Convergence of the Iterates in Mirror Descent Methods

Abstract

We consider centralized and distributed mirror descent algorithms over a finite-dimensional Hilbert space, and prove that the problem variables converge to an optimizer of a possibly nonsmooth function when the step sizes are square summable but not summable. Prior literature has focused on the convergence of the function value to its optimum. However, applications from distributed optimization and learning in games require the convergence of the variables to an optimizer, which is generally not guaranteed without assuming strong convexity of the objective function. We provide numerical simulations comparing entropic mirror descent and standard subgradient methods for the robust regression problem.

I Introduction

The method of Mirror Descent (MD), originally proposed by Nemirovski and Yudin [17], is a primal-dual method for solving constrained convex optimization problems. MD is fundamentally a subgradient projection (SGP) algorithm that allows one to exploit the geometry of an optimization problem through an appropriate choice of a strongly convex function [2]. This method not only generalizes the standard gradient descent (GD) method, but also achieves a better convergence rate. In addition, MD is applicable to optimization problems in Banach spaces where GD is not [4].

Of more recent interest, MD has been shown to be useful for efficiently solving large-scale optimization problems. In general, SGP algorithms are simple to implement, however they are typically slow to converge due to the fact that they are based in Euclidean spaces, and through a projection operator are inevitably tied to the geometry of these spaces. As a result, their convergence rate may be directly tied to the dimension of the underlying Euclidean space in which the problem variables reside. Alternatively, MD can be adapted, or more specifically tailored to the geometry of the underlying problem space, potentially allowing for an improved rate of convergence; see [3] for an early example. Because of these notable potential benefits, MD has experienced significant recent attention for applications to large-scale optimization and machine learning problems in both the continuous and discrete time settings [21, 11], both the deterministic and stochastic scenarios [7, 15, 20, 18], and both the centralized and distributed contexts [20, 14]. MD has also been applied to a variety of practical problems, e.g., game-theoretic applications [24], and multi-agent distributed learning problems [8, 13, 16, 22, 23].

Hitherto, most of these prior studies have focused on studying the convergence rate of MD. In particular, if the step sizes are properly selected then MD can achieve a convergence rate of or for strongly convex or convex objective functions, respectively, [17, 15]. However, the convergence of the objective function value does not, in general, imply the convergence of the sequence of variables to an optimizer111One can only show the convergence of the sequence of these variables to the optimal set when this set is bounded.. To the best of the authors’ knowledge, there has not been any prior work establishing the convergence of these variables to an optimizer. Our motivation for pursuing a study of the convergence to an optimizer arises from potential applications in Distributed Lagrangian (DL) methods and Game Theory. Specifically, in the context of DL methods, we can apply distributed subgradient methods, or preferably distributed MD methods, to find the solution to the dual problem. In this setting, convergence to the dual optimizer is needed to complete the convergence analysis of DL methods [5, 6]. To motivate our study from a game theoretic viewpoint, note that the dynamics of certain natural learning strategies in routing games have been identified as the dynamics of centralized mirror descent in the strategy space of the players; see [12] for an example. In that context, convergence of the learning dynamics to the Nash equilibria (the minimizers of a convex potential function of the routing game) is critical; convergence to the optimal function value is not enough.

In this paper, our main contribution is thus a proof of convergence to an optimizer in the MD method, where the objective function is convex and not necessarily differentiable; we consider both the centralized and distributed settings.

II Centralized Mirror Descent

Let describe a finite-dimensional Hilbert space over reals, and be a closed convex subset of . Consider a possibly nonsmooth convex and continuous function that we seek to minimize via MD, starting from . We assume throughout that is finite-valued, and its effective domain contains . Further, we assume throughout that has at least one finite optimizer over .

To precisely define MD, consider a continuously differentiable -strongly convex function on an open convex set whose the closure contains . By that, we mean satisfies

Here, denotes the gradient of which is assumed to be diverged on the boundary of . In addition, is the norm induced by the inner product. Define the Bregman divergence associated with for all and in as

| (1) |

Equipped with this notation, MD prescribes the following iterative dynamics, starting from some .

| (2) |

Here, is an arbitrary subgradient of at , the collection of which comprise the subdifferential set , defined as

We note that MD enjoys an optimal convergence rate for nonsmooth functions [17, 4], i.e.,

where is the optimal value of over . Of interest to us in this work is the possible convergence of the problem variables themselves, i.e., whether converges to an optimizer for a suitable choice of step sizes . In the remainder of this section, we prove such a convergence result for centralized , and extend this to a distributed setting in the next section.

Theorem 1

Suppose

-

•

is -Lipschitz continuous over , and

-

•

defines a nonincreasing sequence of positive step sizes that is square-summable, but not summable, i.e., .

Then, optimizes over for ’s generated by MD in (2).

In proving the result, the following two properties of Bregman divergence will be useful. Their proofs are straightforward from its definition in (1).

| (3) |

for arbitrary , , in .

II-A Proof of Theorem 1

Our proof proceeds in two steps. We first show that consecutive iterates satisfy

| (4) |

for each . We then deduce the result from (4).

Proof of (4)

The optimality of in (2) implies

| (5) |

Here, stands for the derivative of the Bregman divergence with respect to the first coordinate. The properties of the divergence in (3) yield

Substituting the above relation in (5), we get

| (6) |

An appeal to Cauchy-Schwartz and arithmetic-geometric mean inequalities allows us to bound the last term on the right hand side of the above inequality, as follows,

The above inequality and (6) together imply

Lipschitz continuity of yields , from which we get (4).

Deduction of Theorem 1 from (4)

Let be the set of optimizers of over , and be an arbitrary element in . Then, the convexity of implies

Using the above relation in (4) with gives

Summing the above over from 0 to , we get

Taking , the right hand side remains bounded, owing to the square summability of the ’s. Bregman divergence is always nonnegative, and so is each summand in the second term on the left hand side of the above inequality. Together, they imply that and converges for each . The non-summability of the ’s further yields

Convergence of for each implies the boundedness of the iterates . Let be the bounded subsequence of ’s along which

| (7) |

This bounded sequence has a (strongly) convergent subsequence. Function evaluations over that subsequence tend to . Continuity of implies that the subsequence converges to a point in . Call this point . Then, converges, and it converges to zero over said subsequence, implying

Appealing to (3), we conclude . This completes the proof of Theorem 1.

Remark 1

This proof should be generalizable to being infinite dimensional, where one would consider weak convergence of to an optimizer of over .

III Distributed Mirror Descent

In this section, we consider a distributed variant of MD. More precisely, we consider a collection of agents who collectively seek to minimize over . Agent only knows the convex but possibly non-smooth function , and thus, the agents must solve the problem cooperatively. The agents are allowed to exchange their iterates only with their neighbors in an undirected graph . Starting from , each agent communicates with its neighbors in and updates its iterates at time as follows.

| (8) |

Matrix thus encodes the communication graph , i.e., if and only if agent can communicate to agent its current iterate, denoted by an edge between and in . Rates for convergence of the function value in the above distributed mirror descent (DMD) algorithm have been reported in [14, Theorem 2]. We prove that DMD drives to a common optimizer of over .

Theorem 2

Suppose

-

•

is -Lipschitz continuous over ,

-

•

defines a nonincreasing sequence of positive step sizes that is square-summable, but not summable, i.e., ,

-

•

is convex,

-

•

is doubly stochastic, irreducible, and aperiodic.

Then, is identical across , and the limit optimizes over for ’s generated by DMD in (8).

The first two assumptions are identical to the centralized counterpart in Section II. The third one is special to the distributed setting, and is crucial to the proof of the result. We remark that Bregman divergence is always strictly convex in its first argument. Our result requires convexity in the second argument. A sufficient condition is derived in [1], that requires to be thrice continuously differentiable and satisfy and for all and in , where stands for the Hessian of . The last assumption defines a requirement on the information flow. Stated in terms of graph that defines the connectivity among agents, it is sufficient to have being connected with at least one node with a self-loop.

III-A Proof of Theorem 2

We first appeal to the optimality of in (8) to conclude

| (9) |

for every . The properties of Bregman divergence in (3) yield

| (10) |

Substituting the above equality in (9), and summing over , we get an inequality of the form

| (11) |

where

for each . We provide upper bounds on each of the summations separately. In the sequel, we use the notation

| (12) |

An upper bound for

We bound each summand in both the summations above. Using the convexity of , we get

| (13) |

The last line follows from the Cauchy-Schwarz inequality and that is -Lipschitz. Further, the Cauchy-Schwarz and arithmetic-geometric mean inequalities yield

| (14) |

The last line is a consequence of being -Lipschitz.

An upper bound for

To bound the right-hand side, we utilize the convexity of in the second argument and the doubly stochastic nature of to obtain

Also, (3) gives

Combination of the above two inequalities then provides the sought upper bound on .

| (17) |

Utilizing the bounds on and

Let be an arbitrary optimizer of over . Applying the bounds in (16) and (17) in (11) with then gives

Summing the above over , we obtain

| (18) |

We mimic the style of arguments in the proof of Theorem 1 to complete the derivation, and provide an upper bound on the double summation on the right hand side of the above inequality.

An upper bound on

To derive this bound, we fix an orthonormal basis for with . Let denote the coordinates of in that basis. The coordinates for the centroid are given by . The inner product in becomes the usual dot product among the corresponding coordinates. The norm becomes the usual Euclidean 2-norm in the coordinates. Define

Let denote a vector of all ones and be the identity matrix. Also, define

for convenience. Equipped with this notation, we then have

| (19) |

Here, and denote the Frobenius and the 2-norm of matrices, respectively. In what follows, we bound from above.

Collecting the coordinates of in similarly to , we have

| (20) |

since commutes with . We bound each term on the right hand side above. For the first term, notice that

Since is doubly stochastic (i.e., ), the Perron-Frobenius theorem [9, Theorem 8.4.4] and the Courant-Fischer theorem [9, Theorem 4.2.11] together yield

| (21) |

where is the second largest singular value of . Further, is irreducible, and aperiodic, implying . To bound the second term on the right hand side of (20), we use that matrix norms are submultiplicative, and hence we have

| (22) |

because . To bound each term in the above summation, we utilize (9) and (10) with to obtain

| (23) |

Since is -Lipschitz, and is -strongly convex, we have the following two inequalities

that together with (23) gives

Summing the above over , we obtain an upper bound on the right hand side of (22). Utilizing that bound and (21) in (20), we get

| (24) |

For convenience we suppress the dependency of on in the sequel. Iterating the above inequality gives

for each , which further yields

| (25) |

Now, and the ’s are nonincreasing. Thus, we have

and using this in (25) gives the following required bound.

| (26) |

Proof of the result by combining all upper bounds

| (27) |

Driving , the right hand sides of (26) and (27) converge as the sequence of ’s are square summable. Further, the ’s are non-summable, and hence, we conclude

-

1.

,

-

2.

,

-

3.

converges.

Convergence of the Bregman divergences for each implies the boundedness of the iterates for each . Recall that denotes the collective iterate for all agents at time . Consider the bounded subsequence of , denoted , along which

This bounded sequence has a (strongly) convergent subsequence. Over that subsequence, the agents’ iterates converge to the centroid, and the function evaluations over the centroid tend to . Continuity of implies that each agent’s iterate over that subsequence converges to the same point in . Call this point . Since converges, it converges to zero over that subsequence, implying for each . Appealing to (3), we infer , concluding the proof.

IV Numerical experiments

Theorems 1 and 2 guarantee the convergence of the iterates to the optimizer, but do not provide convergence rates with non-summable but square summable step-sizes. Given the lack of rates, we empirically illustrate that mirror descent – both in centralized and distributed settings – often outperforms vanilla subgradient methods on simple examples with our step sizes. Our simulations are different from many prior works, e.g., [15], where they choose to guarantee the fastest convergence of the function value.

Consider the following robust linear regression problem over a simplex.

| (28) |

Robust regression fits a linear model to the data . It differs from ordinary least squares in that the objective function penalizes the entry-wise absolute deviation from the linear fit rather than the squared residue, and is known to be robust to outliers [10]. Consider two different Bregman divergences on the -dimensional simplex defined by the Euclidean distance , and negative entropy . Centralized mirror descent with amounts to a projected subgradient algorithm where each iteration is a subgradient step followed by a projection on . With , the updates define an exponentiated gradient method, also known as the entropic mirror descent algorithm (cf. [19, 2]). Its updates are given by

where the objective in (28) is , and

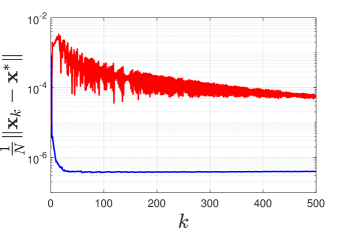

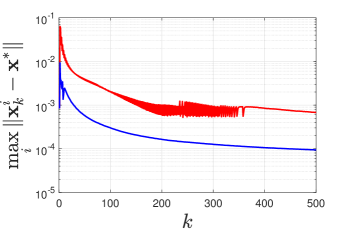

Here, denotes the sign of the argument, and is the -th row of . Negative entropy being a ‘natural’ function over simplex, entropic mirror descent enjoys faster convergence than projected subgradient descent, as shown in Figure 1(a) using step sizes .

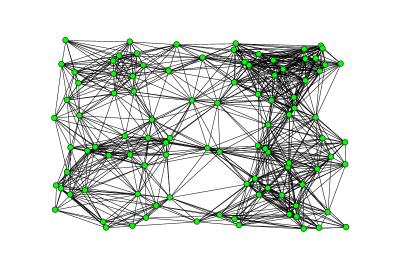

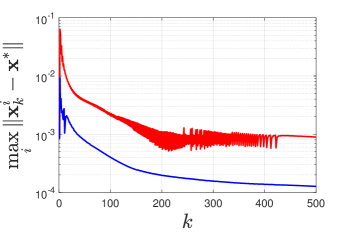

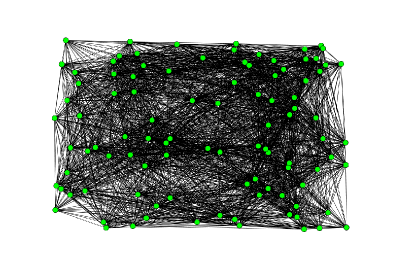

Next, consider the case where each node in a graph only knows and , and they together seek to minimize . Figures 1(b) and 1(c) show how the distributed variant of entropic mirror descent outperforms that of projected subgradient method with steps-sizes . We choose as the transition probabilities of a Markov chain in the Metropolis-Hastings algorithm for the respective graphs. Centralized algorithms converge faster than distributed algorithms; however, the denser the graph, the faster the convergence is of the distributed algorithms.

V Conclusion

In this paper, we proved guaranteed convergence of the iterates (i.e., the problem variables) to an optimizer in MD on a finite dimensional Hilbert space, using a specific choice of step size in both centralized and distributed settings. The convergence holds even when minimizing possibly non-smooth and non-strongly convex functions. This convergent behavior generalizes a similar property of subgradient methods. Extension to the case with additive noise with bounded support, and to infinite dimensional Hilbert and Banach spaces remain interesting directions for future research.

References

- [1] H. Bauschke and J. Borwein. Joint and separate convexity of bregman distance. Inherently Parallel Algorithms in Feasibility and Optimization and their Applications, pages 23–36, 2001.

- [2] A. Beck and M. Teboulle. Mirror descent and nonlinear projected subgradient methods for convex optimization. Operation Research Letters, 31(3):167–175, 2003.

- [3] Aharon Ben-Tal, Tamar Margalit, and Arkadi Nemirovski. The ordered subsets mirror descent optimization method with applications to tomography. SIAM Journal on Optimization, 12:79–108, 2001.

- [4] Sébastien Bubeck. Convex optimization: Algorithms and complexity. Found. Trends Mach. Learn., 8(3-4), nov 2015.

- [5] T. T. Doan and C. L. Beck. Distributed lagrangian methods for network resource allocation. In 2017 IEEE Conference on Control Technology and Applications (CCTA), pages 650–655, 2017.

- [6] Thinh T. Doan, Subhonmesh Bose, and Carolyn L. Beck. Distributed lagrangian method for tie-line scheduling in power grids under uncertainty. SIGMETRICS Perform. Eval. Rev., 45(2), October 2017.

- [7] J. C. Duchi, A. Agarwal, M. Johansson, and M. I. Jordan. Ergodic mirror descent. In Proc. 49th Annual Allerton Conference, pages 701–706, USA, Sept 2011.

- [8] E. C. Hall and R. M. Willett. Online convex optimization in dynamic environments. IEEE Journal on Selected Topics in Signal Processing, 9(4):647–662, 2015.

- [9] R.A. Horn and C.R. Johnson. Matrix Analysis. Cambridge, U.K.: Cambridge Univ. Press, 1985.

- [10] Otto J Karst. Linear curve fitting using least deviations. Journal of the American Statistical Association, 53(281):118–132, 1958.

- [11] W. Krichene, A. M. Bayen, and P. L. Bartlett. Accelerated mirror descent in continuous and discrete time. In Proc. Advances in Neural Information Processing Systems 28 (NIPS 2015), Canada, Dec 2015.

- [12] W. Krichene, S. Krichene, and A. Bayen. Convergence of mirror descent dynamics in the routing game. In 2015 European Control Conference (ECC), pages 569–574, 2015.

- [13] G. S. Ledva, L. Balzano, and J. L. Mathieu. Inferring the behavior of distributed energy resources with online learning. In Proc. 53th Annual Allerton Conference, pages 6321–6326, USA, Oct 2015.

- [14] J. Li, G. Li, Z. Wu, and C. Wu. Stochastic mirror descent method for distributed multi-agent optimization. Optimization Letters, 24(1):1–19, 2014.

- [15] A. Nedić and S. Lee. On stochastic subgradient mirror-descent algorithm with weighted averaging. SIAM Journal of Optimization, 24(1):84–107, 2014.

- [16] A. Nedić, A. Olshevsky, and C.A. Uribe. Distributed learning with infinitely many hypotheses. In Proc. 2016 IEEE 55th Conference on Decision and Control, pages 6321–6326, USA, Dec 2016.

- [17] A. S. Nemirovsky and D. B. Yudin. Problem complexity and method efficiency in optimization. Wiley-Interscience series in discrete mathematics, Wiley, 1983.

- [18] M. Nokleby and W. U. Bajwa. Stochastic optimization from distributed, streaming data in rate-limited networks. IEEE Transactions on Signal and Information Processing over Networks, 170(3):1–13, 2017.

- [19] Doina Precup and Richard S Sutton. Exponentiated gradient methods for reinforcement learning. In Proceedings of International Conference on Machine Learning, pages 272–277, 1997.

- [20] M. Rabbat. Multi-agent mirror descent for decentralized stochastic optimization. In Proc. IEEE 6th International Workshop on Computational Advances in Multi-Sensor Adaptive Processing (CAMSAP)), pages 517–520, Mexico, Dec 2015.

- [21] M. Raginsky and J. Bouvrie. Continuous-time stochastic mirror descent on a network: Variance reduction, consensus, convergence. In Proc. IEEE 51st Conference on Decision and Control, pages 6793–6800, USA, Dec 2012.

- [22] S. Shahrampour and A. Jadbabaie. Distributed online optimization in dynamic environments using mirror descent. IEEE Transactions on Automatic Control, PP(99):1–12, 2017.

- [23] Z. Zhou, P. Mertikopoulos, N. Bambos, P. Glynn, and C. Tomlin. Countering feedback delays in multi-agent learning. In Proc. The 31st International Conference on Neural Information Processing Systems, pages 5776–5783, USA, Dec 2017.

- [24] Z. Zhou, P. Mertikopoulos, A. L. Moustakas, N. Bambos, and P. Glynn. Mirror descent learning in continuous games. In Proc. IEEE 56th Conference on Decision and Control, pages 5776–5783, Scotland, Dec 2017.