Weighted batch means estimators in Markov chain Monte Carlo

Abstract

This paper proposes a family of weighted batch means variance estimators, which are computationally efficient and can be conveniently applied in practice. The focus is on Markov chain Monte Carlo simulations and estimation of the asymptotic covariance matrix in the Markov chain central limit theorem, where conditions ensuring strong consistency are provided. Finite sample performance is evaluated through auto-regressive, Bayesian spatial-temporal, and Bayesian logistic regression examples, where the new estimators show significant computational gains with a minor sacrifice in variance compared with existing methods.

1 Introduction

Markov chain Monte Carlo (MCMC) methods are widely used to approximate expectations with respect to a target distribution, see e.g. Liu, (2001) and Robert and Casella, (2004). In short, an MCMC simulation generates a dependent sample from the target distribution and then uses ergodic averages to estimate a vector of expectations. Variability of the ergodic averages is of interest because it reflects the quality of estimation and can be used to construct confidence intervals or confidence regions (see e.g. Flegal et al.,, 2008; Flegal and Jones,, 2011; Geyer,, 1992; Vats et al.,, 2015; Jones and Hobert,, 2001). Estimating variability is akin to estimation of the asymptotic covariance matrix in a multivariate Markov chain central limit theorem (CLT).

Let be a probability distribution with support and be a -integrable function. We are interested in estimating the -dimensional vector

Let be a Harris ergodic Markov chain with invariant distribution . Then if for , w.p. 1 as . The sampling distribution for is available via a Markov chain CLT if there exists a positive definite symmetric matrix such that

| (1) |

where

Provided an estimator of is available, say , one can access variability of the estimator by constructing a -dimensional ellipsoid. Further, Vats et al., (2015) propose terminating the simulation when the ellipsoid volume is sufficiently small, which is asymptotically equivalent to stopping when a multivariate effective sample size is large enough. One of their necessary conditions is that is a strongly consistent estimator of .

Outside of recent work of Chan and Yau, (2017), Dai and Jones, (2017), Vats et al., (2015), and Vats et al., (2018), estimating the covariance matrix is rarely done in MCMC. Instead most practitioners focus on univariate techniques to estimate only the diagonal components. An incomplete list of univariate estimators includes batch means (BM) and overlapping BM (Jones et al.,, 2006; Flegal and Jones,, 2010; Meketon and Schmeiser,, 1984), spectral variance (SV) methods including flat top estimators (Anderson,, 1994; Politis and Romano,, 1996, 1995), initial sequence estimators (Geyer,, 1992), recursive estimators of time-average variances (Wu et al.,, 2009; Yau and Chan,, 2016), and regenerative simulation (Mykland et al.,, 1995; Hobert et al.,, 2002; Seila,, 1982). Many of these univariate techniques can be extended to the multivariate setting, but practical challenges increase as the dimension increases.

Within the MCMC literature, the most common approach is univariate BM since it is fast and simple to calculate. Speedy calculations are especially helpful in conjunction with sequential stopping rules where multiple variances or a covariance matrix would be calculated each time a stopping criteria is checked (see e.g. Flegal et al.,, 2008; Gong and Flegal,, 2016). Unfortunately, Flegal and Jones, (2010) and Vats et al., (2015) illustrate BM methods tend to underestimate confidence region volumes unless the number of Markov chain iterations is extremely large. Practitioners familiar with the time-series literature may argue for more complex SV estimators using Tukey-Hanning or flat top lag windows. Flat top windows are especially appealing since they tend to reduce bias leading to more accurate confidence region volumes. Despite the popularity in fields where sample sizes are moderate, multivariate SV methods are challenging to use in MCMC since they require substantial computational effort for large sample sizes (see Section 3.3).

This paper introduces weighted BM variances estimators that are especially convenient in MCMC but are applicable in other fields such as time-series and nonparametric analysis. The proposed estimators incorporate the same flexible lag windows of SV estimators while reducing computation time. For example, we later show a weighted BM estimator is approximately 60 times faster for a covariance matrix with iterations. Moreover, the speed up increases as dimension or iteration increases.

The cost one pays for computational efficiency is an increase in relative efficiency. Specifically, we show the variance is 1.875 higher for a flat top lag window using weighted BM versus a traditional SV estimator. Our result is similar to Flegal and Jones, (2010) who show the variance of the BM estimator is 1.5 times higher than that of the overlapping BM estimator.

In addition to calculating relative efficiency, we prove strong consistency of weighted BM estimators. Strong consistency is important since it is required for asymptotic validity of sequential stopping rules, see e.g. Flegal and Gong, (2015), Glynn and Whitt, (1992), Jones et al., (2006), and Vats et al., (2015). In short, asymptotic validity implies the simulation terminates with probability one and ensures the final confidence regions have the right coverage probability.

The performance of weighted BM estimators is illustrated in univariate and multivariate auto-regressive models. These finite sample simulations show weighted BM estimators converge to the true known value and that flat top lag windows enjoy significant bias reduction. As dimension or chain length increases, calculation of weighted BM estimators save significant time compared with SV estimators. Our simulations also illustrate an increase in the variance relative to SV estimators, which depends lag window choice.

We also consider a Bayesian spatial-temporal model applied to temperature data collected from ten nearby weather station in the year 2010. In this example, we estimate the covariance matrix associated with a vector of 185 parameters and again illustrate the improved computational efficiency of weighted BM estimators. Our final example considers a Bayesian logistic regression model that illustrates weighted BM estimators with a flat top window provide more accurate coverage probabilities of multivariate confidence regions.

The rest of the paper is organized as follows. Section 2 summarizes current multivariate estimators of . Section 3 proposes weighted BM estimators, establishes conditions that ensure strong consistency, and calculates the variance when using a Bartlett flat top lag window. Section 3 also investigates how chain length and dimension impact computation times for weighted BM, SV, and recursive estimators. Section 4 demonstrates the finite sample properties of weighted BM estimators via four examples. We conclude with a discussion in Section 5. All proofs are relegated to the Appendix.

2 Covariance matrix estimation

Estimating is rarely done in MCMC output analysis. Instead, most researchers ignore the cross-correlation and only estimate the diagonal entries of . Computationally efficient BM methods are usually preferred, but such methods can lead to lower than expected coverage probabilities. In this section, we provide formal definitions for existing estimators of and provide some motivation for our proposed weighted BM estimators. When these estimators reduce to the usual univariate estimators.

First consider BM estimators where is the number of batches, is the batch size, and . (Note and can depend on , but we suppress this dependency to simplify notation.) For , denote the mean vector for batch as . Then the sample variance of batch means scaled up properly is used to estimate , i.e.

| (2) |

Alternatively, overlapping BM use overlapping batches of length denoted for . Then the overlapping BM estimator is given by

| (3) |

Computing overlapping BM is significantly slower than BM given the increased quantity of batches.

SV methods can also be used to estimate . First consider estimating the lag autocovariance denoted by with

Then the SV estimator of truncates and downweights the summed lag autocovariances. That is,

where is the truncation point and is the lag window.

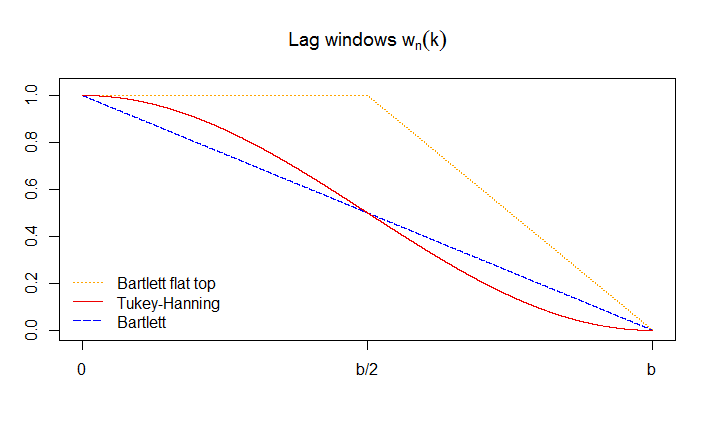

We assume the lag window is an even function defined on such that (i) for all and , (ii) for all , and (iii) for all . Most commonly used lag windows satisfy this assumption, which is necessary for our proof of strong consistency. Our discussion and simulations focus on the Bartlett, Tukey-Hanning, and Bartlett flat top lag windows defined as

| (4) | ||||

| (5) | ||||

| (6) |

respectively (see Figure 1). An interested reader is directed to Anderson, (1994) for more on lag windows.

It is well known the overlapping BM estimator at (3) is asymptotically equal to the SV estimator with a Bartlett lag window apart from some end effects (see e.g. Welch,, 1987; Meketon and Schmeiser,, 1984). Notice in Figure 1 that the Tukey-Hanning lag window slightly reduces downweighting of small lag terms compared to the Bartlett lag window in an effort to reduce bias. Politis and Romano, (1995, 1996) expanded on this idea when introducing flat top lag windows that modify existing windows by letting for near . Their work demonstrates SV estimators with flat top lag windows enjoy significant bias reduction while maintaining comparable variance. Politis and Romano, (1999) later illustrate the superiority of flat top lag windows in nonparametric estimation of multivariate density function.

We only consider the flat top window function constructed from the Bartlett window with for as at (6). For this setting, Politis and Romano, (1995, 1996) show the resulting SV estimator is equivalent to the difference of two Bartlett SV estimators. Specifically, if is the flat top window then

| (7) |

where and denote Bartlett SV estimators with bandwidths and , respectively.

In the next section, we construct weighted BM estimators that inherit desired properties from lag window functions but are computationally efficient due to a nonoverlapping structure.

3 Weighted BM estimators

Consider first an alternative representation of the SV estimator that is akin the overlapping BM estimator. Similar estimators have been previously studied by Damerdji, (1987, 1991) and Flegal and Jones, (2010). To this end, define and . Then recall for and consider the estimator

If -, Liu and Flegal, (2018) show that with probability 1 as , hence the estimators are asymptotically equivalent. Starting with , it is possible to reduce number of batches and computing time by only including non-overlapping batches. First define the more general batch mean vector as for and where . Then the weighted BM estimator is

| (8) |

The estimator is not necessarily computationally efficient. However, if the lag window is such that for certain values then the first summation can be simplified. For the Bartlett lag window at (4) for and . Hence, at (8) reduces to the BM estimator at (2).

We suggest using the Bartlett flat top lag window at (6) in an effort to reduce bias. In this case, it is easy to show , and for all other values. Hence, the first summation in (8) contains two terms which is extremely computationally friendly. For this lag window, Sections 3.3 and 4 illustrate computational and bias advantages, respectively. Since the expression of is similar to that of a second derivative of , other piecewise linear functions would also be computationally efficient.

3.1 Strong consistency

This section establishes necessary conditions for strong consistency of for estimating . Denote the Euclidean norm by and let be a -dimensional multivariate Brownian motion. Then the primary assumption is that of a strong invariance principle.

Assumption 1.

There exists a lower triangular matrix , a nonnegative increasing function on the positive integers, a finite random variable , and a sufficiently rich probability space such that for almost all and for all ,

| (9) |

Our results hold as long as Assumption 1 holds. This includes independent processes, Markov chains, Martingale sequences, renewal processes and strong mixing processes. An interested reader is directed to Vats et al., (2015) and the references therein.

For commonly used Markov chains in MCMC settings, Vats et al., (2018) show Assumption 1 holds using results from Kuelbs and Philipp, (1980). Specifically we require polynomial ergodicity, which is weaker than geometric or uniform ergodicity (see e.g. Meyn and Tweedie,, 2009).

Corollary 1.

Remark 1.

Remark 2.

Under stronger assumptions of geometric ergodicity, a one step minorization condition, and , Jones et al., (2006) and Bednorz and Latuszyński, (2007) provide an exact relationship between and the convergence rate of the chain (see Lemma 3 of Flegal and Jones,, 2010). Establishing a similar result for is a direction of ongoing research.

The weighted BM estimator can only be consistent if the batch size increases with leading to the following additional assumption.

Assumption 2.

The batch size is an integer sequence such that and as , where and are both monotonically nondecreasing.

Theorem 1.

Remark 3.

Simple Truncation: . Since , condition (12) is not satisfied.

Tukey-Hanning: . Appendix E provides a calculation to ensure (10) holds. Vats et al., (2018) show for the more general Blackman-Tukey window (11) and (12) hold if as using their Lemma 1.

Parzen: for . A method of differences calculation shows (10) holds. Vats et al., (2018) again show (11) and (12) hold if as . When this is the Bartlett window at (4) and equals defined at (2). Hence Theorem 1 provides an alternative proof of strong consistency under the same conditions as Vats et al., (2015).

Theorem 2.

Scale-parameter modified Bartlett: where is a positive constant not equal to 1. Vats et al., (2018) show does not converge to 0, hence (12) is not satisfied.

Bartlett flat top: . Condition (10) is satisfied since

However, (12) does not hold since and . We can still ensure strong consistency since the estimator can be expressed as the difference between two BM estimators similar to (7). Specifically,

| (13) |

where is defined at (2) (batch size ) and defines a BM estimator with batch size . With (13), strong consistency follows from Theorem 2.

Corollary 2.

3.2 Increase in variance

Since weighted BM variance estimators are based only on the nonoverlapping batches, a variance inflation is expected relative to SV estimators. Here we focus on estimating the diagonal entries of but the off-diagonal entries behave in a similar manner.

Suppose then denote estimators of the th diagonal element of based on BM and weighted BM with a Bartlett flat top lag window as and , respectively. Further, denote SV estimators with Bartlett and Bartlett flat top lag windows as and , respectively. Results in Flegal and Jones, (2010) imply as

since the overlapping BM estimator is asymptotically equivalent to . The variance of has also been studied by Lahiri, (1999) and Politis and White, (2004).

The following result establishes the variance ratio between weighted BM and SV estimators with a Bartlett flat top lag window at (6). The proof is given in Appendix D.

Theorem 3.

Remark 4.

For the Tukey-Hanning lag window, for all and there is no obvious simplification in the definition of at (8). Hence a variance ratio expression is challenging to obtain. (This difficulty persists for other lag windows where a simplification in the definition of is unavailable.) Alternatively, this ratio can be approximated via simulation as we illustrate in Section 4.

3.3 Computational time

This section investigates how chain length and dimension affect computation time for weighted BM, SV, and recursive estimators. Calculations were completed on a 2016 MacBook (1.2 GHz Intel Core m5) and coded exclusively in R to ensure fairness. Chan and Yau, (2017) provide the R-package rTACM (version 3.1), which we utilize to compute recursive estimators.

As an example, consider the -dimensional vector autoregressive process of order 1 (VAR(1))

for where , are i.i.d. and is a matrix. When the largest eigenvalue of in absolute value is less than 1 the Markov chain is geometrically ergodic (Tjøstheim,, 1990). Further, the invariant distribution is where and denotes the Kronecker product. Consider approximating by . In the CLT at (1), we have

A geometrically ergodic Markov chain is generated with chosen as follows. Consider a matrix with each entry generated from standard normal distribution, and which is a symmetric matrix with the largest eigenvalue . Then ensures geometrically ergodicity. The corresponding is estimated by weighted BM and SV estimators with window functions at (4), (5) and (6) using a truncation point of . Recursive estimators use default settings from the rTACM package while only storing the final variance estimate.

For each combination of and , Table 1 presents average computing time over 10 replications. There are significant computational gains for weighted BM with flat top and Bartlett lag windows. However, there is minimal computation gain for the Tukey-Hanning lag window since the double sum in (8) must be evaluated fully. Table 1 also shows recursive estimates are significantly slower. When and , recursive, flat top SV, and flat top weighted BM estimators take approximately 30 minutes, 60 seconds, and one second, respectively. Increasing to iterations, the same estimators require approximately one hour, three minutes, and two seconds, respectively. Computational gains continue to increase with further increases to or (see e.g. Section 4.3).

| Weighted BM | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Window | Flat top | BM | Tukey-Hanning | ||||||

| p=10 | .1 s | .1 s | .4 s | .1 s | .1 s | .2 s | 1.9 s | 4.8 s | 27 s |

| p=20 | .1 s | .2 s | .6 s | .1 s | .1 s | .4 s | 2.5 s | 6 s | 36 s |

| p=30 | .1 s | .2 s | .9 s | .1 s | .1 s | .6 s | 3 s | 6.8 s | 41 s |

| Spectral Variance | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Window | Flat top | Bartlett | Tukey-Hanning | ||||||

| p=10 | .8 s | 2 s | 13 s | .8 s | 2.1 s | 13 s | .8 s | 1.9 s | 12 s |

| p=20 | 1.9 s | 5.5 s | 32 s | 1.9 s | 4.9 s | 33 s | 1.8 s | 4.5 s | 31 s |

| p=30 | 3.4 s | 7.9 s | 59 s | 3.5 s | 8.1 s | 59 s | 3.3 s | 7.7 s | 57 s |

| Recursive | |||

|---|---|---|---|

| p=10 | 42 s | 1.6 min | 6.1 min |

| p=20 | 1.7 min | 3.5 min | 14.9 min |

| p=30 | 3.2 min | 6.3 min | 28.5 min |

4 Simulation studies

This section considers four examples to evaluate the finite sample properties of weighted BM estimators. Our first two examples consider geometrically ergodic Markov chains generated from univariate and multivariate vector auto-regressive models. The aim here is to compare weighted BM and SV estimators in terms of accuracy since the true value of is known. Our final two examples compare performances of the two estimators on real datasets where the true values are unknown.

4.1 AR(1) model

Consider the autoregressive process of order 1 (AR(1)) where

and are i.i.d. N(0,1). For the Markov chain is geometrically ergodic. Consider estimating by , then in the CLT at (1) we have

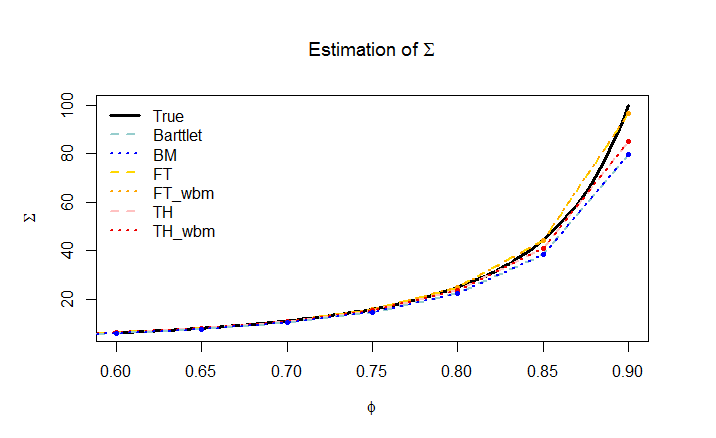

A range of from to are evaluated and the true value of is used to compare weighted BM and SV estimators.

For each , generate an AR(1) Markov chain of length 1e5 and compute weighted BM and SV estimators using the three lag window functions at (4), (5) and (6). Truncation point equals to for all six estimators. The procedure is repeated independently for 500 times and the average of 500 replications are shown in Figure 2. When the autocovariance is low, all the estimators perform well. As increases, the flat top lag window outperforms Bartlett and Tukey-Hanning windows for both SV and weighted BM estimators.

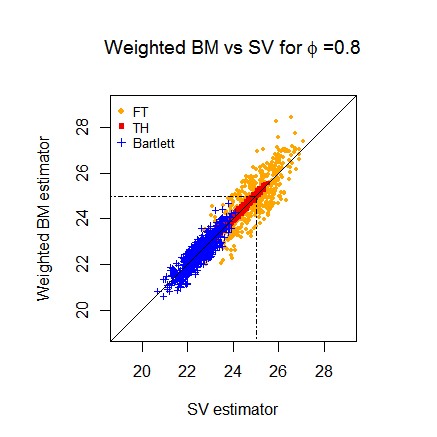

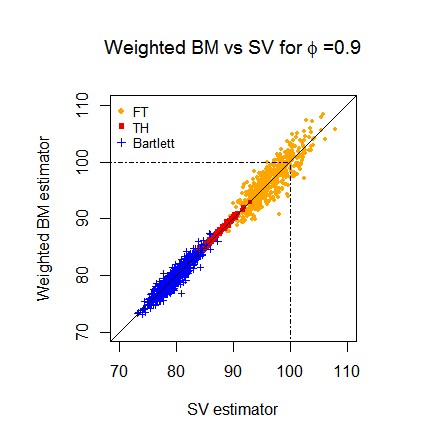

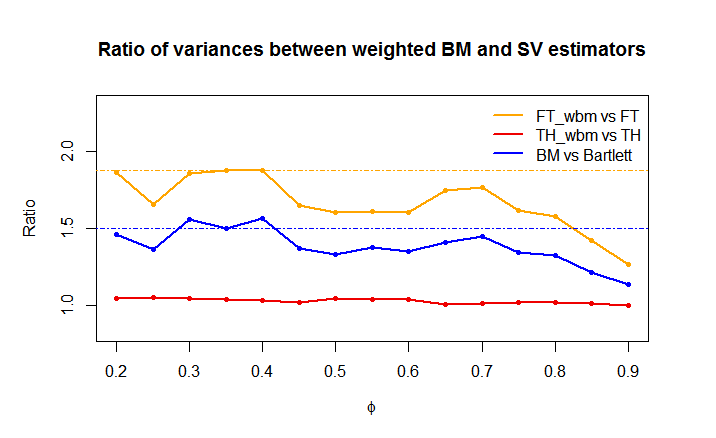

Weighted BM and SV estimates with the same lag window are very close as in Figure 2. To explore this relationship in more detail, Figure 3 plots SV against weighted BM estimates for the same Markov chain realizations when . Again we see the flat top lag window reduces bias but the variability increases slightly agreeing with our theoretical results. Another interesting observation is the Tukey-Hanning window estimates are closer to the identity line implying its variance ratio is closer to one. Figure 4 verifies this observation showing the Tukey-Hanning ratio is empirically very close to 1. Figure 4 also shows the Bartlett and flat top windows variance ratios are close to the theoretical values of and , respectively.

4.2 Vector auto-regressive model

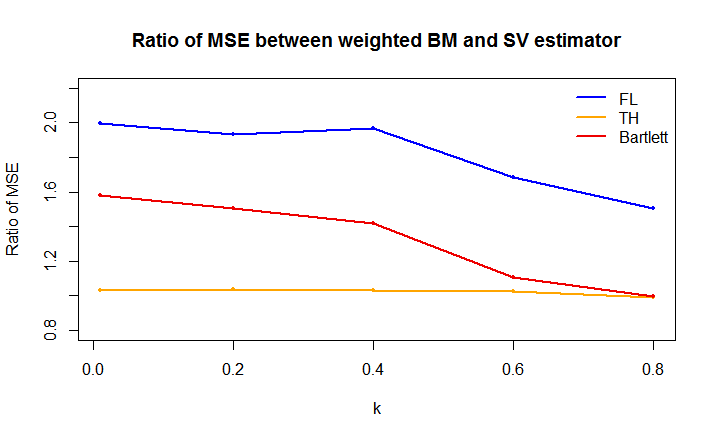

Consider again the -dimensional VAR(1) from Section 3.3 where we are now interested in the accuracy of weighted BM and SV estimators. We now obtain 50 independent replications for each combination of and for a given with and as in Section 3.3. Finally, let , where . It is easy to see larger implies stronger autocovariance and cross-correlation in the chain. These are used to generate geometrically ergodic Markov chains from which is estimated. For an estimator , define and consider mean squared error (MSE) over the entries of as a measurement of accuracy, i.e.

Figure 5 shows the averaged MSE ratio between weighted BM and SV estimators over 500 replications. Weighted BM estimators have inflated MSE but the ratios are below 2 across . Ratios for the Bartlett and Tukey-Hanning lag windows have a significant drop for resulting from large MSEs. Flat top window estimators show less of this trend since they are more accurate when . Combining computation and accuracy information, weighted BM estimators with flat top lag windows exhibit superior performance.

4.3 Bayesian dynamic space-time model

Consider monthly temperature data collected at 10 nearby station in northeastern United States in 2000, a subset of NETemp data described in R package spBayes (Finley et al.,, 2007). A Bayesian dynamic model proposed by (Gelfand et al.,, 2005) is fitted to the data and the model treats time as discrete and space as continuous variable.

Suppose denotes the temperature observed at location and time for and . Let be a vector of predictors and be a coefficient vector, which is a purely time component, and denotes a space-time component. The model is

where is a spatial Gaussian process where , is an exponential correlation function with controlling the correlation decay, and represents the spatial variance components. The Gaussian spatial process allows closer locations to have higher correlations. Time effects for both and are characterized by transition equations, delivering a reasonable dependence structure. Priors follow defaults in the spDynlM function of the spBayes package. We are interested in estimating posterior expectations for 185 parameters denoted .

| Weighted BM | ||||||||

|---|---|---|---|---|---|---|---|---|

| Flat top | BM | Tukey-Hanning | ||||||

| .5 s | .9 s | 1.9 s | .3 s | .6 s | 1.3 s | 11 s | 25 s | 56 s |

| Spectral Variance | ||||||||

| Flat top | Bartlett | Tukey-Hanning | ||||||

| 52 s | 2.2 min | 5.6 min | 52 s | 2.2 min | 5.6 min | 51 s | 2.2 min | 5.6 min |

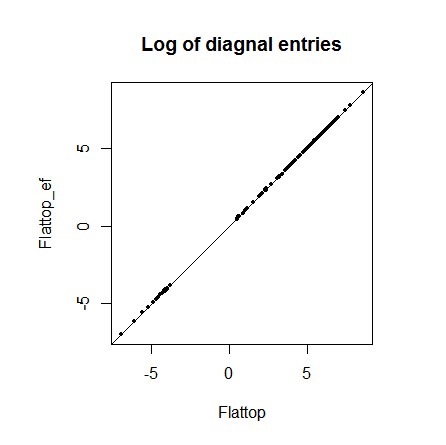

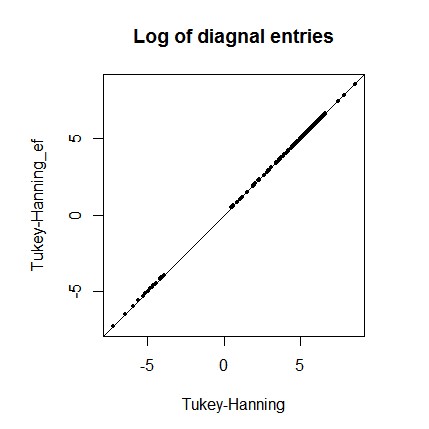

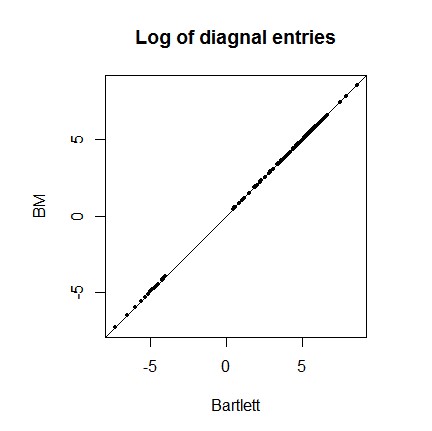

Again we consider Markov chains of length , and and compute computational time ratios in Table 2. For this high-dimensional Bayesian analysis, weighted BM estimators are much cheaper to compute for Bartlett and flat top lag windows. Figure 6 plots estimates of the diagonal elements of obtained with weighted BM and SV methods on the log scale. Since the points are close to the identity line it is clear both methods produce similar estimates.

4.4 Bayesian logistic regression model

Environmental data of 1000 site observations in New Zealand are considered to study the determinants of presence or absence of the short-finned eel (Anguilla australis) in R dismo package (see e.g. Elith et al.,, 2008; Hijmans et al.,, 2010). Five continuous variables, SegSumT, DSDist, USNative, DSMaxSlope, and DSSlope, along with a categorical variable Method with five levels (Electric, Spo, Trap, Net, Mixture) are chosen as in Leathwick et al., (2008) to predict Auguilla australis presence via a Bayesian logistic regression model.

For the th observation, suppose denotes presence and denotes absence of Anguilla australis. Let be a covariate vector and be the coefficient vector where . Consider the following Bayesian logistic regression model

Priors for are chosen to be as in Boone et al., (2014) and the MCMClogit function in the MCMCpack package is used to sample the Markov chain.

Using methods from Vats et al., (2015), we construct a confidence region of the 10 dimensional parameter based on the BM estimator, the SV estimator with a flat top lag window, and the weighted BM estimator with a flat top lag window. Coverage probabilities of these confidence regions from 1000 repeated simulations are used to evaluate the performance of each method. Since the true value of is unknown, the average of 500 chains each of length 1e6 is used as the “truth”. Table 3 shows the coverage probabilities for chains of length , , , and and two different batch sizes. When , both estimators based on a flat top window are far superior to the BM estimator. When , the improvement remains but is less substantial.

| Weighted BM | 0.342 | 0.657 | 0.741 | 0.853 | 0.714 | 0.825 | 0.849 | 0.868 |

|---|---|---|---|---|---|---|---|---|

| BM | 0.168 | 0.400 | 0.506 | 0.705 | 0.643 | 0.806 | 0.835 | 0.868 |

| SV | 0.368 | 0.655 | 0.739 | 0.858 | 0.764 | 0.844 | 0.866 | 0.879 |

5 Discussion

This paper considers a family of weighted BM estimators and obtains conditions for strong consistency. These estimators are fast to compute and comparable to existing SV estimators in terms of accuracy. Within this family, we advocate the flat top weighted BM estimator which is a computationally efficient robust estimator. Other estimators considered either require heavy computation or yield less desirable finite sample properties. By targeting both accuracy and computing effort, the advocated estimator is convenient to apply in modern high-dimensionally MCMC simulations. The proposed estimator can be further incorporated in a sequential stopping rule, where strong consistency and computational efficiency are necessary. Computational efficiency is also helpful when calculating valid asymptotic standard errors for the generalized importance sampling estimator (Roy et al.,, 2018; Roy and Evangelou,, 2018).

Computational complexity of the flat top weighted BM estimator is since it can be expressed as a difference between BM estimators (see e.g. Alexopoulos et al.,, 1997). Memory complexity will also be if is allowed to to increase by ones since the entire chain must be stored. Gong and Flegal, (2016) propose a low-cost alternative sampling plan that satisfies conditions necessary for strong consistency. Specifically, they set so that increases by doubling the batch size. It is then possible to store only the batch means and merge every two batches when the batch size increases twofold. Such a sampling plan reduces memory complexity to . Moreover, the estimator can be updated in computational steps using a recursive variance calculation.

The weighted BM estimator with a Tukey-Hanning window does not reduce computational time significantly. As mentioned earlier, the proposed estimators are more beneficial for lag window functions with for certain . Nevertheless, as dimension and chain length increases, weighted BM still save some computing time. More efficient coding or a linear approximation could provide additional efficiency if one prefers the Tukey-Hanning window.

All estimators in this article use the same truncation point for a fair comparison, which are not necessarily the best. In fact, finite sample coverage probabilities should improve by choosing better truncation points as suggested by Liu and Flegal, (2018). These optimal truncation points are those that minimize the asymptotic mean-squared error. If one wants to omit further exploration, we suggest using the same truncation point for weighted BM estimators as the corresponding SV estimators. Flegal and Jones, (2010) provide an illustrative example regarding optimal batch sizes for BM and overlapping BM. For flat top windows, Politis, (2003) suggests an empirical rule for the optimal truncation point selection. However, optimal batch size is a direction of future research for weighted BM estimators.

Acknowledgments

We are grateful to the anonymous referees, anonymous associate editor, Galin Jones, and Dootika Vats for their constructive comments and helpful discussions, which resulted in many improvements to this paper.

Appendix A Preliminaries for Theorem 1

We first introduce some notations and propositions. Recall is a -dimensional standard Brownian motion. Denote , and . The Brownian motion counterpart of is

where the individual entries are denoted as .

Recall is the lower triangular matrix satisfying and denote as the individual entries of . Finally define , as the th component of , , and .

Proposition 1.

Appendix B Proof of Theorem 1

Lemma 1.

Proof.

Proof.

We will show the result componentwise, i.e. that where denotes entry of the matrix . For ease of exposition, let and define and . Then

| (16) |

Define vectors

Then it is easy to show

| (17) |

Using the definition of at (8) with (16) and (17), we have

| (18) | ||||

Taking absolute value of (18)

| (19) | |||

We will show each of the seven terms in (19) goes to 0 as w.p.1. First we establish the following useful inequality. From (9) in Assumption 1, for any component and sufficiently large ,

| (20) |

- 1.

- 2.

- 3.

- 4.

- 5.

- 6.

- 7.

Since each of the seven terms in (19) goes to 0 as w.p.1, as w.p.1. ∎

Appendix C Preliminaries for Theorem 3

Consider the general family of Bartlett flat top SV estimators introduced by Politis and Romano, (1995, 1996) defined as

where . When , the resulting estimator is the SV estimator based on lag window at (6) denoted previously . Further define the Brownian motion expression of as

whose variance is given by Lemma 3. Denote by .

Lemma 3.

Under Assumption 2,

Proof.

Note and first consider

| (25) |

where

| (26) |

| (27) |

| (28) |

Denote

| (29) |

| (30) |

| (31) |

Then can be expressed as

| (32) |

To calculate at (29), consider . Let where and note are i.i.d. . Then for ,

Notice

since

and

Then

with

| (33) |

and

Therefore

| (34) |

By (29),

| (35) |

Define and for and Then (30) can be approached by

We will obtain through the joint distribution of . Since and are linear combinations of i.i.d. standard normal variables, denote , then where

The joint distribution of is

Recall if

and is non-singular, then the conditional distribution of is

In our case,

Using iterated expectations

Notice that

Plugging into (30) yields

| (36) |

Similarly as , we will calculate at (31) by first calculating where , for and . The joint distribution of and is

resulting in

Then

| (37) |

Plugging into (31), we have

| (38) |

Combine (35), (C) and (C), (C) can be calculated by

| (39) |

Similarly, we can obtain at (27) by

| (40) |

To calculate at (28), let for and satisfying and , denote

| (41) |

and

| (42) |

Then has the following expression:

| (43) |

First consider . Denote and for and satisfying and , then

resulting in

Then

| (44) |

thus

| (45) |

To calculate at (41), define , . For and

resulting in

Therefore

Notice

Then at (41) can be approached by

| (46) |

Next calculate at (42). First consider the joint distribution of and for and

resulting in

Then

| (47) |

Plug in (42),

| (48) |

Combine (C), (C) and (C), then at (C) can be calculated by

| (49) |

From , , at (39), (40), (C), at (C) becomes

| (50) |

We also need to calculate . By (33),

Therefore

and

Then

| (51) |

∎

Corollary 3.

Under Assumption 2,

Recall denotes the univariate weighted BM estimator with the Bartlett flat top lag window at (6). Suppose , then consider the corresponding Brownian motion expression

Lemma 4.

Under Assumption 2

Proof.

Since , first consider .

| (52) |

where

| (53) |

| (54) |

| (55) |

Denote

and

Then (53) can be expressed as

| (56) |

First consider . By (34),

hence

| (57) |

From (C),

and therefore

| (58) |

Plug , at (C) and (C) in (C), we have

| (59) |

Next consider at (54). Denote

and

then

| (60) |

By (34)

hence

| (61) |

To calculate , define and for and Consider the joint distribution of Denote , and are linear combinations of i.i.d. standard normal variables, then where

The joint distribution of is

. The conditional distribution of and the marginal distribution of are

Now we have the expectation

Then

| (62) |

| (63) |

To calculate at (55), consider . For and let in (C)

For and , let in (C).

Then at (55) equals to

| (64) |

Combine at (C),(C) and (C), we can approach at (C) by

Next consider

Therefore

∎

Lemma 5.

Proof.

Lemma B.4 of Jones et al., (2006) shows

| (67) |

under a slightly different condition from (65) and geometric ergodicity. Following the same argument, it can be shown that each component of goes to 0 under Assumption 1 and (65). Hence (67) also holds under conditions of Lemma 5. It then follows from Lemmas 12, 13 and 14 of Flegal and Jones, (2010) that

| (68) |

and

| (69) |

From (7), can be expressed by a linear combination of two Bartlett SV estimators which are asymptotically equivalent to , and can be expressed as a linear combination of two BM estimators, (68) and (69) result in Lemma 5. ∎

Appendix D Proof of Theorem 3

Appendix E Tukey-Hanning calculation

References

- Alexopoulos et al., (1997) Alexopoulos, C., Fishman, G. S., and Seila, A. F. (1997). Computational experience with the batch means method. In Proceedings of the 29th conference on Winter simulation, pages 194–201. IEEE Computer Society.

- Anderson, (1994) Anderson, T. W. (1994). The Statistical Analysis of Time Series. Wiley-Interscience.

- Bednorz and Latuszyński, (2007) Bednorz, W. and Latuszyński, K. (2007). A few remarks on ‘Fixed-width output analysis for Markov chain Monte Carlo’ by Jones et al. Journal of the American Statistical Association, 102:1485–1486.

- Boone et al., (2014) Boone, E. L., Merrick, J. R., and Krachey, M. J. (2014). A Hellinger distance approach to MCMC diagnostics. Journal of Statistical Computation and Simulation, 84(4):833–849.

- Chan and Yau, (2017) Chan, K. W. and Yau, C. Y. (2017). Automatic optimal batch size selection for recursive estimators of time-average covariance matrix. Journal of the American Statistical Association, 112(519):1076–1089.

- Dai and Jones, (2017) Dai, N. and Jones, G. (2017). Multivariate initial sequence estimators in Markov chain Monte Carlo. Journal of Multivariate Analysis, 159:184–199.

- Damerdji, (1987) Damerdji, H. (1987). On strong consistency of the variance estimator. In Proceedings of the 19th conference on Winter simulation, pages 305–308. ACM.

- Damerdji, (1991) Damerdji, H. (1991). Strong consistency and other properties of the spectral variance estimator. Management Science, 37:1424–1440.

- Damerdji, (1994) Damerdji, H. (1994). Strong consistency of the variance estimator in steady-state simulation output analysis. Mathematics of Operations Research, 19:494–512.

- Elith et al., (2008) Elith, J., Leathwick, J., and Hastie, T. (2008). A working guide to boosted regression trees. Journal of Animal Ecology, 77(4):802–813.

- Finley et al., (2007) Finley, A. O., Banerjee, S., and Carlin, B. P. (2007). spBayes: an R package for univariate and multivariate hierarchical point-referenced spatial models. Journal of Statistical Software, 19.

- Flegal and Gong, (2015) Flegal, J. M. and Gong, L. (2015). Relative fixed-width stopping rules for Markov chain Monte Carlo simulations. Statistica Sinica, 25:655–676.

- Flegal et al., (2008) Flegal, J. M., Haran, M., and Jones, G. L. (2008). Markov chain Monte Carlo: Can we trust the third significant figure? Statistical Science, 23:250–260.

- Flegal and Jones, (2010) Flegal, J. M. and Jones, G. L. (2010). Batch means and spectral variance estimators in Markov chain Monte Carlo. The Annals of Statistics, 38:1034–1070.

- Flegal and Jones, (2011) Flegal, J. M. and Jones, G. L. (2011). Implementing Markov chain Monte Carlo: Estimating with confidence. In Brooks, S., Gelman, A., Jones, G., and Meng, X., editors, Handbook of Markov Chain Monte Carlo, pages 175–197. Chapman & Hall/CRC Press.

- Gelfand et al., (2005) Gelfand, A. E., Banerjee, S., and Gamerman, D. (2005). Spatial process modelling for univariate and multivariate dynamic spatial data. Environmetrics, 16(5):465–479.

- Geyer, (1992) Geyer, C. J. (1992). Practical Markov chain Monte Carlo. Statistical science, pages 473–483.

- Glynn and Whitt, (1992) Glynn, P. W. and Whitt, W. (1992). The asymptotic validity of sequential stopping rules for stochastic simulations. The Annals of Applied Probability, 2:180–198.

- Gong and Flegal, (2016) Gong, L. and Flegal, J. M. (2016). A practical sequential stopping rule for high-dimensional Markov chain Monte Carlo. Journal of Computational and Graphical Statistics, 25:684–700.

- Hijmans et al., (2010) Hijmans, R., Phillips, S., Leathwick, J., and Elith, J. (2010). dismo: species distribution modeling. r package version 0.5-4.

- Hobert et al., (2002) Hobert, J. P., Jones, G. L., Presnell, B., and Rosenthal, J. S. (2002). On the applicability of regenerative simulation in Markov chain Monte Carlo. Biometrika, 89:731–743.

- Jones et al., (2006) Jones, G. L., Haran, M., Caffo, B. S., and Neath, R. (2006). Fixed-width output analysis for Markov chain Monte Carlo. Journal of the American Statistical Association, 101:1537–1547.

- Jones and Hobert, (2001) Jones, G. L. and Hobert, J. P. (2001). Honest exploration of intractable probability distributions via Markov chain Monte Carlo. Statistical Science, 16:312–334.

- Kuelbs and Philipp, (1980) Kuelbs, J. and Philipp, W. (1980). Almost sure invariance principles for partial sums of mixing B-valued random variables. The Annals of Probability, 8:1003–1036.

- Lahiri, (1999) Lahiri, S. N. (1999). Theoretical comparisons of block bootstrap methods. The Annals of Statistics, 27(1):386–404.

- Leathwick et al., (2008) Leathwick, J., Elith, J., Chadderton, W., Rowe, D., and Hastie, T. (2008). Dispersal, disturbance and the contrasting biogeographies of New Zealand’s diadromous and non-diadromous fish species. Journal of Biogeography, 35(8):1481–1497.

- Liu, (2001) Liu, J. S. (2001). Monte Carlo Strategies in Scientific Computing. Springer, New York.

- Liu and Flegal, (2018) Liu, Y. and Flegal, J. M. (2018). Optimal mean squared error bandwidth for spectral variance estimators in MCMC simulations. ArXiv e-prints.

- Meketon and Schmeiser, (1984) Meketon, M. S. and Schmeiser, B. (1984). Overlapping batch means: Something for nothing? In WSC ’84: Proceedings of the 16th conference on Winter simulation, pages 226–230, Piscataway, NJ, USA. IEEE Press.

- Meyn and Tweedie, (2009) Meyn, S. and Tweedie, R. (2009). Markov Chains and Stochastic Stability, volume 2. Cambridge University Press Cambridge.

- Mykland et al., (1995) Mykland, P., Tierney, L., and Yu, B. (1995). Regeneration in Markov chain samplers. Journal of the American Statistical Association, 90:233–241.

- Politis, (2003) Politis, D. N. (2003). The impact of bootstrap methods on time series analysis. Statistical Science, 18:219–230.

- Politis and Romano, (1995) Politis, D. N. and Romano, J. P. (1995). Bias-corrected nonparametric spectral estimation. Journal of Time Series Analysis, 16(1):67–103.

- Politis and Romano, (1996) Politis, D. N. and Romano, J. P. (1996). On flat-top kernel spectral density estimators for homogeneous random fields. Journal of Statistical Planning and Inference, 51(1):41–53.

- Politis and Romano, (1999) Politis, D. N. and Romano, J. P. (1999). Multivariate density estimation with general flat-top kernels of infinite order. Journal of Multivariate Analysis, 68(1):1–25.

- Politis and White, (2004) Politis, D. N. and White, H. (2004). Automatic block-length selection for the dependent bootstrap. Econometric Reviews, 23(1):53–70.

- Robert and Casella, (2004) Robert, C. P. and Casella, G. (2004). Monte Carlo Statistical Methods. Springer, New York, second edition.

- Roy and Evangelou, (2018) Roy, V. and Evangelou, E. (2018). Selection of proposal distributions for generalized importance sampling estimators. arXiv preprint arXiv:1805.00829.

- Roy et al., (2018) Roy, V., Tan, A., and Flegal, J. M. (2018). Estimating standard errors for importance sampling estimators with multiple Markov chains. Statistica Sinica, 28:1079–1101.

- Seila, (1982) Seila, A. F. (1982). Multivariate estimation in regenerative simulation. Operations Research Letters, 1:153–156.

- Tjøstheim, (1990) Tjøstheim, D. (1990). Non-linear time series and Markov chains. Advances in Applied Probability, pages 587–611.

- Vats et al., (2015) Vats, D., Flegal, J. M., and Jones, G. L. (2015). Multivariate Output Analysis for Markov chain Monte Carlo. ArXiv e-prints.

- Vats et al., (2018) Vats, D., Flegal, J. M., and Jones, G. L. (2018). Strong Consistency of Multivariate Spectral Variance Estimators in Markov Chain Monte Carlo. Bernoulli, 24:1860–1909.

- Welch, (1987) Welch, P. D. (1987). On the relationship between batch means, overlapping means and spectral estimation. In WSC ’87: Proceedings of the 19th conference on Winter simulation, pages 320–323, New York, NY, USA. ACM.

- Wu et al., (2009) Wu, W. B. et al. (2009). Recursive estimation of time-average variance constants. The Annals of Applied Probability, 19(4):1529–1552.

- Yau and Chan, (2016) Yau, C. Y. and Chan, K. W. (2016). New recursive estimators of the time-average variance constant. Statistics and Computing, 26(3):609–627.