Maximal discrete sparsity in parabolic optimal control with measures

Evelyn Herberg111Mathematisches Institut, Universität Koblenz-Landau, Campus Koblenz, Universitätsstraße 1, 56072 Koblenz, Germany. Michael Hinze∗ Henrik Schumacher222Institut für Mathematik, RWTH Aachen University, Templergraben 55, 52062 Aachen, Germany.

(November 19, 2019)

Abstract. We consider variational discretization [18] of a parabolic optimal control problem governed by space-time measure controls.

For the state discretization we use a Petrov-Galerkin method employing piecewise constant states and piecewise linear and continuous test functions in time. For the space discretization we use piecewise linear and continuous functions. As a result the controls are composed of Dirac measures in space-time, centered at points on the discrete space-time grid.

We prove that the optimal discrete states and controls converge strongly in and weakly- in , respectively, to their smooth counterparts, where is the spatial dimension.

Furthermore, we compare our approach to [8], where the corresponding control problem is discretized employing a discontinuous Galerkin method for the state discretization and where the discrete controls are piecewise constant in time and Dirac measures in space. Numerical experiments highlight the features of our discrete approach.

where the state solves the following parabolic

state equation

(1)

with real, regular Borel measures and .

Here

is an open, bounded domain with boundary of regularity to be discussed later.

We fix an open, relatively compact interval

and a relatively compact subdomain

and define the space-time control domain .

By the Riesz representation theorem (see [26, Theorem 6.19.]), we may identify the space of regular Borel measures on a subset with the dual space of , the closure of the space of continuous, compactly supported functions in the supremum norm.

In particular, we have

Moreover, the total variation norm for measures coincides with the dual norm:

Where appropriate, we identify with the space , and accordingly

with . Furthermore, , are

given penalty parameters.

The state is supposed to solve (1) in the following very weak sense, equivalent to [8, Definition 2.1.] :

The solvability of (2) and of problem () have already been established in

[8, Theorem 2.2.] and [8, Theorem 2.7.].

We will also discuss this matter in greater detail later in Section 2.

For the moment, we just state that both (2) and () are well-posed with unique solutions provided that (i) is a sufficiently regular (e.g. is of class ) and that (ii) .

Optimal control with total variation norm of measures has several applications since its solutions admit a sparsity structure (see, e.g., [16, 17, 28]). For example, the problem of identifying the location of a pollution source or the time instance of a pollution based on measurements can be formulated as an optimal control problem with measures. The sparsity structure of the controls here allows for a precise prediction of the pollution source or the time instance at which pollution takes place.

For the practical implementation, we propose a discrete concept which delivers discrete controls with a maximal sparsity structure, i.e., variational discretization from [18], which allows to control the discrete structure of the controls through the choice of Petrov-Galerkin ansatz and test spaces in the discretization of the state equation.

The problem can also be discretized by a full discretization approach as is proposed in, e.g., [8], where piecewise constant controls in time and Dirac measures in space are used. This limits the maximal possible sparsity in this setting to controls which are constant on time intervals.

For the variational discretization we obtain analogous convergence results as reported in [8, Theorem 4.3.]. More precisely, we will prove Theorem 2, where () denotes the variational discrete version of the problem (). We denote the implicitly discrete control space , in which () has a unique solution (see Theorem 11), and the discretization parameter , where indicates time and indicates space (see Section 3 for more details on the notation).

Our main result reads as follows:

Theorem 2.

Let be a bounded open domain of class and let satisfy .

For fixed , let be the unique solution of problem () that belongs to ,

and denote the associated state by .

Then for each sequence of discretizations with , we have the following convergence properties:

(3)

(4)

(5)

where is the unique solution of () and its associated state.

Let us briefly comment on related contributions in the literature.

In [6, 11, 24], control of elliptic partial differential equations with measures is considered and control of parabolic partial differential equations with measures can be found in [7, 8, 9, 21].

In [9], the special case of initial data is covered and in [21, 24] a priori error estimates are derived. Of particular interest for our approach are the techniques proposed in [11], where Fenchel duality is used to set up a predual problem.

In this context we also consulted the lecture notes by Clason [10], where Fenchel duality is discussed in detail.

The variational discrete concept that we use has been introduced in [18] and the time discrete-scheme in a variational discrete setting has been analyzed in [12, 15].

The paper is organized as follows: In Section 2 we analyze the continuous problem () and its sparsity structure.

We will then set up the predual problem, show that it has a unique solution and apply the Fenchel duality theorem. The predual problem will be discretized with two different strategies.

The first one is by variational discretization., We discuss it in Section 3, where we derive also a semi-smooth Newton method to solve the variational discrete problem (). The second strategy is a discontinuous Galerkin discretization (see Section 4). The emerging fully discrete problem () is solved analogously to (). Computational results of both approaches are compared in Section 5.

2 Continuous optimality system

In this section, we take a closer look at the solution structure of ().

2.1 State Equation

First, we have to discuss solvability of the state equation (1),

to be interpreted in the form (2).

To this end, for an arbitrary open domain , we introduce the following anisotropic Sobolev spaces

and define the space

where is the Hölder conjugate of .

Because of ,

the existence and uniqueness theory for weak solutions of parabolic partial differential equations (see e.g.,

[14, Chapter 7]) implies that the operator

is an isomorphism of vector spaces. Equipped with the norm

,

is a reflexive Banach space and is an isomorphism of Banach spaces.

The heat operator

is the adjoint of in the sense that holds for all and all :

Since is continuously invertible, so is its adjoint .

Next we show that embeds continuously into .

This will justify putting measures on the right hand side of ().

We choose two further subdomains , with smooth boundaries such that .

By interior regularity estimates (see, e.g., [20, Theorem 4.3.7]), there exists a such that

Notice that the norms on the left hand side topologize .

Thus, the restriction operator given by is continuous.

For (which corresponds to ), one has a continuous embedding of into (see [3, Theorem 10.4]).

Thus, we have a continuous embedding

.

Utilizing the restriction operator

,

,

we define the continuous linear operator

This allows us to rewrite (1) and (2) into the following very compact form:

(6)

As we have already established that is continuously invertible, the well-posedness of (1) and (2) is now evident.

It will soon be essential that is injective.

Because of

it suffices to show that has dense image.

By virtue of Tietze’s extension theorem (see [22, Theorem 35.1.]),

the restriction operator is surjective. So it suffices to show that has dense image.

Next we observe that is an extension domain and that

each element of can be arbitrarily well approximated by the restriction of a function

with .

We pick a mollifier with and

and put for all .

By construction, we have and , showing that has indeed a dense image. Thus is injective.

2.2 Fenchel Duality

As we want to solve our problem numerically by utilizing Newton-based methods, we have to cope with the fact that, because of , the contribution in the objective function is not twice differentiable.

Even worse, and are not differentiable at all.

Fortunately, as demonstrated in [11, Chapter 2.1.], Fenchel duality can help here:

It allows us to transform problem () into an optimization problem () that enjoys sufficient differentiability to make it amenable to the semi-smooth Newton method.

As a convenient side effect, this will also allow us to show that () has a unique solution.

We define the problem () as follows; as it will turn out in Theorem 5, this problem is indeed the Fenchel predual of ():

()

where and

are given by

Theorem 3.

Let satisfy . Then problem () has a unique solution .

Proof.

Let be a minimizing sequence so that

From , we know that , which allows us to assume without loss of generality that for all and hence for all . With Hölder’s inequality and Young’s inequality in the form , we see

and hence .

For all we have , which implies that is a bounded sequence in .

Recall that is reflexive. Hence the bounded sequence admits a weakly convergent subsequence: in as .

Likewise, we have in .

As the indicator function of a closed, convex set, is convex and weakly lower semi continuous

Thus, we are lead to . Also is weakly lower semi continuous, so we obtain:

This shows that is a minimizer of ().

Moreover,

is convex

and

is strictly convex ( is injective and ),

hence is also strictly convex. Thus, there cannot be more than one solution of ().

∎

Now we recall the Fenchel duality theorem in a similar notation as in [10] and [11, Chapter 1.1.3.]. We also refer to [13, Chapter III.4.].

For a convex, lower semi continuous functional

on a normed space with ,

we define its Fenchel conjugate by

Theorem 4(Fenchel Duality).

Let and be normed spaces with topological duals and and let be a continuous linear operator.

Let and be convex lower semi continuous functionals and suppose that and are not identically equal to .

Consider the primal problem

(7)

and the dual problem

(8)

Suppose the following two conditions are fulfilled:

The regular point conditions is fulfilled, i.e., there exists an , such that

and

for all in a sufficiently small neighborhood of .

Then also the dual problem

has at least one solution and one has the identity

(9)

Furthermore, for and , the following three statements are equivalent:

1.

is a solution of the primal problem (7)

and is a solution of the dual problem (8).

2.

.

3.

and

We are going to apply the Fenchel duality theorem to , , and .

To this end, we show first that () and () are dual to each other.

Theorem 5.

The Fenchel dual problem of () coincides with ().

Proof.

It suffices to show that .

In order to calculate , we use the equivalence of the following statements on and :

(10)

Here denotes the subdifferential of the convex functional .

Since is Fréchet differentiable, we have .

Hence is given by

.

Solving for leads to

(11)

Substituting this into

(10)

and utilizing for all , we derive

In order to derive we can interpret , as consisting of two summands, which represent an indicator function with only one constraint respectively, where we want to use the following notation:

Here, we make use of and . From [27, Theorem 2.2.8] we know that for it holds that :

Looking at both conjugates separately, we can use (10) and derive:

where

.

Analogously, we observe that .

Assembling this information, we obtain

∎

Theorem 6.

Problem () has a unique solution , which is characterized by

(12)

where is the unique solution of ().

The optimal state can be retrieved from via

Proof.

We have seen already in the proof of Theorem3 that

both and are convex and lower semi continuous and that is even strictly convex. Furthermore we set .

By Theorem3, the problem () has a at least one minimizer.

For , we have and , showing that and .

Due to , is continuous at so that also the regular point condition is fulfilled.

Thus, we may apply the Fenchel duality theorem, which implies that () has at least one solution.

Since is injective and , is strictly convex, hence there is only one solution .

By the the third condition from Theorem4,

each solution has to satisfy

and ,

where is a solution of ().

∎

2.3 Sparsity Structure

We recall the optimality conditions for the solution of () from [8, Theorem 3.1.] and the resulting sparsity structure [8, Corollary 3.2.] of the optimal controls .

These results can be directly transferred to our setting since the latter is a special case of the formulation in [8].

Lemma 7.

Let denote a solution to with associated state .

Denote by the unique solution of

which follows from the first part of (12) by solving for .From the second part of (12) we have that , hence satisfies

and

Remark 8.

Under the assumptions of the previous Theorem we have the following sparsity structure:

where and are the Jordan decompositions. Let us note that is the adjoint in ().

If one considers it as the generic case that the function is not constant on sets of measure greater than zero,

the controls have support sets of measure zero. This is our motivation to propose a discretization strategy which reflects this behavior on the discrete level in space and time.

3 Variational Discretization

Here we want to achieve the desired maximal discrete sparsity, i.e., Dirac-measures in space-time, by choosing the Petrov-Galerkin-ansatz and -test space that will induce this structure. The variational discretization concept was introduced in [18] and its key feature is to not discretize the control space. Instead, via the discretization of the test space and the optimality conditions, an implicit discretization of the control is achieved. This is how we control the discrete structure of the controls. Looking at the relation (11) between the optimal adjoint state and , it is obvious, that the discrete structure of the test space affects the structure of the optimal controls . This motivates the following choice of discrete spaces: We define the state space consisting of continuous and piecewise linear functions in space and piecewise constant functions in time, whereas we define the test space consisting of continuous and piecewise linear functions in space and time.

In the following we discretize () and analyze the structure of the controls. We will see that the above choice of discrete state and test spaces in combination with the optimality system of the discrete problem induces Dirac measures in space and time for the controls. Afterwards, we discuss the existence and uniqueness of solutions to the variational discrete problem. We then prove the convergence properties stated in Theorem 2. Afterwards we discretize (), reformulate the problem equivalently, and derive an optimality system by a Lagrange approach.

If the necessary conditions are fulfilled, we can apply a semismooth Newton method to solve the optimality system. Utilizing Fenchel duality, we can finally calculate the optimal solution of ().

As a first step to characterizing the discrete spaces, we have to set up the space-time grid.

Define the partition .

The time interval is decomposed in subintervals for and .

We point out that we defined the intervals such that they cover the full time interval , which is crucial because we deal with measures that can be supported on isolated points.

The temporal grid size is denoted by , where .

Let be a finite triangulation of with grid size .

We set and denote by the interior,

by the boundary of , and by the discrete space-time domain. We assume that vertices on are points on .

The interior vertices of are denoted by .

We combine the two discretization parameters and into the vector and define the following discrete state and test spaces:

(13)

such that for is ensured. Here, and

denote the nodal basis formed by continuous, piecewise linear functions on and , respectively.

Moreover, denotes the indicator function of the time interval .

We also define the space

In order to set up the variational discrete state equation, we start by deriving a very weak formulation of (1), which will be discretized afterwards. By multiplication with , integration over the domain , and utilizing , we arrive at

(14)

Inserting and testing against all yields the following variational discrete representation of the state equation: Find , such that

(15)

holds for all .

This allows us to formulate the variational discrete problem

We refrain from giving a detailed derivation for an optimality system and the sparsity structure for this problem as this would closely follow the procedure in the continuous setting (see Lemma 7 and Remark 8).

Instead, we focus on analyzing how the controls are implicitly discretized. First we define the following sets of indices:

We may suppose that the space-time discretization is sufficiently fine so that and are nonempty.

Utilizing these sets, we define the following discrete spaces:

Notice that both spaces are spaces of continuous functions, i.e., we have

and

.

The discrete version of the mapping , decomposed into two parts, reads as follows:

(16)

(17)

We suppose that is polygonal and that is an exact triangulations of , i.e.,

and similarly for .

From the discrete optimality system (whose precise derivation has been omitted), we obtain:

(18)

(19)

where the denote the coefficients of the optimal adjoint variable , i.e.,

.

Although we did not mention the mapping explicitly in the continuous optimality system,

we do so here for clarity.

As discrete sparsity structure, we obtain the following (see also Lemma 7)

(20)

By construction, the discrete adjoint state is piecewise linear, both in space and time.

Thus, and attain their extremal values and in the grid points contained in and , respectively.

Generically, and attain their extrema only in these grid points, in which case we have

This leads us in a natural way to the discrete control spaces

(21)

(22)

Notice also that the natural pairings and

induce the dualities and in the discrete setting.

Here we see the effect of the variational discretization concept:

The choice for the discretization of the test space induces a natural discretization for the controls.

The following operators will be useful for the discussion of solutions to ():

Lemma 9.

Let the linear operators and be defined as below:

Then for every and the following properties hold.

(23)

(24)

(25)

(26)

These results follow directly from restricting [8, Proposition 4.1.] to .

We derive also an analogous result for the space-time discrete spaces and , which is similar to [8, Proposition 4.2.], but adjusted to our choice of spaces. The structure of the proof remains the same, only technical calculations are different.

We deduce that there exists a subsequence, denoted in the same way, such that

For any , it holds that as . We derive

This shows and for the whole sequence and hence

∎

Next, we observe that is convex, but not strictly convex. In the continuous setting, the strict convexity of was caused by the norm for and the injectivity of . Here we have the discrete operator , defined as , with . We can rewrite the discrete state equation (15) as

(31)

The mapping is in general not injective, hence the uniqueness of the solution cannot be concluded. In the implicitly discrete setting however, we can prove uniqueness similarly as done in [7, Section 4.3.].

Theorem 11.

The problem () has at least one solution in and there exists a unique solution . Furthermore we know for every solution of () that .

Proof.

The existence of solutions can be derived as in the proof of Theorem 6 because the control domain is still continuous.

Let be a solution of problem () and let .

We deduce from (23) and (27) that

(32)

Additionally, (25) and (29) deliver and .

Combining these properties, we deduce .

This validates the existence of solutions in the discrete space .

The operators and act as identities on and .

Furthermore, the operator is injective and we also know that .

Hence we deduce the injectivity of for discrete controls .

Now strict convexity of on follows

from . Consequently, problem () has a unique discrete solution .

For every solution of (),

the projection

is a discrete solution.

Moreover, there exists only one discrete solution.

So we deduce that all projections must coincide, showing the second statement of the theorem.

∎

Since all projections of solutions of () yield the unique discrete solution , it suffices to analyze the convergence properties of for .

Furthermore we may find solutions of () numerically, by restricting the control space to .

We can now prove the convergence result formulated in Theorem 2 along the lines of the proof of [8, Theorem 4.3.].

Proof.

Observe that . This implies that the norms , and are uniformly bounded for all . Now, let be a sequence with . Boundedness in norm implies that there exists a subsequence , such that the following holds true for :

(33)

We will split the proof into three steps.

I - is the solution of (1) corresponding to , i.e., . By constructing a suitable Friedrichs smoothing operators and by using standard results in approximation theory (e.g., cubic spline interpolation, see [2, Theorem 1]),

one realizes that is dense in . Consequently, it is sufficient to test the smooth state equation (2) against with satisfying and .

Let be approximated by , such that

(34)

Indeed, one has the error estimate for the Ritz projection.

For details see Corollary 2 and Remark 4 in [23].

Moreover, let be the continuous, piecewise linear interpolation of on the time grid and put .

By construction, we have for . Furthermore, , where , for since

We have from (34)

and can be confirmed by splitting into its subintervals , integrating and using for all .

Testing (15) against this , we obtain

(35)

On the right hand side, we can perform the limit directly:

Applying the very definition of and integration by parts, we observe that

Along with and ,

this implies that for all tensor product functions , Thus, we deduce from (35).

II - coincides with the unique solution of () that lies in

In order to prove this, it suffices to show .

Recall that we identified and with and , respectively. In this sense, the sets and are dense in and with respect to the sequential weak-* topology.333This can be seen by utilizing that and have to satisfy certain uniform cone conditions (because they are Lipschitz domains, see [1, Paragraph 4.8]) and by convolution against suitable Friedrichs mollifiers that are compactly supported in the interior of finite, convex cones. Notice also that such convolutions do not increase the -norms.

Consequently, we may pick a specific minimizing sequence , where and satisfy and . Then the states are solutions of the heat equations

It follows now from maximal regularity (recall that is now assumed to be of class ), that for all . Thus the finite element discretizations of the states converge to in and thus also in .

More precisely, we have for each fixed that

We choose a suitable subsequence of as follows:

We put and pick recursively such that

Now using

the projection properties (25),(29) and (32) in combination with the above, we obtain

Next, we use the weakly lower semicontinuity of in combination with (33), then apply to both sides of the above inequality, and finally use the facts that is a minimizing sequence and that solves problem ():

III -proof of (3), (4) and (5) Altogether, we know that every sequence with has a subsequence , such that

Since the limits are always the same and and are unique, this implies already that

Because of , the space is an uniformly convex Banach space; thus weak convergence together with the convergence of the norms implies strong convergence (see [5, Proposition 3.32]).

This shows (3).

In a similar way we can prove the first part of (5)

Finally, the second part of (5) follows directly from and the fact that we already showed the convergence of the other two terms.

∎

Now we discretize () with and equivalently reformulate the problem in the following way:

()

s.t.

(37)

Similar to the continuous setting, it can be shown that () is the Fenchel predual of the problem () restricted to . In order to solve (), we want to represent by a matrix, as done in [7]. From [12, Section 4] and [15] we know that the matrix representation of yields a Crank-Nicolson scheme with a smoothing step. We will derive this first.

Let be the mass matrix and the stiffness matrix corresponding to .

We define for , and for . We then obtain the following :

For , we have .

In order to represent the discrete state equation (15) by a system of equations, we also need to calculate . Due to the implicit discrete structure of the controls , we can define with and for and for . Then we have

with for and . Since and , we get

For the remainder of this section, we identify elements from and with vectors in , and elements from with vectors in , respectively. The discrete elements can be expressed via their respective expansion coefficients. To simplify the notation, we define and write . Analogously, we define for .

We represent the discrete state equation by the following -matrix:

(38)

We point out that is in fact the operator concatenated with the space-time mass matrix that maps from to , which is an important detail for the implementation. A representation of , also concatenated with a space-time mass matrix, is the matrix . If we now actually want the representative of , it is necessary to multiply with the inverse of the space-time mass matrix .

Furthermore the embedding , defined in (16) and (17), can be represented by a restriction matrix:

From duality we conclude that can be represented by , such that is the matrix vector formulation of (15).

We equivalently reformulate the constraints (37) in using (18) and (19):

We can now formulate linear inequality constraints that are equivalent to (37).

All inequalities are strictly fulfilled for , thus is an interior point of the feasible set and thus the Slater condition is satisfied (see e.g. [19, (1.132)]).

We discretize the desired state by sampling it on the dual time grid:

(39)

By doing so, we assume that has a certain minimum continuity. However, discretization by local averaging is also possible.

If we make sure that for , then using in () instead of does not interfere with the convergence result Theorem 2.

We proceed by setup the corresponding Lagrangian with multipliers and :

For the sake of simplified numerics, we use a lumped mass matrix approach for computing , where is a vector, i.e., with a slight abuse of notation, we employ

where .

We also use a lumped mass matrix approach for .

We can now form the optimality system using the Karush-Kuhn-Tucker conditions (see, e.g., [4, (5.49)]).

Since the Slater condition is satisfied,

the Karush-Kuhn-Tucker conditions state that at the minimum ,

there must be the partial differential of at the point has to vanish

and that the following complementary conditions have to be fulfilled:

which can be equivalently reformulated for all and with an arbitrary :

We define

containing the left sides of our optimality system and solve the equation by a semismooth Newton method ([19, Algorithm 2.11]). In this algorithm we need to choose the matrix to be used in the semismooth Newton equation from the set of matrices denoted by Clarke’s generalized Jacobian ([19, Example 2.4]):

where denotes the convex hull.

Here, a choice has to be made for the numerics since the generalized Jacobians of

, need not be singletons.

This is due to the -functions and because we have

for every differentiable scalar function .

Here, we make the decision to always choose , if .

Using this, we define:

(40)

for the semismooth Newton method. An interesting observation is that for we have a symmetric matrix on the active sets.

We want to remark that we could follow [7] and employ Fenchel duality to recover a problem in the variable . However, this would require to add the representation of the adjoint from (11) to our optimality system. As the exponent is strictly smaller than 1, which is problematic for derivative based methods and was our main motivation to use the Fenchel duality approach in the first place.

Instead, we solve for the optimal adjoint and recover the optimal control through the discrete version of (12):

(41)

One could come to the conclusion that this is problematic since is in general only injective, not surjective.

But the expansion coefficients and of the discrete solution

have to vanish anyways for

and (see (20)).

So the remaining coefficients have merely to be read off.

4 Discontinuous Galerkin Discretization

This section deals with a full discretization concept of (), namely discontinuous Galerkin discretization, which is suggested in [8].

The discretization strategy will be adapted to our setting and notation.

Also a convergence result for the fully discrete problem () analogous to Theorem 2 is proven in [8].

We use the discrete spaces as introduced before in (13), (3), (21), respectively and the space-time discrete control space:

In [8], an implicit Euler time stepping scheme is used for the discrete state equation.

For and for every , we define .

Let be given and arbitrary.

Then the following equations form the discrete state equation:

(42)

where is the unique element satisfying:

(43)

Here denotes the scalar product in .

We denote the solution of the discrete state equation (42)

by ,

and define the discrete objective function

This allows us to formulate the following discrete optimization problem

()

Similar to [7], we set up the system matrix for the discrete state equation.

One difference that we need to consider is .

This leads to further degrees of freedom for the state

and also to additional columns and additional rows in the system matrix; see [29, Chapter 12] for further details.

With the mass matrix and

the stiffness matrix ,

the left hand sides of (42) and (43)

can be encoded into the following matrix of size :

As in Section 3, this matrix represents the state-to-control-operator concatenated with the space-time mass matrix . The representation of the adjoint state equation is .

With the discrete representations

and using that the “mass matrix” is the identity in , we obtain the following for the right hand side in (42):

Analogously, with , the right hand side from (43) turns into

Restriction matrices similar the those in 3 can be derived and the discrete state equation can be written in matrix form.

This can be used to discretize (), leading to an optimization problem in the variable .

The setup for the fully discrete problem and the derivation of the optimality system are almost identical to the procedures from Section 3;

one only has to replace by

and to keep in mind that the number of degrees of freedom changes from to .

5 Computational Results

We numerically solve () by a semismooth Newton method as derived in Section 3. To simplify, we fix . Therefore the condition in problem () disappears and so do and in the Lagrangian . The dimension of the optimality system is reduced accordingly since and do not have to be considered. For the discontinuous Galerkin discretization from Section 4 of problem (), we proceed similarly. Furthermore, here the first row and column of can be eliminated.

In this section all variables are specified as their discrete representatives, hence we omit the indices. As our domain for both examples, we choose

, , and the relatively compact Lipschitz domain .

We assume that our mesh is equidistant, consequently every cell is of size . We set and so that .

Let us remark that can lead the the matrix being singular.

The cause of this trouble is the second derivative of ; it appears as central building block of and is nearly singular whenever is not pointwise bounded away from .

We circumvent this problem by adding a suitable multiple of the residual to the second derivative of ; as it is well-known (see, e.g., [25]), such a regularization does not deteriorate the convergence rate of Newton’s method.

The purpose of our first numerical example is to illustrate the differences between variational discretization and discontinuous Galerkin discretization.

Therefore, we use a relatively coarse space-time grid with and . We generate a discrete desired state by setting

for the measure control ;

afterwards, we discretize according to (39), where we utilize a truncated Fourier expansion in order to evaluate on the points .

Consequently, this problem is a source identification example that inherits sparsity.

If the penalty parameter equals zero, the only admissible point for the predual problem is . Hence, (41) shows that in this case the optimal discrete controls and for the two discretization approaches can be calculated by applying the discrete heat operator to .

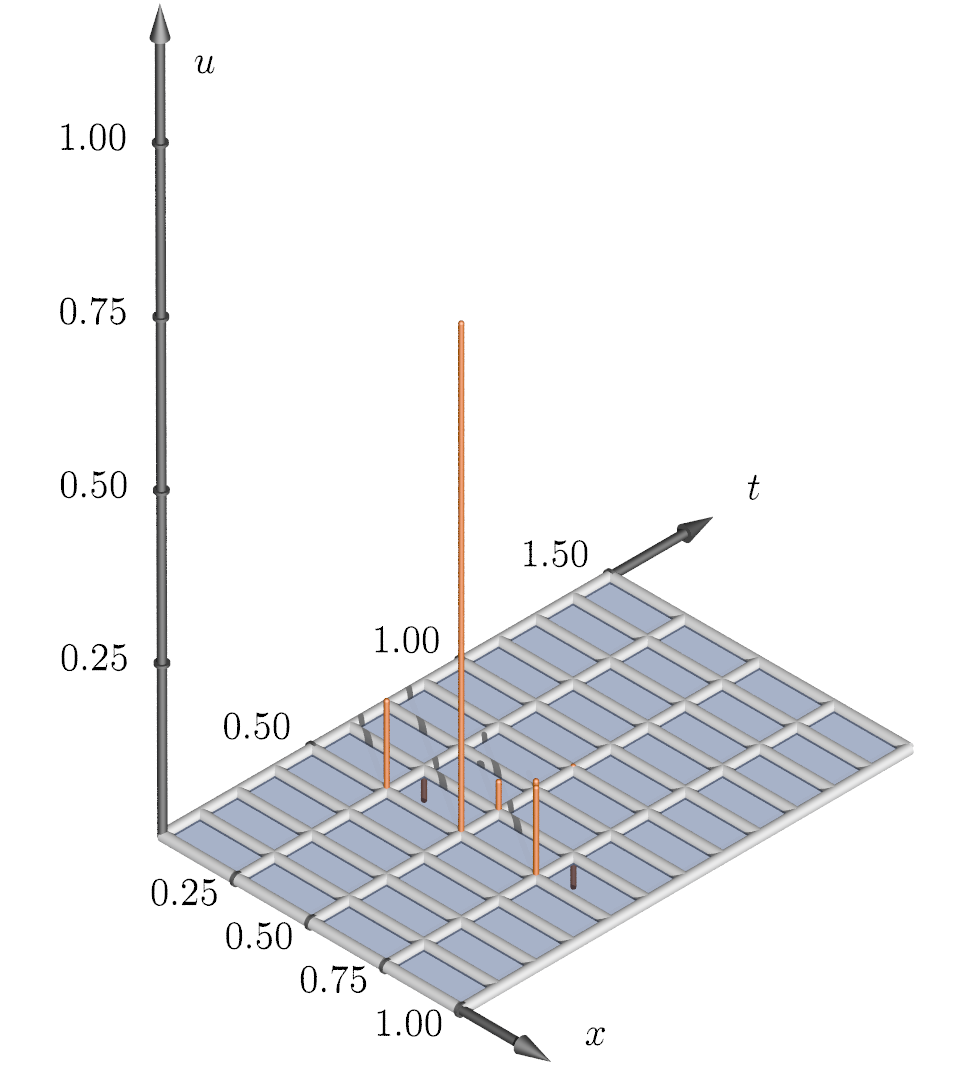

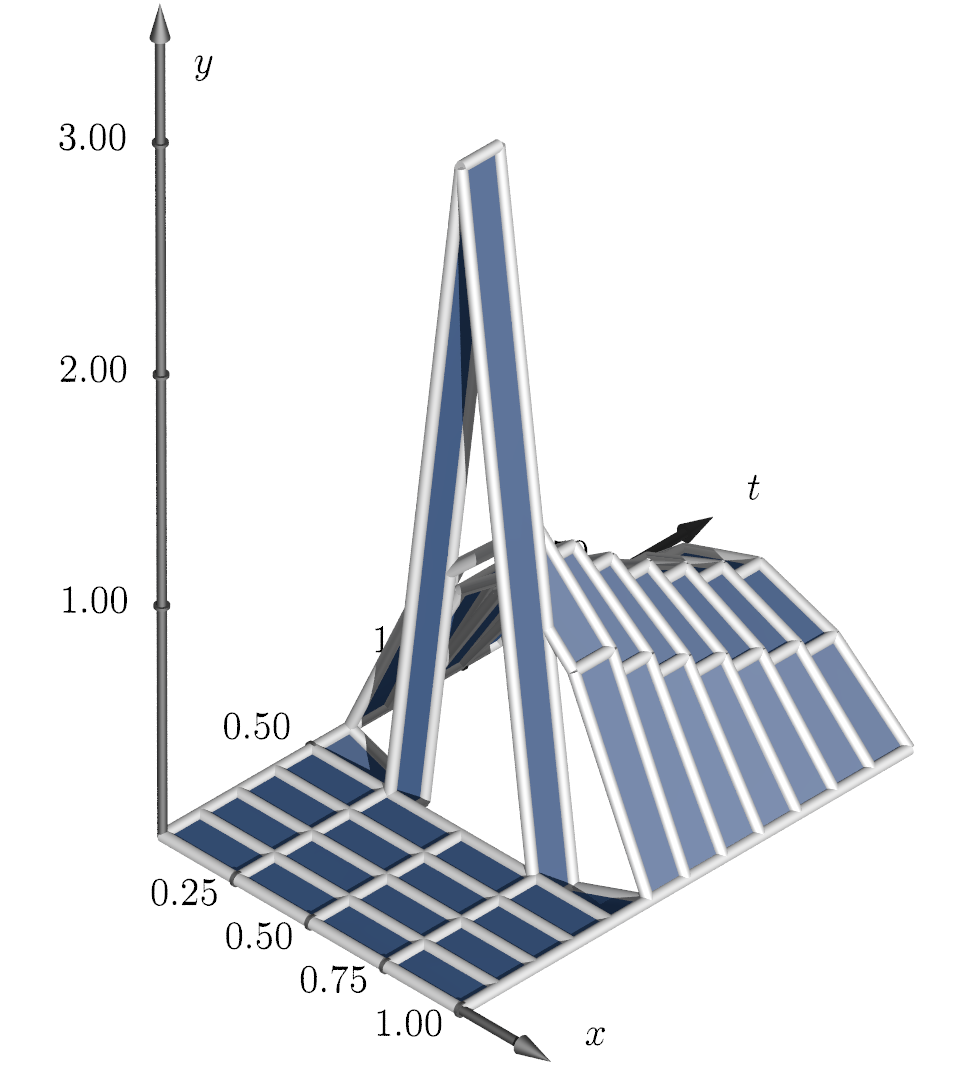

This is meaningful since, for , the only term remaining in the objective functional is the tracking term . In this sense the controls and are the solutions to () and () for with the chosen . Due to the different discretization approaches the calculated controls differ, which can be observed in Figure 1. As a consequence of the discretization error in , we are not able to reproduce exactly in either case.

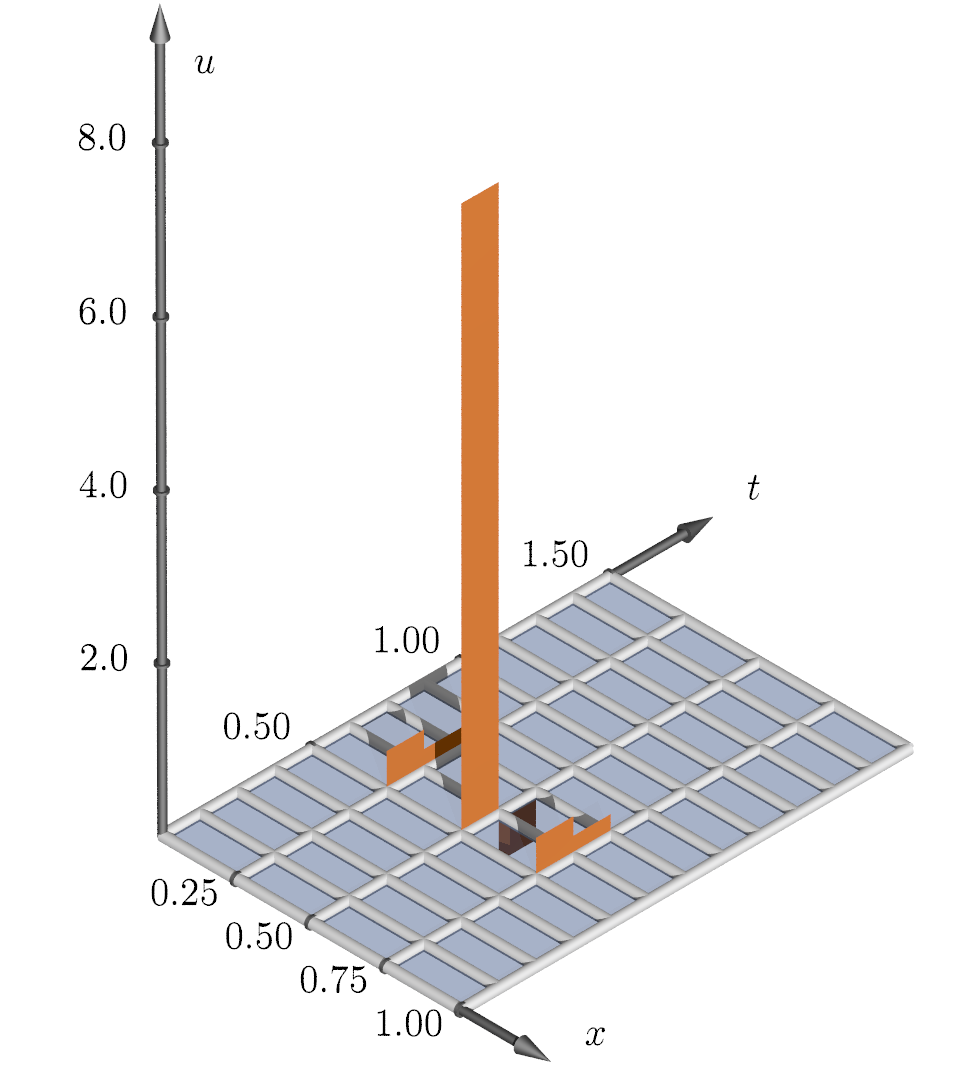

control

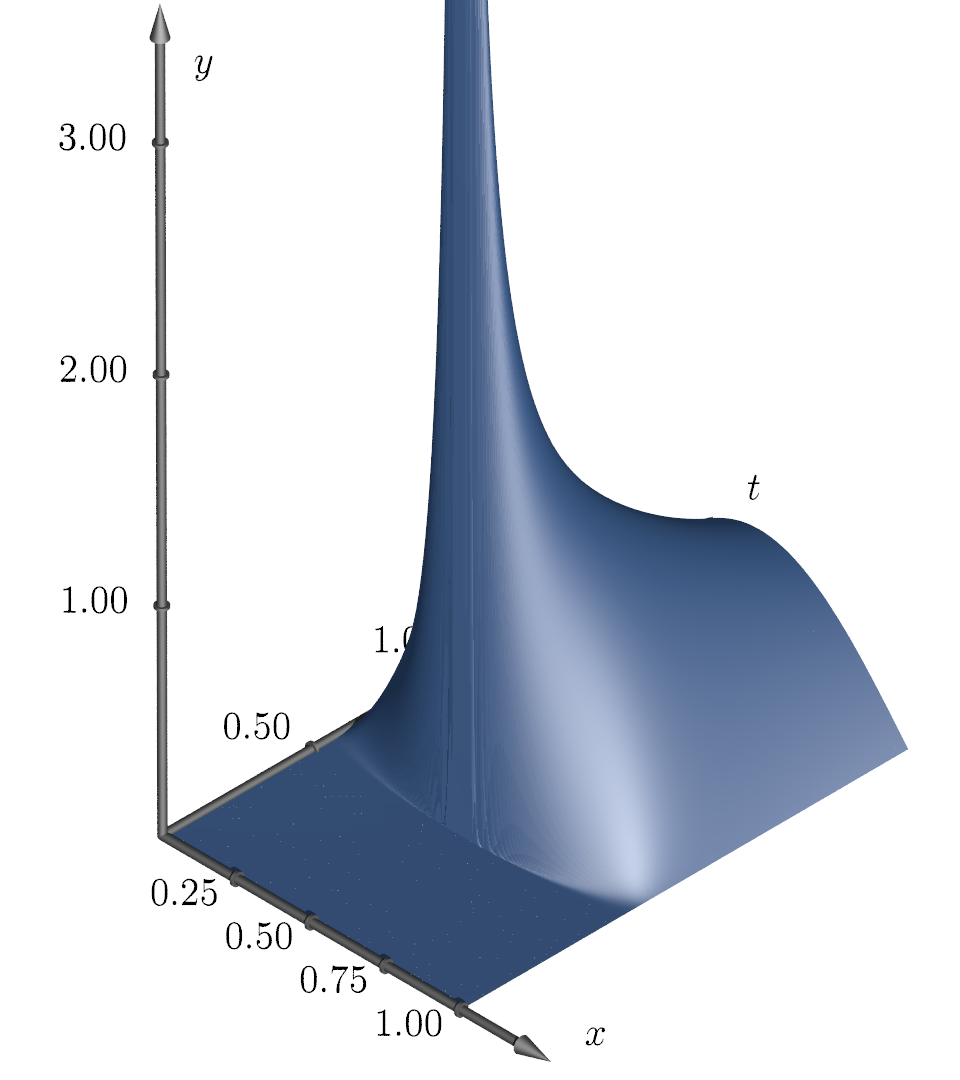

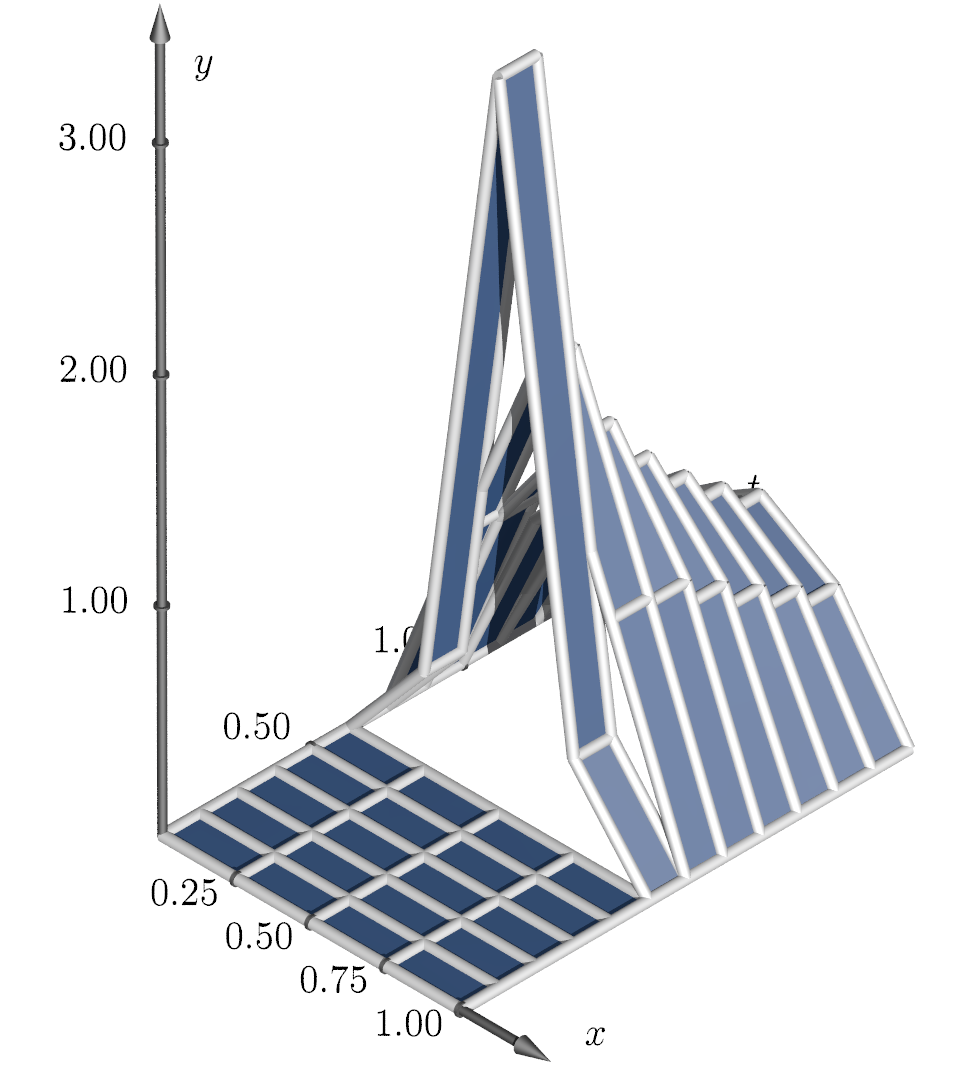

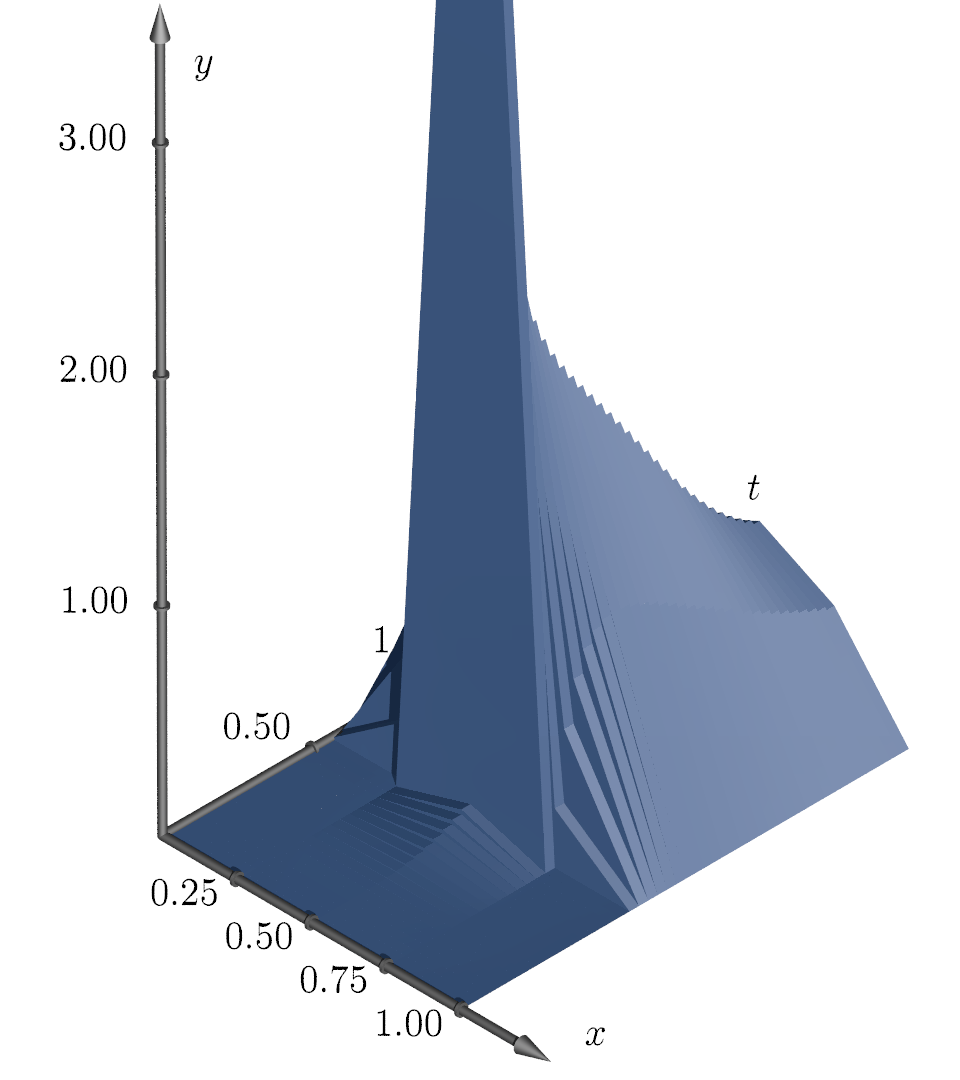

associated state

desired state

(),

(),

Figure 1: Numerical setup on space-time grid with . From left to right: control , associated state (sampled from the analytic solution with spacial Fourier modes), discrete desired state and calculated controls and for .

Here the controls are represented by their coefficients.

In the case of piecewise constant controls in time, which are used in the discontinuous Galerkin setting, this leads to coefficient values, which are scaled with .

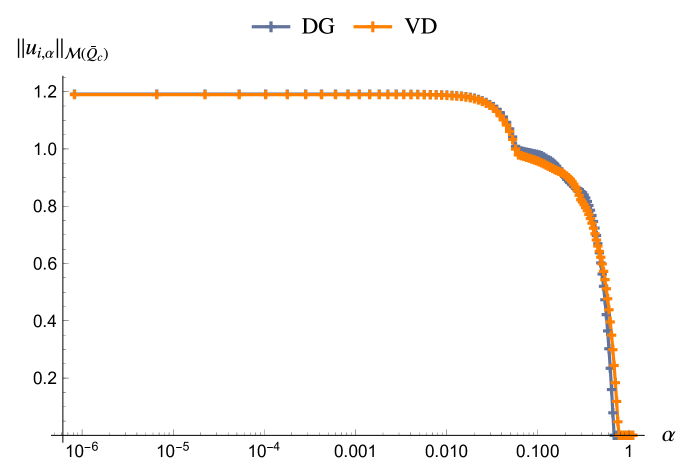

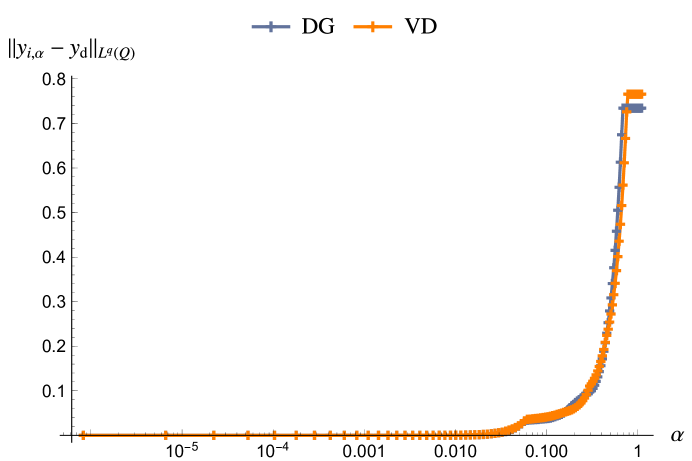

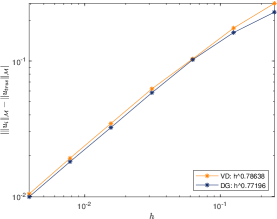

To identify the source location, we raise the penalty parameter because this will lead to a decrease in the norm of the control and we expect a smaller support. The influence of can be observed by plotting the norm of and respectively for a range of .

For each , there exists a value , such that for all the optimal control corresponding to is . Additionally it is interesting to look at the values of

for and various values of ; we plotted the dependences in Figure 2.

According to our expectations, the control norms are monotonically decreasing in and eventually go to zero, while the errors in the tracking terms grow. The graphs for both strategies look very similar. This makes perfect sense, as we discretize the same problem and both discretization strategies converge towards the true solution.

Figure 2: The dependence on the penalty parameter of the measure norm of and (left) and the errors and in the norm (right).

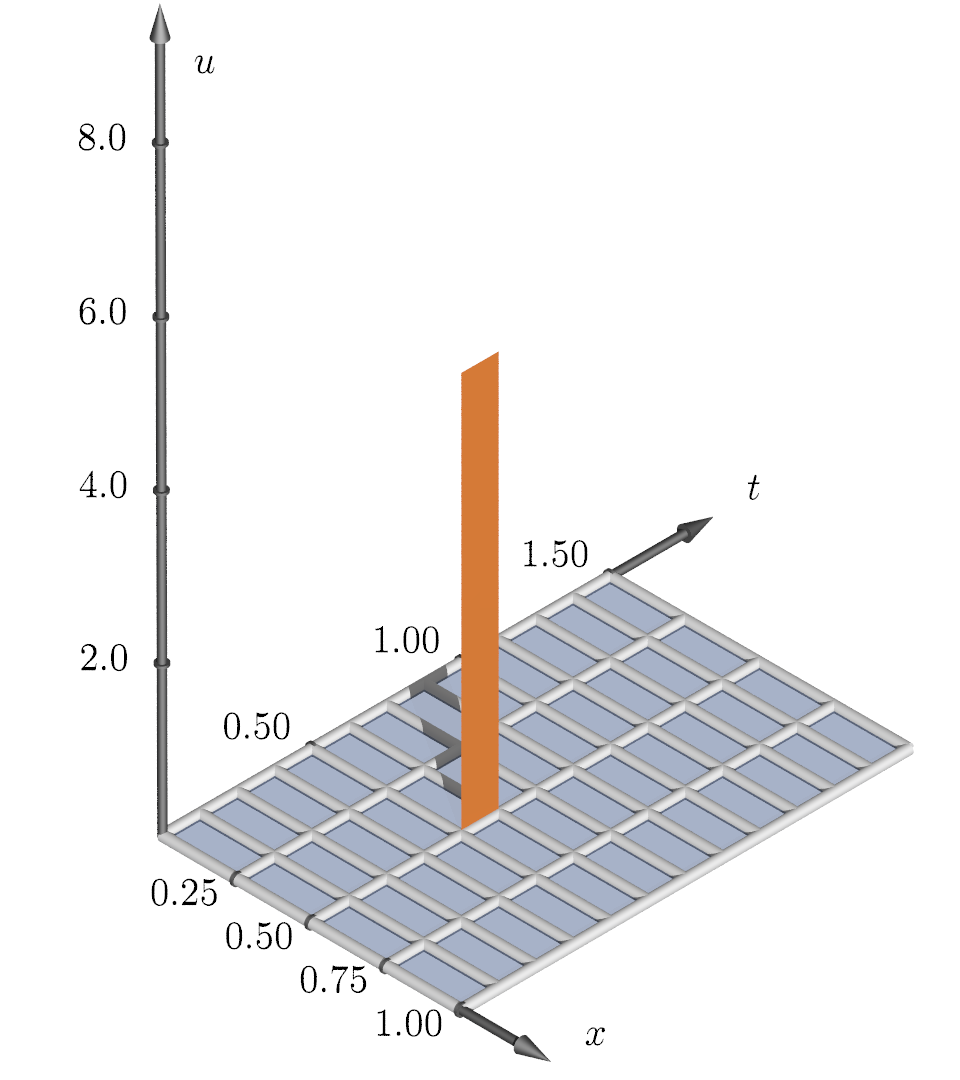

For further comparison of the two discretization strategies, we choose a value of that leads to a norm of the controls, that is neither zero nor maximal. For , the reconstructed controls and states are displayed in Figure 3.

Here we see that the measure norm values and both differ from the true value . Furthermore we observe that and , where the first coincides with the support of .

The control in the discontinuous Galerkin discrete setting can also be represented by a Dirac measure. In order to do so, it has to be multiplied by and the location of the measure in the time interval has to be chosen.

setup

() with

() with

Figure 3: Top row: The measure control and the optimal controls and .

Bottom row: The associated state (sampled from the analytic solution with spacial Fourier modes) and the associated states and .

If the control is not located on our space-time grid, it will be impossible to reproduce its support exactly. In the variational discretization approach a remedy might be choosing a test space consisting of piecewise quadratic – or even higher order – functions in time. Thereby the maximal values of the test functions could be attained not only at grid points, but also inside the time intervals. Determining the location of these maximal values would mean to determine the exact position in time of the potential support of the control. This will be part of further research.

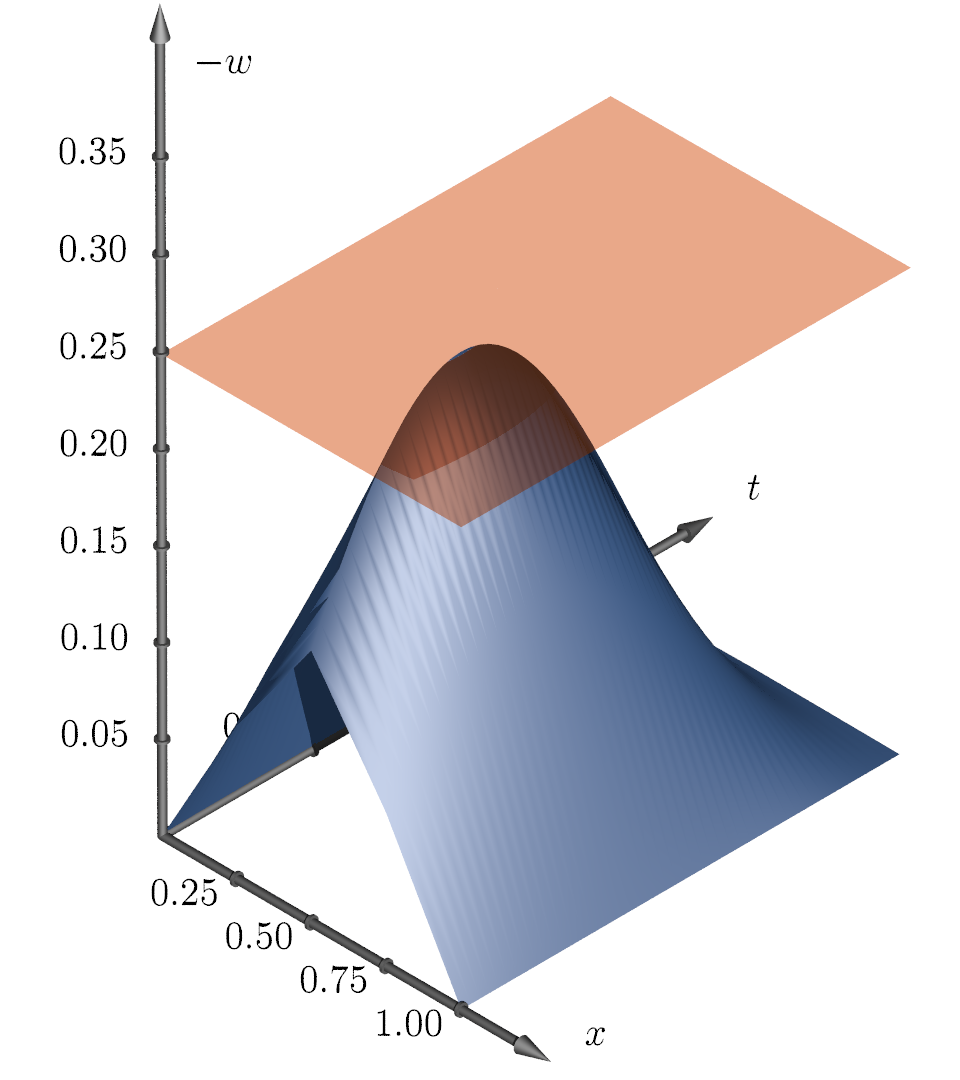

Our second numerical example aims at visualizing the convergence properties from 2 and [8, Theorem 4.3.] for . Utilizing Fenchel duality, we can generate a discrete desired state from a chosen true solution for chosen . From (12), we deduce:

We set and the associated state sampled from the analytic solution with spacial Fourier modes.

Furthermore, we take , such that and for all other values it holds .

For example, with , this is fulfilled by

In the following we fix . The setup is visualized exemplary on an equidistant -grid in Figure 4.

true control

associated state

adjoint state

desired state

Figure 4: Numerical setup on a space-time grid with . From left to right: true control , interpolation of the associated state , adjoint state multiplied by for easier visualization and desired state calculated using Fenchel duality.

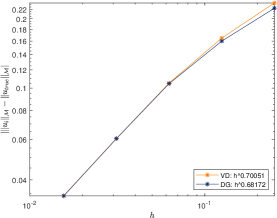

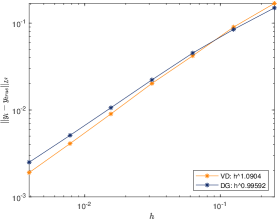

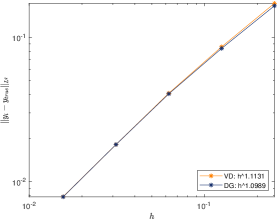

For both discretization strategies, i.e. , we have the following convergence properties:

In 5 we --plot the errors and ,

versus the gridsize .

Figure 5: Top row: The difference of the measure norms of the true control and calculated optimal control , for (left) and (right). Bottom row: The norm of the difference of the associated states , for (left) and (right).

The proven convergence properties can be observed, as the errors go to zero for , which is equivalent to since is always linked to . It is interesting to mention that in the variational discrete setting, oscillations in the state occur for small gridsizes, where . This is caused by the Crank-Nicolson-like scheme. Nevertheless, we see convergence also in this case.

In the legend of the plots we display the slope in orders of of linear fitting curves of the errors, respectively. Proving general convergence rates will be part of further research.

We observe many similarities in the derivation of the algorithms to solve the discrete problems.

The implementation and the level of difficulty in programming is comparable for both approaches and we also observe similar iteration counts.

The main advantage of the variational discretization compared to the discontinuous Galerkin discretization is the maximal discrete sparsity of the control achieved by choosing a suitable Petrov-Galerkin-ansatz and -test space.

Acknowledgment. We thank the referees for their helpful remarks that improved the manuscript.

References

[1]Robert A. Adams and John J. F. Fournier

“Sobolev spaces” 140, Pure and Applied Mathematics (Amsterdam)

Elsevier/Academic Press, Amsterdam, 2003, pp. xiv+305

[2]J. H. Ahlberg and E. N. Nilson

“Convergence properties of the spline fit”

In J. Soc. Indust. Appl. Math.11, 1963, pp. 95–104

[3]Oleg V. Besov, Valentin P. Il’in and Sergey M. Nikol’skiĭ

“Integral representations of functions and imbedding theorems.

Vol. I” Translated from the Russian, Scripta Series in Mathematics,

Edited by Mitchell H. Taibleson

V. H. Winston & Sons, Washington, D.C.; Halsted Press [John Wiley & Sons], New York-Toronto, Ont.-London, 1978, pp. viii+345

[4]Stephen Boyd and Lieven Vandenberghe

“Convex optimization”

Cambridge University Press, Cambridge, 2004, pp. xiv+716

DOI: 10.1017/CBO9780511804441

[5]Haim Brezis

“Functional analysis, Sobolev spaces and partial

differential equations”, Universitext

Springer, New York, 2011, pp. xiv+599

[6]Eduardo Casas, Christian Clason and Karl Kunisch

“Approximation of elliptic control problems in measure spaces

with sparse solutions”

In SIAM J. Control Optim.50.4, 2012, pp. 1735–1752

DOI: 10.1137/110843216

[7]Eduardo Casas, Christian Clason and Karl Kunisch

“Parabolic control problems in measure spaces with sparse

solutions”

In SIAM J. Control Optim.51.1, 2013, pp. 28–63

DOI: 10.1137/120872395

[8]Eduardo Casas and Karl Kunisch

“Parabolic control problems in space-time measure spaces”

In ESAIM Control Optim. Calc. Var.22.2, 2016, pp. 355–370

DOI: 10.1051/cocv/2015008

[9]Eduardo Casas, Boris Vexler and Enrique Zuazua

“Sparse initial data identification for parabolic PDE and

its finite element approximations”

In Math. Control Relat. Fields5.3, 2015, pp. 377–399

DOI: 10.3934/mcrf.2015.5.377

[10]Christian Clason

“Nonsmooth Analysis and Optimization”, 2017

eprint: arXiv:1708.04180

[11]Christian Clason and Karl Kunisch

“A duality-based approach to elliptic control problems in

non-reflexive Banach spaces”

In ESAIM Control Optim. Calc. Var.17.1, 2011, pp. 243–266

DOI: 10.1051/cocv/2010003

[12]Nikolaus Daniels, Michael Hinze and Morten Vierling

“Crank-Nicolson time stepping and variational discretization

of control-constrained parabolic optimal control problems”

In SIAM J. Control Optim.53.3, 2015, pp. 1182–1198

DOI: 10.1137/14099680X

[13]Ivar Ekeland and Roger Témam

“Convex analysis and variational problems” Translated from the French 28, Classics in Applied Mathematics

Society for IndustrialApplied Mathematics (SIAM), Philadelphia, PA, 1999, pp. xiv+402

DOI: 10.1137/1.9781611971088

[14]Lawrence C. Evans

“Partial differential equations” 19, Graduate Studies in Mathematics

American Mathematical Society, Providence, RI, 1998, pp. xviii+662

[15]Christian Goll, Rolf Rannacher and Winnifried Wollner

“The damped Crank-Nicolson time-marching scheme for the

adaptive solution of the Black-Scholes equation”

In Journal of Computational Finance18, 2015, pp. 1–37

DOI: 10.21314/JCF.2015.301

[16]Wei Gong

“Error estimates for finite element approximations of

parabolic equations with measure data”

In Math. Comp.82.281, 2013, pp. 69–98

DOI: 10.1090/S0025-5718-2012-02630-5

[17]Wei Gong, Michael Hinze and Zhaojie Zhou

“A priori error analysis for finite element approximation of

parabolic optimal control problems with pointwise control”

In SIAM J. Control Optim.52.1, 2014, pp. 97–119

DOI: 10.1137/110840133

[18]M. Hinze

“A variational discretization concept in control constrained

optimization: the linear-quadratic case”

In Comput. Optim. Appl.30.1, 2005, pp. 45–61

DOI: 10.1007/s10589-005-4559-5

[19]M. Hinze, R. Pinnau, M. Ulbrich and S. Ulbrich

“Optimization with PDE constraints” 23, Mathematical Modelling: Theory and Applications

Springer, New York, 2009, pp. xii+270

[20]N. V. Krylov

“Lectures on elliptic and parabolic equations in Sobolev

spaces” 96, Graduate Studies in Mathematics

American Mathematical Society, Providence, RI, 2008, pp. xviii+357

DOI: 10.1090/gsm/096

[21]Karl Kunisch, Konstantin Pieper and Boris Vexler

“Measure valued directional sparsity for parabolic optimal

control problems”

In SIAM J. Control Optim.52.5, 2014, pp. 3078–3108

DOI: 10.1137/140959055

[22]James R. Munkres

“Topology” Second edition of [ MR0464128]

Prentice Hall Inc., Upper Saddle River, NJ, 2000, pp. xvi+537

[23]J. A. Nitsche

“-convergence of finite element approximation”

In Journées “Éléments Finis” (Rennes,

1975)Univ. Rennes, Rennes, 1975, pp. 18

[24]Konstantin Pieper and Boris Vexler

“A priori error analysis for discretization of sparse elliptic

optimal control problems in measure space”

In SIAM J. Control Optim.51.4, 2013, pp. 2788–2808

DOI: 10.1137/120889137

[25]Roman A. Polyak

“Complexity of the regularized Newton’s method”

In Pure Appl. Funct. Anal.3.2, 2018, pp. 327–347

[26]Walter Rudin

“Real and complex analysis”

McGraw-Hill Book Co., New York, 1987, pp. xiv+416

[28]Georg Stadler

“Elliptic optimal control problems with -control cost

and applications for the placement of control devices”

In Comput. Optim. Appl.44.2, 2009, pp. 159–181

DOI: 10.1007/s10589-007-9150-9

[29]Vidar Thomée

“Galerkin finite element methods for parabolic problems” 25, Springer Series in Computational Mathematics

Springer-Verlag, Berlin, 2006, pp. xii+370