Portfolio Optimization with Delay Factor Models

Abstract

We propose an optimal portfolio problem in the incomplete market where the underlying assets depend on economic factors with delayed effects, such models can describe the short term forecasting and the interaction with time lag among different financial markets. The delay phenomenon can be recognized as the integral type and the pointwise type. The optimal strategy is identified through maximizing the power utility. Due to the delay leading to the non-Markovian structure, the conventional Hamilton-Jacobi-Bellman (HJB) approach is no longer applicable. By using the stochastic maximum principle, we argue that the optimal strategy can be characterized by the solutions of a decoupled quadratic forward-backward stochastic differential equations(QFBSDEs). The optimality is verified via the super-martingale argument. The existence and uniqueness of the solution to the QFBSDEs are established. In addition, if the market is complete, we also provide a martingale based method to solve our portfolio optimization problem, and investigate its connection with the proposed FBSDE approach. Finally, two particular cases are analyzed where the corresponding FBSDEs can be solved explicitly.

Keywords: Portfolio optimization; Delay factor models; FBSDEs; Martingale method.

1 Introduction

Owing to globalization and transparency, financial markets cannot be treated as a local system. The interaction between markets and markets among different areas is observed. Hence, in order to catch this characteristic, we take the factor model into account where the coefficients of the underlying financial assets depend on another stochastic processes denoted as factors. These factors can be described as the information or influence coming from external financial markets. The optimal portfolio problems based on the factor models are widely discussed. If the factor processes affect the underlying assets only through their current status values, i.e., the effect is Markovian, the dynamic programming can be applied to derive the corresponding Hamilton Jacobi Bellman (HJB) equations, and the candidates of Markov or feedback optimal strategies can be obtained through the first order condition. The optimality of the strategy can be guaranteed by the verification theorem. See Bauerle and Rieder (2004); Berdjane and Pergamenshchikov (2013); Castañeda-Leyva and Herñandez-Herñandez (2005); Delong and Kluppelberg (2008); Fleming and Herñandez-Herñandez (2003); Fleming and Pang (2004); Fleming and Sheu (1999, 2002); Fouque and Hu (2017); Hata and Sheu (2012a, b); Hayashi and Sekine (2011); Liu (2007); Nagai (1996, 2003, 2014) for thorough discussion.

In real financial markets, the significant dependence from historical information is available according to the discussion in Lo et al. (2007); Hsu and Kuan (2005); Lorenzoni et al. (2007); Dokuchaev (2012), which can be used for the short term forecasting. The influence of factors usually does not arise immediately but has time delay feature, see Dokuchaev (2015). The stochastic control problems with delay are extremely important in applications and have been extensively studied in various settings. An optimal solution satisfying Pontryagin-Bismut-Benssoussan type stochastic maximum principle for delay in state variables is introduced by Øksendal and Sulem (2001); Øksendal et al. (2011). In addition, Larssen (2002); Larssen and Risebro (2003) reduce the system with state delay to a finite dimensional problem by using dynamics programming principle. The general stochastic control problems with both the state delay and the control delay are discussed in Gozzi and Marinelli (2006); Gozzi et al. (2009); Gozzi and Masiero (2015) for the abstract space and the corresponding HJB approach. In addition, Chen and Wu (2011), Chen et al. (2012) and Xu (2013) studied above general optimization problem with delay using the forward and advanced backward stochastic differential equations (FABSDEs) approach. In particular, the linear quadratic stochastic game with delay for finite players is studied in Carmona et al. (2016). Bensoussan et al. (2015) consider the linear quadratic mean field Stackelberg game with delay.

In this article, we propose a portfolio optimization problem in the incomplete market by taking into account the factor models with delay. In particular, the coefficients of the underlying risky assets involve both pointwise time delay factors and integral time delay factors. The optimal strategy for the portfolio optimization problem is identified by maximizing the expected power utility. Since the delay feature leads to the non-Markovian structure, the dynamic programming principle and HJB approaches cannot be applied any more. We utilize the stochastic maximum principle and forward and backward differential equations (FBSDEs) to characterize the optimal solution. A verification theorem is provided by applying the positive super-martingale property. See Theorem 3.1 and Theorem 3.2. See also Hu et al. (2005). The existence and uniqueness of the corresponding FBSDEs driven by the optimal strategy are included. Due to the complexity of the coupled FBSDEs, the explicit solutions cannot be obtained in general. However, we propose two particular cases where the explicit solutions can be obtained, and discuss the corresponding financial implications. Furthermore, if the market is complete, we also provide a martingale based approach to solve our optimization problem, and investigate its connection with the proposed FBSDE approach. We make a precise statement of the relation in Theorem 4.1. See also a related discussion in Horst et al. (2014). To our best knowledge, it is the first work to systematically study the portfolio optimization problem with delayed factor models.

The reminder of this paper is organized as follows. In Section 2, the basic framework and notations are introduced. In Section 3, we provide the solution for our proposed optimal portfolio problem in the incomplete market. Section 4 illustrates the comparion of the solution between the FBSDE approach and the martingale in a complete market with delay. Two particular cases which have explicit solutions are studied in Section 5. The conclusion and discussion are provided in Section 6. The technical proof is given in the appendices.

2 Delay Factor Model

Let be a filtered complete probability space, where a dimensional Wiener process is defined. Let and be two finite positive integers smaller or equal to , and

are deterministic measurable functions satisfying the following conditions:

-

•

(A1) , , , , and are globally Lipschitz and twice differentiable; furthermore, we assume their first and second order derivatives are bounded and continuous;

-

•

(A2) is nonnegative and bounded;

-

•

(A3) is bounded, where denote be the transpose operation;

-

•

(A4) is globally Lipschitz and differentiable.

The price of the risk free asset and the risky stocks are modelled by the following stochastic differential equations:

where is the component of , is the element of . The -valued and -adapted process is called the factor process which describes the information from external markets, and is the exponentially weighted average delay factor (Hayashi and Sekine, 2011; Chang et al., 2011) defined by

| (1) |

and is the pointwise delay factor

| (2) |

and , are fixed positive constants. The differential form of can be written as

For simplicity, we shall use following notations in the rest of discussions

The financial market consists of one bound with interest rate and stocks. In the case of , we face an incomplete market.

For a given portfolio and under the self-financing condition, the dynamics of the wealth process can be written as

| (3) |

where denotes the -dimensional column vector whose components are all of 1. Note that is the proportion of the wealth to hold the -th risky asset for , and is the proportion of holding the risky free asset. The portfolio is an admissible portfolio if it is progressively measurable and

The goal of this article is to find the optimal portfolio to maximize the expected power utility

| (4) |

where with .

3 Main Results

Since the wealth process (3) involves the delay factor, the conventional HJB approach is no longer applicable. We apply the stochastic maximum principle described in Bismut (1978) (see also Peng (1993) and Horst et al. (2014)) to solve the optimization problem (4). Following the idea in Horst et al. (2014), by applying Itô formula to , we get

| (5) | |||||

The Hamiltonian is given by

| (6) |

which is a strictly concave function of . Here we omit the dependence of on . Recall that are functions of . Therefore, the optimal portfolio satisfies the first order condition:

which leads to the candidate of the optimal strategy

| (7) |

where is the dual processes given by

In (7), we implicitly assume for all . Substituting (7) into (5) and using the notation

| (8) |

we obtain the following forward backward stochastic differential equations (FBSDEs):

| (9) | |||||

| (10) | |||||

with boundary conditions and . We want to show that FBSDEs (9-10) has a unique solution, which is denoted by a triple processes .

It should be noticed that FBSDEs (9-10) is a decoupled system in the sense that the coefficients of the backward equation (10) do not involve the forward process . Besides, for a given , the coefficients of the forward equation (9) are globally Lipschitz in , then it follows from the standard SDE theory that (9) admits a unique solution provided the backward stochastic differential equation (BSDE) (10) is uniquely solvable. Therefore, in order to establish the unique existence of solution to FBSDEs (9-10), it is sufficient to show BSDE (10) has a unique solution.

We introduce the new variables , and where we implicitly assume for all . The corresponding new FBSDEs satisfied by becomes

| (11) | |||||

| (12) | |||||

with the boundary condition where is the identity matrix. Note that the backward dynamics is quadratic in .

The following spaces are needed to study the solution of quadratic FBSDEs (11-12):

Here, is the collection of stopping times taking values in ,

and for a probability measure on , the bounded mean oscillation (BMO) norm with respect to is defined by

where is the quadratic variation of the -martingale from to and the essential supremeum is taken over all possible stopping times . Our first result states that the quadratic FBSDEs (11-12) admits a unique solution.

Theorem 3.1.

Proof.

We apply the method developed in Tevzadze (2008) (see also Touzi (2012)) to prove the unique existence of solution . The technical proof is given in Appendix A.

We next prove that is a martingale. An application of Itô formula to yields:

which implies is a local martingale. Besides, in light of the fact and the established results and , we can obtain that

Therefore, we can conclude that is a martingale.

∎

The second main result of this paper is the following verification theorem that ensures defined by (13) is the optimal strategy for our proposed portfolio problem (4).

Theorem 3.2.

Proof.

Equations (11-12) has solution implies the equations (9-10) has solution , where . Since is a martingale, then . Define . We can show by Ito’s formula,

and after simplifying the equation, we have

Here is given by (13).

For an arbitrary strategy , by applying Itô formula to , we can obtain that

| (16) | |||||

By using for , is a nonnegative supermartingale. We can conclude

Since and

we have

which implies the optimality of . ∎

Note that the optimal portfolio strategy can be written as

| (17) |

where the first term is proportional to the Sharpe ratio which is independent to the wealth and equal to the solution of the original Merton problem, the second term is by solving the BSDE (12).

4 Complete Market Analysis

In Section 3, we developed the solution for the optimization problem (4) by using the FBSDE approach. It should be noticed that our general result holds without requiring the market to be complete. In this section, we develop another different martingale approach to solve the primal problem (4) under the complete market assumption. This result provides a comprehensive investigation of the connection between FBSDE and martingale approaches similar to the discussion in Horst et al. (2014).

If the market is complete, that exists, then (9-10) become

| (18) |

and

| (19) |

On the other hand, the optimal strategy for our portfolio problem (3) and (4) can be obtained through the martingale method, which is an application of the duality technique and the martingale representation theorem. Referring to Chapter 3 in Karatzas and Shreve (1998), we review the martingale method in Appendix B. Based on with , the optimal portfolio is given by

| (20) |

where is a martingale defined by

| (21) |

with

and

| (22) |

and is the unique solution such that

Therefore, by setting , we can obtain

| (23) |

and

Moreover, is a square integrable process comes from the martingale representation theorem:

| (24) |

We now investigate the relation between the BSDE and the martingale . In addition, we guarantee

with

being the solution for (10) by verifying the terminal condition .

Theorem 4.1.

Proof.

We only need to prove (27). By (19), we have

Here we use (25). Then

After simplification, we have

| (28) | |||||

Here we use

which can be uniquely solved to obtain an expression of ,

From (21), we have

| (29) |

Therefore, putting (28) and (29) together, we finally obtain

which gives if we take . This completes the proof.

∎

5 Two Particular Cases

This section is devoted to analyzing two particular cases where the quadratic FBSDEs (11-12) and the corresponding optimal strategies (13) can be obtained explicitly.

5.1 Infinite Delay Time

In this case, we consider in (1), i.e.

and there is no pointwise delay factor in the dynamics and . For simplicity, we assume treated as the complete market. Note that given the dimension of the factor such that is a -dimensional process, the case of incomplete markets () is also solvable using the same argument. Hence, is a 1-dimensional Brownian motion, and

and

| . |

The differential form for the equation can be written as

We have the following results for the solution of BSDE and the optimal strategy .

Proposition 5.1.

The solution for the BSDE is given by

| (30) |

where

with the corresponding dynamics

The optimal strategy for the optimization problem with the infinite delay time is given by

| (32) |

Proof.

We make an ansatz written as

| (33) |

Applying Itô formula to , we get

| (34) | |||||

We then compare the BSDE (12) written as

| (35) | |||||

to identify

| (36) |

We also obtain the equation for written as

| (37) |

with the terminal condition . Let . Hence, (37) can be rewritten as

| (38) |

with the terminal condition . Using (38) and Ito’s formula, we have the corresponding dynamics given by

where and satisfy

The candidate of the solution for is written as

Using the proposed regularity conditions (A1-A4) and applying Theorem 2.9.10 in Krylov (1980), we obtain is first order continuous differentiable with respect to , second order continuous differentiable with respect to and first order continuous differentiable with respect to . Moreover,

| (39) |

is a martingale to guarantee that (LABEL:eta-infinite) is the solution for . The optimal strategy is given by defined in (32). ∎

Financial Implications

Based on (32), we observe that the first term is proportional to the Sharpe ratio and the second term is driven by the ratio of and . Hence, in the case of , the investment for risky assets increases in the factor volatility . For example, in the domestic stock market, if we treat the factors as foreign stocks, the larger volatility of foreign stocks implies the optimal proportion of the wealth in risky assets becomes larger.

We now study one particular case of the infinite delay time, assuming being a constant and

| (40) |

with the parameter constraint . We make an ansatz for written as

where for are deterministic functions driven by satisfying

| (41) | |||||

| (42) | |||||

| (43) | |||||

| (44) |

with the terminal conditions for by identifying the coefficients of , , , and the zero order term. The existence and uniqueness of the coupled ordinary differential equations can be verified based on the condition . The corresponding first order derivative with respect to is given by

the corresponding optimal strategy is given by written as

| (45) |

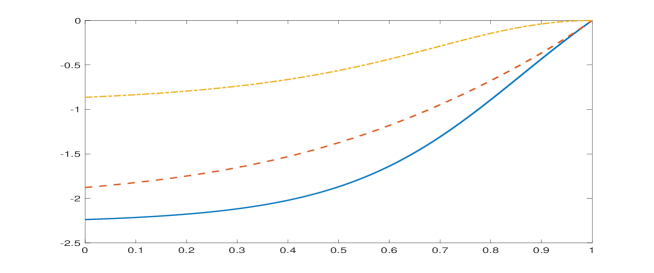

In the case of and , and stay in negative for . See Figure 1 for instance. Therefore, in the case of and , investors intend to invest risky assets rather than risk-free assets based on the larger proportion of the wealth to hold risky assets since for leading to

However, given and , the proportion of the wealth to hold risky assets becomes smaller owing to implying

5.2 Pointwise Delay

Based on Chang et al. (2011) and Pang and Hussain (2015), we assume , being a constant, and

| (46) |

and and for satisfy

| (47) |

The optimal strategy is obtained as follows.

Proposition 5.2.

Given the assumption (46), the solution for the is given by

| (48) | |||||

| (49) | |||||

The optimal strategy for the optimization problem is given by

| (50) |

Proof.

Based on the assumption (46), assuming independent of , the ansatz for is given by

Hence, applying Itô formula to , we get

| (51) | |||||

Identifying (51) and (12) implies

| (52) |

and satisfies

with the terminal condition . Consequently,

with the terminal condition . We obtain the solution for given by

| (53) |

where and are deterministic functions of satisfying

| (54) |

with the terminal condition and leading to the solutions given by

We then obtain the solution for (48-49). Here we use the condition (47). This leads to the optimal portfolio given by in (50). The last result follows from (13) and the expression (50).

∎

Financial Implications

Given the optimal strategy of the pointwise delay written as (50), the proportion for the risky assets grows linearly in the factor volatility if depending only on and being the coefficient of the pointwise delay term. Namely, assuming , when the terminal time is large enough given by , the investors prefer risky assets in the case of the factor volatility becoming larger. Obviously, implies for all . In this case, the proportion of investment in risky assets increases in the factor volatility .

6 Conclusions

In this paper, we consider the portfolio optimization problem with the delay factor model based on the power utility. Due to the non-Markovian feature, we apply the stochastic maximum principle and the FBSDE approach to characterize the optimal strategy and prove the existence and uniqueness for the corresponding FBSDEs. We further propose a different approach using martingale method to solve the optimization problem in the complete market, and investigate its connection with the FBSDE approach. In addition, two explicitly solvable cases are also discussed. The proposed problem in this paper can be extended toward many directions including the general utility and insurance analysis.

From the financial point of view, it would be of great interest to study the portfolio optimization problem through maximizing the exponential utility or the general utility where the assets are driven by the delay factor model. In addition, the one player optimization problem can be extended to the multiple players optimization problem with game feature using the relative performance proposed by Espinosa and Touzi (2015). From the mathematical point of view, under (non)-Markovian structure, the discussion of the existence and uniqueness of the corresponding coupled quadratic FBSDEs is also needed. In the Markovian cases, the solvability of HJB equations is also worth to study. We will pursue to address these problems in the future work.

Appendix A Proof of Theorem 3.1

The quadratic FBSDE is

Define the following notations

Then we can write the dynamics of as follows

| (A.3) |

Denote

Consider the probability measure

where

| (A.4) |

is the Dolans-Dade exponential martingale and

is a -Brownnian motion. Then (A.3) is equivalent to

| (A.7) |

where

and

Showing the system (A.3) has a unique solution is equivalent to showing (A.7) has a unique solution. Note that (A.7) is equivalent to the following system:

| (A.11) |

where

and

We prove that (A.11) has a unique solution for bounded terminal condition .

A.1 Local Solution

The first result states that when is small, the system (A.11) has a unique solution.

Proposition A.1.

Let . Suppose , there exists a unique solution for the system (A.11) with the norm .

Proof.

Consider the mapping by the relation

| (A.14) |

Using the Ito’s formula for we can obtain that

Let be a stopping time taking valued in . Taking conditional expectation on both sides of above equation, where denotes the conditional expectation the probability measure and filtration , and using the inequality , we can obtain that

In the rest of the proof of this Proposition, we use the notation

for a -martingale . Note that

The essential supremum is taken over , the collection of stopping times taking values in . We obtain that

Recall the definition

therefore, we can obtain that

We can pick such that

if and only if . For instance,

| (A.15) |

satisfies this quadratic inequality. Therefore the ball

is such that .

A.2 Global Solution

We next show that (A.11) has a unique solution for any bounded . For any , it can be represented as sum

with and is a finite integer. Consider the following iterated system, where :

| (A.19) |

From Proposistion A.1 we have known the existence of provided . Next we show that if , the solution for the following QBSDE exists:

| (A.22) |

Proposition A.2.

Suppose , there exists a unique solution for the system (A.22).

Proof.

Note that

Then (A.22) becomes

| (A.25) |

Using the Girsanov’s theorem and Property 3 of BMO in Section 11.1.2 of Touzi (2012), we can define the probability by

where is defined in (A.4), and the Brownian motion

so that (A.25) becomes

| (A.28) |

which has the same form as (A.11). Using the same argument as that in Proposition A.1, we can show that under the condition , the system (A.28) has a unique solution in the space .

∎

A.3 Global Uniqueness

Lemma A.1.

Let . Assume that is a solution such that is bounded. That is, . Then is in .

Proof.

Let be a solution of (A.3), and there be a constant such that

Denote as a stopping time such that . Let be a fixed real number (to be chosen later). Applying the Ito’s lemma for and using the boundary condition , we have

If is square integrable martingale, taking conditional expectation in above inequality, we obtain

which implies that

Taking

we can have

for any stopping time . Since , then we can obtain that

Finally, we can conclude that the solution to (A.3) belongs to and .

∎

Theorem A.1.

There exists unique solution of (A.3) such that and .

Proof.

Suppose that and are two solutions to (A.3). Let

and

We have

Let

for where and are the component of and . Let

Thus

Then we have

From Lemma 4.1,

then by Property 3 of BMO in Section 11.1.2 of Touzi (2012) and Girsanov Theorem, we define a new probability

where is defined in (A.4). Then we obtain that is a -martingale, which yields

∎

Appendix B Martingale Method

In the case of complete markets, we consider the portfolio optimization problem written as

where is denoted as the utility function. Namely, is increasing, concave, and . The above problem can be rewritten as

with

with the notation

where given by the budget constraint. Hence, we have

| (B.1) |

The equation (B.1) attains its maximum at

where is denoted as the inverse of . We further assume the following condition

for all . Using being strictly decreasing in with and , there exists a unique such that . We now define

where is a filtration with probability measure and by using the martingale representation

| (B.2) |

In addition, applying Itô formula to gives

| (B.3) |

and is chosen such that . By identifying (B.2) and (B.3), we obtain

References

- Bauerle and Rieder (2004) N. Bauerle and U. Rieder. Portfolio optimization with markov-modulated stock prices and interest rates. IEEE Transactions on Automatic Control, 49:442–447, 2004.

- Bender and Zhang (2008) C. Bender and J. Zhang. Time discretization and markovian iteration for coupled FBSDEs. Annals of Applied Probability, 18(1):143–177, 2008.

- Bensoussan et al. (2015) A. Bensoussan, M. H. M. Chau, and S. C. P. Yam. Mean field stackelberg games: Aggregation of delayed instructions. SIAM Journal on Control and Optimization, 53(4):2237–2266, 2015.

- Berdjane and Pergamenshchikov (2013) B. Berdjane and S. Pergamenshchikov. Optimal consumption and investment for markets with random coefficients. Finance and Stochastics, 17:419–446, 2013.

- Bismut (1978) Jean-Michel Bismut. An introductory approach to duality in optimal stochastic control. SIAM review, 20(1):62–78, 1978.

- Carmona et al. (2016) R. Carmona, J.-P. Fouque, M. Mousafa, and L.-H. Sun. Systemic risk and stochastic games with delay. arXiv:1607.06373, 2016.

- Castañeda-Leyva and Herñandez-Herñandez (2005) N. Castañeda-Leyva and D. Herñandez-Herñandez. Optimal consumption-investment problems in incomplete markets with stochastic coefficients. SIAM Journal on Control and Optimization, 44(4):1322–1344, 2005.

- Chang et al. (2011) M.-H. Chang, T. Pang, and Y. Yang. A stochastic portfolio optimization model with bounded memory. Mathematics of Operations Research, 36(4):604–619, 2011.

- Chen and Wu (2011) L. Chen and Z. Wu. The quadratic problem for stochastic linear control systems with delay. Proceedings of the 30th Chinese Control Conference, Yantai, China, 2011.

- Chen et al. (2012) L. Chen, Z. Wu, and Z. Yu. Delayed stochastic linear-quadratic control problem and related applications. Journal of Applied Mathematics, 2012.

- Delong and Kluppelberg (2008) L. Delong and C. Kluppelberg. Optimal investment and consumption in a black-scholes market with levy-driven stochastic coeffcients. Annals of Applied Probability, 18:879–908, 2008.

- Dokuchaev (2012) N. Dokuchaev. On detecting the dependence of time series. Communications in Statistics-Theory and Methods, 41(5):934–942, 2012.

- Dokuchaev (2015) N. Dokuchaev. Modeling possibility of short term forecasting of market parameters for portfolio selection. Ann. Economics and Finance, 16:143–161, 2015.

- Espinosa and Touzi (2015) G.-E. Espinosa and N. Touzi. Optimal investment under relative performance concerns. Mathematical Finance, 25(2):221–257, 2015.

- Fleming and Herñandez-Herñandez (2003) W.H. Fleming and D. Herñandez-Herñandez. A consumption model with stochastic volatility. Finance and Stochastics, 7:245–262, 2003.

- Fleming and Pang (2004) W.H. Fleming and T. Pang. An application of stochastic control theory to financial economics. SIAM Journal on Control and Optimization, 43:502–531, 2004.

- Fleming and Sheu (1999) W.H. Fleming and S.J. Sheu. Optimal long term growth rate of expected utility of wealth. Annals of Applied Probability, 9(3):871–903, 1999.

- Fleming and Sheu (2002) W.H. Fleming and S.J. Sheu. Risk -sensitive control and an optimal investment model II. Annals of Applied Probability, 12(2):730–767, 2002.

- Fouque and Hu (2017) J.-P. Fouque and R. Hu. Asymptotic optimal strategy for portfolio optimization in a slowly varying stochastic environment. SIAM Journal on Control and Optimization, 55(3):1990–2023, 2017.

- Gozzi and Marinelli (2006) F. Gozzi and C. Marinelli. Stochastic control of delay equations arising in advertising models-vii. lect. notes pure appl. math. Stochastic Partial Differerential Equations and Applications, 245:133–148, Oct 2006.

- Gozzi and Masiero (2015) F. Gozzi and F. Masiero. Stochastic optimal control with delay in the control: solution through partial smoothing. Preprint, 2015.

- Gozzi et al. (2009) F. Gozzi, C. Marinelli, and S. Savin. On control linear diffusions with delay in a model of optimal advertising under uncertainty with memory effects. Journal of Optimization Theory and Applications, 142(2):291–321, 3 2009.

- Hata and Sheu (2012a) H. Hata and S.J. Sheu. On the Hamilton-Jacobi-Bellman equation for an optimal consumption problem: I Existence of solution. SIAM Journal on Control and Optimization, 50:2373–2400, 2012a.

- Hata and Sheu (2012b) H. Hata and S.J. Sheu. On the Hamilton-Jacobi-Bellman equation for an optimal consumption problem: II Verification Theorem. SIAM Journal on Control and Optimization, 50:2401–2430, 2012b.

- Hayashi and Sekine (2011) T. Hayashi and J. Sekine. Risk-sensitive portfolio optimization with two-factor having a memory effect. Asia-Pacific Financial Markets, 18:385–403, 2011.

- Horst et al. (2014) U. Horst, Y. Hu, P. Imkeller, A. Réveillac, and J. Zhang. Forward-backward systems for expected utility maximization. Stochastic Processes and their Applications, 124(5):1813–1848, 2014.

- Hsu and Kuan (2005) P.-H. Hsu and C.-M. Kuan. Reexaming the profitability of technical analysis with data snooping checks. Journal of Financial Econometrics, 3(4):606–628, 2005.

- Hu et al. (2005) Y. Hu, P. Imkeller, and M. Müller. Utility maximization in incomplete markets. Annals of Applied Probability, 15(3):1691–1712, 2005.

- Karatzas and Shreve (1998) I. Karatzas and S. Shreve. Methods of Mathematical Finance. Springer-Verlag New York, 1998.

- Krylov (1980) N.Y. Krylov. Controlled Diffusion Processes. Springer-Verlag New York, 1980.

- Larssen (2002) B. Larssen. Dynamic programming in stochastic control of systems with delay. Stochastics and Stochastics Reports, 74(3-4):651–673, 2002.

- Larssen and Risebro (2003) B. Larssen and N.H. Risebro. When are HJB-equations for control problems with stochastic delay equations finite-dimensional? Stochastic Analysis and Applications, 21(3):643–671, 2003.

- Liu (2007) J. Liu. Portfolio selection in stochastic environments. Review of Financial Studies, 20:1–39, 2007.

- Lo et al. (2007) A. W. Lo, H. Mamaysky, and J. Wang. Foundation of technical analysis: computational algorithms, statistical inference, and empirical implementation. Journal of Finance, 55(4):1705–1765, 2007.

- Lorenzoni et al. (2007) G. Lorenzoni, A. Pizzinga, R. Atherino, C. Fernandes, and R. R. Freire. On the statistical validation of technical analysis. Revista Brasileira de Finaças, 5(1):1–28, 2007.

- Nagai (1996) H. Nagai. Bellman equation of risk-sensitive control. SIAM Journal on Control and Optimization, 37:74–101, 1996.

- Nagai (2003) H. Nagai. Optimal strategies for risk-sensitive portfolio optimization problems for general factor models. SIAM Journal on Control and Optimization, 41:1779–1800, 2003.

- Nagai (2014) H. Nagai. H-J-B equations of optimal consumption-investment and verification theorems. to appear in Applied Mathematics and Optimization, 2014.

- Øksendal and Sulem (2001) B. Øksendal and A. Sulem. Maximum principle for optimal control of stochastic systems with delay with applications to finance. Optimal Control and PDE, Essays in Honour of Alain Bensoussan, pages 64–79, 2001.

- Øksendal et al. (2011) B. Øksendal, A. Sulem, and T. Zhang. Optimal control of stochastic delay equations and time-advanced backward stochastic differential equations. Stochastic Methods and Models, 2011.

- Pang and Hussain (2015) T. Pang and A. Hussain. An application of functional Itô’s formula to stochastic portfolio optimization with bounded memory. 2015 Proceedings of the Conference on Control and its Applications, 2015.

- Peng (1993) Shige Peng. Backward stochastic differential equations and applications to optimal control. Applied Mathematics and Optimization, 27(2):125–144, 1993.

- Tevzadze (2008) Revaz Tevzadze. Solvability of backward stochastic differential equations with quadratic growth. Stochastic processes and their Applications, 118(3):503–515, 2008.

- Touzi (2012) Nizar Touzi. Optimal stochastic control, stochastic target problems, and backward SDE, volume 29. Springer Science & Business Media, 2012.

- Xu (2013) X. Xu. Fully coupled forward-backward stochastic functional differential equations and applications to quadratic optimal control. arXiv:1310.6846, 2013.