Stochastic differential switching game in infinite horizon

Abstract

We study a zero-sum stochastic differential switching game in infinite horizon. We prove the existence of the value of the game and characterize it as the unique viscosity solution of the associated system of quasi-variational inequalities with bilateral obstacles. We also obtain a verification theorem which provides an optimal strategy of the game. Finally, some numerical examples with two regimes are given.

AMS subject classifications: 49N70, 49L25, 60H30, 90C39, 93E20

: stochastic differential game, switching strategies, quasi-variational inequality, value function, viscosity solution

1 Introduction

Differential game theory involves multiple persons (also called players or individuals) decision making in the context of dynamic system. The study of the two-person zero-sum differential games could be traced back to the pioneering work by Isaacs [21], which inspired further research in this area.

In 1989, Fleming and Souganidis [15], for the first time, studied two-person zerosum stochastic differential games. They adopted the definitions of upper and lower value functions introduced by Elliott and Kalton [13] and proved that the two value functions satisfy the dynamic programming principle and they are the unique viscosity solutions to the associated Hamilton–-Jacobi–-Bellman–-Isaacs partial differential equations (HJBI PDEs). Their work generalized that of Evans and Souganidis [14] from the deterministic framework to the stochastic one and is now regarded as one of the outstanding results in the field of stochastic differential games. In 1995, Hamadène and Lepeltier [17] introduced the backward stochastic differential equation (BSDE) theory into the study of stochastic differential games, and there exist also many other works using this BSDEs approach, such as Hamadène, Lepeltier, and Peng [18]. Subsequently, Buckdahn and Li [2] extended the findings presented in [17, 18], and generalized the framework introduced in [15].

In this paper we consider the state process of the stochastic differential game, defined as the solution of the following stochastic equation:

with . Here is a d-dimensional Wiener process, while

with the cost functional

| (1.1) |

The first player chooses the control a from a given finite set to maximize the payoff (1.1), and each actions is related with one cost C, while the second player chooses the control b from to minimize the payoff (1.1), and each of his actions is associated with the other cost . The zero-sum stochastic differential games problems we will investigate is to show the upper and lower value functions coincide and the game admits a value. The Isaacs’ system of quasi-variational inequalities for this switching game is the following: for any , and ,

| (1.2) |

and

| (1.3) |

where,

In the finite horizon framework, the switching game have been studied by several authors. The most recent work discussing this topic includes the papers by Djehiche et al. (2017) ([8]), Tang and Hou (2007) ([32]).

The objective of this work is to establish existence and uniqueness of a continuous viscosity solution of (1.2) and (1.3). The second contribution of our paper is the Verification Theorem which provides an optimal strategy of the game, To the best of our knowledge, this issue have not been addressed in the literature yet.

This paper is organized as follows: in Section 2 we list all the notations, state the full set of assumptions, and define viscosity sub- and supersolutions along with equivalent characterizations. In Section 3, we shall introduce the stochastic differential game problem and give some preliminary results of the lower and the upper value functions of stochastic differential game. In Section 4, by the dynamic programming principle we prove that the lower and upper value functions of the game satisfy the Isaacs’ system of quasi-variational inequalities in the viscosity solution sense. In Section 5, we show that the solution of Isaacs’ system of quasi-variational inequalities is unique. Further, the upper and the lower value functions coincide and the game admits a value. In Section 6, we present a verification theorem which gives an optimal strategy of the switching game, while finally Section 7 will present some numerical examples.

2 Assumptions and problem formulation

Throughout this paper and are two integers. Let the finite set of regimes, and assume the following assumptions:

[H1] and be two continuous functions for which there exists a constant such that for any and

| (2.1) |

Thus they are also of linear growth. i.e., there exists a constant such that for any and

| (2.2) |

[H2] is a continuous function for which there exists a constant such that for each , :

| (2.3) |

| (2.4) |

[H3] For any The switching costs and are constants, and we assume the triangular condition :

| (2.5) |

| (2.6) |

which means that it is less expensive to switch directly in one step from regime to than in two steps via an intermediate regime . Notice that a switching costs and may be negative, and conditions (2.5) and (2.6) for prevents an arbitrage by simply switching back and forth, i.e.

| (2.7) |

| (2.8) |

We set and .

We now consider the following Isaacs’ system of quasi-variational inequalities: for any , and ,

| (2.9) |

and

| (2.10) |

Where

(i) is a positive discount factor and is the following infinitesimal generator:

(ii) For any and

We now define the notions of viscosity solution of the system (2.9). We can similarly define the notions for (2.10).

Definition 1

Let such that for any , is continuous, is called:

(i) A viscosity supersolution to (2.9) if for any , for any and any function such that and is a local maximum

of , we have:

| (2.11) |

(ii) A viscosity subsolution to (2.9) if for any , for any and any function such that and is a local minimum of , we have:

| (2.12) |

(iii) A viscosity solution if it is both a viscosity supersolution and subsolution.

There is an equivalent formulation of this definition (see e.g.[5]) which we give since it will be useful later. So firstly we define the notions of superjet and subjet of a continuous function .

Definition 2

Let , an element of and finally the set of symmetric matrices. We denote by (resp. , the superjets (resp. the subjets) of at x, the set of pairs such that:

Note that if has a local maximum (resp. minimum) at , then we obviously have:

We now give an equivalent definition of a viscosity solution of of the system (2.9).

Definition 3

Let such that for any ; continuous , is called a viscosity supersolution (resp. a viscosity subsolution) to (2.9) if for any , for any and any (resp.

| (2.13) |

It is called a viscosity solution if it is both a viscosity subsolution and supersolution.

3 The zero-sum switching game

3.1 Setting of the problem

Consider a complete probability space () and a -dimensional standard Wiener process defined on it. Let be the natural filtration generated by the Wiener process, completed with the -null sets of . We begin by description of the zero-sum switching game.

Definition 4

Assume we have two players I and II who intervene on a system (e.g. the production of energy from several

sources such as oil, cole, hydro-electric, etc.) with the help of switching strategies. An admissible switching process

for I (resp. II) is a sequence (resp. where:

(i) (resp. , the action times, is a sequence of -stopping times such that (resp. and (resp. ).

(ii) (resp. , the actions, is a sequence of -valued random variables, where each (resp. ) is -measurable (resp. -measurable).

Next let be fixed. We say that the admissible switching strategy of I (resp. (resp. II) belongs to (resp. ) if (resp. ).

Given an admissible strategy (resp. ) of I (resp. II), one associates a stochastic process (resp. which indicates along with time the current mode of I (resp. II) and which is defined by:

| (3.1) |

The evolution of

the state of the game is described by the following stochastic equation:

| (3.2) |

We assume that for any and , there exists a unique strong solution to (3.2). Let now (resp. be an admissible strategy for I (resp. II) which belongs to (resp. ). The interventions of the players are not free and generate a payoff which is a reward (resp. cost) for I (resp. II) and whose expression is given by

| (3.3) |

Following Buckdahn and Li [2], we define nonanticipative strategy as follows.

Definition 5

A nonanticipative strategy for player I is a mapping

such that for any stopping time and any , , with on it holds that on .

(with the notation

A nonanticipative strategy for player

II

is defined similarly. The set of all nonanticipative strategies (resp. ) for player I

(resp. II) is denoted by

(resp, .

We define the upper (resp. lower) value of the game by

| (3.4) |

(resp.

| (3.5) |

The game has a value if

3.2 Preliminary results

In this section we present some properties of the lower and upper value functions of our switching game.

Lemma 1

(see e.g. [29]) The process satisfies the following estimate: There exists a constant such that

| (3.6) |

Proposition 1

Under the standing assumptions (H1), (H2) and (H3), there exists some positive constant such that for , the lower and upper value function are satisfy a linear growth condition: for all and there exists a constant such that

| (3.7) |

: We make the proof only for the lower value function , the other case being analogous. for every we consider the particular strategy: given by for all we have

| (3.8) |

Then for every , there exists a strategy such that

| (3.9) |

The switching cost is dominated by

| (3.10) |

for any , which can be proved by induction as in [26]. Indeed, (3.10) obviously holds for N= 1. Suppose now that it is also verified for some and let us show that it is valid for . When holds as . When , we have

Combining (3.9) and (3.10) gives us

| (3.11) |

Now, from estimate (3.6) and the polynomial growth condition of in (H2), there exists and such that

| (3.12) |

Therefore if we have

On the other hand, by considering the particular strategy given by for all , and for there exists a strategy such that

| (3.13) |

For all we have

Then, we get

| (3.14) |

As a consequence, there exists and such that

| (3.15) |

Therefore if , we have

from which we deduce the thesis.

Lemma 2

There exists some positive constant such that for , and we have

for some positive constant C.

It is enough to show that the conclusion holds for the gain functional .

For every , we have

By a standard estimate for the SDE applying Ito’s formula to and using Gronwall’s lemma, we then obtain from the Lipschitz condition on , the following inequality

From the Lipschitz condition on , we deduce

for . This ends the proof.

In the sequel, we shall assume that is large enough, which ensures that the value functions are Lipschitz continuous. We now present the dynamic programming principle of the zero-sum switching game.

Theorem 1

For any and , we have

| (3.16) |

| (3.17) |

where is any stopping time.

4 Isaacs’ system of quasi-variational inequalities

In the present section we prove that the two value functions are viscosity solutions to (2.9) and (2.10). But we make the proof only for (2.10), the other case is analogous. We begin with the following lemma.

Lemma 3

For any , the lower and upper value functions satisfy the following properties: for all ,

| (4.1) |

| (4.2) |

We make the proof only for the lower value function , the other case being analogous. For every and we define by

Note that Let and , then

from which we deduce that the following inequality holds:

Therefore

In a similar way we can prove , hence deducing the thesis.

Theorem 2

For any , the lower value function and the upper value function are viscosity solutions of (2.9).

We state the proof only for lower value function, the other case is analogous. First, we prove the supersolution property. Fix and let such that is a minimum of with . We have, by Lemma 3

If

then we are done. Now suppose

we prove by contradiction that

Suppose otherwise, i.e., . Then without loss of

generality we can assume that and on .

Define the stopping time by

Let , using the dynamic programming principle, we deduce the existence of a strategy such that

Therefore, without loss of generality, we only need to consider such that . Then

By applying Itô’s formula to and plugging into the last inequality, we obtain

which is a contradiction. Therefore, we must have

.

Thanks to Lemma 3, it is enough to show that given

such that

Then

| (4.3) |

Which is the supersolution property. The subsolution property is proved analogously.

5 Uniqueness of the solution of Isaacs’ system of quasi-variational inequalities

We prove that the (2.9) admits a unique viscosity solution. We need to make an additional assumption on the switching costs.

[H5] (The no free loop property)

For any sequence of pairs such that and for either or , we have

We begin with the technical lemma.

Lemma 4

Let and be a viscosity subsolution and a viscosity supersolution to the equation (2.9), respectively. Let be fixed and such that

| (5.1) |

and

| (5.2) |

Then there exists such that

| (5.3) |

and

| (5.4) |

. Suppose that , then there exists , such that

| (5.5) |

Since is a subsolution, it satisfies

| (5.6) |

which implies that

Hence

| (5.7) |

Then (5.5), (5.6) and (5.7) imply

Similarly if hold, then there exists such that

and

Now if the new index ( or ) verify (5.2) , we repeat this reasoning . If this case continues to occur, finally we find a loop such that

Hence we obtain a contradiction to the assumption (H5). Thus (5.3) and (5.4) holds for some

Theorem 3

Let (resp. a family of continuous viscosity subsolutions (resp. supersolutions) to (2.9), and satisfying a linear growth condition. Then, for all

Let us proceed by contradiction. For some suppose there exists there exists such that

| (5.8) |

We divide the proof into two steps.

Step 1. Using Lemma 4 we derive the existence of and such that

| (5.9) |

and

| (5.10) |

For a small , let be the function defined as follows.

| (5.11) |

Let be such that

| (5.12) |

From we have

| (5.13) |

and consequently is bounded,

and as , . Since

and are uniformly continuous, then as

Next, recalling that and are continuous, then, for small enough and at least for a subsequence which we still index by , we obtain

| (5.14) |

Step 2. Let us denote

| (5.15) |

Then we have:

| (5.16) |

Then applying the result by Crandall et al. (Theorem 3.2, [5]) to the function

at the point , for any , we can find such that:

| (5.17) |

Then by definition of viscosity solution, we get:

| (5.18) |

and

| (5.19) |

which implies that:

| (5.20) |

we have :

| (5.21) |

where which hereafter may change from line to line. Choosing now yields the relation

| (5.22) |

Now, from (H1), (5.17) and (5.22) we get:

Next

So that by plugging into (LABEL:viscder) we obtain:

| (5.23) |

By sending , and taking into account of the continuity of , we obtain which is a contradiction. Thus, , for any , which is the desired result.

6 A verification theorem

In this section, we present a verification theorem which gives an optimal strategies of our zero-sum stochastic differential game.

We suppose that a classical solution of (2.9) exists, denoted by . Then for each separates the space into four regions:

Let us define the strategies (resp. as follows:

and for any ,

(resp.

We are now ready to present the verification theorem for our switching game.

Theorem 4

For each , , and assume that . Then we have

First for each and we define an increasing sequence of stopping times by

Then the cost functional is rewritten as:

| (6.1) |

Now, let associated with and , then when we have

| (6.2) |

Then by Itô’s formula (see, e.g., Sect. IV.45 of [31]), we obtain

| (6.3) |

Substituting this into (6.1), we obtain

| (6.4) |

We now estimate the term in the right-hand side of (6.4) for each .

-

•

If for some we have

(6.5) -

•

If for some we have

(6.6) -

•

If for some we have

(6.7)

By (6.4) and the estimates in (6.5)-(6.7) it follows that

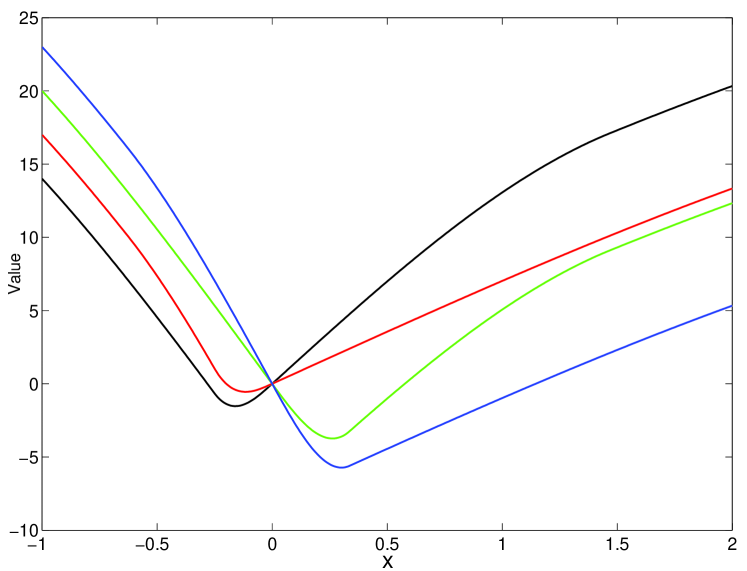

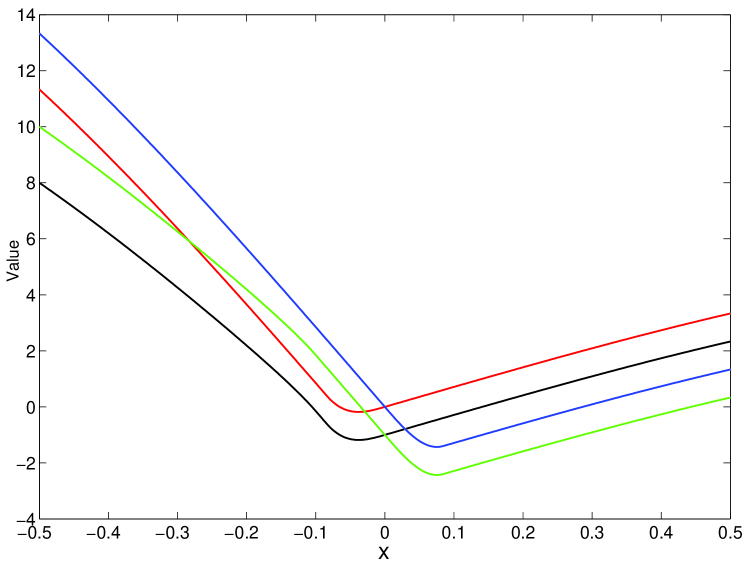

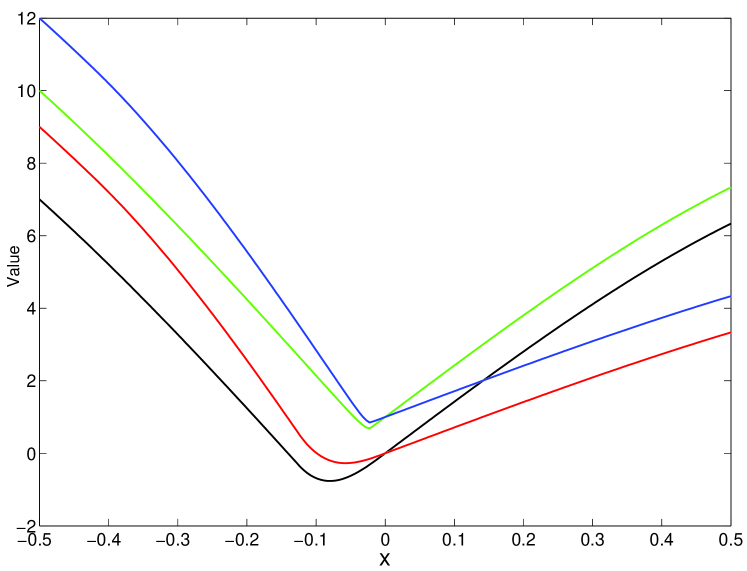

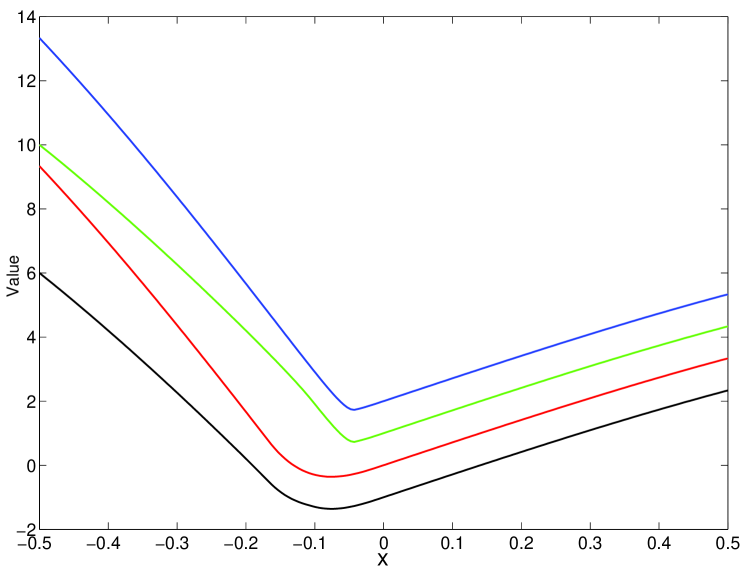

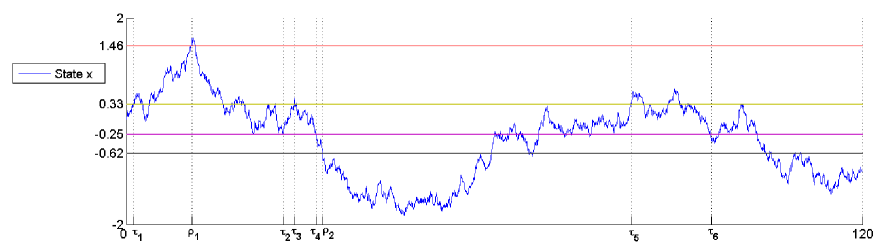

7 Numerical results

In this section, we present the results of some numerical simulations on the game by

using MATLAB, here we apply the policy iteration algorithm for solving numerically(2.9).

In particular, for the numerical example we consider a two-regime switching problem where the diffusion is independent of the regime and follows a geometric Brownian motion, i.e and for

some and .

We consider the following game problem:

| (7.1) |

In the flowing figures, we plot the value functions for different switching costs.

.

Next, we plot the optimal strategies of our zero-sum stochastic differential game. We focus on exemple in figure . First let . Then by figure (exemple we get

| (7.2) |

References

- [1] G. Barles : Solutions de Viscosité des équations de Hamilton-Jacobi. Mathématiques et Applications (17).Springer, Paris (1994).

- [2] R. Buckdahn and J. Li, Stochastic differential games and viscosity solutions of Hamilton– Jacobi-–Bellman–-Isaacs equations, SIAM J. Control Optim., 47 (2008), pp. 444–-475.

- [3] R. Carmona and M. Ludkovski: Valuation of energy storage: an optimal switching approach. Quant. Finance 10 (2010), no. 4, 359–374.

- [4] J.-F. Chassagneux, R. Elie and Kharroubi, I.: Discrete–time approximation of multi-dimensional BSDEs with oblique reflections. Ann. Appl. Probab. 22 (2012), no. 3, 971–1007.

- [5] M. Crandall, H. Ishii, H and P.L. Lions, User’s guide to viscosity solutions of second order partial differential equations, Bull. Amer. Math. Soc, 27 (1992), 1–67.

- [6] B. Djehiche, S. Hamadène, and M.-A. Morlais : Viscosity Solutions of Systems of Variational Inequalities with Inter-connected Bilateral Obstacles. Funkcialaj Ekvacioj, 58 (2015), pp.135–175.

- [7] B. Djehiche, S. Hamadène, and A. Popier: A finite horizon optimal multiple switching problem, SIAM Journal Control and Optim, 48(4): 2751–2770, 2009.

- [8] B. Djehiche, S. Hamadène, M.-A. Morlais, X. Zhao: On the equality of solutions of max–min and min–max systems of variational inequalities with interconnected bilateral obstacles. J. Math. Anal. Appl. 452(1), 148–175 (2017)

- [9] B. El Asri Deterministic minimax impulse control in finite horizon: the viscosity solution approach. ESAIM: Control Optim. Calc. Var., 19, 63–77.

- [10] B. El Asri Minimax Impulse Control Problems in Finite Horizon. arXiv:1305.0914

- [11] B. EL Asri and S. Mazid: Zero-sum stochastic differential game in finite horizon involving impulse controls. IN arxiv preprint arxiv: 1706.08880 (2017).

- [12] R. Elie and I. Kharroubi: Probabilistic representation and approximation for coupled systems of variational inequal-ities. Statist. Probab. Lett. 80 (2010), no. 17-18, 13881396.

- [13] R. Elliott and N. Kalton, The Existence of Value in Differential Games, Mem. Amer. Math. Soc. , American Mathematical Society, Providence, RI, .

- [14] C. Evans and E. Souganidis. Differential games and representation formulas for solutions of Hamilton-Jacobi-Isaacs equations. Indiana Univ. Math. J., 33(5):773-–797, 1984.

- [15] W. H. Fleming and P. E. Souganidis, On the existence of value functions of two-player, zero-sum stochastic differential games, Indiana Univ. Math. J., , pp. 293–314.

- [16] S. Hamadène and M. Jeanblanc,: On the starting and stopping problem: application in reversible investments. Math. Oper. Res. 32 (2007), no. 1, 182–192.

- [17] S. Hamadène and J.-P. Lepeltier, Zero-sum stochastic differential games and backward equations, Systems Control Lett., 24 (1995), pp. 259–-263.

- [18] S. Hamadène, J.-P. Lepeltier, and S. Peng, BSDEs with continuous coefficients and stochastic differential games. in Backward Stochastic Differential Equations, N. El Karoui and L. Mazliak eds., Pitman Res. Notes Math. Ser., 364, Longman, Harlow (1997), pp. 115–-128.

- [19] Y. Hu and S. Tang: Multi-dimensional BSDE with oblique reflection and optimal switching, Proba. Theo. and Rel. Fields, 147, N. 1-2: 89–121, 2010.

- [20] H. Ishii and S.Koike: Viscosity Solutions of a System of Nonlinear Second-Order Elliptic PDEs Arising in Switching Games. Funkcialaj Ekvacioj, 34 (1991) 143-155.

- [21] R. Isaacs. Differential games. A mathematical theory with applications to warfare and pursuit, control and optimization. John Wiley and Sons, Inc., New York-London-Sydney, 1965.

- [22] M. Ludkovski: Stochastic switching games and duopolistic competition in emissions markets. SIAM J. Financial Math. 2 (2011), no. 1, 488–511.

- [23] K. Li, K. Nystrom and M.Olofsson: Optimal switching problems under partial information. Monte Carlo Methods and Applications, 21(2), 91-120 (2015).

- [24] N.L.P. Lundstrom, K. Nystrom and M. Olofsson: Systems of variational inequalities in the context of optimal switching problems and operators of Kolmogorov type. Annali di Matematica Pura ed Applicata (2014) Volume 193, Issue 4, pp 1213–1247.

- [25] N.L.P. Lundstrom, K. Nystrom and M. Olofsson: Systems of Variational Inequalities for Non-Local Operators Related to Optimal Switching Problems: Existence and Uniqueness. Manuscripta Mathematica, Nov. 2014, Vol. 145, Issue 3, pp. 407–432.

- [26] V. Ly Vath and H. Pham, Explicit solution to an optimal switching problem in the two-regime case, SIAM J. Control Optim., 46 (2007), pp. 395–-426.

- [27] M. Perninge and L. Soder: Irreversible investments with delayed reaction: an application to generation re-dispatch in power system operation. Math. Methods Oper. Res. 79 (2014), no. 2, 195–224.

- [28] H. Pham, L.V. Vathana and X.Y.Zhou: Optimal switching over multiple regimes. SIAM J. Control Optim. 48 (2009), no. 4, 2217–2253.

- [29] D. Revuz and M. Yor, (1991): Continuous Martingales and Brownian Motion. Springer Verlag, Berlin.

- [30] S. Tang and S.-H. Hou : Switching games of stochastic differential systems, SIAM J. Control Optim., 46(3): 900–929, 2007.

- [31] L.C.G. Rogers and D. Williams, Diffusions, Markov processes, and martingales. John Wiley and Sons, New York (1987).

- [32] S. Tang and S.-H. Hou : Switching games of stochastic differential systems, SIAM J. Control Optim., 46(3): 900–-929, 2007.

- [33] S. Tang and J. Yong (1993) : Finite horizon stochastic optimal switching and impulse controls with a viscosity solution approachâ€, Stoch. and Stoch. Reports, 45, 145–176.

- [34] M. Zervos : A problem of sequential entry and exit decisions combined with discretionary stopping. SIAM J. Control Optim. 42 (2003), no. 2, 397-421 (electronic).