This paper studies local asymptotic relationship between two scalar estimates.

We define sensitivity of a target estimate to a control estimate to be the directional

derivative of the target functional with respect to the gradient direction of the control

functional.

Sensitivity according to the information metric on the model manifold is the asymptotic covariance

of regular efficient estimators.

Sensitivity according to a general policy metric on the model manifold can be obtained from

influence functions of regular efficient estimators.

Policy sensitivity has a local counterfactual interpretation, where the ceteris paribus

change to a counterfactual distribution is specified by the combination of a control parameter and

a Riemannian metric on the model manifold.

††May 18, 2018

1. Introduction

Balancing simplicity of statistical methodology with complexity of economic modeling is a

challenge in empirical work. Structural models lead to estimators with nontransparent dependence

on data. Both structural and predictive models are subject to specification choices that have

nontransparent influence on inferences. However, regular estimators of parameters in these models

have simple asymptotic behavior and can be understood well locally.

Regularity allows to draw local comparisons (approximations) between two estimators and

obtain local counterfactuals of their values.

For example, it may be useful to know that a structural estimator is locally well approximated

with a simple {mean, variance, quantile, etc}.

Or that two alternative specifications provide similar results not only at the sampling

distribution but in a neighborhood around it.

Sensitivity measures formalize local comparisons and counterfactuals, and add transparency

to inferences made with structural models.

We examine geometric foundations of estimator sensitivity and highlight the role

of the information metric in asymptotics of regular estimation. Covariance of joint

asymptotic distribution is the information inner-product that measures alignment of

first-order approximations to regular parameters. This is a natural measure of local

approximation quality between two estimators.

Differentiability has a prominent role and a long history in regular asymptotics from von

Mises (1947) [42] to van der Vaart (1991) [60] and

Newey (1994) [46], we go a step further and develop complete

differential calculus on the model.

We define sensitivity as a directional derivative and propose it as a general tool for local

counterfactual analysis as in Stock (1989) [57] and

Chernozhukov, Fernández-Val and Melly (2013) [15].

Instead of specifying a counterfactual distribution of control variables, we think of

policy as shifting the value of a control parameter. Sensitivity measures the effect of

policy on the value of a target parameter.

For example, the local effect of changing the {mean, variance, quantile, etc} of a

distribution on the {mean, variance, quantile, etc} of the distribution.

Both the implicit counterfactual distribution and the sensitivity (directional derivative)

depend on the way policy measures distances on the model.

Asymptotic covariance is shown to be such a directional derivative with a particular

choice of geometric primitives.

To put our work in perspective, let us disassemble empirical analysis in economics into a

stack of layers and interfaces.

At the top level, there is a model of economic quantities that are defined independently

of data.

This can be a structural model or a descriptive relationship between control and response

variables, say, quantity is of interest to the researcher.

For example, a price elasticity, a rate of return, a parameter of utility

function, a location or scale parameter. At the bottom of the empirical analysis stack,

there are data from unknown distribution on sample space that can be

described with a statistical model .

For example, a random sample from a parametric, nonparametric or semiparametric model.

At the interface between the application and the data layers, high-level object

is identified with a particular feature of the statistical model .

Thus, the middle layer between data and application is a specification

that assigns a statistical parameter to the economic

quantity under modeling assumptions of the researcher, say, index set

describes all specifications entertained by the researcher.

Three logically independent types of variation in empirical inference about can be

distinguished based on the application, specification and data layer anatomy.

Application model sensitivity analysis examines dependences within the mathematical

relationships of the application layer, [[, e.g.,]]sobol1993sensitivity, 1404.2405.

Specification sensitivity arises from variations at the interface layer in mapping .

For example, can be

identified with a coefficient in a linear regression model or an iv equation, both

ols and iv can be set up with different sets of covariates or instruments.

Omitted variable bias is the quintessential example of variation in specification.

Both the statistical model and the unknown distribution of sampled data remain fixed

across different specifications, only the choice of statistical functional that is used

for inference about changes.

Exploring specification variation for a fixed is analytically straightforward –

estimates of all interesting choices can be obtained, hopefully

uniform, inferences can be reported, a parametrization can be differentiated with techniques

from calculus to find local effects of changing specification.

This paper studies sensitivity of a fixed statistical functional defined on a statistical

model

to local variations of the data distribution within model . We work strictly at the

data layer, holding specification fixed, but suggest both data level and application level

interpretations. In mathematical terms, we consider differential calculus of functionals on the

model manifold under different Riemannian geometries.

Statistical model sensitivity is a directional derivative of the statistical functional.

Since a typical statistical model behind economic

applications is an infinite-dimensional space, it is helpful to identify a direction on the model

with a tractable statistical parameter, denoted .

Sensitivity with respect to parameter is the partial derivative along its

gradient vector , denoted by operator:

Practical utility of sensitivity analysis comes from the fact that it is closely related to

asymptotic approximations for a large class of estimators.

The main observation is that influence functions are gradients according to the information

geometry of the model. Gradients in any other geometry on the model are linear

transformations of influence functions. By varying geometric primitives in the definition

of sensitivity , researcher obtains different local counterfactual values of

, corresponding to different perturbations on that change in a

controlled way. One of such counterfactual is given by the asymptotic covariance of two

regular estimators.

For a pair of estimators on statistical model with standard asymptotic behavior

(1)

Definition 1.

the estimator sensitivity of to is

and estimator sufficiency of for is

The measures were introduced by Gentzkow and Shapiro (2015) [22]

for the purpose of comparing a nontransparent estimator to a tractable statistic

.

Andrews, Gentzkow and Shapiro (2017) [4] interpreted as a

measure of local specification sensitivity of gmm functionals implicitely parametrized by

the population value of moments .333From the fact that Jacobian

of moments does not depend on specification parameter , it follows that dependence of moments

on must be additive.

We define sensitivity directly on the model using techniques of differential geometry, rather than

in terms of the asymptotic distribution of estimators as in [22].

We then relate our sensitivity of functionals to asymptotic distributions of estimators using

results from semiparametric efficiency theory.

This relationship is similar to Newey (1994) [46],

but in our definition we allow for an explicit choice of geometric primitives.

We show that, in information geometry of :

Estimator sensitivity is (i) the directional derivative of

in the direction of .

Estimator sufficiency is (ii) the square of cosine of the angle made by linear

approximations to and at , (iii) the relative size of partial derivative of

along to total derivative of , (iv) the efficiency gain in estimating obtained

by fixing population value of . With other geometries on , measures (i-iii) are

available but not reflected in the asymptotic distribution of estimators.

Our investigation is inspired by [22] but we proceed in a different direction from

their line of inquiry.

The main objective of this paper is to provide interpretation of measures from

semiparametric efficiency perspective. This leads us to information geometry and motivates our

local counterfactual interpretation of sensitivity, which we generalize by allowing a policy

metric instead of the intrinsic information metric of the geometry behind statistical

efficiency.

Apart from generalizations, our inquiry fundamentally diverges from [22] in that

we make a clear distinction between varying specification , holding fixed, and

varying distribution , holding specification fixed, and consider only the

latter exercise. By contrast, [4, 22] are primarily concerned

with variation in the specification of moment conditions in gmm functionals,

which are not deviations on the statistical model.

This paper and [4, 22] obtain complementary interpretations

for quantities which should only increase their value in practice.

We suggest two types of applications of statistical model sensitivity. A data level

interpretation as a measure of local alignment of two functionals can be used to

compare competing specifications or target specifications to tractable statistics. An

application level interpretation as a derivative can be used for local

counterfactual analysis and policy evaluation.

Measures (ii-iv) above quantify the quality of local approximation of by in a

neighborhood of .

Linear approximation of determines first order asymptotic

behavior of estimates . Sensitivity thus provides an analytic tool for exploring

inferences based on the asymptotic distribution of estimates of . Reporting sensitivity to

tractable parameters helps explain how inferences about are obtained from

.

See [4, 22] and references therein for a discussion on

transparency and empirical examples.

In the case with multiple specifications for , the natural course is to report all

estimates . This provides a one-point comparison of different

specifications at the sampling distribution .

Reporting similar to , positive estimator sensitivity

and estimator sufficiency close to

one, can be offered as formal evidence that results are not sensitive to specification in a

neighborhood of . We call these applications estimator or information sensitivity.

444

Note that identification and consistency of estimates are global properties of the

functional and the model and thus are outside of the scope of local sensitivity analysis.

Directional derivatives (i) provide a simple description of the local behavior of functional at

distribution .

For streams of random samples generated by ,

where is the gradient of , the limits under of estimators and

are:

We see that sensitivity is the local effect

on the value of of a ceteris paribus change in the value of accomplished by

changing the underlying distribution from along .

This is the local version of the

counterfactual analysis that typically takes to be some location parameter of a

response variable and to be the marginal distribution of a policy variable

[[, e.g.]]stock1989nonparametric,heckman2007econometric,chernozhukov2013inference.

Finally, one can use the identification of statistical functionals with economic

quantities of the application layer and interpret the local relationship

as the partial derivative of with respect to .

We call these applications policy sensitivity and argue that it should be based on a geometry of

with a policy metric motivated by the application, rather then the information metric

dictated by technicalities of asymptotic approximations.

Policy metric is a local notion distance on the model . Asymptotic inference implicitly

relies on the information metric that measures “statistical” distances on the model. Metric

determines the direction on the model along which policy shifts in the value of are

achieved. Thus, the combination of control functional and policy metric determines the path

of counterfactual distributions along which sensitivity of target functional is

measured. We describe a simple procedure for specifying and interpreting policy metrics, and

illustrate the analysis with a Monte Carlo experiment.

Parametrizing directions on the model by a control functional and a policy metric is a tractable

and flexible way to reason about local counterfactuals.

The scope and contribution of this paper is to provide geometric foundation for

statistical model sensitivity analysis and to highlight the importance of the metric of the model.

We provide new geometrically motivated methodology for counterfactual analysis. This appears to be

a novel use of geometry in econometrics and statistics. More specifically,

we introduce the notion of a policy metric on a statistical manifold, including semiparametric and

nonparametric models. We then define sensitivity as a directional derivative with respect to

policy gradient of a control statistical parameter.

This geometric formulation enables us to interpret policy sensitivity, including the covariance of

asymptotic distribution, as a local counterfactual.

In order to compute and estimate policy sensitivities, we obtain a result that relates policy

gradients to influence functions. We provide high level conditions for consistency of estimated

sensitivity. Detailed econometric analysis of estimation and inference for real-valued and

distributional local counterfactuals is left to future work.

This paper draws on and contributes to several seemingly unrelated literatures.

Geometric foundations in statistical inference have been investigated by many authors:

Hotelling (1930) [28] considers the spaces of statistical parameters as curved

surfaces embedded in Euclidean space, one of which can be seen in Figure3.

Mahalanobis (1936) [40] defines general distances between statistical

populations and notes parallels with special relativity.

Rao (1949) [53] writes down the information metric of a population space

(parametric model) in local coordinates and describes geodesics between two distributions.

Amari (1985, 2000) [1, 2] provides geometric insight into asymptotic

efficiency in parametric models. To this literature we contribute by applying differential

geometry to infinite-dimensional models and by new methodology motivated by geometry.

Specification sensitivity analysis based on was introduced by Gentzkow and

Shapiro (2015) and Andrews, Gentzkow and Shapiro (2017) [22, 4].

Semiparametric efficiency theory shows that variance of asymptotic Gaussian distribution in large

statistical models is the information norm of the differential e.g.

Stein (1956) [56],

Koshevnik and Levit (1976) [35],

Pfanzagl (1982) [49],

van der Vaart (1991) [60],

Bickel et al. (1993) [10]

but does not make explicit use of modern geometry.

We contribute to the efficiency literature by modelling large models as manifolds.

We organize the paper as follows:

In Section2 we define sensitivity using econometrics language of

semiparametric efficiency and provide a Monte Carlo example to illustrate the methodology.

To make geometric ideas of this paper accessible without requiring familiarity with Riemannian

geometry and semiparametric efficiency, we consider in Section3 the special case of a

two-dimensional statistical model embedded in . This allows a graphical illustration of

methodology and explicit calculations.

In Section4 we review required foundations from differential geometry, state the general

definition of sensitivity measures, explain how they depends on geometric primitives of the model,

and discuss analytic interpretation of these measures.

In Section5 we apply results of semiparametric efficiency theory to obtain

information sensitivity from regular efficient estimators, relate policy gradients to influence

functions, and briefly consider consistency of estimated policy sensitivity.

We work out some simple examples in Section6 and give a self-contained summary of

efficiency theory results we cite in Section7.

2. Econometric Introduction to Sensitivity

This section provides an informal introduction to sensitivity, explains how it relates to

geometry of the statistical model and shows how to compute sensitivity for tractable policy

metrics.

We provide an axiomatic development and technical details in Sections4 and 5, and

focus on the main ideas below, all calculations are deferred to Section6.

Let be a statistical model.

We are interested in estimating

parameter or, possibly, a set of alternative specifications

defined on the same model.

Statistical functionals estimable at the parametric rate are smooth. Therefore we can

define sensitivity as a directional derivative of along a tangent vector to the model

at the sampling (true) distribution . Tangent vector is the score of a

one-dimensional parametric submodel defined in a neighborhood of :

For the purposes of interpreting sensitivity, score stands for any submodel that

satisfies above derivative condition in quadratic mean. All such submodels admit the same local

counterfactual interpretation of sensitivity. The collection of different scores , obtained

from all smooth submodels through , is called the tangent set, denoted . On a

fully nonparametric model, the tangent set is the space of square-integrable

functions with zero mean. Parametric and semiparametric models restrict the tangent set in

significant ways. Because we are not concerned with efficiency here, we can assume that the

tangent set is unrestricted.

Sensitivity of along the tangent vector is the local effect

of changing the distribution in the direction of score :

Here the perturbation is understood to be any one-dimensional submodel with

score . For example, or . To compute sensitivity

we can use the influence function of :

As defined above, sensitivity is not very useful. The problem is that tangent space

typically does not have an obvious parametrization that would enumerate

all scores and put different sensitivities into context of the application layer.

To make sensitivity analysis convenient for the practitioner, the direction should be

associated with a tractable parameter of interest to the researcher.

This can be a statistical functional motivated by the

application layer, e.g. a related economic quantity or an alternative specification of the same

quantity. Or this can be a data level parameter that provides a tractable summary of distribution

, e.g. a mean or a quantile. We call this parameter a control functional and denote it by

.

The natural direction to associate with is the gradient where functional increases most

rapidly. This is analogous to the way Cartesian coordinates work, if we think of

coordinates as functions of the point.

However, it is not enough to pick a control functional to specify the direction of sensitivity.

This should not be surprising, because is a large space, for which we have not

introduced any structure.

Gradients depend on the notion of distance on the model . A metric at is an

inner-product norm on tangent vectors . The distance between and

along submodel is the sum of lengths of tangent vectors along the curve:

Different metrics define different distances on and generate the different geometries.

Influence function is the gradient of according to the information geometry of

that has metric . Information

measures statistical discrepancy between and a perturbation in the direction of score

.

Influence function is the direction on the model along which change in the value of

the functional is greatest per statistical deviation away from . This direction is least

favorable on the model for estimating from random samples of .

Calculation of influence functions is a standard exercise in efficiency literature, we refer to

Ichimura and Newey (2015) [30] for a modern treatment and use their

formula as a convenient definition:

(2)

Let us fix a simple example. Let the target functional be a generic moment of data

, and let the control functional be a quantile of data

. The mean and the -quantile have influence functions

The information sensitivity of the mean to the quantile

is the asymptotic covariance of regular efficient estimators .

To interpret this, rescale and recall

the original definition of information (in infinite-dimensional models) form Koshevnik and Levit

(1976) [35]: is the effect on the mean of a perturbation to

along a one-dimensional submodel that satisfies two requirements:

(-i)

generate an increment in the value of quantile , so that

;

(-ii)

minimize the information distance between and .

Information sensitivity measures the effect of this perturbation on the counterfactual

value of the mean:

Sensitivity to perturbations along the least favorable submodel is interesting for comparing

statistical properties of estimators. For example, if are two alternative

specifications for the same economic quantity, then information sufficiency

is a natural

measure of local similarity of the two estimates.

But the choice of least favorable submodel as the counterfactual distribution when measuring

the response in to changes in has no structural or causal foundation. Our point

is to make this choice explicit.

A general sensitivity of parameter can thus be specified by a combination of:

(S-i)

control functional whose value is being manipulated;

(S-ii)

metric on the tangent space that determines the direction of the

one-dimensional submodel along which control functional changes most rapidly.

To contrast general sensitivity with information sensitivity, we will call the metric used to

determine gradients a policy metric, the direction along which the sensitivity is measured

a policy gradient, and the directional derivative itself a policy sensitivity.

Control functionals and a policy metric provide a partial parametrization of the tangent space

that enables local counterfactual analysis motivated by the application.

A tractable way to specify a policy metric is to postulate a policy distribution whose density

function reflects the cost of displacing a unit of mass at location in the sample

space. The choice should be motivated by the application.

The resulting policy metric is .

Policy sensitivity with this metric is

where the scaled gradient is the score

of a one-dimensional submodel that solves the following

program for a sufficiently small :

Under some regularity conditions, policy gradient of functional with respect to

policy metric is

The effect of changing the metric from information to policy is very intuitive: the influence

function is rescaled by the likelihood ratio of information to policy and recentered.

Policy sensitivity measures the effect on the counterfactual value of target functional

from the perturbation to the value of control functional along any submodel with policy

gradient :

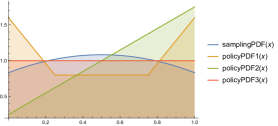

2.1 Monte Carlo example.

(a)Policy distributions

(b)Policy gradients of the median

Figure 1:

Let be continuously distributed according to joint distribution on the interval

, and suppose that is a measure of income, is a measure of education.

Application layer postulates that is a response variable, whereas is a control variable of

intereset.

Let the target and control functionals

be the mean of response variable and the median of control variable .

In our simulation, we take

the conditional mean of income given education is positively correlated with education. Marginal

distribution of is shown on fig.1, marked

samplingPDF(x).

We are interested in the predictive effect on income, via target functional , of a policy

that perturbs the marginal distribution of education. It is assumed that the perturbation does not

change the conditional distribution .

Policy is designed to increase the median level of education by some prescribed amount

( in the simulation). Three implementations of policy are proposed.

The perturbation along the least favorable submodel in the direction of the influence function of

the median has the effect on the mean . The influence

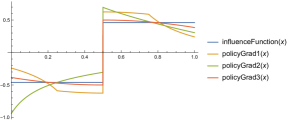

function is marked influenceFunction(x) in fig.1.

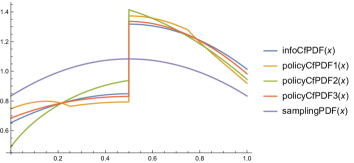

The density function of the counterfactual distribution

that produces is marked infoCfPDF(x) in

fig.2. The information counterfactual value of the mean is

.

The first policy proposal minimizes the taxpayers’ cost of policy.

It is argued that increasing the proportion of highly educated workers and reducing the

proportion of workers with most basic education is progressively more costly as one approaches the

extremes of the distribution. This may be due to higher investment requirements of

displacing workers at the extremes. This proposal is summarized with policy cost density function

, marked policyPDF1(x) in fig.1. Distribution

defines policy metric on deviations from sampling distribution of

education and produces a policy gradient function , marked

policyGrad1(x) in fig.1. The resulting counterfactual

distribution, marked policyCfPDF1(x) in

fig.2, is closer to the original sampling distribution below

the first and above the third quartiles, and further away at the interquartile range, compared to

the information counterfactual. The counterfactual value of the median is

, and the policy sensitivity is ,

so the counterfactual value of the mean is

.

The second policy proposal minimizes economic inequality by designing the perturbation to have the

strongest effect at the lowest levels of education and tapering off toward the highest levels of

education. This is achieved with policy distribution , marked

policyPDF2(x) in fig.1, and confirmed by the

counterfactual distribution marked policyCfPDF2(x) in

fig.2. The sensitivity fits in between

the information sensitivity and the policy sensitivity . This is

explained by noting that the mean of is positively related to the mean of , and that

deviations with more mass at the tails effect the mean stronger than deviations that displace more

mass around the median of the distribution.

The third policy proposal minimizes the macroeconomic shock by assigning equal cost to deviations

across all levels of education.

Perturbation profile, the gradient , under policy metric

is most similar to the influence function of the information metric

.

This is because both the sampling distribution and the policy measure are relatively flat.

The similarity is reflected in the counterfactual distributions and sensitivities as well.

Counterfactual value of in each case is approximately .

We compute the sensitivity of to changes in under each of the four counterfactual

distributions and report results in fig.2.

(a)Counterfactual distributions

Metric

Sensitivity

0.304102

0.251316

0.283477

0.289154

(b)Sensitivity of mean to median

Figure 2: Local counterfactuals

Remark 2.

The control functional determines the overall profile of the perturbation to .

The distribution in the policy metric determines the intensity with which the perturbation is

applied across the sample space with higher policy density attenuating the perturbation and lower

policy density intensifying the perturbation.

2.2 Sensitivity of GMM.

In this section we illustrate sensitivity analysis with gmm and descriptive statistics.

We consider gmm functionals on the nonparametric model that is constrained only by

regularity (smoothness, integrability) conditions. Application layer provides a parameter space

for the economic quantity of interest and a vector of moment

criterion functions

assumed to be sufficiently smooth in parameter and sufficiently integrable over the

sample space . Integrals with respect to distribution of data are written

as .

It is assumed that the economic quantity is “over-identified”, meaning that ,

and that and are full rank at

.

Researcher specifies that the value of is given by a function

of the statistical model. gmm estimation is set up from the

application layer assumptions that

()

These assumptions are typically optimality conditions of the interactions described by the

application layer model or postulated by the researcher orthogonality conditions.

Often these models are highly stylized and are not expected to

describe real-world data precisely.

Our view is that eq. assumptions should not be taken literally

to data, that the role of specification is nontrivial and deserves attention (but not our

focus here).

gmm functionals are defined by

In the over-identified case, weighting determines the functional and should be chosen based on

application layer considerations. We consider only deterministic positive definite weighting

matrices for now.

We compute a set of information sensitivities to compare a given gmm functional

to tractable summaries of the data and to alternative specifications obtained by using

a different weighting.

As directions we use descriptive statistics such as quantiles

and generic moments of the data. Here the moment function can be, for example, a

component of the data or a component of the moment criterion vector .

Information sensitivity is simple to compute and offers greater insight into inferences based

on asymptotic approximations. Consider the gmm functional. The economic model that leads

to formulation of functional may be complicated, but the asymptotic distribution

of estimates, and inferences derived from it, are completely determined by the local behavior of the

functional at . Information sensitivities and the complementary sufficiency measures provide tractable

one-dimensional summaries of this local variation:

Information sufficiency is an statistic that indicates how well the control functional

approximates local variation of the target functional . Specifically, is the

square of cosine of the angle made by tangent hyperplanes to and .

If is close

to one, then inferences based on asymptotic approximations around are obtained from

in the same way as inferences about . By making local comparisons of complicated

structural functionals to simple features of the data , the statistical

part of the empirical analysis can be made transparent [22, 4].

Another application is to compare two competing specifications and locally in

the neighborhood of . Reporting close to one can be offered as formal

evidence that the choice of weighting does not change results in a neighborhood of .

Conversely, observing close to zero warrants careful examination of

specification.

Asymptotic distribution of gmm estimators on misspecified models has been investigated by

Imbens (1997) [31], Hall and Inoue (2003) [25], we derive the

influence function and policy gradients of the functional in order to provide sensitivity

analysis.

The influence function of the gmm functional on a fully nonparametric model where moment

conditions () are possibly violated is

The sign of sensitivity shows if

the two specifications for move in the same direction at , and sufficiency

quantifies the alignment of two specifications locally at .

Furthermore, sufficiency measures the amount of local variation in the

estimate of contributed by the local variability of th moment function at .

Policy sensitivity

gives the local counterfactual value of the economic

quantity identified with to the perturbation of size in the value of

statistical parameter according to policy metric . Measure can be a policy

relevant reference distribution on the sample space. Taking the empirical measure as policy

measure is a convenient choice in terms of estimation.

3. Statistical surfaces

Let be a collection of probability measures on a sample space .

The starting point for our investigation is to realize a statistical model as an object with

intrinsic geometry – a space with notions of smoothness, length and angle.

In this section we consider a special case of a two-dimensional statistical model and

employ graphical aid to provide a nontechnical exposition.

The idea is to map a two-dimensional statistical model onto a surface in while preserving

the intrinsic metric properties of the model. We can then forget about the set of probability

measures and work with the surface in . For details on geometry of surfaces we refer to

[11].

The natural space to host statistical models is the set of square-integrable functions ,

with some dominating measure for elements of the model . In this ambient space,

probability distributions are identified with square-roots of their densities

, the model is a subset of the unit ball of

, and the tangent set is a subset of a hyperplane in . This simple

setup provides

a lot of structure to the model , in particular, the information distance between two

distributions and is the length of the shortest curve on the model joining them. The

length of a curve is obtained by adding magnitudes of velocity

vectors along the curve:

(3)

The curve in is . Its velocity at time is the tangent vector

, whose length, doubled for purely technical reasons,

is the information metric norm. Finally,

the sum of velocities along the trajectory of the curve

is, by definition, the length of the curve.

The problem of embedding into is to find a surface such that

length of the image of any curve on , computed according to the Euclidean geometry of

, coincides with the value in eq.3.

Isometric embedding is an active area of research. Conditions for preserving the metric are

formulated with a system of partial differential equations whose solvability requires enough

degrees of freedom provided by the dimensionality of ambient space. A general 2-manifold can be

embedded into by Nash’s theorem and its extensions [26].

The metric ultimately determines the shape of the surface required for the embedding.

Assumption 3.

Assume that is a smooth 2-manifold with metric given by eq.3 that

admits a smooth isometric embedding onto a regular surface at least locally at .

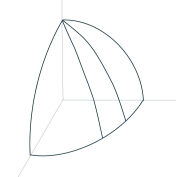

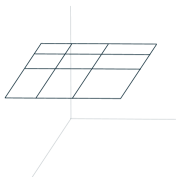

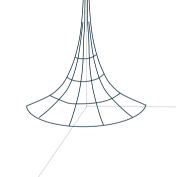

We consider three examples of statistical models with constant Gauss curvature:

(a)

(b)

(c)

Figure 3: 2-dimensional statistical models with constant curvature

Example 1.

Multinomial family

has Gauss curvature and isometric embedding

onto an orthant of a sphere in . See fig.3.

Example 2.

Bivariate normal model

with known variance

has zero Gauss curvature and can be isometrically embedded into globally as a plane or

locally onto a cylinder. See fig.3.

Example 3.

Univariate normal model

with location and scale parameters

has constant Gauss curvature .

By Hilbert’s theorem it has no global isometric imbedding into

but is locally isometric to the surface of a tractricoid (saddle shape).

See fig.3.

From a statistical model and its information metric we obtain a surface

and from a statistical functional

we obtain a function defined on the points of the surface. We use

the surface to show that local behavior

of at , summarized by its derivative, determines the asymptotic behavior of estimates of

. Calculations near point on are carried out by means of a parametrization by an

open subset . There are many choices of a parametrization

around a point , the only requirements are that be differentiable with derivative

that is full rank for all .

For example, can be parametrized by or or coordinates

of its points, or by latitude and longitude, or by points of the inscribed simplex.

Parametrization deforms a flat two-dimensional

neighborhood by stretching, shrinking and bending onto a neighborhood of the surface.

Because of the deformation, distances and angles in are different from those in .

Calculations in each parametrization appear to be different but the values on the surface are

invariant similarly to how mle is parametrization invariant.

Differential calculus works on tangent vectors that are the infinitesimals.

At every point there is a unique tangent plane to the surface.

The derivative of the parametrization maps vectors in anchored at into

tangent vectors in .

Tangent vectors and span

and are known as scores555I would appreciate a reference to the etymology of this terminology..

Due to deformation by , orthonormal vectors in have images

that are not orthogonal and not unit length in . This is because the

model is not flat at in its metric. Consequently sensitivity of parameters

on is not zero.

A function is differentiable if its expression in local coordinates

is differentiable. The derivative maps tangent vectors to

at into vectors in anchored at .

Recall that we took care to preserve distances and angles while mapping model into surface .

The inner product induced on vectors of the tangent plane

is in agreement with intrinsic metric structure of the statistical model .

This intrinsic statistical metric determines the sensitivity of statistical

functional to another parameter as follows.

By a basic fact of linear algebra, the linear map has a simple representation by

the gradient vector of function .

The gradient is the unique tangent vector that satisfies

{IEEEeqnarray*}c”t”c

⟨∇f_P,x_u⟩_P = df_P(x_u)

& and

⟨∇f_P,x_v⟩_P = df_P(x_v).

Gradient points in the direction on the surface along which values of

increase most rapidly and has magnitude equal to the rate of the

increase at on model . Since gradient determines the

linearization of functional at , it is natural

to take it to be the “-direction” of the model at . This is in perfect analogy with the

direction of -axis in where the coordinate is the linear function

on with gradient . This motivates our

measure of local statistical dependence:

Definition 4.

Sensitivity of functional to a statistical parameter on statistical

model is the directional derivative

{IEEEeqnarray*}c

∂_νψ(P) ≔dψ_P (∇ν_P) = ⟨∇ψ_P,∇ν_P⟩_P.

In the first equality we differentiate in the direction of given by the

gradient of . Second equality follows from definition of the gradient of .

Next we use parametrization to compute the derivative and establish

that parameter sensitivity of 4 and estimator sensitivity of

1 agree for many estimators, specifically that

. Let

, and

denote the expression of the inner-product on in local coordinates. And let

denote the Fisher information matrix for this parametrization. Information matrix appears in the

expression for sensitivity because it reconciles distorted distances in with statistical

distances on .

In local coordinates,

can be differentiated as usual to obtain partial derivatives ; these are

the directional derivatives of on along scores . From relationships

and

we solve for the expression of in basis:

{IEEEeqnarray}c

∇f = G fu- F fvEG-F2x_u + E fv- F fuEG-F2x_v.

Theorem 5.

Let be a two-dimensional statistical model with smooth isometric embedding into

. Let be a parametrization of the model with information matrix

. Let be differentiable functionals defined on .

The directional derivative of along is

(4)

Corollary 6.

In addition to conditions of 5 assume that for some function

and for every and in

and that mle estimators are consistent.

Then eq.1 holds for mle plug-in estimators ,

and parameter sensitivity is equal to the estimator sensitivity

:

{IEEEeqnarray}c

∂_νψ= σ_ψν.

Proof.

Formula of 5 follows directly from isometry assumption and definition of

gradient. Asymptotic normality eq.1 follows from [59, p65, theorem

5.39] by the delta method.

Using parametrization , we compute the

sensitivity of the functionals that make up the parametrization and

.

The scores of the parametrization are

and

.

From section3 we compute

{IEEEeqnarray*}c”c

∇ψ= u(1-u) x_u -uv x_v &

∇ν= -uvx_u + v(1-v)x_v.

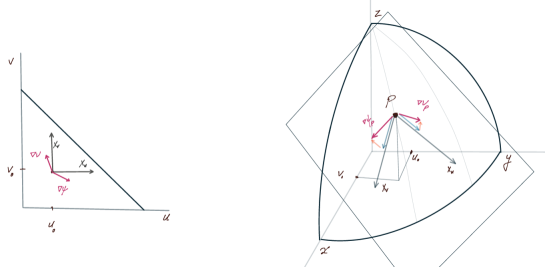

Refer to fig.4. The sensitivity of the probability of first outcome to

the probability of the second outcome is negative and decreases with each of the probabilities:

.

4. Geometry of statistical models

In this section we define general sensitivity measures of two statistical parameters.

Sensitivity is defined through differential calculus of a statistical functional.

Functionals are real-valued maps of a set of possible distributions of each observation.

Sensitivity quantifies the local relationship between a functional of interest and any set of

regular functionals. We can relate this to regression and designate the functional of interest as

response or target and the set of regular functionals as controls. We only consider sensitivity to

a single control, but the extension to a set of controls is straightforward and the partialling

out reasoning of regression applies. Sensitivity measures the deviation in the value of response

functional under the perturbation of the value of control functional.

Unlike regression coefficients, sensitivity is a bona fide directional derivative. The direction

depends on local properties of the control statistical functional and the notion of distance

between two distributions. Sensitivity can be used to make local counterfactual inferences about

economic quantities of interest in empirical work and to gain greater insight into asymptotic

distributions.

The set of possible sampling distributions is generally not linear, but can be modeled, in a

neighborhood of every point, as a smoothly transformed open subset of some linear space.

The idea takes some effort to develop methematically but the result provides great intuition.

We introduce necessary elements of Riemannian geometry for completeness, and refer to

do Carmo (1976, 1992) [11, 12] and Lang (1999)

[36] for more details.

Most elements of differential geometry that we need to define sensitivity are also employed in the

semiparametric efficiency literature.

However, efficiency theory makes use of the ambient Hilbert space of square roots of

measures [[, e.g.]p 739]Koshevnik76. From the model inherits the differential structure

(pathwise differentiability) and the information metric (Hellinger distance), similarly to our use

of in Section3.

By contrust, we define sensitivity based on a development of differential calculus on the model

without an ambient space and make dependence of sensitivity on the metric explicit.

Our development is similar to the setup in van der Vaart (1991) [60].

The point here is to allow local counterfactual “policy” analysis at the population level to be

independent of the asymptotic approximations and statistical efficiency analyses.

We allow a general Riemannian metric on the model manifold, which we call a policy metric, to be

used for sensitivity measures at the population level. We describe how these policy sensitivities

can be obtained from asymptotic distributions in Section5.

Let be a collection of distributions on sample space .

We introduce a differentiable structure on ; this enables us to consider smooth functions

which can be approximated on at a given point along directions

of the tangent space;

differential provides linear approximation of along any direction

; metric is an inner-product on tangent spaces that provides a Riesz representations

of the differentials of ; finally, the sensitivity is

the directional derivative of along the gradient direction of .

We consider only the simplest case of an open manifold. Extensions that allow for manifolds with

boundaries, corners, etc., common with statistical models, are possible but are not considered here.

Tangent sets for the purposes of this paper are always complete linear spaces. Our approach to

start with an arbitrary manifold structure and consider inclusion into the space of square roots

of measures can be used to restrict the tangent space in an explicit way and allows us to

consider any metric in definition of sensitivity.

4.1 Differential structure.

Statistical models can have many parametrizations. For example, the family usually

parametrized

by the vector of means , can alternatively be specified using spherical coordinates

; a (regression) function can be

parametrized by the coefficients of different Fourier bases. Parametrizations are necessary

for computation, but as long as we consider only compatible parametrizations, calculations we

do and quantities we define will be invariant of the chosen parametrization.

A differential structure is an equivalence class of compatible parametrizations. A manifold is a

set with a differentiable structure.

An atlas on is a collection of local parametrizations (charts)

satisfying the following conditions:

AT1

Each is a subset of and the union of covers .

AT2

Each is a one-to-one and onto correspondence of with an open

subset of a Banach space and for any

is open in .

AT3

The composition

is a diffeomorphism for each pair of charts.

Let be manifolds. A map is differentiable if, given , there are

charts at and a chart at such that and the

composition

is differentiable as a map between normed linear spaces. The composition is called expression of

in local coordinates. Similarly, we define directional and compact differentiation

[5, 6, 48] by applying

the definition to the expression of in local coordinates.

4.2 Tangent space.

Let be Banach spaces. A tangent vector in is a direction

with a position . Given a smooth curve

with position and direction at time , and a

differentiable map , we can associate the tangent vector with the directional

derivative operator

Let be a manifold modelled on a Banach space . A curve on is a differentiable map

. A tangent vector at , corresponding to the direction of , is

the directional derivative operator on differentiable maps

The set of all tangent vectors to at point , obtained from all curves passing

through , is called the tangent space.

A tangent vector corresponds to the direction of the

expression of the curve in local coordinates. Tangent space is in

bijective correspondence with and has the same structure of a topological vector space.

Definition 7.

Let be manifolds, let be a differentiable map. For and tangent

vector let be a curve with and . Then is a curve in .

The differential of at is the map

given by . It is a continuous linear map between tangent spaces.

4.3 Metric.

Geometric primitives discussed above are closely related to the ideas employed in semiparametric

efficiency. The next geometric primitive is implicit and fixed in the efficiency bounds theory but

has an active role in our local counterfactual analysis of functionals. The idea is to give the

statistical model a notion of distance by giving each tangent space an inner product. In

semiparametric efficiency theory this object is called information and it measures the

“statistical” (Hellinger) distances between distributions.

However, the empirical researcher identifies statistical functionals with

economic quantities and wants to understand the local relationship between

and at the data generating point on the model . There is no reason to

assume that “economic” distances on coincide with “statistical” distances.

Therefore we consider a completely general metric for policy analysis purposes.

A Riemannian metric on a statistical model is a correspondence that assigns to every point

a continuous bilinear symmetric positive-definite form

on the tangent space , and varies smoothly over .

For direction we can think of the norm as the

economic cost of a deviation from on at rate . We will call a policy metric

to contrast it with the statistical metric given by information .

4.4 Sensitivity.

The metric determines gradient directions of functions of as follows.

Definition 8.

Let be a differentiable functional. The differential

is a continuous linear map on the Hilbert space . The Reisz representation

vector of is the gradient of at .

It is the unique tangent vector that satisfies

From definition it is clear that gradient of depends on the metric .

The choice of metric determines the problem of approximating with a single tangent

vector.

By Cauchy-Schwarz,

According to the metric , gradient is the direction of most rapid increase

in the value of the function.

The norm is the slope of the tangent to the

restriction of along any curve through with unit speed and direction .

Definition 9((General sensitivity measures)).

Let be differentiable functionals on statistical model with policy

metric . Fix a point on the model. The partial derivative of with

respect to or

Clearly numbers and the linear map depend on the choice of metric through gradients of .

Directional derivatives and measure response in the value of

to a perturbation in the value of that is achieved by a deviation from on

in the direction of most rapid change in . This is analogous to partial derivatives in

linear spaces with respect to functionals of a coordinate system.

Projection vector gives the local approximation of by its partial derivative

along in all directions on ; this is the regression of

onto locally at . An interesting fact is that the coefficient of this local regression,

the sensitivity, is a genuine derivative in this case.

Sufficiency is the coefficient of

determination in this regression and measures the alignment of and in a

neighborhood of on M. Specifically, is the square of cosine of the angle between

and .

A value of close to reflects high degree of similarity in the local

behavior of at the data generating distribution; a value close to reflects that

move in orthogonal directions of the model . When is close to any

perturbation that moves will have a proportional effect on the value of , where as

with close to any perturbation that significantly moves will have

negligible effect on the value of .

Lemma 10(Local counterfactual interpretation of sensitivity measures).

Suppose statistical model is a manifold. Researcher measures distances on with policy

metric and is interested in parameters that are smooth functionals

on the model.

Let be any smooth curve on with tangent vector

at . Then

so that sensitivity is the local effect on of a change in the value of

along .

Furthermore, the projection is the partial derivative (partial gradient) of

along the gradient direction of parameter : for any tangent vector

so that sensitivity is the partial effect on from changing the value of

by any local perturbation at . The measures the relative size of the

partial derivative to total derivative .

Furthermore, the sufficiency , where the angle

measures the alignment between and locally at .

Extension to a set of control functionals is straightforward by analogy with regression.

Here sensitivities are coefficients of the projection of onto the linear span of

. The interpretation of sensitivity coefficient of is as

above but for the local variation in and that is orthogonal to the linear span of

[20, 39].

5. Sensitivity of regular estimators

Let be a semiparametric model described in Section4, let

be Hadamard differentiable functionals on . In this section we consider estimation based on

random samples from and relate the asymptotic distribution of estimators

to the sensitivity measures defined in

Section4.

Efficiency bounds on the asymptotic distribution of regular estimators

depend on local properties of functionals on the

image of the inclusion

of the model manifold into the Hilbert space of square roots of measures, see Koshevnik and Levit

(1976) [35] for the role of this embedding and Neveu (1965)

[45, p. 112] for the definition of the space .666[35]

cite [45] but the English translation of [35]

references pages in the Russian translation of [45].

We collect details of semiparametric efficiency theory in Section7.

Our setup with inclusion of into is similar to van der Vaart (1991)

[60], but we emphasise the intrinsic geometry of the model where as

[60] is concerned with pathwise differentiability.

The following is a standard

Assumption 11.

Inclusion map is differentiable with derivative that is a continuous

linear map

of tangent vectors to the model manifold into scores of parametric submodels that are

functions with mean zero .

Manifold determines the set of pathwise differentiable one-dimensional submodels and

the tangent space , which are important elements of the

efficiency theory.

Note that differential need not be isomorphic and need not be isometric.

If range of is not closed in , then is not bounded, and

bilinear functional is not continuous on the tangent space .

For example, , the Sobolev space of functions with derivatives.

We make the following stronger assumption that simplifies our functional analysis.

Roughly speaking, we consider models that behave either like finite dimensional smoothly

parametrized families or like fully nonparametric models.

Assumption 12((Regularity of policy geometry)).

Inclusion map is differentiable with derivative that is an isomorphism of

with , in particular, is closed and is

continuous.

It follows that metric is continuous on the embedded tangent space

, and the inner-product

is continuous on the manifold tangent spce , and that inclusion differential has an

adjoint such that

Since is the derivative of the inclusion map, we can treat it as the identity operator on

. Furthermore, from functional analysis identity and

continuity of , conclude that has a continuous inverse , and

(5)

Theorem 13(Relationship between sensitivity and efficiency).

Let be a statistical model with a policy metric as in Section4.

Let be Hadamard differentiable with gradients ;

suppose policy regularity 12 holds; then functionals

are differentiable with influence functions and

Proof.

Differentiability of follows from [60] or

directly from being a diffeomorphism by the inverse function theorem. From

eq.5 and 8 we have

(6)

Formulas for policy directional derivative and sensitivity follow from eq.5 by

substituting above expression for and the same expression for .

Definition 14.

We will call the gradient operator because of eq.6.

Corollary 15((Characterization of estimator sensitivity)).

Let be regular efficient estimators of on statistical

model .

Then estimator sensitivity is the sensitivity with

respect to the information metric on .

Estimator sufficiency is the information sufficiency of for

and, in addition to interpretations of Lemma10, is the efficiency gain in

estimation of , obtained by restricting the statistical model by setting the value of

to its population value .

Proof.

From the nonparametric version of Hájek’s convolution theorem (see 28),

the asymptotic distribution of a regular estimator

is , where

,

and

.

For any efficient estimator sequence, the noise term

is a point mass at zero so that asymptotic distribution is just . If

metric on is given by the information inner-product of at , then operator

is a unitary isometry, is the identity operator on . It follows that

influence functions are gradients and

sensitivity is the asymptotic covariance .

Characterization of estimator sufficiency follows from considering the restricted model

that is a local submanifold of determined by the closed subspace

of the tangent space (see [36, ch2 §2]).

Efficient influence function on is

therefore estimator sufficiency gives the reduction in the

asymptotic variance of a regular efficient estimator of on relative to the

bound for .

Estimator sufficiency is informative of the local statistical relationship between and

, and specifically, to what extent regular estimates of parameter determine

inferences based on the asymptotic distribution of regular estimators of in the sense of

efficiency gain.

5.1 Gradient operator of an absolutely continuous policy measure.

Here we consider a tractable example of policy and obtain explicit relationships between policy

gradients and influence functions.

Consider a nonparametric model , fix a distribution , and let the tangent space

be unrestricted. Suppose that policy metric on is given by

(7)

where policy distribution satisfies the following regularity condition

Assumption 16.

and the likelihood ratio satisfies .

Probability measure may be a social weighting on sample space that is relevant for

policy. Policy probability density is the cost of displacing a unit of mass in at

location of the sample space .

We want to find the policy relevant response of the

change to economic quantity associated with statistical functional that would result from a

perturbation to .

This can be computed from influence functions, obtained as part of the asymptotic distribution

derivation for estimators of or from an efficiency bound calculation. We assume that

policy regularity condition 12 and find the gradient operator , which we

can then verify to be isomorphic.

From definition 8 we have the following relationships

It follows that for every

so that

To solve for the centering constant , use the fact that

, to find that

. Conclude:

(8)

Thus, we have expressed the policy gradients in terms of the influence functions

and can compute the policy sensitivity as follows.

Theorem 17(Policy measure sensitivity).

Suppose that policy metric given by eq.7 satisfies 16.

Then 12 holds and policy sensitivity of statistical functionals

is

And the gradient operator is the multiplication operator:

(9)

Remark 18.

This is similar to propensity score reweighting. The likelihood ration

adjusts for the discrepancy between the policy distribution and sampling distribution.

Remark 19.

The condition is not necessary if is understood to be the density of

the absolutely continuous part of in the Lebesgue decomposition with respect to .

5.2 Estimating sensitivity.

Reporting sensitivity in empirical work requires

estimating it along with the asymptotic variance. We consider two distinct scenarios. If the

policy metric has a fixed relationship with the distribution of data, then estimating

sensitivity is straightforward

and consistency follows (roughly) from consistency of the asymptotic approximation. If the policy

metric depends on the distribution in a general way, then gradient operator needs

to be estimated and consistency requires additional justification.

We consider the typical situation where one estimates a vector of parameters and

obtains an estimate of the asymptotic variance by plugging in the estimate to obtain

influence functions . Here could be some functions of

.

We first assume that has a fixed relationship to so that the gradient operator is

known. We use notation for the empirical measure.

Theorem 20.

Let be a Glivenko-Cantelli class

of functions; let and in

. Then

is a consistent estimator of sensitivity .

Proof.

By triangle inequality

We use uniform law of large numbers over the class to control term

We use triangle inequality, Cauchy-Schwarz and convergence to control term

With the additional assumption that functions are

Glivenko-Cantelli, one can form a consistent estimator of sensitivity coefficient .

More primitive conditions can be based on e.g. bracketing entropy. If an estimate

of bracketing numbers is available for functions and preserves point-wise order

at each like the multiplication operator Section5.1, then one can estimate

bracketing numbers for .

Estimator of sensitivity derivative when gradient operator depends on can be based on

the plugin estimate with empirical distribution or mollified empirical distribution

(10)

E.g. the multiplication operator of Section5.1 is of this form because the likelihood ratio

of the data generating to policy cost distribution depends on unknown .

We leave consistency of the general form eq.10 to future work and consider

consistency of policy sensitivity of Section5.1 formulated with a policy cost distribution

.

Theorem 21(Consistency of plug-in estimator of policy measure sensitivity).

Suppose (i) functions

are Glivenko-Cantelli;

(ii)

and in ;

(iii)

estimator of likelihood ratio is consistent in the empirical MISE sense

in ;

(iv)

likelihood ratio satisfies 16.

Then plug-in estimator of policy sensitivity

(11)

is consistent.

Proof.

We formulated conditions for influence functions and likelihood ratio estimator independently.

Our strategy is to avoid interacting influence functions with likelihood ratio estimates in terms

that require uniform convergence. This is accomplished with Cauchy-Schwarz and triangle

inequalities. Let and . We need to control

convergence of the following two remainder terms:

To separate from in term we center at

and use triangle inequality to obtain terms and :

The first term on the right of is by the uniform and convergences, where as the

second term is by assumption (iii) on the estimator of likelihood ratio. Term

is by the assumed uniform convergence, uniform bound on likelihood ratio and

convergence of influence functions with plug-in.

We center term at and use triangle

inequality to obtain terms :

Term is controlled similarly to term and term similarly to term . Term

is bounded by a Cauchy-Schwarz estimate. Term is bounded by and law of large

numbers for .

Term converges to by the argument for term .

From (iii), Cauchy-Schwarz and law of large numbers have

. Conclude

that is by continuous mapping argument.

Possible variation on above strategy is to assume that likelihood estimates are bounded and apply

Hölder’s inequality instead of Cauchy-Schwarz.

An alternative strategy is to investigate uniform convergence of the product of influence

functions and likelihood ratio approximations.

6. Examples

Here we continue with our example setup of a nonparametric model with full tangent space

on sample space with Borel -algebra.

Ichimura and Newey (2015) [[, IN]]ichimura2015influence describe how

influence functions can be computed. Their idea is to use Lebesgue differentiation to recover the

influence function from its integral in 8.

It is enough to consider a sequence of curves

and compute

for

an approximation to identity . In models with tangent sets that are a proper

subspaces of , the efficient influence function is the projection onto the subspace.

6.1 Mean

functional has information gradient

.

6.2 Variance

functional has influence function

.

The policy sensitivity derivative of the mean with respect to the variance according to policy

metric as in Section5.1 is

6.3 p-quantile

of a continuous strictly increasing distribution is

. IN formula allows to use paths through distributions with

these properties. Influence function can be derived from the following algebraic identity

or

Differentiating both sides with respect to and evaluating at , obtain

Solving for the , simplifying and taking limit on , obtain

.

The policy derivative of the mean with respect to the -quantile according to metric of

Section5.1 is

6.4 GMM.

We study gmm functionals on the nonparametric model that is constrained only by

regularity (smoothness, integrability) conditions.

Application layer provides a parameter space

and a vector of moment criterion functions

Specification layer maps the economic quantity to a function

of the statistical model. gmm estimation is setup from the

application layer assumptions that

()

This assumption is usually an optimality condition of the interactions described by the

application layer model. Often these models are highly stylized and are not expected to

describe real-world data precisely.

Our view is that this assumption should not be taken literally to data, and

that the role of specification layer is important and deserves attention

(but is beyond the scope of this paper).

We derive the sensitivity measures to provide a local characterization of a given

gmm functional.

Specifically we describe the local identification of gmm functionals

on the nonparametric model by measuring the local dependence of the estimated

parameter on the values of individual moments

The direction and absolute magnitude of the dependence is measured by the derivative

.

The relative magnitude of dependence on to total local

variation in is measured by local sufficiency . The latter also

measures the extent to which (statistical) uncertainty about the value of in the model

determines inference about in the application layer.

Asymptotic distribution of misspecified gmm estimators was first considered tangentially

in [31] and derived explicitly in [25]. We derive the influence

function (information gradient) of the functional

and use it to compute sensitivities. Our derivation provides a characterization of the tangent set

to the classical gmm model that is restricted by assumptions

() in the over-identified case . As a bonus, this also shows

directly the semiparametric efficiency of ‘optimally weighted’ estimator

on and

of all gmm estimators of different functionals on the

nonparametric model .

Although the values of functionals coincide on their

sensitivities to directions ruled out by () are

different.

Chamberlain (1987) [14] first showed efficiency of over-identified

gmm estimators via discrete approximations.

We consider only deterministic weighting matrices . In the over-identified case weighting

determines the functional and should be chosen based on application layer considerations (we call

this specification). gmm functionals are defined by

or locally by the first order condition

(foc)

To establish differentiability (relative to embedding) of the functional and to find the

influence function we assume it along with necessary regularity conditions to proceed with

a formal calculation that yields a candidate for the information gradient.

Once the gradient is found,

Riesz representation implies differentiability777this method has the name a priori estimate

in PDEs.

Let be a smooth curve in with score vector at . The

functional satisfies the (foc) along the curve :

(12)

We use denominator layout for derivatives of vectors (so that is by ); our

reference for matrix calculus is [18]. Differentiating with

in (12) obtain

Derivative in terms has two components: perturbing distribution in the

direction changes the integrals and also the value of the functional which enters

the moment criterion functions.

Consider the first element of the vectorized term above

Define the matrix and a vector by stacking the underlined

terms in last screen

{IEEEeqnarray*}c”cH_1 ≔∂∂θ vec[( ∂∂θ g(θ) )^T ]

&

H_2 ≔vec[( ∂∂θ g(x,θ) )^T ]

then

Similarly

Above manipulation implicitly assumes that is differentiable relative to the

embedding of statistical model into . Recall that the differential has a Riesz

representation

The last equality is termed pathwise differentiability in bounds literature. The point of our work

in section4 was to argue that the notion of differentiability used in bounds literature is

precisely the same as the one used with linear spaces and that directional

derivatives can be naturally interpreted.

By differentiating with in (12) we obtained the following expression

that relates the pathwise (directional) derivative and an integral involving the

tangent vector :

{IEEEeqnarray*}c’c’l0

&=

{

M P[H_1]

+

P[∂_θg(θ)^T] W P[∂_θg(θ)]

} ⋅˙θ+

P{( M H_2 + P[∂_θg(θ)]^T W g(θ) ) ⋅ξ}

.

From above expression we can solve for the

(13)

Above derivation relies on smoothness and integrability conditions of moment functions and its

(parameter) derivatives. Since the tangent space is unrestricted, we conclude that

eq.13 is the information gradient of and that functional is smooth

under these conditions.

Note that at where moment assumptions () hold, we have

, which reduces the gradient to the familiar expression. Although at all the

functionals obtained from different choices of weighting coincide, their gradients

are different along the directions that point outside the model .

Assumptions () imply restrictions for tangent set . We

characterize these restrictions next.

Differentiating along a path similarly to above in (), obtain

This condition states that the change in the integral of criterion functions due to perturbing the

measure must be offset by the change in the value of the parameter. Since moments can move in

independent directions, where as parameter deviations can span only

of them, the condition is restrictive. Define continuous linear

operator

We will derive projections onto and

onto the orthocomplement .

First we reduce the problem to finite dimensional spaces by splitting

and noting that any vector that is orthogonal to does not change

the integral of the moment functions and therefore does not change the value of ,

as evident from eq.13. Hence, .

It is then enough to consider operator which is an isomorphism.

If then or , therefore

is the orthogonal decomposition of onto directions that are in and those

that point outside the classical gmm model. We have the refined decomposition of

nonparametric tangent space:

To compute the projection onto the range we fix the orthonormal

basis , where ,

then obtain the matrix of to be and apply

the regression formula for projection onto the range of

Finally the projection onto of tangent vector is

obtained by removing the component that can be computed by passing to

coordinates and applying above projection matrix

The classical gmm model restricts dimensions off of nonparametric tangent

space. Specifically, vectors of the form

(14)

are restricted, whose span is of dimension .

The efficient influence function for gmm on is obtained by

projecting any in eq.13 onto the (mildly) restricted

:

Consequently, the sensitivity of the “efficient”

gmm functional to any direction that points out of the model is

zero, where as sensitivities of are nonzero. Estimators suffer larger

asymptotic variance because they estimate the (local) values of the functional outside

of and have nonzero sensitivities to local deviations in those directions.

7. Appendix

In this section we collect results necessary to provide a self-contained proof of the convolution

theorem. My main two sources are [59, 10] but neither

provides an exposition that is both concise and self-contained. For completeness I provide all

the details with minor variations on the proofs.

7.1 Contiguity.

Characterization of asymptotic distribution of estimators is achieved by requiring that the

convergence be sufficiently uniform. The limit distribution then is invariant under a sufficiently

rich class of converging sequences of probability measures. These sequences provide complementary

pieces of information about the invariant limit distribution and allow for a sufficiently complete

characterization.

The property of sequences of probability measures that allows extracting information about the

limit distribution of a sufficiently robust estimator is an asymptotic counterpart of absolute

continuity. The idea is to be able to obtain limit distribution of estimator under sequence

of laws from the limit distribution under laws .

Let be a sequence of sample spaces, we consider laws and that are

dominated by sigma-finite measures . Sequence is contiguous to sequence

, denoted , if for every sequence of events with it

holds that . A good way to think about this definition is to interpret as critical

regions for testing against , then contiguity requires that there be no test

whose level gets close to zero and whose power stays bounded away from zero.

Let and be the Lebesgue

decomposition of with respect to . The following proposition provides a low-tech

characterization of contiguity as asymptotic uniform absolute continuity that is intuitive and

useful in proofs.

Proposition 22.

The following are equivalent:

(i)

;

(ii)

and are uniformly absolutely continuous with

respect to ;

(iii)

and Radon-Nikodym derivatives are

uniformly -integrable;

Proof.

From have that .

Uniform absolute continuity means that for any there is a such that for any

sequence of events it holds that implies . This

follows from by contradiction.

Under , from Markov’s inequality

(15)

obtain uniform control on probabilities of the tail event and infer uniform bound on

for a suitable . Uniform integrability in

follows immediately since

Fix events with . Then

can be made arbitrarily small by first choosing large enough to control the last term, and

then demanding to be large enough to control the first two terms.

Next we state a high-level characterization of contiguity that is useful in practice. Note that

the sequence of random variables is tight under from

eq.15.

Proposition 23((Le Cam, van der Vaart)).

The following statements are equivalent:

(i)

;

(ii)

If along a subsequence,

then

(iii)

If along a subsequence,

then ;

Proof.

Let be Skorohod representation of . By

proposition22 ; are uniformly integrable so

that .