Interpretable Sparse Proximate Factors for Large Dimensions††thanks: We thank Bryan Kelly, Kay Giesecke, Serena Ng, José Luis Montiel Olea, Dacheng Xiu and seminar and conference participants at Stanford University, Columbia University, NBER-NSF Time-Series Conference, SoFiE Meeting, California Econometrics Conference, SoFiE Summer School on Machine Learning and Empirical Asset Pricing and INFORMS for helpful comments.

First draft: May 2018; First draft: May 2018

This draft: July 2020)

This paper proposes sparse and easy-to-interpret proximate factors to approximate statistical latent factors. Latent factors in a large-dimensional factor model can be estimated by principal component analysis (PCA), but are usually hard to interpret. We obtain proximate factors that are easier to interpret by shrinking the PCA factor weights and setting them to zero except for the largest absolute ones. We show that proximate factors constructed with only 5-10% of the data are usually sufficient to almost perfectly replicate the population and PCA factors without actually assuming a sparse structure in the weights or loadings. Using extreme value theory we explain why sparse proximate factors can be substitutes for non-sparse PCA factors. We derive analytical asymptotic bounds for the correlation of appropriately rotated proximate factors with the population factors. These bounds provide guidance on how to construct the proximate factors. In simulations and empirical analyses of financial portfolio and macroeconomic data we illustrate that sparse proximate factors are close substitutes for PCA factors with average correlations of around 97.5% while being interpretable.

Keywords: Factor Analysis, Principal Components, Sparse Weights, Shrinkage, Interpretability, Large-Dimensional Panel Data, Extreme Value Theory

JEL classification: C14, C38, C55, G12

1 Introduction

Large dimensional datasets are becoming increasingly relevant to study problems in economics and finance. These datasets contain rich information and open the possibilities of new findings and new efficacious models, which is feasible only if we better understand the datasets. Factor modeling (Bai and Ng, 2002; Bai, 2003; Fan, Liao, and Mincheva, 2013) is a method that summarizes information in large-dimensional panel data and is an active research topic. In a large-dimensional factor model, both the time dimension and the cross-section dimension of the data sets are large and most of the co-movement can be explained by a few factors. Latent factors estimated from the data are particularly appealing as the underlying factor structure is usually not known. These factors are usually estimated by Principal Component Analysis (PCA). Latent PCA factors have been successfully used in economics and finance, for example for prediction and forecasting (Stock and Watson, 2002a, b), asset pricing of many assets (Lettau and Pelger, 2020b; Kelly, Pruitt, and Su, 2019), high-frequency asset return modeling (Pelger, 2019; Aït-Sahalia and Xiu, 2019), conditional risk-return and term structure analysis (Ludvigson and Ng, 2007, 2009) and optimal portfolio construction (Fan, Liao, and Mincheva, 2013).111Of course, the application of latent factor models goes beyond the applications listed above, e.g. inferring missing values in matrices (Xiong and Pelger, 2020; Candès and Tao, 2010; Candès, Li, Ma, and Wright, 2011). However, as the latent PCA factors are linear combinations of all cross-sectional units, they are usually hard to interpret. This poses a challenge for modeling and understanding the underlying structure to explain the co-movement in the data. This becomes particularly relevant for applications in economics and finance where the objective is to understand the underlying economic mechanism.

Practitioners and academics alike have used an intuitive approach to interpret latent statistical factors by focusing on the largest factor weights. A pattern in the largest factor weights suggests an economic interpretation as suggested by Lettau and Pelger (2020b) and Pelger (2020). In this paper, we formalize this idea and show that the factors that are only based on the largest factor weights provide already an excellent approximation to the population factors. This step further reduces the dimensionality of the problem helping to better understand the economic mechanism in the problem.

We propose easy-to-interpret proximate factors for latent factors. We exploit the insight that cross-section units with larger factor weights have a larger signal-to-noise ratio, hence providing more information about the underlying factors. We start by estimating the underlying factor structure with conventional PCA, which returns the weights of PCA factors as the eigenvectors of the largest eigenvalues of a sample covariance matrix. Our method consists of three simple steps. First, we set all factor weights to zero except for the largest absolute ones. Second, the proximate factors are obtained from a simple regression on the thresholded factor weights. Third, the loadings are obtained from a regression on the proximate factors. We work under a general scenario where the factor weights and loadings in the true model are not sparse, i.e. the number of nonzero elements is proportional to the size of the cross-section, while the sparse factor weights have only a finite and small number of nonzero entries.

We show that one needs to make a clear distinction between factor weights and loadings. In a conventional PCA analysis the loadings serve two purposes: First, they measure the exposure of the cross-sectional data to the factors. Second, they correspond to weights to construct the latent PCA factors. The same view is for example taken in a sparse PCA setup where loadings and hence also the factor weights are shrunk to a sparse matrix. We show that in an approximate factor model with non-sparse factor weights and loadings, we can construct proximate factors with sparse factor weights that are very close to the population factors. These proximate factors have non-sparse loadings which are consistent estimates of the true population loadings. The proximate factors are considerably easier to interpret as they are only based on a small fraction of the data, while enjoying the same properties as the non-sparse factors.222A common method to interpret low-dimensional factor models is to find a rotation of the common factors with a meaningful interpretation. This approach uses the insight that factor models are only identified up to an invertible transformation and represent the same model after an appropriate rotation. The criterion proposed by Kaiser (1958) is a popular way to select factors whose factor weights have groups of large and negligible coefficients. However, in large-dimensional factor models with non-sparse factor weight structure, finding a “good” rotation becomes considerably more challenging. It is generally easier with our sparse proximate factors to find a rotation that has a meaningful interpretation.

We develop the statistical arguments that explain why the sparse proximate factors can be used as substitutes for the non-sparse PCA factors in general approximate factor models. The conventional derivations used in large-dimensional factor modeling to prove consistency do not apply to our proximate factors. The conventional non-sparse PCA factors are a weighted average over a large number of cross-sectional units which diversifies away the idiosyncratic noise. In contrast, proximate factors are weighted averages over only a finite and small number of cross-sectional units, which in general do not average out the noise and lead to biased estimates of the population factors. However, we show that, by selecting the most informative units as weights, this bias can become negligible. The closeness between proximate factors and true factors is measured by the generalized correlation.333Generalized correlation (also called canonical correlation) measures how close two vector spaces are. It has been studied by Anderson (1958) and applied in large-dimensional factor models (Bai and Ng, 2006; Pelger, 2019; Pelger and Xiong, 2019; Andreou, Gagliardini, Ghysels, and Rubin, 2019). We provide an asymptotic probabilistic lower bound for the generalized correlation.444In simulations, we verify that the lower bound has good finite sample properties. This lower bound is easy to calculate and depends on the number of nonzero elements in the sparse factor weights and on the tail distribution of population factor weights which we can characterize with Extreme Value Theory (EVT). This lower bound provides guidance on constructing the proximate factors that are guaranteed to have a high correlation with the true factors. One insight of this bound is that in the case of heteroskedastic errors the most informative factor weights are the units with the largest loadings relative to the unit-specific noise variance. Moreover, when factor weights have unbounded support, we show that proximate factors asymptotically span the same space as latent factors. Importantly, the estimated loadings of the proximate factors converge to the true population loadings up to the usual rotation. This surprising result is due to the two-stage procedure for estimating the loadings that averages out the idiosyncratic noise in the time dimension. Hence, regressions based on the more interpretable proximate factors will asymptotically yield the same results as using the harder to interpret PCA factors.

Our results are of practical and theoretical importance. First, we provide a simple and easy-to-implement method to approximate latent factors by a small number of observations. These sparse proximate factors usually provide a much simpler economic interpretation of the model, either by directly analyzing the sparse composition or after rotating them appropriately. Our method has already been successfully used in Lettau and Pelger (2020b) to interpret asset pricing factors and in Pelger (2020) to interpret high-frequency factors. Second, we show in empirical and simulation studies that this approximation works surprisingly well and almost no information is lost by working with the sparse factors. Third, an important contribution of this paper is to characterize the asymptotic properties of a sparse factor estimator if the population model is not sparse. Our asymptotic bounds for the correlations between the proximate factors and the population factors provides the theoretical reasoning why our method works so well. In particular, it clarifies under which assumptions the proximate factors are a good approximation or even converge to the population factors. Fourth, the asymptotic bounds provide guidance on how to select the key tuning parameter for our estimator, that is, the number of nonzero elements.555The degree of sparsity can also be chosen to obtain a sufficiently high generalized correlation with the estimated PCA factors or by cross-validation arguments to explain a sufficient amount of variation in the data. Our theoretical bound provides an alternative to select the tuning parameter based on arguments that should also hold out-of-sample.

We need to overcome three major challenges in the derivations of the probabilistic lower bound for the generalized correlation. First, we need to show that the estimated loadings converge uniformly to some rotation of the true loadings under the general approximate factor model assumptions.666We impose assumptions similar to Bai and Ng (2002). Uniform consistency of the estimated loadings is necessary for our argument that cross-section units with the largest estimated loadings have the largest probabilistic “signal” for the underlying factors. Second, the hard-thresholding procedure that sets most weights to zero to get the sparse factor weights has the down-side that we lose some of the large sample properties in the cross-section dimension. We need to take into account the cross-section dependency structure in the errors among a few cross-section units, which directly affects the noise level in calculating the generalized correlation. Third, the sparse factor weights, as well as proximate factors, are in general not orthogonal to one another in contrast to their non-sparse estimated version. A proximate factor for a specific population factor can also be correlated with other latent factors, which is reflected in the generalized correlation. Our assumptions and results need to take these complex inter-factor correlations into account.

In two empirical applications, we apply our method to a large number of financial portfolios and a large-dimensional macroeconomic dataset. We find that in both datasets, proximate factors with around 5-10% of the cross-sectional units can very well approximate the non-sparse PCA factors with average correlations of around 97.5%. The proximate factors explain almost the same amount of variation as the non-sparse PCA factors. The sparse factors have an economic meaningful interpretation which would be hard to obtain from the non-sparse representation. For example, in the portfolio data, the non-sparse PCA factor weights are nonzero for all 370 assets, which makes any interpretation challenging. In contrast, the 30 nonzero weights for the proximate factors are grouped together in portfolios with specific characteristics that allow us to assign an economic label to these factors. For example, we discover the well-known “momentum” factor as one of the latent factors.

Sparse loadings have already been employed to reduce the composition of factors and to make latent factors more interpretable. Most work formulates the estimation of sparse loadings as a regularized optimization problem to estimate principal components with a soft thresholding term, such as an penalty term or an elastic net penalty term (Zou, Hastie, and Tibshirani, 2006; Mairal, Bach, Ponce, and Sapiro, 2010; Bai and Ng, 2008; Bai and Liao, 2016).777Choi, Oehlert, and Zou (2010); Lan, Waters, Studer, and Baraniuk (2014) and Kawano, Fujisawa, Takada, and Shiroishi (2015) estimate the sparse loadings by minimizing the sum of the negative log-likelihood of the data with a soft thresholding term. An alternative approach is to take a Bayesian perspective and specify sparse priors for factor loadings and use Bayesian updating to obtain posteriors for sparse loadings (Lucas, Carvalho, Wang, Bild, Nevins, and West, 2006; Bhattacharya and Dunson, 2011; Kaufmann and Schumacher, 2019; Pati, Bhattacharya, Pillai, Dunson, et al., 2014). All these approaches assume that loadings are sparse in the population model, which allows these approaches to develop an asymptotic inferential theory. Nevertheless, the assumption of sparse population loadings may not be satisfied in many datasets. For example, the exposure to a market factor is universal and non-sparse in equity data. It is important to understand that this line of work typically does not distinguish between factor weights and loadings, i.e. it uses the shrunk loadings for factors weights and exposure. In contrast, we only estimate sparse factor weights, but non-sparse loadings. Additionally, we do not assume that the population factor weights are sparse. It is possible to adjust the sparse PCA method to make this important distinction between factor weights and loadings, i.e. loadings are obtained from a second stage regression. However, in contrast to our approach, there is no statistical theory explaining and justifying this adjusted sparse PCA approach in the same general setup that we are using. Furthermore, lasso-type estimators have the well-known shortcoming that they create biased estimates by the way how they are shrinking large elements and a similar non-optimal shrinking happens for sparse PCA. It turns out that sparse PCA performs substantially worse than our method in simulations and empirical applications.888Another method to increase the understandability and interpretability of factors is to associate latent factors or factor loadings with observed variables. Some latent factors can be approximated well by observed economic factors, such as Fama-French factors for equity data (Fama and French, 1992) or level, slope, and curvature factors for bond data (Diebold and Li, 2006). Fan, Ke, and Liao (2016) propose robust factor models to exploit the explanatory power of observed proxies on latent factors. Another approach is to model how the factor loadings relate to observable variables. Connor and Linton (2007), Connor, Hagmann, and Linton (2012), and Fan, Liao, and Wang (2016) at least partially employ subject-specific covariates to explain factor loadings, such as market capitalization, price-earning ratios, and other firm characteristics. However, in order to explain latent factors by observed variables, it is necessary to include all the relevant variables, some of which might not be known. Our sparse proximate factors can provide discipline on which assets and covariates to focus on.

The rest of the paper is structured as follows. Section 2 introduces the model and the estimator. Section 3 shows the consistency result for the estimated loadings and the asymptotic probabilistic lower bound for the generalized correlation. Section 4 presents simulation results. In section 5 we apply our approach to financial and macroeconomic data. Section 6 concludes the paper. All proofs and additional empirical results are delegated to the Internet Appendix.

2 Model Setup

2.1 Estimator

Suppose we observe a large dimensional panel data set with units over time periods, where both and are large. Furthermore, suppose has a latent factor structure with common factors:

| (1) |

where , , and are common factors, factor loadings, and idiosyncratic components which are all unobserved.999We assume that we have consistently estimated the number of factors . A -factor model can be estimated from the panel data by PCA. The PCA factors and loadings minimize a quadratic loss function

| (2) |

where is the observation of the -th cross-section unit at time , is the factor value at time , and is the factor loading of the -th cross-section unit. Latent factors and loadings are only identified up to an invertible transformation: For any invertible matrix , and specify the same factor model as in (1). Under the standard identification assumption that is an identity matrix and is a diagonal matrix, the solution to the optimization problem (2) is the PCA estimate101010We refer to as a sample covariance matrix and as in our applications we first demean the data. However our theoretical and empirical results are only based on the spectral decomposition of a second moment matrix and hold for general nonzero means. Lettau and Pelger (2020a) provide an answer when to demean the data.

| (3) | |||

| (4) |

The estimated loadings are the eigenvectors of the -largest eigenvalues of multiplied by . The estimated factors are the coefficients from regressing on . denotes a diagonal matrix with the largest eigenvalues in descending order. Note, that serves two purposes here: First, the estimated loadings are the cross-sectional weights to construct the estimated factors as shown in equation (4). Second, is also the estimated exposure to the factors. Bai (2003) shows that in an approximate factor model, and are consistent estimators of and up to an invertible transformation.

The general approximate factor model framework assumes that the loadings and thus their consistent estimator are not sparse, which is a necessary assumption for a consistent estimator of the factors in the presence of noise . Here sparse means that only a finite number of elements in the loadings are nonzero that does not grow with and . As the estimated factors are linear combinations of the cross-section units weighted by a non-sparse , they are composed of almost all cross-section units, which are hard to interpret.

We propose a method to estimate proximate factors that are sparse and hence more interpretable. The method is based on the following steps:

-

1.

Sparse factor weights: are the standard PCA estimates of the loadings. The proximate factor weights are the largest elements in obtained as follows: We shrink the smallest entries in absolute values in each estimated loading vector to 0 and only keep the largest elements to get the sparse weight vector for each , where is finite. We normalize each sparse weight vector to have length one, that is, . 111111Formally, denote as a mask matrix indicating which factor weights are set to zero. has 1s and 0s. The sparse factor weights can be written as (5) where is -th estimated loading. The vector has the element 1 at the position of the largest loadings of and zero otherwise. denotes the Hadamard product for element by element multiplication of matrices.

-

2.

Proximate factors: We regress on to obtain the proximate factors :

(6) -

3.

Loadings of proximate factors: We regress on to obtain the loadings of the proximate factors:

(7)

Proximate factors approximate latent factors well as measured by the generalized correlation. The generalized correlation equals the correlation between appropriately rotated proximate and population factors as defined in the subsequent sections. It is natural to measure the distance between two factors by their correlation. If two factors are perfectly correlated they explain the same variation in the data and provide the same results in linear regressions.

2.2 Illustrative Example

We illustrate the intuition in a one-factor model. In this case, the generalized correlation is equal to the squared correlation between and . For simplicity, assume that the factors and idiosyncratic component are i.i.d. over time, that is and . Furthermore, our proximate factor consists of only one cross-sectional observation, i.e. . Without loss of generality, the nonzero entry in is which is normalized to . The squared correlation between and equals

where denotes the signal-to-noise ratio.121212The second equation follows from . The correlation increases with the size of and the signal-to-noise ratio . If the largest population loading is sufficiently large, the correlation will be close to one. In the rest of the paper, we formalize this idea under a general setup. In the first part we discuss the proximate factors based on the largest loadings. Then, we generalize the idea to select the weights with the largest information content relative to the noise.

2.3 Assumptions

We impose several assumptions that are close to, but slightly stronger than, those in Bai and Ng (2002). In order to show that is “close” to as measured by the generalized correlation, needs to be a uniformly consistent estimator for up to some invertible transformation. The following assumptions are necessary for all theorems in this paper and are standard assumptions for the general approximate factor model.131313Assumption 1 about the population factors is the same as Bai and Ng (2002). Assumption 2 allows loadings to be random. Since the loadings are independent of factors and errors, all results in Bai and Ng (2002) hold. Assumption 3.1 imposes moment conditions for errors, which is the same as Assumption C.1 in Bai and Ng (2002). This assumption implies that is bounded. Assumption 3.2 is close to Assumption 3.2 (i) and (ii) in Fan, Liao, and Mincheva (2013). This assumption restricts the cross-section dependence of errors and is standard in the literature on approximate factor models. Since is symmetric, is equivalent to . implies that . Together with being the same for all from the stationarity of , this assumption implies Assumption C.3 in Bai and Ng (2002). Assumption 3.3 allows for weak time-series dependence of errors, which is slighter stronger than Assumption C.2 in Bai and Ng (2002). Assumption 3.6 is the time average counterpart of Assumption C.5 in Bai and Ng (2002). Assumption 4 implies Assumption D in Bai and Ng (2002). The fourth moment conditions in Assumptions 3.6 and 4, together with Boole’s inequality or the union bound, are used to show the uniform convergence of loadings, without assuming the boundedness of loadings. Since Assumptions 1-4 imply Assumption A-D in Bai and Ng (2002), all results in Bai and Ng (2002) hold.. We assume that there exists a positive constant that can be used in all the assumptions. For a matrix we define the Frobenius norm as , the -norm as and spectral norm as where is the largest singular value of .

Assumption 1 (Factors).

and for some positive definite matrix .

Assumption 2 (Factor Loadings).

and for some positive definite matrix . Loadings are independent of factors and errors.

Assumption 3 (Time and Cross-Section Dependence and Heteroskedasticity).

Denote

, . Then for all and ,

-

1.

, ;

-

2.

is stationary, is the covariance matrix of with ;

-

3.

, for some , ;

-

4.

.

Assumption 4 (Moments).

For all , .

We use to denote the maximum of the square root of total pairwise squared correlations among cross-section units. Since each proximate factor is a linear combination of cross-section units, the estimation error of the proximate factor is determined by the errors of these cross-section units. Note that if is i.i.d, then . If the errors of the cross-section units are perfectly dependent, . In general it holds that .

3 Theoretical Results

3.1 Consistency

Bai and Ng (2002) and Bai (2003) show that factors and loadings can be estimated consistently with PCA under Assumptions 1-4 when . A key element is that the loadings are pervasive which implies that , because the errors can be cross-sectionally diversified away. Here is the conventional invertible rotation matrix.

However, consistency does not hold in general for proximate factors for the following reason:

and where is the index of the -th largest element in , that is, the sums are only taken over the finite number of nonzero weight entries. Even in the special case when the idiosyncratic components are i.i.d with variance , the variance of the -th entry in is , which does not vanish as . In summary, PCA factors average the idiosyncratic component over infinitely many non-sparse loadings leading to a law of large numbers, while for proximate factors this average is taken over only a finite number of elements without diversifying away the noise. Although proximate factors are in general inconsistent, they can still be very close to the population factors. We will show under which conditions the correlations between the population and proximate factors are very close to one.

3.2 Loadings of Proximate Factors

The estimated loadings of the proximate factors asymptotically span the same space as the population loadings and hence will lead to the same regression or projection results. Hence, up to an invertible transformation, the loadings of the proximate factors are consistent.141414Note, that our notion of consistency does not imply point-wise consistency, i.e. for a finite number of cross-section units the loadings can be distinct. This result actually does not depend on the degree of sparsity . The key element is that the loadings are obtained in a second stage regression that diversifies away idiosyncratic noise in the time dimension. Hence, it is important to distinguish between loadings and factor weights as sparse loadings are in general not consistent estimator of the population loadings.

One of the major problems when comparing two different sets of loadings is that a factor model is only identified up to invertible linear transformations. Two sets of loadings represent the same model if the loadings span the same vector space. As proposed by Bai and Ng (2006) the generalized correlation is a natural candidate measure to describe how close two vector spaces are to each other. Intuitively, we calculate the correlation between the loadings of the proximate and the population factors after rotating them appropriately. The generalized correlation measures of how many loading vectors two sets have in common. The generalized correlation between the loadings of proximate and population factors is defined as

Here, the generalized correlation , ranging from 0 to (number of factors), measures how close and are. If lies in the space spanned by , then . Otherwise, if the space spanned by is orthogonal to the space spanned by , then .151515The generalized correlation is also known as canonical correlation. Our measure is based on the Euclidian inner product without demeaning the loadings which is appropriate for measuring the span of the loading matrix. Our generalized correlation measure is the sum of the squared individual generalized correlations. The first individual generalized correlation is the highest correlation that can be achieved through a linear combination of the proximate loadings and the population loadings . For the second generalized correlation, we first project out the subspace that spans the linear combination for the first generalized correlation and then determine the highest possible correlation that can be achieved through linear combinations of the remaining dimensional subspaces. This procedure continues until we have calculated the individual generalized correlations. Mathematically the individual generalized correlations are the square root of the eigenvalues of the matrix .

Bai and Ng (2002) and Bai (2003) show that the PCA loadings are consistent estimators of the rotated loadings . The rotation matrix is defined as based on the spectral decomposition , that is, are the eigenvalues of in decreasing order and are the corresponding eigenvectors. If the population factor model has the same rotation as the PCA estimates, that is, is diagonal and then simplifies to an identity matrix. In this case, the generalized correlation simplifies to the sum of squared correlations between the vectors of estimated and population loadings.

The rotation is relevant as our factor weights are only close to the largest rotated population loadings . Our results depend on Proposition A.1 in the Appendix that shows the uniform consistency of the estimated loadings. Hence, weights based on the largest estimated loadings are asymptotically very close to weights derived from the largest rotated population loadings . We denote by the matrix of the largest factor weights based on the rotated population loadings, i.e. it follows the same definition as but applied to the population loadings .

We need to impose one additional weak assumption on the residuals:

Assumption 5.

The largest eigenvalue of is .

Assumption 5 is very weak and essentially satisfied in any sensible approximate factor model. It is standard and has been imposed in many related papers, e.g., Fan, Liao, and Mincheva (2013). It is slightly stronger than Assumption 3.3, that implies that the largest eigenvalue of the population residual auto-covariance matrix is bounded. Under suitable additional assumptions on the tail behavior of the residuals, Assumption 3.3 implies that is which would be sufficient.

The assumption that is essentially a full rank assumption on . It requires that the sparse set of cross-section units, which we use to construct the proximate factors, is affected by all factors in a non-redundant way. In the case of only one factor, i.e. , it is trivially satisfied. In the case of multiple factors, we need to rule out that the largest elements of two loading vectors are identical. This is an assumption on the tail dependency of the loadings. If for example the loading vectors are independent and , then this condition is satisfied.

Our notion of consistency does not imply point-wise consistency of the loadings, i.e., for a finite number of loading elements can be different from . Our notion of consistency measures the asymptotic difference between vectors whose length goes to infinity and hence a finite number of elements have a negligible effect. The generalized correlation measure is the appropriate measure if we intend to use loadings for projections or in a cross-sectional regression. The strong result in Theorem 1 states that cross-sectional regressions with loadings of proximate factors yield the same results as using the population loadings up to an invertible matrix . Note that this theorem has broader implications that go beyond proximate factors. For example, it justifies why an iterative procedure to estimate latent factors leads to a consistent estimator after a few iterations.161616Instead of applying PCA, latent factors can also be estimated by an iterative procedure where for a set of candidate factors a first stage set of loadings is estimated with a time-series regression, which is then used in a second stage to obtain factors in a cross-sectional regression. This procedure is iterated until convergence. For example, Bai and Ng (2019) use a variation of this approach. Our result shows that in an approximate factor model one step is sufficient to obtain a consistent estimator of the loadings. Next, we will show that the proximate factors themselves are also very close to the population factors.

3.3 One-Factor Case

We start with the one-factor model and characterize the correlation between population and proximate factors with a lower bound based on order statistics. Under additional assumptions, we can give explicit expressions for these order statistics with counting statistics and extreme value theory. In both cases, we derive analytical solutions for the lower bound. We use the results for comparative statics and preparing for the more general case.

The properties of the proximate factors depend on the probabilistic properties of the largest loadings that are used as weights. We denote by the -th largest element in . Theorem 2 provides a closed-form lower bound on the squared correlation between proximate factors and population factors, , in terms of the probability distribution of the -th largest loading , the signal strength and the noise level .

Theorem 2.

Theorem 2 guarantees that the squared correlation is above the target threshold with at least the probability . In practice we might set the probability bound to 95% and find the lower bound for the correlation . This theorem allows us to derive comparative statics about when proximate factors work well. Denote the right-hand side of Inequality (8) as . Given a limiting order statistic for the loadings, the exceedance probability depends only on :

-

1.

The larger , the larger and the smaller the exceedance probability ;

-

2.

The larger the signal-to-noise ratio , the smaller and the larger ;

-

3.

The larger the cross-section dependence of errors , the smaller ;

-

4.

The number of nonzero elements affects in two ways: First, in most cases, decreases with , which raises . Second, larger results in more subtraction terms in with the opposite effect leading to a trade-off.

If the population loadings are i.i.d., then we can provide an explicit expression for in (8). Furthermore, if the loadings have unbounded support, the correlation between the proximate and population factor converges to one.

Proposition 1.

Proposition 1 states that if the loadings have unbounded support, then the correlation between the proximate and population factor converges to one. At a first glance, it seems to be at odds with our previous observations that the idiosyncratic component in a proximate factor cannot be diversified away. The intuition behind this consistency result is based on the growing signal-to-noise ratio. If loadings are sampled with an unbounded support independently of the idiosyncratic component, then for growing the largest loadings are unbounded and their signal-to-noise ratio explodes. Hence with high probability, the largest absolute loadings do not coincide with large idiosyncratic movements and the variation of these cross-section units is essentially only explained by the factor. Hence, selecting the cross-section unit with the largest loading is close to picking the factor itself. Proposition 1 shows that a more dispersed distribution of leads to a larger , where the unbounded support is just an extreme case of this observation.

After proper rescaling, loadings with unbounded support can also be interpreted as approximately sparse population loadings. If some loading elements diverge and we normalize , a large number of elements in need to converge to 0. Hence, a sparse estimator is consistent if the true population model is sparse itself. The important contribution of this paper is that we can also characterize the asymptotic properties of the sparse estimator if the population model is not sparse.

A more general perspective for providing a lower bound for employs EVT, which relaxes the i.i.d. assumption of and which we will also pursue for the multi-factor case. The distribution of the largest loadings can be modeled by EVT under general conditions. We denote the loading with the largest absolute value by . Under the assumptions of EVT, there exist sequences of constants , such that with the generalized extreme value (GEV) distribution . The three parameters location , scale and shape completely characterize the GEV. The results for the -th largest loading in the case of dependent loadings is more complex and summarized in Lemma A.1 in the Appendix.171717Lemma A.1 is adapted from Theorem 3.3 in Hsing (1988). is indexed by the cross-section units. We assume that are exchangeable and can be properly reshuffled to satisfy the strong mixing condition. Lemma A.1 provides the limiting distribution for the extreme order statistic of a strictly stationary sequence satisfying a strong mixing condition. In more details, it provides the necessary and sufficient condition such that there exists a sequence and function with .

Proposition 2.

Suppose Assumptions 1-4 hold and the population loadings and sequence satisfy the assumptions in Lemma A.1. Then, the -th largest loading satisfies and the result in (8) holds with equal to

| (10) |

for . Both and the constants are determined by ’s distribution and its dependence structure.

The result simplifies for i.i.d. loadings. Suppose Assumptions 1-4 hold, is i.i.d. and there exist sequences , such that converges to a non-degenerative distribution function. Then, , in Equation (10) and Theorem 2 holds with

| (11) |

The extreme value parameters and are determined by the distribution of .

The sequences and determine to which of the three extreme values distributions, Gumbel, Frechet and Weibull, the tail distribution of belongs. Table 1 lists examples for common distributions and the corresponding extreme value parameters. If the distribution of the loadings is known, its parameters can be estimated with maximum likelihood and for many distributions, the bounds in Proposition 2 can be directly inferred. More generally, the parameters of the GEV distribution can be estimated with block maxima methods as described in Ancona-Navarrete and Tawn (2000), Leadbetter (1982) and Hsing (1988).

| Family | Distribution | ||||||

|---|---|---|---|---|---|---|---|

| Gumbel | 1 | 0 | 1 | 0 | |||

| 0 | 1 | 0 | |||||

| 0 | 1 | 0 | |||||

| Frechet | 0 | 1 | 1 | 1 | |||

| Weibull | 1 | 1 | 1 |

3.4 Multi-Factor Case

The arguments of the one-factor model extend to a model with multiple factors. As our simulations and empirical results illustrate, the simple thresholding method provides proximate factors that explain very well the non-sparse PCA factors. However, formalizing the properties of the lower bound is more challenging. First, we have to work with generalized correlations instead of simple correlations to take into account the possible rotations of the latent factors. Second, the sparse factor weight vectors are in general not orthogonal to each other in contrast to the PCA-loadings. Third, we need to study the joint distribution of extreme values for multiple loading vectors. In order to derive analytical bounds, we need to include additional correction terms. Under additional assumptions, we can sharpen the theoretical bounds and neglect the correction terms.

One of the major problems when comparing two different sets of factors is that a factor model is only identified up to invertible linear transformations. We will again use the generalized correlation to measure how many factors two sets have in common. The generalized correlation between proximate factors and population factors is defined as

Here, the generalized correlation , ranging from 0 to the number of factors , measures how close and are. If lies in the space spanned by , then .181818The individual generalized correlations are the square root of the eigenvalues of the matrix .

The multivariate bounds in Theorem 3 have three adjustments relative to the one-factor model. The first adjustment arises from using the generalized correlation measure. Hence, we derive bounds on the sum of eigenvalues instead of a simple correlation. These bounds use eigenvalue inequalities which essentially change the value of in the one-factor case in Theorem 2. The second complication arises because the sparse weights are in general not orthogonal to each other. We will subtract a correction term from the lower bound that provides a bound on this effect. If the proximate weights are “non-overlapping”, that is, do not share nonzero entries for the same indices, the correction term vanishes. The third complication in the multi-factor case is the relationship between the sparse and non-sparse eigenvectors. As is in general not a diagonal matrix we need to take the off-diagonal elements into account which adds a second correction term to the lower bound. Under additional assumptions on the population loadings and non-overlapping sparse weights, we can also neglect this correction term. Below we illustrate the intuition behind these correction terms with an example.

Theorem 3.

Suppose Assumptions 1-4 hold and there exists a continuous function such that the joint -th order statistic for the columns in , denoted as , follows . Then for any given finite , , and we have

| (12) |

where are the eigenvalues of in decreasing order and

is the minimum singular value of and is the index of the -th largest element in . are the sparse weights based on the rotated population loadings and where if there exists such that and 0 otherwise.

In the proof of Theorem 3 we show that the generalized correlation can be bounded from below by . If the two matrices that appear in this product converge to diagonal matrices, then both correction terms disappear.

The additional parameter accounts for the impact of the off-diagonal terms to the trace of the matrix . In the special case when these off-diagonal terms converge to zero, it holds that and for . In order to illustrate this point we will consider the simple example of and , i.e. a two factor model where the proximate factors only take the largest loading values. Without loss of generality, we assume the first element is the largest element for the first vector and the second element is the largest element for . Then, we have

The smallest singular value of the matrix is a measure for how large the off-diagonal elements are. In the special case of a diagonal matrix , the smallest singular value equals 1. Our lower bound will depend on an asymptotic probabilistic bound for , which depends on the distribution of the loading vectors. For example in the special case of independent vectors , that have i.i.d normally distributed elements, a random element of the rotated loading vector is , while the largest element is unbounded in the limit. Hence, the ratio is . For this special case the multi-factor case is a direct extension of the one-factor model, i.e. we can apply the one-factor result to each factor in the multi-factor model individually. Another special case is when the population loadings have sparse structures themselves. More specifically, it is sufficient to have non-overlapping weight vectors and “locally sparse” , that is, the vector has elements that are sufficiently small for the indices of nonzero elements of . In both special cases we have while our theorem allows us to also take into account a more complex structure.

The additional parameter accounts for the impact of the off-diagonal terms in . In the special case of non-overlapping entries in , it holds for that and hence we can neglect this term. This is implied by independent loading vectors. In that case the joint -th order statistic for the columns also simplifies to the product of the marginals as summarized by the next proposition.

Proposition 3.

Suppose Assumptions 1-4 hold, and are asymptotically independent for , and there exists a continuous function such that the -th order statistic for each column follows . Then Inequality (12) simplifies to

| (13) |

If each column satisfies the assumptions of Proposition 2, then each equals Equation (10) for dependent and Equation (11) for i.i.d. .

The same comparative statics holds as in the one-factor case. In addition, the bound is sharper if the rotated loadings for different factors have less dependence and share fewer nonzero entries.

Our analysis uses the conventional PCA rotation of the loadings that implies . All our results extend to any arbitrary rotation of the PCA loadings where is a full-rank matrix. We simply replace the estimated PCA loadings by , the rotated population loadings by and rotated population factor by and all theorems and propositions continue to hold. Theorem 3 provides guidance on how to choose a rotation that provides proximate factors with a higher guaranteed correlation. If the estimated weights are non-overlapping we can avoid or at least reduce the correction terms which increases the correlation. However, this can come a cost of taking loading elements with lower absolute value and hence lower signal to noise ratio. Our theorem provides the exact trade-off between these choices.

3.5 Weighted Proximate Factors

Weighted proximate factors are a generalization of our approach to select more informative sparse weights. It is motivated by the observations that the cross-sectional units with the largest loadings relative to the standard deviation of the idiosyncratic noise should provide a better approximation to the factors. We estimate the weighted proximate factors by applying a cross-sectional weight to the observations before extracting the PCA factors and selecting the largest weights. This is different from selecting a rotation of the PCA factors as discussed in the previous section.

We denote by a cross-sectional weight matrix. The weighted proximate factors are obtained from a weighted PCA. First, we cross-sectionally re-weight the observations and then apply PCA to to obtain the weighted PCA loadings .191919Note that the weighted PCA loadings need to be multiplied by to be consistent estimates for the population loadings up to the usual rotation matrix. Second, we apply the same procedure as in Section 2.1 to obtain the sparse weighted factors weights that have nonzero elements and length 1. Third, we regress on to obtain the proximate factors :

| (14) |

Finally, the loadings of the proximate factors are the coefficients of the regression of on :

| (15) |

We propose to use the inverse of the standard deviation of the residuals as weights. This choice is motivated by efficiency arguments and can also improve the efficiency for the non-sparse weighted PCA. Bai (2003) shows that under the assumptions of an approximate factor model and for the estimated PCA loadings follow the same distribution as an OLS regression of the population loadings on :

Let us set . It is straightforward to show that the weighted PCA factors from a regression of on have the same distribution as the following generalized least square regression

Under additional assumptions on the residuals this choice of the weighting matrix will lead to the most efficient pointwise estimator for the factors while the estimator for the loadings is not affected by the weighting.202020The efficiency argument requires that the time and cross-sectional dependency of the residuals can be separated. This would be satisfied if residuals are generated as where the matrix has i.i.d. entries and the weak cross-sectional correlation is captured by the matrix , while the matrix captures the time-series correlation. However, estimating the large dimensional residual covariance matrix is challenging and appears to be empirically unstable.212121There are various shrinkage estimator for estimating a large dimensional residual covariance matrix, for example the hard-thresholding estimator proposed in Fan, Liao, and Mincheva (2013). A simpler and more stable weighting matrix is the diagonal matrix with the inverse noise standard deviations as diagonal elements as proposed by Jones (2001) and Boivin and Ng (2006). A simple consistent estimator is based on the diagonal elements of . This would result in the most efficient estimator if the residuals are uncorrelated. Under heteroskedastic and correlated residuals it could still be more efficient. The result is analogous to weighted and generalized least square regressions.

Under heteroskedastic noise the most informative proximate weights should be the largest loadings after reweighing them by the noise standard deviation. Using the same setup as in the toy example in Section 2.2 but with and the nonzero weight for unit , the correlation is maximized by the largest :

Proposition 4 provides a complete characterization for the generalized correlation between the weighted proximate factors and the population factors for diagonal weighting matrices.

Proposition 4.

Suppose Assumptions 1,3 and 4 hold, the weighting matrix

is a diagonal matrix with for all , and Assumption 2 holds for the weighted loadings .

In the one-factor case, we assume that the -th order statistic of , denoted by , satisfies for some continuous function . Then Inequality (8) in Theorem 2 continues to hold with

| (16) |

where and . If then

In the multi factor case, we assume that the -th order statistic for each weighted column denoted as satisfies for some continuous function . Then Inequality (12) in Theorem 3 continues to hold with replaced by and replaced by . If then

The proposition states that in the one-factor case the weighted proximate factor based on the inverse noise standard deviation will always have a higher correlation bound than the unweighted proximate factor. In this sense the weighted proximate factor strictly dominates. The situation is more complex in the multi-factor case. There are three terms in (12) and we can always improve the first term using the weighted approach with the inverse standard errors. However, the comparison is unclear for the second and third terms because these two terms involve maximum and minimum eigenvalues of matrices determined by the distribution of rotated loadings and the weighting itself can change the distribution. Our simulation and empirical analyses indicates that the weighted proximate factors always perform at least as well as the unweighted proximate factors.

3.6 Number of Nonzero Elements

The results for the multi-factor model generalize to different levels of sparsity for each proximate factor. To simplify the presentation of the results, we have used the same number of nonzero elements for each of the proximate factors. When we use a different number of nonzero elements to construct each proximate factor , the asymptotic bounds have to be modified as explained by the following proposition.

Proposition 5.

We will show in our empirical results that stronger PCA factors can usually be approximated well with fewer nonzero units compared to weaker PCA factors. This result directly follows from the theoretical bounds with factor specific sparsity .

In order to select the number of nonzero elements in the proximate factors, we propose two approaches. First, we use the theoretical results to choose that achieves a target probabilistic lower bound for the generalized correlation. In our empirical analysis we set the probability lower bound to 95% and calculate the generalized correlation that is achieved with at least 95% for different , that is, . Then, we select to achieve a target generalized correlation. As we show in the simulations and empirical data there is typically a sharp increase in the correlation by setting to 5-10% of the data but only minor increases by including more observations. Second, we use a completely data-driven approach. We estimate the average generalized correlation between the estimated PCA factors and our proximate factors and set to achieve a target correlation. This second approach can be implemented on a training data set to obtain the factor weights and the nonzero elements and then evaluated out-of-sample on test data. We also pursue this second approach in our empirical analysis. We confirm again that for our applications 5-10% of the observations are sufficient to replicate the PCA factors very well.

3.7 Comparison with Sparse PCA

Our method is closely related to using Lasso (Tibshirani, 1996) to sparsify loadings estimated from PCA. Most papers about estimating sparse principal components are more or less related to the method proposed by Zou, Hastie, and Tibshirani (2006). They estimate sparse loadings by adding an penalty term222222A generalization is to add an penalty term which leads to an Elastic Net penalty (Zou and Hastie, 2005). to the objective function (2) yielding the formulation

Both methods, proximate factors and sparse PCA, are easy to implement. However, our method is different from sparse PCA in three aspects. First, our method does not impose the sparsity assumption on the loadings. The sparse factor weights are used to construct the proximate factors. However, the loadings of the proximate factors are in general non-sparse. It is a key insight of our paper that the factor weights and loadings should be treated differently. Second, even though all methods have tuning parameters, these parameters work differently. In our method, is the number of nonzero entries in each factor weight vector. Although in Lasso controls the sparsity of loadings, cannot control the exact number of nonzero entries in individual loadings.232323The number of nonzero elements in all loadings for the Lasso estimator is monotonically decreasing in the parameter . Hence, under certain conditions, there is a one-to-one mapping between the level of sparsity of the full loading matrix and the penalty weight. However, except for special cases, cannot control the sparsity of a specific loading vector. Using different penalties for different loading vectors allows for more control for the sparsity level in a specific loading vector, but it is not straightforward and not always possible to select any desired sparsity level. Third, the thresholding in our approach is essentially a variable selection without changing the proportion of the largest weights, while the shrinkage in sparse PCA selects and rescales the largest loadings. It is well-known that a Lasso estimator is biased because it scales down the population parameters. A similar phenomenon occurs with sparse PCA where the largest elements in each loading vector are scaled differently. For a simple case, we can show in Proposition 6 below that this downscaling makes sparse PCA factors always worse than our proximate factors that do not suffer from this bias.

We want to point out that the comparison between sparse PCA and our proximate factors is not the key element of this paper. Our important insight, that factor weights are different from factor loadings, could also be taken into account with sparse PCA methods, that is, the sparse PCA loadings can be used as factor weights and the loadings could be obtained from a second stage regression. This is different from how sparse PCA is considered in the literature. The important contribution of our paper is to provide a statistical framework for a sparse estimator of a non-sparse population model which is missing for sparse PCA. Furthermore, our method gives applied researchers more control over setting a desired sparsity level for individual factors and is very transparent in its application.

We consider now the special case of a one-factor model with cross-sectionally i.i.d. distributed errors. For sparse PCA with penalty similar to Jolliffe, Trendafilov, and Uddin (2003) we can map this estimator into our framework. In more detail, we estimate the loadings by minimizing and use them as weights to construct the sparse PCA factors . The difference in the generalized correlation between the our method and sparse PCA is

| (18) |

Proposition 6.

Assume a one factor model and . The two tuning parameters and are chosen such that proximate factors and sparse PCA select the same number of nonzero elements. As , we have with probability one .

4 Simulation

We evaluate proximate factors (PPCA), weighted proximate factors (PPCA (wt)) based on inverse standard errors, and sparse PCA (SPCA). We confirm that proximate factors are a very good approximation of the population factors and that the lower bounds are an accurate description of the exceedance probabilities for the generalized correlations.

Our baseline model assumes

In this model errors are heterogeneous. 242424We also simulate data with time-series dependence or with cross-section dependence in the errors. The results are presented in Section IA.D in the Internet Appendix. We study the impact of varying , , and . For each set of parameters and a fixed threshold , we run 1000 Monte-Carlo simulations to calculate the empirical probability of by counting the percentage of times that .

4.1 Probabilistic Bounds

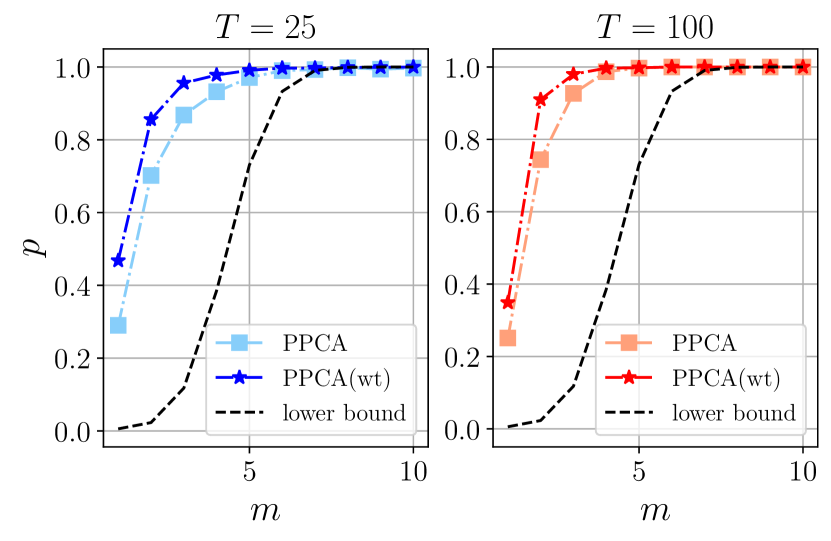

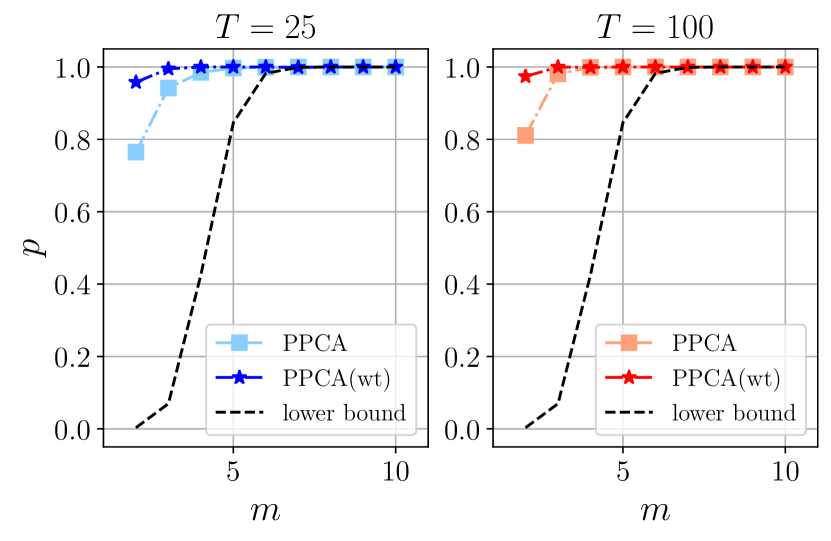

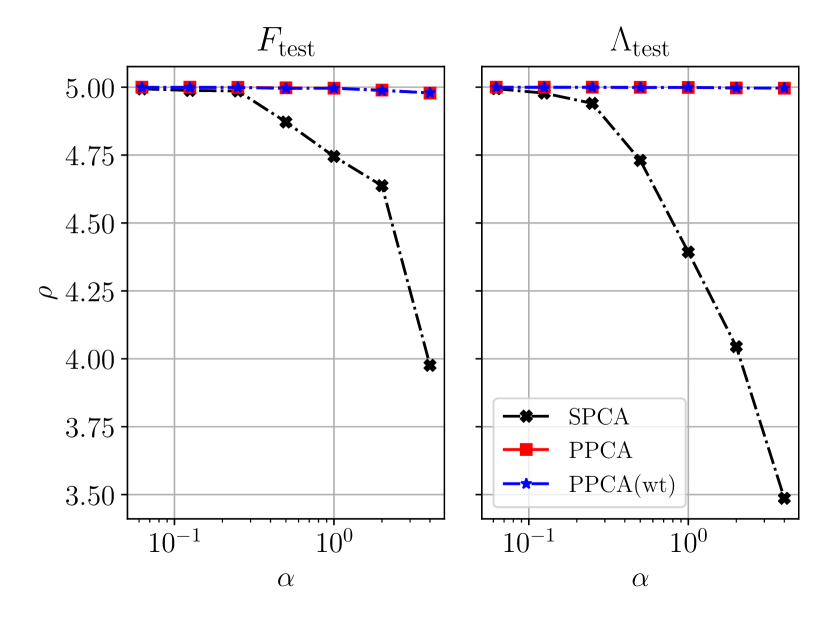

We start with the case of only one factor and study the probability bound provided in Theorem 2 and Proposition 2. We set for the squared correlation which means that we want to evaluate the probability that the proximate factors have correlation of at least 97.5% with the population factors. The probabilist lower bound depends on which in our setup simplifies to as and . Equation (11) and the GEV for in Table 1 simplify the expression for :

| (19) |

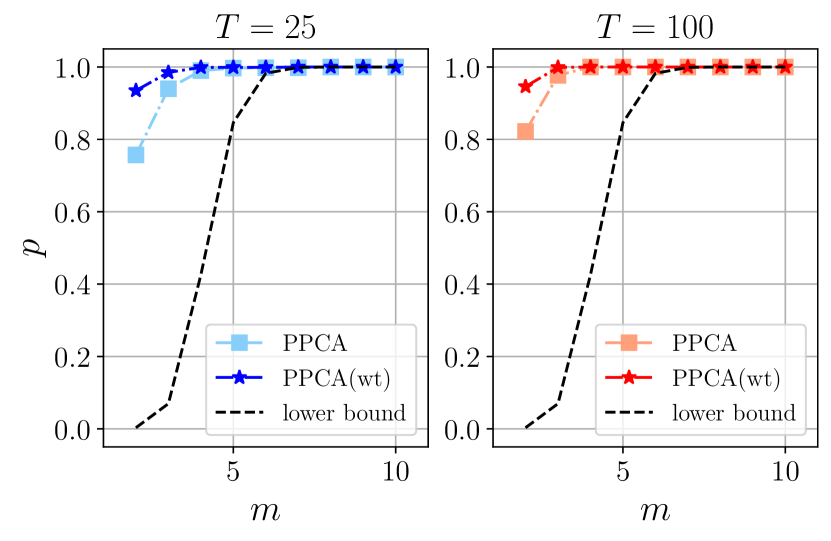

Figure 1 shows how and change with different , and signal-to-noise ratio . First, all probabilities are monotonically increasing in , that is, less sparse factors are closer to the population factors. Second, there is a sharp incline in probabilities for but then becomes very close to 1. This means that has 97.5% correlation with , but is based on less than 10% of all observations. Third, in both cases the lower bound closely approximates the probability for and hence can be used for guidance on evaluating the proximate factors. Fourth, the larger the signal-to-noise ratio, the larger and . Fifth, proximate factors are more highly correlated with the population factors for larger . Equation (8) has an term and this term decreases with . Last but not least, the weighted proximate factors perform better in this setup with heteroskedastic errors.

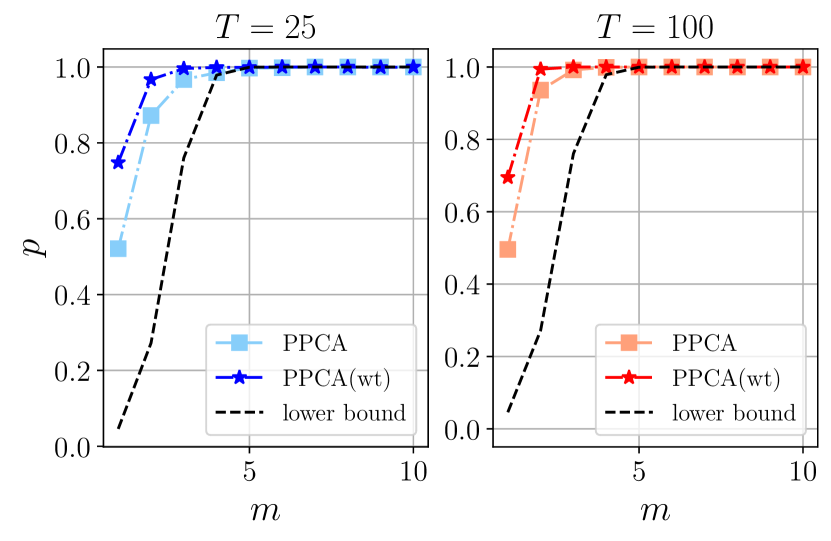

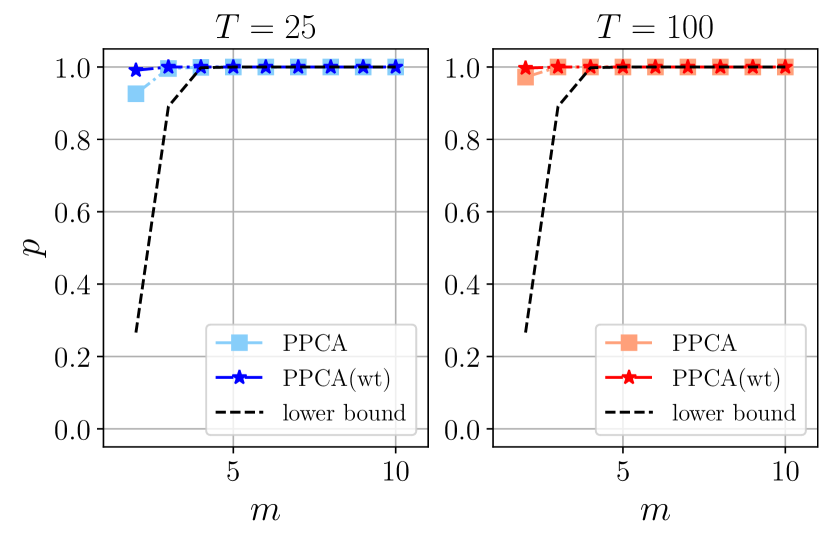

Figure 2(a) shows that, as increases, both and converge to 1 with only nonzero weight elements. This confirms our result in Proposition 1. As is normally distributed with unbounded support, our approach selects the units that are themselves very close to the population factors.

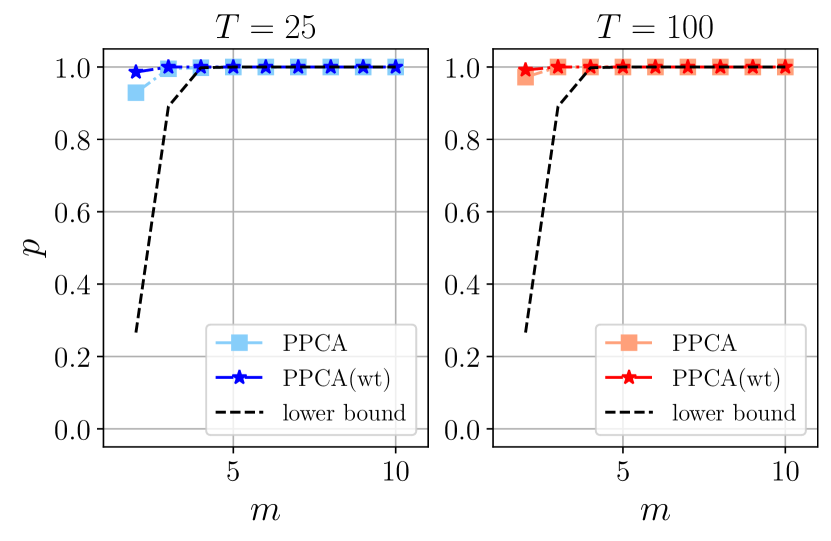

Next, we consider the case of two factors, i.e. and study the probability bound provided in Theorem 3 and Proposition 3. We set and assume that the factors are independent with . For independent and normally distributed loadings the non-overlapping condition is satisfied and the correction terms in (13) can be neglected. We set , which simplifies the bound to

| (20) |

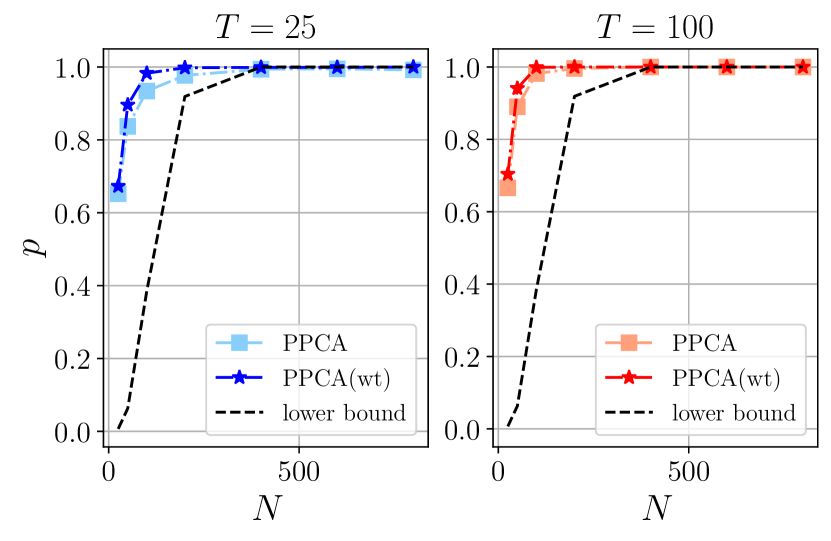

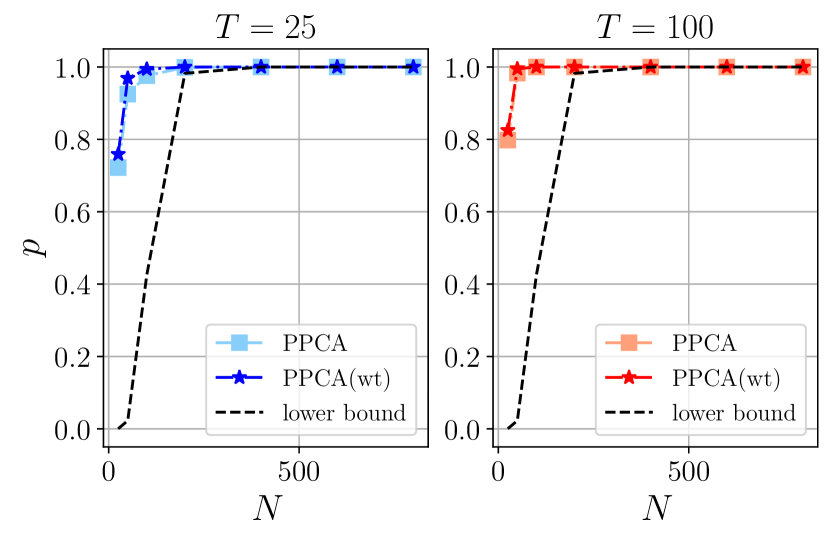

In our special case and take the same form as in the one-factor case in 19. Figure 3 displays the probability and as a function of for different and factor variances in the multi-factor case. All the results from the one-factor case carry over to multiple factors.

4.2 Comparison with Sparse PCA

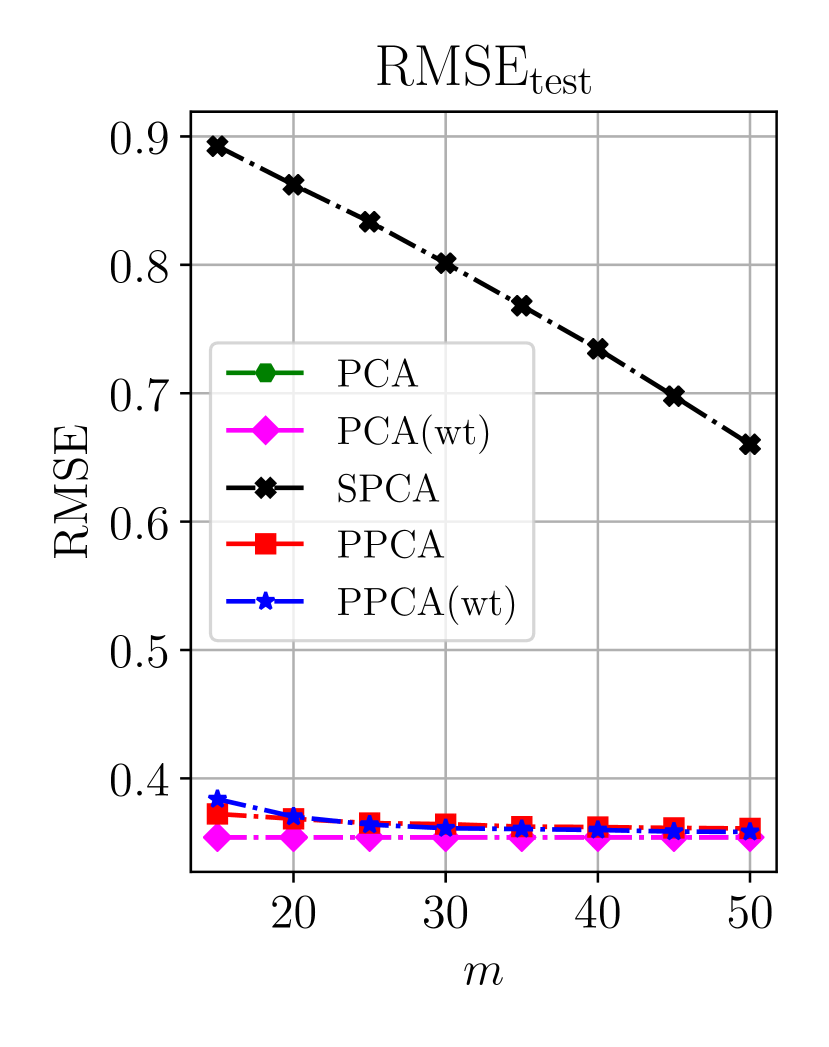

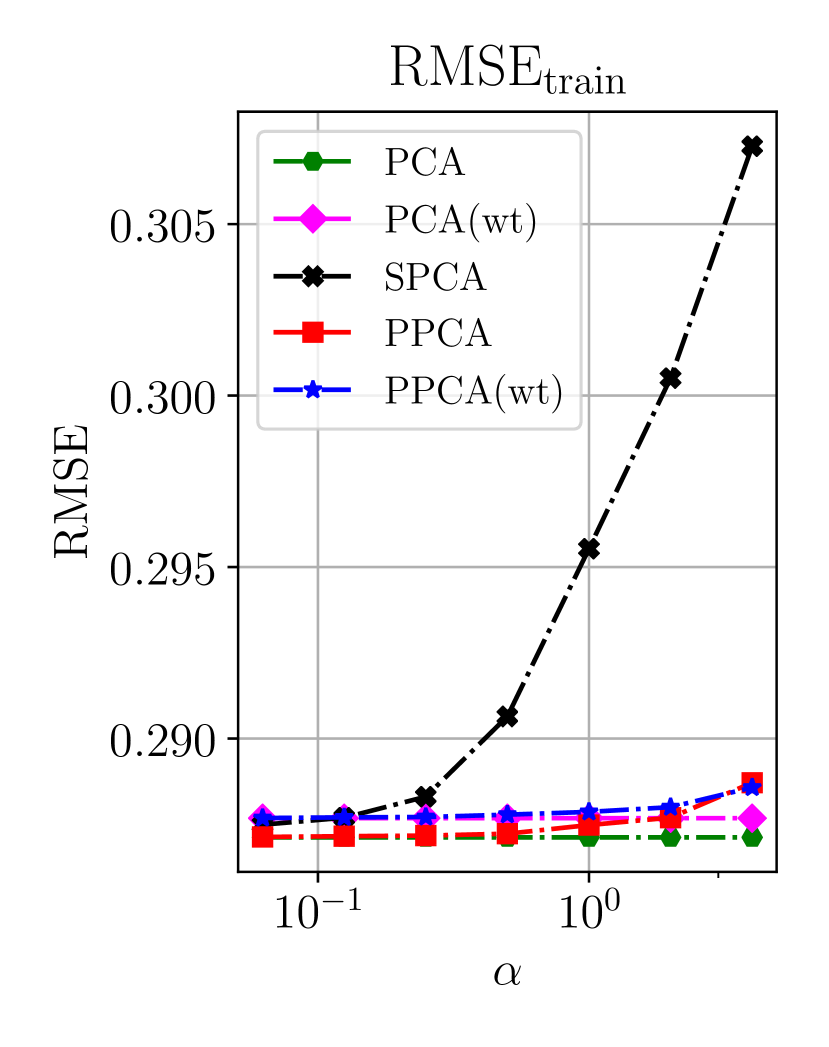

We compare the estimation of the factors, loadings and the common component of our methods PPCA and PPCA (wt) with SPCA. We have already shown theoretically that in the special case of a one-factor model with homoskedastic errors, the proximate factors provide a better estimator for the population factors than sparse PCA. We consider now the more general setting of multiple factors with dependent and heteroscedastic errors. For the various estimators we calculate the generalized correlation of estimated factors and loadings with the population values and also calculate the root-mean-squared error (RMSE),

for different estimators and . The loadings for PPCA and PPCA (wt) are obtained from a second stage regression on the factors as specified in (7) and (15). The SPCA factor and loadings are the solution to the optimization problem (3.7) for different penalties . In order to make various approaches comparable, we choose the number of nonzero elements for each factor weight in PPCA and PPCA (wt) to match the number of nonzero elements in each factor weight for SPCA for a given penalty . This means that all methods have the same degree of sparsity for each factor but can use different entries and magnitudes for the weights.

We report the in-sample (training) and out-of-sample (test) results. For the first case, we estimate the parameters on the training data set and calculate the goodness-of-fit measures on it. For the second case, we use the factor portfolio weights estimated on the training data set to construct the factors and loadings on the test data set.252525The loadings for SPCA on the test data set are the same as on the training data set. However, the loadings of PPCA and PPCA (wt) are different on the training and test data as they are estimated in a second stage regression.

Motivated by our empirical application, we simulate a factor model where and errors are correlated and heterogeneous:

-

•

Heteroskedasticity: , and

-

•

Cross sectional dependence: , where with

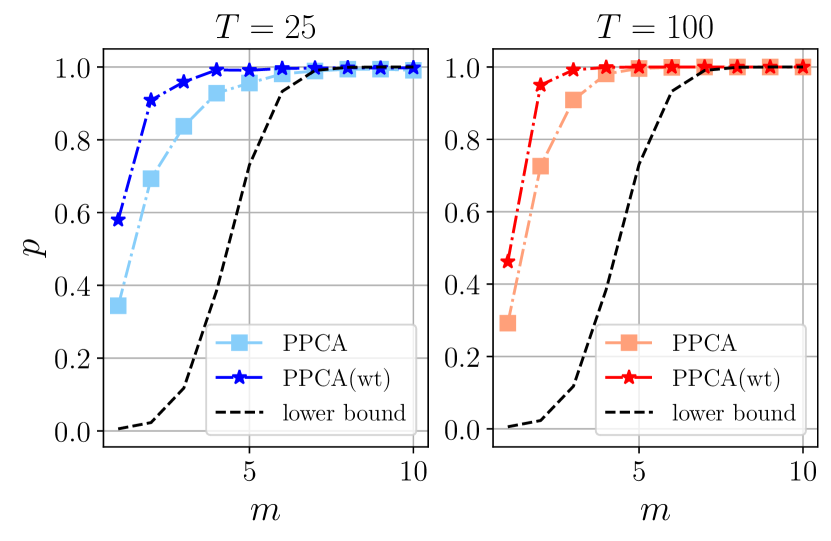

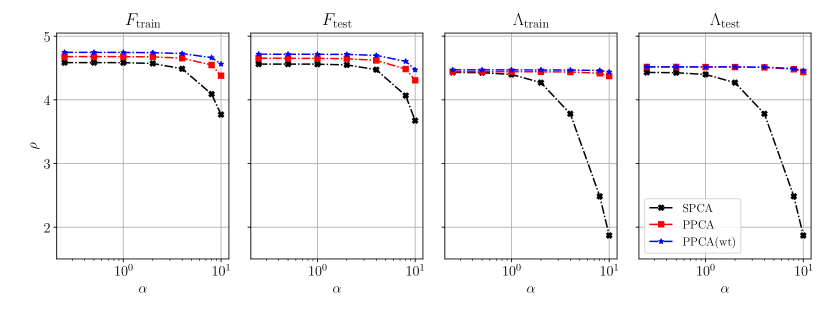

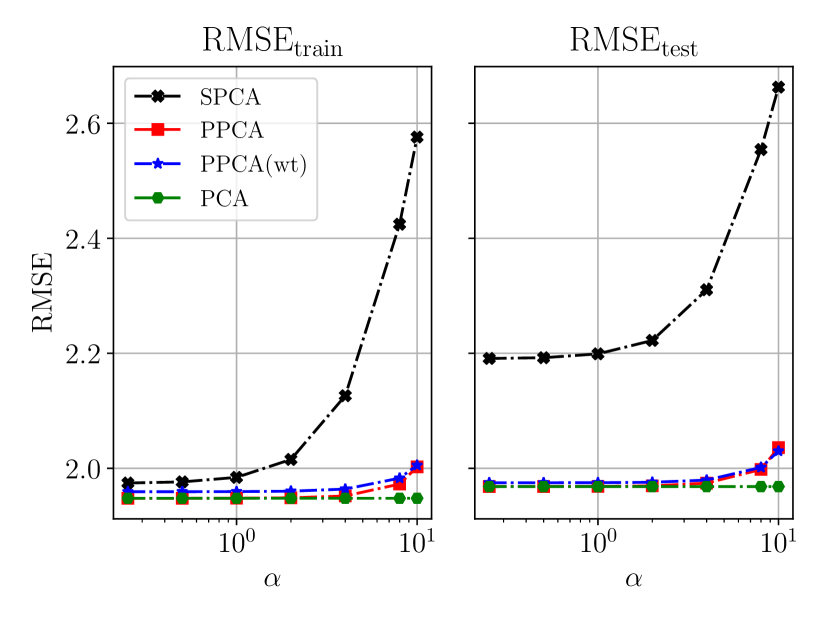

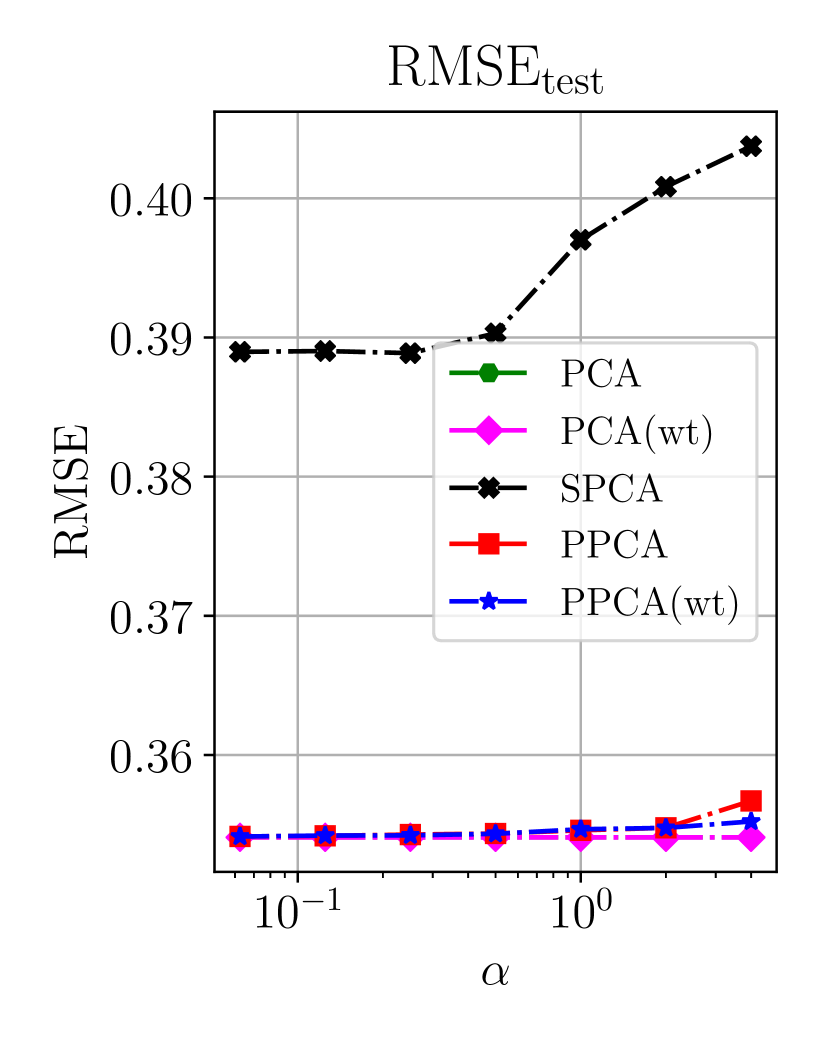

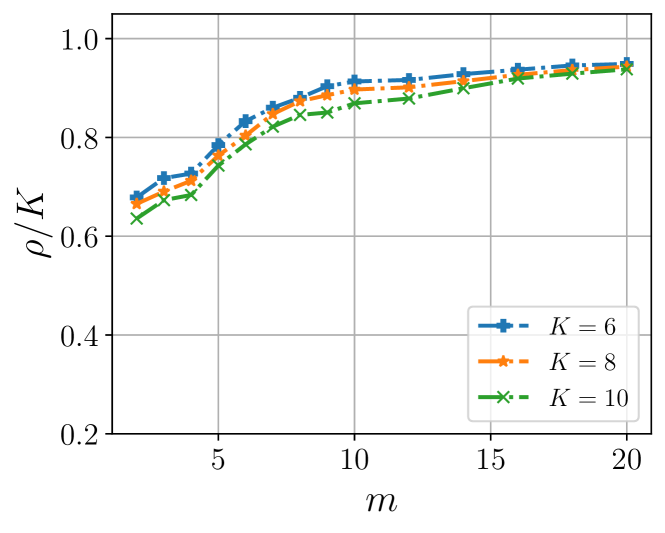

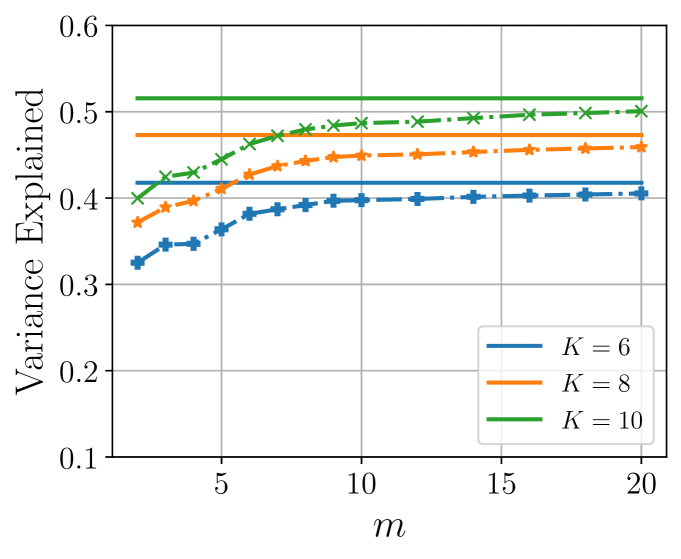

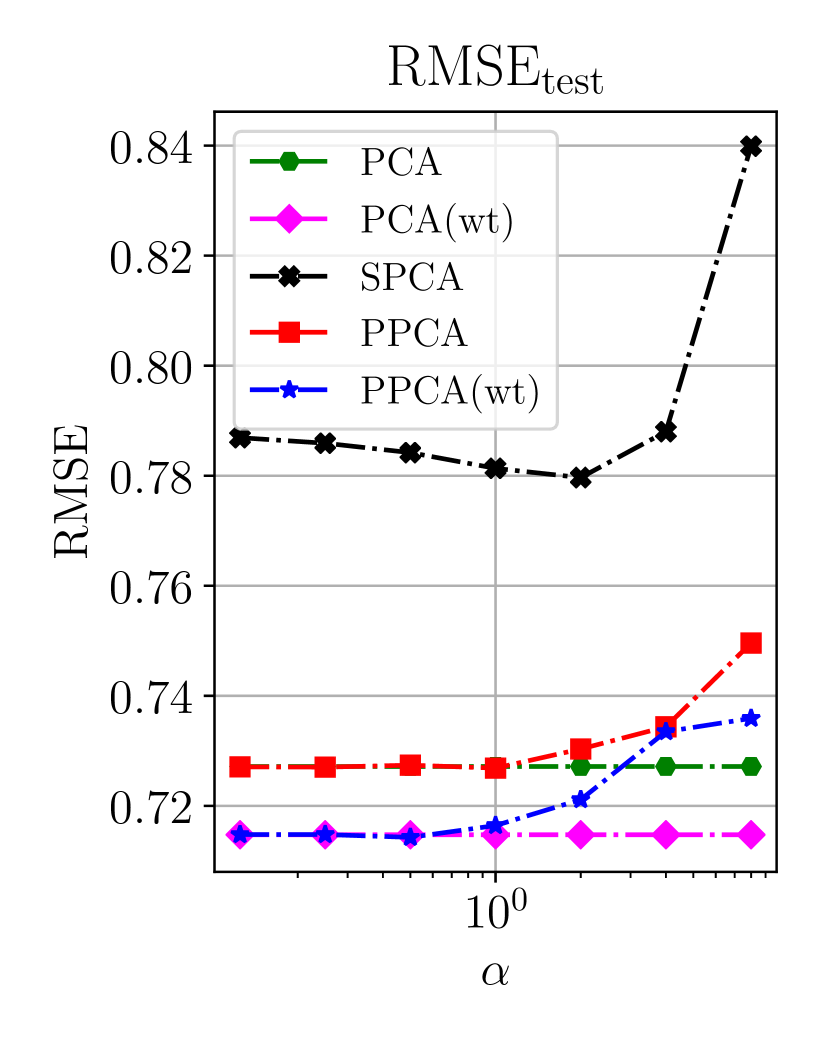

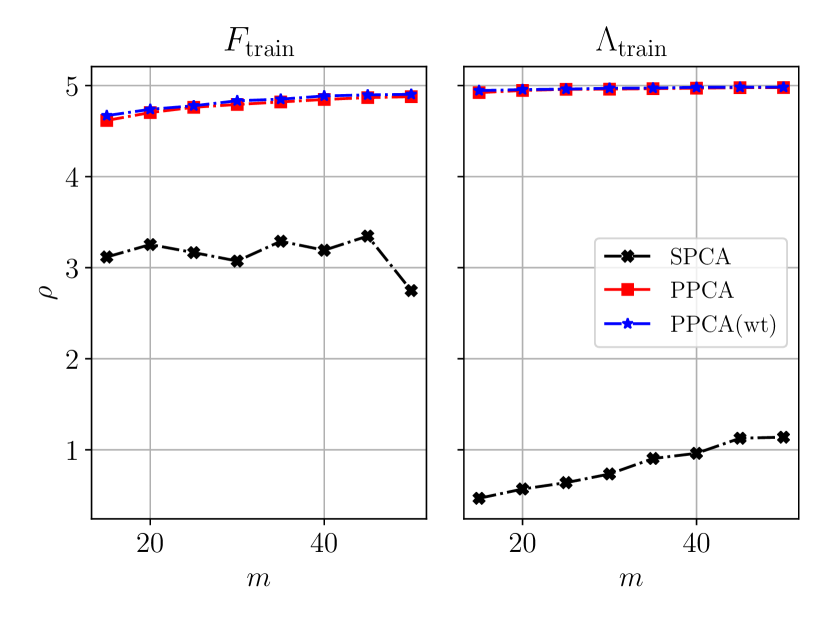

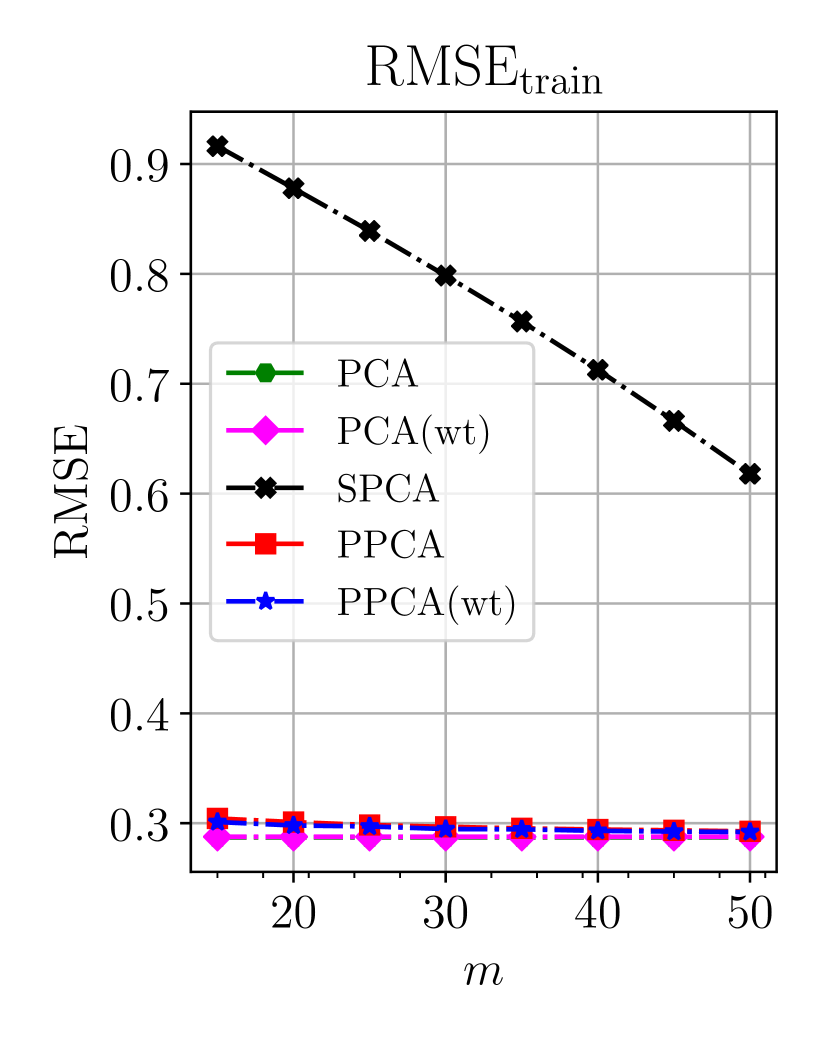

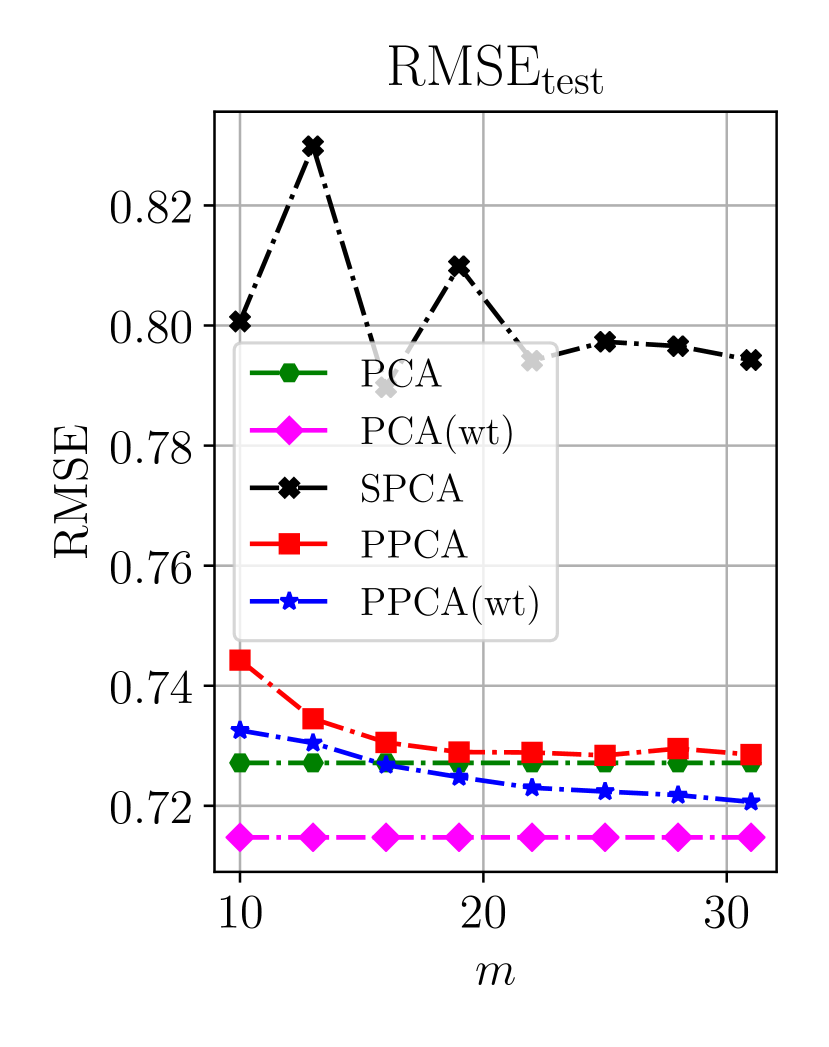

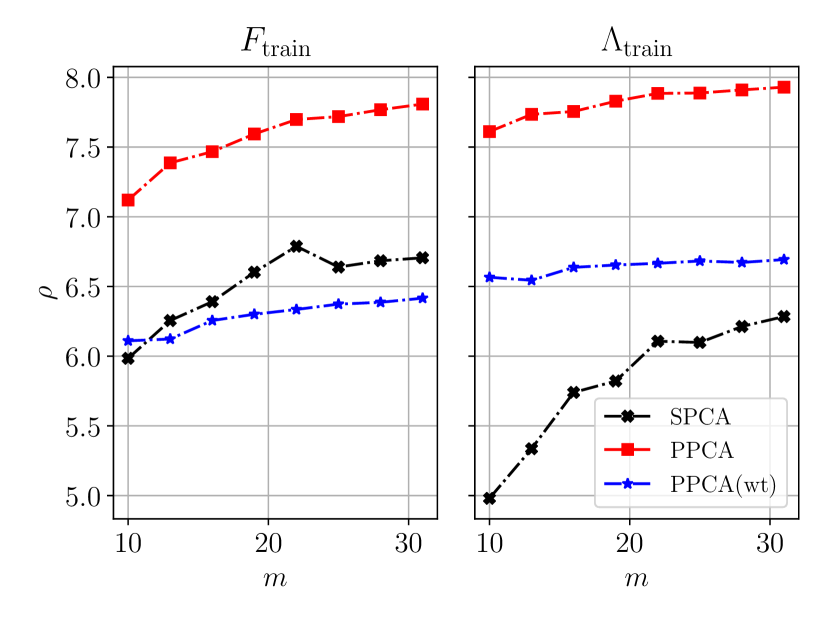

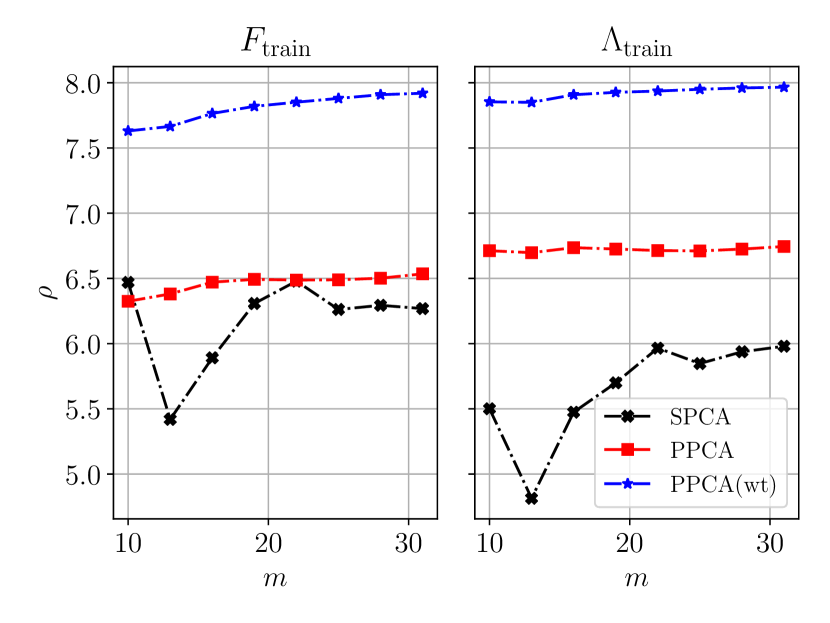

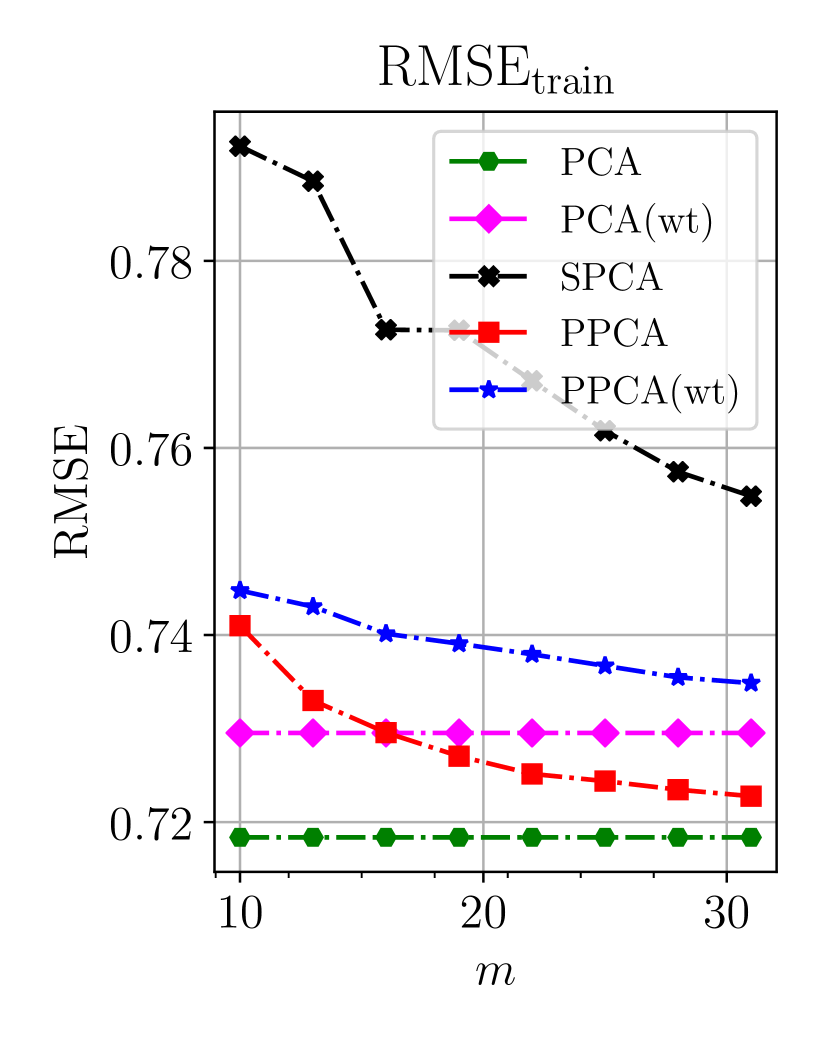

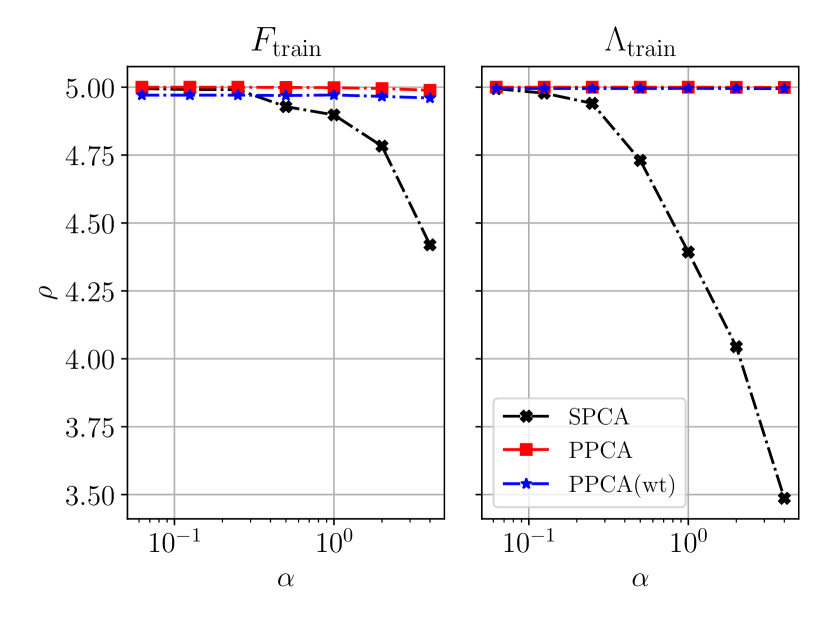

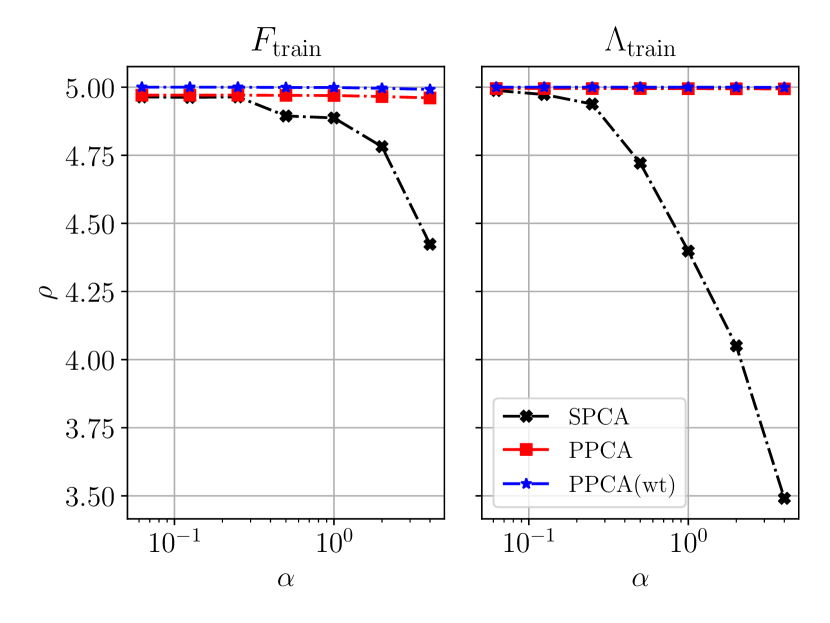

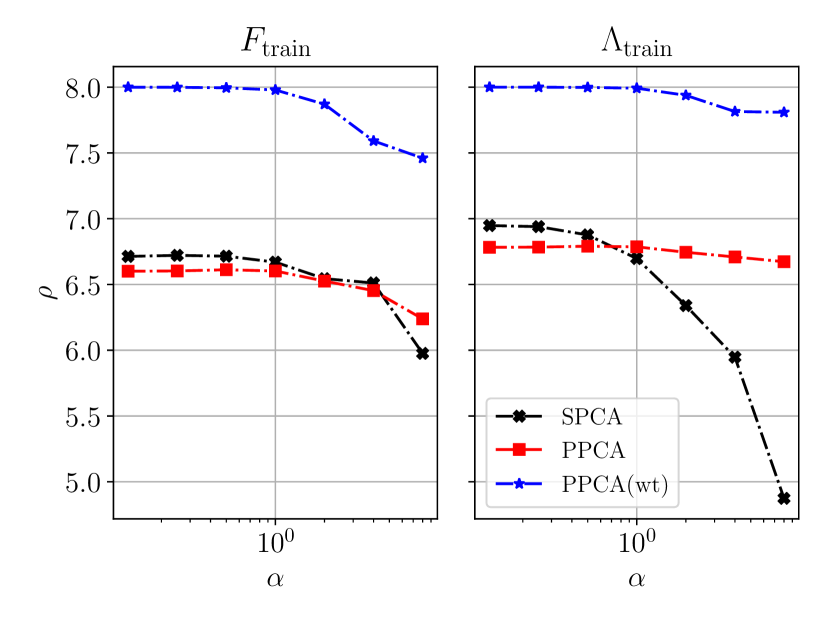

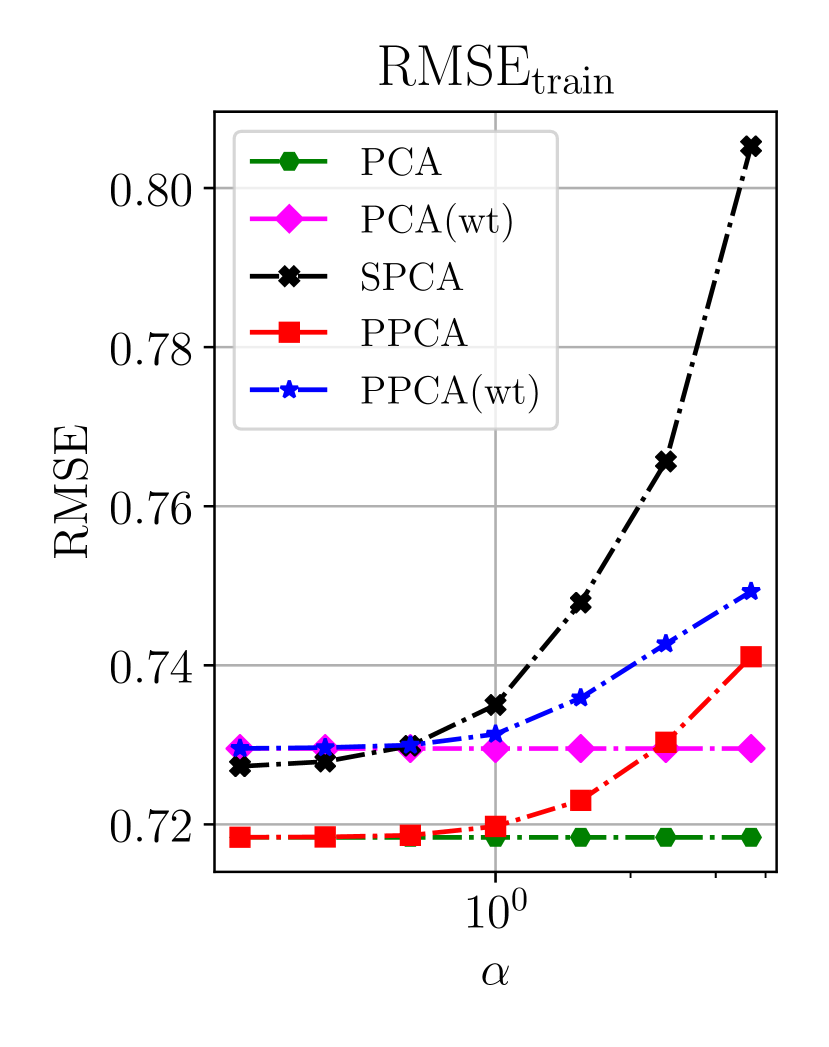

Figure 4 reports the generalized correlations for factors and loadings and RMSE for the different methods. On both training and test data, PPCA and PPCA (wt) have higher correlations with the population factors and smaller RMSE than SPCA. Interestingly PPCA and PPCA (wt) can actually provide as good a fit as conventional PCA without thresholding. Moreover, PPCA (wt) better approximates the population factors and has smaller RMSE than unweighted PPCA which supports our arguments in Section 3.5.

We have already argued in Proposition 6 that under certain conditions sparse PCA factors provide a worse approximation to factors than PPCA. This result seems to continue to hold in more general setups. More importantly, estimating sparse loadings in a population model with non-sparse population loadings is simply miss-specified. It is striking how much lower the correlations of the SPCA loadings are with the population loadings. This loading estimation error leads to the substantially larger RMSE. Both, PPCA and PPCA (wt), have correlations and errors that can be almost twice as good as SPCA.

5 Empirical Application

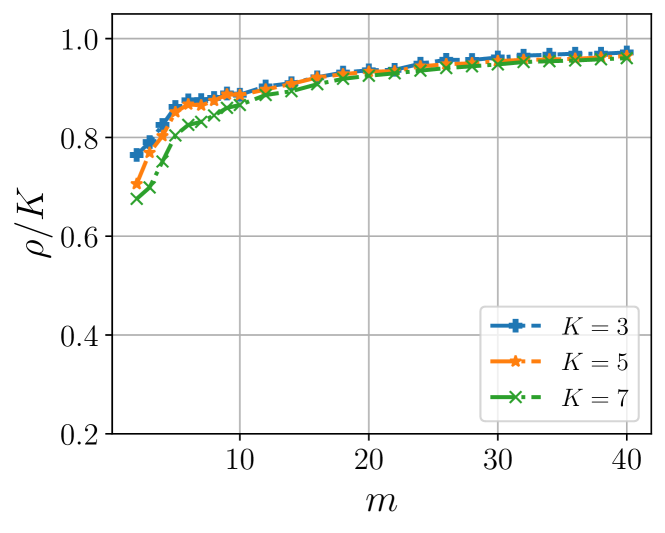

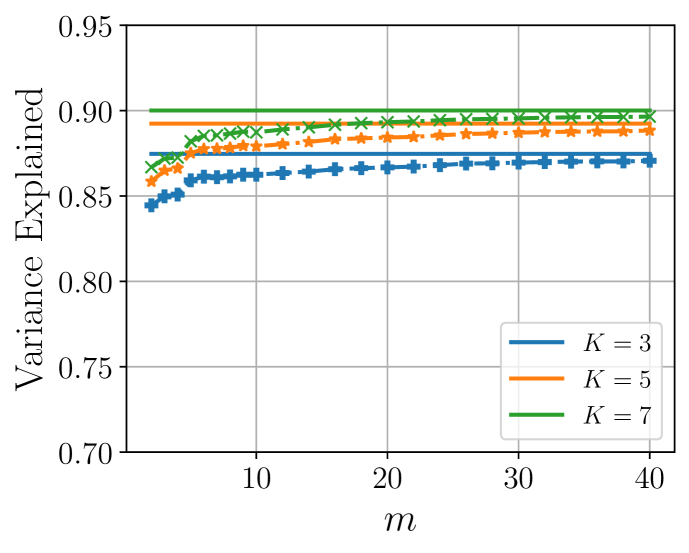

In this section, we apply our method to two relevant datasets, 370 financial portfolios and 128 macroeconomic variables. We compare the proximate factors with the PCA factors by two metrics, the generalized correlation between and and the proportion of variation explained by and . In both datasets, proximate factors constructed from our approach with 5-10% of cross-section observations are very close to the conventional PCA factors. As proximate factors are composed of only a few cross-section observations, we can find economically meaningful labels for each latent factor.

5.1 Financial Portfolio Data

We study the monthly returns of 370 portfolios sorted in deciles based on 37 anomaly characteristics from 07/1963 to 12/2016. For each characteristic, we have ten decile-sorted portfolios that are updated yearly and are linear combinations of returns of U.S. firms in CRSP. These are the same portfolios studied in Lettau and Pelger (2020b) and are compiled by Kozak, Nagel, and Santosh (2020).262626We thank Kozak, Nagel, and Santosh (2020) for allowing us to use their data. These 37 anomaly characteristics are listed in Table IA.1 in the Internet Appendix.272727Kozak, Nagel, and Santosh (2020) use a set of 50 anomaly characteristics. We use 37 of those characteristics with the longest available cross-sections. The same data is studied in Lettau and Pelger (2020b). Each of these portfolios can be interpreted as an actively managed portfolio based on a signal that has been shown to be relevant for the risk-return tradeoff. In contrast to individual stock data these managed portfolios are more stationary and Lettau and Pelger (2020b) show that they can be modeled by a stable factor structure.

| 10 | 0.993 | 0.912 | 0.771 | 0.918 | 0.837 |

|---|---|---|---|---|---|

| 20 | 0.995 | 0.948 | 0.883 | 0.949 | 0.890 |

| 30 | 0.996 | 0.965 | 0.935 | 0.966 | 0.910 |

| 40 | 0.997 | 0.971 | 0.958 | 0.975 | 0.923 |

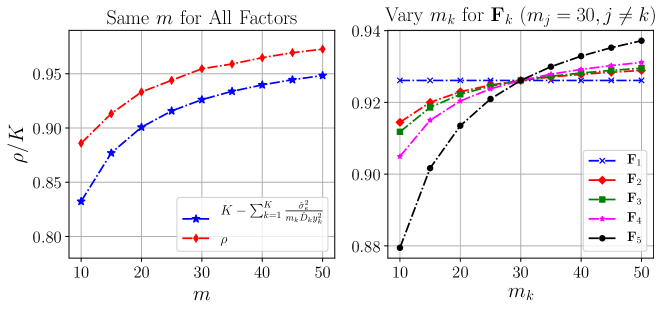

In Figure 5, we calculate the generalized correlation between estimated PCA and proximate factors and compare the proportion of variation explained by these factors for different number of factors . We normalize the generalized correlation by the number of factors. The closer to 1, the better the sparse factors approximate the non-sparse PCA factors. The more portfolios we include in the proximate factors, the larger the correlation and the amount of variation explained. When the number of nonzero entries in each sparse loading is around 20, corresponding to around 5% of the cross-section units, the ratio is close to 0.9, implying that the average correlation between each proximate factor in and each estimated factor in is around 95%. The explained variation is defined as , where is the based on the estimated factors and loadings. As the data is demeaned the explained variation equals the percentage of variance explained in the data. By construction, PCA factors maximize the explained variance in-sample. However, the variance explained by becomes very close to that by when is constructed with the 10 cross-section units with the strongest signals.

Table 2 shows the generalized correlations for each of the five factors with their proximate version. As by construction, the PCA factors are uncorrelated, the individual generalized correlations correspond to the s from a linear regression of each PCA factor on the five proximate factors. Even with only 10 portfolios, we can capture each of the latent factors very well, in particular the first two factors. 30 portfolios are sufficient to almost perfectly replicate the latent factors.282828As many investors trade on factors, trading on proximate factors can also significantly reduce trading costs.

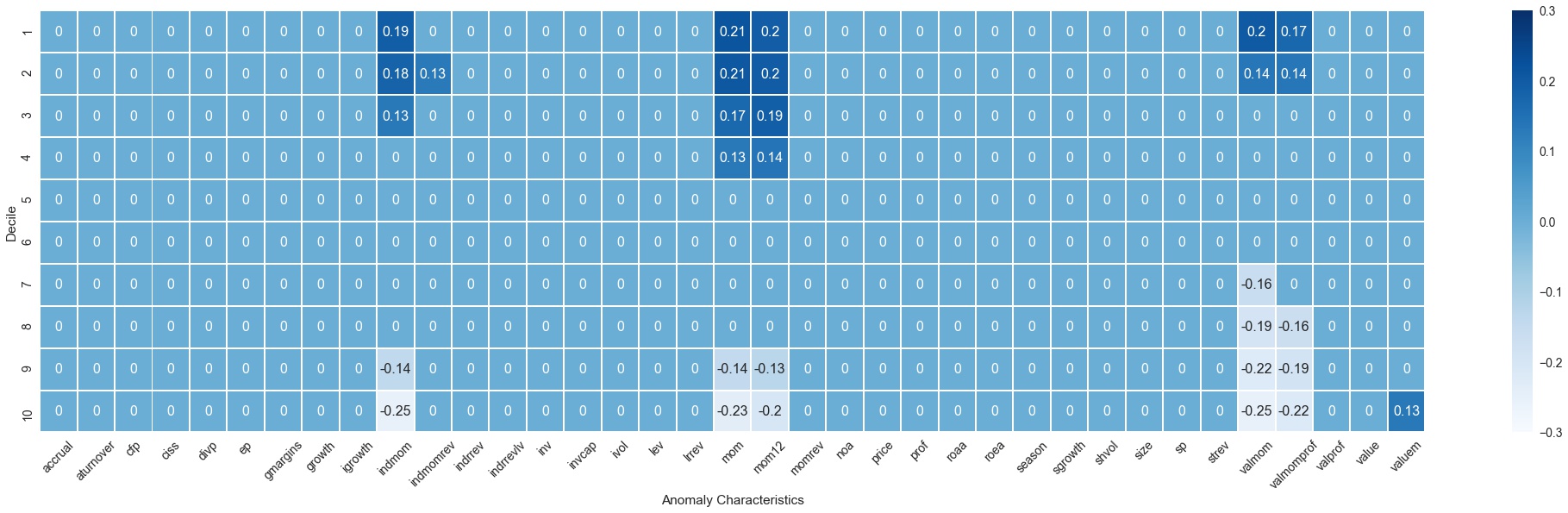

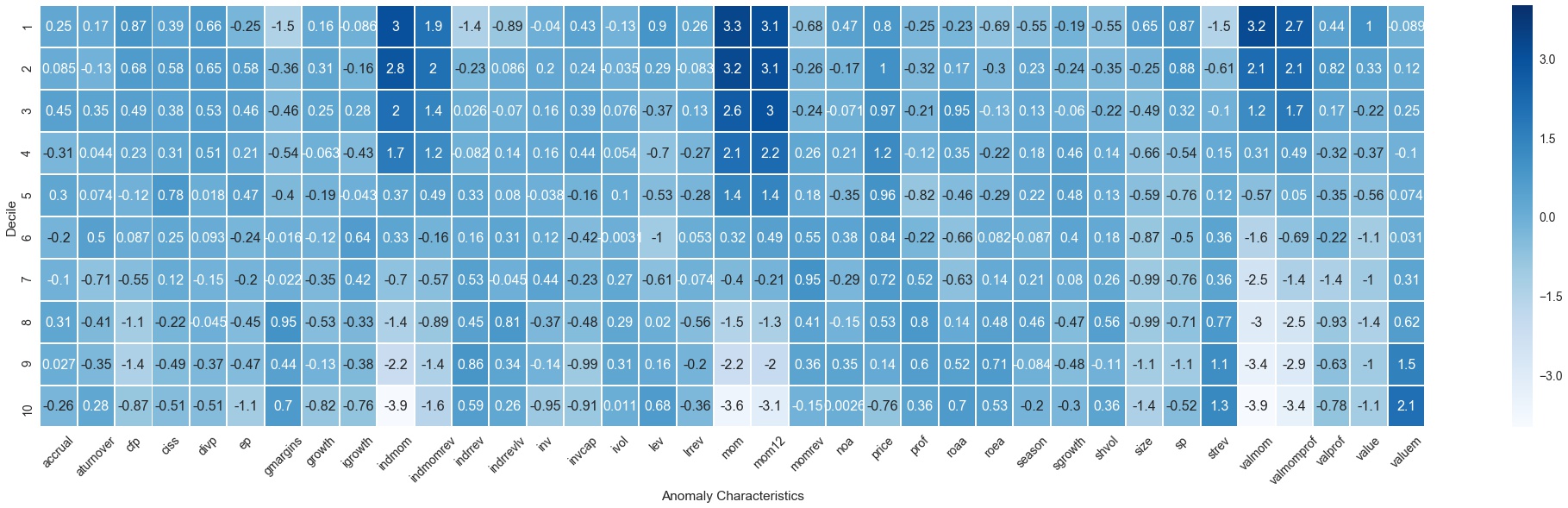

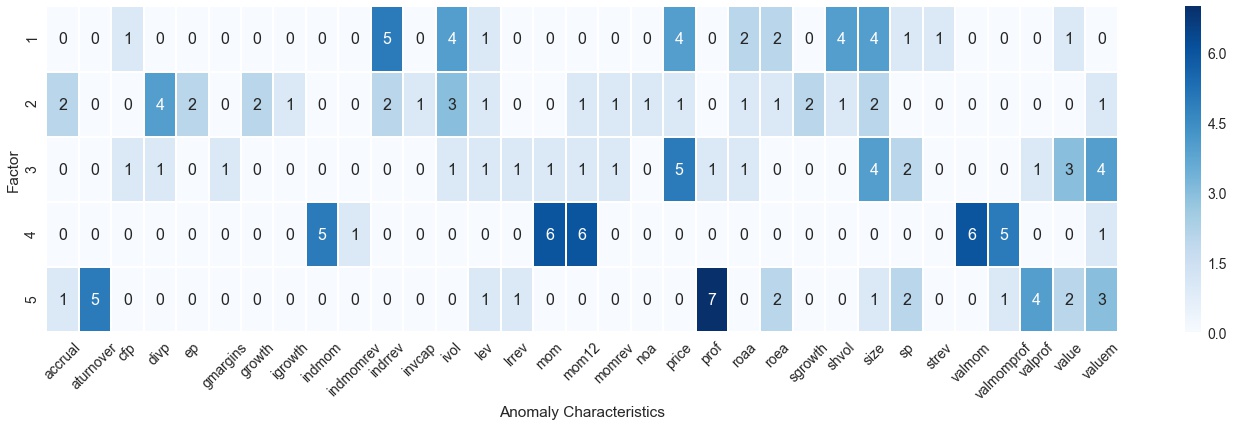

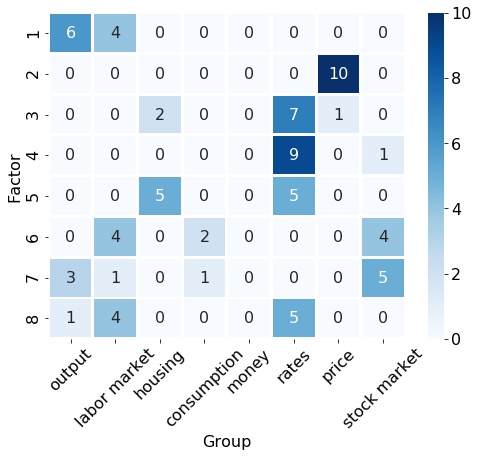

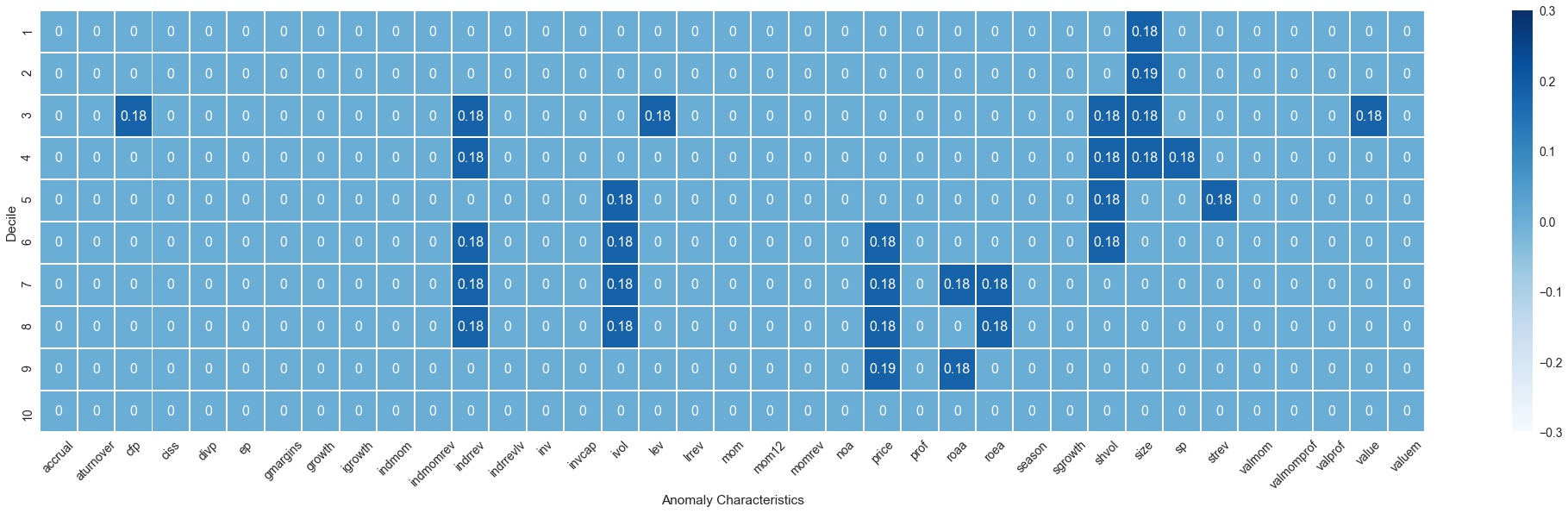

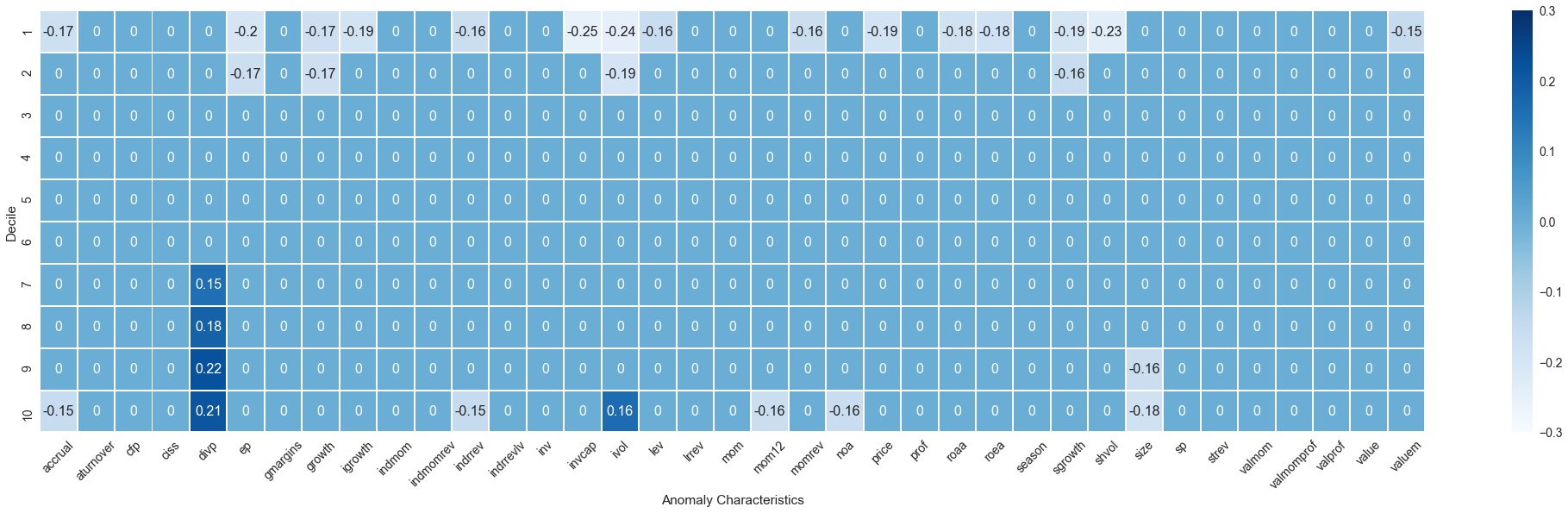

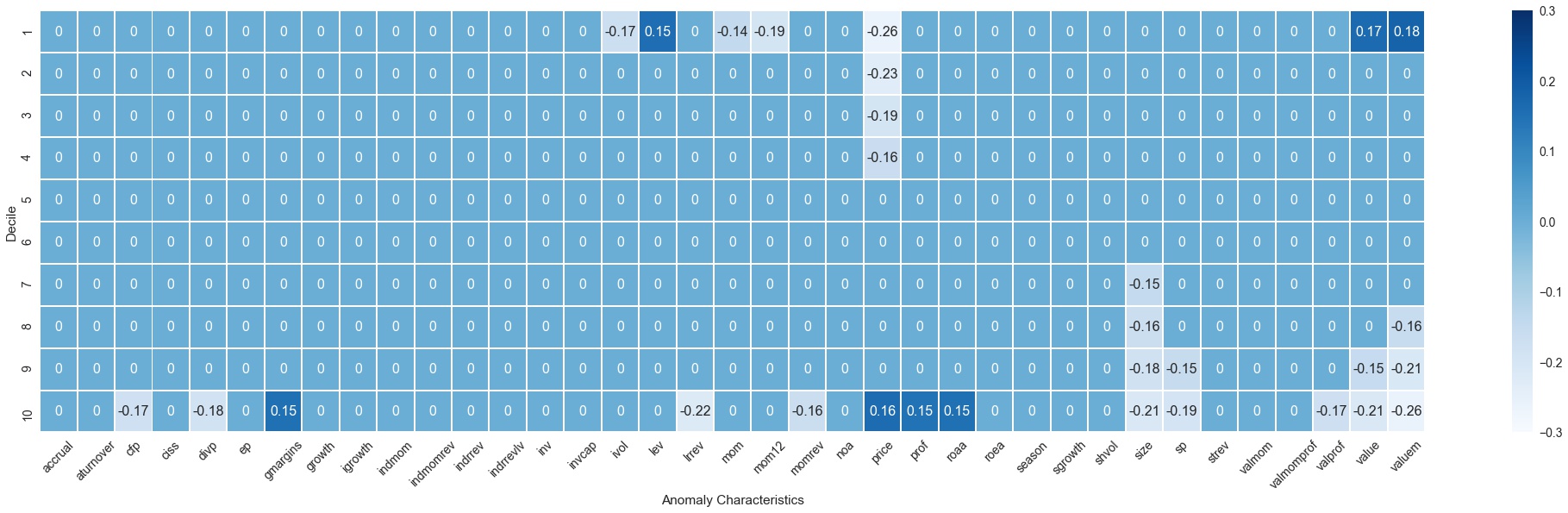

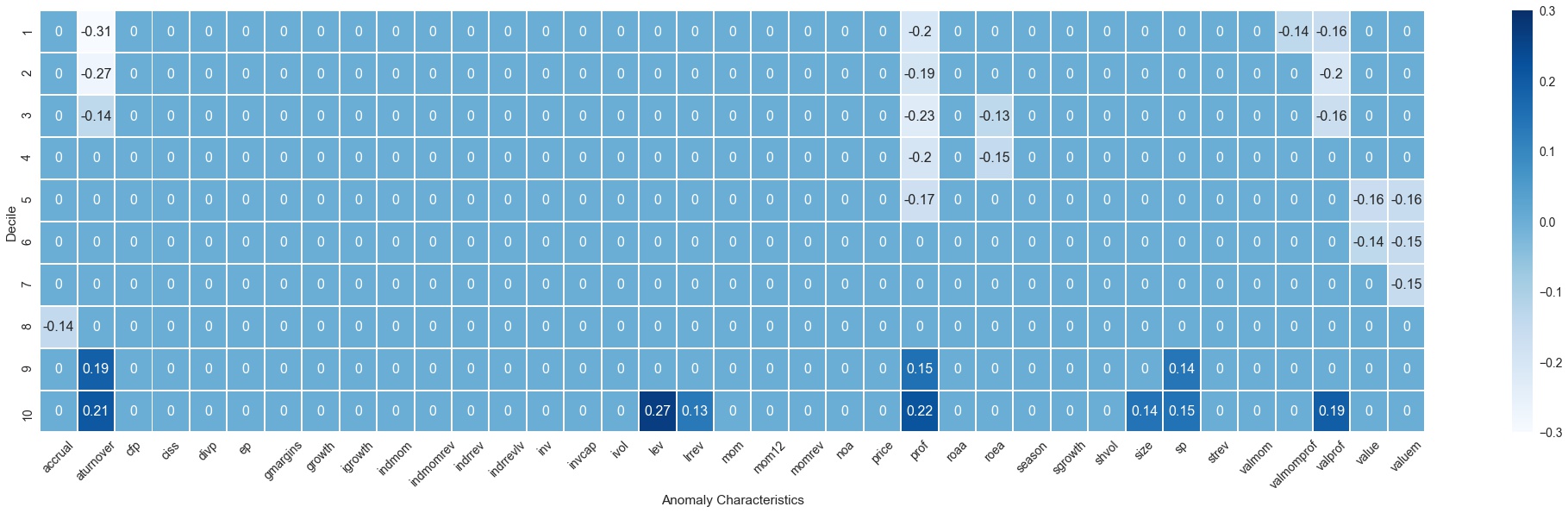

We study each of the five proximate factors in more detail. Figure 6 provides a clear picture of the assets used to construct the fourth factor, labeled as the momentum factor. We use the fourth factor as an example and present the figures for the other factors in the Internet Appendix. First, the fourth proximate factor is only composed of five strategies related to momentum, which are Industry Momentum, 6-month Momentum, 12-month Momentum, Value Momentum and Value Momentum Profitability. Second, this factor is a long-short factor, i.e., it has negative weights for the smallest decile portfolios and positive weights for the largest decile portfolios. Most financial factors are constructed as long-short factors to capture the difference between the extreme characteristics. For comparison, we also show the portfolio weights for the fourth PCA factor in Figure 7. The pattern suggests that the fourth factor is related to momentum, but our proximate factor provides the argument that the information for this factor is almost completely captured by momentum portfolios.

Figure 8 displays the composition of each latent factor based on the characteristic groups. It provides a first intuition for interpreting each latent factor. Based on Figures IA.7 to IA.10 we assign the following labels to the other latent factors: The first factor is a “long”-only market factor. The second factor loads on categories such as dividend/price, earning/price, investment capital, and asset and sales growth suggesting a “value” interpretation. The third factor loads strongly on price and large market capitalization and hence we label it as a big-price factor. The last factor is clearly an asset turnover-profitability factor.

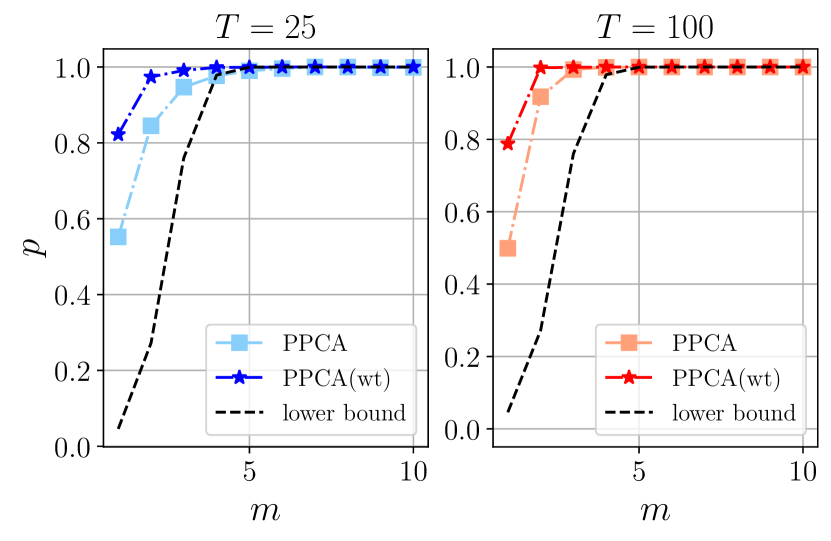

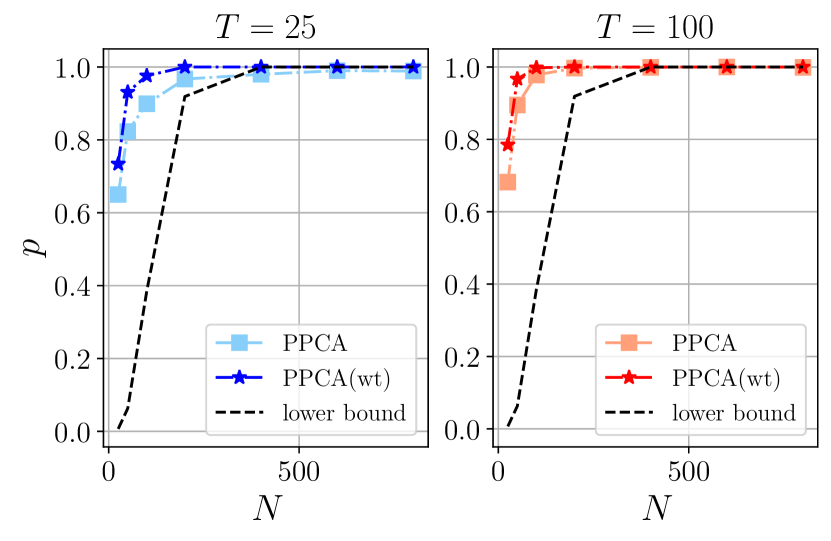

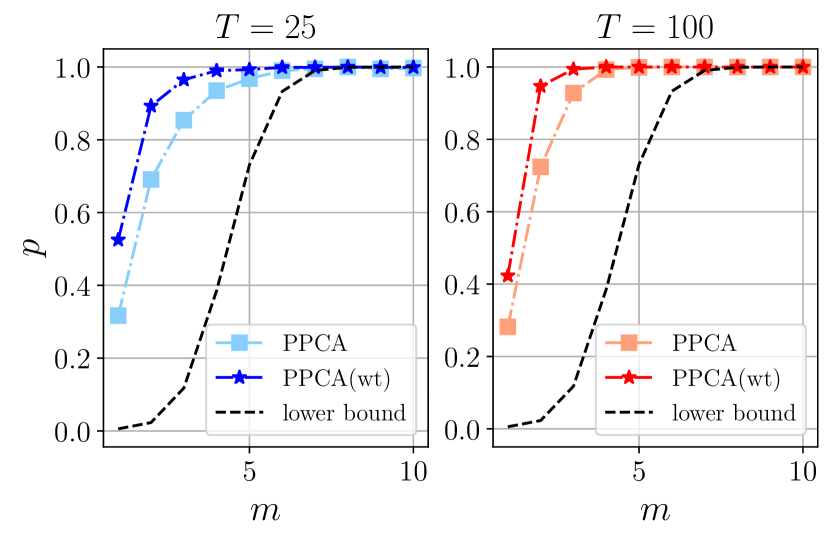

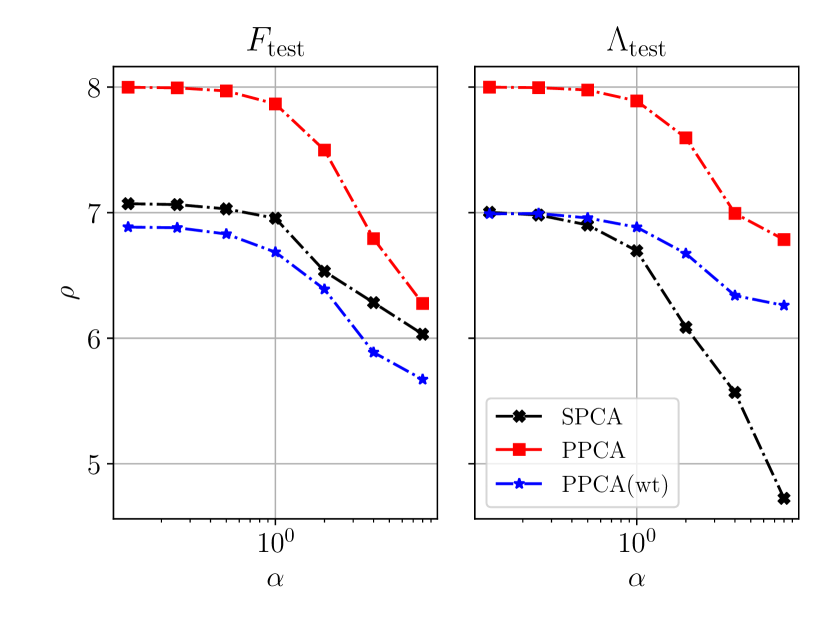

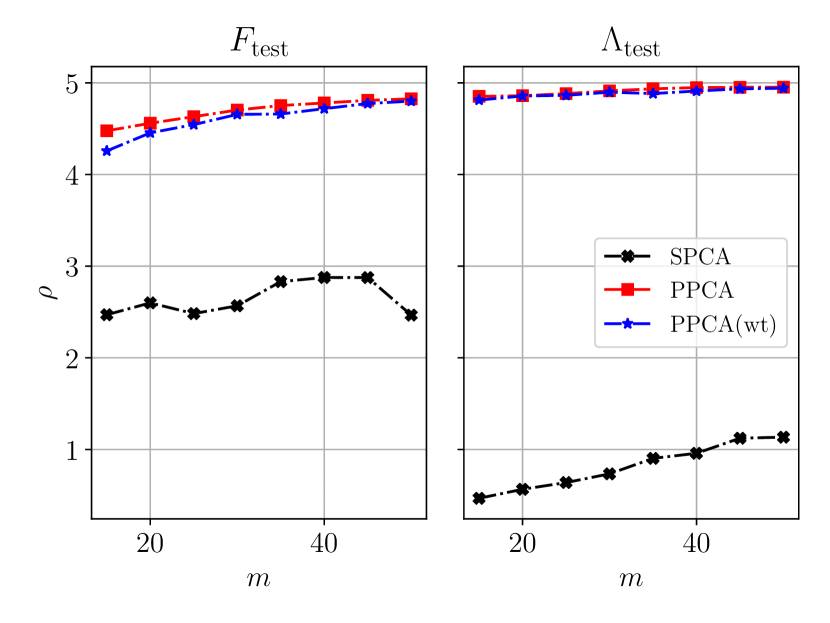

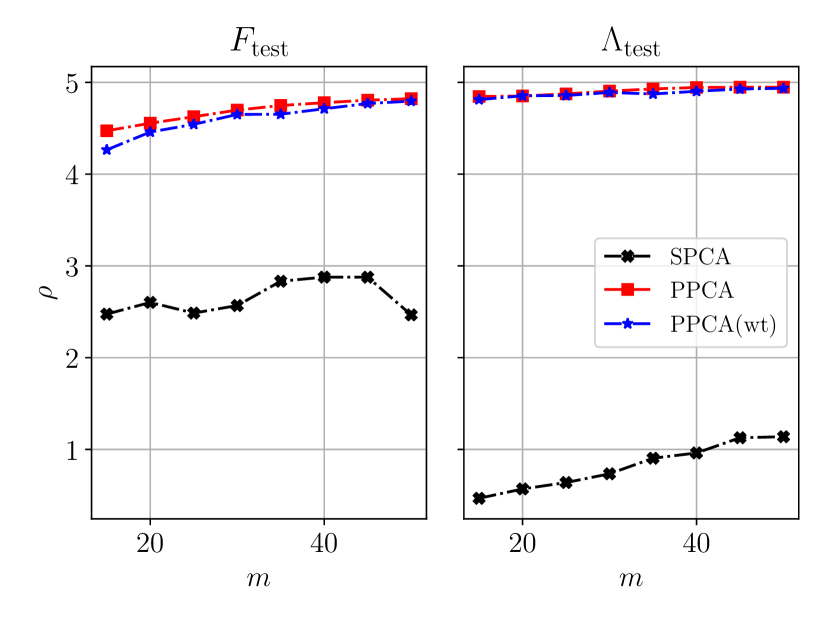

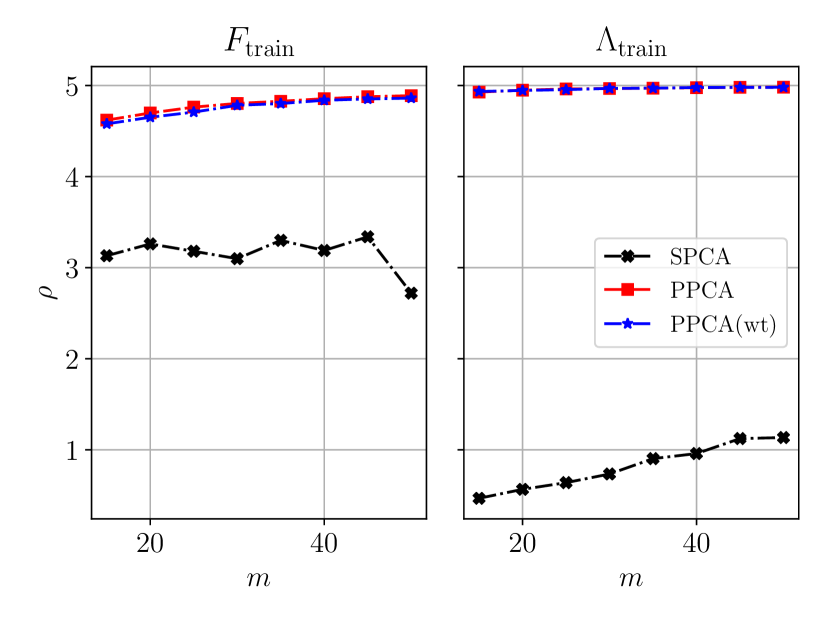

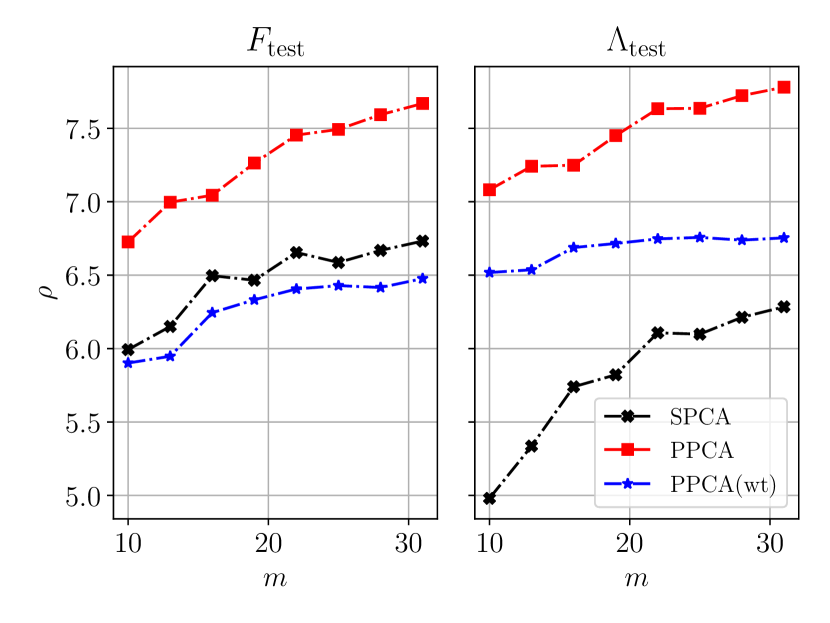

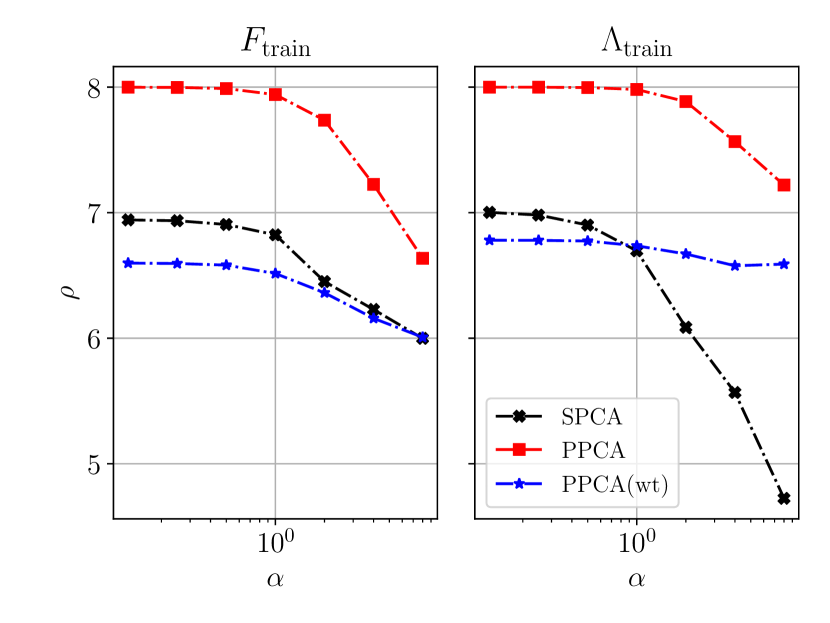

Figure 9(c) compares proximate factors with sparse PCA using the same metrics as in Section 4.2. As the population factors and loadings are unknown, we compare the proximate and sparse factors and loadings with the non-sparse PCA factors and loadings. We also include the weighted PCA factors with the inverse standard deviation of the residuals as weights.292929We use the residuals from a 5-factor model to estimate the standard deviation of the errors. The results are robust to this choice. Both, unweighted PCA factors and weighted PCA factors are consistent estimators of the population factors. However, in the presence of heteroskedastic errors, we expect the non-sparse weighted PCA estimates to be more efficient and hence to be the more appropriate comparison benchmark. The first half of the time-series serves as the training and the second half as the test data set. The number of nonzero elements for each proximate factor is set equal to the number of nonzero elements of the corresponding SPCA factor for a given -lasso penalty .303030We only report the out-of-sample results in the main text. The Internet Appendix collects the in-sample results with very similar findings. An alternative approach to implement sparse PCA is to directly impose the cardinality constraint rather than using the penalty term in the optimization problem (3.7), where equals the number of nonzero elements in . Sigg and Buhmann (2008) develop an expectation-maximization (EM) algorithm based on a probabilistic expression of PCA to solve this optimizaton problem with constraint . This approach will in general return sparse loadings with nonzero elements in each sparse loading vector when is reasonably small. The Internet Appendix collects the results for this alternative implementation with very similar findings as in the main text.

First, unweighted PCA factors and loadings are almost identical to the weighted PCA factors and loadings as the residuals have only a low degree of heteroskedasticity. As the two sets of proximate factors are very close approximations of the corresponding PCA factors, PPCA and PPCA (wt) are also almost identical with a slightly lower RMSE for PPCA (wt) out-of-sample. Second, sparse PCA performs substantially worse. For a higher degree of sparsity, the SPCA factors are neither close to the unweighted nor the weighted PCA factors. In particular, the sparse loadings are miss-specified, resulting in a higher out-of-sample RMSE for all levels of sparsity.

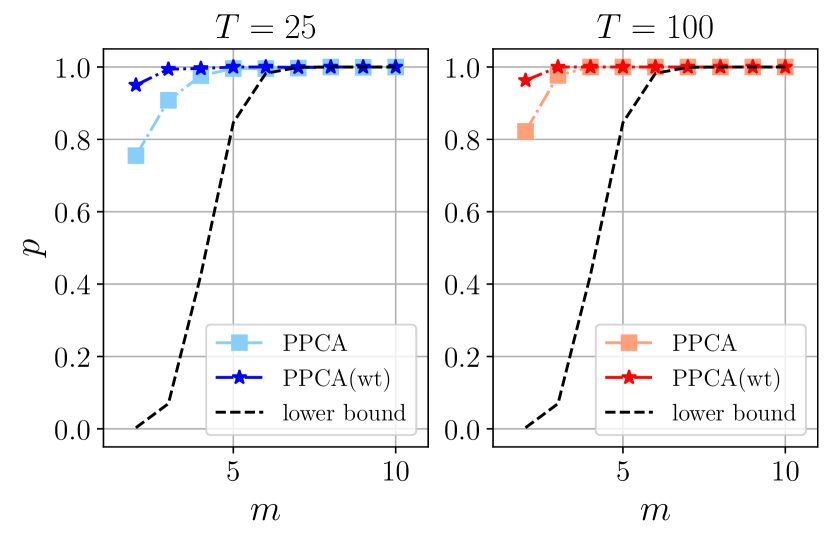

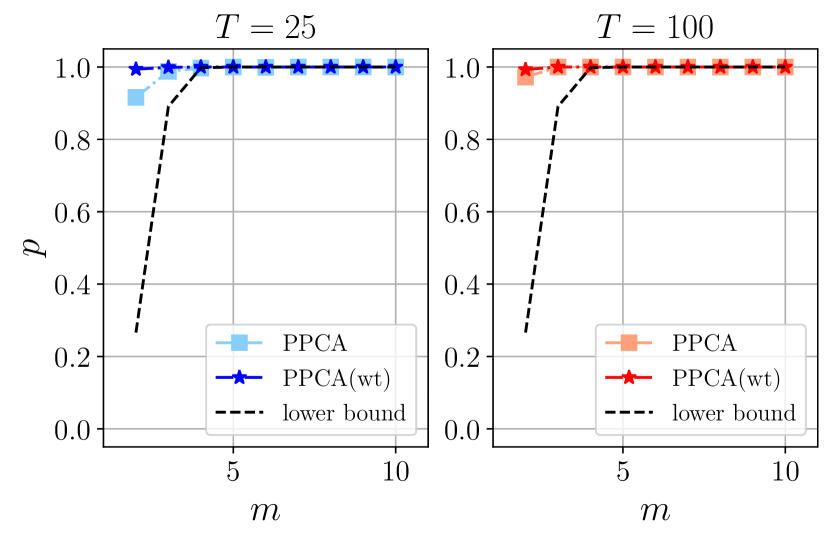

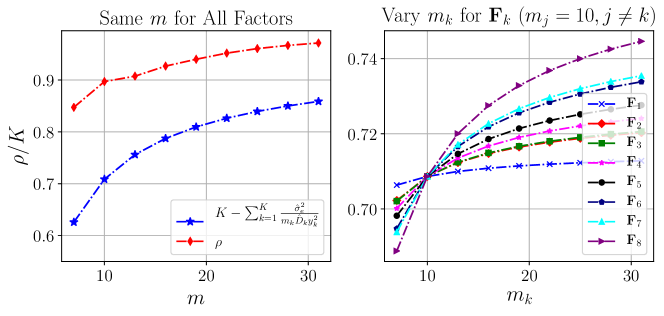

Last but not least, we show how the theoretical lower bound in Theorem 3 and Proposition 3 can serve as a guidance to select the number of nonzero in factor weights. We consider the case where each proximate factor can have a different number of nonzero entries . For analytical tractability we use the simple model where we assume that population loadings are i.i.d normally distributed, but it turns out that this simple model already provides a very accurate description capturing the relevant trade-offs. More specifically, we assume that and estimate the mean and sample variance following from . The parameters of the GEV distribution are only a function of and and known in closed-form as specified in Table 1. For the given target probability we solve for in . We want each factor to contribute equally to the generalized correlation and set . Hence, we obtain

The theoretical lower bound for equals which holds with probability . The noise variance is estimated by and factor variances are estimated by the largest sample eigenvalues.

Figure 10 shows the theoretical bound as a function of . First, the theoretical lower bound captures the same trade-offs as the generalized correlation with the PCA factors. In particular, the slopes of the curves in the left subfigure are almost identical and indicate that the largest gains can be achieved by adding the first 30 nonzero elements. In the right subfigure, we study the partial effect of changing the sparsity of the -th factor while keeping the sparsity level of the other factors constant. The results illustrate that weaker factors which explain less variation require more nonzero weights while stronger factors can already be approximated well with very sparse proximate factors. These theoretical predictions support the empirical findings in Table 2.

5.2 Macroeconomic Data

We study 128 monthly U.S. macroeconomic indicators from 01/1959 to 02/2018 as in (McCracken and Ng, 2016). This data is from the Federal Reserve Economic Data (FRED) and is publicly available.313131This dataset is updated in a timely manner and is available at https://research.stlouisfed.org/econ/mccracken/fred-databases/ The 128 macroeconomic indicators can be classified into 8 groups: 1. output and income; 2. labor market; 3. housing; 4. consumption, orders, and inventories; 5. money and credit; 6. interest and exchange rates; 7. prices; 8. stock market (McCracken and Ng, 2016). Macroeconomic datasets have been successfully analyzed with PCA factors for forecasting and estimation of factor augmented regressions (Stock and Watson, 2002b; Boivin and Ng, 2005). McCracken and Ng (2016) estimate 8 factors in this macroeconomic data.

Figure 11 plots the generalized correlation between and normalized by and the proportion of variance explained with different number of factors. When the number of nonzero entries in each sparse factor weight vector is around 10, which is less than 8% of all macroeconomic variables, the ratio of to is close to 0.9, which corresponds to an average correlation of 0.95%. The amount of variation explained by and also indicate that consisting of around 15 macroeconomic variables can approximate very well.

In the following, we study the 8-factor model in more detail. Table 3 shows the generalized correlations for each factor which correspond to the in regressions of each PCA factor on all proximate factors. The first five factors can be captured well by proximate factors with 10 macroeconomic variables in each proximate factors. The sixth to eighth factors are weaker, but they can be reasonably captured by proximate factors with around 20 variables.

| 10 | 0.953 | 0.959 | 0.949 | 0.953 | 0.961 | 0.799 | 0.833 | 0.767 |

|---|---|---|---|---|---|---|---|---|

| 15 | 0.967 | 0.970 | 0.958 | 0.956 | 0.964 | 0.857 | 0.867 | 0.837 |

| 20 | 0.977 | 0.974 | 0.957 | 0.963 | 0.961 | 0.905 | 0.919 | 0.891 |

| 25 | 0.983 | 0.980 | 0.961 | 0.979 | 0.973 | 0.937 | 0.943 | 0.929 |

Figure 12 shows a clear interpretation of the statistical factors. When each hard-thresholded loading has 10 nonzero entries, we see a strong pattern in the composition of each latent sparse factor that allows us to label each one. The first factor is a labor and productivity factor; the second factor is a price factor; both third and fourth factors are interest and exchange rate factors; the fifth factor is a housing and rate factor; the sixth factor is a labor and stock market factor; the seventh factor is a productivity and stock market factor; the eighth factor is a labor and rate factor. Macroeconomic variables in groups of output, income, labor market, and prices are the main compositions of the first and second factors. The third, fourth, fifth, and eighth latent factors are mainly composed of macroeconomic variables in the group of interest and exchange rates. Variances explained by latent factors are in decreasing order. Thus, variables in groups of output, income, labor market, prices, interest and exchange rates explain most of the variation in the whole dataset.

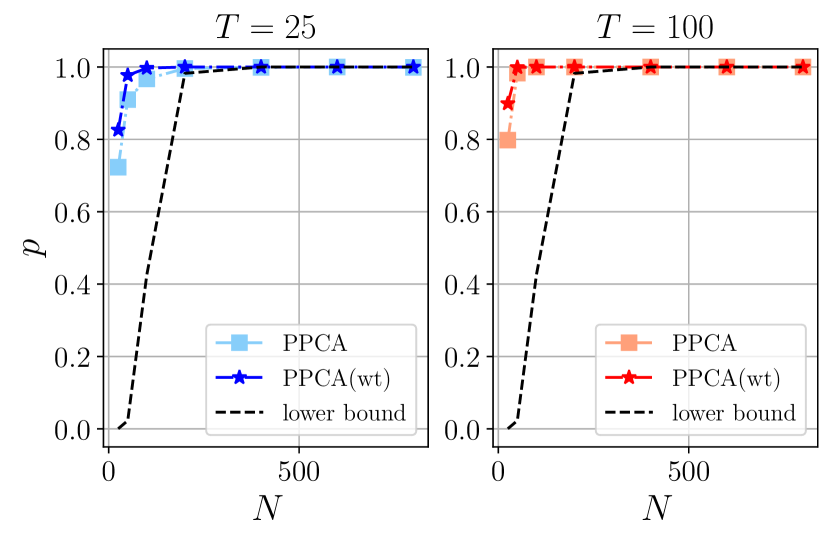

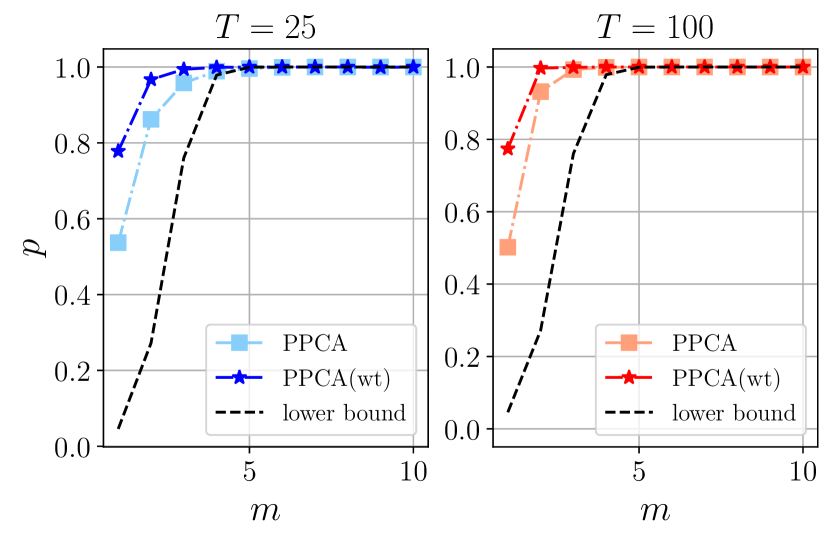

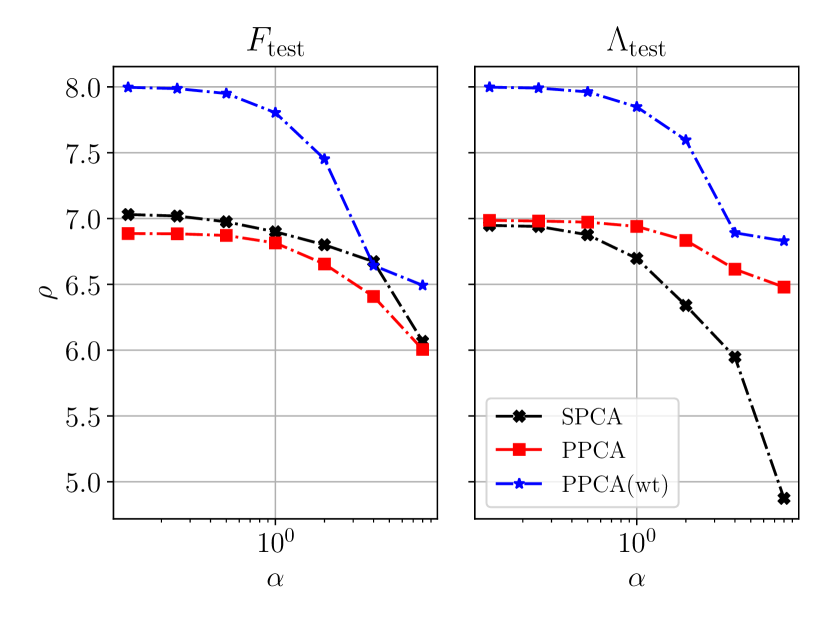

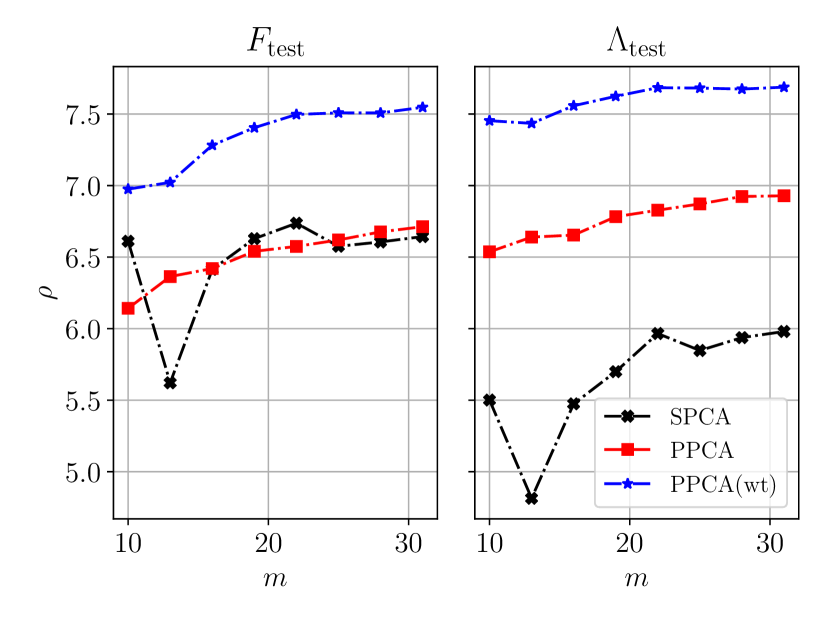

Figures 13 and 14 apply the same analysis as in Figures 9(c) and 10 to the macroeconomic data with similar insights. The key difference is that the macroeconomic time-series are more heterogeneous. Hence, the weighted PCA achieves a lower RMSE out-of-sample than the unweighted PCA. Note that as expected the weighted proximate factors are more highly correlated with the weighted PCA factors while unweighted proximate factors mimic the unweighted PCA factors. This is also reflected in the RMSE. Sparse PCA overall performs significantly worse as expected. The theoretical lower bound provides similar guidance as in the portfolio case. Note that in the macroeconomic data the factors are generally weaker and explain less variation than in the portfolio data which leads to a larger gap between the empirical and theoretical generalized correlation bound. Overall the empirical results justify why we can use the proximate factors as a replacement for standard PCA factors.

6 Conclusion

In this paper, we propose a method to construct proximate factors that consist of only a small number of cross-section units and can approximate latent factors well. These proximate factors are usually much easier to interpret than PCA factors. The closeness between proximate factors and latent factors is measured by the generalized correlation. We provide an asymptotic probabilistic lower bound for the generalized correlation based on extreme value theory. This lower bound explains why proximate factors are close to latent factors and provides guidance on how to chose the sparsity in the proximate factors. Simulations verify that the lower bound closely approximates the exceedance probability of the generalized correlation, especially in the most relevant case of an exceedance probability close to 1. The proximate factors have non-sparse loadings which are consistent estimates of the true population loadings. Empirical applications to two different datasets, financial portfolios, and macroeconomic data, show that proximate factors consisting of 5-10% of the cross-section units can approximate latent factors well. Using these proximate factors, we provide a meaningful interpretation of the latent factors in our datasets.

References

- (1)

- Aït-Sahalia and Xiu (2019) Aït-Sahalia, Y., and D. Xiu (2019): “Principal component analysis of high-frequency data,” Journal of the American Statistical Association, 114(525), 287–303.