Experimental Design via Generalized Mean Objective Cost of Uncertainty

Abstract

The mean objective cost of uncertainty (MOCU) quantifies the performance cost of using an operator that is optimal across an uncertainty class of systems as opposed to using an operator that is optimal for a particular system. MOCU-based experimental design selects an experiment to maximally reduce MOCU, thereby gaining the greatest reduction of uncertainty impacting the operational objective. The original formulation applied to finding optimal system operators, where optimality is with respect to a cost function, such as mean-square error; and the prior distribution governing the uncertainty class relates directly to the underlying physical system. Here we provide a generalized MOCU and the corresponding experimental design. We then demonstrate how this new formulation includes as special cases MOCU-based experimental design methods developed for materials science and genomic networks when there is experimental error. Most importantly, we show that the classical Knowledge Gradient and Efficient Global Optimization experimental design procedures are actually implementations of MOCU-based experimental design under their modeling assumptions.

I Introduction

The mean objective cost of uncertainty (MOCU) quantifies the performance cost of using an operator that is optimal across an uncertainty class of systems as opposed to an operator that is optimal for a particular system within the class [1]. MOCU-based experimental design selects an experiment that maximally reduces MOCU, thereby optimally reducing uncertainty with respect to the operational objective [2]. For instance, if one wishes to design a Wiener filter when the relevant power spectra not fully known but belong to an uncertainty class of power spectra, then the problem is to design a linear filter that is optimal relative to both mean-square error (MSE) and the probability mass over the uncertainty class. An optimal experiment maximally reduces MOCU relative to uncertainty in the relevant power spectra [3].

This letter provides a generalized formulation of MOCU not necessarily dependent on the particularities of the underlying system model or involving a design problem focused on operators. We show that the corresponding generalized experimental design encompasses existing formulations in signal processing, genomics, and materials discovery, and that it fits within Lindley’s paradigm for Bayesian experimental design [4]. Within this generalized framework we examine the connection and differences of MOCU-based formulations with other Bayesian experimental design methods. In particular, we show that the generalized MOCU generates the same policies as Knowledge Gradient (KG) [5, 6] and Efficient Global Optimization (EGO) [7] under their modeling assumptions, that is, for optimal experimental design under Gaussian belief and observation noise for an offline ranking and selection problem. Not only does the generalized MOCU framework unify disparate problems, it opens up Bayesian experimental design for reduction of objective related uncertainty, as demonstrated by materials discovery using Ginzburg-Landau theory.

II Generalized MOCU

We first formulate experimental design in terms of generalized MOCU and then give the standard method by simply defining the terms in the generalized model appropriately. In this letter, the lower case Greek letters denote random variables or distribution functions and capital Greek letters denote the corresponding domain space. We assume a probability space with probability measure , a set , and a function , where , and are called the uncertainty class, prior distribution, action space, and cost function, respectively. Elements of and are called uncertainty parameters and actions, respectively. For any , an optimal action is an element such that for any . An intrinsically Bayesian robust (IBR) action is an element such that for any .

Whereas is optimal over , for , is optimal relative to . The objective cost of uncertainty is defined by the performance loss of applying instead of on :

| (1) |

Averaging this cost over gives the mean objective cost of uncertainty (MOCU):

| (2) |

The action space is arbitrary so long as the cost function is defined on . It can be a set of filters defined on a random process with being mean-square error or a set of drug interventions with quantifying patient condition.

As noted in [1], MOCU can be viewed as the minimum expected value of a Bayesian loss function that maps an operator to its differential cost (for using the given operator instead of an optimal operator). The minimum expectation is attained by an optimal robust operator that minimizes the average differential cost. In decision theory, this differential cost is called the regret, which is defined as the difference between the maximum payoff (for making an optimal decision) and the actual payoff (for the decision that has been made). From this perspective, MOCU can be viewed as the minimum expected regret for using a robust operator.

Suppose there is a set , called the experiment space, whose elements, , called experiments, are jointly distributed with the uncertainty parameters . Given , the conditional distribution is the posterior distribution relative to and denotes the corresponding probability space, called the conditional uncertainty class. Relative to , we define IBR actions and the conditional (remaining) MOCU,

| (3) |

where the expectation is with respect to . Taking the expectation over gives the expected remaining MOCU,

| (4) |

which is called the experimental design value. An optimal experiment minimizes , i.e.,

| (5) |

also minimizes the difference between the expected remaining MOCU and the current MOCU:

| (6) |

With sequential experiments, the action space and experiment space can be time dependent, i.e., they can be different for each time step. Hereafter, in sequential experiment setups, the action space and experiment space at time step , and the optimal experiment selected at to be performed at the next time step are denoted by , , and , respectively. Let be the posterior distribution after observing the selected experiments’ outcomes from the first time step through , and denote the corresponding conditional uncertainty class. When experiments are selected sequentially and there is no fixed limited budget of experiments but instead the experimenter wants to stop the iterative procedure when only negligible knowledge regarding the objective can be gained from additional experiments, the form in (6) is useful because it incorporates the difference between the expected remaining MOCU and the current MOCU. The iterative procedure may be stopped if it falls below a threshold. While this procedure is optimal at each step, it is not optimal given a fixed number of experiments to be performed. This latter kind of finite-horizon optimal design using MOCU is treated in [8] using dynamic programming.

In the standard formulation, MOCU depends on a class of operators applied to a parameterized physical model in which is a random vector whose distribution depends on a physical characterization of the uncertainty. For instance, in a gene regulatory network, uncertainty arises regarding regulations and experimental design decides which unknown regulations should be determined via experiments so as to minimize the cost of uncertainty relative to the objective of minimizing the long-run likelihood of the cell being in a cancerous state [1, 2, 9]. is an uncertainty class of system models parameterized by a vector governed by a probability distribution and is a class of operators on the models whose performances are measured by . For each operator , is the cost of applying on model . Initially proposed for optimal intervention in Markovian regulatory networks [1] and optimal robust classification [10], IBR operators have been designed for linear and morphological filters [11] and Kalman filters [12].

As originally formulated [2], experimental design involves experiments , where experiment exactly determines the uncertain parameter in . The conditional uncertainty vector is composed of all uncertain parameters other than , with now determined by . is the reduced uncertainty class given . The IBR operator for , the remaining MOCU given , and the experimental design value take the forms , , and , respectively. The optimal experiment is specified by .

Returning to the generalized MOCU formulation, there is wide flexibility in experimental design, depending on the assumptions regarding the uncertainty class, action space, and experiment space, leading to many existing Bayesian experimental design formulations. Bayesian experimental design has a long history, in particular, utilizing the expected gain in Shannon information [13, 14, 15, 16]. In 1972, Lindley proposed a general decision theoretic approach incorporating a two-part decision involving the selection of an experiment followed by a terminal decision [4]. Supposing is a design selected from a family and is a data vector, and leaving out the terminal decision, an optimal experiment is given by

| (7) |

where is a utility function (see [17] for the full decision-theoretic optimization).

With generalized MOCU, each experiment corresponds to a data vector and the expected remaining MOCU is

| (8) |

From (8), the optimization of (5) can be expressed in the same form as (7), with in place of and utility function .

Hence, in descending order of generality, we have Lindley’s procedure, generalized MOCU, and MOCU. The salient point regarding the latter is that the uncertainty is on the underlying random process, meaning the science, and its aim is to design a better operator on the underlying process. As stated in [18], there is a scientific gap in constructing functional models and making prior assumptions on model parameters when the actual uncertainty applies to the underlying random processes. We next show how generalized MOCU includes other existing objective-based experimental-design formulations.

III Guiding Simulations in Materials Discovery

In [19], optimal experimental design based on MOCU is applied to a computational problem for shape memory alloy (SMA) design with desired stress-strain profiles for a particular dopant at a given concentration utilizing time-dependent Ginzburg-Landau (TDGL) theory. The TDGL model simulates the free energy for a specific dopant with a specified concentration, given the dopant’s parameters. The assumption is that there is a set of potential dopants and each dopant can be characterized by two parameters, its strength and its range of stress disturbance . The concentration of the dopants can be selected from a set of pre-specified values. The true values of these dopant parameters are unknown; however, there exists a prior distribution over the dopant parameters. In summary, we have and , where and , and and represent the sample spaces of and , respectively. Thus, fully characterizes dopant .

Since the computational complexity of the TDGL model is enormous, the goal is to find an optimal dopant and concentration to minimize the simulated energy dissipation, with the least number of times running the TDGL model (least number of experiments). Following [19], for this purpose, a surrogate model is trained based on fitting some initial data generated from the TDGL model. The surrogate model can approximately predict a dissipation energy for a specified dopant and concentration, and it is used as the cost function throughout the experimental design iterations. The TDGL model acts as the true underlying system, or Nature, and the surrogate model is the model of the true system. The action space is , where each action is using the th dopant with the th possible concentration. The cost function is . The experiment space is , where corresponds to obtaining a noisy measurement of the dissipation energy when using the th dopant with the th concentration. , where is a probability distribution.

IV Dynamical Genetic Networks

In [9], optimal objective-based experimental design is derived for networks with multiple dynamic trajectories, modeling in [9] is based on [20]. Briefly, the network’s nodes and their corresponding values represent entities, proteins/chemicals or genes, and their corresponding concentration levels or expression levels, respectively. The values are assumed to be nonnegative integers. Each edge represents an interaction with its input, regulation, and output nodes. Each interaction can dynamically happen if all of its input and activator nodes are nonzero and its inhibitor nodes are zero. All interactions are known. When the network is in state , it can have one or more possible interactions based on the node values, where if any takes place, the network transitions to a next state. When multiple interactions exist, if knowledge of the relative priorities of these competing interactions exist, we can completely determine the state trajectory of the network from an initial state .

The assumption is that these relative priorities are not known but can be measured one at a time with experimental error. If the network has of these competing interactions, i.e., interactions that can dynamically happen at the same time, then the uncertainty class consists of a set of Boolean random variables, , and , where . The th experiment can determine the value of with an experimental error having probability . Specifically, if is selected to be measured, with probability the outcome of the experiment is , and with probability is . Here, , each experiment corresponds to measuring , and

| (11) |

An action blocks an interaction from happening, so the action space is , where is the number of interactions that can be blocked. Each action changes the dynamic trajectory of the network. If the set of possible state trajectories is denoted by when the th action () is taken, then the probability of each trajectory is

| (12) |

where is the indicator function ( if is true and is 0 otherwise), and is the deterministic trajectory for a fixed initial state and , when action is taken. Here, , where denotes the set of all possible initial states. For each trajectory , the dynamic performance cost is defined as the distance (in terms of any appropriate norm) of the steady-state vector corresponding to that trajectory () from a desired distribution , i.e. . Thus, the cost function for a fixed and action is the expected cost over the possible trajectories, .

The IBR action for this problem is

| (13) |

According to (4) and (5), the optimal experiment can be derived as

| (14) |

where “” denotes set subtraction in the subscripts. The second line holds because only the posterior distribution of depends on experiment ; and the last equality follows from the independence of from . The last line is exactly the policy derived in [9] but there the policy derivation was based on adding the objective-based cost of experimental error to the previous notion of objective cost of uncertainty, whereas here we directly apply the generalized formulation of MOCU as we have formulated in Section II.

V Connection of MOCU-based Experimental Design with KG and EGO

Knowledge Gradient (KG) [5, 6], which is used in different fields, from drug discovery to material design [21, 22], was originally introduced as a solution to an offline ranking and selection problem, where the assumption is that there are actions (alternatives) that can be selected, i.e., . Each action has an unknown true reward (sign-flipped cost) and at each time step an experiment provides a noisy observation of the reward of a selected action. There is a limited budget () of the number of measurements we can make before the time arrives to decide which action is the best, that being the one having the lowest expected cost (or the highest expected reward).

The assumption is that we have Gaussian prior beliefs over the unknown rewards, either independent Gaussian beliefs over the rewards when the rewards of different actions are uncorrelated, or a joint Gaussian belief when the rewards are correlated. In the independent case, for each action-reward pair , . In the correlated case, the vector of rewards, , has a multivariate Gaussian distribution with the mean vector and covariance matrix , with diagonal entries . If the selected action to be applied at is , then the observed noisy reward of at that iteration is , where is unknown and is independent of the reward of .

Here, the underlying system to learn is the unknown reward function and each possible model is fully described by a reward vector in the uncertainty class . For the independent case, . For the correlated case, . The experiment space is , where experiment corresponds to applying and getting a noisy observation of its reward , that is, measuring with observation noise, where . In the independent case the state of knowledge at each time point is captured by the posterior values of the means and variances for the rewards after incorporating observations as , and in the correlated case by the posterior vector of means and a covariance matrix after observing as , where and the diagonal of is the vector . The probability space is equal to and the cost function is .

For this problem, the IBR action at time step is

| (15) |

Again, by (4) and (5), the optimal experiment at time step can be derived:

| (16) |

The derived policy (16) by direct application of the generalized MOCU is exactly the same as the original KG policy in [5], [6], and [23]. As KG is shown to be optimal when the horizon is a single measurement and asymptotically optimal (the number of measurements goes to infinity), the same holds for the MOCU-based policy for this problem.

Efficient Global Optimization (EGO) [7], which is based on expected improvement (EI), is widely used for black-box optimization and experimental design. As shown in [22], KG reduces to EGO when there is no observation noise and choosing the best action at each time step is limited to selecting from the set of actions whose rewards have been previously observed; that is, at each time step if we want to make a final decision as to the best action to be applied, it must be an action whose performance has been previously observed from the first time step up to that time. Thus, MOCU-based learning can also be reduced to EGO under its model assumptions. We will show this directly.

Consider the ranking and selection problem with no noise in the observations, so that for all . Each experiment corresponds to applying and observing the true value of . Moreover, the choice of the best action at each time step is confined to the set of actions whose rewards have been previously observed. Let denote this set: . The IBR action at time is

| (17) |

where the last equality is due to the fact that the reward of an action whose performance is already observed is known, since there is no observation noise. Let denote the set of experiments performed up to the current time , where experiment corresponds to being applied at and its reward being observed, in other words, measurement of at . Since there is no point in measuring an action’s reward more than once, the next experiment is selected from the set of remaining experiments, so that the experiment space at time step is . From (4), (5), and (17), the optimal experiment selected at is

| (18) |

which is exactly the EGO policy in [7].

There are fundamental differences between the general MOCU formulation and KG (or EGO): (1) with MOCU the experiment space and action space can be different, enabling more flexible experimental design compared to the assumption of the same experiment and action space in KG (or EGO); (2) MOCU considers the uncertainty directly on the underlying physical model, which allows direct incorporation of prior knowledge regarding the underlying system, whereas in KG (or EGO) the uncertainty is considered on the reward function and there is no direct connection between prior assumptions and the underlying physical model.

VI A Simulation Study to Compare MOCU-based Experimental Design and KG

In this section, we perform a simulation study to illustrate the flexibility of MOCU-based experimental design compared to KG, especially the importance of the flexibility of dissecting the uncertainty class assumptions to better incorporate prior knowledge regarding the underlying model. Here we compare the experimental design performances by MOCU and KG based on a simulated quadratic function example with one input variable as the underlying reward function that we want to maximize: , i.e. . The observation noise is additive Gaussian with the distribution . In this simulation model, , , and are unknown parameters. We take as the set of actions (possible input values ). The corresponding experiment for each action is to apply so that we can observe the outcome (the reward):

| (19) |

Note that as shown in Section V, under model assumptions of KG, MOCU-based experimental design results in the same policy as KG. But here, as opposed to KG that directly models the rewards (and corresponding costs) of actions with Gaussian distributions with (prior) fixed parameter values (either known or estimated), MOCU-based experimental design computes the generalized MOCU by modeling the uncertainty of the reward function by incorporating the uncertainty over the underlying parameters, to guide the experimental design procedure.

For both MOCU-based experimental design and KG, we assume that there is no prior knowledge on the model parameters . For MOCU, the non-informative prior is used, which updates to a Gaussian-inverse-gamma distribution () when measurements become available when experiments are carried out in sequence. For KG, to model the rewards of actions directly with correlated Gaussian distributions, approximate beliefs are constructed at each experiment since the noise variance is unknown and no joint Gaussian prior distribution exists over the reward values of the actions. For this approximation, following [24] and [22], a Gaussian process regression (GPR) model [25] with a quadratic basis (mean) function and a squared exponential covariance matrix with additive Gaussian observation noise is trained using the measurements performed (experiment outcomes observed) up to that time step (by maximizing the marginal log-likelihood of the observations).

In our simulation, is drawn from ( denotes the uniform distribution over the interval ); is set to , where is drawn from ; is sampled from ; and is set to , where and denotes the true standard deviation of the reward values of actions based on the given model parameters. Each simulation starts with four randomly selected actions, for which noisy observations of their rewards are simulated as initial training data to both MOCU-based experimental design and KG. The sequential experimental design procedures based on MOCU and KG are both continued for five iterations. For KG at each time step , the (posterior) vector of means (), the covariance matrix (), and the noise variance are estimated by training a GPR model on the available measurements, and the next experiment is selected by (16). For MOCU-based experimental design at each time step , the (posterior) Gaussian-inverse-gamma distribution after incorporating the available measurements is used in (6) to optimally select the next experiment.

To compare the performances, we check the average opportunity cost metric, defined as the difference between the true maximum of the reward among all the actions and the true reward of the action selected as the best one based on two experimental design strategies. Note that this best action might be different from the next suggested experiment by each policy. The best action at each time step is the one that would be selected to be applied if the iterative experiments are stopped at that time. In other words, each experimental design policy suggests the next experiment, and after observing the outcome and based on its updated beliefs selects the best action (that would be applied if the iterative experiments were to stop) and the next experiment to be performed (if experimental budget is not exhausted). When following the MOCU-based policy, the next suggested experiment is the minimizer of the expected remaining MOCU, but the best action at each time step is the IBR action that maximizes (minimizes) the expectation of the reward (cost) with respect to the (posterior) Gaussian-inverse-gamma distribution of uncertain parameters based on the latest belief at that time step. When following the KG policy, the best action at each time step is the one that maximizes the (posterior) GPR mean value at that time step which might be different from the suggested next experiment by KG.

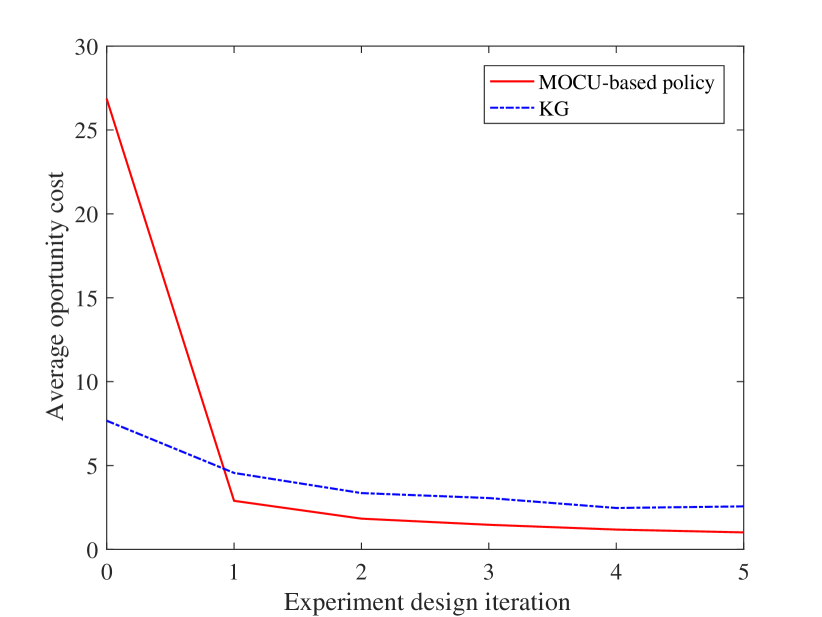

Figure 1 illustrates the average opportunity cost for MOCU-based experimental design and KG over 1,000 simulation runs. As can be seen from the figure, as soon as the experimental design iterations begin MOCU-based policy consistently has the lower average opportunity cost compared to KG. This confirms that directly incorporating the model uncertainty (the uncertainty of model parameters in this simulation study as we assume that we have the model functional form) in the generalized MOCU framework results in a better experimental design policy. Note that at iteration 0 no experiment selection by any of the methods is performed, and only four randomly selected experiment outcomes are available. Since the flat (non-informative) prior is assumed for the parameters in the MOCU-based framework, the IBR action selection as the best action can be very conservative before beginning the experimental design procedure. The maximizer of the direct approximation of the reward function by GPR at iteration 0 is better than the IBR action for this simple simulation model. But as soon as the first experiment is selected by the policies, MOCU-based policy greatly reduces the uncertainty pertaining to the objective very sharply with the observed measurements and performs consistently better than KG.

VII Conclusions

In this letter, we present a generalized MOCU framework, leading to the MOCU-based experimental design pertaining to the maximum uncertainty reduction of differential cost with respect to the actual operational objectives. The proposed framework fits into Lindley’s utility paradigm [4] in classical Bayesian experimental design and is more flexible for the development of corresponding experimental design strategies for different real-world applications compared to the existing KG and EGO methods with their corresponding model assumptions. As we have shown in the simulation study (Section VI) and in the recent applications to life and materials science (Sections III and IV), our generalized MOCU framework, with the benefits from flexible dissection of the uncertainty class, action (operator) space, experiment space, and utility function depending on operational objectives, can lead to better objective-based uncertainty quantification and thereafter better experimental design to converge to desired objectives with smaller operational cost.

Acknowledgments

The authors acknowledge the support of NSF through the projects CAREER: Knowledge-driven Analytics, Model Uncertainty, and Experiment Design, NSF-CCF-1553281; and DMREF: Accelerating the Development of Phase-Transforming Heterogeneous Materials: Application to High Temperature Shape Memory Alloys, NSF-CMMI-1534534.

References

- [1] Byung-Jun Yoon, Xiaoning Qian, and Edward R. Dougherty, “Quantifying the objective cost of uncertainty in complex dynamical systems,” IEEE Transactions on Signal Processing, vol. 61, no. 9, pp. 2256–2266, May 2013.

- [2] Roozbeh Dehghannasiri, Byung-Jun Yoon, and Edward R. Dougherty, “Optimal experimental design for gene regulatory networks in the presence of uncertainty,” IEEE/ACM Trans. Comput. Biol. Bioinformatics, vol. 12, no. 4, pp. 938–950, July 2015.

- [3] Roozbeh Dehghannasiri, Xiaoning Qian, and Edward R. Dougherty, “Optimal experimental design in the context of canonical expansions,” IET Signal Processing, vol. 11, pp. 942–951, October 2017.

- [4] Dennis V. Lindley, Bayesian Statistics, A Review, SIAM, Philadelphia, 1972.

- [5] Peter I. Frazier, Warren B. Powell, and Savas Dayanik, “A knowledge-gradient policy for sequential information collection,” SIAM Journal on Control and Optimization, vol. 47, no. 5, pp. 2410–2439, 2008.

- [6] Peter I. Frazier, Warren B. Powell, and Savas Dayanik, “The knowledge-gradient policy for correlated normal beliefs,” INFORMS Journal on Computing, vol. 21, no. 4, pp. 599–613, 2009.

- [7] Donald R Jones, Matthias Schonlau, and William J Welch, “Efficient global optimization of expensive black-box functions,” Journal of Global optimization, vol. 13, no. 4, pp. 455–492, 1998.

- [8] Mahdi Imani, Roozbeh Dehghannasiri, Ulisses M. Braga-Neto, and Edward R. Dougherty, “MOCU significantly outperforms entropy for experimental design,” Submitted, 2017.

- [9] Daniel N. Mohsenizadeh, Roozbeh Dehghannasiri, and Edward R. Dougherty, “Optimal objective-based experimental design for uncertain dynamical gene networks with experimental error,” IEEE/ACM Transactions on Computational Biology and Bioinformatics, 2017, doi: 10.1109/TCBB.2016.2602873.

- [10] Lori A. Dalton and Edward R. Dougherty, “Optimal classifiers with minimum expected error within a Bayesian framework–part i: Discrete and Gaussian models,” Pattern Recognition, vol. 46, no. 5, pp. 1301–1314, 2013.

- [11] Lori A. Dalton and Edward R. Dougherty, “Intrinsically optimal Bayesian robust filtering,” IEEE Transactions on Signal Processing, vol. 62, no. 3, pp. 657–670, Feb 2014.

- [12] Roozbeh Dehghannasiri, Mohammad S. Esfahani, and Edward R. Dougherty, “Intrinsically Bayesian robust Kalman filter: An innovation process approach,” IEEE Transactions on Signal Processing, vol. 65, no. 10, pp. 2531–2546, May 2017.

- [13] M. Stone, “Application of a measure of information to the design and comparison of regression experiments,” Annals of Mathematical Statistics, vol. 30, pp. 55–70, 1959.

- [14] Morris H. DeGroot, “Uncertainty, information and sequential experiments,” Annals of Mathematical Statistics, vol. 33, no. 2, pp. 404–419, 1962.

- [15] Morris H. DeGroot, Concepts of Information Based on Utility, pp. 265–275, Springer Netherlands, Dordrecht, 1986.

- [16] José M. Bernardo, “Expected information as expected utility,” Annals of Statistics, vol. 7, no. 3, pp. 686–690, 1979.

- [17] Kathryn Chaloner and Isabella Verdinelli, “Bayesian experimental design: A review,” Statistical Science, vol. 10, no. 3, pp. 273–304, 1995.

- [18] Xiaoning Qian and Edward R. Dougherty, “Bayesian regression with network prior: Optimal Bayesian filtering perspective,” IEEE Transactions on Signal Processing, vol. 64, no. 23, pp. 6243–6253, 2016.

- [19] Roozbeh Dehghannasiri, Dezhen Xue, Prasanna V. Balachandran, Mohammadmahdi R. Yousefi, Lori A. Dalton, Turab Lookman, and Edward R. Dougherty, “Optimal experimental design for materials discovery,” Computational Materials Science, vol. 129, no. Supplement C, pp. 311–322, 2017.

- [20] Daniel N. Mohsenizadeh, Jianping Hua, Michael Bittner, and Edward R. Dougherty, “Dynamical modeling of uncertain interaction-based genomic networks,” BMC Bioinformatics, vol. 16, no. 13, pp. S3, Dec 2015.

- [21] Si Chen, Kristofer-Roy G. Reyes, Maneesh K. Gupta, Michael C. McAlpine, and Warren B. Powell, “Optimal learning in experimental design using the knowledge gradient policy with application to characterizing nanoemulsion stability,” SIAM/ASA Journal on Uncertainty Quantification, vol. 3, no. 1, pp. 320–345, 2015.

- [22] Peter I. Frazier and Jialei Wang, “Bayesian optimization for materials design,” Information science for materials discovery and design, vol. 225, pp. 45–57, 2016.

- [23] Yingfei Wang, Kristofer G. Reyes, Keith A. Brown, Chad A. Mirkin, and Warren B. Powell, “Nested-batch-mode learning and stochastic optimization with an application to sequential multistage testing in materials science,” SIAM J. Scientific Computing, vol. 37, 2015.

- [24] Warren Scott, Peter Frazier, and Warren Powell, “The correlated knowledge gradient for simulation optimization of continuous parameters using Gaussian process regression,” SIAM Journal on Optimization, vol. 21, no. 3, pp. 996–1026, 2011.

- [25] Carl E. Rasmussen and Christopher K.I. Williams, Gaussian Processes for Machine Learning, Adaptative computation and machine learning series. University Press Group Limited, 2006.