Flexible and Robust Particle Tempering for State Space Models

Abstract

Density tempering (also called density annealing) is a sequential Monte Carlo approach to Bayesian inference for general state models; it is an alternative to Markov chain Monte Carlo. When applied to state space models, it moves a collection of parameters and latent states (which are called particles) through a number of stages, with each stage having its own target distribution. The particles are initially generated from a distribution that is easy to sample from, e.g. the prior; the target at the final stage is the posterior distribution. Tempering is usually carried out either in batch mode, involving all the data at each stage, or sequentially with observations added at each stage, which is called data tempering. Our paper proposes efficient Markov moves for generating the parameters and states for each stage of particle based density tempering. This allows the proposed SMC methods to increase (scale up) the number of parameters and states that can be handled. Most of the current literature uses a pseudo-marginal Markov move step with the states “integrated out,”and the parameters generated by a random walk proposal; although this strategy is general, it is very inefficient when the states or parameters are high dimensional. We also build on the work of Dufays, (2016) and make data tempering more robust to outliers and structural changes for models with intractable likelihoods by adding batch tempering at each stage. The performance of the proposed methods is evaluated using univariate stochastic volatility models with outliers and structural breaks and high dimensional factor stochastic volatility models having both many parameters and many latent states.

Keywords: Factor stochastic volatility model; Hamiltonian Monte Carlo; Outliers; Structural change; Particle Markov chain Monte Carlo; Diffusion process

1 Introduction

Joint inference over both the parameters and latent states in nonlinear and non-Gaussian state space models is challenging because the likelihood is usually an intractable integral over the latent states. In a seminal contribution, Andrieu et al., (2010) propose two batch particle Markov chain Monte Carlo (PMCMC) methods for state space models. The first method is the particle marginal Metropolis-Hastings (PMMH), where the parameters are generated with the unobserved latent states “integrated out”; this technically means that the likelihood is replaced by its unbiased estimate. The second method is the particle Gibbs (PG), which generates the parameters conditional on the states and conversely. Both methods run a particle filter algorithm within an MCMC sampling scheme at each iteration. Andrieu et al., show that for any finite number of particles, the augmented target density used by these two algorithms has the joint posterior distribution of the parameters and states as its marginal distribution. A number of papers, including Lindsten and Schon, (2013), Lindsten et al., (2014), Olsson and Ryden, (2011), Mendes et al., (2020), and Gunawan et al., 2020a , extend their work.

Density tempering sequential Monte Carlo (SMC) is an alternative to MCMC as a computational approach for Bayesian inference. It is a sequential importance sampling approach (Neal,, 2001), where samples are first drawn from an easily-generated distribution, e.g., the prior, and then moved towards the target distribution through a sequence of intermediate stages, with each stage having its own target distribution. Del Moral et al., (2006) outline the sequential Monte Carlo (SMC) method, which consists of resampling, reweighting and Markov move steps at each stage of the SMC.

It is generally recognised (Del Moral et al.,, 2006) that SMC has the following advantages compared to MCMC, and in particular, PMCMC approaches: (a) the Markov chain generated by an PMCMC sampler often gets trapped in local modes; it is also difficult to assess whether the chain mixes adequately and converges to its invariant distribution. SMC explores the parameter space more efficiently when the target distribution is multimodal; assessing convergence is also easier. (b) It is usually difficult to use PMCMC to estimate the marginal likelihood, which is often used to for model choice (Kass and Raftery,, 1995; Chib and Jeliazkov,, 2001). Using SMC to estimate the marginal likelihood is more straightforward. Section 4.2 also shows the usefulness of the sequential SMC approach to estimate the sequence of independent standard normal random variables used to form the goodness of fit statistics to test for the model adequacy of a general time series state space model as in Smith, (1985), Shephard, (1994), and Gerlach et al., (1998). Using PMCMC to compute the goodness of fit statistics can be very time-consuming as it is necessary to repeatedly construct the full Markov chain for each time period ; see, for example, Gerlach et al., (1998). (c) PMCMC algorithms are not parallelisable in general, whereas SMC algorithms can be parallelised (subject to some caveats); see, for example, Neal, (2001), Del Moral et al., (2006), and Duan and Fulop, (2015). Section 2.2 discusses this further.

Duan and Fulop, (2015) extend the annealing/density tempering method of Neal, (2001), and Del Moral et al., (2006) to time series state space models having intractable likelihoods. Their approach processes the time series as a batch. Fulop and Li, (2013) and Chopin et al., (2013) propose full sequential Bayesian inference on the parameters and call their algorithm Marginalised Resample-Move (MRM) and , respectively.

Our paper builds on this literature by proposing flexible SMC approaches that use Markov move steps that are more efficient than the density tempered SMC approach of Duan and Fulop, (2015), MRM of Fulop and Li, (2013), and of Chopin et al., (2013). The first Markov move approach is based on the PG algorithm of Andrieu et al., (2010); we call it sequential Monte Carlo with particle Gibbs (SMC-PG). The second is based on the Hamiltonian Monte Carlo (HMC) algorithm (Duane et al.,, 1987; Neal,, 2011; Girolami and Calderhead,, 2011; Hoffman and Gelman,, 2014; Betancourt,, 2017); we call it sequential Monte Carlo with Hamiltonian Monte Carlo (SMC-HMC). The third is based on the particle hybrid sampler of Gunawan et al., 2020a , which combines a step similar to the correlated PMMH of Deligiannidis et al., (2018) and the particle Gibbs of Andrieu et al., (2010); we call it sequential Monte Carlo with the particle hybrid sampler (SMC-PHS). The Markov move step based on PHS generates the parameters that are highly correlated with the states in PMMH steps. All other parameters are generated by particle Gibbs steps conditioning on the latent state variables.

The Markov moves based on PG, PHS and HMC are important for two reasons. First, they permit applications to much higher dimensional parameter spaces and much better proposals than random walk proposals; in particular, in some cases we are able to sample from the full conditional distribution using Gibbs steps. Second, Section 5.2 shows that using particle Gibbs Markov moves can substantially reduce the number of particles required because it is then unnecessary for the variance of the log of the likelihood estimate to be in the range of 1 to 3. In addition, if we suspect that some parameters converge slowly because they are highly correlated with the latent states in the model, then they can be generated using the PMMH step of the PHS.

Dufays, (2016) robustifies data tempering by adding batch tempering at each data point. His approach is suitable for models with a tractable likelihood enabling the Markov move steps to be carried out by MCMC. The target densities in Dufays, depend only on the parameters and the method is applied to standard GARCH models and GARCH models with change-point, and both only have a few parameters. Our article extends Dufays,’s approach to handle state space models with intractable likelihoods and with the latent states also appearing in the target densities; this makes it possible to obtain joint inference on both the parameters and the latent states.

Section 4.3 and Section 10.2 of the Supplement show that the proposed SMC is more stable than the methods of Fulop and Li, (2013) and Chopin et al., (2013) in datasets with outliers and structural breaks because it incorporates information from the data more gradually.

Our proposed sequential approach with tempering is different to previous approaches. It provides joint sequential inference on latent states and parameters up to time , , whereas the provides sequential inference on the parameters only. Johansen, (2015) does not propose density tempering or data tempering or a combination of both for making inference on the parameters, states, or both. Johansen, proposes a block tempered particle filter to estimate the likelihood unbiasedly and provides the filtered state distribution . Johansen, mentions that the block tempered particle filter can be used within the PMCMC for making inference on the parameters of the state space models, although he does not show it. His particle filter algorithm can also be used within our SMC algorithm, although we do not pursue this idea.

The Markov move step in SMC helps to diversify the particles to provide a better approximation to the tempered target distribution at that temperature level. Duan and Fulop, (2015), Fulop and Li, (2013) and Chopin et al., (2013) use a particle marginal Metropolis-Hastings (PMMH) approach with the likelihood estimated unbiasedly by the particle filter in the Markov move step. There are two drawbacks to a Markov move based on PMMH. First, it is computationally costly to follow the guidelines of Pitt et al., (2012) for high dimensional state space models and set the optimal number of particles in the particle filter such that the variance of the log of the estimated likelihood is in the range of to ; see the empirical example in Section 5.2. It is possible to implement the correlated PMMH of Deligiannidis et al., (2018), which is more efficient than standard PMMH for low dimensional state space models. However, the correlated PMMH is ineffective for a model with a high dimensional state, e.g. the factor SV model in Section 5.2. Second, it is hard to implement the PMMH Markov move efficiently for a high dimensional parameter as it is difficult to obtain a good proposal for the parameter because the first and second derivatives with respect to the parameters can only be estimated. Nemeth et al., (2016) and Mendes et al., (2020) find that the behaviour of the particle Metropolis adjusted Langevin algorithm (MALA) depends critically on how accurately we can estimate the gradient of the log-posterior. If the variance of the estimate of the gradient of the log-posterior is too large, then there is no advantage in using particle MALA over the random walk proposal. The random walk proposal is easy to implement, but is very inefficient in high dimensions.

We illustrate the proposed SMC methods empirically using a sample of daily US stock returns to estimate the univariate stochastic volatility (SV) models with outliers and structural breaks and the multivariate high dimensional factor SV model. The factor SV model is popular because it parsimoniously models a vector of returns. Most applications of multivariate factor stochastic volatility models are in financial econometrics (Nardari and Scruggs,, 2007; Aguilar and West,, 2000; Zhou et al.,, 2014). Current popular MCMC estimation approaches for the factor SV model by Chib et al., (2006) and Kastner et al., (2017) are neither exact nor flexible; neither paper corrects for the approximation errors. They follow the approach proposed by Kim et al., (1998) to approximate the distribution of log outcome innovations by a carefully constructed seven component mixture of normal distributions. In the empirical application in Section 5.2, we show that the MCMC sampler of Kastner et al., (2017) can give very different results to the PHS for some parameters of the factor SV model. The accuracy of the proposed SMC approaches are also compared to the PHS. Section 5.2 shows that the proposed SMC samplers give accurate estimates of the posterior densities of the parameters and predictive densities. We also consider a factor SV with the log-volatilities of the idiosyncratic errors to follow continuous time Ornstein-Uhlenbeck (OU) processes (Stein and Stein,, 1991). Although the continuous time OU diffusion model has a closed form transition density (Brix et al.,, 2018), the SMC methods are applied to the Euler approximation of the OU process and hence can handle the diffusion processes that do not admit closed form transition densities (Ignatieva et al.,, 2015). Section 5.3 gives further details.

The rest of the article is organised as follows. Section 2 outlines the state space model and its estimation by SMC. Section 3 discusses the proposed flexible Markov moves. Section 4 presents empirical results for the univariate example. Section 5 introduces and presents empirical results for the factor SV model. The online Supplement to the paper contains some further technical and empirical results.The following notation is used in both the main paper and the online Supplement. Eq. (1), Section 1, Algorithm 1 and Sampling Scheme 1, etc. refer to the main article, while Eq. (S1), Section S1, Algorithm S1, and Sampling Scheme S1, etc. refer to the Supplement.

2 Flexible Density Tempering

This section introduces the state space model and discusses the SMC approaches.

2.1 The State Space Model

We use the colon notation for collections of variables, i.e. , , and .

We consider a state space model where the latent states determine the evolution of the system. The density of is and the transition density of given is for . The observations for are linked to the latent states through the observation equation . Denote the -dimensional Euclidean space by . We suppose that (i) the state vector and the observation , where and ; (ii) the parameter vector , where is a subset of .

Our aim is to perform Bayesian inference over the latent states and the parameters conditional on the observations . By using Bayes rule, the joint posterior of the latent states and the parameters is

is the prior density of and is the marginal likelihood of . For notational simplicity, we often write and .

Examples

This section illustrates the state space model by the univariate stochastic volatility model,

| (1) |

with and and independent. We call the latent log volatility process. The vector of unknown parameters is . To ensure that the model is stationary, we restrict the persistence parameter so that .

2.2 The SMC Approach for State Space Models

2.2.1 Batch Estimation Method

This section discusses the proposed SMC method for batch estimation problems. The main idea is to begin with an easy-to-sample distribution and propagate a particle cloud through a sequence of tempered target densities , for , to the posterior density of interest which is much harder to sample from directly. The tempered densities are defined as

The tempering sequence is such that . If it is both easy to generate from the densities and , and evaluate them, then we take , and hence

| (2) |

Algorithm 1 summarizes the general SMC approach, which we now discuss. The initial particle cloud is obtained by generating the from , and giving the particles equal weight, i.e., . The weighted particles (particle cloud) at the st level (or stage) of the annealing is an estimate of . Based on this estimate of , the SMC algorithm goes through the following steps to obtain an estimate of . The move from to is implemented by reweighting the particles by the ratio of the two unnormalized densities , yielding the following weights, , where

| (3) |

where is defined in Eq. (2). We follow Del Moral et al., (2012) and choose the tempering sequence adaptively to ensure sufficient particle diversity by selecting the next value of automatically such that the effective sample size (ESS) stays close to some target value chosen by the user. The ESS is used to measure the variability in the , and is defined as . The ESS varies between 1 and , with a low value of ESS indicating that the weights are concentrated only on a few particles and a value of means that the particles are equally weighted. An ESS close to the target value is achieved by evaluating the ESS over a grid of potential values and selecting as the value of whose ESS is the closest to . Other approaches to select the tempering sequence, such as that in Del Moral et al., (2012), may be used instead. The particles are then resampled proportionately to their weights , which means that the resampled particles then have equal weight . This has the effect of eliminating particles with negligible weights and replicating the particles with large weights, so the ESS is now . We use multinomial resampling for all the examples in the paper.

Repeatedly reweighting and resampling can seriously reduce the diversity of the particles, and lead to particle depletion. The particle cloud may then be a poor representation of . To improve the approximation of the particle cloud to , we carry out Markov move steps for each particle using a Markov kernel which retains as its invariant density. Thus, at each annealing level, we run a short MCMC scheme for each of the particles.

Steps and 2a-2d of Algorithm 1 are standard and apply to any model, with only slight model-specific modifications; hence, it is only necessary to discuss the Markov move step in detail for each model. We propose three Markov move algorithms that leave the target density invariant. The first algorithm is based on particle Gibbs (Andrieu et al.,, 2010), and is denoted as SMC-PG. The second algorithm is based on Hamiltonian Monte Carlo (Neal,, 2011), and is denoted as SMC-HMC. The third algorithm is based on the particle hybrid sampler (PHS) of Gunawan et al., 2020a , and is denoted as SMC-PHS.

By Del Moral et al., (2006), the SMC algorithm provides consistent inference for the target density as goes to infinity. See also Beskos et al., (2016) for recent consistency results for the adaptive algorithm employed here and the associated central limit theorem.

Section 1 states that the SMC algorithm can be parallelised. However, parallelising SMC is not straightforward due to the resampling in step (2d) of Alg. 1. In our applications given in Sections 4 and 5.2, the optimal number of annealing levels, , obtained from the adaptive approach described above is moderate and therefore resampling has little effect on the efficiency of the SMC algorithm. The reweighting in step (2c) and the Markov moves in step (2e) are easily parallelised for each SMC sample because the computations required for each sample are independent ofthe other SMC samples.

-

1.

Set and initialise the particle cloud , by generating the from , and giving them equal weight, i.e., , for

-

2.

While the tempering sequence do

-

(a)

Set

-

(b)

Find adaptively by searching across a grid of values to maintain ESS around some constant .

-

(c)

Compute new weights,

(4) -

(d)

Resample using the weights to obtain .

-

(e)

Markov moves

-

i.

Let be a Markov kernel having invariant density . For , move each times using the Markov kernel to obtain .

-

ii.

Set .

-

i.

-

(a)

2.2.2 Sequential Estimation Method

We now discuss the extension of the density tempered SMC approach in Section 2.2.1 to the situation where we are interested in sequential estimation of both the states and parameters as new observations arrive. This approach has very useful applications, especially in finance and economics. For example, in finance, investors need to update their volatility and return forecasts whenever new data become available. As another example, economists need to revise their forecasts as news on the state of the economy changes. Here, PMCMC techniques are expensive and time-consuming to use as they need to repeatedly restart the MCMC as new observations arrive.

The main challenge is how to jointly sample and propagate the states and parameters as new observations arrive. Our framework deals with this by extending the SMC sequence of target distributions as the number of observations increases. The main idea is to propagate a particle cloud that reflects the joint posterior of states and parameters at time through a sequence of tempered target densities , for , to the joint posterior density of states and parameters at time . The tempered densities are defined as

The move from to is implemented by reweighting the particles by the ratio of the two unnormalised densities , yielding the weights

Section 4.3 and Supplement 10.2 show that our sequential approach is robust to outliers and structural breaks; this happens because tempering incorporates the information in new observations gradually. It also means that it is easy to maintain the ESS close to its target .

The sequential approach in Chopin et al., (2013) only targets the posterior density of the parameters by “integrating out” the latent states, , up to time . Our sequential tempering approach targets the joint posterior density of the parameters and latent states, , up to time .

3 Flexible Markov Moves

This section discusses the Markov move steps in step (2e) of Algorithm 1. The first is based on the Hamiltonian Monte Carlo (HMC) algorithm (Neal,, 2011). The second is based on the particle Gibbs (PG) algorithm of Andrieu et al., (2010). The third is based on the particle marginal Metropolis-Hastings (PMMH) algorithm of Andrieu et al., (2010). The fourth is based on the particle hybrid sampler of Gunawan et al., 2020a .

3.1 Hamiltonian Monte Carlo

The Markov move has two steps. The first step updates the latent states conditional on the parameters using Hamiltonian Monte Carlo (HMC). The second step updates the parameters conditional on the states .

Sampling the high dimensional latent state vector is discussed first. Suppose we want to sample from a -dimensional distribution with a density proportional to , where . In Hamiltonian Monte Carlo (Neal,, 2011), we augment with an auxiliary momentum vector , having the same dimension as the latent state vector , with the density , where is a mass matrix. We define the joint conditional density of as

where is called the Hamiltonian. In an idealised Hamiltonian step, the state vector and the momentum variables move continuously according to the differential equations

where denotes the gradient with respect to . In practice, this continuous time Hamiltonian dynamics needs to be approximated by discretizing time, using a step size . We can then simulate the evolution over time of via the “leapfrog” integrator using Alg. 2.

Sections 9.1 and 9.2 of the Supplement give the details for the univariate SV model. Sections 13.1 and 13.2 of the Supplement give the details for the factor SV model.

Given initial values of , , , where is the number of leapfrog updates

Sample

For to

Set

end for

With probability

set , , else retain current .

function Leapfrog(,,)

Set

Set ,

Set ,

return ,

3.2 Particle Gibbs

The Markov moves based on PG, PMMH, and PHS run a particle filter algorithm at each iteration. Section 3.2.1 discusses the particle filter. Section 3.2.2 then discusses particle Gibbs based Markov move steps.

3.2.1 Particle Filter

This section describes the particle filter methods used to obtain sequential approximations to the densities for . The particle filter algorithm recursively produces a set of weighted particles such that the intermediate densities are approximated by

where is the Dirac delta distribution located at . In more detail, given samples representing the filtering density at time , we use

to obtain the particles representing , by first drawing from a known and easily sampled proposal density function and then computing the unnormalised weights to account for the difference between the target posterior density and the proposal, where

these are then normalized as .

Chopin, (2004) shows that as the number of time periods increases, the normalised weights of the particle system become concentrated only on a few particles and eventually the normalised weight of a single particle converges to one. This is known as the ‘weight degeneracy’ problem. One way to reduce the impact of weight degeneracy is to include resampling steps in a particle filter algorithm. A resampling scheme is defined as , where indexes a particle in that is chosen with probability . Section 16 of the Supplement states some assumptions on the proposal density and resampling scheme. In our empirical applications, we use the bootstrap filter with as a proposal density and multinomial resampling.

3.2.2 Particle Gibbs (PG) Algorithm

This section discusses the Markov move based on the particle Gibbs algorithm. Unless stated otherwise, we write PG to denote both the particle Gibbs (PG) and particle Metropolis within Gibbs Markov moves. Let denote the collection of particles in the particle filter algorithm, together with their associated indices defined in Section 3.2.1. The SMC-PG constructs a sequence of tempered densities , , based on the augmented tempered target density that includes all the particles generated by the particle filter. Section 11 of the Supplement gives further details of the augmented tempered target density.

Algorithm 3 gives the Markov move based on the particle Gibbs algorithm. Let be a partition of the parameter vector into components, where each component may be a vector.

For SMC samples,

-

1.

For , sample from the proposal density

. -

2.

Accept the proposed values with probability

- 3.

- 4.

Parts 1 and 2 of Algorithm 3 update each parameter block of conditional on a trajectory . Part 3 is the conditional sequential Monte Carlo of Andrieu et al., (2010) that is the key part of the Markov move steps. It is a particle filter algorithm in which a particle , and the associated sequence of ancestral indices are kept unchanged with all the other particles and indices resampled and updated. The collection of all random variables except the chosen particle trajectory is denoted by . Part 4 of Algorithm 3 samples the new indices sequentially using backward simulation given in Algorithm 10 of Section 15 of the Supplement, obtains the new particle trajectory , and discards the rest of the particles. Following Whiteley, (2010) and Lindsten and Schon, (2013), the conditional density in Part 4 is

for and . The Markov move based on the PG algorithm is useful in generating the vector of high-dimensional parameters, except when some of the parameters are highly correlated with the latent states.

3.3 Particle Marginal Metropolis-Hastings

Algorithm 4 describes the Markov move based on the particle marginal Metropolis-Hastings (PMMH) approach (Andrieu et al.,, 2010); this is useful for generating parameters that are highly correlated with the states. The PMMH algorithm requires an unbiased estimate of the likelihood, which is obtained from the particle filter.

Given initial values for , , and , for SMC samples. One iteration of PMMH involves the following steps:

-

1.

Sample from the proposal density .

- 2.

- 3.

-

4.

Accept the proposed values of , , and with probability

(5)

Parts 1 to 3 of the Algorithm 4 propose the values of , , and , which are then accepted with the probability in Eq. (5). Algorithm 4 targets the joint posterior density of the latent states and the parameters . Duan and Fulop, (2015) use a PMMH method, with the likelihood estimated unbiasedly by the particle filter, in the Markov move component. However, they only target the posterior distribution of the parameters . We call their method SMC-PMMH-DF.

3.4 Particle Hybrid Sampler

Mendes et al., (2020) propose a new particle MCMC sampler that combines the particle Gibbs and PMMH algorithms of Andrieu et al., (2010). The sampler generates parameters that are highly correlated with the states using PMMH, with the rest generated by PG. Deligiannidis et al., (2018) propose the correlated PMMH method, which correlates the random numbers used in constructing the likelihood estimates at the current and proposed values of the parameters. They show that the correlated PMMH can scale up with the number of observations compared to standard PMMH, as long as the state dimension is not too large. Gunawan et al., 2020a propose a novel PMCMC which involves a non-trivial combination of the correlated PMMH and the PG algorithms; Gunawan et al., 2020a call it the particle hybrid sampler (PHS). Unlike Andrieu et al., (2010), its augmented target density is expressed in terms of basic uniform and standard normal random numbers. The parameters that are efficiently generated by conditioning on the latent states are generated in a particle Gibbs step. All other parameters are drawn with PMMH steps by conditioning on the basic uniform and standard normal variables used in the particle filter algorithm. The PHS sampler is scalable in the number of observations and the number of parameters. See Gunawan et al., 2020a for further details.

The PHS Sampling Scheme

Algorithm 5 outlines the Markov move steps based on the particle hybrid sampler. For simplicity, let partition the parameter vector into 2 components. It generates using a PMMH step and the vector parameter using a PG step. The elements in and are sampled separately in the PMMH step and PG step, respectively.

Given initial values for , , , and . For (SMC samples), one iteration of the PHS involves the following steps:

- Part 1:

- Part 2:

-

Part 3:

Particle Gibbs (PG) sampling.

-

(a)

Sample

-

(b)

Accept the proposed values with probability

-

(a)

- Part 4:

Part 1 generates using PMMH, conditioning on the random numbers and obtained from Part 4, the parameters , and the current parameters . Part 2 samples the new indices using the backward simulation algorithm, obtains the new particle trajectory , and discards the rest of the particles. Part 3 generates the parameters using PG, conditioning on the selected particle trajectory , the parameter and the current parameter . Part 4 updates the basic random numbers using constrained conditional sequential Monte Carlo (Gunawan et al., 2020a, ); see Section 15.1 of the Supplement.

3.5 Marginal Likelihood Estimation

The marginal likelihood is often used in the Bayesian literature to compare models (Chib and Jeliazkov,, 2001). An advantage of the SMC method is that it offers a natural way to estimate the marginal likelihood. We note that , , so that

Because the particle cloud obtained after iteration approximates , the ratio above is estimated by

giving the marginal likelihood estimate

4 Univariate Examples

4.1 Univariate Stochastic Volatility Model

This section illustrates the proposed SMC-PG and SMC-HMC methods for batch estimation problems by applying them to the univariate stochastic volatility (SV) model and compares their performance to the exact particle hybrid sampler (PHS) of Gunawan et al., 2020a and the SMC-PMMH-DF of Duan and Fulop, (2015). Posterior distributions obtained from the PHS method are treated as the ‘ground truth’ for comparing the accuracy of the posterior density approximations for two reasons. The first is that we have extensively applied PHS to stochastic volatility models, and in our experience it has always worked well. Second, PHS belongs to the class of PMCMC methods of Andrieu et al., (2010) and their key property is that they are an ‘exact approximation’ to the idealised MCMC algorithms targeting the joint posterior density of the latent states and parameters (Andrieu et al.,, 2010). We follow South et al., (2019) and Gunawan et al., 2020b by comparing the posterior densities of the parameters estimated using different SMC algorithms and exact MCMC methods.

The vector of unknown parameters of the SV model in Section 2.1 is . The parameters have the following priors, and are assumed to be independent apriori: (a) . (b) Following Jensen and Maheu, (2010), the prior for is inverse Gamma with and . (c) To ensure stationarity, the persistence parameter is restricted to ; we follow Kim et al., (1998) and choose the prior for as , with and . We apply our methods to a sample of daily US food industry stock returns obtained from the Kenneth French website, using a sample from December 11th, 2001 to the 11th November 2013, a total of observations.

The performance of SMC-HMC depends on choosing suitable values for the three tuning parameters i) the mass matrix , ii) the step size , and iii) the number of leapfrog steps . The step size determines how well the leapfrog integration approximates the Hamiltonian dynamics. If it is too large, then a low acceptance rate may result, but if it is too small, then it becomes computationally expensive to obtain distant proposals. Similarly, if is too small, then the proposal will be close to the current value of the latent state vectors, resulting in undesirable random walk behaviour. If is too large, then HMC will generate proposals that retrace their steps. The precision matrix of the AR(1) process of the latent states is a sparse tridiagonal matrix whose diagonal elements are , except for the first and last diagonal elements which are ; the super- and sub-diagonal elements are . We set . Our article uses two adaptive approaches. The first follows an adaptive method based on Garthwaite et al., (2015) to select an that yields a specified average acceptance probability across all particles and is set to some fixed value; we denote this method as SMC-HMC-I. The second adaptive approach is to select both and based on the adaptive method by Buchholz et al., (2020) and denote it as SMC-HMC-II.

Table 1 summarises the estimation results for the univariate SV model estimated using the PHS, SMC-HMC, SMC-PG, and SMC-PMMH-DF methods. The PHS chain consists of 5000 iterates for burnin and another 50000 iterates used for inference. All the SMC estimates are obtained using 10 independent runs, each with samples, to generate a total of samples for each algorithm. We set the constant . The computations are done using Matlab on a single desktop computer with 6-CPU cores.

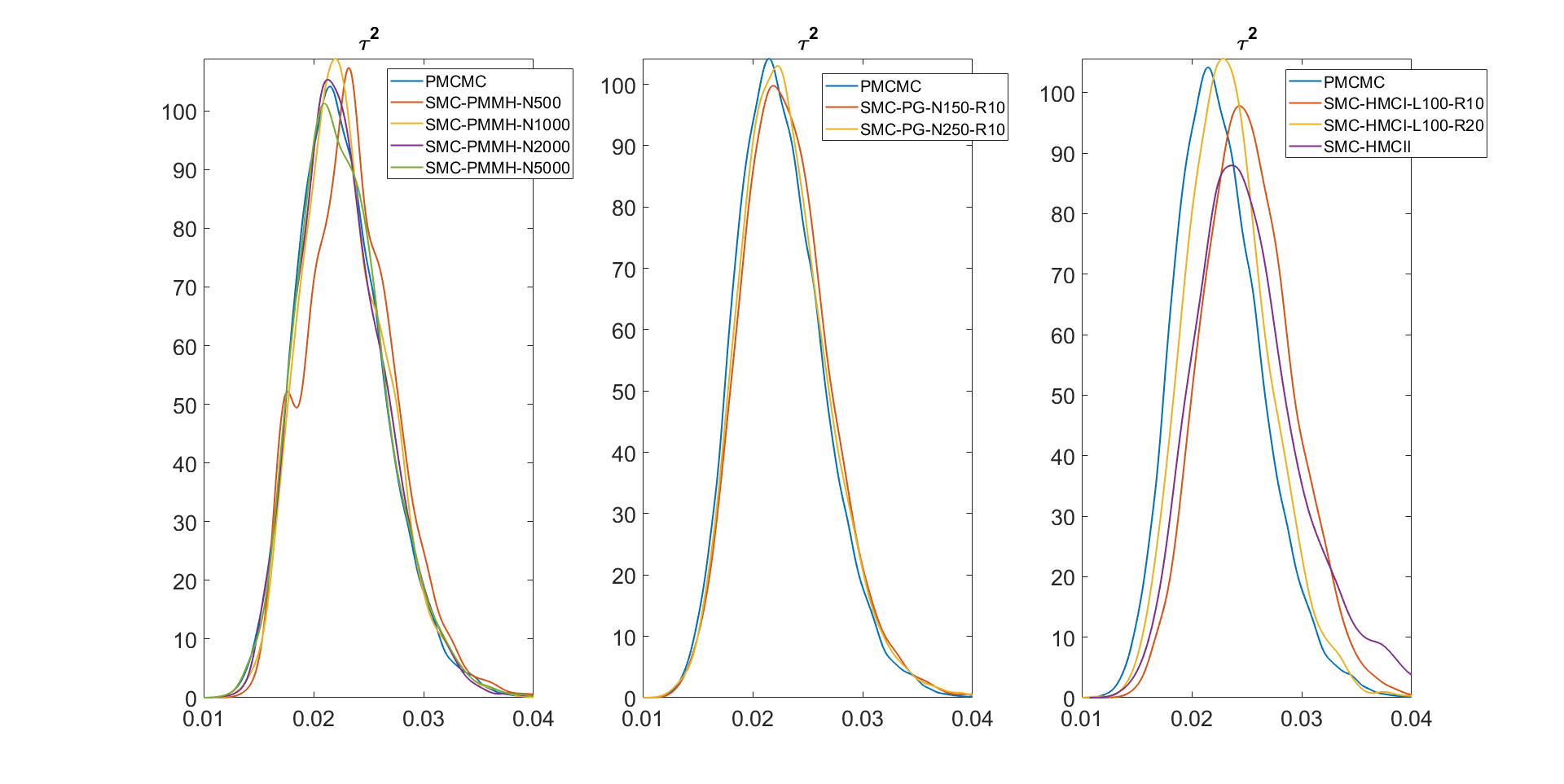

Table 1 shows that all the SMC-PG estimates are very close to the PHS estimates for all parameters even with as few as particles and Markov move steps. The middle panel of Fig. 1 shows the kernel density estimates of the marginal posteriors of the univariate stochastic volatility parameters estimated using the PHS and the SMC-PG methods with different numbers of particles. The density estimates from the SMC-PG methods are very close to the density estimates of the PHS sampler.

Table 1 shows that the estimates of and estimated using the SMC-HMC-I with is the closest to the estimates of the PHS compared to SMC-HMC-I with and SMC-HMC-II. But in general, they are very close to each other. The right panel of Fig. 1 shows the kernel density estimates of the marginal posteriors of the univariate SV parameters estimated using the PHS and the SMC-HMC methods. The figure confirms that the densities estimates of estimated from SMC-HMC-I with are the closest to the estimates from the PHS, but still sligthly inaccurate compared to the SMC-PG estimates. In general, SMC-PG is more accurate than the SMC-HMC, but its CPU time is slightly larger. Table 1 also shows that the optimal number of Markov move steps obtained from the adaptive approach described in Section 2.2 are similar for SMC-PG and SMC-HMC methods.

The left panel of Fig. 1 shows the kernel density estimates of the marginal posteriors of the univariate SV parameters estimated using the PHS and the SMC-PMMH-DF methods. The density estimates from SMC-PMMH-DF with and particles are close to the PHS estimates. The number of Markov move steps of SMC-PMMH-DF are smaller compared to the SMC-PG and SMC-HMC methods because it only targets the posterior density of SV parameters and not the latent log-volatilities. The SMC-PG with particles is still slightly faster than SMC-PMMH-DF with particles.

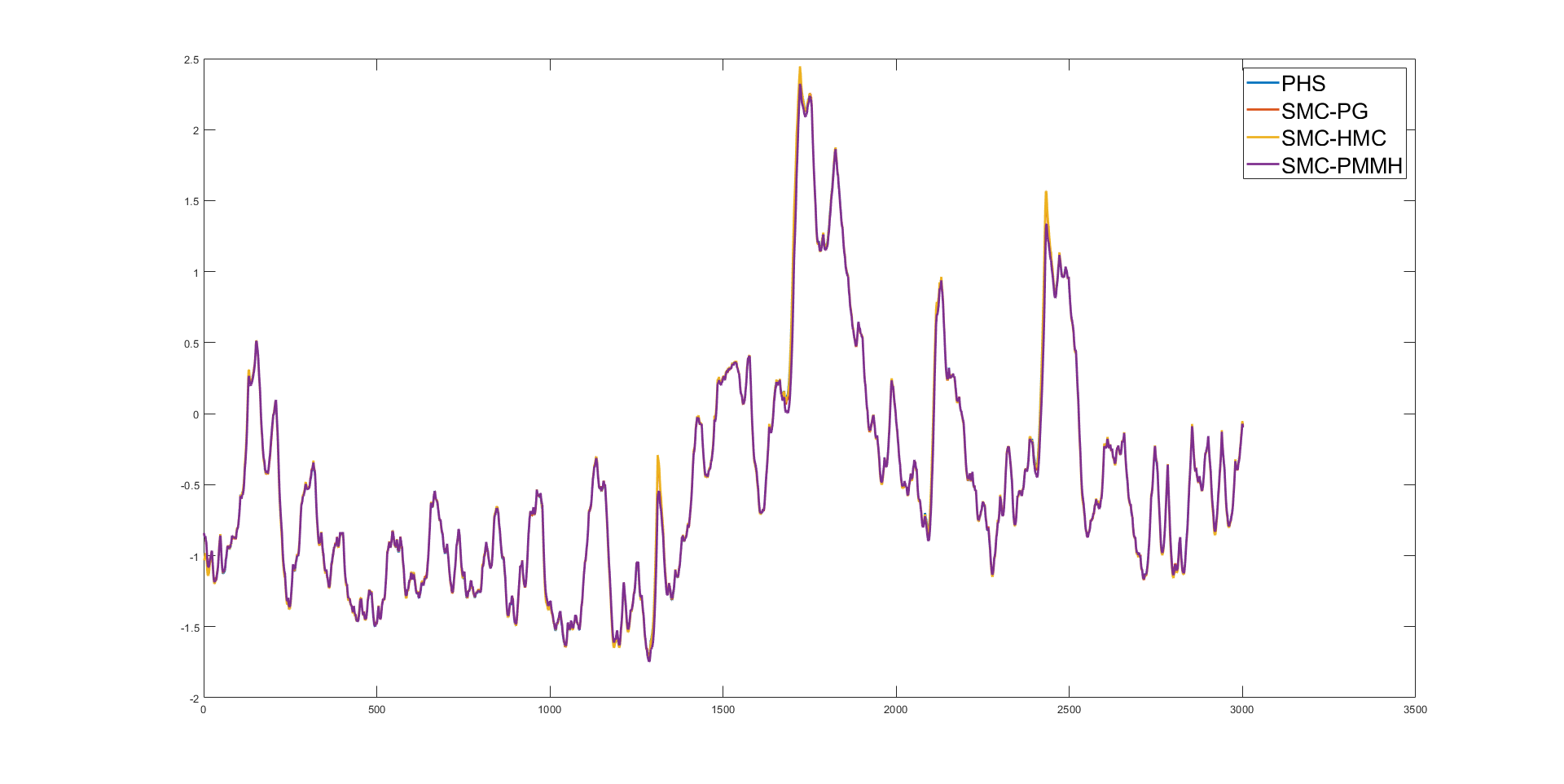

Fig. 2 shows the posterior mean estimates of the latent log-volatilities estimated using PHS with , SMC-PG with , SMC-HMC-I with , and SMC-PMMH-DF with . The SMC-PG, SMC-PMMH-DF, and PHS estimates are indistinguishable. The estimates from SMC-HMC-I are slightly less accurate at some time points. This study suggets that (a) The SMC-HMC methods are less accurate compared to SMC-PG and SMC-PMMH-DF methods for estimating the standard univariate SV models; (b) The SMC-PG with is as accurate as the SMC-PMMH-DF with , and faster than the SMC-PMMH-DF for this example; (c) The SMC-PMMH-DF provides inference only on the parameters, and not the latent states. Two steps are needed to obtain the posterior density of the latent states. First, the SMC draws of the parameters are obtained from running the SMC-PMMH-DF algorithm. Second, the particle filter and backward simulation algorithms are run for each parameter draw to give the posterior density of the latent states.

| Method | Time | |||||||

|---|---|---|---|---|---|---|---|---|

| PHS | 100 | - | - | - | 513 | |||

| HMC-I | - | 100 | 10 | 57 | 62.87 | |||

| HMC-I | - | 100 | 20 | 57 | 123.68 | |||

| HMC-II | - | 100 | 20 | 57 | 137.23 | |||

| PG | 150 | - | 10 | 59 | 109.27 | |||

| PG | 250 | - | 10 | 57 | 156.18 | |||

| PMMH-DF | 500 | - | 10 | 15 | 58.03 | |||

| PMMH-DF | 1000 | - | 10 | 14 | 105.63 | |||

| PMMH-DF | 2000 | - | 10 | 14 | 226.18 | |||

| PMMH-DF | 5000 | - | 10 | 13 | 671.94 |

The above analyses suggest that for this example the SMC-PG and SMC-PMMH-DF are the most accurate SMC methods. The next example compares the performance of the SMC-PG and SMC-PMMH-DF for estimating the univariate SV model with a larger number of parameters. The measurement equation is now

| (7) |

where and is a vector of covariates at time . We compare the performance of the following samplers: (I) the PHS with , (II) SMC-PG with , (III) SMC-PMMH-DF with and . We apply the methods to simulated data with observations, , , , . The parameters are generated independently of each other from normal distributions with mean zero and standard deviation , for all . The covariates are generated randomly from a multivariate normal . The prior for is for .

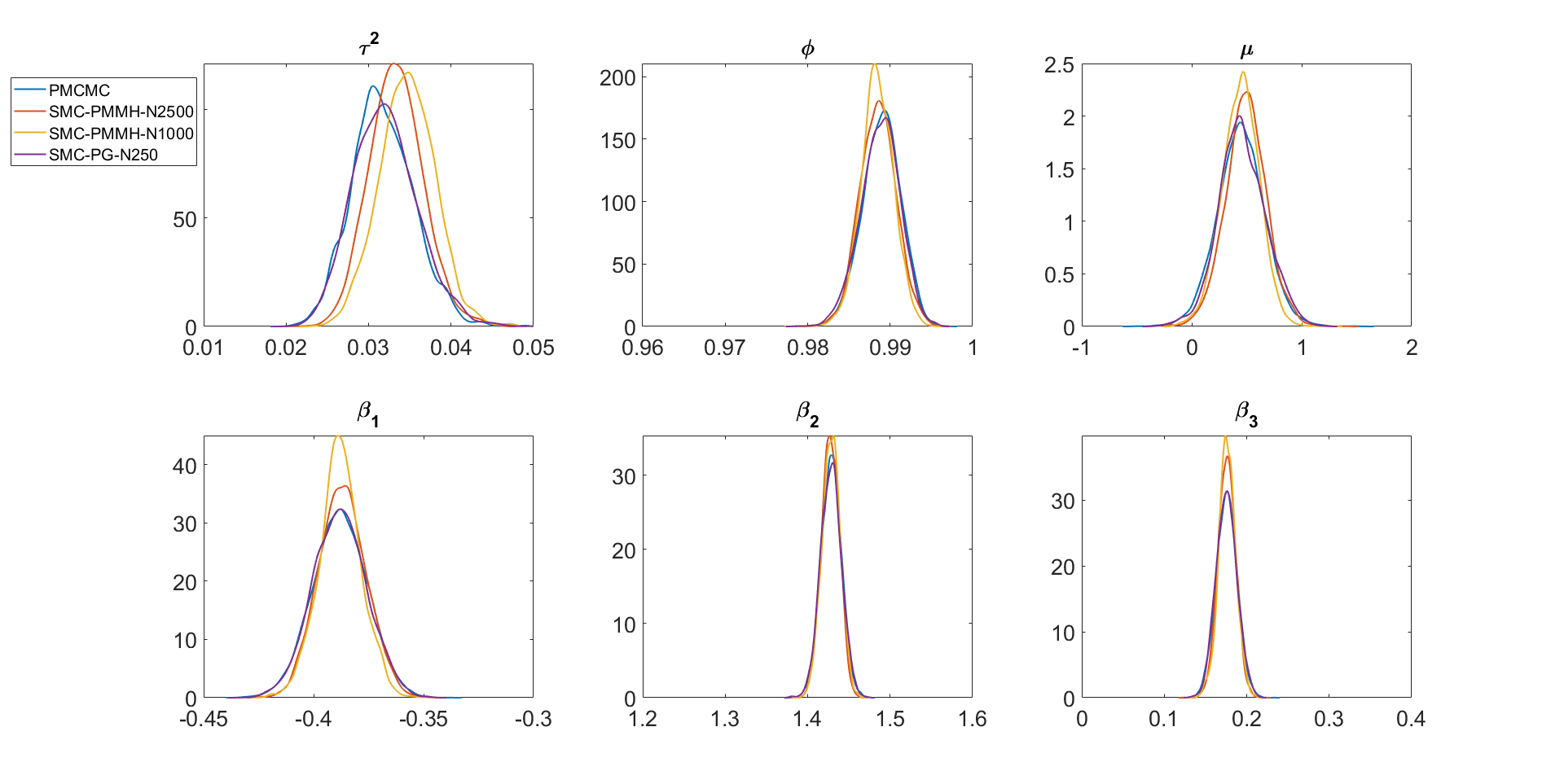

Fig. 3 shows the kernel density estimates of some marginal posterior densities of the univariate SV parameters with the covariate coefficients estimated using the PHS, the SMC-PMMH-DF and the SMC-PG methods. The figure shows that the SMC-PG estimates are very close to the PHS estimates for all SV parameters and the three covariate coefficients . The estimates from the SMC-PMMH-DF are different to the PHS even with particles. Similar conclusions hold for other coefficients given in Figure 14 of Supplement 10. Table 2 summarizes the estimation results of the SV model with covariates. Interestingly, the number of Markov move steps for the SMC-PMMH-DF is similar to the SMC-PG method for this example. The SMC-PG method is more accurate and 4.76 times faster than the SMC-PMMH-DF with particles.

This example suggests that (a) The SMC-PG performs better than the SMC-PMMH-DF for estimating the univariate SV parameters with covariate coefficients. The vector of parameters are high dimensional and not highly correlated with the states, so it is efficient to generate them in a PG step. (b) SMC-PMMH-DF gives different estimates to the PHS even with particles. SMC-PMMH-DF uses a PMMH approach with a random walk proposal for the parameters in the Markov move component. The random walk is easy to implement, but is not efficient for high-dimensional parameters. However, SMC-PMMH-DF is a more general algorithm than SMC-PG. It only needs an efficient estimate of the likelihood. Section 5.3 discusses an example that uses the SMC-PHS method where it is useful to generate parameters that are highly correlated with the states using PMMH steps and the other parameters are generated using PG steps by conditioning on the states.

| Method | N | R | P | Time |

|---|---|---|---|---|

| PG | 250 | 10 | 89 | 754.79 |

| PMMH-DF | 1000 | 10 | 72 | 1081.29 |

| PMMH-DF | 2500 | 10 | 72 | 3590.80 |

4.2 Time Series Diagnostics

The sequential SMC approach in Section 2.2.2 allows us to efficiently estimate the sequence of standard normal random variables used to form the goodness of fit statistics to test for the adequacy of a general time series state space model (Gerlach et al.,, 1998). Let be a sequence of time series observations generated by the continuous random variables . If the correct model is fitted to the data, then the sequence

| (8) |

is a realization of independent uniform random variables. A sequence of independent standard normal random variables is obtained by setting , where is the standard normal cumulative distribution function. To obtain , it is necessary to integrate out the parameters and the latent states by evaluating

| (9) |

For many statistical models, such as the stochastic volatility model, the integral in Eq. (9) cannot be evaluated analytically. One way to estimate is to use MCMC or particle MCMC methods. Given a sample of MCMC draws, and (), from , then

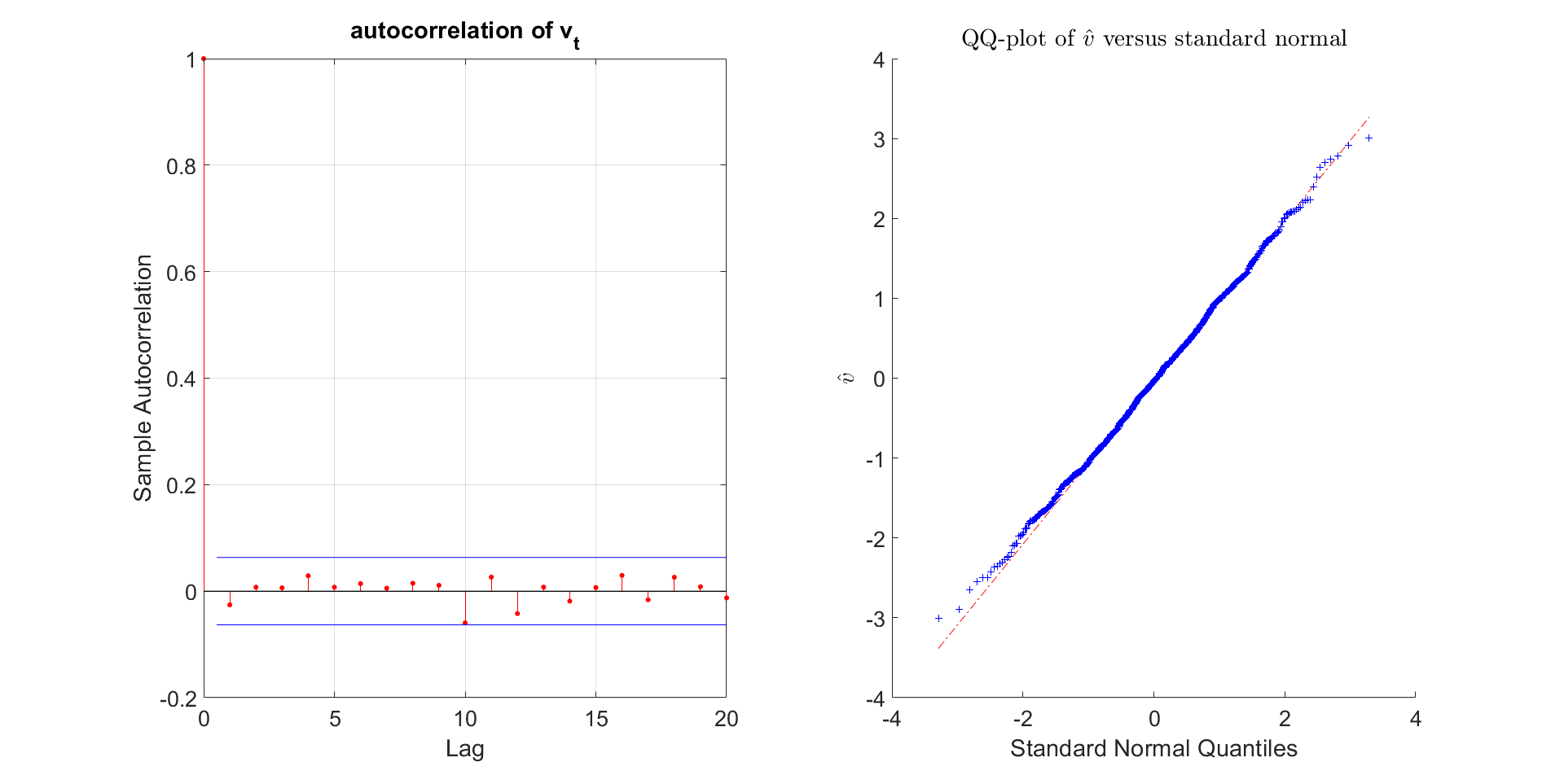

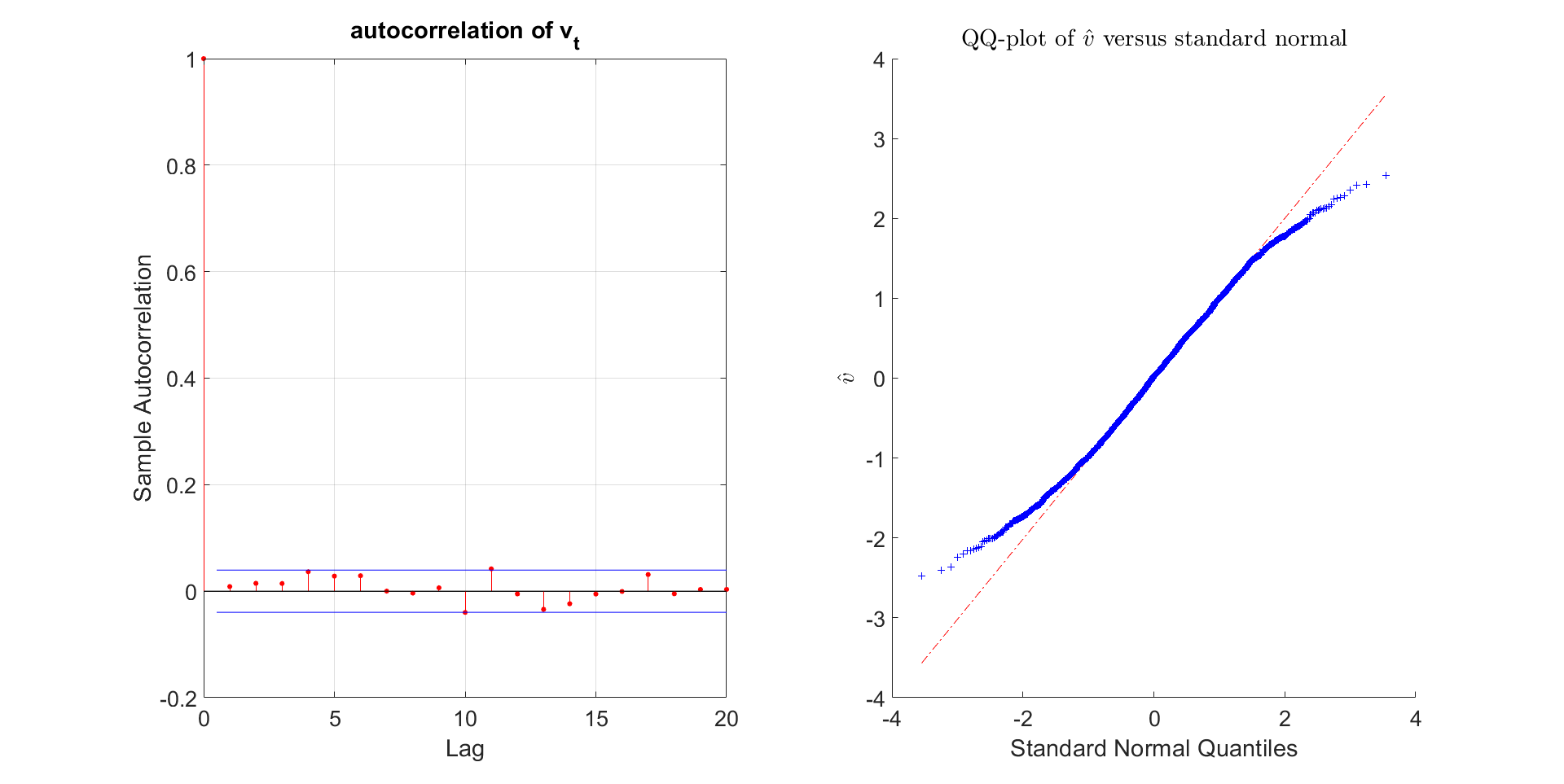

is an estimate of . The sequence is obtained by setting for . However, MCMC can be very time-consuming as it is necessary to repeatedly construct the full Markov chain for each time period ; see, e.g., (Gerlach et al.,, 1998). The sequential approach, denoted by SMC-PG-seq, can be used to estimate efficiently. If the model is correct, the sequence of is uniform and independent and the sequence of is standard normal and independent. We apply the approach to test for model adequacy using simulated and real data. The simulated data uses the parameter values , , , and observations. A single run of the sequential approach, SMC-PG-seq, with samples is used to obtain the estimate of and , for . Fig. 4 shows the diagnostic plots for the series for . The autocorrelation plot in the figure suggests that the series is uncorrelated. The QQ-plot suggests the series is normal. The Anderson-Darling test (Stephens,, 1974) can also be used to test the null hypothesis that the series is normally distributed; the null hypothesis is not rejected at the 5% level of significance (p-value=0.65). This is expected because the dataset is simulated from the SV model. We now apply the methods to a sample of daily US food industry stock returns as in the previous section. Fig. 5 shows the diagnostic plots for the series for the real data. The autocorrelation plot in the figure suggests that the series is uncorrelated; (2) the quantiles of are similar to the quantiles of the standard normal distribution, except in both tails. The Anderson-Darling test for normality of the series is rejected at the 5% level of significance (p-value=0.00). We conclude from this result that the standard univariate SV model is inadequate for this series.

This shows the usefulness of the SMC-PG-seq to estimate efficiently the sequence used to form the goodness of fit statistics to test for the adequacy of a general time series state space model. Another important advantage of sequential SMC over MCMC is that it provides sequential one-step ahead predictive densities of the log returns, and hence prices; this is particularly useful for financial applications. See Section 10 of the Supplement.

4.3 SV Model with Outliers

This section uses data simulated from a standard SV model contaminated by outliers to study the performance of the proposed sequential approach SMC-PG-seq with tempering (denoted by SMC-PG-seqT) in Section 2.2.2 and compares it to the standard sequential approach without tempering (denoted by SMC-PG-seqNT). In each scenario, a dataset is generated with observations using parameter values , , and . The generated observations are then contaminated with noise , where is a Bernoulli indicator with parameter and is normally distributed with mean zero and standard deviation . The parameter controls the degree of contamination and is set to . A single dataset is simulated in each case. Duan and Fulop, (2015) find that the density tempered SMC method is more robust to outliers than the standard sequential approach because it incorporates the information from the data gradually. We use the estimates of the SMC-PG method as the “gold standard” to assess the accuracy of the sequential SMC-PG-seqT and SMC-PG-seqNT approaches. All the SMC estimates are obtained using 10 independent runs, each with samples. For the SMC-PG and SMC-PG-seqT, is set to .

Table 3 summarises the simulation results for the SV models with different degrees of data contamination . The first three rows report the standard error of the posterior mean estimates of the SV model parameters over the 10 runs of the algorithms; the fourth and fifth rows report the mean and standard error of the log of the marginal likelihood estimates. The SMC-PG-seqT and SMC-PG provide stable results for all values of , but the performance of SMC-PG-seqNT deteriorates as increases. When , the standard error of from SMC-PG-seqNT is and times larger than from SMC-PG-seqT and SMC-PG, respectively. The Monte Carlo error of the SMC-PG-seqNT increases as outliers become larger in magnitude. The outliers lead to highly variable weights in the reweighting step of the SMC-PG-seqNT algorithm and very low effective sample size (ESS) of the particles. More importantly, the Monte Carlo error of the log of the marginal likelihood estimates seem to deteriorate much faster than the parameter estimates as increases. When , the standard error of the log of the marginal likelihood estimate from SMC-PG-seqNT is 28.05 and 21.49 times larger than from SMC-PG-seqT and SMC-PG, respectively. The log of the marginal likelihood estimates from the PG-seqNT are substantially different to the estimates from SMC-PG-seqT and SMC-PG for . Section 10.1 of the Supplement gives further empirical results. Section 10.2 of the Supplement discusses the flexibility of the SMC-PG-seqT to estimate a two state Markov switching SV model.

| SMC-PG-seqT | SMC-PG-seqNT | SMC-PG | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 5 | 10 | 15 | 25 | 5 | 10 | 15 | 25 | 5 | 10 | 15 | 25 | |

| std err. | 0.0100 | 0.0062 | 0.0058 | 0.0048 | 0.0094 | 0.0051 | 0.0081 | 0.0047 | 0.0040 | 0.0026 | 0.0025 | 0.0020 |

| std err. | 0.0006 | 0.0023 | 0.0014 | 0.0021 | 0.0007 | 0.0022 | 0.0018 | 0.0039 | 0.0003 | 0.0040 | 0.0010 | 0.0025 |

| std err. | 0.0011 | 0.0058 | 0.0027 | 0.0069 | 0.0009 | 0.0063 | 0.0034 | 0.0196 | 0.0004 | 0.0087 | 0.0028 | 0.0094 |

| mean | -1381.15 | -1431.94 | -1276.53 | -1348.71 | -1381.83 | -1457.13 | -1289.08 | -1459.16 | -1382.53 | -1432.79 | -1278.11 | -1349.54 |

| std err. | 0.3812 | 0.5907 | 0.3311 | 0.5871 | 0.5808 | 13.1455 | 7.2123 | 16.4654 | 0.1548 | 0.3069 | 0.3321 | 0.7661 |

5 The Multivariate Factor Stochastic Volatility Model

5.1 Model

The factor SV model is a parsimonious multivariate stochastic volatility model that is often used to model a vector of stock returns; see, for example, Chib et al., (2006) and Kastner et al., (2017). It is a high dimensional state space model having a large number of parameters and a large number of latent states.

Suppose that is a vector of daily stock prices and define as the vector of stock returns. We model as a factor SV model

| (10) |

where is a vector of latent factors (with ), and is a factor loading matrix of unknown parameters. The model for the latent factor is with . The time varying variance matrices and depend on the unobserved random variables and such that

Each of the log-volatilites and is assumed to follow an independent first order autoregressive process, with

| (11) |

and

| (12) |

For and , we choose the priors for the persistence parameters and , the priors , , and as in Section 4. For every unrestricted element of the factor loadings matrix , we follow Kastner et al., (2017) and choose independent Gaussian distributions . These priors cover most possible values in practice.

We also consider the factor stochastic volatility models, where the log-volatilities follow a continuous time Ornstein-Uhlenbeck (OU) process , introduced by Stein and Stein, (1991). The process satisfies,

| (13) |

where are independent Wiener processes. Although the continuous time OU diffusion model has a closed form transition density (Brix et al.,, 2018), we investigate the performance of the proposed SMC samplers to estimate state space models using an approximation such as the Euler discretisation.

The Euler scheme can be used as an approximation by placing evenly spaced points between times and . We denote the intermediate volatility components by and set and . The equation for the Euler evolution, starting at is

| (14) |

for , where . We use the following priors for the OU parameters and assume the parameters are independent apriori: (a) , (b) the priors for and are inverse Gamma with and , for . Section 14 of the Supplement discusses parameterisation and identification issues regarding the factor loading matrix and the latent factors .

Conditional Independence in the factor SV model

The key to making the estimation of the factor SV model tractable is that given the values of , the factor model in Eq. (10) separates into independent components consisting of univariate SV models for the latent factors with the th ‘observation’ of the th factor univariate SV model and univariate SV models for the idiosyncratic errors with the th ‘observation’ on the th idiosyncratic error SV model. Section 12 of the Supplement discusses the SMC-HMC, SMC-PG, and SMC-PHS methods for the factor SV model.

5.2 Examples

This section investigates the performance of the SMC samplers to estimate the multivariate factor SV model discussed in Section 5.1 using one factor. A sample of daily returns for value weighted industry portfolios is used, from December 11th, 2001 to 29th November 2005, a total of observations. The data is obtained from the Kenneth French website, with the industry portfolios used listed in Section 18 of the Supplement. As in Section 4.1, the PHS is regarded as the “gold standard”; it is run for iterates, with another iterates used as burn-in.

Our first study discusses how well SMC-PMMH-DF (Duan and Fulop,, 2015) estimates the factor SV model. SMC-PMMH-DF uses the PMMH Markov steps and follows the Pitt et al., (2012) guidelines to set the optimal number of particles in the particle filter to ensure that the variance of the log of the estimated likelihood is around . The PMMH Markov step generates the parameters of the latent factors, with the factor and idiosyncratic log-volatilities “integrated out”, resulting in a dimensional state vector. The tempered measurement density at the th stage is

Eq. (11) gives the state transition densities for the idiosyncratic log-volatilities () and Eq. (12) gives the state transition equations for the factor log-volatilities ().

Table 4 shows the variance of log of the estimated likelihood for different numbers of particles evaluated at posterior means of the parameters obtained using the PHS of Gunawan et al., 2020a with . It shows that even with particles, the PMMH Markov step would get stuck. Deligiannidis et al., (2018) proposed the correlated PMMH method and it is possible to implement it in the Markov move step instead of the standard PMMH method of Andrieu et al., (2010).

| Number of Particles | Variance of log of estimated likelihood | Time |

|---|---|---|

| 250 | 2198.72 | 4.86 |

| 500 | 1164.51 | 9.88 |

| 1000 | 813.53 | 20.13 |

| 2500 | 439.05 | 50.43 |

| 5000 | 345.85 | 99.24 |

The correlated PMMH correlates the random numbers used in constructing the estimators of the likelihood at current and proposed values of the parameters and sets the correlation very close to 1 to reduce the variance of the difference in the logs of estimated likelihoods at the current and proposed values of the parameters appearing in the Metropolis-Hastings (MH) acceptance ratio. Deligiannidis et al., (2018) show that the correlated PMMH can be much more efficient and can significantly reduce the number of particles required by the standard PMMH approach when the dimension of the latent states is small. However, the current example considers a high dimensional latent state vector in the one factor-Factor SV model. Mendes et al., (2020) found that it is very challenging to preserve the correlation between the logs of the estimated likelihoods for such a high dimensional state space model. The Markov move based on the correlated PMMH approach will also get stuck at lower temperatures unless enough particles are used to ensure the variance of the log of the estimated likelihood is around 1.

A second drawback of the PMMH Markov move step as in Duan and Fulop, (2015) is that the dimension of the parameter space in the factor SV model is large making it very hard to implement the PMMH Markov step efficiently. Section 4.1 shows that SMC-PG is much more efficient than SMC-PMMH-DF for estimating univariate SV model with covariates. It is difficult to obtain good proposals for the high-dimensional parameters because the first and second derivatives of log of the estimated likelihood with respect to the parameters are unavailable analytically and can only be estimated. Sherlock et al., (2015) note that in general it is even more difficult to obtain accurate estimate of the gradient of the log of the estimated likelihood than it is to obtain accurate estimates of the log of the estimated likelihood. Nemeth et al., (2016) and Mendes et al., (2020) found that the behaviour of particle Metropolis adjusted Langevin Algorithm depends critically on how accurately we can estimate the gradient of the log-posterior. If the variance of the gradient of the log-posterior is insufficiently small, then there is no advantage in using particle MALA over the random walk proposal. Table 4 shows that the variance of the log of the estimated likelihood is still very large, even with particles. Therefore, there is no advantage in using particle MALA. The random walk proposal is easy to implement, but it is very inefficient in high dimensions.

The second study compares PHS to the approximate MCMC sampler of Kastner et al., (2017) for estimating the factor SV model. Kastner et al., use the approach proposed by Kim et al., (1998) to approximate the distribution of innovations in the log outcomes by a mixture of normals. Kim et al., correct their approximation by importance sampling, which gives a simulation consistent estimation for the univariate SV model. However, the Kastner et al., estimator is not simulation consistent because it does not correct for these approximations for the factor SV model. The PHS is simulation consistent in the sense that as the number of samples of the parameters and latent states tends to infinity, the PHS estimates converge to their true posterior distributions. We implement the MCMC of Kastner et al., using the R package factorstochvol (Hosszejni and Kastner,, 2019), using the default priors in the R package factorstochvol in the comparison. The priors for for and for are gamma density with shape and scale . The prior for for is . We use the priors given in Section 5.1 for the other parameters.

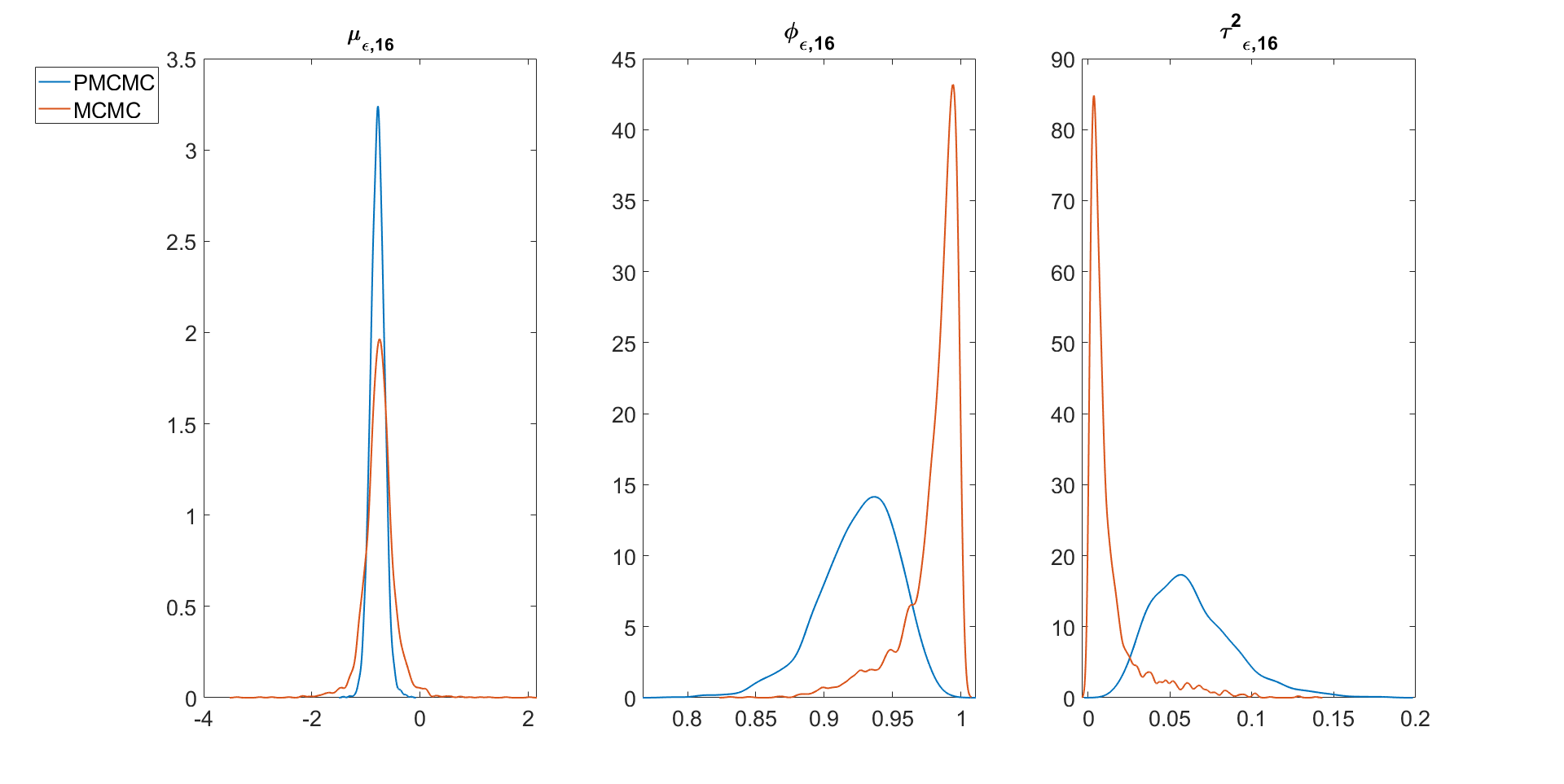

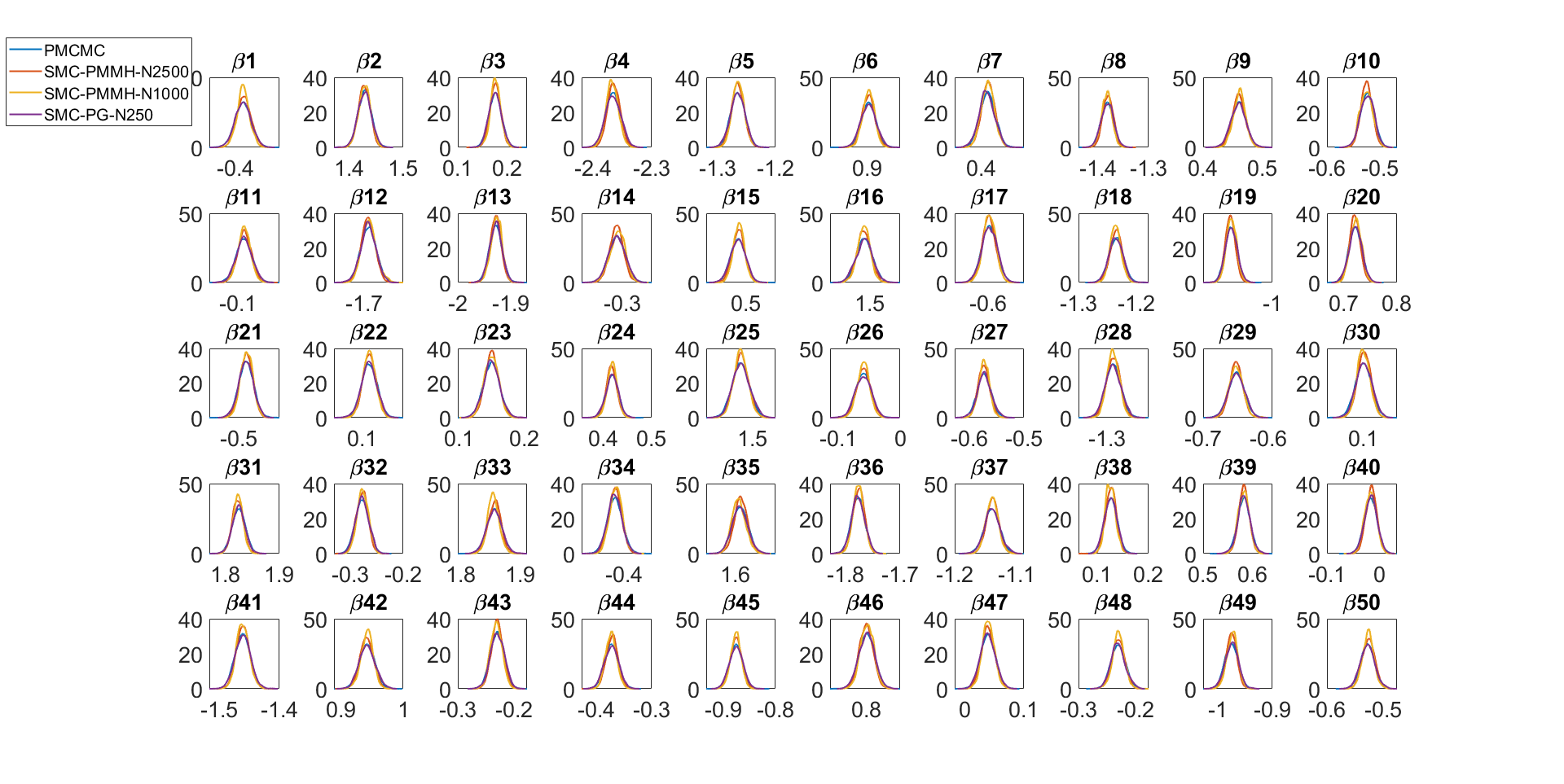

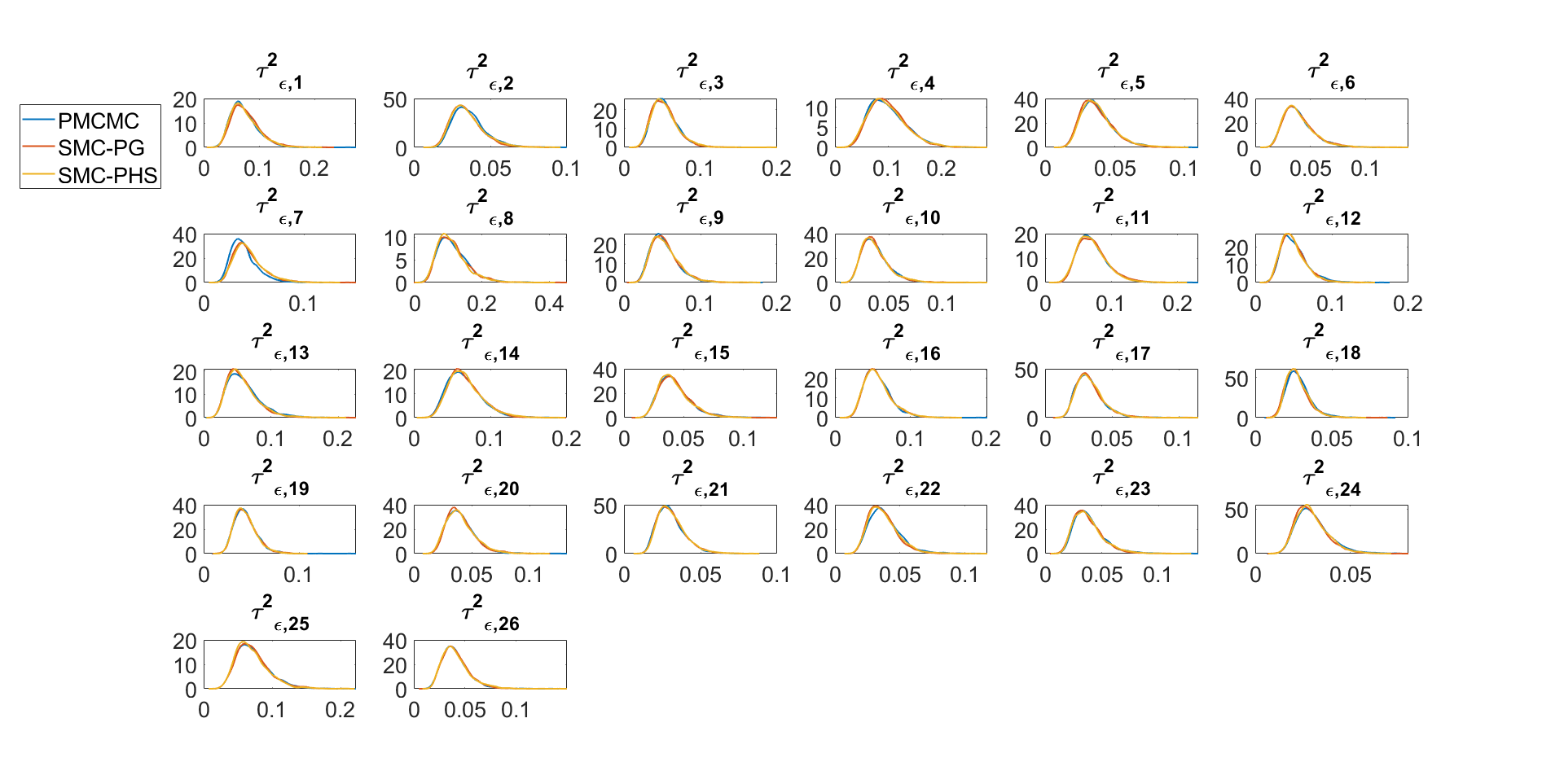

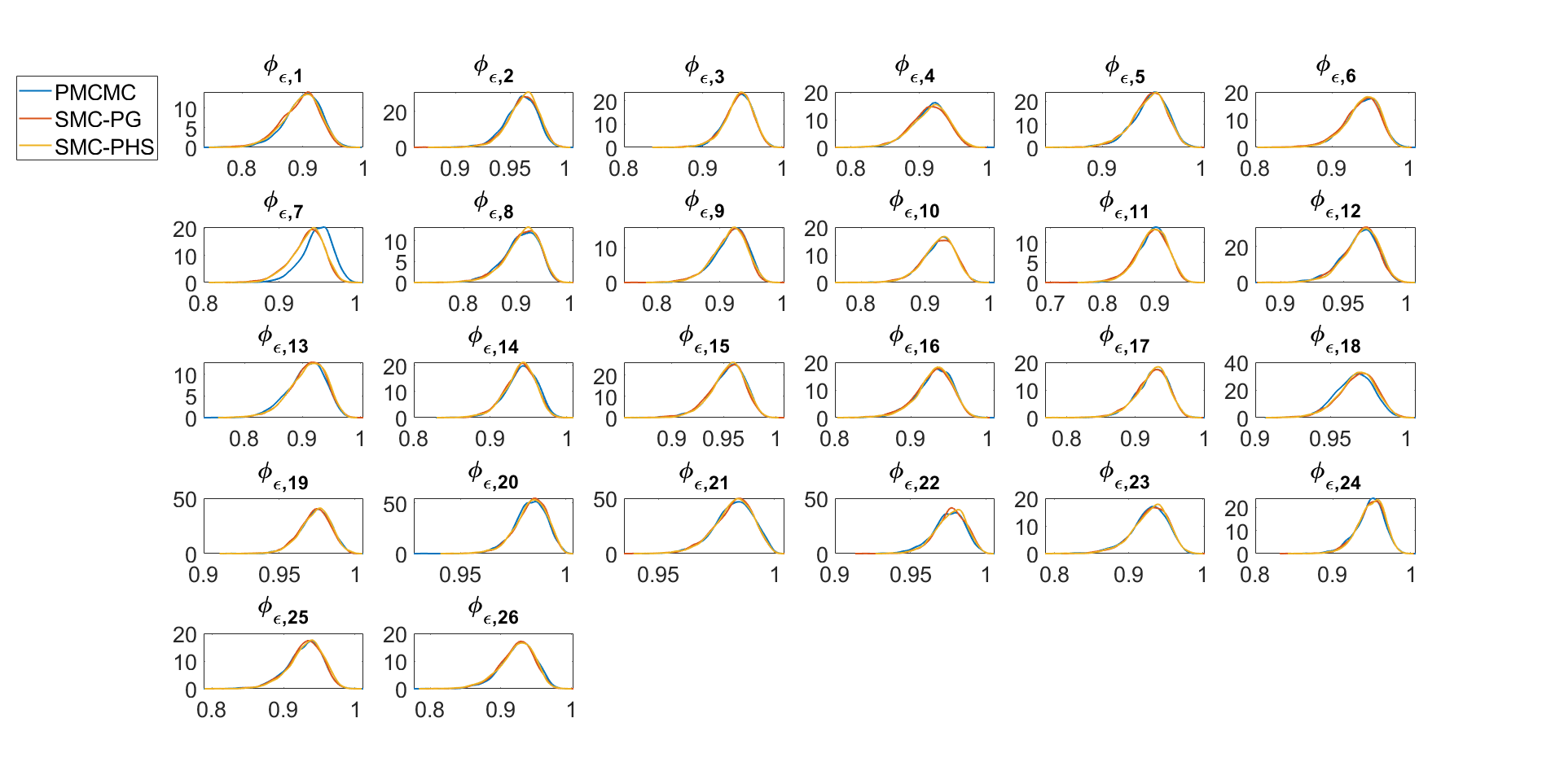

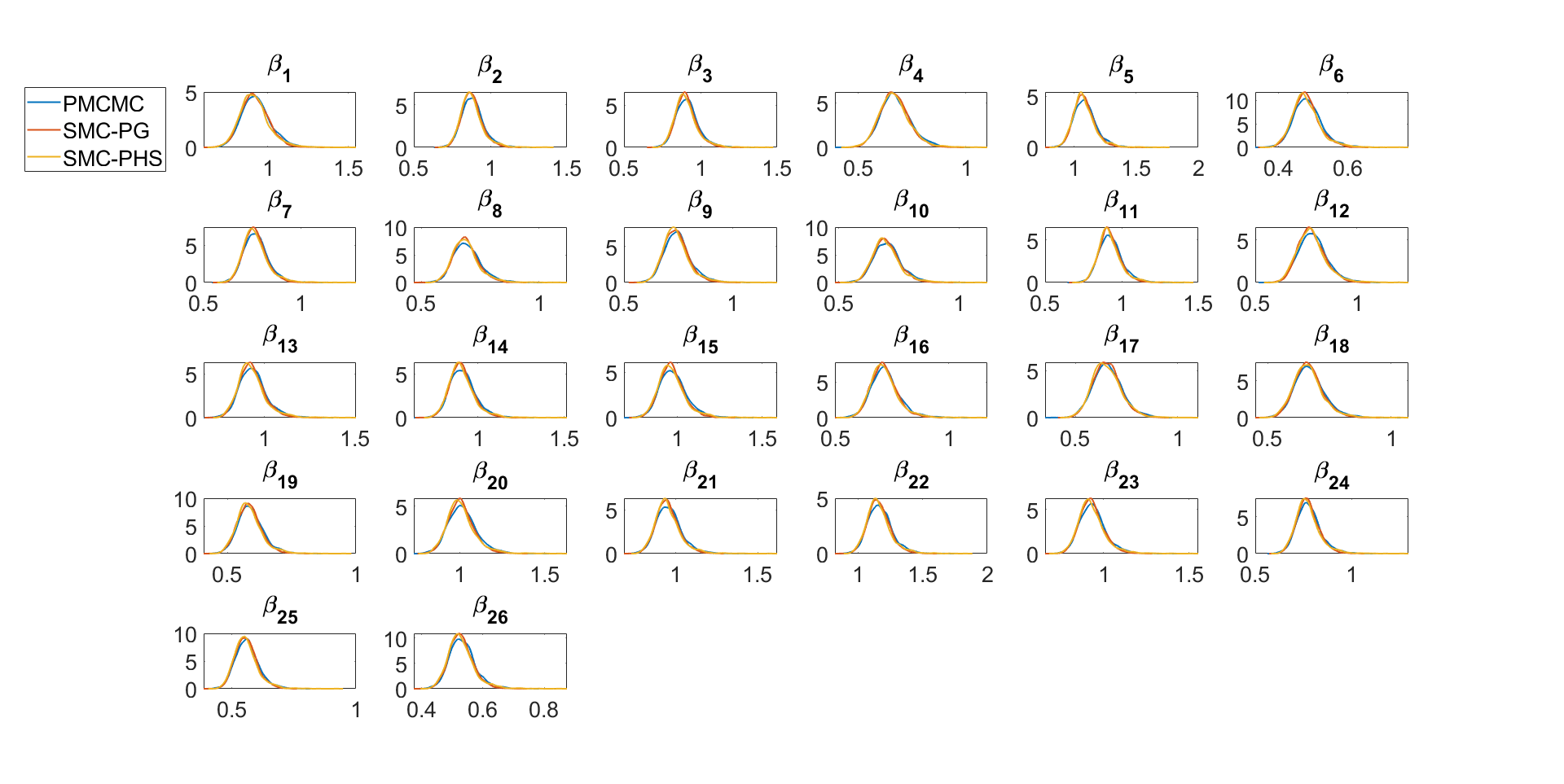

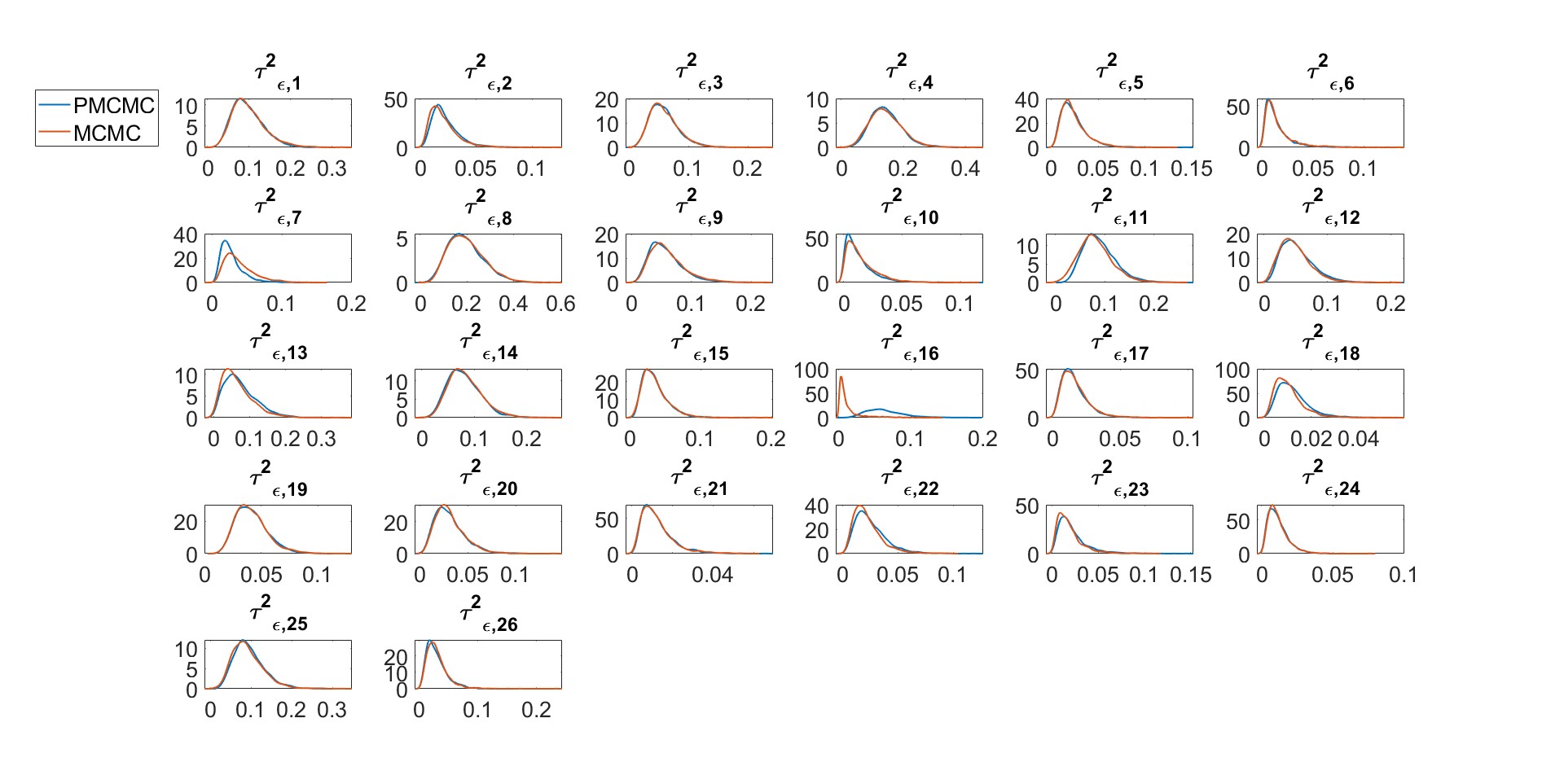

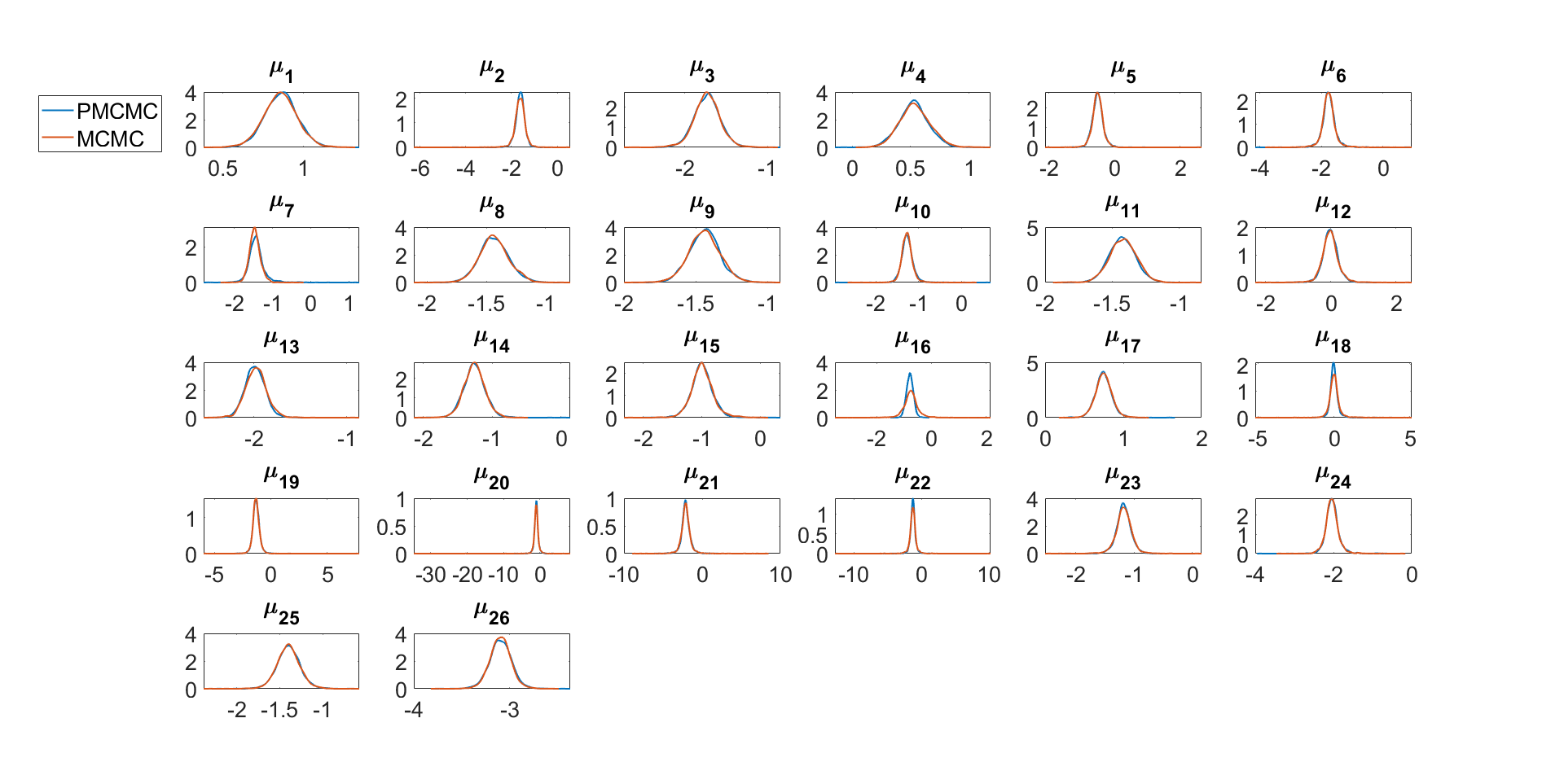

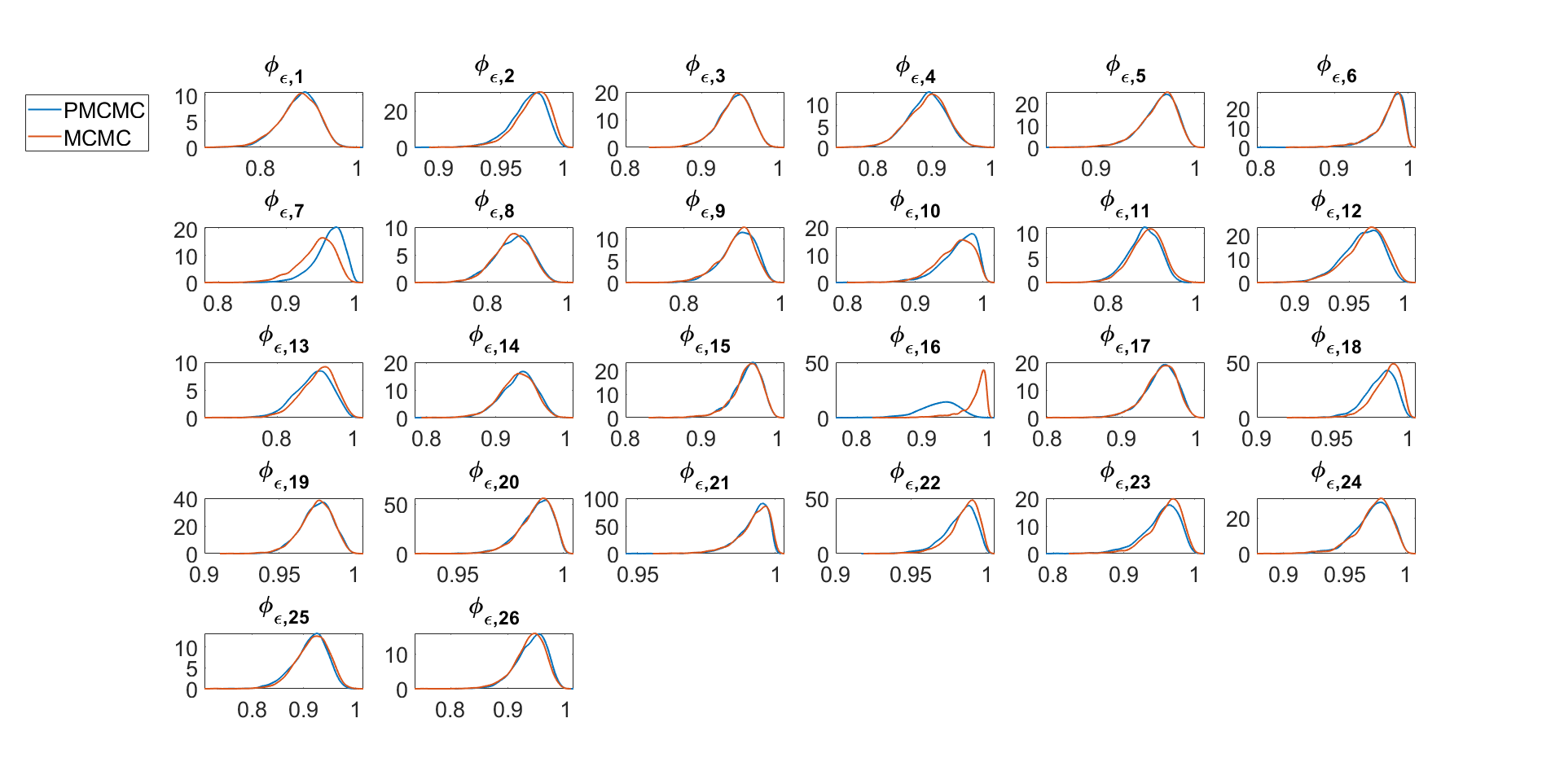

Fig. 6 shows the marginal posterior density estimates of the parameters , , and of the factor SV model using PMCMC (PHS) and the MCMC sampler of Kastner et al.,. The figure shows that the MCMC sampler gives different estimates to PHS. Figures 23 to 26 of Section 19 of the Supplement give results for the other parameters in the factor SV model. The figures show that although some of the parameters estimated using the MCMC Kastner et al., sampler are close to the PHS, some others are quite different. In addition, the Gibbs type MCMC sampler as in Kastner et al., cannot handle the factor SV with the log-volatility following diffusion processes discussed in Section 5.3. It is well known that the Gibbs sampler is inefficient for generating parameters for a diffusion model, in particular the variance parameter (Stramer and Bognar,, 2011).

The third study investigates the performance of the SMC-PG and SMC-PHS methods and compares them to the PHS. The SMC estimates are obtained using 10 independent runs with samples to generate a total of samples for each algorithm. For the SMC methods, . The computation is done using a Matlab implementation of the algorithms and 28 CPU-cores of a high performance computer cluster.

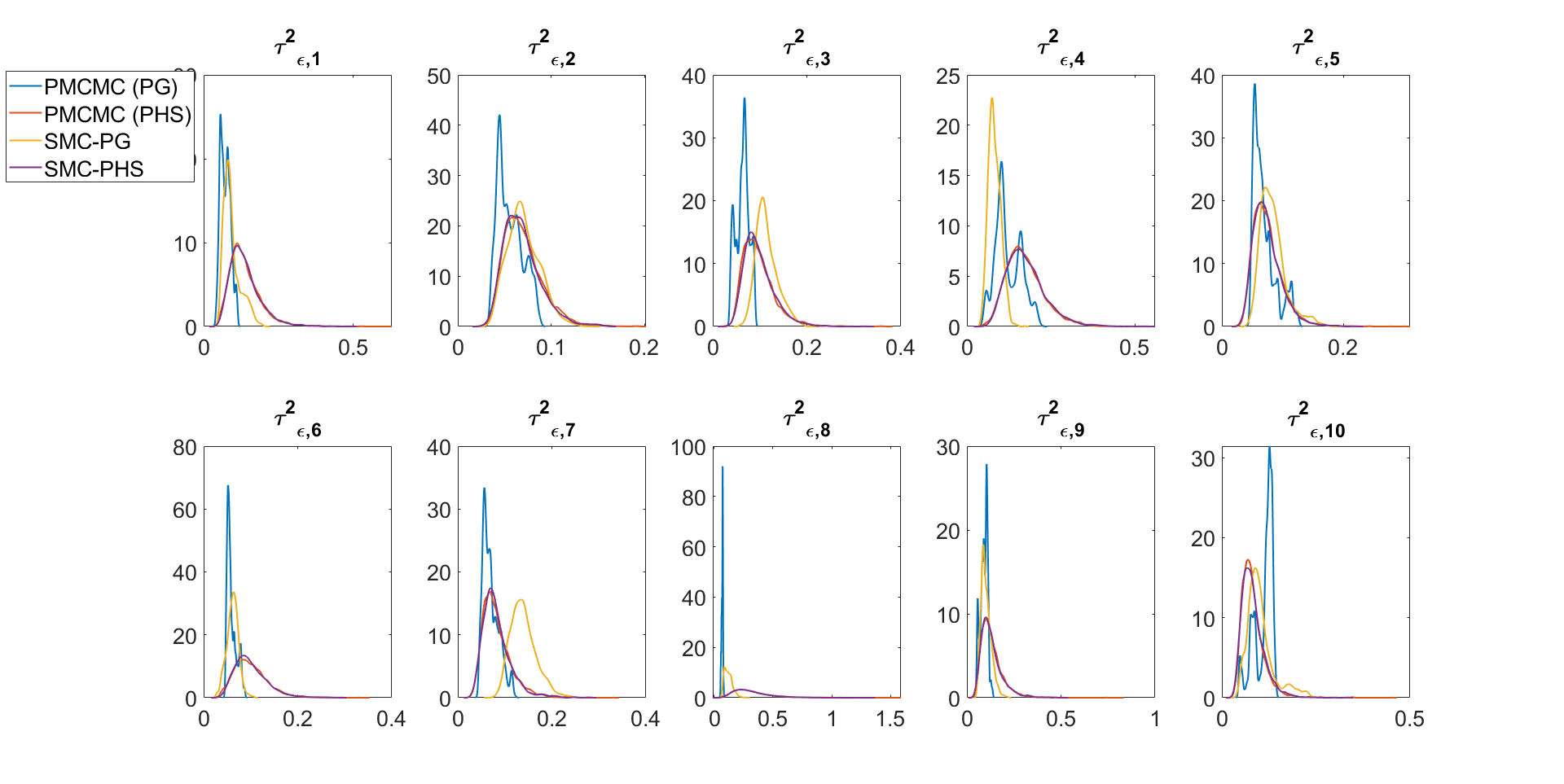

We use the following notation: means sampling using the SMC-PG method; means sampling in the PMMH step in Part 1 of Algorithm 5 and in the PG step. The strategy for the SMC-PHS method is to generate parameters that are subject to slow convergence using a PMMH step and the rest of the parameters are generated conditional on the states using PG steps. We first run the particle Gibbs (PMCMC) sampling algorithm for all the parameters to identify which parameters have convergence issues. We then generate these parameters in the PMMH step in SMC-PHS algorithm. Gunawan et al., 2020a find that the particle Gibbs sampler usually generates the variance parameters in the state transition equation inefficiently, i.e., for and for . We compare the following methods: (I) the SMC-PHS , (II) the , (III) PHS .

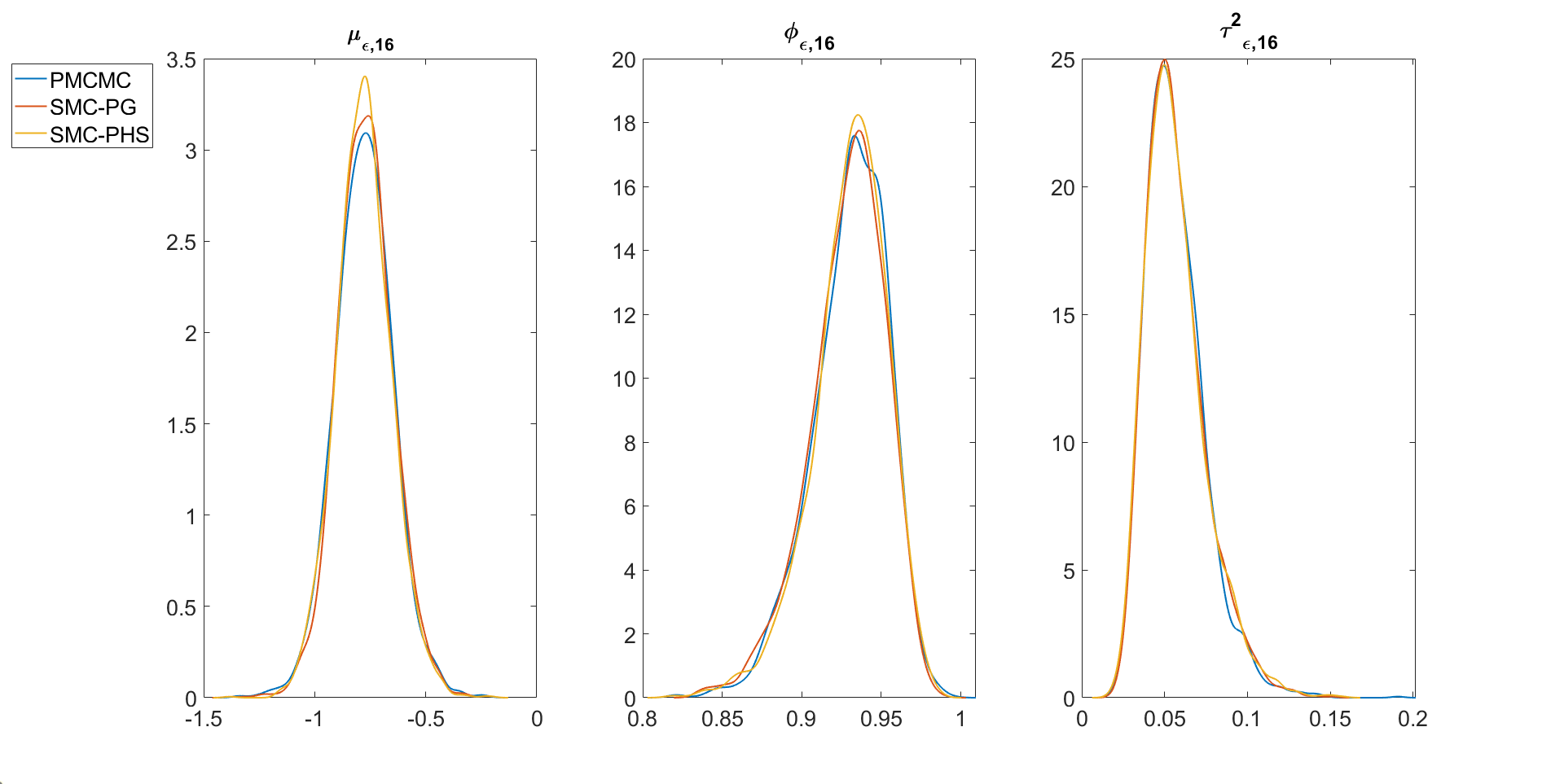

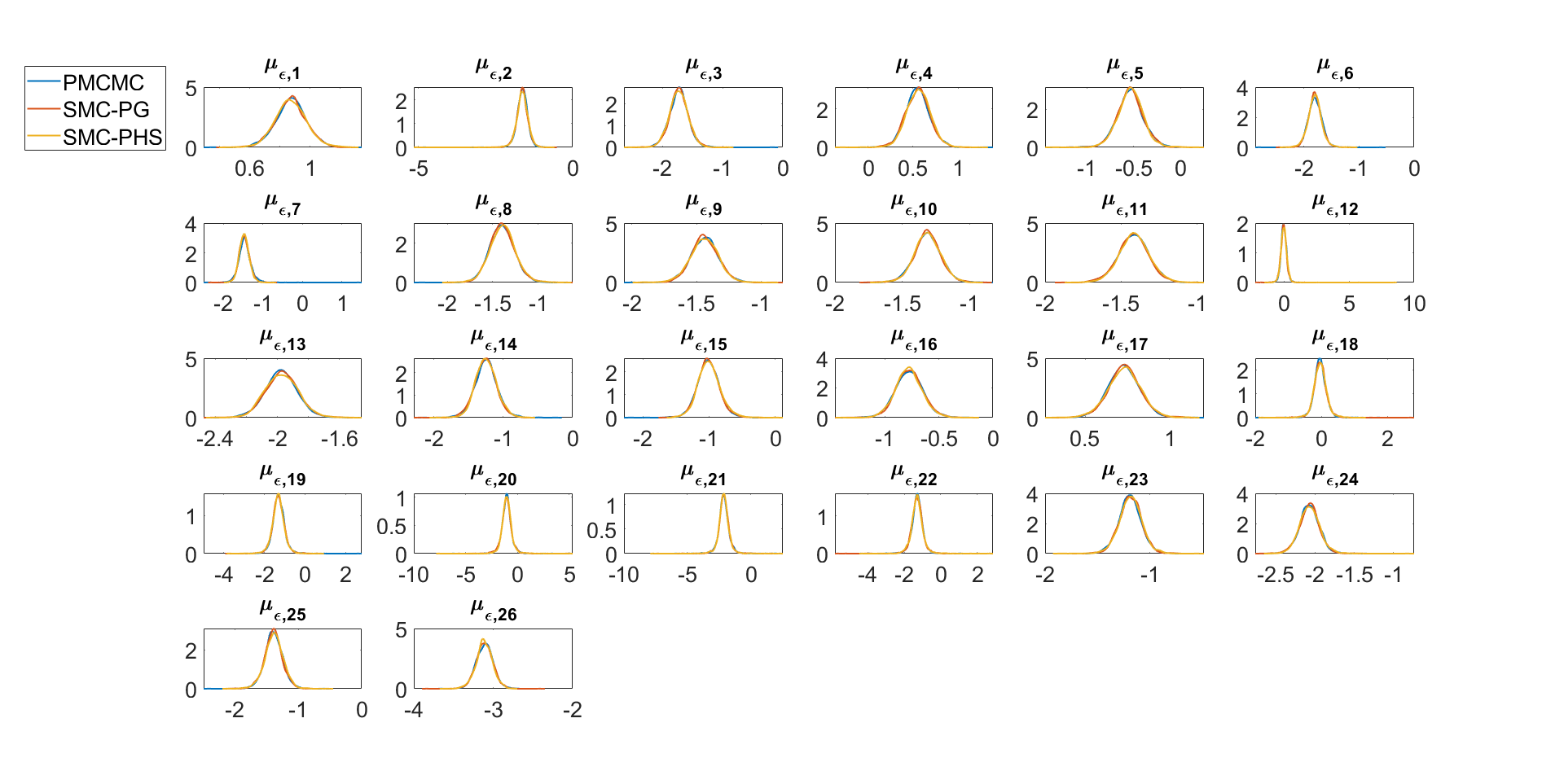

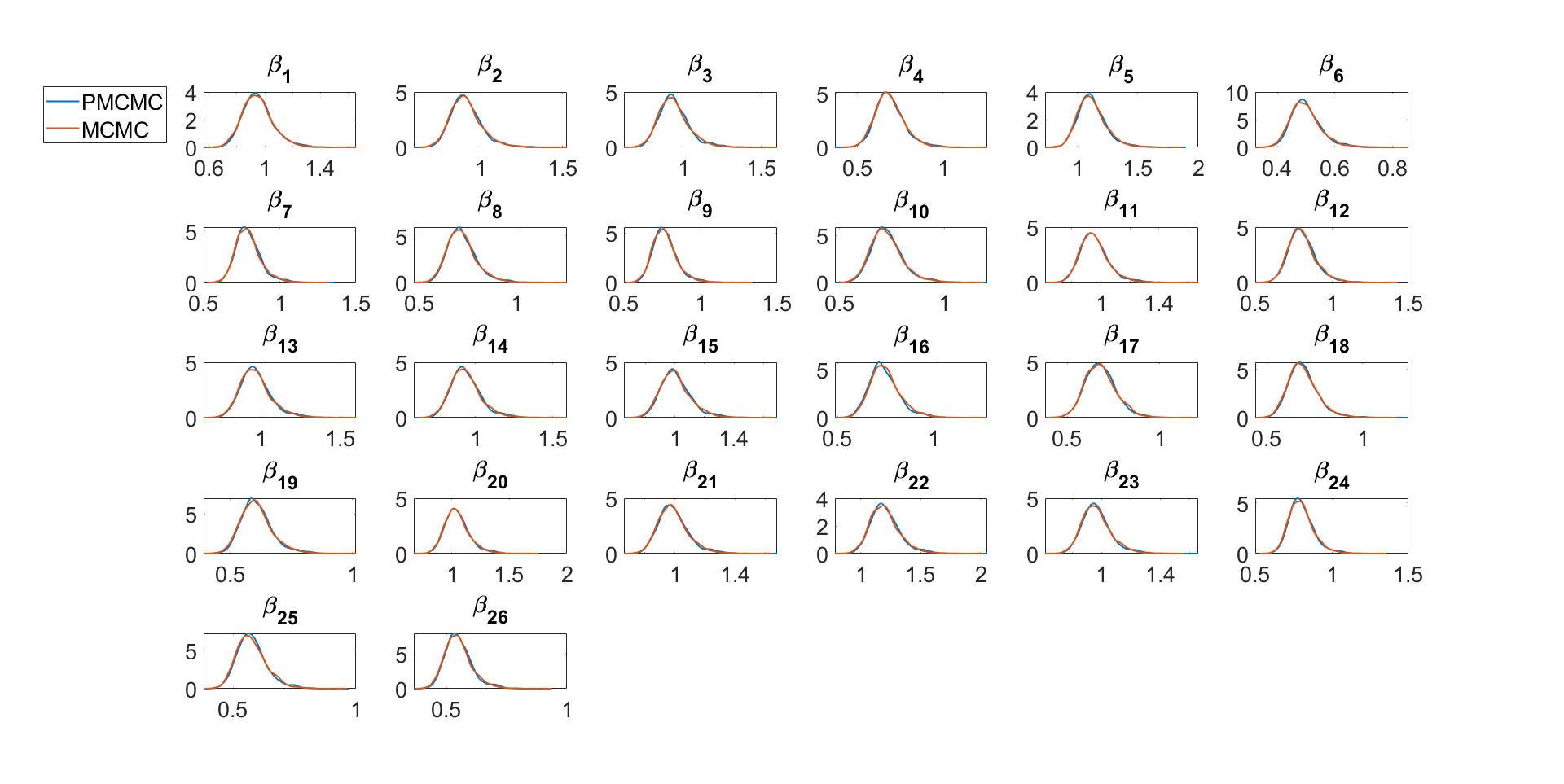

Fig. 7 plots the marginal posterior density estimates of the parameters , , and of the factor SV model estimated using PMCMC (PHS), SMC-PG and SMC-PHS. The figure shows that the SMC-PG and SMC-PHS methods give the same estimates as PHS, with SMC-PG slightly more accurate at estimating . Figures 19 to 22 in the Supplement show all the other parameters of the factor SV model. In general, the SMC-PG and SMC-PHS estimates are very close to the PHS estimates for all parameters. Table 5 shows the estimates of the log of the marginal likelihood for the one factor model estimated using the SMC-PHS and SMC-PG methods. The table shows that the estimated standard errors of the estimates of the log of the marginal likelihood estimated using SMC-PHS are 1.87 times bigger than for the SMC-PG methods. The standard errors can be reduced by increasing the number of SMC samples and setting the . The table also shows that the number of annealing steps of SMC-PG and SMC-PHS methods are comparable. The Markov move based on the PHS is computationally more expensive than the Markov move based on PG only because it is necessary to run the particle filter twice at each iteration.

We now compare the predictive performance of the SMC-PG and SMC-PHS methods with the (exact) PHS. The minimum variance portfolio implied by the step-ahead time-varying covariance matrix , is considered; it can be used to uniquely define the optimal portfolio weights (Bodnar et al.,, 2017),

where denotes an S-variate vector of ones. The optimal portfolio weights give the lowest possible risk for a given expected portfolio return.

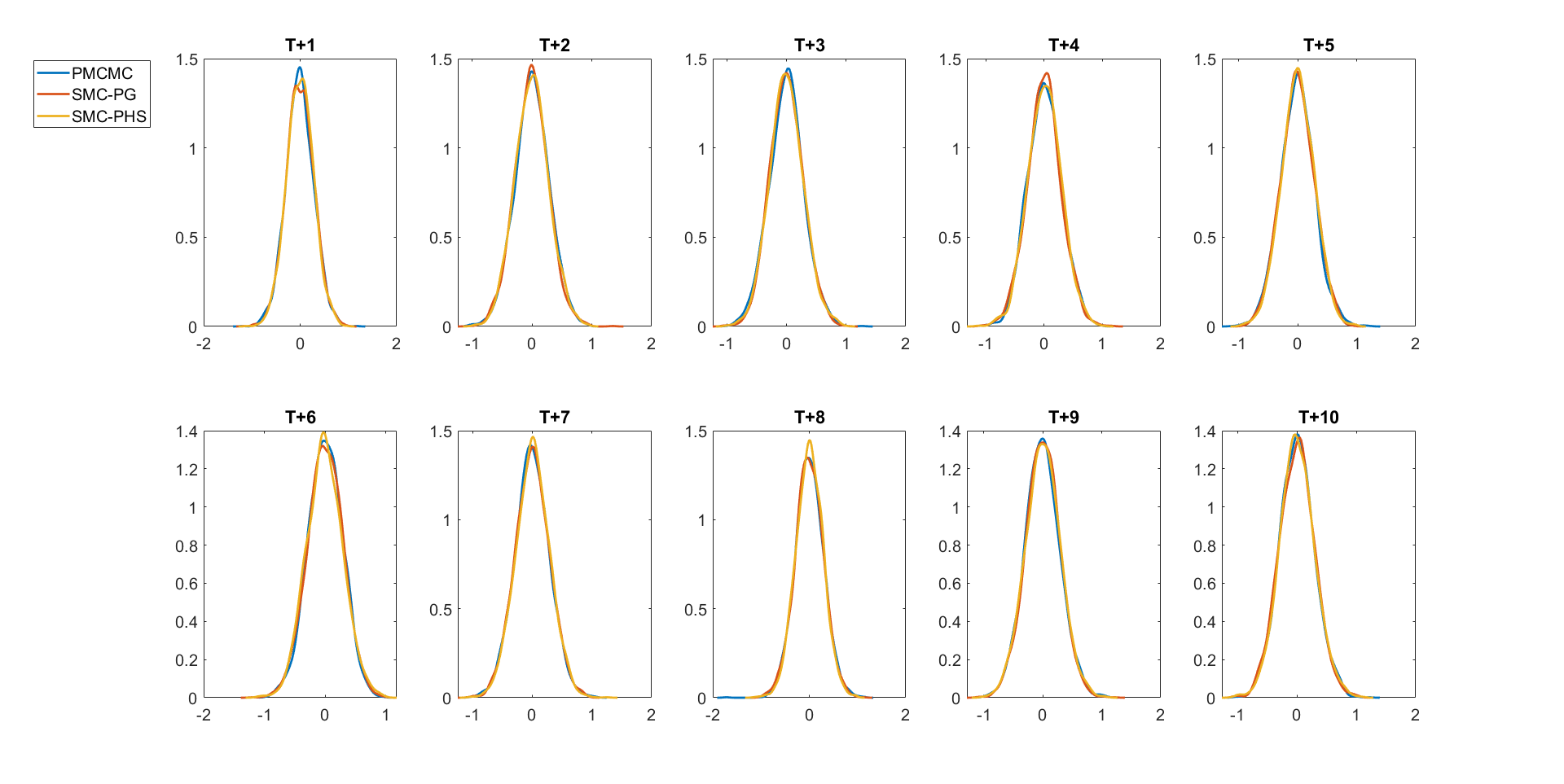

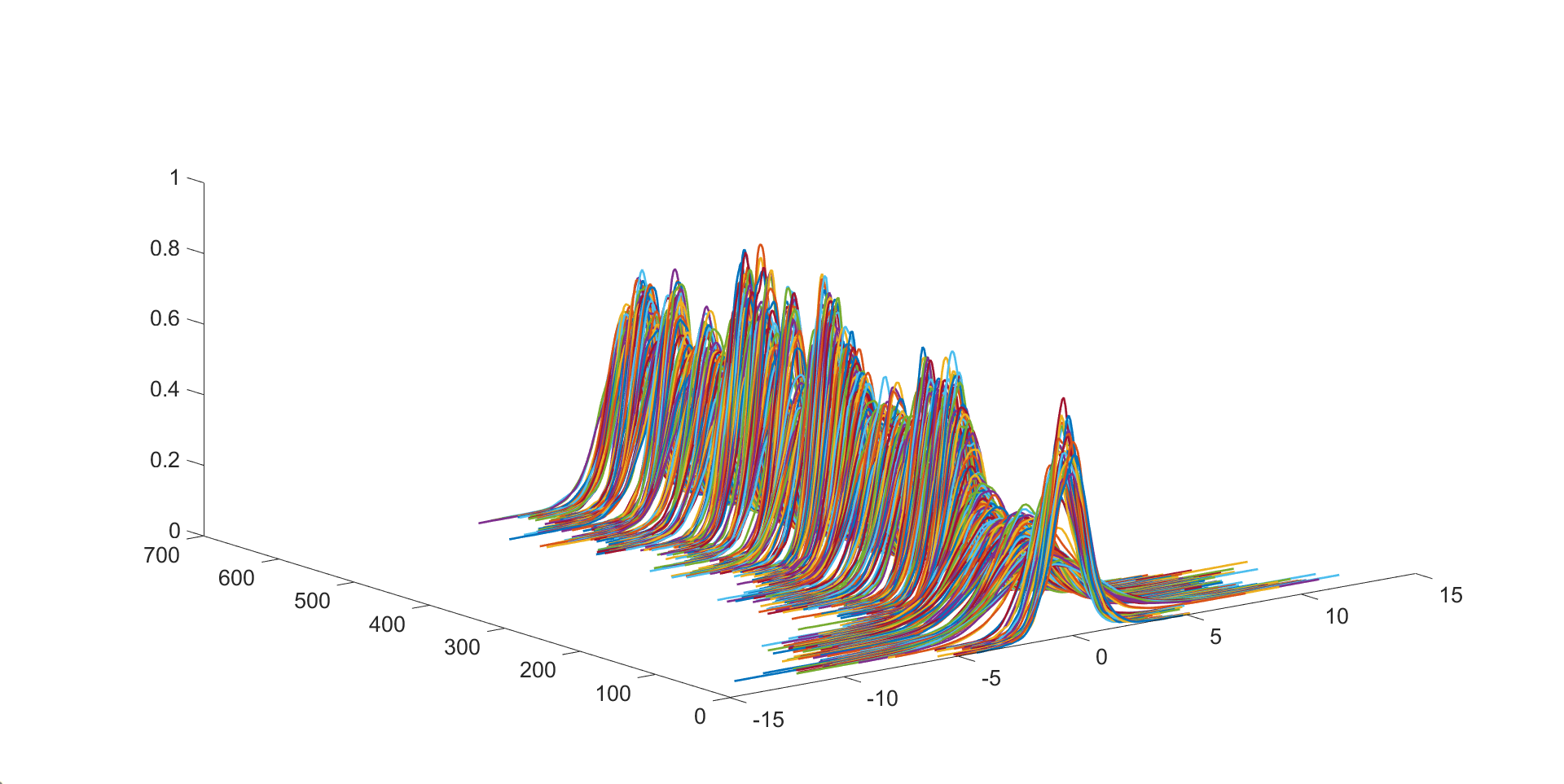

Figure 8 shows the multiple-step ahead predictive densities of an optimally weighted combination of all series, for obtained using SMC-PG, SMC-PHS, and PHS. The figure shows that the predictive densities obtained using SMC-PG method are very close to the exact predictive densities obtained from the PHS. The predictive densities obtained using SMC-PHS are slightly less accurate. Section 19 of the Supplement give additional empirical results for the factor SV model.

This example suggests that: (a) the PMMH Markov move is expensive for the factor SV model, as it requires the number of particles to be greater than ; (b) the PMMH Markov move is unsuitable for the factor SV model because the dimension of the parameter space in the factor SV model is large; (c) the approximate MCMC method of Kastner et al., can give unreliable estimates for some parameters in the factor SV model; (d) for the standard factor SV model, SMC-PG is faster and slightly more accurate than SMC-PHS in estimating the posterior densities of the factor SV parameters and the predictive densities.

| Method | N | R | P | Time | |

|---|---|---|---|---|---|

| SMC-PG | 250 | 10 | 289 | 2307.38 | |

| SMC-PHS | 250 | 10 | 274 | 6003.34 |

5.3 Factor SV Model with the Ornstein-Uhlenbeck Diffusion Processes

This section considers the factor stochastic volatility model, where the log-volatilities of the factors follow a standard SV model and the idiosyncratic log-volatilities follow a continuous time Ornstein-Uhlenbeck (OU) process (Stein and Stein,, 1991). Although the continuous time OU diffusion model has a closed form transition density (Brix et al.,, 2018), this section investigates the performance of SMC-PG and SMC-PHS when estimating the state space model using an approximation such as the Euler discretisation. For this example, we use the first daily portfolio returns listed in Section 18 of the Supplement, from December 11th, 2001 to 29th November 2005, a total of observations.

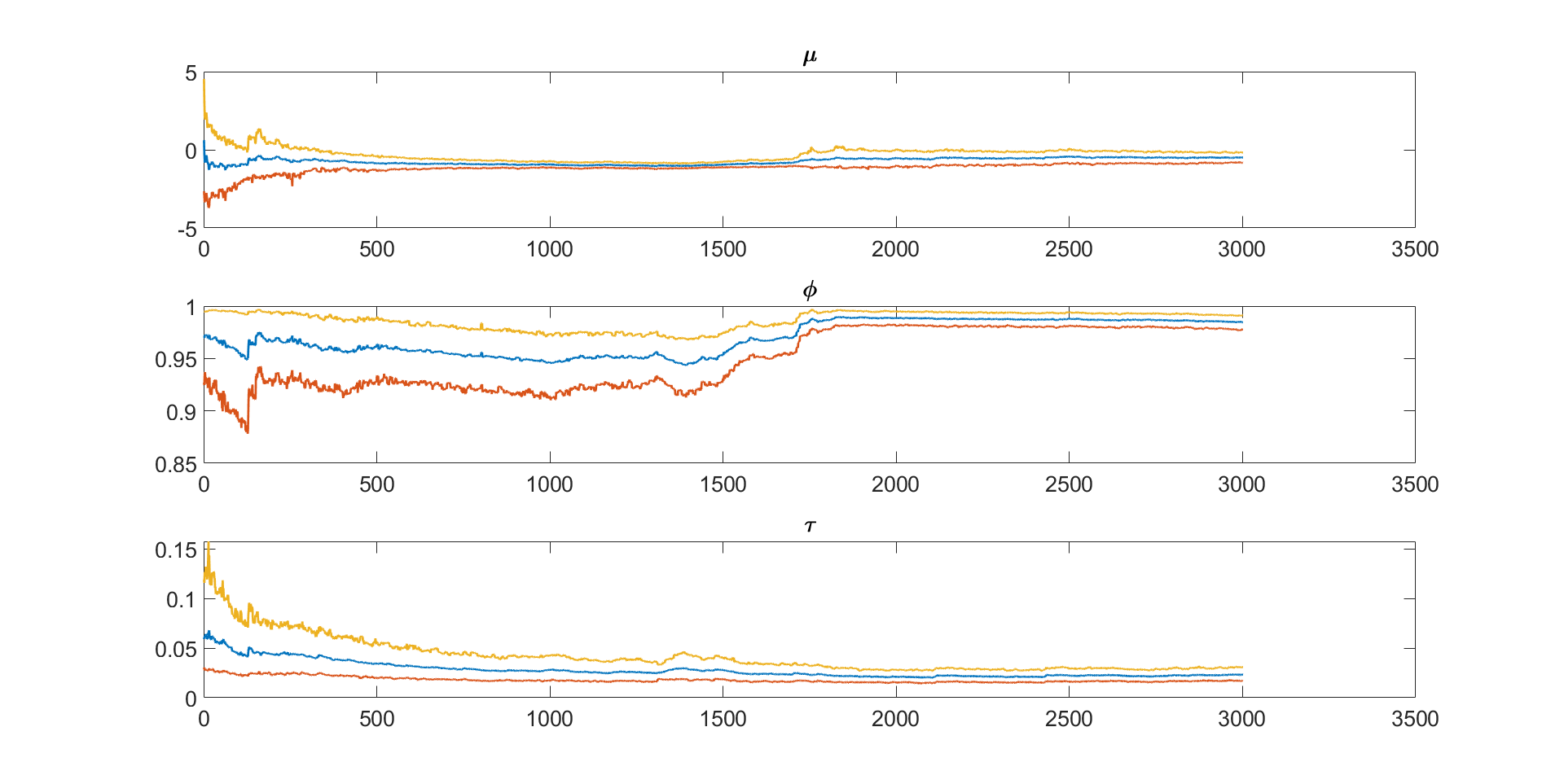

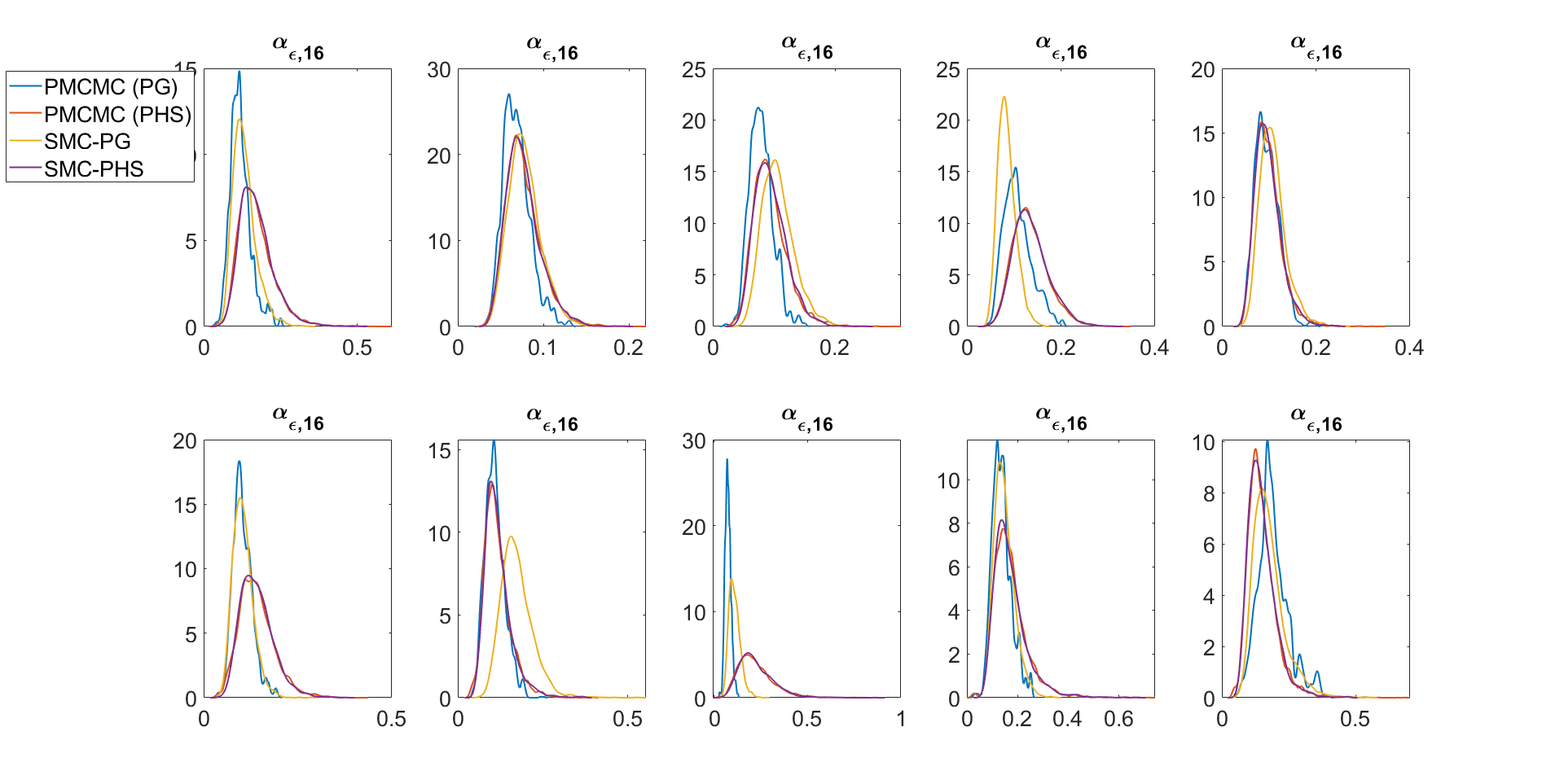

Fig. 9 shows the trace plots of the parameters , , and of the factor SV model, where the idiosyncratic log-volatilities follow OU processes and the factor log-volatilities follow the standard SV model estimated using particle Gibbs. The figure shows that the posterior draws of and are highly autocorrelated and fail to converge. We estimate all the OU parameters in the PMMH steps in PHS and SMC-PHS. We compare the following samplers: (I) the SMC-PHS , (II) the , (III) PHS , and (IV) the . The PG and PHS are run for 20000 iterates with another 5000 iterates used as burn-in.

Fig. 10 shows the marginal posterior density plots of the parameters of the factor SV models, where the idiosyncratic errors follow OU processes estimated using the PHS, PG, SMC-PG, and SMC-PHS methods. The figure shows that the PG and SMC-PG estimates are very different to PHS. SMC-PHS gives the same estimates as PHS. Similar observations hold for the parameters in Fig. 27 of Section 19 of the Supplement. This example suggests that: (a) The SMC-PG estimates for the model parameters are unreliable and are highly correlated with the states. (b) The SMC-PHS estimates are accurate as they generate the parameters that are highly correlated with the states using PMMH steps, and the other parameters are generated using PG steps.

6 Conclusions

The paper proposes flexible SMC approaches that can be used for both batch and sequential state and parameter estimation problems, and which also lead to accurate one-step and multiple-step ahead predictions. The approaches are based on Markov move steps that are more efficient than in previous SMC approaches in Duan and Fulop, (2015), Fulop and Li, (2013), and Chopin et al., (2013). We show that the methods work well for both simulated and real data and can handle higher-dimensional states and parameters than previously possible by current SMC approaches. The data analyses suggest that (a) SMC-PG gives parameter and states estimates close to PHS for both univariate and standard factor SV models. It also accurately estimates the predictive densities of individual stock returns and the minimum variance portfolio. (b) SMC-PG gives inaccurate parameter estimates for and for the factor SV model with the idiosyncratic log-volatilities following OU processes. This is because the OU parameters, in particular, the and are highly correlated with the states. (c) SMC-PHS provides flexible Markov move steps, where the parameters that are highly correlated with the states are generated by PMMH and all other parameters are generated by PG steps conditioning on the states. Section 5.3 shows that the SMC-PHS gives accurate estimates for the OU parameters. (d) The SMC-PMMH-DF of Duan and Fulop, (2015) cannot handle state space models with a large number of parameters and states. Section 5.2 gives further details. (e) The MCMC sampler of Kastner et al., (2017) gives similar results to the PHS for most of the factor SV parameters, but some parameter estimates are different. The Gibbs type MCMC sampler as in Kastner et al., (2017) cannot handle the factor SV with the log-volatility following diffusion processes. (f) The sequential SMC approach allows us to efficiently estimate the sequence of standard normal random variables used to form the goodness of fit statistics to test for the adequacy of a general time series state space model. (g) The sequential approach with tempering provides joint sequential inference for states and parameters and is more robust than the sequential approach without tempering.

7 Acknowledgement

We thank the AE and the four reviewers for their comments which improved both the presentation and the technical content of the paper.

8 Supplementary Material

This article has an online supplement that contains additional technical details and empirical results.

Online Supplement: Robust Particle Density Tempering for State Space Models

We use the following notation in the supplement. Eq. (1), Alg. 1, and Sampling Scheme 1, etc, refer to the main paper, while Eq. (S1), Alg. S1, and Sampling Scheme S1, etc, refer to the supplement.

9 Markov move steps for the univariate SV model

9.1 Sampling the latent volatilities using Hamiltonian Monte Carlo

For the univariate SV model Eq. (1), we need the gradient of the log-likelihood with respect to each of the latent volatilities. The required gradient for is

the gradient for is

and, for , the gradient is

9.2 Sampling the Univariate SV parameters

For , we sample from truncated to , where

and

We sample the persistence parameter by drawing a proposed value from truncated within , where

and

and accept with probability

We sample from , where and .

10 Additional Results for univariate SV models

The terms SMC-PG, SMC-PG-seq, and SMC-PG-batch-seq for SMC-PG denote batch estimation, sequential estimation, and a combination of batch and sequential estimation, respectively. For the SMC-PG-batch-seq method, batch estimation is used for the first 80% of the data and sequential estimation is used for the rest.

Fig. 11 presents the sequential parameter learning in the univariate SV model estimated using SMC-PG-seq. Clearly, all parameter estimates vary a lot at the start when the number of observations is small, then stabilise as the number of observations gets larger. This sequential approach can take into account impacts of parameter and model uncertainties on decision-making over time.

Another important advantage of SMC-PG-batch-seq is that it provides sequential one-step and multi-step ahead predictive densities of the future observations .

Fig. 12 shows the sequential one-step ahead predictive density for log-return of the US food industry from 22/06/2011 to 11/11/2013 estimated using the SMC-PG-batch-seq method. Financial risk measures such as value at risk (VaR) can be computed from the one step ahead predictive densities. The VaR is the most widely used measure of market risk (Holton,, 2003). The -period -VaR of a return series, denoted as , is defined by

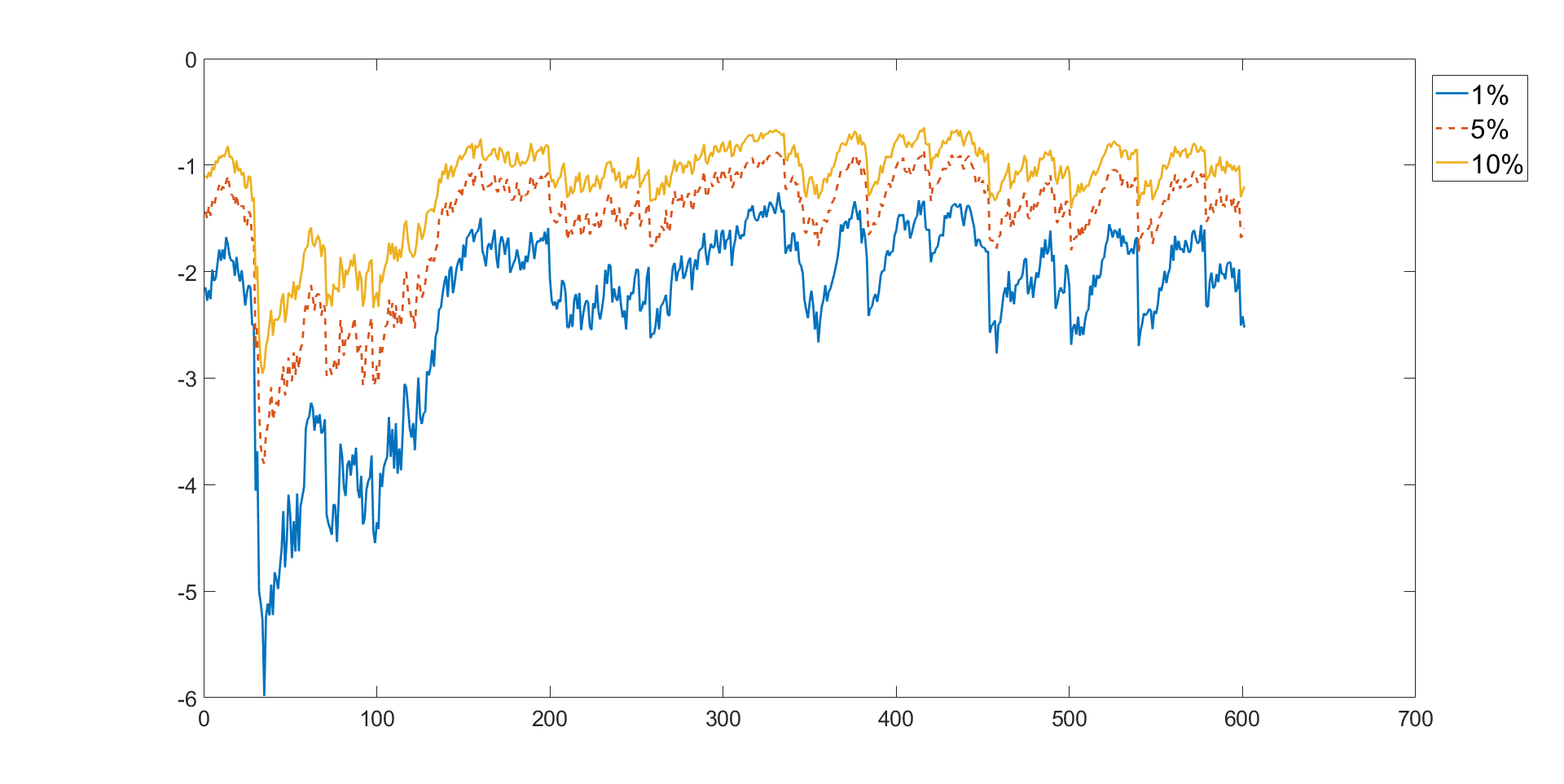

where is the information available to time . The one-step ahead -VaR, , can be estimated using the th-quantile of the posterior predictive return distribution at time given the information up to time . Fig. 13 shows the sequential one-step ahead VaR estimates at risk levels , , and for the log return of the US food industry from 22/06/2011 to 11/11/2013. The lowest VaR estimates are between 08/08/2011 to 18/08/2011 obtained using the SMC-PG-batch-seq method.

Figure 14 shows that the SMC-PG estimates are very close to the PHS estimates for all the covariate coefficients. The SMC-PMMH-DF based estimates differ from the PHS estimates even with particles. SMC-PMMH-DF uses a PMMH approach with random walk proposal for the parameters in the Markov move component. The random walk is easy to implement, but is not efficient for high-dimensional parameters.

10.1 Additional results for the SV model with outliers

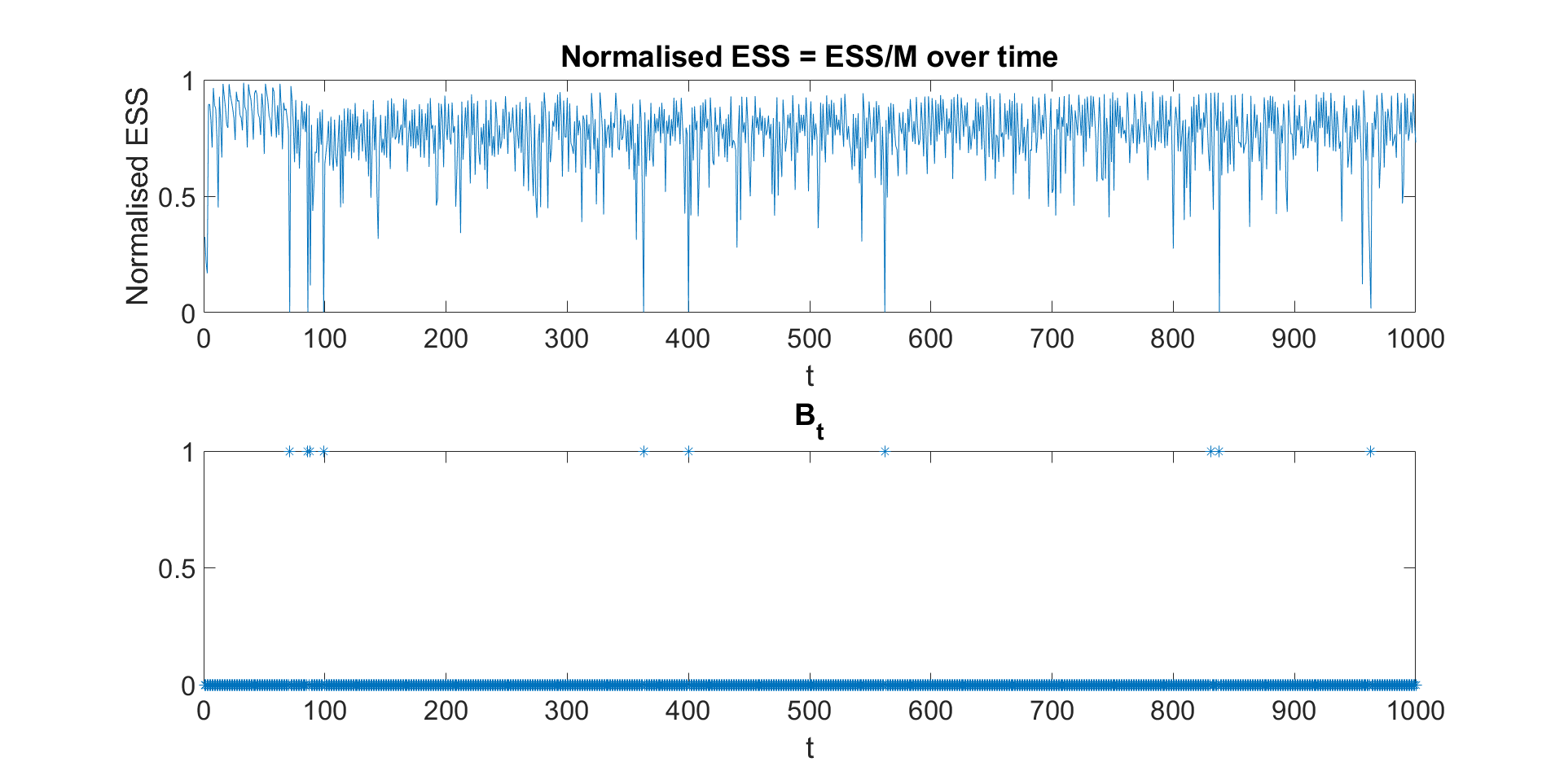

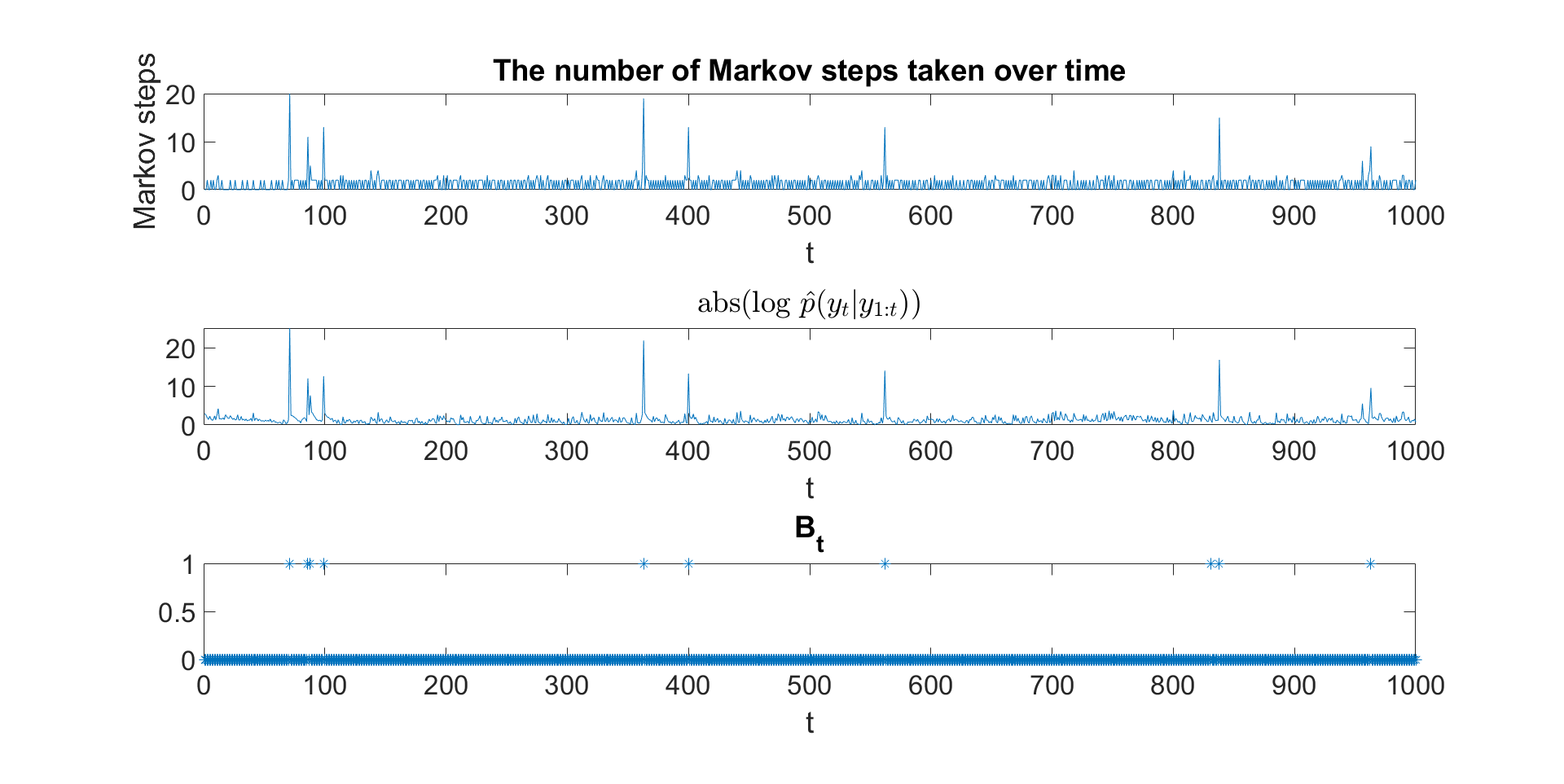

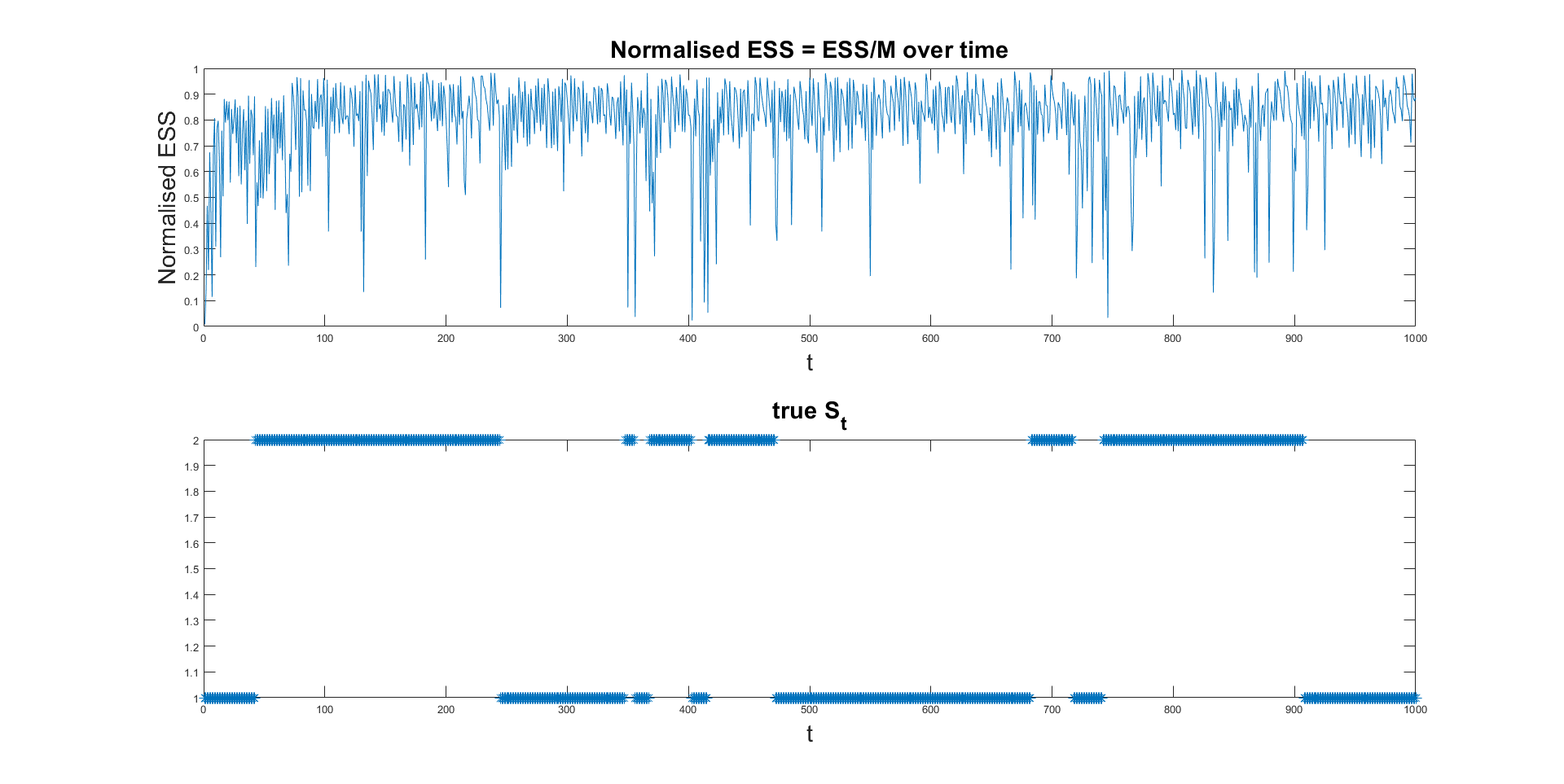

Fig. 15 shows the normalised ESS over time obtained from a run of SMC-PG-seqNT for the SV model with . The normalised ESS is close to zero when the data point is the outlier. This suggests that SMC-PG-seqT is more stable than the SMC-PG-seqNT, as it ensures the ESS stays close to . Fig. 16 (top panel) shows the number of Markov steps over time obtained from a run of SMC-PG-seqT algorithm.

The top panel of Fig. 16 shows that a larger number of Markov move steps are taken when the data is an outlier. The middle panel of Fig. 16 shows the absolute value of the log of for . This figure can be used to identify outliers in the data by investigating the unusually large absolute value of the log of for .

10.2 Markov Switching Stochastic Volatility Models

This section demonstrates the flexibility of SMC-PG-seqT by applying it to the two state Markov switching SV model

, , , and indicates that is from regime . This model is similar to that in Chib, (1998).

The one-step ahead transition probability matrix for is

where is the probability of moving from regime at time to regime at time . The prior for and is ; the prior and is . The same priors as in Section 4 are used for the other SV parameters.

We compare the performance of SMC-PG-seqT to SMC-PG-seqNT and SMC-PG for this model. A dataset is generated with observations using parameter values , , , , , and for . The SMC-PG method is used as the “gold standard” to assess the accuracy of the SMC-PG-seqT and SMC-PG-seqNT. All the SMC estimates are obtained using 10 independent runs, each with samples. For the SMC-PG and SMC-PG-seqT, the is set to .

Table 6 summarizes the simulation results for the Markov switching SV model. The first seven rows report the standard errors of the posterior mean estimates of the model parameters over the 10 runs; the eighth and ninth rows report the mean and standard error of the log of the marginal likelihood estimates. In general, the standard error of the posterior mean estimates obtained by SMC-PG-seqT and SMC-PG is smaller than SMC-PG-seqNT. The standard error of the log of the marginal likelihood estimates from PG-seqNT is about 3 times larger than from SMC-PG-seqT and SMC-PG. Fig. 17 shows the normalised ESS over time obtained from a run of PG-seqNT algorithm. Clearly, the normalised ESS is quite small when the state changes from 1 to 2 or from 2 to 1.

| SMC-PG-seqT | SMC-PG-seqNT | SMC-PG | |

| std err. | 0.0013 | 0.0013 | 0.0008 |

| std err. | 0.0015 | 0.0025 | 0.0013 |

| std err. | 0.0003 | 0.0003 | 0.0001 |

| std err. | 0.0004 | 0.0002 | 0.0003 |

| std err. | 0.0084 | 0.0066 | 0.0033 |

| std err. | 0.0007 | 0.0008 | 0.0004 |

| std err. | 0.0005 | 0.0005 | 0.0005 |

| mean | |||

| std err. | 0.5100 | 1.5235 | 0.5071 |

11 Augmented Target Density for SMC-PG

Similarly to Andrieu et al., (2010), the SMC-PG constructs a sequence of tempered densities , , based on the following augmented target density

| (15) | ||||

The next lemma shows that the marginal distribution of the augmented target distribution in Eq. (15) is proportional to the joint tempered posterior density of the parameters and states

Lemma 1.

The target distribution in Eq. (15) has the marginal distribution

Proof.

We prove the lemma by carrying out the marginalisation similarly to the proof in Andrieu et al., (2010) for particle Gibbs MCMC. The marginal distribution is obtained by integrating over . We begin by integrating over to obtain

| (16) | |||

We repeat this for , to obtain,

Finally, we integrate over , to obtain

∎

12 Augmented Intermediate Target Density for the Factor SV model

This section provides the augmented tempered target density for the factor SV model; It includes all the random variables produced by the univariate particle filter methods that generate the factor log-volatilities , for , and the idiosyncratic log-volatilities for , as well as the latent factors and the parameters . Eq. (11) specifies the particle filters for the idiosyncratic SV log-volatilities for , and Eq. (12) specifies the univariate particle filters that generate the factor log-volatilities , for . The weighted samples at time for the factor log-volatilities are denoted by and the idiosyncratic error log-volatilities by . The corresponding proposal densities are , , , and for the . The resampling schemes are denoted by , where each indexes a particle in and is chosen with probability ; is defined similarly.

The vectors of particles are denoted as

and

The joint distribution of the particles given the parameters is

for and

for .

Next, we define indices for , the selected particle trajectory , indices for and the selected particle trajectory .

The augmented intermediate target density in this case consists of all the particle filter variables

| (17) | ||||

The next lemma shows that the target distribution in Eq. (17) has the required marginal distribution. Mendes et al., (2020) give a similar lemma and proof for describing the augmented target density of the factor SV models for PMCMC methods.

Lemma 2.

The target distribution in Eq. (17) has the marginal distribution

Proof.

Similarly to the proof of Lemma 1, we can show that the marginal distribution

is obtained by integrating over for , and for . ∎

12.1 Application of the SMC-HMC method to the Multivariate Factor Stochastic Volatility Model

This section discusses the application of the SMC-HMC method to the multivariate factor SV model described in Section 5.1 in a batch context. We first define the appropriate sequence of intermediate target densities,

| (18) | ||||

Algorithm 6 gives the Markov move step based on Hamiltonian Monte Carlo for the multivariate factor SV model with the target densities . Steps 1 to 4 update the idiosyncratic log-volatilities parameters for , factor log-volatilities parameters for , the factor loading matrix and the latent factors , respectively. Section 13.2 discusses updating the idiosyncratic and factor log-volatilities parameters. Section 14 discusses sampling of the factor loading matrix and the latent factors . Steps 5 and 6 update idiosyncratic log-volatilities, and factor log-volatilities using Hamiltonian Monte Carlo, respectively. Section 13.1 presents the details on updating the idiosyncratic and factor log-volatilities.

for each ,

-

1.

for

-

(a)

Sample

-

(b)

Sample

-

(c)

Sample

-

(a)

-

2.

For

-

(a)

Sample

-

(b)

Sample

-

(a)

-

3.

Sample the factor loading matrix

-

4.

Sample the latent factors

-

5.

For , sample using Hamiltonian Monte Carlo.

-

6.

For , sample using Hamiltonian Monte Carlo.

12.2 Application of the SMC-PG and SMC-PHS methods to the Multivariate Factor Stochastic Volatility Model

This section discusses the application of the SMC-PG method to a multivariate factor SV model in a batch context. Similarly to Section 12.1, Eq. (18) gives the appropriate sequence of intermediate target densities. Section 12 discusses the augmented intermediate target density for the multivariate factor SV model.

Algorithm 7 describes the SMC-PG Markov moves for the multivariate factor stochastic volatility model. Steps 1 to 4 update the idiosyncratic log-volatilty parameters for , factor log-volatility parameters for , the factor loading matrix and the latent factors , respectively. Section 13.2 discusses updating for the idiosyncratic and factor log-volatility parameters. Section 14 shows how to sample the factor loading matrix and the latent factors . Steps 5 and 7 update the for and for , respectively, by running conditional sequential Monte Carlo algorithms. Steps 6 and 8 update the indices and , by running backward simulation algorithms. SMC-PHS is similar to Algorithm 7, but generates and using a PMMH step with a random walk proposal for and .

for ,

-

1.

For ,

-

(a)

Sample

-

(b)

Sample

-

(c)

Sample

-

(a)

-

2.

For ,

-

(a)

Sample

-

(b)

Sample

-

(a)

-

3.

Sample the factor loading matrix .

-

4.

Sample the latent factors for .

-

5.

For , sample

-

6.

For , sample

for and -

7.

For , sample

-

8.

For , sample

for and .

13 Markov moves for the Factor SV model

13.1 Sampling the latent volatilities using Hamiltonian Monte Carlo

We obtain the gradient with respect to each of the latent volatilities . The gradient for is

the gradient for is

and the gradient for is

We now obtain the gradient with respect to each of the latent volatilities . The gradient for is

the gradient for is

the gradient for is

13.2 Sampling the idiosyncratic and factor log-volatilities parameters

For , sample from truncated within , where

and

For , we sample by drawing a proposed value from truncated within , where

and

The candidate is accepted with probability

For , we sample from , where and . For , we sample by drawing a proposed value from truncated within , where

For , we sample from , where and .

14 Sampling the factor loading matrix and the latent factors

This section discusses the parameterisation of the factor loading matrix and the latent factors, and how to sample from their full conditional distribution.