that IPMAN can leverage mathematical structure to generate decisions that learn from data whose covariate contexts are shifted from the target environment.

7.1 Automated Portfolio Optimization: A Comparison with Optimization

We consider a non-convex, cardinality-constrained portfolio optimization model (see Kim et al. 2019) with stocks and contextual features per user. These contextual features map to a personalized risk tolerance, as well as minimum and maximum constraints on the number of stocks each user is willing to purchase, which are parameters that would typically require estimation. Motivated by recent successes of predict-then-optimize frameworks in estimating parameters for portfolio optimization (e.g., Ban et al. 2018, Elmachtoub and Grigas 2017, Ferber et al. 2020, Yu et al. 2020), we develop several optimization baselines for comparison. Below, we highlight the setup and main results. We include details on the decision-making problem, data generation process, baselines, and algorithms, as well as additional ablations in Section 12.

7.1.1 Data and Model.

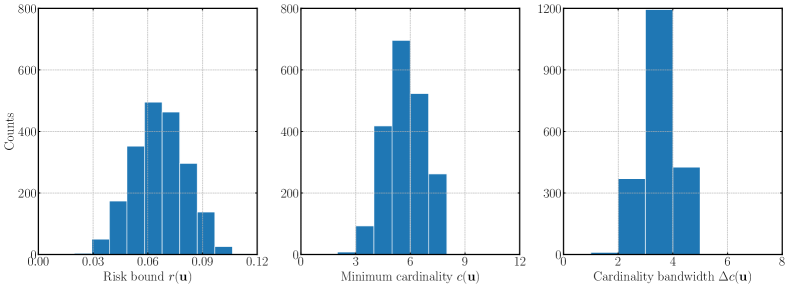

We collect daily prices of stocks sampled from the Nasdaq, NYSE, and NYSE American over a four week period from August 1, 2020 to construct a return vector and a covariance matrix . Then, we create a framework for generating artificial data that simulates investor behavior by sampling three quantities, , that represent the “true relationship” of an user’s (i) risk tolerance , (ii) minimum cardinality constraint , and (iii) cardinality bandwidth requirement . Without loss of generality, these relationships are generated so that the average user desires a low-risk portfolio containing five to ten stocks, making the optimization problems sufficiently difficult.

Given the above user data generation model, we create a data set of i.i.d. randomly sampled context vectors for users and then randomly split the data into three groups of size , , and for training, validation, and hold-out testing, respectively. User parameters are used as input to the following personalized portfolio optimization problem

| subject to | ||||

where represents context-dependent feasible sets and the simplex are the bounding constraints. Note that our data-driven portfolio optimization problem differs from the common setting where and/or are estimated. In our case, we assume and are known (Li 2020, Yu et al. 2020), while the parameters , and are unavailable for test set users. However, we have collected the true parameters , , and for users in our training and validation sets. Not only is this necessary to evaluate model quality in training by evaluating whether training decisions satisfy the context-dependent constraints, but we can use this information to construct a look-up-table-based feasibility oracle such as the one introduced in Example 5.1. The oracle is:

| (10) |

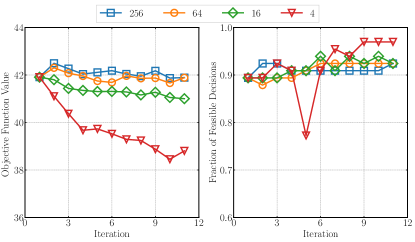

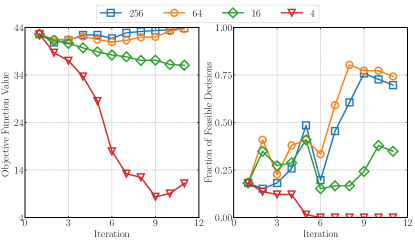

To construct our initial and , we generate 10 feasible and 10 infeasible portfolios per user (for a total of data points) by solving random approximations and relaxations of . We then implement two feed-forward neural networks as our generator and classifier. We train these models with IPMAN for iterations. Finally, we consider a single dual regularization parameter , which was selected via cross-validation using our training and validation sets. We implement IPMAN using PyTorch with an Nvidia GTX 1080 GPU. At test time, our generator can generate a decision in approximately ms.

Our baseline models consist of predict-then-optimize frameworks that estimate , , and from and then solve . Rather than building a specific prediction model, we instead assume that the baselines have perfect predictions of these parameters in the experiments in Section 7.1.2, and then evaluate the effect of noisy estimators in Section 7.1.3. Furthermore, we implement three different optimization algorithms as baselines: a Mixed-Integer Quadratic Program (MIQP), a low-latency version MIQP ( s) where we set the time out to ms to match IPMAN, and a constrained regression reformulation (MIQP-R) that replaces the risk constraint with a Lagrangian relaxation and a quadratic regularization (Bertsimas and Cory-Wright 2022). The MIQP-R baseline represents a conventional approach for addressing complicating constraints by leveraging custom structure in the optimization problem. All baselines are solved using Gurobi with a time out of s for MIQP and MIQP-R.

7.1.2 Experiment 1: Quickly Generating High-quality Decisions.

We evaluate our generator over the set of solvable by analyzing the average optimality gap and the fraction of generated solutions that satisfy the constraints. Feasibility is defined as meeting all constraints to within a relative tolerance of . Note that Kim et al. (2019) use approximately the same tolerance level for their related work in generating optimal portfolios.

| All points∗ | MIQP optimizer runtime windows | ||||

| s | s | s | |||

| MIQP | Fraction of instances (%) | 58.9 | 6.3 | 26.8 | 25.8 |

| Average model run time (s) | 25.9 | 0.7 | 5.6 | 53.2 | |

| Fraction of feasible decisions (%) | 100 | 100 | 100 | 100 | |

| MIQP (0.2 s) | Average model run time (s) | 0.2 | 0.2 | 0.2 | 0.2 |

| Fraction of feasible decisions (%) | 100 | 100 | 100 | 100 | |

| Optimality gap (%) | 40.9 | 10.5 | 36.0 | 53.6 | |

| MIQP-R | Average model run time (s) | 18.4 | 4.2 | 10.1 | 30.6 |

| Fraction of feasible decisions (%) | 88.8 | 100 | 96.5 | 78.3 | |

| Optimality gap (%) | 4.9 | 11.5 | 2.1 | 6.4 | |

| IPMAN | Average model run time (s) | 0.2 | 0.2 | 0.2 | 0.2 |

| Fraction of feasible decisions (%) | 97.6 | 100 | 99.6 | 95.0 | |

| Optimality gap (%) | 17.4 | 25.9 | 22.2 | 9.9 | |

Table 1 compares IPMAN with optimization models stratified by optimizer runtime. Generating a decision with IPMAN requires, on average, 130 ms, whereas the baseline optimizer MIQP requires over s for of the test set instances. Furthermore, for problems that require less than s for MIQP, IPMAN-generated decisions are consistently feasible and achieve low optimality gap, making our generative model a high-quality approximator of the optimizer in orders of magnitude less time. The low-latency MIQP, which has similar decision-generation time as IPMAN, achieves an average optimality gap of %, which is more than two times a large as IPMAN. We also compare against MIQP-R and observe that IPMAN-generated decisions are still generated in orders of magnitude less time and are feasible on average percentage points more often; however, the MIQP-R baseline has lower optimality gap, conditional on it finding a feasible solution. We conclude that our method can deliver decisions that are feasible nearly all of the time but with better objective function value than an optimization model under similar latency requirements.

Finally, recall that these experiments compare against a perfect predict-then-optimize baseline that always knows the true parameter values of the optimization model. A realistic predict-then-optimize framework would inevitably introduce estimation errors in the parameters. We next show that prediction errors in constraint parameters lead to large optimization errors whereas IPMAN can generate feasible decisions even in the face of noisy feasibility estimates.

7.1.3 Experiment 2: Predicting Optimal Solutions under Noisy Information.

| Noise | Fraction of feasible decisions (%) | Optimality gap (%) | ||

|---|---|---|---|---|

| MIQP (0.2 s) | IPMAN | MIQP (0.2 s) | IPMAN | |

| 0.0025 | ||||

| 0.0075 | ||||

| 0.0125 | ||||

| 0.0175 | ||||

| 0.0225 | ||||

| 0.0275 | ||||

In practice, there may be a discrepancy between user features and problem parameters. As a result, predict-then-optimize models would introduce estimation errors and IPMAN would synthesize noisy labeled data. We explore this issue by considering a noisy predict-then-optimize baseline versus a noisy oracle for IPMAN. Since the parameter data has a linear relationship with the user’s features (, , and ), we replace in (10) with a black-box oracle that uses a noisy linear model , , and where . The predict-then-optimize baseline uses the same noisy linear model to estimate constraint parameters for test set users.

We perform five trials with progressively increasing the noise variance from to . Note that at the highest level (i.e., ), the noise variance is almost half the average risk (see Section 12 for further details). This implies that as the noise variance increases, we may find instances of optimization problems that are infeasible for the baseline model and for the oracle in IPMAN. In Table 2, we compare IPMAN against the noisy predict-then-optimize MIQP ( s). Both methods have equivalent run times, which allows fair comparisons of the fraction of feasible decisions and average optimality gap on the test set.

When the noise level is modest (i.e., ), IPMAN can consistently generate both feasible and optimal decisions. In contrast, MIQP ( s) has a larger average optimality gap while the average fraction of feasible decisions is lower; both metrics can be up to percentage points worse than IPMAN. Furthermore, the variance in the feasibility rate between instances is several times larger for MIQP ( s) as compared to IPMAN. For large noise levels (i.e., ), although the average feasibility rate for MIQP ( s) is higher than IPMAN, the variance between instances is so large so as to render the model unpredictable. The findings suggest that, as compared to a competitive predict-then-optimize baseline, IPMAN generates optimal solutions that are more robust to noise while the variance remains consistent between instances.

The intuition behind these results is that due to the mislabeled decision data, the classifier may incorrectly have support over new infeasible regions for many . As a consequence, may train the generator on larger relaxations of the true feasible sets, leading to lower feasibility rates as the noise increases. On the other hand, the initial data set contains a diverse set of correctly labeled decisions. Moreover, the barrier function term in (7) acts as a regularizer controlled by that helps the generator learn to produce more robust solutions. Thus, IPMAN can consistently generate decisions with lower optimality gaps even when sacrificing feasibility. In contrast, MIQP ( s) must find an optimal solution with respect to incorrect parameters obtained from a noisy estimator. These estimation errors are not discernible to the optimization model, meaning MIQP ( s) may not find a solution that is also feasible under the true problem parameters, even with small amounts of noise. Finally, the latency requirement means that MIQP ( s) struggles to find solutions with small optimality gaps.

7.1.4 Implementation Guidelines.

In these experiments, we simulate investor behavior with an artificial data set of user contexts. In a real-world implementation, one would first deploy a baseline model (which could be an alternate ML model or a predict-then-optimize framework) over a trial period to a group of users. For each user in the group, one would collect their context features, recommend investments with the baseline, and observe their adherence to the recommendations in order to construct our decision data sets. At the end of the trial period, each user could be surveyed, and their true risk tolerance levels and cardinality requirements would be recorded. One could then use IPMAN to train a model and validate it by using these recorded preferences. This validation process would also serve as the feasibility oracle in the active learning algorithm.

7.2 Personalized Cancer Treatment: A Comparison with Deep Learning

In radiation therapy treatment planning, solving an optimization problem to produce a personalized treatment that clinicians are likely to find acceptable is challenging and time-consuming. Increasingly, machine learning models are being deployed to quickly generate personalized dose distributions that satisfy the relevant clinical constraints. The current state-of-the-art uses deep neural networks to map a patient’s contoured computed tomography (CT) image to a 3-D dose distribution via supervised learning (Kearney et al. 2018, Mahmood et al. 2018, Babier et al. 2019). Below, we highlight the setup and key results. Details on the clinical problem, the data and algorithm, including data augmentation, and full results are provided in Section 13.

7.2.1 Data and Model.

We use a data set of clinically approved treatments for 217 patients with head-and-neck cancer. Each patient’s CT image is discretized into a tensor whose elements are voxels (3-D volumetric pixels) of the patient’s geometry. Thus, for each patient , we have a 3-D dose distribution (representing the treatment decision) that was approved by the oncologist and a contoured CT image (representing the context vector) that the oncologist would have used to determine whether the dose was acceptable for that patient. We randomly split the data into 100, 67, and 50 patients for training, validation, and hold-out testing, respectively. We then apply a data augmentation step to update the 100 doses into approximately 5,000 doses (i.e., 50 per patient) binned into feasible and infeasible training sets.

Each patient possesses up to seven structures that each correspond to a clinic-mandated constraint. There are four organs-at-risk (OARs)—Right Parotid, Left Parotid, Larynx, Mandible—that each possess an upper bound constraint on the dose to the structure. There are also three targets, called planning target volumes (PTVs)—PTV70, PTV63, and PTV56 where the number indicates the amount of radiation that at least 90% of the structure should receive (i.e., the 90% Value-at-Risk). Let and index the OARs and PTVs, respectively, and let index all structures of interest. For each structure , let index the voxel set, which are the elements of and that correspond to structure . Thus, the context-dependent clinical constraints for each structure are written as (see column 2 of Table 3), where is equal to the clinic-specific bound if an oncologist were to require this constraint to be satisfied for patient with context for it to be approved, and equal to (i.e., no constraint) otherwise. Finally, our non-convex radiation therapy optimization problem minimizes the sum of average doses measured in gray (Gy) delivered to the OARs subject to patient-specific clinical constraints and a fixed set of known safety constraints on the average dose (see Babier et al. 2018):

| subject to | |||||

Each comprises the patient-specific clinic constraint and upper/lower bounds (, ) on the average dose to the structure if . These bounds are sufficiently large so that each is compact. Let and .

For each patient in our data set, we can evaluate the clinically approved dose (the actual dose that was delivered to the patient) and determine which of the clinical constraints are satisfied. When we use IPMAN to train a generator to produce a dose , we can determine whether is feasible if it satisfies all of the same clinical constraints as the clinically approved dose . As a result, the oracle used to label generated decisions as feasible or infeasible is a look-up table that uses on-off constraints such as in Example 5.2.

We implement IPMAN using two convolutional neural network (CNN) models. Our generator and classifier are modified from the generative adversarial network (GAN) of Babier et al. (2019). We train four generators for for iterations with our training set. We compare against two state-of-the-art baseline models from the clinical automated planning literature: a U-net CNN (Nguyen et al. 2019) and a GAN (Babier et al. 2019). The CNN is trained by minimizing the mean-squared error of predicted doses from clinical doses. The GAN is composed of two networks that are trained adversarially via minimax.

7.2.2 Experiment 1: Generating Feasible and Optimal Dose Distributions.

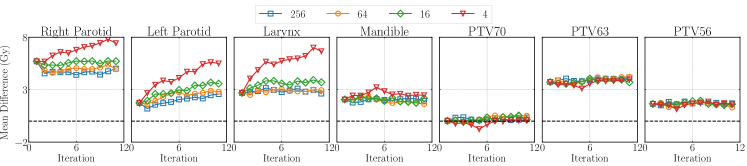

Table 3 shows the percentage of dose distributions that are feasible with respect to the clinical constraints, as well as their average objective function value for IPMAN and the two baseline models on the hold-out test set. We further evaluate each model on the percentage of dose distributions that individually satisfy each of the relevant clinical constraints (first seven rows) to within a Gy relaxation, which is within acceptable limits (Low et al. 1998).

| Structure | Constraints (Gy) | Baselines | IPMAN () | ||||

|---|---|---|---|---|---|---|---|

| GAN | CNN | 256 | 64 | 16 | 4 | ||

| Right Parotid | |||||||

| Left Parotid | |||||||

| Larynx | |||||||

| Mandible | |||||||

| PTV70 | |||||||

| PTV63 | |||||||

| PTV56 | |||||||

| Fraction of feasible doses (%) | |||||||

| Average objective function value (Gy) | |||||||

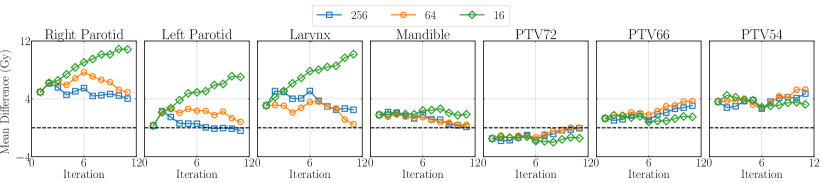

In general, the IPMAN models for satisfy almost all of the relevant constraints at equal or higher rates than the baselines. At , IPMAN dominates both baselines in constraint satisfaction as well as the average objective function value. That is, this model predicts dose distributions that deliver lower dose to healthy tissue while better satisfying the relevant clinical constraints. Thus, it is possible for IPMAN-trained models to produce solutions that are feasible more often and exhibit lower objective function value on average, compared to existing state-of-the-art methods.

7.2.3 Experiment 2: Adapting to the Policies of Different Institutions.

Different clinics mandate different clinical constraints (Wu et al. 2017), meaning that a data set obtained from one clinic may not satisfy the institutional requirements at another. Further, new clinics may have low patient volumes making it difficult to obtain sufficient data to properly train generative models using conventional supervised learning techniques (Boutilier et al. 2016). IPMAN can potentially address this issue by using training set data from a high-volume clinic and encoding the constraints specific to the new clinic into the oracle to adaptively learn to satisfy the new clinic’s policies.

We train IPMAN to generate doses to satisfy the clinical constraints from Geretschläger et al. (2015), who seek doses of 72 Gy, 66 Gy, and 54 Gy for the three targets in each patient, rather than the 70 Gy, 63 Gy, and 56 Gy, respectively, from our data set. For this experiment, we rename the target sites to PTV72, PTV66, and PTV54 and then update the clinical constraint bound in our oracle. Although we do not know the exact preferences of oncologists at the new clinic in determining when a constraint is necessary, we assume that oncologists at both clinics decide the necessity of a constraint in the same manner, i.e., patients for whom the PTV criteria is necessary in our original clinic would require the analogous dose bound at the new clinic.

| Structure | Constraint (Gy) | Baseline | IPMAN () | |||

|---|---|---|---|---|---|---|

| GAN | 256 | 64 | 16 | 4 | ||

| Right Parotid | ||||||

| Left Parotid | ||||||

| Larynx | ||||||

| Mandible | ||||||

| PTV72 | ||||||

| PTV66 | ||||||

| PTV54 | ||||||

| Fraction of feasible doses (%) | ||||||

| Average objective function value (Gy) | ||||||

Table 4 shows the performance on the hold-out test set for the generator. Here, the best model corresponds to . In comparison to the previous experiment, a higher performs better since it encourages more conservative training with respect to feasibility, which is aligned with our goal of satisfying a different set of clinical criteria. Our baseline model is the best baseline from the first experiment, namely the GAN model, which does not possess the active learning aspect of IPMAN. As a result, few plans () produced by the GAN baseline satisfy the new constraints. In particular, an unacceptably low % of the PTV72 and 77.8% of the PTV66 criteria are satisfied. In contrast, IPMAN is able to learn to satisfy these new constraints at rates of 95.2% and 96.3%, respectively. As a result of learning higher doses to the PTVs, IPMAN solutions have slightly higher average objective function values. However, this trade-off would be tolerable since the primary goal of the treatment is to ensure sufficient dose to the targets.

7.2.4 Implementation Guidelines

These experiments use real clinical data to create a look-up table labeling oracle to guide our generators, i.e., doses that are generated during training must satisfy the same constraints as the clinically delivered ones. In a real implementation, oncologists would play the role of the oracle, as current practice already requires them to manually review all treatments plans and determine which ones are acceptable. In the second experiment, we make a mild assumption that clinicians at both clinics decide the importance of constraints in the same way. To correct for human variability between clinics, we could request clinicians at the second clinic to review our data set of treatments, report which ones they find clinically acceptable, and use the feasible decisions in the same manner as above to train IPMAN. Finally, we assume that all oncologists at the same clinic also have the same preferences. Here, we could use the same approach to create personalized data sets and models for each clinician. We emphasize that reviewing existing treatments (i.e., relabeling data) is significantly easier than collecting new personalized data.

8 Discussion and Conclusion

This paper presents a new machine learning-based approach to solving contextual decision-making problems where a large universe of contexts affect the feasibility of decisions, a set of complicating constraints are controlled by the contexts, and there is need to quickly generate high-quality solutions. Our learning algorithm, IPMAN, consists of three components: (i) a generative model that outputs optimal decisions given an input context vector; (ii) a classification model that predicts whether a decision is feasible or infeasible and is used to train the generator to satisfy context-dependent constraints; and (iii) an active learning loop that uses the outputs of the generator to iteratively refine both models during training. We prove that our approach admits in-sample and out-of-sample guarantees on the optimality of generated decisions and, in doing so, derive new results for interior point methods whose barrier functions are defined over a relaxation of the feasible set. We demonstrate the effectiveness of our approach by numerically studying portfolio optimization and personalized treatment design problems. As compared with predict-then-optimize baselines, IPMAN more quickly generates solutions that are of similar quality and are more robust to estimation errors in the constraint parameters. When compared with deep learning baselines, IPMAN generates better solutions that are just as fast while being robust to distribution shift.

Our methodology addresses several issues that affect the deployment of machine learning systems in environments where high-quality decisions are critical (e.g., Lamanna and Byrne 2018).

The tradeoff between speed and quality. In many settings, safety issues may arise due to the sub-optimality of the generated decisions (Bertsimas et al. 2020). At the same time, there often exists a trade-off between solution quality and decision-generation speed (e.g., Baeza-Yates and Liaghat 2017). This paper directly addresses this trade-off by developing a model that generalizes the classical -optimality property of interior point methods while also permitting real-time decision generation. Not only are these guarantees necessary for large-data environments where a mapping between contexts and feasible decisions must be estimated (e.g., Li et al. 2021), but our approach learns to produce optimal solutions from past decisions that were not necessarily optimal.

Better capturing the variation in decision-maker behavior induced by contexts. Automated decision-making systems can at times be inflexible. As a consequence, this may lead to a disconnect between solutions prescribed by a model and the real actions undertaken by decision-makers based on their understanding of the contexts that are guiding the instance (Bendoly 2011, 2013, Cotteleer and Bendoly 2015, Chan et al. 2020). For example, the parameters of context-dependent constraints may be sensitive to estimation errors (e.g., Hurley and Brimberg 2015), which may cause downstream optimization models to produce drastically different solutions than what a decision-maker would implement. To address these issues, IPMAN learns a model-free representation of contextual feasible sets (i.e., an explicit formulation of the constraint set is not necessary) and learns to generate -optimal decisions. As a result, decision-makers do not have to mathematically articulate every problem detail, yet the algorithm can still generate good solutions. By tuning the learning parameters that control , our approach naturally allows for decisions that are more likely to be feasible, which provides some degree of robustness to estimation errors.

Including expert judgment in model development. The active learning component of IPMAN permits for the inclusion of expert judgement—which introduces information into the training process that is not necessarily contained in the data—when designing automated ML systems. Indeed, it is common to have decision-making problems possess valuable structural information that can be used as an aid in model development (e.g., Wilder et al. 2019, Fioretto et al. 2020). In our experiments, expert judgment comes in the form of using the structural information in the oracle to automatically evaluate the quality of decisions generated during the training process. Alternatively, one can employ a group of expert human decision-makers or platform users to perform this task. For instance, having medical practitioners evaluate the acceptability of generated treatment decisions based on their tacit preferences allows them to participate in the creation of the AI algorithm. An ancillary benefit of this human-in-the-training-loop approach is that by participating in the development of the model, practitioners may eventually be more comfortable in adopting the tool (Vollmer et al. 2020, Faes et al. 2020).

Additional issues and future extensions. Structural information that is present may not always align with the preferences of the decision-maker. Consequently, automated labeling methods may produce synthetic data that is incorrectly classified with respect to whether the generated decision is feasible for that decision maker. In our portfolio optimization experiments, we evaluate the effect that mislabeled data has on the quality of generated solutions. Although we show that our framework is robust to a modest degree of label noise, a potential extension may be to more formally integrate our learning approach with the deep learning literature that studies settings with noisy labels (Natarajan et al. 2013, Li et al. 2017, Han et al. 2019). Further, our numerical experiments on cancer therapy explore the generation of treatments that meet a set of context-dependent constraints that correspond to a clinic policy that differs from the policy under which the initial data was generated. A natural extension is to investigate the extent to which known structural information in a decision-making problem can be used to guide a machine learning model to adapt to covariate or domain shift (Ben-David et al. 2010, Redko et al. 2020). Finally, while IPMAN generates certifiably optimal decisions for a large number of contexts, subsequent research should investigate how training can be modified to produce personalized decision-making models. One such extension, for example, is to run an experiment with human decision-makers in the training loop to measure the concordance of the produced decisions against their preferences.

References

- Agrawal et al. (2019) Agrawal A, Amos B, Barratt S, Boyd S, Diamond S, Kolter JZ (2019) Differentiable convex optimization layers. Advances in neural information processing systems, 9562–9574.

- Amos and Kolter (2017) Amos B, Kolter JZ (2017) Optnet: Differentiable optimization as a layer in neural networks. International Conference on Machine Learning, 136–145.

- Angalakudati et al. (2014) Angalakudati M, S B, Calzada J, Chatterjee B, Perakis G, Raad N, Uichanco J (2014) Business analytics for flexible resource allocation under random emergencies. Management Science 60(6):1552–1573.

- Angluin (1988) Angluin D (1988) Queries and concept learning. Machine learning 2(4):319–342.