Efficient estimation of stable Lévy process with symmetric jumps ††thanks: This work was partially supported by JSPS KAKENHI Grant Number JP26400204 and JST CREST Grant Number JPMJCR14D7, Japan (HM).

Abstract

Efficient estimation of a non-Gaussian stable Lévy process with drift and symmetric jumps observed at high frequency is considered. For this statistical experiment, the local asymptotic normality of the likelihood is proved with a non-singular Fisher information matrix through the use of a non-diagonal norming matrix. The asymptotic normality and efficiency of a sequence of roots of the associated likelihood equation are shown as well. Moreover, we show that a simple preliminary method of moments can be used as an initial estimator of a scoring procedure, thereby conveniently enabling us to bypass numerically demanding likelihood optimization. Our simulation results show that the one-step estimator can exhibit quite similar finite-sample performance as the maximum likelihood estimator.

1 Introduction

Let be a -stable Lévy process with a drift and symmetric jumps defined by

where denotes the standard symmetric -stable Lévy process characterized by its characteristic function

We refer to [23], [26] for a comprehensive account of the stable distribution. Throughout, we assume that the process is observed on regularly spaced time points for in the high-frequency setting with sampling stepsize as and with the terminal sampling time satisfying

| (1) |

The asymptotically efficient estimation of the three-dimensional unknown parameter

is considered in this paper.

As was shown in [1] and [18], the joint estimation of the scale and stable (or self-similarity) index leads to a singular Fisher information matrix as long as a diagonal-matrix norming rate is used. Consequently, the conventional convolution and minimax theorems are not of direct use, and an asymptotically minimal covariance matrix of sequences of estimators cannot be deduced in this statistical experiment. Any proper notion of efficiency for this experiment has not been detailed as yet in the literature, despite the theoretical and practical importance of the high-frequency data analysis and the fact that the stable Lévy processes constitute a fundamental class of non-Gaussian Lévy processes.

The asymptotic degeneracy is an intrinsic feature coming from the self-similarity of the underlying model. Recently, in the context of the observation of fractional Brownian motion observed at high-frequency, the singularity issue has been untied in [2] by using a non-diagonal norming matrix, and a classical local asymptotic normality (LAN) property of the likelihoods has been obtained with a non-degenerate Fisher information. The associated Hájek-Le Cam asymptotic minimax theorem is derived as a corollary; we refer to [12] for a detailed account of the LAN property and its consequences. It is worth mentioning that a non-diagonal norming has also been considered in proving the LAN property for the drift and scale parameters of a possibly skewed locally stable Lévy process from high-frequency data, when the activity index is assumed to be known (see [13, Remark 2.2] for some related remarks), and in the joint estimation of the index and the scale parameters of a stable subordinator when observing the biggest jump sizes with their jump instants precisely (see [11]).

Contrary to the large sample asymptotics with fixed sampling stepsize, the LAN property of the likelihoods cannot be deduced from Le Cam’s second lemma in the high-frequency setting. Consequently, this study enlarges the domain of application of the LAN theory already proved for i.i.d. classical setting [10], [15], ergodic Markov chains [22], ergodic diffusions [9], diffusions under high-frequency observations [8], diffusions with observational noise [6], [7], [20], several Lévy process or Lévy driven models [3], [14], [18] and fractional Gaussian noise [2], [4].

The purpose of this paper is twofold. Firstly, the LAN property of the likelihoods for the aforementioned high-frequency statistical experiment is proved with a non-diagonal norming rate and a non-singular Fisher information matrix. In particular, a Hájek-Le Cam lower bound for any estimator can be derived so that efficiency can be described. A sequence of maximum likelihood estimators (MLE) is shown to be asymptotically normal and asymptotically efficient. In the proofs, the analytic properties of the probability density function of is fully used.

Although the exact likelihood function can be numerically computed, the likelihood function considered here involves the local scaling by the factor , making numerical evaluation of a maximum-likelihood estimate more time-consuming compared with the i.i.d. model setup (see (2) below). In this respect, it is beneficial to construct a computationally easy-to-use estimator which is asymptotically equivalent to the MLE. Therefore, as a second purpose of the present study, we exemplify such an asymptotically optimal estimator through a preliminary method of moments combined with the scoring procedure.

2 Likelihood asymptotics

We write for the ordinary uniform convergence (for non-random quantities) with respect to over any compact set contained in . For any continuous random functions and , , we introduce the following two modes of uniform convergence: we write if

as for every bounded uniformly continuous function , where denotes the distribution of ; also, letting denote the distribution of we write if for every ,

as . We will omit the subscript “” to denote the convergences without the uniformity. We write when there exists a universal multiplicative constant such that for every large enough. For positive functions and , we denote if for any compact .

Let , the th increments of the process . Since has independent and stationary increments, the log-likelihood function based on observing is given by

| (2) |

where denotes the density of and

The distribution of associated with is denoted by and the associated expectation operator by . For each and , ’s are -i.i.d. -stable random variables under .

Let be a continuous mapping of the block-diagonal form

| (3) |

This matrix will play the role of the proper rate matrix of the MLE. As with [2], concerning the upper-left part of we assume the following conditions:

| (4) |

where the last condition must hold for any compact set ; these conditions naturally come from the form of the normalized score function (see (14) below). For later reference, we note that for every such ,

Under (1), it holds that and

Hereafter, we will often omit the dependence on and/or on from the notations, such as , , , and so on.

We deduce from [5] (see also the references therein and [19]) that for each nonnegative integers and ,

| (5) |

Let

By the property (5) together with the facts that and are even and odd, respectively, the symmetric matrix

| (6) |

which only depends on among the components of , is continuous in , and satisfies that . Moreover, we introduce the non-degenerate block-diagonal matrix ( denotes the transpose)

which will turn out to be the asymptotic non-degenerate Fisher information matrix.

The normalized score (central sequence) is defined by

and the normalized observed information matrix by

The main claim of this section follows below.

Theorem 2.1.

-

1.

The uniform LAN property holds:

for any compact set , where and is positive definite for each .

-

2.

There exists a local maximum of with probability tending to , for which

Several remarks on Theorem 2.1 are in order.

-

1.

The non-degeneracy of and in Theorem 2.1 is essential. Let be any non-constant function such that: ; the set is convex for each ; is continuous at ; finally, for all . Then, it follows from the Hájek-Le Cam asymptotic minimax theorem ([10], [12, Chapter II.12], [15]) that for each and and for any sequence of estimators we have

where denotes the density of the three-dimensional standard normal distribution. Theorem 2.1 ensures that a sequence of MLE is asymptotically efficient. It should be emphasized that the element does depend on a spcific choice of the non-diagonal norming matrix .

-

2.

Several examples of rate matrices satisfying the conditions (4) can be elicited. For instance, the two following rate matrices

(7) which gives , , and and

(8) which gives , , and can be considered. Remark that these examples are non-diagonal rate matrices depending on the scale parameter and the stable index . For each and , using the rate matrix (7) and the function we can deduce the lower bound

(9) for specified in (6). Likewise, using the rate matrix (8) and the function , we can deduce that

(10) -

3.

The explicit form of itself will not explicitly appear in the proof of Theorem 2.1. It is expressed as

(14) for which a direct application of the Lindeberg-Feller theorem yields that under .

-

4.

What is essential in the derivation of the likelihood asymptotics is the self-similarity of , hence the stable-distribution property of since the stable Lévy process (including a Wiener process, of course) is the only self-similar one among the whole family of Lévy processes. Further, in the nature of high-frequency asymptotics, small-time behavior of is of primary concern. In this respect, it is readily expected that a similar LAN and/or LAMN phenomena can be deduced for locally stable Lévy processes, and even more generally, for non-linear stochastic differential equations driven by a locally stable Lévy process, where a Lévy process is said to be locally -stable if weakly convergence to as . Of course, such considerations must require expertise of stochastic calculus on Poisson space. We refer to [13] and [3] for related previous studies in case of known .

Proof of Theorem 2.1.

We will complete the proof by verifying Sweeting’s conditions [C1] and [C2] in [24], which here read as follows.

-

•

Uniform convergence of the observed information matrix:

(15) where is positive definite for each .

-

•

Uniform growth rate of the norming matrix :

(16) for any , where

a shrinking neighborhood of , and where denotes the -identity matrix.

-

•

Yet another uniform convergence of :

(17) for each , where

Having proved these three claims, by means of [24, Theorems 1 and 2] it is straightforward to deduce the assertions as in [18, Theorem 2.10]; although the latter theorem deals with the diagonal norming, the proof can be traced without any essential change.

Proof of (15).

Since , we have . Schwarz’s inequality then shows that , hence we also have : is positive definite for each . It remains to show that

we refer to [18, the proof of Theorem 3.2] for the explicit expressions of all the elements of . We will repeatedly make use of the following basic fact without mention: for a row-wise independent triangular array with for each , we have if both and .

Proof of (16).

Fix in the rest of this proof. Write

for the upper-left -part of . Then it suffices to show that

To this end, we first prove

| (24) |

Note that for , where . Let

whose absolute value under (4) is bounded away from : . For convenience, we will write

| (resp. ) if (resp. ) |

for any function on . Straightforward algebra leads to the identity

| (25) |

with satisfying that

and

By the continuity in , we have

The minimum eigenvalue of the first term in the right-hand side is

with and ; by completing squares, we see that the term is nonnegative. Since is monotonically decreasing on and , we conclude that

Therefore, by (25) we have

so that , hence (24).

Proof of (17).

For we have

It follows from (2) and (5) that for each ,

Hence, we can (rather roughly) estimate as follows:

| (27) | |||

where the supremum is taken over both lying in a closed ball with center and radius of for some constant possibly depending on ; for the estimate (27), we made use of the last part of the proof of (16) and also the fact that to replace by . ∎

3 Simple efficient estimator

The log-likelihood function (2) is rather complicated and not given in a closed form except for the Cauchy case . In particular, by the parameter which is here also present inside the density , the optimization issue has difficulty not shared with the classical i.i.d. setting where , hence the standard library for fitting a stable distribution on computer, such as [21] and those cited in [19], cannot be of direct use. Still, once an easy-to-compute initial estimator having an asymptotic behavior good enough, we can benefit from the classical scoring, which enables us to bypass time-consuming numerical search for . The purpose of this section is to provide such an efficient estimator.

We keep using the notations introduced in Section 2. Throughout this section, we fix a true value , and proceed with the single image measure (so ).

3.1 Scoring procedure and asymptotic normality

By Theorem 2.1 we can consider a sequence of -measurable random variables such that and that . Suppose for a moment that we have an estimator such that

| (28) |

Define the one-step MLE by

| (29) |

which is well-defined with probability tending to . Then, by means of Fisher’s scoring together with making use of the properties (15), (16), and (17), we see that is asymptotically equivalent to the MLE, that is . By Theorem 2.1, this implies that

| (30) |

We remark that the likelihood function , its partial derivatives and the components of (recall (6)) can be computed through numerical integration with high precision (see [19] and the references therein).

3.2 Initial estimator

We here show that the method of moments based on appropriate moment matchings with sample median adjustment provides us with an initial estimator satisfying (28). We will follow the same scenario as in [16] (also [18, Section 3.3]), as described below.

For brevity (yet without loss of generality) we set to be odd, say . Let

| (31) |

where denote the order statistics of . From theory of order statistics or that of the least absolute deviation estimation, we know that is rate-efficient ([16], [18]):

| (32) |

its asymptotic distribution being .

Let be a function such that the following two conditions hold: there exist a constant and a Lebesgue integrable function such that

| (33) |

and moreover

| (34) |

Then we consider

where we removed the index for the summation to subsume cases where is not defined, such as the case considered later on. Note that at this stage the elements of the vector may be infinite, or even not well-defined, depending on specific value of . It will be convenient to introduce an auxiliary value such that

| (35) |

(recall that we are fixing a true value ); this form is enough to cover the example in Section 3.4, where we will demonstrate that the restriction (35) does not force us to narrow the parameter space of beforehand. Under the conditions (33) and (34) we can apply the median-adjusted central limit theorem [18, Theorem 3.7] for , hence in particular . Assume that the random equation

| (36) |

with respect to has a unique solution with -probability tending to , and let

Now, we claim that (28) holds for any norming matrix satisfying (4) (though we here do not require the uniformity in ), if the following conditions hold:

| a.s. and ; | (37) | ||

| (38) | |||

| (39) | |||

| (40) |

where (39), which comes from the rate-matrix condition (4), should holds for any such that . As a matter of fact, it will turn out that the distribution of is asymptotically (non-degenerate) normally distributed.

Recall the notation and that denotes the upper-left -submatrix of (see the expression (3)). Write and . To deduce the claim, we expand around on the event :

where is a point on the segment joining and . It follows from (37) and (38) that is -consistent and that

Further, by (4) we have . Building on these observations combined with (39) and direct computations based on (4), we obtain the following chain of equalities between matrices:

This clearly shows that the condition (39), which may seem unusual at first glance, combined with (4) is quite natural in our framework. By [18, Theorem 3.7], the random variable is asymptotically normally distributed with non-degenerate asymptotic covariance matrix. Piecing together what we have seen and the invertibility condition (40) gives

| (41) |

The tightness (28) now follows from the stochastic expansions (32) and (41) together with the form (3) of .

3.3 Asymptotic efficency

Theorem 3.1.

Assume that the conditions (33) and (34), and (37) to (40) hold. Then, the random equation (36) has a unique solution with -probability tending to , and we have (28) for any norming matrix satisfying (4) (without the uniformity in ). Moreover, the estimator defined by (29) is asymptotically efficient in the sense that the asymptotic normality (30) holds.

3.4 Examples and simulations

Here we discuss the two specific examples of treated in [18]:

| and . |

The choice is closely related to Todorov’s result [25], where he derived a stable central limit theorem associated with the power-variation statistics for a class of pure-jump Itô semimartingales.

It suffices to set and for and , respectively; note that the latter choice comes from the condition (34). Since should be given a priori, this implies that we are forced to pick a such that

| (42) |

with the true value being unknown; of course, this problem does not appear when, for example, we assume from the very beginning that has a finite mean, so that we may set and any can be used. In Section 3.4.1 we will first verify the aforementioned conditions (37) to (40) for both of and in parallel, with supposing that the tuning parameter satisfies (42) for . Then in Section 3.4.2 we will show that by introducing an auxiliary estimator of through splitting data we can proceed as if the condition (42) does hold without any prior knowledge about . 111We are grateful for the anonymous reviewer for suggestion on this point.

3.4.1 Verification with knowing (42) for

The estimating equation (36) can be successfully solved with respect to , and appropriate delta methods leads to the asymptotic normality of ; see [18, Sections 3.3.5 and 3.3.6] for details. The next step, estimation of , is of primary importance in the present study. Plugging into the first components of the original estimating equations (corresponding to and respectively for and ), and then again using the tightness of , we deduce the following stochastic expansions:

for the cases of and , respectively; these expansions clarify asymptotic linear dependence of and , which is quite similar to [17, Eq.(3.76)] in the context of moment estimation of a skewed stable model without drift. Thus, the tightness condition (38) holds in both cases.

We know that

| (45) | ||||

| (48) |

for the cases of and , respectively, where

with : the differentiability (37) is trivial. Solving the random equation is numerically easy and fast: we have the explicit solution in the case, and also we can apply the simple bisection search for the case.

For any random sequence , straightforward computations lead to the following:

| (51) |

for the case, and also

| (54) |

for the case. Let be a -consistent estimator of , and recall that . Then, the right-hand sides of (51) and (54) both equal , hence the condition (39).

3.4.2 Verification without knowing (42)

Now let us consider when we do not know if (42) holds or not. Pick an increasing sequence such that

Let denote the -moment estimator of constructed only from the first increments . As was seen in Section 3.4.1 we have .

Let be a (small) number, and set

Then we observe that

| (55) |

Now, denote by the sample-median based estimator of defined as in (31) except that it is now constructed from ; here again, we may set odd. Also, denote by the th-moment estimator of defined as in Section 3.4.1 except that it is computed based on with plugging-in . Then, we define

By its construction, is independent of . Further, since and have the same distribution, the distribution of the estimator conditional on the event is the same as the one of based on where we can regard as a constant sequence converging to as . Hence, under the additional condition

| (56) |

it follows from (55) that

That is, as an initial estimator meets the condition (28). This together with Theorem 3.1 and what we have seen in Section 3.4.1 concludes that the estimator given by (29) with is asymptotically efficient. Thus, we have shown that under the condition (56), the th-moment estimator can be used as if (42) is true without any previous knowledge of ; in practice, we first compute and then fix any , followed by for that .

3.4.3 Simulation

Finally we present a simulation result. We set for brevity and focused on comparing performances of joint estimation of through the MLE, the one-step MLE, and the th-moment estimator with ; for simplicity, we implicitly assume that (42) holds, that is, . We set and simulated Monte-Carlo samples of i.i.d. symmetric -stable random variables with index and scale for . The th-moment estimator was also used as the initial estimator in the one-step MLE (29) with rate matrix being the upper-left -submatrix of (7).

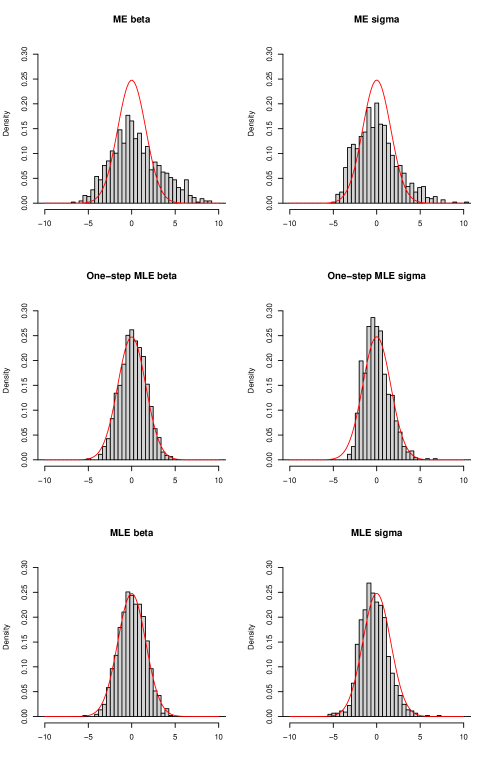

Figure 1 shows the histograms based on the normalized statistical errors

| and |

on the left and the right, respectively, for being the simulated sequences of the moment estimators (ME, on the top), the one-step MLEs (in the center), and the MLEs (on the bottom). In each panel, the solid line represents the asymptotic normal distribution with efficient variance ; see (9) and (10). The implementations of the likelihood, the score and the Fisher information for computing the sequences of the MLE and the one-step MLE are based on [19]. From Figure 1, we can observe that the histograms of the moment estimators are far from the efficient asymptotic normal distributions, whereas both of the one-step MLE and the MLE sequences show much better performances.

Acknowledgement. The authors also thank the reviewers and the associated editor for their valuable comments, which in particular led to substantial improvements of the arguments in Sections 3.2 and 3.4. HM especially thanks Professor Jean Jacod for letting him notice the mistake in [16], which has been fixed in the present paper.

References

- [1] Y. Aït-Sahalia and J. Jacod. Fisher’s information for discretely sampled Lévy processes. Econometrica, 76(4):727–761, 2008.

- [2] A. Brouste and M. Fukasawa. Local asymptotic normality property for fractional gaussian noise under high-frequency observations. arXiv preprint arXiv:1610.03694, To appear in Ann. Statist.

- [3] E. Clément and A. Gloter. Local asymptotic mixed normality property for discretely observed stochastic differential equations driven by stable Lévy processes. Stochastic Process. Appl., 125(6):2316–2352, 2015.

- [4] S. Cohen, F. Gamboa, C. Lacaux, and J.-M. Loubes. LAN property for some fractional type Brownian motion. ALEA Lat. Am. J. Probab. Math. Stat., 10(1):91–106, 2013.

- [5] W. H. DuMouchel. On the asymptotic normality of the maximum-likelihood estimate when sampling from a stable distribution. Ann. Statist., 1:948–957, 1973.

- [6] A. Gloter and J. Jacod. Diffusions with measurement errors. I. Local asymptotic normality. ESAIM Probab. Statist., 5:225–242, 2001.

- [7] A. Gloter and J. Jacod. Diffusions with measurement errors. II. Optimal estimators. ESAIM Probab. Statist., 5:243–260, 2001.

- [8] E. Gobet. Local asymptotic mixed normality property for elliptic diffusion: a Malliavin calculus approach. Bernoulli, 7(6):899–912, 2001.

- [9] E. Gobet. LAN property for ergodic diffusions with discrete observations. Ann. Inst. H. Poincaré Probab. Statist., 38(5):711–737, 2002.

- [10] J. Hájek. Local asymptotic minimax and admissibility in estimation. In Proceedings of the Sixth Berkeley Symposium on Mathematical Statistics and Probability (Univ. California, Berkeley, Calif., 1970/1971), Vol. I: Theory of statistics, pages 175–194, Berkeley, Calif., 1972. Univ. California Press.

- [11] R. Höpfner and J. Jacod. Some remarks on the joint estimation of the index and the scale parameter for stable processes. In Asymptotic statistics (Prague, 1993), Contrib. Statist., pages 273–284. Physica, Heidelberg, 1994.

- [12] I. A. Ibragimov and R. Z. Has′minskiĭ. Statistical estimation, volume 16 of Applications of Mathematics. Springer-Verlag, New York, 1981. Asymptotic theory, Translated from the Russian by Samuel Kotz.

- [13] D. Ivanenko, A. M. Kulik, and H. Masuda. Uniform lan property of locally stable lévy process observed at high frequency. ALEA Lat. Am. J. Probab. Math. Stat., 12(2):835–862, 2015.

- [14] R. Kawai and H. Masuda. Local asymptotic normality for normal inverse Gaussian Lévy processes with high-frequency sampling. ESAIM Probab. Stat., 17:13–32, 2013.

- [15] L. Le Cam. Limits of experiments. In Proceedings of the Sixth Berkeley Symposium on Mathematical Statistics and Probability (Univ. California, Berkeley, Calif., 1970/1971), Vol. I: Theory of statistics, pages 245–261. Univ. California Press, Berkeley, Calif., 1972.

- [16] H. Masuda. Joint estimation of discretely observed stable Lévy processes with symmetric Lévy density. J. Japan Statist. Soc., 39(1):49–75, 2009.

- [17] H. Masuda. On statistical aspects in calibrating a geometric skewed stable asset price model. In Recent Advances in Financial Engineering 2009: Proceedings of the KIER-TMU International Workshop on Financial Engineering 2009, pages 181–202, 2010.

- [18] H. Masuda. Parametric estimation of Lévy processes. In Lévy matters. IV, volume 2128 of Lecture Notes in Math., pages 179–286. Springer, Cham, 2015. Edited by Ole E. Barndorff-Nielsen, Jean Bertoin, Jean Jacod, and Claudia Küppelberg.

- [19] M. Matsui and A. Takemura. Some improvements in numerical evaluation of symmetric stable density and its derivatives. Comm. Statist. Theory Methods, 35(1-3):149–172, 2006.

- [20] M. Reiß. Asymptotic equivalence for inference on the volatility from noisy observations. Ann. Statist., 39(2):772–802, 2011.

- [21] Robust Analysis, Inc. User manual for stable 5.3 R version. 2017. Available at http://www.robustanalysis.com [Accessed on November 1, 2017].

- [22] G. G. Roussas. Contiguity of probability measures: some applications in statistics. Cambridge University Press, London-New York, 1972. Cambridge Tracts in Mathematics and Mathematical Physics, No. 63.

- [23] K.-i. Sato. Lévy processes and infinitely divisible distributions, volume 68 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge, 1999. Translated from the 1990 Japanese original, Revised by the author.

- [24] T. J. Sweeting. Uniform asymptotic normality of the maximum likelihood estimator. Ann. Statist., 8(6):1375–1381, 1980. Corrections: (1982) Annals of Statistics 10, 320.

- [25] V. Todorov. Power variation from second order differences for pure jump semimartingales. Stochastic Process. Appl., 123(7):2829–2850, 2013.

- [26] V. M. Zolotarev. One-dimensional stable distributions, volume 65 of Translations of Mathematical Monographs. American Mathematical Society, Providence, RI, 1986. Translated from the Russian by H. H. McFaden, Translation edited by Ben Silver.