Non-concave optimal investment with Value-at-Risk constraint: an application to life insurance contracts

Abstract

This paper studies a Value-at-Risk (VaR)-regulated optimal portfolio problem of the equity holders of a participating life insurance contract. In a setting with unhedgeable mortality risk and complete financial market, the optimal solution is given explicitly for contracts with mortality risk using a martingale approach for constrained non-concave optimization problems. We show that regulatory VaR constraints for participating insurance contracts lead to more prudent investment than in the case of no regulation. This result is contrary to the situation where the insurer maximizes the utility of the total wealth of the company (without distinguishing between contributions of equity holders and policyholders), in which case a VaR constraint may induce the insurer to take excessive risks leading to higher losses than in the case of no regulation, see [4]. Compared to the unregulated problem, the VaR-constrained strategy leads to a higher expected utility for the policyholders, highlighting the potential usefulness of a VaR-regulation in the context of insurance. The prudent investment behavior is more significant if a VaR-type regulation is replaced by a portfolio insurance (PI)-type regulation. Furthermore, a stricter regulation (a smaller allowed default probability in the VaR problem or a higher minimum guarantee level in the PI problem) enhances the benefit of the policyholder but deteriorates that of the insurer. For both types of regulation, the gains in terms of expected utility are greater for higher participation rates, while being smaller for higher bonus rates. We also extend our analysis to frameworks where dividend and premature death benefit payments are made at an intermediate time date.

JEL classification: C61, G11, G18, G31

Key words:Non-concave utility maximization, Value-at-Risk, optimal portfolio, portfolio insurance, risk management

1 Introduction

This paper investigates the equity holders’ optimal investment problem of a participating contract under financial regulation. This problem is particularly relevant for insurance companies that operate under Solvency II with a Value-at-Risk (VaR) constraint. Participating contracts are life insurance products which provide the policyholders at least a guaranteed amount in downside market situations and a shared profit in good market scenarios. To participate in such a contract, the policyholders pay a premium (participation fee) which is collected together with the (equity holders’) insurer’s participation amount in an investment pool. At maturity, the policyholders receive a payoff which is linked to the investment performance. The equity holders’ payoff is determined as the residual amount. Our derivation of the optimal solutions relies on the combination of a martingale approach for non-concave and non-differentiable objective functions and a point-wise optimization technique with constraints.

Earlier studies on equity-linked life insurance contracts usually analyze pricing or optimal design problems. Some focus on the policyholders’ perspective assuming specific investment strategies like constant proportion portfolio insurance (CPPI) or generalized constant-mix see, e.g., [11, 30, 33]. Recently, [16] considers participating life insurance contracts from the policyholders’ perspective under a fair pricing constraint and tax privileges.

In this paper, we consider two common contract designs. In the first design, we assume that the equity holders have only limited liability, i.e., the policyholders’ payoff is less than the guaranteed amount in case of a default of the insurance company. In the second design, we assume that the policyholders are fully protected against an insolvency of the insurance company (i.e., the final payoff to the policyholders always exceeds or equals the guaranteed amount). Note that in the case of full protection, the equity holders may suffer a negative payoff in case of insolvency. To describe the behavior of the equity holders in the loss domain, we use an -shaped utility function adopted from prospect theory, see [42, 25, 29].

Risk management and regulations based on a terminal VaR constraint are well-known in banking and insurance regulations. Banks are allowed to develop their own internal VaR models which are subject to supervisory approval based on standardized back-testing procedures controlled by the Basel Committee on Banking Supervision. In insurance contexts, to ensure that pension funds fulfill their obligations to pensioners, pension regulators usually impose a VaR-type constraint on nominal funding ratios. The new regulatory framework for insurance companies in Europe, Solvency II, advocates risk-based regulation which focuses on downside risk and suggests using measures such as the ruin probability or VaR. The problem of utility maximization/optimal asset allocation under VaR-type constraints has been studied extensively in the literature, see e.g. [4, 10, 18, 20, 31, 44, 17, 43].

This paper solves the equity holders’ problem of utility maximization under a regulatory constraint imposed at maturity. We obtain closed-form solutions for various kinds of constraints. We first explicitly solve the problem for the two kinds of contracts mentioned above under a VaR regulation extending the martingale approach to non-concave utility maximization problems with constraints. Second, motivated by the fact that regulators usually affect insurance contract designs by imposing a minimum capital requirement which is used to control adverse events, we consider a portfolio insurance (PI) constraint to enhance the protection for the policyholders. Finally, we extend the result to a two-period optimization framework where premature death benefits and dividends can be paid at an intermediate date. This analysis is particularly useful for insurers which need to set a long-term investment while having to follow short-term liabilities with periodic VaR-type regulations. A further extension to multiple periods along these lines is possible but is omitted.

Our theoretical and numerical results show that already in the case of no regulation there is a moral hazard problem since the insurer does not have an incentive to ensure that there is any capital in the loss states where the terminal wealth falls below the minimal guarantee. The reason is that any terminal wealth in those states only benefits the policyholders and comes at the expense of a lower terminal wealth in the more prosperous states where the equity holders receive a positive residual. On the other hand, introducing a VaR constraint as in Solvency II forces the equity holders to enlarge the proportion of hedged loss states, leading to a genuine improvement for the policyholders. This result is contrary to the situation where the insurer maximizes the utility of the total wealth of the company without distinguishing between equity holders and policyholders, in which case a VaR constraint may induce the insurer to take excessive risk leading to higher losses in the worst 1% of scenarios than in the case of no regulation, see e.g. [4, 17, 26, 18, 43]. Compared to the unregulated problem, the VaR-constrained strategy leads to a higher expected utility for the policyholders, implying an increase in the attractiveness of participating contracts. This more prudent investment behavior described above is more pronounced if a VaR based regulation is replaced by a PI-based regulation. Furthermore, a stricter regulation (a smaller allowed default probability in the VaR problem or a higher minimum guarantee level in the PI problem) will enhance the benefit of the policyholder but deteriorate that of the insurer. For both (VaR and PI) types of regulation while being stronger for higher participation rates, this regulatory effect becomes less for smaller bonus rates (given the same participation rate). Our results also show that in certain situations, for instance in the cases of relatively high participation rates and relatively low bonus rates, policyholders overall may prefer a VaR regulation over a PI regulation with a relatively low minimum guarantee level in terms of expected utility. Finally, the introduction of a full protection makes the equity holders’ investment also generally more prudent in bad market scenarios but changes the investment behavior relatively little in good market scenarios.

The problem of non-concave utility maximization without constraints has been considered by many authors e.g., [15, 38, 22, 14, 36, 8, 28], using concavification techniques. In a framework without constraints, [36] proves the existence of an optimal terminal wealth. However, no specific payoff is provided. We remark that the technique developed here to deal with VaR constraints can be applied for the principle-agent problem with option-like compensations considered e.g. in [15, 38]. Note that such a risk-sharing problem may require some kind of fairness condition that guarantees that neither party can systematically benefit from the contract. In insurance contexts, when such a condition (being referred to as fair pricing constraint or participation constraint see, e.g., [35, 16]) is satisfied, both the parties are willing to participate in the contract initially. While the optimization developed here can be applied to such a framework we mainly focus on regulatory aspects of VaR constraints motivated from the Solvency II regulations rather than on the problem of optimal product design. On the other hand, our framework allows for a pool of multiple contracts of heterogeneous policyholders with mortality risk for which the individual fairness is not the main point from the insurer’s perspective as it might be too challenging to take it into account for every policyholder. It seems in our setting more reasonable to assume that only those policyholders enter the contract in the first place, for whom a fair pricing constraint holds without the need for the insurer to readjust its strategy. In addition, it seems very challenging to specify even for one policyholder the individual fair participating constraint in the two-period framework with death and dividend payments studied above due to the market incompleteness and possible intermediate money withdrawals.

When finishing this paper we noticed that [29] has independently investigated participating insurance contract problem with a power utility function without regulation or mortality, doing extensive, interesting numerical comparisons between various hedging portfolio insurance strategies, and also numerically analyzing possible restrictions on the portfolio weights. We on the other hand consider general utility functions with mortality risk focusing on the impact of regulation for a pool of multiple contracts of heterogeneous policyholders. To the best of our knowledge, non-concave utility maximization problems together with (non-concave) constraints have not been considered before. Moreover, we extend the results to a two-period framework where premature death benefits and dividend payments can be considered at an intermediate date, which shows the flexibility of our method.

The paper is organized as follows: In Section 2, we introduce the asset model and the parametric family of contract payoffs. We then solve the unregulated problems with mortality in Section 3. In Section 4, we investigate the constrained problems. The results are numerically illustrated in Section 5. An extension to a two-period framework is presented in Section 6. All technical proofs are reported in the Appendix.

2 The financial market and participating contracts

2.1 The financial market

We fix a probability space equipped with a -dimensional Brownian motion , where is the natural filtration of and is the time horizon. All equations and inequalities are assumed to hold almost surely. We consider a complete financial market without transaction costs consisting of one risk free asset (the bank account) and traded risky assets whose price dynamics are -adapted processes. Let be the unique equivalent martingale measure such that the discounted risky assets , are -local martingales. We remark that the Radon-Nikodym derivative is -measurable and can be easily be extended to larger filtrations by setting .

To unify notation, we assume in the sequel that is the filtration which is identical to in the case of no mortality and in the case of additional mortality risk is an enlarged filtration (containing and additional mortality events to be specified later) such that is a local martingale.

A trading strategy is defined as a -adapted predictable process , , representing the vector of holdings in the assets. We interpret as a self-financing strategy, so that its portfolio process with initial value can be represented as

To exclude arbitrage opportunities, we only consider strategies such that is bounded from below and the above stochastic differentiable equation admits a unique strong solution. Hence, the discounted portfolio is a supermartingale. Choosing a self-financing portfolio strategy is equivalent to choosing a terminal wealth which can be financed by .

The set of attainable terminal wealth values is defined by

where is the pricing kernel defined by with being the Radon-Nikodym derivative. Throughout this paper we will assume that does not have any atom. Note that can be interpreted as the (Arrow-Debreu) value per probability (or likelihood) unit, of a security which pays out $1 at time if the scenario happens, and else. As this value is high in a recession and low in prosperous times, has the property of directly reflecting the overall state of the economy at time . We remark that in a consumption based pricing model in equilibrium corresponds to a constant times the marginal utility of consumption and is also called pricing kernel or stochastic discount factor.

Examples of complete markets are the Black-Scholes model, local volatility models, stochastic interest rate models with a zero-coupon bond or the Heston stochastic volatility model with a financial derivative as an additional hedging instrument.

2.2 Participating contracts and payoffs

Participating life insurance contracts are contracts that provide a return guarantee and participation in the surplus of the insurance company’s performance. These products have been widely considered in major European life insurance markets, see Table 1 in [37]. Valuation and hedging of participating life insurance contracts have been well documented in the literature e.g. [13, 2, 7, 23, 6, 39, 32].

In this paper, we look at the insurer’s investment problem related to a pool of multiple participating contracts having the same maturity. In particular, we assume that there are () policyholders who each invest a single premium into an equity-linked life insurance contract with a maturity of years with . At the initiation of the contract, each policyholder () invests an amount . The total premium is given by . The shareholders (equity holders) provide an initial equity . In the sequel we assume that the insurance company or its management acts on behalf of the group of equity holders by maximizing their total utility. The initial portfolio value is given by the sum of all contributions, i.e., . We denote by the total share of the policyholders’ contribution (or equivalently the debt ratio of the insurance company). is also called the policyholders’ participation rate.

We assume that the individual policyholder receives the guaranteed payment plus some bonus which is proportional to her relative participation rate . Note that . For simplicity, we assume that the guaranteed interest rates are the same for all policyholders, in particular, , where is the total guaranteed liability. For example, in a Black-Scholes setting with constant interest rate , we can choose , , where .

The aggregated payoff of the insurance company to the group of policyholders is then defined as follows: If the terminal portfolio value is less than the total guaranteed liability , bankruptcy is declared (default event) and the policyholders take what is left, . If the terminal portfolio value exceeds , i.e. , the surplus will be shared between the equity holders (represented by the insurer) and policyholders. In particular, we assume that the policyholders receive a surplus equal to , where the surplus (bonus) rate is the percentage of surpluses that is credited to the policyholders. When the terminal asset value lies between and (the threshold where the participation bonus kicks in), the insurer is only able to distribute its guaranteed commitment . To summarize, the insurer at time pays out to the policyholders

| (1) |

or in a more compact form111 denotes the maximum .,

The terminal payoff will be shared among the policyholders corresponding to their relative contributions . Thus, the payoff of policyholder () is given by with .

To exclude unrealistic cases, we assume throughout the paper that and . Hence, the policyholders take a long position in the bonus option and a short position in a defaultable put and benefit from the potential upsides over the final maturity guarantee. This type of defaultable contracts is frequently used in the literature of insurance contracts, see, for example [12, 13, 24, 3, 5, 6, 29, 16]. The equity holders then receive the residual asset value

| (2) |

Agreeing on the contract, the insurer takes a long position of the call and short positions of the bonus call with strike price .

For our analysis, we introduce

| (3) |

Hence, is the actual (achieved) bonus rate of the policyholders, is the difference between the bonus threshold and the guarantee, and is the payoff that the insurer receives in case that the wealth is greater than the bonus threshold .

Like any profit-seeking company, the life insurance company sets up its investment mix to primarily maximize the benefits of its shareholders. Hereby, we assume that the shareholders value their benefits through a strictly concave utility function defined on the positive real line, which is twice differentiable and satisfies the usual Inada and the asymptotic elasticity (AE) (see [27]) conditions

| (4) |

We assume furthermore that . The case where is easier and can be treated without the concavification procedure, see more in Corollary 3.3. As usual, we denote by the inverse of , the first derivative of the utility function.

2.3 Full protection and -shaped utility function

The policyholders of the defaultable contract defined by (1) have to bear the risk of insolvency. This contract design may not serve well policyholders who aim at purchasing default-free policies. Motivated by [5], we assume that the contract at maturity gives the policyholders at least some guaranteed amount without the possibility of default. More precisely, at time the policyholders receive the following payoff

In case that the insurance company is unable to fund the guarantee, this assumes that the guaranteed amount is taken over by an insurance guarantee fund or by the state government. As in the case of defaultable contract, the individual policyholder () payoff can be defined by .

Fully protected contracts have also been considered in [29, 16]. The equity holders take the residual portfolio value

Hence, in this full protection case, the equity holders take more risk because they may have a negative payoff in the insolvency case where . Since the insurance company may have to pay this amount back at a later point in time and faces a loss of its reputation, we assume that the equity holders use an -shaped utility (convex on the loss domain left to a reference point and concave on the gain domain right to a reference point) suggested by prospect theory [42] which allows for negative payoff values. In particular, the insurance company utility takes the form , where

| (5) |

where and are two strictly concave utility functions satisfying to guarantee that is continuous at . We assume furthermore that satisfies the Inada and (AE) conditions. For example, we can take , for some loss aversion degree , see [42]. Note that for such fully protected contracts, the guarantee level is considered as the reference point which is naturally used to distinguish gains and losses.

Remark 1.

It has been suggested in [5] that the policyholders’ payoff can take the following mixed form , for some . This means that the insurer “sells back” a portion of the default put to the policyholders. Note that leads to a defaultable contract while corresponds to a fully protected policy. In this paper we only focus on these extreme cases ( or ) and remark that the optimal investment problem for mixed contracts can be treated similarly.

2.4 Contracts with mortality risk

Mortality is one of the most important risk factors in life insurance, strongly affecting pricing and premium principles. Note that when non-tradable stochastic mortality is considered, the market becomes incomplete. In this section we incorporate mortality risk into the optimal investment problem of the equity holders. We assume that the premature death of policyholder is modelled by the event , where is a binomial random variable. We suppose that are mutually independent and independent of the financial risk, see e.g. [2, 7]. We now work on an enlarged probability space , where is the enlargement of the financial filtration that contains the information generated by the premature death variables . In other words, represents the structure of the global information available to the insurer. Since are discrete variables independent of , we obtain for all and . In Section 6 we will also allow deaths to be observed before maturity.

First, consider the case of defaultable contracts. As discussed above, we suppose that policyholder receives the amount if she is alive at maturity. On the other hand, her family will receive a benefit in case of death which we for simplicity first assume to be the guarantee in case that the insurance company is solvent and else. In Section 6 we will also allow for arbitrary large death benefits and additionally take dividend payments into account. Overall, the payoff to policyholder will be equal to . We note that we can also consider other death benefits than with our method. The policyholder ’s payoff is given by

Hence, the equity holders’ payoff will be given by the difference between the terminal portfolio value and the total amount paid to the policyholders, i.e.,

or (noting that )

| (6) |

where . Economically, represents the total proportion of the guaranteed payment that the insurer has to pay to those who have died before maturity.

Remark 2.

When all are identical, i.e., , for all , the set of possible outcomes of is . Assuming furthermore that the death probabilities are the same for all policyholders, i.e., for all , we can compute the probability densities of as follows:

In general, the distribution of is called generalized Poisson Binomial distribution (see e.g. [46]) which can be computed using Panjer’s recursion or the normal power approximation technique. Similar discussions in insurance contexts can be found in [34].

For the case of a full protection, we still assume that the guarantee will be paid if policyholder dies before maturity. In other words, the policyholder ’s payoff is given by

Thus, the equity holders’ payoff in the case of full protection is given by

As before, the equity holders’ payoff in this case can be expressed as

| (10) |

We remark that for both cases mortality only affects the region , where the guarantee is met and profit is shared with the policyholders.

2.5 Insurer’s optimization objective

The insurer who is assumed to act on behalf of the equity holders wants to solve the following optimization problem

| (11) |

where is an -shaped utility of the form (5) and the payoffs and , are defined in (7) and (10). We remark that for defaultable contracts without mortality the insurer does not encounter negative values of the payoff. Therefore, without loss of generality, we can set in this case.

We furthermore assume the following integrability condition:

Assumption (U): For any , we have

where .

It is straightforward to check that Assumption (U) holds for commonly used utility functions like power or logarithmic. This condition is needed below to guarantee the existence of the Lagrangian multiplier .

Let be the finite set of all possible outcomes of . Using the independence of and we define

| (12) |

where stands for the conditional expectation operator with respect to the distribution of . In other words, is a finite sum of concave functions weighted by the probability masses with . The following lemma is a direct consequence of the concavity of and the fact that .

Lemma 2.1.

The function is strictly increasing and concave on with derivative given by

| (13) |

Hence, its marginal inverse exists. Moreover, .

Note that a.s corresponds to the extreme case where all policyholders almost certainly die before maturity. Similarly, the case where all policyholders survive at maturity with probability of 1 corresponds to a.s. Below, we write and for the utility of these cases respectively. In particular,

Thus, when all policyholders almost surely survive at maturity the equity holders’ payoff takes the form (2.2) (excluding mortality). However, when no policyholder survives until maturity, the insurer’s payoff simply equals the difference between the portfolio value and the guaranteed payment, .

Now, using the independence of the mortality and the reference portfolio we rewrite the optimization problem (11) as

| (14) |

where the objective utility is defined by

| (15) |

with and . It follows from Lemma 2.1 that is an -shaped utility function. We remark that the derived utility (the case of defaultable contracts) coincides with (the case of the full protected contracts) on . For convenience, we introduce

| (16) |

and treat the case of defaultable contracts as a special case of an -shaped utility.

3 Unconstrained problem

As mentioned above, the derived utility function is neither concave nor differentiable. Motivated by non-linear compensation schemes for a fund manager, the maximization of the utility of terminal wealth for non-concave utility functions has been considered in [15, 22, 14, 36, 8]. Similar characterizations can be found in [28, 30] where non-linear contract payoffs or changing preferences are considered.

To obtain explicit solutions, below we use a Lagrangian approach to determine the optimal solution and point out the links to the concavification points of the derived utility function which are determined below. Recall that is a strictly increasing and concave function on with first derivative given by (13). Let and define

| (17) |

The parameter represents the upper bound of the losses in case of an -shaped utility function being used to deal with negative wealth. In particular, we set in the case of full protection and in the case of defaultable contracts. The optimal solution crucially depends on the sign of at the utility changing point . From Lemma 2.1 we observe that

The optimal solution will be characterized by and given in the following lemma.

Lemma 3.1.

Let and be defined as in (17). If then there exists a positive number satisfying , i.e.,

| (18) |

If then there exists a positive number satisfying , i.e.,

| (19) |

In fact, is the tangency point of the straight line starting from the point to the curve in the first case and is the tangency point of the straight line starting from to the curve in the second case.

Proof. We prove the first property. To this end, note that the left hand side of (18) is an increasing, continuous function in due to the concavity of . By Inada’s condition, it takes values in and the conclusion follows from the intermediate value theorem. The second statement can be proved in the same way using the asymptotic elasticity condition of . ∎

Below we solve the optimization problem (14) using a Lagrangian approach. The optimal terminal wealth will be expressed as a function of the price density price and a Lagrangian multiplier defined via the budget equality. Recall that for both payoffs, the derived utility function defined in (15) takes an -shaped form.

The optimal terminal wealth of Problem (14) is characterized by the following theorem.

Theorem 3.1.

The optimal terminal wealth of Problem (14) is given by

where and

| (20) |

The Lagrangian multiplier is defined via the budget constraint.

Proof. See Appendix A.1. ∎

Let us give some comments on Theorem 3.1. First, when or equivalently, the concavification point of lies in the interval , the optimal terminal wealth takes a four-region form determined by the utility changing points and . For or equivalently, for the concavification point being in the interval , the optimal terminal wealth takes a two-region form and is determined by . When , concavification is needed on the interval . The concave hull is then equal to the linear segment connecting zero with and coincides with on . In this case the optimal terminal wealth takes a three-region form. In all cases, the optimal terminal wealth is decreasing in and ends up with zero from a certain value of the price density on, i.e., in the worst economic states. This reflects the moral hazard problem that the insurer does not have an incentive to ensure that there is any capital in case the terminal wealth falls below the minimal guarantee. The reason is that any terminal wealth in those states only benefits the policyholders and comes at the expense of a lower terminal wealth in the more prosperous states. We will later see that introducing a VaR constraint ameliorates this situation.

Optimal policy of wealth distribution: Like the classical concave utility maximization problem, the optimal terminal wealth is given as a function of the state price density at maturity and the Lagrangian multiplier which is determined via the budget equation. In particular, we observe from Theorem 3.2 that for , the four-region form solution is characterised by wealth levels defined by corresponding to the partition of the terminal market states with boundary points . In other words, the wealth level at time is respectively assigned to on the sub-interval , to on , to on and finally to zero on . Therefore, it is convenient to represent the terminal wealth in dependence of the state price as

In the same spirit, the optimal wealth for the case and the case can be respectively represented by the three-region and the two-region wealth distributions as

Thus, the optimal terminal wealth in Theorem 3.1 can be expressed as

| (21) |

These representations of wealth distribution will be used in the rest of the paper for notational convenience.

Let us now consider the case where , i.e., all the policyholders die before the maturity of the contract. In this case, the optimal terminal wealth is given by the following all-or-nothing form.

Corollary 3.1.

If , the optimal terminal wealth is given by , , where satisfies the budget constraint.

We conclude this section by presenting the optimal solution without mortality for both kinds of contracts, i.e., . In this case, the inverse marginal function in Lemma 2.1 can be computed explicitly as

| (22) |

Note that is a decreasing mapping from to .

Corollary 3.2 (Defaultable contract without mortality).

The optimal solution to the unconstrained problem is given by

where

and and is defined via the budget constraint .

Corollary 3.3.

The optimal terminal wealth for a fully protected contract without mortality takes an all-or-nothing form which is given in the following Corollary.

Corollary 3.4 (Fully protected contract without mortality).

The optimal solution to the -shaped utility unconstrained problem for the full-protection payoff without mortality is given by

where

and is defined via the budget constraint .

Remark 3.

We observe that for any , , which implies that whenever they both exist. Similarly, whenever they both exist. This means that the concavification area for the full protection case will be reduced in comparison to the case of a defaultable contract, assuming that the insurer uses the same concave utility function for the gain part.

Optimal strategy: We have determined the optimal terminal wealth as a function of and a multiplier that satisfies the budget constraint. For the reader’s convenience, we briefly discuss how to deduce the optimal strategy by applying the martingale representation theorem in the case of a Brownian filtration. To simplify the presentation we consider a simple Black-Schole’s model with one risky asset given by

and where are positive constants. The pricing kernel admits the dynamics , , where is the market price of risk. The wealth process starting with an initial wealth related to the strategy (the amount invested in the risky asset at time ) can be expressed as

| (23) |

To guarantee the existence of the strong unique solution of (23) we require to be a -progressively measurable process satisfying the square integrability condition a.s. Recall that in this case.

Now, let be the optimal terminal wealth and define . Then, the process is a martingale under . Therefore, by the martingale representation theorem, there exists an adapted process such that a.s. and

or equivalently, . On the other hand, applying Itô’s lemma we get

Since a.s. we remark that the process being the unique strong solution of the above stochastic differential equation is a continuous process in . Now, identifying the dynamics of with equation (23) we deduce that the optimal strategy is given by

Using the inequality and the continuity of the processes and we obtain

which implies that is admissible.

The same argument can be applied for the constrained problems below. More explicit representations can be provided for power and logarithmic utility functions.

4 Optimal investment under regulations

4.1 The VaR-constrained problem

As seen in the previous section, under the absence of regulation the insurer on behalf of the equity holders will optimally choose a strategy which may lead to insolvency at maturity. In this case, the policyholders suffer severe losses since the terminal portfolio value may be zero for very bad market scenarios. In practice, an appropriate investment must take some regulatory constraints into account. According to Solvency II, the insurance company needs to ensure that a VaR-type regulation (i.e., a default probability constraint) shall be satisfied. In addition, the insurance company is interested in achieving at least a target payment to serve the promised guaranteed amount to the policyholders. Therefore, the insurer has to choose an optimal dynamic portfolio under a VaR constraint, which can be stated as

| (24) |

for some allowed default probability level .

Theorem 4.1.

Let and define so that . Suppose that . Then, the VaR-constrained problem (24), , admits the following optimal solution:

-

•

If then

-

•

If then

-

•

If then

In each case, the Lagrangian multiplier is defined via the budget constraint.

Proof. See Appendix A.2. ∎

We observe first that when // in the first/second/third case, the VaR constraint is not binding and the corresponding unconstrained solution given by (3.1) is still optimal for (24). On the other hand, when the VaR constraint is binding (active) the terminal wealth will be (partially) shifted to the right of the concavification point. We can observe that for , there exists such that

meaning that the VaR-terminal wealth dominates the unconstrained terminal wealth for the most negative loss states (due to the fact that and are decreasing functions of ). Furthermore, the inequality is strict for some states. Hence, introducing a VaR-constraint forces the equity holders to enlarge the proportion of hedged loss states, leading to a genuine improvement for the policyholders. This result is contrary to the situation where the insurer maximizes the utility of the total wealth of the company without distinguishing between equity holders and policyholders, in which case a VaR constraint may induce the insurer to take excessive risk leading to higher losses than in the case of no-regulation, see [4]. However, there is still a region of market scenarios in which the optimal terminal wealth equals zero, which means that a VaR regulation does not lead to a full prevention of moral hazard. The intuitive reason is that under a VaR regulation, the insurance company is only required to keep the portfolio value above with a given probability . Once the regulation is probabilistically fulfilled the insurer can push the remaining risk into the tail to seek a higher potential wealth level in good market states. This is consistent with the classical VaR-constrained asset allocation problem with concave utility functions [4]. Nevertheless, in our case with participating contracts, the use of a VaR constraint does not lead the insurance company to bigger losses than in the case of no regulations as in the classical VaR problem. On the contrary, our results show that a VaR constraint strictly improves the risk management for the loss states.

4.2 The PI-constrained problem

In this section, we try to better protect the policyholders from the equity holders’ moral hazard by, instead of having a VaR constraint, assuming that the insurance company has to keep the portfolio value almost surely above some given level minimum capital requirement . Hence the insurance company needs to solve

| (25) |

For simplicity we assume that is deterministic.

Let us first consider the case . As before, concavification is characterized by the following generalized version of Lemma 3.1.

Lemma 4.1 (Tangency point for PI-problem).

Let and be defined by

If then there exists a positive number satisfying , i.e.,

If then there exists a positive number satisfying , i.e.,

As before, is the tangency point of the straight line starting from the point to the curve in the first case, and is the tangency point of the straight line starting from to the curve in the second case. For our problem with the loss magnitude is equal to for defaultable contracts or for fully protected contracts.

We remark that to hedge against the minimum capital level , the investor must start with at least as the initial capital. Next, we show in Theorem 4.2 that the optimal terminal wealth under a PI constraint takes a similar form as in the unconstrained case but with bounded losses. The moral hazard is restricted thanks to the additional guarantee .

Theorem 4.2.

Proof. See Appendix A.3. ∎

In this theorem the moral hazard problem shown in Theorem 3.2 is solved by introducing a minimal bound. However, this comes at the expense of lowering the wealth significantly in the prosperous states and is thus rather costly, see the numerical illustration given below.

Let us now turn to the case where the minimum amount lies between the utility changing points (i.e., between the guarantee and the bonus threshold). In this case, the derived utility function is strictly increasing and globally concave in the considered domain . However, is not smooth at due to Lemma 2.1, which makes the classical utility maximization result inapplicable. We remark that concavification is not needed because we have global concavity in the optimization domain. The case is just the classical portfolio insurance problem with concave utility function and can be dealt with similarly. The following result can be directly obtained using the same Lagrangian technique.

Proposition 4.1.

Assume that . Then, for , the optimal solution to the portfolio insurance problem (25) is given by

where . When the optimal terminal wealth is

which can be seen as a limiting case by sending in (4.1) to infinity. For , the optimal terminal wealth is given by where . The Lagrangian multiplier satisfies the budget constraint.

5 Numerical examples

We assume that the insurer’s utility function is given by with . For the full protection case, we assume that . The market coefficients are The contract has a maturity and the total contribution (i.e., the initial capital) is fixed with . The guarantee is given by , where the guaranteed interest rate is . Note that the threshold where the participation bonus kicks in is now fixed and independent of the participation rate in the comparative analysis below. For simplicity we do not consider mortality risk. Below we look at the investment behavior of the reference portfolio decided by the insurer in order to maximize its expected terminal utility with and without regulations. Note that constant proportion portfolio insurance (CPPI) strategies can be considered as a possible benchmark for comparative analysis, see [29]. We emphasize that CPPI strategies are not optimal and provide less expected utility for the insurer. For an analytic discussion, it may therefore be useful to compare the insurer’s strategy with the Merton strategy which maximizes the insurer’s utility of the total wealth of the company without distinguishing between the equity and policyholders starting with the same total initial endowment.

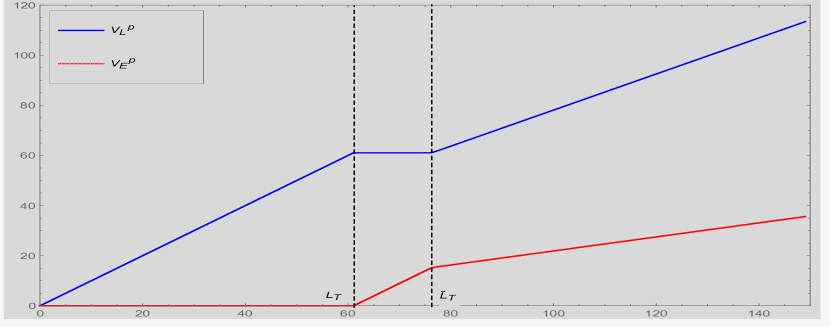

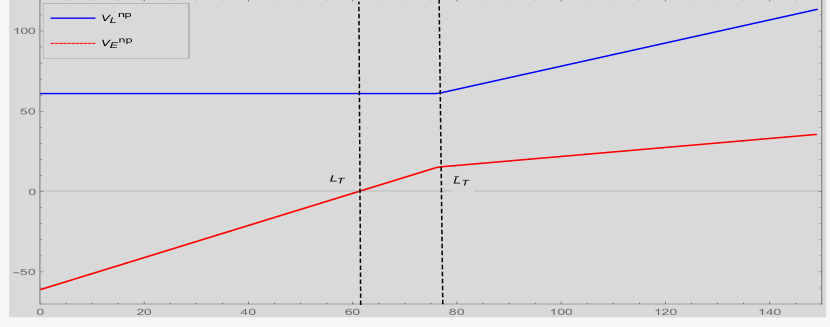

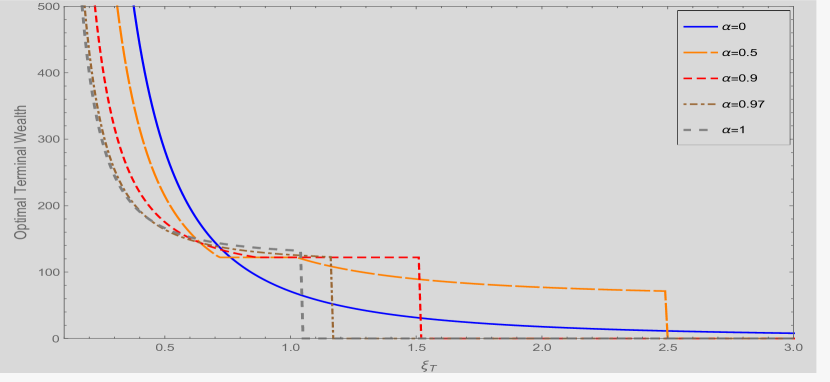

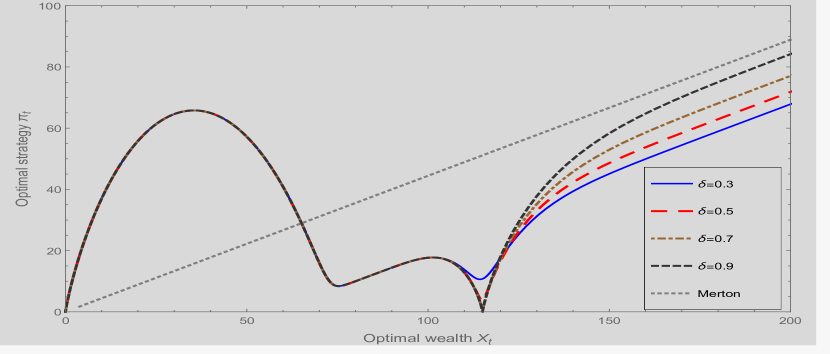

Figure 2 plots the optimal terminal portfolio with different values of for the case with a defaultable contract and with a fully protected contract. It can be observed that the optimal terminal wealth can take a two-, three- or four-region form as also shown in Theorem 3.2. The first thing to note from the graph is that in both cases (with a defaultable or a fully protected contract) the investment riskiness admits a monotonicity in the overall participation rate . In particular for defaultable contracts, the insurer is most risk seeking for very large values of which can be seen by the fact that these values in good states (i.e., for small values of ) yield a relatively high terminal wealth while in bad states the terminal wealth is lower, and the unhedged region where the terminal wealth is zero increases. The reason might be that as will be seen below very high participation rates mean that the insurer contributes very limitedly in the investment pool for which it tries to compensate (since the bonus rate is fixed) by taking on more risks in order to mimic a Merton like terminal wealth in the good states for itself. Since in this case the insurer gets a bonus without contributing much, this is a classical moral hazard induced behavior. Similar effects can be observed for fully protected contracts.

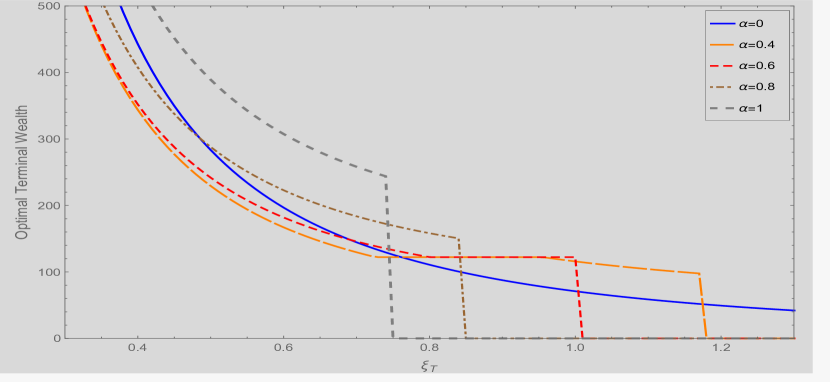

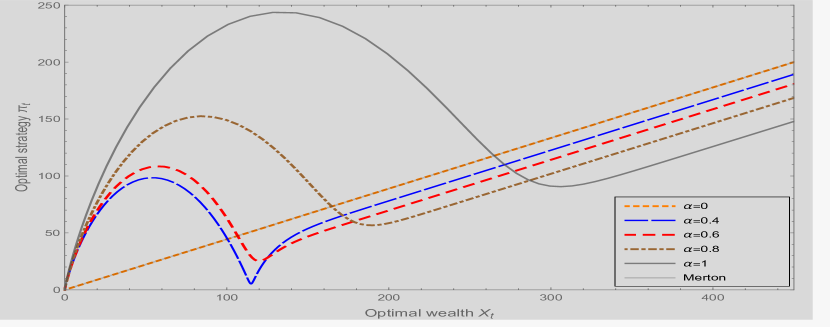

Figure 3 depicts the effect of the participating ratio and the bonus rate on the relationship between the optimal strategy and the wealth level at time , two years before maturity. As revealed in the figure, the optimal amount invested in the risky asset is always non-negative and exhibits a peak-valley structure. The reason for the peak is that if the wealth becomes low the equity holder (insurer) is left with nothing or even with negative wealth and will try push the wealth back “into the money” by significantly investing into the risky asset. Once the wealth is above the guarantee level the investment behavior normalizes, i.e., becomes more like the Merton benchmark case.

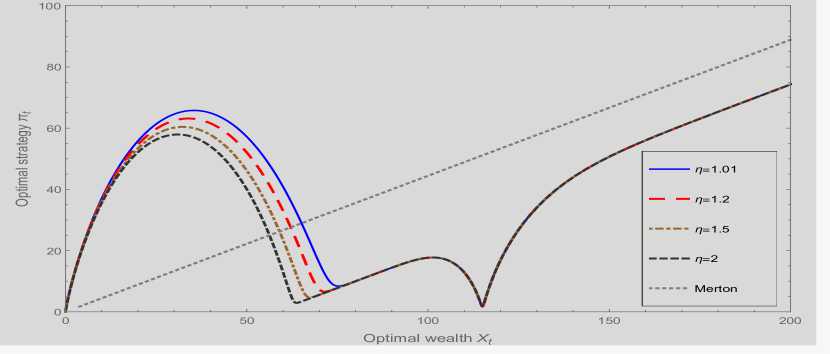

Consistent with what has been observed in Figure 2, the investment riskiness for a fixed bonus rate increases if the policyholder contributes very much to the contract. The effect of the bonus rate on the optimal strategy is presented in the right panel of Figure 3, showing that for a given participation rate the exposure to risk decreases for low terminal wealth and increases for a larger terminal wealth if the contract provides the policyholder a higher bonus rate . Again this is due to two effects: the first effect is that with higher bonus rates the contract becomes less valuable for the equity holder, implicitly lowering her wealth and shifting the curve to the left. The second effect is that in order to mimic the Merton strategy for her personal account the equity holder needs to actually increase the riskiness of their position when higher bonus rates are paid to the policyholder. The graph shows that the first effect outweighs the second effect in bad economic scenarios while the second effect is stronger in good economic scenarios where the strategy overall is less sensitive to shifts in wealth.

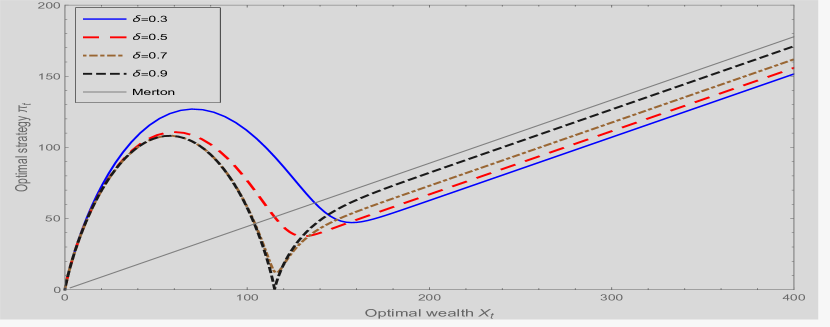

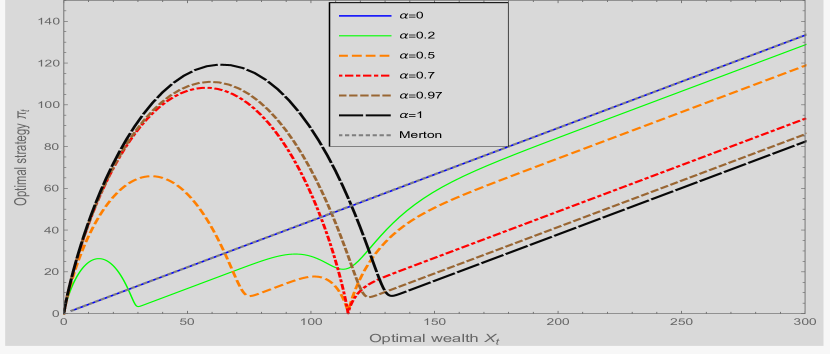

The effects of the participation rate , the bonus rate and the loss degree for a fully protected contract are illustrated in Figure 4. It can be observed from the left panel that in line with what has been discussed in Figure 3 given a fixed bonus rate and a loss degree, changing leads to monotone changes in the optimal strategy. In particular, high participation rates goes hand in hand with relatively risky investments of the insurance company in the loss states. Furthermore, the middle panel shows that given a participation rate, an increase in for fully protected contracts does not lead to a significant change in the exposure to risk in bad market scenarios. Hence, in these scenarios the investment of the insurer is rather robust with respect to the bonus rate and investments seem more motivated by the desire to avoid losses. Moreover, the higher , the closer the strategy to the Merton strategy in case of good performance. The right panel also shows that increasing the loss aversion leads the insurer to more prudent investment strategies in case of bad performance. However, the risky investment is almost the same in case of good performance. To explain this, we remark that an increase in only leads to higher sensitivity with respect to losses while the gain part is not influenced.

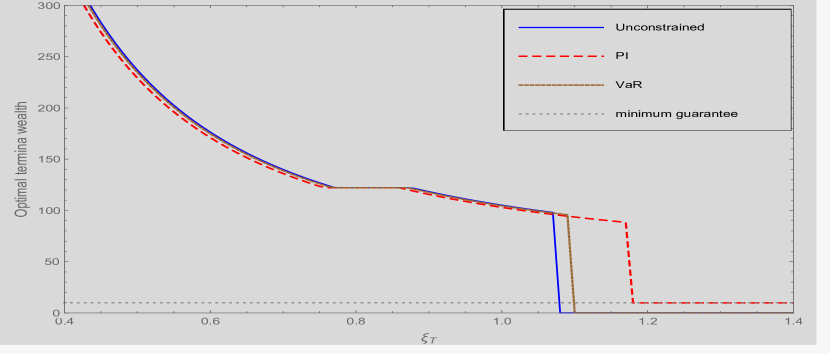

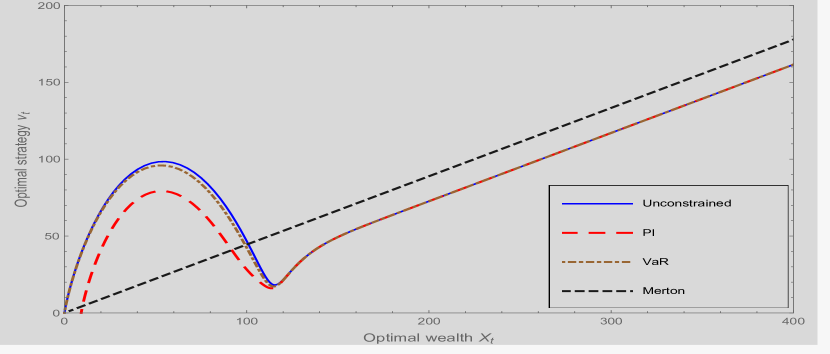

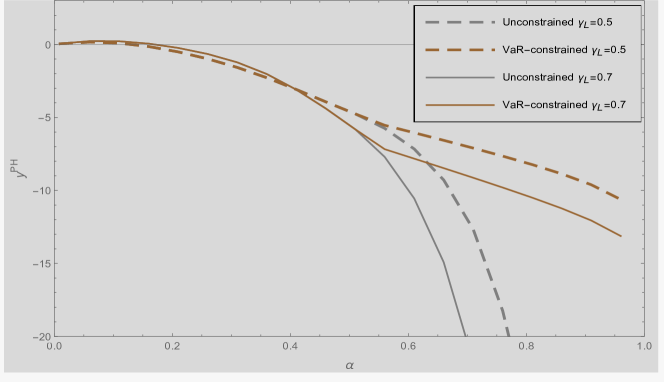

Let us now compare the unconstrained investment strategy with the constrained one under a VaR or a PI constraint. To serve this aim, the minimum guarantee in the PI problem and the default probability are chosen as and . The comparison of different strategies is presented in Figure 5 from which we can observe that the exposure to risk when the wealth process is small (the market condition gets worse) will be reduced by a VaR constraint. In particular, the region where the terminal wealth is zero shrinks. Furthermore, we observe that the Solvency II VaR-type constraints lead to more prudent investment than investments which are not regulated (i.e., come from unconstrained optimization problems). This result is contrary to the situation where the insurer maximizes the utility of the total wealth of the company (without distinguishing between equity holders and policyholders), in which case a VaR constraint may induce the insurer to take excessive risk leading to higher losses than in the case of no regulation, see [4, 17, 26, 18, 43]. These effects are more significant if a PI regulation is used. We also obtain similar effects on the optimal strategies for the case of full protected contracts.

In Figure 6, we report the effect of the participation rate in the policyholder’s well-being which is measured by the difference between the certainty equivalent of the unconstrained/VaR solution with the individual (unconstrained) Merton solution using as the initial capital. It can be observed that while the policyholder overall may suffer losses for high participation rates, she can even profit from participating in the contract for low participation rates. However, compared to the unregulated solution, losses are reduced by the use of a VaR constraint, which means that the policyholder will prefer a VaR-constrained portfolio to an unregulated portfolio. Moreover, the greater the risk aversion the more pronounced this effect, and different bonus rates overall do not change this conclusion.

In Table 1 we look at the certainty equivalents of both sides of a defaultable contract under a VaR or a PI regulation. We assume that the single policyholder also evaluates her terminal payoff by a power utility with the same risk aversion as the equity holder. To see the effect of the (VaR or PI) regulation (compared to the unregulated problem), we compute (resp. ) as the difference between the certainty equivalent of the VaR-solution/PI-solution and the unconstrained solution for the policyholder (resp. the equity holder). Some interesting conclusions can be derived from Table 1. Firstly, while both VaR and PI regulations imply a smaller expected utility for the insurer, it is in favor of the policyholder, i.e., she receives more expected utility from a VaR or a PI-constrained portfolio than from an unregulated portfolio. For both types of regulation, the gains in terms of expected utility are greater for higher participation rates, while being smaller for higher bonus rates. This observation is consistent with Figure 6. Secondly, a stricter regulation (a smaller allowed default probability in the VaR problem or a higher level in the problem) will enhance the benefit of the policyholder but deteriorate that of the insurer.

| VaR, | 0.1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

|---|---|---|---|---|---|---|---|---|---|

| 0.3 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| 0.5 | 5.3812 | -0.62107 | 1.59776 | -0.10904 | 0. | 0 | 0 | 0. | |

| 0.7 | 27.2518 | -5.54112 | 16.7027 | -2.37756 | 4.85723 | -0.41025 | 0 | 0 | |

| 0.9 | 55.9921 | -16.2817 | 47.4525 | -10.4539 | 35.6956 | -4.83685 | 8.81385 | -0.35244 | |

| VaR, | 0.1 | 0 | 0 | 0. | 0. | 0 | 0 | 0 | 0 |

| 0.3 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| 0.5 | 2.93424 | -0.176109 | 0 | 0 | 0 | 0 | 0 | 0 | |

| 0.7 | 24.004 | -4.14662 | 14.0463 | -1.53169 | 2.78551 | -0.11097 | 0 | 0 | |

| 0.9 | 51.7909 | -13.9376 | 43.9733 | -8.84345 | 32.9618 | -3.94988 | 6.86441 | -0.17468 | |

| PI, | 0.1 | 3.12 | -3.75 | 2.20 | -2.66 | 1.50 | -1.86 | 1.00 | -1.28 |

| 0.3 | 0.25411 | -0.02999 | 0.12641 | -0.01546 | 0.05253 | -0.00695 | 0.01686 | -0.00261 | |

| 0.5 | 5.78032 | -0.98316 | 2.99816 | -0.49857 | 0.98081 | -0.17662 | 0.10744 | -0.03192 | |

| 0.7 | 18.8767 | -3.35867 | 14.8676 | -2.04577 | 6.31463 | -0.76591 | 0.48069 | -0.07828 | |

| 0.9 | 30.1992 | -5.43378 | 29.6519 | -3.98221 | 27.0092 | -2.45201 | 10.5917 | -0.50173 | |

| PI, | 0.1 | 3.23 | -3.89 | 2.24 | -2.75 | 1.53 | -1.92 | 1.02 | -1.32 |

| 0.3 | 0.28132 | -0.03518 | 0.13706 | -0.01783 | 0.05567 | -0.00789 | 0.01737 | -0.00291 | |

| 0.5 | 7.81038 | -1.54023 | 3.61826 | -0.71464 | 1.02386 | -0.22852 | 0.08654 | -0.03771 | |

| 0.7 | 28.8837 | -6.73458 | 19.1421 | -3.55756 | 6.63452 | -1.10254 | 0.38439 | -0.08946 | |

| 0.9 | 48.5809 | -13.1827 | 45.0528 | -9.4583 | 37.6635 | -5.35405 | 10.1804 | -0.67902 | |

| PI, | 0.1 | 3.23 | -3.89 | 2.24 | -2.75 | 1.53 | -1.92 | 1.02 | -1.32 |

| 0.3 | 0.28147 | -0.03522 | 0.1371 | -0.01785 | 0.05567 | -0.00790 | 0.01737 | -0.00292 | |

| 0.5 | 7.90473 | -1.56879 | 3.62667 | -0.72132 | 1.02165 | -0.22938 | 0.08613 | -0.03776 | |

| 0.7 | 30.5322 | -7.50628 | 19.1683 | -3.72849 | 6.56806 | -1.11328 | 0.38303 | -0.08952 | |

| 0.9 | 60.1018 | -19.1469 | 50.6672 | -12.4667 | 37.9901 | -6.00355 | 10.1406 | -0.68012 | |

6 A two-period optimization framework

In this section we assume that the insurer is able to update the intertemporal information at an intermediate time point , with . More precisely, we assume that policyholders participate in the pool at time zero and the death event of policyholder in the first period is modelled by , where is a binomial random variable. Let be the number of deaths in the first time interval . At time , dividends are paid out to the survivors and death benefits are paid out to the designated beneficiaries of the persons deceased. We suppose that are mutually independent and independent of the assets .

Given that policyholder has survived in the first period, i.e., , we model by the death event of policyholder in the second period . To be consistent with the results in the previous sections, we assume that conditional on , is a binomial random variable, and a.s. if . Again, we suppose that are mutually independent and independent of the financial assets.

For such a two-period framework, we now have to work on an enlarged probability space , where is the enlargement of the financial filtration that contains the information generated by the death variables. represents the structure of the global information available to the insurer over the time horizon . Specifically, let , be the sigma algebra generated by the death variables in the first and second period. From the model setting, we can choose the enlargement as follows

Our admissible strategy is defined as where is an -adapted process and is an -adapted process. Note that the investment strategy in the last period depends on the death realizations at time . Due to the death benefit and dividend payments, the portfolio process admits a downside jump at whose size is equal to the total death payment in the first period . The policy of death and dividend payments will be specified below. We note that such a policy needs to guarantee the admissibility in the interval under a VaR regulation at maturity .

Let be the number of deaths in . The number of policyholders alive at maturity is given by . We assume that conditional on , the death variables in , , are independent. Put , which economically represents the total proportion of the guaranteed payment that the insurer has to pay to those who have died between and . General death benefit and dividend payments will be specified below.

We assume that the insurer has to satisfy a VaR regulation imposed at . To simplify the presentation we consider the case of a defaultable contract in what follows. The case of fully protected contracts can be treated in a similar way. The insurer has to solve the following VaR optimization problem:

| (27) |

for some probability default level . We remark that for any admissible portfolio of Problem (27) the unconditional VaR constraint always holds.

For simplicity below we drop the dependency of the portfolio on the strategy and initial wealth. Due to the information updated at the intertemporal time , Problem (27) can be solved recursively. More precisely, given the death information and the wealth level at time (after death benefit and dividend payments are made), from time on, an optimal strategy has to attain the supremum in

| (28) |

However, Problem (28) can be transformed into an equivalent optimization in a fully complete market as in Section 2. To this end, let be the finite set of all possible outcomes of . Using the independence of and we define

where stands for the conditional expectation operator with respect to the distribution of given . As shown in Lemma 2.1 the function is strictly increasing and concave on with derivative given by a similar form as in (13).

Problem (27) on the interval is equivalent to the following optimization in a fully complete market:

| (29) |

and the budget constraint Note that the VaR constraint will only be fulfilled if the wealth value after death payment at time is greater or equal to the time- value of the (stochastic) level , where is implicitly determined by , that is,

| (30) |

The optimal terminal portfolio is given by Theorem 4.1. For simplicity, we assume that the first case holds, i.e., and the optimal terminal wealth is given by

| (31) |

where the second term indicates the case where the VaR constraint is not active. The other cases can be treated similarly. Note that the reference points are defined by (20) where the multiplier is characterized by the budget equation at time :

| (32) |

Hence, should be considered as a function of , the wealth level after death benefit payment at time .

Indirect value function: Assume . Consider the indirect value function of the VaR constrained problem which will serve as the objective function in the next backward period.

| (33) |

For simplicity in the rest of this section we assume a simple Black-Schole’s model in which the wealth process starting with an initial wealth related to the strategy (where is an -adapted process and is an -adapted process) can be expressed as , where

| (34) |

and minus the death benefit and dividend payments at time , and

| (35) |

where are positive and deterministic processes. We denote by the market price of risk. Recall that the investment strategy in the last period depends on the death realizations at time . Due to death benefit and dividend payments, the portfolio process admits a downside jump at whose size is equal to the total death and dividend payment in the first period , i.e., the starting capital for the last period is defined by subtracted by the total death and dividend payment. The policy of death payment will be specified below. We note that such a policy needs to guarantee the admissibility in the interval under a VaR regulation at maturity .

We follow the technique in a multiple-VaR framework in [18]. Note that our current framework (27) is more general due to the non-concavity of and the presence of mortality. To make the presentation self-contained we will present the argument in detail. To this end, let us introduce some notation.

Notation: Below, stands for the Lebesgue norm of a deterministic function on , i.e. Note that the subscript is used to emphasize the considered interval time for . This notation will frequently appear in the sequel. For convenience, we will make use of the following functions

| (36) |

Hence, is the accumulated interest rate in the interval . The following simple property is frequently used in the analysis below.

Remark 4.

For any and with the notation above, we can write the state price density as

| (37) |

where is a standard normal variable independent of .

Now, it is straightforward to see that

| (38) |

where is the lower -quantile of the standard normal law. Let

| (39) |

The following result is useful for our analysis.

Lemma 6.1.

For any and , we have

| (40) |

Proof. As in Remark 4, observe that and the conclusion follows from a straightforward calculation. ∎

For later use we define

| (41) |

where we have applied Lemma 6.1. Economically, gives us the market value at time of $1 paid at time in case of an intermediate market scenario where .

The optimal wealth process is given by the following lemma:

Lemma 6.2.

Given a realized wealth level at time , the optimal wealth process on is given by , where

| (42) |

where is CDF of the log-normal variable and satisfies the budget constraint at time .

Note that the dependency on results from the reference points which are defined by (20) where the multiplier is characterized by the budget equation at time . Importantly, taking (20) into account we can represent the wealth process as , a functional of the product .

Recall that the VaR constraint at time may not be active if the wealth level at time is large enough. In this case the optimal terminal wealth is given by the unconstrained solution whose optimal portfolio is given by

| (43) |

which results from replacing with in (42). This critical wealth level can be explicitly determined from setting , or equivalently,

which is independent of . As before, we can consider the unbinding wealth process as , a functional of the product . Using the monotonicity of the inverse marginal utility function, one deduces that the terminal VaR constraint is not binding if and only if or equivalently, the wealth level at is greater or equal to

| (44) |

The value function at time for the case of a binding VaR constraint can be computed similarly as

| (45) |

Analogously, the indirect value function for the unbinding terminal VaR constraint can be computed by taking in (45) to obtain

| (46) |

Therefore, the indirect value function at time is given by

| (47) |

where is the natural switching point at which the terminal wealth “jumps” from the binding VaR case to the unbinding VaR case. It can be checked directly that is strictly increasing and is a continuous point of . Moreover, we observe that both value functions and , can be seen as functions of the product , and is a “smooth switching point” at which is continuously differentiable. Due to the budget constraint at time , the multiplier can be viewed as a function of the wealth level at time , .

Lemma 6.3.

The indirect value function is a globally strictly concave function satisfying Inada’s condition on and its two first derivatives are given by

| (48) |

Moreover, the inverse of is given by which is defined by

| (49) |

where

| (50) |

and

| (51) |

Proof. Following the same steps as in Lemma 5 in [18] and noting it can be checked directly that

Similarly, for we have and . ∎

Death benefit and dividend payment: Below we assume that at time the death and dividend payments are made only up to the level that the portfolio value after such payments is sufficient to satisfy the VaR regulation at maturity. In particular, let be a constant which represents the payment size for each death in the first period . Hence, the total death payment is equal to . We assume that each surviving policyholder receives a dividend payment equal to for some constant . We observe that the dividend payments are proportional to the difference of the portfolio value and the sum of the total death payment and the initial capital . This dividend policy takes an option-like form on the portfolio level with strike price equal to the sum of the minimal capital for the VaR constraint and the initial investment. These full death benefit and dividend payments are only possible if , i.e., if the portfolio value at time is sufficient to cover the VaR constraint at maturity.

If , the payments are made up to the level , the minimal capital level that is needed to satisfy the VaR regulation at maturity. The total death and dividend payment for this case is measured by .222From the insurer’s perspective, further specifications on the payments are not needed for the optimization problem (54).

Thus, due to death benefit and dividend payments, the portfolio value at time admits a downside jump which is characterized by

| (52) |

Let

The portfolio value after death benefit and dividend (if applicable) payments is given by

| (53) |

Recall that the insurer’s value function at time is given by , defined by (47). Due to the dynamic programming principle, the insurer therefore has to solve the following optimization problem

| (54) |

Note that the condition has been implicitly included in the use of the indirect value which is only defined on . Now, let us introduce for . By conditioning on the financial filtration and using the assumption that is independent of we can represent the optimization problem (54) as

| (55) |

Note that (55) is expressed as a non-concave optimization problem in a complete market. To solve it we look at its static version

| (56) |

subject to the usual budget constraint . For convenience, we introduce the sequence defined by

| (57) |

with and by convention. For the presentation of the solution we introduce the following sequence of increasing and concave functions defined in

| (58) |

Note that by construction, , which is a constant. Now, it can be observed that the objective function is identical to in the interval for each , or more precisely,

| (59) |

It is clear that is a continuous, increasing and piecewise concave function in . Note that is not differentiable at because

| (60) |

The solution of the non-concave optimization (56) is given by looking at the concavified function which is the double conjugate of . The convex conjugate of itself can be related to a family of upper-half hyperplanes whose intersection equals the region below the graph of . In particular, each member of this family is the smallest affine function of the form which dominates , i.e.,

Then, for a given slope , the corresponding conjugate of is the smallest constant being determined by

Since is not differentiable at the utility changing points , we have to first compute the above supremum on each interval . The convex conjugate follows from a comparison among these local maximums. In addition, is concave on each of these intervals and the corresponding supremum defines a convex and decreasing function in . Therefore, can be seen as a decreasing, convex and differentiable function except at a finite number of points (which are explicitly determined below as the tangency points depending on our parameters). Classical results from convex analysis ensure that the double conjugate is the smallest concave function which dominates , and on an interval where , is linear [14, 36]. The optimal terminal wealth is then given333 stands for right derivative of by for some Lagrangian multiplier determined via the budget constraint. For more details, see [15, 22, 14, 36, 8].

Theorem 6.1.

Assume that The optimal wealth before death benefit and dividend payments at time is then given by , where is determined via , the budget constraint at time zero.

Proof. This essentially follows from the results in Section 3 and 4 of [36]. It remains to check the integrability for the value function . Indeed, for any admissible portfolio value at time , we observe from (56) that

where is the unconstrained optimal terminal wealth for the case of defaultable contracts. ∎

We conclude this section by looking at the case where there is one policyholder in the pool, i.e., and only the death payment is made at time , i.e., . In this case, the solution can be given explicitly. First, noting that the value function defined by (59) is given by

In this situation, the concavified function of can be determined explicitly leading to an explicit solution. To this end, let be the inverse function of the first derivative , . We are now able to present the solution of the optimization problem (56).

Theorem 6.2.

Assume that and The optimal portfolio of Problem (56) is given by

| (61) |

where is defined by

| (62) |

and is determined such that the budget constraint is satisfied.

Before presenting the proof let us remark that (62) defines the linear line that is jointly tangent to the curve (defined on ) at a point (say ), and (defined on ) at another point (say ). The concavified function of is then defined by on , the joint tangency line on , and on .

Proof. For and , consider the Lagrangian

| (63) |

Note first that attains maximum at , . Furthermore, it follows from (58) that and for all and . Let . We observe that is increasing in and decreasing in if . This implies that is the global maximizer of for . Assume next . The global optimality of results from the comparison of and . To this end, consider the function Obviously , which implies that is decreasing in . Furthermore, since and we obtain . On the other hand, noting that we obtain

because is strictly concave in . Therefore, there exists such that which gives the concavification equation (62). Note that is strictly positive in and strictly negative in . The global maximizer of is then given by if or if . The sufficient verification can be done similarly as in the proof of Lemma A.1. ∎

Remark 5.

It is important to note that the modelling with one terminal constraint does not fully reflect the optimization problem of financial institutions in practice. More precisely, the assumption that the financial institutions never reevaluate their VaR portfolios after the initiation is quite unrealistic, especially for long-term portfolios. In practice, VaR constraints are imposed over a yearly, monthly or weekly time horizon.444For instance, according to Solvency II, the solvency capital requirement for the insurance companies is based on an annual VaR-measure calibrated to a 99.5% confidence level (c.f. Article 100 of Solvency II directive). Note that the regulation horizon is typically chosen by regulators, and financial institutions in general have to periodically report their VaR estimates for a prefixed shorter holding period555For example, as noted in [1], regulatory VaR requires that VaR estimates be made for a holding period of 10 working days at a significance level of 1%. Regulators use the number of violations as a proxy for the quality of the VaR modelling and an internal model is only accepted by the regulator if the number of violations is smaller than or equal to 10., leading to a multiple-VaR constrained optimization problem. Such a multiple-VaR regulation has been considered in the literature by many authors e.g. [21, 40, 26, 45, 41, 18] and we refer the reader to these works for further discussions. In particular, it is shown in e.g. [18] that for a concave utility framework under a multiple VaR constraint, by taking intertemporal time instances into account, the regulator can better control the risk of intertemporal bankruptcy before the terminal time period is reached, which is ignored if only the terminal VaR constraint is considered. Furthermore, a dynamic regulatory framework allows the financial institution to consistently update its overall strategy based on new information at the end of each period.

The two-period optimization framework in this section essentially shows that the utility maximization considered in this work can be extended to frameworks where there are multiple VaR constraints imposed within the regulation horizon and death benefit and dividend payments are made at a finite number of intermediate time points. This means that our analysis can be implemented according to the Solvency II capital requirement for insurance companies. Note that our analysis can be considered as an extension of the setting in [18] where the utility function is strictly concave and the entire market is assumed to be complete.

Fair pricing constraint: The above unconstrained optimal strategy maximizes the equity holders’ utility, leaving the question whether the policyholders are willing to participate in such a contract. To make the contract more attractive the insurer can choose the investment strategy that results from an optimization under a so-called fair pricing or fair participating constraint (see, e.g., [35, 16]), meaning that the initial value of each policyholder’s payoff is equal to her initial contribution. Note however that in this paper we mainly focus on regulatory aspects of VaR constraints motivated from the Solvency II regulation rather than on the problem of optimal product design. On the other hand, our framework allows for a pool of multiple contracts of heterogeneous policyholders with mortality risk for which the individual fairness is not the main point from the insurer’s perspective as it might be too challenging to take it into account for every policyholder. It seems in our setting more reasonable to assume that only those policyholders enter the contract in the first place, for whom a fair pricing constraint holds without the need for the insurer to readjust its strategy. In addition, it seems very challenging to specify even for one policyholder the individual fair participating constraint in the two-period framework with death and dividend payments studied above due to the market incompleteness666To incorporate fair pricing constraints in an incomplete market setting, one might use “good deal bounds” (initiated by [19] and extended by [9]) to narrow the set of pricing measures and discuss possible ways of defining the fair pricing constraint. and possible intermediate money withdrawals.

Below we briefly explain how the optimization developed here can be applied to the case of one policyholder without mortality or dividend payments. Mathematically, we now consider the following optimization problem (for )

under the fair pricing constraint , where the objective utility is defined by (15).

We remark first that if (i.e., the fair pricing constraint is not binding), the policyholder is willing to participate in such a contract because her contract value is higher than her initial investment . The solution to this problem is identical to the unconstrained solution given in Theorem 3.1. We exclude these cases in the following by assuming that the contract parameters satisfy . The optimization problem now reads

| (64) |

To solve the fair-pricing constrained optimization problem (64) we can rely on a Lagrangian approach with the usual concavification technique

for multipliers and . For each type of payoffs, we consider the convex conjugate

| (65) |

This leads to as a candidate for the optimal terminal wealth. The verification step is analogous to Lemma A.1 and the proof of existence of the Lagrangian multipliers requires some additional analysis of indifference curves which can be done along the lines of Appendix E in [16].

The analysis can be extended to the case where a VaR constraint at maturity is included. Obviously, such a study requires a more thorough analysis. However, as mentioned above it seems very challenging to treat all individual fair participating constraints for a pool of individual contracts in the two-period framework with death and dividend payments and a regulatory VaR constraint.

7 Conclusion

We solve a non-concave utility maximization problem for the equity holders of a participating life insurance contract under a VaR-type regulatory constraint imposed at maturity. We obtain a closed-form solution extending the martingale approach to constrained non-concave utility maximization problems. Our theoretical and numerical results show that for the case of a defaultable contract, the risk exposure in bad market conditions will be reduced by a VaR constraint. This result is contrary to most other results derived for VaR risk management e.g. [4, 17, 26, 18, 43] where the introduction of a VaR constraint increases the losses in the bad states as the risk manager has an incentive to push significant parts of the remaining risk into those parts of the tails not captured by VaR. The effects of the parameters of the contract are also discussed numerically. It is shown that the policyholders indeed benefit from a Solvency II type VaR-regulation in the sense of having greater expected utility. The prudent investment behavior for participating insurance contracts is more pronounced if a VaR-type regulation is replaced by a PI-type regulation. Furthermore, a stricter regulation (a smaller allowed default probability in the VaR problem or a higher minimum guarantee level in the problem) enhances the benefit of the policyholder but deteriorates that of the insurer. For both types of regulation, the gains in terms of expected utility are greater for higher participation rates, while being smaller for higher bonus rates. However, our results also show that in certain situations, for instance in the cases of relatively high participation rates and relatively low bonus rates, policyholders overall may in terms of expected utility prefer a VaR regulation, over a PI regulation with a relatively low minimum guarantee level. These results can be extended to multiple periods.

A Proofs

A.1 Proof of Theorem 3.1 (the unconstrained case)

This section is devoted to the detailed proof for the uncontrained problem (11). This problem can be solved by considering the static optimization of the Lagrangian

| (66) |

Notice that is not concave, which makes the problem more challenging to solve. We make use of a modified dual approach which shows that the global maximal value of can be attained at the local maximizers or at the utility changing points and , or even at the boundary point . Note that is not differentiable at and .

Lemma A.1.

For and , the unique solution of the problem , for , is given by

Proof. Note first that we are looking for the global maximizer of a three-part function , for where

Clearly, are concave functions having local maximizers and respectively. Note that since is convex, its maximum can be attained at the boundary points zero or . Due to the continuity at , i.e. , the global optimum is obtained by comparing with and .

From (20) we observe first that iff and iff . Therefore, we study the Lagrangian on the following subintervals of values of :

-

(a)

For , we have and so the Lagrangian is increasing from to and decreasing again in . So global optimality can be attained at or . To conclude, we consider

which is a decreasing function in . It follows that . If then and the global maximizer is . When , by Lemma 3.1 there exists such that . In this case, the global maximizer can be chosen as for or zero for .

-

(b)

For , but so the Lagrangian is increasing from to and decreasing again in . So global optimality can be attained at or . To conclude, we consider , which is a decreasing function in . It follows that . If then and the global maximizer is . When , the global maximizer is zero. It remains to consider the case . By Lemma 3.1, and . This implies that the global maximizer is for or is equal to zero for .

-

(c)

For , and so the Lagrangian is increasing from to and decreasing again in . So global optimality can be attained at or . We need to study which is a decreasing function in . Thus, . Therefore, zero is the maximizer if Suppose now that . By Lemma 3.1, there exists such that and the global optimality is attained at for and at zero for , respectively.

Note that is equivalent to (19) with , whereas is equivalent to (18) with . ∎

We now prove Theorem 3.1 and then Corollaries 3.2 and 3.4. Let us prove that defined by (A.1) is the solution to Problem (14). For any terminal wealth satisfying the budget constraint we have

| (67) | ||||

The last equality folows from . Hence, is optimal. The existence of the Lagrangian multiplier follows from the lemma below.

Lemma A.2.

For any , we have

-

1.

;

-

2.

;

-

3.

Furthermore, if for any , the mapping is strictly decreasing, continuous and surjective from to .

Proof. The first two conclusions follow from the observation that