Multifractal analysis of financial markets

Abstract

Multifractality is ubiquitously observed in complex natural and socioeconomic systems. Multifractal analysis provides powerful tools to understand the complex nonlinear nature of time series in diverse fields. Inspired by its striking analogy with hydrodynamic turbulence, from which the idea of multifractality originated, multifractal analysis of financial markets has bloomed, forming one of the main directions of econophysics. We review the multifractal analysis methods and multifractal models adopted in or invented for financial time series and their subtle properties, which are applicable to time series in other disciplines. We survey the cumulating evidence for the presence of multifractality in financial time series in different markets and at different time periods and discuss the sources of multifractality. The usefulness of multifractal analysis in quantifying market inefficiency, in supporting risk management and in developing other applications is presented. We finally discuss open problems and further directions of multifractal analysis.

keywords:

Econophysics , Multifractal analysis , Financial markets , Complex systemsPACS:

89.65.Gh, 89.75.Da, 02.50.-r, 89.90.+n, 05.65.+b1 Introduction

1.1 A very brief history of econophysics

Physicists have long being interested in financial markets both practically and academically. On the investment side, Sir Isaac Newton, one of the greatest scientists in history, is reported to have invested in the South Sea Company stock in the 1720s and to have lost 20000 pounds (about 3 million US dollars in today’s money) as a result of the burst of the infamous South Sea bubble. His speculative endeavors made for the famous quote that “I can calculate the motions of heavenly bodies, but not the madness of people.” In 1991, Doyne Farmer co-founded the Prediction Company together with Norman Packard and James McGill to design automatic statistical arbitrage strategies. Prediction Company was quite successful and was sold to UBS in 2006 and was then re-sold to Millenium Management in 2013. In 1994, Jean-Philippe Bouchaud and Didier Sornette founded together a research company called Science & Finance, which was merged with Capital Fund Management in 2000. In the mean time, Sornette left Science & Finance and Bouchaud became Chairman and Chief Scientist of Capital Fund Management. Many other examples abound of physicists flirting with Wall Street, Emmanuel Derman being a role model [1].

Intellectually, there are deep relationships (as well as crucial differences) between physics and finance [2, 3] that have inspired generations of physicists as well as economists. In general, physicists apprehend financial markets as complex systems and, as such, they conducted numerous scientific investigations. In the 1930s, Ettore Majorana wrote a paper entitled “The value of statistical laws in physics and social sciences”, which was published by Giovanni Gentile Jr in 1942 after his disappearance [4], and its English translation by Mantegna was presented in the journal of Quantitative Finance in 2005 [5]. In the 1960s, Benoit B. Mandelbrot pioneered an empirical approach, which would be later viewed as a precursor of econophysics, in a series of seminal works of income distributions [6, 7, 8, 9, 10], price variation distributions of speculative assets [11, 12], and long-term correlations in financial and economic time series using the rescaled range (R/S) analysis [13, 14].

The current flourishing econophysics has multiple seeds that date from the 1990s. One can identify four main directions of research that are among the most actives in the field of econophysics in the past two decades. Following Mandelbrot’s ideas, the first stream of studies focused on the distribution of financial returns, as well as conceptual formulations. In 1991, Rosario Mantegna studied the Lévy-walk-like superdiffusive behavior of indices of the Milan stock exchange [15], and with Gene Stanley the scaling behavior of the S&P 500 index in 1995 [16, 17]. In 1996, Ghashghaie et al. studied the evolving return distributions at different timescales and the multifractal behavior in the structure function of the US dollar - German mark exchange rates [18]. In 1998, Laherrère and Sornette proposed stretched exponential distributions for time series in nature and economy as a complement to the often used power-law distributions [19], while Gopikrishnan et al. observed the inverse cubic law [20, 21, 22]. We note that, compared with power laws, stretched exponentials [23, 24, 25] and lognormals [26] are competing alternatives for return distributions that share hard-to-distinguish tail properties.

A second stream was devoted to the macroscopic modelling of financial markets. In 1994, Bouchaud and Sornette generalized the Black-Scholes option pricing problem for a large class of stochastic processes [27] using the functional integration and derivative approach well-known in field theory. In 1996, Sornette et al. proposed the log-periodic power-law singularity (LPPLS) model to study financial crashes modelled as critical events [28],. This approach was soon exploited further by Sornette and Johansen [29, 30], Feigenbaum and Freund [31, 32], Vandewalle et al. [33, 34], Drożdż et al. [35], Sornette and Zhou [36, 37, 38, 39] and many others. Identification of financial bubbles and forecasting of market turning points advanced successfully in diverse markets [40, 41, 42].

The third stream is concerned with computational econophysics. In 1992, Takayasu et al. [43] developed the first agent-based model in econophysics with the goal to provide an alternative to dynamical stochastic general equilibrium (DSGE) models by incorporating agents’ heterogeneous characteristics and the role of extended networks. In 1994, Palmer et al. designed an artificial stock market model composed of adaptive agents with bounded rationality [44]. In 1996, Bak et al. introduced a multi-agent model based on diffusion and annihilation [45]. In 1997, Challet and Zhang introduced the minority game [46]. In 1999, Lux and Marchesi proposed an agent-based model with heterogenous chartists and fundamentalists [47]. In general, there are three basic ingredients for the price formation process in financial markets, including global news that influence more or less all market participants, mutual imitations among traders, and idiosyncratic preferences of traders [48, 49]. Overconfidence of traders in interpreting the predictive power of global news, which mis-attributes the success of news to predict returns to traders’ own stock picking ability and leads to positive feedbacks and herding behavior, plays a crucial role in generating the main stylized facts [48, 49, 2], such as the fat-tailed distribution of returns, the absence of linear correlations in returns, the long memory in volatilities, and the multifractal nature of financial time series.

A four stream of investigations has been involved in the more recent use of the emerging field of network theory applied to finance. In 1999, Mantegna studied the hierarchical structure of the US stock market from the angle of minimal spanning trees [50]. Laloux et al. and Plerou et al. applied random matrix theory to stock return correlation matrices to identify the information contents hidden in eigenvalues and their corresponding eigenvectors [51, 52, 53].

1.2 Stylized facts

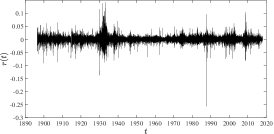

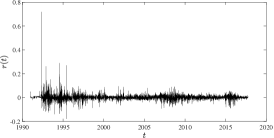

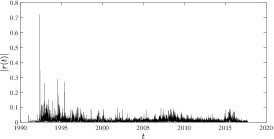

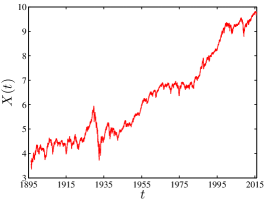

Financial markets are complex adaptive systems, in which universal and non-universal statistical laws emerge at the macroscopic level from the microscopic behavior of heterogeneous traders through reactions to external stimuli in a self-organized manner [54, 55, 40, 41, 56, 57, 58, 59]. These laws can be explored from the rich dataset of financial stock market price time series. As an illustration, the left pannel of Fig. 1 shows the daily price trajectories of two stock market indices, the Dow Jones Industrial Average (DJIA) index from 26 May 1896 to 29 December 2017 and the Shanghai Stock Exchange Composite (SSEC) index from 19 December 1990 to 29 December 2017. These two stock markets are representative of developed and emerging markets that are of great interest. The logarithmic return of over a time interval is defined by

| (1) |

The middle panel of Fig. 1 illustrates the daily return time series with day and the right panel shows the corresponding volatility time series. Here, the volatility for a given day is defined as the square root of the sum of the squares of intraday returns of that day, where the intraday time scale needs to be sufficiently short (say 1 minute) to provide a good convergence of the volatility estimator. Clear bursty behaviors can be observed in the return time series, which are associated with volatility clustering.

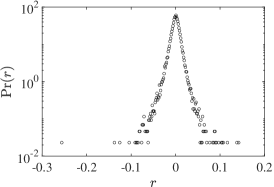

Numerous statistical regularities or stylized facts have been reported in different financial markets [60, 61, 62, 63]. We first recall three main stylized facts, which are universal properties of financial markets. The first stylized fact is the fat-tailed distributions of financial returns. The form of the distribution of asset price fluctuations plays crucial roles in asset pricing and risk management [54, 55, 25]. Early empirical and theoretical works argued that asset prices follow geometric Brownian motions [64, 65], which is the main assumption of the Black-Scholes option pricing model [66]. In the 1960s, Mandelbrot suggested that incomes and speculative price returns follow the Pareto-Lévy distribution, which has power-law tails

| (2) |

whose exponents claimed to be in the domain of attraction of stable Lévy laws [6, 7, 10, 9, 11]. Recall that Lévy laws generalise the Gaussian distribution, and their family exhausts all possible distributions that are stable under convolution, with no or only weak dependence between the random variables.

The possibility that financial returns might be distributed according to Lévy laws rather than being Gaussian immediately attracted the interest of notable financial economists, such as Fama [67], Fama and Roll [68], Samuelson [69], Sargent [70], and others. But there was also immediate resistance to abandon the statistical theory that exists for the normal case, which was non-existent for the other members of the Lévy laws, with the like of Cootner [71] and Granger and Orr [72] opposing strong arguments. Further in-depth studies concluded to the error of Mandelbrot, in the sense that, while the distributions of returns are fat-tailed, they are not so heavy as to be described by Lévy laws: more and more statistical tests brought increasing and unavoidable evidence that the variance of the return is not infinite (and thus the exponent is larger than ), thus irremediably excluding the heavy tail regime of Lévy laws with tail exponent less than [73, 74, 75, 76]. The tools based on variance and covariance could still be used after all. This led to a lull in the interest of fat-tailed distributions, which was interrupted by the re-discovery by econophysicists in the early 1990s [15, 16, 17].

More recent empirical investigations with more data converge to (or more prudently that ) [20, 21, 22]. Further empirical investigations have been conducted on financial returns at different time scales and reported that distributions vary from exponential to stretched exponential to power law [19, 77, 78, 79, 80, 81, 82, 83, 84, 85, 86, 87, 88, 89, 90, 91, 92, 93, 94]. These observations are in agreement with the fact that the fat-tailed nature of the distributions of returns at small scale with implies that the domain of attraction at large scales is the Gaussian distribution. One should thus observe and we do observe a progressive transition from a power law like regime at small time scales to a Gaussian regime at large scales [18]. Note that the stretched exponential distribution serves as a convenient bridge between exponential and power-law distributions [19, 95]. In fact, the power law family of distributions can be shown to be asymptotically nested in the stretched exponential family, the later converging to the former in the limit of vanishing stretched exponential exponent [23, 24, 25]. This apparently esoteric property is very useful practically as it provides the robust Wilks test to compare power laws and stretched exponentials for any data set of interest.

As illustrations of the above, the left column of Fig. 2 shows the empirical distributions of daily returns of the DJIA and SSEC indices. There are evident fat tails and outliers, compared with the inverted parabola shape that would be expected under the Gaussian hypothesis.

Two other main stylized facts are the absence of long memory in returns and the presence of long memory in volatility, as shown respectively in the middle and right panels of Fig. 2. Quantitatively, performing detrended fluctuation analysis or detrending moving average analysis of the return and volatility time series allows one to obtain the corresponding Hurst exponents.

1.3 Benchmark econometric models

In econometric finance, there are several cornerstone models, such as the autoregressive conditional heteroskedasticity (ARCH) model [96], the generalized autorregressive conditional heteroskedasticity (GARCH) model [97], the exponential GARCH (EGARCH) model [98], the integrated GARCH (IGARCH) model [99], the fractionally integrated generalized autoregressive conditional heteroskedasticity (FIGARCH) model [100], and the autoregressive fractionally integrated moving average (ARFIMA) model [101, 102].

An autoregressive model of order , AR(), is defined as

| (3) |

where are the parameters of the model, is a constant, and is white noise. To model a financial time series using an ARCH process [96], the error term is split into a stochastic piece and a time-dependent standard deviation such that

| (4) |

The random variable is a strong white noise process. The series is modelled by

| (5) |

where and for .

Considering a regression with coefficient between a variable and , the GARCH model of the residuals is given by [97]

| (6) |

where is the order of the GARCH terms and is the order of the ARCH terms . In finance, one usually applied the GARCH model to the return time series formulated as (4) with given by (6).

In the ARCH, GARCH and EGARCH models, the autocorrelation of volatility decays at exponential rates. In contrast, the volatility of the integrated models has long memory. Empirical analyses show that GARCH-type models without long memory in volatility can hardly capture the multifractal nature in financial time series, while other models with long memory component can capture partly the apparent multifractality, which is however spurious by definition of the integrated models [103, 104, 105, 106, 107, 108, 109, 110, 111, 112]. Therefore, benchmark economic models fail to capture an important dimension of market complexity, namely the multifractal nature of financial market [113, 114].

1.4 Introduction to multifractality

Multifractality has been observed in many diverse complex systems [115, 116, 117, 118, 119, 120, 121], including financial markets [113]. The term “multifractal” was coined by Frisch and Parisi in 1983 [122], as confirmed by Benoit B. Mandelbrot [123], who is the well respected Father of Fractals [124]. The concept of multifractality can be traced back to Novikov [125] and Mandelbrot [126, 127] in their study of turbulence in fluid mechanics. On the other hand, two groups led by Grassberger and Procaccia generalized the fractal dimension, the information dimension and the correlation dimension into a unified expression of generalized dimensions through the Rényi entropy [128, 129, 130], with the initial aim of describing strange attractors in nonlinear dynamics [131]. Halsey et al. also made seminal contributions in the early development of multifractal theories, with applications to fractal growth processes [132].

There are two equivalent descriptions of multifractals, i.e., via the function or the function , where is the order of certain moments, is the mass exponent function, is the singularity strength, and is the singularity spectrum. These two representations are related through the Legendre transform [122, 132] such that

| (7a) | |||

| and | |||

| (7b) | |||

Concerning the representation, there are two additional equivalent functions and . The function presents the generalized dimensions that are determined by

| (8) |

while is defined by

| (9) |

and corresponds to the generalized Hurst exponents. The detailed meaning of these quantities and there relations will be made clear later.

In the study of turbulence, there are two classical methods for the analysis of multifractals, i.e., the structure function approach and the partition function approach [133, 134, 125, 126, 127, 135, 122, 136]. Due to the striking similarities between turbulence and financial markets, though the analogy has its limitations [137], the multifractal nature of financial time series has attracted much interest [18, 17]. The structure function approach dominated in the first wave of multifractal analysis in econophysics [138]. Since the seminal work of Kantelhardt et al. in 2002 [139], the multifractal detrended fluctuation analysis soon became the dominant method not only for financial time series but also for other time series. In 2008, Podobnik and Stanley introduced the detrended cross-correlation analysis for non-stationary time series [140], which was extended by one of us (Wei-Xing Zhou) to analyze multifractal time series [141]. These milestone works triggered the third wave of simultaneous multifractal analysis of two time series and the invention of many variant types of multifractal analyses.

In financial markets, risk is a central concept in all financial activities. Large financial fluctuations, especially finance “tsunamis” such as the one that broke out in 2008 [42], usually cause tremendous economic distress and are followed by vigorous changes in risk perception and regulations [40, 41]. Identifying, measuring and forecasting financial risks are of great theoretical and practical significance in risk management. Econophysicists have shown that multifractal analysis provides an alternative way in studying market risks. Indeed, large singularity strengths qualify the behavior of small fluctuations, while small singularity strengths characterize large fluctuations. Therefore, quite a few efforts have been made to apply multifractal analysis to quantifying market inefficiency, measuring financial volatility, and so on.

This review provides an extensive survey of the multifractal analysis of financial time series. We start with different methods of multifractal analysis for univariate and multivariate time series in Section 2 and Section 3. We review also the methods that were invented in other fields, because they have potential application value in econophysics. We discuss important mathematical and econophysical models in Section 4 that can deepen our understanding of the multifractal nature of financial markets. Important properties and subtle issues associated with the algorithms used in empirical multifractal studies are discussed in Section 5, many of which are often overlooked by researchers leading to unreliable results. In Section 6, we give an extensive survey of the literature on empirical multifractal analysis of financial time series, which overall confirms the presence of multifractality in financial markets. We raise in Section 7 the important issue of apparent and effective multifractality and discuss different sources causing apparent multifractality. Different applications of the multifractal nature of financial time series are reviewed in Section 8. We discuss open problems and provide perspectives for future research in Section 9.

Although this review focuses on the multifractal analysis of financial markets, most of its contents are suitable for multifractal time series analysis in all other fields. Moreover, a large part of this review can be usefully read to inspire multifractal analyses of measures on surfaces and in higher dimensional spaces.

2 Multifractal analysis

2.1 Partition function approach (MF-PF)

2.1.1 Generalized dimensions and mass exponents

Consider a measure embedded in a geometric support , whose density is at position . By definition, . The measure in the neighbourhood of is . Using the idea of the classic box-counting method [124], we cover the geometric support using boxes of size . The integrated measure in the th box is

| (10) |

where for any . The fractal dimension of can be determined as follow

| (11) |

where the term gives the number of non-empty boxes needed to cover the support . Note that fractal dimension is also called similarity dimension or capacity dimension. It is obvious that, if there is no measure distributed in a box, the box should not be counted. In most cases in handling financial time series, we have . In the empirical determination of , we plot against in log-log scales and the slope of the linear part in a proper scaling range is regarded as its estimate.

The information entropy or Shannon entropy of the measure can be defined as [142, 143]

| (12) |

and one can define the information dimension as follows

| (13) |

which was introduced by Balatoni and Rényi in 1956 [144, 145] and used to study strange attractors [146, 147].

A third index used to characterize the measure is the correlation dimension [148, 149]. The correlation dimension was originally introduced to study the scaling behavior of the correlation integral of time series of length :

| (14) |

where is the Heaviside function. The correlation dimension is defined as follows

| (15) |

These three dimensions , and can be unified into one framework of generalized dimensions [129, 128, 130]. We define the -order Rényi entropy as [150, 151]

| (16) |

and the generalized dimension as [152]

| (17) |

where

| (18) |

is the -order partition function of the measure. It is easy to verify that , and . In practice, we can compute according to Eq. (17). For a given , we plot against for various box sizes and perform linear regression in a proper scaling range to obtain the slope .

We can rewrite Eq. (17) as follows

| (19) |

or

| (20) |

where

| (21) |

In practice, we can compute according to Eq. (20). For a given , we can compute for various box sizes and perform a linear regression of against in a proper scaling range to obtain . Alternatively, can be transformed from using Eq. (21).

Recently, Xiong and Shang proposed a variance-weighted partition function approach and established the relationship between the corresponding multifractal functions [153]. Numerical simulations show that the variance-weighted partition function approach performs comparatively as the standard partition function approach.

2.1.2 Scaling behavior of partition functions

Based on the box-counting idea, the geometric support is partitioned into non-overlapping boxes of size . The local singularity strength in the th box is defined according to the following relationships [132]:

| (22) |

which may differ for different boxes. Let denote the number of boxes in which the singularity strengths are within . Hence, the fractal dimension of the set is determined according to

| (23) |

where is the density of the singularity strength and is the fractal dimension of the boxes under consideration [132], which is usually called multifractal spectrum or singularity spectrum. One can directly obtain from Eq. (22) and from Eq. (23) using local and pointwise singularity methods [154, 155, 156].

Inserting Eq. (22) into the partition function (18) and rewriting the sum into an integral over , we have

| (24) |

Assume that is nonzero and non-singular. It therefore contributes a constant proportional factor to the leading behavior of the integral. Because is small, according to the method of steepest descent, the integral will be dominated by the value of that makes the power smallest. We thus replace by , which is defined by the extremal condition:

| (25a) | |||

| and | |||

| (25b) | |||

Then, Eq. (24) becomes

| (26) |

It follows from Eq. (25b) that

| (27a) | |||

| and | |||

| (27b) | |||

which means that the multifractal spectrum is a concave function and its slope at point is .

Comparing Eq. (20) and Eq. (26), we have

| (28) |

Taking the derivative of Eq. (28) with respect to , we have

| (29) |

| Rewriting Eq. (28) and Eq. (29), we have | |||

| (30a) | |||

| and | |||

| (30b) | |||

This shows that is the Legendre transform of [122, 132]. Therefore, after obtaining , we can determine numerically using Eq. (30a) and using Eq. (30b). To qualify a multifractal measure, we can use either or , which are equivalent.

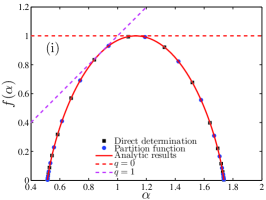

2.1.3 Direct determination of a multifractal spectrum

From the canonical perspective, we can obtain the function directly [157, 158]. We can define the canonical measures

| (31) |

The singularity strength and its spectrum can be computed by linear regressions in log-log scales using the following equations:

| (32a) | |||

| and | |||

| (32b) | |||

To compute , we can plot against , determine the scaling range and obtain the slope by linear regression. The function can be determined similarly based on Eq. (32b). Combining Eqs. (20) and (32b), we can verify Eq. (28) easily. The mass exponent function can be obtained by using Eq. (28).

2.1.4 Inverse partition function and inversion formula

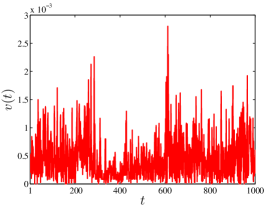

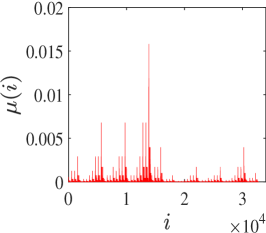

For financial volatilities, we can further define the inverse partition function [159]. We start with an illustration of the partition function approach using a high-frequency volatility time series.

Denote the price time series of a financial asset. The logarithmic return at the finest time resolution is calculated by

| (33) |

where . The absolute return is utilized as a proxy for volatility according to

| (34) |

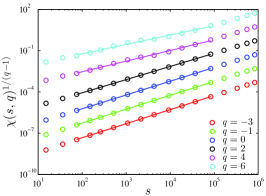

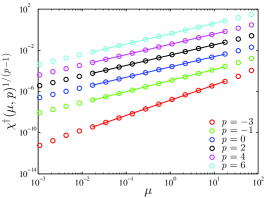

Figure 3(a) illustrates a segment of the 1-min volatility time series of the S&P 500 index, in which, according to the partition function method, the original volatility time series is divided into boxes with identical size . The box sizes are chosen such that the number of boxes of each size is an integer to cover the whole time series.

We define the continuous volatility measure for any by

| (35) |

where . The cumulative function of the volatility measure is obtained as

| (36) |

The function of in Fig. 3(a) is presented in Fig. 3(b). The measure in each box of size is determined by

| (37) |

which is also illustrated in Fig. 3(b). Usually, one computes the measure in a discrete way,

| (38) |

in which must be an integer to avoid edge effects (see Section 5.1.2 for more information). When the continuous measure is used, more choices for values are possible as can be any integer.

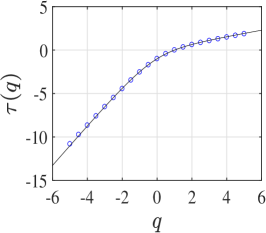

For a given order , the direct partition function can be estimated by using

| (39) |

In Fig. 3(d), we plot as a function of for different ’s. The scaling exponent function can be obtained through power-law regressions to the data points in the scaling range, which spans about three orders of magnitude. We find from Fig. 3(f) that is a nonlinear function of , confirming the presence of multifractality in the volatility measure.

We now turn to investigate the inverse partition function. For each threshold , a sequence of exit times can be determined successively by

| (40) |

where is an integer. Graphically, Fig. 3(c) shows how the exit times can be determined. The inverse measure is defined as the normalized exit time

| (41) |

and the inverse partition function can be determined as follows:

| (42) |

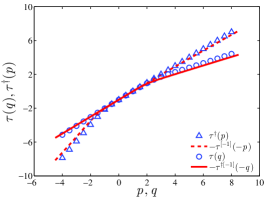

Figure 3(e) shows the dependence of as a function of the thresholds for different values. Power-law scaling can be observed over about three orders of magnitude:

| (43) |

The scaling exponent function can be obtained through power-law regressions to the data points in the scaling range, as is shown in Fig. 3(f). The nonlinearity of the function confirms the presence of multifractality in the exit time measure.

An important issue arises concerning the relationship between and . Mandelbrot and Riedi proved an elegant inversion formula mathematically for both discontinuous and continuous multifractal measures [160, 161]. Roux and Jensen independently proved the exact relation between the direct and inverse scaling exponents for the classical binomial measures [162]. Xu et al. provided a simple “proof” of the inversion formula for multinomial measures [163], which is presented below.

Let be a probability measure on with its integral function . Then its inverse measure can be defined by

| (44) |

where is the inverse function of . If is self-similar, then the relation holds, where the ’s are similarity maps with scale contraction ratios and with . The multifractal spectrum of measure is the Legendre transform of , which is defined by the generating function

| (45) |

It can be shown [160, 161] that the inverse measure is also self-similar with ratio and , whose multifractal spectrum is the Legendre transform of , which is defined implicitly by

| (46) |

It is easy to verify that the following inversion formula holds

| (47) |

Two equivalent testable formulae follow immediately

| (48) |

where the superscript denotes the inverse function operator. Figure 3(f) verifies that the inversion formulae (48) hold for the high-frequency volatility time series of the S&P 500 index [159].

We can also relate the direct and inverse singularity strengths and the direct and inverse singularity spectra. From Eq. (47), we have

| (49) |

Combining Eq. (47), Eq. (49) and the Legendre transform, we have

| (50) |

Rigorous proofs of these results can also be found in Refs. [160, 161]. It is easy to obtain the relation between direct and inverse generalized dimensions [164]:

| (51) |

where is the inverse generalized dimension function.

2.1.5 Ensemble averaging

In the multifractal analysis of financial time series, almost all studies with very few exceptions focused on individual time series. One can further investigate an ensemble of financial time series of individual assets [165]. Ensemble averaging was developed to determine the multifractal dimensions of Diffusion-Limited Aggregations [166, 167, 168, 169, 170], and unearthed a subtle discrete hierarchy quantified by complex fractal dimensions [171].

One defines the quenched and annealed mass exponents and as follows,

| (52) | ||||

| (53) |

where the angular brackets signify the ensemble average over all time series. The annealed exponents are more sensitive to rare samples of the ensemble with unusual values of , while the quenched exponents are more characteristic of typical members of the ensemble [172].

The reasoning under the ensemble averaging lies in the consideration that one performs the measurement many times of the dynamics of an “ensemble” of financial instruments. The ensemble averaging method provides an alternative way to measure market risks from individual equities other than the market index. It is also different from directly averaging the risk measures of many individual equities. In addition, although the method was initially developed for the partition function approach, its extension to other multifractal analysis methods is straightforward.

2.2 Structure function approach

2.2.1 Direct structure functions (MF-SF)

Another important statistical quantity of turbulent fields is the structure function of velocity increments [133, 134]. Classical experiments have been carried out to measure the structure function and its nonlinear scaling behaviors [135]. Such nonlinear scaling behavior is also termed as multifractality [136, 122]. The structure function approach has been also employed to investigate financial time series [173, 18, 138]. The th-order structure function is also called the th-order height-height correlation function in the literature [174, 175].

Consider a time series . The increments or innovations over time scale are defined as

| (54) |

For financial assets, is the logarithmic price and is the return over the time interval of duration . The th-order structure function is defined as the th-order moment of the increment distribution:

| (55) |

We stress that for time series in turbulence [135], finance [176, 138], and other fields, because can be zero such that the moments of negative orders are not defined. When , we have , which is independent of the scale . When , is proportional to the autocorrelation function [176, 138].

For self-similar time series, we expect to have

| (56) |

where is the generalized Hurst exponent. The scaling function is obtained as [177]

| (57) |

When , we have

| (58) |

In practice, for each fixed , we calculate the values with varying values and perform a linear least-squares regression of against in a properly chosen scaling range to obtain and . It follows that

| (59) |

We can further determine the singularity function and the singularity spectrum through the Legendre transform. When is monofractal, is a constant. When has a multifractal nature, decreases with .

According to the definition of , we have

| (60) |

where is the sum for with . Denote the proportionality coefficient of the scaling relation (56). It is obvious that . Combining Eq. (56) and Eq. (57), we have

| (61) |

Let . We have when and when .

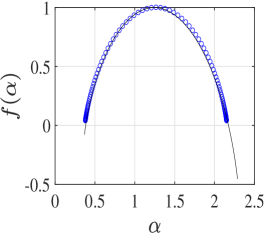

Figure 4 presents the results of the multifractal analysis of the daily time series of the logarithmic price of the Dow Jones Industrial Average index (DJIA, 1896-2015) based on the structure function approach.

In a seminal study [173], Müller et al. presented a statistical analysis of financial data documenting scaling laws in the form of Eq. (56) for and , though they did not mention “multifractal”, “multiscaling” or “structure function”. Their analysis included intra-day prices over 3 years and daily prices over 15 years of four foreign exchange spot rates (DEM/USD, JPY/USD, CHF/USD, USD/GBP) and intra-day prices over 3 years of gold (XAU/USD). Similar analyses for the first- and second-order moments have been adopted by other economists [178].

2.2.2 Multifractal fluctuation analysis (MF-FA)

The method of fluctuation analysis is a classical approach to extract the Hurst exponent of time series [179], which has been applied extensively in econophysics [180, 181, 182, 183, 184]. The fluctuation function can be calculated as follows,

| (62) |

where is the fluctuation analysis (FA) exponent, i.e. approximatively the Hurst index. A value of the Hurst exponent larger than means that the time series is correlated, For , the time series is anti-correlated, and for , it is uncorrelated.

One can extend the fluctuation analysis in equation (62) to higher orders as follows [185, 186, 187],

| (63) |

which enables us to understand the multifractal nature in the dynamics of markets. The relationship between the scaling exponent and the generalized Hurst exponent can be described by Eq. (57). When , is the Hurst exponent presented in Eq. (63). Using the Legendre transform, we can obtain the singularity strength and its spectrum .

2.2.3 Inverse statistics and inverse structure functions

Analogous to the inverse measure in the partition function approach [188, 161], Jensen [189] investigated the moments of exit time or first passage time. For a given increment , using definition (54), the exit time scale at time is defined by

| (64) |

which is the minimal time needed for the fluctuation to exceed the threshold . The first passage time has important usage in finance. For instance, Cho and Frees adopted it to construct an asymptotically unbiased volatility estimator [190]. They argued that the natural volatility estimator focuses on how much the price changes, whereas the “temporal” estimator based on the first passage time focuses on how quickly the price changes [190]. The inverse statistics have also some connections to the persistence probability [191, 192, 193, 194]. The variable and derived quantities have natural interpretations in finance, such the “time to recovery” after a drawdown and are part of metrics used in a standard way in evaluating performance of financial strategies and hedge-funds. This explains that inverse statistics have been extensively applied in finance, as well as in other fields like in the study of heart beat rate and cardiac diseases [195].

If is a Brownian motion, the distribution of is solved analytically as a Gamma distribution [196, 197]:

| (65) |

where is proportional to . Since asset prices are not Brownian motions, Simonsen et al. [198] proposed a generalized shifted Gamma distribution

| (66) |

which has a power-law tail . The Gamma distribution in Eq. (65) is recovered if , , and . They analyzed the wavelet filtered logarithmic daily closing prices of the DJIA (26 May 1896 to 5 June 2001) and found that the distribution (66) with fits the data well. This observation seems quite ubiquitous for uniformly spaced time series of indices and stocks in different markets [199, 200, 201], although there are studies reporting that can deviate from 0.5 [202, 203]. For tick-by-tick data at the transaction level, the tail exponent can be larger than 0.5, as found for five highly liquid stocks (AstraZeneca, GlaxoSmithKline, Lloyds TSB Group, Shell, and Vodafone) in the electronic market (SETS) of the London Stock Exchange (LSE) during the year 2002 [200] and the foreign exchange rate of DEM against USD for the full year of 1998 () [204].

Simonsen et al. [198] argued that the most probable first passage time is the optimal investment horizon and found that scales with as a power law,

| (67) |

where , deviating from for Brownian motions. It is found that holds for regularly spaced samples in most markets and the value is larger in developed stock markets than emerging markets [199, 205]. For tick-by-tick data that are unevenly sampled, it was reported that [206].

For asset prices, it is natural to also consider the minimal time needed for the price to depreciate by a certain return . Then, the exit time at time is defined by [207]

| (68) |

A lot of research has shown that the optimal investment horizon is longer for gains than for losses, which is termed the gain-loss asymmetry [207, 208, 209, 210, 211, 205, 212, 213, 214, 215]. Several models have been proposed to reproduce the gain-loss asymmetry [216, 217, 218]. Nevertheless, there are also assets that do not show significant gain-loss asymmetry [202, 219].

An analysis in the frequency space based on the discrete wavelet transform showed that the gain-loss asymmetry is introduced mainly by the low-frequency content of the price series and the asymmetry disappears if enough of the low-frequency content is removed [218]. Alternatively, the gain-loss asymmetry is found to be caused by the non-Pearson-type autocorrelations in the time series [220]. Furthermore, the gain-loss asymmetry vanishes if the temporal dependence structure is destroyed by shuffling the time series [221].

The gain-loss asymmetry can be related to the leverage effect as follows. Recall first that the leverage effect is the fact that, after a large negative return, the volatility increases significantly and then relaxes back, usually roughly exponential in time [222, 223, 224]. In contrast, after a positive return, there is no significant change of volatility. And the causality is from (negative) returns to future volatility and not the reverse, in the sense that a variation of volatility does not produce any measurable change of the expected return in the future. The leverage effect can be interpreted as due to the impact of a loss on the risk perception of the firm, which increases as the equity over debt ratio has decreased as a result of the loss [222]. It also reflects a behavioral response of investors, who after a loss frantically reassess their risk exposure and readjust their portfolios, leading to large price moves. The leverage effect allows one to account for both (i) the asymmetry in the average time for a price drop of a fixed percentage versus a price gain of the same value (for instance 10 days for a loss of 5% and 20 days for a gain of 5% on the DJIA) and (ii) the fact that this asymmetry in waiting times for positive vs negative objectives is stronger for indices and weaker or absent for individual stocks [221, 218]. ? Consider a fixed drop target of -5%. Such a drop is achieved by a succession of daily returns, more negative than positive. When some negative loss occurs on one day, the leverage effect leads to an increase of the amplitude of the next daily return. Because we are calculating a waiting time conditional to a cumulative drop of -5%, the following returns will tend to be negative and with larger amplitude due to the leverage effect. In contrast, for the waiting time to reach a positive gain of +5%, a majority of the daily moves will be positive, and the leverage effect will be weaker or absent if there are no or weak negative returns along the price path. As a consequence, as the amplitude of the daily returns tend to be small for a sequence of daily returns involved in a positive level (+5%), the average waiting time to reach a positive return (+5%) is larger than for a negative return goal. The asymmetry of a single stock is small because the leverage effect has a rather short memory and the difference between the number of up and down daily moves for reaching the target threshold is not large. In contrast, for an index, or equivalently a portfolio of stocks, one must account for the ubiquitous existence of correlations between the returns of the stocks constituting the portfolio. These correlations, which are in general positive (most stocks move approximately together on average), produce an amplification of the gain-loss asymmetry, because the leverage effect is stronger by the averaging over the idiosyncratic residuals of the constituting stocks. This also leads to predict that the gain-loss asymmetry for a portfolio is the stronger, the stronger is the average correlation coefficients of its constituting stocks.

The moments of the exit time, called the distance structure functions [189] or inverse structure functions [225, 226], are defined by

| (69) |

Due to the duality between the structure function and the inverse structure function, one can intuitively expected that there is a power-law scaling stating that

| (70) |

where is a nonlinear concave function [189].

Synthetic data for the GOY shell model of turbulence show perfect power-law dependence of the inverse structure functions on the velocity threshold [189]. For two-dimensional turbulence, the inverse structure functions exhibit well-defined multifractal properties [226]. In contrast, for three-dimensional turbulence, the inverse structure functions of an experimental time series at high Reynolds number do not exhibit clear power law scaling [225]. Nevertheless, different experiments show that the inverse structure functions of three-dimensional turbulence exhibit a more general scaling behavior called extended self-similarity (see next subsection) [227, 228, 229]. To our knowledge, the behavior of inverse structure functions of financial asset prices has not been studied.

The inversion formula relating the direct scaling exponents of direct structure functions and the inverse scaling exponents of inverse structure functions can also be derived [230, 231] and give

| (71) |

These expressions are verified by the simulated velocity fluctuations from the shell model [162]. However, this prediction (71) cannot be confirmed by wind-tunnel turbulence experiments (Reynolds numbers ) [228], which is not surprising because the inverse structure function does not scale as a power law of the velocity increment thresholds [225, 228].

2.2.4 Extended self-similarity

To investigate the scaling properties of the inverse structure functions, one can define a set of relative exponents using the framework of extended self-similarity (ESS) [232]:

| (72) |

where is the order taken as a reference value. If Eq. (56) holds, we have

| (73) |

When the time series is monofractal, is independent of , that is, . It follows for monofractal time series that

| (74) |

In the case of velocity structure functions in fluid mechanics, is a natural choice based on the exact Kolmogorov’s Four-Fifth Law [233, 229]. For financial time series, we suggest to choose because is the Hurst index. Generally, the ESS approach provides a wider scaling range for the extraction of scaling exponents.

Fig. 5(a) presents the log-log plots of against for with . The straight lines hold over more than two orders of magnitude and over at least 3.5 orders of magnitudes for , showing the existence of extended self-similarity in the structure functions. The scaling range for small ’s seems to be broader than for large ’s. The ESS scaling exponents are shown in Fig. 5(b). There is a weak indication that has a nonlinear dependence as a function of , with a downward curvature making the curve depart from the linear dependence observes for small ’s.

Whether a time series possesses monofractal or multifractal behaviors is related to the innovation distributions. For simplicity of notation, we denote . By definition, we have

| (75) |

where is the distribution of , is the standard deviation of , is the normalized volatility, and is the distribution of . Eliminating using , it follows that

| (76) |

If is universal and independent of , then the last term in Eq. (76) is a number independent of (and thus of ) and the monofractal behavior follows. Fig. 5(c) shows the distributions of the normalized volatility at three different scales. Although the three curves well overlap in their tails, they show clear differences in the bulk around . This suggests that the ESS cannot be nonfractal, which is consistent with the presence of nonlinear curvature in Fig. 5(b).

We note that the ESS analysis is not constrained to the structure functions. Rather, it can be used for the moments of other multifractal analysis approaches. In validating and qualifying the multiscaling behaviour of the recurrence intervals of financial volatility, the relative dependence of recurrence interval moments of different orders of empirical time series has been investigated [234], which is in essence an ESS analysis [235].

2.3 Wavelet transform approaches

2.3.1 Multifractal analysis based on wavelet transform (MF-WT)

The wavelet transform is widely used as a mathematical microscope to analyze time series [236, 237]. In particular, it can be used to analyze the singular structure of fractal and multifractal time series [238, 239, 240].

The wavelet transform of function is [236, 237]

| (77) |

where is the position parameter, is the dilation parameter, is the analyzing “mother” wavelet. Gaussian wavelets are widely adopted [241] and are defined as derivatives of the Gaussian function:

| (78) |

where is the normalization coefficient. The second order () Gaussian wavelet is known as the Mexican hat.

To perform wavelet transform on a time series , one usually discretizes Eq. (77) in which can take any value along the sampling spacing and takes scales forming a geometric sequence:

| (79) |

where . The discretised wavelet transform of a given time series is then

| (80) |

The wavelet transform is used to identify different types of singularities in the signals in the time-scale plane, depending on the order of derivative of the mother wavelet (78). More generally, choosing a mother wavelet satisfying implies that the wavelet transform is blind to polynomial dependence up to order and only higher order powers are detected. For instance, for , the wavelet transform is independent of the level of the signal and informs essentially on the local slope. For , the wavelet transform is independent of the level of the signal and of its local slope, and it informs on the local curvature. We should also mention the existence of orthogonal wavelet transforms [242, 243, 241] and biorthogonal wavelet transform [244], which can be used directly to determine the Hurst index of a long-range correlated time series [245, 246, 247].

To investigate the multifractal nature of a time series, one can calculate the th order moments of the wavelet coefficients [248, 249]

| (81) |

and we expect that

| (82) |

We note that might diverge for because some values of might be close or equal to 0.

One can obtain the scaling exponents through ordinary least-squares regression. Or, we can adopt the weighted least-squares regression by putting more weight on the points with smaller variance [247]. Denoting

| (83) |

the corresponding weight is

| (84) |

and the objective function is

| (85) |

The estimate of is determined as follows:

| (86) |

2.3.2 Wavelet transform modulus maxima (WTMM)

A more elegant approach, which removes the redundancy contained in continuous wavelet transforms, is based on the wavelet transform modulus maxima (WTMM) [250, 249, 251, 245]. At each scale , there exists several local maxima of . These maxima form several maxima lines in the plane. The WTMM is capable of detecting all the singularities of a large class of time series [252]. The traditional method based on partition functions may face problems in dealing with the situation of . However, we will find that the multifractal analysis based on WTMM can overcome this difficulty because the wavelet coefficients on the WTMM line are local maxima that are non 0 [251].

Assume that there are local maxima at scale and is the th local maximum located at . The th order moments defined on the WTMM are

| (87) |

or alternatively the partition functions read

| (88) |

For multifractal time series, we have

| (89) |

The generalized dimensions and singularity spectrum can then be calculated straightforwardly.

Analogous to the thermodynamic approximation in the direct determination of singularities and singularity spectrum in Section 2.1.3, we can define the canonical measure [250],

| (90) |

such that the singularity strength is

| (91) |

and the singularity spectrum is

| (92) |

In applications, we use different scales and perform (weighted) linear regression on the log-log scales.

2.3.3 Wavelet leader (MF-WL)

A more recent multifractal formalism is based on wavelet leaders [256, 257, 258, 259, 260, 261]. Wavelet leaders, introduced by Jaffard [256, 257], are defined based on discrete wavelet coefficients, which decompose the time series on the bases composed of discrete wavelets . The integers and define the scale and location . The discrete wavelets are space-shifted and scale-dilated templates of an analyzing wavelet :

| (93) |

which usually uses the Daubechies wavelet of order 1 for the mother wavelet. The discrete wavelet coefficients are defined as

| (94) |

One defines a dyadic interval as

| (95) |

and denotes the union of interval and its two adjacent neighbors as ,

| (96) |

The wavelet leader is defined by [256, 257]

| (97) |

which corresponds to the largest value of the absolute wavelet coefficients calculated on intervals with . Note that, to compute the wavelet leaders, all the fine scales must be considered.

The multifractal analysis based on wavelet leaders can be described as follows [256, 257, 258, 259, 260, 261]. As usual, we can define the moments of order by

| (98) |

where is the number of wavelet leaders at scale . One can also expect the following scaling behavior if the underlying processes are jointly multifractal,

| (99) |

where is related to by

| (100) |

We can also provide a canonical approach to determine the singularity strength function and the multifractal spectrum directly, as for the WTMM case in Section 2.3.2.

An interesting application of wavelet leaders is the pointwise wavelet leaders entropy [262], which is defined over different scales () for a given point () by

| (101) |

where if and

| (102) |

When applied to the DJIA index (1928-2011), the resulting wavelet leader entropy is able to identify historical large market fluctuations [262].

Recently, wavelet -leaders are introduced to characterize the -exponents of negative pointwise regularity [263]. Based on the wavelet coefficients calculated in Eq. (94), the wavelet -leaders are defined by

| (103) |

The -leader multifractal formalism relies on the sample moments of the -leaders [264]:

| (104) |

It is found that MF-DFA characterizes local regularity via the 2-exponent, not the Hölder exponent, and the wavelet -leader multifractal formalism can be viewed as an wavelet-based extension of MF-DFA [264]. The -leaders suffer from finite-resolution effects, which can be resolved through an explicit and universal closed-form correction [265].

2.4 Detrended fluctuation approaches

2.4.1 General framework

Consider a time series , whose data points are usually the cumulative sums of a time series of innovations. Let be the local trend function, which is usually determined locally around the data points using some method. The detrended residuals are defined by

| (105) |

We divide into non-overlapping segments with boxes of size , where is the largest integer that is no larger than . We denote the th segment as . The local detrended fluctuation function in the th box is defined as the r.m.s. of the detrended residuals:

| (106) |

The th-order overall detrended fluctuation is

| (107) |

where can take any real value except . When , we have

| (108) |

according to L’Hôspital’s rule.

When the whole series cannot be completely covered by boxes, one can use boxes to cover the series from both ends of the series, where and a short part at each end of the residuals may remain uncovered [139]. We denote the th segment partitioned from left to right as for and the th segment partitioned from left to right as for . The local detrended fluctuation function in the th box is defined as the r.m.s. of the detrended residuals,

| (109a) | |||

| and | |||

| (109b) | |||

The th-order overall detrended fluctuation is

| (110) |

where can take any real value except for . When , we have

| (111) |

according to L’Hôspital’s rule.

Varying the values of the segment size , we can determine the power-law relation between the function and the size scale ,

| (112) |

According to the standard multifractal formalism, the multifractal scaling exponent can be used to characterize the multifractal properties, which reads

| (113) |

where is the fractal dimension of the geometric support of the multifractal measure [139]. For time series analysis, we have . If the scaling exponent function is a nonlinear function of , the time series is regarded to have a multifractal nature.

Following the approach determining directly from the partition function [157, 158, 266], the singularity strength and its spectrum in the detrended fluctuation approaches can also be determined directly [267]. Defining the canonical measure

| (114) |

we have

| (115a) | |||

| and | |||

| (115b) | |||

Numerical experiments based on the -model and fractional Brownian motions showed that MF-DMA and its direct determination variant have comparative performance to unveil the fractal and multifractal properties [267].

2.4.2 Multifractal detrended fluctuation analysis (MF-DFA)

The Detrended Fluctuation Analysis (DFA) was invented originally to investigate the long-range dependence in coding and noncoding DNA nucleotide sequences [268]. The multifractal extension of DFA, MF-DFA, was developed shortly thereafter [269, 270]. Since the work of Kantelhardt et al. [139], MF-DFA has become one of the most important methods for multifractal analysis in diverse fields.

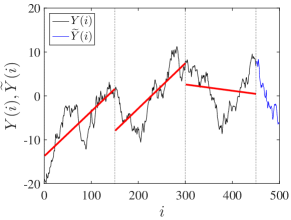

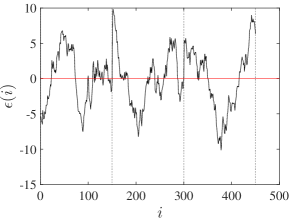

In the MF-DFA method, the trend function is a polynomial [139], and the linear trend is most generally adopted. For each point , its trend value is determined together with other points in the same box , using a polynomial fitting of order to the data points in :

| (116) |

The detrending process for is shown in Fig. 6. The figure shows a case with in which the data points at each end of the time series should not be included to form a box. Otherwise, one obtains incorrect results with , as will be elaborated in Section 5.1.2. In the standard procedure implementing MF-DFA, researchers remove the constant shift from the increments and work on the cumulative profile

| (117) |

where is the sample mean of the series. However, when the trend function is polynomial, this manipulation does not have any impact on the results.

A subtle issue of the MF-DFA method is the choice of polynomial order. Using classic mathematical models (fractional Brownian motion, Lévy process and binomial measure) and real-world time series (foreign exchange rate and literary texts), Oświȩcimka et al. found that the calculated singularity spectra could be very sensitive to the order of the detrending polynomial and this sensitivity depends on the analyzed time series [271]. Without a deep understanding of the underlying mechanism driving the dynamics, it is hard to determine which polynomial order should be used. Anyway, for financial time series such as returns, we can check if the value of the Hurst index is close to 0.5, based on the fundamental stylized fact of the absence of long memory in financial returns [60], which however might not hold at the transaction level [272].

A possible solution is to use “feasible trend functions” in the multifractal feasibly detrended fluctuation analysis (MFFDFA) [273]. One presets a priori a set of any trend functions, say, , and fit each segment with all the preset trend functions. For each segment, only one detrended function is chosen which has the maximum coefficient of determination . Hence, for each time scale , the trend functions for different segments are not necessary the same. Numerical experiments on fractional Brownian motions and binomial measures show that the MFFDFA method outperforms the MF-DFA method [273]. For binomial measures, the improvement is partially due to the fact that the fluctuation functions for MFFDFA have much smaller log-periodic oscillation amplitudes, which reduces the impact of the choice of scaling ranges [274].

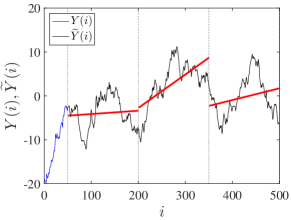

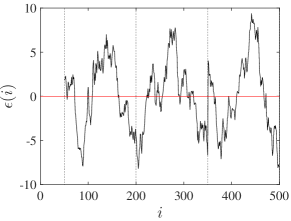

2.4.3 Multifractal detrending moving average analysis (MF-DMA)

Based on the moving average (MA) technique for estimating the Hurst exponent of self-affinity signals [275], the Detrending Moving Average (DMA) analysis considers the difference between the original signal and its moving average function [276, 277]. The DMA method can also be easily implemented to estimate the correlation properties of non-stationary series without any a priori assumptions, which is widely applied to the analysis of real-world time series [278, 279, 280, 281, 282, 283, 284, 285] and synthetic signals as well [286]. Extensive numerical experiments unveil that the performance of DMA is comparable to DFA with slightly different priorities under different situations and both DFA and DMA remain “The Methods of Choice” in determining the Hurst index of time series [287, 288, 289].

The DMA method was generalized to MF-DMA for the investigation of the multifractal nature of time series [290]. The main difference between the MF-DFA and MF-DMA algorithms is about the detrending procedure. In the MF-DMA approach, one calculates the moving average function in a moving window of size [283],

| (118) |

where is the largest integer not greater than , is the smallest integer not smaller than , and is the position parameter. In other words, one considers data points in the past and points in the future to determine . When is close to each of the endpoints, the size of the box might be less than . One can either abandon those points or calculate the moving averages directly. Usually, we consider three special cases, corresponding to three representative versions of MF-DMA:

-

1.

MF-BDMA. The first case refers to the backward moving average [287], in which the moving average function is calculated over all the past data points of the signal.

- 2.

-

3.

MF-FDMA. The third case is called the forward moving average, where considers the trend information of data points in the future.

We note that the size of the window used to calculate the moving averages must be identical to the segment size in calculating the detrended functions [290, 291]. The detrending process is illustrated in Fig. 7.

2.4.4 Other detrending algorithms

Although determining the intrinsic trend embedded in non-stationary time series is difficult, there are many different options [292]. Because the intrinsic trend of a time series is usually unknown, methods have different performances for different types of time series. Hence, quite a few variants of MF-DFA and MF-DMA have been proposed. Local trends can be be further classified into discontinuous ones and continuous ones. MF-DFA and MF-DMA belong respectively to these two classes (see also Fig. 6 and Fig. 7).

Zhou and Leung proposed the multifractal temporally weighted detrended fluctuation analysis (MF-TWDFA) in moving windows [293]. For each , they fit a linear function to the data points in the moving window of size , using weighted least-squares regression. The objective function is

| (119) |

where ’s are weights that decrease with increasing . In other words, the deviation has a larger weight when is far from . The weights in MF-TWDFA are defined by [293]

| (120) |

For the equally weighted case,

| (121) |

we obtain the multifractal moving window detrended fluctuation analysis (MF-MWDFA) [293]. These two methods belong actually to the continuous class, since the trend changes mildly without jumps. Indeed, when , we recover the centered MF-DMA method [293].

The empirical mode decomposition (EMD) is an innovative method of analysis for nonlinear and non-stationary time series, which decomposes the time series into a finite number of intrinsic mode functions (IMFs) [294]. Let . The decomposition is a sifting process, which has six steps [292]: (1) Identify all extrema of ; (2) Interpolate the local maxima to form an upper envelope ; (3) Interpolate the local minima to form a lower envelope ; (4) Calculate the mean envelope:

| (122) |

(5) Extract the mean from the signal

| (123) |

(6) Check whether satisfies the IMF conditions. If the IMF conditions are fulfilled, is an IMF, and the sifting stops. Otherwise, let and keep sifting. Finally, we obtain the EMD-based local trend of the time series segment :

| (124) |

Qian et al. used this local trend in the MF-DFA method and developed the EMD-based MF-DFA method [295]. Numerical experiments on multifractal binomial measures indicate that the EMD-based MF-DFA method has comparable performance with respect to the MF-DFA method except that the EMD-based method performs slightly better for small singularities [295]. The method has been applied to analyze stock market indices [295, 296], foreign exchange rates [297], and Certified Emission Reduction (CER) and European Union Allowances(EUA) futures prices [298], all of which confirm the presence of multifractality in financial returns.

In order to handle time series with highly non-stationary sinusoidal and polynomial overlying trends, Horvatic et al. proposed to detrend with polynomials of varying orders [299]. In this method, the polynomial order is not fixed but increases with the scale and the detrended fluctuations at different scales should be normalized to secure an identical intercept. Although an objective criterion for the determination of the varying order is lacking, a subjective choice ( for , for , for , for , and for ) seemingly works well [299]. The underlying logic is that we need high-order polynomials to detrend properly the oscillations.

Du et al. constructed the dual-tree complex wavelet transform based multifractal detrended fluctuation analysis (DTCWT-MFDFA) for non-stationary time series [300]. Based on the anti-aliasing and nearly shift-invariance of the dual-tree complex wavelet transform [301, 302], the raw time series is decomposed through the pyramid algorithm to extract the scale-dependent trends and the fluctuations from the wavelet coefficients. The length of the non-overlapping segment on each time scale is computed through the Hilbert transform and each of the extracted fluctuations is partitioned into non-overlapping segments with identical size. The detrended fluctuation function for each segment can be calculated. The DTCWT-MFDFA method is found to outperform the MF-DFA method for multifractal binomial measures [300].

In order to perform the MF-DFA, Manimaran et al. proposed to detrend using discrete wavelet transform [303]. The discrete wavelets belonging to the Daubechies family are adopted to analyze the raw time series up to level . The resulting low-pass coefficients capture the polynomial trends in the data. One then reconstructs a time series using these low-pass coefficients to represent the local trends at different scales. The method has been tested for synthetical time series and applied to NASDAQ and BSE indices [304, 305]. Ghosh et al. used Db4 and Db6 basis sets to isolate respectively the local linear and quadratic trends at different scales from the closing prices of fifteen large-capitalization companies listed on the New York Stock Exchange (NYSE) [306]. Multifractality is observed in the investigated stock indices and individual stocks.

We note that other detrending methods used to preprocess the raw time series in Section 5.3.6 can also be used in the local detrending at different scales to construct variants of MF-DFA.

2.5 Other methods

In this section, we will review several other multifractal analysis methods. It should be keep in mind that different multifractal analysis methods have been proposed in diverse fields and it is hard to mention all of them. We focus on the methods that are relevant to those discussed in the previous sections and that are utilized for financial time series analysis. Besides the ones presented below, we would like to mention the multifractal signal fluctuation analysis based on the 0-1 test [307] and the focus-based multifractal formalism [308].

2.5.1 Multiplier method

The concept of the multiplier was introduced by Novikov to describe the intermittency and scale self-similarity in turbulent flows [125]. In econophysics, one can apply this concept to study volatility multipliers. For high-frequency financial data, we first construct an additive measure in the time interval , which is the sum of absolute returns:

| (125) |

The absolute return is actually a measure of the volatility on [309]. The volatility time series is divided into boxes of identical size . Each mother box is further partitioned into daughter boxes, in which is called a base. The multiplier is determined by the ratio of the measure on a daughter box to that on her mother box [310, 311].

If the multiplier is scale invariant, for any two bases and , the multiplier density functions and are related through Mellin transform as follows [311]:

| (126) |

which leads to

| (127) |

The mass scaling exponent of the moment of can be obtained as [310, 311]

| (128) |

where is the fractal dimension of the support of the measure. For time series, we have .

The local singularity exponent and its spectrum are related to through the Legendre transform. It follows that

| (129) |

and

| (130) |

Eqs. (127-130) imply that, for each , each of these characteristic multifractal quantities converges to a constant in the scaling range and is independent of the base .

Note that, for financial volatility, [312], which is quite analogous to the situation in turbulence [228]. Because the returns can be zero, the multiplier can be zero and the probability density at . When is smaller than a small number , is a constant. For a given small , is finite. However, the moment

| (131) |

diverges when . This property is verified empirically [312], based on the idea that the integrand diverges for a given [313, 229].

The scale-invariant multiplier distribution is perceived to be more fundamental than the standard multifractal spectrum [310, 311]. Moreover, it needs exponentially less computational time and is more accurate than the partition function approach [310, 311].

Using 1-min high-frequency data of the S&P 500 index, Jiang and Zhou reported that the volatility multiplier is scale invariant and the volatility has the property of multifractality [312]. Niu and Wang confirmed the presence of scale invariance in the multiplier distributions in the Shanghai SSEC index and in the simulated data from the model of “voter interacting dynamic system” [314].

2.5.2 Multifractal Hilbert-Huang spectral analysis

The Hilbert-Huang transform combines the EMD and the Hilbert spectral analysis [294, 315], in which the Hilbert transform is applied to each component in Eq. (123). The overall trend can be expressed as

| (132) |

where . For each mode, the Hilbert-Huang spectrum is defined as the squared amplitude

| (133) |

The Hilbert-Huang marginal spectrum of the original time series is then written as

| (134) |

which corresponds to an energy density at frequency . This method is known as EMD-based Hilbert spectral analysis (EMD-HSA), which we term the Hilbert-Huang spectral analysis (HHSA) for simplicity.

Huang, Schmitt, Lu and Liu proposed the multifractal Hilbert-Huang spectral analysis (MF-HHSA) by generalizing the Hilbert-Huang transform from the second order to arbitrary order [316, 317]. The Hilbert-Huang spectrum represents the original signal at the local level and can be used to define the joint probability density function of the frequency and amplitude . The Hilbert-Huang marginal spectrum in Eq. (134) can be rewritten as

| (135) |

which corresponds to the second-order moment. Huang et al. generalize Eq. (135) into arbitrary-order moments

| (136) |

where and . In the inertial range, we assume the following scaling relation,

| (137) |

where is the corresponding scaling exponent function in the amplitude-frequency space.

Li and Huang applied this MF-HHSA method to the CSI 300 index of the Chinese stock market and confirmed the presence of multifractality [318].

2.5.3 EMD-based multifractal methods

Welter and Esquef proposed an EMD-based dominant amplitude multifractal formalism (EMD-DAMF), which is implemented as follows [319]:

-

Step 1: Perform EMD on to obtain IMFs .

-

Step 2: Determine the amplitude and characteristic timescale for . The characteristic timescale could be estimated in each mode by the Hilbert spectral analysis (HSA) as the reciprocal of the mean frequency, or simply by twice the mean time interval among all adjacent zero crossings.

-

Step 3: Determine the dominant amplitude coefficients

(138) where is the number of local maxima of and is a time support around the th maxima of .

-

Step 4: Calculate the th order moment for different values:

(139) where the characteristic time scale can be obtained by HSA in each mode as the reciprocal of the mean (linear) frequency or simply by the mean time interval among all adjacent zero crossings.

-

Step 5: Estimate the scaling function

(140)

In real applications, Welter and Esquef suggested that the number of siftings is fixed to ten (that is, ) and signal envelopes are computed through cubic spline interpolation [319]. They validated the method with fractional Brownian motions [320], Lévy processes [321], Multifractal random wavelet cascades [322, 323], and multifractal multiplicative cascades from the model [324]. Note that the EMD-DAMF method has a small number of amplitude maxima at larger scale modes and a limited number of scales [319]. The latter drawback might impact the determination of the scaling range.

Alternatively, Zhou et al. proposed the so-called EMD-DFA method [325]. The integrated time series is decomposed into a set of intrinsic mode functions and a residual or trend component. All intrinsic time scales are identified by computing the number of data points between each neighboring local minima throughout each intrinsic mode function (IMF). For a given , all IMFs are resampled through replacing by 0’s all data points corresponding to scales not equal to and the fluctuation time series is obtained by summing all resampled IMFs. The overall fluctuation at scale is the root mean square of :

which produces better scaling than the DFA method [325]. The EMD-DFA method can be extended for multifractal time series by working on the -order moments:

| (141) |

Note that the EMD-DFA method does not have an explicit detrending form like Eq. (105).

2.5.4 Multiscale multifractal analysis

Gieraltowski et al. proposed the multiscale multifractal analysis (MMA) based on the MF-DFA method [326]. After calculating all values of the overall fluctuations by the MF-DFA method, rather than estimating from Eq. (112) in the scaling range, they proceeded to estimate the local generalized Hurst exponents in moving windows around different scales. In this method, two free parameters are introduced, the moving window size and the step. Although the original MMA method is designed for MF-DFA, it can obviously be applied to other methods of multifractal analysis.

The MMA method has been applied to investigate the multifractal nature of daily returns of the Dow Jones Industrial Average (DJIA), New York Stock Exchange Index (NYSE), S&P 500 Index, Heng Seng Index (HSI), Shanghai Stock Exchange Composite Index and Shenzhen Stock Exchange Component Index (SZCI) from 12 May 1992 to 8 May 8 2012 [327, 328] and nine stock market indices (CAC 40, DAX, FTSE 100, HSI, NIKKEI 225, SSEC, NASDAQ, S&P 500) from 3 January 2000 to 1 October 2014 [329].

More generally, this method is equivalent to calculate the local logarithmic slopes of the functions:

| (142) |

which is widely utilized in the study of structure functions in turbulence [226, 229], as well as in DFA [330]. The idea to estimate local logarithmic slopes is especially informative when the scaling range is narrow and it can serve as a method for the determination of scaling ranges. Different numerical methods can be adopted to estimate numerically the local logarithmic slopes and the linear fitting in a moving window suggested in the MMA method is one of them. Empirical analyses have been performed on financial time series, such as the WTI crude oil market [331] and stock market indices [332], without referring to the name of multiscale multifractal analysis.

2.5.5 Time-varying multifractal analysis

To quantify the evolution of a multifractal spectrum, one can perform a multifractal analysis of time series in moving windows or rolling windows. We would like to stress that short window sizes will reduce the estimation accuracy of multifractal quantities and increase the uncertainty of the results. Time-varying multifractal quantities have practical implications, as discussed in Section 8.2.4.

Alternatively, Xiong and Zhang proposed the time-varying multifractal spectrum distribution (TM-MFSD) [333]. The key idea is to perform multifractal analysis on the instantaneous autocorrelation function

| (143) |

rather than the raw time series , where the time-delayed conjugation of the analyzed series is selected as the window function. To obtain the time-varying multifractal spectrum distribution of a time series, one can adopt different multifractal analysis methods described in previous sections, such as WTMM [333], wavelet leaders [334, 335], MF-DMA [336], and MF-DFA [337]. Essentially, the multifractal analysis is performed with these methods on moving windows.

2.5.6 Phase space reconstruction

A classic method in nonlinear dynamics is to embed properly the time series into a phase space and estimate the generalized dimensions of the data points in the phase space [128, 149, 148, 338], which is however less applied in econophysics. Based on the delay embedding technique [339], the time series can be converted into a sequence of vectors:

| (144) |

where is the number of points (or vectors) in the phase space, is a suitably chosen time delay, and is the embedding dimension of the phase space. The embedding dimension and the delay can be determined in different ways [149, 340, 341, 342, 343, 344].

The relative number of data points within a distance to point is calculated by

| (145) |

where is the Heaviside function. The generalized correlation integral is [345]

| (146) |

which is the generalization of the correlation integral [128, 149, 148]. The generalized dimensions are given by [338]

| (147) |

Lee investigated the multifractal characteristics of the 1-min volatility of the Korea composite stock price index KOSPI from 20 March 1992 to 28 February 2007 [346]. The volatility time series is first detrended with a wavelet filter and then a multifractal analysis in the phase space with and is performed to confirm the presence of multifractality.

2.5.7 Asymmetric multifractal analysis