Nonparametric Pricing Analytics with Customer Covariates

Abstract

Personalized pricing analytics is becoming an essential tool in retailing. Upon observing the personalized information of each arriving customer, the firm needs to set a price accordingly based on the covariates such as income, education background, past purchasing history to extract more revenue. For new entrants of the business, the lack of historical data may severely limit the power and profitability of personalized pricing. We propose a nonparametric pricing policy to simultaneously learn the preference of customers based on the covariates and maximize the expected revenue over a finite horizon. The policy does not depend on any prior assumptions on how the personalized information affects consumers’ preferences (such as linear models). It is adaptively splits the covariate space into smaller bins (hyper-rectangles) and clusters customers based on their covariates and preferences, offering similar prices for customers who belong to the same cluster trading off granularity and accuracy. We show that the algorithm achieves a regret of order , where is the length of the horizon and is the dimension of the covariate. It improves the current regret in the literature (Slivkins, 2014), under mild technical conditions in the pricing context (smoothness and local concavity). We also prove that no policy can achieve a regret less than for a particular instance and thus demonstrate the near optimality of the proposed policy.

Keywords: multi-armed bandit, dynamic pricing, online learning, regret analysis, contextual information

1 Introduction

Personalized pricing refers to the practice that a firm charges customers different prices for the same product, depending on customers’ information such as education backgrounds and zip codes. It is increasingly popular in online retailing, as sellers can acquire/infer the personalized information from customers’ account profiles or browsing histories (cookies). The demand (purchasing probability) of each customer depends not only on the price, but also on the personalized information. The firm observes the information of each arriving customer and sets a personalized price accordingly. We are interested in finding pricing policies of the firm that maximize the long-run revenue.

Personalized pricing presents several challenges to the firm. First, for new entrants to the online business, the demand function and how it depends on the personalized information is generally unknown. Thus, the optimal pricing cannot be obtained by directly solving an optimization problem. The firm may experiment with different prices to learn the personalized demand function, and then sets optimal prices according to the estimation. There is usually a finite horizon that forces a trade-off between gathering more information (learning/exploration) and making sound decisions (earning/exploitation). This problem, sometimes referred to as the learning/earning dilemma, has attracted the attention of many researchers.

A second challenge is the presence of personalized information, or covariates. On one hand, the covariate of each customer provides extra information for the firm to predict the personalized demand more accurately. On the other hand, the demand is peculiar to each instance and changes over time, which adds significant complexity to the learning problem described above. In particular, learning a market-wise demand function is not sufficient, and the firm has to learn the personalized demand by experimenting with prices for customers of similar profiles.

A third challenge is the selection of a predictive model to estimate the demand. Consider a toy example: the demand function only depends on the address of each customer and nothing else. The firm may postulate a linear model

and uses historical sales data to learn the parameters , and and maximize revenue according to the estimation. However, whether the model is specified correctly plays an important role in the performance of the pricing policy. In the particular example, linearity in the location (latitude and longitude) implies that the customers along the straight line that is orthogonal to have the same demand. This hardly reflects the reality, as customers from the same neighborhood tend to have similar shopping patterns and neighborhoods are usually clustered geographically. By postulating a parametric (linear) model, the firm faces the risk of misspecification and not learning what is supposed to be learned. A nonparametric model is more appropriate in this setting.

In this paper we study the pricing policy of a firm which tries to maximize the unknown expected revenue , where is the price, is the personalized demand function for a customer of covariate . We assume both quantities are normalized so and . In period , the firm observes an arriving customer with a random covariate , and sets a personalized price . The earned revenue is multiplied by a Bernoulli random variable with success rate , representing the event of a purchase. The expected revenue is thus .

We propose a nonparametric learning policy for the firm. That is, the policy does not depend on specific forms of and only assumes general structures such as continuity and smoothness. The policy achieves near-optimal performance compared to a clairvoyant who knows and sets for a customer of covariate . More precisely, the expected difference in total revenues between the proposed policy and the clairvoyant policy, which is referred to as the regret in the literature, grows at as . The rate is sublinear in , implying that when the length of horizon tends to infinity, the average regret incurred per period becomes negligible. Moreover, we prove that no pricing policies can achieve a lower regret than for a reasonable class of unknown objective functions . Therefore, we successfully work out the learning/earning dilemma with covariates.

The main contribution of the paper is the design of a near-optimal nonparametric learning policy for the personalized pricing problem. Nonparametric learning policies are introduced in more general settings by Rigollet and Zeevi (2010); Perchet and Rigollet (2013); Slivkins (2014). The formulation in this paper is originally introduced in Slivkins (2014), and our policy builds upon the idea of adaptive binning proposed in Perchet and Rigollet (2013)111Perchet and Rigollet (2013) study discrete decision variables (multi-armed bandit). . Motivated by the application of personalized pricing, we assume that the expected revenue is smooth and locally concave in the charged price . This deviates from the Lipschitz continuous condition in Slivkins (2014) and can be viewed as a special “margin condition” in Rigollet and Zeevi (2010); Perchet and Rigollet (2013). By utilizing this condition, we are able to show that our policy is near-optimal and achieves improved regret over merely continuous objective functions ( versus in Slivkins (2014)).

1.1 Literature Review

This paper is motivated by the recent literature that analyzes a firm’s pricing problem when the demand function is unknown (e.g. Besbes and Zeevi, 2009; Araman and Caldentey, 2009; Farias and Van Roy, 2010; Broder and Rusmevichientong, 2012; den Boer and Zwart, 2014; Keskin and Zeevi, 2014; Cheung et al., 2017). den Boer (2015) provides a comprehensive survey for this area. Since the firm does not know the optimal price, it has to experiment different (suboptimal) prices and update its belief about the underlying demand function. Therefore, the firm has to balance the exploration/exploitation trade-off, which is usually referred to as the learning-and-earning problem in this line of literature. Our paper considers the pricing problem with personalized information and it does not consider the finite-inventory setting as in some of the papers mentioned above.

More recently, several papers investigate the pricing problem with unknown demand in the presence of covariates (Nambiar et al., 2016; Qiang and Bayati, 2016; Javanmard and Nazerzadeh, 2016; Cohen et al., 2016; Ban and Keskin, 2017). The existing literature has adopted a parametric approach: for example, the actual demand can be expressed in a linear form (Qiang and Bayati, 2016; Ban and Keskin, 2017), where is the feature vector of a customer, and are vectorized coefficients, and is the random noise. Because of the parametric form, a key ingredient in the design of the algorithms in this line of literature is to plug in an estimator for the unknown parameters ( and ) in addition to some form of forced exploration. In contrast, we focus on a setting where the demand function cannot be parametrized. Thus, the firm cannot count on accurately estimating the function globally by estimating a few parameters. Instead, a localized optimal decision has to be made based on past covariates generated in the neighborhood. It highlights the different philosophies when designing algorithms for parametric/nonparametric learning problems with covariates. As a result, the best achievable regret deteriorates from or (parametric) to (nonparametric).

The dependence of the optimal rate of regret on the problem dimension has been observed before. For example, Cohen et al. (2016) find a multi-dimensional binary search algorithm for feature-based dynamic pricing, which has regret ; Javanmard and Nazerzadeh (2016) propose a policy for a similar problem that achieves regret , where represents the sparsity of the features; in Ban and Keskin (2017), the near-optimal policy achieves regret . In their parametric frameworks, the dependence of the regret on is rather mild—it does not appear on the exponent of ; Javanmard and Nazerzadeh (2016); Keskin and Zeevi (2014) also provide methods to deal with the sparse strucutre. In contrast, in our nonparametric formulation, the optimal rate of regret increases dramatically in , making the problem significantly harder to learn in high dimensions. This is similar to the nonparametric formulation in the network revenue management problem (Besbes and Zeevi, 2012), in which the dimension of the decision space is and the optimal rate of regret is 222It is shown in Chen and Gallego (2018) that if the number of inventory constraints , then learning the dual variables may effectively reduce the problem dimension.. From the literature, it seems that the dimension significantly complicates the learning problem in a nonparametric formulation.

This paper is also related to the vast literature studying multi-armed bandit problems. See Cesa-Bianchi and Lugosi (2006); Bubeck and Cesa-Bianchi (2012) for a comprehensive survey. The classic multi-armed bandit problem involves finite arms, and the algorithms (Kuleshov and Precup, 2014; Agrawal and Goyal, 2012) cannot be applied directly to our setting. Recently, there is a stream of literature studying the so-called continuum-armed bandit problems (Agrawal, 1995; Kleinberg, 2005; Auer et al., 2007; Kleinberg et al., 2008; Bubeck et al., 2011), in which there are infinite number of arms (decisions). Although there is no contextual information in those papers, Kleinberg et al. (2008); Bubeck et al. (2011) have developed algorithms based on a similar idea to decision trees, because the potential arms form a high-dimensional space.

For multi-armed bandit problems with contextual information, parametric and regression-based algorithms have been proposed in, for example, Goldenshluger and Zeevi (2013); Bastani and Bayati (2015). Our paper is related to the literature studying contextual multi-armed bandit problems in a nonparametric framework Yang et al. (2002); Langford and Zhang (2008); Rigollet and Zeevi (2010); Perchet and Rigollet (2013); Slivkins (2014); Elmachtoub et al. (2017). The analysis builds upon the idea of adaptive binning in Perchet and Rigollet (2013). Our algorithm is designed for continuous decisions. In fact, applying the algorithm in Perchet and Rigollet (2013) designed for discrete decisions to our problem with simple discretization may result in worse-than-optimal regret. In terms of the formulation and the rate of regret, this paper is closely related to Slivkins (2014). Slivkins (2014) investigates a more general model, in which the decision can be a vector, and assumes that is Lipschitz continuous. The optimal rate of regret in this setting has been shown to be in previous works, where and are the dimensions of and , respectively. Slivkins (2014) introduces an adaptive zooming algorithm, and uses the covering dimension of the space in the analysis. The extension accommodates more general spaces of than the Euclidean space. For Euclidean spaces, the algorithm recovers the optimal rate of regret . In our setting, letting and leads to the rate .333Applying our assumptions and following Equation (8) of Slivkins (2014) give , and the regret improves to . Motivated by personalized pricing, we impose additional assumptions on (smoothness and local concavity, see Assumption 3), and improve the optimal rate to as a result. The additional assumption may act as a special margin condition (Tsybakov et al., 2004; Rigollet and Zeevi, 2010; Perchet and Rigollet, 2013) and affects the optimal rate. It is unclear whether the algorithm in Slivkins (2014) could be adapted to accommodate the additional assumptions and achieve the improved rate. The design of our algorithm is based on adaptively partitioning the covariate space into rectangular bins, rather than overlapping balls as in Slivkins (2014).

2 Problem Formulation

Suppose the personalized demand function (purchasing probability) is , where is the observed feature vector, or covariate, summarizing the customer’s personalized information, and is the price set by the firm. Since the purchasing event is a Bernoulli random variable with success rate when the firm sets price for a customer of covariate (henceforth abbreviated to customer ), the expected revenue is thus . If the firm knew , or equivalently, , then it would set . Denote the optimal expected revenue from customer by . We will be primarily dealing with the expected revenue instead of the personalized demand .

Initially, neither nor is known to the firm. In period , a customer arrives with covariate . Upon observing , the firm sets a price . The revenue earned in period is denoted by where is a Bernoulli random variable with mean , independent of everything else. The objective of the firm is to design a pricing policy to maximize the total revenue over the horizon . Note that itself is likely to be random even though the firm is not adopting a randomized policy. This is because the pricing decision made in period may depend on the observed customers, set prices, and earned revenues in the previous periods. That is, . Formally, we refer to as the pricing policy that determines how depends on the past information. We also denote .

2.1 Regret

To measure the performance of a pricing policy, it is standard in the literature to benchmark it against the so-called clairvoyant policy and study the regret. Suppose is known to a clairvoyant firm. The optimal pricing policy is rather straightforward for a clairvoyant: having observed customer , set in period and earn a random revenue with mean .

For the firm, the expected revenue in period cannot exceed that of the clairvoyant: . Thus, we define the regret of a pricing policy to be the revenue gap

In period , the expectation is taken with respect to the distribution of as well as , which itself depends on and . Our goal is to design a policy that achieves small when .

However, because also depends on the unknown function , we require the designed policy to perform well for a family of functions, i.e., we seek for optimal policies in terms of the minimax regret

Although it is usually impossible to find the exact policy that achieves the minimax regret, we focus on proposing a policy whose regret is at least comparable to (of the same order as) the minimax regret asymptotically when .

In this paper, we study functions that cannot be parametrized. It implies that the family is much larger than parametric families: it includes all the functions that satisfy some mild assumptions presented in the next section. In other words, the worst-case scenario can potentially be much worse than a parametric family. As a result, the achievable minimax regret is also higher.

2.2 Assumptions

In this section, we formally provide a set of assumptions that and the stochastic process has to satisfy and their justifications.

Assumption 1.

The covariates are i.i.d. for . Given and , the revenue is independent of everything else.

Both i.i.d. covariates and independent noise structure are standard in the literature.

Assumption 2.

The functions and are Lipschitz continuous given and , i.e., there exists such that and for all and () in the domain.

This assumption is equivalent to . Lipschitz continuity is a common assumption in the learning literature. In personalized pricing, it implies that the expected revenues are close if the firm charges similar prices for two customers with similar covariates. If this assumption fails, then the historical sales data of a certain type of customer is not informative for a new customer with almost identical background and learning is virtually impossible.

To introduce the next assumption, consider any hyper-rectangle , including a singleton . Define for . Clearly is the expected revenue when charging for a customer that is sampled from a subset .

Assumption 3.

We assume that for any ,

-

1.

The function has a unique maximizer . Moreover, there exist uniform constants such that for all , .

-

2.

The maximizer is inside the interval .

-

3.

Let be the diameter of . Then there exists a uniform constant such that .

This assumption is quite different from those in the setting without covariates (Besbes and Zeevi, 2009; Wang et al., 2014; Lei et al., 2017) or the parametric setting (Ban and Keskin, 2017; Qiang and Bayati, 2016). To explain the intuition of , suppose the firm only observes but not the exact value of , and thus cannot apply personalized pricing for customers in . In this case, the learning objective is the expected revenue and the clairvoyant policy that has the knowledge of is to set . This class of learning problems are important subroutines of the algorithm we propose and Assumption 3 guarantees that they can be effectively learned.

For part one of Assumption 3, we have

Proposition 1.

If is continuous for , and twice differentiable in an open interval containing the unique global maximizer with , then part one of Assumption 3 holds.

Therefore, part one states that is smooth and locally concave around the maximum. If is a singleton, then it can be viewed as a weaker version of the concavity assumption in Wang et al. (2014); Lei et al. (2017), i.e., for all in their no-covariate setting. As a result, if is the revenue function of linear or exponential demand, then part one is satisfied automatically.

Part two of Assumption 3 prevents the following scenario: If the optimal price for the aggregate demand of customers , , is far from the optimal personalized pricing , then collecting more information for does not help to improve the pricing decision for any individual customer . Such obstacle may lead to failure to learn and is thus ruled out by the assumption. Similar types of assumptions have been imposed in other applications of revenue management. For example, Proposition 1.16 in Gallego and Topaloglu (2018) provides conditions under which the optimal price of the aggregated market lies in the convex hull formed by the optimal prices of each market segment when discriminatory pricing is allowed.

Part three imposes a continuity condition for the optimal price. It is equivalent to, for example, some form of continuous differentiability of , because solves the implicit function from the first-order condition .

Remark 1.

Assumption 2 is a variant of similar assumptions adopted in the literature. Assumption 3, although appearing nonstandard, is also satisfied by the parametric families studied by previous works. We give a few examples that satisfy Assumption 3.

-

•

Dynamic pricing with linear covariate (Qiang and Bayati, 2016): if , then and .

-

•

Separable function: consider . Then . If are concave functions and are positive, then we may be able to solve the unique maximizer for some continuous function .

-

•

Localized functions: the covariate only plays a role in a subset . See Section 5 for a concrete example.

As we shall see in Sections 4 and 5, the optimal rate of regret under Assumption 3 is , in contrast to without it (taking in Equation (3) of Slivkins 2014). Technically, we suspect that Assumption 3 plays a similar rule to the margin condition in the contextual bandit literature (Tsybakov et al., 2004; Goldenshluger et al., 2009; Rigollet and Zeevi, 2010; Perchet and Rigollet, 2013). However, because of the continuous decision variable studied in this paper, the margin condition cannot be translated in a straightforward way. It remains a future direction to present the assumption in a general form (the degree of smoothness such as the Hölder and Sobolev classes) and study how it affects the optimal rate of regret.

We summarize the information available to the firm. In the beginning of the horizon, the length of the horizon , the dimension and the constants are revealed444In fact, only is needed in the algorithm.. In period , the price can also depend on and .

3 The ABE Algorithm

We next present a set of preliminary concepts related to the bins of the covariate space, and then introduce the proposed pricing policy: the Adaptive Binning and Exploration (ABE) algorithm.

3.1 Preliminary Concepts

Definition 1.

A bin is a hyper-rectangle in the covariate space. More precisely, a bin is of the form

for .

We can split a bin by bisecting it in all the dimensions to obtain child bins of , all of equal size. For a bin with boundaries and for , its children are indexed by and have the form

Denote the set of child bins of by . Conversely, for any , we refer to as the parent bin of , denoted by .

Our algorithm starts with a root bin , which contains all possible customers, and successively splits the bin as more data is collected. Therefore, any bin produced during the process is the offspring of , i.e., for some , where is the th composition of the parent function. Equivalently, is an ancestor of . For such a bin, we define its level to be , denoted by . Conventionally, let .

In the algorithm, we keep a dynamic partition of the covariate space consisting of the offspring of in each period . The partition is mutually exclusive and collectively exhaustive, so for , and . Initially . In the algorithm, we gradually refine the partition; that is, each bin in has an ancestor (or itself) in .

3.2 Intuition

The intuition behind the ABE algorithm is to use a partition of the covariate space to aggregate customers in each period. It tries to find the optimal price for customers in each bin , i.e., defined in Section 2.2. As is refined dynamically, i.e., becomes smaller, such aggregation is almost identical to personalized pricing.

To do that, we keep a set of discrete prices (referred to as the decision set hereafter) for each bin in the partition. The decision set consists of equally spaced grid points of a price interval associated with the bin. When a customer arrives with covariate inside a bin , a price is chosen successively in the decision set and charged for the customer. The realized revenue for this price is recorded. When a large number of customers are observed in , the average revenue for each price in the decision set is close to , which is defined as in Section 2.2. Therefore, the empirically-optimal price in the decision set is close to , with high confidence.

There are two potential pitfalls of this approach. First, the number of prices has an impact on the performance of the policy. If there are too many prices in a decision set, then for a given number of customers observed in the bin, each price is experimented with for a relatively few times. As a result, the confidence interval for the associated average revenue is wide. On the other hand, if there are too few prices, then inevitably the decision set has low resolutions. That is, the optimal price in the set could still be far from the true maximizer because of the discretization error. We have to select a proper size of the decision set to balance this trade-off.

Second, even if the optimal price for the aggregate revenue in the bin is correctly identified, it may not be a strong indicator for for a particular customer . Indeed, averages out all customers , and the optimal price for an individual customer could be very different. This obstacle, however, can be overcome as the size of decreases, as implied by Assumption 3. In particular, part two and three of the assumption guarantee that when is small, is concentrated within a neighborhood of as long as . The cost of using a smaller bin, however, is the less frequency of observing a customer inside it.

To remedy the second pitfall, the algorithm adaptively refines the partition and decreases the size of the bins in as increases. When a bin is large, the aggregate optimal price is not a strong indicator for , . As a result, we only need a rough estimate and split the bin when a relatively small number of customers are observed in . When a bin is small, the optimal price provides a strong indicator for , . Therefore, we gather large sales data from customers to explore the decision set and estimate accurately, before it splits.

A crucial step in the algorithm is to determine what information to inherit when a bin is split into child bins. The ABE algorithm records the empirically-optimal price in the decision set of the parent bin. In the child bins, we use this information and set up their decision sets centered at it. As explained above, when the parent bin (and thus the child bins) is large, its optimal price does not predict those of the child bins well. Therefore, the algorithm sets up conservative decision sets for the child bins, i.e., they have wide intervals. On the other hand, when the parent bin is small, its optimal price provides an accurate indicator for those of the child bins. Thus, the algorithm constructs decision sets with narrow ranges for the child bins around the empirically-optimal price inherited.

3.3 Description of the Algorithm

In this section, we elaborate on the detailed steps of the ABE algorithm, shown in Algorithm 1.

The parameters for the algorithm include

-

1.

, the maximal level of the bins. When a bin is at level , the algorithm no longer splits it and simply applies the median price of its decision set whenever a customer is observed in it.

-

2.

, the length of the interval that contains the decision set of level- bins.

-

3.

, the maximal number of customers observed in a level- bin in the partition. When customers are observed, the bin splits.

-

4.

, the number of prices to explore in the decision set of level- bins. The decision set of bin consists of equally spaced grid points of an interval , to be adaptively specified by the algorithm.

We initialize the partition to include only the root bin in Step 4. Its decision set spans the whole interval with equally spaced grid points. That is, the th price is for . The initial average revenue and the number of customers that are charged the th price are set to .

Suppose the partition is at and a customer is observed (Step 6). The algorithm determines the bin which the customer belongs to. The counter records the number of customers already observed in up to when is in the partition (Step 8). If the level of is (i.e., is not at the maximal level) and the number of customers observed in is not sufficient (Step 9 and Step 10), then the algorithm has assigned a decision set to the bin in previous steps, namely, for . There are prices in the set and they are equally spaced in the interval . They are explored successively as new customers are observed in (explore for the first customer observed in , for the second customer, …, for the th customer, again for the th customer, etc.). Therefore, the algorithm charges price where for the th customer observed in (Step 11). Then, Step 13 updates the average revenue and the number of customers for the th price.

If the level of is and we have observed a sufficient number of customers in (Step 9 and Step 14), then the algorithm splits and replaces it by its child bins in the partition (Step 16). For each child bin, Step 18 to Step 21 initialize the counter, the interval that encloses the decision set, the grid size of the decision set, and the average revenue/number of customers for each price in the decision set, respectively. In particular, to construct the decision set of a child bin, the algorithm first computes the empirically-optimal price in the decision set of the parent bin ; that is, in Step 15. Then, the algorithm creates an interval centered at this empirically-optimal price with width , properly cut off by the boundaries . The decision set is then an equally spaced grid of the above interval (Step 19 and Step 20).

If the level of is already , then the algorithm simply charges the median price (Step 25) repeatedly without further exploration. For such a bin, its size is sufficiently small and the algorithm has narrowed the range of the decision set times. The charged price is close enough to all , , with high probability.

3.4 Choice of Parameters

We set , , , and

To give a sense of their magnitudes, the edge length of the bins at the maximal level is approximately . The range of the decision set () is proportional to the edge length of the bin (). The number of prices in a decision set is approximately . Therefore, the grid size is for a level-. The number of customers to observe in a level- bin is roughly before it splits. When is small, can be zero according to the expression. In this case, the algorithm immediately splits the bin without collecting any sales data in it.

3.5 A Schematic Illustration

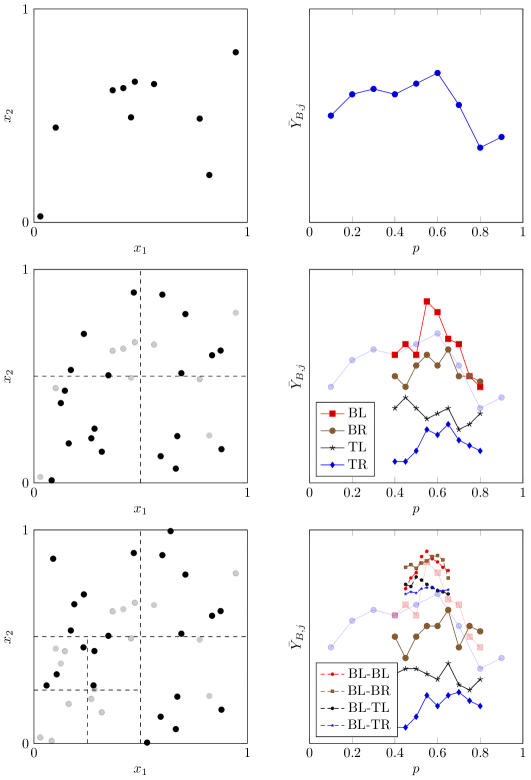

We illustrate the key steps of the algorithm by an example with . Figure 1 illustrates a possible outcome of the algorithm in periods (top panel, mid panel, and bottom panel respectively). Up until period , there is a single bin and the covariates of observed customers for are illustrated in the top left panel. In this case, the decision set associated with the root bin is , illustrated by the top right panel. The average revenue of each price is recorded, and is the empirically-optimal price. At , a sufficient number of customers are observed and Step 14 is triggered in the algorithm. Therefore, the bin is split into four child bins.

From period to , new customers are observed in each child bin (mid left panel). Note that the customers observed before in the parent bin are no longer used and colored in gray. For each child bin (the bottom-left bin is abbreviated to BL, etc.), the average revenues for the prices in the decision sets is demonstrated in the mid right panel. The decision sets are centered at the empirically-optimal price of their parent bin, which is from the top right panel. They have narrower ranges and finer grids than that of the parent bin. At , a sufficient number of customers are observed in BL, and it is split into four child bins.

From period to , the partition consists of seven bins, as shown in the bottom left panel. The BR, TL and TR bins keep observing customers and updating the average revenues, because they have not collected sufficient data. Their status at is shown in the bottom panels. In the four newly created child bins of BL (the bottom-left bin of BL is abbreviated to BL-BL, etc.), the prices in the decision sets are used successively and their average revenues are illustrated in the bottom right panel.

4 Regret Analysis: Upper Bound

To measure the performance of the ABE algorithm, we provide an upper bound for its regret.

Theorem 1.

We provide a sketch of the proof here and present the details in the appendix. In period , if for a bin in the partition , then the expected regret incurred by the ABE algorithm is . Since the total regret simply sums up the above quantity over and all possible s, it suffices to focus on the regret for given and . Two possible scenarios can arise: (1) the optimal price of the aggregate demand in , i.e., , is inside the range of the decision set, i.e., (Step 19); (2) the optimal price is outside the range of the decision set.

Scenario one represents the regime where the algorithm is working “normally”: up until , the algorithm has successfully narrowed the optimal price (which provides a useful indicator for all , when is small) down to . By Assumption 3 part one, the regret in this scenario can be decomposed into two terms

The first term can be bounded by the length of the interval . The second term can be bounded by the size of given by Assumption 3 part two and three. By the choice of parameters in Section 3.4, the length of the interval decreases as the bin size decreases. Therefore, both terms can be well controlled when the size of is sufficiently small, or equivalently, when the level is sufficiently large. This is why a properly chosen can guarantee that the algorithm spends little time for large bins and collect a large amount of data for small bins. When the bin level reaches , the above two terms are small enough and no more exploration is needed.

Scenario two represents the regime where the algorithm works “abnormally”. In scenario two, the difference can no longer be controlled as in scenario one because and can be far apart. To make things worse, usually implies , where is a child of . This is because (1) is close to for small , and (2) is created around the empirically-optimal price for , and thus overlapping with . Therefore, for any period following , the worst-case regret is in that period if or its offspring.

To bound the regret in scenario two, we have to bound the probability, which requires delicate analysis of the events. If scenario two occurs for , then during the process that we sequentially split to obtain , we can find an ancestor bin of (which can be itself) that scenario two happens for the first time along the “branch” from all the way down to . More precisely, denoting the ancestor bin by and its parent by , we have (1) is inside (scenario one); (2) after is split, is outside (scenario two). Denote the empirically-optimal price in the decision set of by . For such an event to occur, the center of the decision set of , which is , has to be at least away from .555Recall that . Because of Assumption 3 and the choice of , the distance between and is relatively small compared to . Therefore, the empirically-optimal price must be far away from . The probability of such event can be bounded using classic concentration inequalities for sub-Gaussian random variables: the prices that are closer to and thus have higher means turn out to generate lower average revenue than ; this event is extremely unlikely to happen when we have collected a large amount of sales data for each price in the decision set.

The total regret aggregates those in scenario one and two for all possible combinations of and . It matches the quantity presented in the theorem.

5 Regret Analysis: Lower Bound

In this section, we show that the minimax regret is no lower than for some constant . Combining with the last section, we conclude that no non-anticipating policy does better than the ABE algorithm in terms of the order of magnitude of the regret in (neglecting logarithmic terms).

We first construct a family of functions that satisfy Assumption 2 and 3. The functions in the family are selected to be “difficult” to distinguish. By doing so, we will prove that any policy has to spend a substantial amount of time exploring prices that generate low revenues but help to differentiate the functions. Otherwise, the incapability to correctly identify the underlying function is costly in the long run. Therefore, unable to contain both sources of regret at the same time, no policy can achieve lower regret than the quantity stated in Theorem 2.

Before introducing the family of functions, we define to be the boundary of a convex set in . Let be the Euclidean distance between two sets and . That is . We allow or to be a singleton. To define , we partition the covariate space into equally sized bins. That is, each bin has the following form: for ,

We number those bins by in an arbitrary order, i.e., . Each function is indexed by a tuple , whose th index determines the behavior of in . More precisely, for , the personalized demand function is

and thus

The optimal personalized price for customer is if and if .

The construction of follows a similar idea to Rigollet and Zeevi (2010). For a given , we can always find another function that only differs from in a single bin by setting to be equal to except for the th index. The firm can only rely on the covariates generated in to distinguish between and . For small bins (i.e., large ), this is particularly costly because there are only a tiny fraction of customers observed in a particular bin and the difference becomes tenuous. It also requires to be far from to detect the difference, which happens to be the optimal price when . This makes the exploration/exploitation trade-off hard to balance. Now a policy has to carry out the task for bins, i.e., distinguishing the underlying function with tuples that only differ from in one index. The cost is inevitable and adds to the lower bound of the regret. Moreover, we assume the customers are uniformly distributed in .

In the appendix, we show that the constructed satisfies all the assumptions. The main theorem below shows the lower bound for the regret.

Theorem 2.

For the constructed , any non-anticipating policy has regret

for a constant .

6 Future Research

As shown in Theorem 1 and Theorem 2, the best achievable regret of the problem is of order . As a result, the knowledge of the sparsity structure of the covariate is essential in designing pricing policies. More precisely, the provided customer covariate is of dimension , while the personalized demand may only depend on entries of the covariate where . In this case, being able to identify the entries out of significantly decreases the incurred regret from to . Indeed, in the ABE algorithm, if the sparsity structure is known, then a bin is split into instead of child bins. It pools the observations that only differ in the dimensions corresponding to the redundant covariates so that more observations are available in a bin, and thus substantially reduces the exploration cost. An important research question is then whether it is possible to design a binning algorithm that selects one dimension and the position to split, based on a certain criterion, like regression/classification decision trees (Hastie et al., 2001). This may significantly improve the regret in the presence of sparse covariates.

References

- Agrawal (1995) Agrawal, R. (1995). The continuum-armed bandit problem. SIAM journal on control and optimization 33(6), 1926–1951.

- Agrawal and Goyal (2012) Agrawal, S. and N. Goyal (2012). Analysis of thompson sampling for the multi-armed bandit problem. In Conference on Learning Theory, pp. 39–1.

- Araman and Caldentey (2009) Araman, V. F. and R. Caldentey (2009). Dynamic pricing for nonperishable products with demand learning. Operations research 57(5), 1169–1188.

- Auer et al. (2007) Auer, P., R. Ortner, and C. Szepesvári (2007). Improved Rates for the Stochastic Continuum-Armed Bandit Problem, pp. 454–468. Berlin, Heidelberg: Springer Berlin Heidelberg.

- Ban and Keskin (2017) Ban, G. and N. B. Keskin (2017). Personalized dynamic pricing with machine learning. Working paper.

- Bastani and Bayati (2015) Bastani, H. and M. Bayati (2015). Online decision-making with high-dimensional covariates. Working paper.

- Besbes and Zeevi (2009) Besbes, O. and A. Zeevi (2009). Dynamic pricing without knowing the demand function: Risk bounds and near-optimal algorithms. Operations Research 57(6), 1407–1420.

- Besbes and Zeevi (2012) Besbes, O. and A. Zeevi (2012). Blind network revenue management. Operations research 60(6), 1537–1550.

- Broder and Rusmevichientong (2012) Broder, J. and P. Rusmevichientong (2012). Dynamic pricing under a general parametric choice model. Operations Research 60(4), 965–980.

- Bubeck and Cesa-Bianchi (2012) Bubeck, S. and N. Cesa-Bianchi (2012). Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Foundations and Trends® in Machine Learning 5(1), 1–122.

- Bubeck et al. (2011) Bubeck, S., R. Munos, G. Stoltz, and C. Szepesvári (2011). X-armed bandits. Journal of Machine Learning Research 12(May), 1655–1695.

- Cesa-Bianchi and Lugosi (2006) Cesa-Bianchi, N. and G. Lugosi (2006). Prediction, learning, and games. Cambridge university press.

- Chen and Gallego (2018) Chen, N. and G. Gallego (2018). A primal-dual learning algorithm for personalized dynamic pricing with an inventory constraint. Working paper.

- Cheung et al. (2017) Cheung, W. C., D. Simchi-Levi, and H. Wang (2017). Dynamic pricing and demand learning with limited price experimentation. Operations Research 65(6), 1722–1731.

- Cohen et al. (2016) Cohen, M. C., I. Lobel, and R. Paes Leme (2016). Feature-based dynamic pricing. Working paper.

- den Boer (2015) den Boer, A. V. (2015). Dynamic pricing and learning: historical origins, current research, and new directions. Surveys in operations research and management science 20(1), 1–18.

- den Boer and Zwart (2014) den Boer, A. V. and B. Zwart (2014). Simultaneously learning and optimizing using controlled variance pricing. Management Science 60(3), 770–783.

- Elmachtoub et al. (2017) Elmachtoub, A. N., R. McNellis, S. Oh, and M. Petrik (2017). A practical method for solving contextual bandit problems using decision trees. Working paper.

- Farias and Van Roy (2010) Farias, V. F. and B. Van Roy (2010). Dynamic pricing with a prior on market response. Operations Research 58(1), 16–29.

- Foucart and Rauhut (2013) Foucart, S. and H. Rauhut (2013). A mathematical introduction to compressive sensing, Volume 1. Birkhäuser Basel.

- Gallego and Topaloglu (2018) Gallego, G. and H. Topaloglu (2018). Revenue management and pricing analytics. In preparation.

- Goldenshluger and Zeevi (2013) Goldenshluger, A. and A. Zeevi (2013). A linear response bandit problem. Stochastic Systems 3(1), 230–261.

- Goldenshluger et al. (2009) Goldenshluger, A., A. Zeevi, et al. (2009). Woodroofe’s one-armed bandit problem revisited. The Annals of Applied Probability 19(4), 1603–1633.

- Hastie et al. (2001) Hastie, T., R. Tibshirani, and J. Friedman (2001). The Elements of Statistical Learning. Springer Series in Statistics. New York, NY, USA: Springer New York Inc.

- Javanmard and Nazerzadeh (2016) Javanmard, A. and H. Nazerzadeh (2016). Dynamic pricing in high-dimensions. Working paper.

- Keskin and Zeevi (2014) Keskin, N. B. and A. Zeevi (2014). Dynamic pricing with an unknown demand model: Asymptotically optimal semi-myopic policies. Operations Research 62(5), 1142–1167.

- Kleinberg et al. (2008) Kleinberg, R., A. Slivkins, and E. Upfal (2008). Multi-armed bandits in metric spaces. In Proceedings of the fortieth annual ACM symposium on Theory of computing, pp. 681–690. ACM.

- Kleinberg (2005) Kleinberg, R. D. (2005). Nearly tight bounds for the continuum-armed bandit problem. In Advances in Neural Information Processing Systems, pp. 697–704.

- Kuleshov and Precup (2014) Kuleshov, V. and D. Precup (2014). Algorithms for multi-armed bandit problems. Working paper.

- Langford and Zhang (2008) Langford, J. and T. Zhang (2008). The epoch-greedy algorithm for multi-armed bandits with side information. In Advances in neural information processing systems, pp. 817–824.

- Lei et al. (2017) Lei, Y., S. Jasin, and A. Sinha (2017). Near-optimal bisection search for nonparametric dynamic pricing with inventory constraint. Working paper.

- Nambiar et al. (2016) Nambiar, M., D. Simchi-Levi, and H. Wang (2016). Dynamic learning and price optimization with endogeneity effect. Working paper.

- Perchet and Rigollet (2013) Perchet, V. and P. Rigollet (2013). The multi-armed bandit problem with covariates. The Annals of Statistics 41(2), 693–721.

- Qiang and Bayati (2016) Qiang, S. and M. Bayati (2016). Dynamic pricing with demand covariates. Working paper.

- Rigollet and Zeevi (2010) Rigollet, P. and A. Zeevi (2010). Nonparametric bandits with covariates. In A. T. Kalai and M. Mohri (Eds.), COLT, pp. 54–66. Omnipress.

- Slivkins (2014) Slivkins, A. (2014). Contextual bandits with similarity information. The Journal of Machine Learning Research 15(1), 2533–2568.

- Tsybakov (2009) Tsybakov, A. B. (2009). Introduction to Nonparametric Estimation (1 ed.). Springer-Verlag New York.

- Tsybakov et al. (2004) Tsybakov, A. B. et al. (2004). Optimal aggregation of classifiers in statistical learning. The Annals of Statistics 32(1), 135–166.

- Wang et al. (2014) Wang, Z., S. Deng, and Y. Ye (2014). Close the gaps: A learning-while-doing algorithm for single-product revenue management problems. Operations Research 62(2), 318–331.

- Yang et al. (2002) Yang, Y., D. Zhu, et al. (2002). Randomized allocation with nonparametric estimation for a multi-armed bandit problem with covariates. The Annals of Statistics 30(1), 100–121.

Online Appendix for Nonparametric Pricing Analytics with Customer Covariates

Appendix A Table of Notations

| The smallest integer that does not exceed | |

| The positive part of | |

| The cardinality of a set | |

| The -algebra generated by | |

| The distribution of the covariate over | |

| The empirically-optimal decision in the decision set for | |

| The boundary of |

Appendix B Proofs

Proof of Proposition 1:.

Define for

By L’Hopital’s rule, is continuous at . In addition, because is continuous, is continuous for all . By Weierstrass’s extreme value theorem, we have and both and are attained. By the definition and the uniqueness of the maximizer, for . Therefore, we must have . This establishes the result. ∎

B.1 Upper Bound in Section 4

We first introduce the following lemmas.

Lemma 1.

A Bernoulli random variable satisfies

This lemma follows directly from the Hoeffding’s lemma. It implies that a Bernoulli random variable is sub-Gaussian.

Lemma 2.

Suppose for given and , the random variable is sub-Gaussian with parameter , i.e.,

for all . Then the distribution of conditional on for a set is still sub-Gaussian with the same parameter.

Proof.

Let denote the distribution of . We have that for all

where the last inequality is by the definition of conditional expectations. Hence the result is proved. ∎

Proof of Theorem 1:.

According to the algorithm (Step 7), let denote the partition formed by the bins at time when is generated. The regret associated with can be counted by bins into which falls. Meanwhile, the level of is at most . Therefore,

We will define the following random event for each bin :

Recall that is the unique maximizer for by Assumption 3; is the range of the decision set to explore for . According to Step 19 of the ABE algorithm, the interval is constructed around , the empirically-optimal price of the parent bin that maximizes the empirical average .

We will decompose the regret depending on whether occurs.

| (1) |

We first analyze term 1. Because is always true ( always encloses according to Step 4), we can find an ancestor of , say (which can be itself), such that occurs. In other words, up until , the algorithm always correctly encloses the optimal price of the ancestor bin of in the intervals . Therefore, when occurs, we can rearrange the event by such . Term 1 in (1) can be bounded by

| (2) |

The first inequality is due to Assumption 2. In the second inequality, we start enumerating from instead of because never occurs. In the last equality, we rearrange the probabilities by counting the deterministic bins instead of the random bins .

Now note that are exclusive for different s because is a partition and can only fall into one bin. Moreover, because . Therefore,

Thus, we can further simplify (2):

| (3) |

The last equality is because of the fact that for given and , the event and . Therefore, the two events are independent.

Next we analyze the event given in order to bound (3). This event implies that when the parent bin is created, its optimal price is inside the interval . At the end of Step 14, when customers have been observed in , it is split into children. The optimal price of its child bin , that is , is no longer inside . By Step 19, and , where is the empirically-optimal price for . Therefore, implies that . Combined with Assumption 3 part two, which states that , we have

That is, either or . By Assumption 3 part three, because the level of is . Hence by Assumption 3 part two, and . Combining the above observations, could only happen when . On the other hand, implies that . Therefore, could occur only if there exist two grid points in Step 14 for bin , such that

-

1.

The th grid point is the closest to the optimal price for the bin . That is, .

-

2.

The th grid point maximizes . That is . It implies that in Step 15.

-

3.

.

In other words, the empirically-optimal price is the th grid point, while the th grid point is closest to the true revenue maximizer in bin , i.e., . Given that the two grid points are far apart (by point 3 above), the probability of this event should be small.

To further bound the probability, consider . In Step 15, it is the sum of or independent random variables with mean . By Lemmas 1 and 2, they are still sub-Gaussian with parameter . This gives the following probabilistic bound (recall the definition of in Section 2.2):

Here and can be either or ; and are independent mean-zero sub-Gaussian random variables with parameter . Their averages are the centered version of and , and thus their means are moved to the right-hand side. In the last inequality, represents the positive part. The inequality follows from Assumption 3 part one and the previously derived facts that and . By the property of sub-Gaussian random variables (for example, see Theorem 7.27 in Foucart and Rauhut, 2013), the above probability is bounded by

By our choice of parameters, , , . Therefore, when , we have:

Therefore, there exists a constant such that

With this bound, we can proceed to provide an upper bound for (3). Because , we have

| (4) |

We next analyze term 2 of (1). By Assumption 3 part one, . By the design of the algorithm (Step 12 and 25), ; conditional on the event , we have for . On the other hand, by Assumption 3 part two and three, for . Therefore, term 2 can be bounded by

| (5) | |||

For the first term in (5), note that occurs for at most times for given with . Moreover, there are bins with level , i.e., . Therefore, substituting into the first term yields an upper bound . For the second term in (5), because form a partition of the covariate space and always falls into one of the bins. Therefore, (5) is bounded by

| (6) |

for and .

Combining (4) and (6), we can find constants such that

| (7) |

We choose

to minimize in (7). More precisely,

for some constants , and

for a constant . Therefore, (7) implies that we can find a constant such that

Therefore, by our choice of , the regret is bounded by

for some constant . Hence we have completed the proof. ∎

B.2 Lower Bound in Section 5

Next we show that Assumption 1 and 2 are satisfied by the construction in Section 5.

To give some intuitions, note that by the construction of , both and are Lipschitz continuous in . Such continuity guarantees the desired properties.

Proof of Proposition 2:.

For Assumption 2, we discuss two cases. The first case is , i.e., the two customers are in the same bin. In this case,

When , the assumption is already satisfied. When , by the triangle inequality we have

The second inequality is because and when . The third inequality is because

and similarly . Therefore, we have shown that for case one.

The second case is and for . If , then by the previous analysis, we already have . If and , then

The last inequality is because the straight line connecting and must intersects . The distance from to the intersection is no less than . Therefore, . If and , then the result follows similarly. If , then by the same argument,

Therefore, combining both cases, we always have

For Assumption 3, note that

For part one, because the second-order derivative of is always bounded between ,

and part one holds for , . For part two, note that the maximizer

Because is a monotone function of , it is easy to check that part two of Assumption 3 holds. For part three, consider and . If and , then . If either or , then

by the previous analysis. If and , then similarly we have . Therefore, part three holds with . ∎

The proof of Theorem 2 uses Kullback-Leibler (KL) divergence to measure the “distinguishability” of the underlying functions. Such information-theoretic approach has been a standard technique in the learning literature. The proof is outlined in the following.

Among all functions , we focus on each pair of and that only differ in a single bin. For example, consider and for some . Because the indices of and are identical except for the th, and only differ in bin . Denote and to highlight this fact. Distinguishing between and poses a challenge to any policy. In particular, for , the difference of the two functions is diminishing when in . Thus, charging a price different from makes the difference more visible and helps to distinguish and . However, if deviates too much from the optimal decision or , then significant regret is incurred in that period.

To capture this trade-off, for a given and , define the following quantity

| (8) |

where the expectation is taken with respect to a policy and the underlying function . This quantity is crucial in analyzing the regret. More precisely, if is large (which implies that is large), then and are easy to distinguish but the regret becomes uncontrollable.

Lemma 3.

On the other hand, if is small, then the KL divergence of the measures associated with and is also small. In other words, the firm cannot easily distinguish between and which impedes learning and incurs substantial regret.

Lemma 4.

Since the effects of are opposite in Lemma 3 and Lemma 4, combining the two bounds, we can find a positive constant independent of and so that

In the second inequality above, we minimize the expression over positive . Since can be an arbitrary positive integer, we let in the last quantity. Calculation shows that it is lower bounded by for a constant .

Lemma 5 (KL divergence for Bernoulli Random Variables).

For two Bernoulli random variables and with means and , we have

Proof.

The proof can be found in, e.g., Rigollet and Zeevi (2010) and thus omitted. ∎

Lemma 6 (The chain rule of the KL divergence).

Given joint distributions and , we have

where and represent the marginal distribution, and represent the conditional distribution.

Proof.

The proof can be found from standard textbooks and is thus omitted. ∎

Proof of Lemma 3:.

We use to highlight the dependence of the expectation on the policy and the underlying function . Note that

In the last inequality, we have used the fact that and the supremum is always no less than the average.

For a given bin , we focus on and , which only differ for . Therefore, we can rearrange to . We have the following lower bound for the regret

In the second inequality, we have neglected the regret for . The last equality is by the definition of in (8). Hence we have proved the result. ∎

Proof of Lemma 4:.

By the same argument as in the proof of Lemma 3, we have

Because is uniformly distributed in , . By conditioning on the event , we have

Since is measurable with respect to the -algebra generated by and , by the tower property, we have

Let denote and let denote the conditional probability . By Markov’s inequality, for any constant we have

| (9) | |||

| (10) | |||

where we define event . In the second equality, we have used the fact that for , when , ; when , . The motivation of introducing is as follows: consider the classification rule associated with tries to distinguish between and . It is defined as

In other words, classifies the underlying function as if is closer to the optimal price of , and as vice versa. For , a misclassification on the event is . It implies that

which on , implies as . Similarly, . Therefore, by the fact that , we have

| (11) |

Next we lower bound the misclassification error (11) by the Kullback-Leibler (KL) divergence between the two probability measures associated with and . Intuitively, if the two probability measures are close, then no classification (including ) can incur very small misclassification error. Formally, introduce the KL divergence between two probability measures and as

where indicates that is absolute continuous w.r.t. . By the independence of and , the two measures we want to distinguish in (11), and , can be expressed as product measures

where is a measure of depending on and and is a measure of conditional on . By Theorem 2.2 (iii) in Tsybakov (2009),

| (12) |

The second line follows from Lemma 6; the third line follows from the fact that is the same distribution for and , independent of .

To further simplify the expression, note that can be decomposed as

where is the measure (uniform distribution) of and is the measure of conditional on and . We apply Lemma 6 again:

It is easy to see that the second term is zero. For the third term, we first conditional on and then on the covariate . Because depends only on and , is the same for and conditional on and . Therefore, and are two Bernoulli distributions with means and , respectively. By Lemma 5, we have

In the second inequality, we used the fact that as long as we choose and thus . In the last inequality, we have used the fact that the distance of a vector inside to the boundary of is at most . Therefore, we can obtain an upper bound for

Therefore, combining it with (9), (11) and (12), we have shown the lemma:

where in the last step, we have set . ∎