Pricing European option with the short rate under Subdiffusive fractional Brownian motion regime

Foad Shokrollahi

Department of Mathematics and Statistics, University of Vaasa, P.O. Box 700, FIN-65101 Vaasa, FINLAND

foad.shokrollahi@uva.fi

(Date: March 15, 2024)

Abstract.

The purpose of this paper is to analyze the problem of option pricing when the short rate follows subdiffusive fractional Merton model. We incorporate the stochastic nature of the short rate in our option valuation model and derive explicit formula for call and put option and discuss the corresponding fractional Black-Scholes equation. We present some properties of this pricing model for the cases of and . Moreover, the numerical simulations illustrate that our model is flexible and easy to implement.

Nowadays, the Black–Scholes model [1] is still classical and most popular model of the market. However, empirical research shows that

it cannot capture many of the characteristic features of prices, such as: long-range correlations, heavy-tailed and skewed

marginal distributions, lack of scale invariance, periods of constant values, etc. Therefore, improvements of the model

itself did not stand still either. Since fractional Brownian motion has two important

properties called self-similarity and long-range dependence, it has the ability to capture the typical tail behavior of stock prices or indexes [15, 14, 2, 13]. The model is an improvement of the model, by replacing the with the Brownian motion in the

standard model. That is

(1.1)

here are constants, and is a with Hurst parameter .

Subdiffusive Brownian motion is an another generalization of the model, which is introduced by Magdziarz [9]. In order to describe properly financial data exhibiting periods of constant

values, he put forward the subdiffusive strategy based on the geometric Brownian motion

to describe financial data with the periods of the constant prices. He

replaced the physical time with inverse -stable subordinator in the standard model

where . Magdziarz showed that the considered model is arbitrage-free but incomplete, and obtained the corresponding

subdiffusive formula for the fair prices of European options. Moreover, Hui Gua et al. [4] applied subdiffusive regime

(1.2)

as the model of asset prices exhibiting subdiffusive dynamics. Here the parent process is the defined in Equation (1.1),

is the inverse -stable subordinator with . Later, many scholars made some improvements of this model [4, 16, 6].

Constant short rate during the life of the option is the assumption at all above studies. This assumption is clearly at odds with reality because, as a matter of fact, the

short rate is evolving random of time. Hence, in this study, we combine the stochastic nature

into our option pricing model. Specifically, we will consider the option pricing of the European options under the Merton short rate model [12] in a subdiffusive regime. That is, in which follows

(1.3)

and the stock price in which follows

(1.4)

where are constant, and are two with Hurst parameter and correlation coefficient . is the inverse -stable subordinator with defined as follows

(1.5)

is a -stable Levy process with nonnegative increments and Laplace transform: .

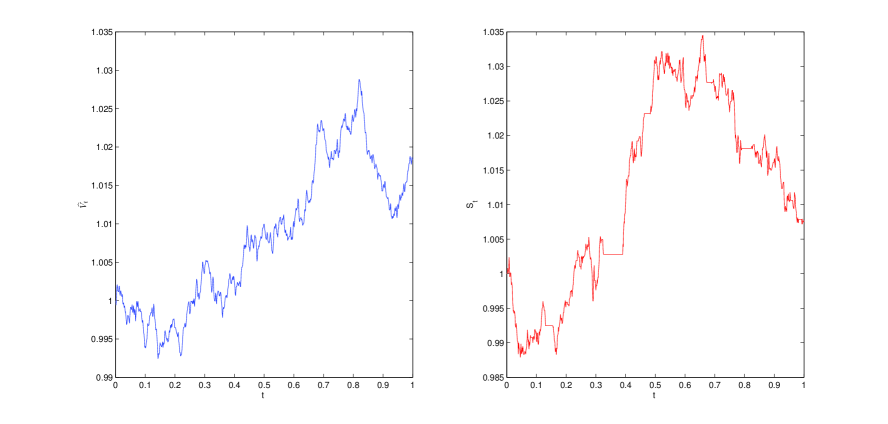

Fig. 2 shows typically the differences and relationships between the sample paths of the stock price in the model and the subdiffusive model.

Figure 1. Comparison of the sample paths of the stock price in the model (left) and the subdiffusive model (right) for .

Here, assume that is independent of and . Specially, when , it is a subdiffusion process mentioned in Refs. [10, 11] and when , reduces to physical time . In this study, we apply the subdiffusive mechanism of trapping events in order to describe financial data exhibiting periods of constant values.

This paper is organized as follows. In Section 2, we derive the formula for the price of a riskless zero-coupon

bond paying $1 at maturity. In Section 3, we obtain the corresponding equation by using delta hedging argument and discuss some special cases of this equation. In Section 4, we present an

analytic pricing formula for the European call and put options. In Section 5, we study some special properties of this pricing formula. Furthermore, we show how to use our model to price options by numerical simulations. The comparison of our model and traditional models is undertaken in

this section. Finally, Section 6 draws the concluding remarks.

2. Pricing formula for zero-coupon bond

The purpose of this section is to derive the pricing formula for zero-coupon bond . Here, , that is, the zero-coupon bond will pay

for 1 dollar at the expiry date .

We assume that the short rate satisfy Equation (1.3), and , then by applying the Taylor series expansion to we obtain that

The purpose of this section is to derive the fractional equation for European options when the short rate and stock price satisfy Equations (1.3) and (1.4), respectively. We assume that and are two with Hurst parameter and correlation coefficient .

Let be the price of a European call option at time t with a strike price that matures at time . Then we

have.

Theorem 3.1.

Assume that the stock price short rate and satisfy Equations (1.3) and (1.4), respectively. Then, satisfies the following fractional equation

(3.1)

where

(3.2)

(3.3)

are constant, and and .

Proof:

We consider a portfolio with units of stock and units of zero-coupon bond and one unit of . Then,

the value of the portfolio at current time is

Further, if , , and be a constant, from Equation (3.12) we have the celebrated equation

(3.13)

4. Pricing formula under subdiffusive fractional Merton short rate model

In this section, we propose an explicit formula for European call option when its value satisfy the partial differential equation (3.1) with boundary condition . Then, we can get

Theorem 4.1.

Let satisfies Equation (1.3) and satisfies Equation (1.4), then the price of European call and put options with strike price and maturity are given by

(4.1)

(4.2)

where

(4.3)

(4.4)

(4.5)

is given by Equation (2.16) and is the cumulative normal distribution function.

Proof:

Consider the partial differential equation (3.1) of the European call option with boundary condition

Suppose that the short rate satisfies Equation (1.3) and the stock price satisfies Equation (1.4), then the price of European call and put options with strike price and maturity are given by

Suppose that the short rate satisfies Equation (1.3) and the stock price satisfies Equation (1.4), then the price of European call and put options with strike price and maturity are given by

(4.28)

(4.29)

where

(4.30)

(4.31)

(4.32)

(4.33)

Specially, If , from Equations (4.28)-(4.33), we have

Let us first discuss about the implied volatility of the subdiffusive model, then we will show some simulation findings.

Corollary 5.1.

If , the value of European call option and put option can be written as

(5.1)

(5.2)

where

(5.3)

(5.4)

(5.5)

(5.7)

and is the cumulative normal distribution function.

Now, for an illustration of the differences among these models: the

Merton , subdiffusive Merton and our fractional Merton and subdiffusive fractional Merton models, we report the theoretical prices of some

hypothetical options using different methods. The prices computed by different models are presented in

Table 1, where denotes the stock price, denotes

the prices computed by the Merton model, denotes the price simulated

by the subdiffusive Merton model, shows the price obtained by the model and denotes the price computed according to model.

Table 1. Results by different pricing models. Here, .

S

2

0.0174

0.0334

0.0012

0.0036

1.8826

1.9129

1.7986

1.8347

2.25

0.0638

0.0979

0.0122

0.0236

2.1326

2.1629

2.0486

2.0847

2.5

0.1598

0.2126

0.0587

0.0859

2.3826

2.4129

2.2986

2.3347

2.75

0.3094

0.3754

0.1687

0.2094

2.6326

2.6629

2.5486

2.5847

3

0.5023

0.5752

0.3440

0.3900

2.8826

2.1929

2.7986

2.8347

3.25

0.7235

0.7988

0.5630

0.6086

3.1326

3.1629

3.0486

3.0847

3.5

0.9604

1.0360

0.8026

0.8466

3.3826

3.4129

3.2986

3.3347

3.75

1.2094

1.2801

1.0498

1.0926

3.6326

3.6629

3.5486

3.5847

4

1.4527

1.5275

1.2991

1.3414

3.8826

3.9129

3.7986

3.8347

By comparing columns , , and in Table 1, we have the conclusion that the call option prices

obtained by four valuation models are close to each other in the both in-the-money and out-of-the-money cases with low and high maturities. Meanwhile, we

can see that the prices given by the our and models are smaller than the

prices given by the Merton and subdiffusive Merton models [3, 5].

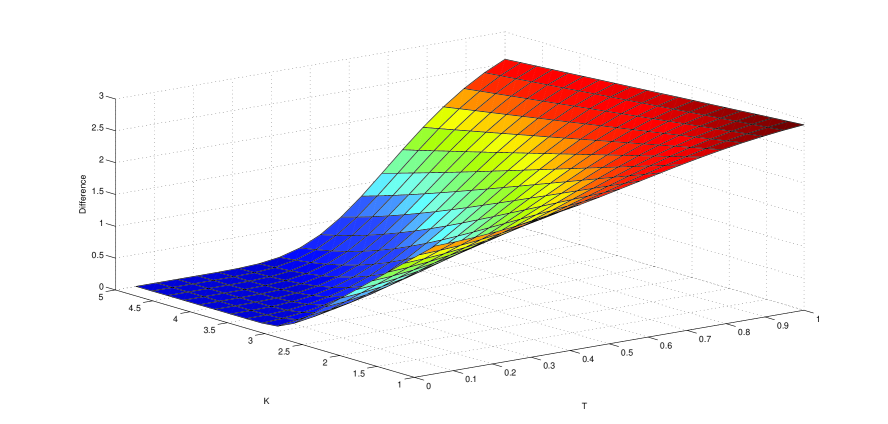

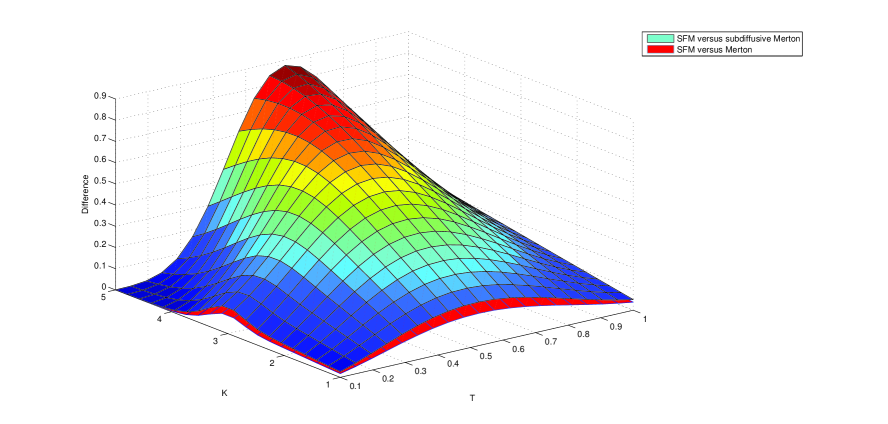

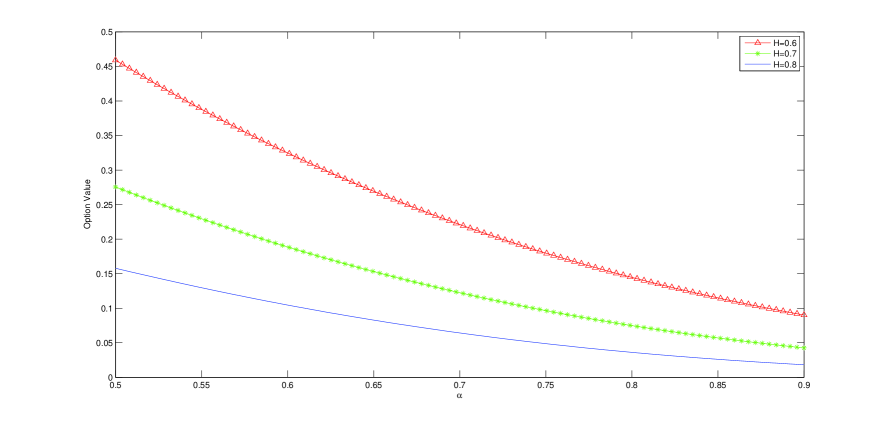

Figure 2. The European call option under . Where .Figure 3. The difference between the price of the European call option under , subdiffusive Merton and Merton models. Where .Figure 4. The European call option under . Where .

We give three figures of the prices of European call options in the model for different parameters (see Figs. 2, 3 and

4). From Equations (5.1)-(5.7), it is easy to see that is just the implied volatility of the classical model.

6. Conclusion

Previous option pricing research typically assumes that the risk-free rate or the short rate is constant during the life of the option. Since

fractional Brownian motion is a well-developed mathematical model

of strongly correlated stochastic processes, in this paper, we incorporate the fractional version of the Merton model with the subdiffusive mechanism to get better subdiffusive characteristic of financial markets. Then, we obtain pricing formula for call and put options when the short rate follows the subdiffusive fractional Merton model short rate and present some simulation results.

References

[1]F. Black and M. Scholes, The pricing of options and corporate

liabilities, Journal of political economy, 81 (1973), pp. 637–654.

[2]P. Cheridito, Arbitrage in fractional brownian motion models,

Finance and Stochastics, 7 (2003), pp. 533–553.

[3]Z. Cui and D. Mcleish, Comment on “option pricing under the merton

model of the short rate” by kung and lee [math. comput. simul. 80 (2009)

378–386], Mathematics and Computers in Simulation, 81 (2010), pp. 1–4.

[4]H. Gu, J.-R. Liang, and Y.-X. Zhang, Time-changed geometric

fractional brownian motion and option pricing with transaction costs,

Physica A: Statistical Mechanics and its Applications, 391 (2012),

pp. 3971–3977.

[5]Z. Guo, Option pricing under the merton model of the short rate in

subdiffusive brownian motion regime, Journal of Statistical Computation and

Simulation, 87 (2017), pp. 519–529.

[6]M. Hahn, K. Kobayashi, and S. Umarov, Fokker-planck-kolmogorov

equations associated with time-changed fractional brownian motion,

Proceedings of the American mathematical Society, 139 (2011), pp. 691–705.

[7]J. J. Kung and L.-S. Lee, Option pricing under the merton model of

the short rate, Mathematics and Computers in Simulation, 80 (2009),

pp. 378–386.

[8]J.-R. Liang, J. Wang, L.-J. Lu, H. Gu, W.-Y. Qiu, and F.-Y. Ren, Fractional fokker-planck equation and black-scholes formula in

composite-diffusive regime, Journal of Statistical Physics, 146 (2012),

pp. 205–216.

[9]M. Magdziarz, Black-scholes formula in subdiffusive regime, Journal

of Statistical Physics, 136 (2009), pp. 553–564.

[10], Stochastic

representation of subdiffusion processes with time-dependent drift,

Stochastic Processes and their Applications, 119 (2009), pp. 3238–3252.

[11], Path properties of

subdiffusion—a martingale approach, Stochastic Models, 26 (2010),

pp. 256–271.

[12]R. C. Merton, A dynamic general equilibrium model of the asset

market and its application to the pricing of the capital structure of the

firm, Working paper, (1970).

[13]C. Necula, Option pricing in a fractional brownian motion

environment, Academy of Economic Studies Bucharest, Romania, Preprint,

Academy of Economic Studies, Bucharest, (2002).

[14]L. C. G. Rogers, Arbitrage with fractional brownian motion,

Mathematical Finance, 7 (1997), pp. 95–105.

[15]T. Sottinen and E. Valkeila, On arbitrage and replication in the

fractional black–scholes pricing model, Statistics &

Decisions/International mathematical Journal for stochastic methods and

models, 21 (2003), pp. 93–108.

[16]J. Wang, J.-R. Liang, L.-J. Lv, W.-Y. Qiu, and F.-Y. Ren, Continuous

time black–scholes equation with transaction costs in subdiffusive

fractional brownian motion regime, Physica A: Statistical Mechanics and its

Applications, 391 (2012), pp. 750–759.