Conditional Moments of Noncausal Alpha-Stable Processes

and the Prediction of Bubble Crash Odds

Sébastien Fries††Address for correspondence: Sébastien Fries, 1105 De Boelelaan, 1081HV, Amsterdam, the Netherlands.

s.f.fries@vu.nl

Vrije Universiteit Amsterdam

Abstract

Noncausal, or anticipative, heavy-tailed processes generate trajectories featuring locally explosive episodes akin to speculative bubbles in financial time series data. For a two-sided infinite -stable moving average (MA), conditional moments up to integer order four are shown to exist provided is anticipative enough, despite the process featuring infinite marginal variance. Formulae of these moments at any forecast horizon under any admissible parameterisation are provided. Under the assumption of errors with regularly varying tails, closed-form formulae of the predictive distribution during explosive bubble episodes are obtained and expressions of the ex ante crash odds at any horizon are available. It is found that the noncausal autoregression of order 1 (AR(1)) with AR coefficient and tail exponent generates bubbles whose survival distributions are geometric with parameter . This property extends to bubbles with arbitrarily-shaped collapse after the peak, provided the inflation phase is noncausal AR(1)-like. It appears that mixed causal-noncausal processes generate explosive episodes with dynamics à la Blanchard and Watson (1982) which could reconcile rational bubbles with tail exponents greater than 1. Applications of the conditional moments to bubble modelling by noncausal processes are discussed and the use of the closed-form crash odds is illustrated on the Nasdaq and S&P500 series.

Keywords: Noncausal process, Conditional moments, Speculative bubble, Crashes, Prediction, Rational expectation

1 Introduction

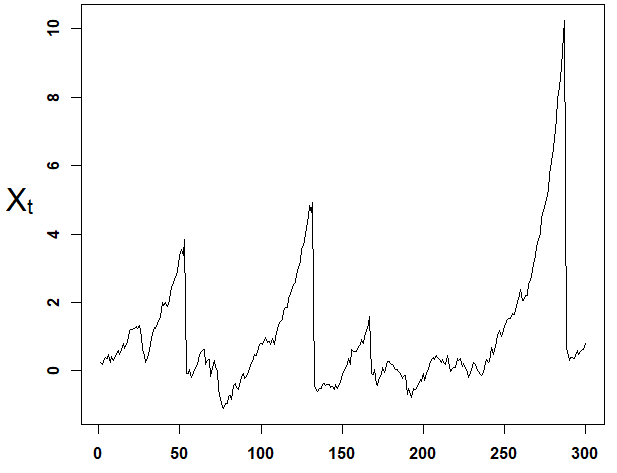

Dynamic models often admit solution processes for which the current value of the variable is a function of future values of an independent error process. Such solutions, called anticipative or noncausal, have attracted increasing attention in the financial and econometric literatures. In particular, noncausal processes have been found convenient for modelling locally explosive phenomena in financial time series such as speculative bubbles, while featuring heavy-tailed marginals and conditional heteroscedastic effects [[Bec et al. (2020), Cavaliere et al. (2020), Fries and Zakoian (2019), Gouriéroux and Jasiak (2018), Gouriéroux and Zakoian (2017), Hecq and Sun (2019)], Hecq et al. (2016, 2017a,b), [Hencic and Gouriéroux (2015)]] (see also [Chen et al. (2017), Lanne et al. (2012b)], Lanne and Saikkonen (2011, 2013)). Figure 1 depicts a typical simulated path of an elementary noncausal process, the -stable noncausal AR(1), featuring multiple bubbles.

Noncausal processes, shown to be suitable candidates for bubble components in rational expectation price models [[Gouriéroux et al. (2020)]], may offer a possibility to forecast the future trajectories of bubbles and to infer the odds of crashes.

This would enable for instance risk managers to assess large downside risks during prolonged bull markets and the regulator to adjust requirements and restrictions to ensure resilience of the financial system.

However, the limited knowledge about the predictive distribution of noncausal processes, especially during explosive bubble events, is impeding the ability to forecast them, thus limiting their use in practical applications.

Taking notice of the absence of closed-form formulae for conditional moments and the predictive density except in special cases, two simulation- and sample-based methods have been proposed in the noncausal literature to approximate the conditional distribution of noncausal processes [[Lanne et al. (2012a), Gouriéroux and Jasiak (2016)]].

While offering flexible alternatives for forecasting noncausal processes beyond the special cases, [Hecq and Voisin (2020)] find that these methods can become computationally intense for larger prediction horizons and that accurately capturing the dynamics during explosive episodes may prove challenging

[see also [Gouriéroux et al. (2019)]].

Partial results have been obtained by [Gouriéroux and Zakoian (2017)] on the conditional moments of noncausal AR(1) processes driven by independent and identically distributed (i.i.d.) -stable errors, which have been extended to mixed causal-noncausal AR processes with single ill-located root by [Fries and Zakoian (2019)]. Despite stable noncausal processes featuring infinite marginal variance, their conditional moments may exist up to integer order four.

In special cases, expressions of the conditional expectation and variance have been obtained, and revealed that noncausal processes can feature GARCH type effects in calendar time despite such effects not being explicitly included in the modelling. Provided the expressions of the conditional moments are derived, this suggests that point forecasts of noncausal processes based on their conditional expectation, variance, skewness and kurtosis could be formulated -as opposed to other predictors specifically introduced to circumvent the infinite variance of -stable processes, such as minimum -dispersion or maximum covariation (see [Karcher et al. (2013)] and the references therein).

The aim of this paper is to provide practical analytical results to compute the conditional moments of -stable noncausal processes and to compute the crash odds of bubbles that such processes generate.

First, the paper extends the literature on the conditional moments of arbitrary bivariate -stable random vectors [Cioczek-Georges and Taqqu (1995a,b, 1998), [Hardin et al. (1991)], Samorodnitsky and Taqqu (1994) ([ST94] hereafter)] by providing formulae for the orders .

We then apply these results to derive a complete characterisation of the conditional moments , , , for an infinite two-sided moving average process driven by i.i.d. -stable errors

| (1.1) |

where is a non-random coefficients sequence satisfying mild conditions for to be well defined and strictly stationary.

Second, the conditional distribution of noncausal processes during explosive bubble episodes is analysed.

Provided the errors have probability tails similar to that of -stable distributions, in the sense that they also feature power-law tails, we obtain closed-form formulae valid during explosive episodes.

These expressions provide illuminating interpretations on the dynamics of the bubbles that such models generate and a practical way to quantify the crash odds.

Implications and parallels with the literature on rational expectation bubble models in the line of [Blanchard and Watson (1982)] are discussed.

The rest of the paper is organised as follows. Section 2 recalls properties of bivariate stable distributions and provides our results on the conditional moments up to order four of arbitrary bivariate -stable vectors.

Applying these results to models of the form (1.1), Section 3 proposes a sufficient condition on the coefficients for the existence of conditional moments, characterises their expressions when they exist, and discusses several examples and methodological aspects.

Section 4 derives closed-form formulae for the predictive distribution of noncausal processes during explosive bubble episodes.

Section 5

proposes an application of the crash odds formulae on the Nasdaq and S&P500 series. Proofs and complementary results are collected in a Supplementary File.

2 Conditional moments of bivariate -stable vectors

We begin by recalling some properties of bivariate stable vectors and then propose new expressions for their higher-order conditional power moments . These expressions will apply to when considering -stable noncausal processes in the next section. Letting , a random vector is said to be an -stable random vector in (see Theorem 2.3.1 in [ST94]) if there exists a unique pair , where is a finite measure on the Euclidean unit sphere and a vector in , such that, for any , the characteristic function of writes

| (2.1) |

where is the canonical inner product, , if , and otherwise, for . The measure and the vector are respectively called the spectral measure and the shift vector of . The pair is said to be the spectral representation of . The spectral measure of a stable vector in particular completely characterises the tail dependence between its components: it holds that as , for any continuity set (Theorem 4.4.8 in [ST94]), where denotes the Euclidean norm. Intuitively, the more mass attributes to some points of the unit sphere , the more likely is to be colinear to these points when it is large in norm. The counterpart of (2.1) for a univariate -stable variable reads , for some asymmetry , scale and location .

Stable distributions are known to have very few moments. However, the distribution of one component conditionally on the other can have more moments according to the degree of dependence between them. If the spectral measure of an -stable random vector satisfies

| (2.2) |

then, for almost every if (see Theorem 5.1.3 in [ST94] for details), entailing that conditional moments up to integer order four may exist although .

The conditional expectation of arbitrary -stable bivariate vectors has been studied in details and its expression is recalled

in Theorem 2.1

below, while the conditional variance received attention most exclusively in the symmetric -Stable case.

We provide and prove new formulae for the conditional power moments of order 2, 3, and 4 of arbitrary (not necessarily symmetric) -stable bivariate vectors . The second order moment in the case , which requires special treatment when not restricting to symmetric stable distributions, is also considered.

In the rest of this section, we assume without loss of generality that the shift vector is zero. This can be done without loss of generality because, assuming the conditional moment of order exists,

where , and has the same spectral measure as and zero shift parameter. We first consider the case and introduce useful constants and functions which generalise existing quantities in the literature. For , when they exist, define

| (2.3) |

where for any . For any , , , define as

| (2.4) |

The quantities and denote the scale and asymmetry parameters of the marginal distribution of , whereas the constants ’s and ’s generalise standard dependence measures invoked in the literature. Noticeably, corresponds to the normalised covariation between and . This dependence measure was been introduced by [Miller (1978)] and [Cambanis and Miller (1981)] to replace the ill-defined covariance between two symmetric -stable random variables, and has been a popular tool to formulate point forecasts of infinite variance -stable processes [see [Karcher et al. (2013)] and the references therein]. The new constants and , introduced here, which intervene in the expressions of the higher order conditional moments of , can be seen as extending this dependence measure to higher powers of and in the asymmetric case. The new family of functions introduced contains functions related to the marginal density of the stable random variable , : . The following result recalls the expression of the conditional expectation in the case .

Theorem 2.1 (Theorem 5.2.2, [ST94])

We now state our result in the case for the conditional moments of order two, three and four.

Theorem 2.2

Let be an -stable random vector with spectral representation .

Proof. See Sections B, C and D in the Supplementary File.

Let us now turn to the case .

The following result recalls the expression of the conditional expectation in this case.

Theorem 2.3 (Theorem 5.2.3, ST94)

We next provide our result for the second order conditional moment when . As for the conditional expectation, two different expressions hold according to whether the marginal distribution of is skewed or symmetric.

Theorem 2.4

Let be -stable, with and spectral representation , where satisfies (2.2) with . Then, for almost every ,

if , and

if . Here, , , , the ’s and the ’s are as in (2.3), and are respectively the marginal density and cumulative distribution function of , , , and U, V and W are given in (E.12)-(E.14) in the Supplementary File.

Proof. See Section E in the Supplementary File.

The expressions of the conditional moments simplify when one considers the asymptotics with respect to the conditioning variable, as becomes large.

Proposition 2.1

Let and let be -stable with , and spectral representation such that the conditional moment of order exists. If , then

and if and , then, .

Proof. See Section F in the Supplementary File.

3 Conditional moments of noncausal -stable processes

Operating the set of properties of bivariate -stable distributions provided in the previous section, we study the existence and expressions of the conditional moments of -stable infinite moving average processes. Discussions on practical aspects as well as examples focusing on modelling practices of the empirical noncausal literature follow the main result. Let us consider a two-sided MA() process as in (1.1) with -stable errors and coefficients satisfying

| (3.1) | |||

| (3.2) |

Conditions (3.1)-(3.2) ensure that converges absolutely almost surely so that is well defined and strictly stationary. A moving average process of the form (1.1) satisfying the above conditions is said to be purely causal if for and purely noncausal if for . Noncausality is found to be crucial for the existence of conditional moments higher than order . An important class of models that we shall consider and which admits MA() representations satisfying the above conditions is the class of ARMA processes. General ARMA processes –causal, noncausal, invertible or non-invertible– are strictly stationary solutions of stochastic recursive equations of the form

| (3.3) |

where (resp. ) denotes the forward (resp. backward) operator, and are polynomials of degrees and , and and are two polynomials of respective degrees and with roots on or outside the unit circle. Equation (3.3) admits a unique strictly stationary solution provided that , for , and that (resp. ) has no common root with (resp. ). The stationary solution is noncausal if .

3.1 Spectral representation of

Because the error sequence is -stable distributed, the bivariate vector , for satisfying (1.1), (3.1) and (3.2), is itself -stable for any horizon and the results from the previous section apply. This is a consequence of the following lemma, which provides the spectral representation of discrete time vectors of linear moving averages driven by -stable i.i.d. errors.

Lemma 3.1

Let . For and real deterministic sequences , , both satisfying (3.1)-(3.2), let , with , and denote for . Then, is an -stable random vector in , with spectral representation given by

| (3.4) |

for any Borel set , where if , else , is the Dirac measure at point , stands for the Euclidean norm, and by convention, if for some , , i.e., , then the th term vanishes from the sums.

Proof. See Section G in the Supplementary File.

3.2 Conditional moments

The results on bivariate stable vectors immediately apply to with . A sufficient condition for the existence of conditional moments is given in the following proposition as well as their expressions. Without loss of generality, we will assume in the rest of this section that the stable errors have zero location parameter, i.e., , unless stated otherwise.

Proposition 3.1

Let be an -stable two-sided MA() process, , , , satisfying (1.1), (3.1)-(3.2) and let .

Assume there is such that

| (3.5) |

Then for .

For , the moments , , when they exist, are given by Theorems 2.1-2.2 with

For , let where is the shift vector as in Lemma 3.1. Then, the first- and second-order moments of are respectively given by Theorems 2.3-2.4 with the ’s, ’s, , as in and

By convention, in all the points above, if , then the th term vanishes from the sums.

Remark 3.1 (Existence of moments)

Point provides a sufficient condition for the existence of conditional moments. Notice that the left-hand side of (3.5) is an increasing function of . Thus, if (3.5) holds for some , it then holds for any , and if it fails for , it then fails for all . Causal processes, say of the form with , automatically fail condition (3.5) for all , as and the th term of the sum is finite only if . In the case of symmetric errors (), Theorem 1.1 by [Cioczek-Georges and Taqqu (1995b)] allows to conclude that (3.5) is also necessary and hence that causal processes do not have finite conditional moments for orders higher than . Conversely, (3.5) may hold for some for noncausal processes provided the coefficients do not decay too fast as . In fact, the slower the decay of as , the higher the values of for which (3.5) will hold. In other terms, the stronger the dependence on <<future>> errors, the higher the order at which conditional moments will exist: hence the intuition that higher-order conditional moments may exist provided that the process is anticipative or noncausal enough. It is easy to show that (3.5) holds for any as soon as decays geometrically or hyperbolically, guaranteeing the existence of conditional moments up to order at all prediction horizons for noncausal ARMA and fractionally integrated processes. Consider for instance a noncausal process of the form (1.1) such that for , for and , for some non-zero constant and . Letting ,

and since , the summability condition (3.5) holds for any . In particular, it holds for and therefore, Point of Proposition 3.1 ensures that admits finite conditional moments up to order . It is possible to find noncausal processes for which (3.5) holds only up to some , i.e., entailing that conditional moments are finite only up to order strictly within , with moreover depending on the prediction horizon. Such processes are necessarily noncausal and typically feature extremely short range dependence on future errors. See Section A.1 in the Supplementary File for an example.

Remark 3.2 (Computational aspects)

From a computational perspective, the conditional moments of given given in Proposition 3.1 can be inexpensively calculated for various horizons and conditioning values . In the case , computing these moments requires evaluating the functions , , appearing in Theorem 2.2, which depend both on and on through the ’s and ’s given in point of Proposition 3.1. These functions can be decomposed into , where and are constants depending only on and fixed parameters of the process, while and are integrals of a single variable which need only to be computed once for a given conditioning value . Computing these integrals requires paying attention to two main hurdles. First, these are improper integrals on , which requires truncating the integral using a high enough cutoff value . This will typically yield a good approximation as the integrand vanishes at exponential speed. Notice that the speed of the decay does not depend on nor and a single sufficiently high threshold will do for all horizons and conditioning values. Second, the integrand contains an oscillatory term, whose <<frequency>> increases with . This requires choosing a sufficiently fine subdivision of the truncated integration interval . For lower magnitudes of , coarser subdivisions will suffice. As grows larger, one might fear that the required fineness of the subdivision will lead to prohibitively expensive computational costs: in this large conditioning value regime, one can however avoid the computation of the integral altogether and favour the asymptotic approximations given by Proposition 2.1. Similar considerations hold for the moments in the case . More details can be found in [ST94] Section 5.5 on numerical techniques for computing the moment of order 1, which recommendations are still relevant for higher orders.

3.3 Examples

3.3.1 Mixed ARMA processes

Mixed causal-noncausal AR (MAR) processes are often invoked in the empirical noncausal literature for speculative bubble modelling. Their conditional distribution and moments are known analytically only in special cases [see [Fries and Zakoian (2019)] for details], and, beyond these special cases, practical forecasting relies on the simulation- and sample-based methods by [Lanne et al. (2012a)] and [Gouriéroux and Jasiak (2016)]. Mixed causal-noncausal ARMA processes with in addition a possibly non-invertible MA components (MARMA) as in (3.3) however, have not yet taken up as much as MAR processes for speculative bubble modelling. This is probably due to the absence of analytical results regarding their conditional distribution. Estimation procedures for such ARMA processes focus on providing estimators of the coefficients of the AR and MA polynomials, whereas the results of Proposition 3.1 rely on the coefficients of the MA() representation . Fortunately, the coefficients can be recovered exactly from the AR and MA polynomials. For a MARMA process solution of Equation (3.3), we have from [Gouriéroux and Jasiak (2016)] Section 2.3 the following decomposition:

| (3.6) |

where and are the two polynomials resulting from the partial fraction decomposition

and where and are defined by and . Letting , the processes and furthermore satisfy the recursions and . When , reduces to a MAR process and and are respectively called the causal and noncausal components of . Identifying the MA() representations in of the left- and right-hand side of (3.6) yields a general expression of the coefficients as

| (3.7) |

where , and are the coefficients of the Laurent expansions of and [[Conway (1978)] p.107], which are such that for ; for ; and otherwise recursively obtained from the AR polynomials as

Proposition 3.1 then applies to the MARMA process with coefficients sequence as in (3.7).

For practical purposes, the infinite sums in Proposition 3.1 can be truncated.

For MARMA processes, vanishes geometrically fast as and truncation will typically yield a good approximation.

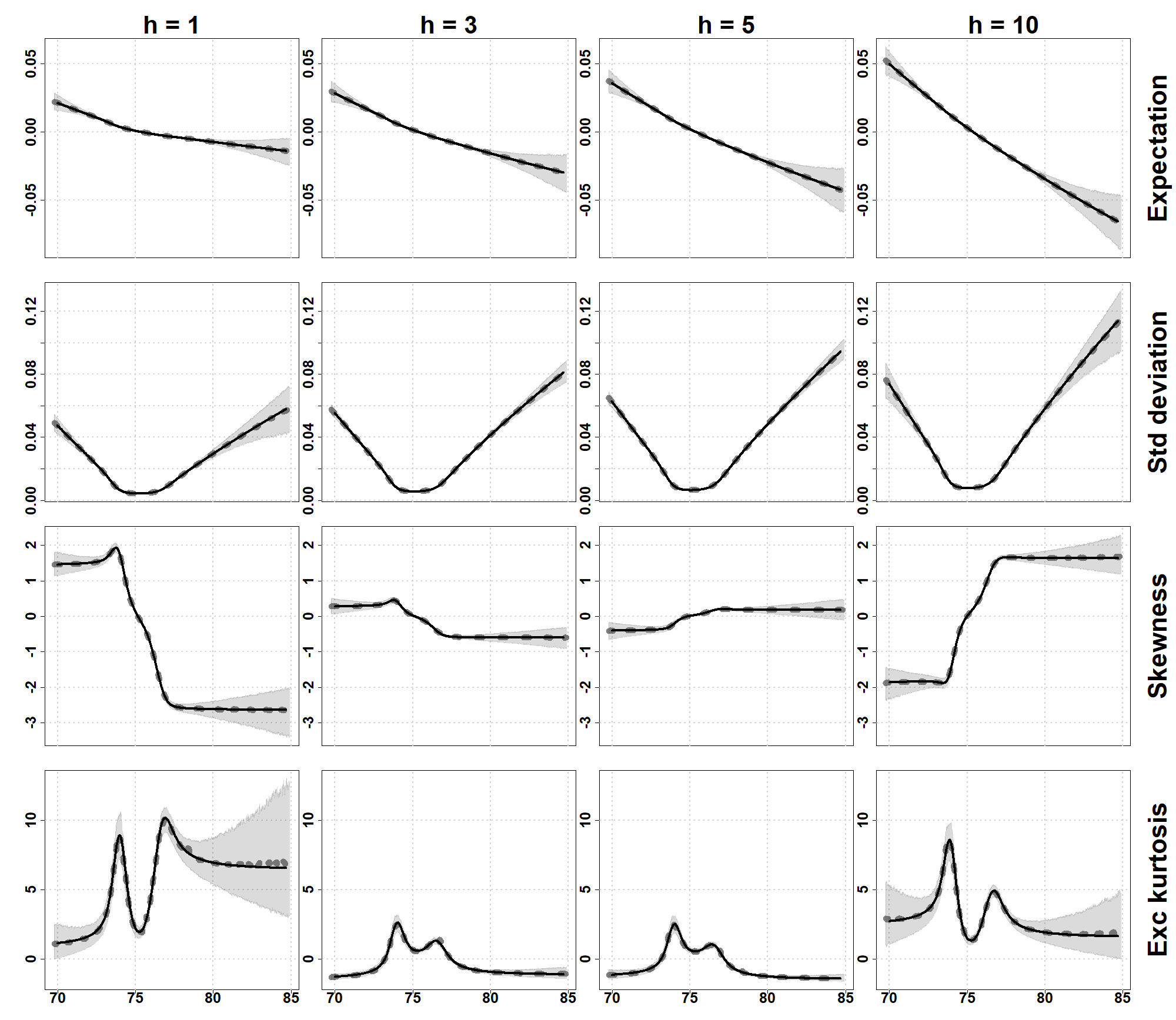

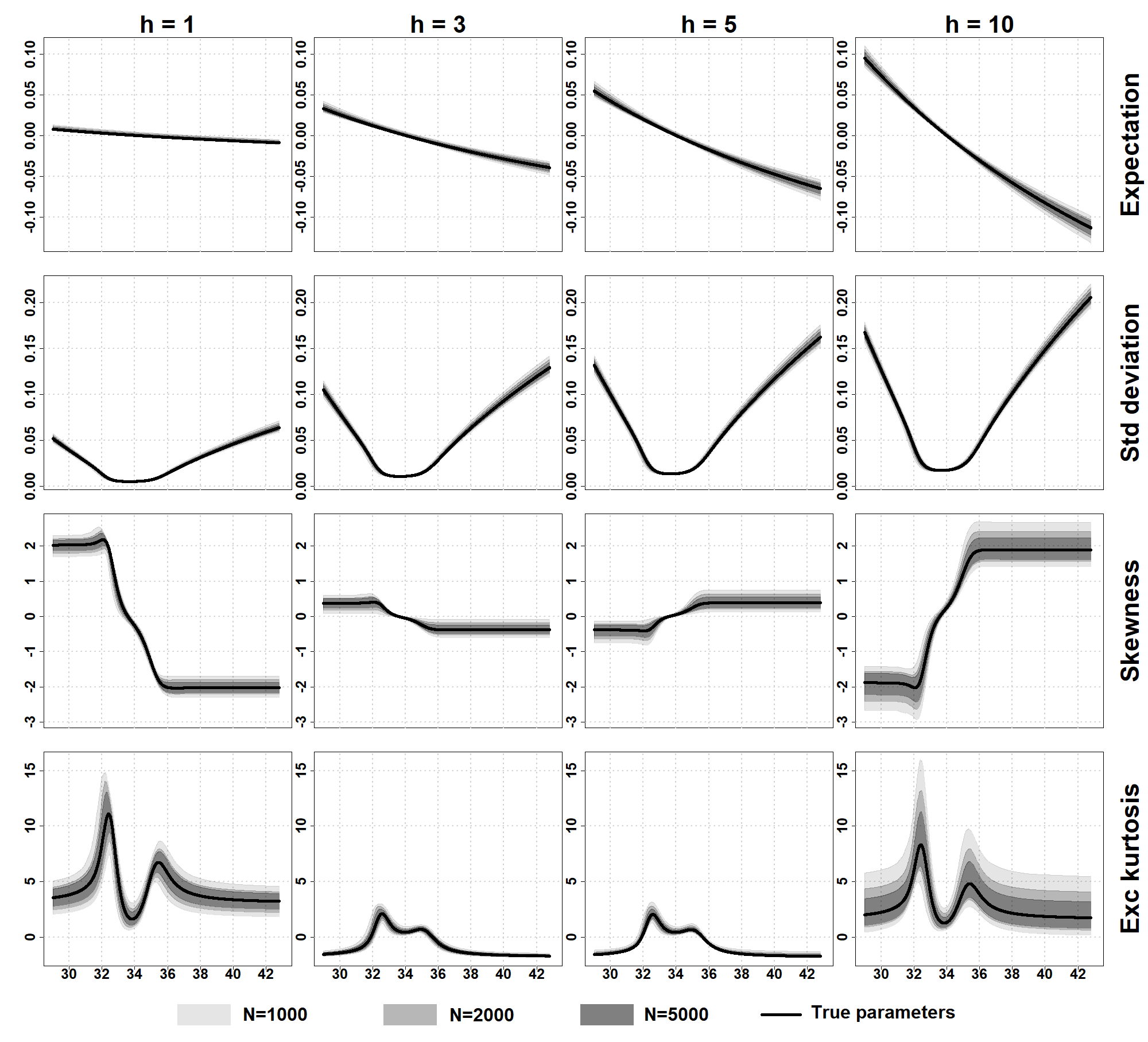

A simulation experiment was conducted to illustrate the results of Proposition 3.1 in the case of a MARMA process. The theoretical conditional moments are compared to model-free non-parametrically estimated counterparts in order to assess the validity of the analytical formulae. Let us consider, for expository purposes, that the price series of an asset is modelled by the MARMA process defined as the strictly stationary solution of , . We will focus on the conditional moments of the returns at horizon of , denoted . On the one hand, we use the formulae of Proposition 3.1 to compute the theoretical expectation, standard deviation, skewness and excess kurtosis of the returns, conditional on the level :

| (3.8) | ||||||

It is just a matter of expanding the powers in the definitions above to express the conditional moments of in terms of , , where admits an -stable MA() representation whose coefficients are given by (3.7). On the other hand, we simulate trajectories , , with observations of the aforementioned MARMA process and obtain model-free estimates of the conditional power moments using Nadaraya-Watson estimator

where is the Gaussian kernel with bandwidth .

Empirical counterparts , , , , , of , , and are obtained by substituting the non-parametric estimates in (3.8) in place of .

We considered prediction horizons , conditioning values in the interval –corresponding to the 0.0005 and 0.9995 quantiles of the marginal distribution of : 99.9% of the probability mass of is supported on – and used a bandwidth of .

Letting denote generically any of , , , , we compute for each quantity the point-wise average of Nadarya-Watson estimators as as well as the point-wise 0.05 and 0.95 quantiles across simulations. Figure 2 compares the theoretical conditional moments obtained using Proposition 3.1 and (3.7) with their empirical non-parametric counterparts.

We notice that the average is very closely matching the theoretical moments curves, and that the theoretical moments lie everywhere within the empirical 0.05-0.95 interquantile.

This provides evidence for the sanity of Theorem 2.2 and Proposition 3.1.

In addition, we notice that the dispersion of the model-free non-parametric estimators is rather important for far from central values, despite the length of the simulated trajectories ( observations).

This suggests that the analytical formulae can hardly be traded for purely data-driven methods when it comes to estimating the dynamics during extreme events, even with massive amounts of data.

To compute the conditional moments in practice, one can now overlook the model-free non-parametric approach and resort to a parametric plug-in strategy: e.g., estimate the MARMA and stable parameters by maximum likelihood and plug the parameter estimates in the formulae of Proposition 3.1.

An additional experiment reported in Section A.2 of the Supplementary File illustrates the reliability of the latter parametric plug-in strategy, and its ability to accurately recover the conditional moments curves for practically-relevant sample sizes.

Illustrations of the shape of the conditional moments for various parameterisations of MARMA processes are also provided.

Remark 3.3

The asymptotic properties of the Nadaraya-Watson for strongly mixing sequences with bounded second order marginal moment have been established by [Hansen (2008)]. In our context, where higher-order conditional moments may be bounded in spite of infinite marginal variance, the validity of the Nadarya-Watson estimator is an open issue. The agreement between the theoretical moment curves and the empirical ones obtained with the Nadaraya-Watson estimator also suggests that the latter’s validity may extend. This is left for further research.

3.3.2 Cauchy MA() processes

MAR processes with Cauchy errors (stable with and ) are a popular benchmark for speculative bubble modelling in the noncausal literature [e.g., [Hencic and Gouriéroux (2015), Hecq et al. (2016), Fries and Zakoian (2019), Gouriéroux et al. (2019), Cavaliere et al. (2020), Hecq and Voisin (2020)]].

An attractive feature of this class of models is that the Cauchy distribution is one of the special cases in the stable family for which a closed-form density is available.

For Cauchy MAR processes with a single noncausal root, i.e., as in (3.3) with , and , the decomposition into causal and noncausal components (3.6) allows to obtain the conditional moments and density in closed-form. The techniques based on decomposition (3.6) do not extend however, and no result is available for more general Cauchy noncausal processes.

Let us apply Proposition 3.1 to with and such that Point guarantees the existence of the first- and second-order moments (e.g., a Cauchy MARMA process).

Then, invoking Point with since , we have for any and ,

In particular, if for all , then and .

Remark 3.4 (Conditional heteroscedasticity of noncausal processes)

[Gouriéroux and Zakoian (2017)] and [Fries and Zakoian (2019)] highlighted that the Cauchy noncausal AR(1) and MAR() processes exhibit GARCH effects in calendar time, although seemingly defined based on i.i.d. errors. The above result shows that this property extends to Cauchy MA() processes. Figure 2 further illustrates that this is not a specific feature of the Cauchy distribution, and that modelling prices with noncausal -stable processes also induces conditional heteroscedasticity in the returns for other values of . In the Cauchy case, the conditional volatility is quadratic in the past values and the authors underlined that admits a semi-strong double autoregressive representation à la [Ling (2007)]. The conditional first and second moments in Proposition 3.1 suggests that a more complex representation may hold in general for . Proposition 2.1 ensures nevertheless that the variance of is still asymptotically quadratic in the conditioning value. This can be noticed in the example of the following section.

3.3.3 -stable noncausal AR(1)

Let be the -stable noncausal AR(1) solution of , with (for simplicity), , and . Then for and , and the conditional moments, when they exist, are given by Proposition 3.1 with

for . For , a clear interpretation of the distribution appears during bubble episodes, that is, as becomes large relative to the central values of process . Letting , , and denote the conditional expectation, variance, skewness and excess kurtosis of given respectively (as in (3.8) with replaced by ), when they exist, we have

as if , if , and () if (). See Section H in the Supplementary File for the proof.

4 Forecasting noncausal bubble crashes

For practical econometric purposes, financial bubbles in stock prices, market indexes and price-dividend ratios are typically characterised as short-lived explosive episodes followed by abrupt or gradual collapses, and are analysed using reduced form models [[Phillips and Shi (2018)]].

In this section, we focus on the dynamics of noncausal processes during such explosive episodes, that is, when the conditioning level of the trajectory takes on large positive or negative values.

The strikingly simplistic forms of the conditional moments of the -stable noncausal AR(1) during such events, as given in Section 3.3.3, are characteristic of a weighted Bernoulli distribution charging probability to the value and probability to .

In the framework of this model, it is thus natural to interpret as the probability that the bubble survives at least more time steps, conditionally on having reached the level .

Such simplification of the dynamics during extreme events is actually not limited to the -stable noncausal AR(1).

We derive here closed-form expressions of the ex ante crash odds of bubbles generated by noncausal processes. We first formally establish in the case of the noncausal AR(1) that the intuition described above holds.

We then show that this intuition non-trivially extends to processes featuring noncausal AR(1)-type bubbles followed by almost arbitrarily shaped collapses after the peak.

We end this section by obtaining an expression of the crash odds in the case of noncausal MA() processes.

As we focus on the extreme events, we do not need to fully specify a parametric distribution for the errors as in Section 3, but only require that their probability tails are similar to those of an -stable distribution in that they decay as power-laws.

Formally, we assume that is an i.i.d. error sequence with regularly varying tails:

| (4.1) |

with tail parameter , asymmetry and any slowly varying function at infinity, i.e., such that as for all . The -stable distribution, with and asymmetry parameter , is a typical example of distribution whose tails are power-law as in (4.1). However, the more general assumption above and the results in the rest of this section encompass not only noncausal processes with -stable errors, for which we derived the moments in the previous section, but noncausal processes with any power-law tailed errors, including (skewed) -student errors often invoked in the empirical noncausal literature. Note furthermore that the tail exponent (or degrees of freedom in the case of the -student) is not restricted to be below 2 in this section but can take any positive value.

4.1 Crash odds of noncausal AR(1)-type bubbles

4.1.1 Purely noncausal AR(1) : exponential bubbles with instant collapses

The following proposition provides the conditional distribution of the noncausal AR(1) during explosive bubble episodes.

Proposition 4.1

Let be the noncausal AR(1) process solution of with , i.i.d. errors satisfying (4.1) for some tail exponent and asymmetry . Then, for any , any , we have as

for any if , and if .

Proof. See Section I in the Supplementary File.

The proposition formalises the intuition that bubbles generated by a noncausal AR(1) with regularly varying errors feature a geometric survival distribution with probability parameter .

This interpretation implies that the survival probability does not depend on the current scale of the bubble.

Surprisingly, given that the noncausal AR(1) is a Markov process, it further implies that the survival probability of bubbles does not depend at all on the past history: such bubbles display a memory-less property.

Several statistics of interest can be easily computed to describe their survival distribution, e.g., crash probability at horizon , hazard rate, expected lifetime. As the bubbles are memory-less, their survival distribution can be fully characterised by the so-called half-life, or median survival time: the duration such that the crash probability at horizon is .

More generally, one can be interested in the -survival quantile, , that is, the duration such that the survival probability at horizon is equal to . Table 1 summarises the expressions of these descriptive survival statistics for bubbles generated by a noncausal AR(1) model with regularly varing errors.

| Crash probability at hor. | Hazard rate | Expected life | -Survival quantile |

Computing these statistics only requires the knowledge of the AR coefficient and of the tail exponent . Typically, bubbles with smaller growth rates ( closer to unity) and driven by heavier-tailed shocks (smaller ) are likely to last longer.

On the one hand, the memory-less property of these bubbles could be appealing from a financial and economic perspective as it implies that the crash date cannot be known with certainty by traders, hence ensuring a form of no-arbitrage condition. Bubbles with crash dates arising according to a constant hazard rate –another feature of the geometric distribution– appear moreover compatible with the implications of game theoretic settings where arbitrageurs attempt to time exponentially increasing bubbles and induce the crash at a random date when the selling pressure they exert is high enough [[Matsushima (2013)]]. On the other hand, the memory-less property also implies that no sophisticated method could allow a forecaster to say anything more regarding the future of AR(1) bubbles than <<growth or crash>> with the probabilities above. In the case of non-exponentially shaped bubbles or if the extreme errors driving bubbles are assumed to be endogenous rather than i.i.d. (as in [Blasques et al. (2018)]), past history could however play a more central role for prediction.

Remark 4.1 (Parallel with [Blanchard and Watson (1982)])

The dynamics of the noncausal AR(1) during bubble episodes is reminiscent of the classical model proposed by [Blanchard and Watson (1982)]:

| (4.2) |

where , is an i.i.d. zero-mean and finite variance error sequence, and are i.i.d. Bernoulli distributed random variables such that . This model recurrently generates exponentially-shaped explosive bubbles: the trajectory follows an explosive path while and ends in a crash when . In view of Proposition 4.1, the bubble episodes generated by a noncausal AR(1) with regularly varying errors follow a dynamics à la Blanchard and Watson with and . Interestingly, while Blanchard and Watson’s model is explicitly designed to feature successive bubble/bust cycles, where the bust probability is a free parameter, the noncausal AR(1) generates trajectories where bubble events intersperse calmer periods. The dynamics (4.1) only emerges during bubble events and the crash probability is rather a function of the other model parameters. The structural constraint on the survival probability –specific to the noncausal AR(1), a linear process shown to be suitable to describe bubble components of solutions to rational expectation price models [see [Gouriéroux et al. (2020)]]– has important statistical implications. In the framework of Blanchard and Watson’s model, statistical information about can only be gathered from the observed durations of past bubbles that have already collapsed. Assuming bubbles of durations are observed on a given time series, say, generated by (4.2), one could propose as an estimator for the parameter of the Bernoulli variables . In bubble modelling applications it is however not uncommon to face very small situations, or even in cases where a single explosive and uncollapsed trend is observed. This renders accurate estimation of difficult at best, and unfeasible at worst. [West (1987)] even considered not to be an identifiable parameter. In contrast, the estimation of can exploit more information present in the data: the sample autocorrelations of the time series and the bubble growth rates provide information about , while the tail heaviness of the time series and of the residuals (obtained after estimation of ) provide information about . A maximum likelihood estimation of the noncausal AR(1) assuming a parametric distribution for the errors, such as -stable or -student, would suffice to obtain an estimate of . Semi-parametric approaches could be operative as well, e.g., estimating by Least Squares and using the Hill estimator.

4.1.2 Mixed causal-noncausal AR(1) : exponential bubbles with arbitrary collapses

To encompass explosive exponential bubble patterns followed by more complex post-peak dynamics, the noncausal literature considered adding a causal component to the noncausal AR(1), resulting in the much-invoked MAR() processes [see for instance [Hecq and Voisin (2020), Gouriéroux et al. (2019)]]. We show here that whatever the form of the causal component adjoined to the noncausal AR(1), i.e., whatever the shape of the collapse after the exponential growth episode, the crash probability –or more accurately, the probability of reaching the end of the exponential growth– still follows from a geometric distribution with parameter . We do not restrict to the case of MAR processes but actually consider any process satisfying (1.1) with for all . Such a process satisfies the autoregression , where , with for all . Letting , , and , we will state our result in the context of a forecaster observing an ongoing explosive exponential episode, that is, observing being close to colinear with , and wishing to forecast the future path . The only restriction that we impose on is the one ruling out <<collapses>> that would be of similar shapes as the initial exponential growth. This assumption is formalised below and the forecasting result follows.

Assumption 1

There is such that for all and ,

Proposition 4.2

Proof. See Section J in the Supplementary File.

The above result enjoys a very intuitive pattern interpretation.

We illustrate this on the example of the MAR(1,1) below.

Let us already highlight that the odds of reaching the end of an observed exponential growth episode at some future horizon are of the same form as the crash odds of a purely noncausal AR(1), i.e., geometric governed by .

This drastically simplifies the peak-date prediction exercise for a forecaster, who only has to estimate two parameters and can even afford to stay agnostic as to whatever form the collapse following the peak will take.

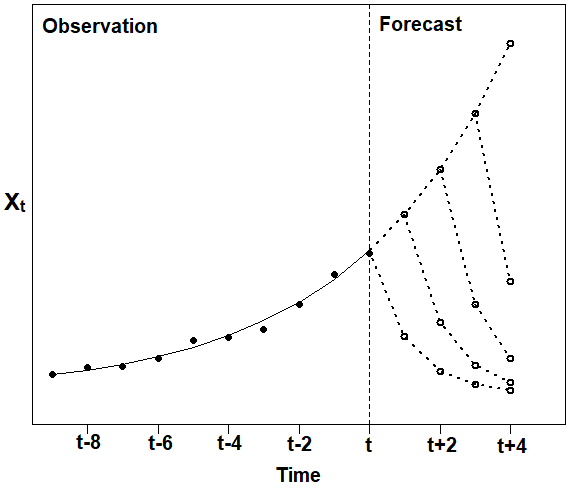

Example 4.1 (Forecasting MAR(1,1) bubbles)

Consider the MAR(1,1) process defined as the strictly stationary solution of

| (4.3) |

where and is an i.i.d. sequence of regularly varying errors as in (4.1) with tail index . The process admits the MA() representation , with for ; for ; and for all . Note that is still an i.i.d. regularly varying sequence with index . Assumption 1 can be shown to hold and Proposition 4.2 applies to with the sequence as described above and

If a forecaster observes during an extreme event of process that the recent past trajectory has approximately an exponential shape of growth rate , i.e., if one observes that is approximately colinear to , then the forecaster may assert that the exponential growth has probability to continue at least until horizon , and probability to stop at an earlier date . Whenever the exponential growth will reach a peak, the trajectory will then enter a phase of exponential decay, with decay rate . Figure 3 illustrates the forecast interpretation from a trajectorial and probability tree perspectives.

|

Remark 4.2 (Rational bubbles and fat tails)

[Lux and Sornette (2002)] showed that the marginal distribution of rational expectation bubble models à la [Blanchard and Watson (1982)] necessarily feature regularly varying tails.

They further established that a necessary condition for any bubble process of the form (4.2) to abide to the rational expectation condition , , where denotes the expectation conditional on all information available at date , is that the tail index of the regular variations be strictly smaller than 1.

Invoking evidence gathered by the empirical literature, which does not support such degrees of fat-tailedness, Lux and Sornette conclude that rational bubble models à la Blanchard and Watson are incompatible with the observed statistical properties of financial data.

Interestingly, it appears that MAR processes could reconcile the rational expectations condition with tail indexes greater than 1.

In the MAR(1,1) example above, we have that during the inflation phase of a bubble generated by (4.3), the one-step ahead conditional distribution is approximately behaved as

Thus, during the inflation phase of a bubble, , and

The rational expectations condition requires , which can be rewritten as

A straightforward analysis shows that, for any , the function is strictly increasing on and that , . For , one retrieves Lux and Sornette’s result. For however, values of above 1 are admissible. This suggests that the MAR(1,1), as a process featuring Blanchard/Watson-like bubbles followed by gradual decays, can reconcile the rational expectations condition with regular variation tail indexes above 1. In fact, tail indexes arbitrarily large could be admissible provided the decay after the peak is slow enough ( close enough to 1).

4.2 Crash odds of noncausal MA() bubbles

Noncausal MA() processes, which encompass general pre-peak bubble shapes, also feature a simplification of their dynamics during extreme events. The following result generalises the second convergence in Proposition 4.1 to express the ex ante crash odds of bubbles generated by noncausal MA() processes.

Proposition 4.3

Proof. See Section K in the Supplementary File.

Similarly to the interpretation of the noncausal AR(1), one can notice that the crash probability of bubbles does not depend on their current scale.

Contrary to the noncausal AR(1) however, the survival probabilities could in general be different if the past history of the bubble was accounted for in the conditioning.

To investigate this question, one has to characterise the conditional distribution of given more past information, e.g., … This problem is out of the scope of the current paper and is addressed elsewhere [[Fries (2018)]].

To evaluate the asymptotic probability (4.4) in practice, only the knowledge of the coefficients and of is needed, whereas asymmetry, scale or location have no role.

We illustrate through simulations that the probability on the left-hand side of (4.4) indeed converges to the right-hand side limit as the conditioning value grows larger.

We simulated trajectories of observations of a noncausal AR(3) process.

For each simulated trajectory , , we computed the following estimator of the probability (4.4):

| (4.5) |

for several horizons and several quantiles of the marginal distribution of . We perform this exercise twice, first assuming that the AR(3) process is driven by -stable errors, and then assuming -student errors with 1.5 degrees of freedom. As our result holds for any heavy-tailed errors in the sense of (4.1) and the tail exponents of the error sequences are equal, the estimated crash probabilities should tend to the same limit as increases. Table 2 gathers the average of the empirical probabilities across the simulations along empirical 95% confidence intervals. One notices that the empirical probabilities indeed come very close to the theoretical ones as increases, both for -stable and -student errors. The dispersion of the non-parametric estimators across simulations again indicates that estimating the crash odds of bubble events by purely data-driven methods might be challenging, even with massive amount of data. The expressions given by Propositions 4.1, 4.2 and 4.3 thus offer the attractive alternative of computing plug-in estimators of crash odds after having estimated the model parameters.

| Mean | -CI | Mean | -CI | Mean | -CI | ||||||

| 8.37 | (8.33 , 8.41) | 33.1 | (33.0 , 33.2) | 42.5 | (42.3 , 42.7) | ||||||

| 9.12 | (9.08 , 9.17) | 30.7 | (30.6 , 30.9) | 37.6 | (37.4 , 37.7) | ||||||

| 17.7 | (17.5 , 17.8) | 65.9 | (65.4 , 66.4) | 83.4 | (83.0 , 83.8) | ||||||

| 18.5 | (18.3 , 18.7) | 69.1 | (68.7 , 69.6) | 87.9 | (87.5 , 88.3) | ||||||

| 20.5 | (19.9 , 21.1) | 75.2 | (73.7 , 76.8) | 94.4 | (93.3 , 95.3) | ||||||

| 20.5 | (19.9 , 21.1) | 75.6 | (74.1 , 77.1) | 94.9 | (93.9 , 95.8) | ||||||

| 20.7 | (18.9 , 22.9) | 76.2 | (71.6 , 80.9) | 95.4 | (92.3 , 98.0) | ||||||

| 20.7 | (18.9 , 22.9) | 76.2 | (71.4 , 81.1) | 95.5 | (92.4 , 98.1) | ||||||

| 20.7 | – | 76.2 | – | 95.5 | – | ||||||

Remark 4.3 (Tail dynamics and GARCH effects)

We here propose some intuition highlighting the connection between the tail dynamics derived in the previous propositions and the emerging GARCH effects of noncausal processes. Consider for simplicity a purely noncausal process with for and for . The ’s being heavy-tailed and i.i.d., if at some date is observed extreme, this likely results from one given being extreme, for some random date in the neighbourhood of such that , i.e., . Because of the i.i.d.-ness of the errors, it is likely that the extreme error is isolated and outweights the other neighbouring ’s contributing to in the sense that for all such that , i.e., . Thus, we have the approximation

In the case of the noncausal AR(1), , and (recall that the random date satisfies ), which recovers the result of Proposition 4.1: the conditional distribution of during extreme events concentrates on the points (crash) and (growth), and the random date has to be interpreted as the peak date of the bubble. Given the information at , which is assumed to contain at least the value of , the conditional variance of can now be approximated as

This analysis shows that provided the distribution of given is not degenerate (note that the existence of a non-zero constant such that for all is ruled out), then and features GARCH effects during extreme events. Continuing with the example of the noncausal AR(1), the above writes (we recognise the asymptotic variance in Section 3.3.3)

highlighting that the conditional variance of stems from the uncertainty in the occurrence date of the peak given the available information. Note that this heuristics does not necessarily presume that contains only information about the past values of . The set could contain information about other variables or noisy proxies of (insider information for instance). Section 3.3.3 and Proposition 4.1 leads us to conclude that observing the infinite past of (recall that the noncausal AR(1) is Markov) does not induce to be degenerate and GARCH effects emerge. Only in case of perfect foresight of , i.e., , does the GARCH phenomenon seem to vanish.

5 Evaluating the odds of crashes of real series

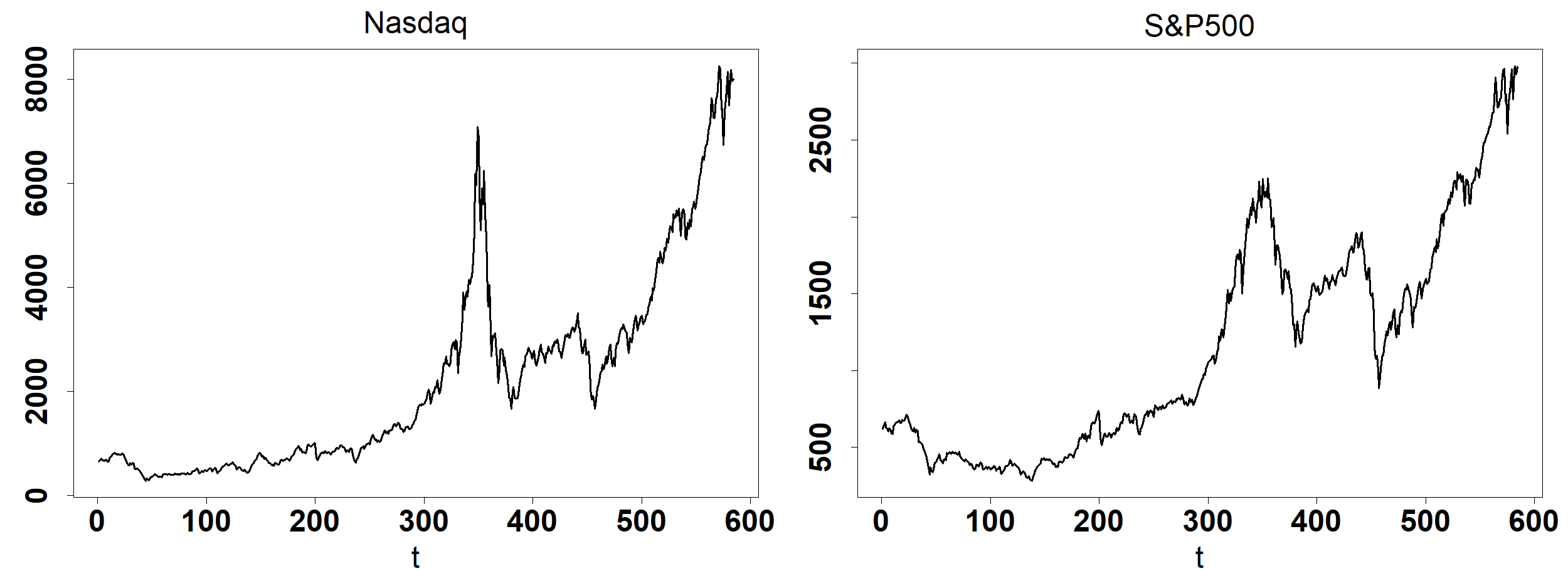

In this section, we consider two series commonly studied in the speculative bubble literature and in which evidence of explosive behaviour has been exhibited: the Nasdaq and S&P500 indexes (see e.g. [Gouriéroux and Zakoian (2017), Phillips et al. (2015), Phillips et al. (2011)]). Figure 4 displays the monthly series of the Nasdaq and S&P500 real prices from February 1971 to September 2019 ( observations each), obtained by inflation-adjusting the nominal series using the Consumer Price Index provided by the Federal Bank of Saint Louis (fred.stlouisfed.org/series/CPIAUCSL).

The two series feature almost uninterrupted growth episodes since beginning of 2009 up to 2019.

[Gouriéroux and Zakoian (2017)] found evidence that a stable noncausal AR(1) bubble dynamics is compatible with the real Nasdaq trajectory.

Unreported results using standard model selection methods from the noncausal literature (e.g., information criteria [[Lanne and Saikkonen (2011), Hecq et al. (2017b)]], coefficient testing [[Cavaliere et al. (2020)]]) further confirm the reasonableness of this specification for both series of interest here.

Starting on the premise that the explosive episodes in the data can be modelled as ongoing realisations of noncausal AR(1) bubbles climbing towards exogenous power-law-scaled peaks, we will be in the position to provide estimates of ex ante crash odds of the recent growth trends based on the results of Section 4.

In particular, we have shown in Section 4.1 that bubbles generated by heavy-tailed noncausal AR(1) models feature geometric survival distributions with probability parameter .

It thus suffices to provide values for the AR coefficient and the tail parameter .

We obtain estimates of these parameters by -stable Maximum Likelihood, which has been shown to yield consistent estimators [[Andrews et al. (2009)]].

We use the fast implementation of [Royuela-del-Val et al. (2017)] to evaluate -stable densities, available in the R package libstableR.

Contrary to which is asymptotically normal, the estimator of the AR coefficient unfortunately features an intractable asymptotic distribution.

We resort to a parametric bootstrap procedure to approximate the finite sample distribution of the estimators and compute confidence intervals.

Table 3 reports the stable noncausal AR(1) fits and the value of the log-likelihood at optima.

We note that the estimate of for the Nasdaq series is close to the one obtained by [Gouriéroux and Zakoian (2017)].

The values of the log-likelihood for fitted stable causal AR(1) specifications, which estimate the AR coefficient to be 1 for both series, is provided for comparison purposes and confirm that the stationary noncausal options are to be preferred.

Under the stable noncausal AR(1) specification, the survival distributions of the recent explosive growth episodes can be completely estimated and characterised by plugging-in the obtained estimates and in the statistics of Table 1.

For instance, an estimate of the crash probability at horizon can be computed as , while the -life, that is, the duration such that the probability of an explosive episode lasting as long as is equal to , can be computed as .

Table 4 displays a summary of bubble survival statistics for both series.

In the case of the Nasdaq and S&P500, our estimates indicate that bubbles generated by the corresponding stable noncausal AR(1) processes should have % chance of lasting 8.3 and 10.6 years respectively, and % chance of lasting 12.7 and 16.3 years respectively.

The observed durations of the growth episodes from 2009 to 2019 are therefore not abnormally long in that respect and appear very well compatible with the implied model properties.

Irrespective of their past durations, as bubbles generated by such processes feature a memory-less property, this analysis suggests relatively important crash probabilities within one year () between 27.9 and 33.4% for the Nasdaq series, and between 18.6 and 34.8% for the S&P500.

Note that these estimates are robust to any behaviour the collapse after the peak may actually feature: as shown in Proposition 4.2, the shape of the collapse has no role in the ex ante probability of reaching the peak of a noncausal AR(1)-type growth episode.

Last, similar values of the survival statistics are obtained if instead of the -stable assumption one opts for -student or skewed- distributions, or if one proceeds to estimate by ordinary least squares and by applying the Hill estimator to the residuals.

The results of the latter robustness checks are available in Section A.3 of the Supplementary File.

| Stable Noncausal AR(1) | Stable Causal AR(1) | ||||

| log-L | log-L | ||||

| Nasdaq | 1.01 | 0.971 | 3608.640 | 3642.348 | |

| (0.925 , 1.11) | (0.969 , 0.972) | ||||

| S&P500 | 1.36 | 0.983 | 3067.574 | 3086.641 | |

| (1.25 , 1.48) | (0.975 , 0.987) | ||||

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

6 Concluding remarks

By embedding -stable two-sided MA() processes into the framework of bivariate -stable random vectors, we described in detail the conditional dependence of on .

We have shown that noncausality plays a crucial role in the existence of conditional moments, and provided expressions for the latter up to the fourth order, when they exist, as well as their asymptotic behaviours when the conditioning variable takes extreme values.

We have detailed practical implementation aspects of the conditional moments as well as the contribution of the results to current methodological practices of the empirical noncausal literature.

A future empirical investigation could determine whether corresponding patterns in the conditional moments of real data can be identified.

These results could serve as a basis to formulate a higher-order moments portfolio allocation problem (e.g., following Jondeau and Rockinger (2006,2012)) where bubble-timing investors optimise over quantities of speculative and safer assets as well as over the holding time through a bubble.

Some limitations of the provided conditional moments formulae could be addressed in further research.

This includes expanding the conditioning to a set of past values or the entire past, as opposed to conditioning only by the present level of the trajectory.

Also, even though Lemma 3.1 allows to extend the formulae of Proposition 3.1 to the conditional moments of, say, given the present level of another process , obtaining a characterisation of the moments in the general multivariate case remains an open issue.

Furthermore, despite noncausal processes admitting more conditional moments, higher-order conditional moments may nevertheless not exist for smaller values of -for instance, the conditional skewness and kurtosis when .

Alternative dependence measures capturing, say, conditional asymmetry and heavy-tailedness in such cases could be investigated.

Focusing on explosive bubble episodes generated by heavy-tailed noncausal MA() processes, we provided closed-form asymptotic formulae for the predictive distribution, which enjoy very intuitive patterns and probability tree interpretations.

This surprisingly revealed that the noncausal AR(1) bubbles are memory-less with a dynamics à la [Blanchard and Watson (1982)].

The survival distribution of such bubbles is geometric and can be fully characterised by the given of the AR coefficient and the tail exponent , both of which can be estimated by classical methods from the data.

Even more surprising is the fact that the augmentation of a noncausal AR(1) bubble by an arbitrarily-shaped collapse after the peak does not alter the survival distribution of the exponential growth phase of the bubble.

From the point of view of a forecaster observing that the past trajectory is approximately exponentially-shaped, the likelihood of the peak being reached at some future horizon has the same simple expression in terms of and whatever is bound to happen after the peak.

Of course, the speed of the collapse still impacts how much is at risk in case of downturn.

Interestingly, bubbles generated by mixed causal-noncausal processes, and those of a MAR(1,1) in particular, feature an extended Blanchard and Watson dynamics with gradual collapse which appears able to reconcile rational expectation bubble models with tail exponents greater than 1, a well-documented statistical property of financial time series [[Lux and Sornette (2002)]].

We further demonstrated how the closed-form formulae of the predictive distribution and of crash odds can be applied on growth episodes of real data.

Statistical methods for agnostically estimating the coefficients of the MA representation, e.g., under low dimensional restrictions, and for robustly estimating the tail index in locally explosive events could enable more refined evaluation of the crash odds.

Acknowledgments

The author is extraordinarily indebted to Jean-Michel Zakoïan, and further thanks Denisa-Georgiana Banulescu, Jean-Marc Bardet, Frédérique Bec, Francisco Blasques, Ophélie Couperier, Gilles De Truchis, Elena Dumitrescu, Christian Francq, Christian Gouriéroux, Alain Hecq, Jérémy Leymarie, Yang Lu, Andre Lucas, Anders Rahbek, Li Sun, Sean Telg, Arthur Thomas and Elisa Voisin for insightful discussions. The author gratefully acknowledges the support of the Groupe des Écoles Nationales d’Économie et Statistique (GENES), the Agence Nationale de la Recherche (via the Project MultiRisk ANR CE26 2016 - CR), and the support of the European Commission (via the Project NONCAUSALBubble H2020-MSCA-IF-2019 896504).

References

References

- Andrews et al. (2009) Andrews, B., Calder, M., and R., Davis. 2009. Maximum likelihood estimation for -stable autoregressive process. Annals of Statistics, 37, 1946-1982.

- Bec et al. (2020) Bec, F., Nielsen, H. B., and S., Saïdi. 2020. Mixed causal-noncausal autoregressions: bimodality issues in estimation and unit root testing. Forthcoming in Oxford Bulletin of Economics and Statistics.

-

Blanchard and Watson (1982)

Blanchard, O. and M., Watson. 1982. Bubbles, rational expectations, and financial markets. National Bureau of Economic

Research, No. 0945. - Blasques et al. (2018) Blasques, F., Koopman, S. J., and M., Nientker. 2018. A time-varying parameter model for local explosions. Tinbergen Institute Discussion Paper, No. TI 2018-088/III.

-

Cambanis and Miller (1981)

Cambanis, S., and G., Miller. 1981. Linear problems in pth order and stable processes. SIAM

Journal on Applied Mathe-

matics, 41, 43–69. - Cavaliere et al. (2020) Cavaliere, G., Nielsen, H.B, and A. Rahbek. 2020. Bootstrapping non-causal autoregressions: with applications to explosive bubble modelling. Journal of Business and Economic Statistics, 38, 55-67.

- Chen et al. (2017) Chen, B., Choi, J., and J. C., Escanciano. 2017. Testing for fundamental vector moving average representations. Quantitative Economics, 8, 149-180.

- Cioczek-Georges and Taqqu (1995a) Cioczek-Georges, R., and M. S., Taqqu. 1995a. Form of the conditional variance for stable random variables. Statistica Sinica, 351-361.

- Cioczek-Georges and Taqqu (1995b) Cioczek-Georges, R., and M. S., Taqqu. 1995b. Necessary conditions for the existence of conditional moments of stable random variables. Stochastic Processes and their Applications, 56, 233-246.

- Cioczek-Georges and Taqqu (1998) Cioczek-Georges, R., and M. S., Taqqu. 1998. Sufficient conditions for the existence of conditional moments of stable random variables. Stochastic Processes and Related Topics, Birkhäuser Boston, 35-67.

- Conway (1978) Conway, J. B. 1978. Functions of one complex variable. Springer-Verlag, New York.

- Fries (2018) Fries, S. 2018. Path prediction of aggregated -stable moving averages using semi-norm representations. ArXiv preprint arXiv:1809.03631.

- Fries and Zakoian (2019) Fries, S., and J.-M., Zakoian. 2019. Mixed causal-noncausal AR processes and the modelling of explosive bubbles. Econom- etric Theory, 35, 1234-1270.

-

Gouriéroux et al. (2019)

Gouriéroux, C., Hencic, A., and J., Jasiak. 2019. Forecast performance and bubble analysis in noncausal MAR(1,1) pro-

cesses. Toulouse School of Economics. 10.13140/RG.2.2.25135.38568. - Gouriéroux and Jasiak (2016) Gouriéroux, C., and J., Jasiak. 2016. Filtering, prediction and simulation methods for noncausal processes. Journal of Time Series Analysis, 37, 405-430.

- Gouriéroux and Jasiak (2018) Gouriéroux, C., and J., Jasiak. 2018. Misspecification of noncausal order in autoregressive processes. Journal of Economet- rics, 205, 226-248.

- Gouriéroux et al. (2020) Gouriéroux, C., Jasiak, J. and A., Monfort. 2020. Stationary bubble equilibria in rational expectation models. Forthcoming in Journal of Econometrics.

- Gouriéroux and Zakoian (2017) Gouriéroux, C. and J.-M., Zakoian. 2017. Local explosion modelling by non-causal process. Journal of the Royal Statistical Society: Series B. 79, 737-756.

- Hansen (2008) Hansen, B. E. 2008. Uniform convergence rates for kernel estimation with dependent data. Econometric Theory, 726-748.

- Hardin et al. (1991) Hardin Jr, C. D., Samorodnitsky, G., and M. S., Taqqu. 1991. Nonlinear regression of stable random variables. The Annals of Applied Probability, 582-612.

- Hecq and Sun (2019) Hecq, A., and L., Sun. 2019. Identification of noncausal models by quantile autoregressions. arXiv preprint arXiv:1904.05952.

- Hecq et al. (2016) Hecq, A., Lieb, L., and S. M., Telg. 2016. Identification of mixed causal-noncausal models in finite samples. Annals of Economics and Statistics, 123/124, 307-331.

- Hecq et al. (2017a) Hecq, A., Telg, S., and L., Lieb. 2017. Do seasonal adjustments induce noncausal dynamics in inflation rates? Econometrics, 5, 48.

- Hecq et al. (2017b) Hecq, A., Telg, S., and L, Lieb. 2017. Simulation, estimation and selection of mixed causal-noncausal autoregressive models: the MARX package. Available at SSRN: https://ssrn.com/abstract=3015797.

- Hecq and Voisin (2020) Hecq, A., and E., Voisin. 2020. Forecasting bubbles with mixed causal-noncausal autoregressive models. Forthcoming in Econometrics and Statistics.

- Hencic and Gouriéroux (2015) Hencic, A., and C., Gouriéroux. 2015. Noncausal autoregressive model in application to Bitcoin/USD exchange rates. Econometrics of Risk, Springer International Publishing, 17-40.

- Jondeau and Rockinger (2006) Jondeau, E., and M., Rockinger. 2006. Optimal portfolio allocation under higher moments. European Financial Manage- ment, 12, 29-55.

- Jondeau and Rockinger (2012) Jondeau, E., and M., Rockinger. 2012. On the importance of time variability in higher moments for asset allocation. Journal of Financial Econometrics, 10, 84-123.

- Karcher et al. (2013) Karcher, W., Shmileva, E., and E., Spodarev. 2013. Extrapolation of stable random fields. Journal of Multivariate Analysis, 115, 516-536.

- Lanne et al. (2012a) Lanne, M., Luoto, J., and P., Saikkonen. 2012. Optimal forecasting of noncausal autoregressive time series. International Journal of Forecasting, 28, 623-631.

- Lanne et al. (2012b) Lanne, M., Nyberg, H., and E., Saarinen. 2012. Does noncausality help in forecasting economic time series? Economics Bulletin, 32, 2849-2859.

- Lanne and Saikkonen (2011) Lanne, M., and P., Saikkonen. 2011. Noncausal autogressions for economic time series. Journal of Time Series Econometrics, 3.

- Lanne and Saikkonen (2013) Lanne, M., and P., Saikkonen. 2013. Noncausal vector autoregression. Econometric Theory, 29, 447-481.

- Ling (2007) Ling, S. 2007. A double AR (p) model: structure and estimation. Statistica Sinica, 17, 161-175.

- Lux and Sornette (2002) Lux, T., and D., Sornette. 2002. On rational bubbles and fat tails. Journal of Money, Credit and Banking, 589-610.

- Matsushima (2013) Matsushima, H. 2003. Behavioral aspects of arbitrageurs in timing games of bubbles and crashes. Journal of Economic Theory, 148, 858-870.

- Miller (1978) Miller, G. 1978. Properties of certain symmetric stable distributions. Journal of Multivariate Analysis, 8, 346–360.

- Phillips and Shi (2018) Phillips, P. C., and S. P., Shi. 2018. Financial bubble implosion and reverse regression. Econometric Theory, 34, 705-753.

- Phillips et al. (2015) Phillips, P. C., Shi, S., and J., Yu. 2015. Testing for multiple bubbles: historical episodes of exuberance and collapse in the S&P 500. International Economic Review, 56, 1043-1078.

- Phillips et al. (2011) Phillips, P. C., Wu, Y., and J., Yu. 2011. Explosive behavior in the 1990s Nasdaq: when did exuberance escalate asset values? International Economic Review, 52, 201-226.

- Royuela-del-Val et al. (2017) Royuela-del-Val J., Simmross-Wattenberg F., and C. Alberola López. 2017. libstable: fast, parallel and high-precision computation of alpha-stable distributions in R, C/C++ and MATLAB. Journal of Statistical Software, 78, 1-25.

- ST94 Samorodnitsky, G., and M. S., Taqqu. 1994. Stable non-Gaussian random processes, Chapman & Hall, London, 516-536.

- West (1987) West, K. D. 1987. A specification test for speculative bubbles. The Quarterly Journal of Economics, 102, 553-580.

Supplementary Materials

[For Online Publication only]

Conditional Moments of Noncausal Alpha-Stable Processes and the Prediction of Bubble Crash Odds

S. Fries

Appendix A Complementary result

A.1 Existence of moments and superexponential decay of : a boundary case

As pointed after Proposition 3.1, noncausal ARMA and fractionally integrated processes whose MA coefficients decay at geometric and hyperbolic speed satisfy condition (3.5) for all (provided there are no index such that and ). Such processes hence admit finite conditional moments at least up to order . Theorem 5.1.3 by Samorodnitsky and Taqqu, Theorems 1.1, 1.2 in [Cioczek-Georges and Taqqu (1995b)] however point to the fact that intermediate cases may arise where moments are finite at most up to order for some value of such that . We propose here a noncausal MA() process with super-exponentially decaying MA coefficients which can reach any intermediate value of the boundary. Consider the noncausal process defined for all by with , , for all , and let be an i.i.d. symmetrically distributed -stable error sequence. Letting , the general term of the series in (3.5) reads for all

which is the term of an absolutely convergent series if and only if , hence if and only if

| (A.1) |

Because we assume to be symmetrically distributed, Theorems 1.1 and 1.2 in [Cioczek-Georges and Taqqu (1995b)] allow to consider (3.5) and (A.1) as sufficient and necessary conditions for the finiteness of , , in most configurations of and (see within [Cioczek-Georges and Taqqu (1995b)] for details).

In particular, one can see that for a fixed prediction horizon , the upper bound (A.1) on can lie anywhere between 0 and according to the parameter .

The smaller , i.e., the slower the decay, the higher the bound on , and conversely, the greater (faster decay), the smaller the upper bound on for the existence of conditional moments.

Furthermore, contrary to the case where decays at geometric or hyperbolic speeds, the finiteness of also depends on the prediction horizon .

Most notably, for any fixed decay speed , on can see that the bound (A.1) tends to 0 as .

For a decay parameter small enough, the moments may thus be finite up to order for short-term prediction horizons while being finite only up to order for longer-term prediction horizons.

A.2 Moments of MARMA processes : Complementary simulations and illustrations

A.2.1 Plug-in estimation of the conditional moments

The simulation experiment of Section 3.3.1 and Figure 2 illustrated the validity of the formulae of Proposition 3.1 by showing their match with model-free, data-driven non-parametric estimates of the conditional moments based on simulated trajectories. To compute the conditional moments in practice, one can now overlook the model-free nonparametric approach and resort to a parametric plug-in estimation approach based on the formulae of Proposition 3.1 as follows:

-

1.

Estimate the parameters of the stable MARMA process, for instance by -stable Maximum Likelihood [[Andrews et al. (2009)]] or M-estimation [[Wu (2013)]].

-

2.

Plug the parameter estimates in the formulae of Proposition 3.1 and compute the conditional moments.

Provided the estimators of step 1 are consistent, as is the case for the two mentioned above, the plug-in estimators of the conditional moments will also be consistent. We provide here the methodology and results of an additional simulation experiment designed to illustrate and gauge the parametric plug-in estimation of the conditional moments. Consider again that the price of an asset is modelled by a MARMA process, say the noncausal-noninvertible solution of

| (A.2) |

where is the vector of true parameter values.

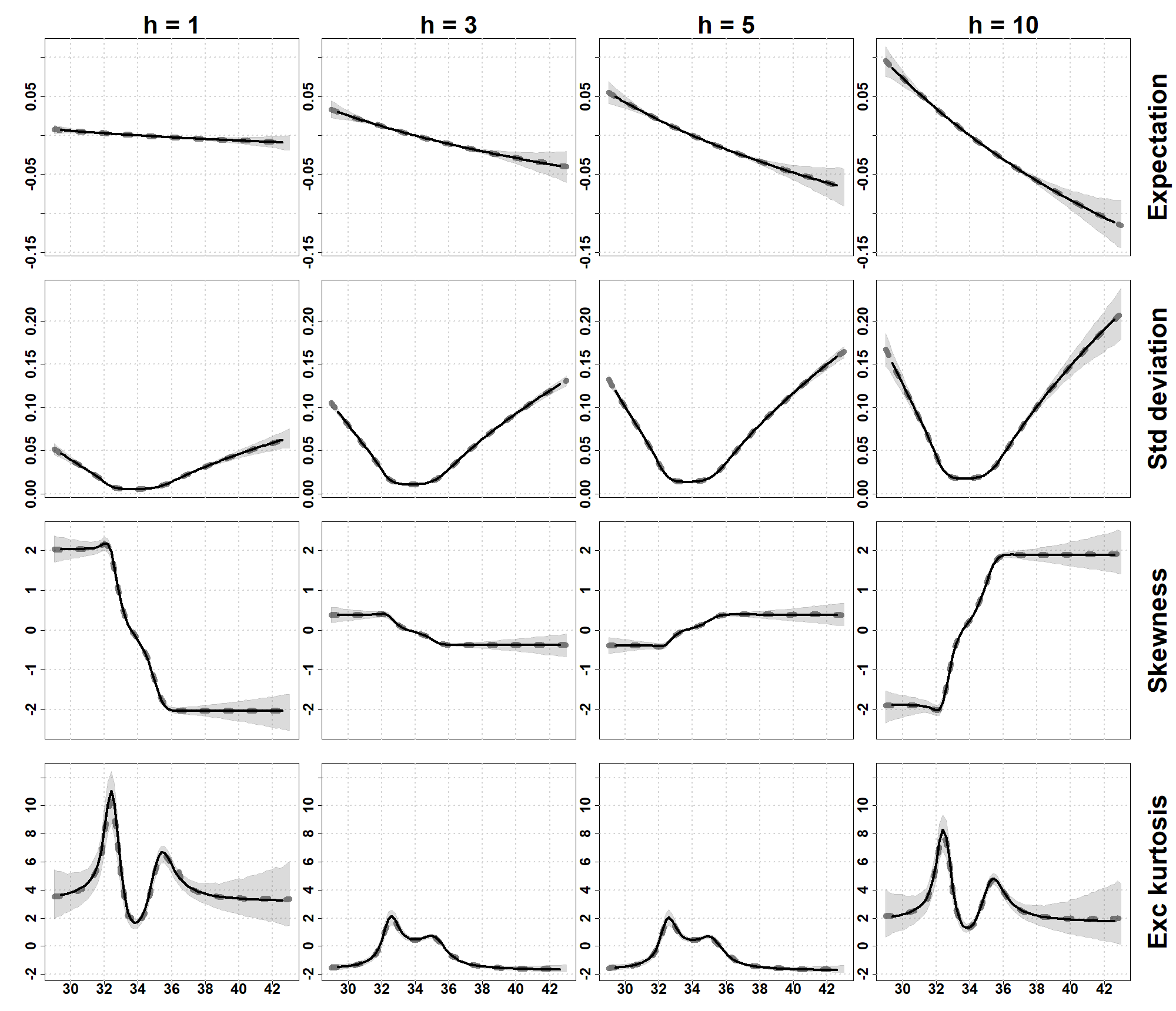

We simulate trajectories , from the above process for sample sizes and and estimate all the parameters by maximum likelihood as follows.

For any candidate vector of parameters , we follow [Wu (2013)] to compute the residuals and evaluate the likelihood.

To fix ideas, let us focus on simulation . For any given candidate vector , we compute the residuals as: first compute according to

for . Compute then the residuals backwards as

. In both steps, one can set initial (terminal) conditions, e.g., , and burn residuals close to the boundary. Based on residuals (possibly accounting for some burn), we can then compute the log-likelihood

where denotes the density of the stable distribution with corresponding parameters. For each simulated trajectory and each sample size , we compute the residuals and the likelihood by following the steps above, and we numerically find the vector of parameters minimising the log-likelihood:

The obtained estimators are then plugged in the formulae of Proposition 3.1 to compute the plug-in estimators , , , , , , of the conditional expectation, standard deviation, skewness and excess kurtosis given in (3.8). Figure 5 represents the pointwise 0.05-0.95 interquantile intervals of the plug-in conditional moments estimators across the simulations, alongside the conditional moments computed using the true values of the parameters . Three interquantile intervals appear on Figure 5, one for each sample size . It can be noticed that even for the smallest sample size, the interquantile interval is extremely narrow around most of the true conditional moments curves. For higher-order moments and at furthest horizons, the interquantile intervals are slightly larger for but narrow down fast as the sample size increases. For comparison purposes, the model-free non-parametric estimators of the conditional moments for model (A.2) have been computed following the same procedure as in Section 3.3.1 and Figure 2, using the Nadaraya-Watson estimator. The non-parametric estimators have been computed based on simulated trajectories of observations. Figure 6 represents the 0.05-0.95 interquantile intervals of the non-parametric estimator alongside the true conditional moments. When comparing Figures 5 and 6, one can notice the dramatic efficiency gain from using the parametric plug-in estimators compared to the model-free non-parametric approach. With sample sizes four orders of magnitudes smaller, the parametric plug-in approach achieves a comparable or better accuracy. Importantly, the plug-in approach is able to extrapolate well the conditional moments for conditioning values far away from the central values of the process , while the error of the model-free non-parametric approach explodes in these regions because of the scarcity of extreme-valued data points.

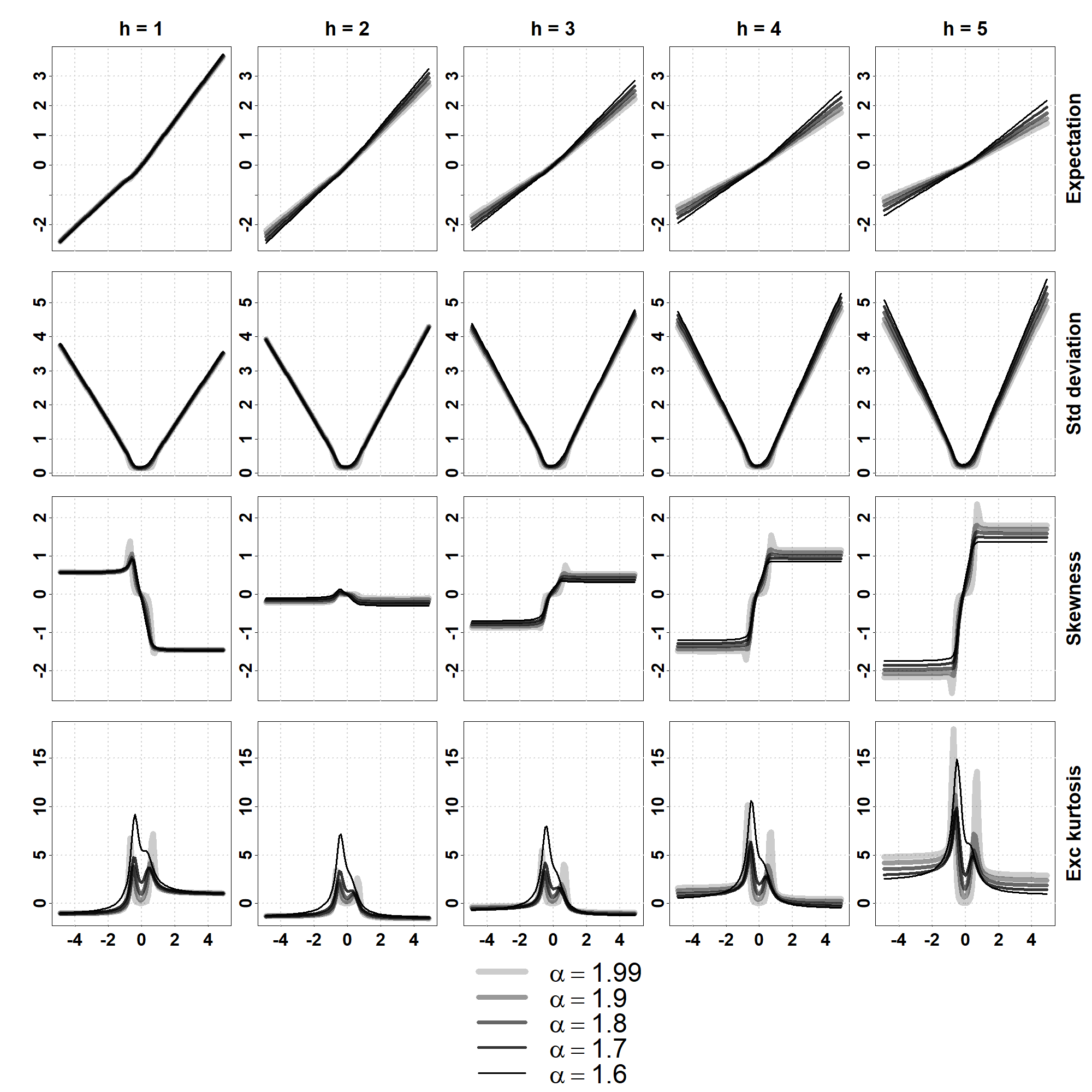

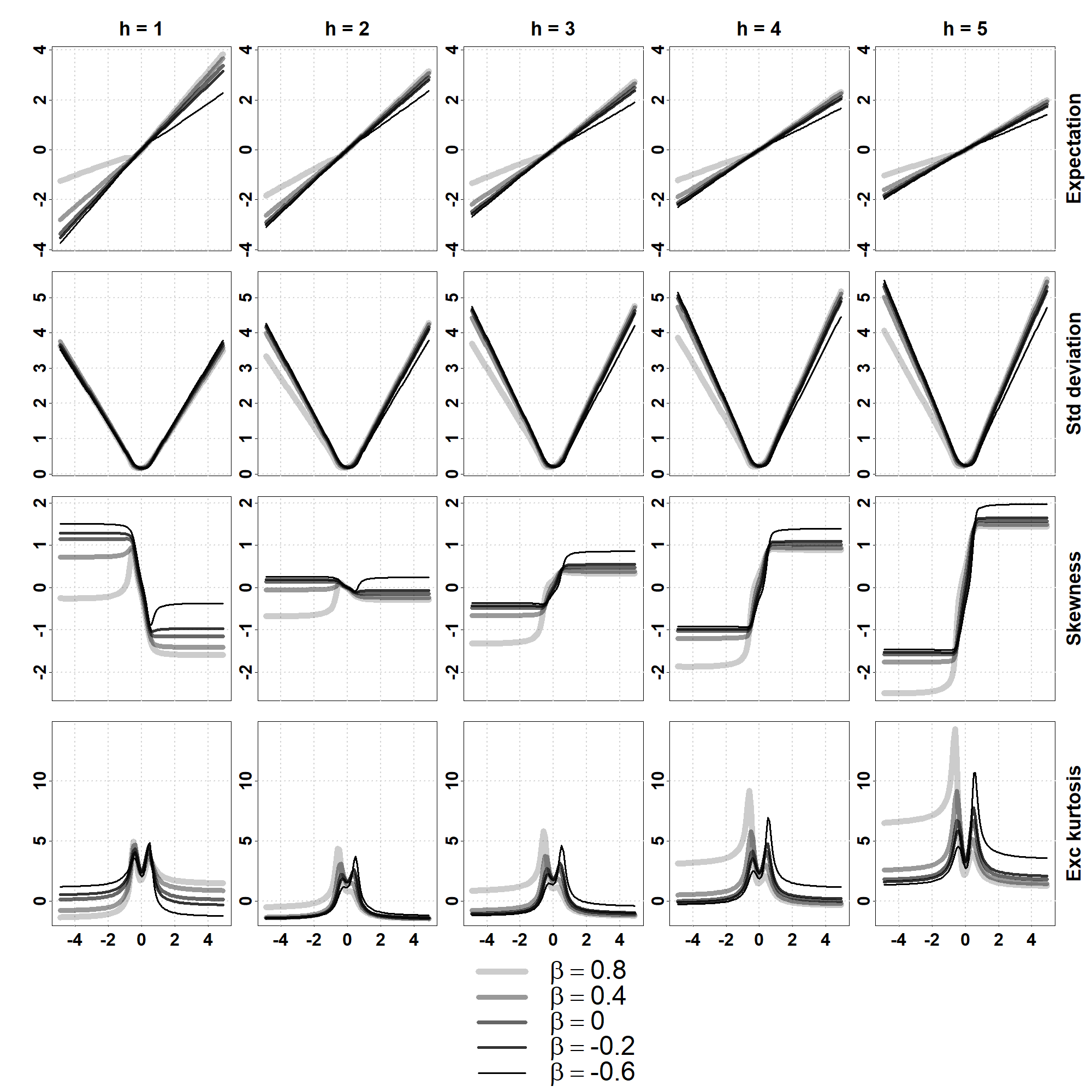

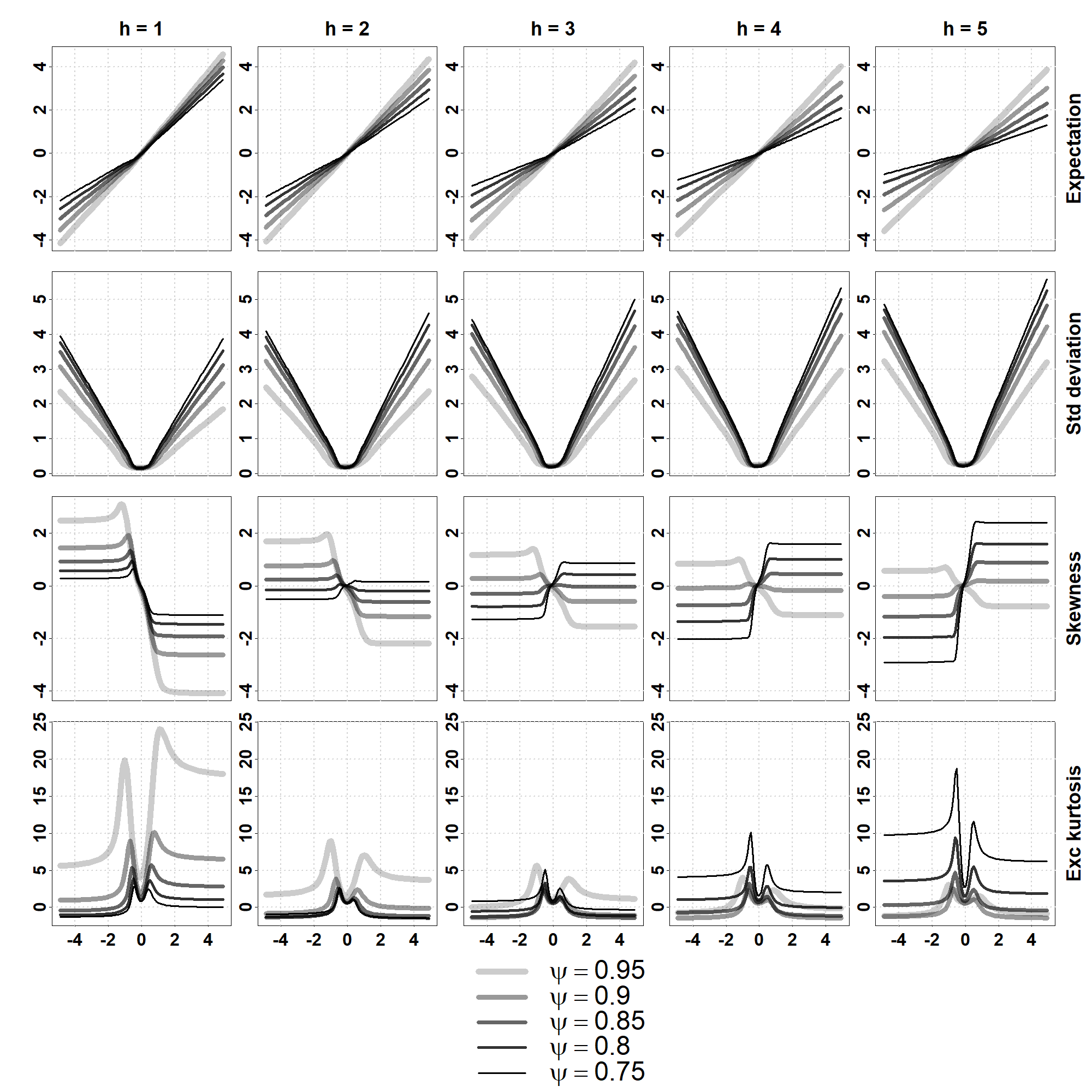

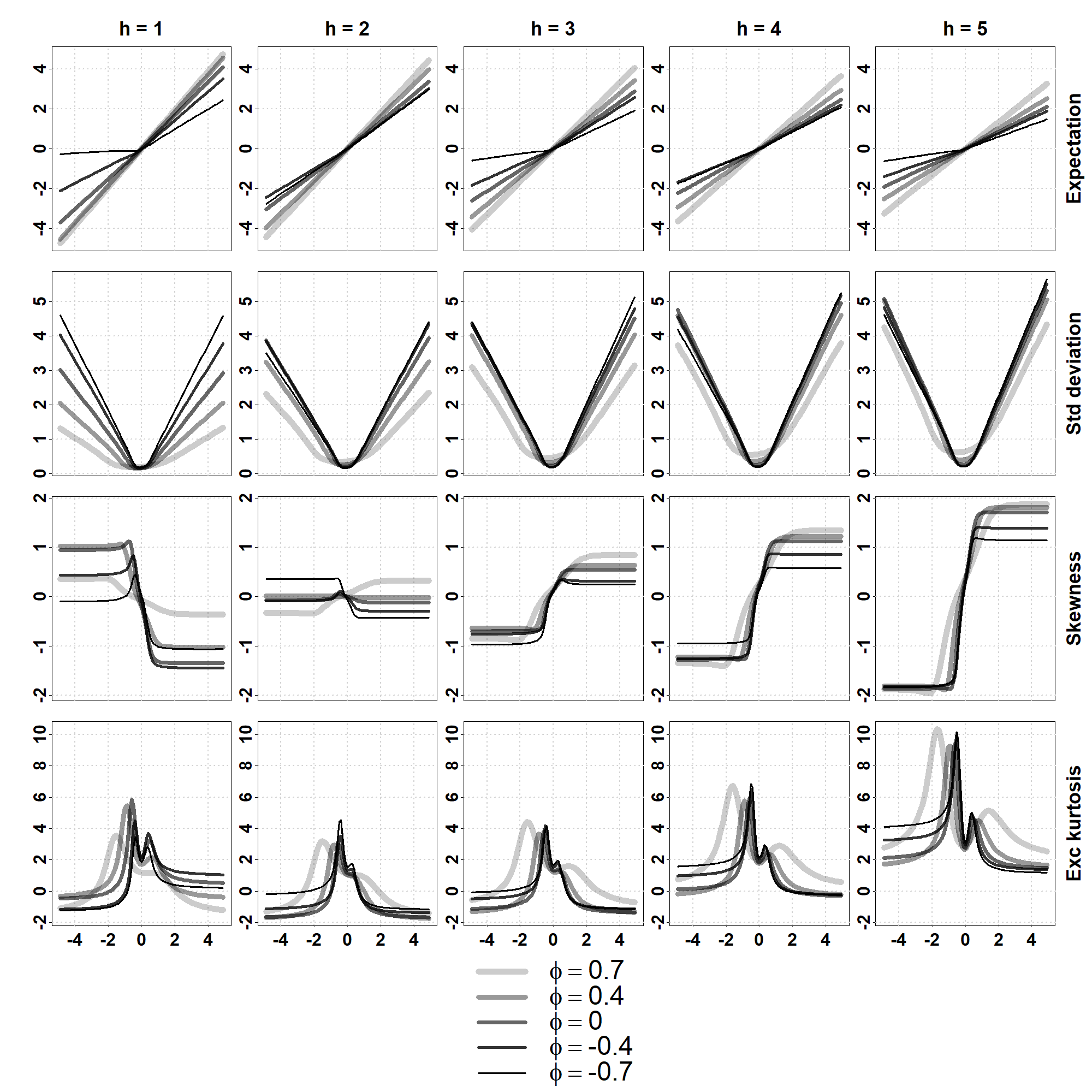

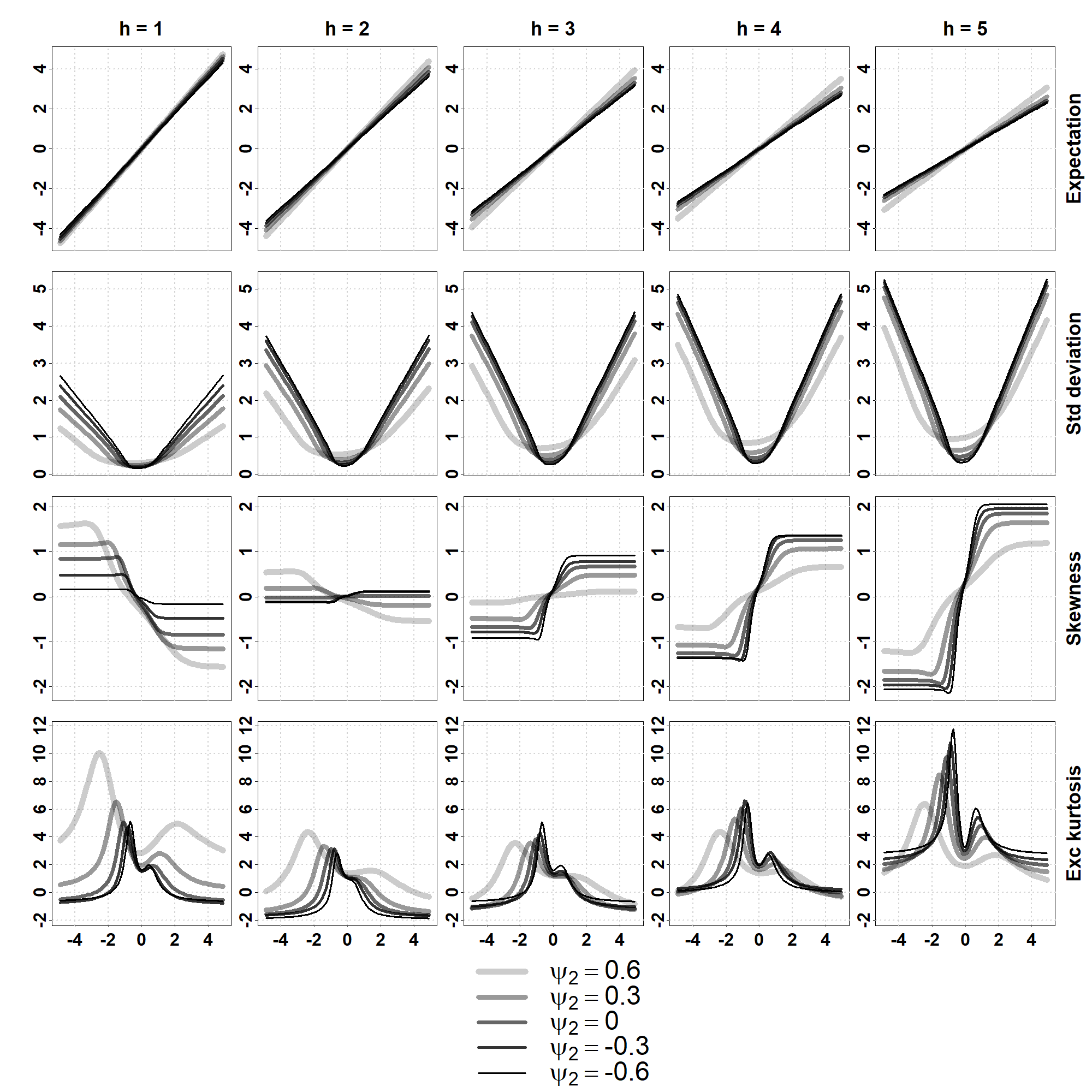

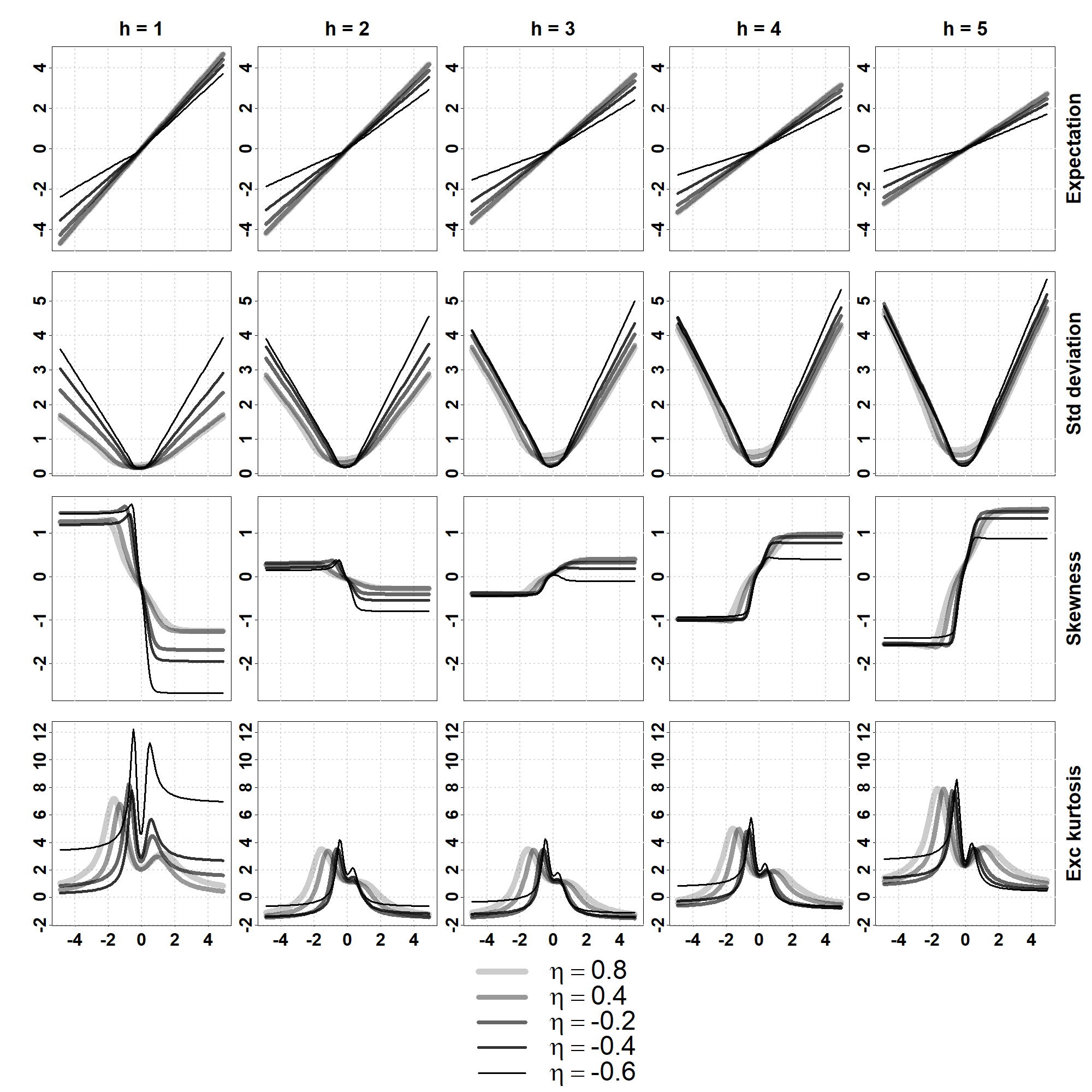

A.2.2 Illustrating the effects of parameters on the conditional moments

We provide here figures illustrating how the shape of the conditional moments of MARMA processes may be affected as we let parameter values vary. We introduce some notations and shorthands: in the rest of the section, we will denote processes solution of

as MARMA(), and processes solution of

as MARMA(). For the errors, we assume as in the previous sections that . Figures 7-12 illustrate the effects of the different parameters on the shape of the conditional moments for the two types of MARMA processes above.

Conditional expectation, standard deviation, skewness and excess kurtosis (in rows) of given , for horizons (in columns) and conditioning values (x-axis of each plot), computed using the formulae of Proposition 3.1, where is the strictly stationary solution of , , .

Conditional expectation, standard deviation, skewness and excess kurtosis (in rows) of given , for horizons (in columns) and conditioning values (x-axis of each plot), computed using the formulae of Proposition 3.1, where is the strictly stationary solution of , , .

Conditional expectation, standard deviation, skewness and excess kurtosis (in rows) of given , for horizons (in columns) and conditioning values (x-axis of each plot), computed using the formulae of Proposition 3.1, where is the strictly stationary solution of , , .

Conditional expectation, standard deviation, skewness and excess kurtosis (in rows) of given , for horizons (in columns) and conditioning values (x-axis of each plot), computed using the formulae of Proposition 3.1, where is the strictly stationary solution of , , .

Conditional expectation, standard deviation, skewness and excess kurtosis (in rows) of given , for horizons (in columns) and conditioning values (x-axis of each plot), computed using the formulae of Proposition 3.1, where is the strictly stationary solution of , , , .

Conditional expectation, standard deviation, skewness and excess kurtosis (in rows) of given , for horizons (in columns) and conditioning values (x-axis of each plot), computed using the formulae of Proposition 3.1, where is the strictly stationary solution of , , .

A.3 Real series application: robustness checks of the crash odds estimation

The crash odds estimates of Section 5 are obtained by maximum likelihood assuming -stable distributed errors. We here propose some additional empirical results assessing the robustness of these estimates to alternative assumptions on the errors and different fitting methodologies. For the Nasdaq and S&P500 series as in Section 5, we fit noncausal AR(1) models by:

-

1.

-student maximum likelihood using the function marx implemented in the R package MARX [[Hecq et al. (2017b)]]. This approach assumes -distributed errors instead of -stable.

-

2.

skewed- regression using the function selm implemented in the R package sn [[Azzalini (2018)]]. This approach assumes skewed--distributed errors instead of -stable.

-

3.

OLS estimation of the AR coefficient , followed by Hill estimation of on the residuals of the OLS step, using the function hillplot implemented in the R package evmix [[Hu and Scarrott (2018)]]. This approach does not make any fully parametric assumption on the errors, but only assumes they are heavy-tailed in the sense of Equation (4.1).

Note that in the three approaches above, the errors are power-law tailed and the results of Section 4 apply. Table 5 gathers the estimates of and , while Tables 6-7 display the survival statistics of bubbles generated by the corresponding heavy-tailed noncausal AR(1) for the Nasdaq and S&P500. One can notice that the survival statistics show similar values to those obtained in Table 4.

| Noncausal AR(1) | |||

| Nasdaq | -student | 1.22 | 0.979 |

| skewed- | 1.18 | 0.972 | |

| OLS+Hill | 1.80 | 0.988 | |

| S&P500 | -student | 2.02 | 0.987 |

| skewed- | 2.12 | 0.983 | |

| OLS+Hill | 2.50 | 0.992 | |

| Nasdaq | |||||||||||||||||||||||||

|

|||||||||||||||||||||||||

| Probability of crash within months (%) | |||||||||||||||||||||||||

| Hazard rate | 3 | 6 | 12 | ||||||||||||||||||||||

| -student | 0.025 | 2.5 | 7.4 | 14.3 | 26.5 | ||||||||||||||||||||

| skewed- | 0.033 | 3.3 | 9.6 | 18.3 | 33.3 | ||||||||||||||||||||

| OLS+Hill | 0.021 | 2.1 | 6.2 | 12.0 | 22.5 | ||||||||||||||||||||

| S&P500 | |||||||||||||||||||||||||

|

|||||||||||||||||||||||||

| Probability of crash within months (%) | |||||||||||||||||||||||||

| Hazard rate | 3 | 6 | 12 | ||||||||||||||||||||||

| -student | 0.027 | 2.7 | 7.8 | 15.0 | 27.8 | ||||||||||||||||||||

| skewed- | 0.037 | 3.7 | 10.6 | 20.0 | 36.0 | ||||||||||||||||||||

| OLS+Hill | 0.014 | 1.4 | 4.3 | 8.4 | 16.0 | ||||||||||||||||||||

Appendix B Preliminary elements for the proof of the main results

B.1 Notations for the proofs of Theorem 2.2 and Proposition 2.1

The proof of Theorem 2.2 is quite involved and relies on techniques used in [[Cioczek-Georges and Taqqu (1994), Cioczek-Georges and Taqqu (1998)]]. It consists in differentiating the conditional characteristic function of up to the fourth derivation order and evaluating the derivatives at 0 to obtain the conditional moments. Formal computation of the derivatives yields divergent terms for the third and fourth order derivatives, as well as for the second order derivative when and special manipulations are needed (in particular the <<appropriate integration by parts>> in [Cioczek-Georges and Taqqu (1994)] (p.106) as well as an additional manipulation to obtain the fourth derivative). We first introduce some notations to make the presentation of the proof as compact as possible, then provide the derivatives in Lemma B.1 and finally show Theorem 2.2 by obtaining the functional forms of the conditional moments.

Let be an -stable vector, with , , and spectral representation . Its characteristic function will be denoted for any , and reads

| (B.1) |

where for , and . As we assume so that is not degenerate, the conditional characteristic function of given , denoted for , equals

| (B.2) |

where denotes the density of . The following notation of the family function will be more handy than that in (2.4): for any and , define the function for as

| (B.3) |

For , denote also,

| (B.4) | ||||

| (B.5) |

Often, we shall invoke functions of the form

| (B.6) |

where and the ’s will be functions of the type , for , for which is well defined and positive integer exponents ’s. As a shorthand when no ambiguity is possible, we shall denote functions like (B.6) by

up to the th term.

B.2 Lemma B.1 for the proof of Theorem 2.2

Lemma B.1

Let be an -stable vector, ,, with conditional characteristic function as given in (B.2). Let . If , or if and (2.2) holds with , the first derivative of is given by

| (B.7) |

If and (2.2) holds with , the second derivative is given by

| (B.8) |